Abstract

Researchers have acknowledged that women leadership plays an important role in the success of organizations. However, the effects of women leadership on the financial performance of firms are mixed results. This article focuses on women ownership (i.e., critical mass and ownership percentage) as a form of leadership and family ownership as two boundary conditions that help us understand when small and medium enterprises (SMEs) benefit from women leadership. We argue that for women leadership to impact the financial performance of SMEs, women need to have a critical mass to influence outcomes and have power through ownership to influence decisions. We also argue that the effects of these relationships are affected by the context of ownership. These ideas are tested with a sample of 10,696 private SMEs from the country of Colombia. Results indicate that the women leadership enhances SME financial performance through both critical mass and a larger percentage of women ownership. However, family ownership negatively moderates the relationship between percentage of women ownership and SME financial performance. Implications of these results are discussed.

JEL CLASSIFICATION: D22; L25

Introduction

Women represent over 40% of the workforce around the world (The World Bank, 2023a); however, they lag behind men in advancing through the organization’s hierarchy and getting top leadership positions primarily within large firms (Catalyst, 2017). To understand why these discrepancies occur and what can be done to “even” the field, researchers have explored how women influence a firm through their actions as leaders (i.e., CEO, Top Management Teams, and Board Membership; Hoobler et al., 2018; Isidro & Sobral, 2015; Post & Byron, 2015) and through their role as entrepreneurs (De Bruin et al., 2006; Jennings & Brush, 2013). The underlying assumption of this work is that “if” research findings support a positive relationship between the presence of women leaders and a superior performance, then there is “hard” evidence for the value of diversity in leadership positions within a firm. This “hard” evidence, in turn, will help make a case for the importance of the presence of women in top level leadership positions (Noon, 2007).

Findings so far indicate that women leaders can play an important role in the success of a firm through the unique skills and perspectives that they bring to the strategic decision-making process (Carter et al., 2010; Kulich et al., 2011) and through the role they play in helping to develop a positive and inclusive climate within the organization (Dwyer et al., 2003; Singh et al., 2001; Torchia et al., 2011). Although having women leaders brings important benefits to organizations, findings linking women leaders to firm performance are mixed. Some findings indicate that organizations who appoint women leaders as CEOs or members of their board of directors perform better financially (Hoobler et al., 2018; Post & Byron, 2015; Terjesen et al., 2016). Other researchers indicate that although women may bring unique capabilities into a firm, these capabilities are not directly related (Dezsö & Ross, 2012; Jia & Zhang, 2013; Manner, 2010; Zhang et al., 2013) or are negatively related to the firm’s financial performance (Inmyxai & Takahashi, 2012; Pathan & Faff, 2013). These mixed results seem to point out that there are important boundary conditions that we need to explore to understand when the presence of women leaders is likely to result in better financial performance for a firm.

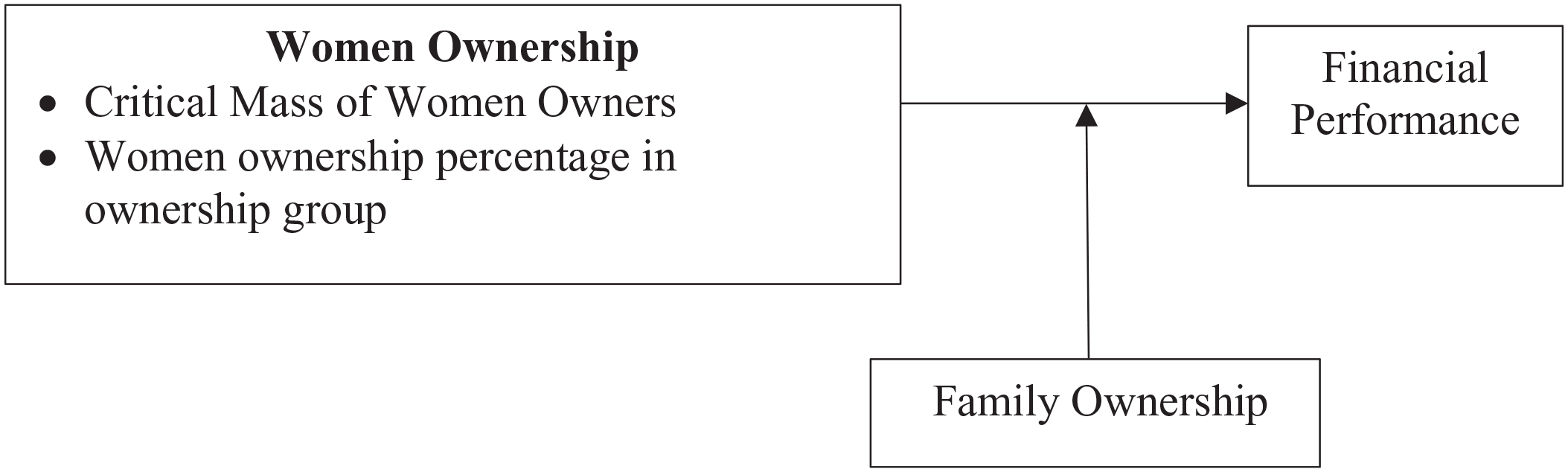

To address this gap, this article considers two of those boundary conditions: (1) the form of women leadership in the firm, and (2) the context in which this leadership occurs. Although women can become leaders in a firm through roles in management or through the board, we argue that women ownership can be another form of leadership that is likely to influence the financial performance of a firm. Ownership bestows individuals with the legal rights to possess, control, and decide over the possessed object (Pierce et al., 2001; Rousseau & Shperling, 2003). These rights give individuals the power to make decisions and have control over the implementation of decisions, which enables them to influence the performance of a firm. Thus, women ownership can be considered as a form of leadership within an organization. It is important to note that women ownership is not a new idea. Previous research has explored this concept under the umbrella of female entrepreneurship. This work focuses on women who start and/or run their own business and who are, for the most part, sole owners of their firm (Jennings & Brush, 2013). However, the focus on sole ownership is misguided given research findings that show women ownership is more likely to occur as part of a group of owners (Rosa et al., 1996; Rosa & Hamilton, 1994). In this sense, exploring women entrepreneurs in the absence of an ownership group provides only a partial picture. This article focuses on women ownership within the ownership group as a unique leadership form that can help us understand the conditions under which women leadership impacts performance.

Context plays an important role in the accuracy and interpretation of results of organizational research (see Bamberger, 2008; Johns, 2006; Rousseau & Fried, 2001). Previous meta-analytic work supports the importance of contextual factors in understanding the influence of women leadership on performance (Hoobler et al., 2018; Post & Byron, 2015). However, we know less regarding how context 1 plays a role in understanding the relationship between women owner and financial performance. This project considers two contextual factors that can play a role in understanding this relationship: (1) family ownership and (2) size of the firm. Entrepreneurial activity is often embedded within families (Aldrich & Cliff, 2003; Dyer, 2003). Family business systems influence the venture process through the resources, norms, attitudes, and values that they provide to family members (Aldrich & Cliff, 2003). Therefore, family members learn to be more accustomed to the presence of women in ownership and may be more likely to be receptive to their ideas and suggestions (Montemerlo et al., 2013) and create unique spaces for women leadership (Hernandez-Linares et al., 2023). Thus, we consider family ownership as an important moderator of the relationship between women leadership and financial performance. Firm size is the second contextual factor we consider. The focus of this study is small and medium enterprises (SMEs). SMEs are important players in the economies around the world (The World Bank, 2023b) and are a unique context to study women leadership (Hernandez-Linares et al., 2023; Kiefer et al., 2022). We argue that in the SME context, owners have a greater capacity to influence the firm with their actions.

Building on social identity theory (Tajfel & Turner, 1979), critical mass theory (Kanter, 1977), and literature on women empowerment (Kabeer, 1999), we argue that women ownership can influence the financial performance of SMEs under two conditions: (1) through critical mass, and (2) through power. Building on critical mass theory, Route 1 suggests that women ownership will influence the financial performance of a firm when there is a critical mass of women owners as part of the ownership group. Building on literature about women empowerment, Route 2 suggests that women ownership will enhance financial performance when women have more power to influence the decisions of the ownership group. To explore the role that context plays in these relationships, we argue that family ownership will act as a moderator of these relationships. Family firms represent a unique context that is more likely to create a gender supportive climate to enable women to use their unique competencies and perspectives to enhance the performance of the firm. Hypotheses are tested with a data set of 10,696 Colombian SMEs. Results show that the positive relationship between women leadership and financial performance in SMEs occurs both when ownership is measured as a critical mass or as a percentage of ownership. However, family ownership negatively moderates the relationship between percentage of women owners and SME financial performance.

Based on these findings, our study offers three important contributions. First, by considering women ownership as a form of leadership, we expand the different ways through which women can enact a leadership role within an organization. This perspective provides additional insights into the different ways that women can influence an organization and its performance (Hoobler et al., 2018; Post & Byron, 2015). Second, our results provide a boundary condition to understand when women ownership as a form of leadership affects SME financial performance. Greater ownership gives women greater power in decision-making, enabling them to incorporate the unique strengths that they bring into SMEs (Carter et al., 2010; Kiefer et al., 2022; Kulich et al., 2011), which then impacts performance. And third, research acknowledges that family ownership is a unique context to explore women leadership (Campopiano et al., 2017; Chadwick & Dawson, 2018; Eddleston & Sabil, 2019; Hernandez-Linares et al., 2023). Our results provide further insights into the importance of context in understanding the relationship between women leadership and performance. Findings show that family ownership negatively moderates the relationship between the percentage of women owners and SME financial performance.

Theoretical framework and hypotheses

The importance of women leadership

Since the introduction of the glass ceiling metaphor (Morrison et al., 1987), researchers have tried to understand and explain the value that women can bring to organizations through their participation in upper-level management (Burgess & Tharenou, 2002; Burke, 1997). In an attempt to show this value, researchers have focused on two broad aspects: (1) identifying the unique characteristics that women leaders contribute to the organization and its functioning, and (2) connecting the presence of women leaders with the financial performance of a firm. Research highlighting the unique characteristics of women leaders has found that female leaders create a diverse climate within top level management that encourages the inclusion of diverse alternatives during decision-making (Dezsö & Ross, 2012; Smith et al., 2006; Vieito, 2012). For example, the diversity that women bring into a board influences boardroom behavior through promoting better understanding of the marketplace, increasing creativity and innovation, improving problem solving, enhancing corporate leadership, promoting effective global relationships, and integrating a diverse workforce (Burgess & Tharenou, 2002; Cox & Blake, 1991; Robinson & Dechant, 1997). Women leaders possess characteristics such as benevolence, concern, lower power orientation, focus on community, and participative communication, which they bring to their leadership teams (Adams & Funk, 2012; Bear et al., 2010; Nielsen & Huse, 2010). These unique characteristics enrich discussions and help in decision-making processes (Dezsö & Ross, 2012), which can lead to better performance (Vieito, 2012; Wiersema & Bantel, 1992).

The important benefits that women bring into the management and leadership of a firm has led researchers to explore the relationship between women leadership and the financial performance (Hoobler et al., 2018). Financial performance is one of the measures of how leaders are doing within a firm. Thus, several studies have looked at the characteristics and composition of different leadership bodies in the firm (i.e., board of advisors, top management team, CEO position) and how this relates to firm performance (Dezsö & Ross, 2012; Smith et al., 2006; Vieito, 2012). This empirical evidence is mixed (Hoobler et al., 2018; Post & Byron, 2015). On one hand, some studies indicate that the presence of women leaders in boards generates higher returns of assets (Nguyen & Faff, 2007; Singh et al., 2001) and positive stock market reactions (Campbell & Minguez-Vera, 2010; Carter et al., 2003). Similarly, the presence of women in the CEO position is connected to better financial performance (Krishnan & Park, 2005; Wiersema & Bantel, 1992). In contrast, other findings show that the presence of females in top leadership (i.e., boards, CEO, and Top Management Team) is negatively associated with financial performance (Lückerath-Rovers, 2013; Mínguez-Vera & Martin, 2011; Pathan & Faff, 2013). Yet, other studies have found that the presence of women in the top leadership positions is unrelated to financial performance (Carter et al., 2010; Dezsö & Ross, 2012; Jia & Zhang, 2013; Manner, 2010). These mixed results suggest that there are boundary conditions that should be considered to understand this relationship (Abdullah & Ismail, 2016; Hoobler et al., 2018; Post & Byron, 2015). This article explores women ownership and family ownership as two boundaries that help us understand when does women in leadership enhance financial performance: (1) women ownership as a form of leadership, and (2) the context in which leadership occurs.

Women ownership as a form of leadership

Ownership is a characteristic that describes the legal rights that individuals have over an object (Etzioni, 1991). A legal owner of a business is an individual or group of individuals who have “the exclusive right to hold, use, benefit from, enjoy, convey, transfer, or dispose of an asset or property” (businessdictionary.com). Ownership is important because it gives individuals the legal right to influence decisions regarding the owned object (Pierce et al., 1991). Ownership can be psychological or formal. Psychological ownership describes a “state in which individuals feel as though the target of ownership (material or immaterial in nature) or a piece of it is theirs” (Pierce et al., 2001, p. 299). Formal ownership is recognized by society and carries with it the legal rights to influence decisions. Formal ownership is defined in relation to three fundamental legal rights: (1) the right to possess some share of the physical or financial value of the object, (2) the right to exercise influence/control over the object, and (3) the right for information about the status of what is owned (Pierce et al., 1991). Thus, when an individual has legal ownership over a firm, they have influence over its strategic decisions and the control necessary to implement those decisions. Our study focuses on the formal ownership that women have in a firm.

In this project, we advance women ownership as a form of leadership within a firm that enables females to have a voice in the strategic decision-making process and to control the implementation of strategic decisions within a firm. Ownership is different from participation in top management or board membership in that it can give women power and control during decision-making, implementation, and execution of the actions of the firm. Up to date, we have a limited understanding of women ownership. The reason for this is that historically the study of women owners has been conducted through research on women entrepreneurship. This line of research primarily explores women who start and/or run their own business and who are, for the most part, sole owners of their firm (Jennings & Brush, 2013), implying that women ownership primarily occurs through sole proprietorship. The problem with this approach is that women ownership is more likely to occur as part of a group of owners (Rosa et al., 1996; Rosa & Hamilton, 1994). Thus, a broader understanding of women ownership requires the exploration of women within an ownership group.

Social identity theory (Tajfel & Turner, 1979) suggests that an individual’s sense of self-concept is derived from membership in social groups. We learn to interact and understand others based on the groups that we are part of. Therefore, the characteristics in the composition of a team result in the development of unique norms that help members understand the expected behavior within a context. When females are part of the ownership group, the norms and expectations within the group will be different. Thus, member composition is likely to affect the norms and behaviors that develop within an ownership group.

The study of ownership groups within the entrepreneurship field suggests that group diversity is positively related to performance 2 (Dai et al., 2018; Jin et al., 2017). Findings indicate that both functional and educational diversity are important for the performance of a firm (Jin et al., 2017; Klotz et al., 2014; Vanaelst et al., 2006; West, 2007). Functional diversity describes the different types of knowledge and perspectives that members offer, while educational diversity represents the extent to which the members of a team contribute different assumptions, mental models, and specific domain knowledge. These types of diversity influence team processes that in turn affect the performance of the firm (Klotz et al., 2014). However, one aspect of diversity that has been largely overlooked is the gender composition of ownership teams (Dai et al., 2018). The limited understanding that we have indicates that within ownership teams, gender composition influences knowledge differentiation and integration, which enhance firm innovation and performance of entrepreneurial firms (Dai et al., 2018). In particular, having women as part of entrepreneurial teams enhances openness (Bird & Brush, 2002; Dai et al., 2018) and the availability of human and social resources to the team (Box & Larsson Segerlind, 2018; Tata & Prasad, 2008), creating dynamics that help in strategic decision-making processes. Given the importance that women can have for an ownership group, our study focuses on the presence of women within these groups and when this presence impacts financial performance.

Women ownership and financial performance

In this project, we argue that the presence of women within an ownership group can influence the financial performance in SMEs through two routes: (1) the critical mass route, and (2) the power route. The critical mass route is articulated based on principles from critical mass theory which suggests that in order for women’s unique competencies and perspectives to be recognized by an organization, women need to have a sufficient number of supporters (i.e., a critical mass) to bring about change (Kanter, 1977). When exploring boards, findings indicate that for women to influence the dynamics within a board, they need three or four other women to endorse their ideas (Jia & Zhang, 2013; Torchia et al., 2011). Having additional women in the board provides legitimacy to women’s contributions and creates an environment in which the unique resources and capabilities of women are likely to be considered, enhancing team decision-making. This in turn influences the performance of a firm. Building on these ideas, we suggest that women ownership will influence SME financial performance when women create a critical mass that enables them to change the dynamics in the group so they can use their unique competencies and share their unique perspectives. A critical mass of female owners can support each other, coordinating themselves as a cohesive group to create an environment in which other women feel comfortable participating and are more willing to listen to and act on these ideas. A critical mass of female owners will enable women to bring their unique competencies and perspectives into the decision-making and organizational control processes, positively influencing the financial performance of SMEs. Building on this rationale, we hypothesize that

H1: Having a critical mass of women ownership within an ownership group will be positively related to SME financial performance.

A second route through which women ownership can influence the financial performance of SMEs is through empowerment in decision-making. Kabeer (1999) defines empowerment as the ability to make a choice. This ability is achieved through interwoven conditions: resources (i.e., having the different material, social and human resources that enable individuals to have a choice), agency (i.e., the ability to determine goals and act upon them), and achievements (i.e., well-being outcomes) (Kabeer, 1999). Different to other types of power, ownership provides women with the control over resources in organizations (Bird & Brush, 2002) and mechanisms to exert power as the ownership team makes their decisions (Kabeer, 1999; Kantor, 2002). This type of empowerment is only possible when women have legal rights over what they own. In this sense, we see women ownership as a form of leadership that enables women to participate in the strategic decision-making process and to control the implementation of strategic decisions within a firm. Ownership also gives women power and control during decision-making, implementation, and execution of the strategic direction of the firm. Building on this logic, we argue that having legal ownership of a firm gives women the ability to make decisions for the firm, manage the resources that are associated with such decisions within the firm, and have control in the execution of these decisions. Thus, the percentage of women owners influences the financial performance of SMEs because it gives weight to the contributions and suggestions of women inside of the ownership team. This legal voice allows women to share their unique ideas and resources creating an environment that improves decision-making, which influences the performance of the firm. Following this rationale, we hypothesize that

H2: Having a higher percentage of women owners within an ownership group will be positively related to SME financial performance.

The importance context

Context plays an important role in understanding behavior within organizations (Johns, 2006; Rousseau & Fried, 2001). Contextual factors help researchers interpret results by sensitizing them to the situational and temporal boundaries of a phenomenon (Bamberger, 2008). Contextual factors are central to understanding the relationship between women leadership and performance given the legal and socio-cultural characteristics that may be at play in understanding the role that women have within a situation (Hoobler et al., 2018; Post & Byron, 2015). Not all companies are likely to be open-minded about women perspectives within the organization. In this project, we focus family ownership as a contextual boundary to understand the conditions under which women ownership can positively influence the financial performance of SMEs. Family firms are companies in which two or more family members (or family groups) own the majority of a company and have strategic control over its decisions (Chua et al., 1999). Previous work has suggested that families influence the resources, norms, attitudes, and values that they provide to family members, which in turn influences how the family engages in business (Aldrich & Cliff, 2003). Thus, family businesses create unique environments in which family members learn to be more accustomed to the presence of women in ownership and may be more likely to be receptive to their ideas and suggestions (Montemerlo et al., 2013). Building on this idea, we argue that being a family firm is likely to change the nature of the relationship between women ownership and firm performance.

Women play important roles within the family firm both in the family and in the business systems (Campopiano et al., 2017; Gupta & Levenburg, 2013; Hamilton, 2006). Women influence family firms through their roles as wives, mothers, and/or daughters (i.e., invisible roles; Gillis-Donovan & Moynihan-Bradt, 1990), or through roles in the business (i.e., accountant, manager, CEO, or Board member). Independent of the type of role they enact, women are believed to have an important positive influence on the family firm through their actions. In this sense, family firms provide a context in which women participation is more likely to occur and be accepted by other members. Because of this, family firms are more likely to be more welcoming of contributions from women owners and the incorporation of unique perspectives that can help enhance the performance of the firm.

In this project, we argue that family firms create a unique context for the active participation of female family members within the ownership of the firm (Cromie & O’Sullivan, 1999). Females who are active owners of a family firm have a strong commitment to the family and the business (Cappuyns, 2007; Poza & Messer, 2001). Their focus is on the continuity of the business (Poza & Messer, 2001). Because of this focus, family firms are more likely to create a gender supportive climate that enables women to use their unique competencies and perspectives to enhance the performance of the firm. Therefore, family ownership will moderate the relationship between women ownership and financial performance (see Figure 1). Given the characteristics of family businesses, we expect that women ownership will be more likely to influence performance because these firms are more likely to have climates that promote women participation in the firm (Campopiano et al., 2017). Building on this rationale, the following hypothesis is advanced:

H3: The relationship between women ownership (either through critical mass or through percentage of women owners) and financial performance in SMEs will be moderated by family ownership such that family ownership will strengthen the positive relationship between women ownership and financial performance.

Visual representation of project.

Method

Context and sample

Data for this project were collected in the country of Colombia. Colombia is located in the northern tip of South America and is the third largest country of the region by population (i.e., estimated as more than 48 million). Seventy percent of this population lives in urban areas, and there are close to 1 million companies in the country (30% are formal organizations listed within chambers of commerce, and 70% are informal in nature). Even though Colombia has been reducing the gender equality gaps, the country is still characterized by a male-dominated socio-economic environment (i.e., Gender Inequality Index for Colombia is .383, World Ranking = 90; UNDP, 2018), with limited adoption of gender equity. Currently, there are no laws or incentives that promote gender equality in the private sector, which results in a limited number of female appointments to high-level positions (Orozco & Baldrich, 2020). Colombia is a highly masculine society that is competitive and status-oriented (Masculinity score Hofstede = 64). Within the organizational context, Colombia is primarily patriarchal, giving men more legitimacy, decision-making power, and importance within the organization.

The data set for this study was constructed by combining information from two different sources. The financial information came from Superintendencia de Sociedades (2016), 3 which annually gathers and publishes financial information of private Colombian firms. Firm ownership information was gathered through BPR Benchmark (i.e., a financial database of companies in Colombia). Ownership information includes the complete names of firm owners and their proportion of shares (Casa Editorial El Tiempo, 2011). The sex of each owner was established through an exhaustive review of the owners’ names and their Colombian identification numbers. When the sex was impossible to determine, it was recoded as a missing value. Our data set is based on information from 2011 to 2016. 4

The sample focuses on SMEs and excludes micro enterprises and large publicly traded firms. SMEs were important to us because it provides an environment where owners are closely connected to the firm and have close control over what happens in their firms. The SME designation was determined based on Colombian law (i.e., Ley 905, 2004) which states that medium firms are those that have between 51 and 200 employees or with total assets that are equivalent to 30,000 minimum monthly salaries. Using the total assets classification, our final sample consisted of 10,969 private firms in 2011, and a variable number from 2012 to 2016. The information from 2012 to 2016 was used to test the robustness of the analysis.

Measures

The financial performance of each firm was assessed by examining return on assets (ROA). These data were calculated for the period 2011–2016. To avoid heteroscedasticity, this variable was log-transformed.

Critical mass approach to women ownership

We followed a similar procedure than Torchia and colleagues (2011) to measure the critical mass of women owners. In this process, we constructed five categories to identify the number of women owners: no women owners (23.13 %), one to two women owners (46.53%), three to four women owners or critical mass (23.74%), five to six women owners (5.04%), and more than seven women owners (1.56%). There was an average of 1.86 women owners per ownership (SD = 1.64), and 76.87% of the firms had women owners.

Ownership percentage approach to women ownership

Women ownership percentage was calculated as the sum of the proportion of shares held by women owners in the firm.

Family ownership was measured as a dummy variable with 1 for firms with at least 51% of firm ownership in the hands of a family and 0 otherwise. Under this rule, 56% of the firms were family owned and 44% were non-family firms. Given that ownership in family firms tends to be consistent over time (Gersick et al., 1997; Tsai et al., 2006), one of the authors cross-referenced owners’ first and second last names 5 to determine family relationships in each ownership team.

Control variables

Given the relevance that industry, firm size, firm age, and having a board can play within SMEs (Fernández et al., 2019), we controlled for these characteristics in our analysis. The industry for each company was determined using the International Standard Industrial Classification of All Economic Activities (ISIC). Six dummy variables were created to represent the following categories: agriculture or extraction (i.e., mining, 7.61%), manufacturing (28.31%), commerce (31.59%), service (31.24%), and transportation (.88%). Firm size was based on the annual income level. Firm age was calculated based on the year that the firm was originally registered by the Colombian Chamber of Commerce. Company ages ranged from 1 to 108 years (M = 19.18, SD = 12.94). The variables firm size and firm age were log-transformed to ensure homoscedasticity among the variables in the model. Finally, given the role that boards can have in reducing agency problems and the effects that agency problems can have on performance (Fama & Jensen, 1983), and the potential specific effects of female board members (Hoobler et al., 2018; Post & Byron, 2015), we also controlled for the number of female board members.

Results

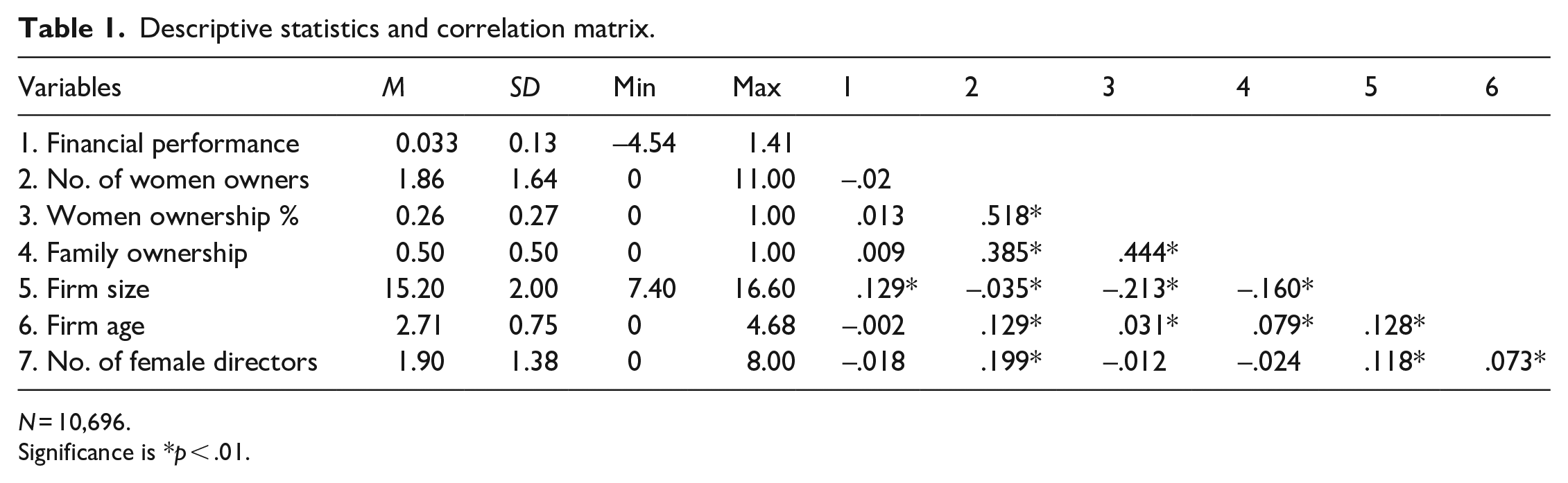

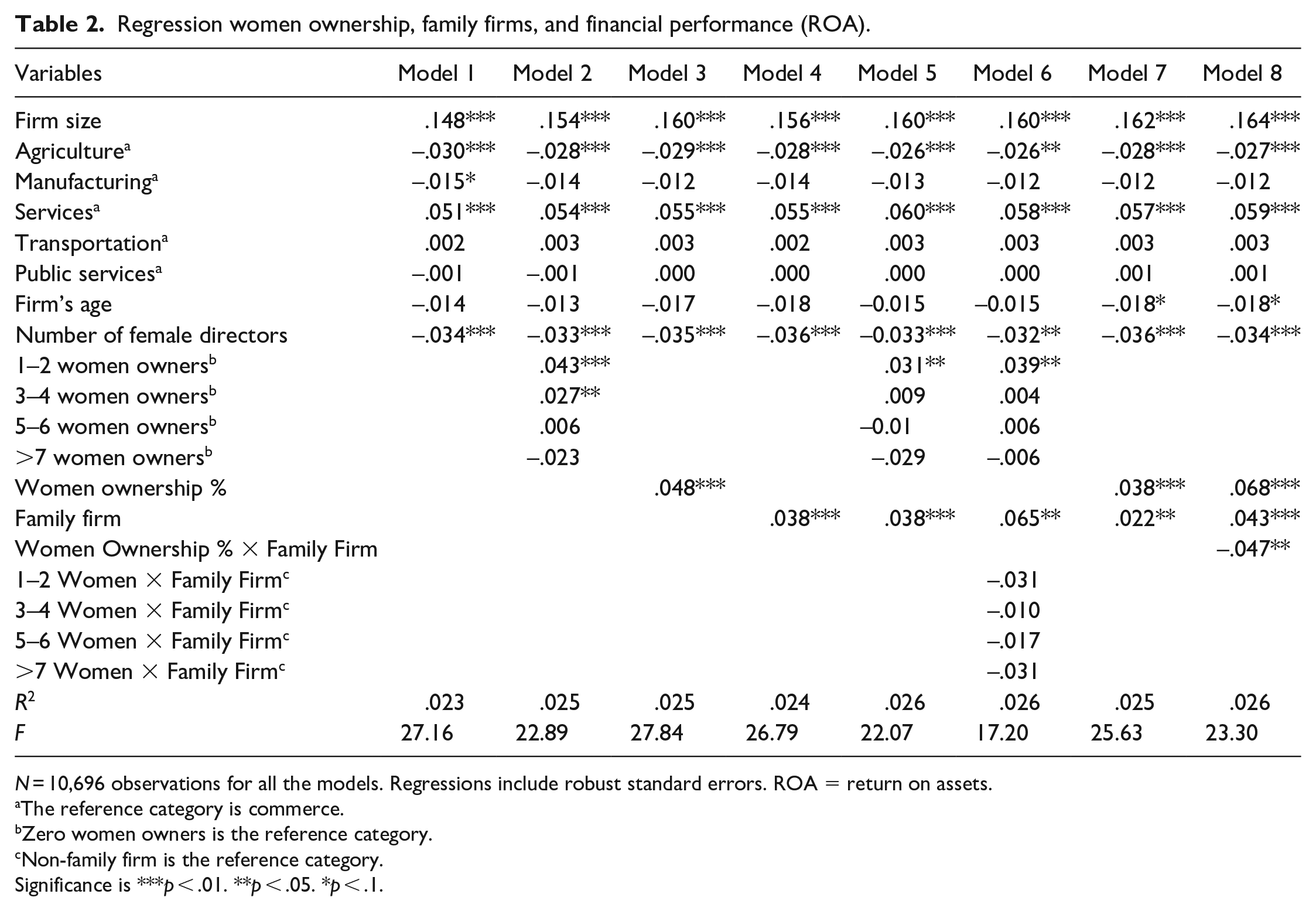

Table 1 provides the descriptive statistics and bivariate correlation for all the variables in the study. Our hypotheses were tested using multiple regression with ROA 2011 as dependent variable. In the analysis, controls were entered in Step 1, and the hypotheses were tested in Models 2 through 8. Hypothesis 1 suggested that having a critical mass of women owners in the ownership group would be positively related to SME financial performance. As can be seen in Table 2, Model 2, our data did support this hypothesis given the significant relationships between the Groups 1–2 and 3–4 of women owners and SME financial performance (β = .043, p < .01, and β = .027, p < .04 respectively). Together, these findings indicate that the critical mass of women owners required for women ownership to be positively related to the financial performance of SMEs is between one and four women owners.

Descriptive statistics and correlation matrix.

N = 10,696.

Significance is *p < .01.

Regression women ownership, family firms, and financial performance (ROA).

N = 10,696 observations for all the models. Regressions include robust standard errors. ROA = return on assets.

The reference category is commerce.

Zero women owners is the reference category.

Non-family firm is the reference category.

Significance is ***p < .01. **p < .05. *p < .1.

Hypothesis 2 suggested that having a higher percentage of women owners in the ownership group would be positively related to SME financial performance. As seen in Table 2, Model 3, results show a positive and significant relationship between the percentage of women owners and SME financial performance (β = .048, p < .1), supporting this hypothesis.

The moderating effect of family ownership on the relationship between women ownership and SME financial performance predicted in Hypothesis 3 was tested two different ways, one for critical mass and one for percentage of ownership. To assess whether critical mass would interact with family ownership, first the relationship between family ownership and performance was tested. As can be seen in Table 2, Model 4, family ownership is positively related to financial performance (β = .038, p < .01) and, as Model 5 shows, this relationship remains significant (β = .038, p < .01) when the categories of the number of women owners make part of the same model. However, this model reduces the magnitude and significance of one to two and three to four women owners. In the last step, we created and added to the previous model an interaction variable for women categories and family ownership. Table 2, Model 6 shows these results. In this model, despite that none of the categories of interaction is significant, their effect on the model increased the magnitude and significance of one to two women owners (β = .039, p < .05) and of family ownership (β = .065, p < .01).

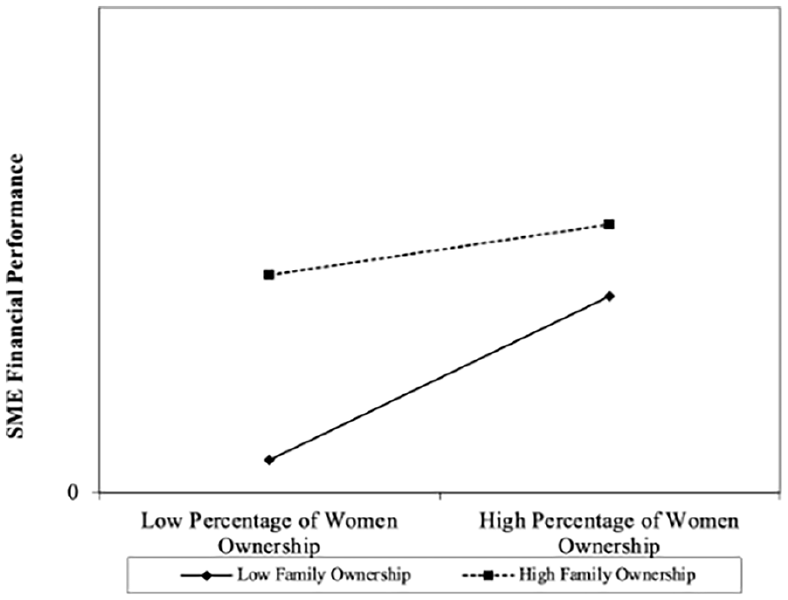

To evaluate whether family ownership moderated the relationship between the percentage of women owners and SME financial performance, we followed a similar procedure. As the relationship between family ownership and financial performance had been previously tested (Table 2, Model 4), the following step included women’s ownership and family ownership in the same model. Table 2, Model 7 shows these results, according to which both variables maintain their positive relationship with financial performance, percentage of women owners with β = .038 (p < .01) and family ownership with β = .022 (p < .05). In the last step, the interaction between the previous two variables was included. Thus, Table 2, Model 8 shows that this interaction is negative and significant (β = –.047, p < .05). This model shows that the inclusion of the interaction variable increases the magnitude and significance of the two variables without interaction (β = .068, p < .01, for percentage of women owners and β = .043, p < .01, for family ownership), suggesting that the relationship between the percentage of women owners and SME financial performance was stronger in the context of family firms. However, our results also show that within family firms having a higher percentage of women owners reduces SME financial performance. Figure 2 helps us interpret this relationship better by showing that the slope of the interaction suggests that the increase of family ownership diminishes the impact that the percentage of women ownership has on SME financial performance. In this model, the interaction of percentage of ownership held by women in the ownership team and family ownership explained 2.6% of the variance in the financial performance of SMEs. Taken together, our data do not provide support for Hypothesis 3.

Interaction between women ownership and family ownership.

Robustness checks

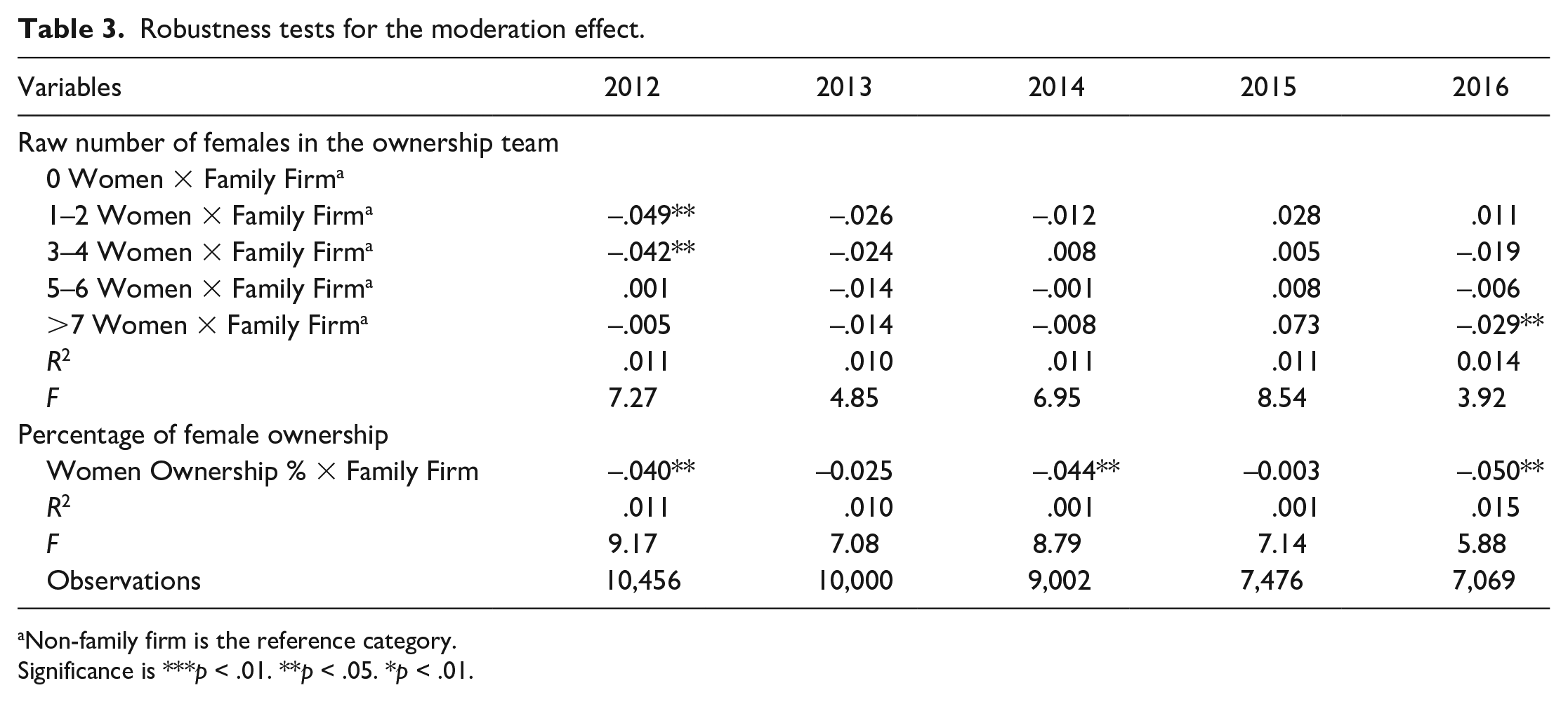

Given that the ownership structure of ownership teams tends to be consistent over long periods (see Gersick et al., 1997, and Tsai et al., 2006 for the case of ownership teams with family ties), we checked the robustness of the results by replicating the regression models for the interactions with ROA information for the period from 2012 to 2016. Table 3 shows that when exploring the critical mass route, the negative interaction terms between the critical mass groups of one to two and three to four women owners and family ownership were significant for 2012. Similarly, the interaction between the percentage of ownership held by women in the ownership group and family ownership was also almost consistent throughout the 5 years. Taken together, these results provide support for Hypotheses 3 and suggest that it is important to consider women ownership and family ownership as two important boundaries to understanding when women leadership enhances the financial performance of SMEs.

Robustness tests for the moderation effect.

Non-family firm is the reference category.

Significance is ***p < .01. **p < .05. *p < .01.

Discussion

The discussion about the importance of women leadership in organizations has been a relevant topic within organizational literature. As more women enter the workforce and face difficulties reaching higher positions in the organization, researchers have been interested in exploring the benefits that come with having diversity in leadership (Eagly & Chin, 2010; Morrison, 1996). The belief is that if we can understand the connection between women leadership and the performance of a firm, we have hard evidence for the benefits that women can bring when they are in critical roles within an organization. The problem is that previous research has provided mixed results regarding the impact that women leaders have on performance (see Hoobler et al., 2018, for a review). Mixed results can indicate the need to explore boundary conditions for the relationship between woman leadership and financial performance. This project explores two of those boundaries: the form of leadership (i.e., women ownership) and the context (i.e., SME focus & family ownership moderator).

Previous work has focused on women leadership as participation in top management teams (TMT), being a CEO or being a board director. We argue that ownership is a different form of leadership that plays a role in the performance of a firm. Ownership gives women the legal power and a voice in decision-making and strategic choices of the firm. The combination of these two factors enables women to bring their unique capabilities to affect what an organization does, and how it performs. The influence of women ownership on financial performance occurs through two routes. Route 1 is based on having a critical mass of women owners within the ownership group that provides legitimacy and support to the women’s point of view. Route 2 is based on the percentage of ownership held by women within the ownership group. Both approaches allow the ownership environment to be more diverse and consider more points of view when making decisions, which results in better financial performance. However, the relationship between women ownership and performance is also affected by contextual factors which can provide opportunities and constraints for this relationship. We conduct our work in the context of SMEs and consider family ownership as an important moderator of this relationship. Family ownership helps create a unique environment in which individuals become more receptive to ideas and suggestions that women provide (Montemerlo et al., 2013). This receptivity helps create organizations that are more attentive to the contributions of women owners and enable them to act in ways that can enhance the financial performance of the firm.

We test our ideas with a sample of 10,696 private SMEs from the country of Colombia. Our findings show that women ownership increases the financial performance of SMEs when women have a higher percentage of ownership within the group. Similarly, having a critical mass of women owners significantly influences the financial performance of SMEs. We also find that that context matters. Particularly, we found that family ownership does not moderate the relationship between critical mass and SME financial performance, while it negatively moderates the relationship between percentage of ownership and SME financial performance. These combined results provide two important insights for understanding the relationship between women leadership and financial performance. First, our results show that context is important to discern the relationship between women leadership and financial performance. In our case, the family business context provides a unique environment that affects the impact that the percentage of women owners can have on SME Financial Performance. Second, our results also show the importance that having a critical mass of women owners and having a higher percentage of women owners in an ownership team can have on SME financial performance. Our findings indicate that the higher the percentage of ownership that women have in a firm, the better these firms perform, independent of the context. Thus, it seems that legal rights enable women to bring diverse thoughts into the ownership team that helps performance. In addition, having a critical mass of one to four women owners in a team also helps enhance SME financial performance.

Research implications

These findings have important implications for research and theory in the areas of women leadership, ownership, and family business. Within the women leadership literature, our findings provide insights about the relationship between women leadership and performance by introducing ownership as a different form of leadership that needs to be considered. Even though previous research on women entrepreneurship has explored how women ownership affects the performance of a firm, most of this work has focused on women owners as sole proprietors (Jennings & Brush, 2013). Women ownership is different from being a member of the top management team, a CEO, or a board member because of the legal rights that individuals acquire when they become formal owners (Pierce et al., 1991). These legal rights give owners influence over strategic direction of a firm and the control necessary to implement decisions. When women are owners in a firm, they have the legal capacity to influence action which can enhance the way we understand how women lead in organizations. In this sense, our work contributes to research by presenting ownership as a unique form of women leadership, expanding the view of how women leadership is enacted.

A second aspect of women leadership research that this project helps to shed light on is the importance of women within the leadership team. Previous research about ownership teams highlights that women are more likely to be members of an ownership team than being sole proprietors of their firms (Rosa et al., 1996; Rosa & Hamilton, 1994). Researchers have also suggested that it is the combination of men and women owners that provides the best settings for women to leverage their unique capabilities to help the organization (Godwin et al., 2006). Results from our study support the importance of incorporating diversity in the leadership team to help the performance of the firm. Our results provide some support for the impact of having more women owners on the financial performance of the firm. Thus, we find that both having a critical mass and having power are important for women. However, we need future research that can continue to explore the type of gender mix necessary to enable the contributions of women to be considered within the strategic decision-making that can impact the financial performance of SMEs.

Another important contribution in the women leadership context is the important role that context plays in helping us understand how women leaders enact their role and the implications of women actions into the outcomes connected to leadership. Our study is embedded in multiple contexts: SMEs, Family Ownership, and the cultural context of Colombia. Our results show the opportunities and constraints that emerge when we consider these three contexts. In this study, we focus on SMEs as a space to explore women ownership. Their smaller size requires unique characteristics and behaviors of owners for their organizations to succeed (Brigham et al., 2007; Chuang et al., 2007). Our study enables us to focus on this unique context to better understand the role of women ownership. At a cultural level, the findings from our study provide insights into the role that ownership can play in cultures that are male-dominated. Previous research suggests that the culture of a country affects the cultural norms that develop within an environment. A cultural norm that is relevant when studying the impact of women leadership within a firm is gender equality (Hoobler et al., 2018). Research suggests that climates of gender equality or inequality are likely to play an important role in the level of participation and the type of behaviors that women engage in within an organization (King et al., 2010). The findings from our study suggest that ownership roles may be a way to counteract the gender norms within society. Given that our data were collected in Colombia which is characterized by lower gender equality (Cárdenas et al., 2014; Torrell, 2019), our findings provide some evidence that there may be certain leadership roles that can help counter the broader inequality climate within a culture. However, instead of being conclusive, these results motivate more research to deepen our understanding of the influence of women ownership on the performance of a firm. For example, future research could explore how the type of company studied plays a role in this relationship, or how different cultural norms could also influence leadership and how it can impact outcomes related to leadership. Our results indicate that context matters and should be an important component when exploring leadership. Thus, future research should incorporate this component in their exploration.

This project also provides interesting insights into the family business literature. Our results support the moderating role of family ownership on the relationship between women leadership and financial performance, however not in the way that we had hypothesized. In our study, women owners within family firms were less likely to enhance the financial performance of SMEs when they have a higher percentage of ownership. These findings complement the work of Hernandez-Linares and colleagues (2023) who find that family businesses provide a unique environment for women to flourish and enhance the entrepreneurial orientation of SMEs. In our case, women ownership within a family firm seems to affect the power that individuals have to implement their ideas. Several studies show that women can develop important ideas within family firms (see Gupta & Levenburg, 2013). However, women are likely to enact roles that are traditionally invisible, which makes it more difficult for their ideas to be heard and implemented (Campopiano et al., 2017; Gillis-Donovan & Moynihan-Bradt, 1990; Maseda et al., 2022). Our results suggest that within family firms the opinions of women may be less likely to be incorporated in decision-making even though they have some control and power over the process and the implementation of strategy. It may be that in family firms, being an owner may not be associated with having power to make things happen within the family group. In this sense, an important contribution of our article is that it also helps shed light into the role of women in family firms, by suggesting that within this context, having a greater percentage of ownership does not always translate into having greater formal and informal power within the family firm. Future research should continue to explore the conditions under which women ownership can impact the processes adopted by organizations, and the outcomes of the organizations.

This study explores a different perspective for measuring ownership. Previous research has relied on concentration of ownership as the most common measure to analyze the relationship between ownership and firm outcomes (Demsetz, 1986; Demsetz & Lehn, 1985). Our findings indicate that there are dynamics associated with two other ways of assessing ownership. The differences in results between the critical mass route and the percentage of ownership route show that there may be different aspects of ownership that need to be assessed to better understand the impact that ownership can have on SME financial performance. Thus, an important contribution of our work is the different ways that we explore ownership and how each approach sheds light into the effects that leadership can have on the financial performance of a firm. To enhance this understanding, future research should consider other ways to assess ownership. For example, including social characteristics of owners may help identify patterns of decisions and power that reflect ownership dynamics, and the consequences of these dynamics for what happens inside the organization. These new approaches can provide additional understanding of the effects of ownership on outcome variables.

At a theoretical level, our results help to better understand when women ownership can influence the financial performance of SMEs. At a general level, we find that both the percentage of women ownership and having a critical mass of women in the ownership group are positively related to SME financial performance. In this sense, our results are consistent with critical mass theory (Kanter, 1977). This is similar to other research looking at the relationship between having women board members and performance (Torchia et al., 2011). In our case, having between one and four women in the ownership group is the sweet spot for women ownership to impact the financial performance of a firm. However, future research would benefit from further exploration of what is the critical mass of women that can impact the different organizational processes and outcomes. Our results also provide insights into women empowerment. Results from our study show that the percentage of women ownership is an important predictor of the financial performance of SMEs. This indirectly suggests that empowering women through ownership can be beneficial for SME performance. Previous work suggests that ownership provides women with the control over resources (Bird & Brush, 2002) and mechanisms to exert power within the ownership team (Kabeer, 1999; Kantor, 2002). In this sense, ownership empowers women by giving them a powerful voice during decision-making. This enables them to bring their unique contributions and insights to strengthen the decision-making of the team. Future research would benefit from further exploration of the type of empowerment that is provided through ownership and what this empowerment does to improve the financial performance of SMEs.

Practical implications

An important practical implication from our findings is the important role that women ownership can play within a firm. Our results show that ownership provides women with an important form of influence within a firm, especially when they have a higher percentage of ownership and when they have a critical mass of one to four other women in the ownership team. In practice, these findings suggest that even though women may have informal power within a firm, having them be part of the ownership group is likely to strengthen the inclusion of the women’s unique point of view and to enhance their participation to enhance the success of the firm. Thus, when business owners want to leverage women’s contributions to a firm, they would benefit from including them as part of the ownership group, and make sure that there are multiple women in the ownership group. These two elements will help women leaders bring their unique capabilities to enhance the performance of a firm. However, our results indicate that within family firms, this may not be the case. Thus, at a practical level, our results also indicate that ownership may work differently in family firms, which needs to be considered when preparing women for ownership roles.

Limitations and future research

There are at least four important limitations for the interpretation of our results: first, the consideration of only one predictor for the financial performance of SMEs. Researchers indicate that SME financial performance is influenced by multiple factors (Fernández et al., 2019). Thus, the consideration of only one predictor does not reflect the complete picture of what matters for financial performance. Even though we tried to control for several factors that could play a role in the performance of the firms in our sample (e.g., firm size, firm age, industry, and having a board), we acknowledge that there are many other factors that can impact the financial results of an SME. Thus, we recommend that future research incorporate other factors that can also play a role in the financial performance of SMEs. Adding these other factors could also shed light on the weight that women leadership can have on financial performance in comparison with other factors.

A second important limitation of our work comes from the nature of our sample. Given that we relied on secondary data to test our ideas, there are at least three aspects that need to be considered when interpreting and generalizing our results. First, it is important to note that our sample is made of SMEs based on their level of assets (i.e., less than 8.5 million in revenue). Focusing on SMEs implies that our results may not generalize to firms with other characteristics. Further exploration is necessary to better understand the effects that women ownership may have in the performance of larger firms. A second limitation based on the nature of our sample comes from the cultural context. Even though we specifically chose the cultural context of Colombia to test our ideas, this one country approach is also a limitation to generalizing the findings. From our point of view, Colombia provided a great context because it represented a country where there is still a very traditional view of the role of women in society. This was important to be able to test whether women did play a role in performance. However, we also acknowledge that there may be unique characteristics of the Colombian context that could also affect our results. With this in mind, we believe that it would be very useful to test our ideas in different cultural contexts to better understand the role that culture can have when understanding how women influence the performance of a firm. A third limitation tied to the nature of our sample is having limited data to understand the linking mechanisms of women leadership and performance. Because we rely on archival data, we are not able to directly ask women owners the question of why they do what they do, or what they bring into an organization that helps the firm perform better. Thus, our data are not able to illustrate directly why women ownership helps organizations perform better. Similar to other authors (i.e., Carter et al., 2003; Dezsö & Ross, 2012; Smith et al., 2006; Vieito, 2012), we argue that women bring a unique set of skills and characteristics that change the dynamics in the groups and bring unique approaches and points of view to consider during the decision-making and implementation of ideas. However, we are unable to test this directly. To address this, future research could approach our question in a qualitative way to better understand how women owners affect the performance of the firm? What is it that they do? And, how and when do their actions result in a stronger performance. This can be done through in-depth case studies of women owners from organizations that have exceptional performance, or through in-depth interviews with female owners.

Another aspect that is important to highlight as a limitation is the presence of many other moderators that could affect this relationship. There may be other cultural- and organizational-level moderators to consider. For example, previous research has found that gender supportive climates play a role when exploring the effect of women participation on a board on the performance of a firm (Post & Byron, 2015). Thus, gender supportive climates can be one of the cultural context-level variables that may also act as a moderator in this relationship. Although we believe that family ownership is an important contextual factor that matters to understanding the relationship between women leadership and performance, we acknowledge that future research needs to explore other moderators. These moderators can be identified through qualitative approaches that can shed light into how and when women leadership impacts financial performance.

A final limitation is based on our narrow definition of performance. The focus of this study is financial performance which takes a narrow approach to performance that is inconsistent with more recent views of performance as having multiple components (i.e., triple bottom line; Elkington, 2004). Taking a broader view of performance may provide an interesting take on the relationship between women leadership and performance. For example, the effect of women leadership may be different based on the type of performance (i.e., people, planet, profit) the researcher is exploring. It may be that due to the way that women are socialized, these other forms of performance could have a stronger impact from having women owners. To explore this idea, future research should consider other forms of performance when assessing the effects of women leadership on performance. These new explorations can make a significant contribution to better understand what types of influences women have in a firm.

Conclusion

This project addressed two general research questions: (a) What is the relationship between women ownership and the financial performance of a firm? And (b) what are the boundary conditions that strengthen or weaken this relationship? Building on previous research on women leadership, and principles from social identity, critical mass theory, and women empowerment, we argued that women ownership has a positive effect on performance because it bestows women with legal power and control during the decision-making and implementation of the strategic choices of a firm. The presence of women within the ownership group creates different group dynamics that can be harnessed when women feel that they have the support from other minority members (i.e., a critical mass), and when they have higher ownership stakes in a firm. However, contextual factors such as family ownership need to be considered to understand the conditions under which women leadership is related to financial performance. We find that having a higher percentage of women owners enhances the financial performance of SMEs. However, the family firm context diminishes the impact of having women owners on financial performance. Particularly, we see that family ownership diminishes the effect that having a higher percentage of women owners can have on the financial performance of an SME. This study complements previous work about the effects of women leadership on performance of a firm, and the role that women can play in family firms. These insights are important to better understand the conditions under which women contribute to the future of organizations.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.