Abstract

Indonesia’s aging population remains active in the workforce, especially older women in rural areas. The aim of this study is to investigate the working conditions, financial constraints, and adaptive strategies of older women entrepreneurs in Purworejo District, Central Java, Indonesia. Using a mixed-methods approach, the authors conducted surveys (n = 100) and qualitative in-depth interviews followed by focus group discussion (n = 21). Quantitative data were analyzed using descriptive and bivariate analysis, while qualitative findings were thematically analyzed. The findings show that most older women work out of financial necessity, choosing businesses according to familiarity and access rather than strategy. Many experiences long working hours, unsafe environments, and lack of health insurance or savings. These results highlight vulnerabilities shaped by age, gender, and work conditions, emphasizing the need for inclusive policies that expand financial access, improve social protection, and promote age-friendly infrastructure to support older women’s livelihoods.

Keywords

In Indonesia, the proportion of those 60 and older steadily increased from 3.2 percent in 1950 to 10.5 percent in 2020 and is projected to reach 21.9 percent by 2050 (Badan Pusat Statistik 2022; UN DESA 2022). More than half (52.55 percent) of older adults in Indonesia remain economically active, particularly in rural areas, where 62.02 percent continue to work (Badan Pusat Statistik 2022). Yet older adults are motivated to keep working because of the lack of nonlabor income, such as pensions (Jamalludin 2020). Moreover, employment offers significant health benefits, providing purpose, status, and financial security (Waddell and Burton 2006). Evidence suggests that withdrawal from the workforce among older adults is correlated with adverse health outcomes, including lower self-rated health, mental well-being, chronic illnesses, and increased sickness absence rates (Nazar et al. 2025).

In 2022, 51.81 percent of Indonesia’s older population were women (Badan Pusat Statistik 2022). Women are more likely than men to experience low job security and less job flexibility (Wang et al. 2025). In Indonesia, only 13.81 percent are working in formal sectors, with a noticeable gender disparity (9.78 percent of older women compared with 16.37 percent of older men) (Badan Pusat Statistik 2022). Economic pressures often push older women, especially in rural areas, into informal self-employment (Badan Pusat Statistik 2022). Accessing financial resources is a major barrier for women-led businesses (Wellalage and Thrikawala 2021). Older rural women also face “decent work deficits,” including unstable jobs, poor working conditions, and limited support (Badan Pusat Statistik 2022). Despite these challenges, older women play a crucial role in supporting their families and communities through paid and unpaid work, contributing to household stability and social cohesion (Seedat and Rondon 2021). Given the disproportionate economic vulnerabilities faced by older women especially in rural Indonesia, this study focuses specifically on their experiences. Centering older women allows a deeper understanding of how gender, aging, and informal work intersect. This focus also enables a more grounded exploration of what constitutes decent work for older rural women, beyond formal employment. From a sociological perspective, decent work is not just about employment status, but includes access to dignity, autonomy, voice, safety, and economic security (Blustein, Lysova, and Duffy 2023)

Despite the Sustainable Development Goals’ emphasis on promoting decent work and gender equality (goals 8 and 5), older women entrepreneurs remain largely invisible in development policy (Chigbu and Nekhwevha 2023). The existing literature about older women, especially in rural areas, generally focuses only on their roles in caregiving, health challenges, and social participation (Absor et al. 2024; Desch et al. 2025; Kurniawan et al. 2024). Research on the specific challenges older women face remains limited, especially in Indonesia, where men and women often have different responsibilities and demands outside of work (Messing 1997). In rural Indonesia, women are also often responsible for managing household resources, food security, and transmitting cultural values across generations (Gunter and van der Hoeven 2004; Najmudin, Maisaroh, and Yuliana 2022).

In this study, entrepreneurs refer to older women engaged in informal self-employment, such as trading or home-based services, without formal business registration (Chen 2007; ILO 2020). This form of entrepreneurship often emerges as a survival strategy among older rural women with limited access to pensions and formal employment (Priebe, Howell, and Nguyen 2019). Unlike agricultural or wage labor, informal entrepreneurship allows more control over time and work type, which is crucial for women balancing economic roles with unpaid caregiving responsibilities (Blustein et al. 2023; Seedat and Rondon 2021). However, it remains precarious, with minimal access to credit, markets, and social protection (Blustein et al. 2023).

This study aims to explore the working conditions of older women entrepreneurs in rural Indonesia, as well as the factors that influence their work-life balance, income, and ability to adapt to external challenges. We address the following research questions:

What are the working conditions of older women entrepreneurs in rural Indonesia?

How do factors such as education, family support, health, and financial access affect older women’s working conditions and economic outcomes?

What challenges do older women face in operating their businesses?

By filling the research gap related to decent work among older women entrepreneurs in rural Indonesia, the results of this study are expected to inform policies and programs that promote inclusive, age and gender sensitive support systems. These findings may also contribute to broader discussions on aging, gender equity, and rural economic development, especially in developing countries.

Literature Review

Reasons for Working and Business Selection

Older women’s motivations to work and their choice of business are shaped by a mix of necessity, capacity, and context. In many parts of the Global South, including Indonesia, the absence of a robust pension system, combined with limited formal employment opportunities in later life, means that self-employment or informal business becomes one of the few viable options (Alfers and Sevilla 2022; Suriastini, Wijayanti, and Oktarina 2024). In this study, business and entrepreneurship refer primarily to small-scale, home-based economic activities rather than formal enterprises. Most older women in rural areas operate moderate ventures such as selling snacks or vegetables from home, running small kiosks, making traditional food for sale, or vending along roadsides (Arsal et al. 2017; Kansil et al. 2019). For these women, the decision to start a business is often not driven by ambition or opportunity but by the need to survive, contribute to the household, or remain socially engaged (Römer-Paakkanen and Takanen-Körperich 2022).

Previous research notes that many older women entrepreneurs enter sectors that are considered low barrier, such as home-based food production, small-scale trade, or services like tailoring and childcare, which often draw on skills acquired earlier in life and require minimal capital investment (Vuciterna et al. 2024). Personal enjoyment and preference for less physically demanding work are also reported as reasons for business choice (Schmitz et al. 2023). However, it is important to recognize that such choices are often constrained by gender norms and life-course inequalities, rather than being entirely voluntary or empowering (Yunis, Hashim, and Anderson 2018). Intersecting factors such as education, physical health, and caregiving responsibilities further narrow the employment options available to older women (Romeu Gordo, Stypińska, and Franke 2022). Women with limited education tend to be channeled into informal work that lacks protections and offers low and unstable income (Nguyen, Shami, and Li 2025). This reflects how gender and ageing shape access to decent work, especially in marginal contexts in which formal job opportunities are scarce and retirement is a privilege few can afford.

Financial Decision Making and Constraints

Financial decisions are deeply influenced by household dynamics. Although some women have financial autonomy, many still consult or depend on spouses, children, or other household members in making decisions about business investments or income use (Wagner and Walstad 2023). Intergenerational dependencies, such as children offering financial support or expecting older women to contribute to household needs can complicate budgeting and savings. Thus, women may prioritize their grandchildren’s education or household expenses over business reinvestment or personal retirement planning (Lusardi, Schneider, and Tufano 2011).

Age and gender bias in financial institutions exacerbate these constraints. Older women are often perceived as high-risk borrowers and are less likely to be targeted by formal financial products, such as loans or insurance schemes (Fang 2023). Moreover, digital financial tools that can increase access to mobile banking or online marketplace remain underused because of lack of familiarity, limited digital literacy, and infrastructure gaps in rural areas (Hasan et al. 2023; Mishra et al. 2024). These barriers place older rural women in a structurally disadvantaged position, reinforcing a cycle of low investment, precarious income, and poor business resilience (Widyastuti, Respati, and Mahfirah 2024).

Challenges to Safe, Fair, and Sustainable Business

Older women entrepreneurs in rural settings often operate in informal and underregulated environments, which create multiple challenges to ensuring that their businesses are safe, equitable, and sustainable. These women frequently work without contracts, occupational safety standards, or formal protection against unfair treatment, wage theft, or business exploitation (Rahman et al. 2023). Because their businesses are typically home-based or mobile, enforcement of labor standards is nearly nonexistent, and any workplace hazards such as long hours and physical strain still less addressed (Ghouse et al. 2017).

Many older women are responsible not only for their businesses but also extensive care work within the household, including looking after grandchildren or sick family members (Carr et al. 2018). These dual burdens can make it difficult to maintain regular business hours, manage customers, or seek support (Khan et al. 2021). The fatigue and stress from managing both domestic and income-generating roles can further endanger their health and well-being, especially in the absence of adequate health care options (Chen, Fan, and Chu 2020).

Adoption of digital tools for customer order and delivery services caused by the coronavirus disease 2019 (COVID-19) pandemic remained out of reach for many older women, especially those with low literacy or little prior exposure to digital platforms (Chan, Burton, and Flower 2024). In addition, environmental and infrastructural constraints, such as inadequate transport networks, unstable electricity, poor market access, and lack of formal storage or production facilities add to the logistical difficulties of running a rural business (Aliamutu and Mkhize 2024) Most older women entrepreneurs also lack access to institutional support, such as business development services, legal aid, or community cooperatives, which could enhance sustainability and fair competition (Gimenez-Jimenez, Calabrò, and Urbano 2020).

Limited Access to Social Security

Access to social security, including health insurance, retirement savings, and income support, is a core component of the ILO’s (2023) decent work framework. However, older women entrepreneurs in rural Indonesia remain largely excluded from such systems (Laksono et al. 2022). Many of them work informally, which disqualifies them from employer-based social protection or formal pension schemes (Muliati 2014).

Previous studies show that women in informal work are less likely to contribute to retirement schemes, especially in rural settings where income is irregular and where awareness of available programs is often low (OECD 2025). In Indonesia, the national health insurance program (BPJS) has expanded coverage, yet enrollment gaps persist, especially among rural people (Sukartini et al. 2022). Affordability concerns, lack of understanding about benefits, and a perception that insurance is unnecessary often deter participation (Roza and Sari 2025). Household composition further complicates the issue, where living with multiple family members may deprioritize their own insurance and saving needs, allocating household resources to dependents instead (Ozawa, Grewal, and Bridges 2016).

Existing studies on older women, particularly in rural Indonesia, have largely emphasized their caregiving roles, health challenges, and social participation, while their economic activities and working conditions remain underexplored. Research rarely considers how older women sustain small-scale businesses, manage financial and social constraints, or adapt to changing conditions in later life. This study addresses that gap by examining the working conditions and challenges of older women entrepreneurs in rural Indonesia through the lens of decent work.

Method

Research Design

We used a mixed-methods design to explore the quality of work among older women entrepreneurs in rural areas, focusing on nonagricultural and nonfishery informal business sectors to capture the diversity of business types and challenges. Informal entrepreneurial work represents a distinct set of working conditions and vulnerabilities, such as access to capital, legal recognition, and exposure to market changes, such as digitalization, which differ from those in agriculture or fisheries. Entrepreneurial work also offers more individualized autonomy, but with less protection or support.

The quantitative component utilized surveys to gather data on demographic characteristics, educational background, and business-related factors (business sectors and location) that influence decent work. The qualitative component included in-depth interviews and focus group discussions (FGDs), aimed at exploring individual experiences, challenges, and perceptions regarding work conditions and economic empowerment. FGDs provided an opportunity for participants to discuss shared themes and collectively reflect on their experiences.

Data Collection

The research was conducted in Purworejo District, Central Java, Indonesia, selected purposively for its large proportion of older women. Two subdistricts, Banyuurip and Kutoarjo, were chosen because both are neither coastal nor mountainous areas. Twelve villages were randomly selected within these areas. Before the main data collection, a pilot test was conducted to assess the clarity, relevance, and appropriateness of both quantitative questionnaire and qualitative interview guides. The instruments were reviewed and refined in collaboration with partner organizations specializing in ageing and community-based research, including SurveyMETER, Yayasan Emong Lansia, and HelpAge International, which served as technical reviewers for this study. The experts evaluated the instruments for content validity, cultural relevance, and alignment with the study’s objectives. Revisions were made to ensure that the instruments were understandable and contextually appropriate for older women entrepreneurs in rural settings.

A total of 121 participants were included: 100 for the quantitative survey and 21 for the qualitative component (10 for in-depth interviews and 11 for FGDs). For the survey, participants were selected using simple random sampling from a list of older women (60 years or older) entrepreneurs provided by village officers. Because of the lack of formal records, a listing process was conducted with the help of multiple village officials, who acted as reliable informants on the basis of their knowledge of the local community. Their collective input enabled a more comprehensive identification of older women entrepreneurs. The resulting list was then verified, particularly for age eligibility. Random sampling from this verified list was used for both the quantitative and qualitative components to improve representativeness across sectors. Although nonprobability sampling is often used in qualitative research to explore specific types of experiences, this list was the most practical and accessible way to identify the eligible participants in our setting. The study was approved by an ethics committee and participants confidentiality was ensured by assigning pseudonyms.

The interviews were conducted by two members of the research team, both of whom have prior experience in qualitative data collection. Conducted in Indonesian, each in-depth interview lasted about 40 minutes and was generally well received. The data collection process proceeded smoothly, with participants engaging openly and no indications that the researchers’ presence affected their responses. However, we acknowledge the potential role of factors such as age and generational differences, the interviewers’ outsider status, and cultural norms related to modesty, respect, and self-presentation. These factors may have influenced how some women articulated their experiences, for example, by downplaying hardship, avoiding criticism of family members, or emphasizing resilience. During the analysis process, we engaged in regular team discussions and discussed themes from the qualitative research in the light of quantitative findings to better situate the women’s stories within their cultural and relational contexts.

Data Analysis

Quantitative data were analyzed using Stata MP software version 17.0 (StataCorp LP, College Station, TX). The main outcome variables reflected key aspects of decent work. Work conditions were assessed on the basis of work environment, working hour, income, and access to social protection. Safe work environment included six indicators: risk for accidents (assessed by walking distance, use of protective gear while riding a motorcycle or bicycle, and comfort of public transportation; categorized as high risk or low risk), road condition (not safe/uncomfortable or safe/comfortable), business location condition (including nearby conditions, floor quality, air circulation, exposure to heat and rain, and lighting; categorized as unhealthy or healthy), risk for respiratory problems from exposure to hazards such as firewood stoves (high risk or low risk), presence of physically burdensome activities over a long period (yes or no), and use of personal protective equipment during business activities (no or yes). Working time was measured using two indicators: total weekly working hours (>40 hours or ≤40 hours) and staying up past 22:00 or waking before 04:00 (yes or no). Income was measured as monthly net income, with respondents earning up to IDR 1,500,000 and those earning more than IDR 1,500,000. Last, social protection was assessed according to health insurance ownership (no or yes), ownership of savings for retirement (no or yes), and receive government assistance (no or yes). Business type was classified into home-industry sectors, trading, and service sectors, while workplace location distinguished between home-based and outside-home settings. Descriptive statistics were used to summarize the characteristics of the participants. Bivariate analysis was conducted using χ2 and Fisher exact tests to examine the association between demographic, educational, and business-related factors and different aspects of decent work. Results are presented as percentages and significance levels (p values) to reflect group differences rather than adjusted effect sizes. Qualitative data were transcribed and analyzed thematically, providing deeper insights into the personal experiences and challenges faced by older women entrepreneurs. These findings helped contextualize the quantitative results and offer a more nuanced understanding of the factors influencing decent work among the study participants.

Results

Quantitative Findings

Respondent and Business Profile

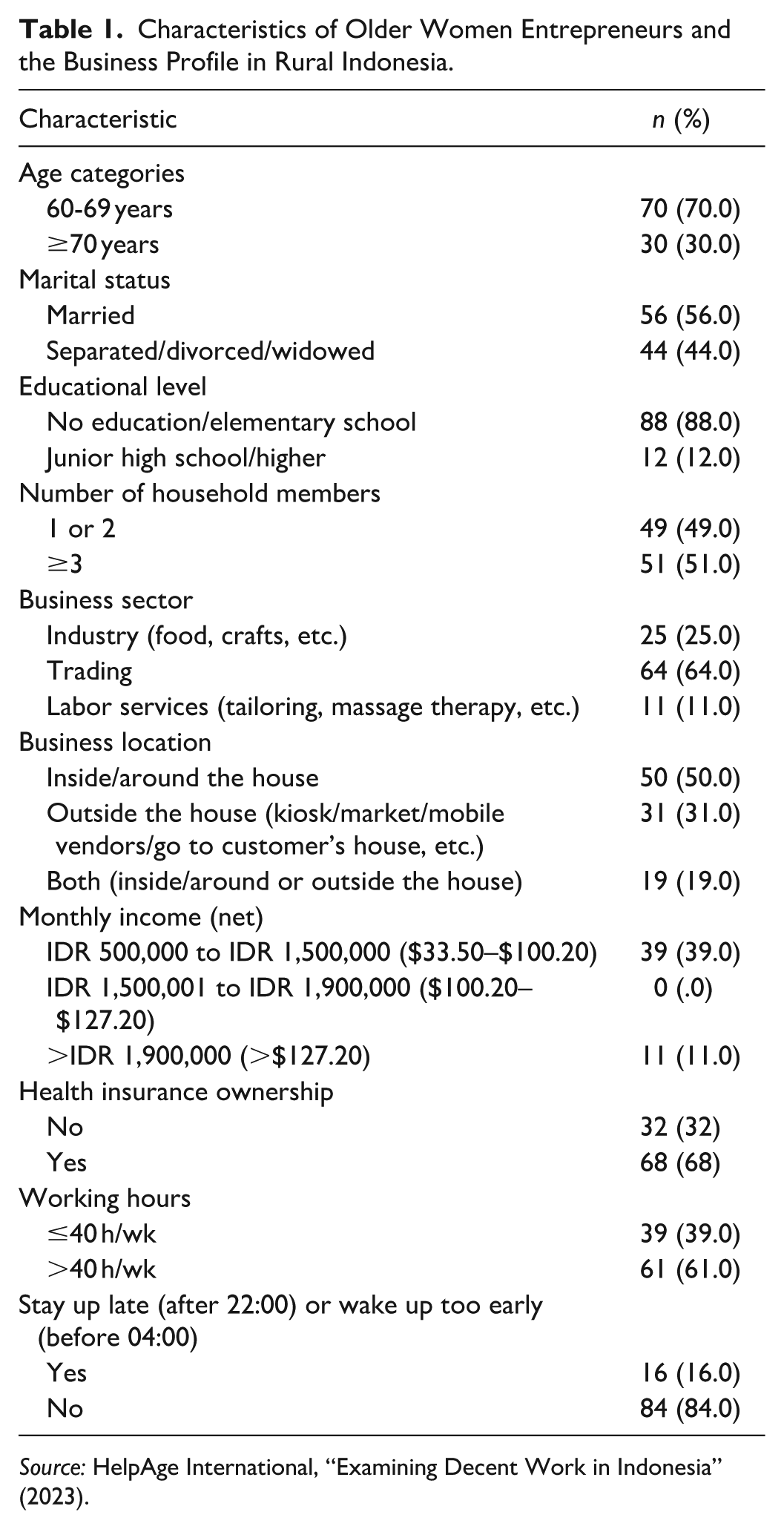

The well-being of older women entrepreneurs is influenced by age, education, living arrangements, and caregiving roles. Table 1 indicates that most respondents are in the young-old group (60–69 years of age), and nearly half are still married. A large portion has either no education or has only finished elementary school. More than half of older women entrepreneurs in rural Indonesia worked in trading sectors, followed by small-scale industry sectors (food, tofu, tempeh, or batik makers), had a grocery store, or worked as retail traders, especially selling vegetables, fruits, or meats. These businesses were typically operated at or around the house. However, despite working long hours (>40 hours per week) and lacking help, most of them had low incomes. These findings reflect how older women in rural Indonesia tend to choose work that suits their ability, but often face low income. Moreover, there are still about 32 percent of older women who do not have any health insurance. These profiles highlight that older women in rural Indonesia tend to engage in small-scale, home-based businesses, often with low incomes, limited education, and partial access to health insurance, which should be considered in policy design.

Characteristics of Older Women Entrepreneurs and the Business Profile in Rural Indonesia.

Source: HelpAge International, “Examining Decent Work in Indonesia” (2023).

Reasons for Working and Business Selection

Understanding motivation and business preference is crucial to support sustainable income for older women. Figure 1 shows that the majority of older women entrepreneurs in rural Indonesia continue working to remain financially independent, while more than half of them do so to stay occupied and most chose their current businesses because they have the relevant skills, because they enjoy the work, and because it is less physically burdensome.

Motivations for continuing working, in percentages (A), and job selection reasons, in percentages (B).

Financial Decision Making and Constraints

Access to financial resources is an important determinant for entrepreneurship sustainability. Figure 2 shows that to start their businesses, more than half of older women used their savings, with very few of them borrowing money from banks. About 80 percent had no loans during business operation, and those who did relied primarily on informal sources, such as arisan (a traditional financing and social activity in Indonesia or sometimes called a “saving club”).

Business capital, in percentages (A), and source of the loan, in percentages (B).

Challenges to Safe, Fair, and Sustainable Business

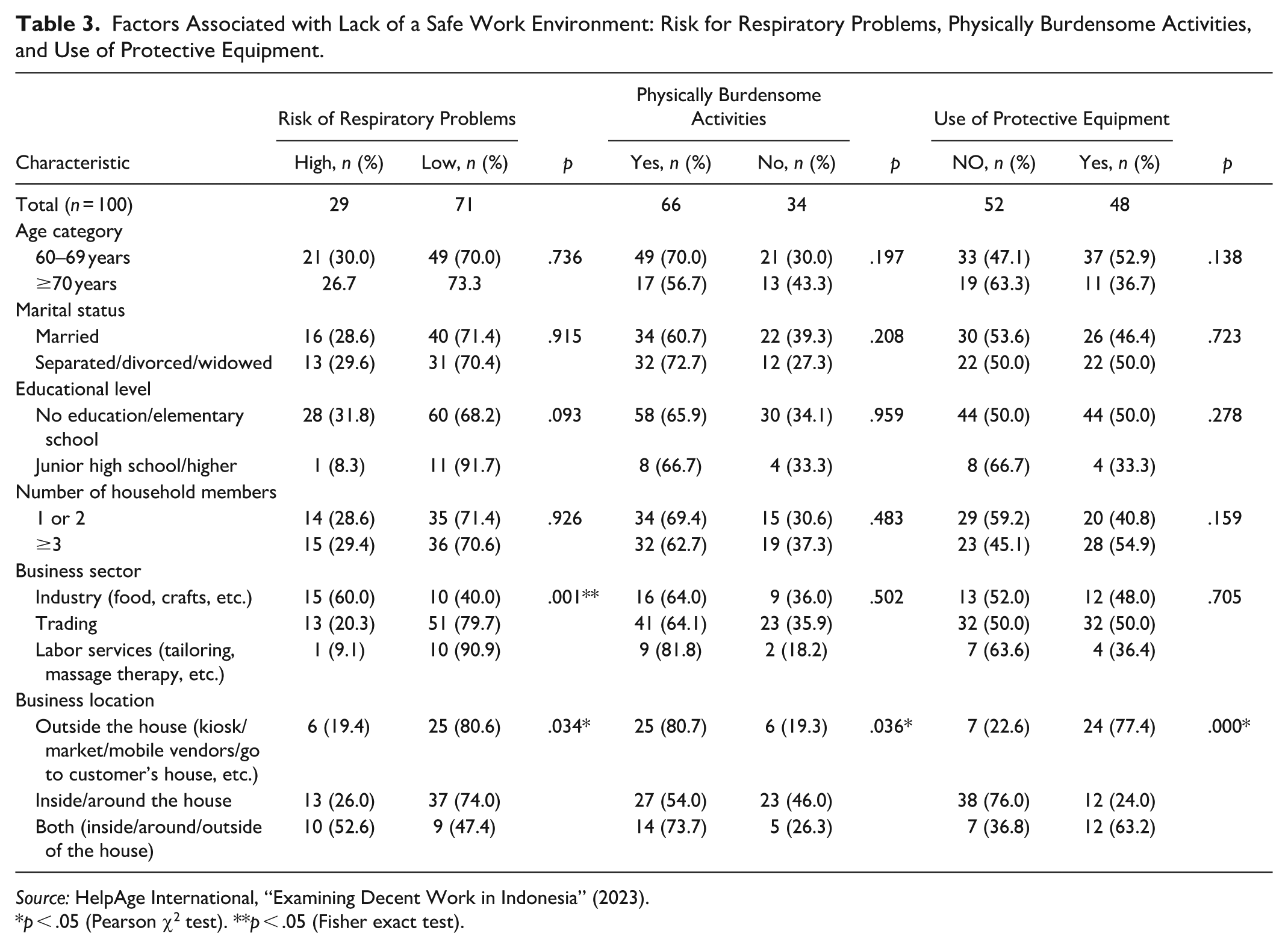

Safety and a healthy environment are components of decent work, which are particularly critical for aging workers. Tables 2 and 3 show several structural and situational challenges that shape older women entrepreneurs’ ability to operate safe, fair, and sustainable businesses. The study demonstrated that the number of household members was significantly associated with both the choice of road for the business (p = .039) and the condition of the business location (p = .009). The proportion of working women in smaller households (one or two household members) facing unsafe road conditions and unhealthy business environments were reported higher than those in larger households (three or more household members), suggesting that limited household support may constrain their ability to secure safer workspaces. There is also an association between business sectors and the risk for respiratory problems (p = .001). Older women in industry sectors were more likely to report risk for respiratory problems compared with those in trading or service sectors. Furthermore, business location was also reported to be associated with older women’s risk for respiratory problems (p = .034), physically burdensome activities (p = .036), and the use of protective equipment (p < .001). Those working inside the house were more likely to report risk for respiratory problem, doing physically burdensome activities, and not using the protective equipment than those working outside or both.

Factors Associated with Lack of a Safe Work Environment: Risk for Accident, Road Condition, and Business Location Condition.

Source: HelpAge International, “Examining Decent Work in Indonesia” (2023).

p < .05 (Pearson χ2 test).

Factors Associated with Lack of a Safe Work Environment: Risk for Respiratory Problems, Physically Burdensome Activities, and Use of Protective Equipment.

Source: HelpAge International, “Examining Decent Work in Indonesia” (2023).

p < .05 (Pearson χ2 test). **p < .05 (Fisher exact test).

Table 4 further shows that several factors were associated with excessive working hours (>40 h/wk), irregular sleep patterns, and low income (≤IDR 1,500,000). Business sectors were associated with working hours (p = .014), where proportion of those working in trading sectors were reported to be higher than the other sectors. A higher proportion of those aged 60 to 69 years were also reported to stay up late or wake up too early (p = .034), which may potentially increase fatigue-related risks. Furthermore, educational level and number of household members were associated with monthly net income. More older women with lower education were reported to have low monthly net income than the ones with junior high school/ higher education (p = .003), while those in smaller households (one or two household members) were also reported to have lower monthly net income than their counterparts (p = .030).

Excessive Working Hours and Low Income.

Source: HelpAge International, “Examining Decent Work in Indonesia” (2023).

p < .05 (Pearson χ2 test). **p < .05 (Fisher exact test).

Limited Access to Social Security

Health insurance coverage is essential for older people who are still working, especially to sustain their livelihood and manage health risks. However, its coverage among this group remains inconsistent, reflecting both structural challenges and individual preferences. Table 5 reveals that health insurance ownership was associated with age and household size. The proportion of older women with health insurance is reported to be higher among those 70 years and older than younger women (p = .031). Women living with fewer household members also showed higher insurance coverage compared with those in larger household (p = .045). Ownership of retirement savings was related to business sectors (p = .043), with those in industry sectors reported to be more likely to have retirements savings than those in other sectors.

Factors Associated with Lack of Access of Social Protection.

Source: HelpAge International, “Examining Decent Work in Indonesia” (2023).

p < .05 (Pearson χ2 test). **p < 0.05 (Fisher exact test).

The results of our survey show that most older women keep working because they need the income and often choose familiar and accessible businesses. Women in smaller households were more likely to face unsafe or unhealthy work environments and earn lower incomes, possibly because they have less help at home. Work type and location also mattered, where women in industry were more likely to report breathing problems, and those working from home often faced more physical strain, respiratory risks, and went without protective equipment. Trading work tended to involve longer hours, while age, education, and household size shaped income levels, work patterns, and access to insurance. Retirement savings were more common among women in industry.

Qualitative Findings

Reasons for Working and Business Selection

The quantitative findings indicated that older women in rural Indonesia primarily work to support household needs. This aligns with the qualitative findings, which further explain that these women often continue working to contribute financially to their family and to fulfill social obligations, such as helping community celebrations. Older women who are widowed, separated, or divorced, rely on their business income to meet daily needs. Additionally, the interviews revealed that continuing to work helps older women stay active, both physically and socially, as one participant shared:

I keep working to help husband fulfill our daily needs. Moreover, because we live in rural areas, we also have to give a donation for neighbors who hold a celebration. It will help them to buy their needs. Working will also make me happy. I’m happy doing trading business because I will be able to interact with others and keep physically active. (In-depth interview, S.G., 68 years old, mobile snack and vegetable vendor)

Results from the FGD also emphasize that work was seen not only as a source of income but also a way to maintain health. Some participants said that doing nothing would make them feel unwell and in contrast, staying active was like doing exercise, helping them stay healthy, youthful, and socially connected. These qualitative insights provide a deeper understanding of motivations behind older women’s continued employment, emphasizing the importance of social and personal fulfillment, in addition to economic necessity.

Financial Decision Making and Constraints

This study highlights that many older women entrepreneurs face significant challenges in accessing financial resources, with most of them opting not to take out any loans. The qualitative findings emphasize that older women’s decision to avoid loans is largely driven by fear of financial instability and inability to meet repayment terms. The instability is reflected in the FGD findings, where most participants reported not calculate profits, and often used income immediately for daily needs, reinvested as business capital, or spent on emergencies. Furthermore, one interviewee shared her hesitation to accept a bank loan despite having a history of successful repayment:

I have experience of taking credit from a bank when I was young. When I started the business again [when she was older], they [the bank] contacted me again to offer a loan. But I was not taking their offer. I was afraid of not having the money when the due dates come. (In-depth interview, K.M., 62 years old, onion cracker producer)

In addition to personal concerns, another participant also shared age-related barriers to obtaining bank loans. This was particularly evident among women older than 60, who reported being ineligible for loans because of their age: “I am not allowed to borrow money from the bank because I am already 65 years old” (in-depth interview, S.U., 67 years old, fruit and produce seller).

Although alternatives such as village loan groups, such as Family Welfare Empowerment Program (Pemberdayaan Kesejahteraan Keluarga [PKK]) 1 or dasawisma (10-household community groups under PKK) 2 exist, many women are still cautious about taking loans through these community-based schemes. These loans, although easier to access through savings from group members, are limited in amount: “We could borrow about IDR 100,000–IDR 500,000 [about $6.70–$10), depending on the amount of money held in the groups. It is easy to borrow from the neighborhood groups since it is basically our savings” (in-depth interview, S.G., 68 years old, mobile snack and vegetable vendor).

These findings illustrate how older women face limitations on accessing credit from formal resources. Although older women can access loans through local community groups, these loans are often small. As a result, they may not be sufficient to cover larger business needs. These highlight the need for financial systems that are more accessible to older women entrepreneurs.

Challenges to Safe, Fair, and Sustainable Business

In the qualitative study, most older women report generally good road conditions, but a seller of agricultural products faced a significant barrier. She described the dangerous and muddy roads she must navigate to obtain fresh produce: “The road is bad! The shortcut is in bad condition and muddy. When it is raining, I might fall because it is slippery. Yesterday, I fell on C’s place. But it couldn’t be helped. It must be done to obtain the bananas” (in-depth interview, S.U., 67 years old, fruit seller).

Furthermore, the results of this study show that some older women entrepreneurs operate in unsafe and uncomfortable environments without any visible use of protective equipment. FGD results found that many participants spent long hours on small stools while cooking or selling. In addition, older women who produce food often rely on wood fuel because of cost constraints. Although economical, it exposes them to smoke and extreme heat, especially in kitchens that lack proper ventilation. No participants mentioned using masks, gloves, or eye protection despite these conditions. One woman described the intense discomfort and health risks of her environment: “When you make peyek [a traditional Indonesian snack, a spiced nut and bean cracker] in pawon [a traditional wood-fueled kitchen], the kitchen becomes blackened and hot. It makes the whole body feel very hot” (FGD, village 07, peyek maker).

This study reveals that older women who were working outside of the house often face physical challenges, such as long hours sitting on uncomfortable chairs, which made it painful to walk afterward, or walking long distances to the market. The long working hours of these entrepreneurs is another challenge. For instance, an interviewee who has to prepare and sell food will begin her work early in the morning and continues until late in the evening, resulting in weekly overload of 63 hours. However, despite the physical demands, most entrepreneurs value the financial benefits their businesses bring, even when it involves lifting heavy goods, such as 10 to 14 kg of cotton mattresses or cassavas. These older women do not complain, seeing the hard work as part of their job.

Safety concerns also arise for those working outside, especially in bad weather conditions. One food trader explained that she avoids going to the market when it rains, fearing the risk for falling and sustaining a serious injury: “I won’t go to the market when it rains. I am afraid of falling because it might cause a fatal wound considering my age. The profit can’t be compared to the risk” (in-depth interview, S.G., 68 years old, mobile snack and vegetable vendor).

When it comes to business expansion, many older women express reluctance, physical limitations, lack of knowledge, and insufficient family support. A tailor mentioned the competitiveness of the field, while another felt that her age and energy levels prevented her from taking on more. However, one entrepreneur has managed to expand her business with the support of her husband by finding tools to increase her productivity of her onion crackers business.

Since the COVID-19 pandemic, the shift in customer behavior has also affected older women entrepreneurs, especially those selling food and agricultural products. Many customers now prefer to shop online or have products delivered, resulting in quieter markets and heightened competition from younger and more agile rivals. The combination of physical limitations, a declining customer base, and intense competition has left many older women feel helpless. “Nowadays, buyers [in the market] are rare . . . there are a lot of online sellers” (in-depth interview, S.A., 64 years old, spice seller at the market).

Last, although the entrepreneurs did not mention policies that directly hinder their businesses, infrastructure issues, such as market buildings with multiple floors, have made it harder for them to sell their products. Some of older women resort to selling on the street instead, although this limits their business hours and potential sales. These challenges illustrate the need for more accessible and supportive business environment for older women entrepreneurs.

Limited Access to Social Security

Despite their active economic contributions, many older women entrepreneurs remain excluded from formal social protection systems. On the basis of the survey, even though this only captures a small number of respondents, there were older women who reported not knowing much about Indonesia’s national health insurance (BPJS). However, among those who are not enrolled, the main reasons cited include lack of awareness, perceived irrelevance, and concern about affordability, even when their children offer to assist with the payments. The qualitative findings further illuminate these patterns: “My children want to take care of BPJS’s registration and payment, but I did not allow it. I rarely need health care services, so why do we have to pay for it?” (in-depth interview, W.A., 68 years old, getuk maker and market vendor).

In addition to national health insurance, the government also provides several social protection programs, such as the Family Hope Program (Program Keluarga Harapan), direct cash assistance, as well as business capital for micro, small, and medium entrepreneurs. However, the accessibility of these benefits is inconsistent and the criteria for receiving the assistance often unclear. An older woman who was registered as a beneficiary but did not receive the expected assistance shared her experience:

He [the village officer] said the assistance will be given for business capital [when being registered], but I did not receive any, only being recorded. He said I should wait for my turn, but until now I have never received any. (In-depth interview, M.R., 73 years old, rice trader)

Although some older women viewed cash assistance as a potential source of capital for their businesses, many participants used it to meet immediate household needs, especially during the pandemic. Moreover, many older women entrepreneurs struggled to save, as their limited income was primarily directed toward household survival, rather than business reinvestment.

These findings highlight that many older women undervalue preventive health measures, especially when they feel healthy, which puts them at risk when illness strikes. Their vulnerability is made worse by limited access to government assistance and the absence of old-age savings. Although some received assistance programs, the distribution is often unclear and inconsistent, which resulted in most older women relying on daily income with little financial protection for emergencies or retirement.

Discussion

Reasons for Working and Business Selection

This study shows that older women in rural Indonesia continue to engage in income-generating activities primarily because of financial necessity, including the need to support daily living expenses and social obligations. This is in line with previous research showing that older women remain in work largely for financial reasons (Palermo et al. 2024; Payne and Doyal 2010). Beyond finances, maintaining work also allows these women to uphold their social roles and dignity, which means remaining economically active reinforces their sense of usefulness, self-worth, and standing within the household or community (Herbert 2023). In contexts where ageing is often associated with decline or dependency, continued work enables older women to challenge stereotypes and assert continued value to their families and communities (Pit and Byles 2012). In rural areas, where formal retirement is rare, even low-income or informal work allows women to stay connected to marketplaces, neighbors, and local networks, which help prevent social isolation and fostering a sense of purpose (Ho et al. 2023; Hussain et al. 2023).

The decision to enter specific business sectors among older women entrepreneurs in this study was primarily influenced by relevant skills, enjoyment, and the perception that the work was less physically demanding. Previous studies have similarly noted that older adults tend to select work that accommodates their physical limitations or caregiving responsibilities (Dadheech and Sharma 2023; Zwar et al. 2021). In rural areas, limited access to formal job opportunities may further influence this trend, directing women toward informal and home-based business (Yuniashri, Susilo, and Wahyudi 2023).

Financial Decision Making and Constraints

This study reveals a pattern that reflects not only older women entrepreneurs’ cautious financial approach in rural Indonesia, but also the broader issue of limited financial access among them. They tend to avoid formal credit, driven by concerns about repayment and restricted loan eligibility because of age, and prefer relying on personal savings or informal sources. Previous research has shown that institutions consider them high-risk borrowers because of their age and limited income (Gutterman 2023). Many who earn income from seasonal activities such as farming or selling in local markets will cause an inconsistent cash flow and this makes it difficult for them to commit to formal loans that require fixed monthly repayments (Komba and Komba 2024). Past experiences with financial hardship, such as family debt or failed ventures, further reinforce a preference for slow and steady business development (Sharma, Lee, and Lin 2023).

Most financial education targets younger or urban groups, which further restricts older women in rural area’s ability to explore credit (Lusardi and Mitchell 2011). Our findings also show that although informal credit is accessible, older women still hesitate to borrow because of small available amounts and concerns over timely repayment. Although relying on informal financing may help sustain their businesses, a previous study explained that its limited capital base and high borrowing costs can restrict their ability to grow or adapt during financial pressures (Mpofu and Sibindi 2022). Although our study did not directly identify stigma as a barrier, prior research suggests that borrowing from formal institutions in rural communities may carry social stigma as a sign of financial weakness, discouraging older women from seeking external support (Fatima 2009). These factors foster making cautious and constrained financial decisions, as it is necessary for their survival and aligns with community expectations.

Challenges to Safe, Fair, and Sustainable Business

This study highlights several challenges in ensuring safe, fair, and sustainable business practices for older women in rural Indonesia. Women living in households with three or more members were less likely to report working in unsafe or unhealthy environments, suggesting a possible protective effect of shared responsibilities or support systems. Previous studies have shown that extended families or multigenerational household can reduce both physical workload and financial pressure on older adults, especially in low-income contexts (Heflin and Patnaik 2023).

Our study shows that older women in industry sectors were likely to report higher risk for respiratory problems, while more of those in trading reported excessive working hours. Higher proportion of those aged 60 to 69 years were also reported to stay up late or wake up too early. Those working inside the house reported doing physically burdensome activities, and not using protective equipment compared with those working outside or both. On the basis of prior research, informal or home-based work environments often lack regulatory oversight, which may contribute to longer working hours and greater exposure to health risks such as musculoskeletal strain and fatigue (Haliza and Nugroho 2024; ILO 2022). Physical strain, such as lower limb pain is the common challenge among older working women and can threaten their ability to keep working. However, such issues often remain underprioritized in health care, with limited tailored support available (Palermo et al. 2024). Our qualitative findings also highlight that age-related constraint, such as declining health, reduced physical capacity, and limited access to formal financial loans because of age restrictions, which further increased the reluctance to expand their businesses or even reduce their workloads. Poor health, especially when combined with the physical demands of work, leads some individuals to avoid taking on additional responsibilities out of concern for their physical and mental well-being (Moor, Spallek, and Richter 2017).

Our study also found that women 70 years and older generally worked fewer hours, which aligns with previous research suggesting that older workers often reduce their working hours because of physical limitations or a preference for leisure as they age (Hansson et al. 2018). Additionally, women with higher education were less likely to have low incomes. This finding aligns with studies showing that education equips individuals with better financial literacy, business planning skills, and access to information and networks, which can improve the performance and profitability of small entrepreneurs, even in rural settings (Reza et al. 2020; Sari et al. 2024). Although our study does not include those who have exited the workforce, these findings suggest that education may enhance the income-generating potential of older women who continue to work. This study also reveals that those in smaller households (one or two household members) were more reported to have low monthly net income than their counterparts. Previous studies explained that those in small households are frequently entirely dependent on their business income, which is in contrast to larger households that can benefit from financial and labor contributions of their productive family members (Ge et al. 2022; Jaikumar et al. 2025). Furthermore, the lack of support system within small families makes it challenging to grow or even maintain a business, as there is less access to the unpaid labor and financial assistance that larger families can provide (Hill, Hirsch, and Davis 2021).

Previous research indicates that age-friendly environments facilitate older adults to remain active in economic and social activities (Shi Ying, Ming Ming, and Siok Hwa 2021). Our qualitative findings reveal that inadequate infrastructure, which was reported by our participants in the form of climbing stairs or walking considerable distances to reach selling locations, burdened them physically. Furthermore, shifting customer behavior to online transactions and delivery systems has posed additional challenges for older women entrepreneurs in rural areas. Previous studies found that older adults often struggle to keep pace with these technological changes, as many are unfamiliar with digital tools and find it difficult to learn new systems without targeted support (Akbar and Wijaya 2024). As consumer preferences increasingly favor speed, convenience, and digital interaction such as online ordering and cashless payments, older women entrepreneurs unable to engage with these systems face the risk of being left behind, which can lead to lower income potential and a growing sense of marginalization (Trisninawati and Sartika 2024).

Limited Access to Social Security

Our study reveals significant disparities in access to social security among older women entrepreneurs in rural Indonesia. In this study, the proportion of older women with health insurance was higher in those 70 years and older than the younger group. This indicates that as people age, reliance on public programs becomes increasingly pronounced. As previous studies explain older adults often face a decline in health status, necessitating greater access to health care, which compels them to seek health insurance (Agyemang-Duah et al. 2024). Another study also indicates that as individuals age, their health care needs and perceived vulnerabilities amplify, leading to higher enrollment rates in health insurance (Debessa, Negeri, and Dangisso 2025).

Furthermore, those living with fewer household members also showed higher insurance coverage compared with those in larger households, suggesting that household composition influences economic and health security in later life. Although our qualitative data do not directly explore household size, they offer some insight into how decisions are made within families. One older woman chose not to let her children pay for her health insurance because she felt she rarely needed medical care. This shows how personal beliefs and a desire not to burden family members can shape decisions around insurance, especially in households where multiple generations live together. A previous study has shown that the presence of multiple dependents may limit financial resources which reduce contribution to savings or enrollment in insurance (Chen, Leeson, and Liu 2017).

Business sectors further influence access to social security. Those working in the industry sectors reported to be more likely to have retirement savings than those in other sectors. These differences may be attributed to the nature of income generation and financial management practices across sectors (Dadheech and Sharma 2023). Industrial work, even in home-based or small-scale settings, may involve more consistent production routines or community-based arrangements, whereas income from trading or services is often more irregular and dependent on fluctuating customer demand, making long-term financial planning more difficult (Magidi 2025).

On the basis of our findings, to support older women entrepreneurs in rural Indonesia, policies should focus on providing training in technology to improve their business activities or involving local young people with tech skills as partners to strengthen their businesses. Offering financial management education would help them make informed decisions, while raising awareness about the importance of health insurance and work-life balance would ensure long-term sustainability. However, although encouraging older adults to remain in the workforce can help ease the pressure of an aging population, it is crucial to recognize that staying in work should not be the only option for socio-economically disadvantage older women who cannot afford to stop working (Palermo et al. 2024). When these women remain in work at the expense of their own health, the long-term societal cost may outweigh the short-term economic gains, especially if it leads to deteriorating health and increased need for long-term care (Carmichael, Charles, and Hulme 2010; Harris et al. 2020; King and Pickard 2013). Finally, revising loan and credit regulations to ease age-related restrictions would improve access to financial resources.

This study highlights the unique challenges older women entrepreneurs in rural Indonesia face regarding financial decision making, limited financial knowledge, reliance on informal financing, and the influence of family and social norms. It reveals how gendered expectations shape their economic behavior and limit their access to resources and opportunities, consistent with prior findings on women’s economic marginalization in later life (Setijaningrum, Triana, and Kassim 2024). These findings contribute to sociological discussion on gender, aging, and informal labor by showing how older women sustain livelihoods in the absence of formal support. Practically, the results point to the need for targeted policy support, such as improving financial literacy programs, facilitating access to affordable credit, and providing flexible social protection schemes (Arwani et al. 2024). These interventions may help improve the quality of work for older women in rural communities.

There are some limitations to this study. It was conducted in only one region of Indonesia, which was purposefully selected because of its large number of older people. Because of that, the findings may not represent the situation of older women in other parts of the country. The study also focused only on entrepreneurs and excluded women working in coastal or mountainous areas, whose experiences may be different.

Conclusion

The aim of this study was to explore the working conditions and influencing factors affecting the work-life balance, income, and adaptability of older women in rural Indonesia, using mixed-methods approach combining surveys, interviews, and FGDs. Our findings reveal that older women in rural Indonesia remain economically active mainly out of necessity, often choosing business sectors according to accessibility and experience rather than strategy. Their financial decisions are shaped by limited access to formal credit, reliance in informal sources, and concerns related to age and repayment risks. Working conditions vary by sector, with trading and workers more likely to work long hours, those in industrial sectors face more physical risks. Household composition and work location can also affect the risk for unsafe environments and inadequate protective equipment use. Higher education plays a protective role toward higher income. Those in larger households remain lacking health insurance, while those in industry sectors are more reported to have retirement savings. Inadequate infrastructure and digital shifts further challenge their ability to sustain their businesses. On the basis of these findings, policy efforts should focus on digital training, inclusive financial education, family involvement, and more flexible credit regulations to support older women entrepreneurs in rural areas.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by HelpAge International, with publication support from Chulalongkorn University.

Ethical Approval and Informed Consent Statements

This study was conducted in accordance with ethical standards for research involving human participants. Informed consent was obtained from all participants after they were informed about the study’s purpose, their voluntary participation, and their right to withdraw at any time. Participant confidentiality and privacy were strictly maintained throughout the study.

Data Availability Statement

The data that support the findings of this study are not publicly available, because of confidentiality agreements and ethical restrictions.

1

PKK is an Indonesian community empowerment program focused on family welfare, particularly through women’s roles.

2

Dasawisma is a neighborhood unit within PKK, typically consisting of 10 households, that implements local welfare initiatives.