Abstract

Most previous studies examining M&As (mergers and acquisitions) have focused on the post-merger integration process. While there have been studies that have partially investigated the importance of deal completion, we argue that firms could learn to increase their deal completions by leveraging their experience from prior successful acquisitions and that their cumulative success could reduce the deal completion time; that is, the time from the announcement of the deal to its resolution. To address this unexplored issue about M&As, we investigated whether prior intra- and/or inter-industry acquisition experiences helped accelerate subsequent focal acquisitions in the semiconductor industry, which is characterized by rapid technological innovation. We tested our hypotheses on data consisting of 323 acquisition deals in the US semiconductor industry between 2000 and 2013. The results showed that both prior intra- and inter-industry acquisition experiences significantly reduced deal completion time.

Keywords

Introduction

Mergers and acquisitions (M&A) are a valuable strategic tool for acquiring technological knowledge that can drive innovations (Kale & Puranam, 2004). Most prior studies on technological M&As have focused on post-merger integration and performance (Puranam et al., 2009; Puranam & Srikanth, 2007). Some scholars have studied how the similarity of the technological knowledge held by both (or all) parties affects performance after an acquisition or merger (Makri et al., 2010; Sears & Hoetker, 2014). However, most of these studies have only examined post-merger integration and the performance of acquirers that have successfully completed acquisition deals. Although it is certainly interesting to study post-acquisition transaction performance, the actual deal process has thus far gone unexplored by M&A scholars, thus limiting their understanding of how deals are completed (Luypaert & De Maeseneire, 2015). While accounting quality plays an important role in the M&A deal process (Marquardt & Zur, 2015), it is still difficult to fully predict which factors affect the success of a deal from its announcement to its completion, and which focal variables from a firm’s previous industrial experiences can shorten the deal completion time.

While the existing literature has generated valuable insights into the M&A deal process and completion time, there has been a glaring lack of research into the effect of a firm’s previous experiences in similar and/or dissimilar industries on deal completion time. Studies investigating the relationship between prior experience and the completion of M&A deals (Collins et al., 2009; Muehlfeld et al., 2012) have determined that previous experiences reduce the occurrence of deal abandonment as well as completion time and failure rate. Since abandoning a deal during the public takeover stage incurs losses that, upon completion of the deal, might outweigh the benefits of post-merger M&A performance, reducing the M&A deal completion time is an important target. Dikova et al. (2010) have found that a higher institutional distance increases the deal completion time of an acquisition, while prior acquisition experience moderates this relationship.

Although prior studies have evaluated deal completion time from the perspectives of auditing (Chahine et al., 2018) and the financial reporting of the target (Skaife & Wangerin, 2013), there is still a need for research detailing why the time it takes for a company to acquire another company is important, as well as the antecedents that lead to reduced transaction completion time. For example, there has been a continuous pursuit of increasingly advanced technology in the semiconductor industry, where it is critical to quickly develop memory that is more than twice the size of an integrated circuit but that fits within the same area. As a result, leading semiconductor firms as incumbents in high-tech industries aim to acquire companies with knowledge similar to their own to develop innovative circuits that differ from existing ones (Makri et al., 2010; Ornaghi, 2009). It is particularly important to elucidate the factors affecting the completion of M&A transactions, as the completion accounts process can involve substantial increases or decreases in value. Therefore, it is crucial to confirm whether clear and suitable guidance is set out in the contract between the target and the bidder, and whether the completion accounts process is appropriately handled. Altogether, the smooth completion of an M&A transaction can make the difference between a good deal and a bad one (Doan et al., 2018).

Meanwhile, M&A deals in the high-tech industry work as a key driver for the rapid absorption of state-of-the-art knowledge in the field. Unlike other industries such as general manufacturing or service, high-tech firms can achieve reduced contract costs (e.g., negotiation, diligence, and financial record transfer) with a shortened deal completion time (Mchawrab, 2016). Furthermore, if uncertainty is inevitable in a company’s evaluation process, the ability to measure the value of the target remains the most important task when a firm is dealing with M&A in high-tech industries (Signori & Vismara, 2018). Although more extensive due diligence with a careful review is needed when a negotiation is in progress to overcome information asymmetry and uncertainty, such conscientiousness is likely to hamper the deal agreement and prolong the deal completion time of M&A in high-tech industries (Wangerin, 2019). However, if the target and the acquirer are within the same industry, the cost-information asymmetry can be reduced because they share similar understandings of the core skills and competencies required (Luypaert & De Maeseneire, 2015).

In this study, we aim to address the shortcomings of the existing literature. First, building on the prior research on M&A deal completion time, we examine the relationship between organizational learning and M&A deal completion time by categorizing prior acquisition experience into two types: depth and breadth of acquisition experience. We define depth of experience as an intra-industry acquisition experience and breadth of experience as an inter-industry acquisition experience (Muehlfeld et al., 2012). Second, we test the effects of intra-industry experience and inter-industry experience on deal completion time in a high-tech industry wherein the environment changes rapidly. Since high-tech firms in such industries have to keep changing their technological capabilities to adapt to environmental changes (Park & Roh, 2019), firms must continually refresh their knowledge to create a competitive advantage for M&A (Tsai, 2001). Thus, M&A is a distinctive vehicle through which firms can gain external knowledge (Park & Ghauri, 2011; Tsai & Wang, 2008), and which drives technological change (Harford, 2005). We tested our hypotheses using data on 323 acquisition deals involving 115 firms in the US semiconductor industry. Our finding suggests that in addition to depth of experience, breadth of experience is also essential in reducing the deal completion time of subsequent M&A deals in high-tech industries.

Our research makes several contributions. First, we investigated the effect of prior M&A experiences on deal completion time, which has been relatively under-examined in M&A literature; while there have been abundant studies on post-merger integration and performance, few studies have investigated intermediate M&A deal completion and deal completion time. Second, we made hypotheses regarding the relationship between learning from successful experiences and deal completion time by dividing learning into two categories: intra-industry and inter-industry learning. We first tested if prior intra-industry M&A successes decrease deal completion time. We also tested if prior inter-industry M&A successes strengthen the relationship between depth of experience and deal completion time in a highly dynamic environment. Finally, our setting is high-tech industries in general, with the focal industry being the semiconductor industry, which has yet to be examined in the previous literature measuring the effects of experience on deal completion time.

Literature review and hypothesis development

M&A deal completion time in a high-tech industry

The process of acquiring and merging can be divided into two stages: the decision-making phase and the integration phase (Dikova et al., 2010). Boone and Mulherin (2007) sub-divided the decision-making phase into two periods, defined by three events: The first stage is called the private takeover stage, wherein private initiation has begun but the firms have yet to make a public announcement. The public announcement marks the beginning of the second stage, which continues until the resolution, which is the beginning of the third stage, which involves the completion or abandonment of the deal.

During the private takeover period, the seller hires an investment banker to look for potential bidders (Boone & Mulherin, 2007). Then, the seller may negotiate with several potential bidders at this stage. Potential bidders typically sign a confidentiality contract requiring them to keep any private information to themselves. This private information is offered to potential bidders to allow them to carry out due diligence and examine the organizational and cultural fit between the acquirer and target (Stahl & Voigt, 2008).

The second stage following a public announcement is called the public takeover process. After an initial contract is signed between a seller and a buyer, it takes several more months before the resolution date at which the deal is completed or abandoned. During this phase, firms negotiate on more specific details, such as compliance with regulations (Zhang et al., 2011) and the implementation process (Reuer & Shen, 2004); information about the ongoing deal is open to investors and the market. In this study, we focus on the deal completion time, which is the period between the public announcement and the resolution date, at which point firms decide whether or not to complete the deal. Although many firms engage in further negotiations after an official announcement has been made to the public, many other firms fail to complete the deal. For example, among a total of 1,638 publicly announced US M&A deals from 2006 to 2008, about 15%–20% of deals ended up failing (Deloitte, 2013) after the public announcement.

With that said, does it matter if a transaction is canceled in the M&A deal process? Abandoning such a deal is considered to be a failure because the firms could not complete a merger or acquisition, which was their intermediate goal before the post-merger integration process or any post-merger developments. Furthermore, abandoning transactions and making extended deal decisions incur sizable costs. For example, an extended intermediary transaction stage forces a firm to divert its attention from other favorable merger/acquisition transactions or investment opportunities (Dikova et al., 2010). Meanwhile, simply resolving in advance any problems that could lead to abandonment of a transaction may not result in high costs. Nevertheless, most of the previous literature on M&A has emphasized either post-merger integration (Puranam et al., 2009) or post-merger performance (King et al., 2004; Wangerin, 2019). Because technology is rapidly changing in high-tech industries, there have been an increasing number of studies examining the relationship between completed deals and deal completion time, but studies investigating the post-merger period have disproportionately focused on the association between deal completion and ex-post performance (Luypaert & De Maeseneire, 2015). Thus, the intermediate goal of deal completion needs to be achieved before aiming for an ultimate goal; therefore, abandoning such a deal is similar to a loss of opportunity.

Completion of the deal seems to be a clear intermediate goal for firms involved in M&A deals. After abandoning deals, firms tend to suffer from a loss of motivation as well as high turnover (ten Brug & Rao Sahib, 2018). Obviously, investment banks are likely to push firms toward completing deals to receive their fees. The market reacts to the abandonment of deals by bringing negative returns to both the bidders and targets (Boone & Mulherin, 2007; Dikova et al., 2010).

Although it is essential to ensure that a deal is completed, it is also crucial to reduce the deal completion time to the extent possible. Meyer and Altenborg (2008) conducted a qualitative study examining the failure of the attempted merger between Telenor and Telia, two state-owned telecommunication corporations from Norway and Sweden, respectively; this merger failed after 9 months in the public takeover process. This extreme case of M&A failure incurred substantial costs. Moreover, even for acquirers who successfully complete a deal, it is essential to reduce the deal completion time as much as possible. This is because if the deal completion time is too long, the costs can outweigh the benefits of M&A performance. In addition, there have been a number of empirical studies investigating the deal completion time of recent M&As: Marquardt and Zur (2015) examined how the accounting quality of target firms affects the speed with which the deal reaches a final resolution as well as the likelihood that the proposed deal will eventually be completed. Luypaert and De Maeseneire (2015) showed how different acquirers, targets, and transactions affect the deal completion time. Chahine et al. (2018) investigated the effect of having a familiar auditor for both the acquirer and target firms in M&A transactions on the completion time of such transactions. Finally, Skaife and Wangerin (2013) found that deals involving more opaque targets are more likely to be terminated.

During the takeover process, many costs can be incurred because of the complexity of the deal process. To date, few studies have examined the complexities involved in the process of finalizing M&A deals after an initial contract has been signed (Reuer & Ariño, 2007). M&A deals are even more complicated than strategic alliances. The acquisition process consists of many complex sub-activities, such as financing, negotiation, and integration, thereby generating high costs. For example, contingent payouts represent one factor that makes firm acquisition highly complex (Reuer et al., 2004).

In 2014, Lenovo announced that it would acquire Motorola Mobility, which was owned by Google. Unlike processes that only involve scouting human resources, M&As require securing all the resources and capabilities of the acquired company, that is, its skills and core workforce (Mchawrab, 2016). Lenovo recorded the largest shipment in its industry in 2013 through its continuous innovations in the mature PC industry, which caused it to surpass its competitors and rise to the top spot. With this technology-based M&A experience, Lenovo is expected to become a threat in the short term, even in the smartphone market (Yu et al., 2019).

In high-tech industries, where technological change occurs quickly and uncertainty is high, knowledge and capabilities acquired from outside are equally important as internal R&D activities (Valentini, 2012), the latter of which take a long time because they are limited by a company’s resources and capabilities. If a company’s accumulated knowledge or competence is insufficient, it is very likely that commercialization will fail. However, although it is expensive to acquire core technologies or recruit outside experts, these can bring immediate benefits (Signori & Vismara, 2018). With a proven technology and workforce, a company’s potential for commercialization is high. Thus, many global high-tech companies are currently aiming to quickly acquire external knowledge and capabilities. In globally competitive high-tech industries, wherein knowledge is even more important than it is in other industries, companies are more keen to acquire outside knowledge (Bertrand & Zuniga, 2006; Ornaghi, 2009; Song et al., 2003). M&As at the corporate level involve the acquisition of not only intellectual assets, such as patents owned by the acquired company, but also secure R&D personnel with core capabilities.

Considering the complex process, amount of factors involved, and strategic aspects, a pre-investigation including target screening can be expected to take a minimum of 6 months, while a company’s M&A may take more than 3 years (Deloitte, 2014). In high-tech industries, the traditional rule of thumb regarding M&As does not apply; as a result, firms have taken riskier and faster decision-making approaches in recent years. For example, in 2012, Cisco acquired the UK-based software company NDS Group for US$5 billion to strengthen its competitiveness in the video communications sector, and Google aimed to own a valuable and useful patent (Toppenberg et al., 2015); Google eventually acquired Motorola Mobility. As mentioned earlier, Google then sold Motorola Mobility back to Lenovo, but retained most of Motorola Mobility’s patents (Gao et al., 2014). Both of these M&A transactions were completed in about 3 months. This is mostly consistent with the idea put forth by Luypaert and De Maeseneire (2015), that “information problems are reduced if target and bidder operate in the same industry” (p. 300). In other words, transactions between targets and bidders within high-tech industries likely have fewer problems caused by asymmetric information than such transactions in other industries.

When the contract negotiation process between a target and a bidder in a high-tech industry becomes more complex, the bidder is more likely to complete an M&A more quickly. Since the bidder has a valuable network including other professional experts, they may have already collected information about the target company (Russo & Perrini, 2006). The core competencies of the high-tech industry, such as the core workforce and patents that can respond to the rapidly changing technological environment, must be used in real time (Song et al., 2003). Suppose a bidder in a high-tech industry takes a long time to acquire a target company with the necessary technology. By the time the deal is complete, the target firm’s key personnel may have already moved to another competitor (Paruchuri et al., 2006). Therefore, shortening the deal completion time is essential in reducing the costs incurred during a public takeover period (Christensen et al., 2011). This leads to the question, what drives the decrease in deal completion time in high-tech industries?

M&A deal completion time and learning motivation

Competitive success and failure develop through organizational learning, which fundamentally stems from experience. Whether intentionally or unintentionally, organizations learn from direct experience. Such experience is obtained from learning by doing, which eventually affects the search routines of the firm (Levitt & March, 1988). An organizational routine is a repository of that organization’s capabilities, and organizations adopt new routines when they discover better ones. The historical success and failure experiences of an organization influences the pool’s richness and direction of an organizational search (Cassiman & Veugelers, 2006; Christensen et al., 2011; Lane et al., 2001).

Firms learn from prior acquisitions and then apply that knowledge to later strategic moves (Vermeulen & Barkema, 2001). In this way, future acquisition capabilities are developed based on prior experience. Experienced acquirers perform better in the integration process following the completion of an M&A deal completion (Puranam & Srikanth, 2007). Learning by codifying prior knowledge is a vital step in the integration stage for improving post-merger performance.

Knowledge articulation and the codification of accumulated prior experience allow firms to develop dynamic capabilities, which Teece et al. (1997) defined as “the subset of competence or capabilities which allow the firm to create new products and processes and respond to changing market circumstances.” Firms’ innovation capabilities are embedded within environmental contexts (Jansen et al., 2006). An organization’s role changes from preserving sustainable competitiveness to managing innovation and change as the environment becomes turbulent and ambiguous. In this vein, continuous innovation and product development, along with dynamic environmental change, become crucial drivers behind a firm’s growth. Regularly introducing new products is one way to turn turbulent times into opportunities.

Notably, external knowledge is complementary to internal knowledge in terms of improving innovation capability. High-tech firms frequently learn from external sources by acquiring firms with technological capabilities that will allow them to innovate (Hagedoorn & Duysters, 2002). Alex Mandl, the chief executive officer of Teligent and the previous number two at AT&T, once said, “M&A has been the single most important factor building up their market capitalization. The need for speed forces companies to acquire rather than build.” Firms acquire knowledge, resources, and companies to innovate, because doing so is much faster than building from scratch in a rapidly changing environment (Carey, 2000).

Firms learn from their acquisition experience how to innovate and how to successfully complete future deals. Prior experiences in domestic acquisition, foreign acquisition, and joint ventures increase the success of international acquisitions. In addition, prior experience within a host country is a stronger measure of subsequent success in international acquisition than prior experience in a non-host country (Collins et al., 2009). Firms can learn to complete M&A deals based on past successes and failures in specific contexts that are structurally similar (Muehlfeld et al., 2012). Furthermore, firms can learn from their prior experience how to achieve a lower deal completion time (Dikova et al., 2010).

Depth of prior M&A experience and deal completion time

The main logic regarding the relationship between successful M&A experience and deal completion time is depth experience. It is difficult for a company with experience only in uncomplicated situations to come up with an idea that can be directly applied in practice (Levinthal & March, 1993; Luypaert & De Maeseneire, 2015; March, 1991). However, according to the absorptive capacity perspective, uncomplicated experience with events, activities, and functions can still improve an organization’s ability to explore new knowledge to its advantage (Cohen & Levinthal, 1990; Park, 2010; Zahra & George, 2002). In terms of absorptive capacity, when dealing with complex knowledge resources, such as M&A in the semiconductor industry, the knowledge gained from previous acquisitions helps the acquiring company find, identify, understand, interpret, and evaluate the merits of any new knowledge (Muehlfeld et al., 2012). In addition, knowing more about how and when certain routines are effective can improve the ability of organizational members to transfer and convey knowledge between themselves (Karim & Mitchell, 2000). Thus, companies can benefit even more from the additional learning gained from participating in new transactions, even if they have already successfully completed a previous acquisition transaction in a similar domain (i.e., within the same industry).

By contrast, companies with fewer successful acquisitions than other companies may find it difficult to learn meaningful lessons if they act inappropriately in the pre-integration process for one of a number of reasons, thus leading to a prolonged negotiation (Doan et al., 2018). First, companies that lack successful M&A experience are less familiar with the pre-integration process and more likely to focus on exploring and processing new tasks, thereby limiting their ability to observe and extract any knowledge from the acquirer’s behavior (Dikova et al., 2010). Second, because they lack an adequate detailed knowledge structure to aid them in developing new knowledge, companies with a lack of successful M&A experience may overestimate or underestimate the importance and outcomes of acquisition transactions. Even if they do extract any meaningful lessons, there is still a concern that the restrictions of the existing knowledge structure may not be quickly resolved due to the fact that the previous knowledge base provides limited guidance on how to access, evaluate, and use knowledge from the target (Carnahan et al., 2010; Madsen & Desai, 2010; Muehlfeld et al., 2012). In other words, we believe that the knowledge gained from successful acquisitions enables firms to gain rich understandings of how to deal with various situations that may arise during the M&As process. Thus, a successful depth experience will help the decision-makers and members involved in the acquisition by giving them a greater understanding of the acquisition transaction in the pre-integration process, which will serve them in the future when acquiring a company with specifically similar characteristics.

Successful intra-industry acquisition experience is the primary source of learning for subsequent intra-industry acquisition (Muehlfeld et al., 2012), because two firms in the same industry are likely to be structurally similar. Furthermore, related acquisitions have substantially better financial outcomes than unrelated acquisitions (Arikan & Stulz, 2016), likely because of the increased ease of knowledge transfer and the better understanding between the acquiring and target firms. The overlap between the knowledge bases of the acquiring firm and the target firm heavily determines the outcome of a technological acquisition (Sears & Hoetker, 2014). Seeking knowledge from a similar context, also known as local search, facilitates additional technological capabilities (Park & Roh, 2019; Toby & Podolny, 1996). In addition, strategic fit and organizational fit, which are driven by the technical relatedness between two high-tech firms, play an important role in improving M&A performance (Hagedoorn & Duysters, 2002). In a similar sense, the ease of knowledge transfer and better understanding may also lead to reduced deal completion times among high-tech firms in the same industry. Hence, we hypothesize the following.

Hypothesis 1. Accumulated successful intra-industry M&A deal experience may shorten the subsequent deal completion time in the high-tech industry.

Breadth of prior M&A experience and deal completion time

Although essential learning stems from intra-industry acquisition, learning from only the intra-industry sector may lead to myopic learning (Lamin & Ramos, 2016). Inter-industry learning can protect firms from falling into learning myopia. Thus, firms need to prepare for future changes by acquiring technology in other sectors as well in uncertain environments.

Whereas the distance of knowledge was once considered a barrier to innovation, a cross-industry approach is beginning to be recognized as a source of innovation (Enkel & Gassmann, 2010). For example, general mechanical skills used in the machine-tool industry have come to be applied to different final products in a wide range of industries. This is because different industries were unwittingly relying on the same sets of skills to produce their desired outcomes. Due to deregulation, globalization, and fundamental breakthroughs that have been made in science and technology, industry boundaries are now more blurred than they ever have been (Park & Roh, 2019). Each high-tech industry can be a separate source of R&D spillovers and at the same time can be affected by R&D spillovers from other industries (Lamin & Ramos, 2016). For example, Apple first started as a manufacturing firm producing personal computers. However, Apple’s products have since diversified into iPods, iPhones, and related devices. Steve Jobs, Apple’s CEO, was initially reluctant to participate in any M&A because of technology spillover risks; he preferred in-house research and development. However, as its product lines diversified, Apple’s acquisitions rapidly became more diverse across different industries, such as satellite communications systems, computer software, internet service providers, semiconductors, flash memory, and displays.

Haleblian and Finkelstein (1999) first emphasized the role of heterogeneity in the learning experience. Focusing on the industry level of acquisitions, they showed that a prior acquisition experience within an industry will improve the performance of a later acquisition in a similar industry. They also suggest that a relatively inexperienced acquirer may improperly generalize an acquisition experience to all subsequent acquisitions, whereas a more experienced acquirer will understand the nuances distinguishing certain acquisitions from others. Barkema and Schijven (2008) argue that too much premature heterogeneity in the acquisition experience can hinder corporate learning in the early stages of competency building. However, even if the acquisition experience includes heterogeneity, successful experiences can still positively affect subsequent acquisitions. That is, companies require substantial organizational learning to acquire targets in heterogeneous industries, and such companies gain deep insight into contingencies after successfully completing an acquisition deal. Because there are significant information costs and risks associated with acquisitions in high-tech industries, companies with experience in acquisitions in heterogeneous industries are more likely to choose targets with signals that mitigate the risk of adverse choices (Wu & Reuer, in press). Therefore, diverse cross-industry acquisition experience may lead to decreased deal completion time. Thus, the next hypothesis was set.

Hypothesis 2. Accumulated successful inter-industry M&A deal experience will shorten the subsequent deal completion time in the high-tech industry.

Interaction of depth and breadth of prior M&A experience on deal completion time

Although the depth of a successful experience could shorten M&A deal completion time, that decrease may be affected by the breadth of successful experience. In other words, the assumption that successful intra-industry M&A experiences can reduce the deal completion time in the high-tech industry is expected to be strengthened when firms have more successful inter-industry M&A experiences.

In terms of organizational change, a pre-integrated understanding period that is shorter than before or compared to that of other bidders gives an advantage to organizations, as they can then spend less time and cost in subsequent focal deals (Angwin, 2004). This path dependence on reducing negotiation costs suggests that the acquirer’s behavioral latitude decreases over time. In addition, when a company creates configurations and functions for other new deals, its ability to make a significant difference in future deal capabilities may be limited, because it conflicts with the successful experiences from prior deals. This myopic learning assumes that, after a successful acquisition, companies have a limited ability to learn and anticipate feedback later in the process (Park & Ghauri, 2011). Therefore, success in an unfamiliar industry is required to overcome the path dependence caused by a successful deal that has already been completed in a similar industry. For example, Korea’s Samsung Electronics began M&A in 2013, starting with the semiconductor and LCD fields. Samsung Electronics acquired Novaled, a company that produces organic light-emitting diodes (OLEDs) from Germany; the price was US$347 million and the acquisition took about 2 years. With the development of IoT and predictions that the connected industry will be a leader in the 4th Industrial Revolution, Samsung Electronics was able to acquire LoopPay (a mobile payment service) and Harman (in the connected car electronics division) in just 4 and 3 months, respectively. Recently, Samsung Electronics completed an acquisition in 1 month by changing all its existing capital investment to 100% in Foodient, an AI-specialized startup connected to its existing partners (J. H. Kim et al., 2019). In other words, the competition regarding M&A in technology-based industries, including semiconductors, has reached the point that a company with sufficiently desirable technology can be taken over by incumbent companies with very little delay.

Since an inter-industry acquisition is more complicated than an intra-industry acquisition (Enkel & Gassmann, 2010), firms with more inter-industry acquisitions experience can achieve shorter deal completion times. Learning only from the depth of experience may cause firms to not know enough about the M&A deal procedure or about how to overcome problems arising in the negotiations during the period between the public announcement and the deal resolution. Based on the arguments above, we set the following hypothesis.

Hypothesis 3. Accumulated successful inter-industry M&A deal experience negatively moderates the relationship between accumulated successful intra-industry M&A deal experience and the subsequent deal completion time in the high-tech industry.

Research setting: semiconductor industry

Because of the high competition in high-technology industries, continuous innovation is vital for firms in such industries to grow (Makri et al., 2010). R&D investments account for more than 20% of revenues in semiconductor companies (McKinsey, 2011). As a result, whether a firm continues to innovate can even determine its survival. For example, American semiconductor firms abandoned the semiconductor memory industry in the 1980s because of the accelerated innovations of rival Japanese semiconductor firms (Tidd & Bessant, 2018). Technology is shifting the nature of competition even faster in the 21st century, thereby necessitating more relevant acquisitions than in the past (Puranam et al., 2009). Competition in a high-tech industry continually requires companies to participate in more mergers and acquisitions to gain technological knowledge. Since technology is changing rapidly, it is becoming increasingly difficult to predict what the industry will be like in a few years. To hedge against risk and prepare for the future, high-tech companies are buying firms that they expect could become the next hot business (Deloitte, 2013).

Another reason for increasing M&A in the semiconductor industry is the short product life cycle. Bollen (1999) noted that the cycle of the semiconductor memory chip “begins in a growth regime characterized by increasing demand, and switches stochastically to a decaying regime, in which demand generally falls.” Figure 1 shows the short life cycle of semiconductor memory chips. It only takes about 3 to 4 years to reach the peak of sales for a particular model of memory chip, followed by a dramatic decrease in demand. Before the demand for a memory chip reaches its peak, a new product is introduced to ensure the continued survival of the semiconductor firm. Each memory chip’s sales display a bell-shaped pattern, and overlaps can be seen with the bell shapes of subsequent products. “The ratio of the product life cycle to product-development time in semiconductors is half that for a mobile phone and a third that for an automobile” (McKinsey, 2011). The product development time of a memory chips is about 16.6 months.

Semiconductor supply history (Bollen, 1999).

The semiconductor industry is one in which M&A frequently occurs every year for knowledge-seeking purposes. Forty deals were closed in 2011, accounting for a cumulative deal value of US$25.1 billion in the United States alone (PriceWaterhouseCoopers, 2013). Acquisitions involving highly intense technological knowledge provide an opportunity for firms to innovate (Makri et al., 2010). The difficulty of developing advanced production capabilities alone is driving the ongoing M&A trend in the semiconductor industry: about 35% of technology-related acquirers named attaining specific product-related technology as their primary purpose for engaging in acquisitions, while 32% picked obtaining product innovation and engineering capabilities (Ranft & Lord, 2000).

The semiconductor industry has three essential characteristics. First, it is a high-tech industry where technological knowledge and innovation determine a firm’s growth and survival. Increasing innovative capacity and patenting is vital in the semiconductor industry. The need for continuous innovation leads to an increase in M&A deals, through which firms seek to gain high-tech knowledge. Second, driven by the rapid pace of environmental change, the semiconductor industry’s product-life cycle continues to shorten; thus, more rapid innovation is required in a given time than in slow-paced industries. Protecting recently developed technology is critical. The third characteristic is that high-tech industries are converging, so acquisitions occur both within the same industry and across different industries. All of these characteristics of M&A in the semiconductor industry make it a robust setting for our research aiming to determine the effect of prior intra-industry and inter-industry acquisition experience on deal completion time.

Method

Sample and data

The unit of analysis in the present study is how subsequent M&A activities by companies within the semiconductor industry affect the deal completion time. Several researchers have taken this approach when studying M&A activities within and between the industries to which companies belong. Because the intra-industry and inter-industry M&A approach requires the collection of massive amounts of detailed data, we randomly extracted 1,072 transactions of U.S.-based public companies in the M&A section provided by Securities Data Company (SDC) and Zephyr. The sample period for this study (2000–2013) covers a sufficient number of primary economic cycles, such as the US economy’s growth and recessions, thus increasing the possibility of generalizing the sample (i.e., the semiconductor industry). Since the economic downturn caused by the US financial crisis began in 2008 and lasted until mid-2009, the period was extended slightly, rather than ending the overall sample in 2009, to include M&As that may have occurred later. Among the samples, only transactions corresponding to 100% equity acquisition were sampled, as cases where an acquirer acquired only a partial stake in a target in the M&A deal were excluded, because too many exogenous variables could have affected the subsequent M&A deal for a partial equity acquisition. Of course, a partial acquisition might represent an opportunity for a semiconductor company to learn new things from heterogeneous experiences. Still, the acquirer learns more from a full acquisition than by participating in the target’s decision-making (e.g., the board of directors in minority ownership). In addition, the valid samples only consisted of those that were entirely transacted, since many M&A deals were abandoned or withdrawn in the middle of the deal process, including due diligence. Furthermore, deal completion plays a major role in this study, which uses propensity score matching as a statistical technique to weaken the selection bias of the sample (Chiu et al., in press).

Our sample is limited to deals for which the acquirer belongs to the semiconductor industry (four-digit SIC code 3674). According to Jiang et al. (2011) and Dikova et al. (2010), the semiconductor industry is an appropriate industry for elucidating how prior experiences within and across industries affect deal completion time. Second, since the semiconductor industry develops through the generation or absorption of cutting-edge knowledge, decision-making in deal participation is path-dependent, and it depends mainly on past experiences. M&A in the semiconductor industry has primarily been used as a strategic tool for creating completely new markets based on existing knowledge while focusing on creating the latest technology faster than competitors can.

This criterion is important, since our research focuses on the fact that the deal completion time of subsequent M&A can be influenced by the prior inter-industry experience of semiconductor companies. Our hypotheses were tested on data from 323 acquisition deals by 115 firms in the US semiconductor industry from 2000 to 2013. The dataset was based on the most recent information about M&A deals available from Zephyr. There were 1,100 deals in the US semiconductor industry from 2000 to 2013. Among these 1100 deals, 1072 were publicly announced. After excluding companies without information on payment, such as cash and stock buyback, 752 deals remained. Removing the deals without information about the size of the target or the acquirer, we deemed 323 deals to be appropriate for our test. Therefore, we ultimately used a sample of 323 deals, which included information on important control variables. Details on the definitions and measurements of all variables are presented in Appendix 1.

Dependent variable

We measured the dependent variable, deal completion time, by calculating the number of days starting from the public announcement of the focal subsequent M&A deal to the resolution date on which firms decided whether or not to complete the deal. This measurement is consistent with that used in prior studies (Dikova et al., 2010). This period is the one at which most crucial issues involving M&A are resolved. We did not include deals announced in 2014, but we did include deals that were completed in 2014.

Independent variables

Consistent with prior research into the M&A experience (Sears & Hoetker, 2014), we measured experience as accumulated prior experience before the focal transaction. Following existing studies (Muehlfeld et al., 2012), this study considers a moving window of 3 years before the focal transaction to measure a firm’s successful deals (i.e., completed deals). Our sample shows significant clustering of M&A in a short time. During that period, 67.6% of companies finished all M&As within 3 years after the announcement. Only 32.4% of companies took more than 3 years between their previous M&A and their most recent M&A. In addition, there were no companies with an M&A period exceeding 5 years; that is, there were no long-term deals. Only prior acquisitions that were successful were counted, because the effect of prior acquisitions that had failed showed an inverted U shape on deal completion (Muehlfeld et al., 2012), and our model only considered positive relationships between prior successful M&A experience and deal completion time.

Then, we separated prior successful M&A experiences into intra- and inter-industry experiences (Muehlfeld et al., 2012; Park & Roh, 2019). An experience was counted as intra-industry if both the acquirer and the target had an SIC code of 3674 (semiconductor industry), which implied that the focal deal occurred within the semiconductor industry. Meanwhile, the experience was counted as inter-industry if the acquirer had an SIC code of 3674 and the target firm had any other code.

Control variables

Our control variables were drawn from prior research on pre-M&A deal completion processes and prior acquisition experience (Collins et al., 2009). Cash payment could affect deal completion time, because payment methods have different effects on negotiation during the process (Faccio & Masulis, 2005; Luypaert & De Maeseneire, 2015; Muehlfeld et al., 2012). Cash was coded as 1, and other payment methods, such as stock, debt, and stock and debt combined, were coded as 0. Relative size was measured as the ratio of the target size to the acquirer’s size, with each party’s size measured in terms of the number of employees. Relative size is an important variable in M&A, because the size of each negotiation party represents its relative power (Ahuja & Katila, 2001; Park & Roh, 2019). Relative size was measured as a logarithm. Deal size could also affect the deal completion time, because a larger deal size might shorten the deal completion time (Y. Kim & Roh, 2014; Luypaert & De Maeseneire, 2015). Conversely, a larger deal size might lengthen the deal completion time due to the long negotiation period. Deal size was measured as the logarithm of the deal value, because it has a substantial standard deviation. The related deal was coded as 1 when the target was an industry related to the semiconductor industry, and it was coded as 0 when it was diversifying (i.e., 36 based on the two-digit SIC; Wangerin, 2019). Target experience was controlled, because the acquirer’s experience and the target’s experience might both have learning effects on the deal completion time. Target experience was measured as the target’s total successful experience until the focal deal, regardless of whether that experience was intra-industry or inter-industry (Muehlfeld et al., 2012). The target’s age and the acquirer’s age were calculated by subtracting the incorporation year from the year when the focal deal was completed (Luypaert & De Maeseneire, 2015; Muehlfeld et al., 2012). The target and acquirer’s advisory analysts were measured by the number of analysts participating in each of the corresponding parties. The tender offer was defined as 1 if the transaction corresponded to a tender offer and 0 otherwise (Marquardt & Zur, 2015; Muehlfeld et al., 2012). The bidder was measured as the number of companies participating in the acquisition of the target (Luypaert & De Maeseneire, 2015). Finally, the average number of companies participating in each deal was 2, and up to 4 companies participated in the bidding for each company.

Estimation techniques

To test our hypotheses, we used ordinary least-squares (OLS) linear regression analysis, because our data consisted of two variables: the first was prior experience, the independent variable, which was measured by the number of acquisitions completed by the acquirer prior to the focal deal, and the second was deal completion time, the dependent variable, which was measured by the number of days from the public announcement date to the deal completion date. The individual effects of explanatory variables may be less precise when there is a correlation between explanatory variables.

Since our main analysis will only validate companies that have done subsequent M&As, there is a risk of selection bias, because subsequent M&As may not be randomly determined, except for a sample of non-subsequent M&As (i.e., sole M&A during the sample period). We tried to implement a two-stage Heckman model to correct for non-randomly selected M&A transactions. During the sampling period, we pooled and matched companies that did subsequent M&As with companies having similar characteristics that only did a single M&A. We used the nearest-neighbor matching method and collected propensity score matching samples for enterprises (Bae et al., 2020). After matching, the t-test result showed that no other counts except for deal size were significant at the 0.05 level, thus indicating a successful matching process.

Heckman’s two-step procedure (Heckman, 1979) corrects for possible sample-selection bias in model specification. Our samples include information only on the deal completion time of the deals that have been completed. Suppose that the decision to complete the deal was not exogenous, but was instead slightly correlated with the completion time’s residuals. In that case, estimates for the completion time may suffer from a sample-selection bias. To remove this possible bias, we controlled for the effect of cash payment, relative size, deal size, and deal type, all of which can influence the deal completion in the first stage of the model. The payment method can affect the deal completion because different payment methods can give different signals to the target. Furthermore, relative size, as measured by the number of employees of the target divided by that of the acquirer, can decrease the deal completion time, because a larger relative size implies the existence of more pressure on the target. In addition, a larger deal size implies that more resources are involved, thus increasing the complexity of the deal. The related industry (Related) was coded as 1 if it was an intra-industry acquisition and coded as 0 otherwise. Different deal types can have different completion rates because of the different structures. In the second stage of the model, we controlled for cash payment, relative size, deal size, the target’s experience, the target’s age, and the acquirer’s age.

Furthermore, we compared the results derived by means of the Hackman selection model with the results of linear regression (OLS) and Poisson count regression, since additional analysis is needed for robustness according to the existing literature (Luypaert & De Maeseneire, 2015). In Heckman’s two-step model, 220 completed deals were identified out of a total of 323 M&A attempts. The proposed hypotheses were again verified through OLS and Poisson count regression using these 220 completed M&As.

Results and discussion

Table 1 lists the descriptive statistics, correlations, and VIF (variance inflation factor) for the overall sample. The average deal completion time was 125 days. The standard deviation of the deal completion time was large, meaning some deals took a long time to complete. The longest deal completion time in our sample was 1,600 days. The VIF for each variable was less than 4, which was below the cutoff point of 10 (Hair et al., 1998) .

Descriptive statistics and correlations.

Note: * p < 0.05 Two-tailed tests, anatural logarithm, Related = intra industry-related offer (at two-digit SIC level), ACQ_EXP = acquirer’s total success M&A experience, TAR_AGE = target age, TAR_Advisors = number of target’s advisory analyst, ACQ_Advisors = number of acquirer’s advisory analyst, INTER = inter-industry experience, INTRA = intra-industry experience

Table 2 presents the main model and the selection model, because we used Heckman’s two-step model to adjust for the effect of possible selection bias. The coefficients of cash payment (

Results of regressions for deal completion time.

Related = intra industry-related offer (at two-digit SIC level); ACQ_EXP = acquiror’s total successful M&A experience; TAR_AGE = target age; TAR_Advisors = number of target’s advisory analysts; ACQ_Advisors = number of acquiror’s advisory analysts; INTER = inter-industry experience; INTRA = intra-industry experience.

Natural logarithm; t statistics in parentheses.

p < .05, **p < .01, ***p < .001.

With all the control variables inserted, Model 1 shows that the coefficient of successful intra-industry experience is significant (

After the two independent variables were mean-centered, the effect of the interaction on the dependent variable was verified. The interaction term’s coefficient between intra-industry and inter-industry acquisition experience is negative and significant (

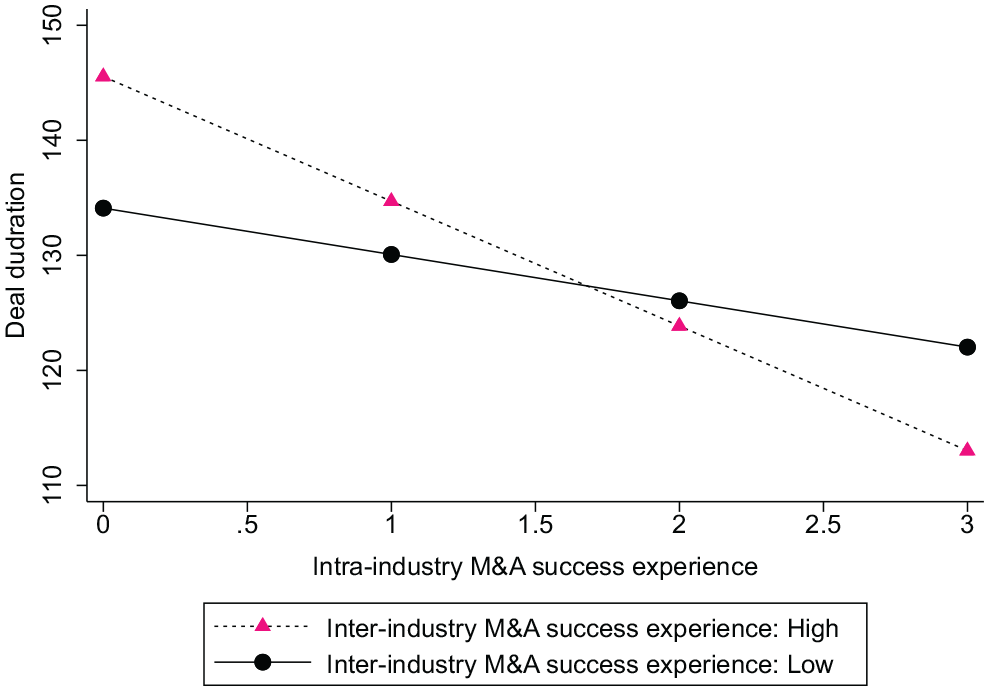

Figure 2 illustrates the interaction effects on the deal completion time for two levels of experience: low is one standard deviation below the mean, and high is one standard deviation above the mean. We graphically display the deal completion time on different levels of intra-industry and inter-industry acquisition experience. As shown in the figure, the deal completion time is lowest when there are high numbers of successful experiences with both intra-industry and inter-industry acquisitions. The results suggest that the completion time is longest when successful intra-industry acquisition experience is low or when successful inter-industry acquisition experience is high. This implies that a successful intra-industry acquisition experience is crucial in completing the subsequent focal M&A deal, although prior successful inter-industry acquisition experience may help.

Interaction between effects of successful intra-industry and inter-industry acquisition experiences on deal completion time.

The endogeneity issue can be raised because there could be an unobserved variable (i.e., omitted variable). We acknowledge that this might lead to issues regarding robustness. For an additional endogeneity test, we used a control function (CF) approach. This method regresses the endogenous regressor into the instrument in the first-stage equation, so they are input as control variables in the first equation. We found an empirical study showing that this often occurs when acquiring a company’s subsidiary while searching for a variable involving the possibility of using managerial overconfidence as a proxy (Liu et al., 2009). Accordingly, the existence of a subsidiary was selected as an instrumental variable. In other words, when the target company is a subsidiary, the exogenous effect of the intra- and inter-industry M&A experience on the deal completion time was tested. Following Dikova et al. (2010), we coded this as 1 when the target company was a subsidiary and as 0 when it was not. The CF approach indicated that the coefficient for the omitted variable (i.e., target subsidiary) was positively significant (p < .05, Chi-square statistic = 76.36), suggesting that both inter- and intra-industrial M&A experiences have excellent predictive power.

Conclusion

Our finding helps elucidate the relationship between experience and deal completion time. Focusing on intra-industry and inter-industry experience, we suspect the hypotheses suggest that every experience is vital in reducing the deal completion time, whether the focal deal is an intra-industry or inter-industry transaction. There is also an interaction effect, which differs substantially from the finding presented by Muehlfeld et al. (2012). They argued that only intra-industry experience is valuable in completing intra-industry deals, and that only inter-industry experience is important in completing inter-industry deals. However, we find that both types of experience reduce the deal completion time, regardless of whether or not the subsequent deal is an intra-industry acquisition. We assume that this difference results from our testing in different industry contexts. Not only is depth of experience remarkably important, but breadth of experience is also crucial for a successful M&A deal in a high-tech industry.

Our theoretical contribution to the M&A literature is that, based on organizational learning theory, learning mechanisms play a central role in reducing the completion time of an M&A deal in a high-tech industry. Although previous studies on M&A focused on deal completion, M&A performance, and post-merger integration, the question of how to reduce the deal completion time and why it matters has been neglected. Being able to quickly complete a deal, that is, having a short time between the public announcement and the deal resolution, is becoming increasingly important in high-tech industries in which the dominant knowledge is changing rapidly and the opportunity cost for deal abandonment is high. In this context, Muehlfeld et al. (2012) argued that firms that could learn from previous successful M&A experiences in the specific context could achieve decreased deal completion times. In particular, as highlighted by Sears and Hoetker (2014), an M&A deal in a high-tech industry requires sophisticated technology expertise; a mix of both broad and deep experiences may allow a firm to accelerate the deal completion time by facing fewer conflicts during the negotiation. In other words, through successful completion of the M&A, acquirers in a high-tech industry can have a chance to understand the process of contractual negotiation and learn about exclusive information (e.g., patents and R&D). Thus, by extending existing M&A deal completion literature by recognizing the importance of the deal completion time, we suggest that depth and breadth experiences in M&As enlarge the learning reservoir, and that if such rich experiences are accumulated, the completion time of the subsequent deal will be curtailed.

Our findings have practical implications for decision-makers who may be interested in acquisitions in a high-tech industry. First, prior experiences by managers can influence the deal completion and the deal completion time. If a firm has prior experience in a hostile acquisition, it may show similar behavior in a future acquisition. In addition, if a CEO is facing reappointment, that CEO might engage in more aggressive M&A to show good performance to shareholders, thereby reducing the deal completion time. The incentive system for a CEO, such as offering a cash bonus after an M&A completion, induces CEOs to engage in more M&A deals and work harder to complete deals (Carey, 2000). Second, while comparing the costs incurred during the deal completion time and the benefits of M&A completion, a firm’s decision-maker should try to codify the knowledge gained from both intra-industry and inter-industry acquisition experiences. Knowledge gained from both the negotiating process and the future planning process between the target and acquirer can be leveraged to reduce the deal completion time of subsequent M&A deals. Efforts taken by managers to understand the key success factors in completing M&A deals may also help reduce the subsequent deal completion time (Reuer & Ariño, 2007; Reuer et al., 2004; Sears & Hoetker, 2014). Their role is to deliver the knowledge gained from the variety of prior experiences to their employees so they can make more effective and efficient strategic moves in the future.

Along with offering these valuable findings, this study has the following limitations. First, our observation is limited to the period after a public announcement has been made. Although this pre-merger stage is important, the period before the announcement has been underexamined; it would be meaningful to figure out why some firms delay announcing their plans publicly. Since some firms may question whether they have selected the right target firm, the period between the private announcement and the public announcement can take some time. However, after a long search for a target, every deal procedure can be expected to go smoothly, and the deal completion time may decrease as a result. Alternatively, the firm might also suffer during the period between the public announcement and the resolution date. Altogether, this relationship between the first stage and the second stage should be further investigated.

Second, our attention in this study has been on the experiences of the acquirer in the M&A deal. We used target experience as a control variable, and its effect on the deal completion time was found to be statistically significant. Previous studies have only emphasized the role of the acquirer, not that of the target. There has been relatively little research into the target. Building upon the relationship between the target and acquirer, the findings regarding relative size have fruitful implications. The relative knowledge between the target and acquirer can also affect the deal completion time and the post-merger performance, because M&A involves interactive communication, not a one-way order from a specific party. Therefore, more attention should be paid to the target in M&A research.

Footnotes

Appendix

Definitions of variables.

| Variable | Definition |

|---|---|

| Deal completion time | The number of days between the public announcement of the focal subsequent M&A deal and the resolution |

| Cash payment | A binary variable equal to 1 if the acquiring firm paid for the deal with cash and equal to 0 otherwise |

| Relative size | The ratio of the target size to the acquirer’s size when each party’s size is measured as the number of employees |

| Deal size | The deal size was measured as the logarithm of the deal value |

| Related | A binary variable equal to 1 if the target was in an industry related to the semiconductor industry and equal to 0 otherwise |

| TAR_EXP | The target firm’s accumulative prior experience until the focal transaction |

| TAR_AGE | The target firm’s age, calculated by subtracting the incorporation year from the year when the focal deal was completed |

| ACQ_AGE | The acquiring firm’s age, calculated by subtracting the incorporation year from the year when the focal deal was completed |

| INTRA | Intra-industry experience was counted if both the acquiring and target firms had an SIC code of 3674 |

| INTER | Inter-industry experience was counted if the acquiring firm had an SIC code of 3674 (semiconductor industry) and the target firm had any other code besides 3674 |

| TAR_Advisors | The number of the target firm’s advisory analysts |

| ACQ_Advisors | The number of the acquiring firm’s advisory analysts |

| Tender | A binary variable equal to 1 if the deal was a tender offer by the SDC and equal to 0 otherwise |

| Bidder | The number of bidders participating in the focal deal |

Authors’ note

Early version of this paper was presented at 2014 INFORMS and 2015 AoM conferences.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by Hankuk University of Foreign Studies and Soonchunhyang University