Abstract

As policymakers grapple with whether or not to forgive student debt, for who, and how much, it is important to explore how student debt forgiveness would relate to intended household decisions and behaviors. We conducted a survey experiment that asked participants with student debt to imagine a scenario in which the federal government forgave a certain amount of student debt. We then had these participants report on how this would affect their decisions and behaviors. A total of 1,053 participants were randomly assigned to one of four conditions that featured different levels of student debt forgiveness. Our results indicate that student debt is strongly influencing intended decisions and behaviors that can have large implications for household economic stability (e.g., emergency savings) and social mobility (e.g., saving for a down payment on a home). These results also demonstrate that the amount of student debt forgiveness matters.

According to a recent report from the Federal Reserve, the national student debt amount in the third quarter of 2023 was over $1.7 trillion spread across over 43 million borrowers (Board of Governors of the Federal Reserve System, 2023). At the same time, roughly four million student loans enter default each year—affecting millions of borrowers and their families (Hanson 2023). Student debt has been associated with individual hardships such as bankruptcy (Gicheva and Thompson 2015), financial distress (Archuleta, Dale, and Spann 2013; Despard et al. 2016), lower rates of homeownership (Mezza et al. 2015), strains in family relationships (Stivers and Popp Berman 2020), and even delays in family formation (Bozick and Estacion 2014). However, the effects of student debt are not only experienced by the individuals who have incurred it. Rather, the effects of student debt are experienced by nonborrowers as well. For example, Bahadir and Gicheva (2019) found that higher student-debt-to-income ratios caused a reduction in state-level consumption. Moreover, the burgeoning student debt crisis has been associated with increases in the racial wealth gap (Percheski and Gibson-Davis 2020), and when considering the influence of parent’s education level on children’s student loan repayments, student debt can be seen as a limit to the meritocratic power of higher education (Oh 2022). Thus, given the size and breadth of student debt holding, the burdens it can have on individuals and communities, and the potential to address student loan burdens through executive—rather than legislative—action (Minsky 2022), student debt forgiveness has received increasing attention from policymakers, the media, researchers, and advocacy groups in recent years.

When considering how much to forgive, policymakers typically focus on universal forgiveness amounts. For example, in presidential runs, then candidate Joseph Biden originally called for $10,000 in student debt forgiveness, whereas others, such as Senator Warren, have called for as much as $50,000 in debt forgiveness. More progressive members of Congress have even called for total debt forgiveness, which would represent a larger amount of spending than the cumulative spending on unemployment insurance over the last 20 years (Looney 2021). However, it is also worth noting that total debt forgiveness is currently available for the Public Student Loan Forgiveness program, which has recently expanded eligibility through a temporary waiver period. In a recent poll from the Center for Responsible Lending, 63 percent of respondents supported permanently reducing student loan debt by $20,000, suggesting that some of the policy propositions in play do have broad support across the population (Barnard 2020). In addition to universal proposals, policymakers have also proposed plans that differentiate between the types of loan borrower (e.g., Pell Grant vs. non-Pell Grant) and plans that have income caps. Most recently, President Biden has signed a bill that provides partial and conditional forgiveness: up to $20,000 in federal student loan forgiveness for Pell Grant borrowers and up to $10,000 for all other borrowers earning less than $125,000. However, the legality of this plan was recently struck down by the U.S. Supreme Court in June 2023. In a six to three decision, conservative justices ruled that the Biden administration did not have the authority to cancel or reduce student loan debt, stating that these decisions must be directly authorized by Congress (de Vogue and Sneed 2023). The administration is currently pursuing other options to reduce the burden of student debt.

Thus, as policymakers grapple with whether or not to forgive student debt, for whom to forgive it, and how much to forgive, it is important to explore how student debt forgiveness would relate to household decisions and behaviors, as well as how these decisions may be affected by student debt and income levels. We therefore ask the following research questions:

Research Question 1: What behavior changes would households report in response to student debt forgiveness?

Research Question 2: How would varying levels of student debt forgiveness affect household behaviors related to economic stability, social mobility, and quality of life?

Research Question 3: Would responses to student debt forgiveness vary across borrowers’ student debt and income levels?

Answering these questions will allow policymakers to understand what types of burdens would be relieved and what types of opportunities might be pursued in the absence of student debt. This also helps contextualize student debt forgiveness within a broader array of policy options aimed at relieving economic hardships.

With few opportunities to leverage natural experiments on debt forgiveness, we conducted a survey experiment aimed at understanding student debt holders’ sensitivity to different levels of student debt forgiveness. In this experiment, which was embedded in a national survey conducted during the COVID-19 pandemic, we asked participants with student debt to imagine a scenario in which the federal government forgave a certain amount of student debt. We then had these participants report on how this would affect their behavioral intentions across an array of consumption, savings, employment, and family formation behaviors. A total of 1,053 participants were randomly assigned to one of four conditions that featured different levels of student debt forgiveness: $5,000, $10,000, $20,000, and all student debt forgiven. Participants could then select different behaviors they expected to undertake if their student debt were forgiven. The response options were intended to capture a wide range of experiences, such as working less, changing purchasing behaviors, having children or getting married, saving for different purposes, or returning to school.

Our results demonstrate how extensively student debt affects debt holders’ intentions. Specifically, responses to the experiment indicate that respondents perceive that their student debt is influencing behaviors that can have large implications for household economic stability (e.g., emergency savings) and mobility (e.g., saving for a down payment on a home). These results also demonstrate that the amount of student debt forgiveness matters. In particular, setting a student debt forgiveness target too low may not lead to broad-based changes in households’ economic behaviors.

Finally, when considering that larger amounts of student debt and household income may be associated with different financial circumstances, we recognize that the association between debt relief and behaviors may vary across levels of student debt and income. Thus, we interact the treatments with the actual amount of student debt held by individuals and their household income. Here, we find that the proportion of student debt forgiven and the income of the borrower alter the relationships between the amount of debt forgiven and intended behaviors.

Framing Student Debt Forgiveness

Equity and Fairness

Proponents in favor of student debt forgiveness suggest that cancellation could have net benefits for both individuals and the communities in which they live. Recent empirical research and economic models associate student debt forgiveness with increased geographic mobility, income, and GDP and decreased unemployment (DiMaggio, Kalda, and Yao 2019; Fullwiler et al. 2018). Proponents also suggest that student debt forgiveness could also help close the racial wealth gap given that Black borrowers tend to have both higher levels of debt and higher rates of default than White borrowers (The Institute for College Access & Success 2020). Whereas student loans purportedly offer avenues for educational attainment and income growth for low-income Black students, the debt risk carries very different returns for these borrowers. For example, Black borrowers are at greater risk of “predatory” student debt, such as private loans offering less favorable loan terms due to lower income and wealth; are more likely to attend for-profit colleges; and have lower college completion rates (Seamster and Charron-Chénier 2017). Black, Latinx, and Asian students have also been found to have higher debt-to-income ratios when compared to White students (Baker 2019), which can strain household finances and limit asset accumulation. Here, debt forgiveness is not only about relieving hardships but also about removing barriers to wealth accumulation (Hamilton and Zewde 2020).

However, some economic models, such as those offered by Catherine and Yannelis (2021), suggest that the loan balances of low-income individuals can actually overstate the value of future payments and that other options, such as income-driven repayment plans that often require no payments from low-income households, would be the least expensive and the most progressive policy option. The progressivity of this approach would further increase if policymakers took steps to reduce enrollment barriers (see Mueller and Yannelis 2019a). Skeptics of student loan forgiveness also argue that forgiving debt may cause a moral hazard for future borrowers, who may expect their debt to be forgiven, while also incentivizing higher education institutions to further increase prices without repercussions from consumers (see Cooper 2019). Furthermore, skeptics often argue that these student debt forgiveness plans tend to be unfair because the breaks do not apply to previous debt holders who have paid off their student loans (Baum 2020).

Enlightened and Credentialed Societies

Moreover, the conversations around student debt forgiveness not only focus on if student debt should be forgiven but also who should get their student debt forgiven and how much should be forgiven. When considering who should get their student debt forgiven, two core perspectives emerge, each with their own set of philosophical underpinnings. Those in favor of universal debt forgiveness tend to see higher education as a public good that should be financed in the same way that K–12 education is financed. Those embracing this “Enlightened Society” perspective (see Bokat-Lindell 2021)—where all individuals have the freedom to pursue higher education without repercussion—tend to see fewer distinctions between better- and worse-off borrowers because higher education should be free for all. Forgiving existing student debt is often seen as the first step toward this vision.

Conversely, those in favor of targeted debt forgiveness tend to see loan cancellation as a way to address economic injustices for worse-off borrowers. Stemming from a “Credentialed Society” perspective (Bokat-Lindell 2021)—where workers buy more education to qualify for the same jobs despite stagnant wages and rising costs (Collins 1979)—higher education is seen as having heterogeneous effects. For some, the benefits of higher education far outweigh the costs (e.g., increased earnings outpace debt payments); for others, the inverse is true—especially when considering those who are not able to graduate or those with “non-degreed debt” (see Jabbari et al. 2023). Those in favor of targeted debt relief also point out the importance of understanding who owes what. For example, households in the top 40 percent of income hold almost 60 percent of the total debt (Baum and Looney 2020). These households also make 75 percent of all student debt payments. Alternatively, households in the bottom 40 percent of income only hold 20 percent of the outstanding debt and make just 10 percent of all payments. At the same time, households with graduate degrees owed nearly half of all student debt in 2016. Because those who owe the most tend to have the highest incomes and lowest rates of default, proponents of targeted approaches argue that these individuals are not in need of debt forgiveness. Because universal approaches tend to be more expensive, proponents of targeted approaches also note fiscal trade-offs because the money used to pay off the “luxuries” of higher earners could instead be used to help lower earners meet basic needs, such as food and housing. To better understand the implications of debt forgiveness, we review the research on student debt, student debt forgiveness, and household behaviors.

Literature Review

Student Debt and Household Behaviors

In 2009, Americans collectively owed $772 billion in student loans. By 2019, that number had more than doubled to $1.6 trillion (Hess 2019). Rising levels of student debt have significant implications for young adults’ careers and economic behavior, which in turn affect their personal well-being, family formation, and economic consumption (Bahadir and Gicheva 2019). For example, graduates with student debt enter the job market sooner after graduation, are more likely to take jobs unrelated to their major, have lower incomes than their peers without debt (Weidner 2016), and are less able to launch small businesses (Ambrose, Cordell, and Ma 2015) or complete graduate school (Fos et al. 2017). It is unsurprising, then, that borrowers report lower job satisfaction (Luo and Mongey 2019). Black borrowers are additionally burdened by persistent job discrimination and wage inequality, making them more likely to carry higher debt-to-income ratios (see Baker 2019) and default on their loans (The Institute for College Access & Success 2020).

Lower net income and credit constraints resulting from student debt can, in turn, affect a borrower’s housing options. For example, higher levels of debt increase the likelihood that young adults will return to live with their parents (Houle and Warner 2017; Zhang 2021). When comparing two cohorts in the National Longitudinal Study of Youth—those born 1965 to 1974 and those born 1980 to 1984—Zhang (2021) finds that student debt accounts for 46 percent of declining homeownership rates. This effect may be greatest for Black young adults (Houle and Warner 2017). When a borrower fails to complete college, every $1,000 in student debt decreases their likelihood of homeownership by 5.6 percent (Gicheva and Thompson 2015). Overall, households with student debt have half the average home equity of those without (Elliott, Grinstein-Weiss, and Nam 2013b).

Student borrowers often struggle to accumulate other assets beyond homeownership. For example, when graduates carry student loans, they have less retirement savings than their peers without debt, even after controlling for income (Elliott et al. 2013c). Median household net worth in 2009 for households with student debt was $174,000 compared to $207,000 among households without debt (Elliott et al. 2013a). Lower savings rates may help to explain why student borrowers also have higher rates of bankruptcy, even though student debt cannot be discharged (DiMaggio et al. 2019). Utilizing data from the nationally representative Survey of Consumer Finances, Gicheva and Thompson (2015) find that every $1,000 in student debt increases the likelihood of filing for bankruptcy by 0.8 percent for all borrowers and 3.8 percent among borrowers who did not complete a bachelor’s degree. Research by Jabbari et al. (2023) also demonstrates the relationships between student debt and financial difficulties, which includes overdraft fees and credit card declines—potentially suggesting high-interest borrowing for immediate expenses.

Student debt also carries significant mental health implications, especially for borrowers of color. Among college students, carrying student debt is associated with higher levels of financial anxiety (Archuleta et al. 2013). However, this significance disappears after controlling for demographic variables. Furthermore, young Black borrowers are at greater risk of sleeping difficulties than White or Latino borrowers, even after controlling for socioeconomic and occupational differences, as well as the presence of children in the home (Walsemann, Ailshire, and Gee 2016). This phenomenon may be at least partially explained by the fact that Black students owe significantly more in student loans than their White classmates (Addo, Houle, and Simon 2016).

The racial disparity in educational debt persists even after controlling for parental income (Grinstein-Weiss et al. 2016) but is greatest when controlling for parent net worth (Addo et al. 2016). At all income levels, Black families have lower net worth than White families because asset accumulation is generational and therefore impacted by decades of discrimination (Darity et al. 2018). As a result, Black families have less overall savings to contribute to their children’s college education even though they are more likely to contribute to their children’s education at lower income levels (Nam et al. 2015). When parents take on loans to help pay for their children’s higher education, they too are at higher risk of depression and poorer mental health (Walsemann, Ailshire, and Hartnett 2020).

Across all races, student debt plays an important role in family formation behavior. Among borrowers over age 29, Gicheva (2012) finds that every $10,000 in student debt decreases the likelihood that the borrower is married by 7 percent. However, the relationship between student debt and marriage is complex because it is also tied to cultural mores around cohabitation. Addo, Houle, and Sassler (2019) also compared the 1979 and 1997 cohorts of the National Longitudinal Study of Youth and found that although the likelihood of being married by age 34 declined overall among the younger cohort (likely reflecting cultural changes in attitudes toward marriage and cohabitation), student debt had differential effects on generational marital decisions. Although women with student debt in the older cohort were less likely to marry or cohabitate, student debt among younger women decreased only the likelihood of marriage but not cohabitation. Among men, student debt actually increased the likelihood of marriage for the older cohort but had no effects on younger men. Analyzing these same two cohorts, Zhang (2021) estimates that rising student debt accounts for 17 percent of the difference in marital rates and that declining wages accounts for another 18 percent.

Student Debt Forgiveness and Household Behaviors

In 2009, when student loan default rates soared due to the Great Recession, President Obama signed into law the Income Based Repayment Program, alternatively called “income driven repayment” (IDR), which capped federal student loan payments at 15 percent of the borrower’s income. This ratio was reduced further to 10 percent in 2010 (Slack 2012). Overall, the policy reduced default rates and insulated program participants from fluctuating home prices in the two years following passage (Mueller and Yannelis 2019b). IDR participants were also more likely to own a home, move to a high-income zip code (Herbst 2023), and engage in higher consumer spending (Mueller and Yannelis 2019b). Weidner (2016) predicts that IDRs increase borrower incomes by an average of 3.5 percent.

Increasingly, however, advocates are calling for more radical student loan cancellation programs, rather than repayment schemes. There is limited but growing evidence that debt cancellation would have further positive microeconomic and macroeconomic effects. For example, Maggio et al. (2019) exploited a series of lawsuits in which defaulted student debt was discharged by an average of $7,901 per borrower. After the discharge, borrowers were more likely to take on new jobs and relocate, while also demonstrating higher incomes. Researchers at the Levy Institute of Bard College modeled the macroeconomic effects of full student debt cancellation (Fullwiler et al. 2018). They estimate that student debt cancellation could increase the GDP by more than $1 trillion over a 10-year period, create 1.2 to 1.5 million new jobs, and reduce unemployment. Furthermore, they estimate minimal effects to inflation and government deficits.

However, researchers differ on the most equitable debt forgiveness scheme. Catherine and Yannelis (2021) argue that full cancellation would disproportionately benefit high-income earners. They find that Black and Hispanic borrowers gain more overall debt reduction than White borrowers through income-driven schemes. Conversely, examining data from the 2016 Survey of Consumer Finances, Steinbaum (2019) compared the effects of Senator Warren’s $50,000 student debt cancellation proposal to Senator Sanders’s full cancellation proposal and predict that full cancellation would more effectively close the racial wealth gap.

Much of the aforementioned research on student debt forgiveness examines household impacts in certain limited instances of forgiveness or by simulating the balance sheet impacts of various forgiveness proposals. Therefore, significant gaps remain that limit our understanding. Specifically, prior studies have not adequately addressed how the amount of student debt forgiveness influences various household economic behaviors. Additionally, the interaction between the amount of student debt forgiveness and variables such as the borrower’s income level and their total amount of student debt has been largely unexplored. Another limitation of the existing literature is the lack of studies utilizing a national sample of households and an experimental survey design to investigate these issues.

In this study, we examine the issue from an alternate perspective by leveraging a survey experiment designed to test how student debt holders would respond to varying levels of student debt forgiveness. As noted, much of the current research on student debt and household behaviors takes into account the amount of student debt and the amount of income. In fact, some of the current policies, such as IDR, take into account the amount of income in determining the amount of relief offered (i.e., through reduced payments). Therefore, to better understand these factors in light of debt relief, we also interact varying levels of student debt forgiveness with both student debt and income levels.

Hypothesis Development

The research on student debt and household behaviors is often more correlational than causal, and thus we cannot formally test the counterfactual. However, we can assume that the inverse associations between student debt and household behaviors may also be true in cases of debt forgiveness. For example, because student debt has been associated with economic instability, social immobility, and lower quality of life, we can assume that, conversely, student debt forgiveness may be associated with economic stability, social mobility, and better quality of life. Despite limited research on student debt forgiveness, research on loan discharges and policy schemes that resemble some of the core aspects of student debt forgiveness in terms of repayments, such as IDR plans, appears to partially demonstrate these inverse patterns. Nevertheless, the full range of these patterns has not been explored, and thus, the assumption that inverse associations between student debt and household behaviors would occur in the case of debt forgiveness has not been formally tested. We therefore construct the following hypotheses to test this assumption.

Hypothesis 1: Student debt forgiveness and economic stability, social mobility, and better quality of life: Generally, we hypothesize that student debt forgiveness will be strongly associated with economic stability and—to a lesser extent—social mobility. Specifically, we expect that across all levels of proposed student debt forgiveness, individuals will make short- and long-term investments that will ensure economic stability, primarily saving for emergencies and retirement and paying down other sources of debt. Additionally, we expect that across all levels of proposed student debt forgiveness, individuals will make investments relating to social mobility, which will primarily include asset accumulation in the form of homeownership; we expect that personal investments in education and business ventures will occur at moderate levels. Finally, concerning quality of life and family formation, we expect that across all levels of proposed student debt forgiveness, a relatively small proportion of individuals will choose to work less, spend money on entertainment, make large purchases, purchase more/better food, and get married/have a child. This hypothesis is primarily supported by the aforementioned research demonstrating the strong relationships between student debt and retirement (Elliott et al. 2013c), high interest borrowing (Jabbari et al. 2023), homeownership (Zhang 2021), and entrepreneurship (Ambrose et al. 2015). Beyond student debt research, recent household financial research exploring exogenous increases in balance sheets, such as research on the expanded child tax credit and guaranteed income experiments, demonstrate that families use balance sheet increases to improve economic stability, social mobility, and better quality of life while not working less (Hamilton et al. 2022; Roll et al. 2023).

Hypothesis 2: Increasing student debt forgiveness: Given the expected relationships in Hypothesis 1, we also hypothesize that as the proposed amount of student debt forgiveness increases, investments in economic stability, social mobility, and quality of life will continue to increase as well. Here, because it is not only the presence of student debt but also the amount of student debt (e.g., Gicheva and Thompson 2015) that is often associated with economic instability, social immobility, and lower quality of life, we therefore expect increased levels of debt forgiveness to be associated with increased levels of reported behaviors related to economic stability, social mobility, and better quality of life.

Hypothesis 3: Moderating effects of student debt amounts and income: We hypothesize that as the amount of student debt held increases, larger amounts of proposed student debt forgiveness will be positively associated with spending categories related to economic stability. Additionally, we hypothesize that as the amount of income increases, larger amounts of proposed student debt forgiveness will be more strongly associated with spending categories related to social mobility. Although there is little empirical research that explores these dynamics, there are practical implications to consider. For example, we expect that loan forgiveness constituting a larger proportion of student debt held may motivate households to improve their economic security. For instance, households may begin to pay down other debts, or–given the ability for large debt payments to crowd out other spending–households may begin to save for emergencies or retirement. Moreover, we expect that higher income households, who may also have higher credit scores, may be better able to use balance sheet increases (through student loan payment reductions) to purchase assets related to social mobility, such as homes.

Methods

Study Design

The survey experiment in this study was embedded in the Socio-Economic Impacts of COVID-19 Survey (Roll et al. 2021), which was a five-wave survey administered over the first year of the COVID-19 pandemic by researchers at Washington University in St. Louis. In this survey experiment, respondents who reported that they had any student debt were asked the following question: “Suppose the federal government forgave up to

Respondents were then presented with a randomly ordered list of different options for how their behaviors might change if their debt were forgiven. These options included: (1) “I would work less,” (2) “I would pay down other debts,” (3) “I would purchase more and/or better food,” (4) “I would move to a better home,” (5) “I would spend more on entertainment (e.g., restaurants, bars, vacation),” (6) “I would get married,” (7) “I would make more large purchases,” (8) “I would have a child (including through adoption),” (9) “I would save more for emergencies,” (10) “I would start a business,” (11) “I would start or grow a college fund,” (12) “I would return to school,” (13) “I would save more for retirement,” (14) I would save for a down payment on a home,” and (14) “other.” Respondents could select multiple of these options. For the purposes of this analysis, we exclude the “other” responses from the study and combine the options for getting married and having a child to capture a general family formation response.

Assumptions

Our study design rests on two core assumptions. First, we assume that under the hypothetical scenarios we present, participants have formed rational expectations about future behaviors. This assumption has been demonstrated in previous research. Most notably, Fuster, Kaplan, and Zafar (2021) use survey experiments that include hypothetical scenarios in which individuals receive unexpected sums of money. Similarly, Fuster et al. use randomized differences in amounts to ascertain the effects of money on future behaviors. Indeed, this analytic approach, often referred to as the “reported preference approach,” has been widely used in research on financial circumstances, including college choices (Delavande and Zafar 2019) and workplace preferences (Mas and Pallais 2017). Moreover, this approach has also been used to understand the impact of potential policies on household spending behaviors, such as universal basic income (Roll et al. 2023).

Second, we assume that these rational expectations will match actual future behaviors. This assumption has also been demonstrated in previous research. For example, recent research by Wiswall and Zafar (2021) demonstrates how future career and family expectations influence college major choices and that these choices forecast later career and family outcomes. Within an experimental context, Chang, Lusk, and Norwood (2009) found that responses to hypothetical prompts around intended food purchasing behaviors were strongly predictive of actual food purchases. These prior studies indicate that study participants’ stated responses to a hypothetical student debt forgiveness policy are proxies for their actual responses to forgiveness, even if there is not a perfect link between stated behavioral intentions and actual future behaviors. We also took steps to create an environment that would solicit self-reports from participants that are more likely to lead to actual behaviors. Specifically, we included a survey pledge at the beginning of the survey that asked participants to confirm that they would provide accurate responses: “Do you commit to providing your thoughtful and honest answers to the questions in this survey?” Information was only used for participants that responded: “I will provide my best answers.” Honesty priming tasks such as this have been shown to reduce response bias in hypothetical choice experiments and thereby improve their external validity (De-Magistris, Gracia, and Nayga 2013). We also engaged in a number of data scrubbing techniques to ensure high-quality responses, such as removing participants that skipped a large portion of questions or completed the survey in an implausibly short period of time. We also reaffirmed participant anonymity throughout the online survey to avoid desirability bias (see Bagozzi, Yi, and Nassen 1998). At the same time, we also acknowledge that there will likely be a gap between stated and actual behaviors because of individual cognitive biases (e.g., Bagozzi et al. 1998; Klein, Babey, and Sherman 1997; Sun and Morwitz 2010) and from external factors like unexpected financial shocks (e.g., Mendenhall et al. 2012). Although this is not a risk to the internal validity of the study, caution is still warranted when considering the generalizability of the study. We discuss these and other limitations in more detail in the limitations section.

Finally, due to the nature of the experiment and the fact that $5,000 is the lowest of the debt forgiveness categories (and therefore the closest to $0), we treat this category as the primary reference group in our study. Nevertheless, we recognize that there are likely some benefits in this condition to the borrower—that forgiving a relatively small amount of student debt is better than forgiving no student debt at all. Here, even a modest amount of student debt forgiveness can increase household balance sheets in the short term (i.e., by reducing the size of student debt payments) or the long term (i.e., by reducing the length of student debt payments).

Data and Sample

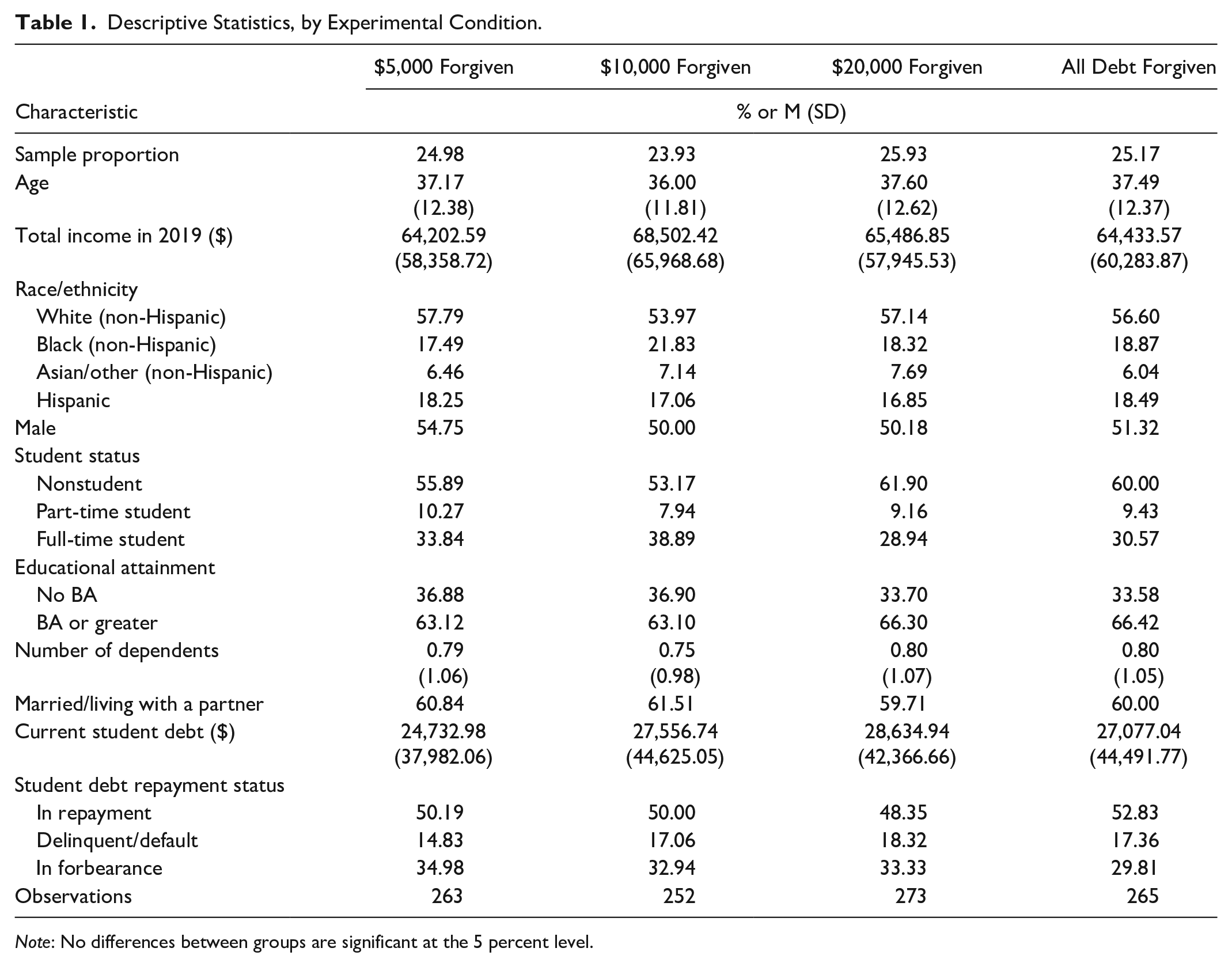

Data for this study come from Wave 4 of the Socio-Economic Impacts of COVID-19 Survey, which was administered between February 4, 2021, and March 18, 2021, through Qualtrics online panels. The survey sample was constructed using a quota-based sampling procedure that ensured the sample would reflect the U.S. population in terms of gender, age, race/ethnicity, and income. 1 In total, the survey had a 13.5 percent response rate, 2 and after exclusions due to quota requirements and nonresponse, 4,893 respondents completed the survey. Of these respondents, 1,053 reported that they held student debt and thus participated in the survey experiment.

Table 1 presents the descriptive statistics for respondents assigned to each of the student debt forgiveness conditions. There were no significant differences between the groups on any of the measured characteristics, indicating that the randomization was successful. On average, student debt holders in this study were around 37 years of age, had incomes of around $66,000 in 2019, and had 0.8 kids. Fifty-two percent of participants were male; 56 percent were White, 19 percent were Black, 18 percent were Hispanic, and 7 percent were Asian or another race/ethnicity; 60 percent were married or living with a partner; 33 percent were full-time students, and 9 percent were part-time. Additionally, at the start of the pandemic, 50 percent were repaying student debt, 17 percent were delinquent or in default, and 33 percent had student debt payments in deferment or forbearance. Our sample held around $27,000 in student debt, with 43 percent holding $5,000 or less in debt, 10 percent holding between $5,001 and $10,000, 12 percent holding between $10,001 and $20,000, 19 percent holding between $20,001 and $50,000, and 16 percent holding more than $50,000 in debt. Table 1 also shows that the sample size within each condition ranges between 252 and 273. A power analysis calculation indicates that these sample sizes are sufficient to pick up effect sizes of between 0.13 and 0.14 (assuming an alpha of 0.05 and a beta of 0.8), which is well below the threshold for what is considered to be a “small” effect size.

Descriptive Statistics, by Experimental Condition.

Note: No differences between groups are significant at the 5 percent level.

To examine the extent to which our study sample was reflective of the broader population of student debt holders in the United States, we compared our sample to student debt holders who participated in the Federal Reserve’s nationally representative Survey of Household Economics and Decisionmaking (see Appendix A in the supplement). We find that our sample of student debt holders is similar to the U.S. population as a whole in terms of age, income, race/ethnicity, gender, family structure, and student debt amount. However, our survey does have substantially higher rates of full-time students (33 percent to 14 percent). 3

Analytic Approach

Because the survey experiment randomized student debt holders into four different experimental conditions, we can estimate the average treatment effects of a given level of student debt forgiveness by testing the effects of the treatment conditions against each other (e.g., the effect of $5,000 of forgiveness vs. $10,000 of forgiveness, $10,000 of forgiveness vs. $20,000, or $20,000 of forgiveness vs. complete debt forgiveness). We assess the significance of these effects using chi-square tests.

We also explore the extent to which a household’s income and student debt amount impact their responsiveness to different levels of debt forgiveness. To do this, we estimate two sets of logistic regression models of the following forms:

where the coefficient of interest,

Results

Student Debt Forgiveness and Economic Stability, Social Mobility, and Better Quality of Life

In Table 2, we report how student debt holders assigned to each debt forgiveness condition said their behaviors would change if their debt were forgiven. Following our previously stated assumptions, results should be interpreted as expected or stated future behaviors, not actual behaviors. As expected, many households reported short- and long-term investments that can improve economic stability and—to a lesser extent—social mobility: Saving for emergencies, saving for retirement, and paying down other (nonstudent) debts were among the most reported expected behaviors, followed by saving for a home, across treatment conditions. On the other hand, relatively few people in any condition said they would work less (between 7 percent and 8 percent), indicating that people generally do not plan to reduce their labor (and, presumably, their incomes) in the absence of student debt payments. Moreover, concerning other quality-of-life measures, relatively few people said they would spend money on entertainment, make large purchases, purchase more/better food, and get married/have a child. This pattern of results confirms previous research suggesting that one of the primary effects of student debt is its tendency to crowd out household savings for both short- and long-term purposes and increase other household liabilities, while also offering a new perspective—that debt forgiveness can have inverse tendencies. Indeed, if student debt can have lasting impacts on economic stability and social mobility, so too can debt forgiveness.

Expected Behavior Change Following Student Debt Forgiveness, by Experimental Condition.

The outcome is significant relative to the $5,000 forgiven group. ap < .05. aap < .01. aaap < .001.

The outcome is significant relative to the $10,000 forgiven group. bp < .05. bbp < .01. bbbp < .001.

The outcome is significant relative to the $20,000 forgiven group. cccp < .001.

Increasing Student Debt Forgiveness

The results in Table 2 also demonstrate that the level of debt forgiveness matters. As expected, compared to the $5,000 debt forgiveness condition, even the relatively modest $10,000 forgiveness condition, as proposed by the Biden administration, nearly doubled the rates of households stating that they would purchase more or better food (16.27 percent vs. 9.13 percent; p < .05), return to school (15.08 percent vs. 7.60 percent; p < .01), or get married/have a child (16.27 percent vs. 9.51 percent; p < .05). The $20,000 forgiveness condition had slightly stronger effects than the $10,000 condition in many cases. Respondents in this condition were significantly more likely than those in the $5,000 condition to report that they would make a large purchase like an appliance (16.12 percent vs. 9.89 percent; p < .05) and save for emergencies (42.86 percent vs. 34.6 percent; p < .05). However, these relationships did not maintain an “additive” quality: The results of tests comparing the $20,000 condition to the $10,000 condition (rather than the $5,000) showed no significant differences on any expected behaviors.

Turning to the complete debt forgiveness condition, we see that total debt forgiveness would lead to large and significant expected behavioral shifts relative to the $5,000 condition. The rate of respondents reporting that they would purchase more/better food more than doubles (20.00 percent vs. 9.13 percent; p < .001), and the reported rate of saving for retirement nearly doubles (44.15 percent vs. 23.57 percent; p < .001) as well. Similarly, respondents in the complete debt forgiveness condition were more likely to report that they would spend more on entertainment (19.62 percent vs 11.41 percent; p < .01), make a large purchase (16.60 percent vs. 9.89; p < .05), save for emergencies (50.57 percent vs. 34.60 percent; p < .001), and save for a down payment on a home (24.91 percent vs. 17.87 percent; p < .05). The complete debt forgiveness condition was also significantly more effective than the $10,000 or $20,000 forgiveness conditions at motivating changes in expected savings behaviors, including saving for emergencies, saving for retirement, and saving for a down payment on a home.

Of note, although paying down other debts was the most commonly reported expected behavior that participants in any condition reported they would engage in, it was also a behavior that was insensitive to the amount of debt forgiven. This may indicate that regardless of the debt forgiveness offered, people would be likely to shift their savings from student debt payments into other debt payments as a first priority. We also observe that some of the relationships between debt amount and expected behavioral changes were nonlinear. For example, reported intentions to return to school were significantly different for the $10,000 relative to the $5,000 condition but not for the $20,000 and all debt forgiven conditions, which are only directionally more effective at driving this behavior relative to the $5,000 condition. Even though “select multiple” question types do not force respondents to make choices between stated behavioral changes, it is possible that respondents intuitively do this in some cases such that higher amounts will open up greater opportunities that respondents pursue instead of (not in addition to) alternative opportunities. For instance, those in $20,000 condition may be more likely to make a large purchase than those in the $10,000 condition (who cannot afford a large purchase with their money), which may in turn make those in the $20,000 condition feel that they are less able to start a business because that money is already theoretically spent. At the same time, given the lack of statistically significant differences between the $10,000 and $20,000 conditions, caution is warranted when interpreting these patterns.

Moderating Effects of Student Debt Amounts and Income

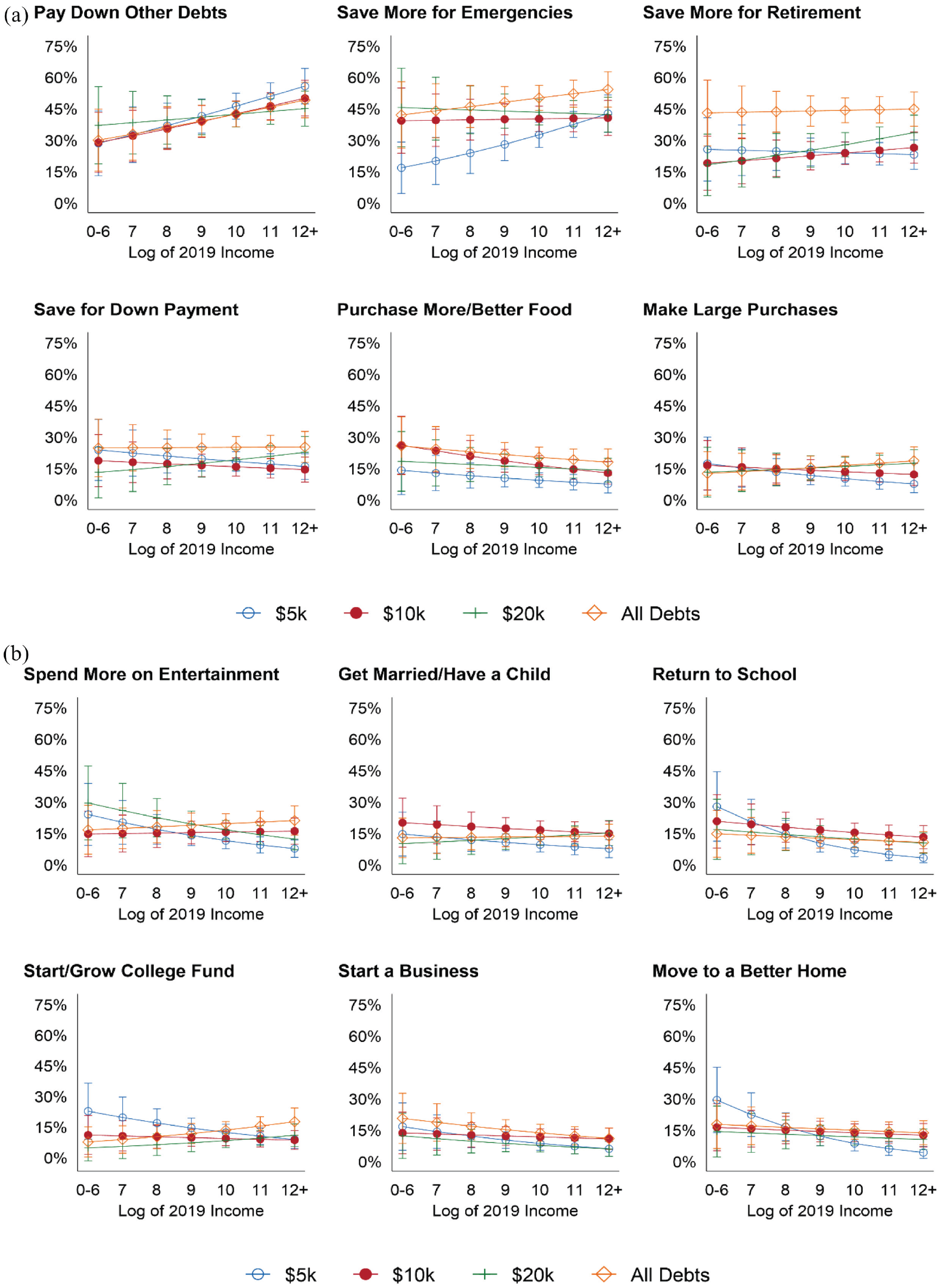

In this section, we examine how the amount of student debt forgiveness interacts with the amount of student debt held and household income. Figures 1a and 1b present the predictive margins of the logistic regression described in Equation 1, in which the student debt forgiveness condition to which respondents were assigned to is interacted with the natural log of their student debt amount. 4 These results show some interesting patterns. First, as expected, we see that as the amount of student debt held increased, participants in higher debt forgiveness conditions were generally more likely to report expecting to use forgiveness as an opportunity to save for emergencies, save for retirement, save for a down payment, or pay down other debts. In particular, respondents offered the largest amounts of debt forgiveness ($20,000 and total forgiveness) appeared very sensitive to the amount of student debt held when it came to savings and paying down debt. Interestingly, the relationship between student debt and expecting to save for college or return to school was relatively flat for the total forgiveness condition but was relatively dynamic for those in the less generous forgiveness conditions. Those with relatively small amounts of debt were highly likely to expect to use the forgiveness to make these kinds of investments, while those with high amounts of debt were much less likely to do so compared to those in other conditions. Rates of intended entertainment spending decreased for those in the lowest forgiveness condition as their debt increased, while entertainment spending increased for those with high debt in the full forgiveness condition. Finally, the relationship between debt forgiveness amount and expected behaviors like food purchases, moving/improving a home, making large purchases, and getting married or having a child appeared relatively insensitive to student debt amounts. Tables C1a and C1b in the Appendix in the supplement present the regression output underlying these figures.

(a) Treatment effects on expected behavior change, by logged student debt amount. (b) Treatment effects on expected household behaviors, by logged student debt amount.

Figures 2a and 2b present the predictive margins of the logistic regression described in Equation 2, in which the student debt forgiveness condition to which respondents were assigned is interacted with the natural log of their 2019 household income. Interestingly, as income increases, respondents in every condition were more likely to say they would use student debt forgiveness to pay down other debts, while the patterns are much less uniformly positive for other measured behaviors. As income increases, households offered $5,000 of forgiveness become much less likely to say they would return to school or move to a better home, while this relationship is relatively flat for the other conditions. Expected rates of starting or growing a college fund decrease for those in the $5,000 forgiveness condition as their income increases, although the relationship between this behavior and income is somewhat positive in the higher forgiveness conditions. Regardless of forgiveness condition, expected rates of starting a business decline somewhat as income increases. In terms of saving for retirement, the relationship between income and both $5,000 and complete debt forgiveness was flat, while it was positive for $10,000 and $20,000 of forgiveness. The relationship between saving for emergencies, household income, and debt forgiveness indicates that at lower household incomes, higher amounts of debt forgiveness are strongly associated with emergency savings, but as income increases, the reported rates of emergency savings for all conditions converged. There did not appear to be strong relationships between income, debt forgiveness amount, and reported intentions to save for a down payment on a home, purchase more/better food, make a large purchase, spend more on entertainment, or get married/have a child. Tables C2a and C2b in the Appendix in the supplement present the regression output underlying these figures. 5

(a) Treatment effects on expected household behaviors, by logged 2019 household income. (b) Treatment effects on expected household behaviors, by logged 2019 household income.

In Appendix E in the supplement, we examine both student debt and household income interactions using alternate specifications of debt and income. Specifically, we use a categorical measure of student debt that better corresponds to our hypothetical debt forgiveness amounts (e.g., $0–$5,000, $5,001–$10,000, etc.) and a measure of income that is indexed to the area median income in the respondent’s zip code. These results are broadly similar to the results presented in the main analysis, although descriptively, the relationships between income/debt amount, debt forgiveness condition, and stated household behaviors appear somewhat less pronounced and relatively flat compared to the models using logged income/debt amounts.

Discussion

As policymakers grapple with whether to forgive student debt, who should get debt forgiveness, and how much should be forgiven, we explore how different levels of student debt forgiveness would relate to household decisions and behaviors. This allows policymakers to understand what types of burdens would be relieved and what types of opportunities would be pursued. In doing so, we help contextualize the student debt forgiveness debate within a broader array of policy options aimed at relieving economic hardships. Although there have been experiments that examine the impact of receiving sums of money (see Fuster et al. 2021; Roll et al. 2023), this is—to our knowledge—the first experiment to examine potential debt forgiveness scenarios. Student debt forgiveness is fundamentally different from receiving sums of money because of the unique credit and liquidity constraints associated with student debt and associated behavioral biases. For example, credit constraints associated with student debt can make it more difficult to take out a home loan; recurring payments can constrain liquidity and put individuals at risk of financial hardships; and long payoff lengths can discourage family formation behaviors (Gicheva and Thompson 2015; Houle and Warner 2017). Indeed, because the impacts of student debt are uniquely different from income, liquidity, and savings (Despard et al. 2016), we can assume the impacts of student debt forgiveness will also be unique.

Thus, we embedded an experiment in a survey that asked participants with student debt to imagine a scenario in which the federal government forgave a certain amount of student debt and then asked them to report how this would affect their decisions and behaviors. Our sample of 1,053 student debt holders with characteristics that broadly reflect U.S. borrowers as a whole were randomly assigned to one of four conditions that featured different levels of student debt forgiveness: $5,000, $10,000, $20,000, and all student debt forgiven.

First, we explore the overall expected behaviors across all debt forgiveness groups. The results demonstrate how extensively student debt affects debt holders. The most common expected behavioral changes across all groups were associated with economic stability and—to a lesser extent—social mobility, including paying down other debts (44 percent), saving for emergencies (42 percent), saving for retirement (30 percent), and saving for a down payment on a home (20 percent). Additionally, concerning other aspects of social mobility, we also observed that around 10 percent of student debt holders expected to invest in themselves or their families by returning to school, saving for college, or starting a business if they received debt forgiveness. Conversely, and contrary to the fears of some policymakers, the least common expected behavioral change was working less (7 percent). These results demonstrate that student debt can limit borrowers’ ability to (a) effectively manage their current financial circumstances, (b) plan for the future, and (c) invest in their own human capital. When considering reported rates of human capital investments along with the fact that relatively few respondents planned on working less, the argument can be made that debt forgiveness could not only have positive effects for borrowers—helping increase their chances of social mobility—but also that debt forgiveness could generate positive externalities through increased economic productivity.

We then consider variation in the outcomes across debt forgiveness groups. In doing so, we found that larger amounts of debt forgiveness were positively associated with expecting to purchase more or better food and save for emergencies. This demonstrates the extent to which student debt may be limiting borrowers’ ability to meet their basic needs. Additionally, there was some evidence that debt forgiveness could influence rates of returning to school or family formation, both of which are seen as important mechanisms for economic growth. Finally, there were some expected behavioral changes that were only associated with total debt forgiveness. These changes tended to be associated with long-term goals, such as making large purchases, moving to a better home, or saving for retirement. Here, student debt may be acting as a credit constraint or a barrier in future orientations toward saving and asset-building.

Next, we interacted the treatments with the actual amount of debt held by individuals and their income. Starting with student debt amounts, some policymakers have suggested that the amount of debt held matters when considering forgiveness. Here, we find that as the amount of student debt increases, individuals with larger amounts of their student debt forgiven are more likely to expect to pay down other debts, save for emergencies and retirement, and save for a down payment on a new home. This demonstrates that as the amount of student debt forgiven makes up a larger proportion of student debt held, borrowers with more student debt are more likely to improve their current financial situations—through debt reductions, savings increases, and long-term asset accumulations. Conversely, as amount of student debt increases, individuals that are only forgiven $5,000 in student debt are less likely to expect to save for retirement, save for a down payment on their homes, or invest in economic mobility than other treatment groups, indicating that targeting a forgiveness amount too low may not have substantial social mobility impacts. In other words, with student debt forgiveness, you get what you pay for. Finally, as the amount of student debt increases, individuals that have all their student debt forgiven are more likely to expect to purchase more/better food and spend more on entertainment, which may signal improved quality of life for high debt holders that are given complete debt forgiveness.

Considering borrowers’ income, policymakers have also suggested that not all debt holders experience the same hardships and that therefore, debt forgiveness policies should also consider one’s income. We find that as the amount of income increases, individuals with larger amounts of their student debt forgiven are more likely to expect to save for retirement, save for a down payment on a home, make a large purchase, and get married or have a child. This demonstrates that larger amounts of debt forgiveness may encourage higher earning borrowers to plan for the future, accumulate assets, and form families. Conversely, as the amount of income increases, individuals that only receive $5,000 of forgiveness are more likely to expect to pay down other debts and save for emergencies and less likely to save for retirement, save for a down payment on a home, move to a better home, return to school/save for college, start a business, make a large purchase, or spend more on entertainment. Here, small amounts of debt forgiveness may encourage higher earners to reduce other areas of debt but will not encourage them to plan for the future, accumulate assets, increase their human capital, or meet other consumption goals. Additionally, as borrowers’ income increases, individuals that have all of their student debt forgiven are more likely to expect to make a large purchase and spend more on entertainment, which may signal improved quality of life for high earners that are given complete debt forgiveness.

Existing literature has explored the effects of student debt on individuals and households, demonstrating its far-reaching influence on decisions that impact household economic stability, social mobility, and economic growth. Our findings align with this body of research because the responses to our hypothetical forgiveness policies corroborate the pervasive influence of student debt on decisions that span various life domains. In particular, our results echo the findings of Ambrose et al. (2015), Elliott et al. (2013b, 2013c), Fos et al. (2017), Gicheva and Thompson (2015), Herbst (2019), Maggio et al. (2019), and Zhang (2021), who highlighted how student debt influences decisions relating to household economic stability. Similarly, the influence of student debt on family formation found in our study is consistent with the observations of Addo et al. (2019), Bahadir and Gicheva (2019), and Gicheva (2012).

However, our study extends the existing literature by demonstrating that the level of student debt forgiveness significantly impacts households’ economic behaviors. This is a notable contribution because the relationship between the amount of debt forgiveness and households’ economic decisions is an area that previous studies have not fully explored. The nuanced findings provided by our study, particularly in showing that lower amounts of student debt forgiveness may not lead to broad-based changes in households’ economic behaviors, can inform future research and policy discussions.

Furthermore, our research underscores the importance of considering the borrower’s income level and the amount of their student debt in discussions about student debt forgiveness—an aspect that is often overlooked in existing research. Our findings suggest that these variables play a crucial role in determining the effects of student debt forgiveness, with more significant benefits accruing to borrowers with higher levels of debt and income. This observation expands our understanding of the dynamics of student debt and debt forgiveness, while highlighting the need for a more targeted approach to policy formulation.

Finally, it is important to note that we also examined race and ethnicity as potential moderators with debt forgiveness by interacting race/ethnicity with debt forgiveness categories. Although we did not find significant effects, it is possible that the absence of effects was due to a lack of power of our study (i.e., we did not have enough power to pick up interaction effects across four treatments and five categories of race/ethnicity). Future research should continue to explore the role of race/ethnicity in student debt and loan forgiveness policies. Recent analyses by the Roosevelt Institute (Eaton et al. 2021) suggest that full student debt cancellation would make significant strides toward closing racial wealth gaps.

Implications

Aside from philosophical considerations, implicit in policy proposals are assumptions that student debt forgiveness will reduce or remove a substantive “drag” on household finances, potentially leading to behaviors that will improve short- and long-term economic conditions and outlooks. Yet without posing the question, there is little evidence that demonstrates how borrowers would respond to different debt forgiveness proposals. In posing this question, we offer novel insights into student debt forgiveness policies.

We find that borrowers would strengthen their household balance sheets by reducing other sources of debt and saving more. This could have far-reaching effects. For example, borrowers’ debt-to-income ratios would decrease while their liquid assets would increase, which would improve two of the most critical underwriting criteria for mortgages. In addition to saving more, we demonstrate that borrowers would further invest in themselves by returning to school or starting a business.

However, our findings suggest the amount of forgiveness should be at least $10,000—especially for borrowers with high amounts of debt. Full forgiveness may boost emergency and retirement savings—two important federal government policy objectives reflected in key initiatives (e.g., Consumer Financial Protection Bureau’s “Start Small Save Up,” the “Ready” national public service campaign for disaster preparedness) and tax policies (e.g., Individual Retirement Accounts, 401k plans).

Our findings also inform ideas about different distributive schemes that frame policy choices. One approach is to support debt forgiveness as a targeted, means-tested policy. Forgiving debt would reduce repayment burden and thus create financial slack needed to smooth consumption—a natural extension of existing income-driven repayment (IDR) policy predicated on assumptions concerning ability to repay. In fact, forgiveness could be tacked onto existing IDR policies wherein borrowers’ repayments would be set to a maximum of 10 percent of gross pay for a standard 10-year term with any remaining principal written off at the end of this term. This approach would help remediate a breach in the social contract of college education–that graduates will enjoy an earnings premium.

Another approach is universal and unconditional loan forgiveness. We find that higher amounts of loan forgiveness may make saving, homeownership, and family formation more likely among those with higher incomes. This approach supports policy goals of using student loan forgiveness as a tool to promote long-term household financial stability and economic growth by strengthening balance sheets and boosting demand across a wide range of borrowers.

Findings from our study may also help guide future research on student debt. In particular, our findings concerning participants’ intentions to reduce other debt if receiving student loan forgiveness suggest that researchers look more closely at total household debt composition among borrowers. Whereas Bahadir and Gicheva (2019) examined aggregate, state-level debt-to-income (DTI) ratios, researchers can also attempt to estimate this at the household level. This line of research could prove useful in juxtaposing findings with ability to repay standards in federal student loan repayment regulations. Estimating household DTI among borrowers could also help better explain the relationship between student debt and homeownership given the salience of DTI in mortgage underwriting. Furthermore, our findings concerning student debt amounts as a moderator and— when considering the distributional characteristics of student debt—suggest that future research might examine the heterogeneity of debt amounts in relation to research questions. Moreover, concerning our findings on retirement savings, researchers may wish to study workers’ access to and use of the Secure 2.0 Act (signed into law in December 2022) that allows employers to count employees’ student loan payments as meeting requirements to qualify for employer retirement plan matches. More generally, our findings concerning a range of prospective behavioral responses suggest that researchers adopt inductive and qualitative strategies to explore how student debt affects borrowers’ behaviors and quality of life, especially disproportionately affected groups such as African Americans, who may simultaneously be confronted by a host of social and economic challenges and injustices.

Limitations

Nevertheless, this study is not without its limitations. First, this study creates a hypothetical scenario involving debt forgiveness and collects information on future behaviors. Although stated intentions are often indicative of future behaviors in hypothetical settings (Chang et al. 2009), discrepancies can exist between intentions and behaviors that bias forecasts (e.g., Bagozzi et al. 1998; Sun and Morwitz 2010). One common approach to reducing this bias in the context of hypothetical public policies is by prompting respondents to consider the consequentiality of their decisions; for example, by informing them that their responses will be important in influencing policymakers’ actions (e.g., Vossler and Watson 2013). However, this approach is much more practical for policies decided on at the local level than a national policy like student debt forgiveness. Instead, we use an honesty prompt in our survey to prime respondents to give accurate answers and exclude anyone who did not provide an affirmative answer to this honesty prompt from the sample. This approach has been shown to reduce bias in hypothetical choice survey (De-Magistris et al. 2013). At the same time, it is likely that the hypothetical nature of the student debt forgiveness experiment still introduces bias into our results and thus limits the external validity of our findings.

Beyond individual cognitive biases influencing these results, external factors may also lead to a discrepancy between stated intentions and actions. In the context of other public benefit policies, Mendenhall et al.’s (2012) research on the earned income tax credit (EITC) demonstrates that external factors (e.g., unexpected emergencies and bills) can lead to gaps between intended usage of the EITC and actual usage of the credit. Thus, although our survey experiment is a necessary step in understanding how future policy options might impact policy recipients, it is important for future research on student debt forgiveness to follow up after a policy is enacted to determine the degree to which these intentions match up with actions. Additionally, a core purpose of this study was not simply to generalize about how student debt holders will respond to forgiveness but, rather, to understand the extent to which different levels of debt forgiveness lead to changes in stated behaviors. Because we explored this relationship experimentally, we are confident in the internal validity of our findings.

Another limitation stems from the fact that because of sample and survey constraints, we limited our treatment to four categories and our outcomes to binary responses of general behaviors. Although Senator Warren has proposed $50,000 in student debt forgiveness, the majority of borrowers have $20,000 or less in student loans. With a limited sample, we therefore include a “total debt forgiveness” category that encapsulates those higher amounts of student debt. Thus, future research should consider additional treatment categories (e.g., $50,000) to better understand nuances in the effects of debt forgiveness policies. Future research should also consider including more detailed responses (e.g., responses with defined amounts and/or time frames) to provide a more comprehensive understanding of the relationships between debt forgiveness and borrower behaviors. This study also lacked a true “control” group that received no forgiveness whatsoever because this approach would have been conceptually difficult to implement within the context of our research questions (i.e., it is difficult to ascertain reported behavior changes to an absence of a stimulus). Rather, we used a relatively small amount of debt forgiveness ($5,000) as a reference group in our analyses because this amount is half of the lowest amount of forgiveness commonly discussed in policy circles. Future studies could consider testing behavioral responses to even lower amounts or alternative (and less valuable) debt remediation schemes as proxies for a control group.

A final limitation comes from the fact that this study was done using an online survey conducted during the COVID-19 pandemic. Although randomization allows us to control for potential biases associated with the treatment (i.e., internal validity), it is possible that the overall relationships in this study are open to potential biases in their generalizability (i.e., external validity) both in terms of study population and survey timing. For example, the 13.5 percent response rate to the survey introduces the possibility of nonresponse bias in our findings, as does the fact that the survey was administered online, thus excluding those without any stable source of internet access. Although our supplemental analyses suggest that our study sample is similar to other nationally representative data sets (see Appendix A in the supplement) and although our results do not change after the application of sample weights derived from U.S. census data (see Appendix B in the supplement), these factors still limit the extent to which we can generalize our findings. Additionally, we are unable to conduct robustness checks in terms of survey timing. Because many loans were in forbearance during COVID-19, it is possible that people’s attitudes toward student debt may change after the forbearance runs out. However, it is important to keep in mind that all forbearance policies had relatively short time horizons, and thus it is unlikely that borrowers would conceive these polices as long term and adjust their perceptions of student debt forgiveness accordingly. It is also possible that the larger economic impacts of COVID-19 may limit the generalizability of the findings to times of social and economic instability. Yet these larger economic impacts can be seen as precipitating the public discourse on student debt forgiveness policies. Here, the timeliness of this experiment in terms of the broader public discourse on debt forgiveness may be seen as outweighing the limitations in generalizability due to the unique context of the time period in which the study was conducted. Nevertheless, future research should continue to explore debt forgiveness policies after the pandemic subsides.

Conclusion

As policymakers consider how to deal with the roughly $1.7 trillion in student debt, it is important to ask what difference loan forgiveness would make in the lives of student debt holders. We answer this question through a novel survey experiment drawn from a national sample of households. These results show three things. First, confirming previous research, our results demonstrate how extensively student debt affects individuals. Overall, responses to the hypothetical forgiveness policies indicate that student debt is influencing decisions that have implications for household economic stability (e.g., emergency savings), social mobility (e.g., returning to school), family formation (e.g., getting married, having a child), and economic growth (e.g., starting a business). Second, we extend the previous literature by demonstrating that the level of student debt forgiveness matters. In particular, lower amounts of student debt forgiveness may not lead to broad-based changes in households’ economic behaviors, whereas larger amounts may yield changes in savings behaviors and human capital investments without leading to large changes in labor supply. Finally, our results demonstrate that the amount of student debt and the borrower’s income levels matter in the relationship between debt forgiveness and household behaviors. Here, borrowers with more debt are more likely to improve their current financial situations—through debt reductions, savings increases, and asset accumulations—with larger amounts of debt forgiveness. A similar relationship exists for higher earning borrowers. By demonstrating the burdens that could be relieved and the opportunities that could be pursued through student debt forgiveness, our findings can inform future policy discussions for whether or not student debt should be forgiven, how much, for who, and under what circumstances.

Supplemental Material

sj-docx-1-srd-10.1177_23780231231196778 – Supplemental material for Student Debt Forgiveness and Economic Stability, Social Mobility, and Quality-of-Life Decisions: Results from a Survey Experiment

Supplemental material, sj-docx-1-srd-10.1177_23780231231196778 for Student Debt Forgiveness and Economic Stability, Social Mobility, and Quality-of-Life Decisions: Results from a Survey Experiment by Jason Jabbari, Stephen Roll, Mathieu Despard and Leah Hamilton in Socius

Footnotes

Authors’ Note

Jason Jabbari and Stephen Roll contributed equally to this work.

Funding

This work was supported by the JP Morgan Chase Foundation, but the views expressed are solely those of the authors.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.