Abstract

The social performance (SP) of a firm is associated with many positive organizational outcomes. Nonetheless, little is known about the effect of the SP of a multinational enterprise (MNE) on the likelihood of cross-border acquisition completion (CBAC). Investigating the link between MNEs’ SP and the likelihood of CBAC is important because it will increase our understanding of how stakeholders reward MNEs with better reputations. Drawing on the signaling and reputation for SP literature, we explore how acquisition complexity, reputational risk, and firm visibility influence CBAC. Based on a sample of 578 cross-border deals undertaken by acquirers in the noncyclical consumer industry (NCCI), our results support a positive relationship between MNEs’ SP and the likelihood of CBAC and strengthening moderating effects of acquirer size and public targets.

Keywords

Introduction

The reputation of multinational enterprises (MNEs) is heavily influenced by their social actions in regard to, for example, community involvement, diversity, labor unions, and customer interactions (Aguilera-Caracuel & Guerrero-Villegas, 2018; Bertrand et al., 2021). Accordingly, the social performance (SP) of a firm has been shown to positively influence a range of favorable organizational outcomes, such as analysts’ recommendations (Luo et al., 2015), reputation (Pérez-Cornejo et al., 2021), attractiveness as an employer (Jones et al., 2014), debt ratings (La Rosa et al., 2018), and financial performance (Aguilera-Caracuel & Guerrero-Villegas, 2018; Gras & Krause, 2020; Tsai & Wu, 2022).

Despite the plethora of research on SP within the management literature, this topic has remained relatively underexplored from an international business (IB) perspective (Marano et al., 2022; Mohr et al., 2022; Muller, 2020; Nardella & Brammer, 2021). Although there are a few studies analyzing the role of SP in the context of acquisitions (Cho et al., 2021; Krishnamurti et al., 2019; Ma et al., 2020), the literature does not clearly answer whether the SP of an MNE affects the likelihood of cross-border acquisition completion (CBAC). Studying the link between the SP of an MNE and the likelihood of CBAC is important not only because of its practical significance—indeed, deal abandonment may cause significant financial and reputational losses—but also because such an examination will increase our understanding of the explanatory mechanism through which an MNE is able to increase its likelihood of CBAC via its SP. This understanding will broaden the horizons of the acquisition outcomes literature, reputation for SP literature, and nonmarket strategy literature from the IB perspective. Thus, the objective of this study is to examine the effect of the SP of MNEs on the likelihood of CBAC.

In a related study based on a sample of mergers in the United States, Deng et al. (2013) showed that an acquirer’s corporate social responsibility (CSR) score is positively associated with the likelihood of deal completion. We extend the work of Deng et al. (2013) in four ways. First, we specifically focus on the SP of acquirers instead of an aggregated CSR measure. 1 Second, our sample is not restricted to a single country. Instead, we use a global data set covering 578 cross-border acquisitions in 21 home countries and 53 host countries. Third, we consider the moderating influence of two variables in our study (acquirer size and public targets). These variables represent salient characteristics of the acquirer and target, respectively, and have crucial theoretical relevance in this study. Fourth, we focus on a useful setting, namely, that of noncyclical consumer industry (NCCI) acquirers. 2

Building on the tenets of the reputation for SP literature which is grounded on signaling theory, we theorize acquisition complexity—negative influences on cross-border acquisition deals from the formal and informal domains of host country institutions. We argue that when MNEs act according to the social regulations and norms prevalent in their host countries, they are subject to less-acquisition complexity. That is, MNEs’ reputation for SP helps them decrease acquisition complexity. We further argue that the effect of reputation for SP on acquisition complexity translates into an increased likelihood of deal completion because cross-border acquisitions represent a context in which acquirers are subject to reputational risk and visibility. Furthermore, we contend that acquirers are subject to a greater degree of reputational risk and visibility when they are large or when they acquire public targets. Thus, large acquirers and acquirers that buy public targets are able to mitigate acquisition complexity to a greater extent than small acquirers and those that buy private targets, respectively. Thus, we hypothesize that acquirer size and public targets strengthen the positive relationship between MNEs’ SP and the likelihood of CBAC. Our hypotheses are supported by logistic regression and a range of robustness tests.

The contributions of this study are threefold. First, our study contributes to the literature on acquisition outcomes (for a review, see Kumar & Sengupta, 2021). To the best of our knowledge, this is the first study that exclusively focuses on the effect of the social dimension of CSR on deal outcomes. Thus, we contribute to the acquisition outcomes literature by introducing an important predictor of the likelihood of acquisition completion. Furthermore, unlike prior acquisition studies that discuss the role of complexity in the post-acquisition phase (Kang et al., 2021; McCarthy & Noseleit, 2022; Zorn et al., 2019), we show that acquisition complexity matters before the postacquisition phase. Second, our study enriches the theory on reputation for SP in an IB context. Prior studies on SP have focused on its antecedents (Gardberg et al., 2019; Zyglidopoulos, 2001, 2004). Despite the enormous amount of money spent by MNEs on reputation building, the IB literature provides limited information on whether stakeholders reward MNEs with better reputations. This study sheds light on the importance of considering the signals that MNEs send to their stakeholders located outside their home countries to increase the likelihood of CBAC. Thus, we contribute to the debate on reputation for SP, from its antecedents to its consequences, in an interesting IB context of cross-border acquisitions. Third, we contribute to the nonmarket strategy literature by illustrating the importance of reputation for SP in an inter-organizational transactional context. Prior literature on nonmarket strategy has generally focused on firms’ interactions with noncommercial external parties such as governments, nongovernment organizations, and local communities (Mellahi et al., 2016). Thus, the ways in which a firm may gain the benefits of CSR investment from other commercial firms remains relatively underexplored (Cho et al., 2021; Krishnamurti et al., 2019; Ma et al., 2020). Our research shows that firms’ nonmarket strategies are advantageous even in an inter-organizational transactional context. That is, a firm can gain economic benefits by investing in nonmarket strategies even from a commercial entity (in the form of a higher likelihood of CBAC).

The rest of the study is organized as follows. The following section presents the theoretical background and hypothesis development. Then, we present the methodology by explaining the sample selection process, the operationalization of the variables, and the empirical model. Afterward, the descriptive statistics, the logistic regression results, and the results of robustness checks are discussed in the results section. The final section includes a discussion and conclusion.

Theoretical background and hypothesis development

Reputation for SP

Reputation for SP has been extensively studied by scholars for decades (Zyglidopoulos, 2001). It refers to stakeholders’ knowledge and emotions regarding the SP of a firm. Literature suggests that reputation for SP is a multidimensional construct composed mainly of two dimensions: awareness and perception (Gardberg et al., 2019). Awareness of SP refers to stakeholders’ collective acknowledgment of a firm’s SP. In contrast, perception of SP encompasses stakeholders’ judgments of whether they consider a firm’s SP to be satisfactory.

For example, a recent Nike advertisement in Japan received extensive attention on social media (Oh & Wha Han, 2022). The advertisement aimed to challenge social stereotypes such as bullying and racism in the context of Japan. Nonetheless, consumers were still divide on whether the advertisement should be praised for challenging social stereotypes or criticized for unnecessarily tarnishing the social image of Japan. Thus, in the typology of the reputation for SP literature, we would say that this advertisement resulted in an increased awareness of SP manifested in high viewership. Nonetheless, perception of SP did not necessarily increase since consumers still debated whether the advertisement was appropriate.

The literature on reputation for SP is profoundly influenced by signaling theory (Spence, 2002). Signaling theory assumes that agents (e.g., individuals, businesses, and governments) have access to different levels of information (Connelly et al., 2011). To reduce information asymmetry, agents try to communicate their underlying qualities to the interacting parties by sending relevant cues or signals. For example, prospective employees try to show their worth by displaying their prestigious educational backgrounds (Spence, 1974). Companies may hire female executives to show their commitment to progressive social norms and challenging the status quo (Reinwald et al., 2022). Likewise, stakeholders give considerable attention to signals given by companies regarding their CSR engagement (Bitektine & Song, 2022). The literature suggests that firms with a high reputation for SP are more likely to be considered attractive employers (Lin et al., 2012). Furthermore, these firms receive more favorable product evaluations from customers (Lii & Lee, 2012).

Signals concerning reputation for SP are particularly important in the IB context. First, cross-border acquisitions are subject to a high level of information asymmetry (Reddy & Fabian, 2020). Second, stakeholders are generally more skeptical of cross-border acquirers compared to domestic acquirers because of additional challenges such as cultural heterogeneity (Kim et al., 2020). Third, cross-border acquirers try to signal their competence and trustworthiness to host country stakeholders (Jiang et al., 2020). Fourth, stakeholders typically do not have access to all the information regarding the SP of MNEs. Thus, to communicate their social efforts to stakeholders, cross-border acquirers send a series of signals to their host country stakeholders. These signals may not necessarily be positive. The unintended results of some firm actions even lead to the transformation of positive signals to negative ones. The reputation for the SP of a firm is based on a series of positive or negative signals conveyed by the firm to its stakeholders (Basdeo et al., 2006). The receivers of these signals choose how to interpret them. As signals are received by the stakeholders, their awareness of SP increases. When signals are interpreted positively by the receivers, their perception of SP increases (Gardberg et al., 2019).

Acquisition complexity

MNEs have to deal with complexities present in the formal and informal domains of the institutional environment (Brammer et al., 2021). In the context of this study, these domains of the institutional environment put forward rules and expectations related to reputation for SP. The formal domain of the institutional environment addresses the rules and regulations that MNEs are bound to follow (Scott, 1995). In other words, the formal domain entails clearly written regulations that a government can enforce. We observe that a significant portion of the rules and regulations in a given territory address how MNEs must deal with labor unions (Levine et al., 2020). For example, in the United States, the responsibility for ensuring labor rights rests with The National Labor Relations Board (NLRB), an independent federal agency. To protect labor rights, this agency conducts union elections, investigates charges, facilitates settlements, decides cases, enforces orders, and engages in rulemaking related to labor issues. The National Labor Relations Act clearly stipulates what constitutes a violation of the law (NLRB, 2020). For example, employers cannot lay off, terminate, transfer, or assign more difficult duties to employees because of their active role in a union. Furthermore, to ensure freedom of participation in union activities to employees, an employer cannot even threaten to lay off employees or close the plant due to union activity. In the European Union, labor law legislation and enforcement come under the jurisdiction of the European Commission. Article 153 of the Treaty on the Functioning of the European Union clearly stipulates laws that set minimum requirements for working and employment conditions and for informing and consulting workers (Europa, 2020). Likewise, every country has a law and an enforcing body that address labor rights. Thus, if an MNE with a low reputation for SP tries to enter a foreign market, it is likely to face formal restrictions imposed by host country regulatory bodies.

In addition to labor laws, regulations regarding customer responsibility are important in the context of this study (Richards et al., 2015). For example, in the food and health care sectors, any negligence in the manufacturing process seriously impacts the health of consumers. Thus, such firms have to comply with complex regulations related to the manufacturing process and ingredients. Foreign firms planning to export food to Japan must follow Japanese regulations that stipulate specifications, standards, and testing methods for foodstuffs (Japan External Trade Organization, 2009). Such regulations are usually very specific. As an illustration, Japanese regulations specifically mention that food items shall not contain any substance that is used as an ingredient in agricultural chemicals or other chemicals. To provide further clarification, the relevant document mentions the names of 20 such substances. Each country has similar regulations that govern food and health care firms. MNEs that do not follow such rules not only face legal penalties but also compromise their reputation for SP. In contrast, MNEs that follow these regulations are respected as law-abiding citizens (Al-Gamrh & Al-Dhamari, 2016). Thus, if MNEs maintain a high reputation for SP by following rules and regulations related to social issues such as labor unions and product quality, they will likely face limited/no resistance from host country regulatory bodies upon entering a foreign market.

The informal domain of the institutional environment deals with the institutional pressures faced by MNEs that arise from social values (Selznick, 1957). We argue that acquisition complexity is lower if there is a high level of consistency between the values shared by an organization and the wider society around it (Parsons, 1960). Because of its tacit nature, the informal domain is more difficult to sense and interpret than the regulatory domain, particularly in a cross-country context (Kostova & Zaheer, 1999). After all, every society has its own interpretation of what constitutes a social issue and how MNEs should contribute to such issues. For this reason, regarding community involvement, MNEs thoroughly inspect the expectations of stakeholders in a given host country and try to meet those expectations (Newburry & Gladwin, 1997). Scholars argue that an MNE’s contribution to society is maximized when it contributes by using its strategic resources and core competence (Hess & Warren, 2008; Pearce & Doh, 2005). For example, McKinsey and Co., a consulting firm, maximizes its contribution to society by providing free consulting services to nonprofit organizations (Bruch & Walter, 2005). In the same way, IBM, which specializes in IT infrastructure, maximizes its social contribution by providing relevant services free of charge to educational organizations (Bruch & Walter, 2005). In some instances, due to their rare resources and competences, MNEs are the only means by which a society can be brought out of a crisis (Dunfee, 2006). In such a case, society may feel that MNEs have a moral obligation to make social contributions. For example, pharmaceutical firms are often criticized for not playing an active role in the eradication of AIDS in sub-Saharan Africa (Dunfee, 2006). Moreover, food companies face similar cultural and societal pressures. In the wake of such expectations, MNEs that respond actively are considered more reputable in the eyes of stakeholders. Richards et al. (2015) examined the CSR activities of six large food companies in Australia and found that approximately 70% of the CSR activities undertaken by these companies were related to social issues regarding consumer responsibility, community engagement, employee relations, partnerships, indigenous communities, and diversity. Thus, MNEs with a high reputation for SP are likely to face limited acquisition complexity when their deals are publicly announced.

Just as MNEs are subject to complexities embedded in formal and informal institutions (Brammer et al., 2021), cross-border acquisitions are no exception (Kang et al., 2021; Lauser, 2010; Zorn et al., 2019). In the context of this study, we define acquisition complexity as the extent to which an acquisition transaction is negatively influenced by formal (regulatory) and informal (social) institutions. We argue that when MNEs act against the rules and norms prevalent in an institutional environment, they face high acquisition complexity. In contrast, MNEs face low acquisition complexity when they act in accordance with institutional regulations and recommendations. That is, we contend that due to the social issues related to the formal and informal domains of the institutional environment, MNEs feel pressured to increase their SP. As a consequence, MNEs that act according to the regulations and expectations of their host country stakeholders are subject to less-acquisition complexity in host countries than those that do not.

Reputation for SP matters for CBAC

In the earlier section, we concluded that MNEs’ reputation for SP helps them decrease acquisition complexity. In this section, we discuss that the effect of reputation for SP on acquisition complexity translates into an increased likelihood of deal completion. Based on the acquisition and reputation for SP literature, we expect that two factors come into play.

First, MNEs are subject to high levels of reputational risk when they make cross-border acquisitions. In the context of this study, we define reputational risk as the likelihood of cross-border acquirers to unexpectedly lose their reputations when they are covered negatively by the media. According to signaling theory, host country receivers keenly assess signals given by cross-border acquirers. Media in the host country tend to focus more on unintended negative signals. Hence, if MNEs are discussed negatively by the media, it may seriously impact the reputation of cross-border acquirers. The biased treatment of MNEs in the host country is likely because of a liability of foreignness (LOF) that MNEs face in host countries (Zaheer, 1995). LOF refers to costs that are unique to foreign firms in a host country, that is, costs that purely domestic firms do not incur. According to Sethi and Judge (2009), these costs could be incidental or discriminatory. Incidental costs are those that foreign MNEs incur in coping with their unfamiliarity with the host country environment without being subject to any form of discrimination. Examples include the cost of understanding customer preferences and the cost of finding suitable partners for product distribution. In contrast, discriminatory costs are those that foreign firms incur to comply with regulations that target only foreign firms or to deal with prejudice and nationalism. For example, foreign firms have a bad reputation in host countries for exploiting local firms (Kostova & Zaheer, 1999). Moreover, due to escalating trends toward anti-globalization, foreign firms are often resisted by local stakeholders with nationalistic agendas (Meyer, 2017). Due to this liability, these firms face difficulty when interacting with their internal and external stakeholders (Crilly et al., 2016). As host country regulatory bodies are influential external stakeholders in cross-border acquisitions, they play a significant role in judging acquirers’ reputation and thereby affecting deal outcomes (Li et al., 2017). Specifically, host country regulatory bodies have the authority to block a specific deal and discourage the takeover of firms in specific industries (Conybeare & Kim, 2010; Xie et al., 2017). Based on the discussion in the previous section, we expect that host country regulatory bodies thoroughly consider the SP of acquirers. Allowing a foreign firm with poor SP to buy a local target may have a negative spillover effect within the corresponding host industry (Zhou & Wang, 2020). Therefore, regulators rigorously review deals that involve an acquirer with poor SP.

Second, MNEs are highly visible by members of the media and global economic watchdog analysts (Graf-Vlachy et al., 2020; Zhou & Wang, 2020). In the context of signaling theory and the reputation for SP literature, we would say that the signals of MNEs are amplified when they make cross-border acquisitions. As M&A deals and social issues are both prominent topics in business news (Aliaj et al., 2020; Posner, 2020), the perception of foreign acquirers in the minds of host country actors is likely to be affected by how their SP is discussed by the media. Moreover, reports published by global organizations such as the United Nations include detailed discussions of the SP of MNEs (United Nations Conference on Trade and Development, 2020). This encourages stakeholders to consider the SP of prospective acquirers. Graebner (2009, p. 442) noted that top decision makers in target management “engage in excessive due diligence” when they lack trust in acquirers. In addition to top decision makers, employees (and other stakeholders who sympathize with employees) are expected to resist a deal if they expect a paternalistic management style from the acquirer (Cooke, 2012; Fleming, 2005).

Based on the above discussion, we state the first hypothesis below.

Hypothesis 1: Ceteris paribus, the SP of MNEs is positively associated with the likelihood of CBAC.

Moderating role of acquirer size

In the previous section, we argued that the effect of reputation for SP on acquisition complexity translates to a higher likelihood of deal completion. In this section, we argue that this phenomenon is more pronounced for large acquirers, as they experience greater acquisition complexity due to their high levels of reputational risk and visibility.

First, the matter of reputation is of critical importance for large firms. If other factors are held constant, size has a positive impact on reputation, meaning that on average, larger firms have better reputations (Kaur & Singh, 2021). Moreover, large firms have high levels of reputational risk. That is, large firms are more likely to suffer severe reputational damage than small firms in the case of an unlikely event. For instance, we observe that large firms are subject to a greater degree of LOF in host countries than small firms. One reason for this phenomenon may be that large firms have greater exploitation power than small firms (Kostova & Zaheer, 1999). In addition, in the wake of anti-globalization campaigns (Meyer, 2017), large firms are more likely to be the target of host country interest groups (Kostova & Zaheer, 1999). Moreover, large firms usually have operations in numerous countries. As a result, their reputational losses in one or more countries are likely to compromise their reputation in other countries as well (Zhou & Wang, 2020). For these reasons, large acquirers may feel a greater need to maintain their reputation than small firms.

We also discussed in the previous section that MNEs’ visibility is another reason why reputation for SP affects the likelihood of deal completion via acquisition complexity. Here, we argue that an MNE’s visibility is a function of its size (Kostova & Zaheer, 1999). Stated differently, an MNE is more likely to be discussed by the media if it is large and reputed (Cabral, 2016). News regarding large firms generates greater readership and/or viewership because large firms usually have more employees, a greater number of products, and more diverse stakeholders than small firms (Ahern & Sosyura, 2015). Thus, from a commercial point of view, media outlets are more likely to cover large firms more extensively than small firms. As a result, large firms are able to obtain more benefits from investments in social issues.

In summary, as large acquirers have high levels of reputational risk and visibility, we expect that such acquirers are subject to greater acquisition complexity, which strengthens the relationship between these acquirers’ SP and the likelihood of CBAC. Therefore, we present the second hypothesis as follows:

Hypothesis 2: Acquirer size moderates the relationship between the SP of MNEs and the likelihood of CBAC such that the positive relationship between the SP of MNEs and the likelihood of CBAC is stronger for large acquirers.

Moderating role of public targets

In the previous section, we argued that the effect of reputation on acquisition complexity translates to an increased likelihood of CBAC. In this section, we argue that this phenomenon is more pronounced for acquirers that buy public targets (as opposed to private targets) because such acquirers experience greater acquisition complexity due to their high levels of reputational risk and visibility.

As mentioned, we argue that acquirers that buy public targets have higher reputational risk than those buying private targets. It is important to consider differences in the number and scrutinizing power of stakeholders associated with public and private targets. Private firms are usually owned by families or small groups of partners (Draper & Paudyal, 2006). In contrast, public firms are heterogeneous—usually owned by many stakeholders. Thus, in the case of a public target, an acquirer’s reputation is judged by a range of stakeholders. In contrast, acquirers that buy private firms have to maintain their reputation with fewer stakeholders. In addition to the number of stakeholders, the SP awareness of stakeholders should be taken into consideration. Public targets, due to their greater size and organizational structure, have more resources with which they increase their knowledge of the SP of potential acquirers. As a result, foreign firms seeking to buy public targets must have a stronger reputation than those seeking to buy private targets (Li et al., 2017). Moreover, interest groups are more likely to rally against MNEs that plan to buy prominent public targets rather than lesser-known private targets (Kostova & Zaheer, 1999).

Another reason acquirers that buy public targets face acquisition complexity is that deals involving a public target are subject to a greater degree of visibility than those involving a private target. Public targets are constantly monitored by regulatory bodies, security analysts, and institutional investors (Capron & Shen, 2007). Thus, media companies are more likely to cover M&A transactions involving public targets to attract larger audiences (Ahern & Sosyura, 2015). Moreover, the difference in information asymmetry between public and private firms is significant (Beatty & Harris, 1999). Public firms are required by law to share much of their information in the form of financial statements. In contrast, private firms do not have any such obligation. Therefore, stories related to public targets are more likely to be covered by the media than those related to private targets. Therefore, the reputational threshold of foreign firms is higher if they acquire a public target rather than a private target.

In summary, we argue that acquirers that buy public targets are subject to a greater degree of reputational risk and visibility than those buying private targets. Therefore, we expect that in the case of public targets, the relationship between MNEs’ SP and the likelihood of CBAC is stronger than in the case of private targets. Formally, we present the third hypothesis as follows:

Hypothesis 3: The public or private status of a target moderates the relationship between the SP of MNEs and the likelihood of CBAC such that the positive relationship between the SP of MNEs and the likelihood of CBAC is stronger for public targets than for private targets.

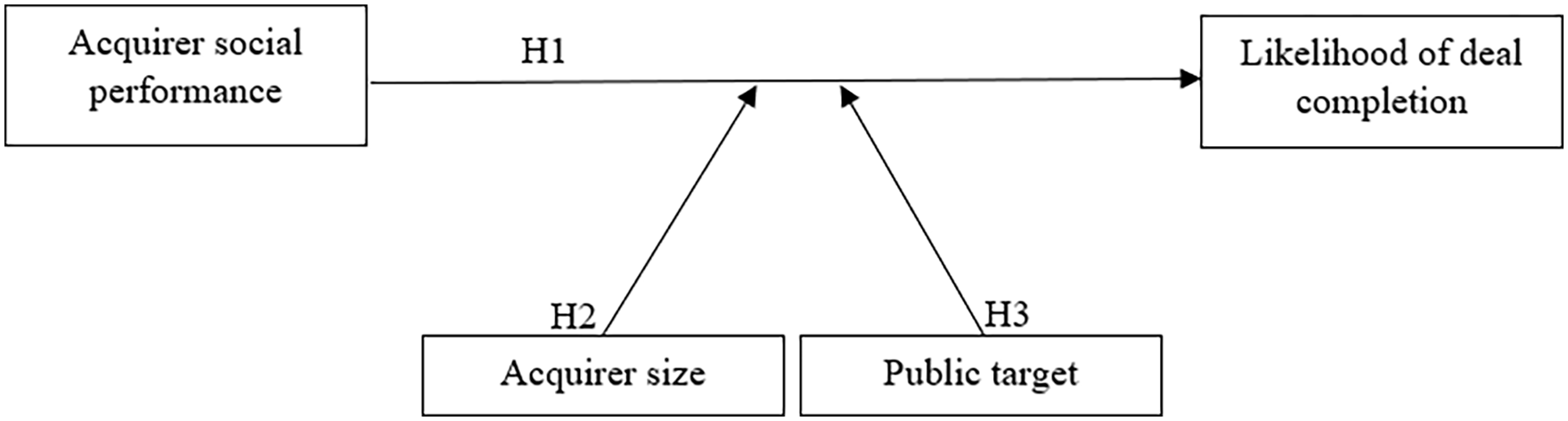

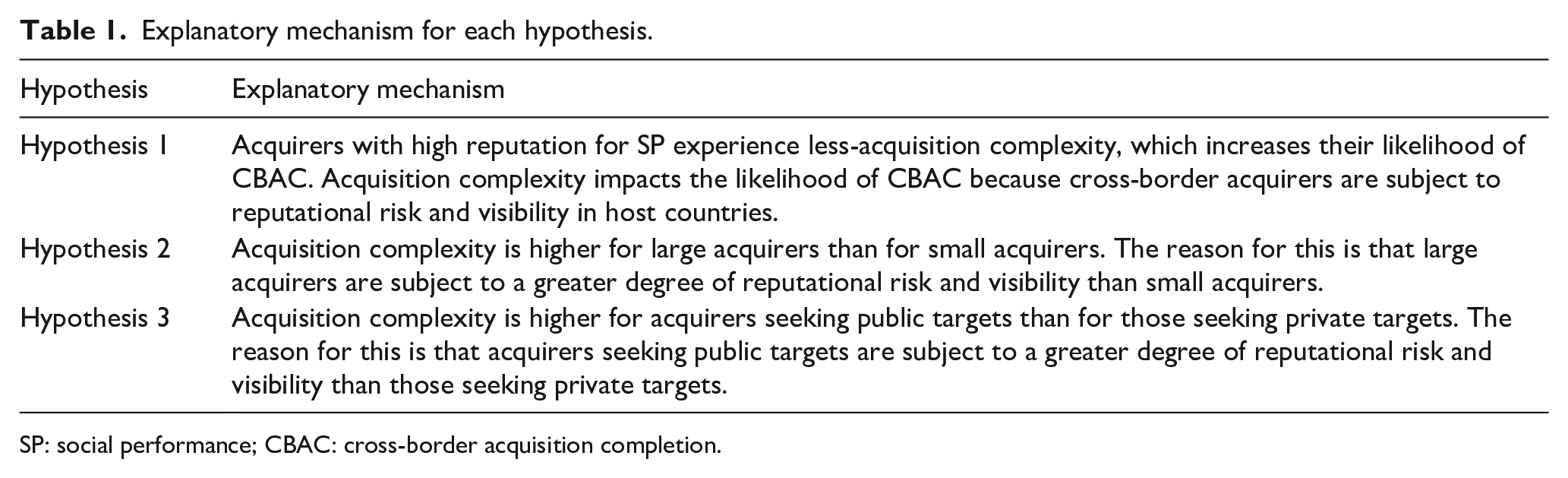

We present the conceptual model in Figure 1. Furthermore, we summarize the explanatory mechanism for each hypothesis in Table 1.

Conceptual model.

Explanatory mechanism for each hypothesis.

SP: social performance; CBAC: cross-border acquisition completion.

Methodology

Sample

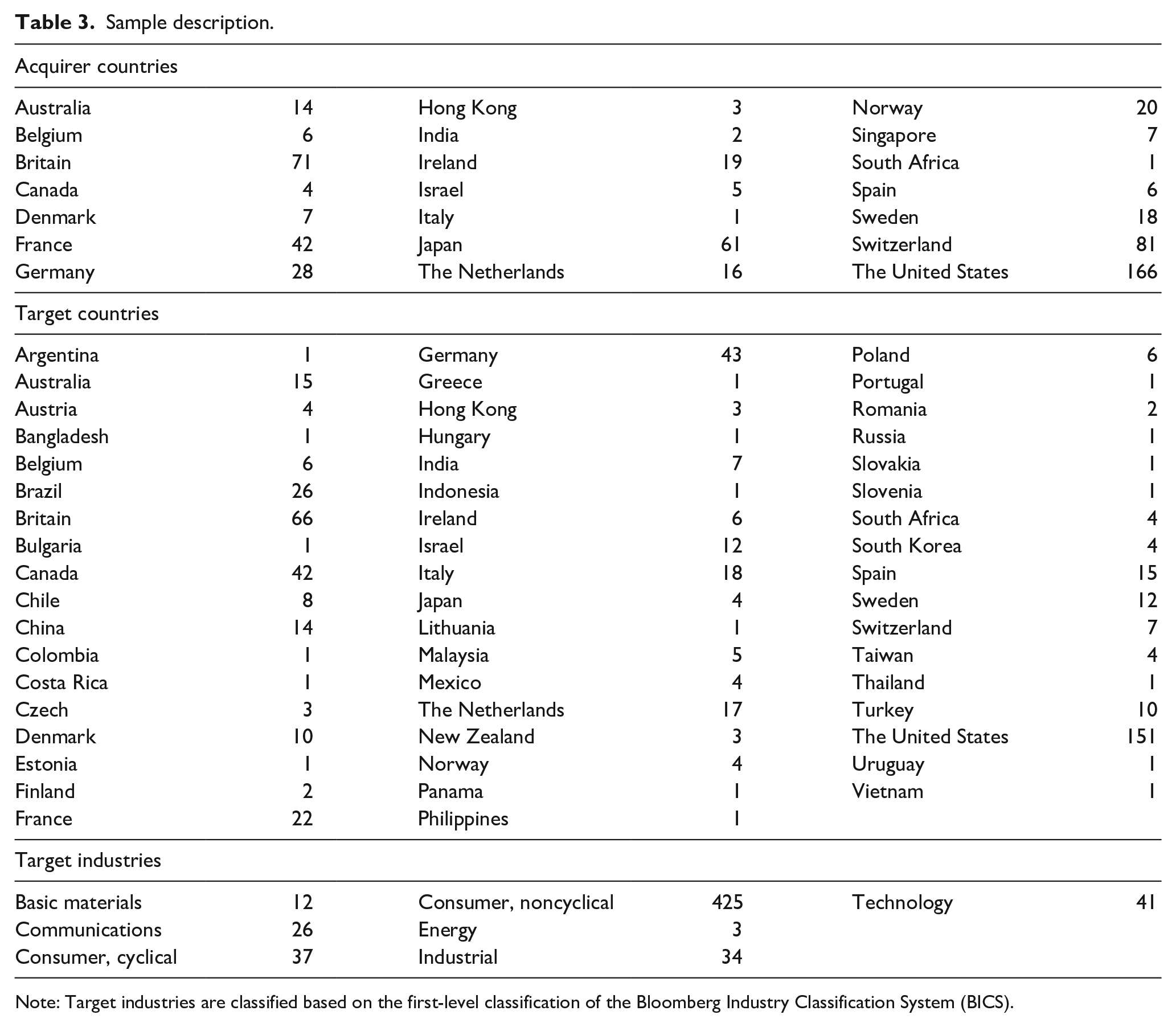

We used the Bloomberg database to download data on cross-border acquisitions (Ahmed et al., 2020; Nkiwane & Chipeta, 2019; Waqar, 2020). We applied several filters to develop the sample for this study. First, we shortlisted cross-border deals in which the acquirer was a public firm in NCCI. We limited the search to public acquirers because only these firms had available data on SP. In addition, it is common to focus on public acquirers in acquisition studies due to the nature of the control variables used (Sartor & Beamish, 2018). However, on the target side, we retained both public and private firms to test H3. Second, we deleted toehold transactions from our sample (Cuypers et al., 2015; Dow et al., 2016). Toehold transactions are those in which the acquirer already has some ownership in the target prior to the focal transaction. Toehold transactions are usually excluded from acquisition studies since the acquirer may have considerable inside information about the target or have ties with key decision makers within it. Hence, due to their peculiar nature, toehold transactions are not analyzed alongside other types of transactions. Third, we shortlisted deals in which the corresponding acquirers gained more than 50% ownership in their targets (Kim & Song, 2017; Li et al., 2019). The cutoff of 50% is important in acquisition studies since an acquirer can obtain majority decision power in its target by owning more than 50% of the target’s shares. Fourth, we excluded targets in the financial industry and diversified industries due to their idiosyncrasies (Fuad & Gaur, 2019; Liang et al., 2009). Fifth, we limited the analyzed acquisition announcement years to those from 2014 to 2018. We used 2014 as the starting point of the deal announcement period because we had access to SP data from 2013 onward. Since we used the data on firm-level variables (including the SP) from the most recent financial statement prior to the deal announcement, 2014 was the earliest announcement year that we could use in this study. We used 2018 as the ending point of the deal announcement period because deals announced in 2019 might still be pending in 2020, when we performed the data collection for this study. Due to data limitations related to the control variables highlighted in the following section, the final sample consisted of 578 cross-border deals.

Before proceeding to our main analysis, we subsampled public targets and tested whether acquirer SP affected acquisition premium. We found that there was no significant impact. Hence, this phenomenon could be generalized across the whole sample (for the public as well as private targets).

Measures

Our dependent variable was deal completion. This was a dummy variable that took a value of one for completed deals and zero for abandoned deals (Kim & Song, 2017; Li et al., 2019).

The independent variable in our study was acquirers’ SP. We measured this variable using Sustainalytics data due to the prominent use of these data in the CSR literature (Auer & Schuhmacher, 2016; Ben-Amar & Belgacem, 2018; Francoeur et al., 2019; Husted & de Sousa-Filho, 2017; Landry et al., 2013; Naciti, 2019; Surroca et al., 2010; Wolf, 2014). Sustainalytics was established in 1992, and it is among the top corporate governance ratings and analysis firms globally. Specifically, the composite index of SP that we used in this study is scored based on four dimensions—preparedness, disclosure, quantitative performance, and qualitative performance—in relation to social issues such as labor relations, employment diversity, and community involvement (Auer & Schuhmacher, 2016). Sustainalytics measures SP based on secondary data sources (such as financial statements and company and media reports) and primary data such as interviews with stakeholders and managers (Ben-Amar & Belgacem, 2018). Furthermore, the scores undergo an internal peer-review process for final corrections (Wolf, 2014). The scores range from 0 to 100, with higher values denoting better SP.

Our study involved two moderating variables. The first moderating variable was acquirer size. We measured this variable as the natural logarithm of the acquirer’s total assets (Chakrabarti & Mitchell, 2016; Li et al., 2017). The second moderating variable was of a categorical nature, denoting the public or private status of the focal target (Dikova et al., 2010; Li et al., 2019). We called this variable public target and measured it as a dummy variable that took a value of 1 for public targets and 0 for private targets.

In this study, we included several control variables identified in the prior literature on deal outcomes. The first control variable was the international experience of the acquirer with respect to cross-border acquisitions. We measured it as the number of cross-border investments completed by the acquirer prior to the focal transaction (Waqar, 2020). To correct for skewness, we added one to this variable and then took its natural logarithm (Reuer et al., 2012). The second control variable was percent sought. It represented the size of the stake the acquirer obtained in the focal deal as a percentage of the target (Fuad & Gaur, 2019). We used its natural logarithmic transformation to correct for skewness. The third control variable was tender offer. We included it as a dummy variable that took a value of one for tender offers and zero otherwise (Hukkanen & Keloharju, 2019). The fourth control variable was cash payment. We included it as a dummy variable that took a value of one if the payment method was purely cash and zero otherwise (Fuad & Gaur, 2019; Liou & Rao-Nicholson, 2019; Rao-Nicholson & Svystunova, 2020; Roh et al., 2021).

The fifth control variable was horizontal deal. A horizontal deal is one in which the acquirer and target have the same primary business, for example, a car manufacturer buying another car manufacturer or a laptop manufacturer buying another laptop manufacturer. In other words, it can be said that a deal is horizontal if the acquirer and target belong to a common industry. Horizontal deals may have a higher likelihood of deal completion since the information asymmetry entailed in such deals is lower, that is, the acquirer and target have sufficient information about each other. We included horizontal deal as a dummy variable that took a value of one if the acquirer and target belonged to the same third-level industry classification according to the Bloomberg Industry Classification System (BICS) and zero otherwise (Ahmed et al., 2020; Waqar, 2020).

The sixth control variable was cultural distance. To operationalize this variable, we first used Hofstede’s (1980) culture data to assign a score to each acquirer or target country along four dimensions of culture: power distance, individualism-collectivism, masculinity-femininity, and uncertainty avoidance. Then, we calculated the cultural distance between the acquirer and target countries using the standardized Euclidean distance formula (Konara & Mohr, 2019).

The seventh control variable was institutional distance. Institutional distance shows the extent to which an acquirer country and the corresponding target country differ in terms of their institutional development. A country’s institutional development is characterized by its political frameworks, policies and legal institutions. To operationalize this variable, we first used Worldwide Governance Indicators (WGI) data to assign 1-year lagged scores to each acquirer and target country along six dimensions: (1) voice and accountability, (2) political stability and lack of violence, (3) government effectiveness, (4) regulatory quality, (5) rule of law, and (6) control of corruption. Then, we calculated the institutional distance between each pair of countries using the standardized Euclidean distance formula (Konara & Mohr, 2019).

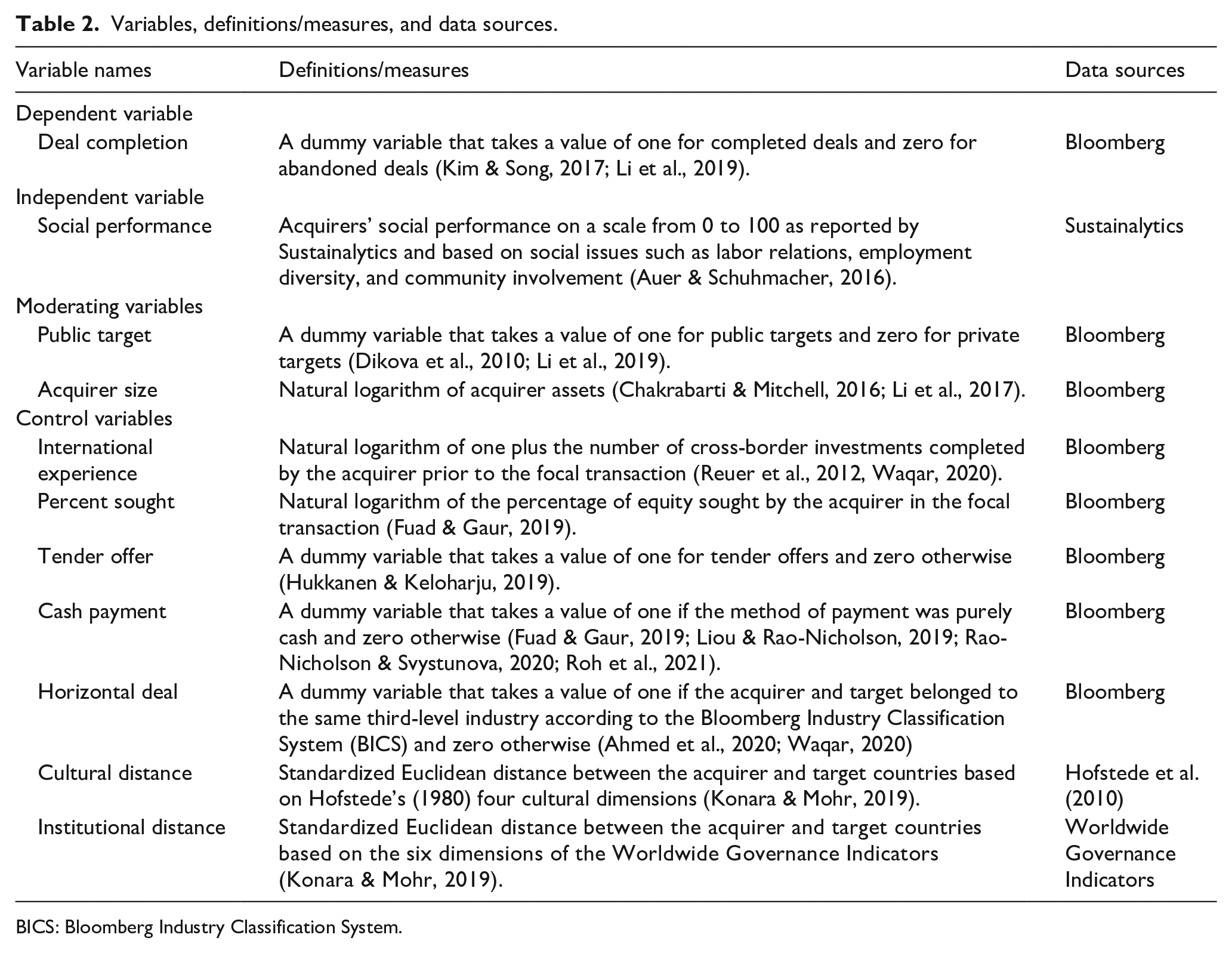

To control for unobserved heterogeneity across time, industries, and countries, we included year, first-level BICS target industry, and target country fixed effects in all our models. We winsorized the continuous variables between 1% and 99% levels to reduce the effect of outliers (Timbate, 2021). The measurements of the variables are summarized in Table 2.

Variables, definitions/measures, and data sources.

BICS: Bloomberg Industry Classification System.

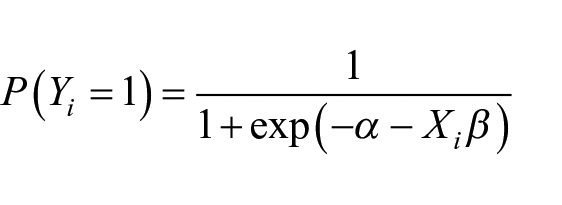

Empirical model

We used a binary logistic regression model since our dependent variable had two categories (abandoned deals and completed deals). The binary logistic model can be denoted as:

Here, Yi represents the binary dependent variable. α is the intercept parameter. Xi is the vector of independent variables for the ith observation, and β is a vector containing the regression parameters. The regression coefficients denote the impact of the independent variables on the likelihood of the event for which the dependent variable takes a value of one—in our case, deal completion. Thus, an estimated coefficient with a positive sign shows that the independent variable increases the likelihood of deal completion and vice versa.

We estimated six models in total. In the first model, we included only the control variables and the fixed effects (year, first-level BICS target industry, and target country). In the second model, we added the moderating variables, namely, acquirer size and public target. In the third model, we added SP—our main independent variable. In the fourth and fifth models, we added the interaction terms of SP with acquirer size and public target, respectively. In the sixth model, we added both interactions together to evaluate the stability of the results. Moreover, to facilitate a meaningful interpretation, we standardized all the continuous independent variables before using them in the regression. We used heteroskedasticity-consistent standard errors to ensure robust results (White, 1980).

Results

Descriptive statistics

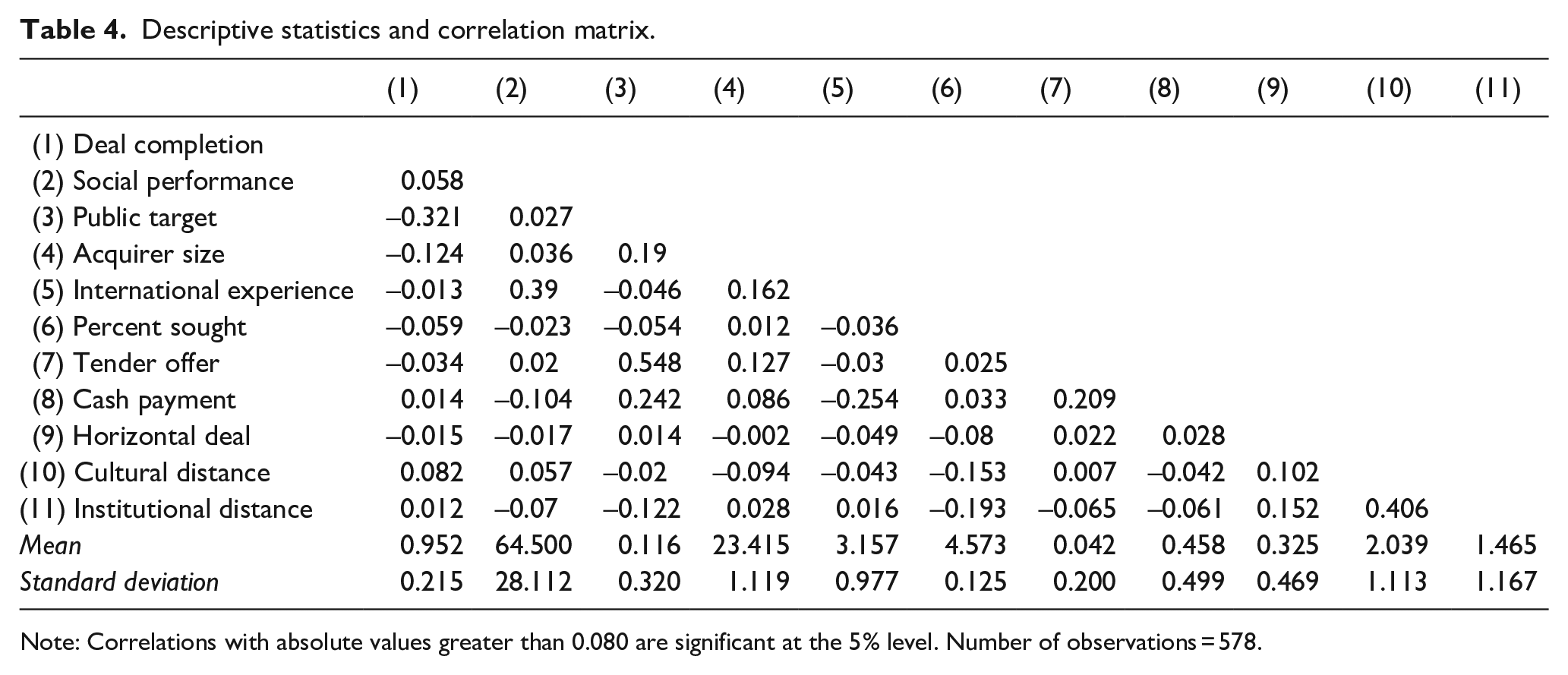

Our sample has 578 cross-border deals involving 21 acquirer countries and 53 target countries from 2014 to 2018. The details on the acquirer countries, target countries, and target industries of the whole sample are presented in Table 3. We also report the country/industry classifications and descriptive statistics of the acquirer assets corresponding to the abandoned deals in Appendix 1. In Appendix 2, we further compare major country, industry and deal characteristics between sample and population. Our sample size is larger than those of many prior studies on deal outcomes (Fuad & Gaur, 2019; Lim & Lee, 2016; Popli et al., 2016). The deal completion rate of our sample is approximately 95%, which is comparable to those observed in many prior studies (Kim & Song, 2017; Li et al., 2017). We report the descriptive statistics and correlation matrix of the variables in Table 4. The correlation among the independent variables is not high. The highest variance inflation factor (VIF) is 3.43, which shows that multi-collinearity is not a concern in our analysis.

Sample description.

Note: Target industries are classified based on the first-level classification of the Bloomberg Industry Classification System (BICS).

Descriptive statistics and correlation matrix.

Note: Correlations with absolute values greater than 0.080 are significant at the 5% level. Number of observations = 578.

Logistic regression

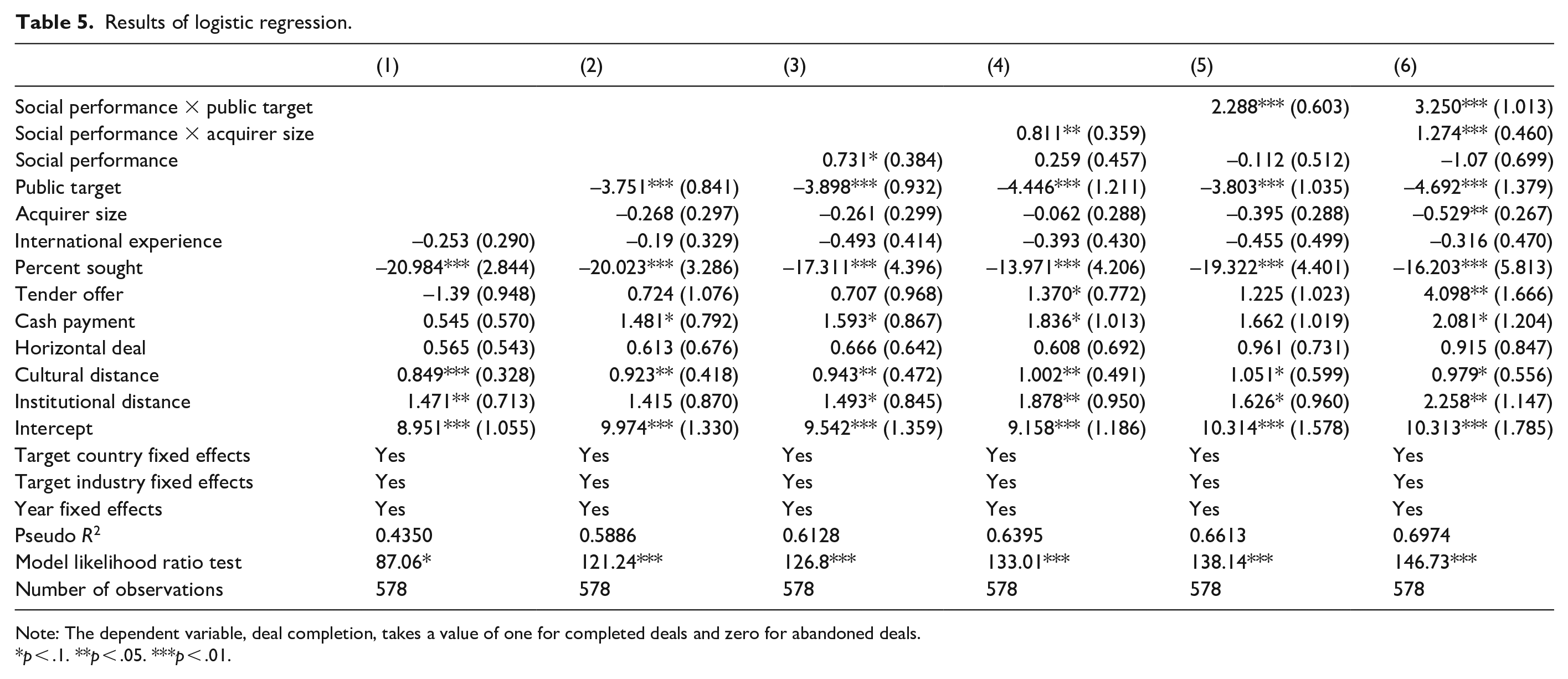

The results of the regression analysis are reported in Table 5. Model 1 includes only the control variables. The coefficients of cultural distance (β = 0.849, p < .01) and institutional distance (β = 1.471, p < .05) are positive and significant, showing that cross-border acquirers are more likely to complete a deal when acquiring a target in a culturally or institutionally different country than when acquiring one in a culturally or institutionally similar country. The coefficient of percent sought is negative and significant (β = –20.984, p < .01), suggesting that the likelihood of deal completion decreases when acquirers seek higher stakes in their targets. Model 2 evaluates the direct effect of the moderating variables (acquirer size and public target). Public target is negative and significant (β = −3.751, p < .01), meaning that acquirers are less likely to complete a deal involving a public target than one involving a private target.

Results of logistic regression.

Note: The dependent variable, deal completion, takes a value of one for completed deals and zero for abandoned deals.

p < .1. **p < .05. ***p < .01.

In Model 3, we examine the direct effect of the acquirers’ SP. The coefficient of SP is positive and significant (β = 0.731, p < .10). This shows that cross-border acquirers with high SP are more likely to reach deal completion than those with low SP. Thus, H1 is supported. In terms of effect size, let us classify an SP value 1 standard deviation below the mean as a low score and an SP value one standard deviation above the mean as a high score. In this case, we find that the odds of reaching deal completion for high-performing acquirers are 331.46% higher than those for low-performing acquirers. 3

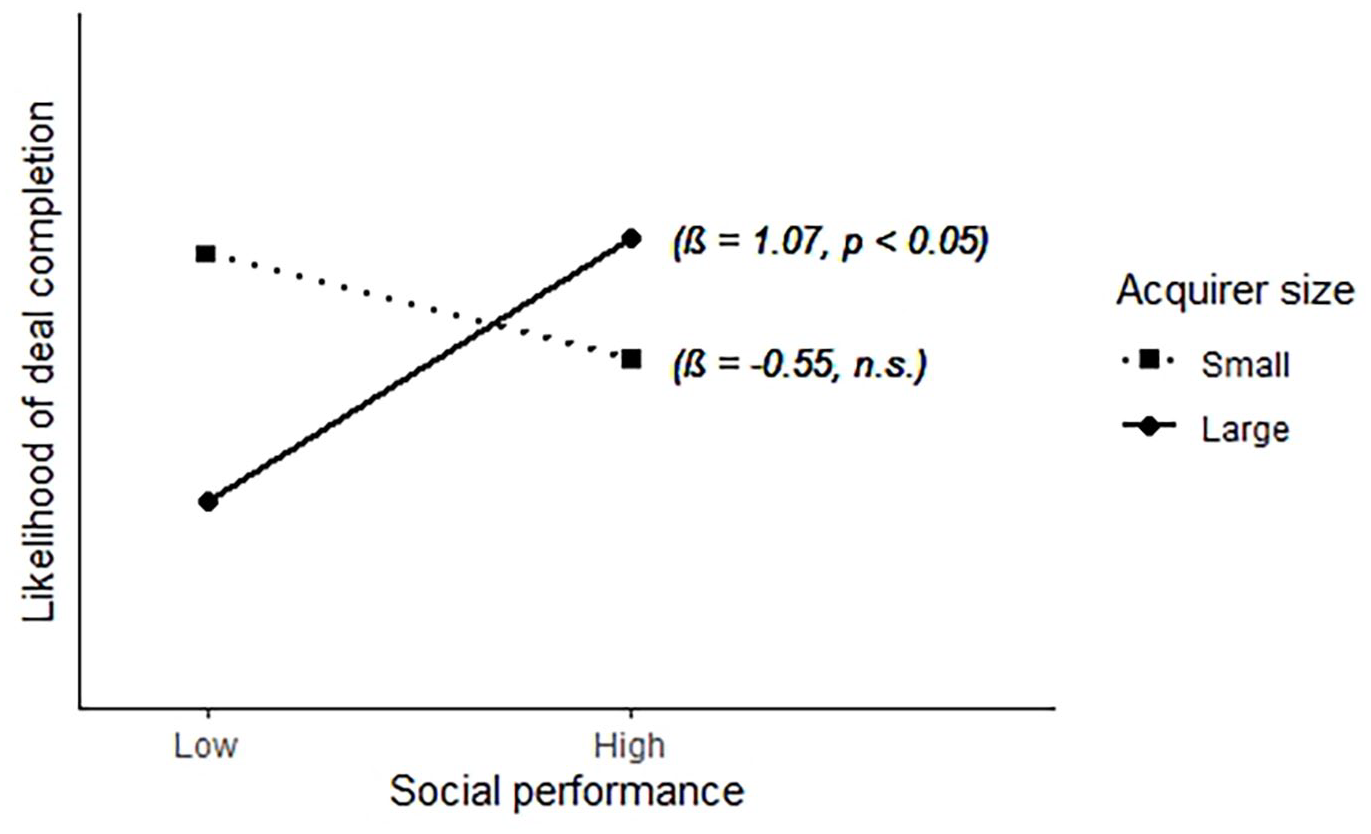

In Model 4, we include the interaction term between SP and acquirer size. This interaction term is positive and significant (β = 0.811, p < .05), showing that the positive relationship between acquirers’ SP and their likelihood of deal completion is stronger for large acquirers than for small acquirers. Thus, H2 is supported. We present an interaction plot depicting the impact of SP and acquirer size on deal outcomes, along with the results of a simple slope analysis, in Figure 2. A small acquirer size corresponds to one standard deviation below the mean, whereas a high acquirer size corresponds to one standard deviation above the mean. The low and high SP values are scored in the same way. The results of this simple slope analysis allow us to estimate the effect size of SP on deal outcomes for small and large acquirers. The results show that the odds of deal completion for high-performing large acquirers are 749.94% higher than those for low-performing large acquirers. In contrast, for small acquirers, the relationship between SP and the likelihood of CBAC is non-significant.

Moderating impact of acquirer size on the relationship between social performance and the likelihood of deal completion.

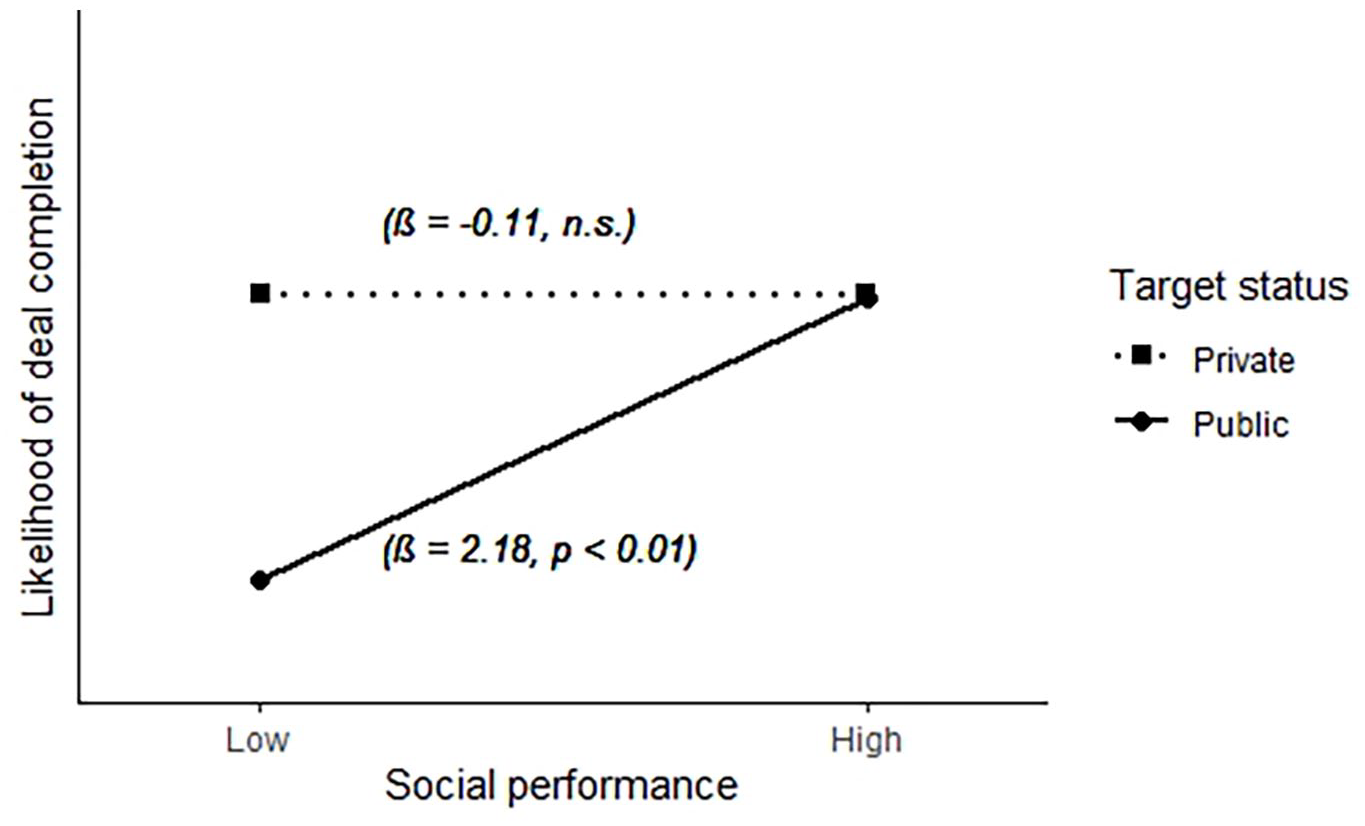

In Model 5, we include the interaction term between SP and public target. This interaction term is positive and significant (β = 2.288, p < .01), showing that the positive relationship between acquirers’ SP and their deal outcomes is stronger for deals involving public targets than for those involving private targets. Thus, H3 is supported. We present an interaction plot depicting the impact of SP and public target on deal outcomes, as well as the results of a simple slope analysis, in Figure 3. The low and high SP values are scored in the same way as in Figure 1. Our analysis regarding the effect size shows that for public targets, the odds of deal completion for high-performing acquirers are 7725.70% higher than those for low-performing acquirers. In contrast, for private targets, the relationship between SP and deal outcomes is non-significant.

Moderating impact of target status on the relationship between social performance and the likelihood of deal completion.

In Model 6, we include all the variables together to evaluate the stability of the interaction terms. We find that our results are stable, that is, both interaction terms continue to retain their significance and signs.

Robustness checks

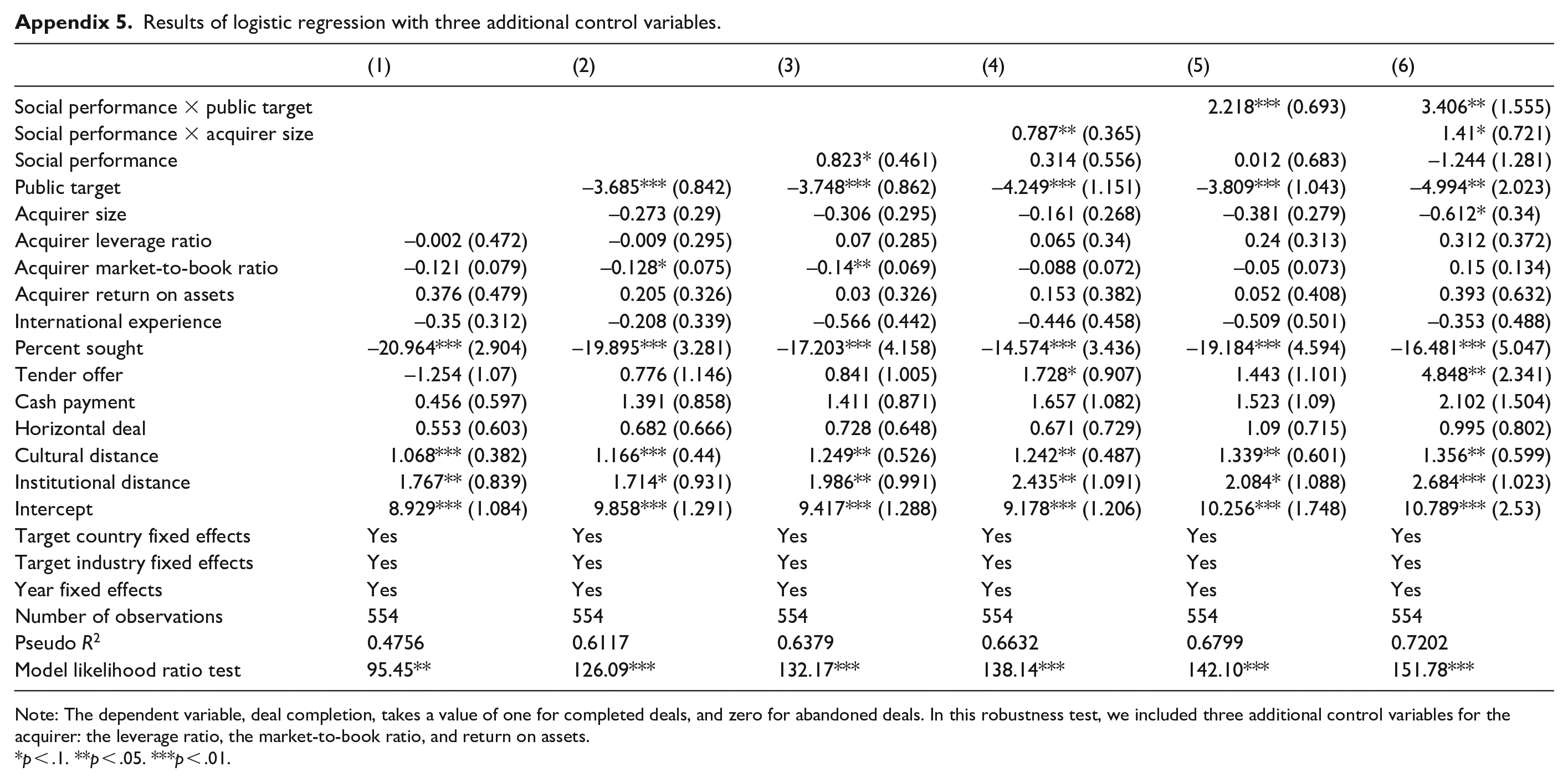

Our dependent variable is dichotomous; thus, we used a logistic model to obtain the main results. Dichotomous dependent variables can also be analyzed with a probit model. In the robustness analysis, we used a probit model and obtained consistent results. These results are reported in Appendix 3. In addition, based on our logistic model, we reported the results regarding the average marginal effects (AMEs) along with the results of the linear probability models (LPMs) in Appendix 4. 4 The findings were consistent with our main results. Moreover, we re-conducted the analysis after adding three more control variables for the acquirer: the leverage ratio, the market-to-book ratio, and return on assets. Again, our results were consistent, and they are reported in Appendix 5.

Furthermore, we conducted a number of unreported robustness tests in our study. We used a natural logarithmic transformation of our independent variable to address any possible skewness. Regarding our moderating variable, we measured acquirer size based on sales instead of assets (Fuad & Gaur, 2019). We also operationalized several control variables using alternative measures and methods. First, in our main results, we measured international acquisition experience based on the number of cross-border investments completed by the acquirer prior to the focal transaction. In a robustness test, we used the number of years since the completion of the first cross-border investment made by the focal acquirer (Ahmed et al., 2020; Chen, 2008; Chen & Hennart, 2004). Second, in our main results, our sample comprised all the acquisitions in which the focal acquirer received more than 50% ownership in the target. In a robustness test, we repeated all the analyses again on a subsample composed of full acquisitions (Becher et al., 2015; Waqar, 2020). Third, regarding cultural and institutional distance, we used a standardized Euclidean distance formula in the main results (Konara & Mohr, 2019). Thus, in a robustness test, we measured the cultural and institutional distance variables based on the commonly used Kogut and Singh index (Kogut & Singh, 1988). In our main analysis, we included country, industry, and year fixed effects. In a robustness analysis, we added country-industry fixed effects and industry-year fixed effects. These fixed effects controlled for country-specific industry characteristics and time-varying industry trends, respectively, that may influence the likelihood of deal completion (Bernstein et al., 2017). In all cases, the results were qualitatively similar to those reported in Table 5. That is, the direct effects of SP and both interaction terms were significant and positive.

Discussion and conclusion

The study makes several contributions to the literature. First and foremost, our study makes a direct contribution to the acquisition outcomes literature (Kumar & Sengupta, 2021). The acquisition outcomes literature suggests that acquirer characteristics such as size and experience are important in explaining the likelihood of deal completion. We show that the SP of acquirers is also a significant predictor of deal outcomes. Furthermore, we enrich the acquisition outcome literature by introducing the concept of acquisition complexity. The idea of complexity is not new in the overall body of acquisition literature (Lauser, 2010; Meglio et al., 2017; Saorín-Iborra, 2008). However, the application of complexity has not been extended to the domain of acquisition outcomes. For example, Zorn et al. (2019) studied nested acquisitions—deals in which acquirers buy target firms that have themselves recently bought other firms. Zorn et al. (2019) argued that post-acquisition performance decreases when acquisition complexity increases as a result of variance within embedded nested targets (greater number, more recent, less related, and larger nested targets). Similarly, Kang et al. (2021) argued that acquisition complexity both moderates and mediates the relationship between cross-border acquisition experience and post-acquisition performance. McCarthy and Noseleit (2022) argued that value creation decreases when acquisition complexity is higher (in competing bids). Our study extends the application of acquisition complexity in the acquisition literature by showing that acquisition complexity also matters before the post-acquisition phase.

Second, our study extends the theoretical boundaries of the reputation for SP literature from an IB perspective. Notwithstanding the importance of prior contributions, the literature on reputation for SP had yet to fully integrate the cross-country nature of corporate SP in their theorizing (Acharya et al., 2022; Cooper et al., 2018; Gardberg et al., 2019; Zyglidopoulos, 2001, 2004). For example, while investigating the moderating influence of reputation for SP on the relationship between greenhouse gas emissions and firm value, Cooper et al. (2018) used a single-country context for the data and hypothesis development portions of their study. Gardberg et al. (2019) examined whether a corporation’s reputation for SP is affected by its philanthropic contributions. Nonetheless, both the data and the hypothesis development sections of this study focused on a corporation’s existence in a single country. Acharya et al. (2022) argued that a reputation for SP is important for socially considerate firms—without discussing whether such a reputation is judged only domestically or by international actors as well. Our study increases our understanding of the reputation for SP theory, showing that signals pertaining to MNEs’ reputation for SP are received by international stakeholders who judge MNEs and subsequently affect their acceptability in a cross-country context.

Third, we contribute to the non-market strategy literature by illustrating the importance of reputation for SP in an inter-organizational transactional context. The non-market strategy literature addresses how firms manage their activities in an institutional or societal context to improve their financial performance (Baron, 1995). Most studies in the non-market strategy literature have primarily drawn on one of five theories to explore the link between non-market strategy and positive organizational outcomes: institutional theory, stakeholder theory, resource dependence theory, resource-based theory, and agency theory (for a review, see Mellahi et al., 2016). Unfortunately, the literature largely focuses on the benefits (such as acceptability) a firm can receive from noncommercial organizations such as governments and social activists. Recently, scholars have begun showing a growing interest in how a nonmarket strategy may prove to be beneficial in commercial dealings with for-profit organizations. For example, Krishnamurti et al. (2019) showed that socially responsible acquirers experience numerous benefits during acquisitions: they pay lower premiums and earn significantly more positive abnormal returns than less socially responsible acquirers. Cho et al. (2021) showed that value creation for the shareholders of the target firm in an acquisition is positively affected by the target’s relative CSR performance (as compared with that of the acquirer), meaning that the higher the target’s relative CSR is, the more value is created in an acquisition deal for the shareholders of the target firm. Ma et al. (2020) found that non-state-owned enterprises in competitive markets are more likely to become M&A targets if their CSR disclosures are of high quality. Our timely contribution adds to this nascent literature by showing that an effective nonmarket strategy can help MNEs receive positive treatment from host country stakeholders in the form of a higher likelihood of CBAC.

Our study has several practical and policy implications. For acquirers, our study highlights the importance of investing in social issues. Managers of acquiring firms should note that their firms’ SP is essentially used as a reputation scale by host country and target stakeholders. Moreover, we suggest that acquirer managers further prioritize SP if they belong to a large firm. Target managers should try to diligently analyze the SP of acquirers, particularly if their firm is private. As highlighted by prior research, private firms are usually owned by families or a few partners (Draper & Paudyal, 2006). Therefore, decision makers in private firms should be cautious when scrutinizing an acquirer. For policy makers, our study notes that acquirers should be thoroughly evaluated based on their SP. Acquirers that have a poor record with respect to SP may not only transfer bad practices to their targets but also normalize such practices in the industry. Therefore, policy makers should be cautious of this issue, especially when dealing with large acquirers, since they have higher exploitation power. In addition, regulators tend to scrutinize deals that involve public targets more strictly. We caution regulators that deals involving private targets should also be given similar attention so that private firms do not fall prey to acquirers that aim to exploit private targets.

In this paper, we relied on Sustainalytics data to measure the SP of acquirers. While this approach increases the comparability of our study with the vast CSR literature built on the same data source, future studies could verify whether the relationship between SP and deal outcomes is positive if SP is measured with the questionnaire responses of target-firm managers and target country regulators. In addition, most deals in our sample represent full acquisitions and only about 8% of deals in our sample represent partial acquisitions. Thus, our sample does not allow us to examine the interesting phenomenon of the subsequent change in equity ownership in the partially acquired targets. Future studies may gather a large sample of partial acquisitions from all industries and examine whether the subsequent increase in equity ownership in the partially acquired targets is affected by the SP of the acquirers. Moreover, since our data consist of only about 12% public targets in our sample, we could not analyze the effect of target SP on the likelihood of deal completion. Future studies may gather a large data set of announced deals involving public acquirers and public targets and jointly examine the effect of acquirer SP and target SP on the likelihood of deal completion.

Overall, we showed that host country stakeholders judge an acquirer’s reputation based on its SP, and thus, acquirers with superior SP are more likely to reach deal completion. We further showed that this phenomenon is more pronounced for large acquirers and for those that buy public targets. We hope that this study inspires future research on the positive effects of SP in the context of cross-border acquisitions.

Footnotes

Appendix

Results of logistic regression with three additional control variables.

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Social performance × public target | 2.218*** (0.693) | 3.406** (1.555) | ||||

| Social performance × acquirer size | 0.787** (0.365) | 1.41* (0.721) | ||||

| Social performance | 0.823* (0.461) | 0.314 (0.556) | 0.012 (0.683) | –1.244 (1.281) | ||

| Public target | –3.685*** (0.842) | –3.748*** (0.862) | –4.249*** (1.151) | –3.809*** (1.043) | –4.994** (2.023) | |

| Acquirer size | –0.273 (0.29) | –0.306 (0.295) | –0.161 (0.268) | –0.381 (0.279) | –0.612* (0.34) | |

| Acquirer leverage ratio | –0.002 (0.472) | –0.009 (0.295) | 0.07 (0.285) | 0.065 (0.34) | 0.24 (0.313) | 0.312 (0.372) |

| Acquirer market-to-book ratio | –0.121 (0.079) | –0.128* (0.075) | –0.14** (0.069) | –0.088 (0.072) | –0.05 (0.073) | 0.15 (0.134) |

| Acquirer return on assets | 0.376 (0.479) | 0.205 (0.326) | 0.03 (0.326) | 0.153 (0.382) | 0.052 (0.408) | 0.393 (0.632) |

| International experience | –0.35 (0.312) | –0.208 (0.339) | –0.566 (0.442) | –0.446 (0.458) | –0.509 (0.501) | –0.353 (0.488) |

| Percent sought | –20.964*** (2.904) | –19.895*** (3.281) | –17.203*** (4.158) | –14.574*** (3.436) | –19.184*** (4.594) | –16.481*** (5.047) |

| Tender offer | –1.254 (1.07) | 0.776 (1.146) | 0.841 (1.005) | 1.728* (0.907) | 1.443 (1.101) | 4.848** (2.341) |

| Cash payment | 0.456 (0.597) | 1.391 (0.858) | 1.411 (0.871) | 1.657 (1.082) | 1.523 (1.09) | 2.102 (1.504) |

| Horizontal deal | 0.553 (0.603) | 0.682 (0.666) | 0.728 (0.648) | 0.671 (0.729) | 1.09 (0.715) | 0.995 (0.802) |

| Cultural distance | 1.068*** (0.382) | 1.166*** (0.44) | 1.249** (0.526) | 1.242** (0.487) | 1.339** (0.601) | 1.356** (0.599) |

| Institutional distance | 1.767** (0.839) | 1.714* (0.931) | 1.986** (0.991) | 2.435** (1.091) | 2.084* (1.088) | 2.684*** (1.023) |

| Intercept | 8.929*** (1.084) | 9.858*** (1.291) | 9.417*** (1.288) | 9.178*** (1.206) | 10.256*** (1.748) | 10.789*** (2.53) |

| Target country fixed effects | Yes | Yes | Yes | Yes | Yes | Yes |

| Target industry fixed effects | Yes | Yes | Yes | Yes | Yes | Yes |

| Year fixed effects | Yes | Yes | Yes | Yes | Yes | Yes |

| Number of observations | 554 | 554 | 554 | 554 | 554 | 554 |

| Pseudo R2 | 0.4756 | 0.6117 | 0.6379 | 0.6632 | 0.6799 | 0.7202 |

| Model likelihood ratio test | 95.45** | 126.09*** | 132.17*** | 138.14*** | 142.10*** | 151.78*** |

Note: The dependent variable, deal completion, takes a value of one for completed deals, and zero for abandoned deals. In this robustness test, we included three additional control variables for the acquirer: the leverage ratio, the market-to-book ratio, and return on assets.

p < .1. **p < .05. ***p < .01.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was funded by Kobe University under “Research Based International Cooperation Education Project” in 2020.