Abstract

Previous studies suggest that a college degree is the great equalizer leveling the playing field. However, the rapidly growing educational debt of college graduates might restrict their life chances throughout adulthood, particularly for those raised in socioeconomically disadvantaged families. This study uses data from the National Survey of College Graduates to examine whether parents’ socioeconomic status is related to their children’s student loan repayment after graduation. Holding the amount borrowed for completing higher education constant, college graduates with less educated parents hold a larger amount of educational debt in adulthood compared with their counterparts with more educated parents. The association between family background and student loan repayment remains significant with the addition of controls for various covariates related to college graduates’ education, occupation, income, and other labor market outcomes. This study suggests that educational debt burdens imposed on individual college graduates limit the meritocratic power of higher education.

Educational debt for college graduates has soared in the United States (Dwyer 2018; Houle 2014b). In the 2015–2016 academic year, more than half of college students borrowed toward their degrees, and the cumulative loan amount of the average indebted bachelor’s degree completer rose to about $32,400 by 2019 (NCES 2020). Aggregate educational debt balances in the United States topped $1.7 trillion in 2021 (Federal Reserve System 2021). This educational debt may delay transitions to adulthood and have negative ripple effects on financial investment, savings, and wealth accumulation, particularly for college graduates with low wealth, racial minorities, and those leaving college without a diploma (Baker, Andrews, and McDaniel 2017; Gross et al. 2009). Although President Biden’s administration has considered universal student loan forgiveness, there has been political controversy regarding who would benefit most from wiping out the educational debts of millions of college graduates (Catherine and Yannelis 2020; Charron-Chenier et al. 2020; Eaton et al. 2021).

As the importance of educational debt for social inequality has increased, many researchers have examined the effects of parents’ socioeconomic status (SES) on the amount of student loans college students borrow for completing higher education (Baker et al. 2017; Choy and Berker 2003; Houle 2014a). However, previous studies have paid less attention to the association between parents’ SES and student loan repayment after graduation. One obstacle for the study of student loan repayment is that many survey data sets do not include information about exact amounts borrowed and still owed in addition to parents’ SES and various other covariates, such as college graduates’ demographic, educational, and occupational characteristics. Because of this data limitation, previous studies often focus on whether college graduates are in default without accounting for exact debt amounts or relevant socioeconomic covariates (Gross et al. 2009).

Further investigation into the association between family background and student loan repayment is imperative for several reasons. First, the importance of student loan repayment for social inequality will continue to increase. As rising college tuition increases the amount college students borrow, educational debt may become more burdensome with long-lasting negative impacts during adulthood. Second, educational debt burdens likely limit the meritocratic power of higher education for reducing socioeconomic disparities between children from different family backgrounds. Even if higher education improves the chances for children from low-SES families to obtain a high-paying job, their life chances will remain relatively restricted if they hold more education debt than their counterparts from high-SES families after graduation. Third, the risk associated with a given amount of educational debt varies based on individuals’ ability to pay off that amount. The disadvantages of student loans are particularly severe for those who cannot repay their student loans quickly. If children from low-SES families are less able to settle their education debt compared with their counterparts from high-SES families, the growth of student loans will widen the socioeconomic disparities between children from different family backgrounds. That is to say, college graduates from lower SES families may benefit more from universal student loan forgiveness programs.

The aim of this study is to examine the associations between parents’ SES and college graduates’ student loan repayment, controlling for an extensive set of covariates. The findings show that parents’ SES is positively related to their children’s student loan repayment after graduation. Holding the amount borrowed constant, college graduates from low-SES families are more likely than their counterparts from high-SES families to hold a large amount of debt during adulthood. The differences by parents’ SES in the amount of debt further increases as the amount borrowed increase. Controls for various covariates—including college graduates’ education, occupation, income, and other labor market outcomes—barely alter the significance of the positive association between parents’ SES and student loan repayment after graduation.

Theoretical Background

Education, Loans, and Social Inequality

Researchers have recognized that education plays a critical role in social stratification (Blau and Duncan 1967; Bloome, Dyer, and Zhou 2018). On the one hand, educational inequality may transmit the effects of parents’ SES on children’s SES. As children of high-SES families are more likely than those from low-SES families to have a high level of educational attainment, parents’ SES is positively correlated with the likelihood of attaining a prestigious occupation and high income (Bukodi and Goldthorpe 2016). On the other hand, the chance for children from low-SES families to achieve upward social mobility may be increased by improving their level of educational attainment. The seminal studies of Hout (1984, 1988) demonstrated that parental effects on children’s SES were much weaker among college graduates than their less educated counterparts in the United States. Weaker intergenerational associations among more educated children are also observed in other industrialized countries, including Britain, France, Germany, and Sweden (Breen and Jonsson 2007; Breen and Luijkx 2007; Vallet 2004). These empirical findings lead to the great equalizer perspective that a college degree enables children raised in low-SES families to overcome their disadvantages related to their family backgrounds.

As the higher education system has rapidly expanded, researchers have increasingly examined social stratification among college graduates. Recent studies have shown substantial parental effects on college graduates’ occupation and income, implying that intergenerational socioeconomic associations have emerged among college graduates (Oh and Kim 2020; Torche 2011; Witteveen and Attewell 2017). A college degree may not necessarily guarantee a level playing field in the twenty-first century. Unarguably, however, the growth of the knowledge economy has continued to increase the educational earnings premium (Autor 2014; Powell and Snellman 2004). Children from low-SES families clearly have better life chances in adulthood if they obtain a higher level of educational attainment (Bloome et al. 2018).

Meanwhile, the influence of taking student loans to obtain a high level of educational attainment on social inequality is debatable (Dwyer 2018; Jackson and Reynolds 2013). Given that education improves the chance of children’s upward mobility, student loans are useful resources that enable students with less financial support from their families to seek a bachelor’s or higher degree. Although student loans of more than $10,000 hinder college completion, lower levels of loans increase the probability of college graduation (Dwyer, McCloud, and Hodson 2012). Loans, if not excessive, can motivate students to study hard with a strong sense of responsibility (Quadlin and Rudel 2015). Thus, one practical strategy for low-SES children seeking upward social mobility may be to take out a loan to complete a profitable degree, which increases their chance of beneficial labor market outcomes. In this respect, one may argue that student loans provide an opportunity for children from low-SES families and thus attenuate parental effects on children’s SES in adulthood.

However, it must be noted that student loans restrict college graduates’ life chances in the future. Indebted college students must manage student loan bills after completing their higher education. As student loans have rapidly grown, the negative effects of educational debt on college graduates’ socioeconomic attainment and well-being have become intense and persistent throughout adulthood (Baker et al. 2017; Dwyer 2018). Arguably, among college graduates who attain the same educational and occupational outcomes, those who hold more educational debt are worse off. Some indebted college graduates may delay marriage (Addo 2014; Bozick and Estacion 2014) and childrearing (Nau, Dwyer, and Hodson 2015). Debt amounts tend to be negatively correlated with homeownership (Houle and Berger 2015; Mezza et al. 2016), financial investment (Batkeyev, Krishnan, and Nandy 2018), savings (Cooper and Wang 2014), pensions (de Gayardon et al. 2018), and wealth accumulation (Elliott and Rauscher 2018; Hiltonsmith 2013). These findings imply that research into student loan repayment has become increasingly important in understanding ongoing social inequality and its reproduction (Dwyer 2018). Insofar as family background is related to children’s borrowing and repaying of student loans, the current education system’s imposition of large educational debt burdens on individual students and their parents should play a role in maintaining, if not reinforcing, the intergenerational socioeconomic association among college graduates.

Previous studies document the close relationship between family background and college students’ loan borrowing (Choy and Berker 2003; Houle 2014a; Quadlin 2017). College students from high-SES families have a low likelihood of being indebted by virtue of their families’ affluence. Some students from low-SES families benefit from need-based financial aid, although many of them do not complete a degree. Compared with children from lower and higher SES families, those from middle-SES families have the highest chance of borrowing (Choy and Berker 2003; Houle 2014a). Nonetheless, the proportion of indebted college graduates and their average debt amount have soared, regardless of family background, because of rising college tuition (Baker et al. 2017; Houle 2014b).

However, the relationship between family background and student loan repayment among college graduates has been relatively less studied. The impact of the same amount of student borrowing on college graduates varies because they do not all have the same capacity to repay their student loans (Baker et al. 2017; Dynarski 1994; Gross et al. 2009; Hillman 2015). The same amount of student borrowing is necessarily more detrimental to those who hold a higher portion of education debt in adulthood. Although some studies suggest the association between family background and the student loan default rate (Gross et al. 2009), the exact debt amounts borrowed and still owed by college graduates have been rarely considered in previous studies. This research examines how college graduates’ capacity to repay their student loan differs by their family background, accounting for various covariates, such as educational and occupational outcomes.

Family Background and Student Loan Repayment

If parents’ SES is unrelated to student loan repayment after graduation, the same student loan amount should be equally burdensome to college graduates from low and high-SES families. The great equalizer argument suggests that parental effects on children’s labor market outcomes are negligible among college graduates (Hout 1984, 1988), implying that effects of parents’ SES on student loan repayment may be trivial among those holding a college degree. Unlike non-college-educated workers or college dropouts, college graduates may have decent jobs and a high financial capacity to repay student loans regardless of their family backgrounds. The first hypothesis tested in this study is that college graduates’ student loan repayment is independent of their family backgrounds (hypothesis 1).

Otherwise, parents’ SES is positively associated with college graduates’ student loan repayment, requiring further investigation into the two other possibilities (hypotheses 2a and 2b). Recent empirical studies criticize the great equalizer argument, finding substantial educational and occupational disparities among college graduates with strong connections to parents’ SES (Manzoni 2021; Oh and Kim 2020; Torche 2011; Witteveen and Attewell 2017). These studies suggest that the current research should consider stratification in and through higher education, which may also affect the rate at which college graduates repay their debt (Looney and Yannelis 2015). Depending on type of degree, field of study, and selectivity of institution, college graduates experience different educational and occupational outcomes and have different patterns of intergenerational social mobility (Kim, Tamborini, and Sakamoto 2015; Oh and Kim 2020; Tamborini, Kim, and Sakamoto 2015; Torche 2011). Children from high-SES families tend to attend more selective private schools and to seek higher level graduate degrees; this leads to high socioeconomic returns in the labor market (Oh and Kim 2020). These socioeconomic outcomes, including stable and high-paying jobs providing high levels of financial stability, are themselves positively correlated with the capacity of replaying student loan. Thus, the second hypothesis is that the positive association between parents’ SES and student loan repayment after graduation becomes nonsignificant after controlling for college graduates’ educational and occupational outcomes (hypothesis 2a).

The last possibility is that the positive association between parents’ SES and student loan repayment is not fully explained by educational and occupational disparities among college graduates. Even if college graduates from low-SES families earn the same education, occupation, and earnings compared with their counterparts from high-SES families, their student loan repayment capacity would be persistently bound up with their family backgrounds. Among college graduates who borrowed a small amount of loan, the importance of family support in student loan repayment may be ignorable. However, as the student loan amount increases, parents’ SES would play an increasingly important role in college graduates’ loan repayment. Gross et al. (2009) pointed out that high-SES families provide a financial safety net that helps their children meet student loan obligations without disruption. This financial safety net is particularly crucial when macroeconomic shocks, such as the Great Recession or the coronavirus disease 2019 pandemic, heighten all college graduates’ risk for student loan delinquency and default (Mueller and Yannelis 2019). During hard times, children from high-SES families can alleviate their economic distress to some extent by relying on their families’ affluence, a resource that may not be available to their peers from low-SES families. Although high-SES parents do not necessarily intend to intervene directly in their children’s debt repayment, family support for other costs, such as those related to homeownership and childrearing, may allow their children to divert a large portion of their earnings to pay back student loans (Furstenberg 2016; Lee et al. 2020; Napolitano, Furstenberg, and Fingerman 2021; Pfeffer and Killewald 2018). Therefore, the third hypothesis is that parents’ SES is positively associated with children’s student loan repayment, even with educational and occupational covariates held constant (hypothesis 2b). To sum up, this study examines the association between parents’ SES and student loan repayment among college graduates without and with controls for various educational and occupational covariates.

Analytic Strategy

Data and Sample

To test the three competing hypotheses on the association between parents’ SES and student loan repayment after graduation, I analyze pooled data from the 2013, 2015, 2017, and 2019 National Survey of College Graduates (NSCG). The NSCG is a nationally representative survey of college graduates holding bachelor’s degrees or higher and currently living in the United States. The NSCG is a unique data source containing a variety of information on college graduates’ educational experiences and labor market outcomes, especially the amount they borrowed for their higher education and the amount still owed as of the survey reference year. NSCG data from earlier years are excluded because of a lack of information on amounts borrowed and owed.

NSCG respondents were asked to participate in a baseline survey and three biennial follow-up interviews. As inclusion of repeated observations may lead to a downward bias in estimating standard errors, which increases the likelihood of type I error, I select a sample consisting of all respondents from 2013 and only new survey participants from each following survey year. Those who did not complete their higher education in the United States are not included. College graduates who did not take out student loans are excluded from the regression analysis but included in descriptive analyses and in adjusting for sample selection bias. The total unweighted sample sizes for regression analysis are 52,612 men and 52,180 women. The final sample sizes after listwise deletions are 46,804 men and 44,476 women.

Variables

The NSCG respondents were asked to choose from a list of categorical dollar ranges (e.g., $1–$10,000), which are capped at $90,000, in reporting how much they borrowed to cover the costs of tuition, room and board, fees, books, and supplies for completing undergraduate and graduate education, as well as how much they still owed as of the survey reference year. I take the median values for each category (e.g., $5,000 for the $1–$10,000 range). For advanced degree holders, I add their values for undergraduate and graduate education. To check the validity of this approach, I compared information from the National Center for Education Statistics (NCES) with the statistics calculated from the NSCG data. The NCES (2020) reported that the average cumulative loan amount borrowed by indebted 2015–2016 bachelor’s degree completers was about $32,400 in constant 2019 dollars. This statistic is almost identical to the estimation of the average amount borrowed by NSCG respondents who attained bachelor’s degrees in the 2010s ($32,539). Pyne and Grodsky (2020) also corroborate that the self-reported loan amounts in NSCG are consistent with more reliable National Postsecondary Student Aid Study results.

The measure of parents’ SES in this study is the highest level of educational attainment obtained by either parent: high school or less (HS), some college (SC), bachelor’s degree (BA), or graduate degree (GRAD). The proportion of parents whose educational level is less than a high school diploma is 5 percent. Because of the small size of this group, I include them in the same category as those with a high-school education. An ideal measure of family background for this study would be parents’ wealth. However, the NSCG respondents were not asked to report their parents’ wealth or other socioeconomic measures, such as occupation and earnings. Because of the lack of these measures of parents’ SES in many survey data sets, including the NSCG data, previous studies have often used parents’ education as a measure of family background that has effects on children’s educational attainment and other long-term labor market outcomes (Breen and Goldthorpe 1997; Kim, Tamborini, and Sakamoto 2018; Mullen, Goyette, and Soares 2003; Oh and Kim 2020; Pfeffer and Hertel 2015). Although parents’ education is not a perfect proxy of family background, parents with wealth are likely to hold a college degree or higher. It should be also noted that most of survey data sets that do include information on parents’ wealth, occupation, or earnings lack other information important for this study, including amounts their children borrowed and still owed in student loans, as well as other educational and occupational outcomes included in the NSCG. Even though educational level may be a limited measure of parents’ SES, the NSCG is still one of the best data sets for studying the association between family background and college graduates’ student loan repayment.

This study includes include the controls for demographical variables: up to a quartic term for age, race (white, Black, Hispanic, Asian, and others), immigration status; place of high school (New England, Middle Atlantic, East North Central, West North Central, South Atlantic, East South Central, West South Central, Mountain, Pacific, or non-U.S.), marital status (currently married, never married, or other), children (none or one or more), and survey year (2013, 2015, 2017, or 2019).

If parents’ SES is significantly related to student loan repayment holding the demographic variables constant, I should reject hypothesis 1 and further examine whether its association is explained by college graduates’ educational and occupational disparities (i.e., hypotheses 2a and 2b). By virtue of the extensive information in NSCG data, this research can consider various socioeconomic outcomes of college graduates. Education variables are highest degree earned (BA, MA, MBA, PhD, or professional degree), type of institution (public or private), Carnegie code (Research University I, Research University II, Doctorate-Granting I, Doctorate-Granting II, Comprehensive I, Comprehensive II, Liberal Arts I, Liberal Arts II, or other), and 31 fields of study. In addition, I control for the year respondents attained their highest degree because time since graduation would be correlated with the repaid loan amount. Occupational variables are log-transformed annual income, employment status (currently unemployed or employed), 39 occupations, sector (for-profit business/industry, nonprofit business/industry, federal government, state/local government, four-year college, two-year college, or self-employed), firm size (10 or fewer, 11–24, 25–99, 100–499, 500–999, 1,000–4,999, 5,000–24,999, and 25,000 or more employees), up to a quadratic term for years worked in current job, and working hours.

Statistical Models

One of the methodological challenges in this study is to examine the association between parents’ SES and the amount still owed as of the survey reference year, accounting for the amount borrowed for completing higher education. One simple way is to control for the amount borrowed in the regression of the amount still owed on parents’ SES. This method would estimate the conditional mean of the differences by parents’ SES in the amount still owed among all indebted college graduates, assuming random variation of differences from the conditional mean. However, high-SES parents may be more actively involved in their children’s student loan repayment when they borrow larger amounts. That is, as the amount borrowed increases, the gaps in the amount still owed by parents’ SES could become wider. Thus, I introduce interaction terms for parents’ SES and the amount borrowed. More specifically, I estimate the following equation:

In section 1 of reported estimates,

This study first estimates the models controlling only for demographic variables (

The statistical models are separated for men and women because previous studies suggest that the student loan repayment period and the default rate differ by gender (Baker et al. 2017; Gross et al. 2009). In addition, the gender segregation in the labor market and the gendered effects of marriage and childrearing may complicate the interpretation of gender-integrated models (Browne and Misra 2003; Mandel and Semyonov 2016). For sensitivity analyses, I use linear probability models and real amounts borrowed and still owed instead of log-transformed amounts. To further examine variations in the findings across educational groups, I also consider college graduates’ type of degree, field of study, and selectivity of institution.

Inverse Probability Weighted Regression Adjustment

Following NSCG guidelines, survey weights, which reflect the portion of the overall population each case represents, are applied to all estimations to address sample selection bias. However, this adjustment may not be enough to address potential sample selection issues in this study, as the regression models do not include respondents who did not borrow a student loan. I admit there is no perfect method to completely remove sample selection bias. Nonetheless, this research may benefit from one of the various methods that many scholars have developed to reduce selection bias (Winship and Mare 1992). One of the most popular methods is the Heckman (1976) correction that applies the inverse Mills ratio obtained from the selection model to the outcome model. However, the Heckman method is often not practical because it assumes the selection model contains at least one exogenous variable not included in the outcome model (Puhani 2000; Winship and Mare 1992).

Alternatively, Wooldridge (2002) suggested a method that adjusts the outcome model using the inverse probability weight gained from the selection model. Although this method assumes that analyses retain sufficient variables to predict selection bias, it does not require an exogenous variable in the selection equation. For the inverse probability weighted regression adjustment (IPWRA), I obtain the inverse probability of taking a student loan using logit models (i.e., selection models) and use it to adjust the weighting procedure of main regression models (i.e., outcome models). The selection models include the controls for all demographic and educational variables (i.e.,

Empirical Results

Amounts Borrowed and Still Owed by Family Background

Table 1 shows the probability of taking a student loan, the amounts borrowed and still owed, and the proportion of the loan repaid. On average, 55.3 percent of men and 60.2 percent of women took out student loans for completing their higher education. The association between parents’ SES and the likelihood of taking a student loan is not straightforward, as previous studies have suggested (Choy and Berker 2003; Houle 2014a; Quadlin 2017). For men, college graduates whose parents’ educational level was high school or less were less likely to take out a loan than those whose parents had some college education (53.4 percent for HS, 60.7 percent for SC). Compared with those with SC parents, college graduates whose parents attained a bachelor’s or graduate degree were less likely to take out a loan (55.4 percent for BA, 53.5 percent for GRAD). Likewise, the descriptive statistics for women also show a reverse U-shaped pattern in which college graduates with SC parents are more likely to borrow than those whose parents have either less or more education (61.4 percent for HS, 66.3 percent for SC, 59.4 percent for BA, and 54.0 percent for GRAD). Among college graduates who took out student loans, the average amount borrowed was $34,457 for men and $37,223 for women in constant 2019 dollars. As parents’ education increases, the indebted college graduates’ loan amount increases. The loan amount gap between college graduates with GRAD parents and those with HS parents is $10,492 for men and $8,456 for women.

Borrowing and Repaying of Student Loans by Parents’ Education.

Note: Person weights are applied. BA = bachelor’s degree; GRAD = graduate degree; HS = high school or less; SC = some college.

The sample size is 88,444 for men and 77,791 for women.

These descriptive statistics are calculated for the respondents who took out student loans. The sample size is 46,804 for men and 44,476 for women.

In the descriptive statistics, why is there a positive correlation between parents’ education and the amount borrowed? One of the reasons would be that children from high-SES families tend to pursue a higher level of educational degree and attend selective private schools requiring higher costs (Oh and Kim 2020; Shavit, Arum, and Gamoran 2007). In fact, controlling for demographic and educational covariates, I find negative associations between parents’ education and the probability of taking a loan and nonsignificant associations between parents’ education and student loan amount among borrowers (Table A1).

Parents’ educational level is also associated with the amount still owed as of the survey year. However, the association of parents’ education with the amount still owed is much weaker than that with the amount borrowed. The difference in the amount still owed between college graduates with GRAD parents and those with HS parents is $3,761 for men and –$88 for women. That is, college graduates with more educated parents had repaid a larger proportion of their student loans than those with less educated parents among men (52.6 percent for HS, 50.1 percent for SC, 54.4 percent for BA, and 55.6 percent for GRAD) and women (38.0 percent for HS, 40.9 percent for SC, 49.5 percent for BA, and 50.6 percent for GRAD). The gap in the proportion of the repaid amount between college graduates with HS parents and those with GRAD parents is larger for women (12.6 percent) than men (3.1 percent).

Given that the educational variables confound the relationships of parents’ education with the probability of taking a student loan and the student loan amount, it is possible that college graduates from high-SES families settle more education debt because they attained a higher quantity and quality of higher education than those from low-SES families. Thus, the next question in this study is whether the positive association between parents’ educational level and the proportion of the loan repaid is significant after controlling for various covariates.

Does Family Background Matter for Student Loan Repayment after Graduation?

To evaluate whether parents’ education is positively associated with student loan repayment after graduation, I estimate the multivariate regression models displayed in Table 2. To reduce potential bias related to the sample selection of indebted college graduates, the IPWRA method is applied to the estimations. I first estimate the predicted probability of taking a student loan, controlling for demographical and educational variables that are related to students’ borrowing (Table A1, section 1). Then, I use the inverse probability weight to adjust the models in Table 2. The dependent variable is the likelihood of still owing educational debt as of the survey reference year for logit models (section 1) and the log amount still owed for linear models (section 2). Model 1 includes controls for demographical covariates only, and model 2 adds controls for educational covariates. Model 3 includes all controls for demographic, educational, and occupational covariates.

Logit and Linear Estimates of Differences in Likelihood of Still Being Indebted and Log Amount Still Owed by Parents’ Education and Log Amount Borrowed.

Note: The sample size is 46,804 for men and 44,476 for women. Numbers in parentheses are standard errors. All variables except for parents’ education are centered at the mean. Personal weights are applied. BA = bachelor’s degree; GRAD = graduate degree; HS = high school or less; SC = some college.

Demographic variables are up to a quartic in age, race, immigrants, place of high school, marital status, children, and survey year.

Educational variables are highest degree earned, type of institutions, Carnegie code, 31 fields of study, and degree completion year.

Occupational variables are log-transformed annual income, employment status, 39 occupations, sector, firm size, up to a quadratic for years of working in current job, and working hours.

p < .05, **p < .01, and ***p < .001 (two-tailed tests).

Section 1 in Table 2 shows that children with more educated parents are more likely to settle education debt before the survey reference year. Although the logit coefficient sizes are not comparable over different models because of the scale variance problem (Mustillo, Lizardo, and McVeigh 2018), it is apparent that parents’ educational level is positively associated with student loan repayment with and without controls for extensive educational and occupational variables, rejecting hypotheses 1 and 2a. Because the logit coefficients are difficult to interpret, I also estimate linear probability models (Table A2). The significance tests using logit and linear probability models yield nearly identical results. Importantly, the interaction terms for parents’ educational level and the log amount borrowed are significantly negative in all models, supporting hypothesis 2b.

According to the linear probability model containing controls for all covariates (model 3), when the average log amount of student loans (approximately $23,000) is borrowed, the likelihood of still holding debt as of the survey reference year is 54.1 percent and 53.2 percent for men and women with HS parents, respectively. When the same amount is borrowed, college graduates with GRAD parents are less likely than those with HS parents to hold education debt; the likelihood of still holding debt is 48.7 percent (0.541 – 0.054) and 49.1 percent for men and women with GRAD parents. As the amount borrowed increases by 10 percent, the likelihood of still being in debt increases by 1.5 percent (0.161 × ln[1.1]) for men with HS parents and 1.0 percent ([0.161 – 0.054] × ln[1.1]) for men with GRAD parents. Likewise, a 10 percent loan amount increase raises the chance of still holding education debt by 1.6 percent for women with HS parents and 1.2 percent for women with GRAD parents. The results support hypothesis 2b, that parents’ SES matters for student loan repayment after graduation, holding all covariates constant.

Section 2 in Table 2, which contains the log-log models estimating the elasticity between the amounts borrowed and still owed by parents’ educational level, suggests that the children of more educated parents tend to hold a smaller amount of educational debt compared with their counterparts with less educated parents, even if they borrowed the same amount in student loans. To some extent, the coefficient sizes are decreased when the controls for educational variables are included. The greater repayment capacity of college graduates from high-SES families may be partly, but not substantially, attributed to the differences in quantity and quality of their education. The additional controls for labor market variables in model 3 barely reduce the coefficient size. This is because college graduates who obtained the same quantity and quality of higher education tend to have similar labor market outcomes regardless of their family background, as suggested by previous studies (Oh and Kim 2020; Zhou 2019). The most noteworthy finding is that controlling for an extensive set of educational and occupational variables does not erase the significance of the coefficients displayed in section 2.

According to model 3 of section 2, when the average log amount is borrowed, the amount still owed by men with GRAD parents is 21.0 percent (exp[–0.559] – 1) less than the amount owed by those with HS parents. Women with GRAD parents owe 23.2 percent less compared with their counterparts with HS parents who borrowed the average log amount. The elasticity between the amounts borrowed and still owed is also lower among college graduates with more educated parents, implying that parents’ education is positively associated with student loan repayment after graduation. As the amount borrowed increases by 10 percent, the amount still owed increases by 19.7 percent (exp[1.886 × ln(1.1)] – 1) and 21.8 percent for men and women with HS parents, respectively. The same loan amount increase raises the amount still owed by 16.0 percent (exp[(1.886 – 0.331) × ln(1.1)] – 1) and 15.8 percent for men and women with GRAD parents. The results consistently support hypothesis 2b, that student loan repayment varies by family background among college graduates, controlling for an extensive set of demographic, educational, and occupational covariates.

Using the results obtained from model 3 in Table 2, in Figure 1 I display the expected changes in the probability of still being indebted and the log amount still owed associated with a one-unit change in the log amount borrowed. For both men and women, the association between the log amount borrowed and the probability of still being indebted (left) and that between the log amounts borrowed and still owed (right) are weaker for those with more educated parents. That is to say, parents’ educational level is positively associated with the capacity to repay student loans after graduation.

Expected changes in probability of still being indebted and log amount still owed associated with one-unit change in log amount borrowed.

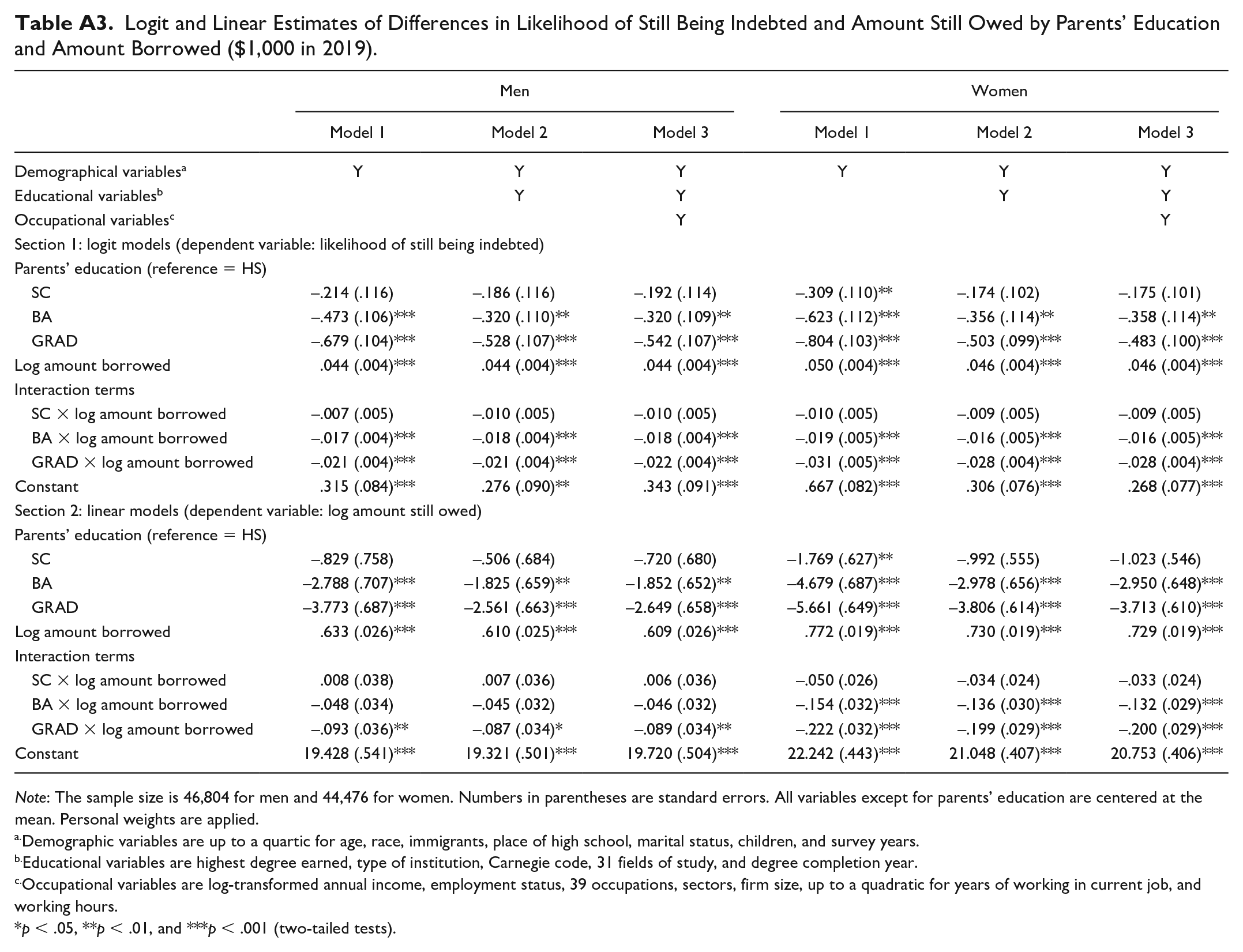

As a sensitivity analysis, I estimate the same models using the real amounts borrowed and still owed, rather than log-transformed amounts (Table A3), finding no substantial difference from the main results. Compared with Table 2, the directions and significance of the coefficients in Table A3 are not much different. When the average real amount (approximately $36,000) is borrowed, the likelihood of still being indebted as of the survey year is lower among men and women with GRAD parents compared with their same-gender counterparts with HS parents. As the real loan amount increases, the debt amounts of men and women with HS parents increase more rapidly than those of men and women with GRAD parents. Similarly, when the average real amount is borrowed, the debt amount as of the survey reference year is $19,720 and $20,753 for men and women with HS parents and $17,071 ($19,720 – $2,649) and $17,040 for men and women with GRAD parents. As the original student loan amount increases by $1, the average remaining debt amount increases by $0.61 and $0.73 for men and women with HS parents and $0.52 and $0.53 for men and women with GRAD parents. The sensitivity analyses corroborate the positive association between parents’ educational level and student loan repayment after graduation net of all covariates considered in this study (hypothesis 2b).

Variations across Educational Groups

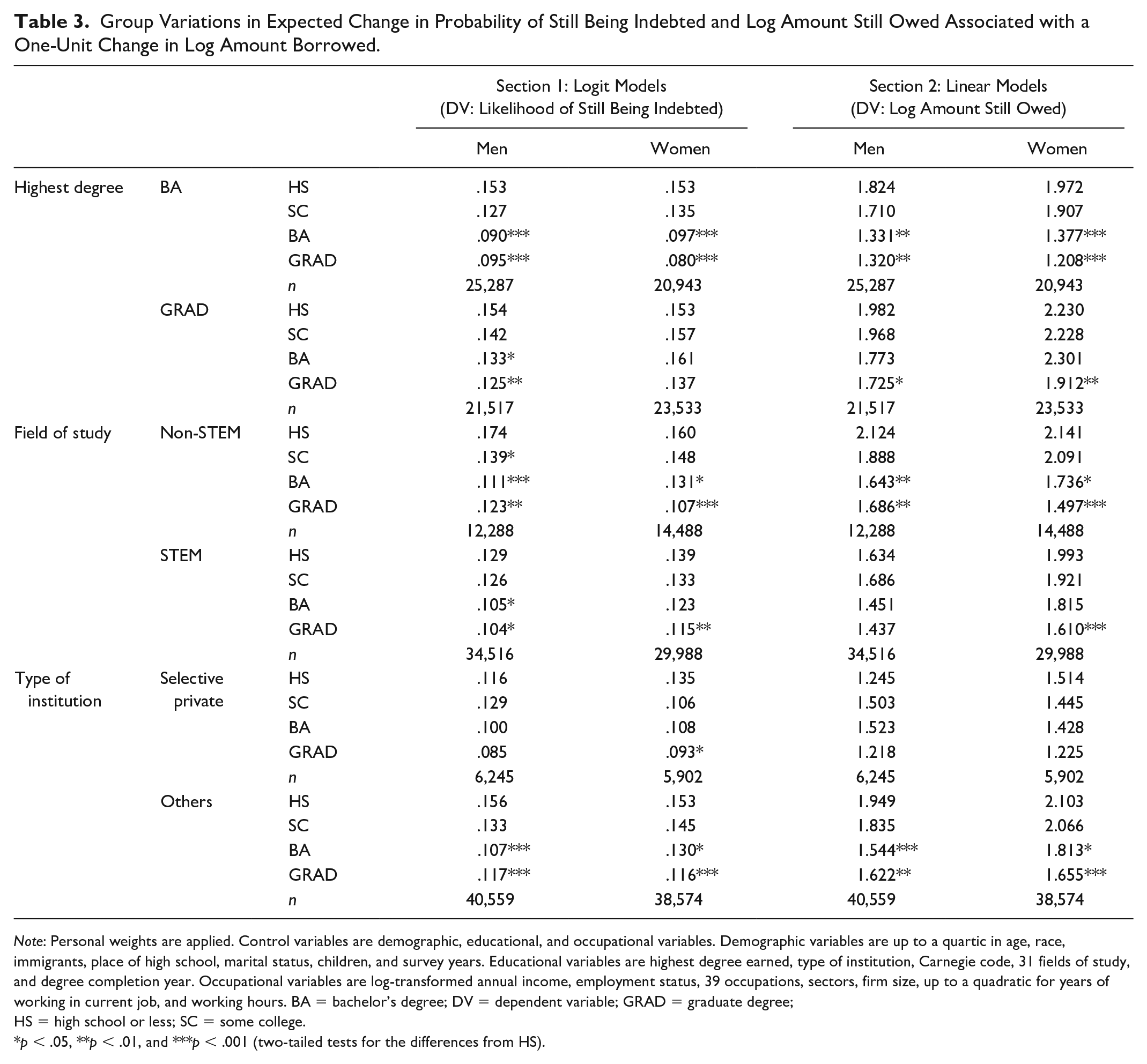

Recent studies report that socioeconomic associations between parents and college-educated children vary depending on the children’s specific educational outcomes, indicating substantial heterogeneity and stratification among college graduates (Manzoni 2021; Oh and Kim 2020; Torche 2011). To further examine whether the association between parents’ education and student loan repayment varies by children’s educational outcomes, I estimate the models separately by highest degree attained (bachelor’s degree or graduate degree), field of study for the highest degree (science, technology, engineering, and mathematics [STEM] or non-STEM), and type of institution conferring the highest degree (selective private institutions or others). Following the classification of Hersch (2019) and Oh and Kim (2020) on the basis of the Carnegie classifications and Barron’s Profiles of American Colleges, I define Private Research I/II and Private Liberal Arts I as selective private institutions. The results are shown in Table 3.

Group Variations in Expected Change in Probability of Still Being Indebted and Log Amount Still Owed Associated with a One-Unit Change in Log Amount Borrowed.

Note: Personal weights are applied. Control variables are demographic, educational, and occupational variables. Demographic variables are up to a quartic in age, race, immigrants, place of high school, marital status, children, and survey years. Educational variables are highest degree earned, type of institution, Carnegie code, 31 fields of study, and degree completion year. Occupational variables are log-transformed annual income, employment status, 39 occupations, sectors, firm size, up to a quadratic for years of working in current job, and working hours. BA = bachelor’s degree; DV = dependent variable; GRAD = graduate degree; HS = high school or less; SC = some college.

p < .05, **p < .01, and ***p < .001 (two-tailed tests for the differences from HS).

The degree of the positive association between parents’ education and student loan repayment after graduation is smaller among graduate degree holders than bachelor’s degree holders, and it is also smaller for STEM majors compared with non-STEM majors. Likewise, the positive relationship between parents’ education and student loan repayment is rarely significant among those who graduated from selective private schools, partly because of the small sample size of this group. However, the variations across educational groups are not statistically significant. Furthermore, for all educational groups, the associations between the amount borrowed and still owed tend to be weaker among those with more educated parents, supporting hypothesis 2b that parents’ SES is positively related to college graduates’ student loan repayment, holding all covariates constant.

As previous studies suggest the racialization of borrowing and repaying of student loans (Houle and Addo 2019; Scott-Clayton and Li 2016; Seamster and Charron-Chénier 2017), I also explore racial/ethnic differences. Consistent with the main findings, the additional analyses (not shown here) indicate that the educational debt burden declines as parents’ educational level increases among white, Hispanic, and Asian college graduates, yet this trend is relatively less clear among their Black counterparts. Compared with other racial/ethnic groups, Black college graduates seem to have relatively high probabilities of still owing and holding a large amount of education debt, regardless of their parents’ educational level. However, I should refrain from emphasizing racial/ethnic differences in this article because I cannot identify immigrant parents who completed their highest level of education outside of the United States due to the data limitations. Historical differences in immigration among racial/ethnic groups and the lower value of foreign education in the U.S. labor market could complicate the interpretation of the racial/ethnic disparities (Bankston and Hidalgo 2006; Zeng and Xie 2004), but the exploratory analyses certainly merit future studies into differences in student loan repayment by race/ethnicity.

Discussion

Motivated by the paucity of studies into inequality in student loan repayment after graduation (Baker et al. 2017; Dwyer 2018), this research has examined the association between family background and college graduates’ student loan repayment. The findings show that college graduates from lower SES families are more likely to hold a large amount of educational debt in adulthood, holding the amount borrowed constant. The positive association between parents’ SES and college-educated children’s student loan repayment is significant, even after controlling for various socioeconomic covariates.

One may suspect that these findings could be explained by other covariates unobserved in this study. I cannot completely rule out this possibility, but this study includes an extensive set of covariates relating to college graduates’ demographic characteristics, education, occupation, income, and other labor market outcomes. Arguably, the control variables used in this study include most of the covariates that previous studies have considered to be associated with family background or loan repayment, if not more (Baker et al. 2017; Bloome et al. 2018; Dwyer 2018; Gross et al. 2009; Hout 1988; Oh and Kim 2020; Torche 2011). The addition of these extensive controls rarely changes the statistical significance of the positive association between parents’ education and student loan repayment. The inclusion of other unobserved variables would not yield a substantial difference from the results reported in this article.

I used the IPWRA method to address sample selection bias, but there is no panacea that can completely remove potential selection bias. For example, compared with those from low-SES families, student loan borrowing may be more optional among college students from high-SES families, as those students may take a student loan only when they anticipate repaying it in a short period. I also note that my analyses focused on college graduates and excluded those who dropped out because, inspired by the great equalizer argument, This research aimed to evaluate the association between family background and student loan repayment among college graduates. Future studies should pay greater attention to college noncompleters. College students from lower SES families are more likely to leave college with debt and no diploma, and those without a college degree are more likely to have severe difficulties competing in the labor market and repaying their student loans than college graduates (Baker et al. 2017). Thus, a study that includes dropouts may show a stronger positive association between parents’ SES and student loan repayment compared with that reported in this research. In addition, the NSCG data do not contain information about the sources of student loans (e.g., schools, banks, or government). Different obligations required by various student loan programs may partly account for the association between family background and student loan repayment. The various flavors of debt cancelation programs also may be related to my findings. Last, as this research used retrospective information, there are potential errors in self-reported responses. The calculation, however, of the average loan amount using the NSCG data is almost equal to the statistics provided by NCES (2020). Pyne and Grodsky (2020) also suggested that the loan amounts reported by NSCG respondents are reliable. Although this study’s limitations may leave certain lacunae in the analysis, I do not believe these shortcomings substantially alter the main findings of this study or their implications.

This research raises a new question about why some high-SES families facilitate their children’s student loan repayment after graduation instead of helping them refrain from taking out a student loan in the first place. I suspect several potential mechanisms driving the positive association between family background and student loan repayment. Previous studies indicate that student loans do not necessarily hinder college students’ academic performance (Baker et al. 2017; Dwyer et al. 2012; Quadlin and Rudel 2015; Zhan 2014). In fact, a small amount of debt tends to increase rates of college enrollment and completion, although massive debt does not (Dwyer et al. 2012; Zhan 2014). Quadlin and Rudel (2015) also suggested that some indebted students actively engage in both study and part-time work. Similarly, students working between 10 and 19 hours per week have higher grade point averages than not only those who work longer hours but also those who work shorter hours (Dundes and Marx 2006). This appears to be due at least in part to the fact that students fully funded by their affluent families tend to enjoy campus life rather than study hard (Armstrong and Hamilton 2013). That is, student loans and working experience, to some extent, can encourage college students to appreciate their educational opportunities and to take greater responsibility for their educational outcomes. Some high-SES parents may let their children take a student loan to raise their sense of independence and responsibility, as well as to cultivate skills necessary to manage economic difficulties during early adulthood. It should also be noted that, compared with other types of loans, student loans are low-cost and low-risk sources of liquidity for wealthy families (Dwyer 2018). For affluent families, then, paying for college out of pocket might come with an opportunity cost, given that they may be able to take advantage of student loan credit to fund their children’s education and invest their liquid cash in highly profitable investments (e.g., stocks).

However, there is no reason for high-SES families to allow their children to default on their student loans, an event resulting in serious financial consequences, including withheld tax returns, decreased credit scores, and an inability to get a mortgage (Baker et al., 2017; U.S. Department of Education 2020). College graduates with educational debt also experience severe mental stress (Doran et al. 2016; Tran et al. 2018). Gross et al. (2009) explained that high-SES families provide a financial safety net to protect their children from student loan defaults. College graduates from high-SES families may take advantage of abundant financial resources in their families, particularly when they face economic downturns difficult for individual young adults to weather without support. In contrast, because of the lack of sufficient financial support from their families, many students from low-SES families may have no option but to rely on a student loan to fund their education, and their families may be unable to provide a sturdy financial safety net that cushions them against financial fluctuations later on.

Another possibility is that the association between family background and student loan repayment is not an intentional consequence of parents’ interventions. In addition to children’s educational attainment, family background has effects on their homeownership (Hall and Crowder 2011; Lee et al. 2020), childrearing (Anderson, Sheppard, and Monden 2018; Pfeffer and Killewald 2018), and the accumulation of wealth (Charles and Hurst 2003; Rauscher 2016). Financial support and wealth transmission would thus likely enable college graduates from high-SES families to ease other financial constraints and more quickly settle their educational debt. These explanations imply that family background has effects on various aspects of college graduates’ life chances over time. The mechanisms behind the effects of family background on student loan repayment and other socioeconomic matters beyond college graduation are worth further investigation.

Conclusion

Until the late twentieth century, previous studies suggested that a college degree is the great equalizer that enables children from low-SES families to reach socioeconomic parity with high-SES families (Hout 1984, 1988). Although it is still true that higher education increases the chance of upward social mobility for children from low-SES families, recent studies show substantial associations between family background and college graduates’ socioeconomic outcomes, indicating that a college degree does not guarantee socioeconomic parity between children from low- and high-SES families in the twenty-first century (Oh and Kim 2020; Torche 2011; Witteveen and Attewell 2017). This research contributes to the previous literature by illuminating the positive association between family background and student loan repayment after graduation. Through higher education, many students from low-SES families strive to increase their opportunities to earn a high income and to achieve upward social mobility. Increases in student loans, however, have limited the potential for higher education to provide upward social mobility for children from low-SES families. As rising college tuition has fueled the growth of student loans, many indebted college graduates have increasingly suffered from financial constraints and psychological distress.

The findings reported in this article have implications for the ongoing debate on student debt cancellation programs. Opponents of student debt cancellation programs argue that these programs are regressive because they would help an already privileged group (Catherine and Yannelis 2020). In contrast, other scholars have found evidence that universal student loan forgiveness would provide more benefits to the disadvantaged groups, such as those without wealth and racial minorities (Charron-Chenier et al. 2020; Eaton et al. 2021). This study supports the latter by showing that the same amount of debt could be more burdensome for college graduates from lower SES familes. During economic crises, such as the coronavirus disease 2019 pandemic, high-SES families would provide a financial safety net that helps their children repay student loan with out disruption. This financial support from families would not be available to college graduates from low-SES families. Universal debt forgiveness programs will particularly alleviate educational debt burdens for college graduates from low-SES families. It should be also noted that the effects of universal student loan cancellation will be immediate but temporary. A mass higher education system that charges high costs for individual students and their parents will continue to reproduce the uneven playing field in the long run. This research calls for policy interventions that provide more accessible financial aids for college students from low-SES families and future studies into the mechanisms that maintain intergenerational socioeconomic associations beyond college graduation.

Footnotes

Appendix A

Logit and Linear Estimates of Differences in Likelihood of Still Being Indebted and Amount Still Owed by Parents’ Education and Amount Borrowed ($1,000 in 2019).

| Men | Women | |||||

|---|---|---|---|---|---|---|

| Model 1 | Model 2 | Model 3 | Model 1 | Model 2 | Model 3 | |

| Demographical variables a | Y | Y | Y | Y | Y | Y |

| Educational variables b | Y | Y | Y | Y | ||

| Occupational variables c | Y | Y | ||||

| Section 1: logit models (dependent variable: likelihood of still being indebted) | ||||||

| Parents’ education (reference = HS) | ||||||

| SC | –.214 (.116) | –.186 (.116) | –.192 (.114) | –.309 (.110)** | –.174 (.102) | –.175 (.101) |

| BA | –.473 (.106)*** | –.320 (.110)** | –.320 (.109)** | –.623 (.112)*** | –.356 (.114)** | –.358 (.114)** |

| GRAD | –.679 (.104)*** | –.528 (.107)*** | –.542 (.107)*** | –.804 (.103)*** | –.503 (.099)*** | –.483 (.100)*** |

| Log amount borrowed | .044 (.004)*** | .044 (.004)*** | .044 (.004)*** | .050 (.004)*** | .046 (.004)*** | .046 (.004)*** |

| Interaction terms | ||||||

| SC × log amount borrowed | –.007 (.005) | –.010 (.005) | –.010 (.005) | –.010 (.005) | –.009 (.005) | –.009 (.005) |

| BA × log amount borrowed | –.017 (.004)*** | –.018 (.004)*** | –.018 (.004)*** | –.019 (.005)*** | –.016 (.005)*** | –.016 (.005)*** |

| GRAD × log amount borrowed | –.021 (.004)*** | –.021 (.004)*** | –.022 (.004)*** | –.031 (.005)*** | –.028 (.004)*** | –.028 (.004)*** |

| Constant | .315 (.084)*** | .276 (.090)** | .343 (.091)*** | .667 (.082)*** | .306 (.076)*** | .268 (.077)*** |

| Section 2: linear models (dependent variable: log amount still owed) | ||||||

| Parents’ education (reference = HS) | ||||||

| SC | –.829 (.758) | –.506 (.684) | –.720 (.680) | –1.769 (.627)** | –.992 (.555) | –1.023 (.546) |

| BA | –2.788 (.707)*** | –1.825 (.659)** | –1.852 (.652)** | –4.679 (.687)*** | –2.978 (.656)*** | –2.950 (.648)*** |

| GRAD | –3.773 (.687)*** | –2.561 (.663)*** | –2.649 (.658)*** | –5.661 (.649)*** | –3.806 (.614)*** | –3.713 (.610)*** |

| Log amount borrowed | .633 (.026)*** | .610 (.025)*** | .609 (.026)*** | .772 (.019)*** | .730 (.019)*** | .729 (.019)*** |

| Interaction terms | ||||||

| SC × log amount borrowed | .008 (.038) | .007 (.036) | .006 (.036) | –.050 (.026) | –.034 (.024) | –.033 (.024) |

| BA × log amount borrowed | –.048 (.034) | –.045 (.032) | –.046 (.032) | –.154 (.032)*** | –.136 (.030)*** | –.132 (.029)*** |

| GRAD × log amount borrowed | –.093 (.036)** | –.087 (.034)* | –.089 (.034)** | –.222 (.032)*** | –.199 (.029)*** | –.200 (.029)*** |

| Constant | 19.428 (.541)*** | 19.321 (.501)*** | 19.720 (.504)*** | 22.242 (.443)*** | 21.048 (.407)*** | 20.753 (.406)*** |

Note: The sample size is 46,804 for men and 44,476 for women. Numbers in parentheses are standard errors. All variables except for parents’ education are centered at the mean. Personal weights are applied.

Demographic variables are up to a quartic for age, race, immigrants, place of high school, marital status, children, and survey years.

Educational variables are highest degree earned, type of institution, Carnegie code, 31 fields of study, and degree completion year.

Occupational variables are log-transformed annual income, employment status, 39 occupations, sectors, firm size, up to a quadratic for years of working in current job, and working hours.

p < .05, **p < .01, and ***p < .001 (two-tailed tests).

Acknowledgements

I thank the editors, the two anonymous reviewers, ChangHwan Kim, Dara Shifrer, Emily Rauscher, Arthur Sakamoto, Robert Antonio, and Matt Erickson for constructive comments.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the Doctoral Dissertation Research Improvement Award from the National Science Foundation (SES-1801820).