Abstract

Financialized urban governance means that local governments have been increasingly reliant on financial techniques and in some extreme cases, been captured by shareholders’ interests. However, financialized governance mutates with various characteristics of local governance. This paper unpacks financialized urban governance in China based on the operation of Shanghai Municipal Investment Corporation (SMI). The Shanghai municipal government uses SMI as an intermediary to finance urban development. Based on the latest corporatization of SMI, we illustrate an embryonic form of financialized governance in which the Shanghai municipal government relies on financial means especially shareholding to manage and support SMI. In doing so, the municipal government internalizes financial techniques to manage state assets, seek funding, and guide urban development projects. The power of the state is not undermined during the process of financialization. Instead, the Shanghai government extends its power to the financial market to achieve its goals.

Introduction

In western studies, local governments have been at the frontier of financial expansion to deal with local budgetary shortfalls caused by structural fiscal pressures since the global financial crisis (GFC) (Lauermann, 2018; Van Loon et al., 2018). The forms of local governance influence the local character of financialization (Weber, 2010). At the same time, the expansion of finance also restructures local governance (Aalbers, 2020; Anguelov et al., 2018; Savini and Aalbers, 2016). In some cases, financial intermediaries and financial products are deployed as a fix for entrepreneurial governance (Beswick and Penny, 2018). But in other cases, local governance tends to lock into a trajectory of financial instability (Peck and Whiteside, 2016; Savini and Aalbers, 2016). Based on Detroit, Peck and Whiteside (2016) find that financialized governance occurs in late entrepreneurialism so that ‘entrepreneurial strategies are increasingly realized through financial mediated means’ (p. 239). There are also variations of the financialization of governance in Europe (Van Loon et al., 2018). Moving beyond classifications of governance forms, Pike et al. (2019) call for granular analyses of how distinct governance forms are articulated in specific institutional, temporal, and spatial contexts. Given this backdrop, we aim to provide a concrete analysis of the financialization of urban development using financial intermediaries in China and to understand the implications for governance.

China has also experienced the financialization of urban development since the GFC, characterized by extensively using financial intermediaries and instruments in urban development (He et al., 2020; Pan et al., 2017; Wu, 2022). This was triggered by a stimulus plan in which the central government aimed to invest four trillion Yuan mostly in infrastructure within 2 years after the GFC. The State Council encouraged local governments to use financial innovation and exploit financial intermediaries, which caused a boom in local government financial vehicles (LGFVs) (Feng et al., 2022; Bai et al., 2016; Liao, 2014). Most of the LGFVs are urban development and investment corporations (UDICs also called chengtou). Chengtou have been established by local governments to undertake multiple goals since the 1990s (Jiang and Waley, 2020). They have greatly developed their financial function in the post-crisis era when they played the role of LGFVs. As central government lifted the criteria for corporate bonds in 2008, many chengtou have become qualified for the bond market, which has led to a soaring market in urban investment bonds (chengtou bonds) (Chen et al., 2020; Pan et al., 2017). Focusing on the financialization of urban development, scholars have stressed the magnitude of local borrowing (Fan and Lv, 2012; Pan et al., 2017), the financial support of local governments for their LGFVs (Liao, 2014; Ong, 2014), and financial maneuvers centered on land (Huang and Du, 2018; Wu, 2022). However, at the urban level, the exact process of how the local government shapes and is shaped by the financial market through using financial intermediaries is less explored. Moreover, as the State Council required LGFVs to transform in 2014 (State Council, 2014), the latest local operations are understudied.

We fill the gap by analyzing how the Shanghai government manages to support urban development through Shanghai Municipal Investment (Group) Corporation (SMI) in the post-crisis era. Shanghai is chosen as the case for two reasons. First, it is the global financial center of China, and the development of Shanghai has a prominent connection with the financial market. Second, Shanghai has been a pioneer in innovating financial mechanisms to support urban development. SMI is the largest chengtou in Shanghai and a pioneer in financial innovation. For instance, Shanghai issued China’s first chengtou bond through SMI in 1995. In 2014, SMI transformed into a state-owned limited liability company as a pioneer in the transformation of LGFVs. Focusing on SMI, we aim to illustrate its operation and implications for urban governance. Furthermore, based on the local government’s support for SMI, we ask to what degree the municipal government has been affected and restructured by the financial market while retaining SMI as a financial intermediary.

The case study relies on a thorough analysis of various sources of documents and interviews with government officials, scholars and managers of chengtou in Shanghai. We observe an embryonic form of financialized governance in Shanghai in that the municipal government achieves entrepreneurial goals through managing SMI using financial techniques such as shareholding. By doing so, the Shanghai government avoids confronting the financial market but retains the power of guiding urban development. SMI is the extended financial intermediary of the Shanghai government in the form of a corporation. Therefore, we offer a critical reflection on the relationship between government and the financial market by arguing that the Shanghai government extends its power through financialization rather than making many compromises with the financial market.

The paper is organized as follows. In the next section, the literature on financialization is reviewed, with a special focus on the financialization of urban governance. The third section reviews urban governance in financing urban development in China. This is followed by a methodology section on the research rationale and data collection. In the empirical sections, we first introduce the history of mobilizing financial capital in the urban development of Shanghai and the corporatization of SMI. Further, we investigate an embryonic form of financialized urban governance based on the operation of SMI and revisit concerns about governance restructuring in financialization. Finally, we conclude on the governance form of Shanghai and discuss its implications for urban governance.

The financialization of urban development and financialized urban governance

The core theoretical underpinning of this research is the state-finance relationship in the financialization of urban development (Belotti and Arbaci, 2020; Guironnet et al., 2016; Pike et al., 2019). In urban studies, the financialization of urban development means that the built environment is increasingly ‘built for financial investment’ (Guironnet et al., 2016), where ‘financial capitalists extract value’ (Farmer and Poulos, 2019). Scholars have evidenced urban financialization in terms of attracting financial investors, using financial instruments and seeking global financial support especially in the post-crisis era (Christophers, 2019; Farmer and Poulos, 2019; Guironnet et al., 2016). Meanwhile, the financialization of urban development is engaged with the mutating of urban governance forms (Pike et al., 2019). It is therefore critical to unpack ‘the important role played by local governments in shaping and being shaped by financial markets’ (Weber, 2010: p. 256).

In the post-crisis era, local governments have enabled financial actors and relied on external financial sources to support urban development or secure public goods to deal with insufficient budgets (Birch and Siemiatycki, 2016; Lauermann, 2018). For instance, in Paris, financial investors were invited into urban development projects, through which financial concerns were integrated into the urban fabric (Guironnet et al., 2016). Although local fiscal problems seem to be resolved by temporary remedies, these resolutions are far from sustainable, and the maneuvers of local governments may be curtailed (Birch and Siemiatycki, 2016; Peck and Whiteside, 2016; Weber, 2010).

Entering the financial market redefines the state–market relationship and leads to governance restructuring (Aalbers, 2020; Wijburg, 2019). In countries with liberal economies, scholars find that the finance rationale captures the decision process in urban governance, and financialized urban governance happens in late-entrepreneurialism (Peck and Whiteside, 2016). As a feature of financialized urban governance in Detroit, ‘the locus of power and control has been shifting from growth coalitions to debt machines and from local business leaders to more distant finance-market interests’ (p.239). Urban governance has been transformed to prioritize shareholder and bondholder value (Peck and Whiteside, 2016). Similarly, in Chicago, Farmer and Poulos (2019) find that local development goals have been diverted to cater to the interests of financial actors. The disciplinary role of financial actors has redefined the urban fabric.

However, there are other possibilities of financialized urban governance characterized by increasing reliance on financial strategies to continue pursuing entrepreneurial goals (Van Loon et al., 2018). In more state-centered economies such as Spain, the Netherlands and Belgium, scholars have found a European variation of the financialization of urban governance (Coq-Huelva, 2013; Van Loon et al., 2018). Local governments overly rely on financial returns to fulfill government goals rather than being captured by finance (Van Loon et al., 2018). Similarly, in London, special purpose vehicles have been used by the local state to deliver housing (Beswick and Penny, 2018). Nevertheless, financial value does not supplant entrepreneurialism. Hence, they use ‘financialized municipal entrepreneurialism’ to understand these practices. Moving beyond classifying urban governance types, it is critical to understand how financialization ‘unfolds in webs of dialectical relations’ (Christophers, 2015: p. 198). To sum, the exact process of urban financialization is rooted in various forms of local governance, which in turn, reshapes urban governance towards financialization (Aalbers, 2020; Weber, 2010). Nevertheless, the financialization of urban governance mutates variously depending on specific financial environment, institutional context and grounded local practices.

Governing and financing urban development in China

Scholars have concurred with the significance of state interference in urban development in China (Lin et al., 2015; Wu, 2018). Recent literature has also stressed the leading role of the Chinese state in promoting financialization (Pan et al., 2017; Petry, 2020; Wang, 2015). As for urban governance, local governments are pivotal in urban development as they act as entrepreneurs to invite investment and promote local growth (He and Wu, 2009; Lin et al., 2015; Yang and Wang, 2008). Different from urban entrepreneurialism, Wu (2018) uses ‘state entrepreneurialism’ to emphasize a form of urban governance combining ‘planning centrality and market instruments’ (p.1383). This understanding is fundamental to comprehending the Chinese characteristics of urban financialization and the state-market relationship. On the one hand, state dominance is significant throughout the process of inviting financial agencies and instruments into urban development. Meanwhile, local governments are empowered and promoted to deploy market instruments to accomplish development goals, which are not confined to economic growth but may contain strategic goals (Wang and Wu, 2019). ‘State entrepreneurialism uses market instruments made available through institutional innovation to extend the state’s position into the market sphere and maintain state power. Rather than being replaced by market power, state power is reinforced by its use of market instruments.’ (Wu, 2018: p. 1396)

Chengtou are a typical form of market instrument devised by local governments to deliver entrepreneurial goals and support urban development. (Pan et al., 2017; Wong, 2013). They are critical both in terms of financing urban development and constructing development projects (Jiang and Waley, 2021). First, chengtou have sought extra-budgetary funds for local development (Pan et al., 2017; Tsui, 2011). Local governments were not eligible to borrow by themselves according to the Budget Law before 2014. Hence, nearly all local governments established their chengtou as a disguise to seek finance and conduct projects (Wong, 2013). Second, chengtou not only raise funds but also construct infrastructure, develop land and fulfill mega urban projects (Feng et al., 2021; Su, 2015). For instance, to implement the mega-urban project of Shanghai Lingang, two development corporations were established to prepare land and infrastructure (Wang and Wu, 2019). Hence, chengtou serve the entrepreneurial goals of local governments (Jiang and Waley, 2021; Wu, 2018).

The operation of chengtou before the GFC was centered on land. That is, chengtou leveraged allocated state-owned land as collateral to seek funding for development projects and repaid the debts using land conveyance fees in the future (Pan et al., 2017; Tsui, 2011). Therefore, chengtou used to be arms of local governments in land development. After the GFC, as the central government promoted local government borrowing through LGFVs, chengtou played the role of LGFVs and extensively expanded their financial functions. Chengtou could even issue corporate bonds, leading to a vibrant chengtou bond market (Pan et al., 2017). An emerging body of literature has focused on the financial operation of LGFVs that is still centered on land (Ang et al., 2015; Huang and Du, 2018; Theurillat et al., 2016). LGFVs expanded their financial channels and this even led to excessive shadow banking and risks of default (Chen et al., 2020; Tsai, 2015). To sum up, the existing literature has stressed that financial expansion through chengtou derives from the political goals of the state to combat the crisis and stimulate the economy (Bai et al., 2016; Feng et al., 2021).

In Western studies, scholars have stressed the disciplinary role of financial actors or financial rationales, which is overlooked in the literature of urban studies in China. The literature has only noticed local financial risks as local governments are tied to their financial intermediaries (Bai et al., 2016; Tao, 2015). For example, as chengtou are backed by local governments, the extensive financial activities of chengtou undermine the sustainability of local finance and local development (Chen et al., 2020; Pan et al., 2017). Nevertheless, it remains unclear how and to what degree a local government may be affected by the financial market when expanding the use of financial intermediaries and instruments. Moreover, as the central government has strengthened regulations since 2014, the latest financial operations of chengtou have been scantly explored. Against this backdrop, we aim to unpack the financial operations of SMI and further examine the implications for governance.

Methodology

Stemming from the literature on governance in the financialization of urban development, we inquire into urban governance in financing urban development in post-crisis China. Empirically, this paper investigates the operation of SMI and examines how the Shanghai government shapes and is shaped by the financial market through deploying SMI to support urban development. Moreover, we ask whether the Shanghai government makes compromises with the financial market and how urban governance is transformed.

The case study relies on data including numerous documents and in-depth interviews. First, we conduct desk research dependent on various documents, including press coverage, policy documents and local statistics released by the central government and the Shanghai government. Based on these data, we review the history of using chengtou to finance urban development in Shanghai and the corporatization of SMI. Second, we examine how the city government and the financial market interact through a financial intermediary based on the operation of SMI. The analysis of SMI relies on various reports retrieved from the China Bond Web site, including auditing reports, credit rating reports, and analysis documents of SMI and its subsidiaries. The analysis is also based on 22 interviews conducted in China from 2019 to 2021. We conducted interviews with government officials, scholars and staff in chengtou to understand the relationship between chengtou and local governments from various angles. Interviews usually lasted from 25 min to 90 min. One of the interviewees is a manager of SMI, who largely contributes to the interpretation of SMI. Data retrieved from the interviewee is generally reliable due to three strategies. First, the interviewee has worked in SMI for more than 10 years and has a thorough understanding of SMI. Second, we did not reach the interviewee in the office buildings but rather provide a relaxed environment for interview. Third, we promised that all the transcripts would be anonymized so that the interviewee would be free to share opinions. Moreover, other interviews with government officials and staff in other chengtou also supplement our understanding of the relationship between SMI and the Shanghai government.

Financing urban development in Shanghai using chengtou

We begin with an introduction to the financing of urban development in Shanghai using chengtou before embarking on a detailed study of SMI. Institutional and financial innovations have been used in Shanghai to support urban development goals. In 1986, the Shanghai government initiated a plan to use foreign investment to promote urban infrastructure, manufacturing, and tertiary industry, and the Shanghai government was responsible for borrowing as well as repayment. The whole plan was fulfilled by a newly established state-owned enterprise (SOE) called Shanghai Jiushi in 1987, which was the first chengtou in Shanghai. It mobilized 1.4 billion USD to support urgent infrastructure projects including Nanpu bridge, metro line one, Suzhou river sewage treatment and Hongqiao Airport terminal renovation. In 1992, SMI was established to undertake urban infrastructure and development projects, including water provision and road infrastructure, and it became the largest chengtou in Shanghai. Apart from these chengtou with comprehensive functions, there have been numerous chengtou in charge of a single project, such as Shanghai Expo Development Group, Shanghai Lingang Economic Development Group and Shanghai Songjiang New Town Development Corporation (Li and Chiu, 2018; Li and Xiao, 2022; Wang and Wu, 2019).

The pervasiveness of chengtou is due to the institutional context of financial repression as well as state entrepreneurialism in China. Shanghai is especially representative. The central government proactively promotes Shanghai to be the ‘dragon head’ to connect the global economy with the domestic market (Wu, 2003). In 2001, the State Council identified that the blueprint for Shanghai was to build ‘four centers’ including an international economic center, an international financial center, an international trade center and an international shipping center before 2020. Due to the strategic position of Shanghai, entrepreneurial goals include both local ambitions of development and top-down political tasks. This echoes ‘state entrepreneurialism’ in that the actual operation of local governments goes beyond chasing land revenue but reflects the ‘alignment with central government policies’ (Wu, 2018: p.1385). To fulfill the plan, the Shanghai government has entrepreneurially invited investment, promoted the business environment, and conducted strategic mega-projects (Jiang and Waley, 2020). This massive development has required a substantial amount of investment and construction. Chengtou effectively connect governmental demands with the financial market as the intermediary. For instance, SMI has accomplished more than 200 substantial projects for the mission of ‘four centers’.

Borrowing through chengtou is an embodiment of urban financialization because urban development projects have been largely financed by debts with the mediation of chengtou (Feng et al., 2021; Jiang and Waley, 2021; Pan et al., 2017). Shanghai Jiushi was a trial for borrowing money overseas when the domestic economy was weak. In 1992, SMI issued the first chengtou bond of 0.5 billion Yuan in China. After this, only a few chengtou entered the bond market to raise funds for urban development projects. While securities contributed a limited portion of the funds raised by chengtou, chengtou used to rely heavily on bank loans. The financial function of chengtou extensively expanded in the post-crisis era when central government encouraged local governments to invest in urban infrastructure, to finance through LGFVs and to issue chengtou bonds. Against this backdrop, Shanghai has seen a boom in chengtou bonds and extensive local borrowing. In a report by the Shanghai Audit Office, the debt of Shanghai government was 845.59 billion Yuan in 2014 with contingent liabilities of 326.16 billion Yuan, which was mostly borrowed by chengtou.

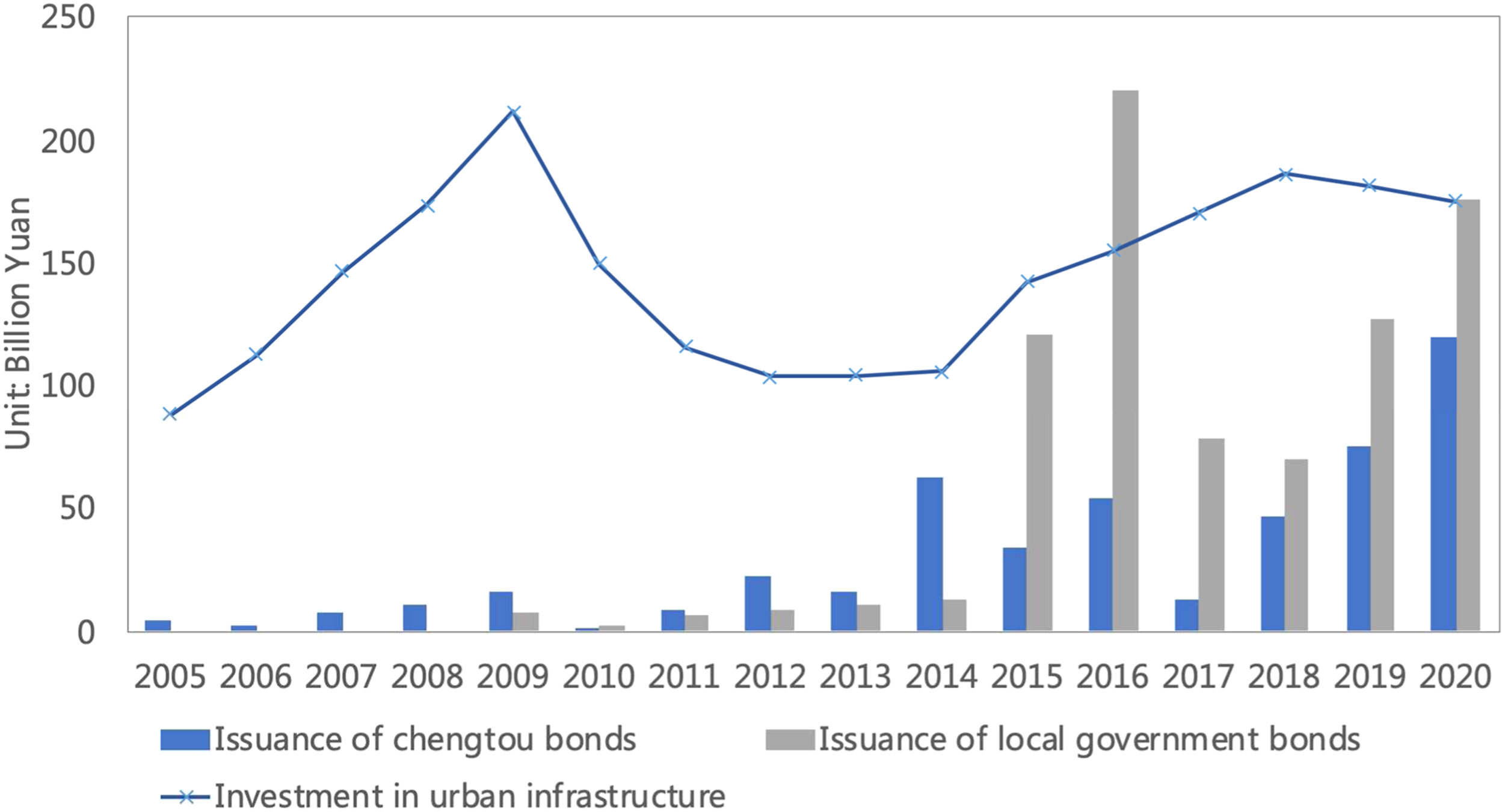

Due to the looming debts of indirect local borrowing, in 2014 the State Council prohibited borrowing via LGFVs (State Council, 2014). In the same year, the Ministry of Finance (MOF) initiated a debt swap plan to swap the contingent debts (mostly borrowed by chengtou) of local governments for local government bonds within 3 years (MOF, 2015). In Shanghai, the swap plan caused an explosive growth in local government bonds from 2015 to 2016. Nevertheless, chengtou in Shanghai are still active in the financial market to issue bonds (Figure 1). Therefore, local governments bonds have not supplanted the financing channel through chengtou. The issuance of chengtou bonds and local government bonds in Shanghai (2005–2020) Data source: ChinaBond website, Shanghai Statistical Yearbooks.

It is thus intriguing to inquire into the operation of chengtou under the stringent control of central government. SMI is an example through which to examine this issue because its transformation has been promoted as a successful model of market-oriented reform. In the following sections, we will investigate the corporatization of SMI and the urban governance form in Shanghai using SMI.

The corporatization of SMI

SMI has been transformed into a state-owned limited liability company that follows company law since 2014. First, unlike that in Western studies where financialized strategies have been adopted to cope with austerities (Beswick and Penny, 2018; Christophers, 2019), the corporatization of SMI is also a local response towards central restrictions on local borrowing. At present, the selected form - corporatized SMI is an innovative strategy adopted by the local state within central regulations.

As mentioned above, the central government stopped LGFVs from borrowing for local governments in 2014 (State Council, 2014). In addition, local governments used to inject land into LGFVs to enhance their asset levels (Tsui, 2011; Wu, 2022). This behavior was also prohibited by central regulations. At the same time, the MOF promoted LGFVs with operating income and cash flow to conduct market-oriented transformation (MOF, 2015). The transformed entities could still undertake government-related projects to provide public goods, but they had to be responsible for their own profits and losses (State Council, 2018). For chengtou like SMI, these regulations mean that their financial function for local governments is prohibited while their function for urban development and construction remains. Against this backdrop, SMI was transformed in 2014 and has become an independent economic entity whose liabilities are not shouldered by the Shanghai government. Nevertheless, whether SMI actually became financially independent needs to be further examined.

SMI mainly adopted two strategies to conduct corporatization. First, SMI took a group management approach to reorganize its business into four divisions, including road infrastructure, water infrastructure, environmental business, and property. Except for property, each division was reorganized into a group company. That is, the Shanghai Chengtou Road Group is for road infrastructure, the Shanghai Chengtou Water Group specializes in water infrastructure, and the Shanghai Environment Group is responsible for the environmental business. This maneuver improves management efficiency by streamlining the number of second-level subsidiaries from 27 to 12. Second, SMI invited other private investors into its subsidiaries to conduct mixed-reform (hungai) recapitalization. For example, Hony Capital, a private investment company, acquired a 10% equity stake in SMI Holding (a subsidiary of SMI) in 2014 with 1.79 billion Yuan.

Despite the transformation, SMI has not altered its major business. It still conducts urban development projects assigned by the Shanghai government. That is, SMI is still pivotal to the implementation of entrepreneurial goals in the post-crisis era. At the same time, the operation of SMI is under the supervision of the financial market as SMI enters the bond market. Nevertheless, most projects proposed by the Shanghai government are not profitable, providing little operational income to SMI. We therefore ask how SMI maintains its operations financially and institutionally.

An embryonic form of financialized governance

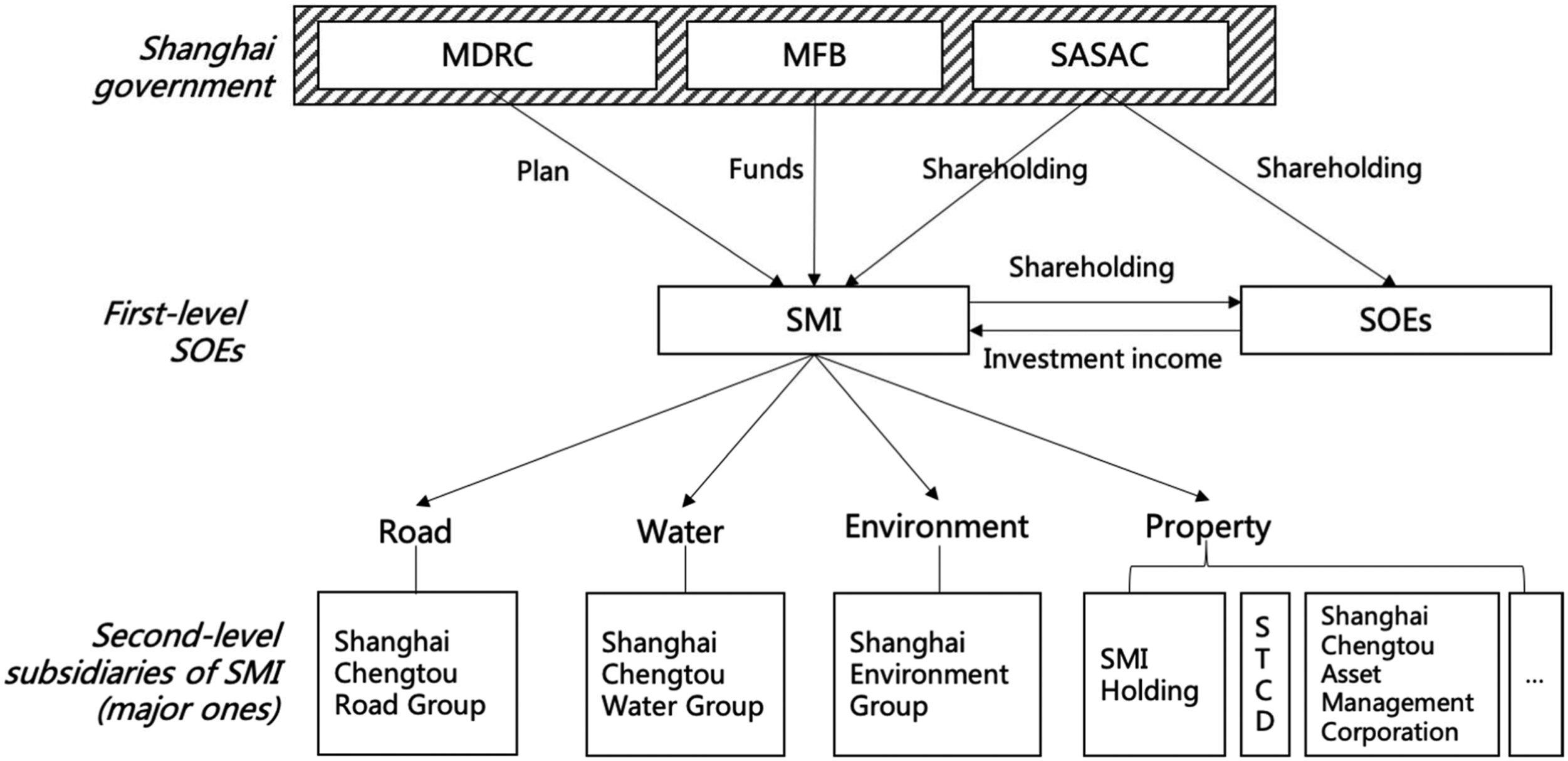

This section not only interprets the operation of SMI in detail but also illustrates the financial techniques adopted by the Shanghai government to support SMI and manage urban development. SMI, owned by the State-owned Asset Supervision and Administration Commission (SASAC) of Shanghai, is a corporatized intermediary for the Shanghai government to manage its assets, seek finance, and fulfill government entrepreneurial ambitions through urban development projects. Based on SMI, we find that state entrepreneurialism takes an embryonic form of financialized governance in terms of increasingly relying on shareholding as a tactic.

First, shareholding legitimates local government power over the management of SMI. SMI is formally owned by the SASAC of the Shanghai government. It directly manages the SMI through staffing. Since the market-oriented transformation, SMI has operated following the modern enterprise management system with a board, managers and a supervisory committee. As the only shareholder for SMI, SASAC appoints almost all the members of the board. Apart from SASAC, SMI has a close relationship with other departments of the Shanghai government (Figure 2). For instance, the Shanghai Municipal Development and Reform Commission (MDRC) puts forward annual plans for substantial projects in various sectors including manufacturing, infrastructure and living environment. In 2018, the MDRC proposed 126 projects of which SMI undertook 33 with a total investment of 26.4 billion Yuan. SMI as a single corporation shoulders a quarter of the whole strategic plan of Shanghai. Although SMI shoulders tasks from the municipal government, it does not carry out urban projects itself. Subsidiaries of SMI conduct the projects. Shareholding empowers SMI to manage its subsidiaries to implement the projects. This is illustrated in a credit rating report: Shareholding as the main strategy in the management of SMI. Notes: MDRC: municipal development and reform commission of Shanghai; MFB: municipal financial bureau of Shanghai; SASAC: state-owned assets supervision and administration commission of Shanghai; SOE: state-owned enterprise; STCD: Shanghai Tower Construction and Development Co.

SMI appoints chief financial officers (CFOs) to subsidiaries to manage and monitor their financial operation. These CFOs also participate in major decisions for their companies including business and staffing. Moreover, the budget of all the subsidiaries should be compiled, reported and approved by the SMI. No subsidiary could amend its budget without the approval of the SMI. (Shanghai Brilliance Credit Rating, 2020)

The Shanghai government imposes its influence on SMI by releasing development plans and ensures the accomplishment of plans through vertical management within SMI. Therefore, in the management of SMI, shareholding legitimates government power from decision to implementation.

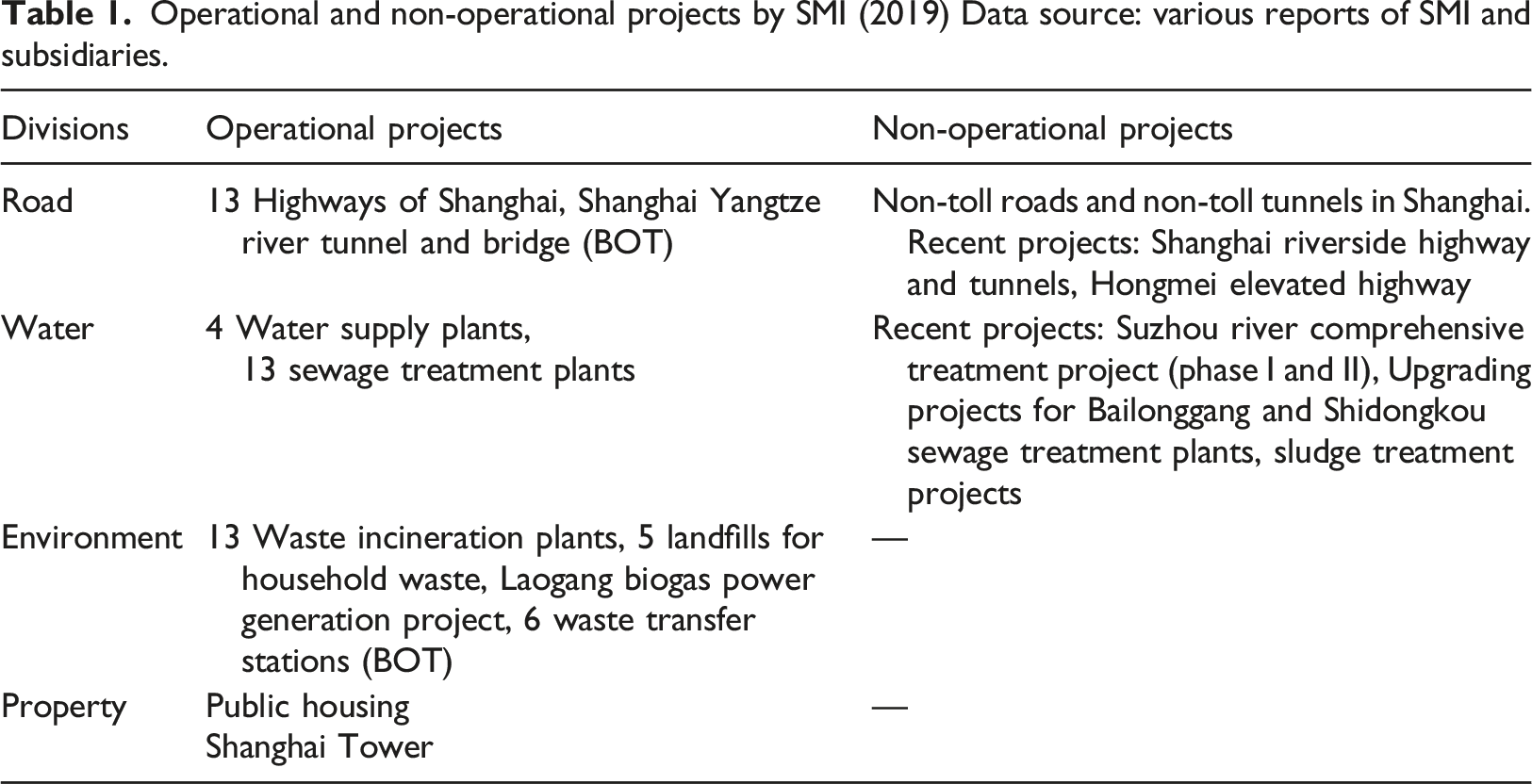

Operational and non-operational projects by SMI (2019) Data source: various reports of SMI and subsidiaries.

The other type of business is operational projects, though profitability is limited. We list the major projects for each division in Table 1. One part of operational projects could retain stable income, but the profitability is low as the price is regulated by the Shanghai government. These projects include road infrastructure, water supply, waster transfer and incineration. Apart from these projects, other operational projects are aligned with governmental ambitions. Two property companies are examples. SMI Holding, for instance, is a property company and is one of the two listed corporations controlled by SMI. However, the main business of SMI Holding is not commercial property but urban regeneration and affordable housing projects. SMI conducts public housing projects and signs initial contracts with relevant local governments (including district-level governments). Local governments finally pay for the public housing based on a principle called ‘baoben weili,’ which means to cover the cost and guarantee small profits. Therefore, profitability is also restricted. In recent years, SMI Holding has expanded its business to rental housing as the Shanghai government is strongly promoting the rental housing market required by the central state. Hence, the business of SMI is aligned with government goals with restricted profits. Besides, other development projects may even lead to negative income. A typical example is Shanghai Tower, constructed and managed by Shanghai Tower Construction and Development Co, Ltd (STCD). Shanghai Tower was completed in 2016, but STCD has suffered losses until now. In 2018, the net profit of STCD was −0.24 billion Yuan. The project of the Shanghai Tower has not been a profit-seeking decision from the start. According to the MDRC, the Shanghai Tower is an important strategic project to build Shanghai as an international financial center, which has been the development goal for the Shanghai government for decades. Building Shanghai Tower was included in the annual list of MDRC for substantial development projects in 2014. Hence it was initiated by the government and accomplished by its market agency SMI. Meanwhile, it seems that SMI suffered a loss in this project, yet the Shanghai Tower is the most valuable investment property owned by SMI to access further finance as collateral. To sum, SMI is an implementer for the entrepreneurial goals of the Shanghai government by carrying out these operational projects.

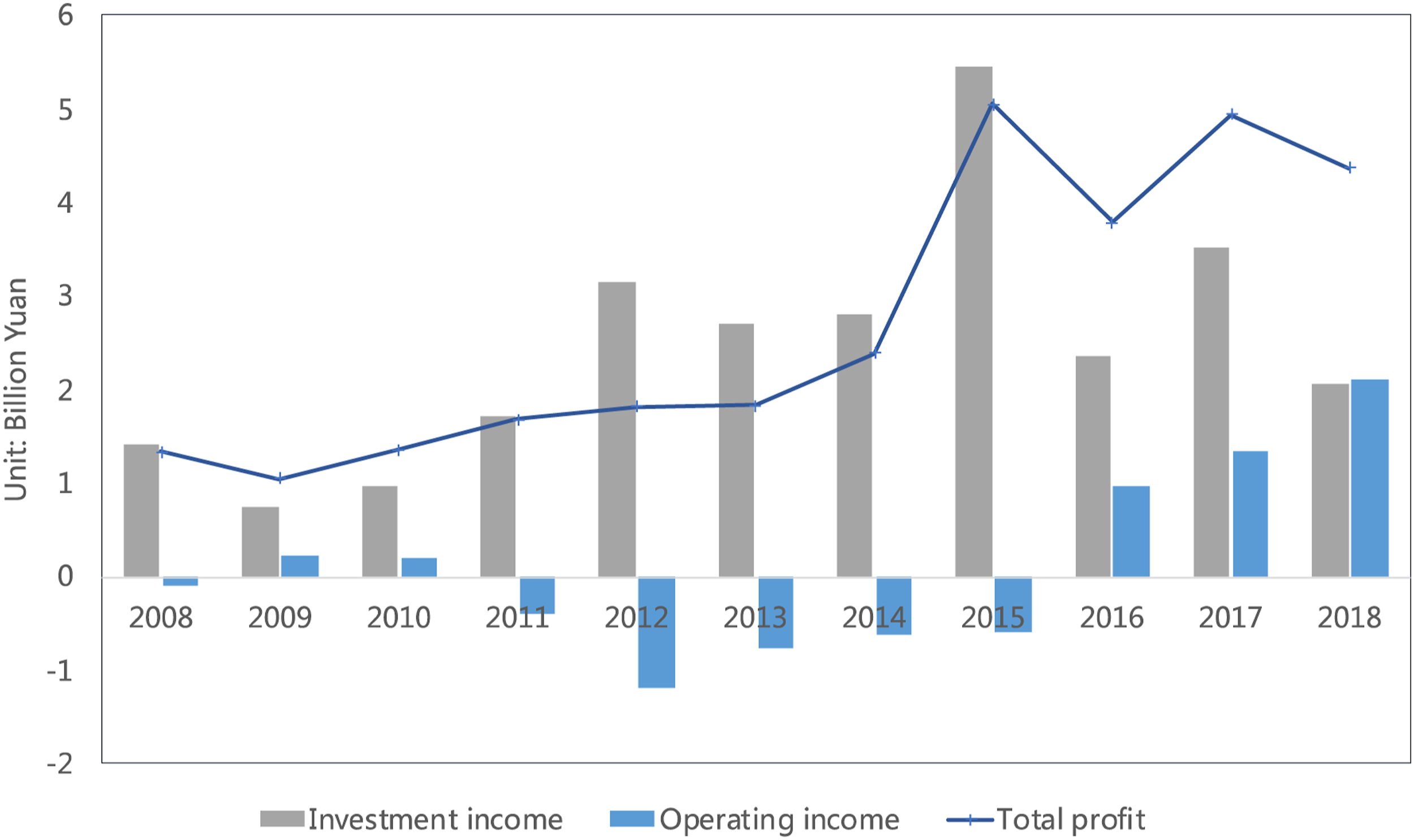

Although the major business of SMI makes small profits, these projects generate a stable income stream. More importantly, the portfolio of SMI guarantees the financial health of SMI. SMI can receive considerable profits from shares in other companies, and this is also tightly associated with the Shanghai government. SMI relies heavily on investment income, which comprises more than 50% of its profits (Figure 3), to enhance its financial performance. From 2011 to 2015, SMI even had negative operating income, but it made positive profits because of the contribution of investment returns. The investment income comes from portfolios, including equity investment and available-for-sale securities (AFS securities). Most of the enterprises invested in by SMI are also controlled by the SASAC of Shanghai (Figure 2). SMI used to acquire the shares of these enterprises from the Shanghai government. As commented by a manager of SMI: The constitution of the profits of SMI (2008–2018). Data source: Audit reports and credit rating reports of SMI (2008–2019).

In the past, SMI invested a lot. The government also gave us some rewards. We got the shares at that time. For some projects, we did not get repaid or we lost money. Some of these (shares) were to balance the financial system of SMI. If you work for the government, (the government) will think about it in the end for sure. (Interview, a manager of SMI, September 2019)

SMI has shares in 33 corporations (subsidiaries are not included) in various sectors, including the food industry, manufacturing, and the financial industry. For long-term equity investment, SMI can generate stable returns. The largest returns derive from its shares in Bright Food (Group) Co Ltd (Bright Food hereafter), which is the largest food company controlled by the SASAC of Shanghai. SMI annually receives around 0.7 billion Yuan from its 39.73% equity stake in Bright Food. Another type of financial assets is AFS securities. AFS securities constitute around 20% of the assets of SMI, annually contributing around one billion Yuan to SMI. Although investment returns fluctuate with the financial market, they have significantly enhanced the financial performance of SMI. As SMI acquired shares from the SASAC of Shanghai, it is clear that the Shanghai government supports SMI using shareholding as a strategy.

Drawing upon the operation of SMI, we illustrate an embryonic form of financialized urban governance reliant on shareholding in three aspects (Figure 2). First, shareholding reasserts the power of the Shanghai government towards SMI as SASAC is the only shareholder for SMI. Second, shareholding legitimates the management within SMI. Therefore, SMI strictly manages its subsidiaries to guarantee that government goals can be accomplished by its subsidiaries. SMI, in this sense, is a professional manager for the Shanghai government to manage urban projects with a form of corporation. Third, SASAC enhances the performance of SMI by allocating shares in other SOEs rather than injecting land assets (cf. Pan et al., 2017; Tsui, 2011). Instead of extensively relying on external financial actors at a distance (Guironnet et al., 2016; Weber, 2010), financialized governance centered on SMI is internalizing financial tactics (especially shareholding) to develop and control government agencies to fulfill governmental goals. Echoing Wang (2015), in China, financialization has been extended from the economy to the state. Although many studies have stressed the enabling role of local governments in financialization (Belotti and Arbaci, 2020), financialization that is internal makes the case in China salient (Whiteside, 2021). Moreover, based on the development of SMI, financialized governance develops from ‘state entrepreneurialism’ featuring the state devising its own market instruments to a stage when financial tactics have been thoroughly used to manage these instruments.

Revisiting governance restructuring

In Western studies, the transformation of urban politics happens when exposed to the financial market (Birch and Siemiatycki, 2016; Peck and Whiteside, 2016; Savini and Aalbers, 2016). Therefore, we ask about the impacts of the financial market on SMI and whether the Shanghai government makes compromises with the financial market.

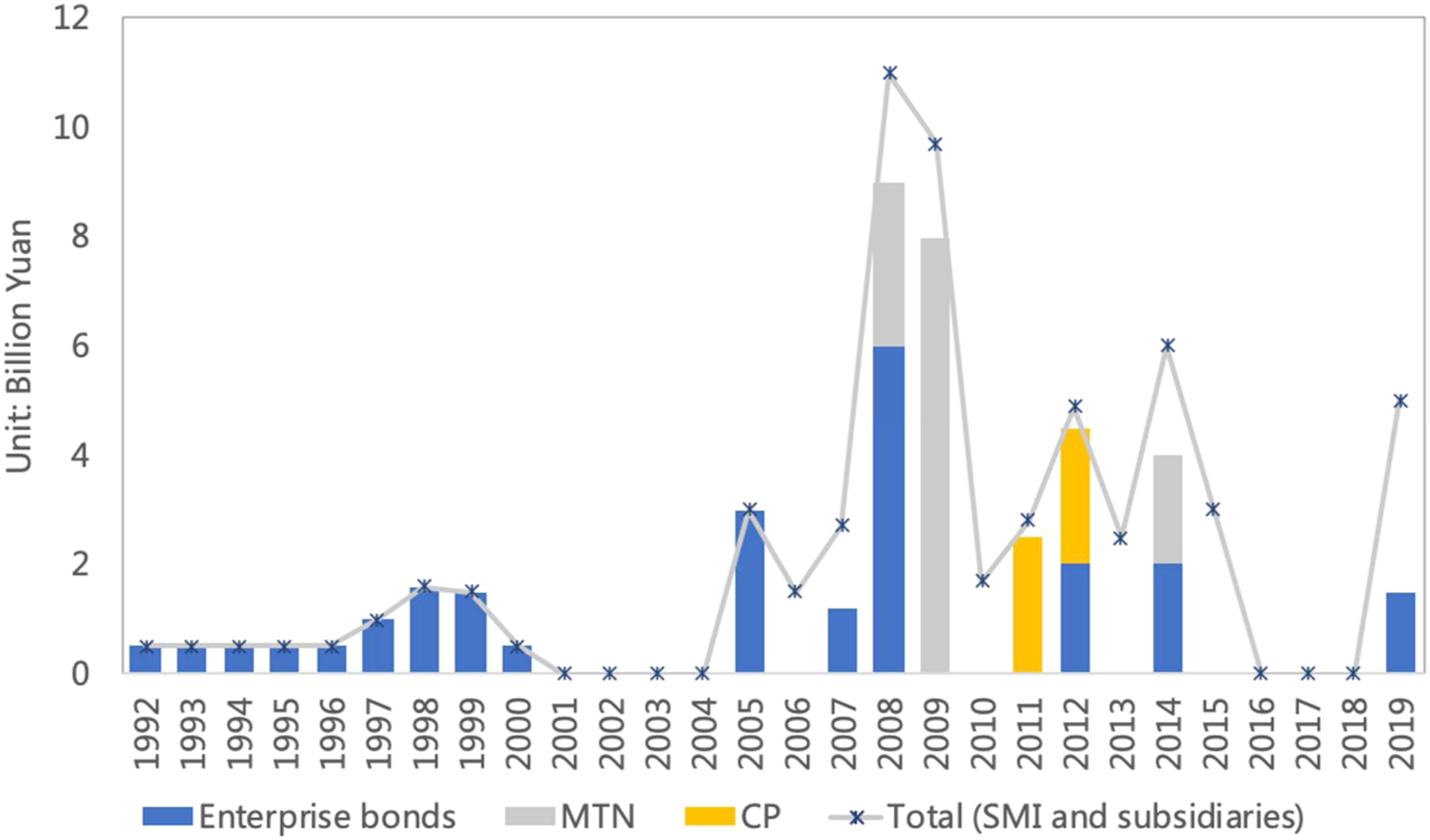

First, SMI is exposed to the financial market and under the surveillance of financial actors. As SMI has larger assets and better financial performance compared to its subsidiaries, SMI raises the funds for most of the projects undertaken by its subsidiaries. Most funds derive from bank loans. SMI also develops other financial instruments and enters the overseas bond market. SMI issued bonds of 40.8 billion Yuan in total (up to 2019), accounting for around 70% of the total bonds issued by SMI and its subsidiaries (Figure 4). Since 2008, it has been more active in the financial market and has explored other financial instruments including mid-term notes (MTN) and commercial paper (CP). The diversity of financial instruments shows that SMI is proficient in the financial market. Bond issuance of SMI (1992–2019). Notes: MTN: mid-term notes; CP: commercial paper. Data source: The prospectus for bond issuance in 2020 by SMI.

Because of its financial activities, SMI is supervised by financial agencies including banks, underwriters and credit rating agencies. For instance, SMI regularly releases reports to follow the rules of the financial market. Nevertheless, we find that the disciplinary role of financial actors is limited. On the contrary, credit reports are aligned with the SMI to reassure investors that SMI is backed by the Shanghai government, which is strategically important in China. Therefore, the possibility of default is low. For example, SMI’s latest prospectus for bond issuance says that ‘the operation of various projects of SMI is essential to secure the operation of Shanghai and people’s livelihood.’ Therefore, ‘the Shanghai government keeps providing strong support to SMI’ (Shanghai Brilliance Credit Rating, 2020). Besides, the lead underwriter for almost all the bonds issued by SMI is Guotai Junan Securities, which is also controlled by the SASAC of Shanghai, and SMI also has shares in this company. As for SMI, it faces little difficulty in raising funds, either from banks or by issuing bonds. As commented by a manager of SMI, ‘banks are willing to give loans to us because SMI is the most reliable enterprise in Shanghai’ (Interview, a manager of SMI, September 2019). Based on the interaction between SMI and actors in the financial market, we find that SMI is privileged in the financial market considering its close relationship with the Shanghai government. Credit rating agencies and underwriters work in tandem with SMI to seek finance.

Although financial actors including banks and credit rating agencies do not exert much pressure on SMI, it still faces the rationale of bondholder value, which is making profits. The corporatization of SMI has increased its concern about profitability. That is, SMI has to care about profits, which it used to ignore. As explained by a manager of SMI:

After becoming an enterprise in 2014, SMI becomes a decision-maker. But of course, the decision-making power is authorized by the government. For now, SMI can negotiate with relevant authorities before starting the project. If the government wants me to do this project, can I balance it? Although the government still requires SMI to undertake necessary projects, most of the projects are done following the operation of the enterprise. If this project is very risky and SMI has no returns, SMI can’t do it. If you (the government) want me to do it, you have to think about the money. For example, if SMI lost money on one project, the government could make it earn some money from another project. That is how we balance it. (Interview, a manager of SMI, September 2019)

The explanation indicates not only how SMI is shaped to consider profitability but also how this transformation impact urban governance. First, SMI is influenced by the market rule so that it has to balance its profits and losses to evidence its financial health. Nevertheless, SMI is not a private company chasing profit maximization. It only needs to balance the losses. The Shanghai government also needs to consider the performance of SMI. This concern is reflected in the task assignment as pointed out by the interviewee. That is also why the Shanghai government supports SMI by allocating shares. Stable financial returns can enhance the performance of SMI. In this sense, the previous form of urban governance has been somewhat restrained when taking into consideration the financial performance of SMI.

On the other hand, external shareholder or bondholder value does not dominate SMI, as SMI is owned and authorized by the Shanghai government. Hence, SMI continues to work for the government to provide public services and fulfill entrepreneurial goals. Moreover, as a corporation, SMI is effective to manage and balance investments in various urban projects and to make SMI (as a whole) competitive in the financial market. Because of the large size of SMI, the risk of a single project can be absorbed. SMI demonstrates an embryonic form of financialized urban governance in which urban projects, financial risks, and asset management are internalized in a single corporation. This integration makes it both a professional manager for the government and an accountable economic entity for the financial market. The corporation itself is a selected form of governance to respond to the central regulations and the discipline of the financial market at present. Although SMI is shaped by the financial market in terms of considering profits, this consideration is not decisive. Instead, the Shanghai government, as the only shareholder of SMI, continues to use SMI as an intermediary to extend its influence in the financial market. Therefore, in this case, state entrepreneurialism persists while taking a more financialized form.

Conclusions

Mobilizing financial actors and products to finance urban development has aroused extensive scholarly attention (O’Brien et al., 2019; Weber, 2010). Focusing on the ‘politics of financialization at the local level’ (Weber, 2010: p. 270), urban governance has been affected by the financial rationale to various degrees (Aalbers, 2020; Savini and Aalbers, 2016). This paper provides a Chinese variant of financialized urban governance although in its embryonic form.

First, we illustrated the financialization of urban governance in Shanghai in which state entrepreneurialism has been increasingly reliant on financial strategies especially shareholding. First, after the corporatization of SMI in 2014, the SASAC of Shanghai is still the only shareholder of SMI. Therefore, the Shanghai government remains its absolute control over SMI through shareholding. At the same time, SMI manages its subsidiaries to comply with government goals and enters the financial market with enhanced performance. In doing so, financial risks, asset management, and urban projects are internalized and managed within SMI. Moreover, the Shanghai government adopts financial techniques to deal with the financial problems of SMI. These include promoting investment income via cross-shareholding among SOEs and issuing local government bonds to swap accumulated debts. These practices echo financialized governance in that ‘finance becomes integral to the business of government’ (Peck and Whiteside, 2016: p.256), yet in a different manner. In Detroit, urban governments have been combating external financial actors such as banks and bondholders. Dealing with debt has been the key concern of the city government (Peck and Whiteside, 2016). In Shanghai, however, financial strategies have been internalized as toolkits for the Shanghai government to manage and support SMI. Echoing Wang (2015), this paper represents ‘the rise of the shareholding state’ at the local level. The variant of financialized governance is more like that in Europe. For example, ‘financialized municipal entrepreneurialism’ in London emerges to provide more housing, and Dutch urban governance is financialized to make local governments profit from real estate markets (Beswick and Penny, 2018; Van Loon et al., 2018). In these European cases, financialized urban governance is to fix entrepreneurialism through financial techniques rather than replacing the previous urban fabric. Similarly, the Shanghai government adopts financial strategies and develops its toolbox for entrepreneurialism.

Meanwhile, local governments have been affected when adopting financial strategies and using financial instruments (Birch and Siemiatycki, 2016; Sanfelici and Halbert, 2019; Wijburg, 2019). However, this paper does not find that using financial techniques has led to the erosion of government power. Instead, we argue that the Shanghai government strengthens its power by adopting financial techniques. The Shanghai municipal government guides the corporatization of SMI to reassert government control over urban development rather than being ‘kidnapped’ by profit-seeking value (cf. Savini and Aalbers, 2016; Ward and Swyngedouw, 2018). Even credit rating agencies and underwriters work with SMI to persuade investors that SMI is reliable as it is backed by the Shanghai government. On the other hand, the impacts of the financial market exist. For instance, SMI has to demonstrate its profitability to enter the financial market, while government-related projects are not that profitable. Therefore, SMI and the city government frequently negotiate on fund balancing. The influence of the financial market is important but not that powerful as SMI still undertakes government projects. Hence, compared with many studies (cf. Birch and Siemiatycki, 2016; Savini and Aalbers, 2016), we do not find that local maneuvers are largely restricted by bondholder value or financial rationale.

The modality of governance in Shanghai is in line with state entrepreneurialism in China in that ‘the state acts through the market rather than just being market-friendly’ (Wu, 2020: p. 326). We echo the proposition that financialization is locally embedded and mutates in its specific institutional context (Christophers, 2019; Pike et al., 2019; He et al., 2020). The corporatization of SMI shows the adaptivity of state entrepreneurialism as the Shanghai government still manages to mobilize the financial market using a market instrument with financial accountability. Therefore, local governments increasingly act through the financial market, and financial techniques are integrated into local governance. Based on the case of Shanghai, we illustrate another possibility for the relationship between state and finance in the financialization of urban development. From the perspective of state entrepreneurialism, we clarify the exact meaning of ‘financializing the Chinese city’ (Wu, 2021) or financialized urban governance which means an extensive use of financial means to achieve state-centered governance and the expansion of financial operation and financial logics without the dominance of external financial institutions.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the China Scholarship Council (201806190221), H2020 European Research Council (Advanced Grant No. 832845‐ChinaUrban), Economic and Social Research Council (ES/P003435/1).