Abstract

Against the backdrop of an acute rental affordability crisis and a resurgent tenant’s rights movement, rental industry groups have frequently argued that tenant protection laws disproportionately harm “mom-and-pop” landlords and, by extension, the disadvantaged tenants they serve. The authors leverage a changing regulatory environment in Seattle to provide a rare empirical interrogation of these claims. This analysis of a novel set of consumer data linked with parcel records provides no evidence that tenant protection laws drove “mom-and-pop” landlords out of the rental market. Moreover, an analysis of a survey of almost 4,000 Seattle landlords suggests that “mom-and-pop” landlords use management practices that are largely similar to those used by landlords with larger rental portfolios. These findings run counter to pervasive political narratives regarding the detrimental effects of tenant protection regulations on the small-scale rental sector and bring needed attention to the repercussions of claims-making for stratification in the housing context.

Although U.S. rental units are increasingly owned by large-scale institutional investors and corporate landlords (Lee 2017), the archetype of the “mom-and-pop” landlord continues to loom large in contemporary debates over rental regulation. 1 In many markets, small-scale landlords have traditionally provided much of the private-sector affordable housing (Garboden and Newman 2012), with the image of the “mom-and-pop” landlord as the nation’s de facto affordable housing provider frequently deployed to resist rental market regulation. In recent years, rental industry groups have centered “mom-and-pop” landlords in their efforts to quash tenant protection laws proliferating in many jurisdictions amid a resurgent tenant’s rights movement. Rental industry groups argue that new tenant protections disproportionately harm small-scale, “mom-and-pop” landlords, and by extension, the low-income and vulnerable tenants housed within that sector.

The U.S. rental housing industry is a powerful political constituency with a long history of successfully aligning policy with landlord interests (Keating and Kahn 2002). Narratives about adverse effects of tenant protection laws on small-scale landlords can chill the willingness of policymakers to regulate rental markets at a moment characterized by unprecedented rental unaffordability and insecurity crises. Despite their potential impact on public policy, such claims rarely receive empirical scrutiny. Although recent research on landlord management practices has helped revive a relational perspective on inequality, sociologists have overlooked how landlords maintain relational inequality through claims-making that shapes the legal and policy environment in which they operate (Tomaskovic-Devey and Avent-Holt 2019).

In this study we leverage a changing regulatory environment in Seattle, Washington, to assess two prominent claims deployed by rental industry organizations to oppose tenant protections: first, that new regulations hasten the decline of the “mom-and-pop” rental sector by driving small-scale landlords to sell their properties and, second, that this outcome harms disadvantaged tenants by further constricting the supply of housing that is affordable and accessible to them.

The latter claim assumes that small-scale landlords manage their properties in ways that are favorable for tenants (e.g., keeping rents relatively low, using more flexible tenant screening procedures, filing for eviction less frequently).

To investigate whether new regulations affected trends in the loss of small rental properties (SRPs), most of which are owned by small-scale, noninstitutional landlords (Congressional Research Service 2022; Freddie Mac Multifamily 2018; Jabir et al. 2023; Travis 2022), we link parcel records with consumer data to identify sales of one- to four-unit rental properties. Using a difference-in-differences (DD) design, we compare trends in the probability of SRP sales in Seattle and in surrounding areas within the county before and after two tenant protection laws were enacted in 2016 and 2017. Then, to evaluate claims that low-income and vulnerable tenants are better served by small-scale landlords, we analyze responses from a survey of Seattle landlords to explore whether the practices of landlords who own four or fewer rental units are different from those of landlords with larger portfolios.

Our findings run counter to political narratives regarding the detrimental effects of tenant protection regulations on the small-scale rental sector. Analyses of SRP sales do not show that two contested tenant protection laws in Seattle drove SRP owners to exit the rental market by selling properties, as rates of SRP sales continued to decline in Seattle following the regulations’ passage, paralleling the trend in the remainder of King County where the regulations did not apply. Meanwhile, our survey analysis paints a mixed picture of practices among small landlords that complicates industry narratives and long-standing assumptions among housing experts about the benefits of “mom-and-pop” rental housing for tenants. Consistent with those assumptions and some of the existing scholarship, we find that, in Seattle, small-scale landlords charge slightly lower rents, impose fewer rent hikes, and file for eviction less than landlords with larger rental portfolios. On the other hand, small landlords were less likely to rent to low-income tenants or those with housing vouchers, criminal conviction records, or requests for disability accommodations, and were no different from larger scale landlords in terms of offering flexible leases. These findings raise questions about variation in the accessibility of housing in the small-scale rental sector, including which tenants benefit from the relative affordability and stability of tenure associated with it.

The present study has timely implications for housing policy at a moment when local and state lawmakers are looking to confront housing crises with the levers at their disposal but worry about externalities of new tenant protection laws for the remaining privately owned and “naturally occurring” affordable housing supply. Our findings demonstrate why arguments wielded by industry groups interested in blocking new tenant protections need empirical evaluation. By investigating whether rental regulations reduced the supply of relatively accessible and affordable housing by driving “mom-and-pop” landlords out of the rental market, our analysis helps policymakers and the public assess the potential costs and benefits of screening protections. Although the practices of small-scale landlords may differ across high- and low-cost cities, this analysis provides answers about dynamics in one market on the leading edge of rental housing policy change and establishes a model for future assessments of rhetorical claims used to limit regulations.

Beyond lessons for housing policy, our study has broader implications for multiple fields of sociological scholarship, including the political economy of housing, regulatory law in practice (Calavita 2016), and relational inequality. First, our findings contribute to an evolving understanding of how rental ownership characteristics shape management practices by complicating the assumption that SRP landlords provide housing on better terms for tenants. The results of our analysis of SRP sales also challenge overly deterministic accounts of regulatory law in action that presume regulated industries will inevitably act to circumvent protective social policies and pass regulatory costs onto the intended beneficiaries. Finally, our case study extends the burgeoning scholarship on relational inequality in the housing context (Martin 2017) by scrutinizing arguments designed to align policy with landlord interests and bringing attention to the repercussions of claims-making for housing inequality.

Background

Worsening rental unaffordability and insecurity in the wake of the Great Recession have precipitated a resurgent tenants’ rights movement and the shift toward a more protenant regulatory environment in many states and localities (Putzier 2019). In the past decade, state and local policymakers enacted new and expanded rent control laws (Dougherty and Ferré-Sadurní 2019; Zaveri 2019), caps on rental fees and security deposits (Ferré-Sadurní 2019; Parker 2020), due-process protections for tenants facing eviction (Beekman 2020; Cohen 2023), and expansions of fair-housing laws prohibiting discrimination on the basis of administrative statuses such as a criminal record and an eviction history (Johnson 2016). Calls for market regulation intensified following the coronavirus disease 2019 pandemic (Dougherty 2022), with rents and the number of cost-burdened renters sharply rising after state and local eviction moratoria expired (Kodé 2023).

These developments triggered intense backlash from the rental housing industry (Oprysko 2021; Tobias 2018) and signal cracks in a traditionally powerful urban business constituency’s grasp on policy. However, contestation over regulatory policy does not typically cease after lawmaking or withstanding challenges in court. Even when unsuccessful in the short term, political backlash to regulation on the part of business groups can successfully shape public understandings in ways that advance the long-term interests of regulated industries (Haltom and McCann 2009). Persuasive narratives about the public costs of regulation borne can delegitimize activists’ calls for greater protections and curtail lawmakers’ future legislative aspirations.

Rental housing industry spokespersons frequently center “mom-and-pop” landlords in public campaigns opposing new regulations. Claims that regulations expose small landlords to unique risks and burdens are not new (Jenkins and Peck 2022; Slater 2021), but such arguments may resonate with the public and policymakers, especially at a time when rental housing owned and operated by small, independent landlords is declining (Joint Center for Housing Studies of Harvard University 2023). Although the concomitant rise in the proportion of rental units owned and operated by institutional investors has been concentrated in a handful of Sunbelt rental markets (Colburn, Walter and Pfeiffer 2021; Fields, Kohli and Schafran 2016; Mills, Molloy and Zarutskie 2019; Seymour et al. 2023), it has sparked concern among tenant advocates, as corporate ownership of rental housing has been linked to rising rents, higher eviction rates, and other exploitative management practices (Burns 2018). Opponents of new tenant protection laws have seized upon such concerns with claims that regulatory overreach hastens the exodus of “mom-and-pop” landlords from the rental market and consolidates ownership in the hands of “Wall Street” landlords. Although we interrogate political claims made in response to policy debates in Seattle, this discursive frame has shaped debates around tenant protection laws in other jurisdictions (Cuozzo 2023; Tomic 2023) and featured prominently in national media coverage of eviction moratoria during the coronavirus disease 2019 pandemic (Conlin 2021; Parker and Ackerman 2021; Vesoulis 2020).

Sociologists have increasingly recognized housing as a central institutional engine of poverty and inequality, as opposed to merely a set of outcomes that help explain the effects of neighborhood inequality on individual life chances (Martin 2017). There has been a flourishing of research on the private rental market, focusing on how individual landlords reproduce inequality through their day-to-day management practices (DeLuca and Rosen 2022). Much less attention has been paid among sociologists to how landlords, as a political constituency, reproduce inequality through claims-making activities that are intended to bring law in line with their interests. However, the implications of claims-making for relational inequality in the employment context offer lessons for housing scholars regarding why, in struggles over resources, opportunities, and power, certain claims are legitimized and subsequently privileged over others (Hanley 2022; Tomaskovic-Devey and Avent-Holt 2019). In addition to characteristics of claims-makers (e.g., skill, position in status hierarchies), various properties of claims themselves increase the likelihood they will be perceived as legitimate, such as resonance with existing cultural frames (Avent-Holt 2012; Somers and Block 2005; Tomaskovic-Devey and Avent-Holt 2019).

Of course, a claim’s legitimacy also hinges on factual validity, or at least perceived validity (Tomaskovic-Devey and Avent-Holt 2019). Specifically, two claims undergird these narratives: that SRP landlords will exit the rental market in response to “unfriendly” regulation and that small-scale landlords provide housing on better terms for low-income and vulnerable tenant populations. In what follows, we identify lessons from research on how landlords respond to regulation and influence the effects of legal efforts to protect tenants. We then review existing literature on “mom-and-pop” landlords’ management practices and business logics, and the extent to which they are distinct from those of larger, professional landlords.

Literature Review

How Do Landlords Respond to Regulation?

Recent research provides a picture of how landlords respond to legal controls on their practices. Case studies have investigated how landlords respond to local tenant protection laws, including habitability standards in Chicago (Bartram 2022), new fair-housing laws regulating tenant screening in Seattle (Reosti 2020), and multiple regulations governing rental housing, including water billing policies and due-process protections for tenants facing eviction, in Cleveland (Greif 2022). Echoing lessons from sociolegal scholarship on workplace, environmental, and consumer law in practice (Edelman 1992; Talesh 2009; Yeager 1993), these studies find that landlords pass the costs of regulatory compliance (real or perceived) onto tenants through rent increases, reduced maintenance, or more exclusionary screening practices. However, landlords’ adaptations to regulatory policy are motivated, constrained, and facilitated by local economic and policy conditions. Rent control laws might otherwise constrain landlords who raise rents after being fined for building code violations (Bartram 2022), while an affordable housing shortage permits landlords to ratchet up screening criteria in response to new tenant background protections without fear of leaving vacancies unfilled (Reosti 2020), and the lingering effects of the 2008 foreclosure crisis motivate landlords in economically distressed neighborhoods to shift the perceived financial risks of regulatory compliance onto tenants (Greif 2022).

Finally, literature on rent control offers some important insights into how landlords respond to regulation. Although economists have long theorized that rent control laws increase rents by constricting housing supply, contemporary empirical studies of local rent control policies paint a more complex picture of the policy’s impacts, complicating the assumption that landlords will respond to it in predictable ways (Autor, Palmer, and Pathak 2014; Diamond, McQuade, and Qian 2019; Sims 2007). Although the impulse to avoid legal controls on price setting on the part of landlords is foreseeable, if not inevitable, comparing findings from studies of jurisdictions with “weak” and “strong” varieties of rent control regimes suggests that landlords’ opportunities and incentives for doing so are variable and contingent (Arnott 1995). Taken together, research on rental housing law-in-action suggests that landlord responses to tenant protection regulation are not invariant or predictable, but instead, shaped by broader features of the market and policy environments in which they operate.

Management Practices of “Mom-and-Pop” Landlords: Are Small Landlords Better Landlords?

Rental industry groups who oppose tenant protection laws argue that such policies will counterintuitively harm low-income tenants by hastening the decline of the “mom-and-pop” rental sector, where rents are more affordable and management practices are friendlier toward tenants. The idea that small-scale landlords offer more affordable housing on better terms for vulnerable tenants also has considerable purchase in mainstream policy circles, reflected in recent proposals to preserve and expand the small-scale (i.e., one to four units) rental stock (Brickman 2023; The White House 2021).

However, inconsistent definitions and operationalizations of “small” or “mom-and-pop” landlords across academic, policy, and popular discourse make it difficult to interrogate claims about differences in the practices of large and small landlords. Researchers typically use either portfolio size (i.e., number of units owned by a landlord) or building size (i.e., number of units in a rental property) to distinguish between small and large landlords, depending on whether data describe landlords or properties. There is considerable overlap between those categories, as the vast majority of single-family and two- to four-unit rental properties are owned by small-scale landlords (Freddie Mac Multifamily 2018; Travis 2022). Regardless of using portfolio or building size, an upper limit of four or five units is common among researchers, policy experts, and housing organizations when defining a small landlord (e.g., Choi and Young 2020; Decker 2021, 2023; Garboden and Newman 2012; Gomory 2022; National Association of Realtors 2023).

In what follows, we review existing research about the practices and business logics of small-scale landlords for three issues that are of special interest to policymakers: rent setting, eviction, and tenant screening.

Rent Setting

Small-scale rental properties have traditionally constituted an outsized proportion of the “naturally occurring” affordable housing stock: private-market housing that is affordable without subsidies. Many renters below the poverty line and most low-income rental households with children live in rental properties with four or fewer units (Decker 2021; Garboden and Newman 2012). The relative affordability of SRPs is partially explained by their age, condition, and lack of amenities compared with larger multifamily properties (Mallach 2007; Newman 2005). Still, case studies of SRP indicate that some charge discounted rents for units in good condition that could otherwise command market rents (Decker 2021). In a nationwide study, Decker (2021) found that 44 percent of one- to four-unit rental properties owners reported deliberately setting rents below market rates and that, outside of length of tenant tenure, few characteristics of landlords or their rental portfolios were consistently predictive of below-market rent setting.

Although Decker (2021) suggested that rent-setting practices are idiosyncratic among small-scale landlords, qualitative research identifies some common motivations that drive them to set below-market rents. Small-scale and nonprofessional landlords report keeping rents affordable to reduce the costs associated with turnover (i.e., repairs, tenant recruitment and screening, risk of extended vacancy) that may be amplified for small-scale owners (Mallach 2007; Reosti and Helmuth 2021). Social considerations can also affect the decision to set lower rents, as they have more interpersonal contact with tenants and may be more attuned to tenants’ financial struggles (Shiffer-Sebba 2020), particularly if they live in the building (Helmuth 2024).

Evictions

Available research suggests large and small landlords differ in terms of their use of eviction, with elevated eviction filing rates among larger and/or corporate landlords (Decker 2023; Gomory 2022; Immergluck et al. 2020; Leung, Hepburn, and Desmond 2021; Raymond et al. 2021), especially institutional landlords in the single-family rental (Fields and Vergerio 2022; Raymond et al. 2018; Seymour and Akers 2021) and extended stay (Seymour 2023) submarkets. Large landlords employ professional property management services that facilitate a routinized response to nonpayment, while also having greater financial and organizational capacity to file evictions (Gomory 2022). On the flip side, small-scale landlords may be less likely to take evictions to court because of the associated costs (Balzarini and Boyd 2021).

However, a few recent studies complicate the broad takeaways from this literature. First, although research demonstrates that portfolio size is positively associated with eviction filing rates, Gomory (2022) found that larger landlords actually execute evictions at lower rates than small landlords. This paradox could be explained by evidence that large landlords practice serial eviction filing as a rent collection tool, using the repeated threat of eviction to compel payment (Garboden and Rosen 2019; Immergluck et al. 2020; Leung et al. 2021). Second, some research suggests that small landlords may be more likely to pursue informal or illegal evictions, such as lockouts and “cash for keys” schemes in an effort to avoid the costs associated with formal eviction (Balzarini and Boyd 2021; Greif 2022). Finally, Decker (2023) argued that small landlords file fewer evictions because they experience nonpayment less frequently, rather than having distinct responses to nonpayment. He theorizes that small landlords keep nonpayment rates down through more “hands-on” and meticulous forms of screening that weed out financially insecure tenants but are also more likely to run afoul of fair-housing law (i.e., compared with the screening methods used by professional landlords).

Tenant Screening

Qualitative studies of landlord practices demonstrate that smaller, independent landlords tend to use more impressionistic and informal tenant screening methods than large-scale, professional landlords (Reosti 2020; Rosen, Garboden, and Cossyleon 2021). Whereas large landlords are more likely to use professional property management services or automated screening tools that exclude applicants deemed “risky” by actuarial standards (Fields 2022; Rosen et al. 2021; So 2023), small landlords are more likely to use flexible screening criteria that facilitate leniency for applicants with tarnished records (Greif 2022; Reosti 2020; Shiffer-Sebba 2020). However, this discretionary benevolence is extended unevenly to renters with background issues (Reosti 2020; Rosen et al. 2021).

Despite the consistency and conviction with which rental industry advocates tout the tenant-friendly management practices of small landlords, available research raises questions about the extent to which large and small landlords differ in their practices and approaches. There are also open questions about whether the flexible and informal property management approaches characteristic of small or “mom-and-pop” landlords uniformly benefit tenants. In the following section, we describe the political developments motivating our case study of landlord management practices and responses to regulation in Seattle.

Case Study

Landlord Backlash to Tenant Protection Policies in Seattle

Seattle epitomizes the conditions that have encouraged policymakers in high-cost cities to more aggressively regulate the practices of private landlords in recent years. The city experienced some of the nation’s fastest annual increases in rents in the past decade (Rosenberg 2016), driven largely by a population boom and influx of high-income technology workers that strained the supply of affordable housing. Aiming to address unaffordability, homelessness, and racialized residential displacement crises, city policymakers enacted a number of tenant protection laws that were far reaching by national standards and generated significant backlash from the local rental housing industry.

In 2016, the city passed the “first-in-time” law requiring landlords to make their rental criteria available to prospective tenants, screen applicants in the order that they apply, and rent to the first qualified applicant (City of Seattle 2016). The measure intended to strengthen an existing law prohibiting source-of-income discrimination after fair housing tests revealed that landlords continued to routinely refuse to rent to housing voucher recipients (Beekman 2016). On the heels of the “first-in-time” law, the City Council then approved the nation’s strongest ban on criminal background checks for rental housing. The 2017 Fair Chance Housing Ordinance prohibits private rental housing providers from using criminal background information to screen and select prospective tenants in nearly all circumstances (City of Seattle, Office of the City Clerk 2017). These laws break from previous legal standards granting landlords considerable latitude to choose tenants on the basis of subjective and idiosyncratic criteria as long as they did not make reference to protected statuses (McCormack 1986; Strahilevitz 2005). As in other domains in which Seattle has spearheaded progressive policy innovation (i.e., minimum wage, paid sick leave), a number of jurisdictions have since enacted rental regulations modeled on the fair chance and first-in-time policies (Bittle 2019; Evans 2019).

First-in-time and fair chance generated intense and sustained backlash from the local rental housing industry. After the ordinances were enacted in the face of considerable organized opposition, professional rental housing interest groups waged a battle on multiple fronts to overturn the laws and publicize potential adverse social and economic consequences of rental regulation. Whether in the context of lobbying, op-eds, press conferences, or litigation, local professional rental housing organizations consistently built their criticisms of the new laws around purported impacts of regulatory overreach on “mom-and-pop” landlords (Gerrald 2021; Kroman 2019).

Small-scale landlords served as plaintiffs in two lawsuits challenging the first-in-time and fair chance laws, alongside a rental housing association (Lloyd 2018a, 2018b). Although the lawsuits have failed to overturn the policies at the time of writing (Kroman 2019),

2

professional rental housing organizations still succeeded in shaping political discourse around the laws in the local media. Following the law’s passage, rental industry spokespersons repeatedly claimed that the laws triggered an exodus of “mom-and-pop” landlords from Seattle’s rental market (Brewer 2021; McNichols 2023; Seattle Times Editorial Board 2021; Triplett 2018). Industry advocates also contend that “mom-and-pop” landlords charge lower rents and use less stringent screening criteria than larger and/or corporate rental companies. As such, the new rental regulations would disproportionately harm the groups they are designed to benefit: low-income tenants, housing voucher recipients, and people with tarnished background records. An op-ed written by one of the attorneys representing landlords who sued to overturn both laws illustrates multiple elements of these narratives: The results of these laws are easy to predict. Small-time landlords . . . will respond in one of two ways: they’ll either try to filter out bad eggs by jacking up rent and toughening rental criteria, or they’ll just sell. Neither are desirable outcomes, but it already appears that many landlords are taking the second option. . . . The great irony is this: the only entities capable of surviving as landlords in Seattle’s regulatory climate will be the large corporate residential leasing companies. . . . Mom-and-pop landlords are a boon to a community. They tend to offer lower rents. They can be more understanding when the rent check is late or your kid tears the towel rack from the bathroom wall. (Blevins 2018, italics added)

With respect to the screening practices of small landlords, one plaintiff in the aforementioned lawsuits told the Seattle Times that the policy stops landlords from “making exceptions to help people,” such as renting to applicants who do not meet minimum screening criteria following a conversation, adding “the city’s only concern is a landlord using discretion to do harm, but the law prevents us from using discretion to do good” (Beekman 2018). These narratives continue to influence political debates around rental housing policy years after the laws’ passage. In a 2022 hearing on a proposed measure requiring landlords to report data on rents to comply with the city’s rental registration program, a city council member argued against any new regulatory action that could exacerbate the ongoing exodus of small landlords from Seattle’s rental market, which she attributed to protections such as first-in-time (Barnett 2022).

In summary, political efforts to oppose renter protection legislation in Seattle center on externalities borne by “mom-and-pop” or small-scale landlords. This rhetorical strategy mirrors anti-regulation campaigns in other domains, particularly those framing labor and workplace safety regulations as threats to small businesses, and by extension, workers’ material interests. These narratives hold sway in political discourse, in part because they resonate with the long-standing valorization of small businesses in the United States (Saad 2023). Although scholars have examined and challenged claims about the perils of regulation for “mom-and-pop” businesses in the employment realm (Atkinson and Lind 2018; Pierce 1998; Shapiro and Goodwin 2013), similar claims in the housing context have been subject to little scholarly scrutiny.

Research Agenda

We draw upon several data sources to interrogate two claims used to oppose new tenant protection laws in Seattle and other jurisdictions: that two contested rental regulations created an exodus of SRP owners from the rental market and that low-income and vulnerable tenant populations are better served in the SRP sector. To investigate whether new regulations affected sales of rental properties likely to be owned by small-scale landlords (i.e., one- to four-unit buildings), we use consumer trace and parcel data with a DD design to compare trends in the share of SRP sales in Seattle and areas of King County outside of the Seattle city limits before and after the passage of two tenant protection laws. We then evaluate the claim that low-income and vulnerable tenants are better served by small-scale landlords by using landlord responses from the Seattle Rental Housing Study (SRHS), using regression analysis to understand how small and large landlords differ in their tenant profiles and rental practices.

Data and Measures

Rental Sale Analysis

Consumer Trace and Parcel Data

We combine consumer trace and parcel data to assess whether landlords exited the market through sales of SRPs. Trends in sales of one- to four-unit rental properties provide a strong signal about how much small-scale landlords are exiting the rental market by selling their properties. Despite the well-publicized growth of large-scale, institutional investors in some Sunbelt rental markets (Colburn et al. 2021; Fields et al. 2016; Mills et al. 2019; Seymour et al. 2023), recent estimates suggest that nationwide, more than 85 percent of single-family and two- to four-unit rentals are owned by small-scale landlords. 3

The consumer trace data are available from Data Axle and are a product of linking records such as credit card statements, utility bills, voter registration, property tax assessments, public financial records, and mailing address changes. Although research using consumer trace data has proliferated (Stewart 2021), most commercial uses of such data are still for identifying target mailing leads or tracking existing customers. Nevertheless, recent scholarship shows how these privately generated data sources provide insight into social processes such as population change and gentrification (Acolin, Decter-Frain, and Hall 2022; Acolin et al. 2023). Relevant to the present study’s aims, research has used consumer data to study rent control laws and housing stability, including policy evaluations for local rental markets (Diamond et al. 2019, Phillips 2020).

We subset the national database to households located in King County and then filter our sample to heads of household because our focus is on identifying whether a renter household resided where a parcel transaction was subsequently observed. This generates a dataset of about 12 million household records, with an average of about 800,000 observations each year. Given the considerable geographic mobility into the Seattle metropolitan area in recent decades, many households are observed for only part of the temporal extent from 2006 to 2020.

We use the street addresses in the consumer data to geocode the records to rooftop or street address coordinates using ArcGIS at a rate of 97.2 percent. These precise geolocations and standardized addresses form the basis for (1) exact address string matching (preferred) or (2) approximate spatial intersection (for sensitivity assessment) with the King County Tax Assessor’s transaction and assessment data for each parcel. Before matching the parcel and consumer data, we standardize the addresses present in the parcel data to ensure the formatting follows the same rules as addresses returned from the consumer data geocoding. This step has a success rate of 99.2 percent.

We create two samples on the basis of the linked data. The first is based exclusively on exact address matches, for which there was a match rate for 86 percent of all 12 million consumer data records. To assess how sensitive results are to this match, we also append parcel identifiers to the remaining 14 percent of consumer data records using a two-stage process of (1) spatial intersections and (2) approximate matching using the closest parcel. We rely on the exact match analysis as the focal results for this part of our study because these consumer-parcel data linkages have the greatest reliability but present results based on the approximate match in the Appendix to show that results are similar under an alternative specification exhausting all possible matches.

Identifying Renter-Occupied Properties

The consumer data enable us to operationalize whether units on a parcel were renter occupied in a given year. After joining parcel identifiers to the consumer data, we are able to append tenure information to about two thirds of all parcel-years in a balanced panel of residential parcels spanning from 2006 to 2020. Notably, the Data Axle records tenure information through an ordinal measure capturing whether the household in a given property is expected to be an owner or a renter. These values are based on a proprietary algorithm that uses real estate data (e.g., property deeds, tax accessor records for characteristics such as homestead exemptions) along with neighborhood-level census estimates to produce this score for whether a household is a homeowner or renter. Most households fall at the extremes of this tenure scale, particularly among homeowners, but there are nonetheless many cases who fall in between. These gradations necessitate a decision rule for converting the scale into categories for owning or renting. We proceed with dichotomizing the renter/owner measure with an even split in terms of the range of values contributing to each level (i.e., renter = 0–4, owner = 5–9), but we also include results using other threshold values to be clear about robustness to alternatives. 4 When we operationalize tenure of a parcel, we do so on a lagged basis and flag if that the parcel was renter occupied the prior year. As such, our effective sample of data covers 2007 to 2020. 5

Identifying SRPs

Definitional imperfections notwithstanding, one of the most common ways that “mom-and-pop” landlords are operationalized in prior literature is through the size of the structures they manage. This measurement strategy is predicated on small operation landlords being unlikely to have the capital to construct or acquire large apartment buildings with more than 50 or even 20 rental units. Measuring SRPs with the parcel data depends on looking at characteristics of the residential structure(s) on the parcel to identify if there are one to four housing units, which we do through appending tables describing features of residential units and apartment complexes to the linked consumer-parcel data.

Small-Scale Landlord Practices

SRHS Data

We use data from the 2018 SRHS to understand if small-scale landlords better serve low-income and vulnerable tenants. This study, fielded by the University of Washington, surveyed Seattle landlords to provide a picture of housing market dynamics, landlord practices, and attitudes toward city housing regulations. The survey included both property owners managing their own properties and nonowner property managers. The voluntary, anonymous, online survey was sent to 18,477 individuals represented in data from the city’s RRIO program and received 3,836 responses. 6 This survey is the first source of data on the experiences and attitudes of Seattle landlords.

Landlord Characteristics

Following convention (e.g., Gomory 2022), we categorize landlords as small if they own and/or manage one to four units, while landlords with five or more units are categorized as large. We describe landlords further by examining characteristics of their professional background and the rental units they own and/or manage. These variables include years of experience (number of years as a landlord), landlord role (owner or manager), financial role of the rental unit(s) they own and/or manage (primary income, investment, retirement), and property type (number of buildings, size of largest building). Small and large landlords likely differ in their experiences and roles in relation to their rental properties, which may shape their business practices. Previous research suggests that large landlords are more likely to use rental properties for their primary income, in contrast to small landlords who are more likely to own rental properties to supplement their primary income for retirement or investment purposes (Thacher 2008).

Landlord Practices

To investigate claims that small landlords offer housing on better terms to disadvantaged renters, we use survey items that capture landlord business practices affecting low-income and vulnerable tenants, which we define as tenants who use vouchers, have criminal records, or request a disability accommodation. To understand whether landlords serve low-income and vulnerable tenants, we also construct binary indicators from landlord responses about the tenant populations they serve. We include whether the average total household income of tenants is above or equal to $50,000 to reflect the extent to which landlords serve low-income renters. We also use binary measures of whether landlords offered tenancies to applicants who might not meet standard requirements, charged above fair market price for rent, or raised the rent or terminated a tenancy (inclusive of both formal and informal evictions) in the year prior to the survey.

Design

Empirical Description of Parcel Data

We begin by describing how the share of renter-occupied parcels in one- to four-unit structures sold in a given year changed from 2007 to 2020. This step provides a baseline about how the outcome of interest changed in the time before and after the City of Seattle’s passage of the first-in-time and fair chance ordinances for the rental market. We estimate these mean values and 95 percent confidence intervals using an ordinary least squares regression with no covariates for this analysis. The corresponding coefficient table for this model can be found in the Appendix.

DD Analysis

Moving beyond empirical description to identifying the effect of the Seattle rental ordinances on “mom-and-pop” rental properties requires that we impute a trend for what would have happened but for the policy. This counterfactual trend is essential for causal inference on our estimand, in our case, the average treatment effect on the treated (Lundberg, Johnson, and Stewart 2021). Following a substantial literature on quasi-experimental designs for assessing policy impacts, we use a DD design to estimate the effect of the Seattle rental ordinances on landlord exit (Bertrand, Duflo, and Mullainathan 2004; Card and Krueger 2000).

Crucially, DD designs depend on two assumptions for identifying a policy’s effect: parallel trends among the treated and control units and no anticipation of the treatment among untreated units. We follow recent studies in using the multiple periods of pretreatment data to (1) test whether the average treated and control group values differed in years leading up to the rental ordinances and (2) test whether there were anticipatory effects for these policies in years prior to the 2016 passage of first-in-time (Callaway and Sant’Anna 2021; Roth et al. 2023).

Because the laws potentially affected the entire rental market of Seattle at one time, there is no concern about heterogeneity in the timing of treatment across different groups (Goodman-Bacon 2021).

The conventional estimator for DD analysis is referred to as two-way fixed effects regression analysis. This framework depends on netting out unit (α i ) and period-specific (µ t ) effects on the dependent variable through dummy variables, with the coefficient (β) for the interaction of the treatment group and period indicators (Xit) providing insight into the average treatment effect on the treated and a residual term (ε it ) capturing unexplained variation. Our outcome Yit of whether a parcel i occupied by a renter was sold [0,1] in a given period t is accordingly modeled using a linear regression with the following equation:

Standard errors can be biased downward in the presence of serial correlation in panel DD (Bertrand et al. 2004), so we use robust standard errors clustered by parcel to attend to this problem and relax the ordinary least squares assumption of homoscedasticity in errors (Cameron and Miller 2015). 7 Models using standard errors clustered at the city level, rather than the parcel level, produce substantively similar results across our two-period and event study specifications.

Importantly, the model coefficients and their uncertainty provide evidence about measurable anticipation or deviations from parallel trends in pretreatment periods. Significant interaction coefficients in periods prior to the treatment in 2016 are evidence against the assumption of parallel trends. Following Sant’Anna and Zhao (2020), we also conduct supplementary tests (available in the Appendix) for anticipatory effects that would violate the other DD assumption. Here, the year of treatment assignment is set one or two years earlier to test for anticipatory effects prior to the ordinances’ official announcement or enactment dates in 2016 and 2017. We find no evidence of anticipation with up to two additional years of possible treatment, and crucially, continue to observe evidence consistent with the parallel trends assumption in these diagnostic checks.

Regression analysis of Landlord Practices

We first provide a description of landlord characteristics to provide background on the landlords in the survey. Then, we use logistic regressions to test for differences in business practices associated with landlord size. These models adjust for the most common unit size reported by the landlord, the Seattle region the rental property is in, and the financial role of the rental property for the landlord. ZIP codes of rental units were grouped into Seattle regions, with an additional category covering those with units in multiple regions. Predicted values for each regression are reported using estimated marginal means for small and large landlords.

Results

Consumer Data and Parcel Sales

Figure 1 provides estimates for the share of renter-occupied one- to four-unit parcels that were sold in a given year between Seattle and broader King County. Across the pretreatment period (2007–2016), there is support for the parallel trends assumption even under this simple specification. Sales in Seattle and broader King County initially decline in the wake of the Great Recession, followed by a steady increase till about 2013. Through the passage of the first-in-time and fair chance ordinances in 2016 and 2017 and eventual trend end in 2018, Seattle and areas outside of the city limits saw a steady decline in the share of renter-occupied “mom-and-pop” parcels sold. Finally, the last years through 2020 covered within Figure 1 show an uptick that is relatively similar between Seattle and other parts of King County.

Share of one- to four-unit renter-occupied parcels sold each year.

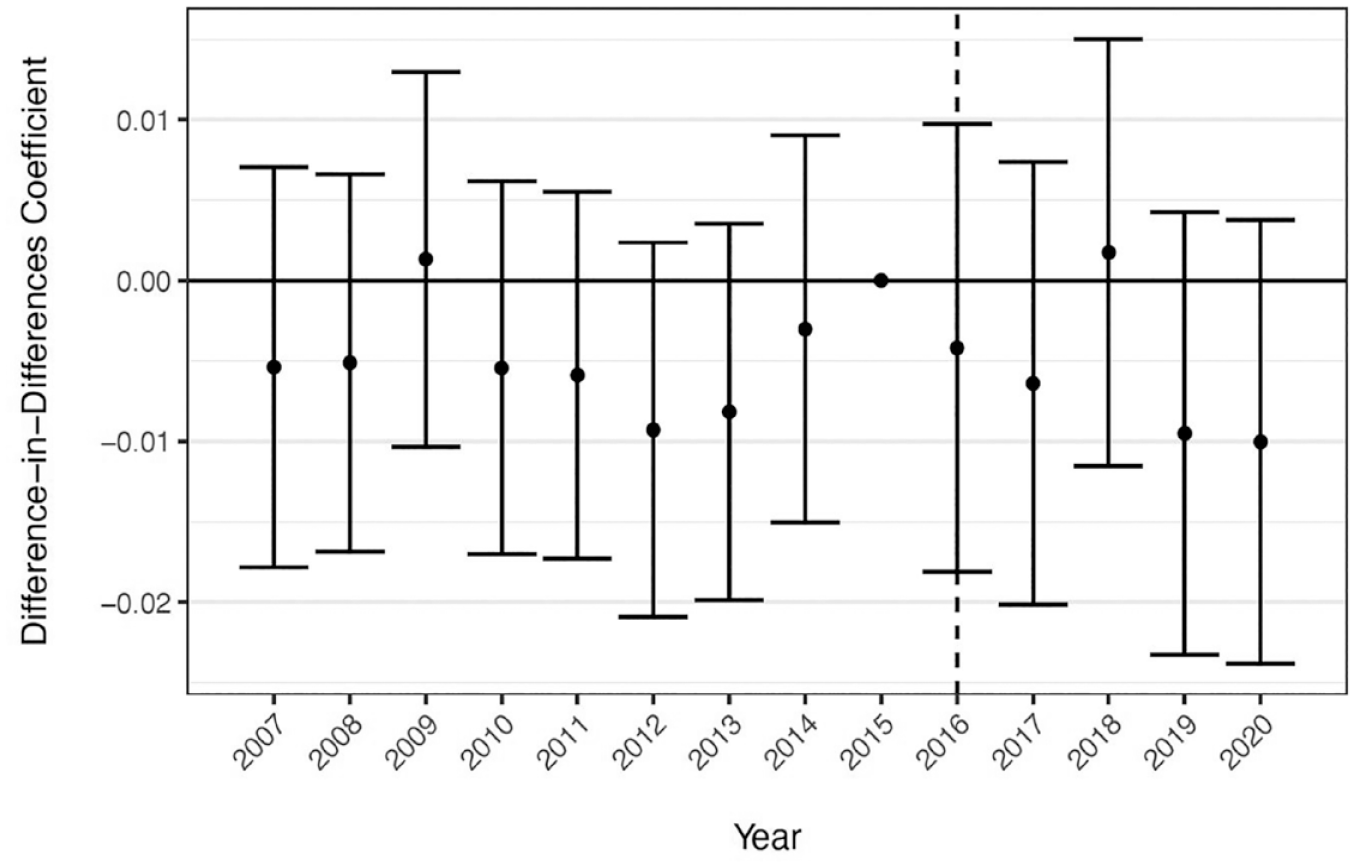

We now turn to results from our DD analysis and consider two specifications for the ordinances’ impact on the rental market in Seattle. First, we use an event study framework test for effects of the local policies on landlord exits on an annual basis. The DD coefficients from this analysis are presented in Figure 2, in which we also display how the results vary across different operational definitions for renters on the basis of the consumer data’s ordinal tenure measure.

Difference-in-differences coefficients for whether a renter-occupied one- to four-unit at t − 1 parcel was sold at t.

Starting with our preferred measure of renter occupancy (four or fewer), all of the pretreatment error bars overlap with the horizontal line around zero and provide evidence in support of the parallel trends assumption for DD analysis. Notably, however, there are no substantial changes in trend for Seattle alone in the posttreatment period starting in 2016, indicating that Seattle and other areas of King County followed essentially similar trends for the outcome of landlord exit in the immediate and intermediate aftermath of first-in-time and fair chance’s passage. Crucially, the other panes of Figure 2 show that under alternative specifications for renter-occupied parcels, in terms of both more conservative and more inclusive approaches, we do not find any substantial difference in the results compared with the preferred renter definition. The most conservative definitions for renter-occupied parcels show minor parallel trends violations in 2008 and/or 2010, but even still, the majority of years leading up the 2016 passage of the Seattle rental ordinances illustrate no significant difference in trend between Seattle and other parts of King County. Equally important, there is no evidence of a posttreatment spike in the probability of sales of renter-occupied “mom-and-pop” parcels in Seattle in the immediate or extended aftermath of the policies enactment. If anything, there is only weak evidence about a potential decline in this outcome in 2018 on the basis of the most conservative definition of renters we consider, a dynamic not captured under any other operational definition for renter-occupied parcels. Among the most inclusive two definitions of a renter-occupied parcel (i.e., tenure values either 5 and 6 or less), we do not find any evidence of significant differences in trends for the outcome across the entirety of the period we observe through our data.

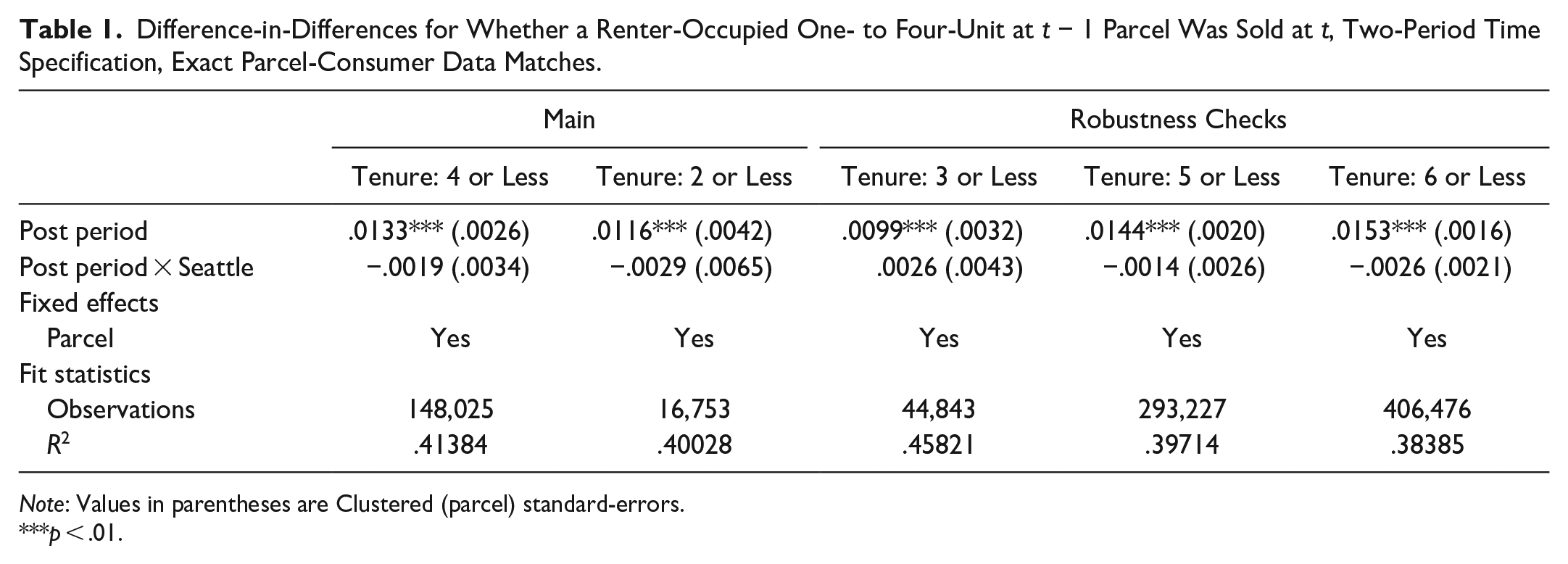

Finally, in Table 1 we present two-period DD to illustrate how even under a specification in which we pool the effects of the policy into a simple pre/post design, we do not find evidence in support of an increase in the rate of “mom-and-pop” rental parcels being sold in Seattle in the time following the first-in-time and fair chance ordinances’ passage. This holds across all operational definitions for renter-occupied parcels that we consider, with results in the Appendix further confirming this with the alternative sample where approximate consumer-parcel data matches are included.

Difference-in-Differences for Whether a Renter-Occupied One- to Four-Unit at t − 1 Parcel Was Sold at t, Two-Period Time Specification, Exact Parcel-Consumer Data Matches.

Note: Values in parentheses are Clustered (parcel) standard-errors.

p < .01.

Landlord Characteristics and Practices

Among the 3,836 landlords surveyed, we find that 76.8 percent of landlords were considered small, per the designation of having four or fewer units. Landlords reported the total number of units they manage or own, and only 14 percent of the 36,192 reported units were owned or managed by small landlords. Nearly all small landlords in the survey (98 percent) either owned or both owned and managed their properties, as did a majority (85 percent) of large landlords (Table 2). Small landlords rarely reported that their rental properties provided their primary income (6 percent), with most responding that properties were investments (68 percent). Relatively few large landlords (34 percent) reported that they derived their primary income from their rental properties. Although respondents had properties in all regions of Seattle, 45 percent of large landlords had properties in multiple regions, compared with only 10 percent of small landlords. Small landlords reported owning more larger units on average for their rental properties than large landlords.

Distributions of Landlord Characteristics Between Seattle Rental Housing Study Respondents Who Own or Manage Small (One to Four Units) and Large (Five or More Units) Properties.

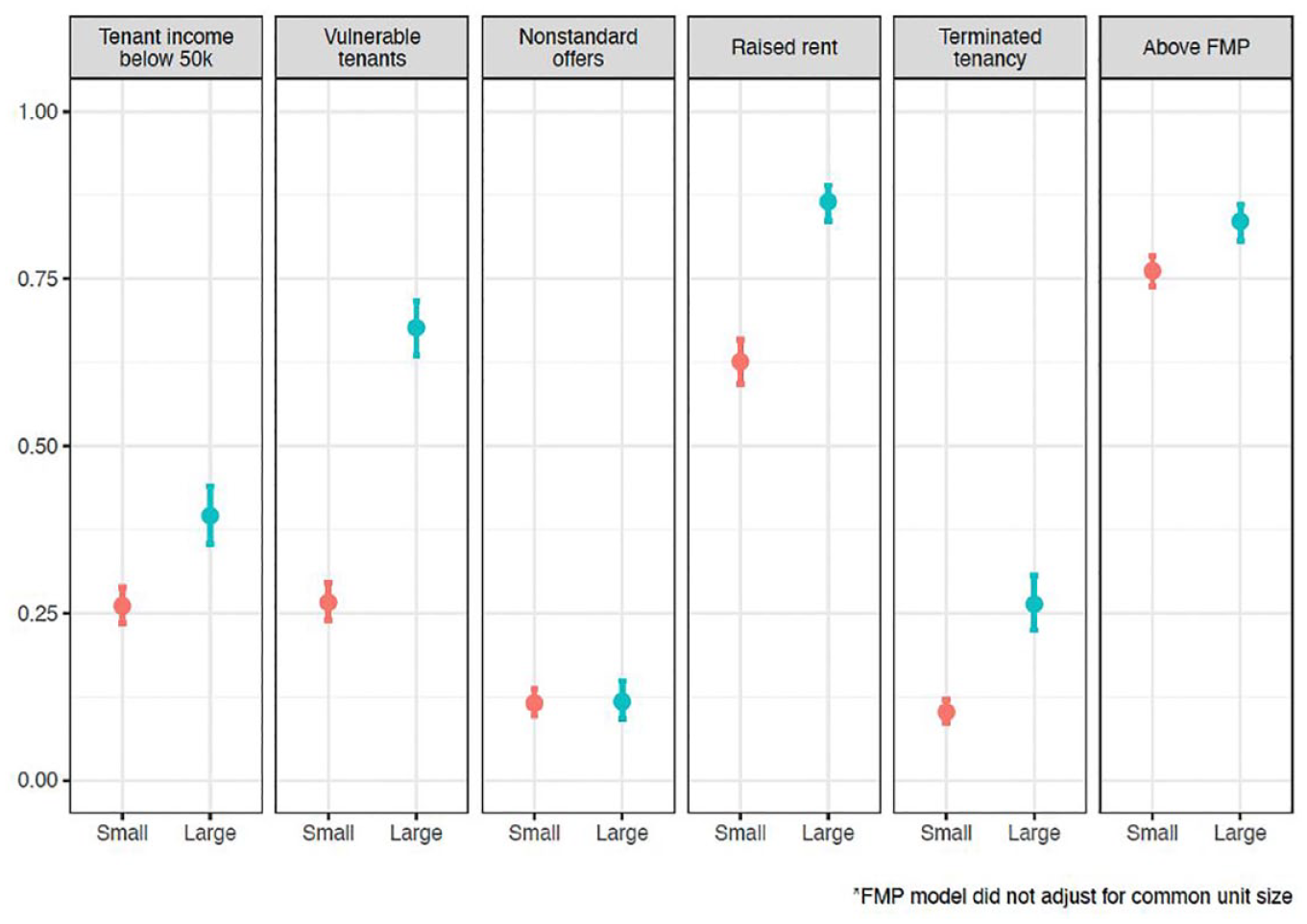

Next, with respect to landlords practices, Figure 3 shows that after adjusting for other landlord characteristics, 40 percent of large landlords reported serving tenants with household incomes below $50,000, in contrast to 26 percent of small landlords. More than two thirds (68 percent) of large landlords, but only about one quarter (27 percent) of small landlords, reported renting to vulnerable tenants. A larger percentage of large landlords may have rented to at least one vulnerable tenant simply because, by definition, they serve more tenants, not because they use policies that are any more friendly to such tenants. Nevertheless, the observed pattern is inconsistent with the popular rhetoric that small landlords are a prime source of housing for tenants requiring special accommodations.

Predicted values for different landlord practices between Seattle Rental Housing Study respondents who own or manage small (one to four units) and large (five or more units) properties.

On the other hand, small landlords were less likely than large landlords to report management practices linked to residential displacement (i.e., charging above fair market rents, raising rents and terminating tenancies). Although the majority of both small and large landlords reported charging above fair market price and raising rents in 2017, small landlords were slightly less likely to report doing so (76 percent vs. 84 percent for large landlords). Twice as many large landlords reported terminating a tenancy in 2017 than small landlords (26 percent and 10 percent respectively). With the exception of nonstandard offers, all practices significantly differed between small and large landlords.

Discussion

Our results suggest that sales of SRPs did not increase following the passage of the Seattle ordinances, even after a period of court limbo ended and both rules’ constitutionality was eventually upheld. This remains true regardless of how we construct our test for impacts of the first-in-time and fair chance ordinances. Furthermore, our analysis suggests that Seattle and surrounding areas followed largely the same trends between the pre- and posttreatment periods. Namely, both parts of the housing market experienced a declining probability of sale of small-scale rental properties through the posttreatment period, a general dynamic inconsistent with the broader narrative about small landlords exiting the market.

Our survey analysis further indicates that landlords of SRPs in Seattle do not neatly fit the theorized expectations of “mom-and-pops” in terms of who they tend to rent to, the affordability of housing they offer, or the flexibility of their practices. Although small-scale landlords in Seattle may be less likely to raise rents and terminate tenancies compared with larger landlords, they nonetheless tend to rent to higher income households more and vulnerable tenants less. Meanwhile, more than three quarters of small and large landlords alike reported charging rents above fair market value. Overall, these results challenge the rhetorical depiction of small landlords as the last bastion of affordable housing for the city’s most vulnerable renters.

In addition to its timely implications for housing policy, our study advances sociological thinking in the areas of housing, law and society, and relational inequality in at least three respects. First, our findings enhance our understanding about how rental ownership characteristics shape management practices and living conditions for tenants. Although a burgeoning literature on the rise of institutional or “Wall Street” landlords has brought attention to the exploitative business practices of such firms, focusing only on this sector may unintentionally cast small-scale or “mom-and-pop” landlords as the foil and help legitimize industry claims about the relative virtuousness of SRPs wielded to oppose regulation. Along with other recent studies (Decker 2021, 2023), our results complicate long-standing assumptions regarding the distinct, and more “tenant-friendly,” management practices of SRP landlords.

Second, our study brings empirical scrutiny to claims deployed by rental industry groups across the country to shape policies governing housing. In addition to undermining specific claims about effects of new tenant protection laws on the small-scale rental sector in Seattle, our findings also challenge accounts of regulatory law in action that invariably assume regulated industries will inevitably act to circumvent protective social policies in ways that pass regulatory costs onto the intended beneficiaries of regulation (i.e., employees, consumers, tenants). Instead, our findings suggest that landlord responses to tenant protection regulation are variable and likely depend on broader features of the market and policy environments in which they operate, either restraining or facilitating the kinds of landlord adaptations to law that have adverse consequences for tenants. In the case of Seattle, those conditions make a wave of either sell-offs by SRP owners or purchases by corporate or institutional investors—outcomes predicted by regulatory opponents—unlikely. 8 Although the responses of small-scale landlords to regulation may differ across tight or slack rental markets, or in response to more or less restrictive policy interventions (e.g., eviction moratoria vs. tenant screening regulations), our analytical approach establishes a model for assessing claims about the impacts of tenant protection policies on the “mom and pop” rental sector across varying policy and market contexts.

Finally, by testing politically salient claims about the purported impacts of rental regulation on small-scale landlords and disadvantaged tenants, this study brings attention to the repercussions of claims-making in the housing context for inequality. Relational inequality theorists argue that claims on power and resources are crucial for enabling two other key mechanisms of relational inequality to be enacted: social closure (i.e., exclusion) and exploitation (Tomaskovic-Devey and Avent-Holt 2019). Research on rental markets and landlords in recent years has greatly expanded our understanding of exploitation (e.g., Desmond 2016; Desmond and Wilmers 2019; Garboden and Rosen 2019) and exclusion (e.g., Faber and Mercier 2022; Rosen et al. 2021) in the housing context. We extend this relational turn in the sociology of housing (Martin 2017) by drawing attention to how landlords not only react to, but shape, the policy environments they operate in. In an era of renewed political contestation over housing policy, empirical research is essential to evaluating claims that can shape the regulatory environment in ways that preserve landlords’ disproportionate market power and allow exploitative and exclusionary rental practices to persist, unimpeded by new legal oversight.

Conclusion

Although our study is novel for several reasons, there are nonetheless limitations to our approach that underscore the need for additional research. First among those is our use of a proxy measure for the behavior of small-scale landlords to test claims about their exodus from Seattle’s rental market. We acknowledge that SRP sales and sales of properties owned by small-scale landlords are distinct phenomena and that our measure may not fully capture salient dynamics in the transactions of rental properties owned by small-scale, “mom and pop” landlords. However, sales of rental properties that are most likely to be owned by small-scale landlords (i.e., one- to four-unit buildings) offer a strong signal of the market activity of such landlords. A second limitation to note is that our consumer data lack a binary tenure measure, requiring us to assess robustness across alternative specifications but leaving unclear how much any strategies may be misclassifying parcels as owner occupied when they are renter occupied and vice versa.

Similarly, although we attend to differences in the geographic representation and property types of different landlords across Seattle in our landlord survey, we acknowledge that the initial sampling frame (i.e., the City of Seattle’s rental registry) itself was not a complete enumeration of the entire population of all landlords. We have endeavored to assess sensitivity to reasonable alternatives but are nonetheless cognizant of how these are sources of lingering fuzziness to our approach.

There are a few distinct future research directions inspired by this study. First, this study highlights the importance of grappling with variation in the practices and policy responses of different types of landlords across the spectrum of housing markets. Although national surveys of landlords reveal the relationship between landlord size and practices such as rent setting and eviction (e.g., Decker 2021, 2023), metropolitan variations in the prevalence, affordability, and renter profiles among different types of landlords, including the emerging presence of institutional investors (Colburn et al. 2021) and increasing formalization among small-scale landlords (Messamore 2023) warrant investigation. The advent of digitized parcel data with comprehensive temporal and spatial coverage may offer new opportunities to investigate these intermetropolitan variations as well as to investigate sensitivity of results to various approaches to identifying “mom-and-pop” landlords. Second, although our survey data provide a unique opportunity to directly assess claims made about the distinct practices of small- and large-scale landlords, future scholarship might fruitfully draw on the perspectives of tenants affected by varying approaches to property management. Methodological advances in identifying rental property ownership (An et al. 2024; Messamore 2023) also offer new opportunities to link data on management practices gleaned from surveys of tenants with information about their landlords, including but beyond portfolio size.

More broadly, this study highlights the need for additional research on the claims-making process itself in the housing context. Scholarship on claims-making in the employment realm helps explain how and why employers’ claims about economic productivity, merit, and compensation were privileged over those of labor during the postwar period, with wide-reaching ramifications for contemporary inequality (Hanley 2022; Tomaskovic-Devey and Avent-Holt 2019). Future research examining the evolution of claims related to rental housing policy, including but not limited to narratives about the impact of regulation on “mom-and-pop” landlords, could draw on insights from cultural sociology to better understand the process by which certain claims are legitimated and privileged over others.

The local industry backlash to the enactment of Seattle’s first-in-time and fair chance ordinances illustrates how new forms of regulatory control over landlord practices prompt discursive strategies about the potential loss of “mom-and-pop” landlords and a corresponding reduction in access to affordable housing within a city. This discourse emerges even when the requisite local evidence about both the loss and the practices of such landlords is unclear or missing altogether. At worst, assumptions about policy impact go unquestioned and produce the desired chilling effect over future efforts to bring fair housing regulations to the rental market.

Concerns about adverse impacts of regulation on the naturally occurring affordable housing supply date back to the advent of modern building codes in the nineteenth century, when policymakers feared that model tenement laws would regulate the slums out of existence (Bauman, Biles, and Szylvian 2000). Such fears often discouraged policymakers from implementing regulatory oversight on private rental markets or aggressively enforcing existing tenant protection laws, particularly at historical moments characterized by extreme shortages of affordable rental housing (Greif 2022; Satter 2009). Given the perennial nature of the affordable housing crisis for poor renters (Bauman et al. 2000) and the near total devolution of responsibility for affordable housing provision to the private rental sector (Goetz 2013), concerns about the unintended consequences of tenant protection laws remain unsurprisingly evergreen in political debates around housing policy. The enduring power of these ideas to shape political discourse should motivate sociologists to interrogate these ideas, lest they become mythology.

Supplemental Material

sj-docx-1-srd-10.1177_23780231241296169 – Supplemental material for “Mom-and-Pop” Landlords and Regulatory Backlash: A Seattle Case Study

Supplemental material, sj-docx-1-srd-10.1177_23780231241296169 for “Mom-and-Pop” Landlords and Regulatory Backlash: A Seattle Case Study by Anna Reosti, Chris Hess, Courtney Allen and Kyle Crowder in Socius

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Support for data access and analyses for this research came from the University of Washington’s Population Health Initiative, the University of Washington’s Student Technology Fee program, the University of Washington’s provost’s office, and a Eunice Kennedy Shriver National Institute of Child Health and Human Development research infrastructure grant (P2C HD042828) to the Center for Studies in Demography and Ecology at the University of Washington. The content is solely the responsibility of the authors and does not necessarily represent the official views of the National Institutes of Health.

Supplemental Material

Supplemental material for this article is available online.

1

Although the term mom-and-pop landlord frequently goes undefined in popular discourse, it is typically used to refer to small-scale landlords who own four or fewer rental units. Existing approaches to defining and operationalizing “mom-and-pop” landlords are discussed in greater depth later in the article.

2

In March 2023, the Ninth Circuit Court of Appeals struck down the component of the “fair chance housing” ordinance banning landlords from asking applicants about their criminal histories but upheld the law’s prohibition on landlords taking adverse action (i.e., rejecting applicants or evicting tenants) on the basis of criminal history information (![]() ).

).

3

Recent estimates suggest that SRPs, including single-family rentals, are still overwhelmingly owned by individual investors with small rental portfolios. A Freddie Mac Multifamily (2018) analysis estimated that 1 percent of the nation’s single-family rental properties are owned by institutional investors, while a report from Moody’s puts that figure at 3 percent (Jabir et al. 2023). Freddie Mac Multifamily also suggested that 88 percent of single-family rentals are owned by “very small” investors, who own 10 or fewer properties. With respect to 1- to 4-unit rental buildings, ![]() , using 2018 Zillow data, estimated that 87 percent of such properties are owned by landlords with 10 or fewer units, and 66 percent are owned by landlords with only 1 or 2 units.

, using 2018 Zillow data, estimated that 87 percent of such properties are owned by landlords with 10 or fewer units, and 66 percent are owned by landlords with only 1 or 2 units.

4

We joined the linked parcel data to Seattle Rental Registration and Inspection Ordinance (RRIO) records from 2018 to inspect how the share of known renter parcels (based on RRIO) changes as we adjust the Data Axle threshold for what is flagged as a renter household. As the tenure threshold is increased from two to six, the share of one- to four-unit parcels flagged as rentals in Data Axle that are also rented on the basis of RRIO increases in turn. Despite this evidence supporting higher values on the tenure scale, we cannot do this check in a time-varying manner or across all of King County and report results using a set of tenure thresholds as a result.

5

We also assessed a contemporaneous measure of parcel tenure and found similar results.

6

We considered weighting our survey sample to the composition of landlords covered in the RRIO registry according to two dimensions, building size and ZIP code of property. However, the RRIO registry does not represent a census of landlords given the timing of when the survey was conducted (relative to the RRIO program’s start date) and the rolling nature of RRIO inspections. We present unweighted estimates as our main findings on the basis of these limitations of RRIO, though such weighting leads to similar results.

7

Although using a linear probability model potentially generates predictions outside the bounds of probability unlike proper models for nonlinear data, the estimation of two-way fixed effects as well as inference on the focal coefficients is complicated by the use of a link function like the logit (Wooldridge 2021). As our results did not substantively differ on the basis of the use of linear compared with logistic regression, we present our main results using linear probability models and include coefficient tables for logistic models in the ![]() .

.

8

High-cost, rapidly appreciating real estate markets such as Seattle’s disincentivize landlords from selling off their properties in response to disfavored policy changes, as property owners in such markets are more likely to treat their properties as long-term investments, an orientation expressed by the majority of small landlords in our survey (see Table 2). In contrast, landlords in more slack and/or distressed rental markets are more financially reliant on regular revenue from rents (Mallach 2007) and consequently may be more reactive to regulatory changes (![]() ).

).

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.