Abstract

The study aims to comprehensively examine the behavioral biases of fund managers by conducting a bibliometric analysis of research papers published during the years 2011–2022 from the Scopus database based on the keywords searched for behavioral biases of fund managers. One hundred and thirty-five articles have been chosen after careful review. This article explains the most cited articles, top authors, leading countries, prolific journals, and important keywords. This study has identified 10 different types of behavioral biases which are summarized in this article. In this review article, we only considered the journal articles excluding conference publications, editorials, and book chapters. This article is based on the existing literature on behavioral biases in investment decision-making processes. This study will be helpful for researchers and academicians to understand the impact of behavioral biases on investment decisions and to reduce it. Finally, this research will provide a roadmap for future research.

Introduction

In the last two decades, researches on behavioral biases have shown a significant rise. Traditional financial theory assumes investor rationality in investment decisions. The efficient market hypothesis (EMH) emerged as a prominent theory in the mid-1960s. It first appeared in Eugene Fama’s book (1970) Efficient Capital Market: A Review of Theory and Empirical Work. Malkiel and Fama (1970) stated that current stock prices fully reflect the existing information.

According to the theory on behavioral finance, individual, retail, and institutional investors make certain irrational decisions and these behavioral biases impact the investment performance (Ahmad et al., 2017). The efficient utility theory (EUT) states that investors should make rational decisions by evaluating each alternative’s benefit and its associated risk and then make a balanced decision. After the 1970s, the empirical results were not consistent with EMH and EUT. Kahneman and Tversky (1979) proposed a prospect as a descriptive theory of decision-making in risky situations; also it was an alternative to EUT for decision-making under uncertainty. It described how humans make decisions when presented with several choices. The theory was depicted in the article ‘Prospect theory: An analysis of decision under risk,’ published in the ‘Econometrics’ journal in 1971. This article dealt with the critiques of the EUT and provided prospect theory as a substitute.

Behavioral finance has appeared as a fascinating field of study in recent years. It tries to explain how investors make financial decisions depending on their cognitive and psychological biases. However, the existing theories are often criticized for their inability to fully comprehend the irrational behaviors of investors. The bounded rationality theory suggests that investors have limited information and cognitive resources and hence make suboptimal decisions. The prospect theory is a function of gain or loss in relation to reference point. It suggests that the investors inclined to focus on possible gains and losses on a particular transaction rather than estimating total wealth (Olsen, 1997). However, individual investors are usually more sensitive to losses than to gains (Kahneman & Tversky, 1979). While these theories have provided useful insights, they have not been able to capture the complexity and dynamic nature of human behavior (Ahmad et al., 2017).

This review article focuses on fund managers, who play a crucial role in investment decision-making. The authors argue that fund managers are also susceptible to behavioral biases and may make irrational decisions. The article identifies 10 behavioral biases that might impact the decision-making of investors. The first bias is anchoring, where investors tend to rely too heavily on the initial information they receive. The second bias is the disposition effect, where investors hold onto losing investments for too long and sell their winning stocks too soon. The third bias is overconfidence, where investors are highly optimistic about their trading results and are overconfident about their abilities, skills, and future expectations. The fourth bias is herding, where investors follow the mass rather than their own analysis. The fifth bias is home bias, where investors are willing to invest in companies that are located in their home country. The sixth bias is loss aversion, where investors are more inclined to take risks to avoid a loss rather than to make a gain. The seventh bias is representativeness, where investors make decisions based on their stereotypes and past experiences. The eighth bias is self-attribution bias, in which investors attribute their success to their own abilities and hard work and put the blame for their failures on external factors. The ninth bias is emotion, where investors let their emotions, such as fear and greed, guide their decision-making. The final bias is conservatism bias, where investors are slow to update their beliefs and tend to stick with their initial assumptions. The authors argue that understanding these biases can help fund managers make better investment decisions and avoid costly mistakes.

In conclusion, this review article highlights the importance of studying behavioral biases in investment decision-making, particularly among fund managers. By identifying and understanding these biases, fund managers can improve their decision-making and avoid common pitfalls. However, it is important to note that these biases are not exclusive to fund managers and can affect any investor. As such, a deeper understanding of these biases can benefit all investors, regardless of their level of expertise.

Researchers propose a bibliometric analysis to answer the following questions:

What are the publication trends in the area of fund managers’ bias? Which are the most influential articles, authors, organizations, countries, and journals? Based on the co-citation of cited references, which are the most highly cited references? Based on the co-occurrence of author keywords, which are the most occurring and strongly linked keywords? Through bibliometric coupling with countries, which are the most influential countries? What are the directions for future research?

The remainder of this article is divided into six sections. The ‘Behavioral Biases and Investment Decision-making’ section discusses the behavioral biases in investment decision-making, the ‘Data and Methodology’ section describes the methodology adopted for this review article, the ‘Bibliometric Analysis (Classification and Analysis of the Literature)’ section displays the results of bibliometric analysis, the ‘Limitation and Scope for Further Research’ section discusses the limitations and scope for future research. The ‘Conclusion’ section concludes the article.

Behavioral Biases and Investment Decision-making

Anchoring is a cognitive bias that occurs when people focus too heavily on pre-existing information or little information, in order to make a decision. Typically, such bias is developed when an investor pays attention to unjustified information, which causes errors in decision-making (Saravanan & Totawar, 2021). Owusu and Laryea (2022) examine how anchoring affects investor decision-making regarding mutual funds and how this bias varies based on gender and financial literacy. They show that females are more likely to anchor than males. Additionally, having more financial knowledge enhances the possibility of anchoring. Furthermore, anchoring bias can be overcome through logical reasoning, diligence, and adopting practical critical thinking rather than emotion (Saravanan & Totawar, 2021). Nevertheless, some significant studies (Kliger & Kudryavtsev, 2008; Shah et al., 2018; Waweru et al., 2008) have been conducted on anchoring biases in investment decisions.

Herding behavior refers to a situation in which investors follow the decision of the crowd instead of their own independent analysis. Casavecchia (2016) stated that the managers who do not have herding behavior perform better as compared to the herding managers. Further, some prominent studies were conducted in this field (Economou et al., 2015; Hudson et al., 2020; Lütje, 2009).

Disposition effect was first introduced by Shefrin & Statman, 1985. It refers to the propensity of the investor to sell winning stocks quickly, but unwillingness to sell losing stocks manifests the irrational investment decision of the investor. Chiang and Huang (2017) state that flow-induced disposition behavior had an impact on fund returns. As a result, selling pressure brought unanticipated outflows which caused the disposition biases of fund managers and harmed the fund performance. Women are more inclined to sell stocks after price rises. Thus, women have a significantly larger disposition than men (Rau, 2014).

Representativeness bias was first developed by psychologists Kahneman and Tversky (1979) during the 1970s. It is a cognitive bias that leads investors to assume that the past record of the remarkable performance of a particular company is a representative of the overall performance that the firm will continue to produce in the future.

Overconfidence is a cognitive bias in which investors are highly optimistic about their trading outcomes. It makes investors too confident about their skills and knowledge and they do not consider the investment risk. Odean (1998) has mentioned overconfident investors trade too much based on the inaccurate belief on their trading skills and information correctness. However, if experienced investors are subject to overconfidence bias, it can be due to high trading activity after a good past performance. Chow et al. (2011) stated that when the performance is good, overconfident investors increase their investment levels. Following that, their performance declined. Puetz and Ruenzi (2009) found that positive past performance leads to overconfidence. Mundi and Nagpal (2020) examined the overconfidence among finance managers and its influence on predicted market return. They found that finance managers’ overconfidence affects their forecasted market returns, also they demonstrated that managers have miscalibrated the situation, it is only due to their overconfidence, not their skills. Further, some significant studies (Adebambo & Yan, 2017; Mishra & Metilda, 2015; Palomino & Sadrieh, 2011; Waweru et al. 2008) have also contributed to this area.

Home bias was first introduced by French and Poterba (1991) in their article titled ‘Investor diversification and international equity markets’ and found that investors throughout the world maintained a sizable amount of their wealth in local assets. It refers to the situation where investors favor their home nation’s market over other markets and thus investing disproportionately more in the home country assets over foreign assets in their portfolio.

Loss aversion bias was covered by the prospect theory (Kahneman & Tversky, 1979). It is a phenomenon under which investors are affected more by the loss than by the gain. Thaler and Johnson (1990) revealed that the level of loss aversion is largely influenced by prior outcomes when it comes to gain and loss. Bailey et al. (2011) found that loss aversion has significantly affected the investor behavior and their decision-making. Kahneman et al. (1991) stated that the investors are influenced by loss aversion and make irrational investment decisions.

Self-attribution bias: It is a tendency in which investors ascribe the success to their own abilities and actions, while they attribute their failure to beyond their control. This theory was first proposed by Bem (1972) in his article titled ‘Self-perception theory.’ Ady (2018) stated that investors are emotionally unstable act irrationally, which results in inefficient portfolio selection and poor returns. Charles and Kasilingam (2015) found that lack of cognition, inexperience, and impetuosity lead to individuals’ emotional instability. Bachmann (2018), Bazley et al. (2021), Peng et al. (2011), and Sourirajan and Perumandla (2022) found that emotional behavior can impact the investment decision.

Conservatism bias is one of the most significant biases that impact the investment decisions of investors. It refers to a situation in which investors predict their own beliefs and do not accept others’ decisions.

Data and Methodology

Bibliometric analysis is quite prevalent and an exacting technique for analysing and summarizing vast quantities of bibliometric data to identify the emerging trends of a broad topic or field. The techniques for bibliometric analysis are classified into two broad categories: performance analysis and science mapping. Performance analysis considers the contributions of research components (e.g. authors, organizations, journals, and countries) of the area, whereas science mapping emphasizes on the connection among the research constituents (Donthu et al., 2021). Performance analysis employs a variety of bibliometric measures to evaluate the effect of the identified themes and thematic areas. Science mapping, also known as bibliometric mapping, depicts the connection between various sciences, specialties, fields, and particular articles or authors (Cobo et al., 2011). It includes techniques like citation analysis, bibliographic coupling, co-citation analysis, co-word analysis, and co-authorship analysis. In recent years, it has gained tremendous popularity due to the accessibility and advancement of bibliometric software like VOSviewer and databases like Scopus and Web of Science (WoS), and it manages large-scale scientific data and creates scientific impact on research (Donthu et al., 2021).

Data Analysis Set

This review article is based on the bibliometric analysis to emphasize the current research trends and their results on the fund managers’ bias. It used the articles which were indexed in the Scopus database. Scopus database has been regarded as the largest storage of citation data and abstracts (Aznar-Sánchez et al., 2019; Mugomeri et al., 2017) and has a huge volume of indexed publications (Mongeon & Paul-Hus, 2016).

Search Strategy

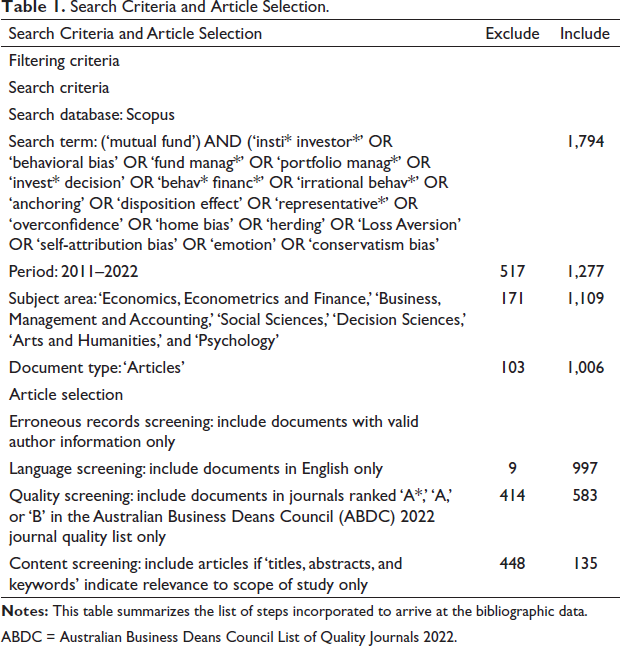

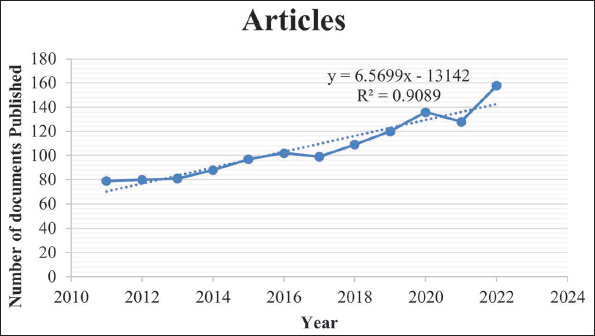

To conduct this bibliometric analysis, we established a search criteria (Table 1) and identified the relevant keywords. The following criteria have been used to find the research articles: (‘mutual fund’) AND (‘insti* investor*’ OR ‘behavioral bias’ OR ‘fund manag*’ OR ‘portfolio manag*’ OR ‘invest* decision’ OR ‘behav* financ*’ OR ‘irrational behav*’ OR ‘anchoring’ OR ‘disposition effect’ OR ‘representative*’ OR ‘overconfidence’ OR ‘home bias’ OR ‘herding’ OR ‘Loss Aversion’ OR ‘self-attribution bias’ OR ‘emotion’ OR ‘conservatism bias’). The search was conducted on March 17, 2023, and included articles starting from 2011 to 2022 because at that interval the research work done on fund managers’ bias started expanding rapidly (Figure 1). While performing the initial search, we found 1,794 documents. After having specified the time span (2011–2022) and subject area, namely, ‘Economics, Econometrics and Finance,’ ‘Business, Management and Accounting,’ ‘Social Sciences,’ ‘Decision Sciences,’ ‘Arts and Humanities,’ and ‘Psychology,’ we got 1,109 documents.

Search Criteria and Article Selection.

ABDC = Australian Business Deans Council List of Quality Journals 2022.

Publication Trends of the Fund Managers’ Bias from 2011 to 2022.

Data Extraction

Blind peer-reviewed journal articles only.

Articles are exclusively published in the English language and provide full-text access.

Subjects are specific to economics, econometrics and finance; business, management and accounting, social sciences, decision sciences, arts and humanities, and psychology.

Articles listed in ‘A*,’ ‘A,’ or ‘B’ in the 2022 Australian Business Deans Council (ABDC) journal quality list.

In order to conduct content screening, we reviewed the titles, abstracts, and keywords of 583 articles which were relevant to the scope of study only. Therefore, a total base of 135 articles was lastly selected for conducting bibliometric analysis.

Publication Trends

The publication trends of fund managers’ bias have been a topic of interest in recent years. Figure 1 illustrates the number of documents published on the subject over the years. As per the figure, there has been a steady rise in the publication of articles from 2011 to 2022. However, there were two instances, in 2017 and 2021, where the number of documents published decreased.

The decline in 2017 may be attributed to various global economic factors, a market crash due to the Trump presidency, an economic recession brought by Brexit in the United Kingdom, and the collapse of the Eurozone due to the implosion of the Italian banking system (Martin, 2017).

Similarly, the decrease in 2021 can be attributed to the global pandemic and the financial crisis that ensued, as mentioned by Ritika et al. (2022). The pandemic led to unprecedented changes in the global economy, resulting in significant fluctuations in the stock market, which could have impacted the publication trends of fund managers’ bias. To determine the consistency of the publication trends, a regression line was drawn, and the coefficient of determination (R square) was calculated as 0.9089, indicating a statistically significant increase in the number of articles published over the time period. This indicates that despite the occasional fluctuations, the trend of publishing articles on fund managers’ bias has been consistent over the years.

It is noteworthy that the publication trends of fund managers’ bias have become increasingly relevant and are gaining greater attention from academicians and practitioners. This is due to the growing awareness of the importance of understanding the biases that can affect fund managers and their decision-making processes, which can ultimately impact investors and their returns.

Categories of Documents

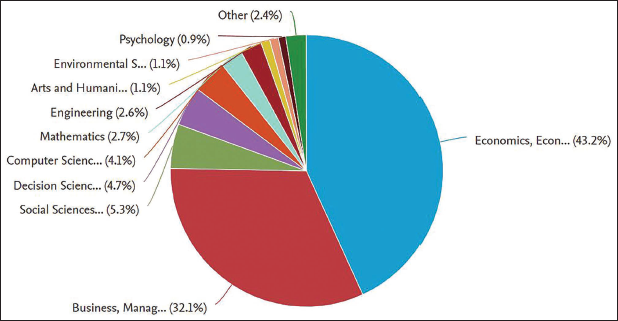

The data presented in Figure 2 highlights the distribution of subject categories in terms of their contributions to the total publications. The results indicate that the subject category of ‘Economics, Econometrics and Finance’ had the highest contribution of 43.5% to the total publications. Following this, the subject category of ‘Business, Management and Accounting’ made a contribution of 32.1%, making these two subject areas the major contributors to the total subject area, accounting for 75.3% of the total publications. On the other hand, the subject category of ‘Psychology’ had the lowest contribution of 0.9%. This indicates that research in the psychology behind investment decision-making has not been as prevalent compared to other subject categories in the given dataset.

Search Criteria for Article Selection

We considered data only from 2011 to 2022, as we observed the research on this area started rising from 2011 and did not take 2023 data, as of 2023 are continuing till now and keeping that we had excluded it.

Bibliometric Analysis (Classification and Analysis of the Literature)

Most Influential Article

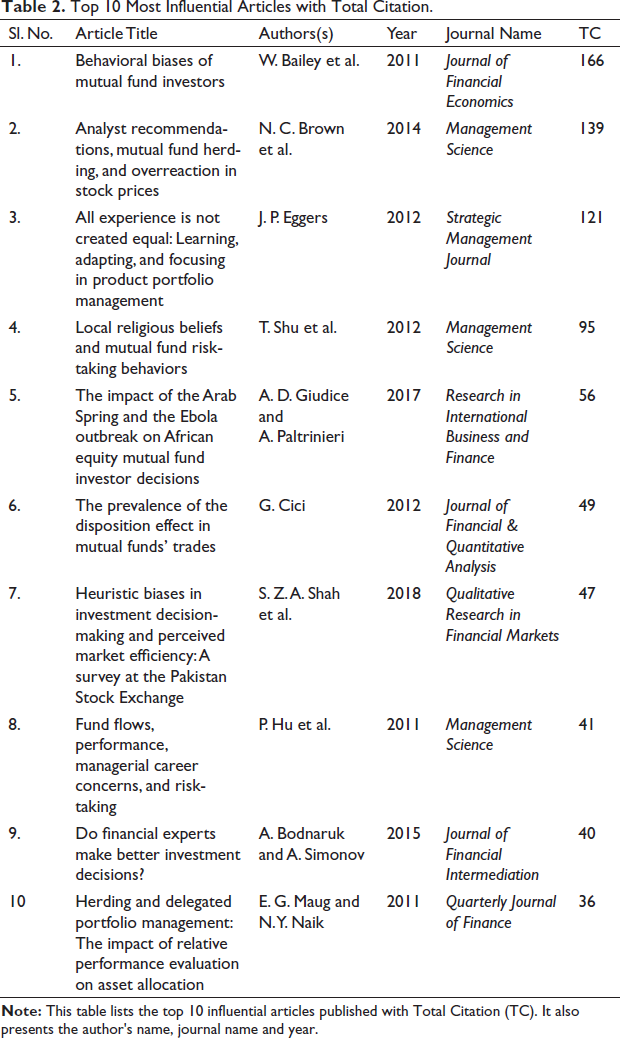

In this portion, we analysed the chosen articles depending on their total citations. Table 2 enlists the top 10 most influential articles from 135 selected articles. The article (Bailey et al., 2011) ‘Behavioral biases of mutual fund investors’ has achieved the highest number of citations 166 in Table 2, which discovered that sophisticated investors are more inclined to invest in mutual funds. However, investors who express strong behavioral biases are less likely to hold mutual funds or choose mutual funds improperly. The second leading article (Brown et al., 2014) ‘Analyst recommendations, mutual fund herding, and overreaction in stock prices’ has obtained 139 total citations, which stated that managers who are more concerned about their careers tend to closely monitor analyst revisions. Overall, mutual funds responded heavily to the analyst revisions and are supported by evidence from high frequency trading data of a sample of funds. The last article (Maug & Naik, 2011) ‘Herding and delegated portfolio management: The impact of relative performance evaluation on asset allocation’ got 36 citations which stated that in some situations fund managers ignore their own better knowledge and choose to go with the flow of information to minimize deviation from their benchmark, also they concluded that incentive assistances for fund managers have a significant role in their decisions about asset allocation.

Top 10 Most Influential Articles with Total Citation.

Most Influential Authors, Organizations, and Countries

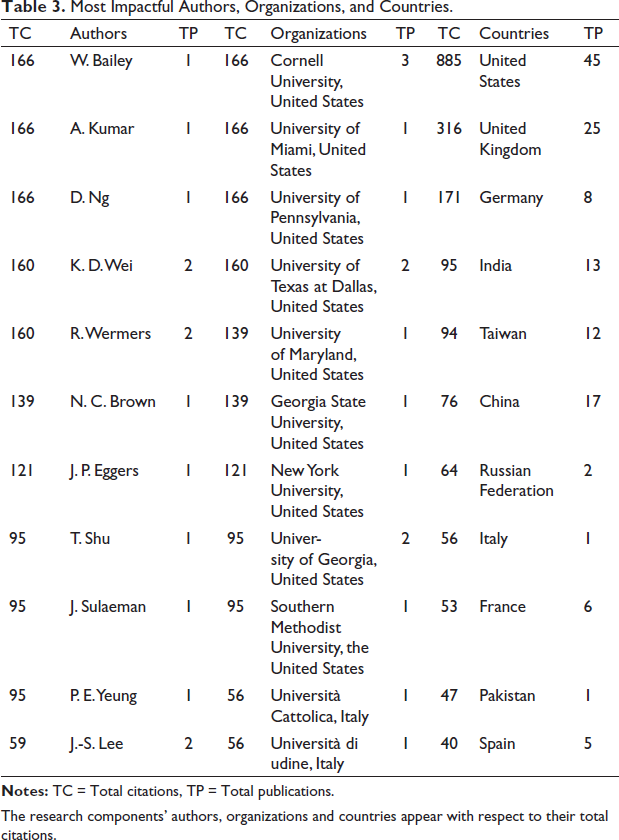

Table 3 provides valuable insights into the top impactful authors, organizations, and countries in the domain of fund managers’ bias. It is interesting to note that W. Bailey, A. Kumar, and D. Ng have emerged as the most impactful authors in this field, with each of them having 166 citations to their credit. This highlights the significant impact that their research on the field and their contribution to the academic discourse.

Most Impactful Authors, Organizations, and Countries.

The research components’ authors, organizations and countries appear with respect to their total citations.

In terms of countries, the United States has emerged as the leader, with 45 publications in the field of fund managers’ bias. This indicates the strong interest and contribution of researchers from the United States in this area of study. Additionally, the United States has achieved the most citations (885) for their publications, indicating the quality and impact of the research from this country.

Regarding the most influential organizations, Cornell University, University of Miami, and University of Pennsylvania, all from the United States, have emerged as the top contributors, each with 166 citations to their credit. Among these, Cornell University has the highest number of publications (three), indicating its strong presence in the field of fund managers’ bias research.

Overall, these findings provide valuable insights into the most influential authors, organizations, and countries in the domain of fund managers’ bias, highlighting the impact of their research on the academic discourse and shaping the future on this field.

Most Influential Journals

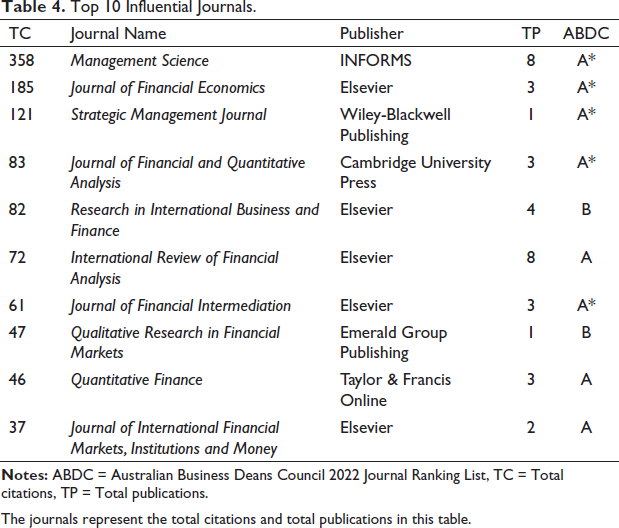

Table 4 provides an informative overview of the top journals that work on fund managers’ bias. By analysing the number of citations received by each journal, it is clear that ‘Management Science’ and ‘Journal of Financial Economics’ are the two most productive journals in this field, with 358 and 185 citations, respectively. These journals have published ground-breaking research that has significantly impacted the study of fund managers’ bias.

Top 10 Influential Journals.

The journals represent the total citations and total publications in this table.

However, it is also noteworthy that productivity is an essential metric to consider in assessing a journal’s impact in a particular field. When evaluating the productivity of the journals in Table 4, we find that Management Science and International Review of Financial Analysis are the two most productive journals. These journals have published eight research articles each, which is a significant contribution to the field.

It is fascinating to observe that the majority of the journals in Table 4 are highly ranked on the 2022 ABDC journal quality list, with most being listed in the ‘A*’ or ‘A’ categories. This indicates that these journals are highly regarded by the academic community and are recognized for their high-quality research in the field of fund managers’ bias.

In conclusion, Table 4 provides a comprehensive overview of the top journals that focus on fund managers’ bias. It highlights the most significant and productive journals in this field, as well as their rankings on the ABDC journal quality list. Researchers and academicians interested in the study of fund managers’ bias can use this table to identify the most relevant and highly regarded journals to publish their work.

Science Mapping

In this review article, we aim to conduct a comprehensive scientific mapping of fund managers’ bias. To achieve this, we employed bibliometric analysis techniques like co-authorship, co-occurrence, co-citation, and bibliographic coupling analysis. These techniques allowed us to identify the key contributors, topics, and trends in the field and to gain a deeper understanding of the intellectual landscape. This bibliometric analysis was conducted using the VOSviewer, is a software program for creating and visualizing bibliometric network which helped us to identify the relevant patterns and relationships.

In terms of data sources, we have access to several databases that can be used with VOSviewer, including WoS, Scopus, Lens, Dimension, and PubMed. Each of these databases has its own strengths and limitations, and the choice of database will depend on the research question and the availability of data. Overall, the use of bibliometric analysis and VOSviewer visualization can greatly enhance our understanding of the intellectual framework of a given domain. By identifying key authors, publications, and concepts, we can gain insights into the evolution of the field and the directions it may take in the future.

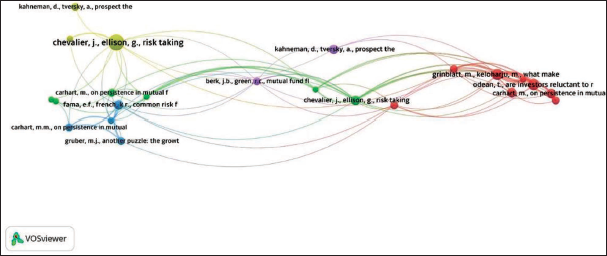

Co-citation and Cited References

Co-citation analysis is a widely used technique to identify influential research articles, authors, or topics in a particular field. In a co-citation analysis, two publications appear in the reference list of other publications (Donthu et al., 2021). In this study, we used the VOSviewer software for co-citation analysis. We set a minimum threshold of three cited references to ensure that only highly cited papers were included in the analysis. The resulting network of co-cited references is shown in Figure 3, which provides a visual representation of the connections between highly cited papers. Our analysis revealed that J. Chevalier, T. Odean, M. Grinblatt, and M. Keloharju were highly co-cited references in the domain under investigation. These references were cited together in multiple articles, indicating their importance and influence in the field. The co-citation of these references suggests that they are highly relevant to the research topic and have contributed significantly to the development of the domain.

Co-citation Analysis with Cited Reference.

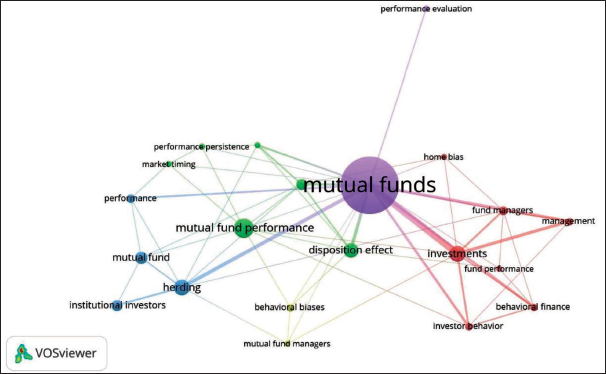

Co-occurrence and Author Keyword

Co-occurrence analysis is a content-analysis technique that used to understand the pattern of connection between the pairs of items. In this study, it was used to explore the relationships between different keywords used by authors in their publications. To conduct the co-occurrence analysis, we employed the VOSviewer software. We set a minimum threshold of three occurrences for each keyword to ensure that only the most relevant and frequently used terms were included in the analysis. The resulting network visualization map, presented in Figure 4, provides a clear picture of the co-occurrence patterns between author keywords in our article. We observed that the term ‘mutual fund’ had the highest occurrence and strongest link with other keywords, indicating its importance in the context of our research. This was followed by other key terms such as mutual fund performance, herding, and disposition bias, which also had strong connections to other relevant keywords.

Co-occurrence Analysis with Author Keywords.

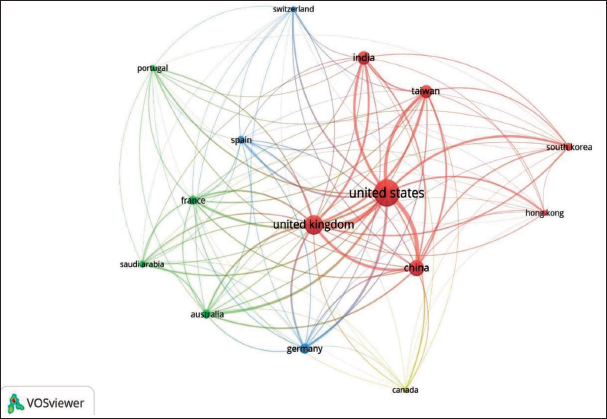

Bibliometric Coupling and Countries

Bibliographic coupling is a technique used in bibliometrics to identify the similarity between two research works by examining the references they have in common in a third work. By analysing the connection between different countries in academic research, the bibliographic coupling can provide insights into the collaborations and networks that exist between researchers in different regions of the world.

To further understand the bibliographic coupling between different countries, we used VOSviewer, a popular software tool for visualizing bibliometric data. The results of our analysis are presented in Figure 5, which provides a graphical representation of the bibliographic coupling between the nations. According to our findings, the United States has the highest number of documents (45) with 885 citations and a total link strength of 7,546. This suggests that the United States is a major player in academic research, with a significant number of publications and a strong network of collaborations with other researchers around the world.

Bibliometric Coupling with Countries.

The United Kingdom, on the other hand, has 25 documents with 316 citations and 4,723 link strengths, indicating that it also has a significant presence in the academic community and collaborates extensively with researchers from other countries.

China, with 17 documents, 76 citations, and 3,485 link strengths, shows that it is also an active participant in academic research, perhaps not yet at the same level as the United States and the United Kingdom. However, given the increasing focus on research and development in China in the recent past, it is probable that the country will continue to grow in importance as a contributor to the global academic community.

Limitation and Scope for Further Research

In this review study, we conducted a thorough examination of the literature on emerging research areas using bibliometric techniques. We focused solely on articles indexed in the Scopus database, eliminating conference publications, editorials, and book chapters. However, it is worth noting that future research could expand on our findings by incorporating other databases, such as WoS and Dimension, into the analysis. Additionally, alternative tools like Bibliometrix R, Bibexcel, and Citespace could be employed to investigate the research areas in more detail.

In this study’s visual representations through VOSviewer displayed a low density of various biases, including the home bias, indicating that this area is still an under-researched topic, presenting ample opportunities for future research. Finally, we noted that there are few works of literature on biases, such as conservatism, representativeness, emotion, self-attribution, and conservatism bias, indicating that further study in this area is possible.

Moreover, with the advancements in technology, robotic services have emerged in the finance and investment industry in the form of robo-advisors (Bhatia et al., 2020). Therefore, further research could be conducted to explore how robo-advisors can mitigate the impact of behavioral biases in investment decision-making. The integration of robo-advisors into investment decision-making processes could have a significant impact on reducing the negative effects of biases on financial decisions. Thus, it is crucial to explore this area further and determine the extent to which robo-advisors can assist investors in making informed investment decisions.

Conclusion

According to behavioral finance, there are a number of behavioral biases that might impact the investors’ decision-making process, which leads them to make irrational and illogical decisions. There is a need for a unified framework to deal with the irrational behaviors’ origin, causes, and effects.

This bibliometric study on fund managers’ bias discusses the trend of the research article on behavioral biases of fund managers through the Scopus database. For the methodological perspective, we identified the trends in this area and classified the top 10 authors’ publications with their citations, journals, and organization. In the scientific mapping, we analysed the co-occurrence of all author keywords, co-citation with cited references, and bibliographic coupling of countries. First, we only used the Scopus database to collect the data. In order to achieve the intended goals, the search was carried out using the search criteria. There were 135 total articles in the sample. Accordingly, it was noted that the studies have been rising over time in this area, with a notable rise starting in 2014. In addition, 2022 stood as the year with most publications, 158. Additionally, it was discovered that Management Science had the most papers in their journal. The most cited article was that by Bailey et al. (2011) with 166 citations, followed by Brown et al. (2014) with 139 citations and Eggers (2012) with 121 citations. Countries such as the United States, the United Kingdom, China, Taiwan, and India produced more publications. By doing qualitative analysis, the most cited countries are the United States followed by the United Kingdom, Germany, and India. The United States is the most productive country in the current study because the most prolific institutions such as Cornell University, University of Miami, University of Pennsylvania, and so on are from there. With the help of this article, we analyse the behavioral biases for further study and create the finest strategy and framework for making a rational decision.

In order to overcome behavioral biases, the knowledge of psychology and behavioral finance is necessary. This study has outlined the behavioral biases of fund managers, along with further research strategy, new trends, and leading topics. It will help the academicians and practitioners to create a structure or strategy that helps investors to recognize their biases and make rational decisions.

Author Contributions

All authors contributed equally to this work.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.