Abstract

Research on employee voice has highlighted the potential consequences for individuals and organizations when speaking up to supervisors. Literature shows that employee voice influences employees’ performance ratings. Nevertheless, these findings are inconsistent, providing evidence for the influence of moderating effects on this relationship. This study contributes to a better understanding of the relationship between employee voice and supervisors’ performance rating by taking into consideration supervisors’ implicit followership theories. To test the moderation effect of supervisors’ implicit followership theories, this study uses an experimental design and a German sample of professional accountants (n = 183). The results show that employee voice affects supervisors’ performance ratings positively and that this relationship is moderated by supervisors’ negative implicit followership theories. When supervisors have negative implicit followership theories they rate employees better in their performance. The study provides insights into supervisors’ responses to employee voice and the influence of implicit assumptions that supervisors have about followers.

Introduction

In recent years, researchers have studied employee voice—that is, employees’ communication about concerns, suggestions and grievances in the workplace (Morrison, 2011)—because of its beneficial outcomes for organizations (see Bashshur and Oc, 2015). It has been shown that engaging in voice can improve organizations’ overall functioning and performance (Frazier and Bowler, 2015; Gao et al., 2011) by helping organizations to create new innovations and to correct and prevent errors (Wei et al., 2015).

To gain these benefits, supervisors rely on employees’ voice because front-line employees are more likely to detect issues and problems than supervisors are (Morrison, 2014). Thus, in rephrase it would seem that supervisors reward employees who speak up because they help the organization and the supervisor to be successful (Burris, 2012). Nevertheless, studies indicate that employees are often afraid to show voice because doing so might have negative consequences for themselves or their colleagues (Milliken et al., 2003).

To date, research on the individual-level outcomes of employee voice is limited, and most of what there is focuses on how voice behavior influences individual employees’ performance ratings and career success (e.g. Burris, 2012; Whiting et al., 2008). These findings show both positive and negative effects (Morrison, 2014). For example, Seibert et al. (2001) found a negative association of employee voice with salary progression and promotions, suggesting that employee voice harms employees’ career success. Moreover, Burris (2012) showed that employee voice has a negative effect on performance ratings when voice is challenging. However, the author pointed out that the effect is positive when voice is supportive, and Whiting et al. (2008) substantiate the positive relationship.

These inconsistent findings are not surprising, since performance ratings are complex processes whose results are influenced by many different factors (e.g. raters’ dispositions, organizational context) in addition to actual performance (for a review, see DeNisi and Murphy, 2017). To better understand the influence of voice on supervisors’ performance ratings it is therefore necessary for the analysis to include factors that can shape this relationship (Chamberlin et al., 2017). In this regard, Scullen et al. (2000) showed that most of the variation in supervisors’ performance ratings depends on implicit assumptions about individuals. That means, raters automatically tend to use categorizations, benchmarks, or schemas that they have stored in their minds to organize information and interpret employees’ behavior based on that information (Feldman, 1981).

In literature, different constructs of such assumptions are distinguished. Some of them refer to the supervisor, some of them to the follower. However, especially the assumptions about the follower might influence the judgment of the supervisor when it comes to performance ratings. Building on this, supervisors’ implicit followership theories (IFTs)—that is, supervisors’ assumptions and beliefs about their followers’ traits and behaviors (Sy, 2010)—might affect how supervisors assess the performance of employees who speak up. Research shows that supervisors’ IFTs can shape the perceptions, judgment, and behavior of supervisors in their interactions with followers (Sy, 2010) as they function as an interpretative frame to understand employees’ behavior. Depending on whether these IFTs are positive or negative, they might affect how supervisors respond to employees’ behavior (Sy, 2010). As such, differences in supervisors’ IFTs can have a significant impact on the relationship between employee voice and supervisors’ performance ratings. Building on this, analyzing the moderating effect of IFTs on this relationship might help to receive a more fine-grained picture of when employee voice leads to positive or negative performance ratings.

Therefore, the aim of this study is to analyze whether supervisors’ IFTs moderate the effect of employee voice on supervisors’ performance ratings. To achieve this goal, I use a quasi-experimental design to analyze how supervisors rate employees’ performance after the employees engage in voice behavior as well as the moderating effect of supervisors’ IFTs on this relationship.

By testing these effects, the paper contributes to the literature in two ways. First, it improves our understanding of the boundary conditions—that are, contingent factors that determine the relation among variables (Gonzalez-Mulé and Aguinis, 2018)—of the individual-level outcomes of employee voice. Although a few studies analyze the effect of employee voice on performance ratings, their results are mixed, suggesting that other factors influence the relationship between these variables (Morrison, 2014). Prior research has found that the relationship might be contingent on the message, context, and source of voice (e.g. Burris, 2012; Whiting et al., 2012). The paper extends this research by taking into consideration supervisors’ IFTs as a moderator variable and adopting a receiver-centered perspective. By doing so, the study provides better insights into the question concerning the conditions under which employee voice has positive or negative effects on supervisors’ performance ratings. Further, analyzing supervisors’ IFTs as boundary conditions are useful to extend the theory of the individual-level outcomes of employee voice.

Second, the study extends the literature on followership. Up to now, the role of followers in the leadership process is widely neglected (Uhl-Bien et al., 2014). This study may help to explain how supervisors’ assumptions and beliefs about followers’ traits and behaviors can affect supervisors’ response to employee voice. More specifically, the paper sheds light on the effects of positive and negative assumptions on individual-level outcomes and calls for a more fine-grained analysis of the characteristics of implicit followership theories.

Conceptual background and hypotheses

The effects of promotive and prohibitive voice on supervisors’ performance ratings

Employee voice is conceptualized as “discretionary communication of ideas, suggestions, concerns, or opinions about work-related issues” (Morrison, 2011: 375). By showing voice behavior, employees provide information about how to improve organizations’ working procedures and how to correct and prevent errors in organizations. As the definition highlights, the term voice can be used for various types of information, which researchers distinguish as either promotive or prohibitive. Promotive voice is the communication of suggestions to improve work practices, while prohibitive voice is the expression of concerns about issues that might be harmful for organizations (Liang et al., 2012).

Previous research on voice focused on identifying the individual and organizational antecedents of employee voice to describe under which conditions employees speak up (for a review, see Morrison, 2023). In this regard, researcher have shown that fear of negative consequences reduces the likelihood of speaking up (Morrison, 2014). However, the understanding of the consequences of employee voice remains scarce. In a long-term study, Seibert et al. (2001) demonstrated that employees who exhibit voice behavior are less likely to be promoted and are more likely to have lower salary increases. Burris (2012) founds a similar effect by analyzing the influence of voice on employees’ performance rating. He showed that supervisors give lower ratings to employees who engage in voice that is rather challenging, thus highlighting that the message’s content influences the supervisor’s reaction. Therefore, how promotive and prohibitive voice act on supervisors’ reaction regarding employees’ performance rating must be analyzed separately.

Promotive voice addresses how organizations can improve processes and functions. Liang et al. (2012) characterize promotive voice as being future-oriented, as it points out how organizations can perform better in the future. Although this behavior might be challenging for the employee’s colleagues, supervisor and organization because it requires taking action, this type of voice is considered to be positive.

According to social exchange theory, people tend to reciprocate a person’s positive behavior by doing the person a favor in exchange (Cropanzano and Mitchell, 2005). If employees speak up about improvements in work processes that their supervisors may not be able to see on their own, they help their supervisors to be successful and efficient in doing their jobs. As a result, supervisors are able to make decisions to improve the organization’s overall functioning and performance (Whiting et al., 2008). In exchange, supervisors reward this positive behavior by rating those who make such observations and speak up about them higher than they rate those who don’t.

In sum, I expect that supervisors will reciprocate the help of employees who engage in promotive voice by rewarding them with performance ratings that are higher than those of employees who do not show promotive voice behavior. Therefore, I hypothesize:

Hypothesis 1a: Promotive voice is positively related to supervisors’ ratings of employee performance.

In contrast to promotive voice, prohibitive voice may be interpreted as more challenging by supervisors. As prohibitive voice points out problems and errors that might be harmful to the organization, it implies that one or more people in the organization made a mistake. It also requires a quick action to prevent damage to the organization, both of which can lead to negative emotions and conflicts in the team. Prior research has shown that the performance ratings of employees whose voice is challenging are lower than those of other employees (Burris, 2012). In a meta-analysis, Chamberlin et al. (2017) reveal that prohibitive voice has a negative effect on performance ratings, so supervisors might perceive it as negative.

According to self-affirmation theory, people strive to develop and maintain a positive self-image. As such, they feel threatened by events that challenge their positive images of themselves as competent and successful (Steele, 1988). This is the case if people do not fulfill the standards of society. To protect their self-esteem people then try to eliminate or devalue the source of the threat (Nadler and Jeffrey, 1986). At work, threats to the self might occur if someone fails to meet the standards of the organization, supervisors, colleagues or followers (Harari et al., 2022). As recipients of prohibitive voice, supervisors may feel threatened if they see it as criticism of their work, and it may make them feel that they are not as competent as they thought they were. To protect their self-esteem, supervisors tend to devalue the behavior of an employee who presents prohibitive voice by giving the employee a poor performance rating, thus making the behavior irrelevant to the supervisor’s self-esteem (Popelnukha et al., 2022) and protecting the supervisor’s positive self-image.

In sum, prohibitive voice may challenge supervisors’ self-image, as it reveals errors or grievances that might be harmful to the organization. To protect their self-image, supervisors might give employees that show prohibitive voice worse performance ratings than they give employees who show no voice behavior at all. Therefore, I hypothesize:

Hypothesis 1b: Prohibitive voice is negatively related to supervisors’ ratings of employee performance.

The moderating effect supervisors’ positive implicit followership theories

Research has determined that performance evaluation is a complex cognitive process in which a person (typically the supervisor) captures relevant information about an employee’s performance (Murphy, 2020). Research showed that raters often draw on information in their memories, such as categorizations, schemas, implicit assumptions, and biases, to make this kind of judgments because of limitations in their information-processing capacity (Ferris et al., 2008).

I argue that supervisors’ performance ratings of employees’ who exhibit either promotive or prohibitive voice are contingent on the supervisors’ IFTs. Supervisors’ IFTs are assumptions about followers’ traits and behaviors stored in the supervisor’s memory that have been developed via socialization and leader-follower interactions in the workplace (Sy, 2010). These assumptions are rarely conscious and often not expressed which is why they are called implicit theories. However, this does not preclude the explicit expression of these assumptions.

In literature, the central components of IFTs are prototypes. These prototypes are defined as “abstract composites of the most representative member or the most commonly shared attributes of a particular category” (Sy, 2010: 74). That means IFTs describe typical assumptions of followers’ traits and behaviors which are shared by a certain group of people. In an exploratory factor analysis, Sy (2010) identified positive and negative characteristics that describe a typical follower most often, resulting in an 18-item measure of IFTs. According to Sy (2010), positive IFTs characterize followers as industrious, enthusiastic, and good citizens. These categories include traits like, for example, being hard-working, loyal, and reliable (Sy, 2010). Negative IFTs characterize followers to be conforming, insubordinate, and incompetent. These categories include traits, for example, as easily influenced, arrogant, and unexperienced (Sy, 2010). The positive and negative characteristics are theoretically independent from each other as they focus on different traits and behaviors. For this reason, it is possible to describe a typical follower with both negative and positive characteristics (Sy, 2010).

Research showed that supervisors’ IFTs serve as a sensemaking function in their effort to understand followers’ behavior (Gao and Wu, 2019; Sy, 2010; Veestraeten et al., 2021), so IFTs affect supervisors’ behavior and reactions when they interact with employees (e.g. Sy, 2010; Uhl-Bien et al., 2014). In everyday evaluations of employees’ performance, supervisors might activate these assumptions depending on whether they are positive or negative. Therefore, differences in supervisors’ IFTs can lead to differences in their ratings of followers.

Research on employee voice indicates that supervisors could interpret voice differently based on whether their IFTs are positive or negative. Positive IFTs carry over to supervisors’ assessments of employee behavior, so employees might be perceived as committed and productive. This suggestion is in line with Sy (2010), who founds a positive relationship between positive IFTs and leaders’ expectations of employees. Therefore, supervisors’ IFTs might shape their interpretations of promotive and prohibitive voice. Supervisors with high levels of positive IFTs might interpret both promotive and prohibitive voice as positive because their IFTs signal that employees who engage in either kind of voice are hardworking and want to improve their organization (Veestraeten et al., 2021). Therefore, supervisors holding high positive IFTs may assess followers’ behaviors positively and may response to these behaviors positively (Sy, 2010). For example, supervisors who think their followers go “above and beyond” in their jobs might expect that their employees engage in voice proactively to help their supervisor and organization and thus, reward this kind of behavior. Therefore, employees showing promotive voice will receive a better rating of job performance when supervisors hold high positive IFTs. In addition, supervisors high positive IFTs will weaken the negative association with prohibitive voice.

Therefore, I propose that positive IFTs shape supervisors’ expectations of employees’ voice behavior such that promotive voice and prohibitive voice will be interpreted more positively. Therefore, supervisors will rate employees higher in performance when they have high positive IFTs. Accordingly, I propose that the positive effect of promotive voice is stronger when supervisors’ positive IFTs are high. Further, I hypothesize that the negative effect of prohibitive voice weakens under those conditions.

Hypothesis 2a: Supervisors’ positive IFTs moderate the relationship between promotive voice and supervisors’ ratings of employee performance such that the positive relationship is stronger when supervisors’ implicit followership theories are positive.

Hypothesis 2b: Supervisors’ positive IFTs moderate the relationship between prohibitive voice and supervisors’ ratings of employee performance such that the negative relationship is weaker when supervisors’ implicit followership theories are positive.

The moderating effect of supervisors’ negative implicit followership theories

In contrast, high negative IFTs may lead to a negative behavior of supervisors (Sy, 2010). Assuming that supervisors’ negative IFTs shape their interpretations of employee’s behavior, supervisors who perceive followers as, for example, inexperienced might evaluate their behavior negatively because they do not expect that these employees have sufficient knowledge to be competent.

Scholars on employee voice show that voice leads to more positive individual outcomes when voice quality is high than when it is not (Brykman and Raver, 2021), when voice is perceived as competent (Weiss and Morrison, 2019) and when it is communicated respectfully (Krenz et al., 2019). Therefore, supervisors who have high levels of negative IFTs are likely to perceive both promotive and prohibitive voice as negative because they interpret it as, for example, incompetent or rude. This might lower supervisors rating of employee’s performance.

Therefore, I predict that negative IFTs shape supervisors’ expectations of employees’ voice behavior such that both promotive voice—despite its usually positive interpretation—and prohibitive voice will be interpreted negatively. Therefore, the direct effect of employee voice on supervisors’ performance ratings will be weaken when supervisors have high negative IFTs. Accordingly, I propose that the positive effect of promotive voice weakens when supervisors’ level of negative IFTs is high and that the negative effect of prohibitive voice strengthens under the same conditions.

Hypothesis 3a: Supervisors’ negative IFTs moderate the relationship between promotive voice and supervisors’ ratings of employee performance such that the positive relationship is weaker when supervisor’s implicit followership theories are negative.

Hypothesis 3b: Supervisors’ negative IFTs moderate the relationship between prohibitive voice and supervisors’ ratings of employee performance such that the negative relationship is stronger when supervisor’s implicit followership theories are negative.

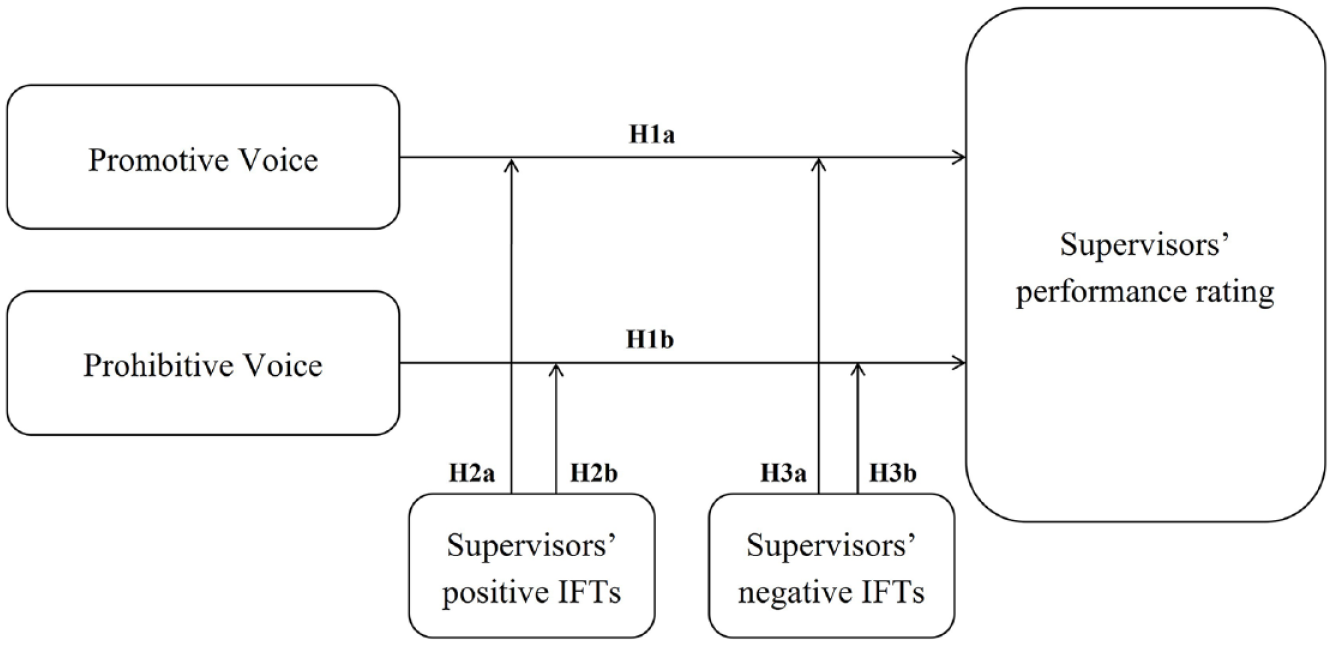

Figure 1 illustrates the overall research model. In summary, the study focuses on the moderating effect of supervisors’ IFTs on the relationship between employee voice and supervisors’ performance ratings. I propose a positive effect of employees’ promotive voice and a negative effect of employees’ prohibitive voice on supervisors’ performance ratings (H1a/b). To better understand the boundary conditions of this relationship, I include supervisors’ positive IFTs (H2a/H2b) and negative IFTs (H3a/b) as moderators in this model.

Conceptual model. H: hypothesis.

Research design

Participants and procedure

To test whether supervisors’ IFTs influence the effect of employee voice on supervisors’ performance ratings, I conducted an online experiment with employees of auditing firms using a scenario-based, between-person approach. I used e-mail addresses from the professional register of the German chamber of public accountants to distribute the survey to auditing firms. Focusing on one occupational group and one context reduces complexity and ensures comparability of the participants (Aguinis and Bradley, 2014). Furthermore, research indicates that professionals differ from rank-and-file employees because of characteristics like autonomy and professional identity (e.g. Brock et al., 2014; Grover, 1993; Von Nordenflycht, 2010).

To test the hypotheses, I manipulated the background information in vignettes from Köllner et al. (2019). All vignettes were in German and were modified (with the help of three experienced auditors) in terms of employee voice (no voice/promotive voice/prohibitive voice) and gender (female/male), resulting in six scenarios. I manipulated the gender of the employee who speak up to control for gender bias because supervisors’ IFTs typically differ for men versus women (Braun et al., 2017).

Participants who responded to the survey were randomly assigned to one of the six experimental conditions, in which they imagined themselves performing an annual audit for a client in the production industry. The participants took the role of a supervisor leading an audit assistant, either male or female, who was performing a balance confirmation task. In each condition, the assistant performs the task well. In the no-voice condition, the assistant does not mention anything noticeable about the task, in the promotive-voice condition, he or she identifies a more efficient way of performing the task, and in the prohibitive-voice condition, he or she encounters a mistake in which the supervisor was involved in the past. After reading the scenarios, the participants rated the performance of the audit assistant.

Pre-test, implementation check and common method bias

I conducted several procedures and tests to ensure that the design of the study minimizes the risk of potential biases and to increase the validity (Podsakoff et al., 2012). First, I developed the content of the scenarios with experienced auditors to ensure that the vignettes are realistic in this specific context. I, further, pretested the wording of the scenarios and the questionnaire on a sample of research assistants and auditors to examine whether the treatments worked as intended. Second, I tested whether there were significant differences in the main variables with regard to participants’ speed of response, which I did not find by using a t-test.

Third, I included an implementation check at the end of the questionnaire to verify that participants read the scenario carefully (Ejelöv and Luke, 2020). Therefore, I asked participants whether the employee in the scenario (a) spoke up about a concern to improve the work process, (b) pointed out a problem, or (c) did not mention anything noticeable. In line with other experimental studies (e.g. Köllner et al., 2019), only those participants whose answers were consistent with the voice manipulation of the scenario were included in the analysis. The instrumental checks resulted in the elimination of 15 participants.

Finally, I conducted two procedures to reduce common method bias (e.g. social desirability, measurement instrument). First, I reduced socially desirable responding by choosing an online experiment (Steenkamp et al., 2010; Weiber and Mühlhaus, 2014). In an online experiment, which can be conducted regardless of time and location, participants are alone and unobserved, ensuring their anonymity. Second, I reduced socially desirable responding, learning effects, and common method bias by using a between-subject design in the quasi-experiment and the randomization of the participants to the scenarios.

Measures

All scales were adopted from previous research to increase the validity and reliability of the measures. Further, the measures were administered in German and were translated and back-translated based on best practices to ensure their validity (e.g. Harkness et al., 2004). The arrangement of the items of the scales was randomly rotated to avoid a specific response behavior and, therefore, to reduce common method bias.

To measure the dependent variable, supervisor’s performance rating, I used a five-item scale adapted from Wayne et al. (1997) to which participants responded with answers ranging from 1 (“strongly disagree”) to 5 (“strongly agree”). Items included, “In my estimation, this employee gets his/her work done very effectively,” “All in all, this employee is very competent,” and “This employee has performed his/her job well.” The reliability of the scale was high as Cronbach’s Alpha was above 0.80 (α = 0.89).

The moderating effect of supervisors’ IFTs was measured with the 18-item scale developed by Sy (2010). Using a 10-point Likert scale, ranging from 1 (“not at all characteristic”) to 10 (“very characteristic”) participants assessed followership positive and negative characteristics. Nine positive items each were combined to form positive IFTs (hardworking, productive, goes above and beyond, excited, outgoing, happy, loyal, reliable, and team player) and negative IFTs (easily influenced, follows trends, soft-spoken, arrogant, rude, bad-tempered, uneducated, slow, and inexperienced). The internal consistency of the scale was on an acceptable level as Cronbach’s Alpha was 0.79 for positive IFTs and 0.71 for negative IFTs.

To avoid that the manipulation of voice impacted the measurement of this construct and the resulting spillover effects, the scale was positioned before the manipulation and the evaluation of the assistant’s performance.

I also measured several demographic variables, including the participants’ gender, age, work experience (“How many years have you been working?”), and leadership experience. According to the last one, I also measured the years of leadership experience and number of followers. Studies has shown that these variables affect supervisors’ performance ratings (DeNisi and Murphy, 2017).

The final sample consisted of 183 auditors from various audit firms in Germany, of which 27% were female and 73% were male. The average age of the participants was 45.84 years (SD = 11.23), and the average job experience was 19.36 years (SD = 9.86). Means, standard deviations, and correlations of variables are displayed in Table 1.

Descriptive statistics and correlations.

n = 183; employee voice was coded as 1 = no voice, 2 = promotive voice, 3 = prohibitive voice; performance rating: 5-point Likert; positive IFT was coded as 1 = low positive IFT, 2 = high positive IFT; negative IFT was coded as 1 = low negative IFT, 2 = high negative IFT; Pearson correlation (bivariate).

***p < 0.001.

Results

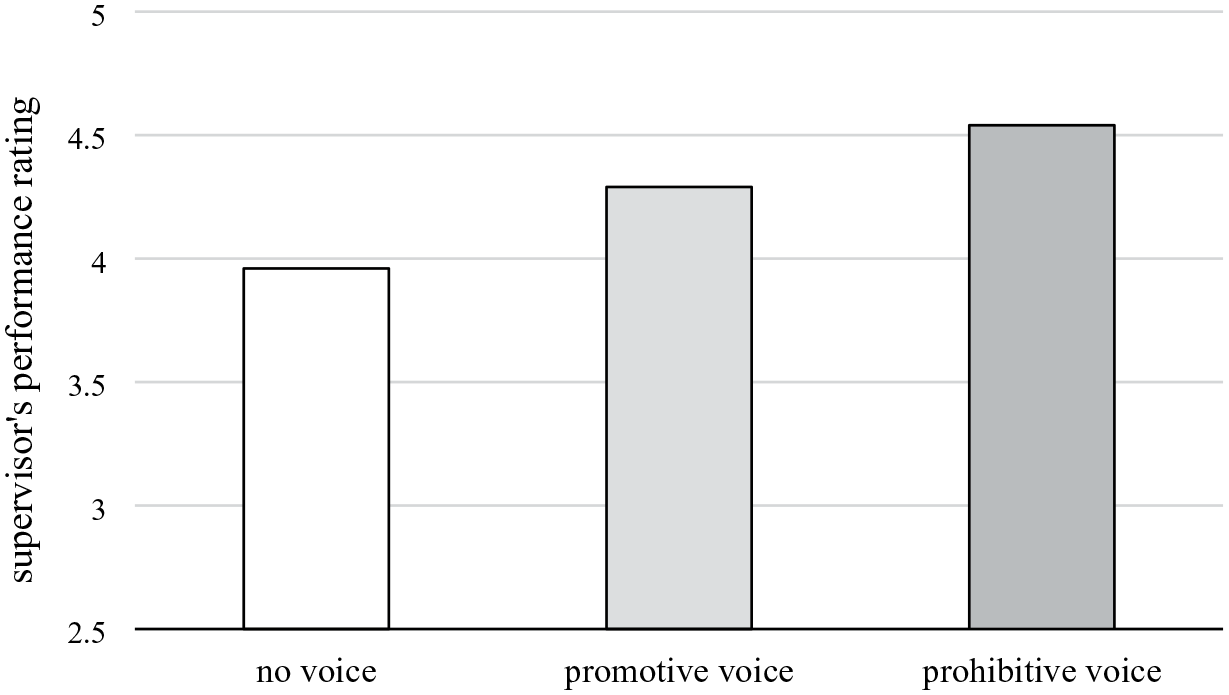

Table 2 shows the means and standard deviations for the experimental conditions. Because there were no significant differences in performance ratings based on the gender of the assistant in the scenario, I combined the male and female conditions of each voice condition.

Means and standard deviations across each experimental condition.

To get an overview of how the supervisor’s performance rating was influenced by the content of voice, I first conducted a one-way ANOVA with the three voice conditions as dependent variable and the supervisor’s performance rating as independent variable. The results indicate a significant differences in the performance ratings across the three conditions (F[2,182] = 9.448; p ⩽ 0.001). A Tukey post-hoc test revealed that this effect is attributable mainly to the difference between the no-voice condition and the two voice conditions, but not to a difference between the promotive voice and prohibitive voice conditions (Figure 2).

Differences in supervisors’ performance ratings.

To determine how supervisors’ performance ratings are affected by employee voice, I conducted two three-way ANOVAs with performance rating as the dependent variable and employee voice and supervisors’ positive and negative IFTs as independent variables.

As Table 3 shows, the first analysis revealed a statistically significant main effect of promotive voice on supervisors’ performance ratings (F[1,114] = 8.885; p = 0.004, part. η2 = 0.077). That is, the performance of employees who engaged in promotive voice was rated significantly higher than that of employees in the no-voice group, providing support for Hypothesis 1a. The analysis revealed no support for Hypothesis 2a, that supervisors’ positive IFTs moderate the effect of promotive voice, as the data showed no statistically significant interaction (F[1,114] = 2.669; p = 0.105, part. η2 = 0.024).

Results of three-way ANOVA for promotive voice.

Dependent variable: supervisor’s performance rating; IFT: implicit followership theories.

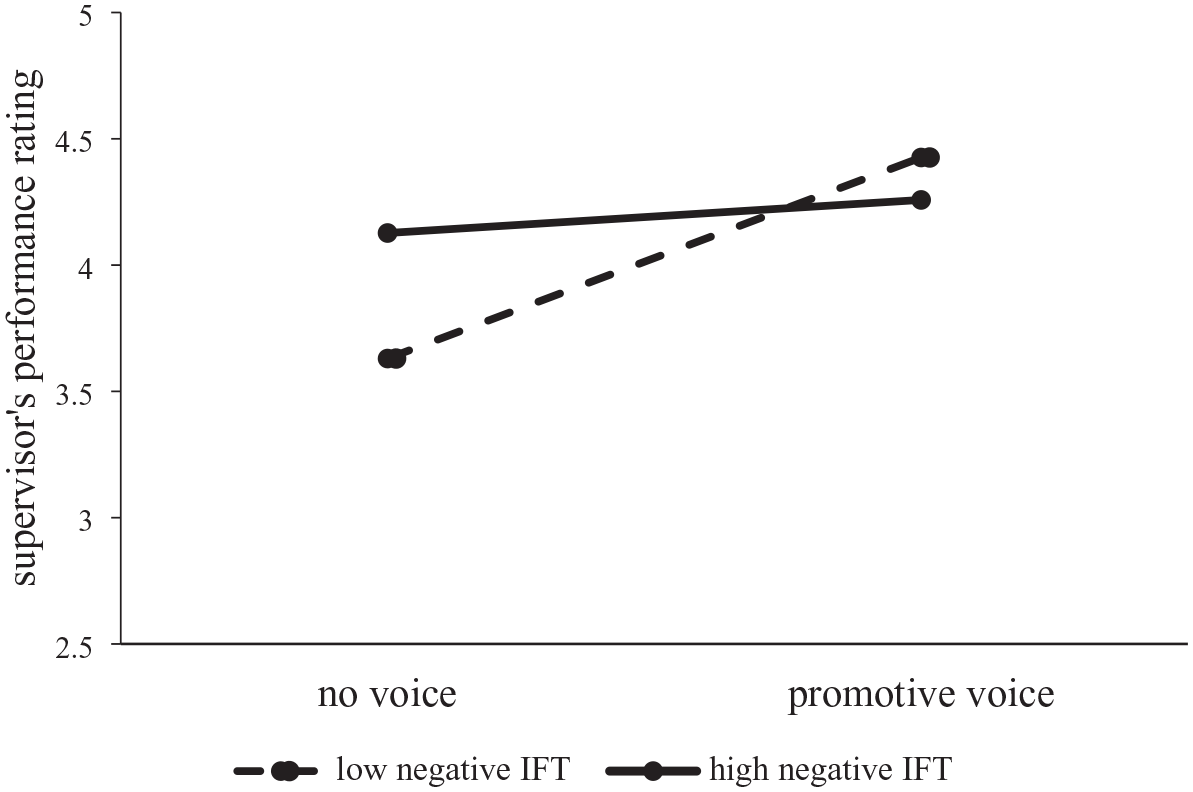

A significant interaction between supervisors’ negative IFTs and promotive voice (F[1,114] = 2885; p = 0.035, part. η2 = 0.041) showed that negative IFTs strengthen the positive relationship between promotive voice and the supervisors’ performance ratings. Because this effect is not how it was hypothesized, Hypothesis 3a is rejected. Figure 3 shows this interaction effect. Employees who engage in promotive voice receive a better performance rating by their supervisor if the supervisors have negative assumptions of followers’ traits and behaviors. This effect is stronger for low negative IFTs than for high negative IFTs.

Moderation effect of supervisors’ negative IFTs on the relationship between promotive voice and the supervisors’ performance ratings.

The second analysis (Table 4) revealed a significant main effect of prohibitive voice on supervisors’ performance ratings (F[1,130] = 23.266; p ⩽ 0.000, part. η2 = 0.159). That is, the performance of employees who engaged in prohibitive voice was rated higher than that of the no-voice group. As we hypothesized a negative effect of prohibitive voice on performance rating, Hypotheses 1a is rejected. Hypothesis 2b and 3b, that supervisors’ IFTs moderate the effect of prohibitive voice, are not supported, as the analysis revealed no statistically significant interactions for positive (F[1,130] = 1.323; p = 0.252, part. η2 = 0.011) and negative IFTs (F[1,130] = 3.483; p = 0.064; part. η2 = 0.028).

Results of three-way ANOVA for prohibitive voice.

Dependent variable: supervisor’s performance rating; IFT: implicit followership theories.

Discussion

Individual outcomes of employee voice have received considerable research attention in the last decade. Studies’ findings of different causal relationships (Chamberlin et al., 2017; Morrison, 2023) indicated that various contingency factors can affect the relationship between employee voice and supervisors’ performance ratings. As a result, Morrison (2023) calls for analyses of moderation effects to clarify this relationship. The present study addresses this call by investigating IFTs’ influence on the relationship between employee voice and performance ratings. Specifically, this study analyzes the moderating effect of positive and negative IFTs on the relationship of employees’ promotive voice and prohibitive voice with supervisor’s performance ratings.

The results of the scenario-based study show that employee voice might affect supervisors’ performance ratings, but that the effects differ depending on the voice form. Further, the study reveals that this relationship might be influenced by negative implicit assumptions that supervisors have about followers.

More specifically, according to the hypotheses, the results indicate that supervisors’ performance ratings of employees are higher when employees showed voice than when they did not, regardless of whether the voice was promotive or prohibitive. These findings are surprising, because the theoretical assumptions only predicted the positive relationship between promotive voice and supervisor’s performance rating, but the positive effect of prohibitive voice is unexpected. A possible explanation, why prohibitive voice may have a positive influence on performance rating might be that the underlying assumptions about the nature of promotive and prohibitive voice are inadequate. According to Liang et al. (2012), supervisors interpret prohibitive voice as negative, as it points out failures that have been made. Thereby, supervisors may feel that their self-esteem is being attacked by this kind of behavior.

However, the nature of promotive and prohibitive voice might be more complex than research suggests, as the supervisor’s evaluation of employee voice can be influenced by factors other than whether the voice is perceived as positive or negative. For example, Brykman and Raver (2021) showed that voice quality and the frequency with which employees use voice affect the evaluation of employees’ voice behavior. In addition, Park et al. (2022) found that managers reward voice behavior more when they perceive it as a proactive behavior, not something they have to solicit. Therefore, promotive and prohibitive voice may not be either positive or negative per se but may depend on the attributions supervisors ascribe to it. Further, even when supervisors feel threatened by employee voice, they might be able to capture the positive thought behind the behavior, depending on the supervisor’s individual disposition (e.g. self-esteem, individual resilience) and his or her ability to deal with challenge and criticism (Ilies et al., 2007).

Another reason for the relationship found might be related to the study’s organizational context, which was accounting firms in Germany. Legal regulations require auditors to report certain errors and grievances that might be harmful to the community (Wirtschaftsprüferkammer, 2018, 2016a, 2016b), so an employee’s prohibitive voice might be seen as an in-role behavior, not as an extra-role behavior. If supervisors expect employees to speak up about errors and grievances, they are likely to interpret this behavior as positive, leading to a better evaluation of prohibitive voice. This suggestion is in line with Nelson and Proell (2018), who identified auditing and healthcare as organizational contexts in which legal regulations shape supervisors’ expectations regarding employees’ use of voice.

The results of the study also indicate that implicit assumptions about followers might moderate the relationship between employee voice and supervisors’ performance ratings. Whereas the analysis found no significant effect of positive IFTs, the effect of negative IFTs on the relationship between promotive voice and supervisors’ performance ratings is contrary to the hypotheses. These findings raise the question concerning how to explain these effects. Based on future research, I stated that IFTs serve as a sensemaking function in efforts to understand followers’ behavior, so they shape supervisors’ expectations of their employees and their performance (Whiteley et al., 2012). Research on performance evaluation showed that observations can be influenced by evaluation errors and (un)conscious biases like the halo effect, leniency and severity errors (DeNisi and Murphy, 2017).

The Pygmalion effect is one of these biases and describes how positive performance expectations can improve employees’ performance (Eden, 1992; Veestraeten et al., 2021; Whiteley et al., 2012). According to the theoretical assumptions behind the Pygmalion effect, employees who engage in promotive voice and/or prohibitive voice may be fulfilling their supervisors’ performance expectations because they show a positive behavior that is expected by supervisors as it is an important in-role behavior of their work. Thus, supervisors might see their positive expectations confirmed by their employees’ voice behavior, so supervisors’ positive IFTs might not alter these effects. Given that IFTs are categorizations that are automatically activated but do not have to be (Sy, 2010), it is plausible that directly perceived performance indicators like employee voice may be weighted more heavily in the moment of judgment. As a result, positive IFTs may have no effect in a single decision situation since promotive and prohibitive voice both are already interpreted as positive.

A possible explanation for the unexpected moderation effect of negative IFTs on the relationship between promotive voice and supervisors’ performance ratings may be (un)conscious bias. Judgments and expectations of others often depend on prejudices that are based on stereotypes or categorizations (DeNisi and Murphy, 2017). However, supervisors who have negative expectations of employees’ performance may be pleasantly surprised when these negative expectations do not come to pass, so they might rate the performance higher than they would have had the expectation been positive.

The effect of negative IFTs may also be explained by the difference between a fixed mindset and a growth mindset. Research on implicit theories states that people who have fixed mindsets believe that people’s characteristics and abilities cannot change over time, whereas those who have growth mindsets assume that these traits can develop and change with time and effort (Dweck, 2006; Kouzes and Posner, 2019; Yeager and Dweck, 2012). People who have growth mindsets tend to motivate and support others to improve performance by, for example, recognizing positive behavior and rewarding it using performance ratings. Thus, supervisors who have growth mindsets may see their employees’ potential when they show voice and want to encourage this behavior by giving them positive performance ratings. Nevertheless, that potential is perceived to be greater when the negative assumptions are not too strong. In this way, supervisors’ growth mindsets might explain why the moderating effect of low negative IFTs is much stronger than for high negative IFTs on the relationship between promotive voice and performance ratings.

Practical implications

The fear of negative consequences is one of the most common reasons why employees don’t speak up about suggestions or failures in the workplace. But the results of this study indicate that the communication of suggestions and failures both might have positive effects on employees’ performance ratings even if supervisors have some negative assumptions about followers. These findings have practical implications for employees and organizations.

For employees, the results encourage them to speak up more often as employee voice not only helps the organization improve its processes but also increases the perception of one’s own performance by others. By speaking up employees demonstrate their professional competencies and that they care about the well-being of the organization. This might lead to positive performance ratings by supervisors. A positive performance rating can then lead to better career opportunities regarding promotions or salary increases.

For organizations, it is important to encourage employees to speak up because of the beneficial organizational-level impacts of employee voice. Therefore, organizations have to create an environment that fosters employees to speak up even if they are afraid of doing so by training leaders about communication and conflict skills. To avoid (un)conscious biases in performance ratings it might be helpful to sensitize supervisors about the impact of implicit assumptions on employees’ evaluations. In addition, the use of 360° feedback might help to reduce those (un)conscious biases through one appraiser.

Limitations and future research

This study has several limitations. First, the external validity of the study is limited because of the study’s design (Aguinis and Bradley, 2014; Trevino, 1992). Research on employee voice frequently uses scenario-based designs (Morrison, 2023), but the scenarios are fictitious and are realistic to only a limited extent. As previous research illustrates, numerous factors affect performance ratings. Therefore, other factors than employee voice should be considered when analyzing supervisors’ evaluations of employees’ performance (DeNisi and Murphy, 2017). However, I reduced the problem regarding the scenarios’ realism by developing and pretesting the scenarios with experts from auditing companies.

Second, individual behavior is shaped by the organizational context (Johns, 2006), which can affect voice behavior. Because this study was conducted in auditing companies in Germany, the results are transferable to other organizations to only a limited extent. Generalizability of the findings is possible if the organizations’ contextual factors are similar to those of auditing firms, which could be the case in other professional service firms. In addition, the legal framework for auditors’ activities in Germany may differ from that in other countries. Future research could validate this study’s results by replicating the study in other organizational and cultural contexts.

Third, we relied on Sy’s (2010) widely used scale to measure IFTs (Lord et al., 2020). Although the scale had good Cronbach’s alpha values, the factor analysis showed lower factor loadings for the items “excited” and “soft-spoken,” perhaps because the translation changed the terms’ meaning. Future research on IFTs in German-speaking countries should take this possible translation problem into account. Validation of a scale on IFTs in German-speaking countries would also be useful, as different cultures may have different assumptions about followers. Further, the 10-point scale of IFTs might be a limitation. One of the main problems is that this scale is very broad, which can make it difficult for respondents to give an accurate assessment. According to Dawes (2008), a change of the scale with no differences in the results is possible by a rescaling and arithmetic adjustment. Nevertheless, changing a validated scale can also lead to various problems for example, the use of midpoint on 5- and 7-point scales (Chyung et al., 2017).

The results of this study provide avenues for future research. Overall, the findings call for a more fine-grained analyses of the supervisor as a recipient of voice. In line with other studies, this study shows that prohibitive voice is not negative per se (Huang et al., 2018; Nelson and Proell, 2018). It would be interesting to explore when supervisors perceive voice as positive and when they perceive it as negative. Future research should take supervisors’ perceptions about the voice expressed (e.g. motives, practicability) into account as mediators.

As highlighted in the discussion and limitations, the perception of prohibitive voice in accounting firms might differ significantly from other contexts, suggesting that future research could benefit from exploring the organizational context of these firms through a multi-method approach. Especially, qualitative studies could provide a deeper understanding of the underlying motivations and behaviors that influence how prohibitive voice is perceived and acted upon. By analyzing this, a qualitative study could shed light on the question under which context-related factors prohibitive voice is perceived as constructive and under which of these it is perceived as destructive.

Further, even though this study did not confirm the application of the self-affirmation theory, it could advance research to investigate such dispositions as self-esteem, self-threat, coping and critical thinking abilities as moderation variables in future analyses. In addition, knowledge about the role of implicit theories in the relationship between employee voice and performance ratings remains incomplete. In addition to implicit assumptions about followers, the literature discusses other constructs of implicit theories, such as implicit theories of personality, communication, or voice. As Knoll et al. (2021) point out, implicit voice theories about when to speak up in organizations shape employees’ perceptions of the organizational climate. Whereas research might use IFTs across organizations, implicit voice theories are more specific to the organization. Nevertheless, analyses of implicit voice theories’ influence on individual outcomes are sparse. Examining their interplay can advance research by considering whether the mindsets behind implicit theories are fixed or growth mindsets and how this difference affects the relationship between employee voice and individual outcomes.

Conclusion

Negative individual consequences are reasons why employees do not speak up to their supervisors. In this regard, research has shown that employee voice might have positive and negative effects on supervisors’ performance ratings depending on contextual factors. This study examined how employees’ promotive and prohibitive voice influence supervisors’ performance ratings in a sample of professional accountants. The aim was to determine whether and how supervisors’ implicit assumptions of followers moderate this relationship. The results of the scenario-based study showed that both promotive and prohibitive voice have a positive influence on supervisors’ performance ratings and that this relationship is influenced by supervisors’ implicit assumptions of followers. More specifically, the effect of promotive and prohibitive voice on supervisors’ performance rating was moderated by supervisors’ negative IFTs, while the moderation effect of supervisors’ positive IFTs were not significant. The analysis revealed that promotive and prohibitive voice are not per se either positive or negative and that implicit assumptions influence supervisors’ judgments on employee voice. This calls for more fine-grained analyses regarding the boundary conditions of employee voice and supervisors’ performance ratings.