Abstract

Shareholder activism is a contentious field where investors confront management over governance and social responsibility matters. Most prior research on shareholder activism focuses on firm traits, such as performance, that explain targeting. We argue that shareholder activism also reflects endogenous dynamics. Although activists target firms because of their characteristics, activists also choose targets based on their position in the relational field. We develop a network approach to mapping contentious fields: Shareholder activism is a social network whose topology reflects self-organizing patterns. We hypothesize four network effects thought to contribute to the observed structure: prolificacy, ignominy, differentiation, and homophily. We use data on shareholder-sponsored proposals targeting Fortune 250 firms between 2006 and 2013. Results from exponential random graph models support our hypothesized effects and suggest that activism sponsorship and targeting follow an endogenous cumulative process. We argue that these self-organization processes help explain the structure of the shareholder activism network.

Introduction

Over the past two decades, shareholder activism has moved from a comparatively rare event to a regular occurrence. As shareholders have gained increased power relative to corporate boards and top managers, investors increasingly attempt to influence corporate decision making and raise public awareness through activism. As a result, shareholder activism has become a central arena in contests for corporate control and concerns over corporate social responsibility (CSR) (Gillan and Starks 2007). One prominent form of activism is the investor-sponsored proposal. In a typical activism scenario, an investor submits a proposal to appear in the annual corporate proxy statements and to be voted on by all shareholders at the annual meeting. Activists typically use proxy access to promote shareholder-friendly changes in corporate governance or advocate for social, political, or environmental issues in the context of the firm’s operations (Goranova and Ryan 2014). Both governance and CSR shareholder activism nearly always results in confrontation between managers and investors, and these confrontations have become more common (Copland and O’Keefe 2015). Proposals have also won increased voting success and are becoming more effective and winning reforms (Renneboog and Szilagyi 2011).

Most research in finance and management examines characteristics of the proposal’s sponsor, target firm, or the proposal itself as important determinants of activism targeting. For instance, many studies consider how a firm’s governance structure, financial performance, or CSR performance predict targeting (Ertimur, Ferri, and Stubben 2010; Goranova and Ryan 2014). Alternatively, organization scholars have long conceptualized shareholder activism through the lens of social movement theory and related theories of organizational fields. Fields are relational arenas comprised of actors, actions, and relations “whose participants take one another into account as they carry out interrelated activities” (McAdam and Scott 2005:10). Scholars have primarily used this theoretical construct to explain how a firm’s position in a broader field predicts activism targeting and outcomes (Bartley and Child 2014; G. F. Davis and Thompson 1994; King and Soule 2007; McDonnell, King, and Soule 2015).

However, one of the primary insights of field theory is that interactions aggregate into larger macro-level patterns that actors then confront when making decisions about future action (Fligstein and McAdam 2012; Giddens 1984; Martin 2003). Conceptually, strategic action within an institutional field reflects endogenous dynamics—an actor’s behavior is both self and other referencing, leading self-organizing dynamics in the field’s structure. Relatedly, some scholars have proposed using network methods to map interactions (e.g., interorganizational alliances) within fields in order to represent them as structures of interdependent roles (Martin 2003; Powell et al. 2005; D. R. White et al. 2004). These empirical representations can be particularly useful because network modeling techniques now allow researchers to gain greater empirical leverage on endogenous network dynamics (where existing tie structures affect new tie formation), which have long been theorized to be crucial mechanisms driving field structure (Powell et al. 2005).

This article develops an innovative network analytic approach to field mapping in shareholder activism, a contentious field. We develop an approach that maps shareholder activism incidents as network ties linking activist investors to target firms. This innovation allows us to examine not only how firm and activist traits affect proposal targeting but also how activism events are situated in a relational structure with its own self-organizing dynamics. Answering calls to extend mechanism-based theorizing on the structure of organizational fields (G. F. Davis and Marquis 2005), we draw on social network theories of embedded action to investigate how endogenous dynamics drive the structure of the shareholder activism field.

Shareholder activism (both governance and CSR related) displays several surprisingly stable structural regularities that have yet to be fully appreciated in existing activism research. For instance, despite the increased incidents of shareholder activism over the past decade, most shareholder proposals are fairly concentrated among a relatively small number of highly active sponsors, including individuals, socially responsible investors (SRIs), and union pension funds. In 2012, just three individuals and their family members accounted for nearly 30 percent of all proposals targeting Fortune 250 firms. 1 A handful of religiously affiliated SRIs, particularly those affiliated with the Catholic Church, accounted for another 29 percent. On the firm side, proposal targeting is also concentrated among a relatively small set of highly ignominious firms who attract a disproportionate number of corporate governance and CSR proposals. More broadly, both the sponsor side and target side exhibit long-tail distributions in their involvement in activism incidents—while there are a small number of highly active sponsors (and ignominious targets) each year, most sponsors (and firms) are involved in very few (if any) activism events each year. Variation in the usual firm-level traits (e.g., the firms’ governance structure, performance, or SRI reputation) are unlikely to explain these structural regularities because these traits are more widely distributed across firms. Alternatively, social network scholars note that such scale-free structures are often the result of preferential attachment dynamics whereby new ties are more likely to attach to well-connected actors (Barabasi and Albert 1999). In our context, this raises the question of whether shareholder activism self-organizes in a similar way.

We draw on theoretical and methodological traditions in social network approaches to field dynamics to analyze the relational structure of shareholder activism, particularly the endogenous dynamics that drive field self-organization (Martin 2003; Powell et al. 2005). We first offer a brief background discussion on the state of research on shareholder activism. We then elaborate our theoretical foundations for developing a network-based field-theoretic approach to shareholder activism. We develop a novel method of representing an annual proxy season as a network where ties represent shareholder-sponsored proposals. The networks are defined as two-mode graphs consisting of two distinct node classes—proposal sponsors and targets. We apply exponential random graph models aimed at parameterizing the generative mechanisms that produce the activism network’s observed structure. In addition to the usual firm and sponsor covariates, we focus on five structural determinants hypothesized to affect shareholder activism—activity, ignominy, activity-ignominy assortativity, strategic congruence/differentiation, and homophily.

The network analysis offers new insights into the relational structure of the field and allows us to explore factors that go beyond firm- and sponsor-centric characteristics. Findings indicate that endogenous self-organizing dynamics are important determinants in shareholder activism. First, we find that activists sort into highly prolific and less prolific activism profiles. Second, we find that activists are more likely to target firms that have been widely targeted by other activists, producing a cumulative ignominy effect where some activism leads to additional activism. Third, we find that the most prolific activists disproportionately target the most ignominious firms. Finally, activists select target firms such that they do not substantially overlap with other activists in the field. Thus, most activists avoid clustering into dense communities in the activism space and carve out specialized niches where they focus on targeting a select set of firms that other activists do not target.

We proceed by briefly reviewing background material on shareholder activism and then develop our theory of endogenous dynamics in contentious fields. We present our analysis of two-mode activism networks and conclude with a discussion of implications and directions for future research.

Background on Shareholder Activism

Shareholder activism refers to a system where investors can voice their concerns about the governance, performance, and corporate social responsibility matters in the firms where they invest. There are a number of activism avenues available to investors, including negotiating directly with the board and management, attempting a takeover, or submitting proposals to be voted on by all shareholders. Shareholder proposals in particular have become more common in recent years, particularly because they represent an activism avenue available to even marginal investors with limited resources, including labor unions or individual retail investors (Gillan and Starks 2007). Governance-related proposals often attempt to reform executive compensation, repeal takeover defenses, or improve shareholder voting rights. Alternatively, CSR proposals can reflect the interests of diverse corporate stakeholders and address a wide range of issues that include environmental impact, worker’s rights, animal welfare, political activities, and social inequality (Goranova and Ryan 2014). In a typical scenario, the sponsoring shareholder submits the proposal to be included in the firm’s annual proxy statement and investors vote on the proposals at the annual meeting or via proxy ballot. Through the proposal process, activists can exert reputational penalties, induce director turnover, or increase scrutiny from the media or shareholder advocacy groups (Ertimur, Ferri, and Stubben 2010; Hillman et al. 2010; Ward, Brown, and Graffin 2009).

Most prior research, particularly in finance and management scholarship, focuses on the characteristics of the targeted firm, the proposal sponsor, or the proposal itself (Goranova and Ryan 2014). Most evidence indicates that firm size and performance drive shareholder activism (Goranova and Ryan 2014). Larger firms are far more likely to be targeted by both CSR and corporate governance activists because they may be more prone to agency problems (Jensen and Meckling 1976), have greater potential to create value for activists (Del Guercio and Hawkins 1999), or capture greater public and media attention (Ferri and Sandino 2009; Rehbein, Waddock, and Graves 2004). Additionally, activists disproportionately target firms with poor operating or stock market performance (Ertimur, Ferri, and Muslu 2010; Renneboog and Szilagyi 2011), governance problems (Ertimur, Ferri, and Stubben 2010; Renneboog and Szilagyi 2011), and excessive CEO compensation. Not surprisingly, SRI activists tend to target firms with poor records for environmental or social responsibility performance (Rehbein et al. 2004).

Several sponsor-level factors are also important. In general, powerful institutional investors constitute a more salient activism threat than individual investors or SRI sponsors (Cheffins and Armour 2011; Gordon and Pound 1993; Ryan and Schneider 2002). Large and concentrated institutional investors are better able to mobilize resources and assemble supportive voting blocs during an activism event. As a result, proposals that are sponsored by institutional investors tend to receive more voting support (Gillan and Starks 2000; Gordon and Pound 1993) and are more likely to be implemented by the firm (Renneboog and Szilagyi 2011).

However, despite their limited effectiveness, individual “gadflies” and SRI activists are the most active proposal sponsors, targeting a wider set of firms over a diverse set of issues (Copland and O’Keefe 2013). This activism imbalance may be somewhat surprising. Given their large and concentrated holdings, institutional investors stand to earn greater returns from their activism, increasing their willingness to bear the costs of direct negotiations with management or lengthy reform efforts at portfolio firms (Ryan and Schneider 2002). Individuals and SRI activists, in contrast, rarely receive sizable financial benefits from their activism. Instead, individual and SRI activists more closely resemble “issue entrepreneurs” in their respective domains (governance and CSR issues, respectively) by defining and promoting grievances for a broader audience (McCarthy and Zald 1977). Many of the most aggressive gadflies and SRI activists claim that their goals are not simply to achieve reforms at targeted firms but to publicize good governance norms or CSR practices (McDonnell et al. 2015; Solomon 2014).

Finally, several proposal-level factors are important. Investors have been particularly successful in using ballot access to encourage governance reforms, especially in recent years (Gillan and Starks 2007). In general, proposals that target the repeal of takeover defenses or attempt to reform audit procedures have been among the most successful at attracting shareholder voting support and gaining implementation from the board (Renneboog and Szilagyi 2011). Although CSR proposals have been less successful at attracting shareholder votes or winning implementation, it is clear that these proposals have helped raise CSR’s profile in the media and public awareness and are often part of broader social movement campaigns.

A Field Framework of Shareholder Activism

While research in management and finance focuses on the firm, sponsor, and proposal determinants of shareholder activism, scholars in sociology and organization studies draw on social movement theory and field theory to examine both corporate governance and CSR-related activism (Bartley and Child 2014; G. F. Davis and Thompson 1994; King and Soule 2007; McAdam and Scott 2005). Much of this work focuses on how activists and target firms are situated in organizational fields and how these contextual factors affect target selection, resource mobilization, and strategies for action. Two themes in particular are worth noting. First, the structure of an organizational field can affect political opportunities to promote governance or SRI reforms. For instance, activism campaigns can hasten the diffusion, or spillover effects, of reforms in the broader field (Strang and Soule 1998). Reid and Toffel (2009) find that firms are more likely to adopt climate change disclosure policies when other firms in their industry have been targeted by related shareholder resolutions. Other researchers report similar effects of corporate governance–related shareholder activism in the diffusion of investor relations departments (Rao and Sivakumar 1999) and employee stock options expensing (Ferri and Sandino 2009). Because of the potential for spillover effects, a firm’s position in the broader field can affect its susceptibility for being targeted, and evidence suggests that highly visible firms make particularly politically opportune targets (Bartley and Child 2014; King 2008).

A second theme highlights how mobilizing structures in the field, including formal organizations and social networks, facilitate collective action among diverse corporate stakeholders, including shareholders, which can in turn help coordinate their interests and engage in more salient activism (McAdam and Scott 2005). Mobilizing structures help diverse stakeholders become aware of one another, cultivate common opinions and interests, and coordinate action (den Hond and Bakker 2007; King 2007). G. F. Davis and Thompson (1994) argue that mobilizing structures among investors, particularly the consolidation of institutional investors and their advocacy groups, helped facilitate the shareholder rights movement in the 1980s. Investors continue to coordinate their interests through formal organizations, including the Council for Institutional Investors, Institutional Shareholder Services, Inter-faith Center on Corporate Responsibility, proxy advisor firms, and informal social networks.

While this research stream has been highly generative, it has yet to develop a theoretical account for how endogenous dynamics affect shareholder activism. Many activist investors sponsor multiple proposals across corporate America, and firms are frequently targeted by diverse shareholders representing varied interests. Each shareholder activism event is embedded in a broader field of other activism events that include proposals sponsored by the focal investor at other firms, proposals sponsored by other investors at the focal firm, and proposals sponsored by other investors at other firms. The structure of this field situates activists and firms within a common relational structure that activists then confront when making future activism decisions. We argue that activists’ targeting decisions are in part an endogenous function of their own and other activists’ targeting decisions. This insight flows directly from field theories about how self-organizing dynamics drive the structure of organizational fields (Martin 2003; Powell et al. 2005; H. C. White, Boorman, and Breiger 1976).

Endogenous shareholder activism, as we conceive of it, rests on the idea that field participants take one another into account when pursuing strategic action (McAdam and Scott 2005). Shareholder activists (both governance and SRI) are quite aware of one another’s behavior. As stated previously, coordinating structures and institutions regularly spread information among activist investors about one another’s activities, voting outcomes, and firms’ responses. This information affects stakeholders’ perceptions of firm’s governance and SRI performance (Aguilera et al. 2007, 2015).

Anecdotal evidence also suggests that investors regularly account for other activists’ activities when making targeting decisions and presenting their arguments to relevant audiences. Indeed, when investors engage in activism, they typically deploy frames constructing legitimate governance and SRI behaviors, and these frames are informed by other activists’ behaviors. Consider the supporting statements that accompany shareholder proposals: When a shareholder proposal appears in a company’s annual proxy statement, it is typically accompanied by a supporting statement, prepared by the proposal’s sponsor, intended to convince other shareholders to vote in favor. These statements (as well as management’s opposition statements) are an important discursive arena where actors construct frames about activism and its goals. These statements often refer to other activists’ proposals at both the target firm and other firms. For example, in 2013, the activist investor John Chevedden included the following material in a supporting statement that accompanied a proposal to repeal supermajority voting requirements at Aetna Inc.:

This proposal topic won from 74% to 88% support at Weyerhaeuser, Alcoa, Waste Management, Goldman Sachs, FirstEnergy, McGraw-Hill and Macy’s. The proponents of these proposals included James McRitchie and Ray T. Chevedden. Currently a 1%-minority can frustrate the will of our 66%-shareholder majority that seeks to improve our corporate governance. Supermajority requirements are arguably most often used to block initiatives supported by most shareowners but opposed by a status quo management. (Aetna Inc. 2013)

In the supporting statement, John Chevedden references specific other investors (including his own father, Ray) and other firms who had been involved in similar activism incidents.

Even when investors do not identify specific other investors, they routinely link their proposals to successful activism campaigns at other firms. For example, the North Carolina Public Pension trust fund included the following material in its supporting statement accompanying a 2013 proposal to declassify 2 the board of directors at Kellogg Co.: “More than 50 precatory declassification proposals passed at annual meetings of S&P 500 companies and the average percentage of votes cast in favor of [these proposals] exceeded 75%” (Kellogg Company 2013).

In each case, the proposal sponsor references other activists’ successful proposals. Although these are interesting examples of strategic framing in activism efforts, they also provide evidence that activists are aware of one another’s behavior and they take it into account when pursuing strategic action. The practice of referencing other activists in supporting statements is widespread: In a sample of all supporting statements accompanying SRI and governance proposals targeting Fortune 250 firms during the 2013 proxy season, we found that over half mentioned at least one other activism event or successful reform effort.

Endogenous Determinants

Our key insight is that shareholder activism patterns not only reflect the characteristics of sponsors or targets but also reflect endogenous structural dynamics where activists’ strategies are affected by their own and others’ position in the field. Social network analysts have elaborated a set of endogenous structural determinants that contribute to observed network structures. By empirically representing shareholder proposals as network ties linking activist investors to targets, we make these endogenous field effects empirically tractable. These effects are endogenous in the sense that network patterns emerge from the internal processes, or self-organization, of the network itself rather than actors’ traits. Similar endogenous structural effects have been applied in diverse contexts such as friendship networks (Goodreau, Kitts, and Morris 2009), congressional legislative co-sponsorship networks (Cranmer and Desmarais 2011), international sanctions (Cranmer, Heinrich, and Desmarais 2014), and organization alliances (Powell et al. 2005).

Consider a two-mode network, where nodes can be classified into two distinct classes, or modes. Ties exist between nodes of different classes but never between nodes of the same class. A classic example of a two-mode network represents a bounded set of individuals, such as a town’s socialites, attending a set of events, such as parties (A. Davis, Gardner, and Gardner 1941). Although an analyst may not directly observe face-to-face interactions, they can infer the structure of relations among the individuals and events by inspecting co-attendance patterns in the network. As a result, individuals and the groups to which they belong constitute a dual structure (Breiger 1974).

Correspondingly, activists and the firms they target constitute a dual structure. We represent shareholder activism during an annual proxy season as a two-mode social network—nodes in the first mode represent activists while nodes in the second mode represent target firms. Ties represent proposals themselves. In what follows, we propose four endogenous structural determinants hypothesized to drive the activism network’s structure: ignominy and activity, ignominy-activity assortativity, strategic consensus versus strategic differentiation, and sponsor type homophily.

Ignominy and Activity

Consider a well-known endogenous structural effect found in empirical friendship networks: popularity (Moody et al. 2011). Popularity, or preferential attachment, is an endogenous structural determinant in the sense that people who are popular in a network tend to gain additional friends. More friends help one gain greater visibility, leading to additional friends. This translates into dispersion in the degree distribution where most actors have relatively few ties but a few actors have a large number of ties (Barabasi and Albert 1999). Endogenous popularity dynamics are by now a well-established phenomenon in friendship networks (Goodreau et al. 2009; Moody et al. 2011) as well as some interorganizational networks such as collaboration and alliances (Contractor, Wasserman, and Faust 2006).

Whereas popularity in a friendship network assumes that ties have a positive connotation, the same concept in other contexts, such as international sanctions or shareholder activism, has a negative connotation. Following Cranmer et al. (2014), we conceptualize accumulative negative ties as an “ignominy” effect. Shareholder activism is likely to attract negative attention for a focal firm, leading to the accumulation of ignominy in the field and still more activism. Prior work provides some indirect evidence of this endogenous effect. One of the strongest firm-level predictors of being targeted for activism in a given year (net of other traits) is having been targeted in a prior year, and this strong relationship holds independent of whether or not proposals are successful (Renneboog and Szilagyi 2011). This suggests that a strong cumulative effect drives shareholder activism targeting—being the target of past activism is associated with being targeted in the future. The top left panel of Figure 1 provides a visual diagram of the popularity structure centered on a targeted firm. As an endogenous structural determinant, this suggests that being highly targeted leads to additional targeting.

Hypothesis 1: Compared to firms that are not targeted, a firm that is targeted by some activists is more likely to be targeted by other activists (degree dispersion of nodes in the firm mode).

Structural effects diagrams in the shareholder activism network.

While the aforementioned describes the endogenous tendency for firms to be targeted, we also expect that similar processes drive activists’ prolificacy; structurally, this translates into a tendency for a small number of activists to sponsor many proposals. Consider corporate gadflies, “small investors who provoke management by repeatedly filing multiple substantially similar shareholder proposals at many companies” (Copland 2011:2). Corporate gadflies are small-stake individual investors (a node-level trait) with a disproportionate degree of activism across a large number of companies (a structural trait) (Sikavica and Tuschke 2012). Case histories of high-profile corporate gadflies such as John Chevedden, William Steiner, or James McRitchie portray their high rates of activism as a cumulative process: Gadflies began with only a few proposals at select firms but leveraged this notoriety into more activism (Duhigg 2007; Solomon 2014). Consequently, the role of corporate gadfly emerged as some actors pursued highly central positions in the shareholder activism network and differentiated themselves from other activists. Structurally, the role of corporate gadfly emerged over time as a highly active hub in the shareholder activism network. We expect similar endogenous structural effects among some activists in other investor classes, particularly public pensions (e.g., CalPERs, NYC Public Pension Funds), unions (AFL-CIO), or social investors (e.g., Catholic Church affiliates, PETA). In each of these investor classes, a handful of activists carve out niche positions as highly prolific sponsors known for promoting similar governance and SRI reforms across the entire corporate field. Meanwhile, most investors are more modest in their levels of activism, only targeting a select few firms but focusing on more firm-specific reforms.

The tendency for activism to be highly concentrated among a few highly prolific investors is likely to be a generalized endogenous feature of the shareholder activism network—some activists differentiate themselves by pursuing a wide variety of activism targets. This translates into degree activity of nodes in the activist mode of the two-mode graph. The top right panel provides a visual representation of the degree dispersion of an activist.

Hypothesis 2: An activist that sponsors some proposals is more likely to sponsor other proposals (degree dispersion of nodes in the activist mode).

Ignominy-Activity Assortativity

In the previous discussion, we suggest that activism tends to endogenously cluster among a few highly prolific proposal sponsors and a few highly ignominious target firms. However, we also expect that highly active sponsors are more likely to target highly ignominious firms while activists who sponsor few proposals will tend to target firms that attract fewer proposals. This assortativity on node degree reflects differentiated niches in activist and firm arenas. Activists who submit only a small handful of proposals may have neither the resources nor inclination to submit proposals across many firms. They are likely to adopt focused strategies that promote specific governance or SRI reforms at key firms where they invest rather than sweeping strategies aimed at field-level reforms. In pursuing a focused strategy, smaller scale activists selectively target firms that many other activists ignore. Conversely, highly prolific activists may seek to improve governance and SRI in the corporate field in general. Highly active shareholders tend to sponsor similar proposals across a number of firms and may be less invested in firm-specific reforms. Targeting highly ignominious firms furthers these goals. This translates into a positive degree correlation between activists and targets—activists who sponsor proposals against many firms are more likely to sponsor proposals against firms that are themselves highly targeted. Conversely, highly specialized activists that target only a few firms are more likely to target firms that receive fewer proposals.

Hypothesis 3: Highly prolific sponsors are more likely to target highly ignominious firms, and low activity sponsors are more likely to target less ignominious firms (sponsor-target degree assortativity).

Strategic Congruence Versus Strategic Differentiation

Clustering is an important structural network effect—two actors who each have ties to a common third will tend to close the triangle and form a relation. In friendship networks, triadic closure may be due to a greater likelihood of frequent contact through the common third actor or cognitive tendencies to hold favorable views toward friends of friends (Goodreau et al. 2009). This clustering can give rise to larger cohesive community structures as new friendships endogenously form out of the pattern of existing friendships.

We might expect similar community structures in the shareholder activism network. However, closed triangles are not possible in two-mode networks because a relation cannot exist between nodes in the same mode (e.g., an activist could not target another activist). In two-mode networks, four-cycles are the analogous network structure—when a pair of nodes in the first mode are each tied to a common pair of nodes in the second mode. In the shareholder activism network, a four-cycle reflects overlap or reinforcement in two activists’ targeting: A pair of activists each target the same pair of firms. The center panel of Figure 1 provides a visual representation of the four-cycle effect in the shareholder activism network. The left graph displays a completed four-cycle—both activists target both firms. In a large network, high levels of activism overlapping suggest a strategic consensus among activists. To the extent that a group of activists target the same set of firms, these activists are pursuing a similar niche in the shareholder activism network. Activists may look to peers for cues about which firms to target and may attempt to choose targets that coincide with other activists. If observed, this targeting consensus could be facilitated by third parties like proxy advisors. As a structural determinant, strategic congruence is represented by a positive four-cycle effect or the tendency for four-cycles to appear in greater number than would be expected if ties were random.

Hypothesis 4a: Activists who target the same firm are more likely to target additional firms in common (positive four-cycles).

The right diagram in the center panel of Figure 1 displays an alternative scenario where activists pursue distinct activism niches and refrain from overlapping with other investors. Here activists do not overlap in the firms they target—activists who target a common firm will tend not to target additional firms in common. Activism sponsorship and support requires considerable resources and effort on the part of sponsoring shareholders. Activists may prefer not to substantially overlap with other activists in an effort to avoid redundant activism agendas that waste resources. In such a case, activists will attempt to define differentiated niches in the activism network rather than reinforcing other activists’ targeting. As an endogenous structural determinant, strategic differentiation is represented by a negative four-cycle effect—four-cycles appear less commonly than if ties were random.

Hypothesis 4b: Activists who target the same firm will tend not to target additional firms in common (negative four-cycles).

Sponsor Type and Homophilous Targeting

In addition to the endogenous network effects described previously and the usual firm-level covariates, we expect that different types of activist investors pursue distinct activism agendas that reflect varying levels of prolificacy. To test these ideas, we categorize proposal sponsors into four types: individuals, public pensions, unions, and social responsibility investors. 3 First, we expect differences in the dispersion of each type of investor’s activism profile. Individual activists, with their antagonistic approach toward management, and SRI activists, with broad reaching CSR concerns, are more likely to resemble social movement entrepreneurs than other types of investors. Reflecting their distinct strategies and position in the field, individual investors and SRIs are more likely to target a wide range of firms with prolific activism. As discussed previously, a few high-profile individual activists, such as John Chevedden, are particularly aggressive at pursing activism agendas across the entire field in an effort to affect governance and raise their own profile. Similarly, socially responsible investors tend to sponsor proposals across a wide range of companies in an effort to have a broader impact, induce spillover effects, and gain greater visibility. Conversely, public and union pension funds are more likely to pursue nuanced agendas related to the specific governance goals or organizing strategies at a subset of firms. Public pensions in particular have increasingly withdrawn from overt activism and have instead redeployed their efforts toward private negotiation with management, reserving public activism for situations where negotiations fail (Gillan and Starks 2007). Unions often use shareholder activism as part of an organizing strategy, focusing on firms where activism is linked to other union activities. In network terms, these expectations translate into higher activity among individuals and SRI activists as compared to other types of investors.

Hypothesis 5: Individual and SRI activists are more active (positive degree in the activist mode) than other types of investors.

In addition to differences in prolificacy, we also expect homophily (or similarity) effects in the network. Independent of other structural effects and covariates, we expect that investors of the same type are more likely to target common firms, particularly less salient investor groups like individual and CSR activists. While large and powerful institutional investors are better able to advocate for their own agenda through private negotiations and sizable voting blocs, individual and CSR activists are more confined to public proposals that attract less voting support. An investor is prohibited from submitting multiple proposals to the same firm during a single proxy season; however, activists can coordinate their proposals to achieve greater impact. In the absence of formal resources, individual and CSR activists are more likely to coordinate with similar marginalized investors to challenge firms. This tactic can generate greater public attention as well induce negative evaluations from corporate governance or CSR analysts. For example, multiple individual or CSR activists may reach a strategic consensus about which firms should be targeted, leading similar types of investors to homophilously target common firms.

In single mode networks, such as friendship networks, homophily predicts that two actors who are similar on some trait, such as race or gender, are more likely to form a tie (Goodreau et al. 2009). In the two-mode case, where nodes in separate modes have different characteristics, homophily predicts that nodes at distance-two are more likely to be similar on some trait. In the present context, this means that two activists of the same type (individual, public pensions, unions, SRI) are more likely to select targets in common (e.g., individuals tend to target firms that other individuals target). This effect reflects strategic consensus among investors of the same type. We expect that this effect is particularly prominent among individual and SRI activists, who may be more likely to coordinate activism with one another to accommodate their limited resources. The bottom panel in Figure 1 illustrates the sponsor type homophily effect—two activists of the same type (node color) target firms in common.

Hypothesis 6: Individual and CSR activists are more likely to select targets in common with other investors of the same type (homophily at distance-two).

Data and Methods

Shareholder activism data come from Proxy Monitor and cover annual proxy seasons from 2006 through 2013. Proxy Monitor collects data on all shareholder-initiated proposals that were successfully submitted and appear in the annual proxy statements of Fortune 250 firms. The data exclude proposals that were withdrawn by the shareholder or that management successfully excluded from the proxy statement by appealing to the SEC. The proxy monitor data include the identities of the target firm and the sponsoring shareholder, or proponent. Proponents are categorized into four types: individuals, public pensions, union pension funds, and socially responsible investors. 4 Given our substantive focus on prominent shareholder activists targeting large firms, we exclude activists who submitted only one proposal during the eight-year observation period. This process removed 118 proponents, almost all of whom were either individual investors (70 percent) or socially responsibly investors (20 percent). Although this constraint eliminates the right tails of the degree distribution, particularly for individuals and SRI, the shape of the distributions remains unchanged. Individuals and SRI are the most highly active proposal sponsors in the field, but they also exhibit the widest degree of distribution. After applying this constraint, our sample includes 162 shareholder activists targeting 220 firms.

We supplemented shareholder activism data with company financials, performance, ownership, corporate governance, and CSR indicators from Compustat, Institutional Shareholder Services (ISS), MSCI’s (formerly KDL) database on corporate social and environmental ratings, and Thomson-Reuters’ database on institutional investor ownership. Our modeling approach for endogenous network dynamics (described in the following) is computationally intensive, so we minimize the number of irrelevant firm-level controls by only including indicators previously found to be important determinants of shareholder activism, including size, accounting and financial performance, institutional investor ownership, corporate governance, and CSR performance. We include a firm-level measure for logged total assets to control for firm size. Indicators for firm performance include return on assets (ROA) and market-to-book ratio. As a measure of institutional investor concentration, we include the Herfendahl-Hirshman index—high scores indicate greater institutional investor concentration. We include a common governance indicator for managerial entrenchment: The e-index is a count of six corporate charter and bylaw provisions found to be negatively associated with shareholder returns (Bebchuk, Cohen, and Ferrell 2009). Governance provisions in the e-index include (1) staggered boards, (2) limits to shareholder bylaw amendments, (3) poison pills, (4) golden parachutes, and supermajority vote requirements for (5) mergers or (6) charter amendments. Finally, we capture corporate environmental and social responsibility issues using MSCI’s ratings data, one of the most widely used tools in research on corporate social and environmental responsibility (Chin, Hambrick, and Treviño 2013; Rehbein et al. 2004). We use MSCI’s summary indicators for total environmental strengths, total environmental concerns, total social responsibility strengths, and total social responsibility concerns. Social responsibility strengths and concerns include issues related to community engagement, human rights, employment relations, diversity, and product safety. 5 In our temporal network models, we also include an indicator of whether the tie existed during the prior proxy season—whether the sponsor targeted the same firm last year. Table 1 provides summary information for the firms and proposal sponsors in our working sample as well as the variable sources.

Summary Statistics for Proponent- and Firm-Level Covariates.

Network Data

After assembling the shareholder activism database from Proxy Monitor and other sources, we prepared a series of two-mode network matrices to represent shareholder activism’s relational structure. First, we prepared unique identifying numbers for each proposal proponent. This involved hand-checking proponent identities for inconsistent listings and correcting cases where the same activist is listed differently. Next, we assembled two-mode activism networks where nodes are divided into two separate classes, sponsors and target firms, and ties represent proposals. 6 We prepared separate two-mode activism networks for each year in the sample, 2006–2013, to be analyzed using temporal network panel models as well as a pooled network that collapses all activism incidents in the observation period. The annual networks were expanded to include firms and sponsors as isolates if they were not involved in an activism event during that year; this procedure yields networks of the same size for each year and facilitates longitudinal network modeling. The temporal network models admit changing firm covariates (e.g., log assets, ROA, e-index, etc.), applied annually. In the pooled 2006–2103 network, we define firm covariates as the within-firm average for each of the changing covariates. The temporal network model allows us to examine structural determinants that affect tie formation within a given proxy season while the pooled network allows us to examine complex endogenous determinants that emerge across proxy seasons. Figure 2 presents network graphs for each of the shareholder activism networks used in the study. Activists are blue, and firms are red; nodes are sized by degree centrality, or the number of unique alters to which they are tied. Appendix A presents detailed descriptive analysis of the network panels.

Shareholder activism network main components: 2006–2013.

Analytic Strategy

Our empirical strategy examines whether endogenous structural determinants, as well as the usual firm- and activist-level traits, affect the structure of the shareholder activism field. 7 We use exponential-family random graph models (ERGMs) and their longitudinal extension, temporal exponential-family random graph models (TERGMs), to model the structure of the shareholder activism network (Cranmer and Desmarais 2011; Hanneke, Fu, and Xing 2010; Lusher, Koskinen, and Robins 2013).

ERGMs (or p* models) have become a popular method for modeling social networks in several disciplines. 8 ERGMs are a family of statistical models for making inferences about network ties and network structure. Conventional regression methods are not suitable for modeling network ties or endogenous structural determinants because ties are, by definition, not independent of each other (Wasserman and Pattison 1996). ERGMs permit researchers to investigate the underlying processes that generate network structures by modeling the probability of a tie as a function of both node-level attributes and network configurations that produce endogenous dependencies between ties. Thus, ERGMs facilitate modeling endogenous network self-organization. The statistical networks literature offers a thorough treatment of endogenous structural determinants and their many forms (Robins et al. 2007; Snijders 2011).

ERGMs estimate the conditional probability of observing a given graph, Y, as:

This equation represents the probability that a random graph Y has a specific realization, y, conditional on covariates, zk(y). Covariates are a vector of k network statistics calculated on graph y. The network statistics correspond to network configurations hypothesized to produce the observed graph and can include such configurations as four-cycles, out-degree activity, in-degree popularity (which we call ignominy), and others.

We also employ a longitudinal extension of ERGMs: temporal exponential-family random graph models suitable for modeling network panels (Desmarais and Cranmer 2012). While the aforementioned approach uses MCMC-MLE to approximate the maximum likelihood distribution, TERGMs take a more computationally tractable approach suitable for larger networks and time-series networks. As implemented in the xergm package in R (Leifeld, Cranmer, and Desmarais 2015), TERGMs maximize the probability of a network’s observed configuration through maximum pseudo-likelihood estimation (MPLE) with bootstrapped resampling. The TERGMs are estimated with 10,000 bootstrap samples. 9

In our ERGM analysis, we test several network configurations associated with the endogenous structural determinants discussed earlier as well as the firm and proponent attributes described in the literature. First, we examine activist prolificacy and firm ignominy as endogenous structural effects, which we specify as the square root of degree-popularity centered on nodes in the activist and firm modes, respectively. The square root specification allows a decreasing marginal return to additional ties; this specification prevents model degeneracy and generally better represents real degree distributions. Second, we are interested in prolificacy-ignominy assortativity, or whether highly prolific sponsors tend to target highly ignominious firms. We specify a network statistic for the difference between activist and firm square root degree. A negative estimate indicates that ties are more likely between sponsors and firms with small degree differences and indicates positive prolificacy-ignominy assortativity. Third, we test whether proponents pursue strategic overlap versus strategic differentiation by specifying a four-cycle network statistic. We test whether sponsors make homophilous targeting decisions, that is, whether activists are more likely to select targets in common with other activists of the same type (individuals, pensions, unions, and SRIs). We specify these effects as nodal attribute-based homophily for the activist-mode in the two-mode graph (Bomiriya, Bansal, and Hunter 2014). Models also include proponent type and several firm-level attributes (size, performance, governance, and institutional ownership) as predictors of whether the proponent or firm is involved in activism events. These node-level attribute effects are interpretable as whether a sponsor or firm is targeted by more activists as a function of its attributes. Finally, the TERGM model includes a dyadic indicator for tie stability—whether the sponsor targeted the firm in the prior year. Many investors sponsor proposals against the same firm year after year, so it is important that we control for lagged tie stability. We follow all procedures for assessing model convergence and fit as outlined in the statistical network modeling literature, and we found that the estimated model accurately reproduces structural features of the observed network in simulations. The goodness-of-fit diagnostics are found in Appendix B.

Results

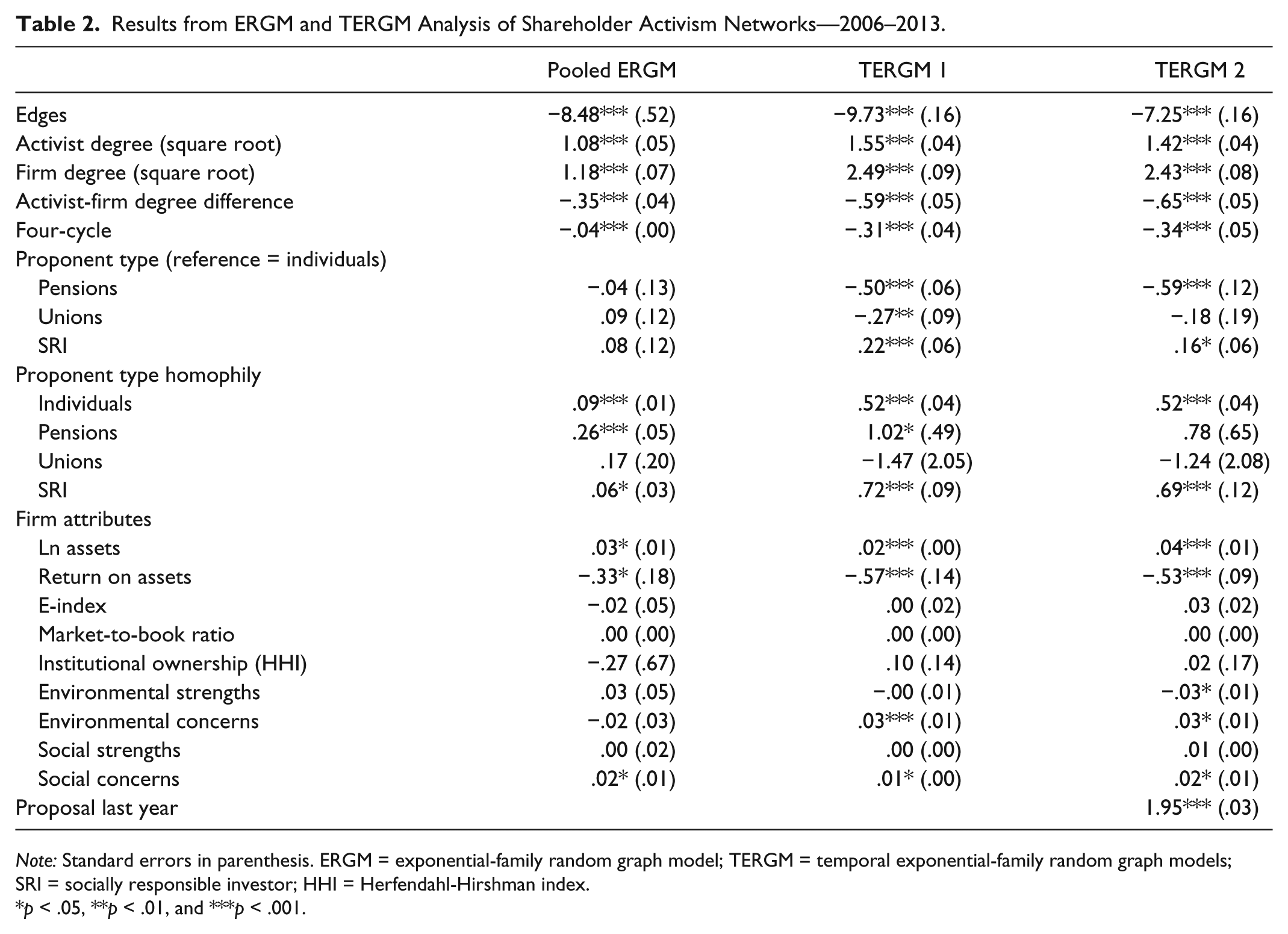

Table 2 presents results from ERGM and TERGM analyses of the pooled 2006–2013 network and temporal network panels, respectively. These models test the hypotheses that endogenous structural determinants affect the structure of the shareholder activism network, independent of firm and activist attributes. The last model (TERMG 2) covers the 2007–2013 network panels but includes the lagged stability indicator for whether the sponsor targeted the firm in the prior year. For each effect in the models, parameter estimates predict the probability of a tie conditional on the respective graph statistic. These are interpretable as the collection of node-level attributes and endogenous structural effects hypothesized to produce the observed graph. First, the edges parameter estimate is almost always negative in real networks, reflecting a general tendency for social networks to be comparatively sparse. Second, activist and firm square root degree is positive and statistically significant in all three models; this corresponds to the high graph centralization. In support of Hypotheses 1 and 2, activism tends to center around a small number of highly prolific sponsors and highly ignominious firms, net of activist and firm attributes and other structural effects. These are endogenous structural effects that predict high variance in the degree distributions centered on each mode. Third, we find negative and statistically significant estimates for activist-firm degree difference in all three models. In support of Hypothesis 3, this indicates that high activists tend to target high degree firms (and low degree activists target low degree firms). The negative estimate indicates that large degree differences predict no tie while small degree differences predict ties. This correlation between activist and target degree centrality corresponds to our hypothesized prolificacy-ignominy assortativity effect—highly prolific sponsors are more likely to target highly ignominious firms.

Results from ERGM and TERGM Analysis of Shareholder Activism Networks—2006–2013.

Note: Standard errors in parenthesis. ERGM = exponential-family random graph model; TERGM = temporal exponential-family random graph models; SRI = socially responsible investor; HHI = Herfendahl-Hirshman index.

*p < .05, **p < .01, and ***p < .001.

Next, we are interested in the amount of overlap in target selection. We hypothesized that activists could pursue either strategic congruence (Hypothesis 4a) or strategic differentiation (Hypothesis 4b) in the targets they select. Our descriptive evidence (Appendix A) suggests that sponsors tend not to choose overlapping targets and the networks are characterized by the absence of four-cycles. The ERGM estimates confirm this descriptive finding. In support of Hypothesis 4b, we find statistically significant negative four-cycle effects in all of the models. This indicates that sponsors tend not to overlap or select multiple targets in common with other sponsors.

We hypothesized about the role of the proponent’s identity as an individual investor, public pension, union, or socially responsible investor (Hypothesis 5). In the temporal models (TERMG 1 and TERGM 2), we found that individuals and SRI activists tend to target more firms as compared to public pensions and unions, suggesting that these types of activists are the most prolific in the field. This suggests that in a given year, individual and SRI activists target more firms, but over the entire observation period, there was no difference. Apparently individual and SRI activists pursue diverse activism strategies within each proxy season, but public and union pension funds diversify their activism strategy over the course of multiple proxy seasons. We also predict that proponents tend to homophilously select targets (Hypothesis 6): Proponents of the same type, particularly individuals and SRI activists, are more likely to target common firms. All three models display positive and statistically significant proponent homophily effects for individuals and SRI activists. While the public pension proponent homophily effect is positive in the pooled ERGM and first temporal ERGM, the effect disappears in the final temporal ERGM after introducing the lagged proposal stability effect. This suggests that proponent type homophily for public pensions may actually reflect a tendency for public pensions to target the same firms year after year. This is perhaps unsurprising given public pensions’ long investment horizons and comparatively low portfolio turnover. Unions do not exhibit homophilous targeting in any model; this is consistent with the interpretation that unions use proposals as part of a broader organizing strategy where each union specializes in a small set of focal firms without substantially encroaching on each other’s territory.

Finally, firm traits are generally consistent with other research on shareholder activism: Larger firms (positive ln assets) and poorer performers (negative ROA) tend to be involved in more activism events. We do not find statistically significant effects for corporate governance, market-to-book ratio, or institutional ownership. This null finding may not be surprising given our study’s focus on large high-profile firms in the Fortune 250 rather than a larger sample, such as the S&P 1500.

Discussion and Conclusion

Shareholder activism in the form of shareholder-presented proposals has become a major arena for governance and SRI-related reforms. Despite the flurry of activity in the shareholder activism field, most activism research has been limited to the firm- or activist-level traits that predict activism rather than theorizing about the relational structure of the field (Goranova and Ryan 2014; Renneboog and Szilagyi 2011). In this article, we examine endogenous effects that contribute to the structure of the shareholder activism field. We advance a novel theoretical and empirical representation of an annual proxy season as a two-mode network where nodes represent activists and firms and ties represent proposals. This representation allows us to theorize about the relational structure of the shareholder activism field and specify empirical expectations about endogenous dynamics that drive field structure. Drawing on empirical models developed in social network analysis, we hypothesize several endogenous structural determinants thought to affect shareholder activism targeting. First, we find that both the proposal targeting (degree in the firm mode) and proposal submission (degree in the activist mode) are highly centralized, independent of other traits. These endogenous structural determinants reflect ignominy and activity effects in the shareholder activism field. Prior work hints that past activism targeting consistently predicts future targeting, independent of firms’ responsiveness (Renneboog and Szilagyi 2011). However, we show that centralization is a persistent endogenous feature of the shareholder activism field’s topology that cannot be explained by the usual set of firm- or activist-level covariates. In addition, highly prolific firms are more likely to target highly ignominious firms (prolificacy-ignominy assortativity). This suggests that while the most prolific sponsors tend to target firms that many other activists have targeted, more focused activists tend to specialize in targeting firms that other activists have not targeted. As a result, the shareholder activism field sorts into a core-periphery structure where highly prolific sponsors and ignominious targets occupy the core containing most proposal activity, but more specialized proponents focus on less ignominious firms in the field’s periphery. Future research should more carefully consider the core-periphery structure of the activism field.

We also specify competing hypotheses that activists could pursue either overlapping or differentiated strategic agendas when selecting proposal targets. We find that activists tend not to overlap with others in selecting their targets—when two activists sponsor proposals against the same firm, they are less likely to sponsor proposals at other common firms. We suggest that this endogenous structural determinant reflects activists’ desire to pursue differentiated activism niches; given limited time and resources, activists tend to pursue positions in the field that are not redundant or overlapping with other activists.

Our final set of findings concerns how the sponsor type affects proposal targeting. Confirming descriptive evidence, we find that individuals and SRI activists consistently sponsor proposals against a wider set of firms because of their emergent role as social movement entrepreneurs in governance and CSR matters. We also find that despite a general pattern of strategic differentiation, individuals and SRI activists tend to homophilously select targets in common with other activists of the same type. Individual investors and SRI activists tend to have less institutional legitimacy and salience as compared to public and union pension funds. As a result, individuals and SRI activists may be more likely to coordinate their activism agendas and present proposals that reinforce and overlap with similar investors. Coordinated strategies of intense overlapping activism may be more likely to generate media attention and attract the notice of corporate governance or CSR monitors.

Our results offer several new insights into the structure of the shareholder activism field. First, results suggest that the large variance in activism targeting and submission may be explained by focusing on self-organizing processes internal to the field. Although observers have long noted that activism is strongly centralized around a handful of prolific activists and highly targeted firms, our study considers whether this topology reflects endogenous self-organizing dynamics. Becoming a highly ignonimous target is not simply a matter of governance or CSR problems. Rather, we argue that these topologies arise from a generalized process of network self-organization that reflects a reverse Matthew effect (de Solla Price 1976) or preferential attachment process (Barabasi and Albert 1999; Lusher and Robins 2013), where firms who are highly targeted attract additional activism. Similarly, on the proposal sponsor side, a small handful of activists present a vastly disproportionate number of proposals—particularly individual shareholders such as John Chevedden and William Steiner or SRI sponsors such as PETA. Our findings suggest that processes of network self-organization drive proposal sponsorship centralization as well. Future work is needed to further verify this theory of network self-organization in shareholder activism on both the target and sponsor sides, but our study presents an analytic framework for testing ideas about self-organization in the corporate activism field.

Our study has a few important limitations. Because of data availability, we are unable to explicitly account for equity ownership in our analytic models. Shareholders most own a predefined threshold in firm equity (usually more than $2,000 in stock or 1 percent of the company) and hold it for at least a year to be eligible to submit a proposal and have it included in the firm’s annual proxy materials. However, this limitation is not critical for at least two reasons. First, this is a relatively low ownership threshold that is unlikely to prohibit prominent investors. Indeed, even individual investors seem to have no trouble acquiring modest ownership stakes in order to submit proposals across the corporate field. Second, the firms in our sample (Fortune 250) are among the largest and most widely held firms in the United States. Although their large market cap may prevent investors from acquiring a sizable ownership stake, the fact that their equity is regularly traded means that motivated investors should have no problem acquiring the minimum $2,000 in equity required to submit a proposal.

Future work should also consider the role of coordinating organizations or networks in producing the observed endogenous effects. Here we have discussed them in terms of network self-organization, but it is also possible that organizations such as the Council of Institutional Investors, the Inter-faith Center on Corporate Responsibility, or proxy advisory firms such as institutional shareholder services mediate these endogenous effects by coordinating activism. The effects of these coordinating organizations are still not well understood in the corporate governance and activism literature. However, our analytic and theoretical approach provides a useful framework for thinking through the ways in which coordinating institutions affect the activism field’s structure.

We also believe that our approach can be expanded to account for other forms of corporate activism through boycotts, letter writing campaigns, and so on as well as other fields where actors confront one another in contentious episodes. Recent research on social movement activism targeting corporations notes the myriad strategies that social movement organizations employ to target firms and induce social change (King 2007; McDonnell et al. 2015). Notably, a relatively bounded set of nongovernmental organizations engage in these and other coordinated activism campaigns. Future work should consider how targeting decisions aggregate into a larger activism field that activists and firms must confront when engaging in strategic action and pursuing differentiated or overlapping positions. Social movement organizations may pursue similar strategies of differention or tactfully coordinate with others in selecting common targets. Analyzing consensus, differentiation, ignominy, and prolificacy offers many theoretical opportunities for social movement scholars. In particular, the concept of endogenous ignominy may be extended to many other contentious fields where ties represent negative interactions, including peer-animosity networks or international sanctions. The extent to which a reverse Matthew effect drives contentious ties theoretically mirrors cumulative advantage processes in positive tie networks and may be theoretically generative for scholars in many subfields. Our approach provides a useful analytic framework for examining the endogenous structural dynamics in a variety of contentious fields.

Footnotes

Appendix

Authors’ Note

The network data from the analysis are available from the first author’s website. The firm-level attributes are available from the cited business databases.

1

2

Some firms maintain “classified” boards, meaning directors are grouped into three classes, with each class serving a three-year term. Classified boards make it more difficult for shareholders to replace the entire board in one year and can function as a takeover defense. “Declassification” refers to implementing the annual election of all directors, making it easier for shareholders to replace the entire board at once.

3

Mutual funds may participate in shareholder activism. However, most mutual funds do not sponsor shareholder proposals and are generally not very involved in investor activism.

4

Note that hedge funds and mutual funds typically do not engage in this type of shareholder activism but are more likely to negotiate directly with management over governance or performance concerns. Only one hedge fund appeared in these data; to preserve parsimony, we coded this shareholder as a pension fund to reflect the general power of most institutional investors. Results were identical when this activist was excluded from the analysis.

6

We did not treat these as valued networks; the structural effects of interest are currently unavailable for exponential-family random graph model (ERGM) analyses of valued two-mode networks.

7

8

An alternative method for modeling longitudinal network dynamics is stochastic actor oriented modeling (SAOM). However, SAOM is more suited to the emergence and durability of relatively stable ties, such as friendships or alliances, rather than relational events, or one-off ties, like an annual proposal or legislative co-sponsorship. Although time dependencies exist, this can be accounted for in the temporal ERGM (TERGM) framework without requiring the assumption that ties are stable across observations.

9

We confirmed that the bootstrapped thetas are normally distributed, so we report standard errors and statistical significance in the results tables.

10

Note that we excluded activists who only sponsored only one proposal during the eight-year observation window. Had we included these single tie proponents, the networks would be even more centralized than we observe in our sample.

11

This simulation approach is more conservative than calculating a null distribution graphs of fixed size and density because fixing the degree marginals allows us to hold the degree distribution constant in the simulated graphs. This also reproduces the observed graphs’ centralization in the null distribution—thus we are comparing observed clustering to a null distribution with fixed size, density, and degree distribution. We do not do this in the CUG test for centralization, presented previously, because fixing the degree marginals would fix the centralization indices to the observed graph, thus defeating the purpose of comparing observed centralization to a null distribution.