Abstract

In 2015, the United Nations launched the SUSTAINABLE DEVELOPMENT GOALS (SDGs) in collaboration with civil society and firms, recognizing that leading firms have the potential to innovate bold solutions at scale to achieve global sustainability. Exploring the impact of the SDGs’ launch on firms, through the lens of normative pressure, we apply computer-aided text analysis to the language used in sustainability reports of 164 large corporations to investigate whether and how the SDGs impacted sustainability reporting. Results show that, when comparing firms’ sustainability reports before and after 2015, increasing alignment was observed with the language of certain SDGs, while alignment did not significantly change for other SDGs. We further analyze these changes across industries, natural resource intensity levels, and geo-institutional contexts, revealing variation among firms based on institutional characteristics that may point to selection priorities and critical gaps as global firms engage with the grand challenges embodied in the SDGs.

Keywords

Introduction

The dire need for a sustainable economic system has been broadly recognized for quite some time. However, it is only more recently that mainstream firms and global institutions are adopting this transition as a core focus (Bansal & Hoffman, 2012; George et al., 2016; Porter & Kramer, 2011). The United Nations (UN) sustainable development goals (SDGs) represent a novel approach to such sustainability-oriented change by providing specific targets instead of binding mandates or general encouragement (UN Global Compact, 2014). To explain how such nonbinding goals may drive meaningful change in this context, we adopt an institutional perspective in this study and suggest that normative pressure is a useful lens for further understanding such linkages (Campbell, 2007; Scott, 2013). To gain empirical traction on the purposefully broad and fairly new context of the SDGs, we focus this study on systematically analyzing changes (or lack thereof) in how firms report on their sustainability efforts by addressing the research question: Did firms’ sustainability reporting change following the launch of the UN SDGs, and if so, how?

In addressing this research question, we build on, and contribute to, previous research on how normative pressure, and specifically the UN’s launch of the SDGs, encourages firms to shift their approach to sustainability, ranging from greenwashing (Delmas & Burbano, 2011) to transformation (Hoffman et al., 2014; O’Rourke & Strand, 2017). In the context of the UN’s launch of the SDGs, such change represents a theoretically thorny issue when considering past findings. Specifically, the SDGs are non binding, broad, flexible, and externally defined (even if firms did have some input in their development). These attributes differ from previous accounts of sustainability-oriented change driven by binding regulations (e.g., the banning of leaded gasoline, Nriagu, 1990), addressing specific technological challenges (e.g., phasing out chlorofluorocarbon (CFC) usage for refrigeration, Manzer, 1990), diffusing of voluntary industry or non-governmental organization (NGO)-developed environmental standards (e.g., Responsible Care, ISO 14001, Delmas & Montiel, 2008), or such efforts originating within professions (Howard-Grenville et al., 2017). As a result, the launch of the SDGs offers not only the possibility of a crucial inflection point on a path toward a more sustainable economic system but also an intriguing empirical window to examine whether the normative pressures implied by such nonbinding, broad, and flexible frameworks can foment systematic sustainability-oriented change.

To generate rigorous answers to our research question, we utilize computer-aided text analysis (CATA) to analyze the sustainability reports of 164 firms ranked as the best sustainability performers in the 2019 S&P Global Sustainability Yearbook. We systematically score the “alignment” of the language of each sustainability report to the language of the SDGs and compare the scores for reports from the periods before and after the UN’s launch of the SDGs. This research design allows us to investigate if the change occurred in general terms, as well as across each one of the 17 SDGs. Our analysis reveals significant changes in firms’ sustainability reporting following the launch of the SDGs, when analyzing both our sample as a whole and when grouping these firms by geo-institutional characteristics (Henisz, 2000), industry sectors, and natural resource intensity levels (Bringezu & Bleischwitz, 2017). In addressing the “how” part of our research question, our findings suggest that normative pressure is a useful, yet limited, lens for understanding how broad, voluntary, multifaceted, and integrated goals such as the SDGs can drive meaningful sustainability-oriented change in firms.

We have organized the balance of this study into five sections. We begin with a literature review focused on firms’ relationships with the SDGs and sustainability reporting. Next, we discuss how normative pressure created by the SDGs could be a catalyst for changes in sustainability reporting. With this as background, we then introduce our empirical approach to assessing changes in corporate sustainability reporting after the launch of the SDGs. This is followed by a presentation of our results and then a discussion of our findings and their implications.

Literature review

Firms’ engagement with the SDGs

Despite their fairly recent launch, the SDGs 1 have generated considerable scholarly attention. As a high-level measure of the volume and breadth of this research, Nakamura and colleagues (2019) constructed a co-citation network from more than 10,000 SDG-related articles found in Web of Science. In addition to illustrating the increasingly dense network of knowledge around the SDGs, their analysis also suggests two somewhat distinct research clusters—one focused on health/health care and the other on the balance of the SDG topics. Using a similar bibliometric approach, but with a narrower focus on 266 articles in management journals, Pizzi and colleagues (2020) highlighted the dramatic growth in this research area and identified four themes—technological innovation, developing countries, nonfinancial reporting, and education.

Complementing these broad overviews are studies on engagement with specific SDGs. These studies range from the use of specific technologies in the pursuit of specific SDGs (e.g., using satellites to track slavery, in service of SDG 8, Boyd et al., 2018) to the creation of SDG-inspired frameworks for specific industries (e.g., building assessment and management, Alawneh et al., 2019). Such specialized studies also foreground the deeply transdisciplinary nature of SDG research, with specific studies clustering around themes as diverse as ecotourism, renewable energy, antimicrobial resistance, and physical activity and health (Nakamura et al., 2019).

Within this impressive body of SDG research, management scholars have carved out some distinct areas for contributions, driven by our ability to work across levels of analysis and embrace complexity (Howard-Grenville et al., 2019). A recent special issue of Academy of Management Discoveries (2019) highlights this potential with studies ranging from market-level analyses (e.g., tempering enthusiasm for using financial instruments for managing catastrophe risks, Etzion et al., 2019) to organization-level analyses of processes for making progress on specific SDGs (e.g., the role of collective agency in creating and sustaining two community-based enterprises in rural Germany, Hertel et al., 2019).

Our reading of this rapidly emerging area of research suggests an interesting and important gap. Specifically, the survey-based efforts (e.g., PricewaterhouseCoopers [PwC], 2015; Salvia et al., 2019; van Zanten & van Tulder, 2018) provide a general base-case for our understanding of firms’ engagement with SDGs by showing some important (if not particularly surprising) patterns, including an uneven prioritization across SDGs and “cherry-picking” of those that may be easiest to make progress on (Heras-Saizarbitoria et al., 2021). In contrast, other research in this area has focused on the processes deployed by organizations or institutions to grapple with specific SDGs (Bode et al., 2019) or examines specific mechanisms that facilitated more general SDG efforts (Williams et al., 2019). It is at the intersection of these two streams that we see an opportunity to merge the depth of these latter studies with the scale and cross-SDG nuance of the former ones.

In doing so, we seek to help eschew the “Winchester Mystery House syndrome” (Davis, 2015; Howard-Grenville et al., 2019), which puts SDG research at risk when we end up “adding too much complexity and novelty rather than building something that clearly and coherently contributes to a well-defined problem” (p. 358). Instead, we contribute a straightforward pre–post analysis of the sustainability reports of large firms, the sort of firms whose scale will be critical for driving meaningful change toward broad-based sustainability, to see if these systematically changed after the UN’s launch of the SDGs, and then we follow this with an examination of the sectoral and geo-institutional patterns within this broader analysis.

Linking sustainability reporting to the SDGs

Sustainability reporting represents an important pathway for firms to communicate their sustainability practices to stakeholders (Kolk, 2010; Reynolds & Yuthas, 2008). Increasing public scrutiny of firms’ actions—as they seek to generate positive social and environmental externalities beyond those related to economic performance (Leyva-de la Hiz et al., 2021; Wartzman & Tang, 2019)—has made firms pay increasing attention to their sustainability practices and communication.

Sustainability practices are articulated in sustainability reports as an accountability mechanism that supports firms’ legitimacy to operate (Cho et al., 2018; Cho & Patten, 2007). Furthermore, sustainability reporting is an important organizational practice by which firms communicate and signal their sustainability commitment and priorities to their stakeholders (Shinkle & Spencer, 2012). Publishing sustainability reports is a way firms respond to such stakeholder pressures by communicating their aspirations and progress (Bebbington & Unerman, 2018; Cho & Patten, 2007; Reynolds & Yuthas, 2008). Sustainability reporting is largely voluntary and less prescribed than its financial counterpart (Berliner & Prakash, 2015; Kolk, 2003), so while certainly imperfect, these reports offer valuable insights on firms’ sustainability efforts, both realized and aspirational (Christensen et al., 2013).

The increasing attention that the SDGs are receiving worldwide (UNGC & Accenture Strategy, 2016) may create normative pressure on firms, thus shaping both the content and form of their reporting. The institutional theory distinguishes different types of pressures exerted over organizations, namely cognitive, regulative, and normative (Campbell, 2007). Using this distinction, the SDGs represent a source of normative pressure because the implementation of such goals is voluntary and rooted in what stakeholders believe the firm should do. Despite sometimes being a constraint, such pressure may also be viewed by firms as an opportunity to disclose their sustainability practices and gain legitimacy in pursuit of market share (Yin & Zhang, 2012; Zhu & Sarkis, 2007).

Recent work shows that such change in reporting due to normative pressure exerted by the SDGs is more than just a theoretical possibility. For instance, Bebbington and Unerman’s (2018) analysis of SDGs in accounting and Pizzi and colleagues’ (2021) study of Italian firms showed how the SDG orientation of reporting is related to certain governance dimensions. Similarly, Rosati and Faria, in a global sample of 90 countries, looked at which institutional (2019a) and organizational (2019b) factors influenced the adoption of the SDGs in firms’ sustainability reports. Given this increasing evidence of meaningful normative pressure exerted by the SDGs, we seek to contribute to this promising line of research by conducting a systematic analysis of changes in firms’ sustainability reports following the launch of the SDGs.

Theory development

Instead of developing specific hypotheses, we take a more open-ended approach to our analysis, mirroring calls for engaging in problem-centered research through robust empirical exploration (Bamberger, 2018). To guide this exploration, we employ an institutional perspective to better understand the linkages between the launch of the SDGs and changes in sustainability reporting. Given that sustainability reporting is a voluntary practice and that the SDGs are nonbinding goals, we focus on the normative dimension of institutional theory—characterized by social obligation, a logic of appropriateness, and moral governance (Scott, 2013).

In a direct pathway for normative pressure, the introduction of the SDGs could lead firms to change their sustainability reporting as stakeholders increasingly view such reporting as an appropriate and expected practice, especially of large firms. In doing so, the SDGs could trigger a broadening of reporting beyond a firm’s core business activities (e.g., an energy firm that had previously reported emissions data may add reporting on working conditions) or a deepening of reporting in current areas (e.g., a retail firm reporting on labor conditions throughout its supply chain, instead of just in its company-owned facilities). Some of this broadening and deepening could simply be repackaging of existing efforts (Mogoutov & Kahane, 2007). However, such changes are in line with the SDGs’ objective of firms considering a broader set of sustainability goals and doing so in a nonsuperficial manner.

Another, albeit less direct, pathway for the SDGs to exert normative pressure on sustainability reporting is by creating a legitimate shared language that stakeholders believe firms should use in their reports. Both sustainability research and implementation are bedeviled by definitional issues (Glavič & Lukman, 2007) and a shared language may help lessen these tensions. If the SDGs could provide an appropriate, legitimate, global, transdisciplinary, cross-sector vocabulary for reporting sustainability efforts, it could clarify targets for firms and make comparisons to both past performance and competitors more credible from the perspective of stakeholders. The benefits of such a shared language may also extend to greenwashing-weary consumers, who may find value in a legitimate and comparable sustainability reporting framework to help guide their purchasing choices.

We believe such a normative lens can help us better understand broad-based change (or lack thereof) in sustainability reporting following the UN’s launch of the SDGs. However, given that the SDGs also represent distinct themes covering a broad set of topics and that prioritization of specific SDGs has been uneven as firms “cherry-pick” goals (Heras-Saizarbitoria et al., 2021; Nakamura et al., 2019; PwC, 2015), these pressures may also be shaping patterns of reporting within the full set of SDGs. For example, a “focusing” pattern could drive firms to concentrate their sustainability reporting on a few areas of sustainability-oriented competence, where they are best equipped to make progress (van Zanten & van Tulder, 2018). This could be because they had ongoing efforts in an area before the SDGs (i.e., “cherry-picking”) or because a given SDG fits with competencies common in a given sector. For example, perhaps a firm in a knowledge-intensive sector, such as financial services, should focus on SDG 8 (Decent Work & Economic Growth) or SDG 5 (Gender Equality) at the expense of broader reporting across SDGs if these are the main thrust of the normative pressure being applied by their stakeholders.

In contrast, the SDGs’ systematic nature could provide pressure for a broadening of firms’ reporting by highlighting opportunities outside of their core areas of operations, heralding a change to a more system-level engagement with sustainability-oriented change (Bansal & DesJardine, 2014; Montiel et al., 2021). This could occur either because reporting on SDGs that are “low hanging fruit” for a given sector would not serve to differentiate the firm from competitors, or reporting would clearly reveal SDGs a firm was not engaging with. Returning to the example of the financial services firm, reporting focused on industry-standard improvements in creating an inclusive workplace (no matter how impressive) could fail to provide a point of differentiation and/or reveal the firms’ narrowness in SDG engagement. Either of these would suggest that stakeholders may expect the firm should increase reporting on SDGs that are less central to its operations if it wants to stand out from competitors by making more meaningful progress toward broad-based sustainability.

In the spirit of exploration, we suggest that these pressures and patterns likely operate in a “both/and” rather than an “either/or” manner, albeit to varying degrees (e.g., firms more deeply engaging with SDGs related to their expertise and also “flirting” with more tangential SDGs), as sustainability reporting is a complex organizational practice and the SDGs span both geography and industries. As a result, our analysis focuses on the changes in the alignment of firms’ sustainability reporting with each of the SDGs and how these patterns may differ when considering different industries, levels of natural resource intensity, and geo-institutional contexts.

Data and methods

We drew our sample from the 2019 S&P Global Sustainability Yearbook (S&P Global, n.d.). The Yearbook, released annually, presents the list of best-performing firms according to the RobecoSAM (SAM) Corporate Sustainability Assessment and in line with the criteria of the Dow Jones Sustainability Index (DJSI). The SAM assessment is an annual evaluation of firms’ sustainability practices. Each year over 7,300 firms around the world are assessed across 61 different industries. Firms ranking in the top 15% of each industry are included in The Sustainability Yearbook and those with scores that are within 10% of the industry-leading scores are classified into three categories: SAM Gold Class, SAM Silver Class, and SAM Bronze Class. We initially included in our sample the 220 firms that received one of these Olympic Medal-inspired distinctions in 2019. In line with our exploratory approach and the scope of the SDG program, we did not apply industry or geographical restrictions to the sample, thereby allowing us to analyze variations in SDG engagement across regions and sectors. The sample consists of publicly traded firms with a global scope. The choice of using large firms that are top sustainability performers follows the reasoning that these firms have the potential to influence the trends and sustainability practices of other industry players (i.e., suppliers) and competitors (Martínez-Ferrero & García-Sánchez, 2017), therefore improving the long-run generalizability of our findings.

Data sources

To answer our research question, we collected two sustainability reports for each of the firms in our sample: one published prior to and another after the launch of the SDGs. Sustainability reports provide substantive information to corporate stakeholders (Rost & Ehrmann, 2017), improving the transparency on corporate social and environmental practices (Bebbington, 2014). We acknowledge previous research on signaling and image theory in corporate sustainability (Bansal & Kistruck, 2006; Cho et al., 2018; Hossain et al., 2019). However, in recent times, firms increasingly recognize the link between sustainability and financial performance (Knox, 2020), stakeholders exercise increasing pressures and punish irresponsible behaviors (Nason et al., 2018), and both auditing (Boiral et al., 2019) and the use of formalized and comparable reporting practices (e.g., GRI) have increased. These efforts have collectively improved the connections between reporting and real practices, especially for publicly traded, global firms.

We collected sustainability reports from publicly available databases and corporate websites when necessary. We used the following criteria for the data collection: for the “pre–SDG” reports, we included the most recent pre-2015 report, which included reports covering 2011 to 2014, and for the “post-SDG” report, we included the most recent report prior to 2020 (the year of our data gathering), which included reports covering 2016 to 2019. We downloaded both reports for 190 firms, for a total of 380 reports. We excluded 30 firms from the original sample of 220 because at least one of the two reports was not available online. We removed 28 reports (both reports for 14 firms) because at least one of their reports was not published in English or contained nonreadable characters when transformed into a text file format, and we removed 24 additional reports (both reports for 12 firms) because the firm shifted from separate sustainability reporting to integrated reporting, confounding the comparison of the two reports. After these adjustments, our final dataset included 164 firms based in 23 countries from the North American, European, Asia Pacific, and Latin American regions.

Firm categorization

As part of our analysis, we categorized the firms in the sample along three dimensions: industry sector, natural resource intensity, and geo-institutional context. The distribution of our sample across these dimensions is presented in Table 1.

Distribution of sample among firm categories.

Industry grouping

In recognition that engagement with the SDGs would likely be meaningfully different depending on the nature of a firm’s activities (e.g., mining vs financial services), we divided the sample into sectors based on the Global Industry Classification Standard (GICS) two-digit codes yielding eleven categories: Energy, Utilities, Industrials, Materials, Communication Services, Information Technology, Consumer Discretionary, Consumer Staples, Financials, Real Estate, Health Care. We regrouped those sectors based on process similarities into the following: (1) Energy-Utilities (n = 20); (2) Industrials-Materials (n = 49); (3) Communications-IT (n = 31); (4) Consumer Products (n = 40); and (5) Financials-Real Estate (n = 24). We removed Health Care as a standalone sector, given its relatively small number of firms in our sample (7) and connections to a fairly separate area of SDG research (Nakamura et al., 2019). We redistributed the firms initially classified in health care based on the GICS into one of the five groups, based on similar activities, placing Cigna Corp. (a health insurance firm) into Financial-Real Estate; CVS (a retail pharmacy firm) into Consumer Products and the remainder (pharmaceutical and medical device firms) into Industrials-Materials.

The consideration of SDGs alignment variation across different sectors fits with previous research showing that different industries engage with sustainable development in different ways (Monteiro et al., 2019; Musavengane, 2019). Legitimacy and isomorphic pressures are acknowledged to be relevant in shaping firms’ behaviors within sectors (Aragón-Correa et al., 2020; Hoffman & Jennings, 2015). For example, some sectors are often under the sustainability-oriented spotlight (e.g., Energy-Utilities), while others may be relatively overlooked (e.g., Financials-Real Estate). Moreover, specific industries have recently been hit by some major scandals, possibly accelerating their alignment with SDGs. Therefore, using this grouping, we aim to uncover cross-sector nuance on how firms have changed their sustainability reporting following the launch of the SDGs.

Resource intensity grouping

Natural resources play a key role in some firms’ strategic decisions (Hart, 1995) and in their centrality to several SDGs that challenge firms to make bold changes in their use of such finite resources (Bringezu & Bleischwitz, 2017; UN, 2015b; United Nations Environment Program, 2011). For example, Duong and colleagues’ (2021) recent analysis on the construction sector underscores the urgency of transforming high resource-intensive industries into more sustainable ones; a call that is shared by a number of other scholars (e.g., Kajander et al., 2012; Tan et al., 2015). Other recent studies have singled out firms in natural resource-intensive sectors for study, in part due to the scrutiny placed on major emitters of greenhouse gases (e.g., Cho et al., 2018; Talbot & Borial, 2018). As the SDGs present a broad-based framework for engaging with social and environmental challenges, it is interesting to consider whether firms in more resource-intensive industry groups might change their sustainability reporting in ways that differ from firms in less resource-intensive industry groups.

We organized our five industry groups into two categories based on the primacy of transformation of natural/physical resources in the activities of those industry groups. These we call high-intensity and low-intensity categories. High-intensity (n = 69) industry groups include Energy-Utilities and Industrials-Materials, while Low-intensity (n = 95) groups include Communications-IT, Consumer Products, and Financials-Real Estate. We acknowledge that there are various ways to define natural resource intensity and that individual firms may have high intensity for some resources and low intensity for others. 2 However, since scrutiny is often applied to entire industries, we believe that our categorization can yield meaningful insights.

Geo-institutional grouping

We found it important to shed light on how the UN SDGs, as a common framework designed to guide and shape global efforts, could be received and absorbed differently by firms operating in specific institutional environments. We explored this by applying an “administrative” perspective of countries’ similarities based on Berry and colleagues’ (2010) influential article in the international business literature and dividing our sample into three geo-institutional groups, capturing both geographical location and institutional tradition in terms of language, colonial ties, norms, and legal system (Ghemawat, 2001; Henisz, 2000; La Porta et al., 1998). Firms that take a strategic perspective on sustainability or corporate social responsibility must take into consideration (and find a balance among) the firm’s self-interest, legal rights, and social responsibilities (Chandler, 2020), a balance that may vary with the legal and social traditions in which firms operate. In our grouping, we attempt to account for geographical areas and also to take into consideration the legal tradition, such as common law versus civil law systems (La Porta et al., 1998).

Firms in our sample were based in 23 different countries. We categorized these countries into three groups: Anglo-Saxon (n = 46), Continental-Europe (n = 70), and Asia-Pacific (n = 48). In applying this geo-institutional perspective, we grouped Indian and Australian firms in the Anglo-Saxon category, along with those based in the United Kingdom, Canada, and the United States. Latin American firms were included in the Continental-Europe group, while the Asia-Pacific group included firms based in Japan, South Korea, Taiwan, and Thailand.

Methodology

To assess the alignment of corporate sustainability reporting to the SDGs, we performed CATA on our sample of reports to quantify the use and patterns of SDG-related terms. CATA has seen growing application in organizational research over the past decade, in part due to its ability to extract and quantify content from firm-level, archival, narrative documents in a manner that can be more efficient and objective than traditional qualitative analytical methods (Payne et al., 2011; Short & Payne, 2020). For example, it has been used to analyze long-term orientation in firms (Brigham et al., 2014), corporate social responsibility reporting (Meyskens & Paul, 2010), and a variety of other organizational constructs. Our analysis consisted of three phases:

Development of a “vocabulary” list of SDG-related terms and analysis of each of the 17 SDGs to quantify the relative usage/weighting of each term.

Analysis of each corporate sustainability report to quantify the usage/weighting of each of the SDG terms and computation of the alignment of each report to each of the 17 SDGs, based on the corresponding term weighting scores.

Pre-SDG versus post-SDG analysis of the alignment scores.

SDG language quantification

As our source for the “language of the SDGs,” we accessed the UN Sustainable Development website (UN, 2015a) and downloaded the descriptions for each of the 17 goals as raw text documents. To quantify this SDG language, we processed these 17 documents using the open-source Tf-idfVectorizer routine from SciKit-Learn (Pedregosa et al., 2011). The Tf-idfVectorizer computes the term frequency (Tf) for each term within each document from a group of documents, modified by an inverse document frequency (idf) that reduces the score as terms occur more commonly across documents in the group. Thus, this weighting captures both the frequency of each term in a document and the specificity or uniqueness of that term to that document versus the rest of the documents in the group. If a term does not occur in a document, that term receives a score of zero for that document. The results are output in separate columns (or vectors) for each document. For a detailed description of the open-source Tf-idfVectorizer program routine and its features, an excellent online reference guide is available from the developer (Scikit-Learn, n.d.).

Using an approach similar to that of Lavin (2019), we instructed the Tf-idfVectorizer to extract “terms” from the SDG description documents that consisted of each individual distinct word used in the 17 SDG descriptions, along with all sequential combinations of up to three words as they occurred in the SDG descriptions. For example, the phrase “global carbon dioxide emissions” would return the following nine distinct terms: “global,” “carbon,” “dioxide,” “emissions,” “global carbon,” “carbon dioxide,” “dioxide emissions,” “global carbon dioxide” and “carbon dioxide emissions.”

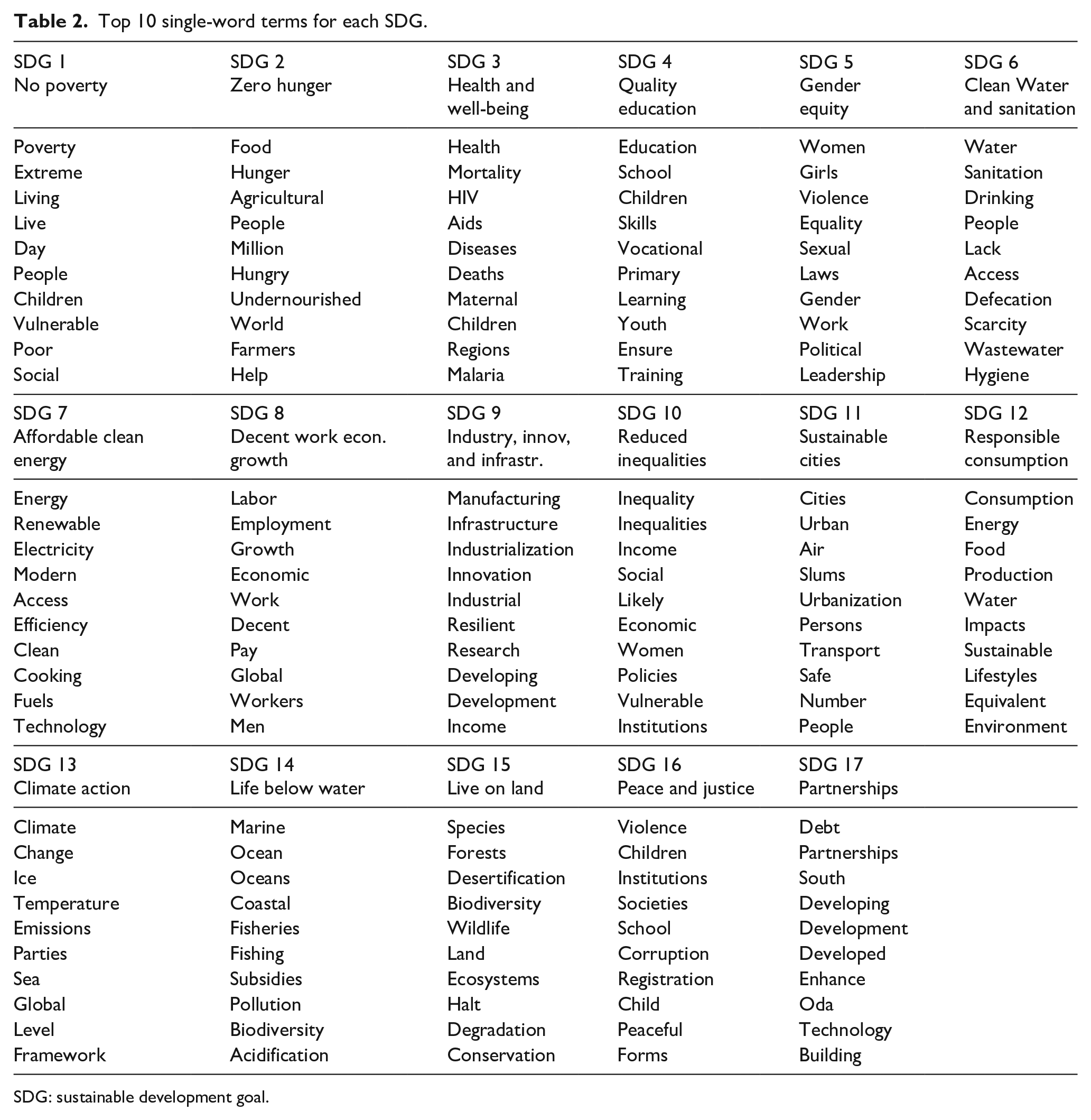

The result was a list that consisted of 14,417 terms, of 1–3 words each, which became our SDG “vocabulary” list for subsequent analyses. This list, along with the resulting 17 SDG Tf-idf vectors, effectively became a numerical representation of the “language of the SDGs,” able to distinguish one SDG from another. 3 This is observable in Table 2, which lists the top 10 single-word terms for each SDG, based on the magnitude of the Tf-idf scores. Each group of terms shows a strong association with the corresponding goal, reflecting the efficacy of this CATA approach. Armed with these SDG terminology vectors, we now have the means to measure the “language alignment” of any document to each of the SDGs.

Top 10 single-word terms for each SDG.

SDG: sustainable development goal.

Alignment of corporate sustainability reports to each of the 17 SDGs

The Tf-idfVectorizer was again used to process the text files from our corporate sustainability reports, with our 14,417 SDG terms as a user-defined vocabulary list and a normalization factor to account for the wide variety of report lengths. For each sustainability report, we compute a vector, just as we did for the SDG descriptions. To assess the alignment of any sustainability report to any one of the SDGs, we take the two corresponding tf-idf vectors and calculate an “Alignment Score” as the sum of the products of the respective tf-idf weights for each term. Only terms that are common to both documents (i.e., two non-zero weights) will contribute to the sum. Terms with higher weighted scores (i.e., higher relevance) in both documents will make the largest contributions to the sum. The presence of the multi-word terms (such as “climate change”), when present in both documents as a phrase, amplifies the alignment score significantly compared to single-word terms. 4 An alignment score was computed for each firm’s pre-2015 sustainability report vector paired with each of the 17 SDG vectors. As a measure of the alignment with the overall SDG language, the average of the 17 individual SDG scores (SDG Avg) was also computed. This was repeated for the firms’ post-2015 sustainability reports, resulting in two frames of data for our sample of 164 firms, each with 18 variables.

Results

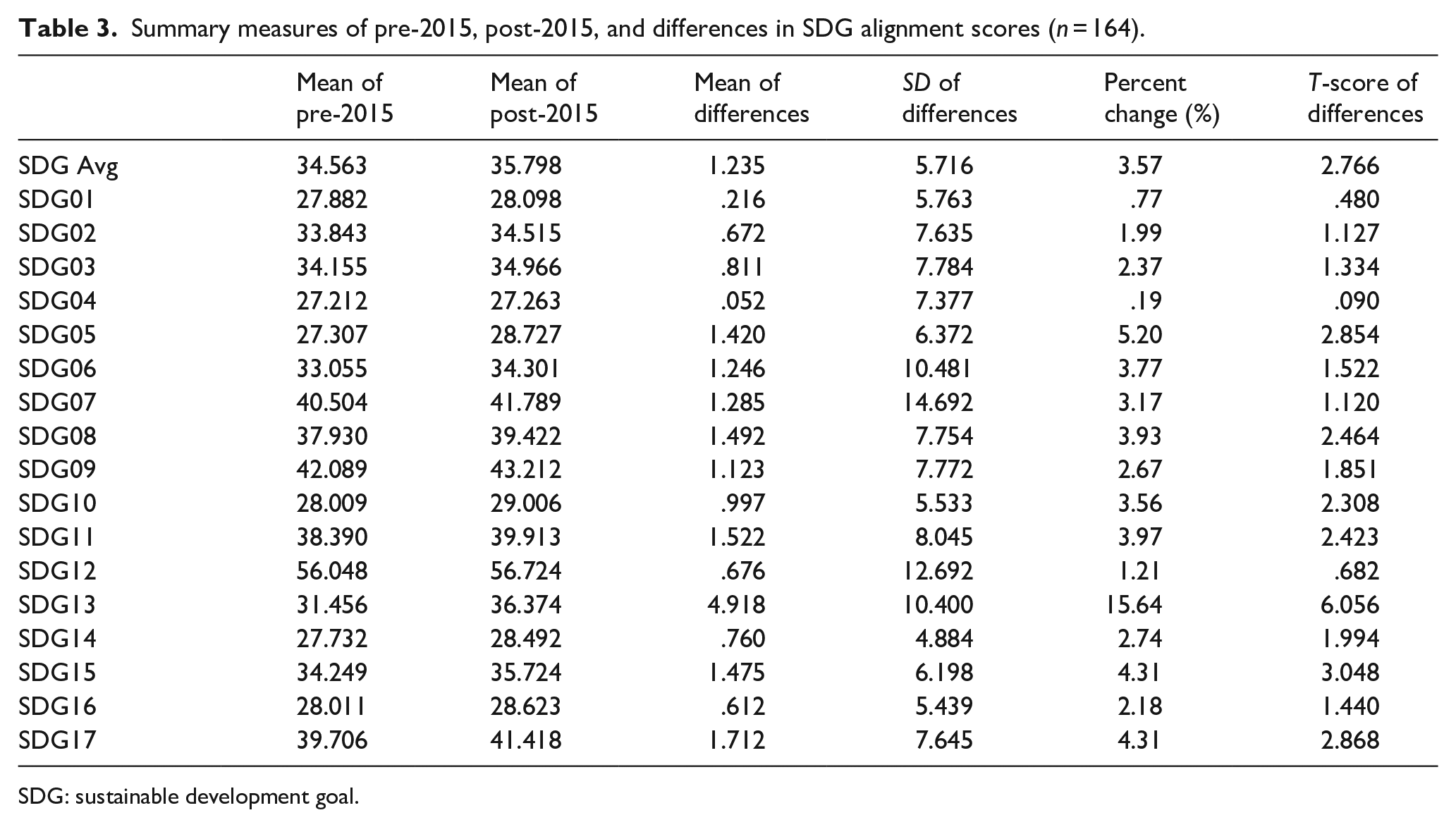

Table 3 summarizes language alignment scores and differences (denoted ∆SDG in the text), averaged across our sample of 164 firms, for each of the 17 SDGs as well as the average across the SDGs. Columns 2 and 3 of the table show the mean of the pre-2015 scores and the mean of the post-2015 scores. These values ranged from a low of 27.212 (SDG 4, Quality Education, pre-2015) to a high of 56.724 (SDG 12, Responsible Consumption and Production, post-2015). SDG 12 stood out from the remaining SDGs, exceeding the next highest score (SDG 9, Industry, Innovation & Infrastructure, post-2015) by more than 13.5 points. In addition, Table 3 presents the changes in SDG alignment for each SDG and the average across the SDGs. These are represented as the average of the post-pre differences for each firm as well as the percent change compared to the pre-2015 scores. The standard deviations of the differences are also presented, along with the corresponding t-test statistics. In terms of incorporation of the overall SDG language, the mean ∆SDG Average score was positive at 1.235 (p < .01) with an SD of 5.716. The average change for each individual SDG was positive, with SDG 13 (Climate Action) showing the largest average change in alignment scores (average ∆SDG13 = 4.918; p < .01), a 15.64% change from its pre-2015 value. It makes sense that SDG13 should experience a greater change in language incorporation, given that 2015 also saw the signing of the UN-sponsored Paris Climate Agreement, which gave additional encouragement to firms to engage with Climate Action. The smallest average change was a .19% increase in alignment for SDG 4 (Quality Education, average ∆SDG4 = .052; not significant).

Summary measures of pre-2015, post-2015, and differences in SDG alignment scores (n = 164).

SDG: sustainable development goal.

Several points emerge from further examination of the data in Table 3. First, there is considerable variation among the SDGs in the incorporation of their language into sustainability reports, with the highest alignment score being more than double the lowest score. Even excluding SDG 12, which appears to be an outlier, the second-highest score is more than 60% higher than the lowest score. Second, the magnitudes of the changes in score for each SDG (post–pre) were small compared to the magnitudes of the scores, with a median percent change of 3.17%. Third, the percent change in language alignment scores varied greatly across the SDGs, in a manner that seemed uncorrelated to the magnitudes. The three smallest changes in alignment belonged to the SDGs that ranked #1, #14, and #17 in terms of the magnitude of pre-2015 alignment. On the other hand, some of the changes in alignment were large enough to change the rank order of the SDGs based on average post-2015 scores. SDG 10 (Reduced Inequalities) moved up one position, from #13 to #12; SDG 5 (Gender Equality) moved up three positions, from #16 to #13; and SDG 13 (Climate Action) moved up four positions, from #11 to #7.

While Table 3 summarizes the results across our entire sample of 164 firms, a similar analysis was carried out for each of our 10 subgroups (5 industry groups, 2 resource intensity groups, and 3 geo-institutional groups). These results are not displayed due to space constraints, but the key points can be briefly summarized. Many of the general observations from the entire sample (as described in Table 3) do carry through to the subgroups, such as the consistently high language alignment of SDG 12 and relatively low alignment of SDGs 1, 4, 5, and 14. However, a subtle variation in relative alignment scores across the subgroups is also found, both in overall magnitude and in the difference between pre- and post-scores. For example, there is higher incorporation of language related to SDG7 in the Energy-Utilities group compared to the other industry groups and the relative inversion of language incorporation of SDGs 5 and 6 in the Financials-Real Estate group compared to the other groups. Other variations observed across the data include the changes (or lack thereof) between pre- and post-scores. It is the statistical significance of these changes, before and after 2015, which is the subject of our subsequent analysis.

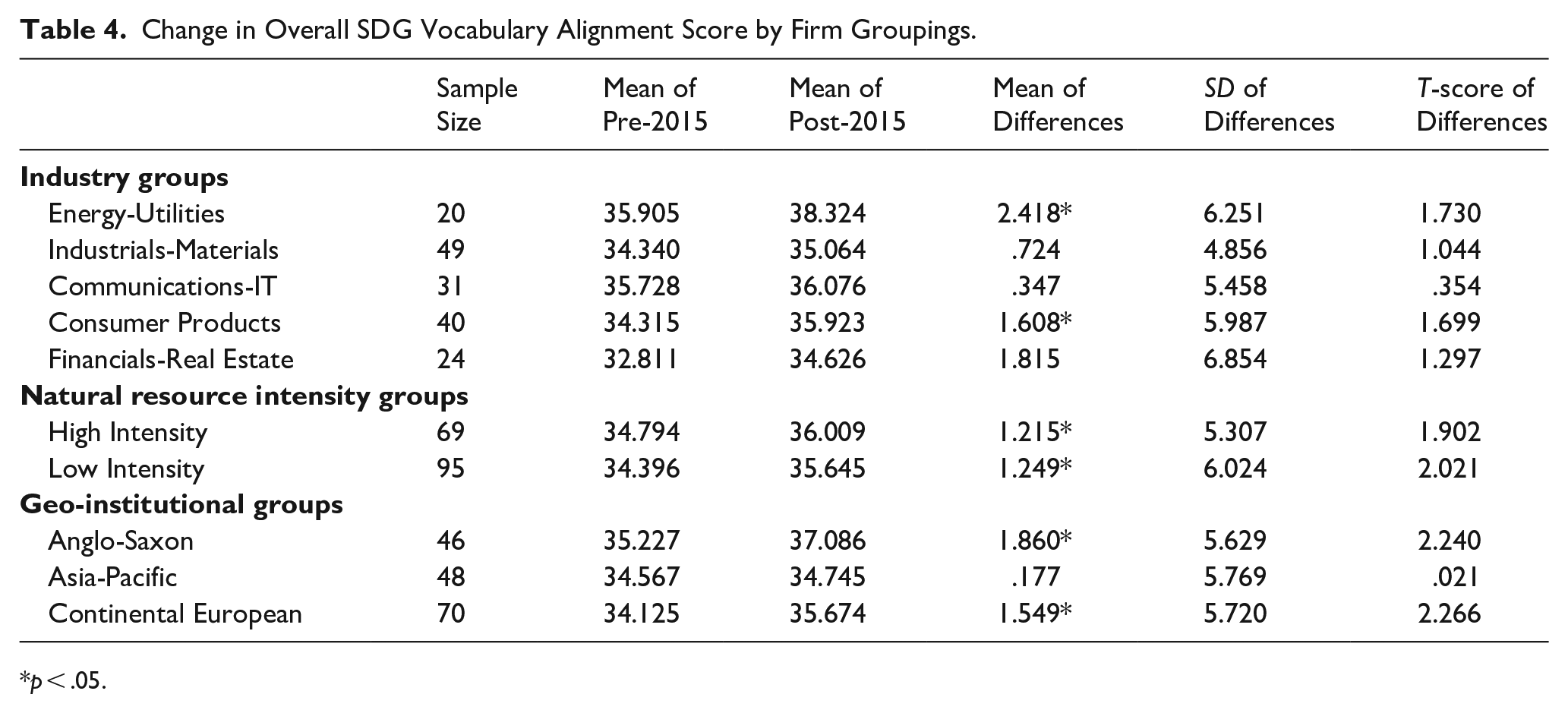

Our calculated ∆SDG scores for individual firms resulted in considerable variation across the dataset, with values ranging from −48.690 to +51.124. SDG14 (Life Below Water) showed the smallest variation in ∆SDG scores (SD = 4.884), with SDG7 (Affordable and Clean Energy) showing the largest spread in ∆SDG scores (SD = 14.692). To explore the variation in the ∆SDG scores, we began by investigating whether or not the change in the incorporation of overall SDG vocabulary (indicated by ∆SDG Avg scores) was significantly greater than zero in each of the firm subgroups in our study. Table 4 presents the results of this analysis for all three dimensions of our firm groupings. The mean ∆SDG Avg value is shown (with statistical significance level), along with the subgroup size, the standard deviation within each subgroup, and the t-test statistic for the mean difference. Along the Industry Group dimension, the Energy-Utilities and Consumer Products subgroups both showed statistically significant increases (p < .05) in the alignment with the overall SDG vocabulary, with t-values of 1.730 and 1.699, respectively. The other Industry groups did not show a significant change. Both natural resource intensity subgroups showed statistically significant increases (p < .05) in overall SDG vocabulary alignment, with t-values of 1.902 and 2.021 for high and low intensity, respectively. Along the geo-institutional dimension, the Anglo-Saxon subgroup and the Continental European subgroups both showed statistically significant increases (p < .05) in the alignment with the overall SDG vocabulary, with t-values of 2.240 and 2.266, respectively. The Asia-Pacific firm subgroup showed a negligible change in alignment with the overall SDG vocabulary.

Change in Overall SDG Vocabulary Alignment Score by Firm Groupings.

p < .05.

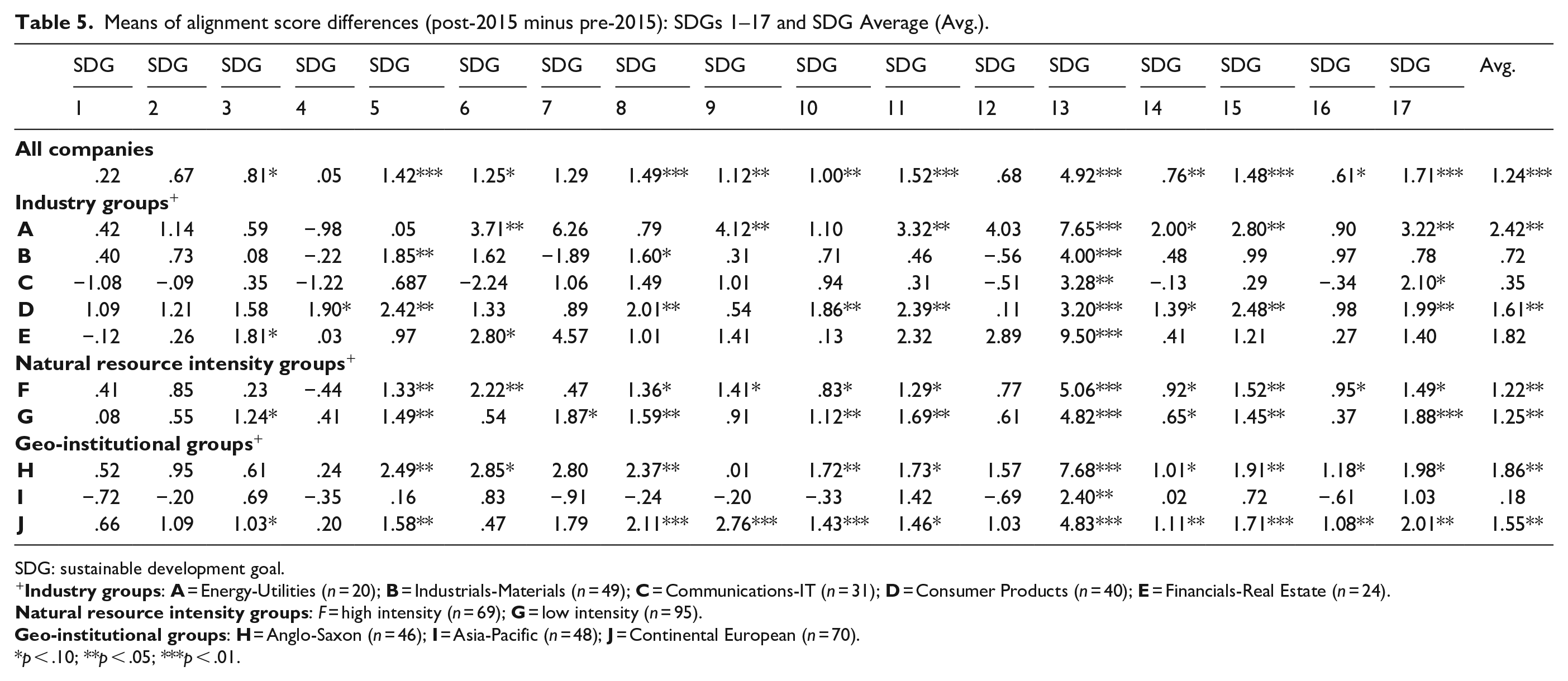

Table 5 shows the statistical t-test results (null difference = 0) for the mean differences for all the SDG scores, including the global average. This analysis shows which individual SDGs featured language that was increasingly incorporated into sustainability reports in the post-2015 period. The top row presents the results for the entire sample of 164 firms, showing the mean ∆SDG scores and their level of statistical significance. The subsequent rows present similar results for each of the firm subgroups analyzed.

Means of alignment score differences (post-2015 minus pre-2015): SDGs 1–17 and SDG Average (Avg.).

SDG: sustainable development goal.

p < .10; **p < .05; ***p < .01.

As can be seen in Table 5, the change in SDG language alignment is not homogeneous across the SDGs nor among the firm subgroups considered in our study. For the entire sample of firms, 5 of the 17 SDGs showed no significant increase in the alignment of their language with the sustainability reports. Nine of the 17 SDGs showed increases in alignment that were statistically significant at the .05 or .01 levels. The remaining three SDGs showed statistically significant but weak (p < .10) increases in language alignment. In addition, there was a heterogeneous change in SDG language alignment across industry or geo-institutional groupings, as can be seen in Figure 1, in which the icons for the 17 SDGs are aligned with the firm subgroups whose sustainability reports showed statistically significant language alignment increases (p < .05). Among the Industry Group categories, Consumer Products saw a significant increase in language alignment for 7 of the 17 SDGs. Energy-Utilities saw increases for 6 of the 17 SDGs, while the remaining industry subgroups saw increases for only 1 or 2 of the 17 SDGs. While both natural resource intensity categories saw a significant increase in overall SDG language alignment, firms in the low-intensity subgroup saw increases for a much higher proportion of the SDGs than high-intensity firms (7 of 17 SDGs vs 4 of 17 SDGs). Among the geo-institutional categories, the Continental European firms saw language alignment increases in 9 of the 17 SDGs. The Anglo-Saxon firms saw increases in 5 of the 17 SDGs, while Asia-Pacific firms only saw an increase in only 1 of the 17 SDGs.

SDGs with a significant increase in alignment to corporate sustainability reports (by firm groupings).

Discussion

The clear need for social and environmental progress, combined with the UN’s considerable efforts in developing the SDGs, has inspired researchers to scrutinize which specific goals firms are addressing (e.g., PwC, 2015; van Zanten & van Tulder, 2021; Williams et al., 2019). While it remains of interest to see which SDGs firms are pursuing and which they are leaving behind, such analysis provides limited insights on whether the UN’s launch of the SDGs changed the trajectory of firms’ sustainability practices. In other words, did firms actually change their breadth or depth of practices (as reflected in their reporting), or does this “embrace” of the SDGs only represent the “cherry-picking” of ongoing efforts and, therefore, a continuation of business as usual?

To begin to untangle these complex relationships, we started with the research question: Did firms’ sustainability reporting change following the launch of the UN SDGs, and if so, how? Based on the preceding analysis, the answer to the first part of this question is a clear but nuanced yes. Furthermore, our findings are consistent with the SDGs driving change by exerting normative pressure on the firms in our sample, although like many other studies suggesting this mechanism, we were unable to directly observe it. In lieu of being able to directly measure normative pressure, we addressed the “how” part of our research question through systematically analyzing patterns of language alignment (or lack thereof) across the SDGs and subgroups of firms that differ by industry, natural resources intensity and geo-institutional context.

Pressure and Patterns

Our full-sample results differ somewhat from the “cherry-picking” pattern of narrow engagement found in previous research by showing significant positive change in alignment across a fairly broad set of SDGs. Specifically, we found that alignment with 9 of the 17 SDGs significantly increased, 3 slightly increased, and 5 did not significantly increase after the UN’s launch of the SDGs. In this regard, it is worth noting that an absence of change does not necessarily indicate a lack of engagement with the given SDG. In Table 3, we can see that the language of SDG1 (No Poverty) and SDG4 (Quality Education) were not highly incorporated before nor after 2015. In other words, firms seem to not focus on discussing SDG1 and SDG4 in their sustainability reporting even after the launch of the SDGs. With respect to SDG2 (Zero Hunger), which had pre- and post-alignment scores that fell toward the middle of our range, our results show an increase in alignment, although it is not statistically significant. In contrast, SDG12 (Responsible Consumption and Production) shows a completely different picture and illustrates the value of examining both changes and levels of SDGs alignment. Specifically, while the change in language alignment was negligible, the relatively high pre- and post-scores indicate that this goal was already embraced by firms before 2015, and it continues to be among the priorities after 2015, suggesting the SDGs did not prompt a meaningful change in this area for the firms in our sample.

Overall, our results do fall short of the UN’s bold objective of driving meaningful change across all 17 SDGs. However, they do suggest a broadening pattern among firms in shifting their view of sustainability to something more, even if not wholly, integrated and systematic. In addition, the breadth of these positive changes is notable given that our “post” data are from not that long after the UN’s initial launch of the SDGs (2016–2019), and it may take more time for firms to report on their engagement with some of the SDGs that are more tangential to their operations, resources and capabilities (or simply take longer to measure progress on). In this regard, policymakers should monitor firms’ reporting on the SDGs to see if it continues to broaden into a truly systematic approach or if certain SDGs remain routinely under-addressed. In the latter case, firms may be able to help address these “orphan” SDGs through strategic partnerships or joint ventures with social ventures or NGOs focused on these areas.

Moving from our full sample to our industry sector analysis, more nuanced patterns of change emerge. For example, the sustainability reports of firms belonging to the Energy-Utilities group showed a positive change in alignment across six SDGs, thus supporting the centrality of the energy sector in sustainability-oriented change. While our results show that this group did not significantly increase alignment on SDG7 (Affordable and Clean Energy), there were positive changes in alignment on slightly more tangential SDGs, including SDG15 (Life on Land). This pattern, mirrored in other groups such as Consumer Products, suggests that these firms may be engaging with the SDGs with something akin to a “related diversification” strategy where they do go beyond simply “cherry-picking” by expanding their engagement to a broader set of SDGs that still connect to elements their expertise, yet fall outside of their core operations (e.g., an energy firm engaging with SDG 15 in addition to SDG 7).

Similar to our sector-based analysis, our natural resources intensity groups provided novel insights on SDG reporting patterns. Both groups show an increase in alignment across multiple SDGs, but with the low-intensity group showing broader scope with significant increases across seven SDGs as opposed to three SDGs for the high-intensity group. While some of these areas of improved alignment are not surprising (e.g., the High-intensity group improving on SDG 6 (Clean Water and Sanitation), others are less expected, such as alignment on SDG 11 (Sustainable Cities and Communities) increasing for the Low-intensity group but not the High-intensity group.

Finally, our analysis of geo-institutional groups shows that firms belonging to Anglo-Saxon and Continental-European groups exhibit significant positive changes in their SDG alignment scores, whereas the Asia-Pacific group showed limited differences between the pre- and post-scores. Whereas traditionally Continental-European firms have been more inclined toward environmental efforts than the Anglo-Saxon ones (Henisz, 2000; Kolk, 2010; La Porta et al., 1998), our analysis shows that both groups are fairly similar in their reporting alignment with the SDGs. This counter-intuitive result suggests the SDGs are reaching beyond the traditional hotbeds of sustainable business to countries like the United States where, if anything, formal regulatory pressures lessened during the timeframe of our “post” data (2016 to 2019). More generally, this pattern suggests that the normative pressure exerted by non binding goals (such as the SDGs) may be able to provide a lodestar for changes in sustainability-oriented business practices in the absence of, or as a complement to, other forms of institutional pressure such as changes in regulations.

While the dynamics at play may be multifaceted, our study demonstrates that a shift has indeed taken place in sustainability reporting, as reflected in changes in the alignment of language with respect to the UN SDGs. This exploration of the firm-SDG interface allows for a nuanced view of how firms in different industries, with different intensity levels of natural resource use and facing different institutional contexts, select among the SDGs to prioritize in their business practices. Ultimately, this provides a deeper understanding of business engagement with the SDGs than just studying the SDGs as a whole.

Limitations

Although this study sheds new light on the degree and scope of firms’ alignment with the SDGs in their sustainability reporting, it is not exempt from limitations that open interesting new research avenues. Perhaps, the most relevant one is the sample selection, where we intentionally examined the top performers of the S&P Global Sustainability Yearbook. This choice of top sustainability performers answers the UN call for leading firms, as they may be regarded as “major actors of change” (SDG Compass: The Guide for Business Action on the SDGs, 2015). Prior to this UN call, a number of scholars had acknowledged the role of such leaders in their industries, as they show other firms the path toward impactful environmental practices, at the same time that they push policymakers toward tougher regulations (Aragón-Correa, 1998; King & Lenox, 2001; Porter & Vander Linde, 1995), hence creating a first-mover advantage effect (Przychodzen et al., 2020). Another limitation is the size of the firms selected. Our analysis is based on large corporations, thus leaving small- and medium-sized enterprises (SMEs) aside. Further work could focus on SMEs to assess their sustainability efforts toward the achievement of the SDGs.

An additional limitation is our reliance on sustainability reports as our primary data source. The stakeholder-facing nature of such reports helped make the scale and rigor of our study possible, but these are also only one of many sustainability-related practices embraced by large firms. Beyond this (and as we detailed earlier), the relationship between reporting and actual outcomes can be somewhat murky in the context of sustainability. Given the high-profile nature of the firms we analyze here, it seems a full decoupling (i.e., reporting and actual sustainability outcomes being totally uncorrelated) would be unlikely. However, some degree of partial decoupling is probably inevitable, whether that be a tactical choice of a given firm or simply a function of the interacting complexities of the SDGs and the type of large firms captured in our sample. Either way, the degree of decoupling, and its associated patterns, form a promising topic for future research. In this vein, future studies could complement our work, which is based on secondary data, with more primary sources. For example, Salvia and colleagues’ (2019) work based on surveys, as well as Ike and colleagues’ (2019) analysis of a case study, both represent apt starting points for a more nuanced understanding of SDGs implementation.

Practical Impact and Conclusion

Our work presents some significant implications for managers and policymakers alike. The systematic changes in sustainability reporting by leading firms show that they may be making progress toward the achievement of the SDGs. However, our analysis also revealed that this change is uneven and incomplete. Specifically, although these firms do not appear to be only narrowly “cherry-picking” in their reporting, they are also not engaging with all the SDGs in a fully systematic way. This could be just a matter of time, but it could also represent organizational limits that make rigorously designing, implementing, and reporting change across all 17 SDGs difficult, if not largely impractical. In addition, our results suggest that efforts reliant on normative pressure alone may not be enough to truly achieve the kind of ambitious, transformative sustainability-oriented change aspired to by the SDGs.

If either proves to be the case, our results suggest that strategic partnerships or joint ventures, for example, between high and low natural resource intensity firms or energy-utility and consumer product firms, might allow for more progress, in a holistic sense, by allowing a certain degree of specialization on SDG engagement. Sparking, supporting, and scaling such creative collaboration would also clearly offer an opportunity for innovative managers and policymakers.

Given the influential nature of the firms we examined and the significant and fairly broad-based engagement with the SDGs they report, managers from firms with poor environmental and/or social commitments should strongly consider changing their practices. Specifically, our analysis suggests that we may be on a path where firms’ contribution to society is becoming the “new normal” even in the absence of binding regulations and that leading firms are increasingly willing to report such progress to stakeholders. Thus, stagnant firms may eventually lose their place in the market as their stakeholders come to expect such transparency and progress.

Although there is a growing tendency toward reporting progress on some SDGs, our results suggest others may be being left behind, hence needing direct policy support and/or creative approaches to partnerships. For example, the case of SDG1 (No Poverty) and SDG2 (Zero Hunger) provide a possible early-warning signal to policymakers, as it seems that firms themselves (at least in our sample), showed low and nonincreasing alignment with these goals. As such, our results suggest the UN should closely monitor engagement (or lack thereof) on these goals (and others showing similar trajectories) that are failing to show early traction among leading firms. In addition, the multi-dimensional nature of our study highlights the extent to which each of the individual SDGs is gaining traction among firms with varying characteristics, as illustrated in Figure 1. This may allow for more targeted interventions to accelerate engagement at key points along the firm-SDG interface.

Ultimately, our analysis shows that, just as excluding firms would likely doom any transition to broad-based sustainability, firms alone may not be able to make transformational progress across the expansive terrain captured by the 17 SDGs. Instead, our work suggests that the SDGs have spurred meaningful, if uneven, change in the sustainability efforts reported by leading firms and that other actors (e.g., governments, NGOs, and SMEs) need to foster and leverage this momentum to collectively make rapid progress on meeting our grandest challenges.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research work is partially funded by the Spanish Ministry of Economy and Competitiveness (Grant No. PID2019-106725GB-I00), the European Regional Development Fund (Grant No. B-SEJ-398-UGR20), and the Andalusian Regional Government (Grant No. P20_00019). Dante I. Leyva-de la Hiz is member of the LabEx Entrepreneurship center (University of Montpellier, France), funded by the French government (Labex Entreprendre, ANR-10-Labex-11-01).