Abstract

This study advances research on the nexus of business insolvency and entrepreneurs’ well-being. We broadly build upon the Conservation of Resources Theory (COR) and explore the severity of the impact of firm insolvency on subjective well-being, stress hormones, and physiological recovery. To test our hypotheses, we compared entrepreneurs operating in 51 businesses affected by insolvency with 51 entrepreneurs in a control group. We conducted our study in Germany, where legal regulations surrounding insolvency are relatively unfavorable for those affected. Our findings indicate that entrepreneurs facing insolvency experience lower psychological well-being, greater vital exhaustion, higher stress hormone levels, and, as revealed by supplementary analyses, poorer risk adjustment. Our study complemented entrepreneurs’ self-reports with objective methods to examine entrepreneurial well-being in times of hardship from three perspectives: psychological, biological, and physiological. Although exploratory, our study provides relevant insights into potential repercussions of business failure.

Introduction

Self-employment can create hardships for those who engage in this form of work. It is associated with income risks (Carter, 2011) such as firm insolvency. Behind every insolvency stands an individual entrepreneur, burdened with heavy stressors generated by multiple lost resources that include money, work-related identity, and self-esteem. Thus, a more nuanced understanding (Newman et al., 2022) of how firm insolvency affects entrepreneurs’ experience and functioning is warranted.

Prior research highlights that insolvency due to business failure can endanger entrepreneurs’ financial and social positions and their self-esteem (Jenkins et al., 2014). Not only can their own job loss and the associated financial problems be devastating for entrepreneurs (Lechat & Torrès, 2017), having to lay off employees may, like its attendant stigmatization (Singh et al., 2015), result in psychological trauma (Jenkins et al., 2014; Ucbasaran et al., 2013). Indeed, financial problems and job insecurity are identified as major concerns associated with strain in this occupational group (Blanchflower, 2004).

Although the negative effects of business failure are well recognized in literature (Ucbasaran et al., 2013), we still know very little about the psychological, biological, and physiological outcomes related to insolvency at the level of the individual entrepreneur. For instance, we lack insights into how financial struggles are potentially detrimental to different types of well-being, including psychological well-being, vital exhaustion, and physiological stress (Stephan, Rauch & Hatak, 2023; Wolfe & Patel, 2021). Moreover, existing research typically relies on self-reports when studying entrepreneurs who are affected by business failure, so objective data (e.g., regarding sleep quality and cognitive performance) and biological markers that reveal stress levels within the body are missing.

Therefore, in this article, we examine the following overarching research question: How strong is the impact of firm insolvency on entrepreneurs’ psychological (well-being), biological (stress hormones), and physiological (e.g., sleep) functioning? To address this question, we draw upon the Conservation of Resources Theory (COR; Hobfoll, 1989), particularly the proposition that “people strive to retain, protect, and build resources and that what is threatening to them is the potential or actual loss of valued resources” (Hobfoll, 1989, p. 516). We view firm insolvency as a loss of key resources that, according to the basic tenet of the COR theory, causes psychological stress and negatively affects well-being (Hobfoll et al., 2018). Insolvency is related to the actual loss of financial, personal (e.g., self-esteem, inner peace), and social (e.g., relationships with employees, customers, business partners, social status) resources and it also may promote future loss of resources. In this study, we investigate the potential repercussions of firm insolvency for entrepreneurs, thereby accounting for the negative path of resource losses and the potential loss spiral postulated in the COR theory (Hobfoll, 1989). We explore how loss spirals elucidate stress and depletion in psychological and physiological resources. We also investigate factors that may predict insolvency.

Our study was conducted in Germany, a context often regarded as unfavorable for insolvent entrepreneurs for the following reasons. First, it is mandatory to disclose insolvencies in a public database (German Federal Ministry of Justice, 2024b) maintained by the Judicial Portal of the Federation and the States. From a psychological standpoint, this public exposure may elicit feelings of shame and lead to social stigmatization. Such negative consequences can influence both the entrepreneur’s self-perception and their position within broader social and professional networks. Second, the process for registering insolvency in Germany is rather lengthy, complicating recovery and making it more challenging to have a fresh start (Fossen & König, 2015), especially since registration hampers an individual’s ability to obtain credit. Therefore, Germany provides a critical context for examining the effects of insolvency on entrepreneurs’ well-being.

To test our related hypotheses, the derivation of which we describe in more detail below, we compare entrepreneurs operating in businesses affected by insolvency against entrepreneurs in a control group from similar but well-performing firms. We invited these entrepreneurs to join our lab study and assessed their psychological (well-being), biological (stress hormones), and physiological (sleep) functioning. In so doing, our research seeks to make several contributions. First, we examine the highly salient context of firm insolvency to expand our understanding of the relationship between self-employment and well-being in a crisis (Nikolaev et al., 2020). Second, we add to the growing literature on biological perspectives in entrepreneurship research (Nicolaou et al., 2021). By introducing cortisol and cortisone in hair as biomarkers of entrepreneurial stress, we expand research examining the influence of hormones in entrepreneurship (Bönte et al., 2016; Greene et al., 2014; Nicolaou et al., 2021; Unger et al., 2015; White et al., 2006). We also add to a new research strand investigating how physiological recovery is related to business success (Wach et al., 2021; Weinberger et al., 2018; Williamson et al., 2021). Overall, our study aims to increase the understanding of the relationship between work-related failures and physiological outcomes in the context of entrepreneurship. This is important, as research shows that entrepreneurs are confronted with different psychosocial risk factors to employees (Lek et al., 2020) and job stressors operate differently for employees and the self-employed (Annink et al., 2016).

Theoretical background

COR theory

We propose that COR theory provides an appropriate framework to study entrepreneurship, particularly firm insolvency. According to this theory, people strive to build and protect their resources, and they experience stress when those resources are under threat. Resources include objects that have primary (physical) and secondary (status-driven) value (e.g., firm, home), personal characteristics (e.g., self-esteem, stress resistance), conditions (e.g., being a business owner, being a spouse), and energies (i.e., time, money, and knowledge). In line with this framework, humans experience stress when their central and valued resources are threatened with loss, which may be an actual net loss of resources or the result of an (effortful) investment of resources not leading to the expected resource gain. The concept of resource loss is central to the COR theory. Loss is disproportionately more salient than resource gain (e.g., the loss vs hiring of a skilled employee). It is also more powerful in terms of the immediate effect, the length of the impact on the individual, and the involved stress reaction.

As Lanivich (2015) remarks, “Not many people realize the critical nature of resource loss like entrepreneurs” (p. 864). Indeed, in the context of entrepreneurship, the loss of valued resources is both sharply experienced and highly prevalent, which is why we exclusively focus on the loss premise of the COR theory in this study.

Hypotheses development

Business failure entails a feeling of loss (Ucbasaran et al., 2013). As documented in qualitative case studies (Cope, 2011; Singh et al., 2007) and literature reviews (Shepherd, 2003; Ucbasaran et al., 2013), business failure generates negative emotional responses such as anxiety, panic attacks, phobias, anger, and depression. In his conceptual framework, Shepherd (2003) drew on the grief perspective to explore emotions related to business failure. He argued that grief can be an extreme negative emotional response to business failure, in which affected individuals experience the type of stress generally associated with the loss of a beloved person. Jenkins et al. (2014) proposed that business failure is not just a cause of financial loss; it is a threat to personal resources such as identity and self-esteem, thus depleting entrepreneurs’ well-being and intensifying stress. Moreover, because entrepreneurial firms satisfy individuals’ needs for competence, relatedness, and autonomy, when these needs are jeopardized by insolvency threats, entrepreneurs experience grief (Shepherd et al., 2016). Overall, existing literature on the psychological and physiological effects of business failure is mainly conceptual (Hayward et al., 2010; Shepherd, 2003, 2004, 2009; Shepherd et al., 2016; Shepherd & Haynie, 2011) and dominated by qualitative studies that rarely include more than a few participants (Cope, 2011; Harris & Sutton, 1986; Singh et al., 2007). This legitimates our research approach in which we conduct a quantitative empirical study of insolvent entrepreneurs.

Past research highlights that entrepreneurs report significantly less work-related stress than wage workers, and job control fully mediates the relationship between self-employment and stress (Hessels et al., 2017). Entrepreneurs facing financial problems or insolvency lack mastery, flexibility to organize their work, and capacity to respond autonomously to their job demands. Such job characteristics are vital for entrepreneurs and their well-being (Stephan, 2018). In accordance with the COR theory (Hobfoll, 1989) and based on prior research, we suggest insolvency will substantially impair entrepreneurs’ well-being for the following reasons. First, experiencing negative emotions related to the loss of valued resources such as a firm, money, and self-esteem, as well as the prospect of losing further resources (e.g., social status, stigmatization) in the future (Shepherd et al., 2016; Shepherd & Haynie, 2011) are likely to devastate entrepreneurs’ well-being. Second, entrepreneurial firms are closely connected to their entrepreneurs’ identities; thus, business failure will threaten entrepreneurs’ identification (Cardon et al., 2009). Third, financial constraints limit entrepreneurs’ sense of autonomy (Gelderen, 2016), a work characteristic closely related to entrepreneurs’ well-being (Stephan, 2018). Based on this rationale, we propose the following hypothesis:

Hypothesis H1: Entrepreneurs experiencing firm insolvency report significantly lower subjective well-being compared with a control group from similar but well-performing firms.

Entrepreneurs view their work and their businesses as an immanent part of their identity (Cardon et al., 2009). They are also emotionally attached to their ventures (Shepherd, 2003) and seek personal development within them (Wach et al., 2016). This is why dealing with insolvency or even temporary closure generates not only a significant level of psychological stress (Stephens et al., 2021) but also negative physiological responses (Ucbasaran et al., 2013). Dealing with a business failure is, like dealing with a grief, typically spread out over time (cf. Stephens et al., 2021). Experiencing loss spirals over a longer period may expose entrepreneurs to chronic stressors and cause increased release of stress hormones.

In this research, we study the effects of firm insolvency on entrepreneurs’ physiological health by measuring their cortisol (HCC) and cortisone (HEC), which are biomarkers of stress. The release of glucocorticoids concentrate in the hair provides a reliable retrospective reflection of stress hormone secretions over several months (Stalder et al., 2017). Many studies have reported elevated basal glucocorticoid levels in individuals who have some forms of depression (Burke et al., 2005; Schmiedgen et al., 2017) or mood and anxiety disorders (Steudte et al., 2011; Wester et al., 2014), making cortisol and cortisone valid biomarkers of stress hormones (Santoso et al., 2022; Staufenbiel et al., 2013). Given that dealing with insolvency is stressful, it is likely that it will manifest in higher levels of hair cortisol (HCC) and cortisone (HEC) concentrations in affected individuals. Therefore, we formulate the following hypothesis:

Hypothesis H2: Stress hormone concentrations in hair are significantly higher in entrepreneurs experiencing firm insolvency compared with the control group from similar but well-performing firms.

In line with the COR theory, sleep is a resource-restoring process that may help protect against loss spirals (Hobfoll et al., 2018). As a crucial recovery-enhancing process (Sonnentag, 2018), sleep is closely related to the regulation of physical and emotional well-being (Haack & Mullington, 2005). Good sleep can prevent serious mental health disorders (Freeman et al., 2020) and promote job performance (Barnes, 2012). In the context of entrepreneurship, high self-reported sleep quality has been found to be a predictor of positive moods and innovative behavior (Williamson et al., 2018).

In contrast, encounters with the daily stressors of entrepreneurship, including lack of financial resources, has been found to increase insomnia (Kollmann et al., 2019) in both experienced and novice entrepreneurs. Insomnia and sleep disturbances have been identified as negative physiological responses to entrepreneurs’ financial setbacks (Ucbasaran et al., 2013). For instance, Singh et al. (2007) examined five cases of business discontinuance to provide empirical evidence of sleeplessness in participants due to anxiety about their future. Their finding is alarming because insomnia has a detrimental effect on entrepreneurs’ health (Levasseur et al., 2019) which, for insolvent entrepreneurs, can already be in jeopardy.

Based on the rationale presented above, we expect that firm insolvency will give entrepreneurs sleepless nights. To our knowledge, no studies have related firm insolvency to objectively measured sleep parameters. Hence, we formulate the following hypothesis:

Hypothesis H3: Objectively measured sleep quality and quantity is significantly lower in entrepreneurs experiencing firm insolvency compared with the control group from similar but well-performing firms.

Method

Study design

Significant variations in bankruptcy laws can be observed across different countries (European Commission, Eurostat, 2024). The EU measures bankruptcies as the number of legal units that have commenced the relevant legal procedure for being declared bankrupt; in the context of Germany, this means the number of firms that have initiated insolvency proceedings (European Commission, Eurostat, 2024). Therefore, in our study, we operationalized business failure as firm insolvency. According to the German Federal Ministry of Justice (2024a), firm insolvency refers to a legal state where a business is unable to meet its financial obligations as they become due. It implies that a business can no longer satisfy creditors’ claims. In Germany, insolvency proceedings assess whether the company can be restructured or if closure remains the only option (IHK Regensburg Für Oberpfalz / Kelheim, 2024). Please note that in this study, bankruptcy is not synonymous with insolvency. Under German law, bankruptcy occurs only when the firm failure is considered a criminal offense according to Section 238 of the German Penal Code (German Federal Ministry of Justice, 2024a). For an act to be classified as a criminal offense, certain conditions must be met, including the requirement that the entrepreneur in question was aware of their over-indebtedness or existing or imminent insolvency, and engaged in conduct that conferred a personal benefit on them while disadvantaging creditors. For ethical reasons, researchers cannot deliberately manipulate insolvency. We have, therefore, chosen to use a cross-sectional design to compare a group of insolvent entrepreneurs (the firm insolvency group) with a group of business owner–managers in Germany (the control group). Inclusion criteria for the firm insolvency group was an ongoing insolvency or the clear risk of it. Therefore, we recruited the vast majority of our study participant from the public insolvency register (German Federal Ministry of Justice, 2024b) with just four participants of the insolvency group coming from personal networks. Regarding sampling, the time between the official filing for insolvency as published in the public register and study participation was < 6 months (ranging from 0.5 to 5.8 months; M = 65 days, SD = 40 days). Response rate was 15%. Control group participants were recruited at networking events, through newsletters, from the Yellow Pages (German business directory), and via the online platforms of chambers of commerce. Response rate was 26%. All study participants were contacted via telephone and email between 2015 and 2017.

Note that our study hypotheses were outlined in the research grant and approved by the German Research Foundation (DFG) prior to the commencement of data collection and analysis. As part of the grant, we performed a power analysis to determine the necessary sample size. For the comparison of group differences between the two independent groups, the a priori power analysis yielded the following results: With a statistical power of 0.95 in a one-tailed test and a medium effect size of d = 0.6, a total of 122 participants (two groups of 61 each) were required. We also conducted a pilot study first and found strong effects of insolvency on hair glucocorticoid concentrations (HGC) and cognitive performance.

Sample

The firm insolvency group consisted of N = 51 entrepreneurs, with 19.7% being women. Entrepreneurs were on average 47 years old, and 43.1% had a higher education degree. They primarily owned micro and small businesses (96%) and had 10 employees on average. Firms operated in both the service industry (66.7%) and manufacturing (30.4%). Most businesses (68%) had been in existence for less than 5 years.

The control group had N = 51 entrepreneurs, of whom 27.5% were women. Participants were on average 45 years old, and 74.5% had a higher education degree. They too primarily owned micro and small businesses (86.3%) with, on average, 22.40 employees. Around half the sampled businesses operated in financial and insurance activities (19.60%), information and communication (17.6%), and construction (15.7%). Other sectors were less represented: administration and support (7.8%), manufacturing (5.9%), and accommodation (2.9%). Almost 60% of businesses had been operational for more than 10 years. The sample characteristics for the firm insolvency and control groups are presented in Table 1. In terms of age, gender, marital status, firm age, and industry sector, the groups are similar; however, participants in the control group were better educated (χ2 (1, N = 102) = 10.36; p = .001) and they employed a greater number of employees (t(100) = 2.01; p < .01). Prior experience of insolvency was reported more frequently by the firm insolvency group ((χ2 (1, N = 102) = 21.79; p < .001).

Sample characteristics.

Note: Gender: 0 = male, 1 = female; Education (University degree): 1 = yes, 0 = no; Living alone: 1 = yes, 0 = no; Past insolvency: 1 = yes, 0 = no; Industry sector: 0 = manufacturing, 1 = services. Significant mean differences between insolvent entrepreneurs and the control group are highlighted in bold.

Firms that had been in existence for 50 and more years were not founded by the current owner–manager (N = 5; the pattern of correlations with the study’s outcome variables remained the same after these cases have been removed).

p < .05.

Measures

Dependent variables

“Subjective well-being” was measured using the German version of the WHO-5 Well-being Index (Brähler et al., 2007). The scale consists of five items (e.g., “I have felt cheerful and in good spirits”) that address participants’ quality of life over the past 2 weeks on a six-point Likert-type scale (from “at no time” = 0 to “all of the time” = 5). High scores indicate a high state of well-being. The total score ranges from 0 (lowest well-being) to 25 (highest well-being). Scores below 13 are indicative of depression symptoms. Cronbach’s alpha reliability coefficient in our sample was good at α = .86.

We also measured entrepreneurs’ vital exhaustion with the nine-item Maastricht Questionnaire (Kopp et al., 2000). The measure includes symptoms such as fatigue and demoralization (e.g., “Do you often feel tired?”). The response alternatives were “Yes” = 2, “? /Indeterminate” = 1, and “No” = 0. The sum score (ranging from 0 to 18) was calculated. Values above 10 indicate severe exhaustion (Schnorpfeil et al., 2002). Cronbach’s Alpha was at α = .86.

“Biological stress” was operationalized via HGC. Stress hormones cortisol (HCC) and cortisone (HEC) were measured using a 2 cm hair segment (representing 2 months of HCC and HEC concentrations), cut as close to the scalp as possible from a posterior vertex position (Wennig, 2000). Hair samples were analyzed according to the published protocol, using liquid chromatography tandem mass spectrometry in a specialized laboratory at our university (Gao et al., 2013). For our analyses, we calculated HGC as the sum of HCC and HEC (Stalder et al., 2017).

“Physiological recovery” was measured objectively via sleep efficiency (sleep quality) and sleep time (sleep quantity) assessed with an actigraph monitor (Actiwatch 2, Respironics Inc., Murraysville, PA) that participants wore for 1 week on average (between 4 and 10 days; M = 7 days). Sleep data were analyzed with Respironics Actiware 6 software (Respironics Inc., Murraysville, PA), with actigraphy watches configured to 30 s epochs, and an awake threshold setting at 20 (low), as recommended by Lichstein et al. (2006) for people with insomnia. We set thresholds for sleep onset and offset to 20 consecutive inactive epochs to obtain high convergent validity to polysomnography (Kollek, 2017). For each night, actigraph monitoring was aligned with light sensor data and self-reports of time going to bed, time of awakening, and time of leaving bed. Sleep variables were calculated using standard algorithms (Respironics, 2009; see https://www.iitg.ac.in/nkashyap/acti.pdf) and included “time in bed” (in hours), “total sleep time” (total of epochs scored as “sleep” by the algorithm, in hours), and “sleep efficiency” (percentage of sleep epochs in the interval between sleep onset and final awakening, also referred to as “percent sleep” or “actual sleep”). All values were averaged across all sleep intervals. Actigraphy measurements using Actiwatch have shown to be quite stable and reliable, with overall high accordance with polysomnography (Rupp & Balkin, 2011).

Participants’ gender, age, education, and marital status were measured, in addition to industry sector, employee number, firm age, and past insolvency. We also calculated participants’ body mass index (BMI) and asked them to indicate whether they had been diagnosed as having diabetes mellitus (“Yes” = 1, “No” = 2).

Results

Descriptive statistics

Table 2 presents descriptive statistics of study variables across groups. Table 3 presents descriptive statistics and correlations among study variables. Regarding psychological well-being, over 67% of participants in the firm insolvency group reported scores indicative of depression (below 13), whereas only 4% of control group participants did so. That is, almost 7 in 10 insolvents reported alarmingly poor well-being, while in the control group it was the case for less than 1 in 10, showing a prevalence rate that was 16.75 times higher than the control group’s [= 0.67/ 0.04]. We compared the firm insolvency group’s well-being scores against those of a representative German sample with similar ages (Brähler et al., 2007) and found that 90% of the representative sample had higher well-being scores than our insolvent entrepreneurs. Even entrepreneurs who were confronted with the Covid-19 pandemic scored considerably better (M = 2.84, SD = 0.98 vs Minsolvent = 1.99, SD = 1.02) on this particular measure of well-being (St-Jean & Tremblay, 2023).

Study variables across groups.

HGC: hair glucocorticoid concentrations (HCC + HEC), DM: diabetes mellitus 1 = yes, 2 = no; BMI: body mass index.

Note: Welch test for equality of means. Significant mean differences between insolvent entrepreneurs and the control group are highlighted in bold.

In pg/mg.

p-value refers to Chi-square test.

Correlations among study variables.

WHO-5: WHO-5 Well-being Index; VE: vital exhaustion; HEC: cortisone; HCC: cortisol; HGC: hair glucocorticoid concentrations (HCC + HEC); DM: diabetes mellitus 1 = yes, 2 = no; BMI: body mass index; SQ: sleep efficiency; SH: sleeping hours.

Note: Group: 0 = control group, 1 = firm insolvency group; Gender: 0 = male, 1 = female; Edu.: education (University degree): 1 = yes; 0 = no; PI: prior insolvency 0 = no, 1 = yes.

In pg/mg.

p .05, **p < .01.

Regarding vital exhaustion, 60% of firm insolvency group participants reported severe vital exhaustion (Schnorpfeil et al., 2002), compared with 24% of control group participants. In other words, there is a greater level of exhaustion in the insolvent entrepreneurs, with the majority (6 in 10) reporting severe vital exhaustion. The prevalence rate is 2.5 times higher than in the control group [= 0.6/ 0.24], which itself had a notable prevalence of vital exhaustion (about one in four). Moreover, the scores for vital exhaustion reported by this study’s group of insolvent entrepreneurs were twice as high (Minsolvent = 10.50, SD = 5.81 vs M = 5.02, SD = 4.76) as those reported in a study that included entrepreneurs who were prospering (Wach, 2016). While our results are not surprising, they are nevertheless alarming because severe exhaustion is a significant risk factor for cardiovascular events (Cohen et al., 2017) and a fundamental indicator of burnout (Maslach et al., 2001).

Regarding stress hormone concentrations in hair, participants in the firm insolvency group showed cortisol levels (pg/mg) that were comparable with those of the sample of healthy individuals (Minsolvent = 4.52 SD = 5.84 vs M = 7.46, SD = 8.97); however, cortisone levels were considerably higher in the firm insolvency group (Minsolvent = 14.28 SD = 17.71 vs M = 11.60, SD = 8.84), which is comparative to the study by Puhlmann et al. (2021). The HGC level (sum of cortisone and cortisol) was substantially higher in the firm insolvency group than in the control group (Minsolvent = 18.81, SD = 23.40 vs M = 9.56, SD = 13.35). Insolvent entrepreneurs exhibited nearly double HGC levels compared with the control group.

Regarding sleep, we found that the insolvent entrepreneurs had efficient sleep with few interruptions (Sleep efficiency ⩾ 85%; Jung et al., 2017), a statistic that is comparable to the sleep efficiency of solvent German entrepreneurs in a study by Wach et al. (2021) (Minsolvent = 86.12, SD = 6.15 vs M = 86.50, SD = 6.79).

We also observed that on average, entrepreneurs in our sample were overweight (BMI: M = 26.49, SD = 4.46). In almost 60% of our study participants, we identified BMI > 24.9, with no significant differences between the firm insolvency and control groups (Minsolvent = 27.01, SD = 4.87 vs M = 25.96, SD = 3.97, F (100) = 2.375, p = .118 n.s.).

Hypotheses testing

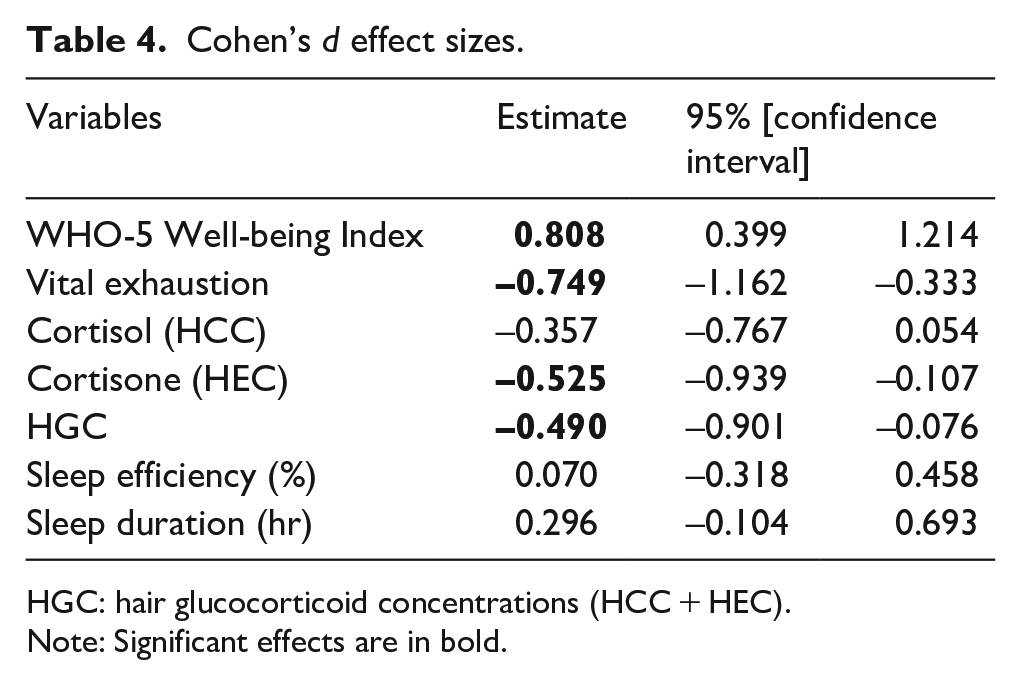

To address our three hypotheses, we conducted multivariate variance analyses (MANOVA). We report partial eta squared (ηp2) as a measure of the effect size that “describes the proportion of variability associated with an effect when the variability associated with all other effects identified in the analysis has been removed from consideration” (Fritz et al., 2012, p. 8). In addition, we calculated Cohen’s effect sizes (Cohen, 1973) (see Table 4). All analyses were performed using SPSS (Version 26.0, 2022, IBM, New York, USA).

Cohen’s d effect sizes.

HGC: hair glucocorticoid concentrations (HCC + HEC).

Note: Significant effects are in bold.

Hypothesis H1 proposed that participants in the firm insolvency group would report lower psychological well-being and greater vital exhaustion than the control group. The MANOVA results show that the group variable (firm insolvency vs control) was significantly related to subjective well-being (Pillai-Spur = .146, F(2, 91) = 7.74, p < .001, ηp2 = .146). The mean score of the WHO-5 Well-being Index was significantly lower in the firm insolvency group relative to the control group (F(1, 93) = 14.68, p = .001, ηp2 = .138; Minsolvent = 10.55, SD = 5.33 vs M = 14.75, SD = 5.29). The opposite effect was found for vital exhaustion (F(1, 93) = 11.99, p < .001, ηp2 = .115; Minsolvent = 10.38, SD = 5.81 vs M = 6.55, SD = 4.81). Age, gender and education were not significantly related to the WHO-5 Well-being Index and vital exhaustion and were, therefore, not included in the multivariate analysis. However, the results remained the same when they were included as covariates.

In hypothesis H2, we expected that participants in the firm insolvency group would show higher glucocorticoids concentrations in hair compared with the control group. Indeed, the group variable was significantly related to hormone levels (Pillai-Spur = .085, F(2, 90) = 4.17, p < .018, ηp2 = .85). The cortisone (HEC) level of insolvency group participants was significantly higher than that of the control group (F(1, 90) = 6.40, p = .013, ηp2 = .066; Minsolvent = 14.28, SD = 17.71 vs M = 6.815, SD = 9.92). The cortisone levels were more than double those of the control group, a difference we consider substantial. However, the groups did not differ significantly in their cortisol (HCC) concentrations (F(1, 90) = 2.965, p = .088, ηp2 = .032). After adding age and gender as covariates, the effects remained; however, when we controlled for education, the effect of insolvency on stress hormones was no longer significant for cortisone (p = .076) or for cortisol (p = .26).

In addition, we conducted univariate variance analysis to test mean differences in HGC and found a significant effect of group membership (firm insolvency vs control) on HGC concentrations (F(1, 89) = 5.572, p = .020, ηp2 = .058). The results remained the same after adding the age and gender covariates. However, when education was added as a covariate, the effect of group membership on HGC concentrations became insignificant (p = .102).

Hypothesis H3 predicted that participants in the firm insolvency group would show lower physiological recovery than the control group. The results partially support this assumption (Pillai-Spur = .063, F(2, 93) = 3.12, p = .049, ηp2 = .063. In particular, sleep efficiency was significantly lower in the firm insolvency group (F(1, 90) = 5.845, p = .018, ηp2 = .059; Minsolvent = 86.12, SD = 6.15 vs M = 88.81, SD = 3.155). Their sleep efficiency was 2.69% lower than that of the entrepreneurs in the control group. Adding education or age and gender as covariates did not change these results. However, we found no significant differences between the sleep time in hours for the two groups (F(1, 90) = 1.24, p = .267, ηp2 = .013). We also found a significant gender effect (Pillai-Spur = .113, F(2, 93) = 5.91, p = .004, ηp2 = .113) on both sleep quality (sleep efficiency; F(1, 90) = 9.68, p = .002, ηp2 = .093) and quantity (sleep duration; F(1, 90) = 4.19, p = .043, ηp2 = .043). Sleep efficiency (Mwomen = 83.42, SD = 11.20 vs Mmen = 77.35, SD = 12.00) and sleep duration (Mwomen = 6.17, SD = 0.86 vs Mmen = 5.70, SD = 0.98) were significantly higher for women than men.

Finally, we tested our hypotheses again including the employee number variable as a covariate. We found this variable to be unrelated to our outcomes. Inclusion of this variable also did not change the results described above.

Exploratory analyses

Analyzing risk of insolvency

As well as testing the negative repercussions of firm insolvency on the individual entrepreneurs, we were interested in characteristics of entrepreneurs and their firms that might potentially increase the risk of firm insolvency. Prior research indicates, for instance, that entrepreneurial firms are especially dependent on the qualifications and knowledge of entrepreneurs (Mayr et al., 2021). Firms seem to be less likely to fail when they are led by older entrepreneurs and by entrepreneurs with greater management experience. Moreover, a large body of entrepreneurship research argues that new firms are highly volatile and more likely to close than established firms (Wiklund et al., 2010). We drew on variables in this study to test whether personal and firm-related characteristics may increase the risk of firm insolvency, using the SPSS program to conduct binary logistic regression. The dependent variable was equal to 1 if the entrepreneur was dealing with firm insolvency, and 0 otherwise. The results are presented in Table 5. They indicate that our model, which incorporates entrepreneurs’ gender, age, education, prior insolvency, firm age, and employee number, explains 41.4% of variance in firm insolvency. The classification in the firm insolvency group based on the included variables is correct in 71.6% of cases. In fact, only one significant predictor can be identified: prior insolvency. The odds ratio for this variable coefficient is 33.629 (p = .001) and the confidence interval does not include zero [3.847; 293.989]. We found that participants who are currently dealing with firm insolvency were almost 34 times more likely to have experienced insolvency before (firm insolvency participants with prior experience of insolvency: 22 out of 51; control group participants with prior experience of insolvency: 2 out of 51).

Logistic regression analysis: Risk of firm insolvency.

Note: Gender: 0 = male, 1 = female; Edu.: education (University degree): 1 = yes, 0 = no; PI: prior insolvency 0 = no, 1 = yes. Significant coefficients are in bold.

Robustness checks

Relationships between firm insolvency and subjective well-being

We conducted structural equation modeling (SEM) with the STATA program to predict subjective well-being. We entered entrepreneurs’ BMI and diagnosis of diabetes mellitus as variables for both groups of entrepreneurs. We found that firm insolvency significantly predicted both WHO-5 Well-being Index (B = –0.417, p < .000) and vital exhaustion (B = 0.327, p = .003) in expected directions. Neither diabetes mellitus nor BMI were significantly related to subjective well-being. The results are presented in Table 6 (see Appendix). They suggest that firm insolvency simultaneously significantly predicts lower well-being and higher vital exhaustion.

Relationships between firm insolvency and stress hormones

We also conducted an SEM to predict stress hormone concentrations in hair. We tested whether glucocorticoids concentrations in hair (HGC) can be predicted by the group variable (firm insolvency vs control), when BMI (Stalder et al., 2012) and diabetes mellitus (Oltmanns et al., 2006; Staufenbiel et al., 2015) are controlled for. As presented in Table 7 (see Appendix), we found that HGC was positively related to firm insolvency (B = 0.226, p = .014) and that BMI was significantly positively related to HGC (B = 0.289, p = .001). This suggests that higher HGC can be predicted by firm insolvency and higher BMI.

Relationships between firm insolvency and sleep effectiveness

We conducted a further SEM to predict sleep efficiency by firm insolvency. As presented in Table 8 (see Appendix), we found that sleep efficiency was negatively related to BMI (B = 0.284, p = .002); however, the relationship with firm insolvency was insignificant (B = –0.155, p = .070). After we excluded the BMI and diabetes mellitus control variables, the relationship between sleep efficiency and firm insolvency became significant (B = –2505, p = .012).

Supplementary analyses

According to Shepherd (2003), the negative emotions associated with firm failure may interfere with individuals’ allocation of attention when processing information, which in turn may lead to considerable decline in their cognitive performance. This notion is in line with the proposal of Klein and Boals (2001) that the more cognitive effort people put into stressful thoughts, the more their working memory suffers because the negative thoughts compete with task demands for attentional resources. Furthermore, cognitive performance may diminish as a result of insufficient sleep. Recent meta-analysis (Wardle-Pinkston et al., 2019) indicated that insomnia was associated with poorer overall cognitive performance for both subjective and objective indicators (e.g., capacity in working memory, complex attention, alertness, and problem solving). A cross-sectional meta-analysis (D’Amico et al., 2020) also revealed negative links between higher allostatic load and poor global cognition and executive functions (e.g., nonverbal reasoning, inhibitory control, processing speed). Based on this rationale, we empirically tested if entrepreneurs in the insolvency group display lower cognitive performance compared with the control group.

We measured “cognitive performance” with the Cambridge Neuropsychological Test Automated Battery (CANTAB; Cambridge Cognition, 2014) presented on a high-resolution touchscreen monitor in our university lab. With a total duration of approximately 1 hr, four different performance tests were conducted in the following order. “Working memory” was tested with the Spatial Working Memory (SWM) test, where a low number of errors indicates high working memory performance. “Sustained attention” was assessed with the Rapid Visual Information Processing (RVP) test in which high level of sustained attention is represented by a high RVP A′ sensitivity score. “Cognitive flexibility” was measured with the Intra-Extra Dimensional Set Shift (IED) test that calculates the total number of errors; low values indicate high cognitive flexibility. “Risk taking and risk adjustment” were measured with the Cambridge Gambling Task (CGT). A higher score in risk taking indicates higher risk-seeking behavior, while a high risk adjustment score represents better adaptation to probability (i.e., rational use of the available information when making decisions).

We conducted a MANOVA variance analysis controlling for age, education, and gender. The results show that the group variable (insolvency vs control group) significantly related to cognitive performance in general (Pillai-Spur = .165, F(7, 84) = 2.33, p < .031, ηp2 = .165). However, a significant effect for the single indicators of cognitive performance was found only with regard to risk adjustment (F(1, 93) = 8.70, p = .004, ηp2 = .089) suggesting that risk adjustment was significantly lower in the insolvency group versus the control group (Minsolvent = 1.05, SD = 0.72 vs M = 1.61, SD = 0.94). The results further showed that cognitive performance was significantly affected by entrepreneurs’ age (Pillai-Spur = .29, F(7, 84) = 4.95, p < .001, ηp2 = .295) in that all indicators of cognitive performance were higher in younger participants. The effects of education (Pillai-Spur = .138, F(7, 84) = 1.90, p = .079) and gender (Pillai-Spur = .141, F(7, 8) = 1.95, p = .072) were insignificant.

Discussion

Although entrepreneurs often derive greater positive well-being from working for themselves rather than for someone else (Stephan, Rauch & Hatak, 2023), they also experience extreme stressors. This study addressed the most stretching workplace stressor for entrepreneurs: firm insolvency. While being an entrepreneur facilitates feelings of autonomy, independence, and personal fulfillment (Wach et al., 2020), business failure contaminates these outcomes, with devastating consequences for the affected individuals. Our study can be described as addressing the downside of engaging in entrepreneurial action.

We developed our hypotheses by building on the COR theory (Hobfoll, 1989), particularly the premises of resource loss, to examine how insolvency affects the psychological, biological, and physiological functioning of entrepreneurs. We expected that insolvency would cause substantial detriment to entrepreneurs’ subjective and objective well-being, and the study’s findings corroborate our hypotheses. We show that firm insolvency has negative effects on the subjective and biological stress markers (ηp2 = .06–.14 and Cohen’s d = –0.490–0.808) of entrepreneurs’ psychological well-being, vital exhaustion, and levels of stress hormones. We found large effects for the WHO-5 Well-being Index, and medium effects for vital exhaustion. These effects are quite substantial (cf. Bosco et al., 2015). We found rather low effect sizes (Haase et al., 1982) for cortisone (HEC) and HGC. These effects vanished after adding education as a covariate.

Using effect sizes as a measure is not unproblematic because they are influenced by sample selection and research design, which makes comparisons against the values obtained in other studies complicated (Richardson, 2011). As recommended in the study by Peng and Chen (2014), we have provided a confidence interval for each effect size (see Table 5). Furthermore, whenever possible, we compared the scores obtained by entrepreneurs facing insolvency against existing population norms, recognized cut-off values, and results from other studies. To increase the robustness of our findings, we conducted SEM analyses and included BMI and diagnosis of diabetes mellitus as control variables. The pattern of our results remained.

Our study contributes to the literature by drawing attention to the effects of insolvency on positive and negative components of entrepreneurs’ well-being. Our results suggest that firm insolvency increases the probability of developing depression and burnout syndrome. Over 60% of entrepreneurs in the insolvency group reported extremely low psychological well-being and very high (clinical) vital exhaustion. This result is consistent with a recent study conducted across 20 countries worldwide, which showed that enhanced firm-level adversity (induced by severe national lockdowns) negatively affected entrepreneurs’ life satisfaction and vitality during the Covid-19 pandemic (Stephan, Zbierowski et al., 2023). In our study, 41% (N = 19 entrepreneurs) of participants in the insolvency group displayed scores of well-being that, according to restrictive cut-off values by Lowe (2004), equaled the levels of well-being of patients with Diagnostic and Statistical Manual of Mental Disorders (4th ed, DSM-IV) major depression. Furthermore, we found a high prevalence of clinical exhaustion in insolvent entrepreneurs (60%). This is alarming because exhaustion is significantly associated with an increased risk for cardiovascular events and all-cause mortality (Cohen et al., 2017). While entrepreneurship is inherently stressful, our findings indicate that insolvency represents a significant risk factor for entrepreneurial well-being. Specifically, insolvency is associated with a 16.75-fold increase in the prevalence of severe mental health impairments and a 2.5-fold increase in vital exhaustion among affected entrepreneurs compared with the control group. Based on the utilization of objective biomarkers and the actigraphy method, we also found physiological impairments (i.e., elevated stress hormone level and slightly lowered sleep quality) within the firm insolvency group. This highlights insolvency as an extreme stressor that may dysregulate endocrine processes in entrepreneurs, leading to physical health disorders (Adam et al., 2017) and higher allostatic load. In fact, stress leads to an enhanced activity of the hypothalamus–pituitary adrenal (HPA) axis, resulting in an increased release of glucocorticoids from the adrenal cortex (Wolf, 2009). In healthy adults, elevated levels of glucocorticoids are associated with working memory impairment (Kirschbaum et al., 1996). In an Irish population-based sample of older adults (> 54 years old; Feeney et al., 2020), high cortisone was found to be inversely associated with memory and global cognition. Our observation that the cortisone levels in the hair of insolvent entrepreneurs were twice as high as those of the control group is concerning, particularly given the potential implications for cognitive impairments (supported by our supplementary analyses, see section 4.4.4.). Our results revealed that insolvency may indeed interfere with cognitive functioning in entrepreneurs as we found a significantly higher inclination for less risk adjustment in insolvent entrepreneurs. Our study participants in the insolvency group did not adapt their (gambling) behavior well to the given risk level, promoting suboptimal decision-making. Inaccurate risk adjustment and related inflexible decision-making may have serious consequences for entrepreneurs dealing with and recovering from insolvency, including risk of inadequate allocation and loss of resources.

Regarding physiological recuperation, we documented significantly poorer sleep quality in entrepreneurs confronted with firm insolvency. Reduced sleep efficiency in insolvents is particularly concerning since allostatic load is a risk factor for morbidity and mortality (McEwen, 2007). In a study of German entrepreneurs, lower objective sleep efficiency predicted diminished psychological well-being (Wach et al., 2021) and less creativity (idea generation) on a subsequent day (Weinberger et al., 2018). On a more positive note, sleep duration (self-reported) has been found to prevent entrepreneurs’ exhaustion (Murnieks et al., 2020), and we found that the sleep quality of all study participants exceeded 85%, which is considered efficient (Jung et al., 2017).

Contrary to the expectation that firm insolvency provides a learning opportunity that helps entrepreneurs who have previously failed to achieve better future performance (Ucbasaran et al., 2013), we observed that participants in the firm insolvency group had experienced prior insolvency significantly more often. This signals that firm insolvency is not always a valuable lesson.

Overall, our study clearly suggests that insolvency is a disastrous experience that may manifest at various levels of entrepreneurs’ functioning. In particular, it negatively affects subjective well-being, upon which it exerts effects of high magnitude.

Theoretical and practical implications

This study was designed on the theoretical pillars of the COR theory (Hobfoll, 1989). While the positive spiral of resource gain predicted in this theory has been studied in entrepreneurship before (Laguna et al., 2017; Laguna & Razmus, 2019; Lanivich, 2015), few researchers have looked at the spiraling nature of a resource loss. The idea that resource loss facilitates stress and harms well-being is highly pertinent to the context of entrepreneurship, particularly given that firm insolvency is on the increase. Our research supports the notion that the COR theory (Hobfoll, 1989) is a viable framework for studying business failure from the individual micro-level perspective; however, as pointed out by Sonnentag and Meier (2024), when gain and loss cycles are being tested, it is necessary to differentiate the within-person processes from the between-person perspective and to account for specific temporal frame. This research strand is promising and should be extended in the future to better understand how entrepreneurs stay healthy and engaged despite setbacks.

Our study has aligned theorizing about the potential effects of firm insolvency on entrepreneurs’ psychological and physiological functioning by utilizing multiple specific measures of such outcomes. In line with the research agenda proposed by Stephan, Zbierowski et al. (2023), we included both positive and negative well-being indicators to extend our understanding of the entrepreneurship–well-being nexus. We found a very consistent pattern of relationships, suggesting that firm insolvency is associated with deficits in functioning in all the considered areas and across various components of well-being. However, the effects regarding stress hormones need to be taken with caution, as they seem to be affected by formal education, which is the most critical human capital investment (Solomon et al., 2022). Our study mirrors other work in finding discrepancies between the subjectively and objectively measured effects of insolvency (i.e., low-size effects in physiological measures vs higher effects in self-reports). This phenomenon has been well documented in the literature (Fried et al., 1984; Semmer et al., 2004).

It is intriguing that cortisone but not cortisol was higher in entrepreneurs in the firm insolvency group, highlighting the need to consider this hormone as a sensitive (and therefore promising) biomarker when exploring stress in the context of entrepreneurship. In addition, relationships between stress hormones and entrepreneurs’ education should be further considered. In that regard, our study results raise the question of whether formal education can help entrepreneurs to offset stress related to insolvency. If so, it is worth empirically testing whether it is formal education or intelligence that accounts for better physiological functioning (better sleep, lower stress hormones levels) in times of financial hardship. For instance, entrepreneurs who score higher on emotional intelligence may be more successful at navigating crises and acquiring social support. Consistent with previous research showing that serious stressful life events are associated with increased HGC (Dettenborn et al., 2010), our study highlights that business insolvency represents an extreme situation in entrepreneur’s lives even though slightly less than half of new firms survive longer than 5 years in the EU’s business economy (European Commission, Eurostat, 2023). Moreover, our examination of vital exhaustion, stress hormone concentrations, and diminished sleep quality allowed us to focus on less-researched aspects of negative well-being, thus addressing the “positivity bias” in entrepreneurship research (Stephan, Rauch & Hatak, 2023).

Our study does not resolve the question about the impact of firm insolvency on entrepreneurs’ functioning, but it proves there are several essential differences between those who suffer from financial hardship and those who do not. Future research should elaborate on temporal perspectives when studying the effects of firm insolvency on specific indicators of well-being. To better understand the underlying mechanisms, it is necessary to consider the short-, medium-, and long-term effects of insolvency. For instance, the grief and negative emotions that accompany firm insolvency may immediately impair sleep quality through rumination and worry (Clancy et al., 2020), whereas long-term exposure to increased glucocorticoid concentrations may affect cognitive functioning in the longer run. Furthermore, studying mediators such as rumination or psychological detachment in the stressor–strain process related to firm insolvency is important. Future research may also want to consider moderators. For instance, coping humor and optimism seem relevant for re-entry into serial entrepreneurship (Hwang & Choi, 2021). The proposition formulated by Patel et al. (2019) that individuals who employ higher levels of problem-focused coping could experience lower levels of allostatic load, which would in turn improve their well-being, could be tested in the context of firm insolvency.

To combat the negative effects of firm insolvency on entrepreneurs, we need research that explores factors that support entrepreneurs in crisis and facilitate learning processes. For instance, self-esteem and self-efficacy could be viewed as potentially protective factors when studying the impact of firm insolvency on entrepreneurs. This is important, given that a study in the context of the Covid-19 pandemic (Meyer et al., 2022) indicated that self-efficacy was the most important resilience factor against the perception of experiencing high levels of stress. Beyond targeting trait-like individual resources, there are multiple ways in which specific interventions can support entrepreneurs in crisis. In this regard, Schermuly et al. (2021) reported that short-term coaching can increase the well-being and vigilance of insolvent entrepreneurs. In similar vein, low doses of mindfulness meditation training demonstrated improvement in specific antecedents of successful opportunity recognition (i.e., alertness creativity and entrepreneurial self-efficacy) in nascent entrepreneurs (Moder et al., 2023). Furthermore, stress management programs seem to effectively decrease vital exhaustion (Koertge et al., 2008). Similarly, engagement in mindfulness exercises and getting longer sleep were both found to significantly reduce perceived exhaustion in entrepreneurs (Murnieks et al., 2020). Yang et al. (2021) suggests that at times when entrepreneurial identity is threatened (e.g., while dealing with firm insolvency), entrepreneurs with a high level of trait mindfulness may be better able to avoid emotional rumination about their work. This may help them to recover better and safeguard their well-being, something that was proposed by Wach et al. (2021), who found that work stressors and a lack of psychological detachment impaired entrepreneurs’ well-being in a study with a short-time perspective.

Finally, based on our supplementary results showing that insolvent entrepreneurs’ risk adjustment is substantially lower than that of the control group, we contribute toward better understanding of how stress might prompt inadequately considered (financial) decisions. To rule out the possibility that poor risk adjustment among entrepreneurs predicts insolvency, future research should examine cognitive performance prior to insolvency, during the stressful period of business failure, and after entrepreneurs have recovered. We argue that future research in this field should complement cognitive performance tests (which are inherently susceptible to age, education, and general mental ability) with measures that are more proximal to entrepreneurship activities (i.e., including indicators of opportunity recognition, alertness, and innovative work behavior).

From the practical perspective, we make the following recommendations. According to the COR theory, individuals who experience resource loss are prompted to protect, rebuild, and develop resources (Hobfoll et al., 2018). This is where practitioners may aid entrepreneurs, perhaps by offering affordable services geared to assisting entrepreneurs’ recovery after an insolvency-related crisis. Such services might include resources-oriented coaching (Schermuly et al., 2021), building resilience (Bullough & Renko, 2013), or capitalizing on the learning benefits of past negative entrepreneurial experience (Lafuente et al., 2019). Our study also offers guidance regarding areas of functioning that are negatively affected by firm insolvency, and which need to be rebuilt and protected. However, we warn against giving less attention to entrepreneurs’ sleep based on our study results. Although we found good sleep efficiency in insolvent entrepreneurs, this might result from the fact that our sleep data were, on average, collected 9 weeks after signing for insolvency. It could be that our participants felt relieved after registering insolvency. In the period preceding this difficult decision, entrepreneurs might have suffered more from insomnia.

According to our findings, subjective well-being must be particularly addressed because business readjustment (including merger, reorganization, bankruptcy, or insolvency) qualifies as a major life event in the sense of Holmes and Rahe (1967). While the death of a spouse is classified as a social event requiring the highest change in ongoing life adjustment, firm insolvency ranks at 15 out of 43 events, representing life stress of significant magnitude. Our findings highlight the need to provide services for entrepreneurs that will help them deal with crises as early as possible to prevent resource loss spirals from forming. Hence, entrepreneurs exposed to firm insolvency should be properly informed about the opportunities for emotional and instrumental support; at the latest, this should be done when they are registering insolvency. As impairments in well-being are consequential not only for the individual entrepreneur but also for their immediate social context, it is also worth considering business partners and family members when designing support for entrepreneurs dealing with firm insolvency.

At the societal level, we suggest that implementation of more entrepreneur-friendly laws might significantly improve the situation of insolvent entrepreneurs. In case of Germany, the insolvency process is primarily structured to serve the legitimate goal of creditor protection (German Federal Ministry of Justice, 2024a). However, this focus often comes at the expense of supporting entrepreneurs in their efforts to achieve a fresh start. This is evidenced by the comparatively high personal costs faced by failed entrepreneurs in Germany, particularly when contrasted with other OECD (Organisation for Economic Co-operation and Development) countries such as United Kingdom, United States, or France (Wölfl, 2021). For example, it can take up to 10 years for German entrepreneurs to be considered creditworthy again after an insolvency. Unfortunately, the stigma associated with business failure is so high that an entrepreneur-friendly insolvency law may be ineffective (Lee et al., 2007). These circumstances not only may hinder psychological well-being and the ability to learn from failure, but they also discourage potential entrepreneurs.

Study limitations

Our study should be regarded as a first step in addressing the impact of firm insolvency on entrepreneurs’ psychological (well-being), biological (stress hormones), and physiological (sleep) functioning. The study’s limitations include its cross-sectional study design, and our inability to collect data prior to insolvency. Together, these prevent us from determining how much of the difference between our two groups of entrepreneurs can be attributed to business insolvency. Although longitudinal studies are costly and demanding, we strongly endorse such research, not least because of its ability to explore reverse causality issues. Given the existing research evidence (including ours), we are inclined to view firm insolvency as a predictor of diminished psychological and physiological functioning. However, future studies should test reversed causality to better understand entrepreneurial well-being as a potential antecedent of firm insolvency. For instance, we found BMI to be positively related to HGC levels, but entrepreneurs may be prone to stress eating. While longitudinally designed studies would better address endogeneity issues, an experimental design and randomization into firm insolvency and control groups are impossible in this field. Nevertheless, future studies should rely on samples matched by key individual- and firm-related characteristics. This failed in this study because entrepreneurs in the control group were better educated, employed more employees, and experienced prior insolvency significantly less frequently.

Our sample turned out to be smaller than we had calculated in the power analyses beforehand. Therefore, to increase trust in our results, we disclosed effect sizes including partial eta squared (ηp2), which quantifies the effect size of a given independent variable on the dependent variable, accounting for the variance explained by other variables in the model. We also reported Cohen’s d effect sizes including confidence intervals and disclosed both statistically significant and non-significant findings. We thus align with the recommendation in the study by Shrout and Rodgers (2018) for improving research practices to advance knowledge in ways that improve replicability.

The majority of studies on business failure have been conducted outside of Germany. Thus, our study introduces a German perspective, which is important considering that each country has a different bankruptcy law (Armour & Cumming, 2008) and different attitudes to business failure (Ucbasaran et al., 2013). Taking a cross-cultural perspective may allow future research to better understand how such contextual factors relate to insolvency and its repercussions.

Our study advances the understanding of the physiological consequences of business failure on entrepreneurs by using unique physiological data, contrasting with previous research that relies on an exploratory qualitative research design (Singh et al., 2007). Although objective physiological measures of strain are influenced by a plethora of factors including circadian rhythms, physical exercise, food intake, smoking, and BMI, and they are not a panacea for all methodological problems, they have the advantage of overcoming the common method bias (Semmer et al., 2004). In particular, non-invasive hair sampling of cortisol and cortisone is free from many of the recognized methodological difficulties (Gerber et al., 2012) and it provides accurate measures of stress unless the investigated entrepreneurs are pregnant (Kirschbaum et al., 2009), suffer from diseases associated with disturbed HPA activation (Thomson et al., 2010), or are athletes, in which case an increase in cortisol can be induced through the repeated physical stress of intensive training and competitive races (Skoluda et al., 2012). Our study’s integration of objective data with self-reported measures enhances the robustness and depth of our findings.

Entrepreneurs operating firms with employees seem to suffer more from work-related stress (Hessels et al., 2017); future studies could therefore consider whether solo self-employment may act as a potential resource for those who are confronted with insolvency. That being said, this study found no significant correlations between employee number and the study’s variables, ruling out their impact on poor subjective well-being. In addition, including employee numbers as a covariate did not affect stress hormones or sleep quality.

From the theoretical perspective, we broadly relied on COR theory (Hobfoll, 1989). However, we did not operationalize entrepreneurial resources and nor did we measure their specific loss. We also focused on the premise of resource loss spirals alone; while this is central to entrepreneurship, it is not exhaustive. Studying how such loss spirals form and which areas of entrepreneurs’ functioning are most immediately or severely affected by firm insolvency was beyond the scope of this study. Future research should seek to gain more knowledge about temporal dynamics and different perspectives when studying insolvency based on COR (Sonnentag & Meier, 2024).

Our study supports the notion that entrepreneurship is an excellent framework to further develop our understanding of mental health and well-being (Gish et al., 2022). However, the physiological stress response related to entrepreneurship is complex (Patel et al., 2019). Studying exhaustion, stress hormones, and sleep cannot fully capture this complexity, and this study therefore only partially addresses the physiological outcomes of self-employment. Nevertheless, we believe that insolvency offers an excellent context to empirically test the nexus of entrepreneurship and well-being, and our study represents an important step toward this.

Despite some theoretical and methodological limitations, our research remains significant. Addressing the replication crisis and fostering confidence in findings within both psychology and entrepreneurship requires concerted efforts from multiple investigators (Maxwell et al., 2015). Our study serves as a foundation for future research, potentially facilitating meta-analyses that synthesize and generalize findings related to the relationship between business insolvency and well-being. Such concerted initiatives will be vital for advancing knowledge in this domain.

Footnotes

Appendix

The effects of firm insolvency on sleep efficiency.

| Coefficient | SE | z | p | [95% |

||

|---|---|---|---|---|---|---|

| Sleep quality | ||||||

| BMI |

|

0.081 | 3.09 | .002 | 0.1039 | 0.4649 |

| DM | 0.284 | 0.092 | −1.40 | .162 | −0.2733 | 0.045668 |

| Group | −0.155 | 0.085 | −1.81 | .070 | −0.3221 | 0.01291 |

| Intercept | 0.025 | 0.081 | 0.30 | .762 | −0.1352 | 0.18463 |

| Variance (HGC) | 0.533 | 0.084 | 0.3914 | 0.7248 | ||

BMI: body mass index; DM: diabetes mellitus 1 = yes, 2 = no; HGC: hair glucocorticoid concentrations (HCC + HEC).

Note: Group: 0 = control group, 1 = firm insolvency group. Coefficients are calculated as z-standardized values. Significant coefficients are in bold. Structural equation modeling (SEM) analyses conducted to predict firm insolvency impact on sleep efficiency. Log likelihood = –765.388, χ2 = 0.00, N = 84.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This project was funded by the German Research Foundation (DFG; WE 1504/22-1 and KI 537/35-1). We gratefully acknowledge the help of Johannes Sperling in the data collection. We would like to express our gratitude to the reviewers and editors of this special issue for their valuable feedback and insightful suggestions, which have greatly enhanced the quality of this article.