Abstract

Since the 1980s US city governments have increased their use of more speculative means of financing economic redevelopment. This has involved experimenting with a variety of financial and taxation instruments as a way of growing their economies and redeveloping their built environments. This very general tendency, of course, masks how some cities have done well through the use of these instruments while others have not. The work to date has tended to pivot around a “winner-loser dichotomy”, which emphasises either the capacity of US cities to be able to experiment and speculate through the use of one financial instrument or another or their failings with these instruments, resulting in bankruptcy and fiscal crisis. This paper presents a case study of Lexington, Kentucky and using archival research and interviews we argue that speculative financial instruments are harder to choreograph for some cities than for others. We draw particular attention to US cities beyond those that tend to be over-represented in the metro-centric academic literature. This argument has conceptual significance. Building theory out of the experiences of US cities such as Lexington, Kentucky turns attention to the work required by city governments as they seek to finance the redevelopment of their downtowns. We make the case for a continued appreciation of the messy politics around the use of financial instruments, and its indeterminate, open and unpredictable nature in an era of fragile and uncertain entrepreneurial US urban policy-making.

If you see cranes Downtown you want to see them moving, you don’t want to see them standing and just weighing in the wind. (#13 elected official, city government, Lexington)

Introduction

Downtown Lexington, Kentucky is at the centre of a hub-and-spoke road network. Like so many US downtowns, it is one in which the car continues to hold sway over the pedestrian. Communities and neighbourhoods adjacent to the centre were dismantled through rounds of development and redevelopment as Lexington’s population grew and suburbanized. Moreover, the downtown itself bears the impact of strategies introduced since the mid-1970s, as it became apparent to city government the city’s once-thriving commercial and retail districts were on the wane (McCann, 2001). Yet regardless of how you get there, whether on South Limestone, South Upper, West Main or West Vine, what awaited you for a full decade after 2008 was a present absence.

At the very centre of the city lies a two-acre site. Since this redevelopment was announced and the razing of existing buildings, architectural designs have come and gone, and with them visions of the future, together with those investors interested in financing the project. Potential tenants have walked away, gone to other cities in the region, frustrated at the apparent inability of those involved to get things done. At the same time, redevelopments adjacent to the site have been proposed (and completed), most notably the 21 C Hotel and the Court House entertainment complex.1 Labelled in the local media as “the hole” or “the pit”, the site became a signature example of governance failure by city government, developers, and landowners.

CenterPointe is the name attributed to the two-acre site at 100 West Main Street, Lexington Kentucky. At the time of writing and almost a decade and a half after the clearance of the site, the CenterPointe development is underway. The first wave of redevelopment was completed in April 2018, after 14 months of building work, This was the 156,906 rentable square feet twelve story office tower (and three levels of condominium residences), 214 room Marriott Hotel, 120 room Residence Inn by Marriott, Jeff Ruby's Steak House, and 700 car below ground parking garage. The development to date is short of the flagship-type structure envisaged. The incremental, stop-start, gradual and piecemeal emergence of this redevelopment is particularly revealing for what is says about the capacity of some US city governments to use speculative financial and taxation instruments. If indeed, as some have suggested, we are witnessing the financialization of US urban redevelopment policy (Farmer and Poulos, 2019; Kirkpatrick, 2016; Launius and Kear, 2019; Pacewicz, 2013, 2016; Singla and Luby, 2020; Sroka, 2016, 2020; Teresa, 2017; Weber, 2010), then it appears to be an on-going, geographically variegated and uneven process. As neither a prominent flagship or landmark development nor a story of terminal downtown decline, we want to suggest that most US cities are likely to constitute a marginalized majority that muddle through, tacking a path between the ever-present spectre of “failure” and the distant prospect of “success” (Williams and Pendras, 2013).

In this paper, we examine the recent history of Lexington city government’s usage of speculative financial instruments to redevelop a central section of the urban downtown. In analysing the Lexington case, we seek to make three principal and related contributions to the wider literature. The first is to emphasize the complex nature of the work required for the assembly and execution of the speculative financing of urban redevelopment. That complexity brings to the fore the thoroughly political nature of the decision to reshape the downtown. The case suggests that this is just as true in Lexington as it is in Chicago, New York and the largest US cities. Our second point is that the majority of US cities lie between the global cities that compete for the largest investment projects and events and the small communities and towns that are more-or-less bypassed in the contemporary competition for urban redevelopment. Thirdly, the case highlights the challenges associated with the use of speculative financing despite its continued proliferation in the US and elsewhere.

With a history that chimes with many of the more fiscally conservative and risk-adverse states of the US geographical South, Kentucky’s sizable rural and small town population combined with its governance through a small and mid-sized county-dominated legislative process, structures the context for both Lexington (and nearby) Louisville city government.2,3 While there is evidence of US cities turning to more risky forms of financing redevelopment (for an overview see Singla and Luby, 2020), this is far from a spatially-uniform pattern that can be assumed to play out smoothly and without contradiction from one city to the next. What the Lexington case suggests is that the use of these instruments is more likely to involve a complex and uncertain cajoling and negotiating by city government, in which the limits to what they are capable of achieving under certain financial systems and land ownership patterns become all too readily apparent.

This paper is based on a two-year period of fieldwork,4 and the second section draws upon and reviews the theoretical literature on US entrepreneurialism and speculative urbanism, specifically work on US municipal politics surrounding the use of financial instruments. It draws on the long-standing literature on US urban politics and policy on the one hand as well as some of the more recent work on financialization in US cities.5 The third section of the paper focuses on Tax Increment Financing (TIF), a debt-based financial instrument now in use across much of the US. Section four examines the case of Lexington, Kentucky. The fifth and final section concludes the paper. It returns to the argument that while US city governments have increasingly turned to financial instruments of one sort or another, long-standing issues of elite politics, land ownership, marketized and politicized relationships and taxation regimes continue to shape and structure the outcomes (Aalbers, 2018; Tapp and Kay, 2019). It argues for a continued appreciation of the politics surrounding that use of financial instruments that constitute one element to the wider financialization of US urban redevelopment policy. Alternatively, to put it another way, the growing use of financial instruments in US urban redevelopment looks quite different when read through the lens of Lexington as compared to that of Chicago or Los Angeles. We suggest there are far more “Lexingtons” in the landscape of US urban redevelopment than there are “Chicagos”, meaning that wider theoretical claims must be attuned to the incrementalism, inertia, path dependency and stasis that can be seen to characterise much of the governance and financing of urban redevelopment.

Entrepreneurial urbanism, financialization and US redevelopment policy

It is perhaps something of a cliché to start a review of the changing nature of US governance with the work of David Harvey (1989). Yet we insist on doing so. Harvey sought to theorize the changing governance arrangements in US cities, involving business elites, community interests and the various agencies of government as part of the transformation in the approach to economic development in a globalizing economic world. Drawing upon his earlier work, in which he examined “the relation between capital development and the social and physical landscapes of urbanisation” (Wood, 1998: 120), Harvey’s (1989) argument centred on the restructuring of the modes and methods of urban governance. In what Peck (2017: 16) describes as “Harvey’s real-time reading of the ‘first front’ of emergence (but ultimately) transformative change”, entrepreneurial urbanism was seen to exhibit three defining features. First, public-private partnerships, of the sort that Novy and Fainstein (2020) argue are central to speculative development, had come to work alongside local governments in order to talk up and boost local economies. Second, that the practices and policies of public-private partnerships had come to be entrepreneurial in character, in so far as they were innovative and speculative in design and delivery, including their use of financial instruments, with growing amounts of public money spent on high-profile marketing and promotional campaigns. And third, in and through entrepreneurial urbanism the emphasis had come to shift from an attention to territory – and the associated provision of housing, education and social services – to a focus on place – and, on particular, civic schemes at specific sites within cities, that were seen as central to projecting the city as cosmopolitan and worldly. However, despite the attention paid to Harvey’s work, our argument in this paper is that “[t]h e absorption of risk by the public sector and in particular the stress on public sector involvement in infrastructural provision” (Harvey, 1989: 11) has been rather under-played. Use of ever more speculative uses of financial instruments and of local taxation regimes have accompanied the shift to entrepreneurial forms of governance are (Aalbers, 2018; Tapp and Kay, 2019).

Using the local tax base speculatively by US city governments to support redevelopment strategies dates back to the early nineteenth century of course (Sbragia, 1983). Set against this longer-term trajectory, Sbragia’s (1996) study of Pittsburgh details how US city governments escalated their level of financial speculation. Nevertheless, what some have argued constitutes the financialization of US urban redevelopment policy (Rutland, 2010) can be seen to have its origins in the late- 1970s and early-1980s. For Levine (1989: 22), by “the 1980s, virtually all major cities had significant financial “exposure” in public-private redevelopment, either through loans or loan guarantees”, as one part of their entrepreneurial turn in response to the combination of federal and international changes. This, according to Weber (2010: 256) marked “a new era of increasing integration between financial markets and the day-to-day operations of local governments.” For state theorists, this appears an example of the “relativization of scale” (Collinge, 1999), as the role of the nation state has been reworked in line with the “hollowing out” thesis (Jessop, 1994) and the emergence of a New Urban Politics in the context of globalization (Cox, 1993). In this vein it is argued that what was witnessed was the “rolling back” of some of the fundamentals of Keynesianism and the “rolling out” of neo-liberalism (Peck and Tickell, 2002), with local government encouraged/required to perform increasingly “entrepreneurial interventions” (Weber, 2002: 186). What this general transformation meant for particular cities, large and small, however, was conjuncturally and relationally variable, as it was interpreted, mediated and translated by a range of “market-making actors” (Weber and O’Neill-Kohl, 2013: 193), such as analysts, consultants, lawyers as well as government officials.

One important aspect of this wider growth in “exposure” (Levine, 1989) has been the emergence of various financial instruments, including some that involve the creation of debt (Singla and Luby, 2020). Finance agencies of various stripes have seen their roles expand, alongside a range of others making claims over financial expertise to facilitate the financial engineering undertaken by many US city governments (Hackworth, 2007; Sbragia, 1983; Singla and Luby, 2020; Weber, 2002; Weber and O’Neill-Kohl, 2013). For some this constitutes the latest in a longer line of entrepreneurial urbanism in which financial experimentation and speculation was an important element (Van Loon et al., 2018). For others it constitutes a qualitative transformation, as “financialized urban governance … succeeds entrepreneurial urban governance.” (Aalbars, 2020: 596), although even in this argument there is a sense that financial risk-taking and speculation was present in the earlier period.

While general revenue bonds have a long history in the US and are issued against the full faith and credit of city government, it is innovation in revenue bonds that has distinguished the last few decades, one element to the “financialization of urban governance” (Aalbers, 2020: 596). This has involved US municipalities extending “credit to privately owned development projects with nonguaranteed debt” (Weber, 2010: 253). The most widely used of these more speculative instruments involves the selling of anticipated revenue streams to investors. It is to Tax Increment Financing (TIF) that this paper now turns.

Tax increment financing: A brief overview

Tax Increment Financing (TIF) is “a local economic development policy that allows municipalities to designate a “blighted” area for redevelopment and securitize the expected increase in property taxes from the area to pay for initial and ongoing redevelopment expenditures” (Weber, 2010: 258). The use of TIF is now widespread across the United States (Beyer, 2015; Briffault, 2010; Launius and Kear, 2019; Mann, 2001; Pacewicz, 2016; Peterson, 2014; Sroka, 2020; Teresa, 2017). Originating in California in the early 1950s as companion to the US Community Redevelopment Act (1945), TIF is now on the books of every US state statue with the exception of Arizona and has evolved in a fragmented fashion (Johnston and Mann, 2001). The decentralized, incremental and relational manner in which TIF has arisen has created a variegated landscape of what is and what is not possible as TIF emerged in the US in the shadow of 1970s federal government cuts to urban renewal assistance in which effectively “cities were left to their own devices” (Hackworth, 2016: 2205).

With a nearly seventy-year history, the relatively recent flourishing of TIF appears to warrant some explanation. According to Weber (2010: 259), the “growing interest of pension funds, banks, and life insurance companies gave municipalities the confidence to float more TIF debt and this once-obscure policy instrument grew in size and repute.” In this interpretation, TIF is increasingly used by US city governments to finance the urban commercial real estate, housing, infrastructure and property development sectors and is one of a number of instruments used in cities around the world that “turn possible future revenues or taxes into something that can be cashed in earlier” (Aalbers, 2020: 597).

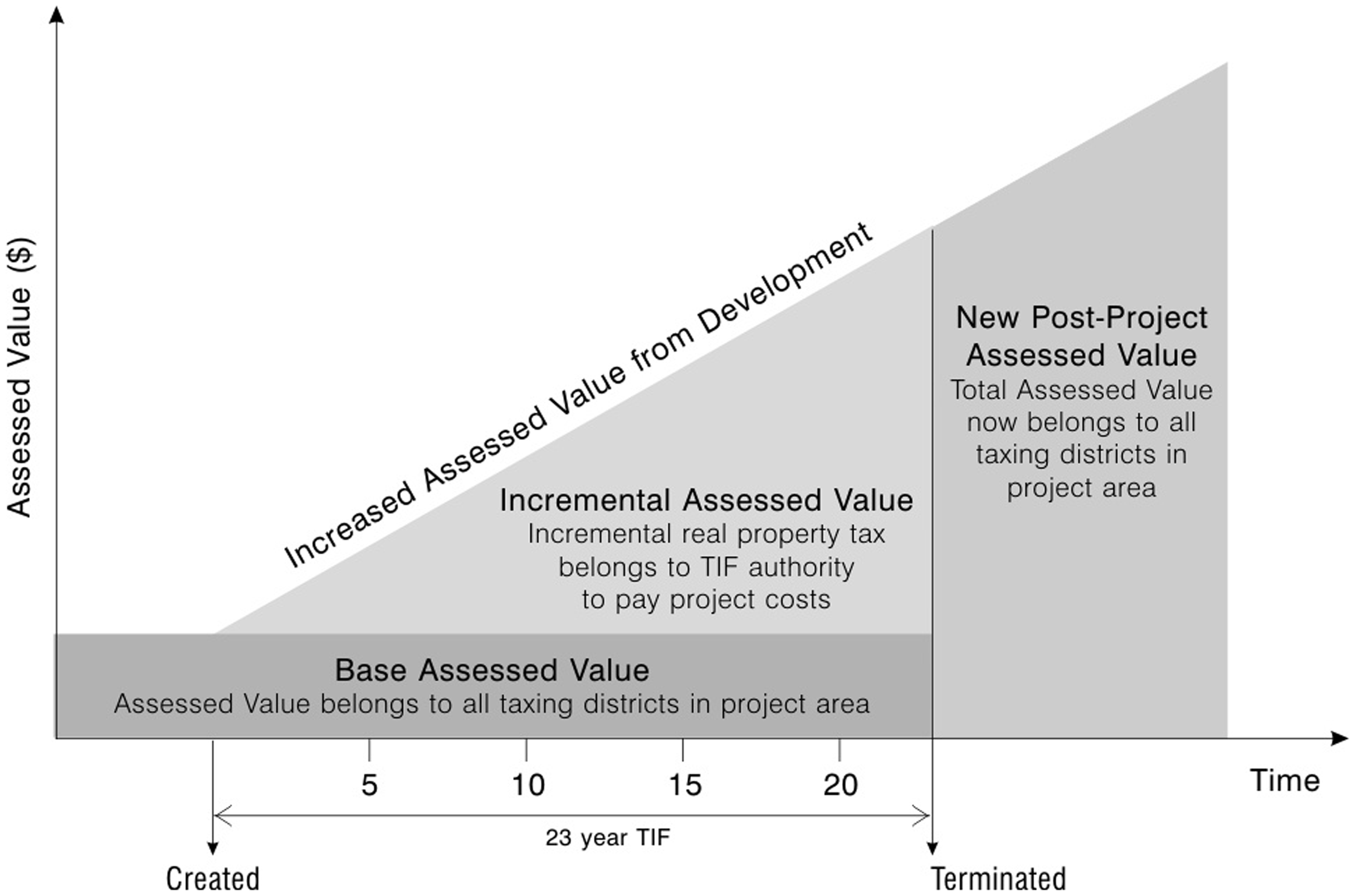

Despite the variable US geography and history to the adoption of TIF, Klacik and Nunn (2001: 26) suggest that the ““basic concept of TIF is the same everywhere.” In its simplest terms, the categorization of an area of land as “blight”, “earmarked” and ring-fenced for redevelopment, is an often contentious and political process. Who makes this decision, the process and practice of decision-making, and the nature of the associated politics differs from one locality to another. Having designated the TIF area, certain rates of taxation on that land (relating to business, education, fire, police, property and the like) are frozen. This is then the “base assessed value” (see Figure 1), which continues to be paid to these taxing bodies. Money is borrowed against the projected increase in taxes predicated on expenditure, normally but not exclusively, on physical infrastructure. This is effectively “securitizing future tax increments” (Launius and Kear, 2019: 1343). In most cases, this borrowing occurs through the issuing of revenue bonds. The effective ring fencing of revenue continues for a specified period, in most cases either 23 or 25 years. Over that time, the payment of “base assessed value” continues to the normal tax-collecting authorities. Meanwhile “the increment” – the difference between the frozen rate and the post-expenditure rate multiplied by the value of the taxable properties in the ring-fenced land – accrues to a separate authority. In some cases, this “TIF authority” is city government itself (e.g. Chicago), while in others (e.g. California) it is administered by a specially established agency. At the termination of the TIF, the land is no longer ring-fenced and the “total assessed value” returns to the jurisdiction of the pre-TIF taxing bodies (for more detailed explanations see Johnson and Man, 2001).

The Tax Increment Financing (TIF) model.

Most US states require that the project area meet both a “blight” and a “but for” requirement. Blight may be construed in a number of ways, although most definitions hark back to the 1960s and 1970s heyday of urban renewal in which the condition is defined as one that threatens public safety, health, morals, or welfare (Breger, 1967). However, as Gorden (2004: 307) notes, it is “less an objective condition that it is a legal pretext for various forms of commercial tax abatement.” The municipality must also attest that the area would not develop in the absence of incremental revenues derived from the creation of a TIF district. In other words, “but for” the use of TIF developers would not invest in the area and redevelopment would not occur.

Views in the US on TIF remain mixed. On the one hand, according to Johnson (2001: 257), “TIF has become a useful, effective instrument for local governments”. There are certainly a host of, largely supportive, studies of how TIF has been deployed (Arvidson et al., 2001; Chapman, 2001; Klacik, 2001; Leavitt et al., 2008; Mason and Thomas, 2010). In contrast are those who take a more critical stance. Arguing, “TIF is not a passive tool, but rather an agent of spatial transformation” (Pacewicz, 2016: 283), there have been various critiques (Briffault, 2010; Kirkpatrick and Smith, 2011; Lefcoe, 2011; LeRoy, 2008; Pacewicz, 2013, 2016; Teresa, 2017; Weber, 2002, 2010). These have argued that the use of TIF has facilitated the displacement of poorer communities, the gentrification of many US downtowns, constituting a revenue “loss to noncity taxing governments” (Pacewicz, 2016: 282) and raising issues of democratic accountability, financial equity, social justice and the right to the city. Yet TIF continues to be widely used across the US to finance urban redevelopment projects of various shapes and sizes (Beyer, 2015; Peterson, 2014). On a variant of Harvey’s urban entrepreneurialism argument, it is possible to understand TIF as subject to endless “serial reproduction” albeit of the means of financing development rather than the flagship projects at the centre of Harvey’s attention.

Experimenting with TIF: Lexington and the example of CenterPointe

Introducing Lexington

With a population just over three hundred thousand and centred in one of the poorest and more rural US states, the recent history of Lexington’s downtown is a familiar one. Situated in the Inner Bluegrass region and its “rolling parkland, seemingly endless lines of white and brown wooden fences, horse barns complete with cupolas; and a scattering of small settlements” (McCann, 1997: 644) is Lexington. It is a city whose initial emergence and formative years, like its near neighbour Louisville, were honed and shaped by its place in the wider US slave system (Cummings and Price, 1997; McCann, 1999). While not Atlanta, Charlotte or Houston – the US “sunbelt boomtown” described by Feagin et al. (1989: 241)6 – McCann (1998) suggests that contemporary Lexington should be understood as part of the contemporary urban South, bearing the imprint of a particular racialized cultural, economic and social landscape (Schein, 1997), “with both racially concentrated poverty and affluence on the rise since 1970” (Shelton, 2018: 283).

From the late 1950s-onwards the suburbanization of capital and (a mostly white) population undermined the central urban core, as it did across many US cities, producing a highly racialized set of inner city neighbourhoods. Lexington’s economic base was restructured such that by the turn of the twenty-first century it had become “a regional service center for producer and financial services and an attractive site for corporate relocation from the ‘rustbelt’” (McCann, 1998: 98). Representationally and reputationally the city and nearby counties remain known primarily for their distilling and thoroughbred horse industries (Roberts and Schein, 2013).7 Yet despite the imaging of the city as tied to horse breeding and distilling, the five largest employers in Lexington are the University of Kentucky, Fayette County Public Schools, Amazon.com, Lexington-Fayette Urban County Government, and Conduent.8

During the 1960s and 1970s, the city government used various federal programs in its attempt to mitigate the effects of suburbanization through urban renewal (Jones, 2003). The construction of the combined Lexington Convention Center/Rupp Arena, opening in 1976, perhaps best encapsulates the approach to the creation of a “new downtown” (Freed, 1983: 39), although as Jones’ notes (2003: 112) “the question of the declining downtown retail district was still an issue” some twenty years later. However, the well-documented withdrawal of federal grants from the late 1970s forced the city government to rethink first their approach to the governance of redevelopment before turning to its financing.

In 1988 The Downtown Lexington Corporation (DLC) was formed as an A 501(c) 4 membership-based event and marketing not-for-profit agency. It sought to promote and represent the downtown as a place for business, residential life and entertainment. Its establishment was a response by downtown economic stakeholders to what they perceived as a favouring of suburban development by city government. It worked with the longer-established branch of the local government, the Lexington Downtown Development Corporation (LDDC), and marked a change in who was involved in envisioning the future of the downtown (Jones, 2003).9

During the 1980s and into the 1990s these agencies led on a regular series of reviews and strategies for the downtown. According to McCann (2002: 2320), the city displayed many characteristics “that would define it as an entrepreneurial city”. The period saw some limited commercial, residential and retail development, as older, more established commercial structures and housing developments were replaced by concrete and glass buildings that gave the downtown a “distinctly Bluegrass, horse farm feel” (McCann,1998: 222).10 Some of the most visible developments, such as the Vine Center and the Lexington Financial Center, completed in 1982 and 1987 respectively, are owned by the Webb Companies, a Lexington-based commercial real estate firm. Family-owned and private, it has been behind many of the most contentious and high profile downtown and suburban developments since the latter part of the 1970s. Over the decades, the Webb family, initially its founders Donald11 and Dudley Webb, and subsequently Donald’s son, Woodford Webb, have used their ownership of a number of key sites in the downtown area to secure a central role in shaping the debate over the future of the city’s downtown. The company was and remains a classic example of those “who have the most to gain … in land-use decisions” (Logan and Molotch, 1987: 62).

Those who govern the city’s downtown –have sought to reimagine its space economy in three relational ways. The first is in its proximity to the historically larger urban centres of Cincinnati and Louisville, as part of a notional “golden triangle” (Whitt, 1987; Whitt and Lammers, 1991; Sroka, 2019). The second is in relation to other similar sized college towns or university cities, such as Ann Arbor, Michigan, Boulder, Colorado and Madison, Wisconsin.12 The third is in comparison to other larger cities in terms of its liveability and walkability, with the claim that “pedestrian movement in downtown Lexington matches levels in much larger cities” (Lexington Downtown Development Authority, 2016: 8). These strategies have sought to re-imagine and re-present the Lexington downtown as comparable and competitive with larger and more obviously urban cities. This racially and spatially selective strategy is geared towards a cosmopolitan, educated and urbane audience drawn to the sites it is seeking to redevelop. It was in this general context that Lexington’s city government turned to Tax Increment Financing (TIF).

The political economy of tax increment financing: the case of Lexington, Kentucky

The balance of political power in the Commonwealth of Kentucky lies with the poorer and less populated rural counties, meaning any attempts to allow some entities to retain taxes that would otherwise accrue at the state level (potentially being redistributed to poorer, rural areas) tend to be resisted. With their (relatively) large urban cores, inherited industrial infrastructure, suburban tendencies and diverse populations at least in relative terms, Lexington (and, of course, Louisville) have had to work hard to match the type of entrepreneurial and speculative financial experimentation and innovation that has occurred in neighbouring states, such as Ohio, as well as across the US more generally. So, while numerous other US cities began using Tax Increment Financing (TIF) during the late 1980s and throughout the 1990s (Johnson and Man, 2001), it was not until 2009 that Lexington’s first TIF project was designated. The early work to enable TIF in Kentucky was undertaken by interests looking to use it in Louisville, and specifically to support that city’s Downtown Marriott redevelopment. The lobbying and pressure involved was a combination of consultants from neighbouring Ohio where TIF was already being used, alongside local elected officials and officers. While the original Kentucky TIF legislation was introduced in the 1980s, there “weren't a lot of definitions and there weren't a lot of rules, and there wasn't a lot of math” involved (#11, Senior Official, Louisville public agency). Eventually it was “declared unconstitutional” (#2, Finance lawyer, private sector, Cincinnati), although not until after Louisville had established four TIF projects (Sroka, 2020).13 The subsequent rewriting of the Commonwealth Statute,14 involving out-of-state-consultants and elected officials, drew upon the perceived success of its use in Louisville and its potential for use elsewhere in the state. Its adoption led other, smaller cities and jurisdictions, to begin to explore its use in their downtowns. In the case of Lexington, interest in TIF within city government began as attention turned (once again) to encourage redevelopment. The interest centred on clearing sites that were understood to be depressing property values and as detrimental to attracting commercial investment in the form of residential and retail development. For Weber (2002: 190) “the miniaturization of fiscal space through TIF assists the local state in preparing urban property for the deep excavation of value”. As different interviewees explained: I was having conversations with folks who were saying we love Lexington but they love Lexington on paper, they come to visit, they walk around and they say ‘where are … the people?’ You know? And … what we realised is that we hadn’t created an environment to encourage investment because … you had folks kind of looking and saying, ‘yeah, I just don’t see, I don’t know how I’m going to lease this’ (#1 Leader, public private partnership, Lexington) Probably ten years ago, downtown was not a place that, you know, many people would go … for entertainment or restaurants. There were a few restaurants, but it mostly kind of a government centre, law offices, that kind of thing, had … very little retail after about 1970 (#9, local journalist, Lexington) Well we want to be able to attract people here … from a liveable standpoint, you want people to want to live downtown because back in the ’80s and ’90s, you know, Lexington was, don’t live downtown, work here but live out in the suburbs, that was the model. However, now, you know, we're trying to get people to live back downtown … to come downtown and be your hub for entertainment, your hub for culture, arts (#13 elected official, city government, Lexington)

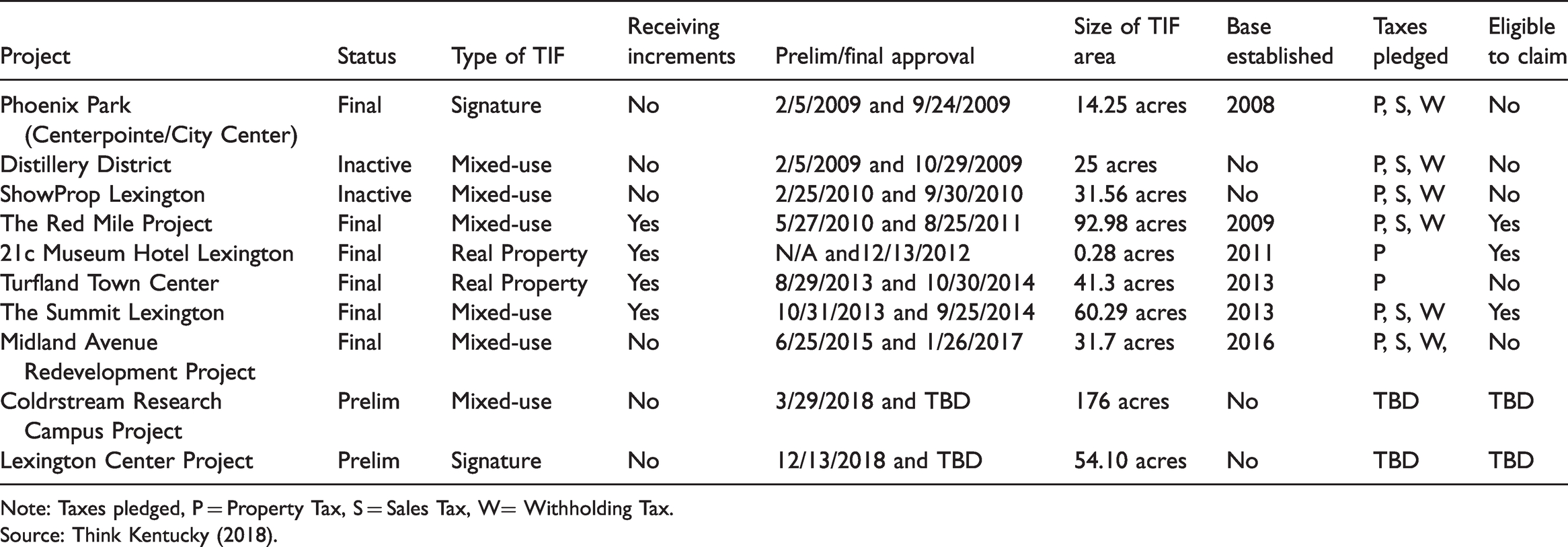

Lexington’s TIF projects, 2018.

Note: Taxes pledged, P = Property Tax, S = Sales Tax, W= Withholding Tax.

Source: Think Kentucky (2018).

First, while three types of TIFs have been approved - “mixed use”, “real property”, and “signature” – over half were designated “mixed use”, which required the city to make a case that the area had indeed experienced “blight” (Team Kentucky, 2019). This has been a contentious process and Lexington has used TIF predominantly as a means to pay the public infrastructure costs associated with entertainment-, residential- and retail-centred- redevelopment. Second, the TIF projects vary considerably in size, ranging from 0.28 acres (21c Museum Hotel) to 176 acres (Coldstream Research Campus), although half are between 25 and 60 acres. Third, the geography of the city’s use of its 10 TIF projects is such that half are within one mile of central downtown, seven of the 10 projects are within 2 miles, and only the Turfland Town Center, The Summit and the Coldstream Research Campus projects lie towards the outer parts of the city. Lexington’s focus appears to have been to develop TIF projects that rest on the redevelopment of inner core brownfield sites, particularly those under-capitalized because of industrial decline and economic restructuring. Fourth, of the city’s ten approved TIF projects, two – the “Distillery District” and “ShowProp Lexington” are “inactive” and two – “Coldstream Research Campus Project” and “Lexington Center Project” – are still at the “prelim” stage. The status of the remaining six, including Centerpointe/Phoenix Park, is “final”. However, of these six, only half are receiving “increments” at the current time - the 21c Museum Hotel, the Red Mile Project and the Summit. In other words, only three of the city’s 10 approved TIF projects have proceeded to the point where the TIF instrument is doing what it is designed to do; to capture the increment in taxes that occurs through redevelopment.

Over the decade since its approval, the Centerpointe TIF has been amended three times, in May and December 2013 and again in May 2014. It remains on the books but has not been “actualized” (Callon, 2007: 230). The renaming of the Phoenix Park TIF as CenterPointe reflected the site’s strategic importance to the realisation of the wider redevelopment scheme, as at the centre – quite literally – of the TIF area is the two-acre site at 100 West Main Street with which we began this paper. The TIF district was designated a “signature project” under the Kentucky statute. In part this reflected the symbolic importance of the site in the city while also signalling that it had local and state involvement and was “judged to be of such magnitude as to warrant extraordinary public support” (Team Kentucky, 2019: 4). Its tax base was set in 2008, with property, sales and withholding taxes pledged, and a TIF term of thirty years was established. Estimated project costs were just under one billion US dollars. After almost a decade of being known as “Centerpointe”, in April 2018 the redevelopment was renamed as “City Center”. This change was “prompted in part by the Marriott hotel group, which has a new brand of downtown hotels with “City Center” in the name”, and which features in the redevelopment.

To some this two-acre site was run down and shabby, meaning relatively low land value, while for others it was part of the character and fabric of the downtown, where use values trumped exchange values. Either way, the Main Street block failed to fit the emerging vision for the area as outlined both by city government and by the landowners. Nor was it understood to be good for the property base (Spriggs, 2014; Weber, 2002). Instead, the site offered significant real estate potential: One of those rare properties … It's in the heart … it literally is the heart of downtown (#13 elected official, city government, Lexington) There had been rumours for some time … but until it was all unveiled, you know, there was really not much of a … no widespread sense of what was going on, um, and it was a big surprise for everyone (#9, local journalist, Lexington) Part of what we lack in Lexington is any geographic marker that says this is the centre of town … So we don’t have a river, we don’t have a beachfront! (#1 Leader, public private partnership, Lexington)

On the one hand, the use of TIF politicized the project given the lack of consultation and engagement with the public prior to the project announcement by the developer: They (the Webb Companies) presented as … this is a done deal, we have the money, we’re ready to go, and they used that to, um, as leverage to get, you know, get permission to, um, you know, get around the historic protection that covered much of the Main Street properties, and … and tear down all the stuff (#9 local journalist, Lexington) In the downtown area, there were some existing buildings that were actually in pretty bad shape, but there were some people who had an interest in preserving those and so… they were upset when the buildings were then demolished (#2, Finance lawyer, private sector, Cincinnati)

Shortly after the confirmation of the TIF, it was announced the “key financial backer” for the project had passed away, rendering the project’s finances uncertain. Jim Gray, the Vice Mayor at the time (who would later go on to become the city’s Mayor between 2011 and 2019) questioned whether the site would ever be developed.16 Yet there were very clear limits to what city government could do to move the redevelopment forward. The broader political context of a moderate-sized city in a conservative State is key to the failure to move forward. Despite Eminent Domain legislation dating back to the mid-1970s, city government “never had the political will to make developers and large property owners — especially those downtown — look out for the city's best interests” (Eblen, 2009: np). As one interviewee noted: Our Mayor learned that, you know, the hard way because he … you know, private property rights in our states are very important, and maybe everywhere, but it's even more so here in Lexington and the law’s very clear. Now you can entice them … We can get on TV. We can do all that kind of fun stuff but at the end of the day legally we really don’t have a fight. It's really his property. He can do what he wants with it (#13 elected official, city government, Lexington)

While the story highlights the power of the property owner, the failure to establish the TIF also stems from the very nature of the instrument itself and the capacity of certain size and types of US cities to deploy it. As we suggested at the outset of the paper, the complexity of financing arrangements can be challenging for local interests that are not well versed or experienced in their use. City government was concerned about the risks involved in establishing the debt through the TIF, particularly in the context of fragile and uncertain relations with the landowners and developers. More than one of our interviewees highlighted the issue: That puts the cities in kind of a tough position because they’re again trying to underwrite projects that are far more complicated than they probably have the ability to underwrite (#1 Leader, public private partnership, Lexington) However, when you’re talking about smaller cities … tax increment financing is very complicated. Whenever someone asks me to go over the details of how it’s set-up, I just, you know, it’s like my brain just explodes and I say, please talk to a tax attorney (#7 senior official, Kentucky public agency, Lexington)

(https://www.wkyt.com/content/news/We-gave-it-a-hell-of-a-run-Lexington-restaurant-closes-years-after-relocating-500856871.html). Moreover, the use of TIF, in this instance, for a retail-development at the fringe of the city might well bring into question the city’s ability to match its financing strategies with its vision of downtown revitalization.

Conclusion

At the time of writing, it is not long since the topping off ceremony for the City Center development. If, as Feagin (1983) suggests, downtown redevelopment is a game then there appear to be no winners in the time that has elapsed since the announcement of Lexington’s flagship development, other perhaps than neighbouring cities in the US urban South. Lexington’s loss is likely to have been at Cincinnati, Louisville and Nashville’s gain.

A lot continues to be written about the growing use of ever more speculative financial instruments by US city governments, particularly that subset that generate debt, such as Tax Increment Financing (TIF) (Pacewitz, 2013, 2016; Sroka, 2016, 2020; Teresa, 2017). Not without precedence, nevertheless, the argument is that recent decades have seen an expansion in the use of an ever-more diverse and complex set of financial instruments to support urban economic and infrastructural development in the US. As various interests have “actively promoted the adoption and subsequent promotion of TIF as an economic development instrument” (Weber and O’Neill-Kohl, 2013: 193) its position has been cemented as “one of the most widely used state and local economic development policies” (Man, 2001: 1). The case of Lexington, Kentucky is one that certainly fits that general trend.

In this paper however, the example of Lexington, Kentucky and of the TIF that never was, suggests that we might want to complicate the story of an enduring and inevitable financialization of urban development. To do that we return to the three arguments introduced at the outset of the paper. First, the case highlights the tremendous amount of political work required to introduce and deploy the type of speculative financing mechanisms that increasingly serve to underpin urban redevelopment.

Furthermore, the case suggests that despite protracted interactions this work is sometimes unsuccessful. The work involved in assembling the TIF for the project at the centre of this paper involved a complex mix of elected officials with various local and State agencies, expert consultants and those with stakes in securing and developing the exchange value of land and property. In short, the financialization of urban redevelopment and the complexities that accompany it are key to understanding the fragmented, haltering politics of downtown development in Lexington, and indeed more generally. Eschewing the tendency towards emphasizing “clean breaks and dramatic, totalizing changes” (Weber and O’Neill-Kohl, 2013: 193), we would argue instead for an appreciation of the indeterminate, messy, open and unpredictable nature of the politics surrounding the introduction of financial instruments to underpin urban redevelopment. The Lexington case highlights the need to explain rather than assume success.

Second, we are keen to highlight those many cities beyond or outside the more high profile centres that attract the “circulation of fast, fictitious money” (Weber, 2002: 190). Lexington was a site off the map for most investors, especially those with extended and diverse geographical reach. It has an altogether more geographically proximate set of real estate developers arguing and lobbing city government for the use of TIF. Echoing older arguments over the centrality of local dependence (Cox and Mair, 1988), the paper has demonstrated the challenges that some US cities face in performing entrepreneurial urbanism using speculative financial instruments. Beyond the global cities that compete for major corporate investments or events of global reach such as the Olympics lie a significant number of cities that are nevertheless engaged in competition with one another. In this sense there is likely to be considerable intellectual mileage in building our theories and understandings from the experiences of “ordinary cities” whether we study Lexington, Kentucky, Fort Wayne, Indiana, Greensboro, North Carolina or Tacoma, Washington to name just four examples (McCann, 1998). As Williams and Pendras (2013: 302) suggest: “many cities … diverge significantly from the political economy of neoliberalism as it has typically been understood to play out in “winner” and “loser” cities”. Perhaps the mundane, faltering and seemingly haphazard story of Lexington, Kentucky’s development is not far from the norm. While the modest size of the city and the more limited set of private actors and elected and appointed officials that come with that might be assumed to simplify and ease the development of a collaborate urban vision and development strategy, the evidence in this case however, suggests that stasis is the default condition despite its parochial character.

Thirdly, and combining these two arguments, the evidence presented in this paper suggests that the complex navigation and successful execution of speculative financing is predicated on a mutual understanding between the key political and economic interests with vested interests in urban development. In the Lexington case, that failure of collaboration – the ‘glue’ that holds together growth coalitions and urban regimes – has ensured that the TIF has worked to disrupt rather than enable urban development.

Augmenting attention to general tendencies in the financialization literature, this paper has highlighted the use of one particular financial instrument that stands in for a much wider suite of riskier and more speculative options for US local governments. The result of the commercial development at the center of this paper highlights the inevitable chance of failure that accompanies speculation. We suggest a continued appreciation of the complications and vagaries attached to the financialization of urban policy particularly in the context of an increasingly fragile and uncertain period of contemporary US urban policy-making.

Footnotes

Author biographies

Acknowledgement

The authors thank all the interviewees in this research project and the anonymous reviewers for their helpful and constructive comments.