Abstract

This case study is based on the epic divestment of Air India which eventually did not take off. Post ill-conceived merger without any synergies, the losses began to enlarge exponentially. This led the carrier to financial losses, apart from that enormous order of 110 fleets without having the capacity to pay, crippled the financial status of the airline substantially. All the government’s effort to restructure and turn around the airline proved to be a failure. The plot for this case is set as, considering the government’s inability to cope with its debts and meet day-to-day expenses in this extremely competitive industry, the Union Cabinet gave its ‘in-principle’ nod to divest holdings in Air India, but had not formally announced for the bidding process, a group of ministers are still working on terms of divestment. Meanwhile the news created a buzz and potential bidders have started informally expressing their interest in Air India. The government is expecting more and more bidders to participate to derive maximum out of the auction. When more and more bidders participate in a bid, the bid amount always ascends and a situation of winner’s curse is created where the winning bidder has a feeling of regret by over-paying the amount in order to win the bid. The subject that this case will fit into is Game Theory and Strategic Management courses and central theme or concept to be taught through this case is situation of winner’s curse and some more concepts related to Auctions and Strategy.

On 28 March 2018, the global aviation industry was stormed by the breaking news.

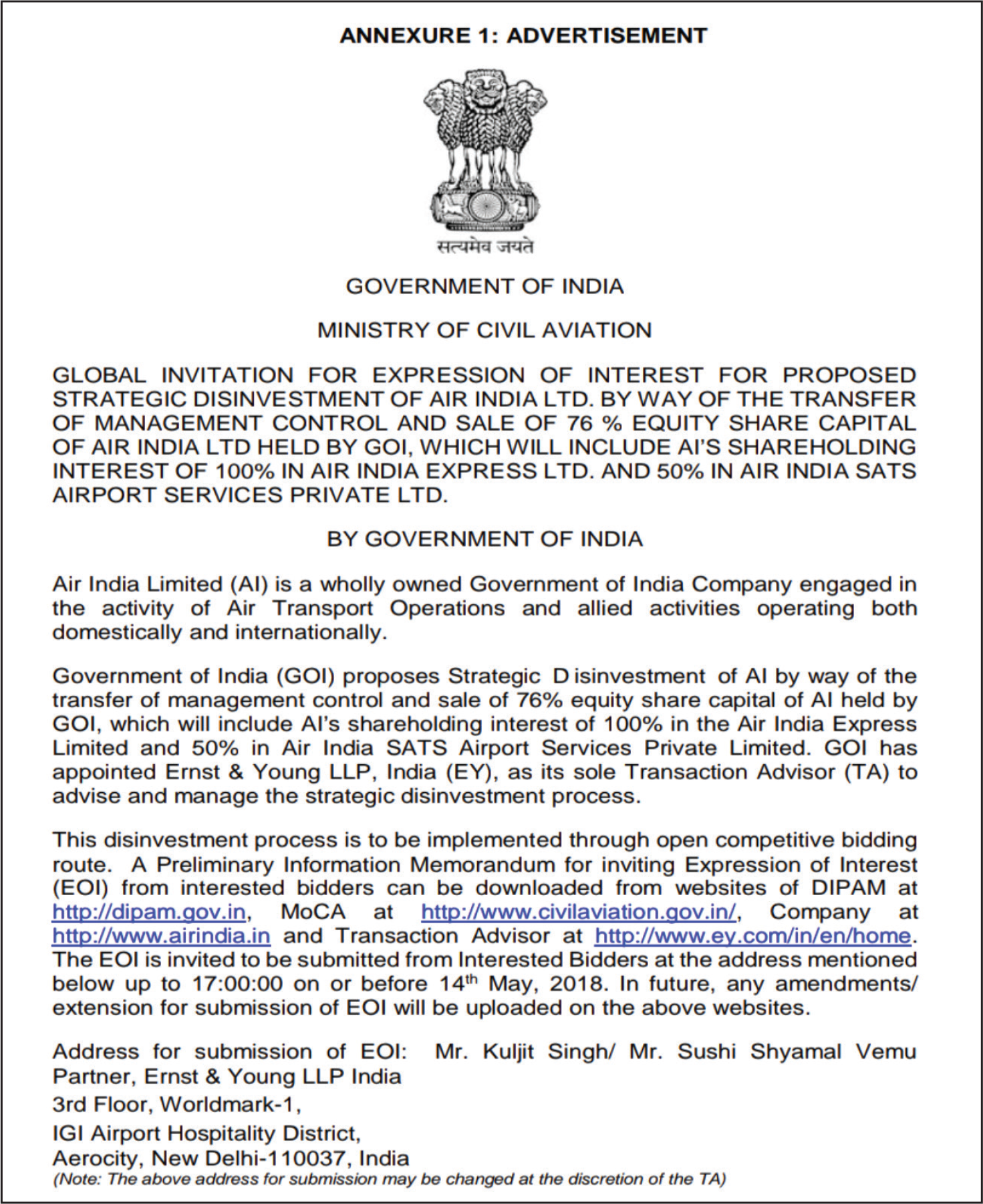

The Government issued a Preliminary Information Memorandum (PIM) inviting Expression of Interest (EI)for strategic disinvestment of Air India. (Service, 2018, May 22; Figure 1)

Air India Limited (AIL), an Indian flag carrier, a government-owned enterprise, operates a fleet of Airbus and Boeing aircraft serving in 94 national and international destinations (Air India, 2019, July 04).

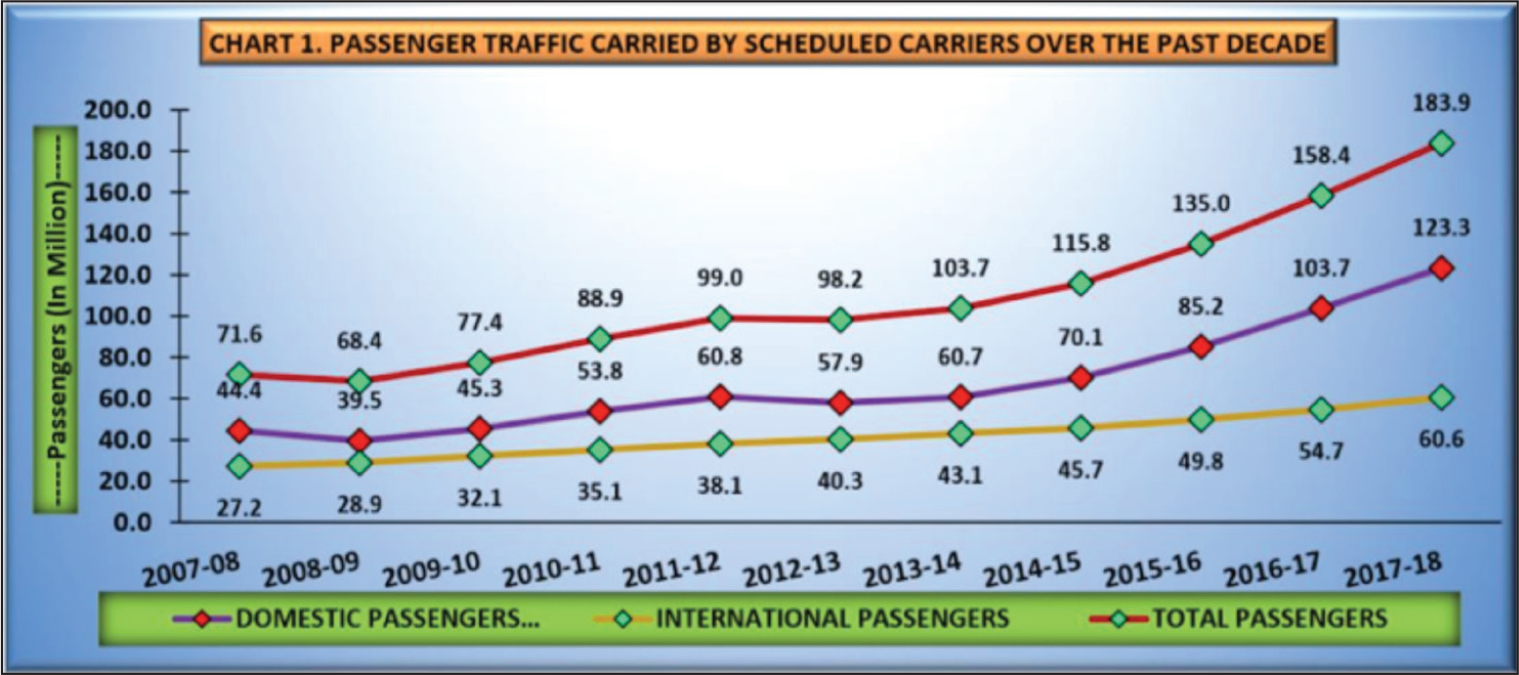

During 2018, Indian civil aviation was classified as the ‘ninth largest aviation sector in the world’ and is anticipated to be ‘the third largest by 2020 and the largest by 2030’ (Reuters, 2018, May 30) (Figure 2). In the last 3 years, Indian civil aviation has been one of the fastest growing sectors in the country and is projected to become ‘the biggest domestic civil aviation industry in the world’ over the next 10–15 years. The passenger market in India is also projected to displace Great Britain and become the third largest passenger market by 2025 (Livemint, 2017, October 24).

It was mostly untapped and would provide enormous growth opportunities (Brand India, n.d.b), keeping in view the fact that air transport was still considered a luxury for the mass population of the country with approximately 40 per cent upwardly mobile middle class (Brand India, n.d.b).

Background

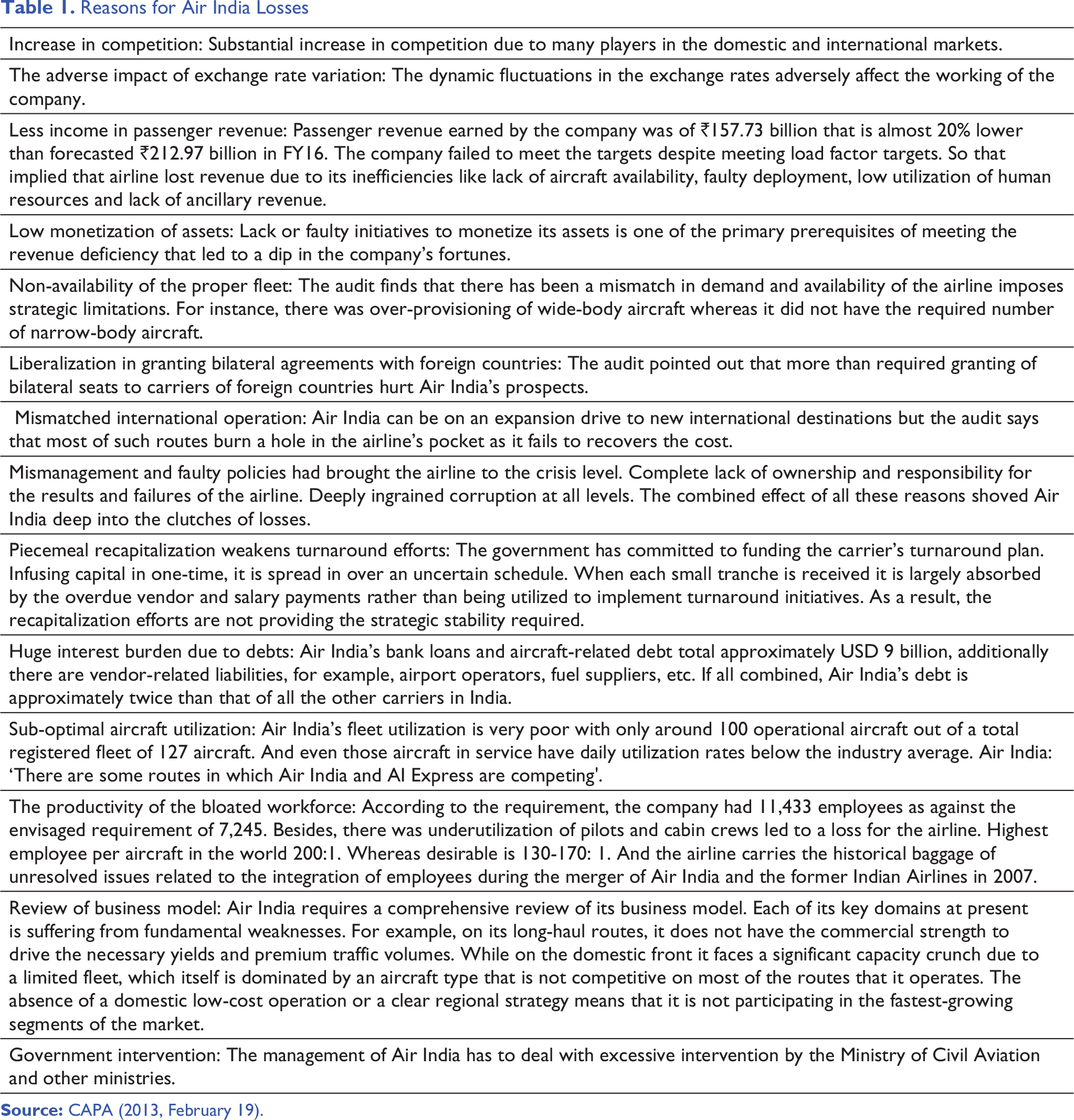

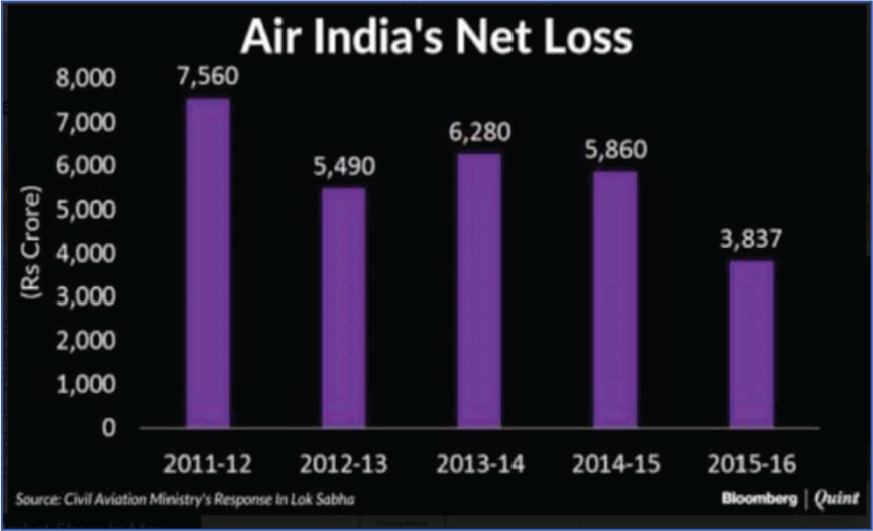

Since Air India has been merged with Indian Airlines in 2007, it has been unprofitable (Kotoky, 2018, January 15). Air India’s losses widened to more than ₹75 billion in the financial year 2011–2012 (Figure 3 and Table 1) and stood at ₹38.367 billion at the end 2016, which had prompted the NITI Aayog1 to propose the divestment of Air India to the Ministry of Civil Aviation (Usmani, 2017, June 28). The Civil Aviation Ministry had discovered the options and methods to turnaround Air India, which was running on a bailout fund of ₹300 billion (Times of India, n.d.).

Reasons for Air India Losses

On 28 June 2017, the Union Cabinet granted in-principle consent to NITI Aayog’s plan for the divestment in the national carrier (Times of India, n.d.). A group of ministers (GOM), with the Finance Minister as its chairman, were to finalize modalities and details of the proposed sale of Air India. Also, the group was mandated to study the balance sheet of Air India with its assets and issues primarily related to debt (Usmani, 2017, June 28). While the government advocated an outright sale of the competitive airline, the Civil Aviation Ministry wanted to continue working as an interested party in the national airline after the management was handed over to the private sector (Correspondent, 2017, June 28).

History of Air India

In 1932, J. R. D. Tata introduced the first planned Indian airline, Tata Airlines, to pilot a single-engine flight from Karachi to Mumbai via Ahmedabad. Nevill Vintcent, a former Royal Air Force (RAF) pilot and J. R. D. Tata’s colleague, flew a plane from Bellary to Chennai to complete the trip.

In its initial year of service in 1933, Tata Airlines travelled 160,000 miles with 155 passengers and 9.72 tons of mail and made a profit of US $840 (₹60,000). In the years that followed, Tata Airlines continued to focus on sales under a mail order agreement with the Indian government.

In 1953 the government passed the aviation law and nationalized the entire aviation sector in India. Eight separate domestic airlines were integrated with Indian Airlines, which was the main domestic carrier, and Air India International took over foreign routes. This privilege has been perpetuated for the next 40 years. On 8 June 1960, the name of the carrier was formally truncated to Air India from Air India International. On 11 June 1960, Air India becomes the world’s first all-jet airline.

Air India experienced tough times in the early 1970s. Around 1976 and 1985, it incurred losses in 3 years. The slowdown in the world economy had a major effect on air transport throughout the globe, and India being no exception. After that, it was the world’s first airline to incorporate into its fleet the innovative A320 fly-by-wire built by French Airbus Industries in 1989.

Air India joined the Guinness Book of World Records for the maximum number of passengers rescued by a passenger airliner during the Persian Gulf War to deport Indian emigrants from Kuwait and Iraq.

It also introduced the Global Distribution System, which enabled agents to access various airline inventories. The government announced its price control policies and market-linked fares came into existence. After 37 years of operation in 1992, the government agreed to break the monopoly of Indian Airlines over domestic civil aviation by opening the doors to East-West Airlines to serve as a national level private airline.

An open-air policy has been adopted that has allowed air taxi companies to run chartered and unchartered flights from any airport and to decide on their flight schedules, freight and passenger fares.

Air India’s low-cost carrier, Air India Express (AI Express), was introduced in April 2005. The same year, an advance check-in service was made accessible at the Air India Building in Mumbai (Nariman Point).

After 2004, both the companies’ sales have been significantly impacted. Their market share decreased to a great extent and, to avoid rivalry, the then Minister of Civil Aviation (2004−2011), Praful Patel, suggested the merger of AIL and Indian Airlines Limited (IAL). Air India was the combined body of AIL and IAL.

Contradictory to their assumptions, the merged entity began to incur massive losses as of 2007. As a result, the major expectations of the merger to plough profits were not fulfilled. Air India suffered losses of ₹280 billion between 1 April 2007 and 31 March 2012.

World Aviation Industry

Although the aviation sector’s revenue is estimated to peak at $35.6 billion in 2016, soft landings in productive areas are projected to make a net income of $29.8 billion in 2017, the eighth consecutive year with a gross return on sales of Airline shows tolerance to shocks that had become the foundation of the sector. On an average, airlines are retaining $7.54 for every passenger they carry.

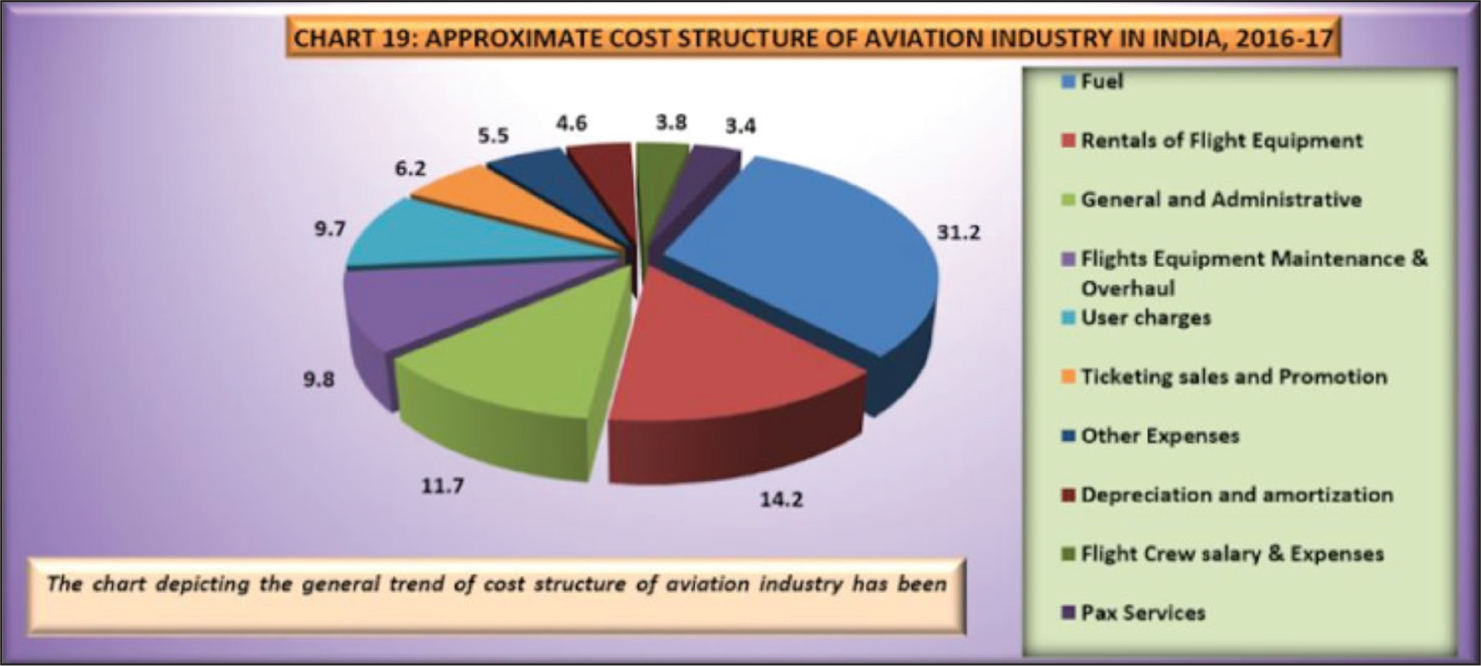

The predicted spike in oil prices will have the biggest effect on the 2017 outlook (Figure 4). Oil rates have hit $44.6/barrel (Brent) during 2016 and have been forecast to grow to $55.0 by 2017. It will raise the price of jet-fuel around $52.1/bar (2016) to $64.9/barrel. (2017). A share of 18.7 per cent of the sector’s cost structure is forecast for 2017, slightly below the previous high of 33.2 per cent in 2012-2013.

The incentive for demand for lower energy costs will stabilize in 2017 and reduce traffic growth to 5.1 per cent versus 5.9 per cent in 2016. Industrial production expansion is however projected to slip to 5.6 per cent after 6.2 per cent during 2016. Capacity development might also surpass increased demand as well as decrease the worldwide passenger load factor to 79.8 per cent from 80.2 per cent during 2016.

The repercussions of under-utilized factors are expected to be partially reconciled with global economic developments. World GDP is forecast to grow by 2.5 per cent in 2017 particularly in comparison to 2.2 per cent during 2016. Along with economic market improvements, this must help to improve the return from both cargo and passenger businesses.

Attractiveness of Air India Acquisition

Indian Civil Aviation Market

India is perhaps one of the fastest growing domestic aviation industries in the world and was to jump to third place in the air traffic after the USA and China (Brand India, n.d.a) (Table 5). According to the forecast by the International Air Transport Association (IATA), the region Asia-Pacific would be the driver with the greatest demand between 2016 and 2036, with even more than 50 per cent of new passenger traffic coming from the region (IATA, n.d.). This incentive in itself will enhance the motivation of every airline with strategic ambitions.

Air India

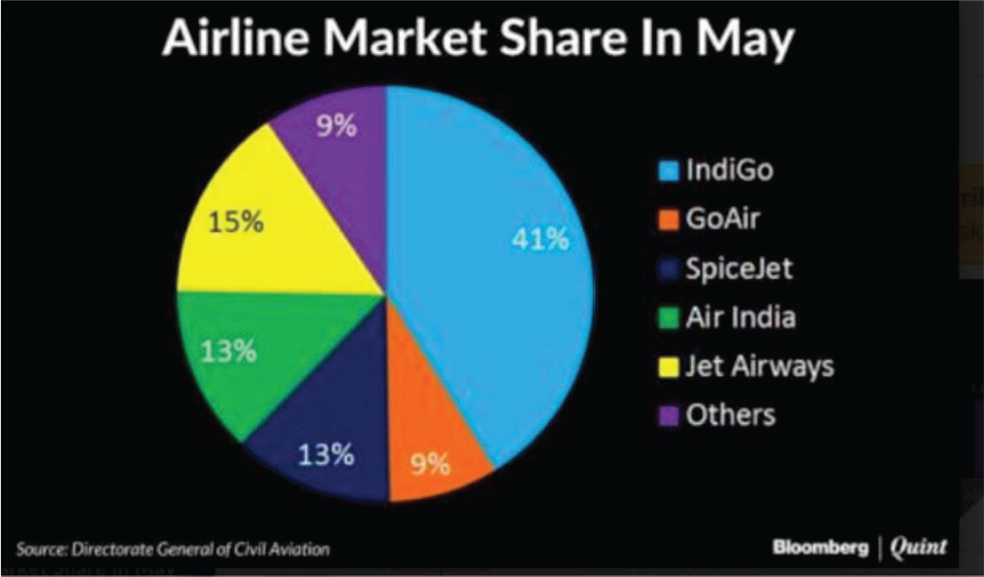

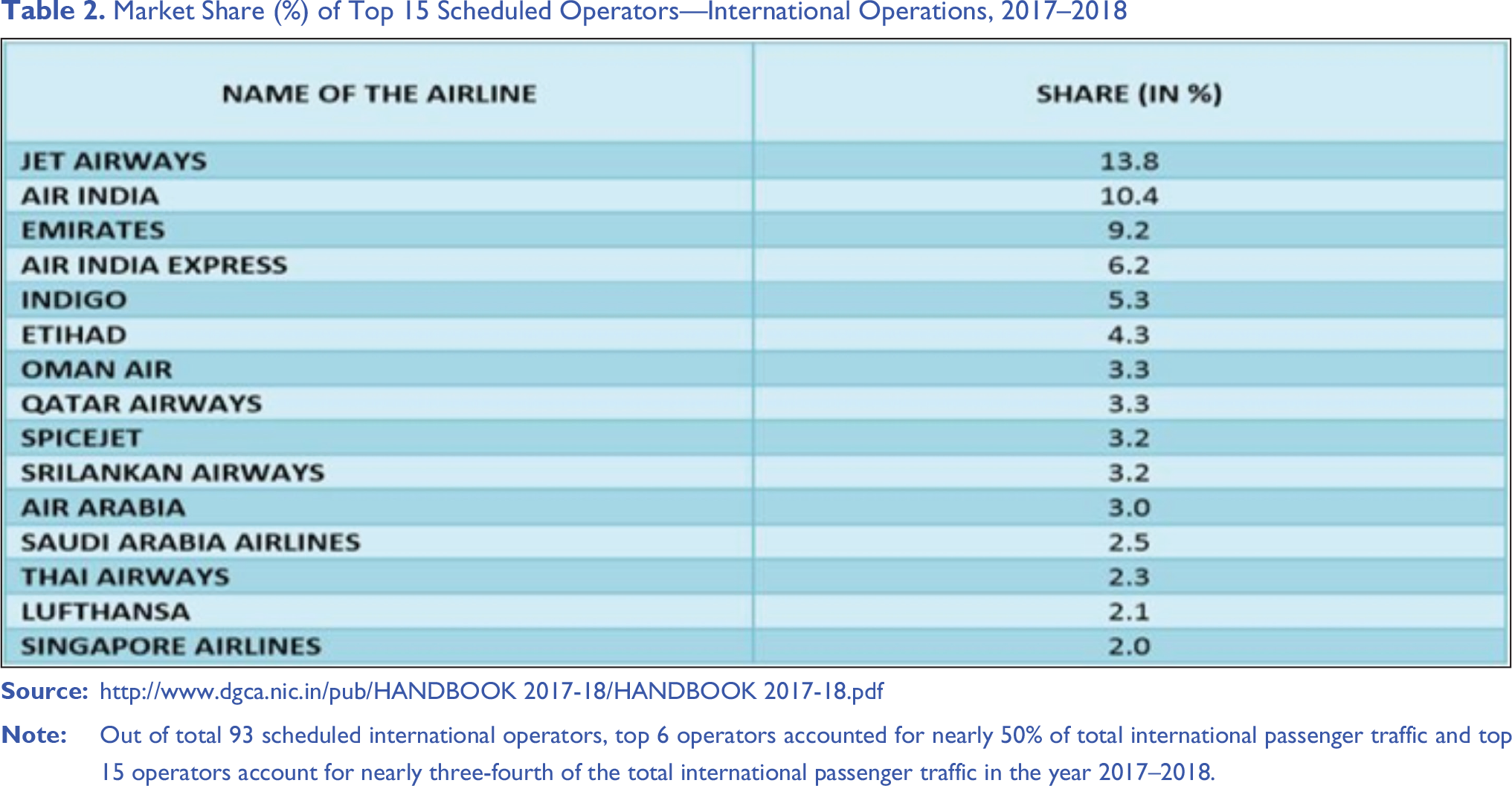

Air India operated a fleet of 140 long-haul aircraft which travelled to almost 41 overseas as well as 72 domestic destinations, representing 13 per cent of the domestic airline industry (Figure 5) and 10.4 per cent of foreign flight operations (Table 2).

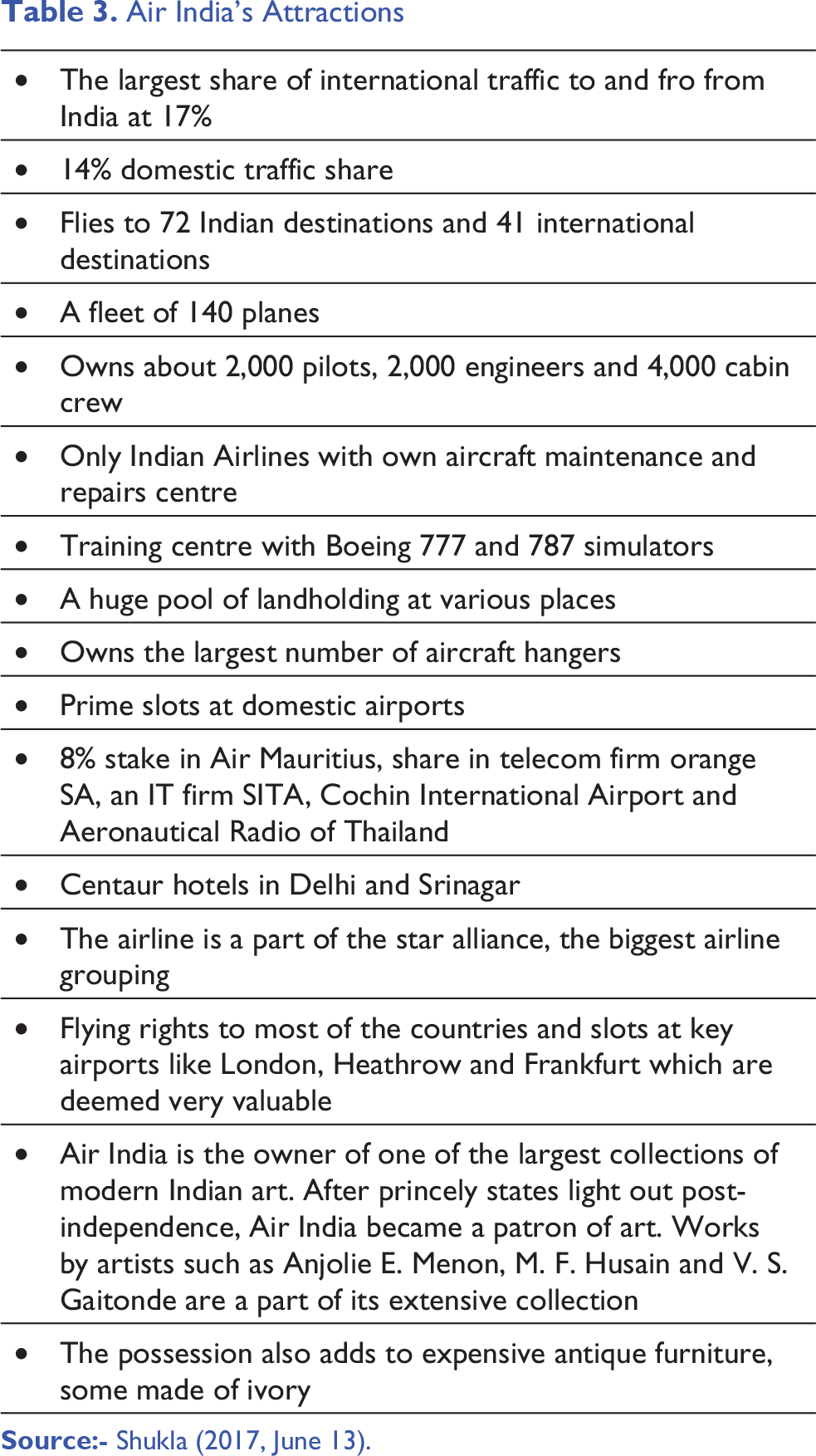

In addition, Air India’s home network, which spans nearly 55 destinations, has been a tremendous advantage to tapping growing Tier II and Tier III market demand in India and is considered one of the largest domestic aviation markets. Air India even had access to airplane parking and hangar amenities in many other significant domestic and global destinations (Table 3).

Besides, the airline was the largest international airline in India with a 17 per cent market share. There were also attractive slots at airports with limited capacity. This could be a significant advantage for a new or existing player looking to enter or expand their markets. As of 31 December 2017, Air India had approximately 280 slot machines out of a total of 3,739 national slot machines and 2,543 international slot machines per year in the Gulf and Middle East region, which included Abu Dhabi, Jeddah, Tel Aviv and Muscat (PTI, 2018, March 29).

Market Share (%) of Top 15 Scheduled Operators—International Operations, 2017–2018

Air India’s Attractions

Potential Bidders in the Market

In April 2018, an SBI Caps research report set Air India’s value at around $2.5 billion (approximately ₹16.2 billion). ‘While most Indian airlines are eligible to bid, the organization of funding could be challenging; airlines with strong balance sheets like IndiGo or those with strong sponsorship support like Vistara are better positioned’, said SBI Caps (Majumder, 2018, April 6)

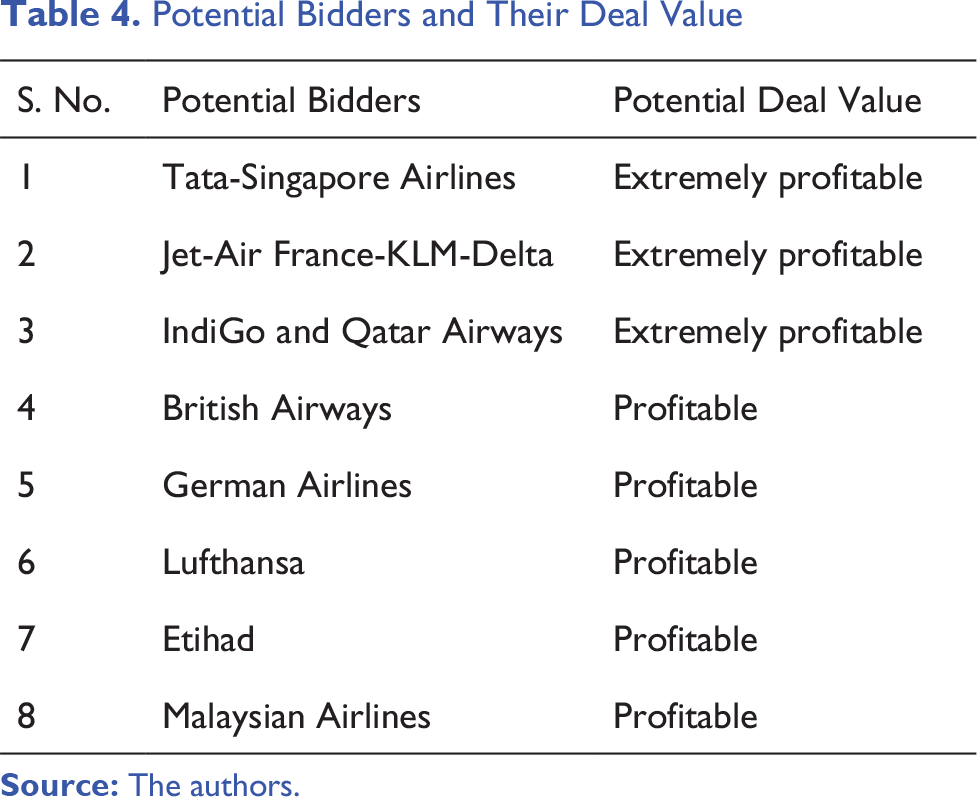

Potential Bidders and Their Deal Value

Immediately upon the approval of the government for the divestment, IndiGo was one among the early players to formally show their keenness in buying stakes in the national carrier (DH News Service, 2017, June 29) and it had expressed interest in acquiring the foreign operations of Air India and the AI Express (ET Bureau, 2018, April 6). Air India may be a lucrative opportunity for IndiGo to carry out its business strategy of ambitious growth in domestic and foreign markets (Haidar, 2018, April 5).

The oldest private airline of India, Jet Airways CEO, Vinay Dube also made the formal announcement indicating that they would consider bidding for Air India after having more clarity on what the government’s position was on the broad outline of Air India’s privatization (Shukla, 2018, March 29).

According to some media reports,

Tata Sons Ltd, which had expressed interest in Air India back in 2000, may again be attracted to future sales and N. Chandrasekaran, chairman of the group, held informal discussions with the government to purchase 51 per cent of the carrier, again collaborating with Singapore Airlines. (Kotoky & Parija, 2017)

Once the news of the Delta had arisen, the other two main airlines, United and American Airlines, had both started to sniff around (Gupta, 2018, March 23).

DEAL IndiGO

For IndiGo it could be a worthy deal, though countries largest carrier operates roughly 900 daily flights (PTI, 2017, July 10), covering 46 destinations including 7 international (Talukdar, 2017, May 9), Air India connects 72 domestic destinations, holds a share of 44 per cent of global passenger traffic among national carriers in comparison to IndiGo’s 9 per cent (Mody, 2017). Also, IndiGo was short of supply for both engineers and pilots and airport infrastructure constraints, IndiGo would land up sending their airplanes to Sri Lanka for repairs, Air India’s in-house technical and engineering department, and its and maintenance division with an overhaul division will be a major asset on its own (PTI, 2014, April 24).

The intangible advantages of Star Alliance providing connectivity to 1,269 destinations in more than 193 countries would make the deal sweeter (Mody, 2017, July 5). At the other side, IndiGo was faced with the challenges of preparing pilots and staff, but Air India has aircraft from Airbus and Boeing with various configurations that may contribute to the difficulty of fleet management. Nevertheless, for IndiGo, it may contribute to more troubling concerns regarding the domestic monopoly scenario, provided that its total market share would automatically grow to about 53 per cent (Gupta, 2018, March 24).

DEAL Tata-Singapore Airlines

The former and current chairman, Tata Group have been informally been discussing their interest in the airline with various government officials. Since the Joint-Venture airline, Vistara would start flying international destinations from the coming (Rai, 2017, June 21). Singapore Airlines that was under pressure with competition from such competitors as Thai Airways, Emirates and Cathay Pacific could become very strong carrier if they were successful in air India’s acquisition (HT Correspondent, 2017, June 22). The Tata Group and Singapore Airlines were interested in acquiring a 40 per cent stake in Air India way back in 2000 as well (Shukla, 2017, October 9). Apart from all these, Ratan Tata was passionate about aviation (just as he was about cars) (Shukla, 2017, June 21).

Considering India’s strategic position in Asia and its wide and rising exit business, Singapore Airlines as well as Delta have had several reasons to make an ambitious bid. Singapore Airlines’ huge fleet of A380 wide-bodied crew and aircraft has been seriously impacted after Emirates collaborated with Qantas. Passengers heading to Europe from Sydney or Melbourne in Australia had the ability to take advantage of the Emirates Hub in Dubai to skip Singapore., For Singapore Airlines, Air India could give the opportunity to aggregate and channel intra-India traffic to fill seats on its A380 flights to the USA, UK and Europe (Gupta, 2018, March 23).

DEAL Jet-Air France-KLM-Delta

Until now (2018) Gulf Airlines has completely controlled traffic via India to both USA and Europe, utilizing its base in Dubai as well as Abu Dhabi, and gradually turning Asia into the hub of the stage (Chowdhury, 2017, April 20). India is expected to attract the focus of US airlines. US switching over to India, following a number of consolidations, the three main carriers, Delta, United Airlines and the American Airlines, are already in pretty good condition. For Delta, a better role in India offers a realistic opportunity to reclaim market share throughout the rising Indian-American business (Gupta, 2018, March 24). For this cause, the USA needed to link with a local collaborator like those of Jet-Air and KLM-Air France in Europe to tackle the gulf airline initiative. Inspired by Delta’s participation in Air India divestment bid, the UK and the USA are expected to join in the bidding war (Gupta, 2018, March 23).

Although AI Express, a low-cost carrier, so far has done a decent job of taking advantage of both the Gulf and South East Asia traffic from its Kerala headquarters. It is said to have been in good condition and to have seen substantial progress. One explanation behind this is that full-service providers no longer retain adequate leverage in negotiations and, in particular, the domestic sector has shifted to low-cost carriers.

Until recently (March 2018), it was expected that only three Indian firms would bid for the sale, they learned that five more international airlines (British Airways, German Airlines, Lufthansa, Etihad and Malaysian Airlines) (Digital, 2018, April 12) had also shown their interest.

The Market Perception

The Tata Group is assumed to be ‘getting closer’ to a Singapore Airlines partner to bid for Air India, according to the Times of India report (Moneycontrol, n.d.). The partnership arrangement is stated to be in place and the Tata Group is anticipated to combine AI Express with Air Asia India, stated in the article. The Tata Group has approached Tony Fernandes, a Malaysian entrepreneur who owns a 49 per cent stake in AirAsia India, for approval of the acquisition of AI Express (Economic Times, 2020, February 5). The story would close the circle of change and not only underlines the sad situation of state-owned companies but also how India’s indigenous market communities fought to disappear even after decades of socialist politics (Economic Times, 2019, November 5).

Regardless of the desire to buy Air India, a serious bidder will not appear until the government decides on the operating mode of sale. The exact number of those who will appear as the top bidders will be announced later when the bidding process is officially announced (Figure 6). While this often happens, a strong list of applicants will certainly have an impact on the size of offers, which is why the government hoped it would be the happiest. Ultimately, the seriousness with which they ultimately bid depends on how important the deal is to their long-term strategic interest. The government had made it clear that it might not divest if the bid price was below the floor price (Financial Express, 2018, May 31).

The government had announced the invitation for expression of interest (EoI) submission on 28 March 2018 (Mishra, 2018, May 1). The buzz received (about Air India stake sale) stood undoubtedly encouraging. The Indian Ministry of Civil Aviation received nearly 160 enquiries from potential bidders (Vikas, 2018, June 12).

However, on 31 May 2018, 5:45 As informed by the transaction adviser, no response had been received for the Expression of Interest floated for the strategic disinvestment of Air India. (Mishra, 2018, May 31)

As the final deadline was approaching, the government officials were getting anxious about the nature of potential bids. But much to their dismay, they realized that Air India did not garner any bids. Despite all signs to the contrary, corporate India is not that keen on acquiring an asset like Air India. Why did Air India not receive any bids? This question will be discussed ad nauseam in the coming days.

Questions for Discussion

Why do you think Air India did not attract any bids?

Do you think Air India was valued the same by all bidders? Or did some bidders have a special affinity for Air India when compared to others?

What could the Government have done to facilitate more enthusiasm among potential bidders?

What do you think were the points of uncertainty for a potential bidder in this exercise?

Footnotes

Acknowledgements

We are very thankful to Prof Viswanath Pingali (IIM-Ahmedabad) for his keen and kind reviews in supervising this Case Study.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.