Abstract

The often long-lasting process of intrafamily business succession involves contracts for management and ownership transfer that unfold in a complex series of stages. The older and larger a family business, the more heterogeneous the involved family members’ interactions and interests can become. These differences become obvious in the succession process. Also, in entrepreneurial families, information is not easy to obtain and is neither perfect nor unlimited, for example, with regard to expectations regarding the duration or the type of business succession. Information asymmetries can arise. This article investigates the drivers of information asymmetries and provides insight into the current research by investigating information asymmetries and their impact during different phases of intrafamily business succession. Data from 215 German firms reveal the occurrence of specific information asymmetries during different phases of intrafamily business succession.

Introduction

Family businesses and their intrafamily dynamics provide an ideal setting for intrigue, conflicts, and family dramas. Over multiple generations, the number of family members increases, with each member holding varying numbers of shares and either working or not working in the family firm. As a result, self-interests can arise, especially with respect to business succession (Madison et al., 2016; Schulze et al., 2003, 2001). The hand-over brings the generations together, and family members’ personal interests must be aligned (Kotlar & De Massis, 2013; Lubatkin et al., 2007). Despite the existence of anecdotal evidence and media reports, a lack of research on family firms in general and information asymmetries in the succession process in particular remains (Madison et al., 2016).

During a long-term succession process, many designated successors work as employees in family business, often without holding shares and with limited power and decision rights (Hernández-Trasobares & Galve-Górriz, 2016; Le Breton-Miller et al., 2004; Schell et al., 2019). This creates a principal–agent situation because until the final succession decision is made, the predecessors have the power to decide who will be the successor(s) and when the succession will occur (Lee et al., 2003; Schell et al., 2019). This also includes the options of business succession, such as selling the business or establishing a foundation. Dehlen et al. (2014) point out possible information asymmetries in this context. However, family businesses still prefer intrafamily business succession (Salvato et al., 2012). This can have various reasons, such as the preservation of socioemotional wealth (Gómez-Mejía et al., 2011; Minichilli et al., 2014), but also that it is the only option for the business. In addition, family members may also have the desire and will to take over the family business and to embrace the entrepreneurial legacy (Jaskiewicz et al., 2015). In this case, the successors have superior knowledge about their commitment and willingness to succeed (Sharma & Irving, 2005). In these situations, information asymmetries can arise and influence the behavior of all parties involved. For example, a firm’s predecessors could withhold information about the real financial situation of the firm to foster the succession of potential and needed or wanted candidates. Conversely, successors could hide information about their ideas for the future strategic development of the firm to avoid being excluded as successors due to the ways in which their plans differ from those of the predecessors. This type of behavior regarding asymmetric information can impact the satisfaction of the actors who are involved in the succession process (Le Breton-Miller et al., 2004) and hamper the further success of the family business—or even the succession itself. Thus, resolving the issues related to asymmetric information is crucial for the long-term survival of the company (Cabrera-Suárez et al., 2001).

The intrafamily business succession process can be understood as a contracting situation in which information asymmetries can occur (Lubatkin et al., 2007). Schell et al. (2019) propose that information asymmetries exist in the selection process of intrafamily successors, which are minimized through signaling processes. Zellweger and Kammerlander (2015) provide first theoretical assumptions that governance structures promote agency costs in family business succession. Dehlen et al. (2014) demonstrate that entrepreneurial exit routes favor internal successors because they create fewer information asymmetries than external ones. These results deliver strong support for the proposition that agency problems can be expected both in family businesses and among family members, and there is a need to discuss the underlying cause of agency costs: general information asymmetries (Madison et al., 2016). There remains a lack of insight into whether information asymmetries exist in intrafamily succession, how such asymmetries are characterized, the extent of the asymmetries at different phases in the process, and how family members handle those asymmetries. However, although all of these studies assume information asymmetries, none of them reveal the exact types of information asymmetries that prevail. For example, the literature on advisors in family businesses also underscores that advisors can help succession participants exchange important information and identify ways in which to compensate for information deficits (Bertschi-Michel et al., 2019; Michel & Kammerlander, 2015; Strike et al., 2018). Advisors are mainly used to manage the complexity of succession. In the context of succession, for example, role conflicts can arise (Cater & Justis, 2009). Both family logics and business logics must be superimposed (Jaskiewicz et al., 2016), and management and ownership succession, which often do not necessarily occur in parallel but rather one after the other and represent the basis for securing the company, generate complexity and the need for communication. However, even this strand of research does not address what specific information is relevant during this period and where it might be withheld. This aspect makes it more difficult for research and practice to analyze, accompany, and, if necessary, promote the exchange of information among the parties involved. Therefore, this study responds to the call of Madison et al. (2016) for additional research on the existence of information asymmetries between predecessors and family-internal successors—and the extent to which and in which situations such asymmetries occur. Thus, we ask the following research questions: What kind of information asymmetries exist in intrafamily business successions? How do the information asymmetries change during different phases of succession? What factors condition the extent of information asymmetries?

To answer these questions, we theoretically derive information asymmetries situations and categories from the business succession literature. Using these categories, we design a quantitative questionnaire, surveying 215 German family businesses with 83 predecessors and 132 successors.

This article aims to make several contributions to the literature on intrafamily business successions and agency behavior in family firms. First, our quantitative study provides new empirical data showing the existence of different information asymmetries in intrafamily successions, offering further evidence for agency costs in family businesses, especially between family members in very different subject areas. Thus, information asymmetries can be very heterogeneous, and this diversity is difficult to capture with standardized questions. Therefore, we created an index that provides insight into the extent of information asymmetries in family firms to enable the comparability of the extent of information asymmetries. This index will enable researchers and practitioners to easily estimate information asymmetries in family businesses and intrafamily successions, allowing a more global view of countering information asymmetries.

Second, we identify several areas in the phases of intrafamily succession where information asymmetries can occur. We show that these areas depend on the phase of the succession process, the number of actors involved, and their relationships and values. Thus, we contribute to the literature on succession processes and add knowledge about specific areas of conflicts that occur when information asymmetries exist. Thus, we increase the understanding of the antecedents of agency behavior in intrafamily business successions by disentangling information asymmetries.

Third, we show the first indications of which measures can contribute to the extent to which information asymmetries emerge and which measures family businesses take to promote the exchange of information and thus counteract information asymmetries. We offer evidence that a structured step-by-step succession process is a tool to professionalize family businesses and decrease information asymmetries (Le Breton-Miller et al., 2004). Through these insights, we provide information on how business families and advisors can deal with the exchange of information and promote it through the use of tools.

Theoretical background and hypotheses

Business successions are step-by-step processes with three phases

The succession of business management and ownership in family firms is widely recognized as a long, step-by-step process that occurs when family businesses have been successful on the market for generations (Ahlers et al., 2014). The recent research divides the intrafamily business succession process into phases (Le Breton-Miller et al., 2004; Michel & Kammerlander, 2015; Nordqvist et al., 2013) and identifies several success factors for a sustainable business transfer. Succession is a situation in which several contracts can exist (i.e., employment contracts for the family CEO before he or she holds any shares or contracts that govern ownership succession) (Lubatkin et al., 2007). Thus, we divide the succession process into three phases: the before phase, the during phase, and the after phase.

The before phase describes the succession before any management positions are transferred, determining the ground rules and the first stage of nurturing and developing the successors (Le Breton-Miller et al., 2004). During this time, family business owners make decisions, that is, whether and when a succession should occur (duration) in addition to the transfer conditions (and which financial and legal approach will be taken). This phase includes expectations regarding whether and for how long predecessors and successors should work together in the family business (teamwork). This aspect often results in expectations regarding the type of education the potential successors’ need (educational requirements) and whether experiences outside the family business are a useful precondition for succession (Chrisman et al., 1998; Schlepphorst & Moog, 2014). Whether successors enter the family business can depend on their commitment and willingness to succeed (commitment) (McMullen & Warnick, 2015). The predecessors may consider potential successors outside the family pool (Chua et al., 1999) (selection).

The during phase describes the selection process and how first ownership is transferred from one generation to another. At this stage, successors should receive hands-on training, improve their level of education and experience, and exercise increasing management power (Cabrera-Suárez et al., 2001; Cater & Justis, 2009). Successors are introduced to networks and invest in building social capital relevant to the family business (Steier, 2001). This period of working together is crucial but depends on the relationship between the involved actors, affecting expectations regarding teamwork and the time frame (duration, teamwork) (P. S. Davis & Harveston, 1999; Kellermanns & Eddleston, 2004). In this process stage, the selection of the final internal succession candidate(s) occurs (selection). The previous research indicates that there are selection criteria that must be fulfilled by the family-internal successor (educational requirements) (Chrisman et al., 1998; Schlepphorst & Moog, 2014). In addition to implicit and explicit selection criteria, the decisions of the predecessors often depend either on business logic or on family logic (Basco & Calabrò, 2017). Business logic can result in human or social capital being ranked higher in the selection criteria (selection, educational requirement, and social capital). In this situation, only the successors know their true commitment, abilities, and motivation to succeed in the family-internal succession (commitment) (Schell et al., 2019; Sharma & Irving, 2005). The financial transfer of shares of a family business can occur, mostly triggered by the predecessors, to maintain fairness within the family by giving all children some shares (Sharma & Irving, 2005) or to reduce tax disadvantages through step-by-step ownership transfer (financial/legal succession) (Molly et al., 2010). The financial transfer is crucial for the future successor’s position in the firm, as ownership is associated with power (finance).

The after phase describes the time beyond the selection of the final successors when the overall transfer of management power occurs and the roles of predecessors and successors change (Cater & Justis, 2009). In this stage, successors are finally the new leaders (formally) and can therefore access the company’s financial information (finance). However, the ownership transfer is not formally completed in this phase. Thus, both the control rights and the decision about when and how ownership will be transferred often remain with the predecessor (duration, financial, and legal succession) (Hernández-Trasobares & Galve-Górriz, 2016; Le Breton-Miller et al., 2004). Because the predecessor retains ownership, he or she can use control rights and demand a position on the advisory board (teamwork, duration) (Cater & Justis, 2009; P. S. Davis & Harveston, 1999). However, successors are in a position to adjust strategy and use their own networks to change important aspects such as advisors or banks, customers, and suppliers (Michel & Kammerlander, 2015). It becomes obvious if important information is missing such as financial or social networks (Steier, 2001).

Information asymmetries in the family-internal succession process

In contrast to the neoclassical theory where there is unlimited and perfect information between parties and contracts work without problems, the concept of information asymmetries assumes that information is neither easy to obtain nor homogeneous (different contract partners have different qualities and quantities of information), and it is neither perfect nor unlimited (Akerlof, 1970; Spence, 1974). This means that one party has more knowledge than the other in a pre- or post-contracting situation, especially with respect to motivation, behavior, and qualities.

As mentioned above, we propose that during family business successions, several contracting situations occur; thus, various types of information asymmetries can exist (Schulze et al., 2003, 2001). Due to the fact that in most family businesses the leadership hand-over occurs without or with only a bit of ownership transfer, we have a continuous principal–agent situation: Predecessors are the owners even when the successors take over the management position. These information asymmetries can occur in all three phases (J. H. Davis et al., 1997), causing problems for the succession process—or even prevent a successful handover.

The overall objective of a successful intrafamily succession process is the firm’s survival in the hands of the family (Cadieux, 2007) and the satisfaction of both family and business goals (McCann et al., 2001). Thus, the family-internal business succession process can be influenced by both family-related and business goals (Kotlar & De Massis, 2013). However, these goals can be diametrically opposed. There is often a negotiation process (Aparicio et al., 2017) among family members regarding appropriate goals regardless of their position in the firm (Jaskiewicz & Klein, 2007; Pieper et al., 2008). In the same context, intrafamily predecessors and successors may favor self-interest goals, and if that is the case, they will act to advance their own interests through opportunistic (Sieger et al., 2013) and often limited rational behavior culminating in information asymmetries among the contracting parties during intrafamily business successions (Madison et al., 2016).

The research shows that during the succession process, potential successors are given more responsibilities, thereby increasing power (Cabrera-Suárez et al., 2001). However, the predecessor also has power and can influence the information exchange among the parties. It can be assumed that the further the process advances, the fewer information asymmetries will exist (Handler, 1994) because of activities such as a long-lasting assessment and the nurturing, development, and renegotiation of contracts; however, until now, there has been no empirical evidence for this phenomenon (Le Breton-Miller et al., 2004; Madison et al., 2016; Schell et al., 2019). In addition, to reduce tax disadvantages, a step-by-step ownership transfer can occur involving both the potential successor and family members who will not receive management power (De Massis et al., 2008; Molly et al., 2010). This partial transfer of shares can be seen as a signal that this successor will ultimately be selected as the final management and ownership successor (Schell et al., 2019). This can, but does not have to, foster the information exchange process by building trust and better aligning individual interests. However, through the transfer of shares, the potential successor receives additional rights to access important documents and information such as contracts and balance sheets (Handler, 1994). Consequently, by ownership transfer, additional interests and engagement are connected, creating a demand for information. We argue that management and ownership transfers can in each case lead to information asymmetries being fostered but also reduced. For example, it is assumed that additional management power is accompanied by the legal right of information (Cabrera-Suárez et al., 2001). The responsibility for staff creates access to staff records and costs. These rights enable potential successors to obtain additional knowledge and information (Cabrera-Suárez et al., 2001). Accordingly, we propose the following hypothesis:

H1. Different kinds of information asymmetries can be observed in all phases of a family-internal succession process in a manner that decreases over time.

Transferring information to a group instead of one person requires additional resources (Avloniti et al., 2014). The more potential successors there are in the succession pool (children, nieces, nephews, others), that is, due to a cousin consortium (Gersick et al., 1997), the greater the likelihood of information asymmetries and individual interests and goals that are diametrically opposed (Basco, 2017; Taylor & Norris, 2000). In their qualitative study, in which they examine the transfer of network contacts to successors, Schell et al. (2018) point out that complexity increases when several potential successors are considered. It may even be necessary to transfer information from one successor to another (Schell et al., 2018). If several potential successors are involved in the process for a long time and thus compete or are held responsible for the exchange of information, it can fuel conflicts and thus possibly lead to information asymmetries, which are in turn caused or promoted by the conflicts (Jayantilal et al., 2016). This is especially likely to occur in the before and during phases of succession (Schulze et al., 2001), because in this phase, several people may be in the pool of successors; however, who is to be the final one has not yet been selected. Furthermore, in the during phase, all candidates may work in the company and be involved in entrepreneurial activities and therefore also be a part of communication processes (Nordqvist et al., 2013; Schell et al., 2019). Ahrens and colleagues (2015) underscore that CEO succession contests involve selectivity. In their study, they found that male family successors are chosen not because of higher human capital levels but because of the contest rulers’ gender preferences in favor of male family heirs (Ahrens et al., 2015). Consequently, even if it can be socially assumed that nepotism and, above all, the choice of the successor under the First Born Act no longer occurs in family businesses, study results still show that there are still selection logics that include factors such as gender. We propose that decreasing the number of potential successors earlier and choosing a successor will allow an earlier transfer of information to a limited pool of candidates (Cabrera-Suárez et al., 2001). Both—the predecessor and the successor—can diminish potential information asymmetries at this stage, declaring to the family and all stakeholders (Steier, 2001) about who will become the final successors—leading to higher levels of candidates’ commitment, generating more trust and diminishing the risk of information asymmetries (Sharma et al., 2001). In addition, the selection of successors gives individuals the opportunity, but also the responsibility, to obtain information independently (Cabrera-Suárez et al., 2001). This leads to the following hypothesis:

H2. More potential candidates lead to a higher degree of information asymmetries.

Regardless of the types of goals that individual family members might have during the succession process, such family members often share common basic values because they have been socialized in the same way (Astrachan Binz et al., 2017). The potential and actual successors’ general behavior can be influenced by their upbringing and shared stories about the family business or values from older generations (Kammerlander et al., 2015). The communication patterns in families are shaped by such socialization (Koerner & Fitzpatrick, 1997). Upbringing can also influence the successor’s relationship with both his or her family and the family firm. The socialization in families shapes the rules, values, and norms of individuals and the next generation.

Hillier et al. (2018) proposed that agency conflicts between shareholders and creditors are lower in family firms than in non-family firms. Yuan and Wu (2018) placed this study into a wider context and proposed to include values when studying family firms, emphasizing values as the “key determinant of family heterogeneity and family firm behavior” (Yuan & Wu, 2018, p. 284). They conclude that a value perspective may explain strategic behavior and family business dynamics, and they consequently developed a conceptual model of family values (Yuan & Wu, 2018). From their point of view, the behaviors of family firms are characterized by a linear connection between values, which influences strategic behavior and subsequently family firm dynamics, which in return influence the values of the family. Consequently, it makes sense to consider values, especially in family businesses. Values are above all individual and can also become group values if the social group negotiates them. The congruence of values reduces conflicts and creates space for communication. It is therefore particularly important in the succession situation that the actors involved align their values and share common values. As a result, sharing the same values can result in fewer information asymmetries. Thus, we formalize the following hypothesis:

H3. If the predecessors and family-internal successors share the same values, there will be fewer information asymmetries.

As in the general literature on information asymmetries and how to avoid them (Akerlof, 1970), the same effects would be expected in the context of intrafamily succession. This could be reached by either professionalizing (Dekker et al., 2015; Stewart & Hitt, 2012) or structuring the intrafamily succession process. In 1988, Lansberg discovered that a lack of succession planning is one of the primary reasons that many family firms do not outlive their founders. These plans can result in both formal and informal actions (Botero et al., 2015) such as a business succession plan and formal selection criteria for the choice of a successor (Schlepphorst & Moog, 2014) enabling a structured and long-term information exchange process (Cabrera-Suárez et al., 2001). Determining the company’s value and performing due diligence, along with ensuring the successor’s access to financial documents, can decrease information asymmetries (Wasserman, 2003; Wennberg et al., 2011). In addition, contracts with guidelines for behavior and the decision-making of incumbents and successors can foster information exchange (Aronoff et al., 2003).

As Chrisman et al. (2007) showed, monitoring family managers can increase a firm’s performance. They also argued that goal misalignment could have a negative impact on firm performance. Therefore, managing the goal alignment process through a strategically planned succession process enhances the possibility of a successful succession. Goal alignment can also be managed through the integration of governance structures as Zellweger and Kammerlander (2015) first described. Their study focused on later-generation family businesses and developed a framework for governance structures such as family offices and trusts and the agency costs that result from these structures. According to them, governance structures can either decrease or increase agency costs. We propose that the same concept applies to information asymmetries as antecedents and, thus, that the existence of governance structures, including clear responsibility for the business succession process and rules for managing communications, decreases information asymmetries (Botero et al., 2015; Suess, 2014). In summary, actions such as informal and formal tools and processes, including implemented governance structures, can minimize information asymmetries during and after succession.

H4. Actions such as informal and formal tools and processes minimize information asymmetries in internal succession and help to counteract their emergence.

Methodology

Research sample

We define our sample of family businesses as follows: (a) the firm should be a self-assessed family business, (b) at least 50% of the shares are held by family, and (c) one family member is involved in managing the firm. Moreover, the family business should either be preparing for a succession (before), be involved in an ongoing process (during), or should have completed the succession (after) (Chua et al., 1999). Following this idea, our dataset includes 27.4% before-succession firms, 32.1% during-succession firms, and 40.5% after-succession firms in regard to the hand-over of management and leadership position and no or only a partial hand-over of shares.

To assess these types of family businesses, we use data from Hoppenstedt, including the addresses of (5.1 million) German businesses and their family business status, size, and industry sector. A total of 10,000 family business addresses were randomly selected, mirroring the range of firms in the database with respect to age, size, industry sectors, and sales to generate a representative address pool. In 2015, a survey was provided to the participants either in a printed or in an identical online version via e-mail; 4.8% of the companies responded to the survey. To ensure that only predecessors and successors were surveyed, we clarified the role of the participant in both the firm and the succession process. Our final sample excluded all cases with missing values, outliers that could be identified as input errors, cases in which neither the predecessor nor the successor answered the survey, and cases in which the company did not fulfill the above-mentioned criteria. Our data cover firms in all three succession phases to catch every stage appropriately in the data, generating data on information asymmetries in internal family business successions.

To test whether a nonresponse bias was present, we analyzed whether the answers of the first respondents differed from the answers of the last respondents. We sorted the dataset by the return date and divided it into three parts (Oppenheim, 2000) and used one-way analysis of variance (ANOVA) in which the order of the returned questionnaires, in the form of the three groups, was used as a factor (Dehlen et al., 2014). We found no statistically significant differences between the mean values for any of the outcome variables by these groups (Armstrong & Overton, 1977; Chrisman et al., 2004). To assess the extent of the sample representativeness and the sample selection bias, we randomly selected the survey participants. In addition, we compared the descriptive data of our dataset to the descriptive data of other studies on family businesses. The average age of the firms in our dataset (73 years) was comparable to those of other datasets of German family businesses (e.g., Sieger et al., 2013: 75 years; Dehlen et al., 2014: 62 years). The average age of the owner-manager was also comparable across studies: 49.6 years in our data versus 45 years (Dehlen et al., 2014), 51 years (Zellweger et al., 2012), and 46 years (Sieger et al., 2013) in those studies. To assess common method bias, we designed the questionnaire and the order of the questions in a way that the respondents’ answers were not influenced by the researchers’ underlying expectations. In addition, we ensured the anonymity of all respondents to reduce any social desirability bias (Podsakoff et al., 2003). Furthermore, we performed a Harman’s single-factor test. An exploratory factor analysis with all variables in the regression (Model 8) led to a five-factor solution with eigenvalues greater than 1. Taken together, these factors explained 55.74% of the total variance. The first factor explained 15.74% of the variance, which suggests that common method bias was not a concern in our study (Podsakoff & Organ, 1986). A bias attributable to possible endogeneity could not be excluded because there are no appropriate instruments available to assess this in our independent variables (Hamilton & Nickerson, 2003).

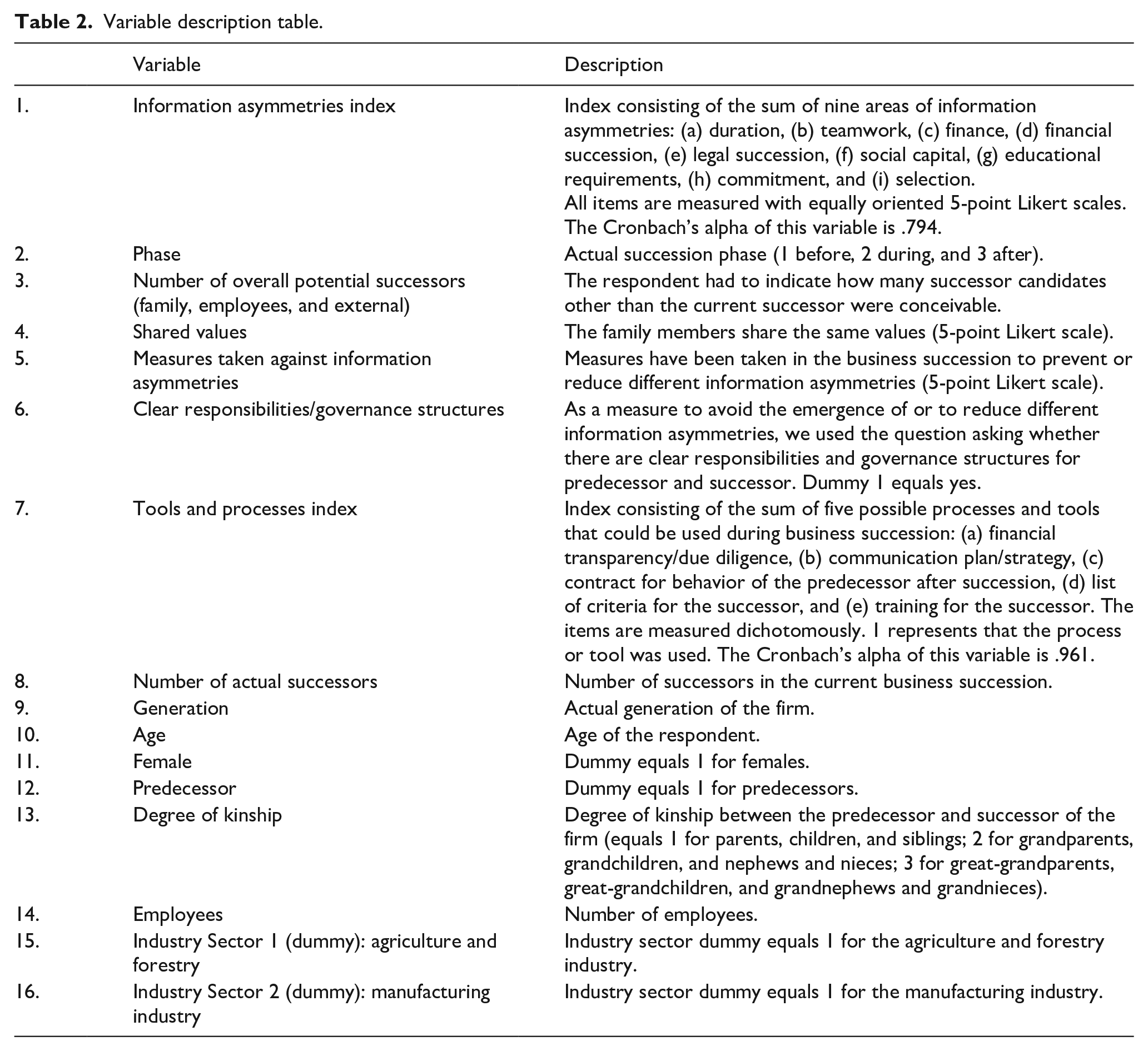

Variables

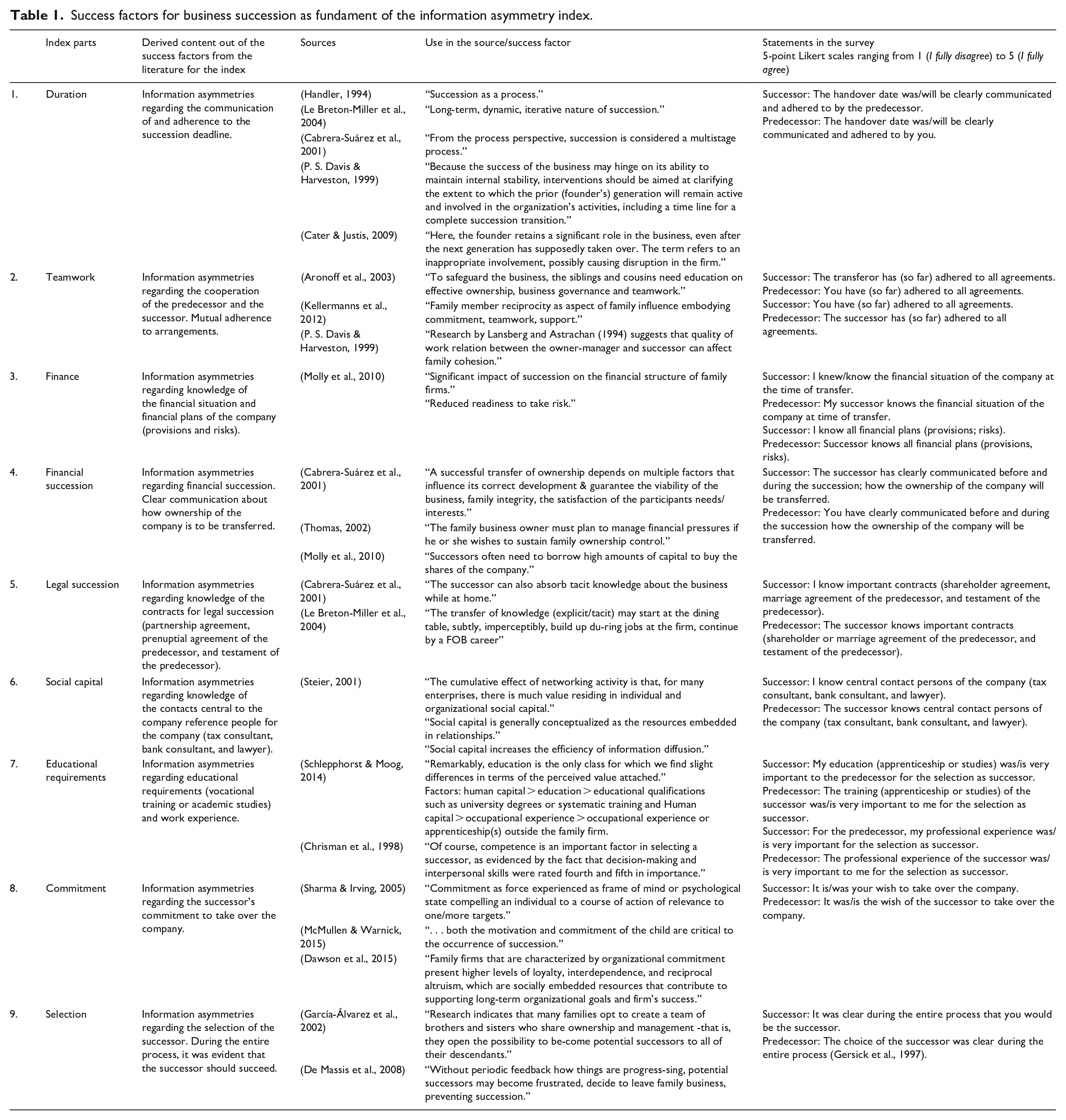

In this study, the focus is on one dependent variable—information asymmetries. Because the family business research does not provide a measurement scale for information asymmetries and more research is needed in this area (Madison et al., 2016), we first develop single-item measurements to check for information asymmetries and additionally create an index combining these single items measuring the existence and strength of information asymmetries overall. To achieve this, we thoroughly elaborated these single-item variables observing information asymmetries according to the state-of-the-art literature on family business succession (see Table 1).

Success factors for business succession as fundament of the information asymmetry index.

At the current stage, the areas of information asymmetries are mostly theoretically motivated and derived from the business succession literature (Zellweger & Kammerlander, 2015). Through a literature review, we identified success factors of planned intrafamily successions. We did this because when information asymmetries arise, the success of the transfer of a family business can be diminished or even completely impeded. To use these success factors, we propose that all involved actors must be aware of these success factors and have the same knowledge and, consequently, be able to fulfill and use these success factors. The identified success factors have been summarized thematically in the following categories: duration, teamwork, finance, financial succession, legal succession, social capital, educational requirements, commitment, and selection. Table 1 provides a detailed summary of the identified success factors derived from the literature, the questions we asked in the survey, and the categories of the index.

In the first step of the analysis, (single) items based on the above-mentioned literature review are used, and questions about whether, how, and in which fields, regarding the identified success factors, different information asymmetries can occur, and if they do, at which phases of the internal family business succession process. In the second step, we determined how these (single) items relate to each other and combined them into an aggregated variable, the information asymmetries index that was designed to measure the level of information asymmetries in general and overall. We are aware that generating an index means at the same time losing deeper information due to the aggregation of variables. However, to obtain a global indicator for the extent of information asymmetries in a company, we decided to create the index. At this stage of the research in this field—because a general measurement is missing as well as a comparison of information asymmetries across companies, the index solution seems more adequate to measure all kinds of information asymmetries to catch the heterogeneity of family businesses and the variety of possible information asymmetries at different phases in the process. The index is generated as the mean of the nine identified items (representing different areas of information asymmetries). First, the mean value for each category was calculated. Second, from these mean values, an overall mean value for the information asymmetries was generated for every surveyed case. The reliability of the information asymmetries index was tested with a Cronbach’s alpha (Cronbach, 1951), and it showed a satisfying value of .794. At this stage of the research, this general index covers all kind of information asymmetries to measure them on an aggregated level and thus to obtain a preliminary idea of whether there are information asymmetries at different stages and to what extent and to identify some of their antecedents or influencing factors.

The following independent variables were included in the analysis to examine the effects of different factors on information asymmetries, derived from the discussion of the current research in the field. The variable phase indicates in which stage the family-internal succession process of the respondent’s firm is classified (before, during, or after) (Le Breton-Miller et al., 2004; Nordqvist et al., 2013). As discussed above, information asymmetries should diminish over time from stage to stage. To measure shared values, a 5-point Likert-type scale is used, and the respondents had to disagree or agree with the following statement: “The family members share the same values.” This question was taken from the Family Influence on Power, Experience, and Culture (F-PEC) Scale from Astrachan et al. (2002). We added the number of overall potential successors to address the fact that more than one succession candidate is being considered and that this aspect could affect the emergence of information asymmetries.

To obtain preliminary insights regarding the effects of instruments and measures to decrease information asymmetries, three variables are generated. The first is measures taken where the respondents agreed or disagreed on a 5-point Likert-type scale on the question “Measures were taken in the business succession process to prevent or reduce information asymmetries.” The second is the measurement of clear responsibilities or governance structures following the recommendations of Zellweger and Kammerlander (2015) to determine whether there are clear responsibilities or governance structures for predecessors and successors to avoid the emergence of or reduce information asymmetries. These two independent variables are measured with single items because there are no validated constructs for the corresponding instruments. We do so because single items are easy to understand, do not require complex psychological backgrounds (Hair et al., 1998), and lead to shorter, easier-to-understand questionnaires without repetition or divergence (Petrescu, 2013). In addition, studies have demonstrated that there are no differences in the predictive validity of multiple-item and single-item measures (Bergkvist & Rossiter, 2007). Finally, the tools and processes index is used to calculate the sum of five often-mentioned processes and tools in the succession literature to plan the family-internal business succession process: (a) financial transparency/due diligence, (b) communication plan/strategy, (c) contract for the behavior of the predecessor after succession, (d) list of criteria for successors, and (e) training for successors (Molly et al., 2010; Steier, 2001). These items were measured dichotomously and coded as 1 when the process or tool was used and 0 if not. The reliability of the tools and processes index showed a high Cronbach’s alpha value (.961).

Control variables: To ensure that other environmental factors not captured by our theoretical discussion do not affect our results, several control variables are included. The number of actual successors shows how many actual successors are involved in the succession process (Gersick et al., 1997). By asking the respondents about the number of generations running the firm, we test for an influence of possible learning effects from previous successions (Cabrera-Suárez et al., 2001). Furthermore, we add the age (metric) of the respondent as well as the gender (dummy variable) coded as 1 when the respondent is female (Sieger et al., 2013). In addition, we add the role as predecessor coded as 1 when the respondent is the predecessor to check for the influence on whether the predecessor or the successor answers the questionnaire.

Furthermore, the degree of kinship between the predecessor and successor of the firm may influence information asymmetries because the more closely related the individuals, the more familiar they might be with each other and the firm. Firm size may also influence information asymmetries; therefore, we control for the number of employees, which is a generally accepted measure of company size. It has been shown that small, medium, and large firms have significantly different (governance and organizational) structures (Haveman, 1993) and that larger companies have a greater number of differing interests at stake. To check for the general impact of industry, the respondents had to classify their firm as one of 22 industries measured by the European Community’s Nomenclature of Economic Activities (NACE) codes (European Commission NACE Rev. 2). The answers are aggregated into three sectors: (a) agriculture and forestry, (b) the manufacturing industry, and (c) service. We use service as a reference category in our regression analyses. In Table 2, we provide a detailed overview of the variables in the regression models and explain their operationalization.

Variable description table.

Analyses and results

Descriptive data

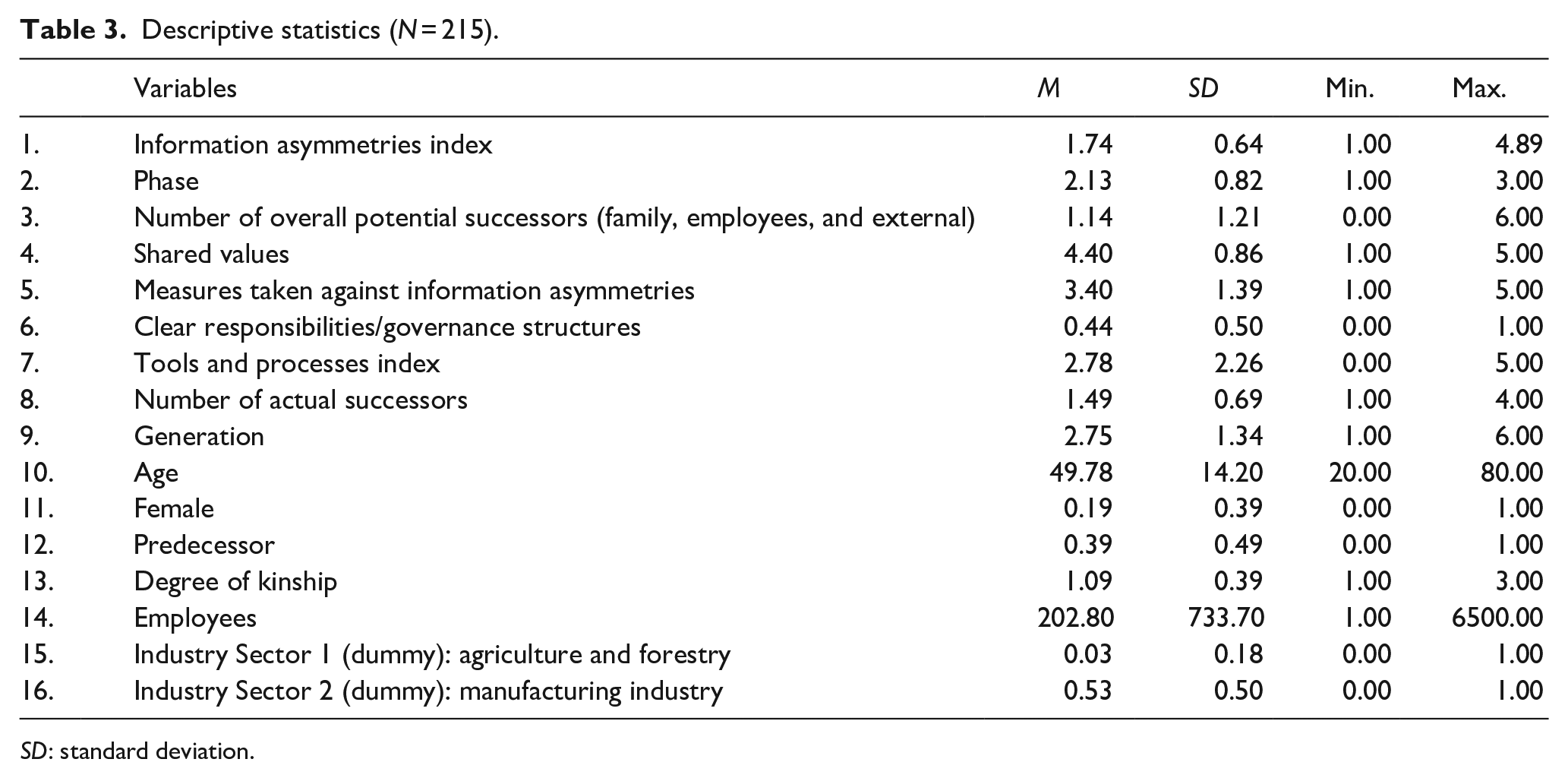

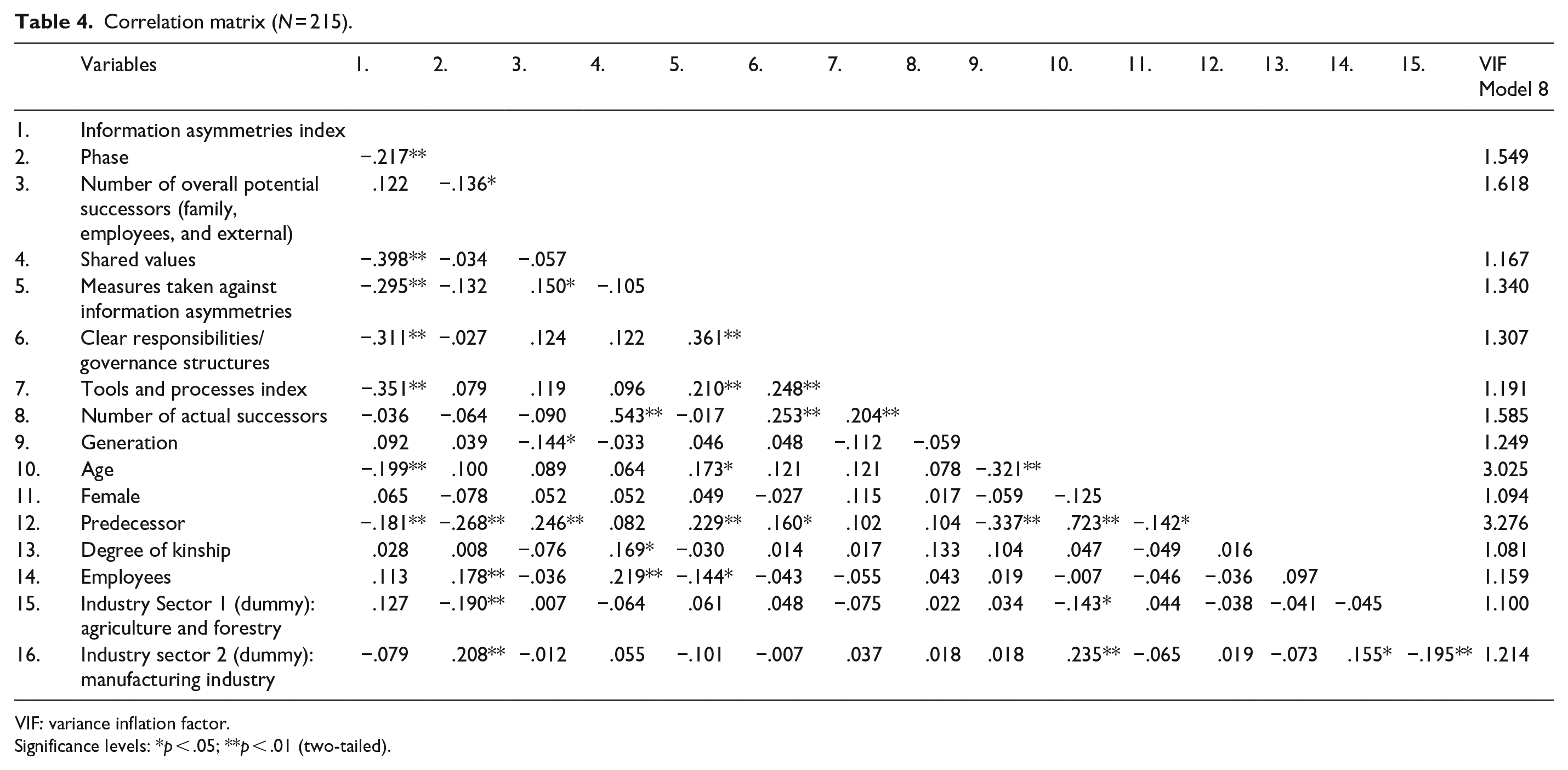

Table 3 presents the mean, standard deviation, minimum and maximum values of the dependent and the independent and control variables used. Table 4 shows the correlations and variance inflation factor (VIF). The tables show that there are correlations and that the VIF indicator ranges between 1.094 and 3.276, which is below the recommended threshold value. Thus, no multicollinearity is present in our data (Hair et al., 1998). The highest VIF value (3.276) is caused by the expected high correlation between the characteristic of being a predecessor and the high age of a person (.723). The high correlation between the number of overall potential successors and the number of actual successors (.543) was also to be expected; however, neither variable has an impact on the model.

Descriptive statistics (N = 215).

SD: standard deviation.

Correlation matrix (N = 215).

VIF: variance inflation factor.

Significance levels: *p < .05; **p < .01 (two-tailed).

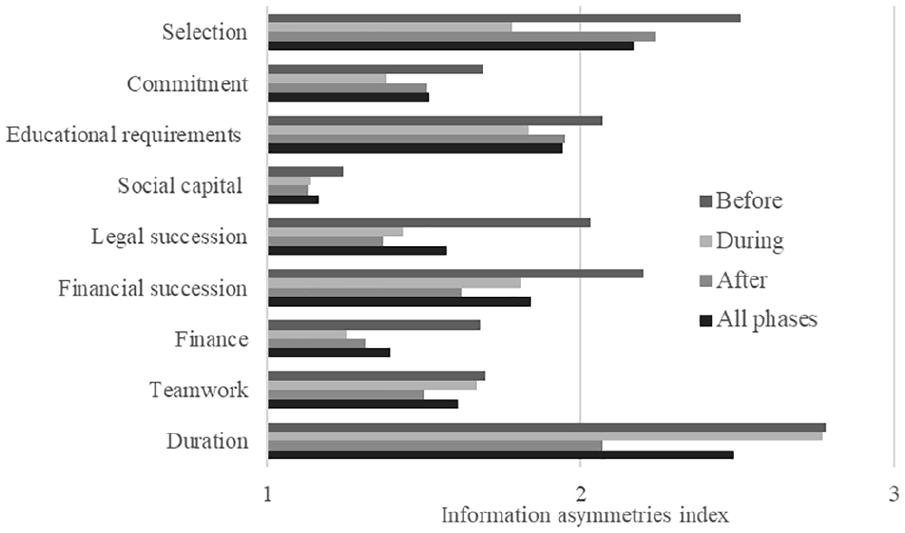

The first goal of the article is to observe information asymmetries in family-internal successions at different stages. Thus, the single-item variables measuring information asymmetries were analyzed as well as the aggregated index. Figure 1 provides an overview of these data.

Information asymmetries by succession phases.

Figure 1 delivers the data that information asymmetries in the intrafamily business succession process can be observed in all subject areas derived from the literature. We especially observe information asymmetries concerning timing and selection issues regardless of the phase of the succession process. Moreover, the data provide preliminary insights regarding all information asymmetries as single items as well as the index that in the before phase, these values are the highest decreasing over time until the after phase (Le Breton-Miller et al., 2004). The aggregation of the single items to the index does not influence these results. With the existence of information asymmetries and a decline over time in the family-internal succession process, these findings provide preliminary evidence to answer our research questions and support our first hypothesis even on a descriptive level that does not deliver any causal results.

Regression analysis

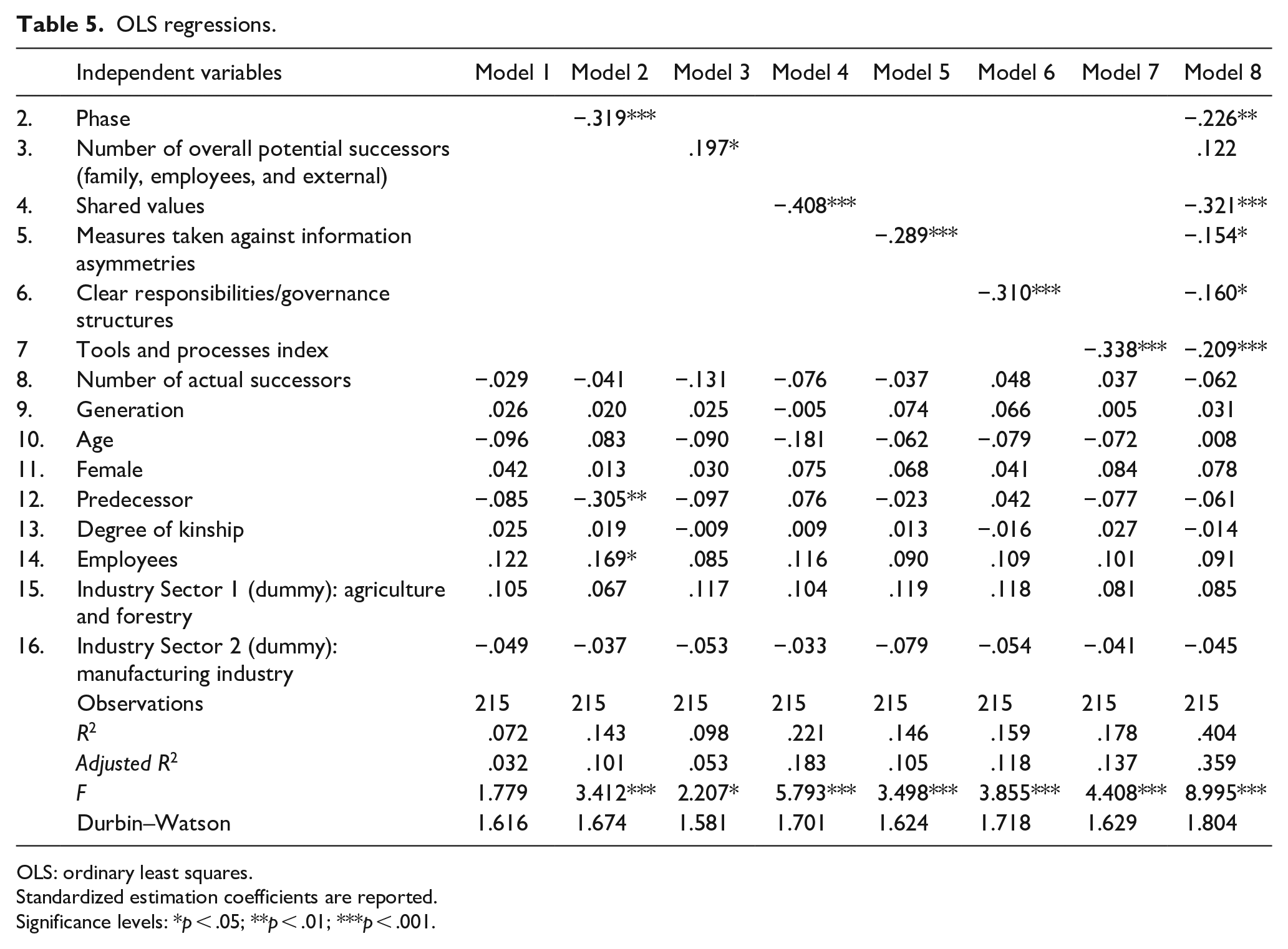

We used ordinary least squares (OLS) regressions to test our hypotheses and the discussed effects in eight models as shown in Table 5. In the first regression model, the control variables are included. In the subsequent regressions, Models 2, 3, and 4 are run to test the single effect of the main independent variables discussed in the theory section. Models 5, 6, and 7 check the effect of the variables that might decrease information asymmetries. In the final model (Model 8), all variables are integrated to check for the robustness of the former results. All models are significant (F-test), and including additional variables provides a better explanation of the spread of information asymmetries (adjusted R2).

OLS regressions.

OLS: ordinary least squares.

Standardized estimation coefficients are reported.

Significance levels: *p < .05; **p < .01; ***p < .001.

The first regressions testing the influence of the phases of family-internal succession processes show a highly significant impact of family values and an effect of the number of overall potential successors (Table 5, Models 2, 3, and 4). These effects are observed with stronger and more information asymmetries in the earlier stages and fewer in the later stages (H1). This result remains robust when testing the phases as dummy variables with the during phase as an anchor. In addition, the number of overall potential successors significantly increased the information asymmetries in all phases (H2). In the overall model, the effect of the number of overall potential successors is not significant (p < .082). This is due to the correlation with the phase that is also included in the overall model and suggests that the negative influence of the number of overall potential successors solves itself simultaneously with the progress through the phases within the succession process.

A strong, significant negative effect of the common and shared values of predecessors and successors on information asymmetries (H3) is observed: The fewer shared values there are between the parties, the more the information asymmetries will increase. These results remained robust in all models.

The second set of regressions (Table 5, Models 5, 6, and 7) reveal highly significant results showing a decrease in information asymmetries when the discussed measures were implemented during the succession process (H4). In addition, Models 6 and 7 present significant effects of clear responsibilities/governance structures and the tools and processes of planning specific issues even during the succession process, decreasing information asymmetries significantly in both cases (H4) when these variables are included. Again, the results remain robust in the overall model.

It is also shown, through the insignificance of the control variables, that the emergence of information asymmetries in intrafamily business succession is independent of the number of actual successors, the generation of the firm, the age of the respondent, the gender of the respondent, the degree of kinship, the number of employees, or the industry.

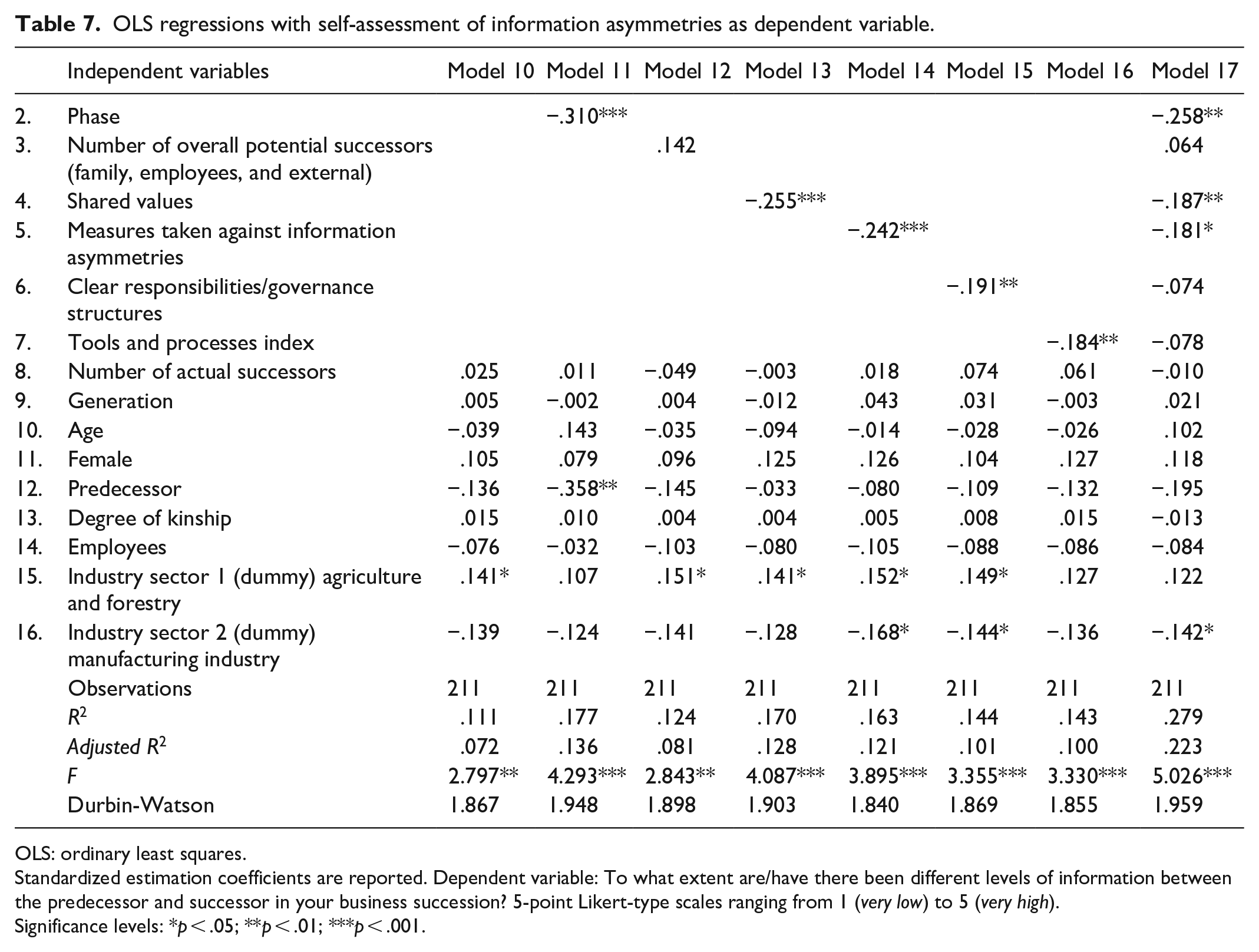

To test the robustness of the results, other industry control variables were included (22 industry dummies instead of the industry sectors) and obtained the same significance levels, directions, and effect sizes. Furthermore, the same regression models were analyzed with information asymmetries as the dependent variable measured as a self-assessment question generating similar significance levels, directions, and effect sizes, which supports the robustness of our results. Please see Appendix I for more information on these results.

Discussion and contributions

Although it is widely claimed that there is limited information on the asymmetries and agency problems among family members in family business, this is not self-evident, and results are often at a qualitative descriptive level, delivering mixed observations (Madison et al., 2016). Most of these studies neglect the heterogeneity, the importance of values, and the numbers and generations of the involved family members and owners, which might foster information asymmetries (Basco, 2017; Muñoz-Bullon et al., 2018; Nordqvist et al., 2014). In addition, even recent studies finding the first empirical support for the notion that information asymmetries and agency problems in family business exist fail to disentangle the different kind of information asymmetries at different stages of succession (Madison et al., 2016). Thus, a more detailed understanding of how information asymmetries occur, and in which areas, is missing. In light of these results, we argue that it is beneficial to further address the question of whether and to what extent do certain kind of information asymmetries occur in family firms during the intrafamily succession process: What kind of information asymmetries exist in intrafamily successions? How do the information asymmetries change during different phases of succession? What factors condition the extent of information asymmetries? Our study is one of the first to provide quantitative data observing various information asymmetries in family firms in different stages of succession. By measuring single-item effects as well as the development of an information asymmetry index, we provide empirical evidence of the extent of information asymmetries and aspects influencing the level and kind at the different succession process stages.

First, we were able to show that during the succession process, information asymmetries exist in general, and the phase of the succession influences the extent of such asymmetries. These findings contribute to the family business research by supporting the ongoing discussion on existing information asymmetries in intrafamily business succession and delivering empirical evidence supporting the idea of antecedents of agency costs (Zellweger & Kammerlander, 2015). This insight can thus also provide the basis for research strands such as the “advisors in family firms” strand. Only when it is known which information is relevant, where there are information deficits, and where the actors involved need support can advisory in family firms be effective (Bertschi-Michel et al., 2019; Michel & Kammerlander, 2015; Strike et al., 2018). That agency’s behavior can also or especially arise during succession, which Madison et al. (2016) already suspected in their paper, is confirmed by the concrete identification of information asymmetries.

Second, we can show that at the beginning of the succession process, information asymmetries are more widely spread than in the later stages (H1). Thus, information asymmetries decrease over time due to the changing roles and influence of the incumbents and successors over time. This is especially an increase of power for successors, enabling them to obtain additional information about, that is, the financial situation of the firm and critical documents or contracts (Cater & Justis, 2009). Specifically, the findings provide clear suggestions for which type of crucial information must be exchanged during succession, either formally or informally to make a generational transfer of the family firm successful. Thus, this research strongly supports the need for a planned, well documented, and transparent intrafamily business succession. Our study shows that, especially in the before and during phases, information asymmetries occur. In line with Schell et al. (2018), who show that there is a signaling process during the business succession situation to minimize information asymmetries over time, this study provides insights that information asymmetries in the categories of the selection criteria are highly relevant, especially regarding teamwork issues between successors and predecessors, the duration of the succession process and commitment (McMullen & Warnick, 2015). Therefore, our study underscores the need for family firms to undertake strategic planning, nurturing programs for potential candidates and a planned step-by-step handover of the family firm, through these actions reducing information asymmetries (Lansberg, 1988). This is also because predecessors have time to verify the commitment level of potential successors and assess their skills in running and leading a business (Basco & Calabrò, 2017).

Third, showing that information asymmetries increase by a greater number of potential successors (H2), our results strongly support the need for communication and planning regarding a clear decision about who should succeed and the selection criteria, supporting the recommendations of the previous research (Schlepphorst & Moog, 2014). The complexity of information exchange increases with the number of people involved (Schell et al., 2018). In addition, it can be assumed that conflicts between siblings may still be stirred up (Jayantilal et al., 2016). This condition gives indications that a consciousness, for example, via the signaling game, can be useful in structuring the succession process and minimizing complexity.

Fourth, our research highlights the importance of family members sharing values and thus a form of family bonding (Jaskiewicz et al., 2015). Individual family members have their own expectations and goals in the ongoing and complex negotiation process of the family’s internal business succession (Astrachan Binz et al., 2017). Common values are beneficial for information exchange, and they decrease information asymmetries (Jaskiewicz & Klein, 2007). This makes it easier to align diversified goals over time if all actors in the process share almost the same values and norms (Frank et al., 2010). This behavior of problem-solving and handling goal alignment is closely connected with stakeholders’ satisfaction of the transfer process (Le Breton-Miller et al., 2004). A lack of information can result in dissatisfied people who feel uninformed and unable to make clear decisions, which is crucial for the long-term survival of a family business.

Finally, the outcomes of the study theoretically and empirically underscore the need to implement (clear) governance structures (Stewart & Hitt, 2012; Suess, 2014) or strategic advisors to diminish and overcome information asymmetries (Michel & Kammerlander, 2015; Strike et al., 2018) to reach a successful succession. The support of H4 suggests that instruments from personnel economics such as monitoring (Lazear, 1998; Schulze et al., 2003) to structure the succession and information exchange process can decrease information asymmetries in the family-internal succession in accordance with the literature on professionalizing family firms (Stewart & Hitt, 2012; Wiklund et al., 2013).

Implications for practice

This study also has important practical implications. First, it is a key finding that information asymmetries in family firms are caused by the heterogeneity of interests among family members (Zellweger & Kammerlander, 2015) in contrast to the idea that family business members may suggest that there are no blind spots among relatives with close connections. To be aware of this phenomenon is important to instate continuous communication to decrease and overcome information asymmetries throughout the various stages of succession. Second, our study shows that family members of different generations have various goals and intentions (Aparicio et al., 2017), which may produce information asymmetries or agency costs. The existence of shared values among predecessors and successors can decrease information asymmetries. Yuan and Wu (2018) underscore that values in family firms could be a main source of family firm heterogeneity. They developed a family business value model based on Schwartz’ bipolar value model. Schwartz (1994) argues that four higher-order value types oppose each other to a certain extent and form two bipolar value dimensions. For example, it is justifiable that values emphasizing change, own thought, and action (openness to change—OC) oppose values emphasizing on traditional practices, self-restriction, and security (conservation—C). Similarly, values focusing on personal success, power, and authority (self-enhancement—SE) oppose values focusing on the general benefit and welfare of others (self-transcendence—ST). It can be assumed that an awareness of the different prevailing values in family businesses can be useful. In addition, certain value orientations could have a positive (openness to change) impact and others a negative (conversation) impact on business succession and information sharing. For example, it is a good idea to have advisors accompany this process who are trusted by all the actors involved (Michel & Kammerlander, 2015; Strike et al., 2018).

This finding highlights the importance of the upbringing of potential successors in multigenerational family businesses (Jaskiewicz et al., 2015) and the sharing of values regarding family and business being crucial to the success of negotiation agreements and succession (Kotlar & De Massis, 2013). Third, our study reveals that the less informed potential successors in the pool for succession are—regarding selection criteria or who might be a successor—the more information asymmetries may exist. These findings support the need for clear and fair communication to develop a transparent plan for a succession supported by all family members—with governance structures and milestones significantly diminishing information asymmetries (Schlepphorst & Moog, 2014). Relevant actors should know about such asymmetries and address the challenges they present to develop family businesses sustainably, and consultancies or politicians should make clear statements acknowledging the existence of information asymmetries.

Limitations, future research, and conclusion

Despite the contributions of our study, certain limitations should be kept in mind when considering our results. First, the outcomes rely on a single informant per firm and the subjective nature of data. However, this trade-off must be weighed against the current missing insight and the complicated access to obtain data on information asymmetries in family firms. Future research should collect dyadic data for a deeper understanding of all involved actors (Gooty & Yammarino, 2011). Second, our data underscore the existence of information asymmetries but offer little information regarding the concrete effects of information asymmetries, that is, how and to what extent they cause agency problems such as adverse selection or moral hazard. Thus, further research should focus more on the effects. Although, for example, the study by Schell et al. (2019) shows that a signaling process takes place during the succession process that reduces information asymmetries with regard to the selection of successors, further possibilities for dealing with information asymmetries, as well as the consequences thereof, remain unexplored to date. It might be helpful for research and practice to investigate these underlying effects. However, we report results on how family firms can either overcome information asymmetries or handle interactions of heterogeneous interests to decrease such interests. Furthermore, as often occurs in the family business research, our study is based on successful German family firms that are still active in the market; thus, those firms could successfully address information asymmetries by finding appropriate solutions. Due to this survival bias, our data cannot answer the question of information asymmetries that lead to failure in family business. Finally, the state of information of predecessors and successors changes over time. Thus, working with cross-sectional data in our study limits the analysis of change processes over time. Nevertheless, we have delivered initial insights into this topic. However, future research should undertake longitudinal studies to offer further insights into the dynamics of information asymmetries. Nevertheless, our study generates preliminary evidence helping to professionalize the planning and execution of succession processes. Even with these limitations in mind, we are confident that our results contribute to the research on family-internal business succession processes, information asymmetries, and strategy.

This study shows that information asymmetries exist in family businesses during intrafamily successions. We present new theoretical and empirical insights into how information asymmetries can be traced back to family structures and phases in the succession process and deliver parallel insights into how these issues can be overcome, that is, family firms can implement processes, planning, and organizational and governance structures as tools to decrease information asymmetries throughout the succession process. The study also delivers evidence that communication in families and family firms is important as a function of information exchange. Beyond these contributions, further research is needed to affirm the agency behavior of family members in family firms, further investigating how family firms address agency behavior during the succession situation and in a dynamic setting as well as the outcomes of information asymmetries.

Footnotes

Appendix 1

OLS regressions with self-assessment of information asymmetries as dependent variable.

| Independent variables | Model 10 | Model 11 | Model 12 | Model 13 | Model 14 | Model 15 | Model 16 | Model 17 | |

|---|---|---|---|---|---|---|---|---|---|

| 2. | Phase | −.310*** | −.258** | ||||||

| 3. | Number of overall potential successors (family, employees, and external) | .142 | .064 | ||||||

| 4. | Shared values | −.255*** | −.187** | ||||||

| 5. | Measures taken against information asymmetries | −.242*** | −.181* | ||||||

| 6. | Clear responsibilities/governance structures | −.191** | −.074 | ||||||

| 7. | Tools and processes index | −.184** | −.078 | ||||||

| 8. | Number of actual successors | .025 | .011 | −.049 | −.003 | .018 | .074 | .061 | −.010 |

| 9. | Generation | .005 | −.002 | .004 | −.012 | .043 | .031 | −.003 | .021 |

| 10. | Age | −.039 | .143 | −.035 | −.094 | −.014 | −.028 | −.026 | .102 |

| 11. | Female | .105 | .079 | .096 | .125 | .126 | .104 | .127 | .118 |

| 12. | Predecessor | −.136 | −.358** | −.145 | −.033 | −.080 | −.109 | −.132 | −.195 |

| 13. | Degree of kinship | .015 | .010 | .004 | .004 | .005 | .008 | .015 | −.013 |

| 14. | Employees | −.076 | −.032 | −.103 | −.080 | −.105 | −.088 | −.086 | −.084 |

| 15. | Industry sector 1 (dummy) agriculture and forestry | .141* | .107 | .151* | .141* | .152* | .149* | .127 | .122 |

| 16. | Industry sector 2 (dummy) manufacturing industry | −.139 | −.124 | −.141 | −.128 | −.168* | −.144* | −.136 | −.142* |

| Observations | 211 | 211 | 211 | 211 | 211 | 211 | 211 | 211 | |

| R 2 | .111 | .177 | .124 | .170 | .163 | .144 | .143 | .279 | |

| Adjusted R 2 | .072 | .136 | .081 | .128 | .121 | .101 | .100 | .223 | |

| F | 2.797** | 4.293*** | 2.843** | 4.087*** | 3.895*** | 3.355*** | 3.330*** | 5.026*** | |

| Durbin-Watson | 1.867 | 1.948 | 1.898 | 1.903 | 1.840 | 1.869 | 1.855 | 1.959 |

OLS: ordinary least squares.

Standardized estimation coefficients are reported. Dependent variable: To what extent are/have there been different levels of information between the predecessor and successor in your business succession? 5-point Likert-type scales ranging from 1 (very low) to 5 (very high).

Significance levels: *p < .05; **p < .01; ***p < .001.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.