Abstract

Determining what factors influence firm performance constitutes an essential issue in both the management and the family firm research fields. This article, building on the resource-based view perspective, develops a mediation model that involves a unique intervening mechanism, namely, technological innovation efficiency (TI efficiency), with the potential to explain the inconsistencies found in prior work on the ways through which family involvement in management affects performance outcomes. Regression analyses utilizing a longitudinal sample of 1,118 Spanish private firms largely support the hypothesized mediating relationship, revealing that TI efficiency leads to richer firm performance in family firms with active family involvement in management. Overall, our findings help elucidate the black box of performance outcomes within family firms and make several contributions to theory and practice.

Keywords

Introduction

Investigating how family involvement in ownership and in management influences firm performance is gaining increasing momentum in management research (Dyer, 2018; Hansen & Block, 2020; Yeniaras et al., 2017). This overwhelming attention is not surprising given that family firms, defined as businesses “dominantly controlled by a family with the vision to potentially sustain family control across generations” (Zellweger, 2017, p. 22), represent ubiquitous and significant organizational forms worldwide 1 (La Porta et al., 1999). However, up to now, the incidence of family involvement, namely in management, as an unequaled resource on firm performance still remains unclear (e.g., Diéguez-Soto et al., 2019) with studies indicating positive (Gallucci et al., 2015; Sciascia et al., 2014), negative (Diéguez-Soto et al., 2019; Miralles-Marcelo et al., 2014), or even non-significant (Westhead & Howorth, 2006) associations between the two constructs.

According to the extant literature, a significant research gap persists in the family firm domain regarding how family firms with family involvement in management can boost their performance outcomes. As enhanced performance is regarded as one of the most critical determinants of family firms’ sustained value creation and long-term survival (Dyer, 2006), it is extremely important to more precisely understand the manners through which performance can be improved in this type of firms. This is consistent with recent calls to include an examination of the role of indirect strategic mechanisms in the family involvement-performance debate (Chrisman et al., 2012; Yeniaras et al., 2017), inasmuch as existing research on family influence (Chrisman et al., 2005) has largely neglected other intervening mechanisms equally or even more relevant than family involvement in management.

Therefore, building on the resource-based view (RBV; Habbershon & Williams, 1999), the aim of this study is to refine the family management–performance relationship by introducing an unexplored intervening mechanism, namely, technological innovation efficiency (henceforth TI efficiency), as the cornerstone to help explain how family involvement in management influences firm performance. TI efficiency, defined as a firm’s capability to maximize innovation outputs given a certain quantity of innovation inputs (Cruz-Cázares et al., 2013), is a reflection of family managers’ actions in orchestrating resources and in exploiting the bundle of family firms’ distinctive intangible assets (Carnes & Ireland, 2013; Muñoz-Bullón et al., 2020). The unique resources of family firms with an active family management promote sustained competitive advantages (Habbershon & Williams, 1999), which leads to increased TI efficiency and, in turn, to greater firm performance. Hence, we propose a mediation model to address the indirect effect of TI efficiency in the relationship between family involvement in management and firm performance. To test the suggested relationships, we apply random-effects regression analysis to a longitudinal sample of 1,118 Spanish private firms over the period 2010–2016.

Our article contributes to the literature in several ways. First, it extends the current family firm research on organizational outcomes (Dyer, 2018; Hansen & Block, 2020) by formally investigating TI efficiency as a mediating variable in the family management–firm performance relationship, thus adding clarification to the black box of performance outcomes within family firms (Pittino et al., 2019). Moreover, although very fresh research is investigating different associations between family involvement, technological innovation, and firm performance (e.g., Diéguez-Soto et al., 2019), most of it is centered on analyzing conditional (moderating) effects. However, to the best of our knowledge, this is the first article that introduces TI efficiency as a unique intervening mechanism through which performance outcomes could be enhanced in family firms with family involvement in management. In addition, the consideration and operationalization of TI efficiency constitute a contribution itself: On the one hand, prior studies have generally focused on the effect of either innovation inputs or outputs on firm performance (e.g., Diéguez-Soto et al., 2016), obviating that the key to improving firm performance is the efficiency with which technological innovation is undertaken (Cruz-Cázares et al., 2013). On the other hand, the way in which TI efficiency is measured, that is, the ratio of the number of product innovations to R&D expenditure, supposes a novelty compared with previous research that operationalizes it by examining innovation inputs and outputs in separate models (Matzler et al., 2015) or by regressing innovation inputs into innovation outputs (Manzaneque et al., 2020). Finally, this study also responds to the call for further investigation on the relationship between TI efficiency and firm performance within a family firm context (Martínez-Alonso et al., 2020).

The remainder of this article is structured as follows. The next section reviews relevant prior literature and advances our hypotheses. The third section describes the data and methodology. The fourth section reports the results, whereas the fifth section presents the discussion.

Theoretical background and hypotheses development

Family involvement in management and firm performance from an RBV perspective

The RBV has been a widely adopted theoretical framework when studying the performance of family firms (e.g., Hansen & Block, 2020; Hatak et al., 2016; Yeniaras et al., 2017). The essence of RBV is that firms differ in their resource endowments and that this resource heterogeneity matters and results in differential performance (Barney, 1991; Tokarczyk et al., 2007). More specifically, for a business to achieve and maintain competitive advantages that generate attractive organizational outcomes, these resources need to be valuable, rare, not easy to imitate, and non-substitutable (Barney, 1991).

Under this view, family firms are complex and dynamic entities, rich in distinctive, intangible resources (Habbershon et al., 2003), and the RBV has the potential to help identifying whether those resources may become family-based competitive advantages and lead to higher firm performance (Cabrera-Suárez et al., 2001; Habbershon & Williams, 1999). Among family firms’ resources, family involvement in the firm, which is conceived as the product of family relationships built over time, is the most valuable and difficult-to-imitate resource (Colbert, 2004; Hatch & Dyer, 2004), solely available to family firms (Shinnar et al., 2013). Family involvement represents a source of sustained competitive advantages because it is unique, inseparable, synergistic, and difficult to duplicate (Nordqvist, 2005). Habbershon and Williams (1999) pointed out that what really makes family firms unique is the involvement of family members in the business, especially when that involvement occurs from an early age, because it allows the generation of socially complex tacit knowledge that is difficult to codify and therefore cannot be easily imitated by others (Berman et al., 2002; Danes et al., 2009). Thus, family involvement can create familiness (Habbershon et al., 2003), that is, an idiosyncratic set of resources and capabilities arising from the interaction between the family and the firm life, which may yield sustained competitive advantages whether the family firm uses them appropriately.

Moreover, when analyzing the effect of family involvement on firm outcomes, it is common to distinguish between two family dimensions: family involvement in ownership and family involvement in management (Cabrera-Suárez & Martín-Santana, 2015; Sciascia & Mazzola, 2008). However, it has been argued that it is the family involvement in management, as opposed to mere ownership, which determines the firms’ outcomes (Gallucci et al., 2015; Martínez-Romero et al., 2020), as the former enables an active family participation in decision-making as well as in the monitoring and execution of businesses’ strategies and activities (Hambrick & Mason, 1984; Vandekerkhof et al., 2018), and therefore implies a greater direct incidence on firm settings, such as performance outcomes (Diéguez-Soto et al., 2019).

According to certain scholars (e.g., Sirmon & Hitt, 2003), family involvement in management may exert a negative effect on firm performance. In this respect, some negative attributes of human capital, such as parental altruism, managerial entrenchment, or the recruitment of family members on the basis of nepotism (Dyer, 2006; Gómez-Mejía et al., 2001), might cause family managers to utilize firms’ resources merely to fulfill family preferences (Bertrand & Schoar, 2006), thereby jeopardizing the firms’ financial outcomes.

Contrary to this negative view, several authors have found that family involvement in management develops family-specific capabilities, which subsequently have positive impact on firm performance (e.g., Allouche et al., 2008). In this vein, family managers possess a strong sense of commitment to the firm (Chrisman et al., 2012; Le Breton-Miller et al., 2011), inasmuch as they are well aware that the survival of the firm and the family harmony largely depend on their degree of effectiveness in managing the firm (Le Breton-Miller & Miller, 2013). In other words, family managers do their work with superior commitment because they perceive firm performance as an extension of their own well-being (Ward, 1988). Because of this, family members actively involved in management positions are expected to be more productive and more efficient than non-family managers (Habbershon & Williams, 1999; Matzler et al., 2015). Nevertheless, this high commitment of family managers may have a socially contagious effect and lead to an increase in the commitment and dedication of non-family employees to the family firm (Barsade, 2002; Zahra et al., 2008), which is critical to achieve greater performance outcomes (Hatak et al., 2016).

Family involvement in management also embeds the firm with other positive attributes of human capital such as unusual motivation, increased trust, cement loyalties, and an unique family language that enables all family firms’ members to communicate and exchange ideas, feedback, and expectations of each other in a more efficient and private way (Kellermanns & Eddleston, 2007; Tagiuri & Davis, 1996). Similarly, family managers may take advantage of these positive attributes to effectively communicate the history, values, and identity of the family firm to potential stakeholders (e.g., customers), thus leading to beneficial firm performance (Gallucci et al., 2015).

According to the reviewed literature built on the RBV, there is a prevailing positive effect of family involvement in management on firm performance. Hence, we propose the following hypothesis:

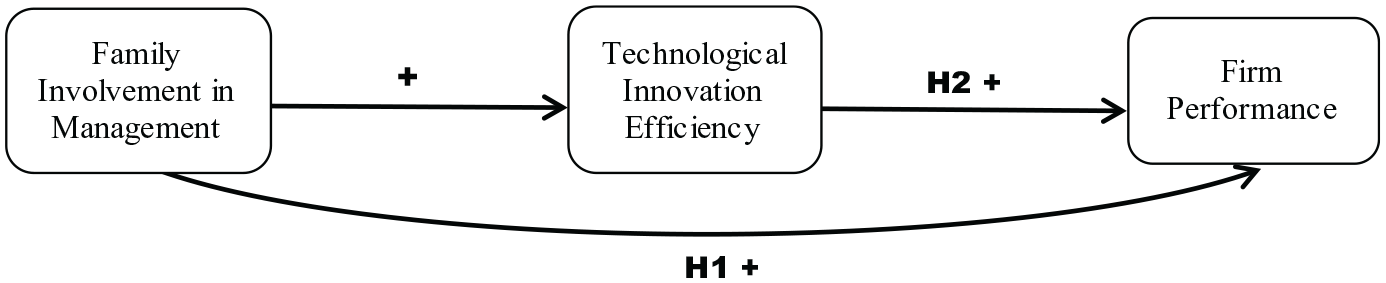

H1. There is a positive relationship between family involvement in management and firm performance

Family management and firm performance: the mediating role of technological innovation efficiency

Traditionally, family firms have been adverse to hiring external managers on the top management team in an attempt to retain family control (Le Breton-Miller et al., 2011; Vandekerkhof et al., 2015), and therefore may lack the appropriate human resources for developing innovation strategies (Sirmon & Hitt, 2003). In this sense, family managers have been found to be hostile toward innovation investments (Block, 2012; Migliori et al., 2020; Muñoz-Bullón & Sánchez-Bueno, 2011). However, despite their unwillingness to innovate, family managers’ ability to achieve innovation outcomes has been demonstrated to be higher than those of their non-family counterparts (Duran et al., 2016; Matzler et al., 2015). This innovation paradox (e.g., Chrisman et al., 2015) has prompted family firms’ scholars to analyze the conversion rate of innovation inputs into innovation outputs (Duran et al., 2016), that is, TI efficiency, and particularly its antecedents with the aim of unlocking family firms’ innovation potential (Rondi et al., 2019).

Drawing on RBV arguments, we propose that family involvement in management, as a key determinant of family firms’ ability to innovate (Chrisman et al., 2015; Diéguez-Soto et al., 2018), is a precondition for enhancing TI efficiency. In this regard, family members actively involved in top management teams, being the main decision-makers in family firms and representing the interface between the family and the firm (Vandekerkhof et al., 2015), constitute one of the most important manifestations of familiness (Ensley & Pearson, 2005; Minichilli et al., 2010). Although this familiness may be regarded as a possible source of disadvantages due to the lack of necessary internal resources to develop innovations (because of, among other reasons, family firms being reluctant to open the business doors to outsiders; König et al., 2013), this resource restriction could encourage family managers to pursue a more efficient or parsimonious (Carney, 2005; Muñoz-Bullón et al., 2020) transformation of innovation inputs into innovation outputs. Particularly, familiness has the potential to affect family firms’ innovate efforts (Carnes & Ireland, 2013), motivating more effective innovation behaviors (Hsu & Chang, 2011; Röd, 2016), and its effects are mainly observed in the orchestration of the firms’ resources by family managers (Sirmon et al., 2011).

In terms of human capital, as family managers have been involved in the business since their early infancy, they are endowed with a deep, largely tacit knowledge of their firms’ resources, routines, and stakeholders (Cabrera-Suárez et al., 2001; Von Krogh et al., 2000). Therefore, family managers are intimately familiar with how the firm’s internal processes and systems work (Sirmon & Hitt, 2003) and also encourage the exchange and dissemination of such knowledge throughout the firm (Patel & Fiet, 2011). Hence, the creation and accumulation of this valuable knowledge internally generated in the firm is essential to reap such advantageous human capital (Diéguez-Soto et al., 2016; Zahra et al., 2007) and will enable a more effective resource orchestration, and therefore a more efficient conversion of innovation inputs into innovation outputs. Another essential component of familiness, that is, social capital (Pearson et al., 2008), is typified by the desire to maintain the firm’s reputation in relation to interested outside parties (Dunn, 1996), as well as to cultivate and develop long-standing relationships with both the firm’s internal and external stakeholders (Berrone et al., 2012; Miller & Le Breton-Miller, 2005). Indeed, the establishment of quality, strong ties with firms’ potential stakeholders (e.g., suppliers) provides family managers with valuable technological resources and knowledge (Das & Teng, 2000; Feranita et al., 2017) that may foster higher efficiency in turning innovation inputs into innovation outputs. Besides, social capital facilitates the participation of family managers in open innovation projects (Bigliardi & Galati, 2018). These projects promote an exchange of ideas, experiences, and opportunities among network members (Miles et al., 2005; Zahra et al., 2007), which helps to reduce the mental rigidity of family managers and develop better cost-efficiency strategies (Diéguez-Soto et al., 2016; Uhlaner et al., 2013), leading to greater TI efficiency.

Accordingly, TI efficiency should have a direct association with improved firm performance. TI efficiency allows businesses to better leverage existing resources to get enhanced innovation outcomes (Guan & Chen, 2010). Moreover, TI efficiency helps businesses to become more competitive in today’s increasingly dynamic and complex resource-constrained environments (Duran et al., 2016). TI efficiency also promotes more fluid communications between firm members (Diéguez-Soto et al., 2018), the exchange of valuable ideas through different departments (Bammens et al., 2015), and consequently better decision-making quality (Vandekerkhof et al., 2018), to the extent that TI efficiency is usually accompanied by a greater commitment to the care and protection of firms’ resources. In other words, TI efficiency represents a powerful engine that can lead to richer performance outcomes (Cruz-Cázares et al., 2013). Then, family involvement in management is expected to have a decisive effect on the turning of innovation inputs into innovation outputs and thereby to influence the impact of TI efficiency regarding the achievement of firm performance (Martínez-Alonso et al., 2020). This suggests an indirect relationship in which TI efficiency mediates the relationship between family involvement in management and firm performance. We thus propose the following hypothesis:

H2. The relationship between family involvement in management and firm performance is mediated by TI efficiency

The theoretical model with the proposed relationships between family involvement in management, firm performance, and TI efficiency is summarized in Figure 1.

Theoretical model.

Research method

Sample and data sources

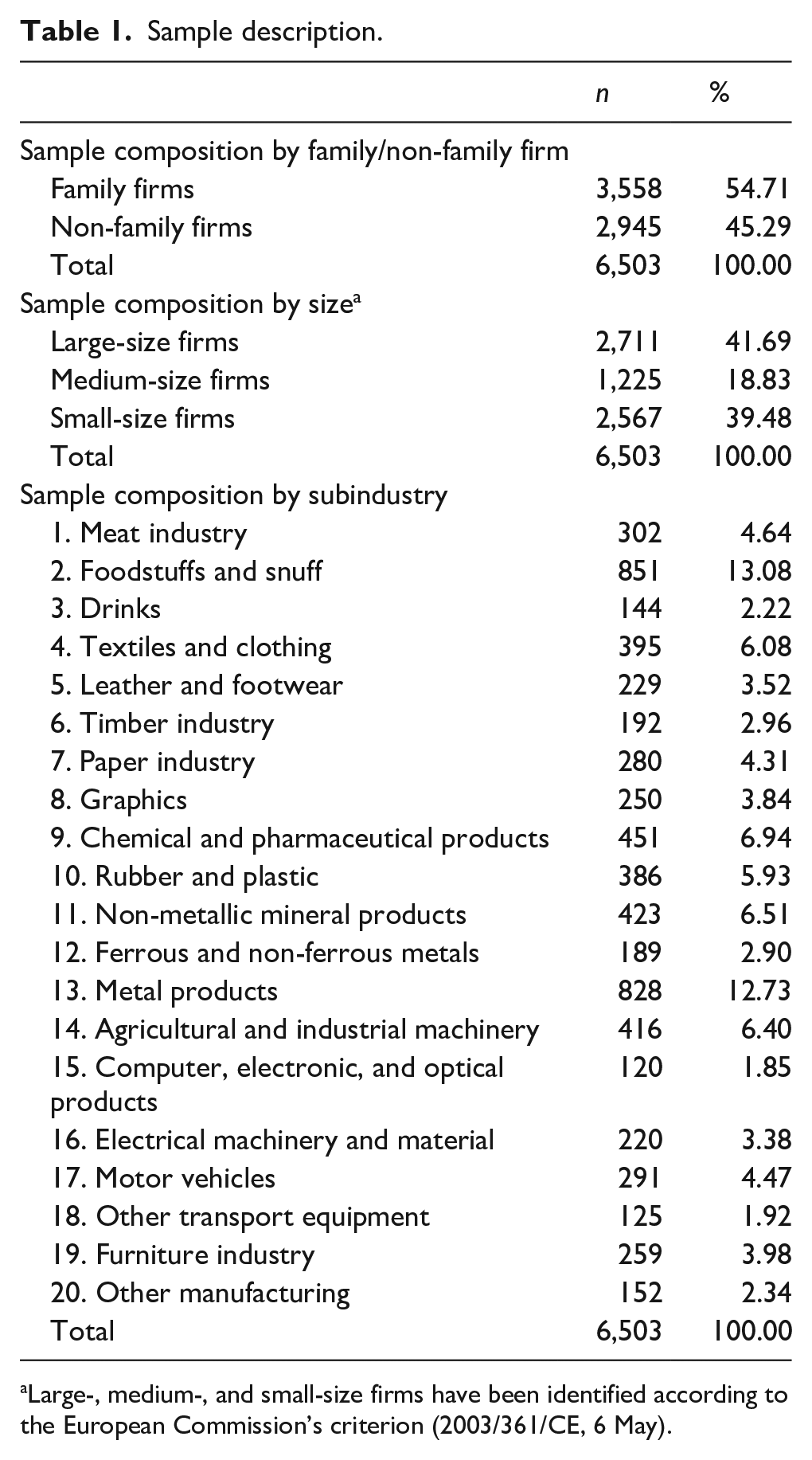

The hypothesized relationships are checked on a representative sample of Spanish private firms from the Survey on Business Strategies (ESEE). This is a yearly survey conducted by the State Partnership of Manufacturing Equity foundation on behalf of the Spanish Ministry of Industry and is composed of manufacturing firms. One of the most important ESEE’s characteristics is its sampling process that ensures the representativeness of the Spanish manufacturing industry. The data comprise the whole population of Spanish manufacturing businesses with 200 or more employees and include a stratified random sample of 5% of the population of firms with at least 10, but fewer than 200 employees. Following the arguments of Dorling and Simpson (1999), the compilation of data by a public organism guarantees the quality of the information and implies a high response rate, a high level of active involvement, and the representativeness of the population. Furthermore, the Spanish manufacturing industry is an ideal context for analyzing the mediating effect of TI efficiency on the family management–performance relationship for several reasons: first, manufacturing firms play a crucial role in the innovation investment made in Spain, accounting for 47.5% of total TI expenditure in relation to other industries (CEOE, 2018); second, around 4 of 10 Spanish firms developing TI belong to the manufacturing industry (CEOE, 2018); and third, manufacturing firms find in innovation the driving force to prevent the high degree of obsolescence they usually experience in their products to maintain and strengthen their market competitiveness (Kotlar et al., 2013). This database has been employed by numerous researchers to analyze innovation and related issues (e.g., Cruz-Cázares et al., 2013; Muñoz-Bullón et al., 2020; Nieto et al., 2015). The survey question about whether the firm is publicly listed enabled us to pinpoint private firms. In total, our sample consists of an unbalance panel of 6,503 firm-year observations covering 1,118 private firms, of which 612 are family firms and 506 are non-family firms, operating across 20 manufacturing subindustries between 2010 and 2016. Table 1 offers a more detailed view of the sample.

Sample description.

Large-, medium-, and small-size firms have been identified according to the European Commission’s criterion (2003/361/CE, 6 May).

Measures

Dependent variable

Firm performance

In this article, firm performance is assessed using gross margin, conceptualized as the difference between sales and the cost of goods sold scaled by sales (De Massis et al., 2018). Gross margin is considered an income statement measure with better predictive power than other accounting ratios (Fama & MacBeth, 1973; Martínez-Romero et al., 2019). Indeed, investors rely on gross margin because it also provides information regarding forecasting revenues and earnings persistence (Lento & Sayed, 2015). The use of gross margin for measuring firm performance is highly suitable for our study as it depicts the firms’ financial wealth and reflects managers’ influence on organizational outcomes. Moreover, gross margin provides certain advantages regarding other common accounting-based indicators (e.g., return on assets [ROA] or return on equity [ROE]) in that it only takes into account operating incomes and expenditures. That is, gross margin neither includes non-cash expenses, such as amortizations, nor taxes or interests derived from financial investments, which is advantageous for obtaining a more reliable performance measure in private firms (De Massis et al., 2018; George, 2005).

Independent variables

Technological innovation efficiency

An optimal measure of innovation efficiency should include both innovation output and innovation input (Cruz-Cázares et al., 2013; Guan & Chen, 2010). Thus, as a proxy of TI efficiency, we calculated the ratio of number of product innovations (innovation output) to R&D expenditure (innovation input) (e.g., Martínez-Alonso et al., 2020). According to this measurement, TI efficiency is enhanced when with the same amount of R&D expenditure more product innovations are produced or when less R&D expenditure is needed to produce the same amount of product innovations (Guan & Chen, 2010). The utilization of a ratio allows capturing the firms’ efficiency in turning innovation inputs into innovation outputs (Xie et al., 2020). The ESEE provides the total amount of money that each firm invests in R&D and the number of product innovations that each firm carries out.

Family involvement in management

The influence of family managers on decision-making is considered an objective measure of family impact on the firm (Cruz et al., 2010; Kotlar et al., 2014a; Muñoz-Bullón et al., 2020). This article utilizes the ESEE data to include both family ownership and family management as indicators of family influence on firms’ decision-making (Kotlar et al., 2014a; Manzaneque et al., 2020; Nieto et al., 2015). Accordingly, we define family involvement in management as the active participation of the controlling family in firm management for those firms that are family-owned (Diéguez-Soto et al., 2019). In this regard, for determining whether the firm is a family firm or not, we first utilized a question from the survey concerning whether the firm is controlled or not by a family. Then, for all those firms that are family-owned, we used another question from the survey that indicates the number of owners and their immediate relatives holding top managerial positions. In view of this argumentation, family involvement in management is measured as a continuous variable including the number of members of the owner-family involved in the top managerial team of the firm (Kotlar et al., 2013).

Control variables

Several control variables have been used to account for possible alternative explanations. Because management capabilities are built on experience and knowledge accumulated over the years (Ruiz-Jiménez & Fuentes-Fuentes, 2016), we controlled for firm age. Firm age is measured as the natural logarithm of the number of years between the business foundation and the observation year (Cabrera-Suárez & Martín-Santana, 2015). Due to larger organizations usually having greater innovation potential and more sophisticated planning and monitoring systems that may influence firm performance (Sciascia et al., 2014), we used firm size as a control variable, measured by the natural logarithm of total assets (Yeniaras et al., 2017). As firms with higher financial resources are more likely to achieve superior firm performance, we controlled for leverage, computed as the ratio of the firm’s debt to total assets (Matzler et al., 2015). Given that dependence on customers may compromise firm performance, we employed customer bargaining power as a control variable, calculated as the percentage of sales earned from the three major customers (Kotlar et al., 2014b). Moreover, as business sectors may have distinct degrees of propensity in relation to TI efficiency and firm performance, we controlled for industry effect (Manzaneque et al., 2020) by including 20 dummy variables representative of each subindustry (see Table 1 for a detailed description of each subindustry). Finally, to control for potential year effects, we included seven dummy variables for the different years covered in our article.

Estimation methodology

To examine the proposed hypotheses, we used a panel data methodology. This technique enables controlling for unobservable heterogeneity, which refers to the specific behavior and features of each sampled firm. Although a distinction between fixed-effects and random-effects is often required when using panel data, we utilized random-effects because the time-invariant nature of industry dummies precludes us from using fixed-effects (Diéguez-Soto & López-Delgado, 2019; González et al., 2013).

To check the relationships between family involvement in management, TI efficiency, and firm performance, we followed the framework of Baron and Kenny (1986). This framework supports mediation when four conditions are fulfilled: first, the dependent variable must be affected by the independent variable; second, the mediating variable must be affected by the independent variable; third, the dependent variable must be affected by the mediating variable, which is assessed by examining the concurrent influence of the independent and mediating variables on the dependent variable; and fourth, the impact on the dependent variable by the independent variable has to be less significant than under the first condition (partial mediation) or become non-significant (full mediation) when concurrently analyzing the influence of both the independent and mediating variables on the dependent variable (Baron and Kenny, 1986).

In the light of the abovementioned considerations, we applied different regression models to our data depending on the nature of the dependent variable utilized in each case. Thus, we performed random-effects generalized least squares (GLS) regression models to capture the effect of control variables, family involvement in management, and TI efficiency on firm performance in Models 1, 2, and 4. Subsequently, we run a random-effects Tobit regression model to test the effect of family involvement in management on TI efficiency in Model 3, as the latter variable is left-censored (TI efficiency does not contain negative values and presents numerous observations with values equal to 0). In this vein, scholars have demonstrated that Tobit models are the best approach when the dependent variable is censored (e.g., Greene, 2003), which can potentially avoid inconsistent parameter estimates and overcome any possible bias (Chen et al., 2013; Gao & Chou, 2015).

In addition, once the regression models were executed, we used the Sobel (1982) test to check the significance of the mediating effect. The Sobel test is highly appropriate for our purpose (Hayes, 2018), as the utilization of a large sample size entails the existence of computer limitations (Agarwal et al., 2016), and thus bootstrapping approaches are not applicable in our particular case (Hayes & Preacher, 2010; Imai et al., 2010). Finally, to confirm the mediating results, we estimated confidence intervals by employing a Monte Carlo Method (Selig & Preacher, 2008).

Results

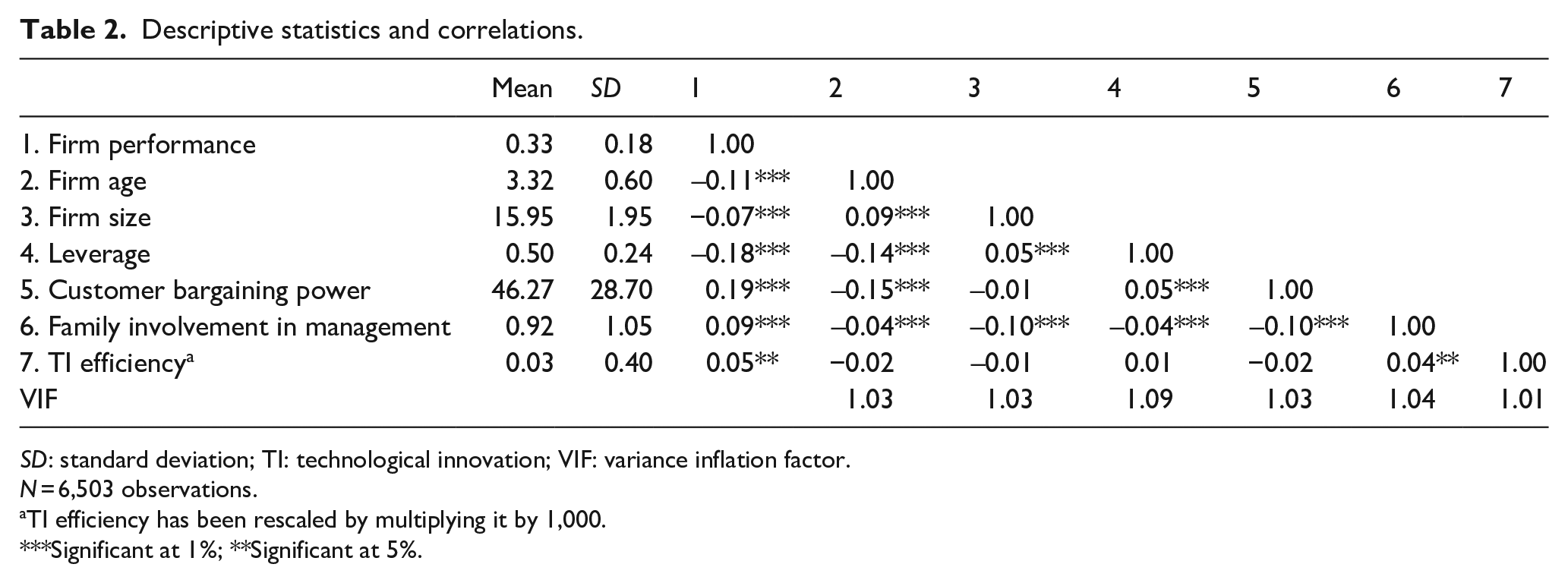

Table 2 reports some descriptive statistics (i.e., mean and standard deviation) and correlations of the variables. Correlation coefficients were relatively low and consistent with our expectations. Similarly, the individual values of the variance inflation factor did not exceed 1.09, being significantly lower than the critical value of 10, proposed as a warning level in prior studies (Neter et al., 1989). Thereby, multicollinearity among independent variables is not a concern in our study.

Descriptive statistics and correlations.

SD: standard deviation; TI: technological innovation; VIF: variance inflation factor.

N = 6,503 observations.

TI efficiency has been rescaled by multiplying it by 1,000.

Significant at 1%; **Significant at 5%.

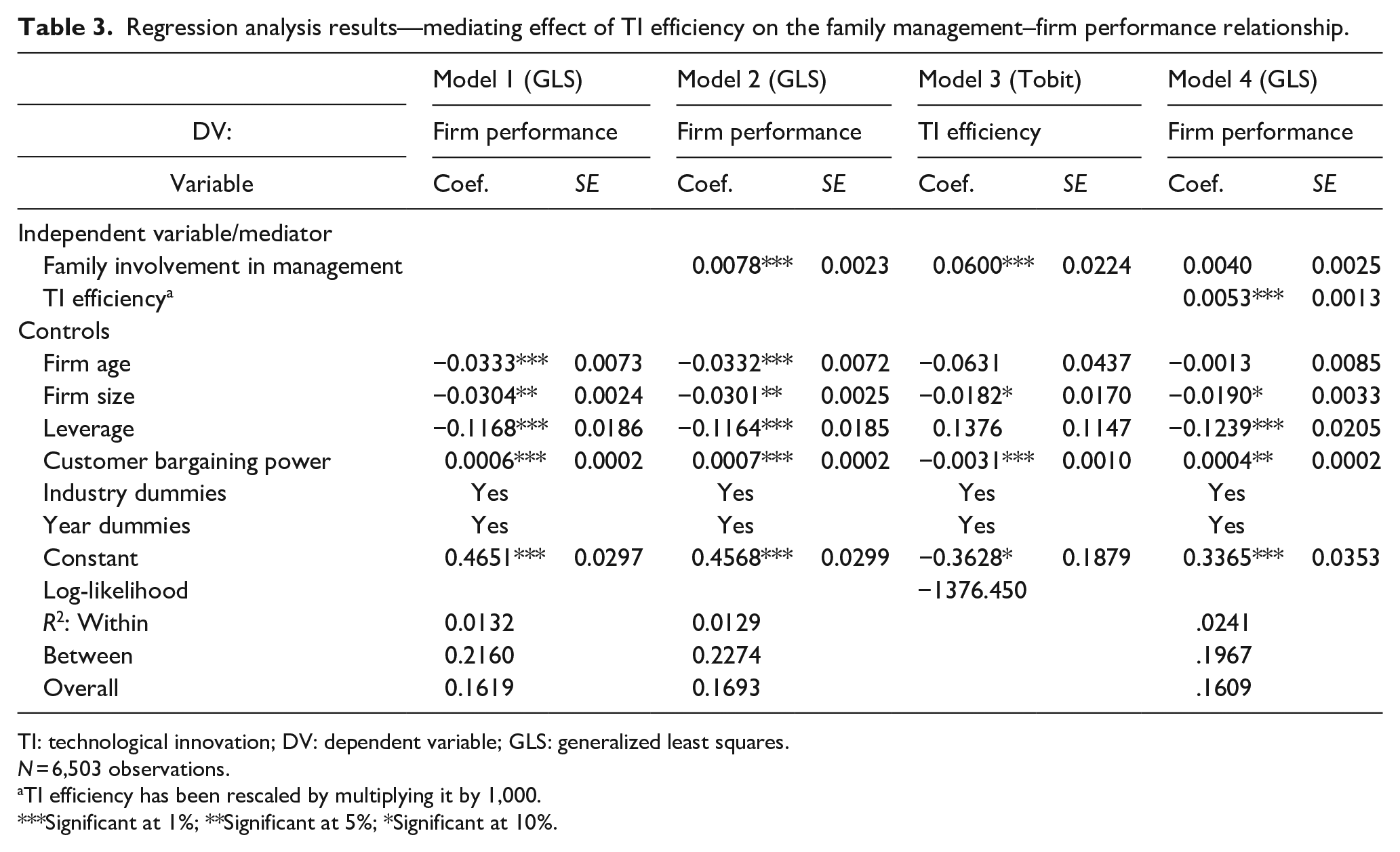

Table 3 presents, by stage, the results of the random-effects regression models. We begin the regression analysis by introducing only control variables (Model 1). Model 2 shows a beneficial impact of family involvement in management on firm performance (β = 0.0078; p < .01). This strong positive relationship between family involvement in management and firm performance is coherent with previous literature (e.g., Gallucci et al., 2015), and therefore H1 is supported. In Model 3, we demonstrate the relationship between family involvement in management and TI efficiency. The positive and significant coefficient of family involvement in management (β = 0.060; p < .01) indicates that as the number of family members actively involved in management increases, the obtained TI efficiency is higher. Model 4 presents the mediation results. Both TI efficiency and family involvement in management are simultaneously introduced in this model. Whereas the impact of TI efficiency on firm performance is strongly positive and significant (β = 0.0053; p < .01), family involvement in management becomes non-significant compared with Model 2 (β = 0.004; n.s.). Hence, the results in Table 3 (Models 1–4) indicate that TI efficiency fully mediates the relationship between family involvement in management and firm performance (Baron & Kenny, 1986), and thus H2 is supported. Moreover, the results also comply with the required conditions for mediation established by Baron and Kenny (1986): in Table 3, Model 2 represents the first condition; Model 3 responds to the second condition; and Model 4 enables the analysis of both the third and fourth conditions.

Regression analysis results—mediating effect of TI efficiency on the family management–firm performance relationship.

TI: technological innovation; DV: dependent variable; GLS: generalized least squares.

N = 6,503 observations.

TI efficiency has been rescaled by multiplying it by 1,000.

Significant at 1%; **Significant at 5%; *Significant at 10%.

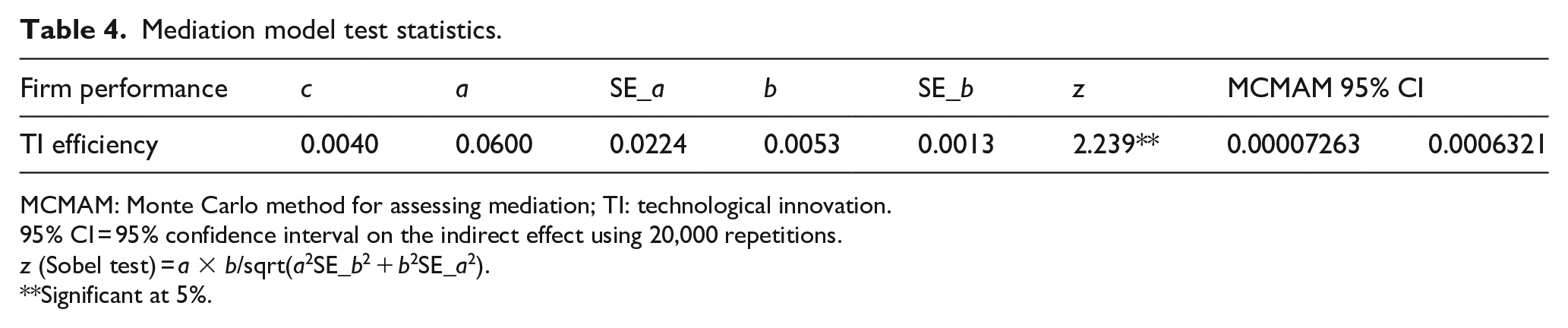

Then, Table 4 reports the results of the Sobel (1982) test and Monte Carlo confidence intervals (Selig & Preacher, 2008). The z-column includes the statistic of the Sobel test with its significance. The last columns of the table show the bottom and top limits of a 95% confidence interval representative of the indirect effect utilizing a Monte Carlo method with 20,000 repetitions. The Sobel test indicates that the mediating effect of TI efficiency is significant (z = 2.239, p < .05). The Monte Carlo Method also shows the significance of the mediating effect, as the 95% confidence interval does not include the value zero.

Mediation model test statistics.

MCMAM: Monte Carlo method for assessing mediation; TI: technological innovation.

95% CI = 95% confidence interval on the indirect effect using 20,000 repetitions.

z (Sobel test) = a × b/sqrt(a2SE_b2 + b2SE_a2).

Significant at 5%.

Robustness checks

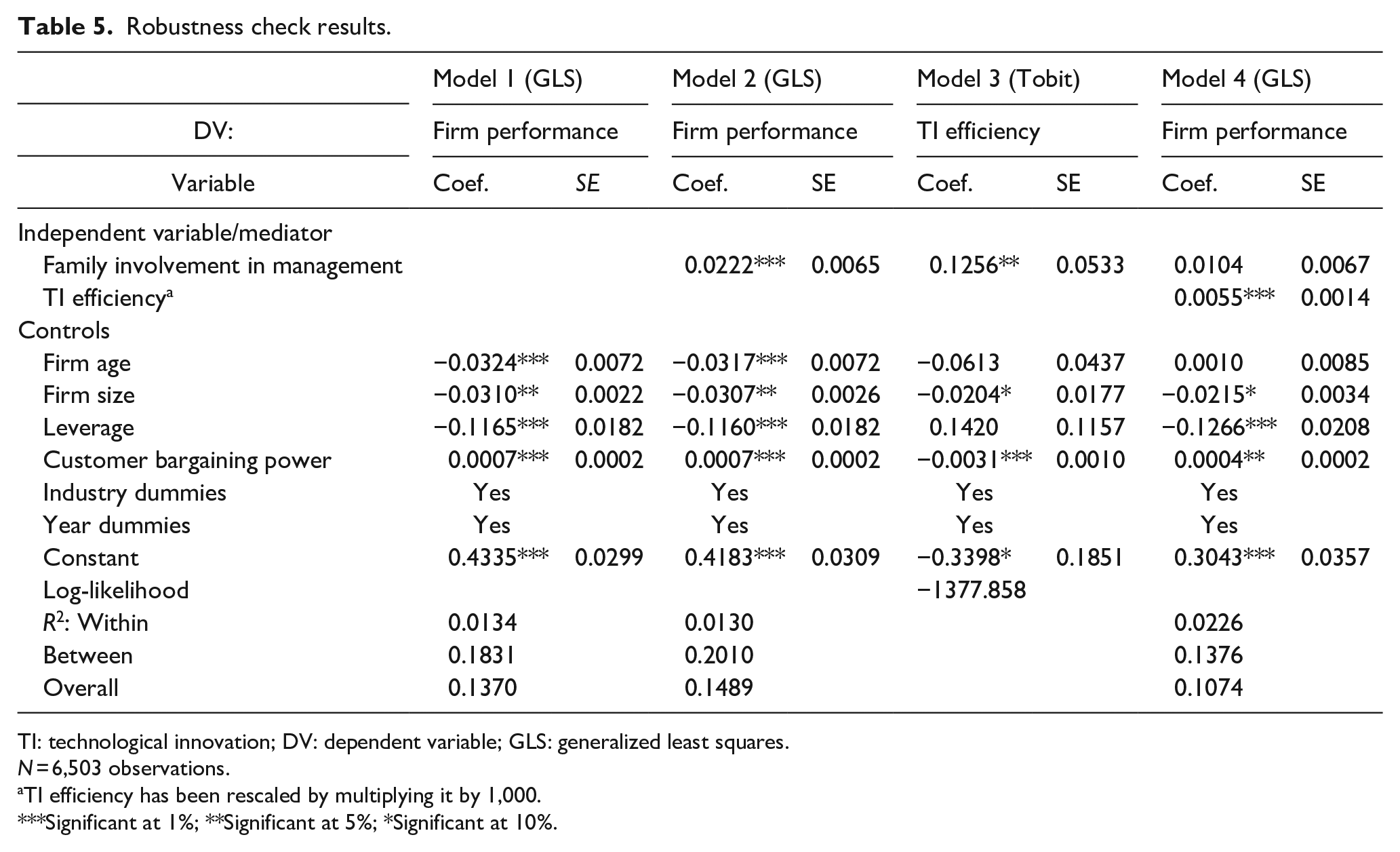

To give robustness to our results, we developed additional checks. First, we used a simplified representation of our independent variable by building a categorical variable operationalized as 1 when one or more members of the owner-family hold posts in the top managerial team of the firm and 0 otherwise (Cruz & Nordqvist, 2012; Sirmon et al., 2008). The results (Table 5) were very similar to those obtained in the main analysis. Second, we conducted a sensitivity analysis by utilizing an alternative firm performance measure, that is, ROA. The results were also similar but slightly less significant than those obtained for gross margin. Concretely, H1 was supported with the same level of significance, but H2 was somewhat less significant. Furthermore, we re-estimated the Sobel test and the confidence intervals of Monte Carlo method for both robustness checks, either with the categorical variable of family management or with ROA. The results were comparable to those presented in Table 4, but again slightly less significant when using ROA as the dependent variable. The results of these latest robustness checks can be obtained from the authors.

Robustness check results.

TI: technological innovation; DV: dependent variable; GLS: generalized least squares.

N = 6,503 observations.

TI efficiency has been rescaled by multiplying it by 1,000.

Significant at 1%; **Significant at 5%; *Significant at 10%.

Discussion and conclusion

Theoretical implications

The primary purpose of this study was to analyze whether family involvement in management influences firm performance directly and indirectly through TI efficiency. We argue and empirically confirm that as family involvement in management increases, the obtained performance outcomes are richer, which is partly explained by the family managers’ distinctive ability to achieve greater efficiency in turning innovation inputs into innovation outputs.

Our findings yield several important implications to previous literature. We fill a gap in existing knowledge regarding how family involvement influences firm performance (e.g., Dyer, 2018; Hansen & Block, 2020) by developing a novel mediation model to better understand the intervening mechanisms through which family involvement in management affects performance outcomes. In doing so, we apply RBV theory, which offers an appropriate means for analyzing how the distinctive set of intangible resources of family firms (familiness) results in sustained competitive advantages, which leads to enhanced TI efficiency and, in turn, to improved firm performance (Cabrera-Suárez et al., 2001; Habbershon & Williams, 1999). The consideration of TI efficiency as a unique intervening mechanism in the relationship between family involvement in management and firm performance is of utmost importance given that knowing how to improve performance levels is crucial for family firms, as enhanced performance favors value creation (Martínez-Romero et al., 2019) and ensures the long-term survival of this type of firms (Dyer, 2006). Moreover, the inclusion of TI efficiency as a mediating variable allows refining our comprehension concerning the existing inconclusive findings on the family management–firm performance relationship (e.g., Diéguez-Soto et al., 2019; Gallucci et al., 2015), contributing to opening up the black box of performance outcomes within family firms (Pittino et al., 2019). Indeed, to the best of the authors’ knowledge, this work is pioneering in identifying family involvement in management as a critical resource to unlock family firms’ potential to innovate efficiently and in examining how TI efficiency impacts the performance behavior of such firms. This is particularly noteworthy because while existing research analyzing distinct linkages among family involvement, technological innovation, and firm performance mainly focuses on conditional (moderating) effects (e.g., Diéguez-Soto et al., 2016; Garcés-Galdeano et al., 2016; Kotlar et al., 2013), research examining mediating effects on the abovementioned relationships is practically non-existent (Calabrò et al., 2019). Furthermore, this article uses a fresh approach in the calculus of TI efficiency, and thus, its incorporation into our model represents a relevant contribution for the following reasons. First, using the number of product innovations as innovation output is more appropriate than using the number of patents or patent citations (Block et al., 2013; Liu et al., 2017; Lodh et al., 2014) because patents can underestimate the firms’ ability to innovative, inasmuch as many businesses do not usually apply for patents due to, among other motives, their inability to cope with the expense and long time involved in the patenting process (Kalantaridis & Pheby, 1999). Second, by using the ratio of number of product innovations to R&D expenditure, we surpass both, a research stream that measures TI efficiency by considering innovation inputs and innovation outputs in distinct models (e.g., Matzler et al., 2015) and a research stream that assesses such efficiency as the effect of innovation inputs on innovation outputs by means of regression models (e.g., Manzaneque et al., 2020).

This study also offers new insights into the debate on the antecedents of TI efficiency in family firms (Duran et al., 2016). We show that family involvement in management is an important precondition that enables family firms to fully exploit their familiness, which is beneficial for the development of the ability to efficiently transform innovation inputs into innovation outputs. Through this, we go beyond previous literature (Duran et al., 2016; Lodh et al., 2014) by revealing that nurturing such distinctive ability for achieving greater TI efficiency requires not only the presence of a family CEO within the top management team but also the active involvement of other family members.

Moreover, this article responds to the call for more investigation on the impact of TI efficiency on firm performance in family firms (Martínez-Alonso et al., 2020). Whereas most studies have primarily focused on merely linking different innovation forms to performance outcomes (e.g., Craig et al., 2014; Diéguez-Soto et al., 2016; Spriggs et al., 2013), we build upon the notion of Cruz-Cázares et al. (2013) considering that the efficiency with which technological innovation is undertaken is the key to increasing firm performance, and we translate this insight to the family firm domain. Thereby, we expand on the innovation–performance relationship by providing empirical evidence that whether family firms want to become competitive and, thus, improve their performance outcomes, besides developing and combining different R&D strategies (Diéguez-Soto et al., 2019; Muñoz-Bullón et al., 2020), they must also be very efficient in turning innovation inputs into innovation outputs.

In addition, this work has certain implications for research on family business heterogeneity (Chua et al., 2012). Prior studies have confirmed that both family involvement in ownership and family involvement in management are primary sources of family firm heterogeneity, as they can differently influence family goals, resources, and behaviors (Daspit et al., 2018; Melin & Nordqvist, 2007). We extend these arguments by suggesting that those family firms with a greater number of family members actively involved in the firm management are able to obtain superior firm performance. This consideration is very valuable to the extent that it overcomes the limitations of previous studies, which have not taken into account such family firm heterogeneity and have identified the family influence by using dichotomous variables that leave out many characteristics of the family essence (Kotlar et al., 2014b; Sirmon et al., 2008).

Practical implications

Our article offers some practical implications, which provide knowledge that is extensively applicable by both managers and practitioners. First, in the light of the obtained findings, it seems more than evident that family firms with family involvement in management should emphasize their unique bundle of resources (e.g., Habbershon & Williams, 1999) to enhance their performance outcomes. Therefore, family-managed firms should implement efficient organizational routines and normative frameworks involving all firm members, such as teamwork (Cohen & Bailey, 1997), information sharing across functions and firms’ departments (Zahra et al., 2004), and coordination and collaboration programs (Gunday et al., 2011). In this regard, family managers should provide incentives and mindsets that facilitate firm members to assimilate and transform tacit knowledge into explicit knowledge (Un & Asakawa, 2015), to be spread along the whole organization. Similarly, family managers should ensure the commitment of all firm members (Cassia et al., 2012), both family and non-family, toward the business outcomes, through, for example, the care of their firm members’ satisfaction and motivation and the equal treatment to all firm members regardless of whether they belong to the business family or not.

On the other hand, our findings reveal how performance outcomes can be accentuated through the achievement of higher TI efficiency in family firms with family members in their top management teams. Thereby, to enhance firm performance through TI efficiency, family managers have to encourage the development of an innovative culture and mentality within the business to fully promote the generation of new ideas and exploit the innovation potential (Matzler et al., 2015). Furthermore, family managers should not be forced to invest heavily in R&D; instead, they should make the most of their limited innovation resources because it does not matter how much they invest, but what they get from such investments (Cruz-Cázares et al., 2013). In other words, innovation outcomes are achievable without the requirement of large innovative investments (Fuetsch & Suess-Reyes, 2017). In addition, the development of greater interactions between family managers and strategic planning processes may also improve family managers’ innovative ability by enriching their understanding for their strategies, goals, and behavior (Hsu & Chang, 2011), which, in turn, would benefit the increase in firm performance (Fuetsch & Suess-Reyes, 2017). Moreover, in those cases in which family managers do not have the likelihood to promote their innovative ability in the short run, they should center on strategic planning in an attempt to ameliorate their firms’ competitiveness (Eddleston et al., 2008).

Finally, policymakers and public authorities can also contribute to the improvement of family-managed firms’ outcomes through the promotion of specific initiatives and innovation plans that boost TI efficiency, inasmuch as these policies entails positive externalities for society (Antolín-López et al., 2015). Specific efforts may include, but not limited to, initiatives such as fiscal incentives for innovation investments and subsidies for acquiring innovative infrastructures, which allows to obtain higher innovation outputs given a certain amount of innovation inputs (Matzler et al., 2015) in order to sustain a virtuous circle of innovation that enhances firms’ innovation success (Greco et al., 2017). Besides, policymakers should give support to family-managed firms for obtaining information regarding market needs and trends, to guide them in the innovation strategic planning.

Limitations and future research avenues

This study is not without limitations. Nevertheless, these limitations bring with them new opportunities to initiate future research. First, although this article only focuses on the Spanish manufacturing industry, which is particularly well suited to the research aim, it may further limit the possibility of generalizing our findings. Future studies should be conducted in countries other than Spain to augment the external validity of our results, especially in high-technology regions or industries. Second, our results can be expanded by using some qualitative research methods, such as multiple cases (e.g., De Massis et al., 2015) or direct interviews with firm members (e.g., Kammerlander & Ganter, 2015). The richness of these alternative methods would favor a better comprehension of the mediating effect of TI efficiency on the family management–firm performance relationship. Third, limitations in our database have made it impossible to control for other key variables, such as the level of family ownership, the generation in charge, or the existence of family governance practices. For example, as the top management team of a family firm typically includes family members from multiple generations with contrasting goals and views (Pittino et al., 2019), it would be particularly interesting to examine whether and how such generational diversity in family firms’ management affects TI efficiency in achieving performance outcomes. Furthermore, given that innovation is a complex multidimensional process and that family influence may create disadvantages in some areas of innovation and advantages in others (Bammens et al., 2015), it would also be of great value to analyze the extent to which TI efficiency, assessed in terms of different innovation inputs (e.g., R&D personnel or external networks) and innovation outputs (e.g., process or services innovations), might affect firm performance. Similarly, future work may explore the indirect incidence of TI efficiency on multifaceted measures of firm performance embracing not only financial but also non-financial indicators (Yeniaras et al., 2017). Finally, understanding how and why some environmental factors, such as industry volatility, munificence, complexity, or technology level, may influence TI efficiency, and thus impact firms’ performance outcomes, can be a fruitful research topic.

In conclusion, our article advances the research stream concerned with the family effect on organizational outcomes. Utilizing insights from the RBV, this study refines our knowledge regarding the influence of family involvement in management on firm performance by integrating this relationship into a novel mediation model that includes an intervening mechanism, TI efficiency, which up to now remains almost unexplored. The results reveal that TI efficiency is of crucial importance to achieve richer performance outcomes in those family firms with an active participation of family members in the firm management. With solid theoretical foundations supporting that TI efficiency is able to explain why some family firms perform better than their competitors and with specific managerial implications of the processes that family firms can undertake to improve their performance outcomes through TI efficiency, the model shown in this study enhances our understanding of the singular but critical topic of performance in family firms.

Footnotes

Acknowledgements

Rubén Martínez-Alonso acknowledges the funding received from the Spanish Ministry of Science and Innovation in the form of a Research Grant to develop his PhD (FPU-17/01359) and thereby this paper.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Rubén Martínez-Alonso received funding from the Spanish Ministry of Science and Innovation in the form of a Research Grant to develop his PhD (FPU-17/01359) and thereby this paper.