Abstract

Motivated by the resource-based view (RBV) of the firm, this study explores whether mergers and acquisitions (M&As) can facilitate or impede a firm’s marketing capabilities. Furthermore, this study also examines whether the influence of M&As on a firm’s marketing capabilities is conditional to the type of deals, that is, domestic versus cross-border acquisitions. Using the difference-in-differences research design with a large sample of 15,509 firm-year observations for 898 US public acquirers, this study tests the postacquisition changes in a firm’s marketing capabilities as reflected in the sensitivity of sales revenue to marketing-related expenditure. The results of the empirical tests show a postacquisition increase in sales sensitivity, suggesting that firms can enhance their marketing capabilities through M&As. However, it is also found that the enhancement in marketing capabilities is limited to domestic M&As and disappears for cross-border acquisitions. This result suggests that more salient differences in a firm’s marketing environment attributable to cross-border acquisitions may disrupt a firm’s marketing capabilities and dampen the positive effect of M&As.

Introduction

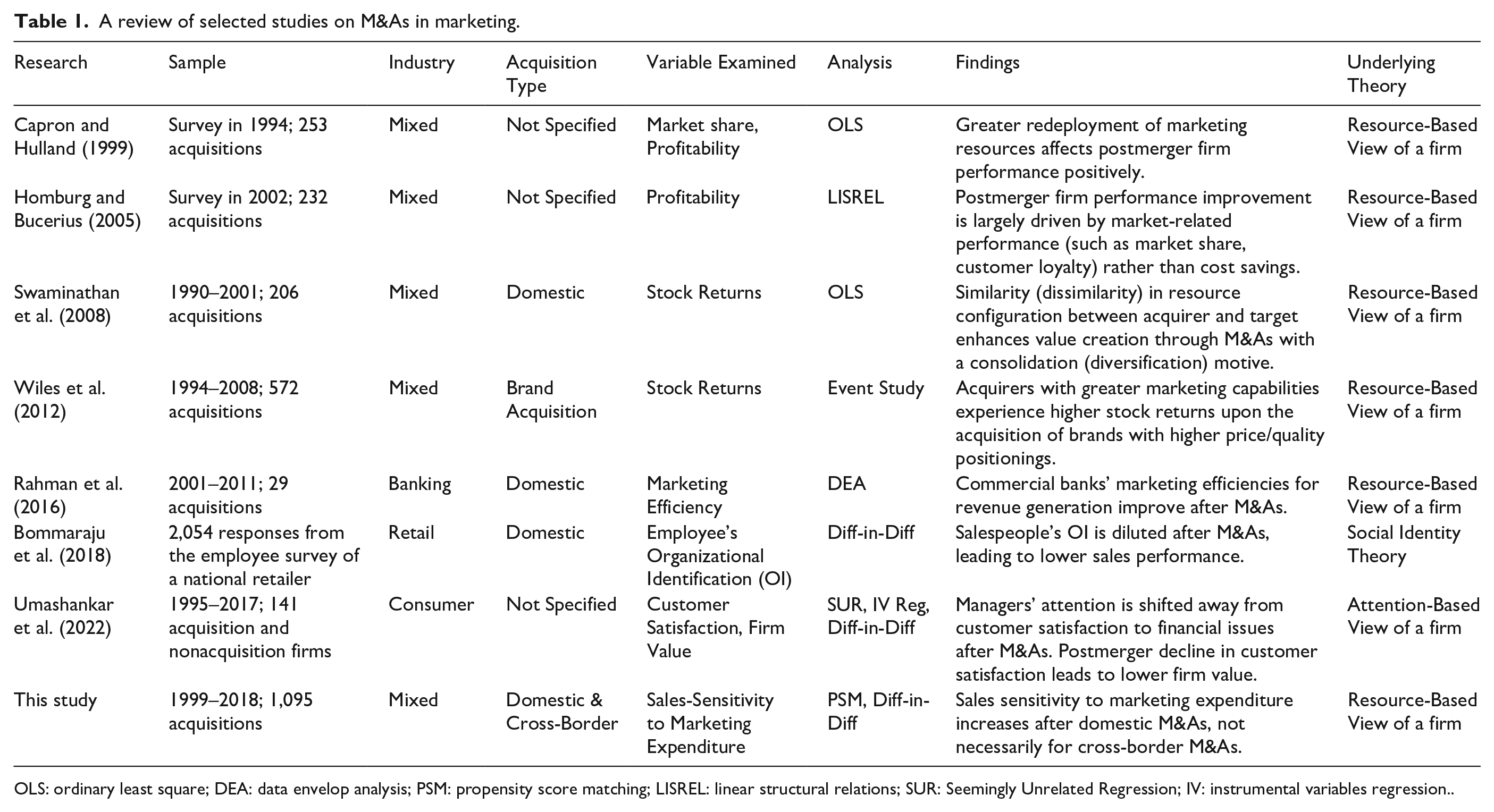

The need for adaptation to a constantly changing business environment calls on a firm’s timely acquisition of organizational assets and capabilities to remain competitive in the market. Organizations commonly fill their resource demands by acquiring function-specific resources either through domestic or cross-border acquisitions (Capron & Hulland, 1999; Haapanen et al., 2019). Motivated by the resource-based view (RBV) of a firm, emphasizing the strategic role of firm resources and capabilities for sustainable competitive advantage, a stream of prior studies has examined whether mergers and acquisitions (M&As) enable the augmentation of a firm’s marketing capabilities, improving its marketing performance and overall firm performance (for a summary, see Table 1). However, the inferences from these prior studies are somewhat mixed, and whether M&As can improve a firm’s marketing performance remains an open, empirical question. In this article, we provide large-sample evidence on the effect of M&As on a firm’s marketing capabilities and propose a contingency explanation for the relationship by considering domestic and cross-border acquisitions separately.

A review of selected studies on M&As in marketing.

OLS: ordinary least square; DEA: data envelop analysis; PSM: propensity score matching; LISREL: linear structural relations; SUR: Seemingly Unrelated Regression; IV: instrumental variables regression..

Marketing capabilities are of high strategic importance (Day, 2011); thus, strategic management and marketing scholars have examined the influence of M&As on marketing capabilities by focusing on overall firm performance (Capron & Hulland, 1999; Day, 2011; Haapanen et al., 2019; Homburg & Bucerius, 2005). While M&As are intended to improve firm performance by integrating and reconfiguring two firms’ resources and capabilities, including marketing capabilities, Kroon et al. (2022) asserted that different functional units aim to achieve different levels of post-M&A integration. Through their in-depth case study of KLM and Air France acquisition integration, Kroon et al. (2022) showed that operational units (such as international sales offices and the cargo division) demonstrate the highest level of intended integration, whereas human resource and marketing units show minimal integration, that is, “one group, two airlines” instead of “one airline.” If so, the effect of M&As on marketing capabilities can be materialized in a different tempo from other functions, which means that the changes in aggregate firm performance may not properly articulate the M&A effect on marketing capabilities. Therefore, instead of using overall firm performance as an aggregate measure of the M&A effect, we examine the post-M&A changes in sales sensitivity to marketing activities as an alternative approach to capturing the effect of M&As on marketing capabilities more directly. Furthermore, given that sparse attention has been paid to the utility of marketing capabilities across different organizational or geographical contexts of the organization, we test whether domestic and cross-border M&As have a different impact on an acquirer’s post-M&A marketing capabilities.

To empirically examine the impact of M&As on a firm’s marketing capabilities, we use a large sample of 15,509 firm-year observations incorporating 898 US public firms engaged with acquisition activities and their matched control firms. To measure a firm’s marketing capabilities, prior studies have often relied on stochastic frontier estimation, such as data envelop analysis (DEA), that cross-sectionally calibrates how well a set of market resources (such as advertising expenditure, selling expenses, brand equity, and trademarks) is transformed into a desired marketing outcome (see, e.g., Dutta et al., 1999; Nath et al., 2010; Rahman et al., 2016). However, this approach cannot be applied to our setting of M&As because the functional form of a firm’s stochastic frontier production would be inconsistent between the pre- and post-acquisition periods (Lieberman & Dhawan, 2005). To circumvent this limitation, we adopt the sensitivity of sales revenue to marketing-related expenditure as an alternative “input–output” measure reflecting a firm’s marketing capabilities.

With this estimation approach for marketing capabilities, we apply a difference-in-differences (DiD) research design with propensity-score-matched nonacquisition control firms and examine whether the sales sensitivity is changed after an acquisition, signaling the effect of acquisitions on marketing capabilities. Furthermore, we test whether the relationship is conditional on the type of acquisitions, that is, domestic versus cross-border deals. We find that firms’ sales sensitivity is improved after the acquisitions, which is in line with the notion that acquiring firms can create value through the extension, recombination, and redeployment of marketing capabilities. In addition, we find that this value-creation effect of marketing capabilities is diminished when the acquisition target firms are from a foreign country, suggesting that marketing capabilities are specialized and context-specific.

The remainder of this paper is organized into five sections. Section 2 explores the background literature related to the marketing capabilities of firms. In Section 3, we describe our hypotheses, positing the effect of acquisitions on the performance of marketing capabilities and teasing out the effects of domestic versus cross-border acquisitions on measures of marketing capabilities. Section 4 outlines our sample and describes the empirical model estimated in this study. After reporting the results of our analysis in Section 5, we conclude with a discussion of the results and suggestions for future research in Section 6.

Conceptual background

The resource-based view (RBV) and marketing capabilities

The RBV of a firm argues that resources and capabilities are the sources of a firm’s strategic competitiveness and superior performance (Barney, 1991; Grant, 1991). RBV depicts that firms are a bundle of tangible or intangible resources (Amit & Schoemaker, 1993; Wernerfelt, 1984). Managerial discretion in resource accumulation and deployment can result in differentiated economic value creation from accumulated resources (Amit & Schoemaker, 1993). In accumulating resources and deploying them, firms gradually develop organizational processes called capabilities (Teece et al., 1997). These capabilities are often the source of a firm’s sustained competitiveness and growth. Firms that are endowed with superior resources and the corresponding organizational processes in the form of capabilities are economically more efficient and fulfill customer needs more cost-effectively (Peteraf, 1993), thus creating greater value from the resources and capabilities.

Consistent with the notion of capabilities as a source of strategic competitiveness, marketing capabilities are recognized as necessary and consequential to a firm’s performance (Day, 1994; Srivastava et al., 2001; Wiles et al., 2012). Nath et al. (2010) defined marketing capabilities as “the integrative process, in which a firm uses its tangible and intangible resources to understand complex consumer-specific needs, achieve product differentiation relative to the competition, and achieve superior brand equity” (p. 319). These capabilities are typically developed via learning processes when the firm’s employees repeatedly apply their knowledge to solving the firm’s marketing problems (Day, 1994; Grant, 1991; Morgan, 2012). Considering that these capabilities enable a firm to bundle its marketing resources and communication channels more efficiently to create customer value in a way other competitors cannot easily imitate, an extensive line of marketing research (e.g., Capron & Hulland, 1999; Fahy & Smithee, 1999; Kull et al., 2016) has applied RBV to connect a firm’s marketing functions and marketing capabilities to an improvement in firm performance (Nath et al., 2010; Song et al., 2007).

Notably, RBV characterizes such strategic capabilities as path-dependent processes, specific and subject to maturation in which these characteristics restrict their imitation (Vicente-Lorente, 2001). Because marketing capabilities are relational, procedural, and context-specific in nature (Srivastava et al., 2001), their transferability can be significantly limited. In other words, capabilities involve intricate coordinated skills and knowledge that are embedded within organizational routines over time (Morgan, 2012), which leads to marketing capabilities remaining a static and context-specific resource. The limitation on transferability is dependent on the firm’s ability to recognize the value of the capability and the ability of the recipient to assimilate the transferred capabilities (Lane & Lubatkin, 1998). The transferability of these marketing capabilities gains importance in the context of the organization’s merger(s) and acquisition(s).

M&As and marketing capabilities

M&As represent one of the most popular strategies employed by organizations to acquire new resources and capabilities (Capron & Hulland, 1999; Haapanen et al., 2019). These newly acquired resources and capabilities by themselves, or in combination with existing resources and capabilities, enable a firm’s superior performance (Morgan, 2012; Vorhies & Morgan, 2005). From a theoretical point of view, M&As can exert two potentially contradicting effects on a firm’s marketing capabilities.

On one hand, Rahman and Lambkin (2015) suggested that M&As can lead to enhanced marketing capabilities by leveraging the economies of scope associated with an increased “market coverage” and expanded “product portfolio” after an acquisition. Furthermore, the benefits of scale economies may accrue to an acquiring firm by reducing selling, general administration, and marketing costs per unit. In line with this view, Capron and Hulland (1999, p. 41) argued that M&As can be a means to obtain “new marketing resources, such as brands and or sales forces, that firms find difficult to develop internally and are unable to buy as discrete entities in the external market,” which can be seamlessly integrated, resulting in the cost-effectiveness/efficiency of marketing functions (Homburg & Bucerius, 2005).

On the other hand, the disruptions in organizational processes and the operating environment arising from M&As can impede an efficient deployment of marketing resources and thereby hamper a firm’s marketing capabilities. Essentially, marketing capabilities are a process-oriented construct related to defining, developing, and communicating customer values through an efficient composition of a firm’s marketing resources (Day, 1994; Morgan et al., 2018). To the extent that marketing capabilities are embedded in a firm’s organizational fabric, the reconfiguration and redeployment of marketing capabilities for the combined post-M&A organization would entail greater uncertainties associated with the enigmatic integration process. In particular, the integration of marketing capabilities will depend on the level of the transfusion of knowledge resources between the acquirer and the target firm (Cording et al., 2008; Paruchuri et al., 2006). Therefore, taking these together, these conflicting theoretical conjectures warrant an empirical investigation of dynamic marketing capabilities.

Hypothesis development

Extending marketing capabilities

A significant body of prior marketing studies has attempted to understand how marketing capabilities create value for a firm (e.g., Evanschitzky, 2007; Song et al., 2007; Vorhies & Morgan, 2005). Firms aspire to grow and create value, which is often associated with the redeployment of resources and the reconfiguration of their use (Farjoun, 1994; Ng, 2007). Therefore, firms often turn to M&As to gain access to valuable and unique resources not available in the marketplace (Swaminathan et al., 2008).

The effects of M&As on a firm’s marketing capabilities may operate through the following two channels. First, through M&A deals, firms can access firm-specific tangible and intangible resources from the target firm, which can be utilized to create synergistic marketing gains. These gains may accrue either through the postacquisition integration, reconfiguration, or redeployments of existing marketing resources. Marketing assets and resources, such as brands, sales force, and marketing expertise, are commonly redeployed and integrated between target and acquiring firms and often redeployed together (Capron & Hulland, 1999). Furthermore, the transfusion of marketing knowledge between acquirer and target firms can breed more creative ideas, which ultimately improves their marketing capabilities. Thus, the ability to exploit such transferred marketing knowledge can become a source of competitive advantage (Schlegelmilch & Chini, 2003).

Second, firms may also achieve gains through the scale economies of a combined firm. In other words, greater economies of scale can increase costs savings and profit margins. Improved economies of scale can be a result of utilizing an acquired company’s resources and capabilities to improve or expand the acquiring firm’s capabilities (Walter & Barney, 1990). It can also be due to the utilization of the acquired company’s personnel, skills, or technology (Walter & Barney, 1990). Thus, the postacquisition integration of marketing resources and the relevant marketing operations may result in cost savings and, in turn, improve the financial performance of the firm (Homburg & Bucerius, 2005).

Taken together, the synergies that may arise from the access to new marketing capabilities and enhanced operational efficiencies are expected to improve the postacquisition performance of marketing capabilities. To test this conjecture, we form our first hypothesis as follows:

H1: The performance of marketing capabilities (postacquisition sales sensitivity) is positively influenced by an acquisition event.

Marketing capabilities under cross-border acquisitions

Despite over half of M&As being known to fail in creating synergistic values, M&As remain a common strategy for firms to gain access to valuable and unique resources not available in the marketplace (Dyer et al., 2004; Swaminathan et al., 2008). Prior studies have revealed that the realization of the intended benefits of M&As is conditional on a seamless integration of the target and the acquired firm (Bauer et al., 2020; Graebner et al., 2017). In particular, the success of integration and postacquisition value creation is partly explained by the relatedness of the resources of the acquiring and the target firms (Datta et al., 1992; King et al., 2004).

Both the acquirer’s and the target’s marketing capabilities can be extended to the newly combined entity to the extent that the capabilities are dynamic and transferable. The effective transfer of such marketing knowledge can improve a firm’s abilities in product development (Krell, 2001; Moreau et al., 2001), customer information (Bennett & Gabriel, 1999), and customer relationships (Davenport et al., 2001). However, given that marketing capabilities are relational, procedural, and context-specific (Srivastava et al., 2001), their transferability can be significantly limited. By its nature, marketing knowledge is highly tacit, socially complex, and therefore highly situation-specific (Simonin, 1999a). Thus, the value-enhancing role of marketing capabilities may not be materialized, especially when the target firm’s operating environment and customer base do not mesh with the acquirer’s marketing capabilities.

The relational and intellectual nature of the marketing function constitutes the specificity of marketing capabilities that are highly intangible and intertwined with the context of their development (Srivastava et al., 2001). Because the “know-what and know-how” of the marketing function are embedded in personnel and processes, marketing capabilities become largely firm-specific and activity-specific (Srivastava et al., 2001). The specificity of the resources results in a narrower user base or higher usage-specificity (Ghemawat & Del Sol, 1998; Zott & Amit, 2006). Therefore, these resources and capabilities can be applied only to specific contexts (Hoskisson et al., 1993; Hoskisson & Johnson, 1992), limiting their applicability to alternative contexts.

To the extent that marketing capabilities leverage context-specific intellectual resources, it can be assumed that marketing capabilities have the potential to create value in a limited set of economic exchanges only, that is, “narrowly valuable” or usage-specific (Ray et al., 2013). In other words, superior postacquisition marketing performance can occur only with the acquisition of related and compatible marketing resources. As a result, firms will only benefit from integrating marketing functions when the marketing environment remains unchanged, or the activities performed by acquiring firms are highly related or similar. One such context is geographical proximity. Cross-border acquisitions may invoke “the liabilities of foreignness” and thereby decrease the utility of the marketing capabilities (Kedia & Reddy, 2016; Schlegelmilch & Chini, 2003). Marketing resources’ relational nature makes them activity-specific, causing impediments in transferability and utility in a context distinct from their original use, leading to a loss of value (Vicente-Lorente, 2001).

Organizational distance and cultural distance are some of the factors responsible for limiting and impeding the ability to transfer and integrate marketing capabilities (Schlegelmilch & Chini, 2003). Organizations separated by geographical borders have distinct processes and knowledge assimilation, which tend to create difficulties in understanding the linkages between marketing inputs and outputs (Simonin, 1999b). Thus, the ability to integrate or transfer marketing resources and capabilities is diminished. Furthermore, the utility of the relational resources and capabilities of firms in distinct markets is limited. The differences in the culture of the societies of acquiring and target firms will also impede the integration of marketing capabilities. Specifically, intellectual marketing resources are highly contextual. The differences in the cultural norms of acquiring and target firm societies reduce the fit and transferability of intellectual marketing resources. The transfer of such context-specific knowledge resources will likely not lead to any positive impact on the firm.

Given that marketing capabilities are narrowly valuable and the economic value that can be created by integrating and transferring these resources is highly context-specific, we advance the following hypothesis:

H2: The positive influence of acquisition on the performance of marketing capabilities (pre-/post-acquisition sales sensitivity) is more pronounced for domestic acquisitions compared with cross-border deals.

Methodology

Research design and data

Our hypotheses require us to evaluate whether the impact of marketing capabilities on a firm’s desired marketing outcome is changed after an acquisition activity. While RBV suggests that a firm’s resources and capabilities create economic value either by increasing its revenues or decreasing costs, or both, it remains unclear which aspect of marketing capabilities drives the results (Srivastava et al., 2001). Furthermore, a firm’s marketing capabilities are largely unobservable and, therefore, cannot be directly measured (Nath et al., 2010). Although marketing capabilities are viewed as a “process” encompassing multiple dimensions, such as customer experience and attachment, the strategic role affecting product market competition, and the creation of marketing assets (Rust et al., 2004), the ultimate realization of marketing effort is arguably related to the generation of sales revenues. Therefore, we assume a firm’s sales sensitivity to marketing-related expenditure would reflect the impact of marketing capabilities.

To capture the sales sensitivity, we follow prior studies (e.g., Assmus et al., 1984; Simon, 1982; Vanhonacker, 1991) and estimate a Koyck-type “sales response model” reflecting the customer holdover and wear-out effect of marketing activities. The Koyck model acknowledges that current-period sales are influenced not only by the current-period advertising and marketing activities but also by prior-period activities. As such, a generic sales response model can be specified as follows:

where SALESt (or t–1) denotes sales at time t (or t − 1), ADVt (or t–1) denotes a firm’s aggregate advertising and marketing expenditure at time t (or t–1), and the intercept term is suppressed for simplicity. By subtracting equation (1a) from equation (1b) and rearranging the lagged terms of SALESt–1, the first difference between equations (1a) and (1b) can be expressed parsimoniously as:

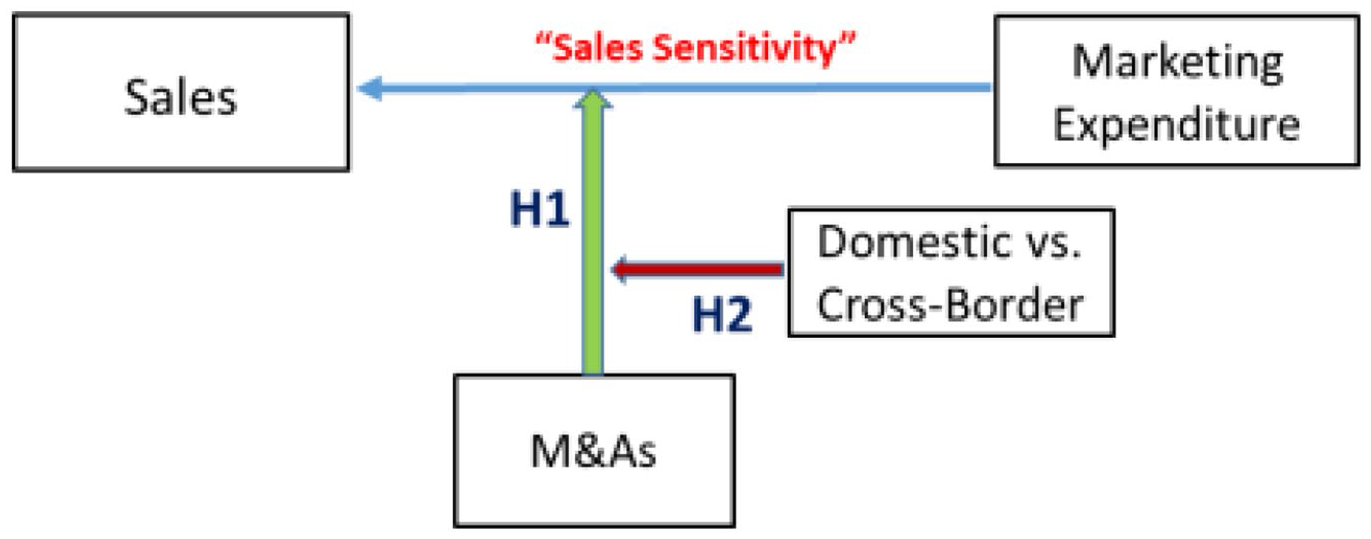

In equation (2) representing the sales sensitivity to marketing expenditure, our operationalization of marketing capabilities is captured by β, the coefficient of ADV. As our conceptual schema in Figure 1 illustrates, our hypotheses require the testing of the changes in β during the pre- and post-M&A periods.

Conceptual Schema for Hypotheses Tests.

Regarding the studies examining sales sensitivity, Liaukonyte et al. (2015) emphasized that endogeneity is a serious concern in identifying the causal effect of marketing-related activities. While the association between marketing activities and sales generation is captured by the sales sensitivity, it does not necessarily mean that the change in sales is caused by marketing activities; it may be driven by, for example, an improvement in macroeconomic conditions increasing overall consumer spending. To mitigate the endogeneity concern, prior studies have adopted a DiD research design that compares the differences between the groups with the treatment effects and the groups without them (see, e.g., Goldfarb & Tucker, 2011; Liaukonyte et al., 2015). Assuming that the difference in the sales responses between acquiring firms and nonacquiring firms would persist without an exogenous intervention (i.e., acquisition), 1 the change in sales sensitivity between the pre- and post-acquisition periods can be regarded as the consequence of the acquisition.

To implement this DiD research design, we form our initial sample using US public firms disclosing their marketing-related expenditure through financial statements over the 20 years from 1999 to 2018. When we merge the initial sample of 59,302 firm-year observations with 7,074 US public acquirers having acquisition deal information obtained from Securities Data Company (SDC), we remove serial acquires (i.e., multiple acquisitions conducted during our sample period), which can make some years double-counted as both pre- and post-acquisition periods. Through the propensity score matching (PSM) procedure performed by one-to-one matching based on the acquisition likelihood for each year, we obtain an unbalanced panel of 17,518 observations from 1,095 acquirers. After removing observations with missing information, our final matched sample consists of 15,509 observations from 898 acquirers.

Propensity-score-matched sample

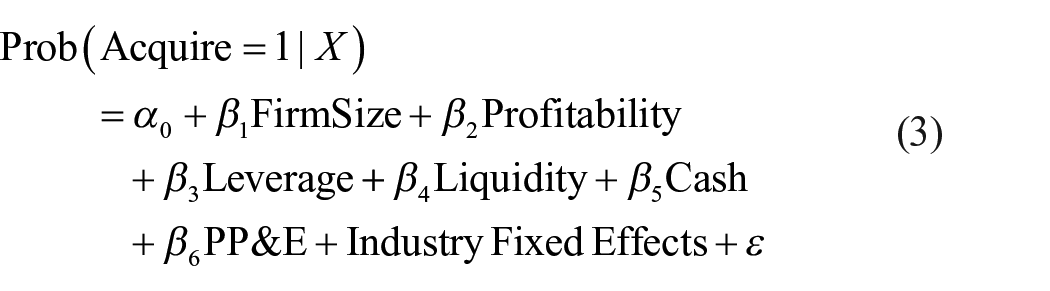

Despite the benefits of using DiD research design, potential endogeneity may create another empirical concern because the acquisition behavior is not random. While DiD presumes that the sales sensitivity to marketing expenditure should be the same between two groups in the absence of the acquisition activities, the potential self-selection of acquisition firms may lead to the violation of this key identification assumption of DiD (Roberts & Whited, 2013). In other words, when dissimilar control firms are included in the test of DiD, their sales sensitivity may vary regardless of the acquisition effect. To mitigate this concern, we identify our control firms based on the likelihood of a firm engaging with an acquisition in a given year, which is known as the PSM procedure (Rosenbaum & Rubin, 1985).

Specifically, we estimate the following logit model separately to capture the acquisition likelihood and match our acquisition treatment firms with non-acquisition control firms with the closest acquisition likelihood:

Acquire is an indicator variable equal to 1 when a firm engages with an acquisition activity and 0 otherwise. We form the acquisition likelihood model relying on prior literature in finance (e.g., Cremers et al., 2009; Harford, 1999). Covariates of the model include: FirmSize (the natural log of total assets); Profitability (the return on assets of the firm); Leverage (the ratio of total debts to total assets); Liquidity (the firm’s cash-payment ability calculated as the ratio of operating cash flows to total assets); Cash (the balance of the firm’s cash holdings); and PP&E [the ratio of tangible assets (property, plant, and equipment) to total assets].

Given that the PSM procedure does not rely on the assumption regarding the functional form of the relationship between a firm’s acquisition decision and other covariates, such as firm size and profitability (Li, 2012; Rosenbaum & Rubin, 1985), the propensity-score-matched control sample obtained through this procedure can reduce the potential systematic bias attributable to a firm’s self-selection into acquisition activities during our tests of sales sensitivity to the marketing and advertising expenditure (Stuart et al., 2014). Furthermore, while the postacquisition period cannot be identified for nonacquisition firms, PSM allows assigning pseudo-treatment periods to the control firms by using the matched treatment firm’s acquisition timing.

DiD model estimation

Similar to our study, Rahman et al. (2016) compared the efficiencies in revenue generation during the pre- and the post-M&A periods by testing a single time-series difference. Although they documented a cost efficiency improvement after M&As, the single difference approach followed by Rahman et al. (2016) cannot rule out the trends in outcome measures attributable to non-M&A-related forces (Roberts & Whited, 2013). Therefore, we use a DiD (or double difference) research design that compares the differences between the treatment and the control groups observed before and after M&As.

Our DiD model can be conceptualized as follows and estimated using ordinary least squares (OLS) regression:

where

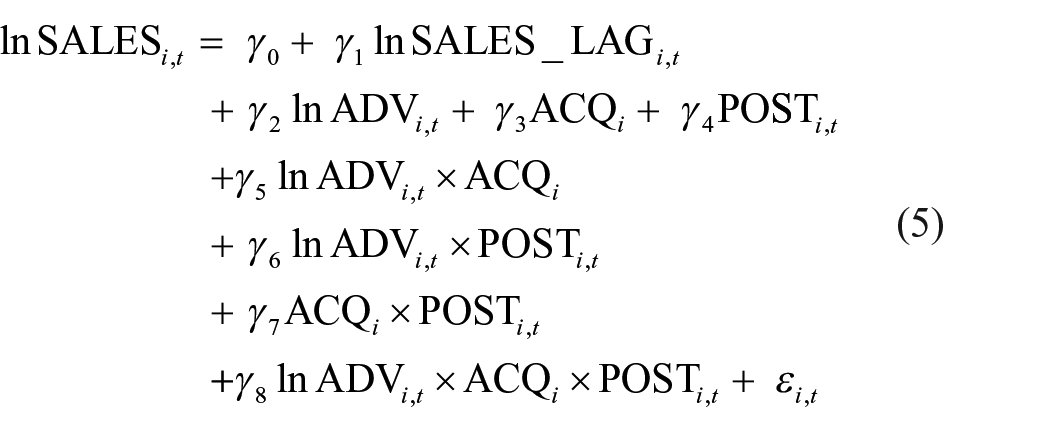

To incorporate the Koyck-type sales response model in equation (2) into the conceptual DiD model in equation (4), we integrate the two equations and specify the following modified DiD regression model:

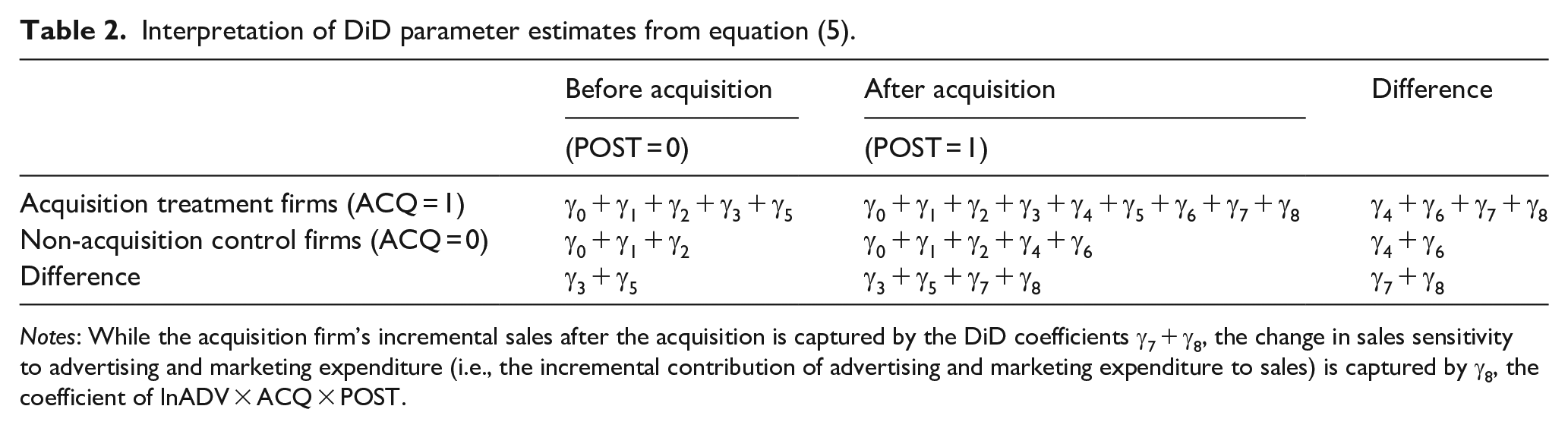

where: lnSALES i,t denotes the natural log of sales revenue scaled by total assets of firm i at time t; and lnSALES_LAG i,t denotes the lagged sales. In this model, our test variable is the interaction term of lnADV with ACQ × POST, which captures the changes in sales sensitivity after an acquisition. Parameter estimates from equation (5) can be interpreted as shown in Table 2. According to H1, to the extent that a firm’s marketing capabilities are intensified through an acquisition, the value created by market capabilities as reflected in the change in the sales sensitivity would be captured by the coefficient lnADV × ACQ × POST. The definitions of all variables are explained in Table 3.

Interpretation of DiD parameter estimates from equation (5).

Notes: While the acquisition firm’s incremental sales after the acquisition is captured by the DiD coefficients γ7 + γ8, the change in sales sensitivity to advertising and marketing expenditure (i.e., the incremental contribution of advertising and marketing expenditure to sales) is captured by γ8, the coefficient of lnADV × ACQ × POST.

Descriptive statistics and correlations.

SD: standard deviation.

denotes significance at a 5% level.

lnSALES Natural log of sales revenue, scaled by total assets

lnSALES_LAG One-year lag of lnSALES

lnADV Natural log of advertising expenditure, scaled by total assets

ACQ An indicator variable equals one for acquisition firms; zero otherwise.

POST An indicator variable equals one for the postacquisition period; zero otherwise.

SIZE Firm size is calculated as the natural log of total assets

PROFIT Return on Asset (ROA) is calculated as the income before extraordinary items divided by total assets

LEV Financial leverage is calculated as total debts divided by total assets

AGE Firm age calculated as the difference between the current year and the first year appears in COMPUSTAT

Results

Descriptive statistics and correlation

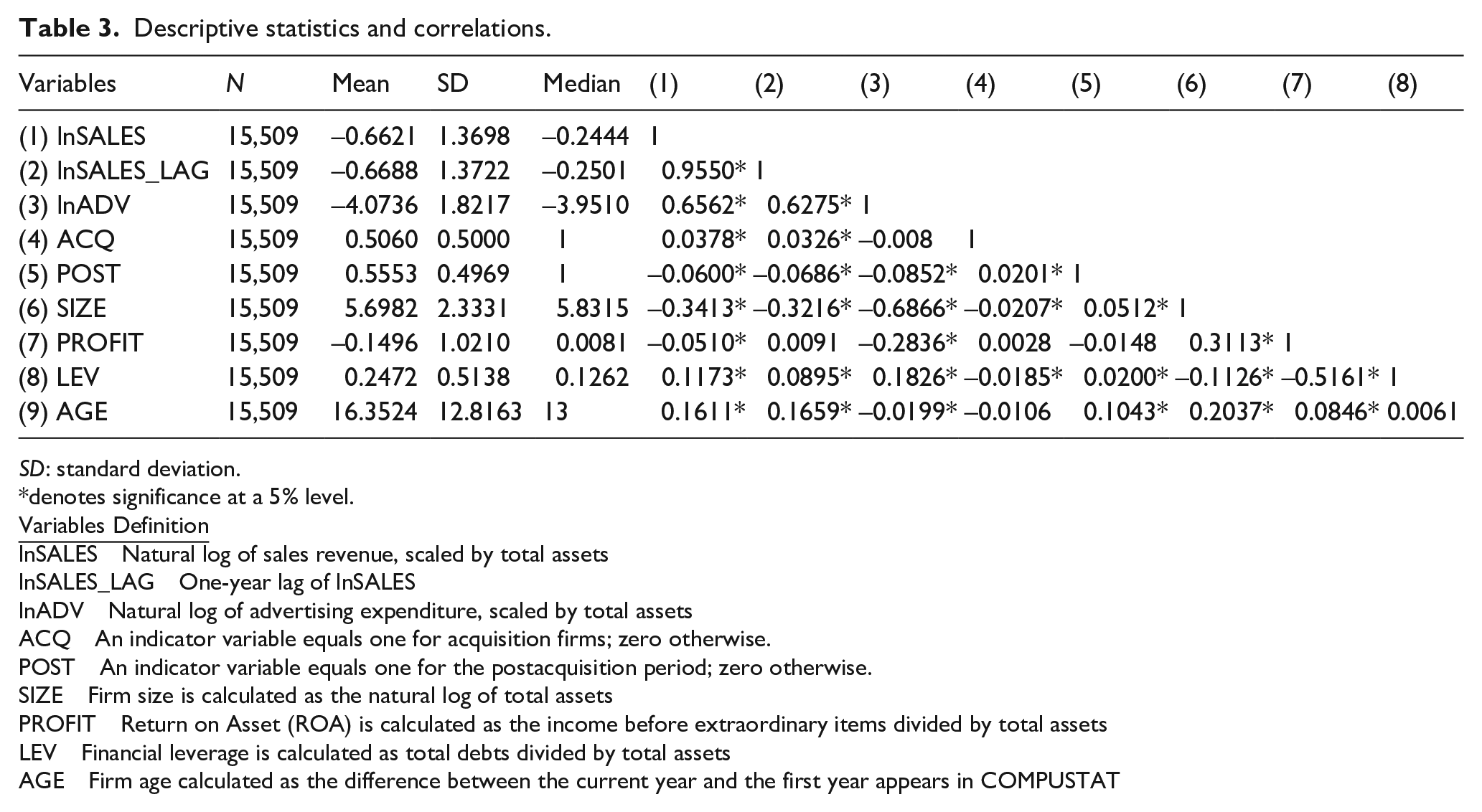

Descriptive statistics and correlations are reported in Table 3. The mean of sales revenue (lnSALES) is –0.6621, which is equivalent to about US$ 1,880 million and 101% of total assets. The mean of advertising expenditure (lnADV) is –4.0736, which is equivalent to US$ 41 million and 3.4% of total assets. Due to our use of one-to-one PSM, the mean of the acquisition dummy (ACQ) is close to 50%. As expected, the bivariate correlation between lnSALES and lnADV is positive and statistically significant, indicating a positive relationship between marketing activities and revenue generation.

Acquisition and value creation by marketing capabilities

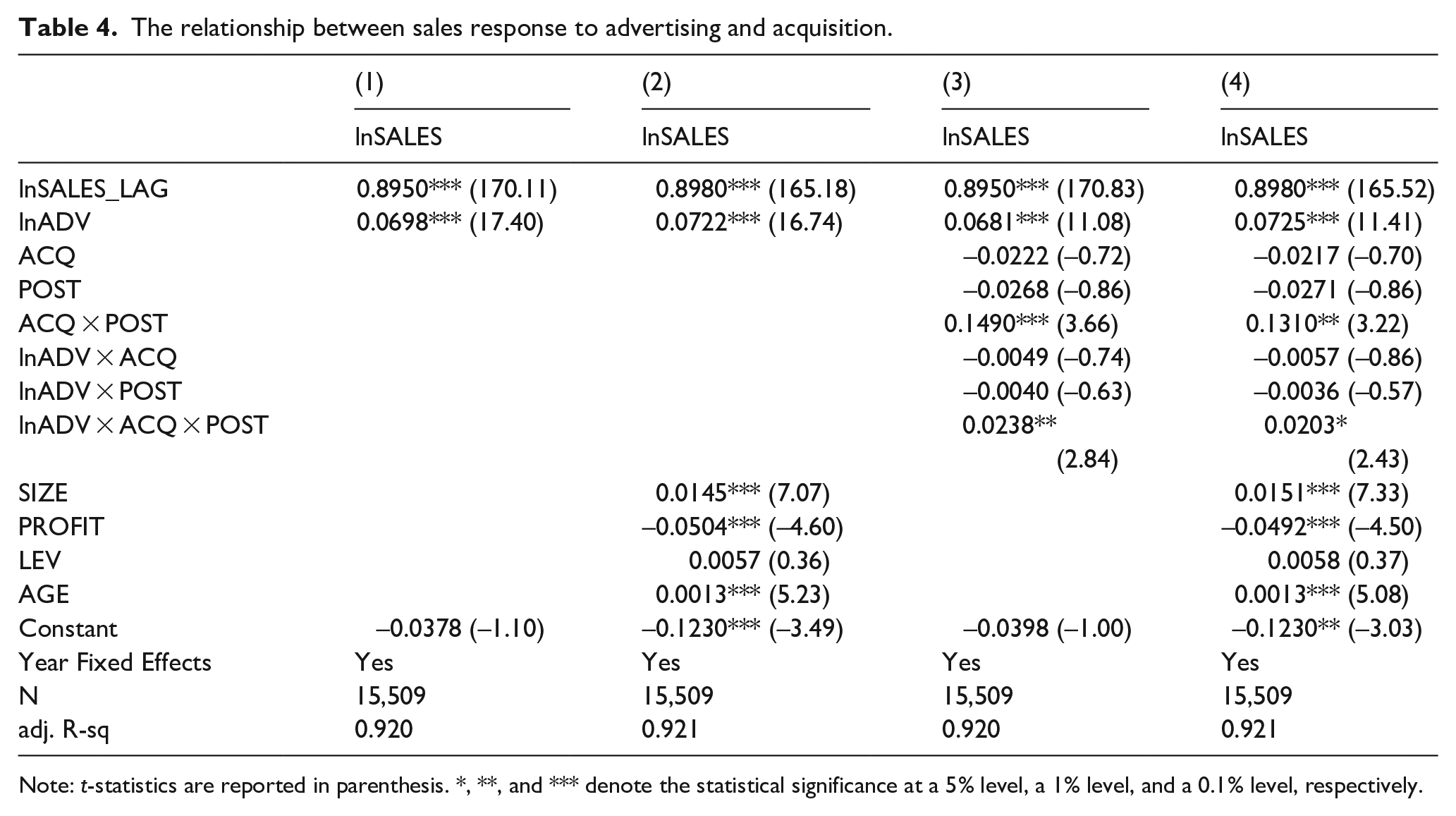

The results of estimating equation (4) using OLS regression with robust standard errors clustered at the firm level are reported in Table 4. As a baseline, we first estimate the Koyck lag model of sales response with several time-varying firm-level control variables and year-fixed effects. Consistent with prior studies, we find that the coefficients of lagged sales (lnSALES_LAG) are positive and less than 1, representing the persistence of sales or potential customer holdover (Simon, 1982). The coefficients of lnADV representing the sales response to advertising are close to 0.07 in column (1), indicating that a 1% increase in marketing advertising expenditure is associated with a 7% increase in sales.

The relationship between sales response to advertising and acquisition.

Note: t-statistics are reported in parenthesis. *, **, and *** denote the statistical significance at a 5% level, a 1% level, and a 0.1% level, respectively.

When we estimate our DiD model in column (3), the incremental effect of the acquisition on the sales response (or the average effect of treatment [AFT]) is positive and significant as captured by the coefficients of the three-way interaction term, lnADV × ACQ × POST (γ8 = 0.0238, p < .05), which is consistent with H1. This result indicates that the sales response to marketing and advertising expenditure is intensified, on average, following an acquisition activity.

In columns (2) and (4), we expand equation (4) to include several firm-level control variables that may confound the postacquisition performance, such as the size of an acquiring firm (SIZE), its financial leverage (LEV), overall profitability (PROFIT), and the maturity of operation revealed through firm age (AGE). We find that the baseline results summarized in columns (1) and (3) are robust to the firm-level controls’ inclusion. Collectively, these findings suggest that a firm’s marketing capabilities, as reflected in the sales response to marketing and advertising activities, are improved after an acquisition, suggesting the transferability of an acquirer’s marketing capabilities to a new entity after the acquisition.

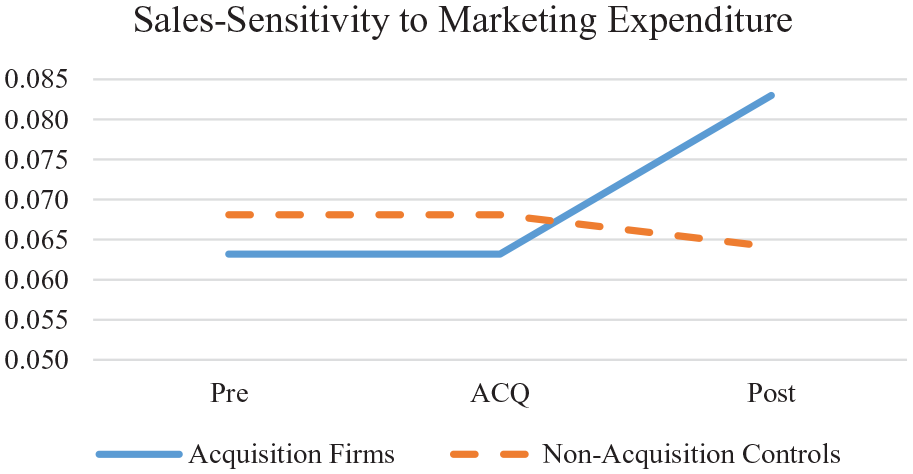

Figure 2 provides a graphical representation of sales sensitivity to marketing expenditure before and after an acquisition activity. Confirming H1, the graph shows an increase in the sales sensitivity of acquisition firms (treatment) relative to nonacquisition firms (control) following the acquisition.

Sales Sensitivity of acquiring firms’—preacquisition and postacquisition.

Value creation by marketing capabilities under cross-border acquisitions

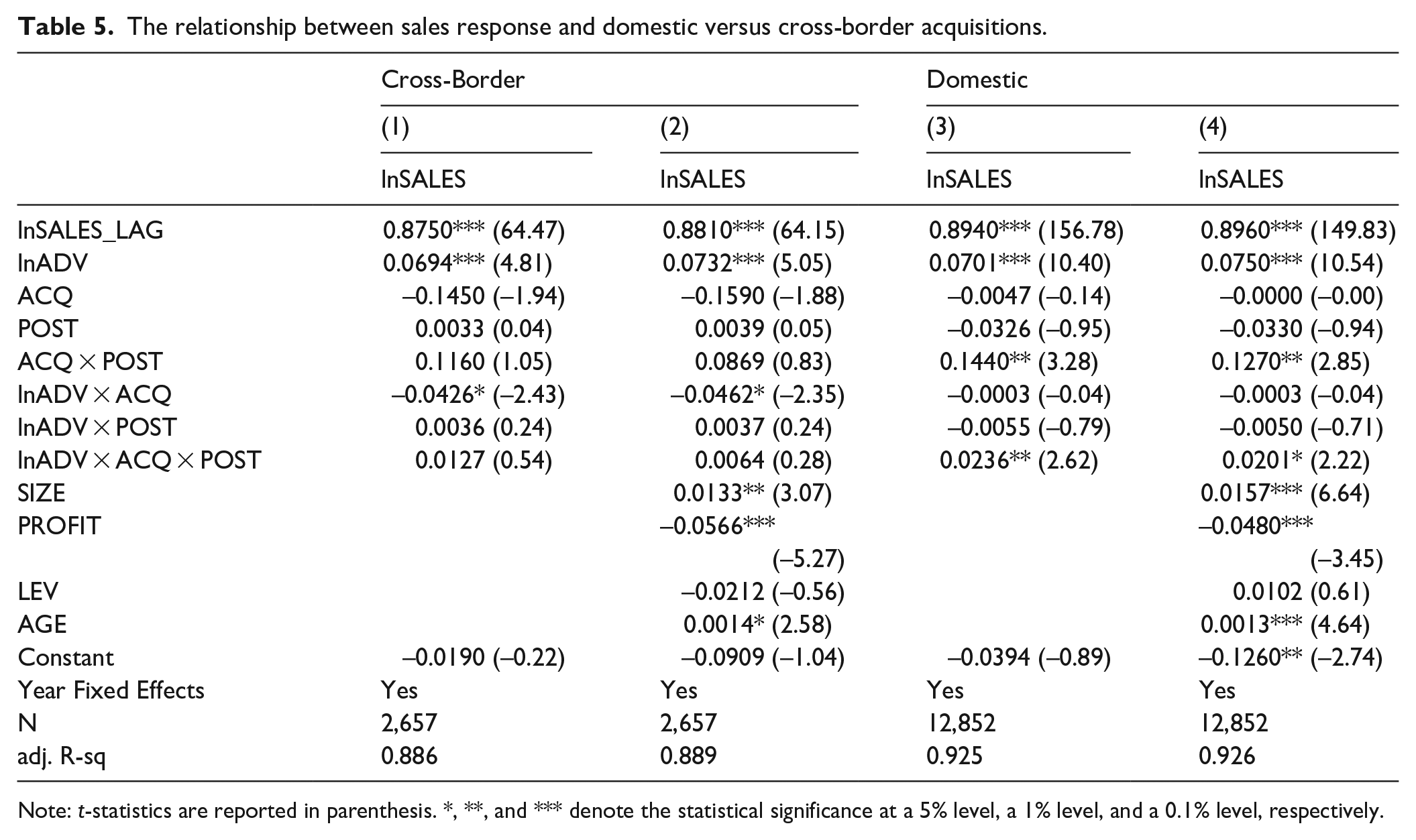

H2 is related to the acquisition’s conditional effect on the sales response for cross-border acquisition versus domestic acquisition. Although the marketing capabilities are transferable in general, these capabilities would be embedded in the social and cultural context of a market and may not be easily exported to foreign countries. Given the specificity of marketing capabilities, we predict that the increase in the sales responses observed after acquisition would be attenuated for cross-border acquisitions. To test this conjecture, we partition our sample into the cross-border and the domestic acquisition subsamples and estimate equation (4) separately.

As reported in Table 5, the incremental effect of the acquisition on the sales response is generally insignificant with cross-border acquisitions. The coefficients of lnADV × ACQ × POST are positive but significant at the conventional level in columns (1) and (2). In contrast, we find that the acquisition effect is sustained with domestic acquisitions. In column (3), the coefficient of lnADV × ACQ × POST is 0.0236 (p < .05), suggesting that the AFT of acquisition on sales sensitivity documented in Table 4 might be driven by the synergetic effect of marketing and advertising of the acquisition of domestic target firms. In contrast, cross-border acquisition does not provide an equivalent effect. Collectively, these results lend support to H2, suggesting that the “liabilities of foreignness” of marketing or the specificity of marketing capabilities to social or cultural contexts impede a firm’s marketing capabilities.

The relationship between sales response and domestic versus cross-border acquisitions.

Note: t-statistics are reported in parenthesis. *, **, and *** denote the statistical significance at a 5% level, a 1% level, and a 0.1% level, respectively.

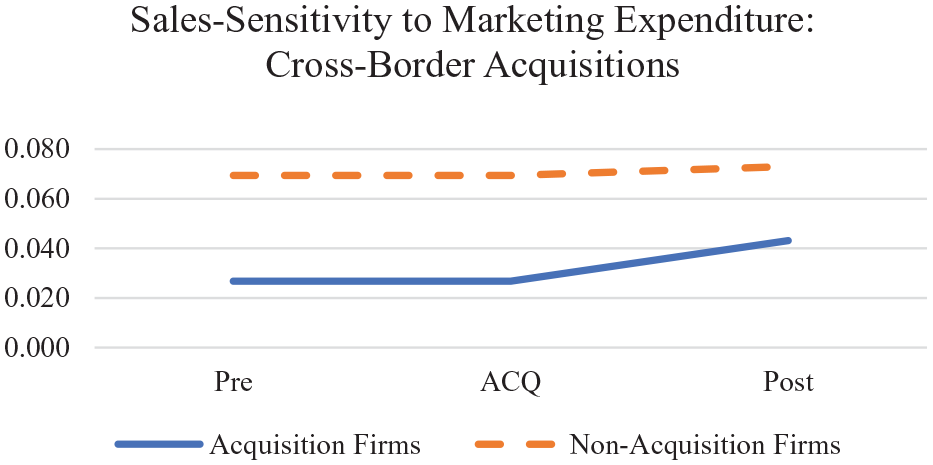

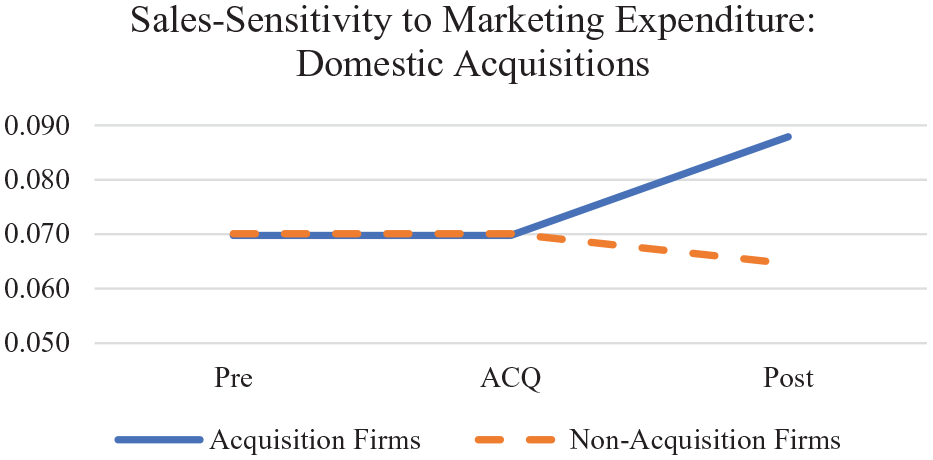

Figures 3 and 4 provide the graphical representation of the obtained results related to H2. In Figure 3, which only displays the cross-border acquisitions, there is no significant difference between the slopes of acquisition firms (treatment) relative to nonacquisition firms (control) following the acquisition. On the contrary, in the case of domestic acquisitions, which are shown in Figure 4, there is a significant increase in the sales sensitivity of acquisition firms (treatment) compared with nonacquisition firms (control) following the acquisition.

Sales Sensitivity of Acquiring firms’—preacquisition and postacquisition in cross-border acquisitions.

Sales Sensitivity of Acquiring firms’—preacquisition and postacquisition in domestic acquisitions.

General discussion and conclusion

There is ample evidence both from theory and practice that has highlighted the importance of marketing capabilities. In this article, we extend the extant literature and explore whether the value creation attributable to a firm’s marketing capabilities can be enhanced through strategic acquisitions. The central theme of this study is that M&As will have an impact on the value created by the marketing capabilities of a firm. The findings of the study provide substantial support for the proposed conceptual framework. The theoretical constructs operate mostly as hypothesized and explain a considerable proportion of the variation in the value created by the marketing capabilities. Specifically, both of our hypotheses are supported. As predicted, the value created by the marketing capabilities shows a positive movement postacquisition for the acquiring firm.

In our empirical tests, we applied the DiD research design and compared acquisition firms’ sales sensitivity with nonacquisition firms before and after the acquisitions. Our findings show that sales sensitivity to marketing expenditure becomes higher after an acquisition compared with other comparable nonacquisition firms. This result supports H1, predicting that corporate acquisitions are critical events providing an opportunity to leverage an acquirer’s marketing capabilities to create greater value for the firm. Our documentation of an increase in the performance of market capabilities after acquisition represents one of the “unidentified moderators” for postacquisition performance suggested by King et al. (2004). In addition, we found an asymmetric response for sales sensitivity between domestic and international acquisitions. Specifically, our results illustrate that the positive effect of acquisitions in improving sales sensitivity is limited to the cases of domestic acquisitions. The muted response from the cases of cross-border acquisitions may suggest that the incompatible market knowledge might hamper the value creation through the acquirer’s marketing capabilities to a foreign country’s contexts, that is, the “liabilities of foreignness” of marketing. This finding is consistent with H2 regarding the limited contribution of international acquisitions to an increase in the value created by marketing capabilities.

Despite the theoretical and empirical advances in the context of marketing capabilities research, our study is not without limitations. First, we did not distinguish between marketing capabilities or between different resources and capabilities. This was due to the diverse set of resources identified in the existing marketing literature. Since the portfolio of resources and how firms combine them to develop marketing capabilities varies across firms, we limited ourselves to measuring the economic impact of marketing capabilities. Second, we only distinguished between domestic and cross-border M&As to evaluate the specificity of marketing resource and capability transfers. We did not differentiate cross-border M&As by country or examine the dimensions that may engender different contexts for marketing activities. The degree of contextual change is dependent on a variety of factors, including cultural distance, language distance, knowledge distance, and so forth. Since ours is one of the first studies examining the transferability of marketing capabilities, we did not attempt to incorporate these elements into our study.

Drawing on the RBV of a firm, this study contributes to the understanding of marketing capabilities and their specialized nature. The findings in this study highlight that the marketing capabilities can be extended by integration, recombination, and redeployment following an acquisition. However, the ability to extend the utility of marketing capabilities is limited due to their specialized nature. Specifically, by demonstrating that the ability of firms to extend the utility of marketing capabilities is limited when the context of the application of capabilities is changed, we highlight the specialized nature of marketing capabilities. These findings also have implications for managers. Managers can employ strategies to improve the market-based capabilities through M&A tactics and by strategically choosing among the potential acquisitions. By choosing target firms with similar contexts, they can extend the utility of marketing capabilities. However, managers choosing targets across geographic borders limit their ability to retool and extend the use of acquiring firms’ marketing capabilities and should not expect any synergistic benefits.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.