Abstract

This study proposes a multidimensional emissions profile (MEP) framework, aiming to analyze how a broad social force systematically and heterogeneously affects four emission components of nations: (1) emissions generated by domestic-oriented supply chain activities, (2) emissions embodied in imports, (3) emissions embodied in exports, and (4) direct emissions of end-user activities. I implement a multiregional input-output approach to operationalize these emission components. Using the MEP framework and dynamic fixed-effects models with the seemingly unrelated regression estimator, I find these four emission components are heterogeneously related to national affluence in high-income nations. As these nations become even wealthier, affluence is gradually decoupled from emissions generated by domestic-oriented supply chain activities and direct end-user emissions, yet it remains strongly coupled with the other two emission components in distinct ways. The findings demonstrate the MEP framework’s utility and contribute a multidimensional perspective to the debate on the economic development–climate change relationship.

Keywords

Introduction

Global climate change causes a multitude of disastrous impacts on ecosystems and human society (Intergovernmental Panel on Climate Change [IPCC] 2021). The Paris Agreement (United Nations Framework Convention on Climate Change [UNFCCC] 2015) and the Glasgow Climate Pact (UNFCCC 2021) recognize that these impacts can be significantly mitigated by limiting global warming to less than 1.5°C above preindustrial levels, which in turn requires substantial reduction in global greenhouse gases (GHG) emissions by 2030 (IPCC 2018). However, the first global stocktake concluded at the UN Climate Change Conference in Dubai (COP 28) underscores that countries are “not yet collectively on track towards achieving the purpose of the Paris Agreement and its long-term goals” (UNFCCC 2023), leaving much to be desired for national actions on emissions abatement (see also, Allan et al. 2021; United Nations Environment Programme 2021). Driven by the urgent need for climate change mitigation, a rich body of research in environmental sociology and sister disciplines on anthropogenic drivers of GHG emissions is devoted to identifying effective leverage points for emissions abatement at the national level (Dhakal et al. 2022; Dietz 2023; Jorgenson et al. 2019; Rosa and Dietz 2012; Rosa et al. 2015). Informed by theories foundational to environmental sociology, researchers identify national affluence and the closely related economic growth as a major driver of emissions (Jorgenson and Clark 2012; Knight and Schor 2014; Liddle 2015; Thombs and Huang 2019; Wang, Assenova, and Hertwich 2021), making the affluence/emissions nexus a focal point in climate mitigation research, theoretical debate, and policy considerations.

Prior cross-national research has primarily focused on how anthropogenic drivers like national affluence affect the total emission accounts of a nation or related quotient measures that adjust for either the size of population or economy. Two of the most widely used aggregate national emissions accounts are the production-based account (UNFCCC 1997) and the consumption-based account (Davis and Caldeira 2010; Peters and Hertwich 2006, 2008). Although the studies using these emission measures are instrumental in testing theoretically grounded hypotheses and guiding climate policies regarding how broad social forces affect nations’ aggregate emissions, little attention has been paid to the multidimensionality of nations’ emissions.

A nation contributes to global GHG emissions in multiple interconnected yet distinct ways (e.g., Meng et al. 2018), such as emissions generated by domestic production activities, emissions embodied in its imports and exports, and emissions by domestic consumer activities. These emission components carry different implications for the justice and effectiveness of climate mitigation. A broad, economy-wide driving force such as national affluence likely affects these emission components in heterogeneous ways. Which emission component increases the most along with growing affluence, and hence must be prioritized in national climate mitigation plans? Which emission components, if any, have been decoupled from affluence and therefore should be further examined to understand how the mechanisms behind the decoupling can potentially be adapted to other emission components? The answers to these questions not only provide crucial policy insights, but also enable more nuanced theoretical understanding of the economic development-climate change relationship in particular and of human drivers of climate change in general. However, prior research relies on aggregate emission measures that are not well equipped to address these questions.

The present study aims to fill this gap. I first propose an analytical framework named “multidimensional emissions profile” (MEP) that focuses on analyzing how a broad social force systematically and heterogeneously affects four distinct emission components of nations: (1) emissions generated by domestic-oriented supply chain activities (DOSCA), (2) emissions embodied in imports, (3) emissions embodied in exports, and (4) direct emissions of end-user activities. I operationalize these emission components using an environmentally-extended multiregional input-output (EE-MRIO) approach. I then use the MEP framework, dynamic two-way fixed-effects models with the seemingly unrelated regression (SUR) estimator, and a general-to-specific data-driven modeling approach to empirically examine the affluence/emissions nexus for a group of 34 high-income nations for the period of 1995 to 2015, focusing on how affluence is associated with the four emission components in potentially heterogeneous ways. The empirical analysis demonstrates the validity and utility of the MEP framework, and contributes a multidimensional perspective and crucial policy insights to the debate on the economic development–climate change relationship.

The article begins with a review of the cross-national research on human drivers of climate change. Then, I discuss the rationale behind conceptualizing nations’ contributions to global GHG emissions as multidimensional, which is followed by the proposal of the MEP framework and its application to analyzing the affluence/emissions nexus. I present the data and methods before reporting the results. I conclude by discussing how the analyses advance the empirical research and theorization of the affluence/emissions nexus, and how other directions of climate drivers and mitigation research can benefit from the MEP framework.

Human Drivers of Nations’ GHG Emissions

Much of the long-standing sociological research on human drivers of environmental degradation is rooted in the IPAT framework that identifies population (P), affluence (A), and technology (T) as the three main drivers of human impacts (I) on the environment (Dietz and Rosa 1994). The STIRPAT model, or stochastic impacts by regression on population, affluence, and technology, was later developed to overcome the IPAT model’s assumption of proportionality, allowing differences in the three drivers’ estimated influences on the impacts (Dietz 2017; York, Rosa, and Dietz 2003). The STIRPAT model also explicitly conceptualizes the technology factor as a combination of many factors that are not captured by population and affluence.

A rich body of empirical research has applied the STIRPAT approach to identify human drivers of emissions, test hypotheses, and inform policy efforts. Empirically identified drivers include—but are not limited to—affluence (Aslanidis and Iranzo 2009; Jorgenson and Clark 2012; Thombs 2018), population size and structure (Dietz and Rosa 1997; Jorgenson and Clark 2010; York 2007), trade (Huang 2018; Jorgenson 2012; Liddle 2018; Prell and Feng 2016), and militarization (Jorgenson and Clark 2016; Jorgenson et al. 2023), with debates on the magnitude of their elasticities and how the elasticities change over time and across geopolitical or macroeconomic contexts (Dietz 2017; Jorgenson et al. 2019). Another rich body of research, mostly outside of sociology, employs decomposition methods to examine drivers of emissions (Brizga, Feng, and Hubacek 2014; Hubacek et al. 2021; Le Quéré et al. 2019; Su and Ang 2012; Wang and Su 2020; Wood, Neuhoff, et al. 2020; Xu and Dietzenbacher 2014).

Earlier cross-national empirical work relies on production-based accounting (PBA) that attributes emissions to nations based on the location of emissions (UNFCCC 1997). Emission measures based on this approach do not account for the emissions embodied in a nation’s imports, which are generated in other nations. The omission is significant because in the past 25 years, around a quarter of global GHG emissions are embodied in international trade; many high-income nations, in particular, have been net importers of embodied emissions through trading with lower-income nations (Davis, Peters, and Caldeira 2011; Peters, Davis, and Andrew 2012; Peters et al. 2011; Wood, Grubb, et al. 2020). In light of the limitations of PBA, consumption-based accounting (CBA) was proposed, which accounts for all global emissions driven by a nation’s consumption demand (Davis and Caldeira 2010; Peters and Hertwich 2008). It is an important methodological and substantive advancement. Researchers argue that switching from PBA to CBA as the basis for mitigation policymaking can improve both the effectiveness and justice of climate mitigation policies (Peng, Zhang, and Sun 2016; Peters and Hertwich 2006; Steininger et al. 2014, 2016). An increasing number of cross-national studies have used CBA either on its own or in conjunction with PBA (Cohen et al. 2018; Huang and Jorgenson 2018; Hubacek et al. 2021; Knight and Schor 2014; Le Quéré et al. 2019; Liddle 2018). Both PBA and CBA are instrumental in understanding how the magnitude of a nation’s GHG emissions are affected by human drivers. However, drivers research using aggregate emission measures tends to overlook the more nuanced multidimensionality in a nation’s contributions to global emissions.

Multidimensionality in Nations’ Contributions to Global GHG Emissions

I use the term multidimensionality to refer to the characteristic of a nation’s contributions to global emissions as being constituted by multiple components, each with different implications for climate mitigation and justice. These emission components may have heterogeneous relationships with human drivers. GHG are emitted by a multitude of human activities, including fossil fuel combustion in various scenarios, cement production, waste treatment, and livestock industries. These activities can be classified according to a number of schemes, including based on the type of GHG emitted; the type of chemical, biochemical, and biological activities that generate the GHG; the economic sector where such activities belong; and the geographical location where the GHG is emitted. Therefore, a nation’s GHG emitting activities and by extension, its GHG emissions are multidimensional. Of particular interest to this study is the classification of GHG emitting activities based on whether the emissions are generated directly by end-user activities or the rest of supply chain activities, and whether the emissions are embodied in imports, exports, or domestic supply chain activities serving domestic end users (hereafter referred to as domestic-oriented supply chain activities, or DOSCA).

Emissions from End-User Activities and the Rest of Supply Chains

Emissions directly generated by end-user activities and by the rest of supply chains are distinct points of intervention for climate mitigation. Some notable end-user activities that directly generate GHG emissions include driving personal vehicles and using fossil-fuel-based household heaters and power generators. In contrast, the rest of supply chain activities that emit GHGs include fossil fuel combustion that occurs outside of the end use stage, a wide range of noncombustion industrial and agricultural activities, and waste treatment.

At the household or individual level, behaviors like driving directly generate emissions, whereas other behaviors, such as meat consumption, do not generate emissions directly but are implicated in the emissions generated elsewhere in the supply chains of associated goods and services. Different intervention strategies are required to target these two types of behaviors. This is in part due to consumers being unaware of the fossil fuel consumption or emissions embodied in goods and services, which is a cognitive barrier that needs to be overcome before consumer behaviors tied to embodied emissions can be effectively targeted to reduce emissions (Abrahamse et al. 2007; Cohen and Vandenbergh 2012; Stern et al. 2016). In contrast, this barrier is less salient for the emissions that are directly generated by consumer behaviors such as driving. Prior research on household emissions at subnational level has found driving forces such as income have differentiated effects on direct household emissions versus emissions from the rest of supply chains tied to household consumption (e.g., Yuan, Rodrigues, and Behrens 2019).

At the organizational level, mitigating direct emissions of end-user activities is related to business organizations’ roles as providers of consumer goods and services: the offering of products with the technical potential to lower direct end-user emissions (e.g., electric vehicles or vehicles with high fuel efficiency), and marketing campaigns seeking to increase the behavioral plasticity of adopting these products and using them in ways that realize the emission abatement potential (Blumstein and Taylor 2013). In contrast, mitigating emissions from the rest of supply chains requires targeting business organizations’ role as emitters of GHG in conjunction with their role as providers of products (Stern et al. 2016). Notably, business organizations need to reduce the emissions from multiple stages of their business operations (Vandenbergh and Gilligan 2017), such as reducing energy used in workplace and production facilities (Sampei and Aoyagi-Usui 2009; Shinn 2011), and reducing emissions from transportation of goods and personnel. Moreover, business organizations that are consumers and suppliers of intermediate goods and services can also influence the emissions generated by other businesses at the upstream and downstream of supply chains (Dietz 2023), as evident in case studies on housing and construction (Biggart and Lutzenhiser 2007; Janda and Parag 2013; Parag and Janda 2014). As suppliers of consumer goods, businesses can offer products, such as high-efficiency appliances, that help lower consumers’ electricity consumption and ultimately lower the emissions from the electricity sector (as part of the emissions from the rest of supply chains) (Blumstein and Taylor 2013; Brown and Kim 2015). Given the differences between direct end-user emissions and emissions generated by the rest of supply chains, it is likely that they have distinct relationships with broad emission drivers or mitigation measures.

Emissions Embodied in Imports, Exports, and Domestic-Oriented Supply Chain Activities

Emissions from the rest of supply chains can be further decomposed based on whether the emissions are embodied in imports or exports or are generated by DOSCA. Due to global production networks and the proliferation of international trade, the end use stage and the rest of supply chain stages of many goods and services have been increasingly separated across national borders. GHG emissions embodied in international trade account for a substantial share of global emissions (Davis et al. 2011; Grubb et al. 2022; Peters et al. 2012; Wood, Grubb, et al. 2020). The emissions embodied in a nation’s imports are generated by supply chain activities outside of its jurisdiction. The importing nation’s government can only exert indirect influence over these supply chain activities, such as through carbon border adjustments, tariffs, and other regulations over imports, which differs from the more direct regulatory power it has over domestic supply chain activities.

Conversely, domestic supply chain activities serving foreign end users, which generate emissions embodied in a nation’s exports, are subject to the indirect influence of foreign state regulations. Some countries also exempt their export sectors from certain environmental regulations (e.g., Grubb et al. 2022). These differences in regulatory dynamics could mean differentiated mitigation strategies are required for a nation to reduce the emissions embodied in its imports, the emissions embodied in its exports, and the emissions generated by its DOSCA. Prior research finds emissions embodied in exports and in imports change differently over time, and these changes are driven by different factors (e.g., Xu and Dietzenbacher 2014).

The three groups of supply chain activities also have different implications for international climate justice. Based on CBA, the emissions embodied in imports can be viewed as a form of emission displacement from the nations that import and consume the traded goods to the nations that produce and export the goods (Peng et al. 2016; Peters and Hertwich 2006; Steininger et al. 2014, 2016). On the flip side, the emissions embodied in exports can be viewed as the emissions displaced from the importing nations to the exporting nations. In schemes that allocate among nations the responsibility for mitigating the emissions embodied in international trade, the emissions in imports and exports are often redistributed to nations along global supply chains for a more just allocation of the responsibility (e.g., Dietzenbacher, Cazcarro, and Arto 2020; Lenzen et al. 2007; Lenzen and Murray 2010; Marques et al. 2012). Unlike emissions embodied in trade, emissions generated by DOSCA generally do not involve transnational displacements of emissions via trade. In sum, among emissions embodied in imports, emissions embodied in exports, and DOSCA emissions, their distinct implications for climate mitigation and international climate justice allude to potential differences in their relationships with broad human drivers of climate change. Yet these differences in relationship are underexplored.

To be clear, prior studies have broken down nations’ emissions into multiple components and analyzed determinants of individual components. For example, Meng et al. (2018) develop schemes that trace nations’ GHG emissions to multiple global value chain routes and stages. Xu and Dietzenbacher (2014) employ structural decomposition analysis to examine drivers specific to emissions embodied in exports and imports, such as the volume, composition, and emission intensity of trade. Adua, Zhang, and Clark (2021) analyze the effects of renewable energy production and energy efficiency gain on CO2 emissions by various economic sectors at the U.S. state level. However, the research on drivers of climate change, especially within environmental sociology, has paid little attention to how broader, economy-wide driving forces such as national affluence are heterogeneously and systematically related to multiple emission components at the cross-national level. This is in part due to the primary focus on aggregate emission measures such as PBA and CBA in existing empirical studies. In the next section, I outline an analytical framework to fill this gap.

Multidimensional Emissions Profile: An Analytical Framework

I propose a multidimensional emissions profile (MEP) framework, focusing on how a broad anthropogenic force affects four emission components of nations in systematic and potentially heterogeneous ways. Drawing from the interdisciplinary literature summarized in the previous section on distinctions among emission components, the MEP framework situates nations’ contributions to global climate change into four components: (1) emissions generated by DOSCA, (2) emissions embodied in imports, (3) emissions embodied in exports, and (4) direct emissions of end-user activities. 1 Figure 1 presents a conceptual diagram of the MEP framework, including the four emission components and their relationships with PBA and CBA.

Conceptual diagram of the multidimensional emissions profile framework, including the four emission components and their relationships with production-based account and consumption-based account.

The main contribution of the MEP framework is that it enables researchers to explicitly study how the impacts of an economy-wide driver may be unevenly distributed among GHG-emitting activities in the end use stage and other stages of supply chains both within and beyond a nation’s borders, therefore creating avenues for more nuanced and targeted empirical analysis and theorization. Importantly, the MEP framework aims to analyze the four emission components systematically rather than in isolation from one another, in order to better account for and explicate the interconnections among the emission components that are part of complex feedback loops in human-environmental interaction systems (Liu et al. 2007; Ostrom 2010). For example, as I demonstrate in the next section, national affluence’s relationship with each emission component is to be analyzed and understood in the context of how national affluence is related to other emission components. If, for instance, as nations become wealthier, affluence is found to be gradually decoupled from one emission component but increasingly strongly associated with the other three components, the MEP framework allows researchers to more explicitly consider and examine the possibility that growth in affluence may cause an emission transfer from the decoupled component to the other three.

The MEP framework includes emissions embodied in imports and in exports, both of which are important, coexisting ways that a nation contributes to global GHG emissions. Emission accounting methods such as PBA and CBA only account for emissions in either imports or exports but not both to avoid double counting. 2 In contrast, the MEP is not an accounting method. It is primarily concerned with capturing how a nation contributes to global emissions in multiple distinct and interconnected ways. To circumvent the double-counting issue, the MEP does not conceptualize the sum of all four emission components as a nation’s total emissions account or as the emissions that the nation is solely responsible for. The MEP also differs from the literature on net emissions transfer via trade, which generally focuses on the degree to which nations are net importers or net exporters of carbon emissions—quantified based on the differential or ratio between the embodied emissions in nations’ imports and exports (Jakob and Marschinski 2013; Peters et al. 2011; Prell and Sun 2015; Wood, Grubb, et al. 2020).

Application of the MEP Framework to the Affluence/Emissions Nexus

I apply the MEP framework to analyze how national affluence—an economy-wide driver—is associated with the four emission components. The motivation is twofold. First, the analyses are used as a proof of concept for the MEP framework. The heterogeneity across the four emission components in how they are related to affluence, if found, will support the notion of multidimensionality in nations’ contributions to global GHG emissions and in the affluence/emissions relationship.

Second, I situate the analyses within the rich body of sociological and environmental social sciences literature on the affluence/emissions relationship—which has been a major point of contention in the broader drivers research and climate mitigation policymaking—and seek to demonstrate how the MEP framework contributes to the research literature and policy considerations. The theoretical debate on the affluence/emissions relationship can be broadly divided into a group of more critical perspectives and a group of more optimistic perspectives (Fisher and Jorgenson 2019). The more critical perspectives, including the treadmill of production theory and metabolic rift theory, argue that increases in affluence as driven by capital accumulation will maintain a strong association with emissions and that the association may even intensify as the economy grows (Foster 1999; Schnaiberg 1980). This is because the pursuit for profits continuously drives both the adoption of productivity enhancing technology that is increasingly more resource- and energy-intensive, and a constant expansion of the scale of production. Such dynamics elevate the scale of resource consumption, disrupt the global carbon cycle through burning fossil fuels and deforestation, and cannot be curbed by social institutions such as the state or the civil society (Clark and Foster 2009; Foster, Clark, and York 2009, 2010; Gould, Pellow, and Schnaiberg 2004; Schnaiberg and Gould 1994).

In contrast, the more optimistic perspectives, such as ecological modernization theory and reflexive modernization theory, argue that political, technological, and cultural changes associated with an elevated affluence level, including state environmental regulations, renewable energy deployment, energy efficiency improvement, and environmental social movements, can alter the societal composition of consumption enough to counteract the upward pressure on emissions induced by an increased scale of consumption (Beck, Bonss, and Lau 2003; Beck, Giddens, and Lash 1994; Buttel 2000; Grossman and Krueger 1995; Mol 2000; Mol, Spaargaren, and Sonnenfeld 2014).

For both sides of the debate, economic development is theorized to affect nations’ GHG emissions via emission-boosting mechanisms and emission-curbing mechanisms (Rosa and Dietz 2012; Rosa et al. 2015). Whether the emission-curbing mechanisms can outweigh the emission-boosting mechanisms is at the core of the debate on whether economic development will decouple national affluence from GHG emissions. The debate also plays an important role in informing the general direction of mitigation policies and particularly whether some alternative forms of economic development are required to limit global warming to below 1.5°C while improving national affluence (Hickel et al. 2022).

Prior cross-national empirical studies have extensively investigated how national affluence is related to aggregate emission outcomes such as PBA or CBA. The majority of them find positive relationships between affluence and total or per capita GHG emissions (Dietz and Rosa 1997; Dong et al. 2018; Jorgenson and Clark 2012; Knight and Schor 2014; Liddle 2015; Lohwasser, Schaffer, and Brieden 2020; Soener 2019; Thombs 2018; Thombs and Huang 2019; Wang et al. 2021), whereas a smaller number of studies find the relationships to be negative for high-income nations (Dogan and Aslan 2017; Schmalensee, Stoker, and Judson 1998). Prior studies also investigate how the relationships change along with the affluence level by including a quadratic term of affluence in regression models; some find the quadratic term to be positively associated with emissions (Musolesi, Mazzanti, and Zoboli 2010; Pablo-Romero and Sánchez-Braza 2017), and others find negative associations (Franzen and Mader 2016; Jebli and Kahia 2020).

Are the impacts of affluence on aggregate emission outcomes evenly distributed among different emission components, meaning that the affluence/emissions relationships are identical across all components? If the relationships are not identical, which emission component increases the most along with growing affluence, and hence must be prioritized in national climate mitigation plans? Which emission components, if any, have been decoupled with affluence and therefore should be further examined to understand how the mechanisms behind the decoupling can potentially be adapted to other emission components? The answers to these questions not only provide crucial policy insights but also enable more nuanced theoretical understanding of the economic development–climate change relationship in particular, and of human drivers of climate change in general.

I focus on high-income nations in the analysis that follows. This is because prior research finds that the relationships between national affluence and GHG emissions differ substantially across nations at different affluence levels and that if there are nations where growth in affluence is decoupled from emissions, they would most likely be high-income nations (Hubacek et al. 2021; Jebli and Kahia 2020; Jorgenson and Clark 2012; Thombs 2018; Thombs and Huang 2019; Wang and Su 2020). Analyzing high-income nations brings the conceptual focus onto the potential decoupling, which is necessary if nations are to maintain growth in affluence while mitigating climate change. Another reason for focusing on high-income nations is the limited availability of data for non-high-income nations, which is discussed in the following section.

Data and Methods

Dependent Variables

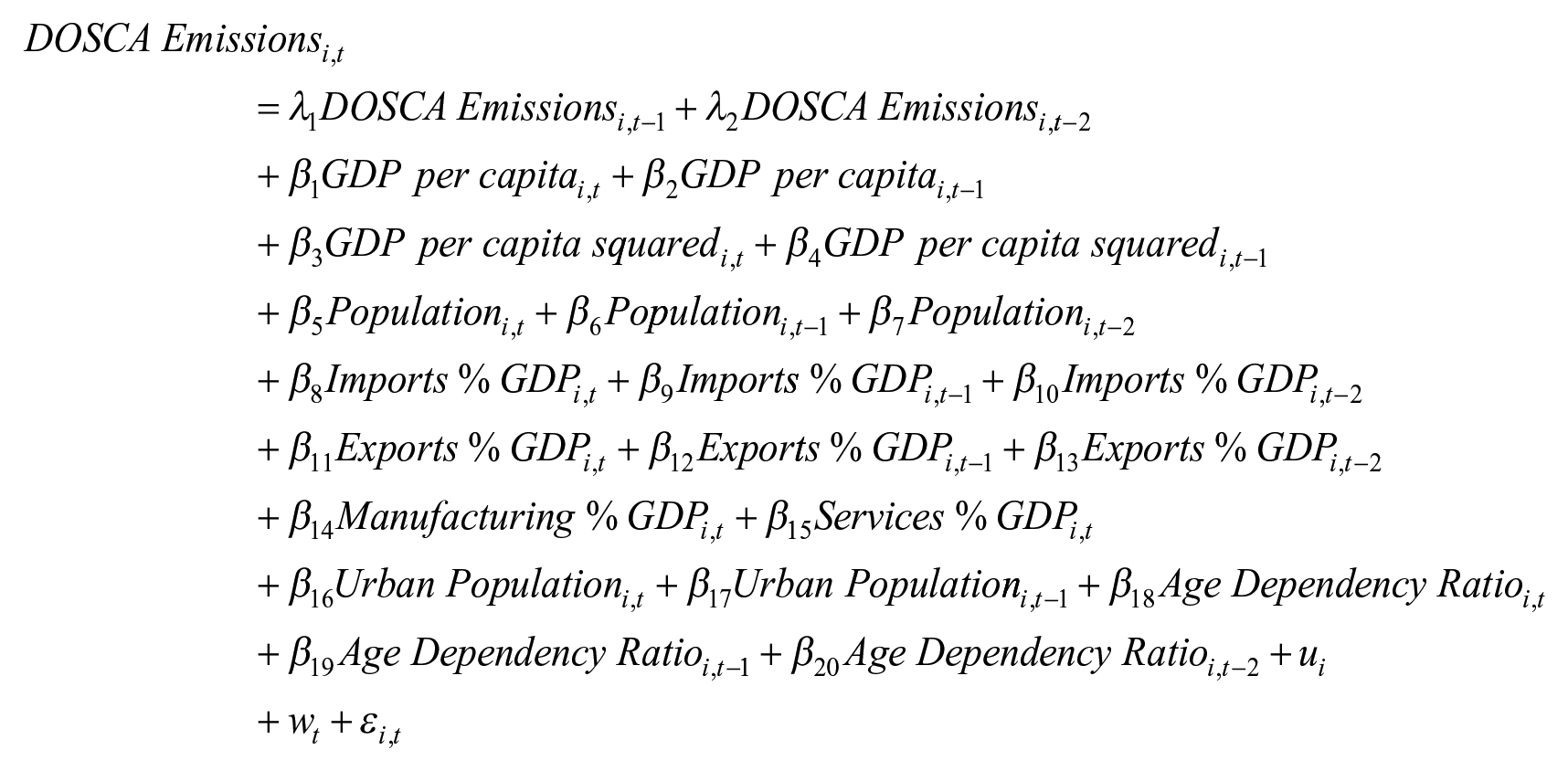

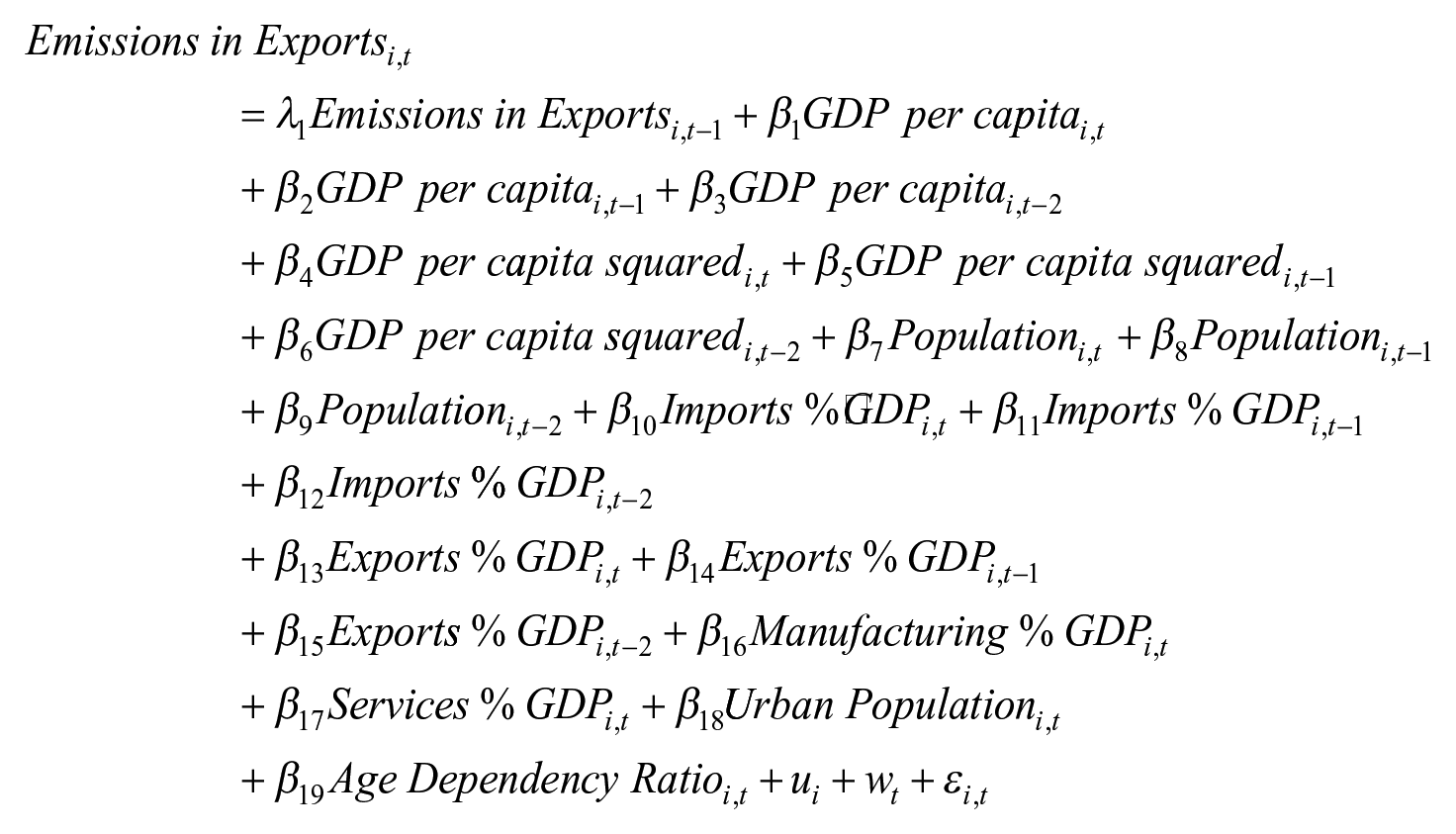

I use panel regression techniques to examine the relationships between nations’ affluence and the four components of their GHG emissions. The four dependent variables are (1) DOSCA emissions, (2) emissions embodied in imports, (3) emissions embodied in exports, and (4) direct emissions of end-user activities, all measured in megaton CO2 equivalents. These emission variables are obtained using the EE-MRIO (environmentally-extended multiregional input-output) method (Miller and Blair 2009) and based on the EE-MRIO tables from the latest version of Exiobase 3 (Stadler et al. 2018, 2021). Prior research has demonstrated that the EE-MRIO method and Exiobase 3 are well suited for analyzing GHG emissions and other environmental impacts of international supply chain activities (Bjelle et al. 2021; Bjørn et al. 2018; Dorninger et al. 2021; Hertwich 2021; Song et al. 2022; Tukker et al. 2016; Wood, Neuhoff, et al. 2020). However, with few exceptions (Prell et al. 2014; Prell and Feng 2016; Prell and Sun 2015), the EE-MRIO method has seen little use in sociology. I use Python package pymrio to parse the EE-MRIO tables (Stadler 2021) and create a matrix with elements representing GHG emissions by 163 harmonized industries in all sampled nations (described in the following) and the rest of the world that are driven by domestic and foreign final demand. To obtain DOSCA emissions, emissions in exports, and emissions in imports of each sampled nation, I add up selective matrix elements based on whether they are driven by domestic or foreign final demand. To obtain direct end-user emissions, I add up the data from Exiobase 3 on the direct emissions by different final demand categories in each nation. Full details of data computation are provided in Supplemental File S1.

Independent Variables

The main independent variable of interest is national affluence operationalized as gross domestic product (GDP) per capita measured in constant 2010 U.S. dollars. To examine whether the association between affluence and emissions varies across different levels of affluence, I also include the squared term of GDP per capita after grand mean-centering.

Additional independent variables are total population, urban population (as a percentage of total population), manufacturing value added (as a percentage of GDP), services value added (as a percentage of GDP), and age dependency ratio (i.e., the population of people younger than 15 or older than 64 as a percentage of the population of those between 15 and 64 years old). These variables are commonly used in research on the anthropogenic drivers of climate change using the STIRPAT approach (Dietz 2017; Jorgenson et al. 2019; Rosa and Dietz 2012). Prior research also includes trade openness, operationalized as the sum of imports and exports (as a percentage of GDP). Given that the dependent variables distinguish the emissions embodied in each nation’s imports and exports, I include imports (as a percentage of GDP) and exports (as a percentage of GDP) as separate independent variables. Data on all independent variables are acquired from the World Bank’s (2022) World Development Indicators Database.

Sample

The overall sample is a balanced panel data set consisting of 714 annual observations for 34 high-income nations in the 21-year period of 1995 to 2015.3,4 The sample includes all nations that have data available for all dependent variables and the main independent variables and are classified as high-income economies by the World Bank. 5 It includes 9 out of the 10 biggest emitters among high-income nations in terms of total production-based CO2 emissions from fossil fuel combustion in 2015. 6 Non-high-income nations are excluded from the sample because Exiobase 3 only provides EE-MRIO data for 9 individual non-high-income nations, whereas other non-high-income nations are grouped into rest-of-world regions. 7 The affluence-emissions relationship differs significantly across national affluence levels (Jorgenson and Clark 2012). Hence, I decide not to include these 9 non-high-income nations in the sample of 34 high-income nations to avoid producing misleading results. Additionally, I decide not to analyze the 9 non-high-income nations as a separate sample because it cannot represent the large and diverse group of non-high-income nations in the world and is smaller than ideal for the modeling techniques used in this study. Notably, although the sample only contains 34 high-income nations, the emission measures of the sampled nations do account for their trade with the rest of the world. For example, Germany’s imports from South Africa are accounted for when calculating the emissions embodied in Germany’s imports even though South Africa is not in the sample. Descriptive statistics of all variables are reported in the Appendix Table A1.

Regression Modeling Techniques and Pre-estimation Tests

I estimate dynamic fixed effects regression models with both time-specific and nation-specific intercepts using Stata 17. I use the SUR (seemingly unrelated regression) estimator to estimate four-equation models with one equation for each dependent variable, which offers several advantages over estimating separate models for the four emission components. First, the SUR estimator is suitable because the four emission components are related with one another via complex processes and feedback loops such as global supply chains and potential carbon leakage mechanisms (Davis et al. 2011; Dietz 2017; Hu et al. 2019; Jarke and Perino 2017; Liu et al. 2007; Peters 2010). The SUR model allows for the error terms of the four equations to be correlated, and therefore better accounts for these potential underlying relationships than models separately estimated for each emission component (Srivastava and Giles 1987). Second, by allowing the error terms to be correlated across equations, the SUR model improves the efficiency in estimating parameters in each equation by using the information from all four equations (Srivastava and Giles 1987). Third, the SUR estimator allows for statistical tests on whether the coefficients for affluence differ across the four emission components.

Two-way fixed effects, estimated by including year and nation dummy variables, account for the unobserved heterogeneity that is unique to each year and affects all nations equally, and the unobserved heterogeneity that is unique to each nation and invariant across the whole period of analysis. I use Stata module sureg to estimate the SUR model, and then use postestimation command suregr by Kolev (2021) to estimate nation-clustered robust standard errors to correct for residual autocorrelation and heteroskedasticity. All nonbinary variables are transformed with natural logarithm, and hence the regression coefficients are elasticity coefficients that represent the percentage change in the dependent variable associated with a 1 percent increase in the independent variables.

Prior literature suggests that changes in national affluence not only contemporaneously affect emissions at the same time point, but also the effect likely persists into the future. For example, York (2012:763) argues that economic growth [at an earlier time point] produces durable goods, such as cars and energy-intensive homes, and infrastructure, such as manufacturing facilities and transportation networks, that are not removed by economic decline [at a later time point] and that continue to contribute to CO2 Emissions even after growth is curtailed (see also, Huang and Jorgenson 2018; York and Light 2017).

Moreover, emission-curbing social changes that are theorized to occur as nations become more affluent, such as state environmental regulations, take time to materialize and can have lasting impacts on emissions beyond the time point when they occur (Mol and Spaargaren 2002). Therefore, a dynamic model is theoretically appropriate for the national affluence-emissions relationship, meaning that the model should include as predictors at least one lag of the dependent variable and potentially lag(s) of the independent variable as well.

However, the prior literature provides little guidance on exactly how affluence’s effect on emissions transpires over time. Indeed, De Boef and Keele (2008) observe that substantive theories in social sciences typically offer limited guidance on how exactly the dynamics should be specified, that is, how many lags of the dependent and independent variables should be included in the model. When theories do not suggest a specific lag structure, identifying the best fitting lag structure using a general-to-specific, data-driven approach has been shown to be a viable alternative that accurately models the true data generating process (De Boef and Keele 2008; Hendry 1995; Hoover and Perez 1999; Plümper and Troeger 2019; Thombs 2022). Adding more lags of the dependent and/or independent variables improves parametric flexibility, and if the lags do belong to the true data generating process, including them can mitigate endogeneity from omitted variable bias and help address residual autocorrelation (Keele and Kelly 2006; Philips n.d.; Pickup 2015). However, adding more lags reduces the degrees of freedom and increases the risk of overfitting. Therefore, using goodness-of-fit metrics that favor parsimony, such as the Bayesian Information Criteria (BIC), is recommended in a general-to-specific, data-driven approach (Philips n.d.).

Based on these theoretical and methodological considerations, I estimate autoregressive distributed lag models, which include lag(s) of dependent and independent variables on the right side of the equation. I use a general-to-specific, data-driven approach and the BIC to identify the best fitting lag structure, which is done separately for each of the four emission components using two-way fixed-effect models (with Stata command xtreg, fe). For each emission component, I start with a general model that includes two lags for the dependent variable and each independent variable. I then loop through all possible model specifications where the number of lags of the dependent variable and each independent variable is individually set to 0, 1, or 2. Adding lags will exclude the earliest years from the sample, causing the sample to vary across models with different lag structures. Therefore, I exclude years 1995 and 1996 in all models to ensure they are estimated based on the same sample, which is important when comparing information criteria across models in the general-to-specific, data-driven approach (Philips n.d.). For each emission component, I identify the model with the smallest BIC statistic (BICmin) and all models with a BIC statistic smaller than BICmin +2. 8 Among them, I select the most parsimonious model specification. If two or more model specifications are equally parsimonious, the one with the smallest BIC is chosen. The statistical significance of the short- and long-run coefficients of GDP per capita squared, together with the BIC, are used to determine whether GDP per capita squared should be included in the model for each emission component; and where it is included, I restrict the lag structure for GDP per capita and GDP per capita squared to be identical.

For the four selected models (one for each emission component), I then conduct the bias-corrected Lagrange multiplier-based test for panel serial correlation (Born and Breitung 2016; Wursten 2018). The models for DOSCA emissions, emissions in exports, and direct end-user emissions have no residual autocorrelation, suggesting that the models approximate the true data generating processes. However, I find residual autocorrelation in the model for emissions in imports, indicating likely omission of lagged independent variables that belong to the true data generating process—an omitted variable bias (Hendry 1995; Pickup 2015; Thombs 2022). I therefore repeat the general-to-specific lag structure selection process for emissions in imports—this time starting with a general model that includes three lags for all independent variables and the dependent variable. The final model for emissions in imports retains all three lags for GDP per capita and age dependency ratio, and passes the test of no residual autocorrelation. Results of the residual autocorrelation tests are reported in Supplemental File S2. Using the aforementioned approach, I identify four different model specifications for the four emission components:

where subscripts i and t represent nation and year, respectively; λs are the autoregressive coefficients;

Correct statistical inference based on the t and F statistics requires an equation balance where both sides of the equation have an I(0) order of integration (Pickup and Kellstedt 2023). To check the equation balance, I conduct multiple unit root tests on all variables (Breitung and Das 2005; Choi 2001; Pesaran 2007; Sangiácomo 2014), and conclude that all dependent variables are stationary and hence I(0), while the independent variables are either stationary or have an I(1) order of integration (i.e., the first-differenced terms are stationary). I then conduct the Kao (1999) panel cointegration tests and find that in each of the four equations, all independent variables cointegrate to produce an I(0) order of integration, therefore achieving an I(0) equation balance. Results of unit root tests and panel cointegration tests are reported in Supplemental File S2. I then estimate a four-equation SUR model based on the selected model specifications. The inclusion of lagged variables means that the data for years 1995, 1996, and 1997 are used as lagged terms only in the SUR model, reducing the sample size to 612 country-year observations.

Results

Figure 2 presents the changes in the four emission components from 1995 to 2015 as a percentage of their respective levels in 1995 for each of the 34 sampled high-income nations. In every nation, the changes vary in magnitude and/or in direction across the emission components, which may indicate that certain human drivers affect the four emission components differently. Comparing across nations, DOSCA emissions increase from 1995 to 2015 in 6 nations and decrease in 28 nations, the emissions embodied in imports increase in 29 nations and decrease in 5, the emissions embodied in exports increase in all nations but the United Kingdom and Romania, and direct emissions of end-user activities increase in 12 nations and decrease in the remaining 22 nations.

Percentage change in four greenhouse gases emission components from 1995 to 2015.

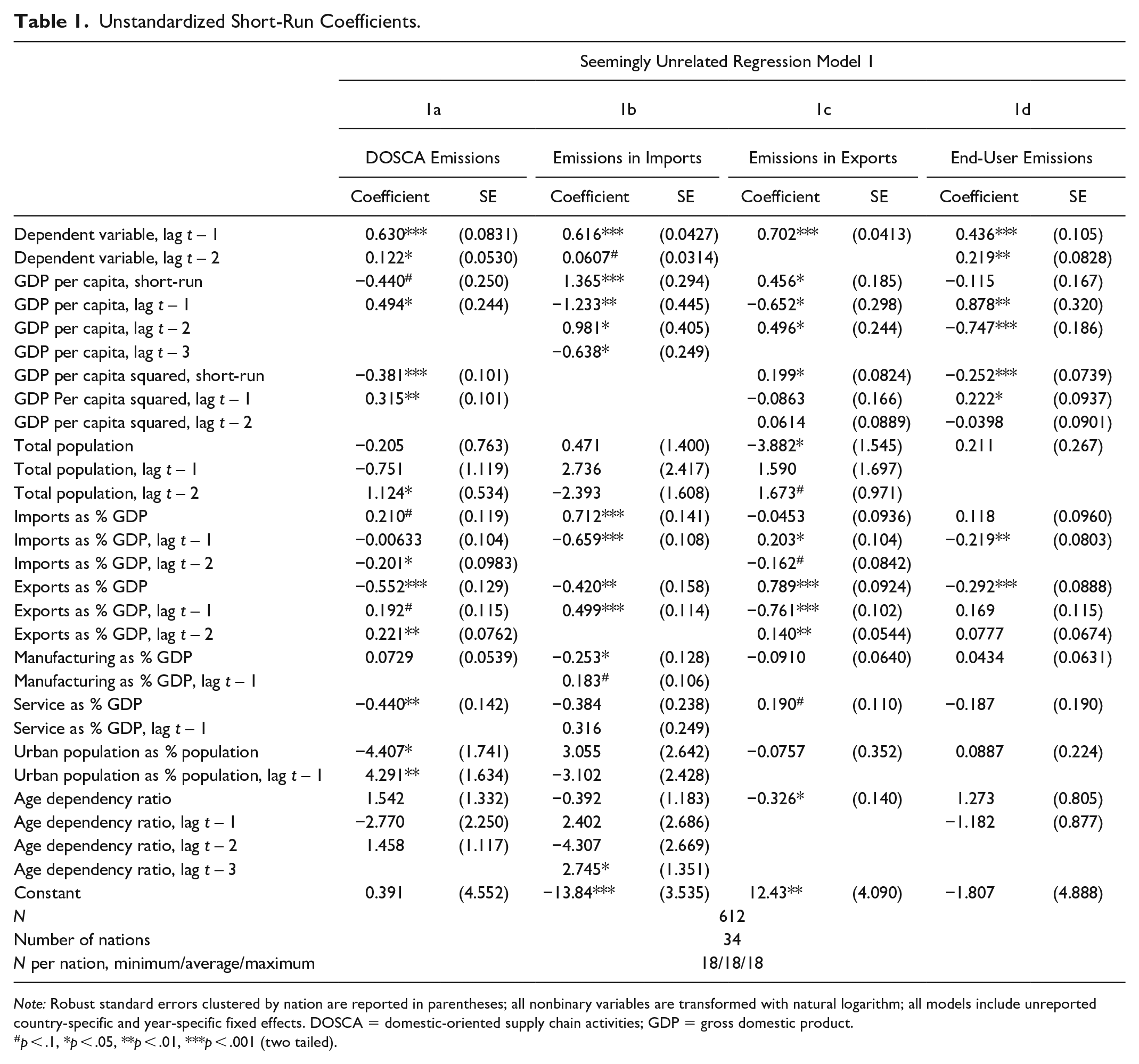

Turning to regression analyses, Table 1 reports the short-run coefficients of Model 1, a four-equation, dynamic two-way fixed-effects model estimated using the SUR estimator. The four equations—labeled as 1a through 1d—each takes a different emission component as the dependent variable. Country-clustered robust standard errors are reported in parentheses, and elasticity coefficients are flagged for statistical significance. The threshold of p < .1 is not considered statistically significant in the analyses and is only marked in the tables to show changes in coefficients’ level of statistical significance across models. The Breusch-Pagan test suggests that error terms of the same observations are correlated across the four equations in Model 1 (χ2 = 58.496, p < .0001), meeting the main assumption of the SUR model (Conniffe 1982; Srivastava and Giles 1987). The SUR estimator also assumes no residual autocorrelation within each equation, which is ensured through the aforementioned general-to-specific model selection process and with the robust standard errors.

Unstandardized Short-Run Coefficients.

Note: Robust standard errors clustered by nation are reported in parentheses; all nonbinary variables are transformed with natural logarithm; all models include unreported country-specific and year-specific fixed effects. DOSCA = domestic-oriented supply chain activities; GDP = gross domestic product.

p < .1, *p < .05, **p < .01, ***p < .001 (two tailed).

The short-run effects of GDP per capita are the changes in the emission components in year t that are associated with a 1 percent increase in GDP per capita in the same year. They are indicated by the coefficients for the contemporaneous terms of GDP per capita and GDP per capita squared. The contemporaneous term of GDP per capita is positively associated with emissions in imports (Equation 1b, p < .001) and emissions in exports (Equation 1c, p < .05) but not significantly associated with DOSCA emissions (Equation 1a) or end-user emissions (Equation 1d). The contemporaneous term of GDP per capita squared is negatively associated with DOSCA emissions (Equation 1a, p < .001) and end-user emissions (Equation 1d, p < .01) and is positively associated with emissions in exports (Equation 1c, p < .05). GDP per capita squared is dropped from the equation for emissions in imports. 9 Joint Wald tests suggest that the coefficients for the contemporaneous terms differ across the emission components for both GDP per capita (χ2 = 23.17, p < .0001) and GDP per capita squared (χ2 = 30.03, p < .0001).

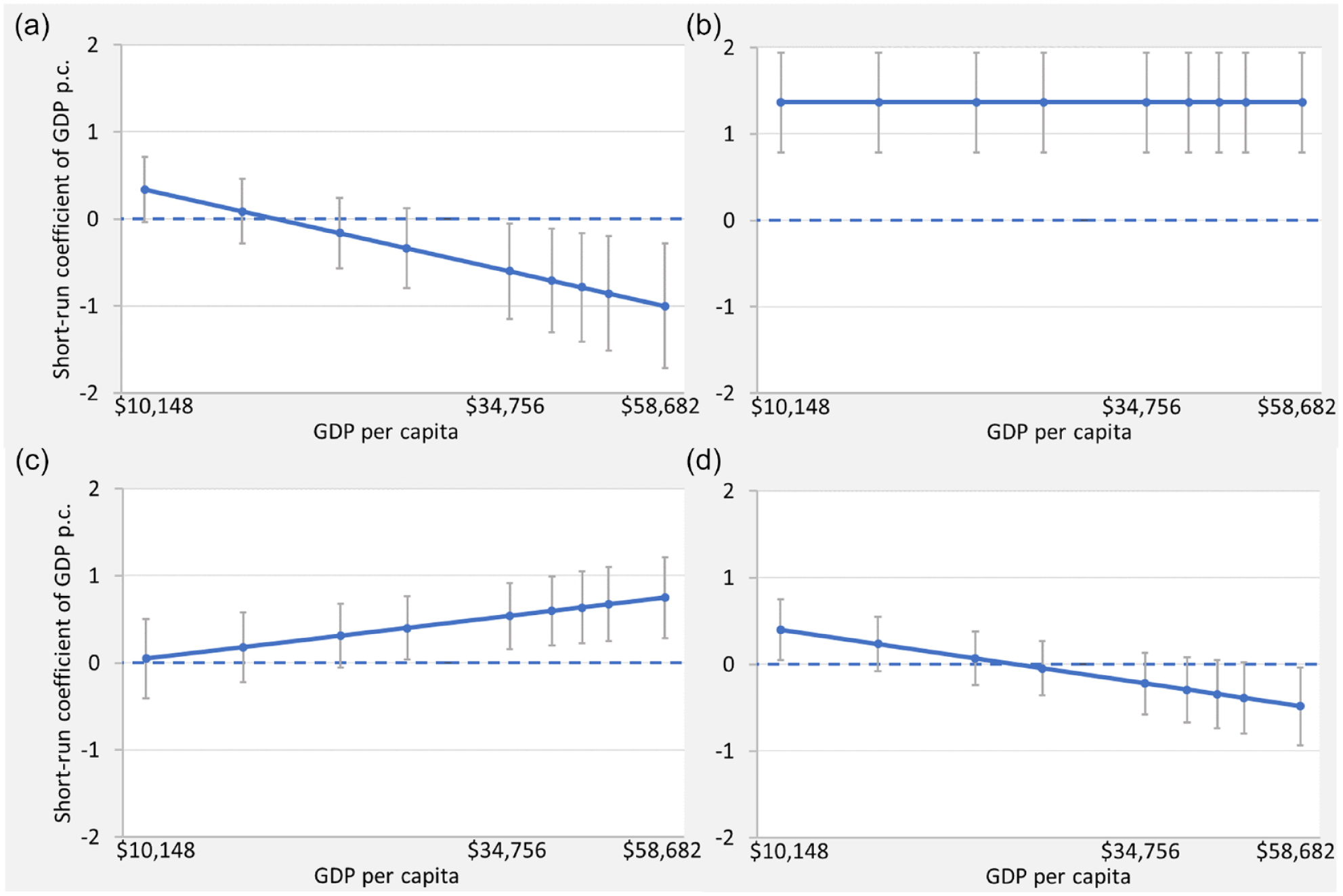

Figure 3 presents the short-run elasticity coefficients of GDP per capita across nine decile points of GDP per capita in the sample, for the four emission components based on Model 1. The 95 percent confidence intervals, illustrated by error bars, indicate whether the elasticity coefficient at each level of GDP per capita is significantly different from 0 (α = .05). Results indicate substantial heterogeneity in how the four emission components are related to affluence in high-income nations. Affluence is not significantly associated with DOSCA emissions when affluence level is at the lower end of the spectrum for high-income nations. As these nations grow wealthier, the association becomes negative and increasingly greater in magnitude. A similar pattern is observed for direct end-user emissions. Its association with affluence changes from positive to negative as high-income nations become even wealthier. In other words, affluence’s short-run relationships with both DOSCA emissions and end-user emissions follow an inverted U-shape curve, and an absolute decoupling of the relationship is observed after affluence reaches certain thresholds. On the contrary, affluence’s relationship with emissions in exports is nonsignificant when the affluence level is relatively low but becomes positive and increasingly greater in magnitude as nations become more affluent. Affluence’s relationship with emissions in imports is positive, linear, and elastic (more than proportional).

Short-run elasticity coefficient of gross domestic product per capita on the four emission components: (a) domestic-oriented supply chain activities, (b) import, (c) export, and (d) end-user.

Turning to the dynamics, the data-driven general-to-specific approach suggests that at least one lag of the emission outcome should be included as a predictor in the equation for each emission component. Additionally, as shown in Table 1, the first lag of every emission outcome is highly significant (p < .001). These results, consistent with the theoretical considerations, suggest that dynamic models are appropriate for modeling the true data generating processes for all four emission components. Table 2 presents the long-run coefficients of GDP per capita based on Model 1, estimated using the nlcom command in Stata. The long-run effects are the total cumulative changes over time from year t onward in the emission components that are associated with a 1 percent increase in GDP per capita in year t. For DOSCA emissions, the long-run coefficient of GDP per capita is nonsignificant, whereas the long-run coefficient of GDP per capita squared is negative (p < .05). For emissions in imports, the long-run coefficient of GDP per capita is positive (p < .001). For emissions in exports, the long-run coefficient for both GDP per capita and GDP per capita squared are positive (p < .001). For direct end-user emissions, the long-run coefficient is nonsignificant for either the level term or the squared term of GDP per capita. Joint Wald tests indicate that the long-run coefficients differ across the emission components for GDP per capita (χ2 = 19.37, p < .0005) and GDP per capita squared (χ2 = 15.50, p < .0005).

Unstandardized Long-Run Coefficients for GDP per Capita.

Note: Robust standard errors clustered by nation are reported in parentheses; all nonbinary variables are transformed with natural logarithm; all models include unreported country-specific and year-specific fixed effects. GDP = gross domestic product; DOSCA = domestic-oriented supply chain activities.

p < .05, ***p < .001 (two tailed).

Figure 4 presents the long-run elasticity coefficients of GDP per capita across the nine decile points of GDP per capita. When the affluence level is relatively low, GDP per capita is positively associated with DOSCA emissions (because the 95 percent confidence interval does not overlap with 0 when GDP per capita is $10,148); the long-run relationship becomes nonsignificant as nations become wealthier, indicative of decoupling. The opposite is observed for emissions in exports. Affluence is not significantly associated with emissions in exports when nations are poorer relative to other high-income nations; yet, as nations become wealthier, the long-run relationship becomes positive and increasingly intensified. Affluence has a positive and elastic linear long-run relationship with emissions in imports. In contrast, the long-run relationship between direct end-user emissions and national affluence is nonsignificant across the nine decile points of GDP per capita. For a nation with a GDP per capita of $10,148 (the 10th percentile), a 1 percent increase in GDP per capita is associated with—in the long run—a 0.765 percent increase in DOSCA emissions and a 1.471 percent increase in emissions in imports; yet it is not significantly associated with emissions in exports or end-user emissions. When the nation’s GDP per capita grows to $58,682 (the 90th percentile), a 1 percent increase in GDP per capita is associated with a 1.471 percent increase in emissions in imports and a 1.857 percent increase in emissions in exports in the long run but is not associated with either DOSCA emissions or end-user emissions.

Long-run elasticity coefficients of gross domestic product per capita on the four emission components: (a) domestic-oriented supply chain activities, (b) import, (c) export, and (d) end-user.

For robustness checks, I conduct the Pesaran (2015) test on weak cross-sectional dependence using the xtcd2 module in Stata (Ditzen 2016). I find that the residuals are weakly cross-sectionally dependent in the equations for DOSCA emissions, emissions in imports, and direct end-user emissions but are strongly cross-sectionally dependent for emissions in exports. Tests on slope homogeneity across nations are conducted using the xthst module (Bersvendsen and Ditzen 2021), revealing significant slope heterogeneity. Despite the existence of slope heterogeneity across nations in all equations and strong cross-sectional dependence in the equation for emissions in exports, a dynamic two-way fixed-effects model is still preferred because it performs better than alternatives, such as dynamic common correlated effects model, when the number of time periods is smaller than 30 (Thombs 2022).

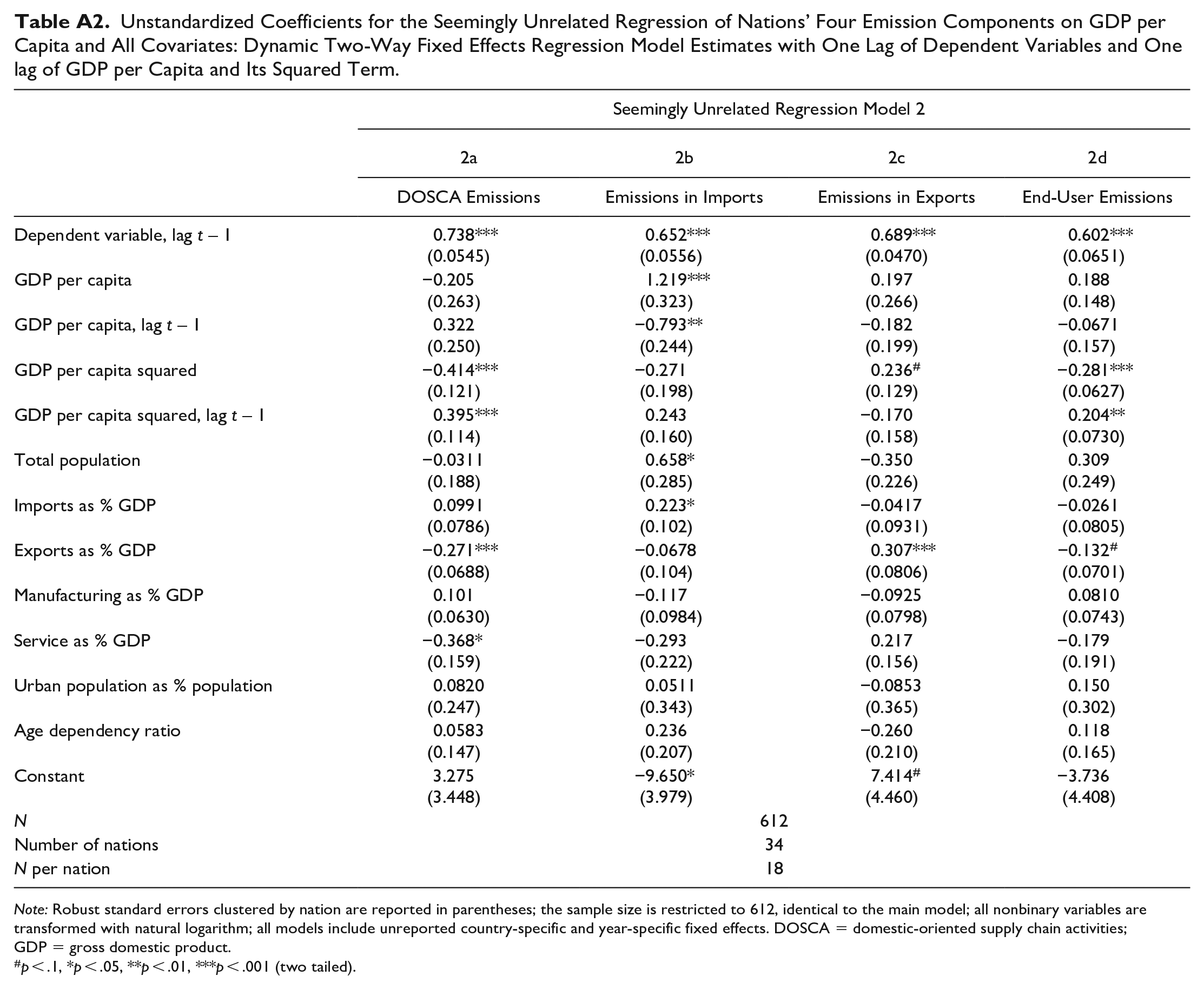

Using a data-driven, general-to-specific approach to derive lag specifications is said to accurately model the true data generating process of the dependent variable (De Boef and Keele 2008; Plümper and Troeger 2019; Thombs 2022). Nonetheless, it raises the question whether the observed heterogeneity across the four emission components is merely due to differences in lag structure. Therefore, I also estimate a seemingly unrelated, dynamic two-way fixed-effects model with identical lag specification for all emission components, as reported in Table A2 in the Appendix. Model 2 has four equations (labeled as 2a through 2d) that each includes one lag for the dependent variable, one lag for GDP per capita and GDP per capita squared, and no lags for other independent variables. The coefficient for GDP per capita is positive for emissions in imports (p < .001) and nonsignificant for other emission components. The coefficient for GDP per capita squared is negative for DOSCA emissions (p < .001) and direct end-user emissions (p < .001), and nonsignificant for emissions in exports (p = .057) and emissions in imports (p = .170). The differences in result between Model 1 (the main model) and Model 2 may be attributed to Model 2 misspecifying the lag structures and inaccurately modeling the true data generating processes (De Boef and Keele 2008; Plümper and Troeger 2019; Thombs 2022; Thombs, Huang, and Fitzgerald 2022). Nonetheless, the main finding stands even when the lag structure is identical across the emission components: The relationships between national affluence and the four GHG emission components are heterogeneous.

Discussion and Conclusion

In environmental sociology and sister disciplines, little attention has been paid to how broader, economy-wide social forces such as national affluence heterogeneously and systematically affect multiple emission components at the cross-national level. This neglect is in part due to the reliance on aggregate emission measures such as PBA and CBA in empirical analysis. Seeking to address the gap, this study proposes the analytical framework of the multidimensional emissions profile (MEP) for a systematic examination of the relationships between social forces and four emission components with distinct implications for climate mitigation and climate justice: (1) emissions generated by domestic-oriented supply chain activities (DOSCA), (2) emissions embodied in imports, (3) emissions embodied in exports, and (4) direct emissions of end-user activities. I apply the MEP framework to empirically analyze the affluence/emissions nexus for high-income nations, in order to demonstrate the validity of the MEP framework and its utility in contributing to the debate on the economic development–climate change relationship—a debate that carries important theoretical and policy implications.

I find substantial heterogeneity across the four emission components in their relationships with national affluence. The data-driven, general-to-specific modeling approach suggests that the true data generating processes of the four emission components are different and best estimated by different model specifications, especially in terms of the lag structure of the dependent variable and GDP per capita, as well as the inclusion of GDP per capita squared and its lag(s). For both short-run and long-run relationships, the estimated relationships between affluence of high-income nations and the four GHG emission components are different in magnitude and how the relationships vary at different levels of affluence, and in some cases, they differ in direction. As high-income nations become even wealthier, affluence is gradually decoupled from DOSCA emissions and direct end-user emissions, yet it maintains a positive and stable relationship with emissions embodied in imports, and its positive relationship with emissions embodied in exports is increasingly intensified. The observed heterogeneity supports the notion of multidimensionality in nations’ contributions to global GHG emissions and in the affluence/emissions nexus, underscoring the validity of the MEP framework.

The results also have substantive implications for the debate on the affluence/emissions nexus. Prior research has theorized and identified both emission-boosting mechanisms and emission-curbing mechanisms through which growth in national affluence affects GHG emissions (Dietz 2017; Fisher and Jorgenson 2019; Rosa and Dietz 2012; Rosa et al. 2015): The more critical theoretical perspectives emphasize that growing affluence elevates the scale of consumption that in turn increases emissions (Foster et al. 2010; Schnaiberg and Gould 1994); the more optimistic perspectives argue that growing affluence may also induce changes that reduce emissions, such as state environmental regulations, environmental social movements, and the development of renewable energy and efficiency-improving technologies (Beck et al. 1994; Mol 2000). The observed heterogeneity in how the four emission components are associated with national affluence underscores the differences in the strength of the emission-boosting mechanisms vis-à-vis emission-curbing mechanisms for each emission component.

For DOSCA emissions and direct end-user emissions, it appears that as high-income nations become even wealthier, the emission-curbing mechanisms grow in strength relative to the emissions-boosting mechanisms and eventually offset the latter. Further increases in national affluence are therefore decoupled from the emissions generated by upstream supply chain activities that fulfill domestic final demand (i.e., DOSCA emissions) and the emissions directly generated by end-user activities, such as driving personal vehicles and household heating that burns fossil fuel onsite. For DOSCA emissions, the decoupling may also be partly explained by ecologically unequal exchange and environmental load displacement processes: High-income nations—occupying more advantageous positions in the global division of labor—are able to offshore polluting supply chain activities that serve their domestic final demand (Bruckner et al. 2023; Givens, Huang, and Jorgenson 2019; Huang 2018; Jorgenson 2012; Roberts and Parks 2007; Shandra, Shor, and London 2009), potentially causing carbon leakage from DOSCA emissions to emissions in imports (e.g., Grubb et al. 2022; Peters 2010). For emissions embodied in exports, the findings show evidence for strong and intensifying emission-boosting mechanisms of growing affluence, whereas the emission-curbing mechanisms are weak and attenuating as nations become wealthier. This is a noteworthy contrast to DOSCA emissions. Even though both DOSCA emissions and emissions in exports are generated by domestic production of goods and services, their relationships with national affluence change in opposite directions as nations become wealthier, likely in part due to the latter being conditioned by foreign final demand and by high-income nations exempting their export sectors from certain environmental regulations in order to maintain competitiveness in the global market (Grubb et al. 2022; Meng et al. 2018).

For emissions embodied in imports, the positive and elastic relationship underscores the sheer magnitude of the emission-boosting mechanisms. In comparison, the emission-curbing mechanisms of growing affluence appear to have little impact on emissions embodied in imports. This may be due to the aforementioned global division of labor where high-income nations offshore polluting industries elsewhere and then import the products back for consumption. This may also be because environmental regulations, social movements, and other emission-curbing mechanisms primarily function domestically and thus have, at best, indirect influence over emissions in imports—which are generated overseas. Although the relationship is strong, its magnitude remains consistent as national affluence continues to grow, suggesting that the offshoring of polluting industries does not necessarily increase in intensity as high-income nations become even wealthier, at least when the volume of imports is controlled for.

In sum, the emission-curbing mechanisms of growing affluence have been more successful in curbing DOSCA emissions and direct end-user emissions but largely remain inadequate in mitigating emissions embodied in imports and exports. While the existing theoretical debate and empirical studies focus on how national affluence affects aggregate GHG emission outcomes, this study finds that the impacts of growing national affluence on emissions are unevenly felt by different components of GHG-emitting activities. As such, this study contributes a novel, multidimensional perspective to the understanding of the economic development–climate change relationship in particular and of human drivers of climate change in general.

This study also generates policy insights. Emissions embodied in imports and exports together account for a substantial and growing portion of high-income nations’ contributions to global GHG emissions. The sum of emissions embodied in imports and exports surpasses the sum of DOSCA emissions and direct end-user emissions in 29 out of the 34 sampled nations in 2015, compared to only 7 nations in 1995. If high-income nations aim to reduce GHG emissions while maintaining growth in affluence, it is imperative for them to achieve absolute decoupling in affluence’s relationships with emissions embodied in both imports and exports. However, absolute decoupling is only observed for DOSCA emissions and direct end-user emissions. Therefore, the findings underscore the importance for high-income nations to shift the focus of their climate mitigation policy agenda to emissions embodied in both imports and exports.

To this end, the present study highlights an important avenue for research and policy considerations: How can the absolute decoupling between national affluence and both DOSCA emissions and direct end-user emissions be replicated to emissions embodied in imports and exports? Specifically, what are the mechanisms accompanying growing affluence that contribute to the decoupling? To what extent do these mechanisms contribute to the decoupling between affluence and CBA or PBA observed in prior research (Hubacek et al. 2021; Longhofer and Jorgenson 2017; Wang and Su 2020)? Whether and how can these mechanisms be incorporated into existent and emerging policy instruments targeting emissions embodied in trade, such as supply chain contracting carbon requirements (Peterson and Whitaker 2022; Zu, Chen, and Fan 2018), carbon border adjustments (Eicke et al. 2021; Marcu, Mehling, and Cosbey 2020), and product carbon footprint labeling (Taufique et al. 2022)?

This study is not without its limitations. First, although the findings are indicative of differences in mechanisms that link national affluence to each of the emission components, this study does not explicitly identify or model those specific mechanisms. Future research can further examine the mechanisms by using the MEP framework together with mediation and moderation analyses, as well as case studies. Second, this study estimates dynamic models for all four emission components, which is both theoretically appropriate and empirically validated by the data-driven, general-to-specific approach. However, the specific lag structures are determined by the data-driven approach due to the limited theoretical guidance on exactly how affluence’s effects on emissions are distributed over time. Although the data-driven approach is a viable alternative when the theorization of specific lag structure is lacking (De Boef and Keele 2008; Hendry 1995; Hoover and Perez 1999; Plümper and Troeger 2019), it does not supersede theories. Therefore, while the lag structures identified in this study advance the understanding of the dynamics of the national affluence/emissions nexus, more research is needed to further theorize exactly how the long-run effects of national affluence on emissions transpire over time. Moreover, as data become available for a longer period, future studies can further unpack the long-run temporal dynamics using statistical techniques that better account for strong cross-sectional dependence and slope heterogeneity across nations. Third, the present study, as a proof of concept for the MEP framework, only focuses on a sample of high-income nations, for which a decoupling between economic growth and aggregate emission accounts is theorized and observed in previous studies. It is important for future studies to apply the MEP framework to examine the multidimensional affluence/emissions nexus for nations in the Global South as data availability and cross-national comparability continue to improve. Additionally, the MEP framework can be further utilized to examine how other broad human drivers and mitigation measures systematically affect the four emission components in potentially heterogeneous ways. Which emission components are more (or less) effectively curbed by a certain mitigation measure? Did the mitigation measure inadvertently cause some emission components to increase due to carbon leakage? The MEP framework can address these questions, contributing to the empirical analyses, theory building, and policy considerations on climate change mitigation.

Supplemental Material

sj-pdf-1-srd-10.1177_23780231241238962 – Supplemental material for Not All Emissions Are Created Equal: Multidimensionality in Nations’ Greenhouse Gas Emissions and the Affluence/Emissions Nexus

Supplemental material, sj-pdf-1-srd-10.1177_23780231241238962 for Not All Emissions Are Created Equal: Multidimensionality in Nations’ Greenhouse Gas Emissions and the Affluence/Emissions Nexus by Xiaorui Huang in Socius

Supplemental Material

sj-pdf-2-srd-10.1177_23780231241238962 – Supplemental material for Not All Emissions Are Created Equal: Multidimensionality in Nations’ Greenhouse Gas Emissions and the Affluence/Emissions Nexus

Supplemental material, sj-pdf-2-srd-10.1177_23780231241238962 for Not All Emissions Are Created Equal: Multidimensionality in Nations’ Greenhouse Gas Emissions and the Affluence/Emissions Nexus by Xiaorui Huang in Socius

Footnotes

Appendices

Unstandardized Coefficients for the Seemingly Unrelated Regression of Nations’ Four Emission Components on GDP per Capita and All Covariates: Dynamic Two-Way Fixed Effects Regression Model Estimates with One Lag of Dependent Variables and One lag of GDP per Capita and Its Squared Term.

| Seemingly Unrelated Regression Model 2 | ||||

|---|---|---|---|---|

| 2a | 2b | 2c | 2d | |

| DOSCA Emissions | Emissions in Imports | Emissions in Exports | End-User Emissions | |

| Dependent variable, lag t – 1 | 0.738***

(0.0545) |

0.652***

(0.0556) |

0.689***

(0.0470) |

0.602***

(0.0651) |

| GDP per capita | −0.205 (0.263) |

1.219***

(0.323) |

0.197 (0.266) |

0.188 (0.148) |

| GDP per capita, lag t – 1 | 0.322 (0.250) |

−0.793**

(0.244) |

−0.182 (0.199) |

−0.0671 (0.157) |

| GDP per capita squared | −0.414***

(0.121) |

−0.271 (0.198) |

0.236

#

(0.129) |

−0.281***

(0.0627) |

| GDP per capita squared, lag t – 1 | 0.395***

(0.114) |

0.243 (0.160) |

−0.170 (0.158) |

0.204**

(0.0730) |

| Total population | −0.0311 (0.188) |

0.658*

(0.285) |

−0.350 (0.226) |

0.309 (0.249) |

| Imports as % GDP | 0.0991 (0.0786) |

0.223*

(0.102) |

−0.0417 (0.0931) |

−0.0261 (0.0805) |

| Exports as % GDP | −0.271***

(0.0688) |

−0.0678 (0.104) |

0.307***

(0.0806) |

−0.132

#

(0.0701) |

| Manufacturing as % GDP | 0.101 (0.0630) |

−0.117 (0.0984) |

−0.0925 (0.0798) |

0.0810 (0.0743) |

| Service as % GDP | −0.368*

(0.159) |

−0.293 (0.222) |

0.217 (0.156) |

−0.179 (0.191) |

| Urban population as % population | 0.0820 (0.247) |

0.0511 (0.343) |

−0.0853 (0.365) |

0.150 (0.302) |

| Age dependency ratio | 0.0583 (0.147) |

0.236 (0.207) |

−0.260 (0.210) |

0.118 (0.165) |

| Constant | 3.275 (3.448) |

−9.650*

(3.979) |

7.414

#

(4.460) |

−3.736 (4.408) |

| N | 612 | |||

| Number of nations | 34 | |||

| N per nation | 18 | |||

Note: Robust standard errors clustered by nation are reported in parentheses; the sample size is restricted to 612, identical to the main model; all nonbinary variables are transformed with natural logarithm; all models include unreported country-specific and year-specific fixed effects. DOSCA = domestic-oriented supply chain activities; GDP = gross domestic product.

p < .1, *p < .05, **p < .01, ***p < .001 (two tailed).

Acknowledgements

I would like to thank Andrew Jorgenson, Juliet Schor, Ryan Thombs, and the Environmental Sociology Working Group at Boston College for helpful feedback and comments on the article. I would like to thank the anonymous reviewers at Socius for their insights on improving this work. I would also like to thank Richard Wood and Arkaitz Usubiaga Liaño for helpful feedback on multiregional input-output analysis. A previous version of this article was presented at the annual conference of the Eastern Sociological Society in 2023.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Drexel University Faculty Start-Up Fund.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biography

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.