Abstract

Many firms may successfully navigate an organizational crisis, but may find themselves entangled in another soon after. Building on a resource-dependence perspective, this study evaluates how certain investor characteristics foster organizational resilience during a crisis by preventing a relapse following recovery. Drawing on data from 2014 to 2019, we analyzed 359 firms that faced a crisis in 2015, as indicated by their Altman Z-score values. Our findings reveal that diversity and patience of investors prevent firms from relapsing into upcoming crises; however, the probability of relapse increases when concentrated investors boost the firm’s capital during the in-crisis period. We bridge the gap between the resource-dependence theory and literature on organizational resilience and contribute by extending previous analyses on the relevance of investors to recover from a crisis to identify how in-crisis investors’ features also state the foundations to avoid future relapses.

Keywords

Introduction

Organizational crises manifest when managerial decisions falter in sustaining the alignment of a firm’s strategy with its evolving external environment (Furrer et al., 2007). Four in five business leaders anticipate that their firms will encounter an organizational crisis within the next 12 months, and nearly half of these leaders have formulated plans to expedite recovery (Deloitte, 2022). However, it is intriguing to note that emerging stronger from an organizational crisis and preventing a quick relapse into an upcoming crisis remains a relatively uncommon occurrence within the business sphere (PwC, 2022). Relapse prevention refers to a firm’s need to follow the right approach to avoid returning to an organizational crisis (Omorede, 2021). This involves implementing strategies and decision-making processes aimed at fortifying a firm’s resilience and mitigating vulnerabilities that could lead to a return to a state of crisis. Recovery from a crisis is urgent, but executive decisions must focus on a long-term implementation process to prevent relapse (Thürmer et al., 2020).

Organizational resilience encompasses the capacity of a firm to effectively respond to and absorb disruptions when they come (Kahn et al., 2018; Linnenluecke & Griffiths, 2010; Ortiz-de-Mandojana & Bansal, 2016; Williams & Shepherd, 2016), and the firm’s adaptive and transformative capabilities to mitigate disruptions before they occur (Lengnick-Hall et al., 2011; Van Der Vegt et al., 2015). Therefore, organizational resilience includes a firm’s capability to prevent relapses into upcoming crises.

In this context, previous management research on firms during organizational crises and the literature on resilience have predominantly focused on examining the decisions and strategies employed by firms to recover from such crises (e.g., Corey & Deitch, 2011; Gittell et al., 2006; Morrow et al., 2007), encompassing financial approaches (Dao, 2017), entrepreneurial management (Kusa et al., 2022), and environmental practices (DesJardine et al., 2019). However, it overlooks the critical aspect of sustaining resilience in the aftermath. While the notion of preventing relapse has been well established in the context of psychology and health-related studies, there is a noticeable gap in the examination of relapses concerning organizational crises, particularly in navigating crises and how external actors may influence a firm’s capability to prevent relapses into upcoming crises.

Resource dependence literature is useful to underscore that executive decision-making during a crisis is markedly influenced by external actors who provide resources (Drees & Heugens, 2013; Hillman et al., 2009; Pfeffer & Salancik, 1978). Among the external actors that can influence relapse prevention, we focused on firm investors because of the firm’s strong dependence on investors in crises situations (Abdurakhmonov et al., 2021; Choi et al., 2012; Desender et al., 2013; Lin, 2019; Schmid & Roedder, 2021). The investors play a relevant role in a crisis recovery by representing the most reliable source of accessible resources (Furrer et al., 2007) and invaluable social resources (Huang & Knight, 2017), and contributing to decision stability (Sakaki & Jory, 2019). However, investors’ influence on executives’ decisions can vary depending on specific investors’ characteristics.

Therefore, based on the resource dependence literature, we propose certain investor features, with underlying psychological characteristics (Duxbury et al., 1996; Nakai et al., 2018), to characterize their influence on executive decisions during a crisis period. Specifically, we propose that the diversity, concentration, and patience of firm investors in crisis situations strongly influence organizational resilience by reducing the risk of rapid relapse following recovery from an organizational crisis.

To empirically test our hypotheses, we selected a sample from all firms listed in the Refinitiv Eikon database that faced financial distress in 2015 (i.e., in-crisis year), but showed stability in 2016 (i.e., recovery year). Our results included a comprehensive analysis of these firms’ financial status from 2014 (the pre-crisis year) to 2019, and revealed that a higher level of investor diversity and patience is associated with a decreased likelihood of relapse following recovery. Conversely, an increase in the concentration of large investors during a crisis elevates the risk of relapse.

This study makes two significant contributions to the literature. First, it extends the resource-dependence perspective (Drees & Heugens, 2013; Hillman et al., 2009; Pfeffer & Salancik, 1978) by emphasizing that a firm’s dependence on external agents is inevitable in certain circumstances, and contributes by confirming that dependence on investors impacts not only the acquisition of diverse external resources and support (Choi et al., 2012; David et al., 2010), but also the development of a firm’s internal competencies such as organizational resilience for preventing relapses. Moreover, our results suggest that some investors’ characteristics, such as diversity and patience, help to understand the psychological traits influencing investors’ behavior in the aftermath of crises, which finally influences executive decisions, contributing to the prevention of relapses in crises.

Second, this study contributes to the domain of organizational resilience (Kahn et al., 2018; Sutcliffe & Vogus, 2003; Williams et al., 2017). The literature on resilience has traditionally focused on internal resources and recovery phase from a crisis, without focusing on factors that positively influence the subsequent phase of a recovery period. Prior literature on relapse prevention has been traditionally associated with psychological (e.g., Brandon et al., 2007; Homan et al., 2023), medical (e.g., Brandon et al., 2012), biological (e.g., Santos-de-Frutos & Djouder, 2021), and technological (e.g., Chen et al., 2021) contexts. By examining the post-recovery period in a management field, this study advances our understanding of crucial investor characteristics for preventing relapse and reinforcing organizational resilience. We find that investor diversity and patience contribute to resilient capabilities by fostering adaptability and long-term orientation in decision-making processes.

To sum up, we address the gaps in the literature regarding the prevention of relapse after a successful recovery from a crisis by examining how certain investor characteristics during the crisis period are crucial for resilience-based processes. We contribute to the resource dependence and resilience literatures by identifying and delimitating the role of investors in sustaining the corporate resilience in the post-crisis period.

Theoretical background

Role of investors in the resource-dependence perspective

In the event of an organizational crisis, internal resources become notably constrained, prompting firms to rely on external agents to acquire resources, thereby fortifying their capacity to navigate challenges (Bass & Chakrabarty, 2014; Morrow et al., 2007). The resource-dependence perspective, articulated by scholars such as Drees and Heugens (2013), Hillman et al. (2009), and Pfeffer and Salancik (1978), extensively delves into mechanisms through which agents who provide these critical resources influence executive decisions (Abdurakhmonov et al., 2021; Bass & Chakrabarty, 2014). Reliance on investors’ resources intensifies during an organizational crisis, driven by the need to overcome the limitations posed by the firm’s internal reservoir of material, social, and financial resources, necessitating an external increase (Marcus & Goodman, 1991). Notably, while many external agents, such as suppliers or financial institutions, may hesitate to support firms facing financial adversity (López-Gutiérrez et al., 2015), investors emerge as a cornerstone of firm survival because they provide both direct and indirect access to resources (Van den Broek et al., 2017). For instance, Chhatwani et al. (2022) conducted a study demonstrating the influence of investors’ resource provision on firm survival during the pandemic. Consequently, investor reliance substantially influences the decision-making processes of firms undergoing crises (Furrer et al., 2007). This influence extends beyond the strategic aspects of decision-making and encompasses a nuanced understanding of the investors and executives’ cognitive and emotional dimensions (Alshebami, 2022; Zhao & Wibowo, 2021), and the individual psychological characteristics involved (Sheeran, 2002; Utsch & Rauch, 2000; Wang, 2014).

Previous studies, such as Duxbury et al. (1996) and Nakai et al. (2018), have delved into the examining psychological characteristics of investors to uncover the motivations behind their investment decisions or behaviors. Nakai and colleagues (2018) emphasize the importance of altruism and risk consciousness as two crucial psychological characteristics to understand the investors’ decisions. Investors may want to prioritize initiatives and decisions that contribute to organizational success, even if the returns are not immediate. However, their investment choices tend to lean toward safety and stability. In this context, Duxbury and colleagues (1996) identify different psychological characteristics in investors that emphasize their internal motivation, strong engagement with their work and investments within the firm, and a desire for autonomy in decision-making processes, alongside a focus on control in their influence on decisions. This autonomy is valued for making independent decisions while maintaining a connection or affiliation to the firm.

In our study, we explore how three pivotal investors’ characteristics (diversity, concentration, and patience) impact corporate decisions intended to reinforce organizational resilience. These investor characteristics are connected to psychological traits. Diversity in investors is related to autonomy in decision-making processes due to the range of perspectives and insights they provide (Gao & Hafsi, 2019; Santoro et al., 2020). The autonomy arises from that each investor’s unique perspective is considered, allowing for a more comprehensive evaluation of options. The desire for control is a psychological characteristic that manifests strongly in concentrated investors, as they seek to actively shape, influence, and guide decisions that align with their strategic vision for the firm (Carpenter & Westphal, 2001; Hadlock & Schwartz-Ziv, 2019). These investors tend to take a cautious, consciousness, and conservative approach to decision-making to minimize risks (Deudon et al., 2015; Thomsen & Pedersen, 2000). Finally, investors’ patience is closely linked to psychological characteristics such as motivation, and high engagement with the firm. When investors exhibit patience, it suggests a high level of motivation and engagement (Thürmer et al., 2020; Tucker, 2017), as they are willing to endure longer timelines in the pursuit of sustained success over immediate returns and uncertainties (Lv et al., 2019; Sajko et al., 2021; Sakaki & Jory, 2019).

We propose that the distinct characteristics of investors play a crucial role in shaping the contributions they make in a crisis situation, highlighting the essential role of their contributions in cultivating a resilient approach to prevent relapse following an organizational crisis.

Developing organizational resilience to prevent relapses

Sutcliffe and Vogus (2003) are notable for pioneering the concept of a “resilient organization” emphasizing an organization’s capacity to rebound from disruptions while fortifying the organizational structure to prevent relapses and foster enduring stability. Recent literature on resilience identified three factors that are crucial for supporting organizational resilience. First, the capability to cultivate adaptive decision-making processes (DesJardine et al., 2019) by incorporating diverse perspectives and information integration (Salas-Vallina et al., 2022; Santoro et al., 2020). Second, organizational resilience is bolstered by the capacity for cohesion (Beckman & Stanko, 2020), collaboration among individuals (Harrison et al., 2010), and the establishment of trustworthy relationships (You & Williams, 2023). Third, organizational resilience is exemplified by consistent performance amid chaos, as evidenced by established routines in which long-term decision-making processes (Farjoun, 2010) enable stability and control in performance despite disruptions.

Drawing on the resilience literature, we propose that investors with specific characteristics such as diversity, concentration, and patience may foster resilient capabilities (Utsch & Rauch, 2000; Zhao & Wibowo, 2021), thereby facilitating executive decisions that hold the potential to prevent relapse (Chhatwani et al., 2022). Specifically, we propose that diverse investors bring adaptability to decision-making processes; concentrated investors support collaborative decision-making, while patients bring stability to decision-making processes, collectively enhancing the firm’s overall resilience and ability to prevent relapses after successfully navigating through an organizational crisis.

Hypotheses

Diversity of investors and relapse prevention

In the aftermath of an organizational crisis, a firm requires fresh perspectives as previous practices and resources are inadequate to prevent a subsequent crisis (Williams & Shepherd, 2016). The diversity of investors during crises can influence the decisions of executives, affecting the future of the organization by providing diverse experiences that encompass various management perspectives (Gao & Hafsi, 2019; Santoro et al., 2020), varied information (Chang & Hong, 2002; Lien et al., 2021), connectivity between the firm and its external environment (Nadeem, 2020), and fostering innovative approaches and strategies (Sakaki & Jory, 2019). This access to a diverse array of information and perspectives from diverse investors during the recovery period brings about more adaptive decision-making processes (DesJardine et al., 2019).

The motivation to retain diverse investors in times of crisis will prompt the executives to adopt more diverse solutions and approaches. To secure continued support, executives must navigate this diversity by tailoring strategies that align with the preferences of different investors (Lv et al., 2019). This decision to adopt a range of different solutions to accommodate investor diversity during crises equips executives with tools to navigate the challenges of the post-crisis period that enhance the organization’s resilience and ability to prevent a potential relapse.

Therefore, the diversity of investors improves executive decisions, as it may integrate diverse information and perspectives to make a better decision (Schulz-Hardt & Mojzisch, 2012) and enable the adaptation of executive decisions to evolving environmental conditions (Choi et al., 2012; Groenendaal & Helsloot, 2020). We propose that this situation may seem relevant to avoid future relapses after a crisis. Therefore, we hypothesize as follows:

Hypothesis 1 (H1). Higher intensity of investor diversity during the in-crisis period is negatively associated with relapse after recovery.

Increase in concentration of investors and relapses prevention

Jabbouri and Naili (2019) define concentrated ownership as “investors holding a significant equity claim in the firm that grants them both the incentive and the power to discipline managers” (p. 284). Previous research has established a correlation between concentrated investors during organizational crises and a reduction in insolvency risk (e.g., Iannotta et al., 2007), an improvement in firm performance (e.g., Gaur et al., 2015), and an increase in firm value, attributed to the effective monitoring capabilities of large investors (e.g., Granado-Peiró & López-Gracia, 2017). We propose that an increased concentration of investors during a crisis influences executives’ behavior in a manner that guides them toward making decisions aimed at preventing relapse by mitigating risks that would be especially negative for these investors.

Considering the high proportion of a firm’s assets that concentrated investors retain (Hamadi, 2010), they exhibit a significant interest in the firm’s survival. Moreover, investors with significant stakes have increased opportunities to influence managerial decisions and shape a firm’s management strategies (Carpenter & Westphal, 2001; Hadlock & Schwartz-Ziv, 2019; Taghian et al., 2015). This results in stronger incentives to limit excessive risk-taking compared with firms including investors with more limited engagement (Deudon et al., 2015; Thomsen & Pedersen, 2000). Therefore, with concentrated investors increasing in times of crisis and exercising influence, the firm tends to take fewer risks, as these investors are deeply vested in the firm’s success and motivated to avoid excessive risk taking.

Moreover, the need for collaboration becomes paramount in the aftermath of an organizational crisis. An increase in the concentration of large investors during times of crisis contributes to the development of a trusting relationship between investors and the executive team (Salas-Vallina et al., 2022), as these investors choose to remain with the firm even during challenging times. Unlike smaller investors, who may opt to exit during crises, large investors with concentrated ownership stakes display a true commitment to firms’ success and resilience.

The concentration of large investors fosters a collaborative and trustworthy climate, and contributes to the establishment of shared leadership in the decision-making processes. In this shared leadership model, large investors align with executives (Lin, 2019), and actively participate in collaborative processes and strategic planning (Dufour et al., 2019; Lin, 2019; Sakaki & Jory, 2019). Hence, the concentrated investors’ commitment with the firm and their interest to reduce future risks make a strong influence in the executives during a crisis period.

Therefore, we suggest that an increase in the concentration of large investors during turbulent times contributes to an organization’s resilience and ability to sustain stability post-crisis. Accordingly, we hypothesize as follows:

Hypothesis 2 (H2). An increase in the concentration of large investors during in-crisis period is negatively associated with relapse after recovery.

Patience of investors and prevention of relapse

Following an organizational crisis, it is relevant for executives to ensure that external stakeholders offer them the opportunity to look at the long-term key aspects of the firm, including financial health, operational functions, and overall organizational coherence. While adopting a long-term orientation in decision-making contributes to preventing potential relapses into crises, a volatile and short-term orientation can impede the development of organizational resilience (Lv et al., 2019; Tucker, 2017).

The degree of turnover among principal investors plays a pivotal role in determining a firm’s inclination toward long- or short-term decision orientation (Dupuy et al., 2010). Drawing from existing literature (e.g., Dupuy et al., 2010; Goyal & Low, 2019; Tucker, 2017), we define “patient investors,” often referred to as “patient capital” or “low-turnover investors,” as those who have been actively involved in organizational decision-making and practices over an extended period. These investors are more likely to influence executives to make long-term decisions because of their stability and commitment to the firm over time (Thürmer et al., 2020; Tucker, 2017). Furthermore, their prolonged involvement allows them to accumulate comprehensive knowledge and insights into the internal performance of the firm as well as the decision-making processes of executives (Dupuy et al., 2010). Therefore, patient investors reflect a genuine interest in a firm’s resilience and survival, along with a strategic, long-term approach (Lv et al., 2019). By contrast, “impatient investors” or high-turnover investors are inclined toward seizing immediate opportunities, advancing self-interest (Dupuy et al., 2010), and exhibiting limited commitment to the firm (Goyal & Low, 2019), resulting in a preference for short-term approach (Wang, 2014).

Consequently, the sustained commitment exhibited by patient investors during disruptions reflects a strategic partnership (Rogbeer, 2009). This temporal stability allows decision-makers to navigate difficulties with greater clarity and looking at the long term because of the influence of patient investors. On one hand, patient investors can afford executives the advantage of time for strategic decisions, enabling a more thoughtful and comprehensive approach to decision-making. Executives can pursue structural advancements that require extended planning and implementation. Unlike situations with impatient investors, where the emphasis may be on immediate performance improvements, the presence of patient investors enables executives to focus on enduring and transformative strategies (Dean & Sharfman, 1996; Khatri & Ng, 2000). On the other hand, these investors remain committed to the organization despite crisis circumstances, enhancing the organization’s credibility, reputation, and reliability from external stakeholders’ perspective. Highly reliable organizations exhibit continuity and error-free functioning even in turbulent environments (Bigley & Roberts, 2001). This improved credibility increases the likelihood of establishing long-term relationships with external agents in times of crisis.

Therefore, we propose that investors who maintain their position in a firm for an extended period are more likely to contribute to the maintenance of organizational resilience over time by influencing executives to maintain long-term approaches that will help prevent relapses. We thus hypothesize as follows:

Hypothesis 3 (H3). Greater continuity of patient investors during the pre-crisis period is negatively associated with relapse after recovery.

Method

Sample and data collection

Our sample encompasses firms listed in the Refinitiv Eikon database showing a pattern of crisis and recovery that allows us to examine potential relapses after recovery. Specifically, we analyzed firms that met the following criteria: maintained a stable financial status in 2014, experienced a financial crisis in 2015, and subsequently recovered in 2016. Consistent with established methodologies in prior research on corporate crises (e.g., Boubakri & Saffar, 2019; Tong et al., 2020), we employed the Altman Z-score index as a metric to evaluate each firm’s financial health (Altman et al., 2017). A score below 1.81 was set as an indicator of a high risk of potential bankruptcy (Altman et al., 2017). This screening process yielded 359 firms for our analysis.

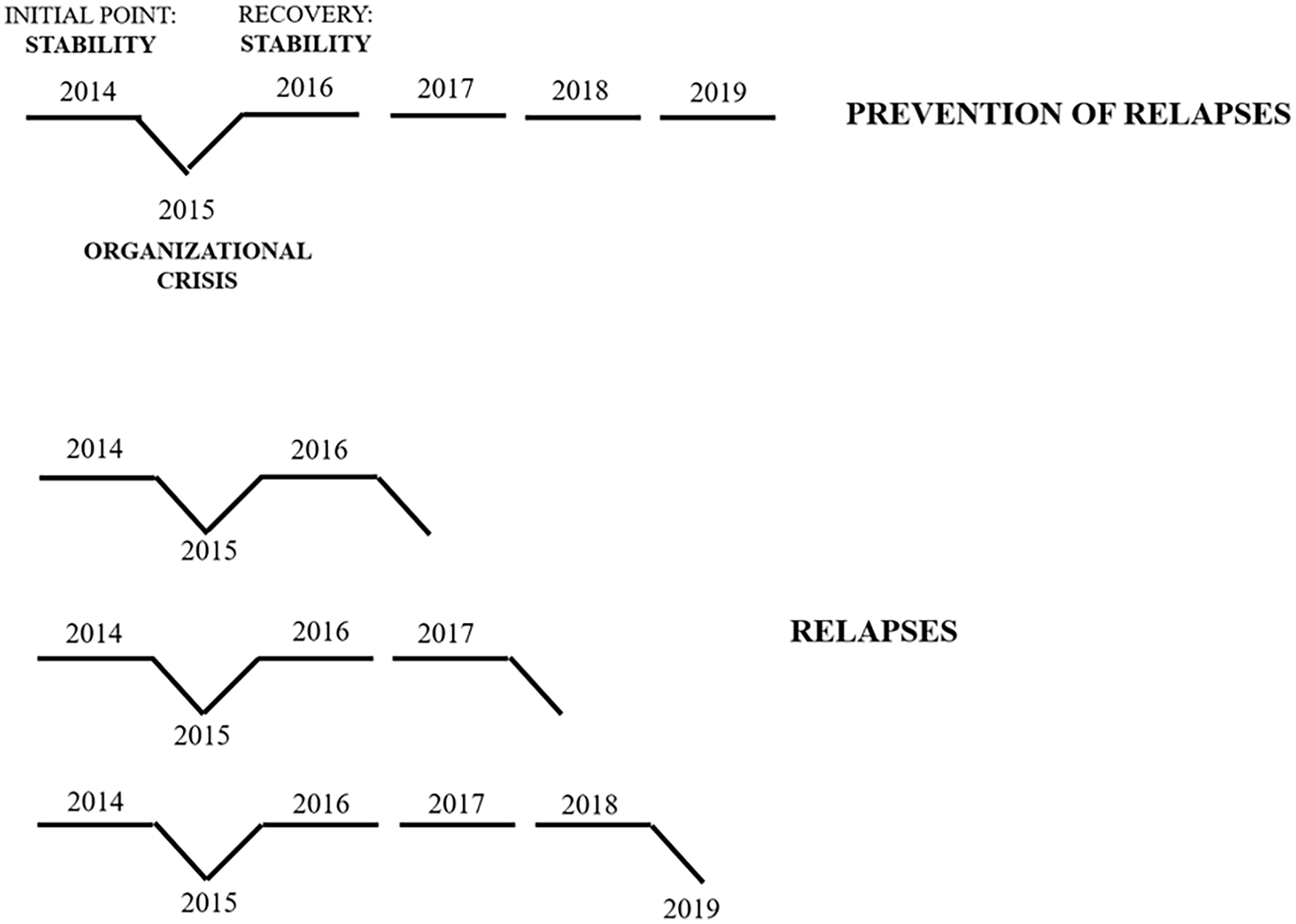

To construct our sample, we initially identified firms in the database that were in the crisis recovery phase. This involved identifying firms facing financial distress in 2015 that subsequently rebounded in 2016. To ensure the exclusion of firms with a protracted history of financial difficulties (which may make them susceptible to relapse), we required a stable financial situation in 2014. In addition, we examined whether these firms encountered subsequent crises in 2017, 2018, and 2019 (see Figure 1). Figure 1 illustrates the profile of an organization that exhibited stability and successfully averted relapses into crises from 2016 to 2019. By contrast, it contrasts with other organizations that encountered relapses into organizational crisis periods in the subsequent years (2017, 2018, or 2019) after a recovery process initiated in 2016. The selected timeframe for analysis, from 2014 to 2019, was deemed appropriate, as it affords a comprehensive view of several consecutive years, encompassing crisis and recovery, and allows for an assessment of the stability of the recovery phase. We excluded data from 2020 and 2021 to avoid potential distortions arising from the global pandemic. The exclusion of these years was deemed necessary to prevent confusing effects in our findings, given the unique and disruptive economic and psychological circumstances that characterized this period driven by the influence of COVID-19.

Prevention versus relapses into organizational crisis period.

Our final sample comprised firms from 42 countries in five regions: America (30.1%), Europe (13.4%), Asia (41.5%), Africa (2.2%), and Oceania (12.8%). They came from different sectors of activity, such as energy and utilities (7.5%), materials (30.9%), industry (16.6%), consumer discretionary and staples (18.4%), healthcare (6.4%), financials (2.8%), information and communication technologies (ICT; 14.8%), and real estate (2.3%). The diversity of sectors and countries provides this study with opportunities for generalization.

Variables

Dependent variable

The dependent variable is referred to as “relapsing after recovery.” It is operationalized as a dichotomous variable. Specifically, it takes a value of 1 if the firm successfully recovered from the corporate crisis in 2016 (indicated by an Altman Z-score > 1.81) but subsequently experienced a relapse in 2017, 2018, or 2019 (signified by an Altman Z-score < 1.81). Conversely, it assumes a value of 0 if the firm recovered in 2016 and did not encounter a relapse into corporate crisis in any of the subsequent years under consideration.

Explanatory variables

The explanatory variables include investor diversity, concentration, and patience. Investor diversity was assessed using a geographic diversification index derived from entropy (Tsai et al., 2020). This index measures a firm’s investors “geographic diversification across different regions” for the in-crisis year (Qian et al., 2010, p. 1021). The entropy measurement results from the

where m is the number of regions from which all investors may have originated. Pi signifies the proportion of the ith region relative to the firm’s overall portfolio percentage across all regions. This is computed by dividing the total investor portfolio percentage in each country by the total investor portfolio percentage in 2015. A high value for this variable indicates a greater presence of diverse investors, whereas a value close to or equal to 0 indicates that most of the firm’s investors are from the same region.

The concentrated investors in each firm were defined as those holding more than 5% of the focal firm’s total holdings (Hadlock & Schwartz-Ziv, 2019; Kim & Cho, 2008; Zahedi et al., 2015). Following this criterion, the portfolio percentages of these large investors were aggregated and our variable of increase in concentrated investors includes the change in investor concentration calculated as the difference between the pre-crisis and recovery years (2014–2016). Elevated values of this variable indicate an increased concentration of large investors during the in-crisis period, whereas diminished values suggest a reduction in the degree of concentration of large investors during the period. Evaluating changes in investor concentration allows for a more detailed understanding of how the influence of large investor evolves over a critical in-crisis period.

Patient investors were measured by counting the years, within the 2010–2015 timeframe, during which the main investor belonged to the low-turnover portfolio category, as per the Refinitiv Eikon database classifications (encompassing high-turnover, moderate-turnover, and low-turnover portfolios). Therefore, this variable ranged from 0 to 6. A higher value (close to or equal to 6) indicates greater patience of the main investor as belonging to the low-turnover category for an extended time, while a value close to or equal to 0 indicates low patience of the main investor as belonging to a high- or moderate-turnover category for the analyzed period.

We also performed a robustness check on our final results, which involved substituting investor diversity in 2015 with a measure from 2010 to 2015. We also replaced concentrated investors, defined as those holding more than 5% of the total holdings, with the top five investors (regardless of their total percentage of holdings; Li et al., 2015; Yang et al., 2023). Furthermore, we replaced the presence of patient capital from 2010 to 2015 with its presence in 2015 alone. The outcomes were comparable to those of the original studies with no significant alterations in the findings.

Control variables. 1

We controlled for several factors that may influence the probability of relapse into a crisis, including firm size, stability of the firm’s country in the in-crisis year (2015), and the regions and sectors in which the firm operates according to the Global Industry Classification Standard (GICS sectors). The size of a firm significantly influences resilient capabilities in a firm (Ferrón-Vílchez & Leyva-de la Hiz, 2023). A larger organizational size may provide a buffer against crises by allowing for the diversification of operations, more extensive networks and collaborations, and increased adaptability driven by external support and resource access (Galkina et al., 2023). We use firms’ total assets value during an in-crisis year as a measure of firm size (Li et al., 2015; Ortiz-de-Mandojana & Bansal, 2016). Moreover, favorable economic development within a country, supported by sound financial policies and robust reserves, is essential for maintaining stable and resilient organizational operations (Dao, 2017; Marcus & Goodman, 1991). To assess the stability of a firm’s country, we measured it using the gross domestic product (GDP) per capita value in the different home countries of the analyzed firms from the World Bank database in the in-crisis year. Finally, we control by region and sector, as the prevention of relapse can be influenced by institutional factors.

Data analysis

Logistic regression models (Cox, 1958) are widely employed and effective statistical techniques for modeling binary dependent variables (Whitaker et al., 2021). Our models estimate the likelihood that specific investor characteristics are present in firms that experience a relapse after recovery (y = 1) compared with those that do not (y = 0). The regression coefficients quantify the influence of independent variables on the probability of an event occurring. A positive coefficient indicates that the variable increases the probability of relapse after recovery, whereas a negative coefficient indicates the opposite.

Results

Table 1 presents the descriptive statistics for the examined variables. Despite the modest correlations among independent variables, we assessed variance inflation factors (VIF) to ensure that collinearity did not influence our analyses. The observed values fell within acceptable thresholds, with no VIF surpassing 10, thereby affirming that heightened correlation is not a factor warranting concern (Hair et al., 1995). Furthermore, we constructed the models in a hierarchical manner to enable a comprehensive evaluation of the enhancement in model fit, while also eliminating the potential for spurious associations (Judge et al., 2010).

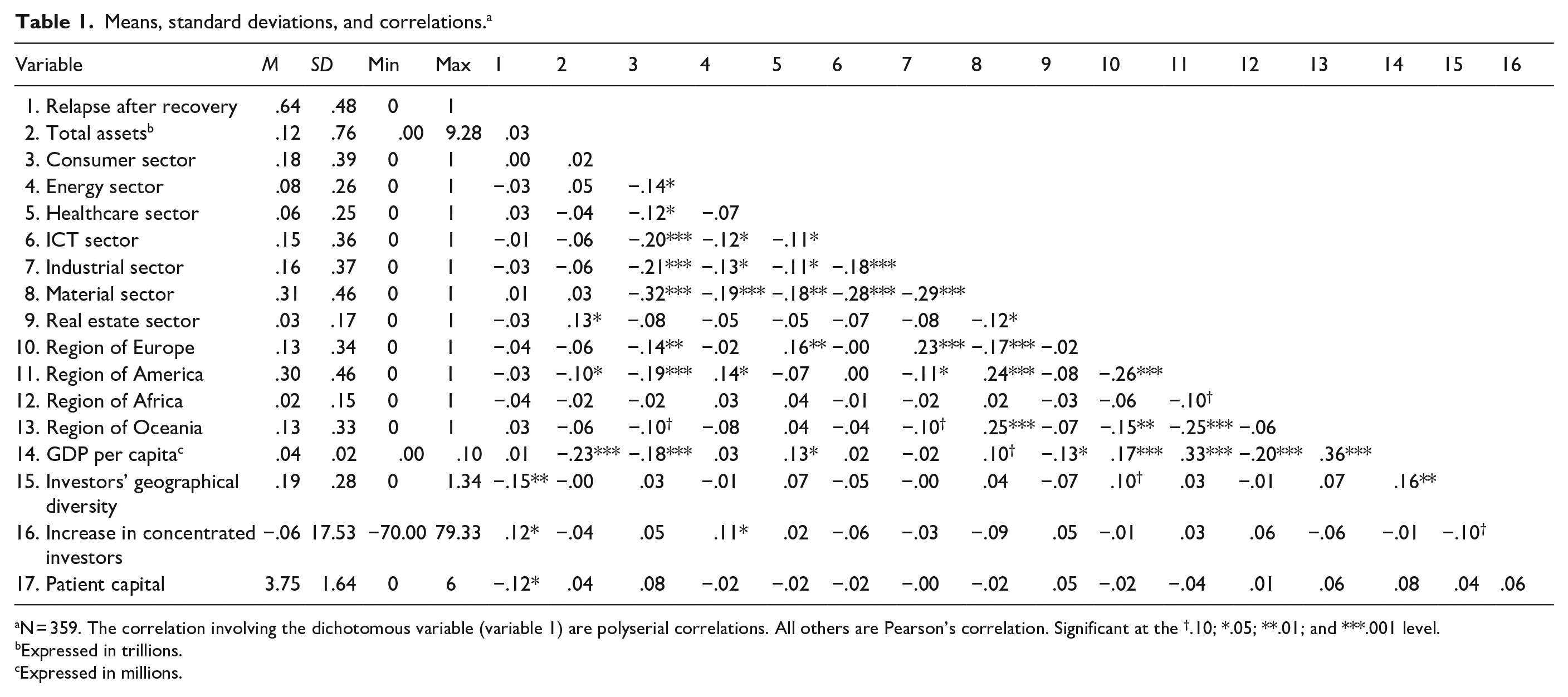

Means, standard deviations, and correlations. a

N = 359. The correlation involving the dichotomous variable (variable 1) are polyserial correlations. All others are Pearson’s correlation. Significant at the †.10; *.05; **.01; and ***.001 level.

Expressed in trillions.

Expressed in millions.

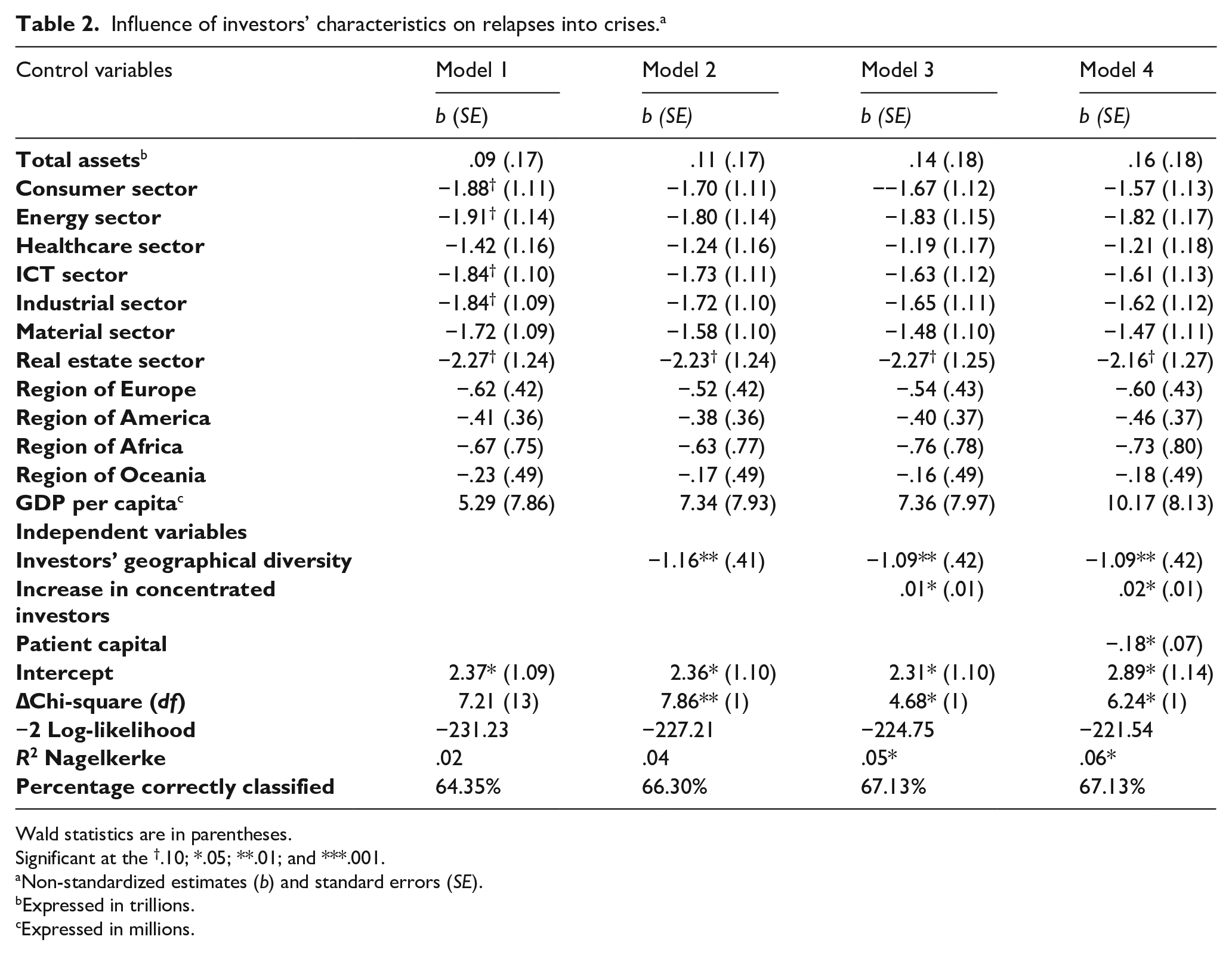

Table 2 presents the results of the binary logistic regression analysis. Model 1 serves as the baseline and encompasses the control variables. Subsequent models (Models 2, 3, and 4) progressively introduce the independent variables under examination. The likelihood ratio chi-square test for our final model (Model 4) demonstrates statistical significance (likelihood ratio [LR] chi-square [17] = 28.06| p = .031). Furthermore, the percentage of correct classifications improved from Model 1 (64.35%) to Model 4 (67.13%).

Influence of investors’ characteristics on relapses into crises. a

Wald statistics are in parentheses.

Significant at the †.10; *.05; **.01; and ***.001.

Non-standardized estimates (b) and standard errors (SE).

Expressed in trillions.

Expressed in millions.

Hypothesis 1 posits that firms characterized by a high degree of investor diversity are less susceptible to a relapse. This hypothesis is supported by the negative and statistically significant coefficient of investor diversity in Model 2 [coef. b = –1.16, odds ratio = .31| p = .005]. This finding suggests that holding all other variables constant, an augmentation in investor diversity during the run-up period with the crisis leads to a reduction in the odds of relapse after recovery by 3.23 times (i.e., 1/odds ratio, as the coefficient for the variable is negative) compared with firms lacking diversity in their investor base. Therefore, we conclude that our results support Hypothesis 1; consequently, investor diversity prevents the risk of relapse into organizational crises.

Hypothesis 2 proposes that an increase in the concentration of large investors diminishes the probability of relapse after recovery. Model 3 in Table 2 reveals a positive and statistically significant coefficient for increase in concentrated investors [coef. b = .01, odds ratio = 1.02| p = .030]. This finding means that the odds of relapsing into an organizational crisis are 1.02 times greater (i.e., the associated odds ratio, as the coefficient of the variable is positive) when large investors augment their degree of concentration during an in-crisis year. Consequently, these results do not support Hypothesis 2 as they show that heightened investor concentration during the in-crisis period amplifies the risk of relapsing into upcoming crises for the sampled firms.

Hypothesis 3 posits that the presence of patient investors reduces the probability of relapse. In Model 4, a negative and statistically significant coefficient is observed for patient investors [coef. b = −.18, odds ratio = .83| p = .013]. This finding indicates that, when compared with their absence, the odds of relapse after recovery are 1.20 times lower in the presence of patient investors (i.e., 1/odds ratio, given the negative coefficient). Consequently, the results empirically support Hypothesis 3, affirming that the presence of patient investors prevents the risk of relapse turning into an organizational crisis.

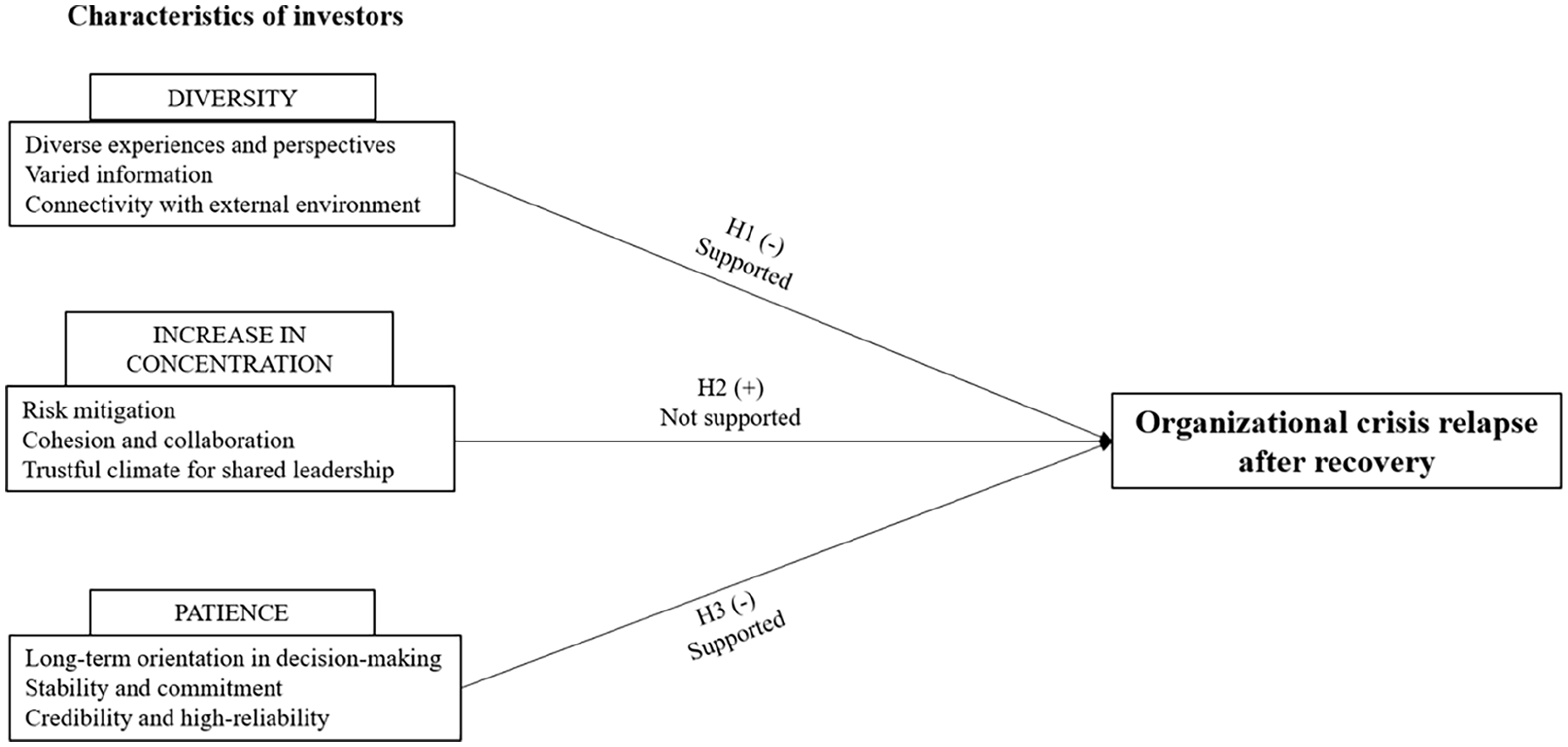

In summary, our findings underscore the positive impact of both investor diversity (Hypothesis 1) and patient investors (Hypothesis 3) on preventing a firm’s relapse. However, they also substantiate the influence of investor concentration, which contradicts our initial expectations and has a negative effect (Hypothesis 2); see Figure 2.

Contributions of each investor characteristic to the organizational crisis relapse prevention.

Robustness check

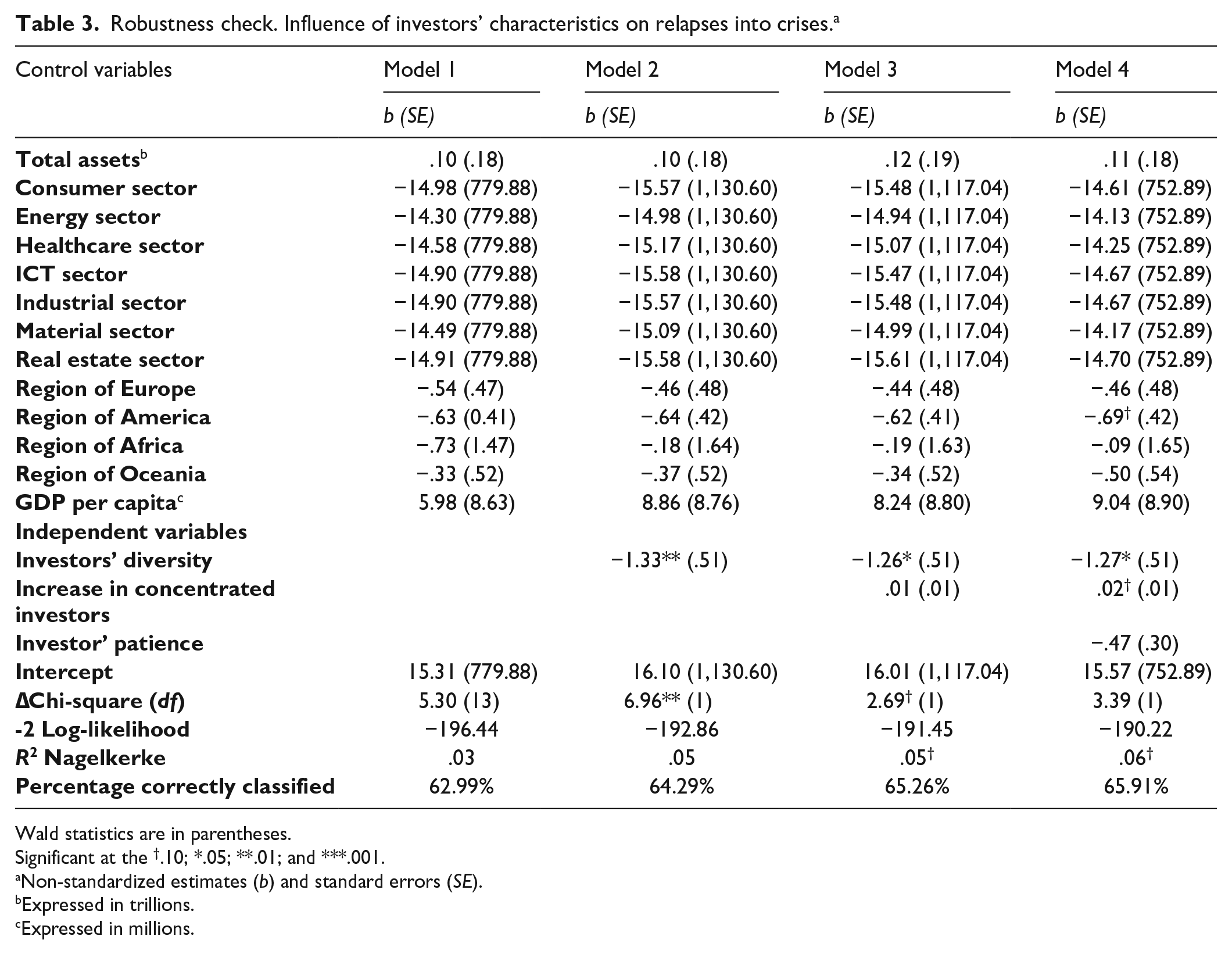

We conducted a robustness check to ensure that our findings were not contingent on idiosyncrasies in the variables. In addition, we employed a binary logistic regression model to examine whether our primary results exhibit variability based on the selection of different periods or investor characteristics. In particular, we analyzed whether the risk of relapse diminishes with investor diversity over an extended period (2010–2015), an increase in the concentration of the top five investors (regardless of their percentage holdings) (Li et al., 2015; Yang et al., 2023), and low turnover behavior in the principal investor in the in-crisis year (see Table 3).

Robustness check. Influence of investors’ characteristics on relapses into crises.a

Wald statistics are in parentheses.

Significant at the †.10; *.05; **.01; and ***.001.

Non-standardized estimates (b) and standard errors (SE).

Expressed in trillions.

Expressed in millions.

Table 3 presents consistent results that affirm the outcomes of our initial models. Model 2 indicates that the presence of investor diversity observed over an extended period leads to a reduction in the odds of relapse after recovery (i.e., the 1/odds ratio, as the coefficient for the variable is negative) by 3.85 times compared with a group of non-diverse investors over the same duration [coef. b = –1.33, odds ratio = .26| p = .008]. Similar to our initial model, Model 3 reveals that the probability of relapse into an organizational crisis is 1.02 times higher (i.e., the associated odds ratio, as the coefficient of the variable is positive) when the top five investors increase their concentration degree during the in-crisis period [coef. b = .01, odds ratio = 1.02| p = .101]. Finally, Model 4 suggests that investors exhibiting a low-turnover behavior in the in-crisis year reduce the odds of relapse after recovery by 1.59 times (i.e., 1/odds ratio, given the negative coefficient) compared with investors with a high-turnover behavior [coef. b = –.47, odds ratio = .63| p = .122].

While the variables for increase in investor concentration and patient capital exhibit a reduction in significance levels, they maintain the direction of the predicted results. This decrease in significance may be attributed to the smaller sample size (comprising 308 observations), which could potentially account for this change.

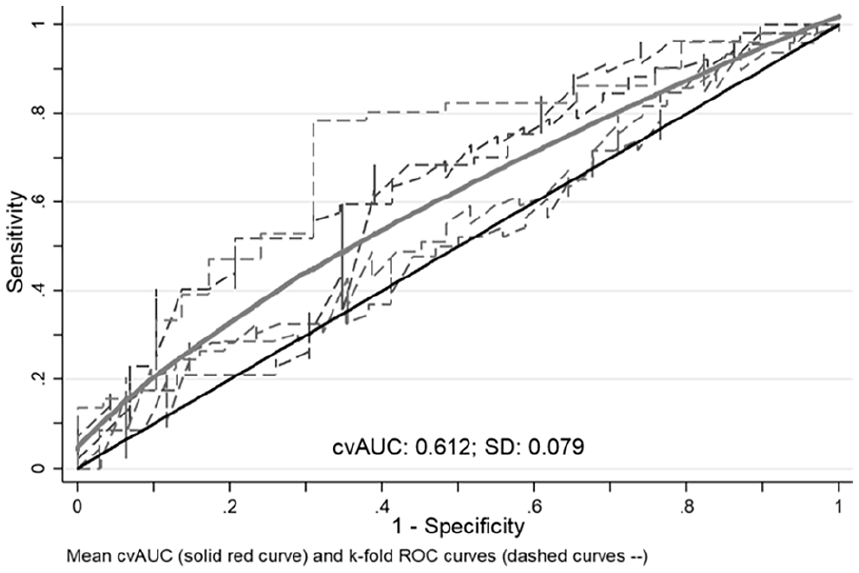

We also conducted a robustness check using a k-fold cross-validation analysis to ensure the reliability and stability of our findings (Huang, 2018). Cross-validation is a widely recognized data resampling method employed to assess a model’s generalization ability and mitigate the risk of overfitting (Berrar, 2018). The robustness check involved categorizing the dataset into “k” subsets, using a portion for training the model and the remainder for testing. The data were categorized into five k-folds of approximately the same size for each fold, yielding five data subsets. For each of the five data subsets, the cross-validation test used four k-folds for training, and one k-fold for testing. This process was repeated k times to obtain a value for each part. The final result was obtained by averaging the values obtained in each iteration, thereby providing a comprehensive assessment of model performance across different data subsets (Berrar, 2018).

Calculation using the cvauroc command in STATA showed 0.0453 points lower accuracy (area under the curve [AUC] = .6124) than the AUC computed using the classical approach from the predicted probabilities of relapse after recovery (AUC = .6577) (Luque-Fernandez et al., 2019). An AUC–ROC (receiver operating characteristic curve) of .6124 indicates that the logistic regression model can discriminate between firms that are at risk of relapse and those that are not. Although the ROC curve did not fully reach the upper-left corner of the graph, it rose above the diagonal reference line, as shown in Figure 3. Therefore, the model has the capacity to identify organizations at risk of relapse.

cvAUC and k-fold ROC curves.

Discussion, limitations, and future research

In the event of an organizational crisis, depletion of internal resources leads firms to rely intensively on external agents for the acquisition of additional necessary resources (Bass & Chakrabarty, 2014; Morrow et al., 2007). Drawing on the resource dependence theory (Drees & Heugens, 2013; Hillman et al., 2009; Pfeffer & Salancik, 1978), external agents that provide critical resources gain influence over executive decisions (Abdurakhmonov et al., 2021; Bass & Chakrabarty, 2014). Therefore, we propose that the characteristics of investors providing resources in a crisis situation influence whether executives can recover from a crisis by developing a more resilience-based orientation in decisions that help prevent relapses.

We analyze how certain investor characteristics (i.e., diversity, concentration, and patience), related to psychological characteristics, such as risk consciousness (Nakai et al., 2018), autonomy and control in decisions, motivation, and a high engagement to the firm (Duxbury et al., 1996), may prevent a rapid relapse following the recovery of a prior crisis period. Our findings complement prior research highlighting the significant dependence of firms in crisis on external resource providers and, consequently, the impact of these actors on managerial discretion (Bass & Chakrabarty, 2014; Morrow et al., 2007). While Wang’s (2014) study reveals that investors’ bargaining power in constraining abnormal accrual usage by managers is contingent on investors’ characteristics such as block-holding levels, investment strategies, and investment durations, our findings show that investors’ characteristics such as diversity and patience prevent the risk of relapse after recovery from an organizational crisis.

After running a logistic regression analysis, we first observe a significant and negative correlation between investor diversity and the probability of a relapse into crisis. These results are congruent with previous research showing that diverse investors contribute to organizational resilience by providing firms with innovative information exchanges (Chang & Hong, 2002; Lien et al., 2021), heterogeneous resources (Gedajlovic & Shapiro, 2002), and varied perspectives (Gao & Hafsi, 2019; Santoro et al., 2020), which subsequently influence the firm’s capacity for adaptive and flexible decision-making processes (Choi et al., 2012; DesJardine et al., 2019; Groenendaal & Helsloot, 2020). Our results show that a higher investor diversity during a crisis is associated with a lower probability of experiencing subsequent crises.

Second, our findings show a strong and positive correlation between investors exhibiting low-turnover behavior in their portfolios during the pre-crisis period and the probability of avoiding relapse into upcoming organizational crises. Our results confirm that patient investors contribute to establishing the requisite commitment for cultivating organizational resilience capabilities, exposing firmness and consistency in their behaviors (Thürmer et al., 2020). Therefore, our results suggest that patient investors’ display of high commitment in a firm’s long-term performance (Dupuy et al., 2010) and stable decisions (Dean & Sharfman, 1996; Farjoun, 2010; Khatri & Ng, 2000) play a relevant role in executives’ decisions that contribute significantly to the prevention of relapses.

Third, relapse prevention decreases when the concentration of large investors increases during an in-crisis period. These results differ from our expectations and suggest that the benefits of concentrated investors in the literature under regular circumstances (De Miguel et al., 2004; Gaur et al., 2015; Gedajlovic & Shapiro, 2002) may be less relevant in the analyzed crisis and post-crisis situations. Our results show that the negative consequences of concentrated capital are stronger than its positive implications when a firm has to recover from crises and suggest that the difficulties of concentrated capital to look at beyond their own short-term interest may influence here. The literature on concentrated capital has already shown that investor concentration may have negative consequences on collaborative relationships and firms’ adaptability (Desender et al., 2013; Zhang, 2006). These features are particularly relevant in developing resilience after a crisis, because collaboration with other agents (Harrison et al., 2010) and flexibility (DesJardine et al., 2019) are key factors in developing innovative processes that avoid previous mistakes (Omorede, 2021). Furthermore, Lo and colleagues (2016) argue that large investors misuse resources for their own benefits; besides, the higher the degree of concentration among investors, the greater the level of financial leverage (Granado-Peiró & López-Gracia, 2017), and lower the firm performance (Hamadi, 2010). Therefore, concentrated investors may focus in the short term to limit their risks in the event of a crisis. Hence, our results seem to indicate that concentrated capital in a crisis situation may be driven more by a desire to protect their immediate interests and ensure stability for themselves than by a long-term interest in the firm. In any case, we acknowledge that further research is warranted to ascertain the circumstances under which concentrated investors may either bolster or hinder organizational resilience.

Our contributions manifest in two ways: first, our article extends the traditional resource dependence theory (Drees & Heugens, 2013; Hillman et al., 2009; Pfeffer & Salancik, 1978) that highlights the implications of an in-crisis firm’s dependence on its investors (Choi et al., 2012; David et al., 2010) by demonstrating how investor characteristics also impact executive decisions that may prevent relapses into upcoming crisis periods. While much of the existing research on dependence resources underscores strategies for firms to mitigate their reliance on external actors, we highlight the significance of recognizing that dependence may be inescapable under particular circumstances, offering insights into its implications. The necessity for resources poses significant challenges in the event of an organizational crisis, and engaging with suppliers, financial institutions, or customers may involve uncertainties and risks. By contrast, main investors are more dependable sources of support (Bass & Chakrabarty, 2014; Dufour et al., 2019; Ramírez et al., 2022; Zheng & Xia, 2018). Therefore, while previous resource-dependence literature has discussed how in-crisis firms are highly dependent on investors during crises (e.g., Abdurakhmonov et al., 2021; Lin, 2019; Schmid & Roedder, 2021), our results show that investors’ characteristics also affect executives’ decisions that contribute to the prevention of relapses into upcoming crises. Our results also highlight the importance of complementing the resource dependence theory with the analysis of the psychological characteristics of investors when analyzing the influence of these external agents on organizational resilience.

Second, this study contributes to the literature on organizational resilience (Kahn et al., 2018; Sutcliffe & Vogus, 2003; Williams et al., 2017). The existing body of literature on organizational resilience has traditionally focused on organizational characteristics that help firms recover from a crisis (e.g., Corey & Deitch, 2011; Morrow et al., 2007; Omorede, 2021), leading to a notable gap in research related to the exploration of the subsequent phase of preventing relapses after a successful recovery to guarantee resilience. By shifting the analytical viewpoint to this often-overlooked phase, our study seeks to advance the understanding of factors that play a crucial role in preventing relapses after an organization has successfully navigated a crisis. Our logic suggests that a firm’s investors influence its organizational resilient capabilities in two distinct ways. On one hand, investors possessing specific characteristics (i.e., diversity and patience) play a role in building resilient capabilities (Choi et al., 2012; David et al., 2010). On the other hand, these characteristics involve heterogeneity in perceptions and information and high commitment and stability in decisions that support resilient capabilities such as adaptive and long-term decision-making processes. Therefore, we enrich the literature on the determinants of resilience, which conventionally concentrates on internal resources (e.g., Gittell et al., 2006) and corporate practices (DesJardine et al., 2019; Ortiz-de-Mandojana & Bansal, 2016), by joining the emergent literature (You & Williams, 2023) that highlights the significance of external actors in their interactions with firms.

This study has significant implications for practitioners. Beyond the provision of resources, our results show that investors wield a heightened influence over executive decisions because of firms’ heightened vulnerability during crises (Dufour et al., 2019). Accordingly, investors should be cognizant of their impact on a firm’s position and strategic orientation given that executives are particularly attuned to their preferences during crises. Moreover, the work exhibits implications in terms of managing investors’ relations to enhance resilience. On one hand, firms must strategically align themselves with investors who possess characteristics conducive to organizational resilience, such as diversity and patience. Actively seeking investors who align with the firm’s long-term objectives and values can contribute to a more resilient organizational strategy. On the other hand, clear and transparent communication channels with investors during both stable and crisis periods may foster commitment to resilience.

Furthermore, this study is relevant for regulators, as it scrutinizes specific pertinent attributes that can inform the development of governmental rescue initiatives. Regulators engaging in substantial investments to salvage firms facing severe financial distress must consider that investors’ characteristics at the time of financial assistance can influence the long-term efficacy of such aid. Understanding how certain investor characteristics influence the long-term effectiveness of financial support provides a basis for designing more effective rescue programs tailored to the specific needs of each situation. Furthermore, policymakers can leverage the study’s insights to advocate for policies that encourage diversity and patience among investors. This can be particularly relevant in regulatory frameworks that incentivize long-term investment strategies, ultimately promoting stability and resilience within the broader economic ecosystem.

In addition, the study has significant social implications, as it extends beyond the corporate realm to potentially impact societal welfare. When organizations adopt strategies informed by the findings of this study (i.e., establish reliable relationships with investors with characteristics that promote resilient capabilities within the firm, such as diversity and patience), they are better equipped to navigate and prevent crises, thereby reducing the negative consequences on employment and overall economic health. Therefore, by emphasizing the promotion of organizational practices that enhance resilience to crises, this study indirectly contributes to safeguarding jobs and maintaining economic stability within communities.

Although we consider the findings to be important for academia and practitioners, this study has certain limitations. Considering the inherent nature of this phenomenon, we conducted a cross-sectional study rather than longitudinal. Although this approach provides valuable insights, it limits our ability to definitively establish causality. In addition, the origin and nature of the crises experienced by the firms in our study remain unknown. Different types of crises (e.g., financial, natural disasters, and global pandemics) may exert distinct impacts on a firm’s internal decisions and actions. Consequently, investors’ contributions to averting a relapse may vary depending on specific crisis contexts. Exploring this issue is a valuable avenue for future research. Moreover, investigating how certain institutional conditions such as regulatory frameworks influence investors’ engagement in a firm’s crisis recovery and future avoidance strategies would be of significant interest. Finally, extending our results to consider how the characteristics of other stakeholders may also be a factor in organizational resilience during the crisis process represents a promising avenue for further research.

Conclusion

The establishment of organizational resilience constitutes a dynamic and intricate process that encompasses various critical factors. Drawing on the literature on resource dependence, we posit that specific investor characteristics may foster conditions conducive to averting future relapses in organizational crises. Our findings show that investor diversity and patience help prevent the probability of relapse following an organizational crisis. Conversely, an increase in the concentration of significant investors heightens the risk of relapse.

This study extends the literature on resource dependency theory and organizational resilience by illuminating the dependence on investors with specific characteristics to fortify organizational resilience and prevent relapses following organizational crises. In essence, our research underscores that investors’ contributions to an in-crisis firm significantly impact its potential to avoid future relapses. We contend that the influence of investor characteristics on executive decisions warrants heightened scrutiny; investors represent more than mere providers of financial resources but rather pivotal agents in shaping a firm’s capacity for resilience.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors thank the financial support from Grant PID2019-107767GA-I00 and Grant PID2022-138331NB-I00 funded by MICIU/AEI /10.13039/501100011033 and by ERDF/UE; Grant TED2021-129829B-I00 funded by MICIU/AEI/10.13039/501100011033 and by European Union NextGenerationEU/PRTR; and Grant C-SEJ-069-UGR23 funded by Consejería de Universidad, Investigación e Innovación and by ERDF Andalusia Program.