Abstract

The international management literature has presented inconclusive results about the effect of institutional voids in a host country on entrant firms’ resource commitment. With the lens of institutional theory and transaction cost theory, this article examines how institutional voids in an emerging market influence a firm’s decision to move resources in that market. Resource commitment in an emerging market is examined in terms of the degree of control of the entry strategy employed. The theory presented argues that as institutional voids in a firm’s host country escalate, the firm sets out different priority actions to mitigate behavioral and environmental uncertainties in the host country, that in turn affect the degree of control of its entry modes. By relying on a sample of 90 Italian firms operating in China between 2001 and 2010, the results support the hypothesis that the institutional voids–entry mode degree of control relationship displays an inverted U-shape.

Introduction

Companies cannot operate in emerging markets without encountering institutional voids, but once they identify the voids that will shape the environment for their businesses, they can find ways to overcome them. (Khanna & Palepu, 2010, p. 40) International entry mode choices are most usefully and tractably viewed as a tradeoff between control and the cost of resource commitments, often under conditions of considerable risk and uncertainty. (Anderson & Gatignon, 1986, p. 3)

Key strategic decisions concerning a firm’s resource commitment in a foreign market, that is, the extent to which a firm controls dedicated assets—physical, intellectual, or human—in the host country that cannot be redeployed to another country without costs (Anderson & Gatignon, 1986; Hill et al., 1990; Petersen & Pedersen, 1999), are known to be driven by various factors. These include reduction in investment risks, economies of scale, knowledge acquisition (Chen & Hu, 2002; Song, 2017), transaction cost reduction (Anderson & Gatignon, 1986; Elia et al., 2014; Hill et al., 1990; Stevens & Makarius, 2015), and the ultimate goal of opening up new revenue streams (Hitt et al., 2006). Within this literature, some authors have focused on the role of institutions in the host country as a factor that may considerably influence entrant firms’ decisions about the amount of resources to move abroad (e.g., Wright et al., 2005). Institutions are “intermediaries [. . .] that insert themselves between a potential buyer and seller to bring these actors together and reduce transaction costs” (Khanna & Palepu, 2010, p. 54). 1 These institutions play a central role in the market economy; they serve as the main pillars on which market mechanisms are supported (North, 1990). If institutions are weak or absent in the market, then institutional voids are said to exist (Khanna & Palepu, 1997, 2010). Khanna et al. (2005) explained that institutional voids are particularly evident in emerging economies, where the lack of market-supporting institutions is likely to increase transaction costs for entrant firms and severely constrain their ability to exploit the benefits of moving resources in these markets. Although institutional voids in emerging markets represent a peculiar challenge for potential entrants, the extant literature presents different and contrasting recommendations on the amount of resources a firm should commit when entering these markets (for a recent meta-analytic review, see Giachetti et al., 2019).

In this article, using the lens of institutional theory and transaction cost economics in international business (e.g., Brouthers & Brouthers, 2003; Gatignon & Anderson, 1988; Yiu & Makino, 2002), we take the perspectives of firms entering an emerging market to analyze how institutional voids in that market influence the resource commitment of those firms. Consistent with the extant literature, we examine a firm’s resource commitment in a foreign country in terms of entry mode degree of control (Giachetti et al., 2019), that is, the extent to which a firm exercises control over its operations when entering a foreign country, which is intellectually rooted in the entry mode literature (Anderson & Gatignon, 1986; Hill et al., 1990; Isobe et al., 2000; Woodcock et al., 1994).

This article is motivated by several gaps in literature. First, despite the growing attention of literature on the institutional voids-resource commitment relationship, results are surprisingly mixed offering no clear consensus (see Table 1A in Appendix). Some authors theorized and found empirical support for a positive relationship between the level of institutional voids in the host country and the entrant firm’s entry mode degree of control (e.g., Chang et al., 2012; Luo, 2001). Other studies have shown that in the presence of institutional voids, firms prefer entry modes with a low degree of control (e.g., Álvarez & Marín, 2010; Brouthers & Brouthers, 2003; Meyer et al., 2009; Sanchez-Peinado et al., 2007; Yiu & Makino, 2002). Finally, other authors found the relationship not to be significant (Ang & Michailova, 2008; Elia et al., 2014). We propose and test a model aimed at finding an explanation for the contrasting theoretical arguments and results offered by the extant literature. To develop our theory, we build on transaction cost theorists’ observation that firms are exposed to two contrasting forces when entering emerging countries: the need to mitigate behavioral uncertainty (arising from possible opportunistic behaviors of host country partners) by increasing control over foreign partners, and the need to mitigate environmental uncertainty (resulting from the volatility of environmental conditions in a host country) by reducing control over assets in a foreign country (Brouthers & Nakos, 2004; Giachetti et al., 2019; Pla-Barber et al., 2010). We argue that as institutional voids in a firm’s host country escalate from low to high, the firm sets out different priority actions to mitigate the two types of uncertainty, and this results in an inverted U-shaped relationship between institutional voids and entry mode degree of control.

Second, there is a dearth of empirical studies examining how firms entering an emerging market encounter institutional voids differently, and how these voids influence the decisions about resource commitment. This gap is particularly important because “different [firms] are not uniform in the ways in which they rely on market institutions, [meaning that] some [firms] are more institution-intensive than others” (Khanna & Palepu, 2010, p. 28). In fact, “institutions not only vary markedly between countries [. . .], but also within them” (Chan et al., 2010, p. 1228). In turn, the choice of different firms to enter the same emerging country may be conditioned differently by the extent to which institutional voids are embedded in their business environment (Hitt & Xu, 2016).

Third, from a methodological perspective, this article responds to a specific call in the international business literature to explore other ways of operationalizing the strength of market-supporting institutions (Garrido et al., 2014; Orr & Scott, 2008). Previous empirical research has measured the strength of market-supporting institutions by combining various indicators related to a country’s economic freedom and institutional development, collected from secondary sources (e.g., Meyer et al., 2009), like the World Bank, International Monetary Fund, and Heritage Foundation. However, these indicators offer an aggregate level of institutional development of a country and do not necessarily reflect the extent to which the management of an entrant firm perceives its business in the emerging market to be affected by voids in the institutional environment (Orr & Scott, 2008). In fact,

such ratings usually fail to account for the fact that the levels of policy risk vary among different investors in a country, some of whom may adapt their business practices to local norms and lobby key policy makers better than others do. (Henisz & Zelner, 2010, p. 93)

The need to fully explicate the influence of individual actions and perceptions about the environment on firm strategy has been recently remarked also by authors in the micro-foundations of strategy literature (Felin & Foss, 2005). In this article, by means of questionnaires, we develop a subjective measure of institutional voids based on CEOs’ perception about the degree to which weak market-supporting institutions in the host country have hampered the firm entry process.

Theory background and hypothesis

Institutional voids in emerging markets and firms’ entry mode degree of control

Within the international business literature, authors have long examined the opportunities that firms based in developed economies may exploit by entering and then moving resources in developing countries (Khanna et al., 2005). Since the early 1990s, developing countries have been the engine of growth for products and services of most multinational companies (MNCs). Firms can reduce costs by locating manufacturing facilities in those areas, where manpower and trained managers are relatively inexpensive (Dagnino et al., 2019; Lampel & Giachetti, 2013). As for those developed country-based firms entering in developing countries with sales activities, successful ones have been those designing strategies for doing business that are different from those they use at home (Khanna & Palepu, 1997). Those firms that took the trouble to understand the institutional differences between countries, and how to adapt the use of resources differently depending on the peculiarities of the host institutional environment, were the most successful (Meyer et al., 2009).

In fact, firms operating in foreign markets encounter different institutional environments that present more diverse challenges than in their home markets. Especially in the case of developed country-based firms operating in their home country or other developed countries, they rely on well-established market-supporting institutions such as specialized market intermediaries, regulatory systems, and contract-enforcing mechanisms (Khanna et al., 2005) to function. However, the story is very different when firms decide to enter into emerging markets. Unlike in developed countries, emerging markets lack some of these market-supporting institutions, thus forcing foreign entrants to cope with institutional voids (Khanna & Palepu, 2010).

As noted by Khanna and Palepu (2010), firms operating in a given country are not uniform in the way they experience a country’s market-supporting institutions. For example, a firm may find a lack of specialized intermediaries in the product market, whereas it may experience an abundance of specialized intermediaries in the labor and capital markets. Another firm operating in the same country may instead encounter unreliable intermediaries in the labor and capital markets but highly efficient intermediaries in the product market. These differences in the way firms entering the same country experience institutional voids can be due, for example, to their different strategic choices, management skills, or business models. Hence, firms whose business relies heavily on the emerging country’s institutions are likely to face higher transaction costs and have less efficient operations, whereas firms that depend less on the emerging country’s institutions are less likely to be influenced by institutional voids and can better benefit from the advantages presented by the emerging country and convert them into more effective competitive strategies to survive in such a turbulent and uncertain environment (Giachetti, 2016; Hoskisson et al., 2000). The extent to which a firm perceives its business to be dependent on a host country’s weak institutions may affect the resources the firm will put into action when entering that country.

Common entry strategies employed in foreign markets include wholly owned subsidiaries, joint ventures, franchising and licensing, and exports (Anderson & Gatignon, 1986; Hill et al., 1990; Johnson & Tellis, 2008), and these entry modes represent different levels of resource commitment expressed in terms of control over foreign operations. Wholly owned subsidiaries have the highest resource commitment, followed by joint ventures, franchising and licensing, and exports (Hill et al., 1990; Woodcock et al., 1994). In what follows, we examine how a firm’s decision to increase resource commitment in terms of control over its entry mode in an emerging market changes depending on the level of institutional voids experienced by the firm in that market. Our argument is based on previous authors’ observation that firms are exposed to two simultaneous forces when entering emerging countries: the need to mitigate both behavioral and environmental uncertainty (Giachetti et al., 2019).

Moreover, as highlighted in the “Introduction” section, the theory and empirical analysis we present in the rest of this article are centered on managers’ perception of institutional voids. In fact, firms within the same industry might respond differently to institutional voids they encounter in the same host country because of different “subjective” points of view of their top managers. Therefore, it is not the host country environment per se that affects managers’ entry decisions, but how each individual firm’s management perceives these voids to constrain their strategic decisions (Orr & Scott, 2008).

Behavioral and environmental uncertainty in emerging markets

Transaction cost scholars have identified two main types of uncertainty that generate transaction costs for firms entering foreign countries: behavioral and environmental uncertainty. Behavioral uncertainty is generated by the inability of a firm to predict the behavior of partners in a foreign country (Chiao et al., 2009; Gatignon & Anderson, 1988). More specifically, it refers to the difficulties and risks a firm encounters in finding, negotiating, and monitoring partners, making it difficult to safeguard against opportunistic behaviors of local partners, like suppliers, distributors, competitors, consumers, and regulators. Opportunistic behaviors in the presence of institutional voids are driven by the information asymmetry between the entrant firm and partners in the host country (Meyer, 2001). Environmental uncertainty, instead, refers to a firm’s inability to predict how the environment in which it operates will change, and it often results from the volatility of environmental conditions in a host country (Anderson & Gatignon, 1986; H. Zhao et al., 2004). Recent literature reviews of entry mode studies (Giachetti et al., 2019) have observed that, despite institutional voids in a firm’s host country bring both behavioral and environmental uncertainties (Khanna & Palepu, 2010), transaction cost theory offers different perspectives about the type of control a firm’s entry modes should have to cope with these uncertainties. Authors suggest that in the presence of behavioral uncertainty, firms should use high-control entry modes to avoid foreign partners’ opportunism (Gatignon & Anderson, 1988), while in the presence of environmental uncertainty, firms should use low-control entry modes to retain the strategic flexibility necessary to rapidly withdraw assets from the host country if the situation so dictates (Brouthers & Nakos, 2004). We integrate these two perspectives by arguing that the extent to which managers of a firm decide to commit resources in emerging markets via entry mode control changes depending on the level of institutional voids (and then uncertainties), that is, low, moderate, and high, and managers perceive they will encounter (or are encountering) in those markets.

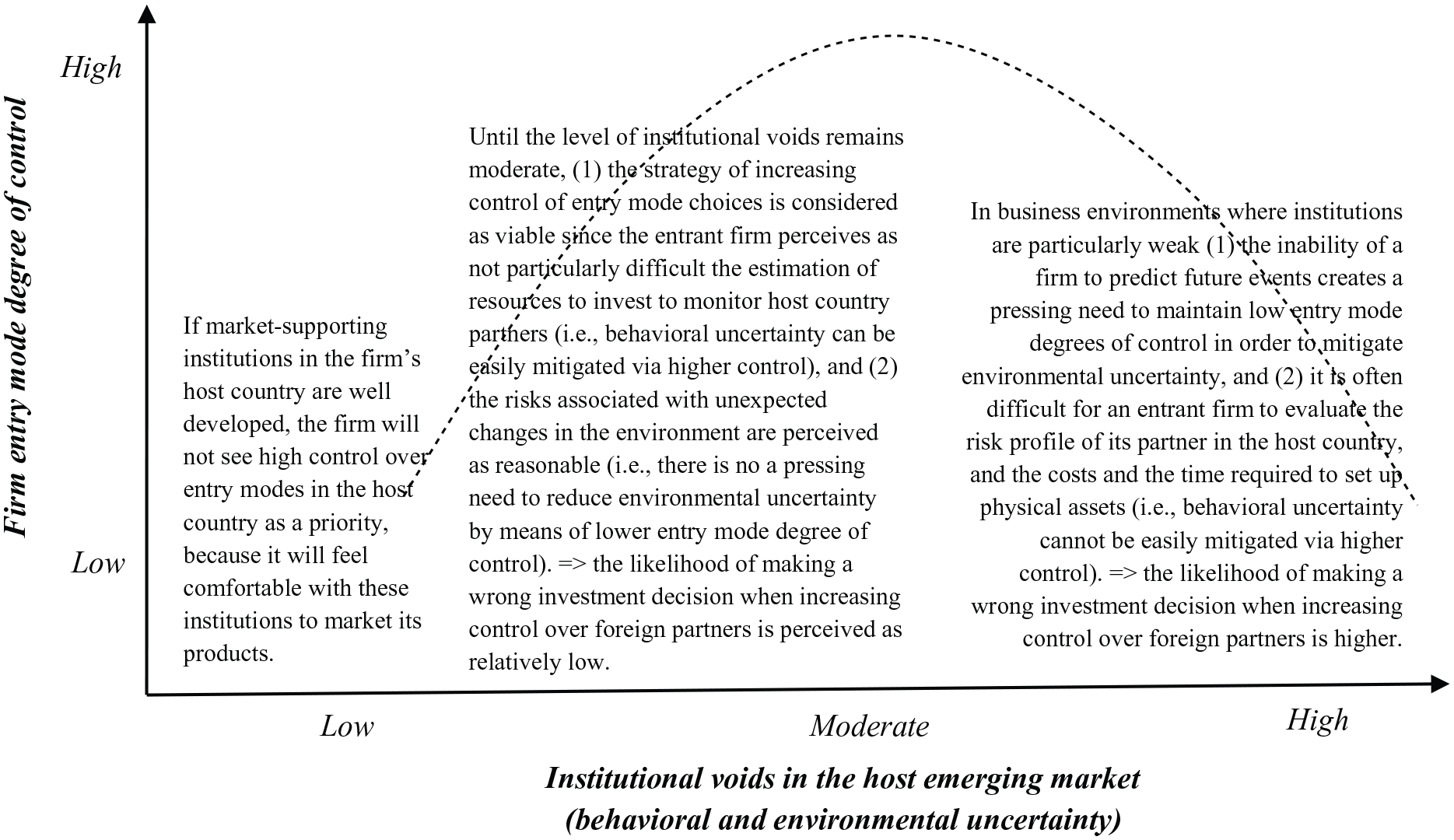

Entry mode degree of control from low to moderate levels of institutional voids

If market-supporting institutions in the firm’s host country are well developed, we should expect that, all other things being equal, the firm will not see high control over entry modes in the host country as a priority because it will feel comfortable with the institutions to market its products (Chang et al., 2012; Luo, 2001). In such a scenario, host country institutions act effectively as intermediaries between the entrant firm and its customers in the host country (Khanna & Palepu, 2010), and thus, the entrant firm will choose not to commit resources to substitute the functioning of host country institutions:

The more open a country’s economy, the more likely it is that global intermediaries will be allowed to operate there. Multinationals, therefore, will find it easier to function in markets that are more open because they can use the services of both the global and local intermediaries. (Khanna et al., 2005, p. 67)

By choosing low-control entry modes, the entrant firm will have instead available resources to invest elsewhere, for example, in countries where greater control of host country partners is needed. In other words, an increasing commitment of resources to support entry modes in countries with low levels of institutional voids is likely to be considered by the entrant as unappropriated because it would drain resources away from markets where it needed the most.

However, as the level of institutional voids increases from low to moderate, managers’ perception of greater behavioral and environmental uncertainty also increases. Given the opposing prescriptions proposed by transaction cost scholars as to how to mitigate the two types of uncertainty, in this scenario, we ask the following: will firms increase or decrease the level of control of their entry modes? In fact, although a perception of increasing environmental uncertainty should lead managers to maintain low entry mode degree of control to retain flexibility in case of unexpected market changes, they will have to cope also with transaction costs associated with increasing behavioral uncertainty, which calls for greater control (Giachetti et al., 2019). We contend that until the level of institutional voids increases but remains moderate, the strategy of increasing control of entry mode choices is more likely. The reason is twofold. First, given the moderate level of institutional voids, the entrant firm can relatively easily scan the risk profile of the host country partners before increasing control over their assets, so that when increasing control it will take a relatively low risk of finding later hidden liabilities, hidden litigations, miscalculations in the evaluation of assets, or overstaffing hard to reduce in the short run (Henisz & Zelner, 2010; Tong et al., 2008). This means that, since the entrant firm perceives as not particularly difficult the estimation of resources to invest to monitor host country partners, behavioral uncertainty can be easily mitigated via higher control. Second, at moderate levels of institutional voids, the risks associated with unexpected changes in the environment, for example, sudden public policy interventions weakening the legal system and making bureaucratic procedures more complicated or ambiguous, are perceived as still reasonable, thus not calling for high strategic flexibility (which is usually obtained through low-control entry modes; Henisz & Zelner, 2010). And this means there is no pressing need to reduce environmental uncertainty by means of lower entry mode degree of control. As a result, a greater control over foreign resources (e.g., partners in the host country) can be achieved at relatively low risk of having to redeploy later these resources elsewhere (e.g., because unexpected changes in the host country make it not worth to stay).

For example, Deng and Tita (2013) noted that in 2014, Whirlpool Corporation, one of the largest producers of white goods, overcame the transaction costs in China, mainly associated with monitoring local partners, by investing significant resources to acquire Hefei Sanyo, a Chinese competitor with a long experience in the consumer appliances market. Similarly, Burkitt (2012) observed that PepsiCo in 2012 responded to the increasing difficulties in gathering information about Chinese consumer preferences to develop products tailored to local taste by establishing its wholly owned subsidiary in Shanghai, focused on R&D and manufacturing activities. According to Deng and Tita (2013) and Burkitt (2012), institutional voids appear to exist in the Chinese white goods and soft drink industries, but the voids were not perceived as insurmountable, and what concerned managers was not unexpected changes in their business environment, but a greater control over people in charge of managing their assets in China.

Therefore, for low levels of institutional voids, firms will choose low-control entry modes, but as institutional voids increase from low to moderate, the need to maintain low control to mitigate environmental uncertainty is outweighed by the priority to mitigate behavioral uncertainty, which leads firms to increase control of their entry modes.

Entry mode degree of control from moderate to high levels of institutional voids

Now, we ask whether and how firms will change their entry mode degree of control as institutional voids in the host country move from moderate to high. Also, in this case, we need to look at how managers’ perception of environmental and behavioral uncertainty is likely to influence their strategic choices. When the host country’s institutional environment is particularly underdeveloped, the need to reduce entry mode degree of control may occur due to a perception of higher levels of environmental uncertainty, arising from the inability of a firm to predict future events (Álvarez & Marín, 2010; Brouthers & Brouthers, 2003; Morschett et al., 2010; Yiu & Makino, 2002; H. Zhao et al., 2004). For example, in business environments, where institutions are particularly weak, local authorities in the host country may suddenly create barriers to entry that restrict the entrant firm’s access to resources or impose restrictions on the foreign transfer of goods (Delios & Beamish, 1999). This creates a pressing need to maintain low entry mode degrees of control to benefit from strategic flexibility in a very unpredictable business environment. As explicitly noted by some authors, “with high environmental uncertainty, companies may be better off selecting non-equity, low-investment entry modes” (Brouthers & Nakos, 2004, p. 234) because this choice “not only avoids resource commitment but frees entrants to change partners or renegotiate contract terms and working arrangements relatively easily as circumstances develop and change” (Anderson & Gatignon, 1986, p. 15). As also noted by Luo (2001) in his study of firms entering the Chinese market when environmental uncertainty triggered by unpredictable governmental interventions were high, “as entry mode decision is associated with risk-taking propensity and resource commitment, an MNE should structure it in such a way as to help accomplish its strategic goals without taking excessive risks” (p. 460).

As for behavioral uncertainty, in the presence of underdeveloped institutions, it is often difficult for an entrant firm to evaluate the risk profile of its partner in the host country (e.g., in the case of joint ventures), as well as the costs and the time required to set up physical assets (e.g., in the case of a wholly owned subsidiary) aimed at substituting the work of foreign partners. As a result, the likelihood of making a wrong investment decision when increasing control over foreign partners to better monitor their operations (and then reduce behavioral uncertainty) is particularly high. For example, in the Chinese heavy equipment industry, Caterpillar lost US$580 million in 2012 after it carried out a set of investments to increase control over a Chinese construction equipment company that had fraudulently inflated its revenues (Areddy, 2013). In fact, the construction equipment manufacturing industry in China has experienced decreasing domestic demand at the end of the 2000s that has generated lots of uncertainty about the future of this sector. Low demand from the construction sector in the country has resulted in low profits for major (often state-owned) companies and small players have incurred huge losses. Also, the competition in the market has been fierce which pushed the major manufacturers to lower prices of their equipment, and this forced many small competitors to either sell their business or liquidate their activity altogether. However, the lack of “debt transparency” and the highly bureaucratic procedures to do business in this industry have resulted in high risk for foreign equipment manufactures which considered committing resources in the country. As noted by Khanna et al. (2005), when examining institutional voids in China in the 2000s, “the [Chinese] government permits greenfield investments as well as acquisitions, [but in some industries] acquired companies are likely to have been state owned and may have hidden liabilities” (p. 11).

Drawing on the arguments noted so far in this section, we contend that, although from low to moderate levels of institutional voids, firms are encouraged to adopt entry modes characterized by higher control mainly with the aim of mitigating behavioral uncertainty; at particularly high levels of institutional voids, the need for flexibility in the use of resources overrides that of control, that is, the costs of environmental uncertainty outweigh the priority to reduce behavioral uncertainty by means of greater control. Thus, we posit the following:

Hypothesis: There is an inverted U-shaped relationship between managerial perception of institutional voids experienced by a firm entering an emerging market and the firm’s entry mode degree of control in that emerging market.

Figure 1 summarizes and illustrates our research model on the relationship between institutional voids and entry mode degree of control.

A model on the institutional voids–entry mode degree of control relationship.

Methods

Setting and sample

The study employed Italian firms with sales activities in China since the turn of the century as an appropriate setting to test the proposed hypothesis. This choice was informed by various reasons. First, China has exerted a pull on a progressively larger amount of foreign direct investment (FDI) since it opened its border to the outside world in 1979 (with the establishment of its special economic zones) and turned out to be the second largest beneficiary of FDI in the world following the United States at the early part of the 1990s. In 2001, China joined the World Trade Organization (WTO), which further liberalized its trading activities and partnership with foreign countries. This move to join the WTO resulted in a further increased trend in FDI, making China one of the investment front lines for foreign firms. Second, Italian firms since 2000 have dramatically expanded their business operations in China either through FDI or through exports (Istituto Nazionale per il Commercio Estero (National Institute for Foreign Trade) [ICE], 2012), in this manner becoming chiefly reliant on the Chinese economy to foster their growth and remain competitive in the global arena (see the Appendix, Table 2A, for details about Italy’s FDI in China over the last decades). Finally, on one hand, China as an emerging market is characterized by institutional voids, creating daunting obstacles for companies that intend to or already operate in the Chinese markets (Khanna & Palepu, 2010); on the other hand, entrant firms have been observed to experience different institutional voids in China since the beginning of the 2000s, leading to marked performance differences among foreign affiliates of MNC operating in different industries and subnational regions within the country (Chan et al., 2010). In the 2000s, the impact of institutional differences among industries and subnational regions within emerging markets like China on entrant firms’ strategy and performance has been shown to be greater than that in advanced economies, like the United States. In fact, soon after the WTO-mandated reforms concluded, several foreign firms in China began to complain of an increase in discriminatory practices, more difficulty in getting licenses, a still ambiguous legal system, and complicated bureaucratic procedures (“China is Still Risky for Foreign Businesses,” 2013), signaling the presence of institutional voids in some business environments as particularly evident. This makes China an appropriate setting for understanding how the institutional environment has different impacts on strategic decisions of entrant firms.

A total list of 922 Italian companies conducting their business operations in China was obtained from the Chamber of Commerce and the Italian National Institute of Foreign Trade (Istituto Nazionale per il Commercio Estero, ICE). This list was made up of most or all Italian companies earning part of their total revenue from the Chinese market. All the CEOs of these companies were contacted and asked to complete an anonymous, detailed questionnaire (in Italian) designed for studying various strategic issues, including those we investigate here. The questionnaire was designed in 2011 by the authors with the help of some market experts and CEOs with long experience in the Chinese market. A pilot test of the questionnaire was carried out, and the questionnaire was modified based on the feedback from the pilot test. The completed questionnaire was sent to the CEOs of all 922 firms at the end of 2011 via email. Firms that did not reply to the initial request were contacted second time. A total of 140 (15.2%) usable questionnaires were received from the firms.

The base population of the survey was initially defined to include all Italian firms conducting their operations in China. However, we employed a subset of firms that entered China from 2001 onward for two main reasons. First, it was necessary to check for possible biases in the data as a result of referring to events too distant in the past (Meyer et al., 2009). Second, it was also important to ensure that the joining of WTO by China in 2001 did not affect the results because the accession to WTO liberalized China’s foreign trade policy and dismantled some barriers to foreign investments in various industries. Following these selection criteria, our final sample consisted of 90 Italian firms operating in China. 2

Measures

The dependent variable of the study is the firm’s resource commitment defined in terms of entry mode degree of control in China (EMDC). The level of institutional voids (INSTVOIDS) present in the firm’s industry within the Chinese market is the main independent variable.

Entry mode degree of control in the emerging market

Studies show that entry strategies can be classified based on the extent to which they allow the firm to exercise control over its operations in the foreign markets (Anderson & Gatignon, 1986). Consistent with empirical measures used in the literature (Giachetti, 2016; Johnson & Tellis, 2008), we employed a 4-point ordinal scale ranging from 0 to 3 to calibrate the entry mode strategies of varying degrees of control and resource commitment as follows: exports (0), franchises and licenses (1), joint ventures (2), and wholly owned subsidiaries (3). Because the firm may decide to enter a foreign market by any of these entry modes or a combination of these, and as the choice of the entry strategy may change over time (Benito et al., 2011), we requested the respondent to indicate all the various entry mode(s) the firm has used in conducting business activities in China since the initial entry in 2001 till 2010. 3 Finally, based on the 4-point scale, the average score of the various entry strategies was used to indicate the overall level of resource commitment by the firm over the considered time frame (2001–2010; see the Appendix, Table 3A, for details of items employed in measuring EMDC).

Institutional voids

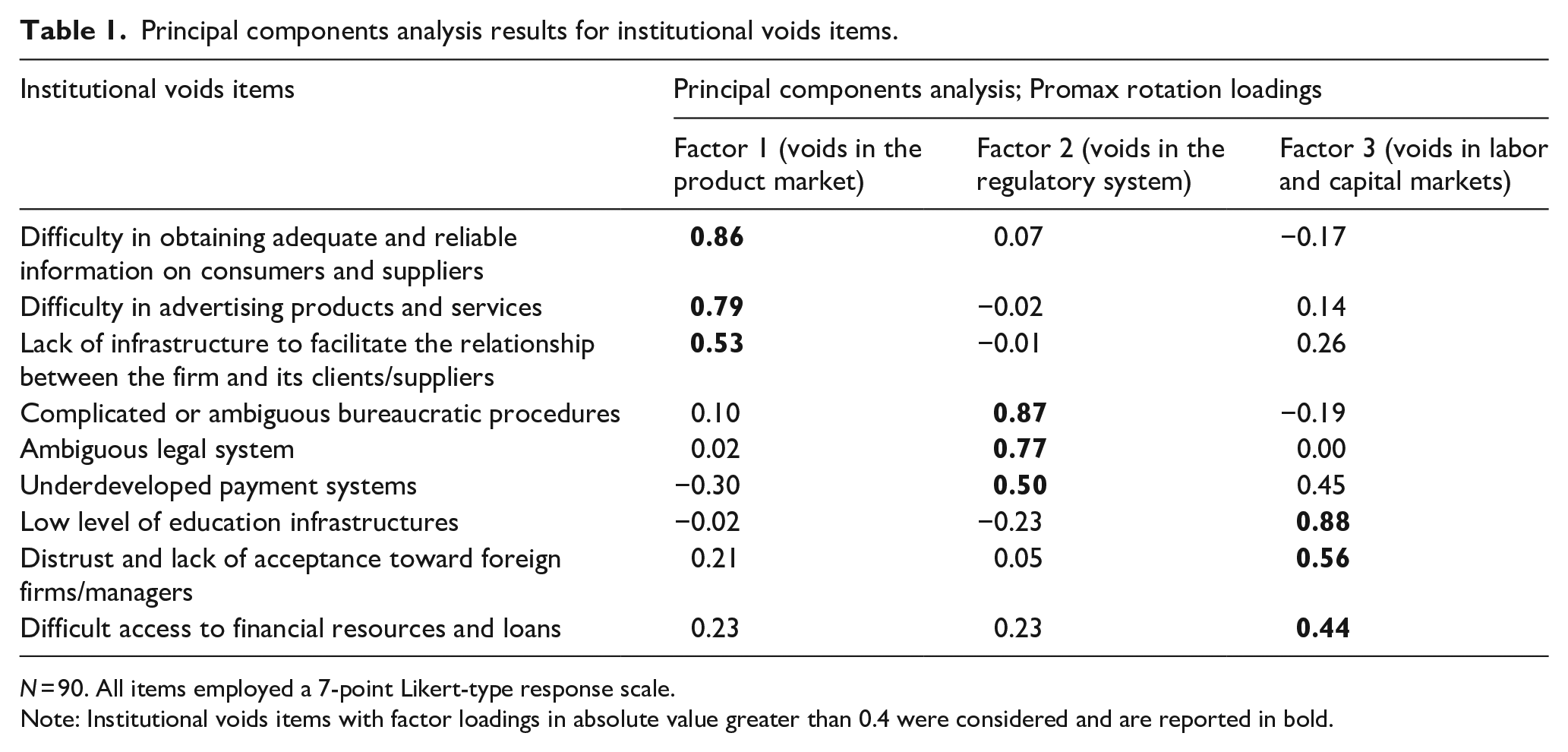

To measure the extent to which institutional voids within the Chinese market are embedded in the entrant firm’s business environment, the respondents were first asked to indicate on a 7-point Likert-type scale, ranging from “almost nothing” to “a lot,” the degree to which they had perceived various institutional voids in their industry within the Chinese market since the firm entered the country (see the Supplemental Appendix, Table 3A). More specifically, we asked an overall judgment on the extent to which institutional voids had hampered the internationalization process of the firm in the Chinese market since its first entry. The nine items used were derived both from the literature (Khanna & Palepu, 1997, 2010) and in-depth interviews with market experts during the questionnaire development and pilot test. Cronbach’s alpha computed on the 9-item scale was found to be above 0.70 (Cronbach’s α = .72), suggesting that the scale is internally consistent (Nunnally, 1978). We also conducted a principal components analysis with Promax rotation on the 9 items of our INSTVOIDS variable, to assess whether factors emerged, and the variable discriminant and convergent validity. As shown in Table 1, the principal components analysis categorized the institutional voids items into three factors (with eigenvalues greater than 1), which we named voids in the product market, voids in the regulatory system, and voids in labor and capital markets, on the basis of factor loadings in absolute value greater than 0.4 (Nunnally, 1978). 4 Interestingly, these three factors are very similar to the macro-types of institutional voids described in the literature (Khanna et al., 2005). Convergent validity is established if the average variance extracted (AVE) for the factors approaches or is greater than 0.5, and discriminant validity is also demonstrated if the variance extracted is greater than the corresponding squared correlation of the factors (Fornell & Larcker, 1981). We found all these conditions to be satisfied. Consequently, the mean score of the 9 items in Table 1 was used for the subsequent analysis, and we repeated the analysis as a robustness check with a measure of institutional voids per each of the three dimensions obtained from the principal components analysis.

Principal components analysis results for institutional voids items.

N = 90. All items employed a 7-point Likert-type response scale.

Note: Institutional voids items with factor loadings in absolute value greater than 0.4 were considered and are reported in bold.

Control variables

Our analysis also calls for controls. Firm size (SIZE) was controlled by the natural logarithm of the firm’s revenue (in 2010). Firm age (AGE) was captured as the natural logarithm of the number of years the firm has existed (Fernandez & Nieto, 2006). Experience in developing countries (EXPEDEVEL) was measured as the number of developing countries and emerging economies in which the firm has operated since its inception. Experience in the Chinese market (EXPECHINA) was measured as the natural logarithm of the number of years the firm has been conducting its business in the Chinese market. Degree of family ownership (FAMOWN), usually quite high in Italian firms, was measured with an ordinal scale based on the proportion of the firm’s total shareholders’ equity controlled by the founding family: <10% (1), between 10% and 30% (2), between 30% and 50% (3), between 50% and 70% (4), and >70% (5). We also wanted to control for the size of a firm’s resource commitment to the Chinese market, that is, the total value of resources invested in China. Although we do not have data on the amount of equity and assets invested in the Chinese operations, we partially captured the effect of this variable by asking respondents to indicate the number of employees directly paid by the firm in the Chinese market (EMPLCHINA). Moreover, to account for the elements of perceived attractiveness of the Chinese market (Elia et al., 2014), respondents were asked to indicate the degree to which each of the three following opportunities has encouraged the firm to operate in the Chinese market (based on a scale from 1 to 7, where 1 = not at all and 7 = very much): (1) market size (number of potential customers) (MARKET_OP), (2) low costs related to production factors (e.g., labor, plant, equipment, raw materials, etc.) (LOWCOST_OP), and (3) presence of on-site advanced technology (TECH_OP). We wanted to account also for the fact that resource commitment decisions may depend on existing resources available to the developed country-based firm at the parent group level. In fact, for a subsidiary of an MNC, the decision to commit resources may be easier because its superstructure (i.e., the parent group) can substitute for institutional voids (M. Zhao, 2006). We thus used a dummy GROUP that takes the value 1 if the firm belonged to a group and 0 otherwise (Giachetti, 2016). Competitive intensity in China (COMPINT) was accounted through a 2-item indicator. Specifically, respondents were asked to express a judgment about the number of their firm’s competitors in the Chinese market (based on a scale from 1 to 7, where 1 = few competitors and 7 = many competitors), and to express an opinion about the degree to which competitive strategies of competitors in the Chinese market have threatened/are threatening the firm’s performance (based on a scale from 1 to 7, where 1 = low threat and 7 = high threat). The items’ mean score was used for the subsequent analysis (Cronbach’s α = .79). We also included a set of 16 industry dummies that enabled us to capture any unobserved industry factors that influence the firm’s operations in China. The coding of the industries was done in accordance with the ATECO codes of economic activities. 5 Finally, although after China joined the WTO in 2001 (the beginning of our observation period) its economy has seen an exponential increase of FDI inflows, we wanted to account for those industries for which the Chinese Government maintained some kind of FDI restrictions during our observation period. To understand which firms in our sample operated in industries that, during the 2001 to 2010 time period, were restricted in terms of FDI inflows in China, we used both several secondary sources, 6 like the China Releases New Foreign Investment Catalogue (which publishes the list of industries with restrictions), and in-depth interviews with market experts the authors contacted during the questionnaire development. Among the 16 industry firms in our sample operated during the observation period, five were labeled under the “restricted” category in terms of FDI (meaning the governments imposed some form of restriction to FDI), while the remaining 11 were labeled under the “encouraged” category (meaning the governments did not impose some form of restriction to FDI). 7 Overall, only seven of our sampled firms belonged to this category. We thus created a dummy industry restricted (RESTRICTED) which took value equal to 1 for such firm-industry observations.

It is worth noting that we took various strategies to avoid common method bias in our analysis. First, we used a procedural remedy to separate our predictor and criterion variables psychologically (Podsakoff et al., 2003) by making sure that the groups of items from which we derived the variables were located in different sections of the questionnaire and were not connected or related to each other (Supplemental Table 3A). Second, we attempted to reduce common method bias by guaranteeing anonymity of the respondents (Podsakoff et al., 2012). Third, after the survey was completed, we performed various in-depth interviews with some managers of the sampled firms to check whether there was consistency with how they rated the items in the questionnaire; no inconsistency was found between the information gathered from the interviews and that collected in the questionnaires.

Results

Test of the hypothesis

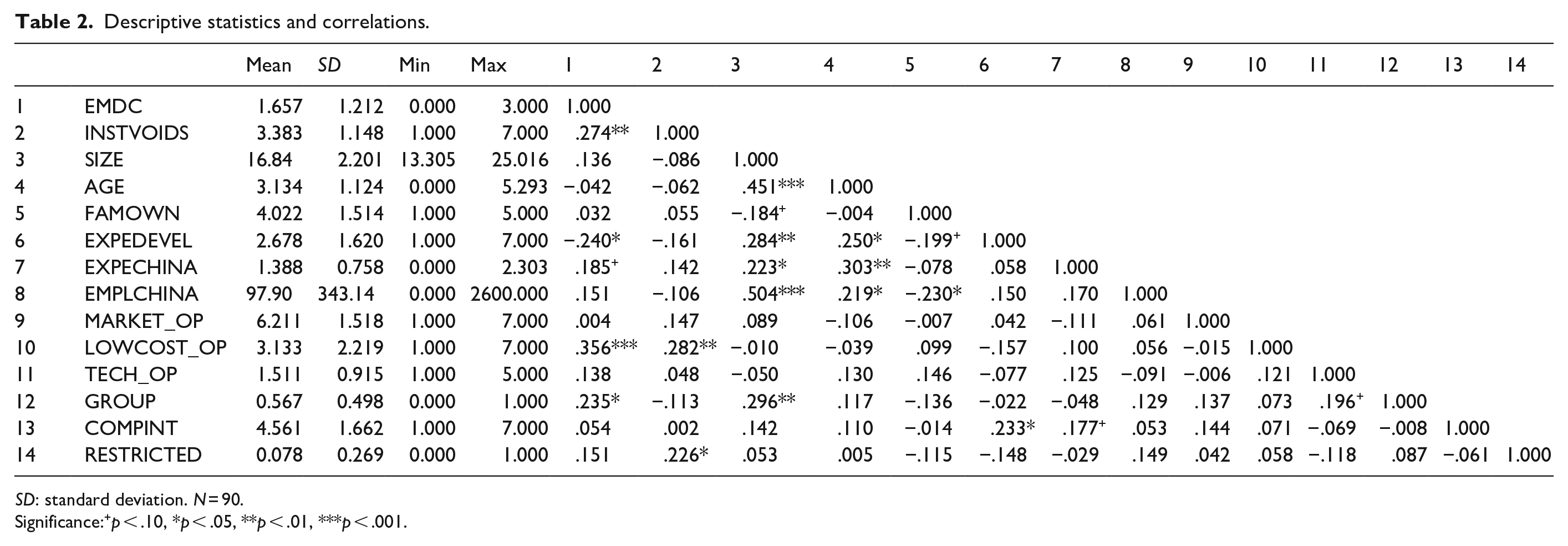

Table 2 reports the descriptive statistics and the correlation matrix for the variables included in the models. The correlations among independent variables are relatively low, suggesting that multicollinearity should not be a problem in the models. This is confirmed by the variance inflation factor (VIF). In our models, VIF values were not higher than 1.85, thereby falling within the acceptable limit of 10 (Chatterjee & Hadi, 2006).

Descriptive statistics and correlations.

SD: standard deviation. N = 90.

Significance:+p < .10, *p < .05, **p < .01, ***p < .001.

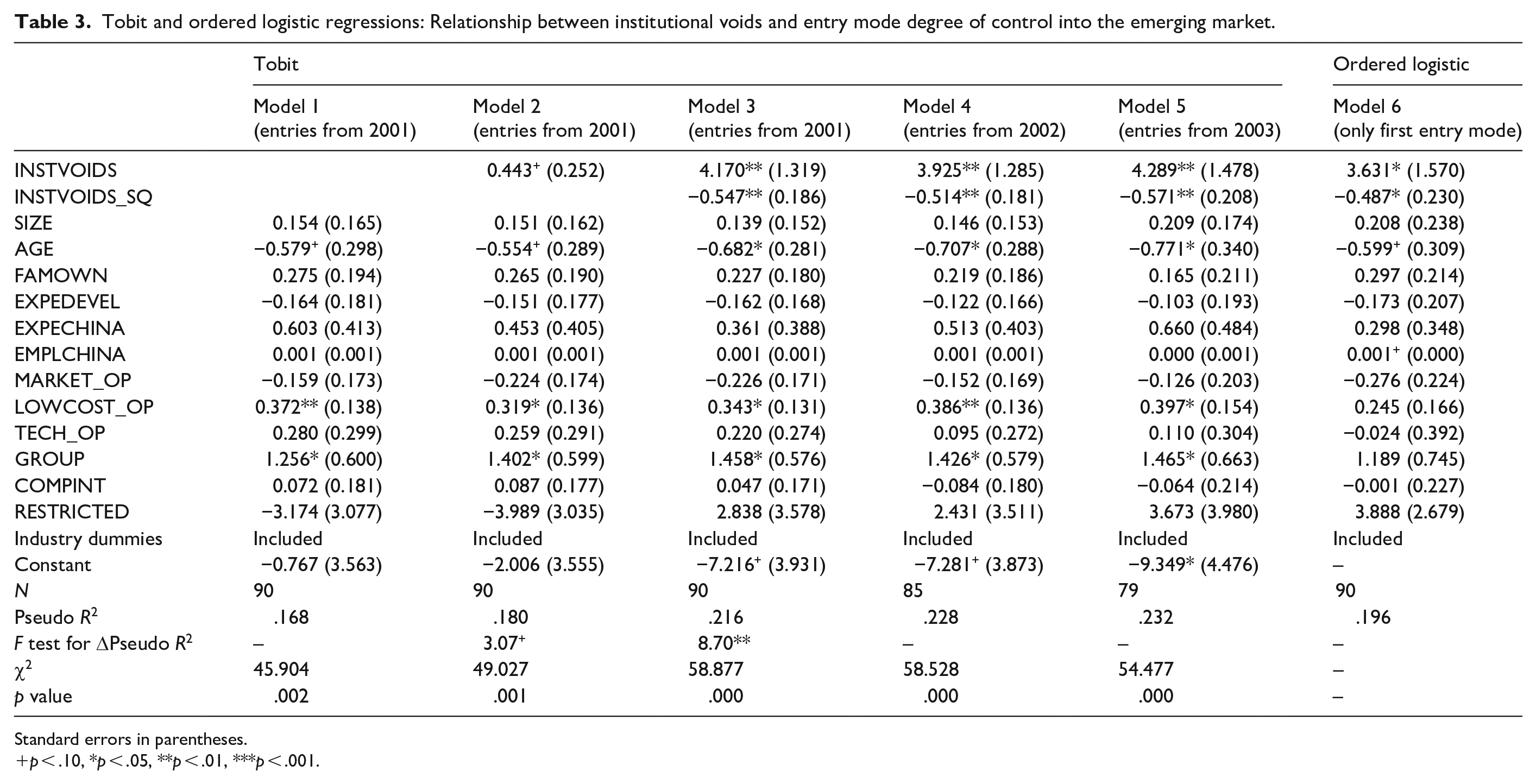

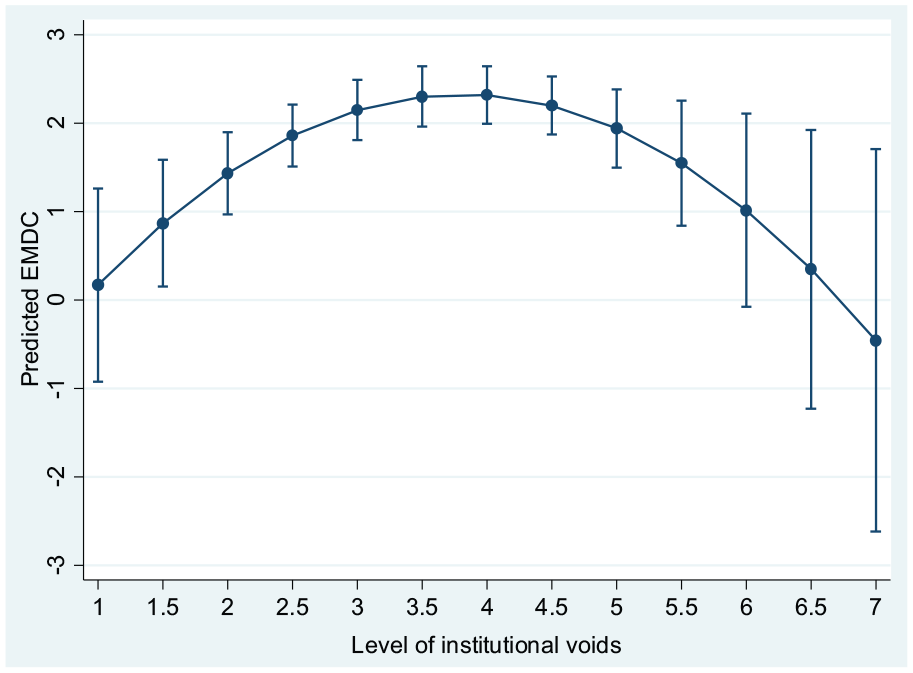

Since our dependent variable is censored between 0 and 3, we tested our hypothesis with a Tobit regression model (Wooldridge, 2002). Table 3 shows the results of Tobit regression models for the proposed inverted U-shaped relationship between institutional voids and EMDC. Model 1 (Table 3) is an examination of control variables on EMDC. In Model 2 (Table 3), we show the result of the linear effect of institutional voids (INSTVOIDS) on EMDC (β = 0.443, p < .1). In Model 3 (Table 3), to test for our hypothesis, we add the squared term of institutional voids (INSTVOIDS_SQ). As shown in Model 3, there is a statistically significant, positive relationship between institutional voids and EMDC (β = 4.170, p < .01) and a negative relationship between institutional voids squared and EMDC (β = −0.547, p < .01). Combining these relationships denote an inverted U-shaped relationship between institutional voids and entry mode degree of control, thereby providing support for our hypothesis. It can be noticed from Table 3 that a comparison of the Pseudo R2 of Models 2 and 3 points out a significant positive change (ΔPseudo R2 = .036; F test for ΔPseudo R2 = 8.70, p < .01) upon the addition of the quadratic term of institutional voids. This gives an indication that Model 3 provides a better fit to the data than Model 2. To facilitate interpretation, the inverted U-shaped relationship between institutional voids and entry mode degree of control we obtained is depicted in Figure 2, according to standard procedures (Dau et al., 2015). As can be noted in Figure 2, as institutional voids move from low to moderate levels (i.e., from 1 to 4), firms, on average, increase their entry mode degree of control from 0 (i.e., export, or a mix of modes with very low levels of control) to slightly above 2 (i.e., joint venture, or a mix of modes with relatively high levels of control); while as institutional voids move from moderate to high levels (i.e., from 4 to 7), firms, on average, decrease their entry mode degree of control from slightly above 2 to 0. However, it is worth noting that confidence intervals for very low and very high levels of institutional voids (i.e., 1, 6, and 7) include “0,” meaning for these values of our key regressor, it is uncertain whether the effect is as we predicted. One reason for explaining the low-precision effect on EMDC at very low levels of institutional voids could be the idea that institutions are “invisible” when markets are well developed (McMillan, 2007; so that entry modes are not the main strategic decision pursued by managers to deal with uncertainty (and, thus, the selection of the resource commitment will depend on other factors, different from institutional voids). One reason for explaining the low-precision effect on EMDC at very high levels of institutional voids could be that, since in very uncertain environments firms often cannot easily and timely manage their resources (Hoskisson et al., 2000), high levels of both environmental and behavioral uncertainty might constrain an entrant firm’s ability, especially if it is small or medium in size, to respond to institutional voids in the host country with the intended entry decisions. However, for the remaining range of values of the institutional voids variable (i.e., 1.5–5.5), the plot of the relationship is clear as predicted.

Tobit and ordered logistic regressions: Relationship between institutional voids and entry mode degree of control into the emerging market.

Standard errors in parentheses.

p < .10, *p < .05, **p < .01, ***p < .001.

Tobit regression: Relationship between institutional voids and entry mode degree of control (predictive margins).

Finally, it is worth noting that, despite our relatively small sample size and the fact that most of our control variables are not or are only marginally significant, our key regressors (i.e., INSTVOIDS and INSTVOIDS_SQ) are highly significant (with a p-value significance always at least at 95% confidence intervals), pointing to the fact that the impact of the antecedents of resource commitment we have examined is not negligible.

Robustness checks

We took various steps to ensure that the results are robust. First, we reran the analysis with two different subsamples, one with firms that entered China from 2002 and one with firms that entered China from 2003, as indicated in Models 4 and 5 (Table 3) for the Tobit regressions. In all these subsamples, the results remained consistent with the findings obtained with the full sample.

Second, as for the EMDC variable, because we asked respondents to also indicate the mode initially used to enter the Chinese market, we reran the analysis presented in Model 3 by considering only this entry mode type. 8 Being in this case the dependent variable a categorical one, we used robust ordered logistic regression. As can be observed in Model 6 in Table 3, the results remained consistent.

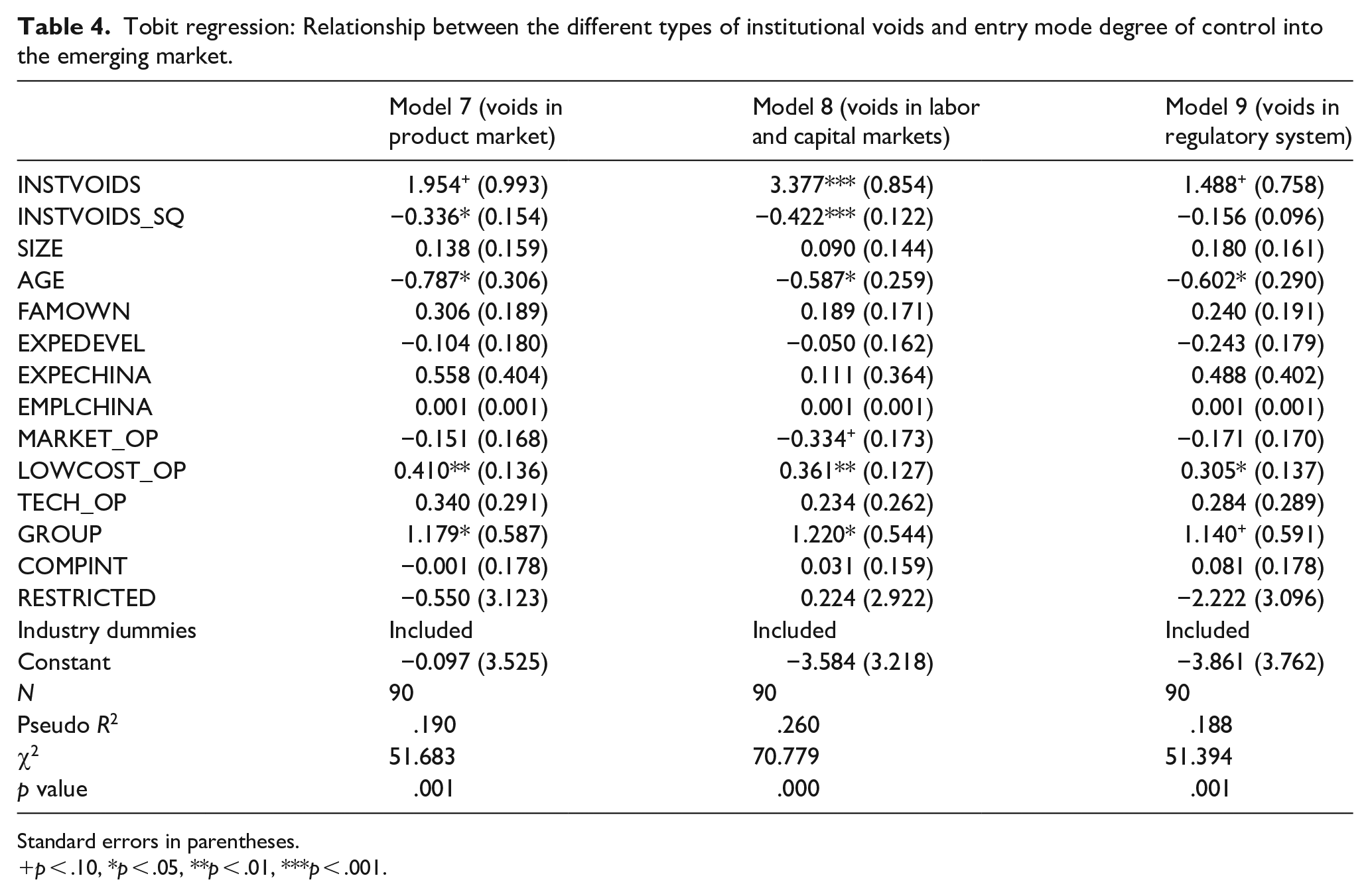

Third, because the principal components analysis categorized the institutional voids items into three factors (Table 1), we repeated the regression analysis with three different measures of INSTVOIDS, with each measure computed as an average of the items referring to a given factor. As shown in Table 4, per each type of dependent variable, that is, entry mode degree of control (Models 7–9), results remained consistent with our predictions in two of the three institutional voids dimensions.

Tobit regression: Relationship between the different types of institutional voids and entry mode degree of control into the emerging market.

Standard errors in parentheses.

p < .10, *p < .05, **p < .01, ***p < .001.

Discussion

Implications for theory

This study builds on the institutional theory and transaction cost theory in international business to examine the impact of institutional voids in an emerging market on entrant firms’ resource commitment. Specifically, the article takes the perspective of firms coping with institutional voids when entering an emerging market. The literature to date has offered mixed results on the relationship between voids in the host country’s institutional environment and entrant firms’ resources commitment (as synthesized in Supplemental Table 1A). In this article, we have shown that the reason for these mixed results is that the relationship is more complex than has been theoretically developed and empirically tested. More specifically, while we agree with the authors providing evidence for a positive relationship between the level of institutional voids and entrant firms’ resource commitment, we contend that beyond a certain level of institutional voids in the host country, the positive relationship no longer holds. This implies that above certain limits of institutional voids in a host country, firms no longer have the incentives to increase the control of their resources in the host country, but rather decrease control, indicating that at lower and higher levels of institutional voids, firms will show lower resource commitment than at moderate levels of institutional voids.

This study complements the literature on the institutional voids–resource commitment relationship by examining resource commitment in terms of a firm’s entry mode degree of control. The inverted U-shaped relationship we present in our hypothesis is drawn from different theoretical mechanisms. We explain the relationship between institutional voids and entry mode degree of control by bridging the institution-based view of strategy with the transaction cost literature of entry mode choices, and we argue that as institutional voids increase, managers’ perceptions about uncertainty also change. In fact, although as institutional voids in the host country increase, they bring both behavioral and environmental uncertainty to the eyes of entrant firms; our theory suggests that from low to moderate levels of institutional voids, the firm priority is to mitigate behavioral uncertainty emanating from the inability of the firm to predict the behavior of partners in the host country, while from moderate to high levels of institutional voids, the firm priority is to mitigate environmental uncertainty resulting from the firm’s inability to predict how the market in the host country will evolve. The result is that, although greater entry mode degree of control may help to reduce behavioral uncertainty, for high levels of institutional voids, the costs of environmental uncertainty will override the priority of greater control, calling for more strategic flexibility, which can be reached with lower control entry modes.

Another contribution of this article is related to the perspective we take about the host country institutional voids, both in terms of the level of analysis and empirical measures. In fact, while the literature on the role of the institutional environment in international business is centered on comparing how countries differ in terms of country-level measures of institutional voids derived from secondary sources (Álvarez & Marín, 2010; Brouthers & Brouthers, 2003; Chang et al., 2012; Meyer et al., 2009), we consider analyzing institutional voids from a CEO’s “subjective” point of view, by means of survey data on managers’ perception of institutional voids in the host country. With this measure, we respond to a specific call in the international business literature to explore other ways of operationalizing market institutions (Garrido et al., 2014; Orr & Scott, 2008), in particular, by means of measures that account for the fact that the level of development of a host country institutional environment may vary radically among different business environments in that host country (Henisz & Zelner, 2010; Khanna & Palepu, 2010). This measure allows us to capture the extent to which firms entering the same country actually perceive to be affected by voids in the institutional environment.

Limitations and suggestions for further studies

This article has some limitations that could benefit from further research. First, our study is limited in the scope of its research design. Considering the diversity among emerging economies, it is important to broaden the scope of the study of strategies in these economies to account for country-specific factors that could affect a firm’s resource commitment to these emerging economies. However, our study focused only on a single country: we sampled Italian firms operating in China. For this reason, questions concerning the generalizability of the findings to other emerging economies remain unanswered. We encourage further studies to consider extending our analysis into other emerging economies.

Second, this article does not take into account the influence of the home country institutional environment on the firm’s resource commitment. We believe that analyzing how both the home and host country institutions affect a firm’s entry strategy simultaneously will provide a deeper understanding and contribute significantly to the literature.

Third, although our questionnaire was directed to top management teams of the sampled firms, it was anonymous, and often we received the completed questionnaire via email by the administrative office of the company (and not by the manager who completed it), with no name indicated. For this reason, we could not be certain of who completed the questionnaire and could not check when he or she joined the company (e.g., before or after the firm’s entry into China). Obviously, in case of changes in management, the previous managers may not have perceived the institutional voids in the same way as the present managers. Although also previous entry mode studies have faced similar potential problems of temporal correspondence between independent and dependent variables developed with survey data (Brouthers et al., 2008; Brouthers & Nakos, 2004), it is worth noting that, given the relatively small size of most of the firms in our sample (the average revenue in 2010 was €20.7 million) and their high family control (on average, in 2010, the percentage of equity controlled by the founding family was between 50% and 70%; see Table 2), turnover among CEOs and top managers should not be particularly frequent among our sampled firms (Huson et al., 2001). We hope future research will replicate our study by controlling for respondent-level characteristics, like years of tenure in the focal firm or possibly look for an alternative way to capture institutional voids.

Fourth, although our measure of entry mode degree of control based on different entry mode types was taken from the extant literature (e.g., Brouthers & Nakos, 2004; Johnson & Tellis, 2008), recent literature reviews of entry mode degree of control have noted that control can be measured also with the percentage of equity owned by the entrant firms in the host country (e.g., Giachetti et al., 2019). This latter operationalization can be useful to take into account the difference of degree of control between equity-based modes of the same type. However, since we do not have this information in our database, we hope future research will replicate our analysis with this alternative measure.

Fifth, as for our measure of “perceived institutional voids since the firm’s entry into China,” we are aware that it is an attempt to capture management perceptions about voids that might have occurred a long time before the survey was conducted. Therefore, although our measure presents elements of novelty with respect to previous studies, on the other hand, it presents also some limitations that might bias its interpretation. Related to this point, it is interesting to note that the variables capturing a focal firm’ experience in China and in developing countries were never significant, while the variable “firm age” was always negative and significant; taken together, this means that older firms are not necessarily those that can get more experience and resources to enter countries with higher levels of resource commitment. Moreover, a firm age (experience) might affect the way a firm perceives voids in a target country. We hope future studies will propose a more precise indicator to measure a firm’s perception about institutional voids in the host country, may be weighting the firm perception for its experience in similar developing countries.

Finally, it is important to note that despite the quality of the institutional environment in the host country, a firm’s decision to commit resources in a foreign country may be induced by the potentially utilizable resources (slack resources) the firm has. These resources are deployed to build capabilities that make firms immune to some operational difficulties (such as those emanating from weak institutions in the host country; George, 2005). In our study, we are unable to account for how the slack resources a firm has influenced the firm’s decision to commit resources in foreign markets. We expect that future studies will find measures to capture the effect of this important variable.

Supplemental Material

APPENDIX – Supplemental material for How much control do firms exercise over their resources when entering emerging markets? The influence of institutional voids on entry mode degree of control

Supplemental material, APPENDIX for How much control do firms exercise over their resources when entering emerging markets? The influence of institutional voids on entry mode degree of control by Claudio Giachetti and Augustine Awuah Peprah in Business Research Quarterly

Footnotes

Appendix

| Question related to the entry mode degree of control in China: Indicate the ways in which the firm has operated on the Chinese market until now (check the appropriate boxes): |

|---|

| Entry modes |

| Subsidiary on the Chinese market entirely controlled by the firm (entity resulting from the acquisition of an existing subject or from greenfield investment) |

| Subsidiary on the Chinese market only partially controlled by the firm (entity resulting from partial acquisition or joint venture) |

| Subsidiary on the Chinese market with which the firm has contractual relationships like franchising, licensing, or joint R&D |

| Export (direct and/or indirect) |

Acknowledgements

We would like to thank Associate Editor José Pla-Barber and the two anonymous reviewers for their invaluable comments and guidance during the review process, which helped strengthen this article. We would also like to thank Elisabet Garrido, Daniele Cerrato and Alessandra Perri for their thoughtful feedback on earlier drafts of this paper.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.