Abstract

This study aims to compare how leading companies in Spain and in Spanish-speaking Latin America communicate corporate social responsibility or sustainability on their web pages. For this purpose, the pages of 68 companies were examined to establish the accessibility of such topics and to trace how their prominence and wording had evolved over time. The results show a trend toward greater uniformity in both Spain and Latin America, with corporate social responsibility/sustainability discourse gaining in prominence and “responsibility”-related terms being gradually replaced by those related to “sustainability.” Various cases hint that changes in terminology may be unrelated to any clear distinction between both terms.

Keywords

In recent decades, the termsCorporate SustainabilityandCorporate (Social) Responsibility(henceforth CS and CSR) have been used by researchers without any clear distinction (Montiel, 2008;van Marrewijk, 2003). Like CS, CSR is considered an umbrella term covering a wide range of concepts related to the relationship between business and society. However, it is also used to refer to other notions such as corporate citizenship, corporate philanthropy, sustainable management, or corporate social performance (Bansal & Song, 2017;Bruhn & Zimmermann, 2017;Matten & Crane, 2005;Matten & Moon, 2008). Moreover, CS and CSR have been employed “interchangeably, inconsistently, and ambiguously” (Bansal & Song, 2017, p. 106). This has caused a blurring of the border between the two terms, both of which have evolved to cover an ever-wider conceptual area. For that reason, no concrete or rigorous definition of either CS or CSR will be given in this work, one of whose underlying hypotheses is that companies themselves have no such definition in mind when using these terms (see Research Methodology section). Instead, the aim is to establish whether companies with Spanish as a corporate language use these terms in a differentiated way, if their use of these terms has evolved, and how they might have evolved.

This article begins with a brief outline of the parallel development of CSR and CS and the rise of nonfinancial disclosure. The following two sections are devoted respectively to a literature review of web-based communication of CSR-related topics and the situation of nonfinancial disclosure in Spain and the Spanish-speaking Latin America. Sections on objectives, methodology, and findings follow. Finally, the findings and how they add to the literature on CSR communication in Spanish reviewed previously are discussed.

Corporate Social Responsibility and Corporate Sustainability

In management contexts, it is impossible to consider the concepts ofresponsibilityandsustainabilityin isolation. And, in fact, CSR and CS are used indiscriminately to refer to the wider semantic field that they jointly cover. Thus,van Marrewijk (2003)uses the acronym CS(R) to cover both concepts, a practice I will adopt here. He underlines the necessity of multiple definitions of CS(R), depending on the particular context in which a corporation operates, the way in which it develops, and the ambitions it harbors. Indeed, CS(R) is a social construction and accordingly may cover a wide variety of topics, while these and the relevant actors may differ depending on the context in which it is socially constructed (Dahlsrud, 2008). Thus, different cultural contexts are thought to convey different approaches to both CS(R) and the way in which it is communicated (Karmasin & Apfelthaler, 2017).

Montiel (2008)andBansal and Song (2017)situate the conceptual convergence of CSR and CS in the early 2000s. By then, the broad concept of CS(R) was being gradually introduced as a factor in shaping corporate strategies. One immediate result of corporations adopting the ideas related to CS(R) was the creation of documents disclosing a company’s actions and the vision to which they related. By 2011, 95% of the world’s 250 largest companies were publishing such CS(R) reports (Fifka, 2014;KPMG, 2011), at a time when production of nonfinancial reports was voluntary and therefore automatically considered a token of goodwill. Many benefits were attributed to responsible corporate behavior, and a business case was made for CSR (Carroll & Shabana, 2010). Thus, various factors such as willingness to improve a corporation’s reputation and the need to respond to stakeholders’ concerns about social and environmental issues, as well as imitative behavior designed to keep up with competitors (Nikolaeva & Bicho, 2011), prompted a rapid increase in reporting activities. In fact, it was probably thanks to this interplay of different factors that visible reporting on CS(R) came gradually to be seen as a necessity for large corporations and multinational corporations. Even so, it has been shown (Nikolaeva & Bicho, 2011) that, in some parts of the world, companies operating in problematic industries started reporting on CS(R) issues earlier than others in an attempt to increase their legitimacy. But, at the same time, it seems that public disclosure on these topics did not necessarily have the expected positive effects (Sen & Bhattacharya, 2001;Swaen & Vanhamme, 2004).

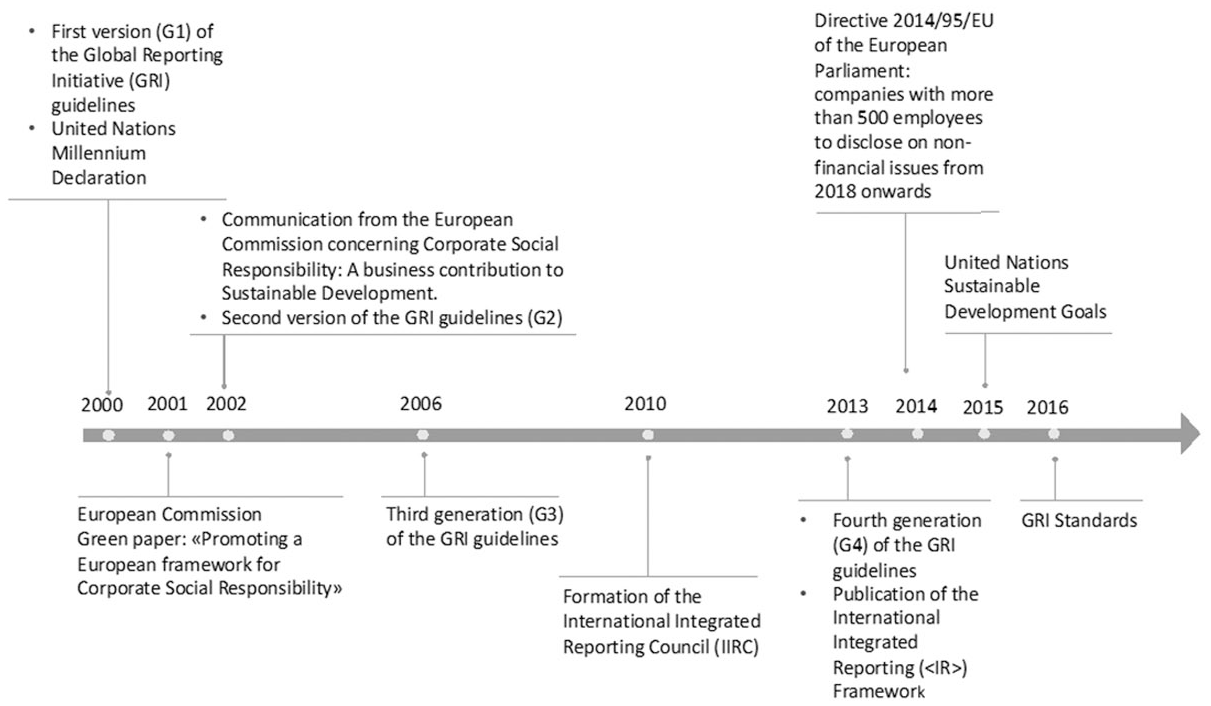

The rising interest in CS(R) issues, and the growing number of companies reporting on them, was reflected in various global and regional initiatives. These sought to guide corporations in best practice reporting on nonfinancial topics, with the aim of enabling comparability (Pistoni & Songini, 2015). A timeline showing some of the most important milestones in this process is shown inFigure 1.

Milestones in the development of nonfinancial reporting frameworks.

The most widely known and influential reporting standards organization is the Global Reporting Initiative (GRI), which has achieved widespread legitimacy (Nikolaeva & Bicho, 2011). As early as 2011, the GRI guidelines were being applied to report on nonfinancial topics by 80% of the world’s 250 largest companies (KPMG, 2011). Six years later, no less than 89% of them were using either a version of these guidelines or the GRI Standards for nonfinancial disclosure (KPMG, 2017b).

Along with the guidelines, and other recommendations on how to disclose on nonfinancial topics, the desire for comparability has encouraged a trend toward uniformity in the contents, form, and language of reports. It is apparent in the evolution of the reports’ names. ThusFifka (2012)hints at the appearance, from the 2000s on, of either “Corporate (Social) Responsibility reports” or “Sustainability reports,” which superseded the “social” or “environmental” reports issued by companies in the past decades of the previous century. Concentrating on terminological evolution in Europe,Gatti and Seele (2014)found that “sustainability”-related terms were gaining ground while “social”- and “environmental”-related terms were losing ground, a development they attributed to a change in the concepts and underlying theories employed by companies.

Web-Based CS(R) Communication

Web pages have long been an essential tool of corporate communication (Argenti, 2006). In fact, their key role in disseminating CS(R)-related information has been attested since the early days of the internet (Bowen, 2003). In 1998, 82% of Fortune 500 companies were already making reference to CSR issues on their websites (Esrock & Leichty, 1998), and by 2011, that figure had increased to 98% (Smith & Alexander, 2013). Web pages are used to pursue the same aims as other corporate external communication channels and practices (Cornelissen, 2014;Garzone, 2007). That is, companies use web pages both to disclose information of importance to companies’ stakeholders (Pollach, 2011) and to enhance their public image (Pollach, 2005), sometimes further legitimizing their actions in the process (Lock & Schulz-Knappe, 2019).

Today, web pages are one of two main channels used by corporations to communicate their agendas on CS(R) topics (Glausch, 2017), alongside conventionally published CS(R) reports. These documents belong to a genre that existed before companies started to communicate with the public via websites, and the first attempts to transmit CS(R)-related content via the new channel relied heavily on them. Indeed, for a number of years, many companies simply uploaded to their sites the CS(R) reports they had already published in printed form. And even today, such reports, or at least the parts devoted to nonfinancial topics, continue to represent one type of web-based CS(R) disclosures.

Nevertheless, the two channels—the web and conventional reporting—differ significantly in the way in which they communicate information (Malavasi, 2017). Certain features of web pages, such as multimodality and hypertextuality, mean that texts published on them are inevitably different in nature from printed reports. Moreover, the content of reports is always restricted to a single year’s performance, whereas web-based CS(R) disclosure tends to take a broader view, encompassing the company’s understanding of its mission and its role as a responsible actor. Accordingly, a second type of web-based disclosure gradually emerged to meet the needs of corporate web pages and to grasp the opportunities afforded by them (Garzone, 2007).

To date, research on CS(R) and web pages has focused mainly on three fields. The first, and by far the most prolific, is the study of CS(R) disclosure on the sites of different types of corporations. Thus, some studies have investigated how CS(R) issues are communicated by companies in particular sectors (e.g., banking:Hetze & Winistörfer, 2016; and banking specifically in Spain:Bravo et al., 2012; the pharmaceutical industry:Sones et al., 2009). Others have focused on particular countries (e.g., Japan:Fukukawa & Moon, 2004; Mexico:Wendlandt Amezaga et al., 2013; Portugal:Augusto, 2017; Spain:Capriotti & Moreno, 2007; the United States:Gómez & Chalmeta, 2011). And still other research has compared CS(R) disclosure in particular countries or regions (e.g., Asia:Chapple & Moon, 2005; China and the United States:Tang et al., 2015; emerging markets:Wanderley et al., 2008; Latin America and South East Asia:Calderón, 2011; Sweden and Spain:Castelo Branco et al., 2014).

Another field of interest for business communication researchers has been the analysis of web pages from a user point of view, focusing on usability, information accessibility, or topic prominence (Adams & Frost, 2006;Adelopo et al., 2012;Capriotti & Moreno, 2007;Chong et al., 2016). This type of research can be extended to relate to other indicators. For instance, a recent study (Chong & Rahman, 2020) suggests a correlation between CS(R) prominence in corporate web pages and the company’s financial performance.

The third approach to studying web pages has been to establish how they have developed. Some studies have focused on their evolution as a corporate communication tool in general (Argenti, 2006). Others pay particular attention to the way in which CS(R) is presented in web pages, the most prominent issues, and the extent to which CS(R) communication in specific web pages has changed over time (Basil & Erlandson, 2008;Meyskens & Paul, 2010;Smith, 2017;Smith & Alexander, 2013;Tang et al., 2015).

This last approach reflects the fact that web-based communication is changing very rapidly. In fact, the continuous, rapid evolution of web-based technologies is leading to constant changes in corporate communication, so that the conclusions of studies such as those quoted above may have lost their relevance. This is particularly the case if the data analyzed were gathered in the early days of the internet. Today, the new setting offered by mass access to Web 2.0 provides the actors involved (both stakeholders and companies) with new means of interaction. Corporate communication is no longer unidirectional (Capriotti, 2017).

CS(R) Disclosure in Spain and Spanish-Speaking Latin America

There is no lack of studies seeking to establish which factors are driving corporations to act diversely in adopting CS(R) measures and reporting about them. In both areas, a crucial role seems to be played by cultural setting—that is, by the contextual environment of the countries or regions where companies are active, including factors such as corporate and human values. Nonetheless, research on corporate communication has largely ignored a factor as important as the language in which companies primarily report. This omission may reflect the dominance of English, which means that some researchers may have a limited perception of the importance of language (Harzing & Feely, 2008).

Most companies operating in Spain and various countries of Latin America use Spanish as their corporate language. As a result, it is a fundamental factor influencing all corporate communication in those countries. Yet research in this direction is scarce. Indeed, one of the only contexts in which the role of language in corporate communication has been thoroughly addressed is in its impact on internationalization processes (Tenzer et al., 2017).

The use of a particular corporate language shapes communication at least as much as other aspects of cultural setting. It is therefore somewhat paradoxical that studies dealing with CS(R) communication in countries where English is not the main corporate language tend to be based on English versions of reports or web pages. This is the case, for instance, ofWendlandt Amezaga et al. (2013, p. 149), who state in their work that choosing Mexico as data source was a challenge because of the language spoken in the country—to which the authors responded by limiting their sample to those large companies in Mexico whose websites had an English version. Yet the English and Spanish versions of a single web page frequently include different contents and wordings, as they are not merely translated but instead are adapted to reach a different target audience. Thus, using data in the original corporate language is essential to ensure proper recording of changes in terminology use. This is also a key means to improve our understanding of international business communication.

Finding an equivalent term in another language for a particular concept will clearly be problematic if the concept itself is different in the two cultures concerned or perhaps not yet fully developed in one of them. As a result, examining the English versions of companies’ websites or public documents is unlikely to be the best way to analyze corporate communication primarily written in a different language.Holden and Michailova (2014)show the complexity of rendering various management terms in Russian and identify three possible problems in this context: lack of equivalence, cultural interference, and ambiguity. Specifically with regard to Spanish and English, it is easy to quote numerous examples of what seem simply to be unfortunate word choices in both languages. For example, in the Spanish version of the UN Sustainable Development Goals, the rendering of “decent work” astrabajo decentewill make most speakers of Spanish at least raise their eyebrows. The worddecentehad strong conservative, moralistic connotations under the Franco regime, and those connotations continue today.

Academic literature on CS(R) disclosure in Spain is abundant as the companies making up the IBEX 35 Index and those of the country’s strong banking sector have been directly and thoroughly addressed (Bravo et al., 2012;Capriotti & Moreno, 2007;Castelo Branco et al., 2014). This is undoubtedly linked to the country’s prolific reporting activity, as Spanish companies began disclosing on nonfinancial issues relatively early. In 2011, 88% of companies were already publishing a separate CS(R) report (KPMG, 2011); 6 years later, 87% of the 100 biggest Spanish corporations were not only publishing such reports but doing so with the use of the GRI guidelines (KPMG, 2017a). This trend was reinforced by the publication of European Parliament Directive 2014/95/EU, ratified by the European Council of 22 October 2014, which made nonfinancial disclosure a legal requirement (Council of the European Union, 2014).

Until very recently, scholarly analyses of reporting practices in Latin America were much less common (Fifka, 2012), as is confirmed by the literature reviews of two recent works. In their general bibliometric study of academic works addressing CS(R) reporting in Latin America,Sepúlveda Alzate et al. (2018)identified a total of 18 works published between 2006 and 2016. And in their investigation of the determinants driving Latin American companies to report on CS(R) topics,Durán and Rodrigo (2018)found just seven relevant studies. Apart from a few studies disseminated in various types of journal, most of the works were concentrated in a 2006 special issue ofThe Journal of Corporate Citizenshipunder the titleCorporate Citizenship in Latin America(Puppim de Oliveira, 2006). In it, one contributor spoke of Latin America as “terra incognita” where CS(R) was concerned (Araya, 2006). This dearth of research is consistent with the relative scarcity of empirical works on reporting practices outside Europe and North America (Araya, 2006;Chapple & Moon, 2005), which in turn probably reflects the fact that, for various reasons, nonfinancial reporting was long uncommon in emerging economies.

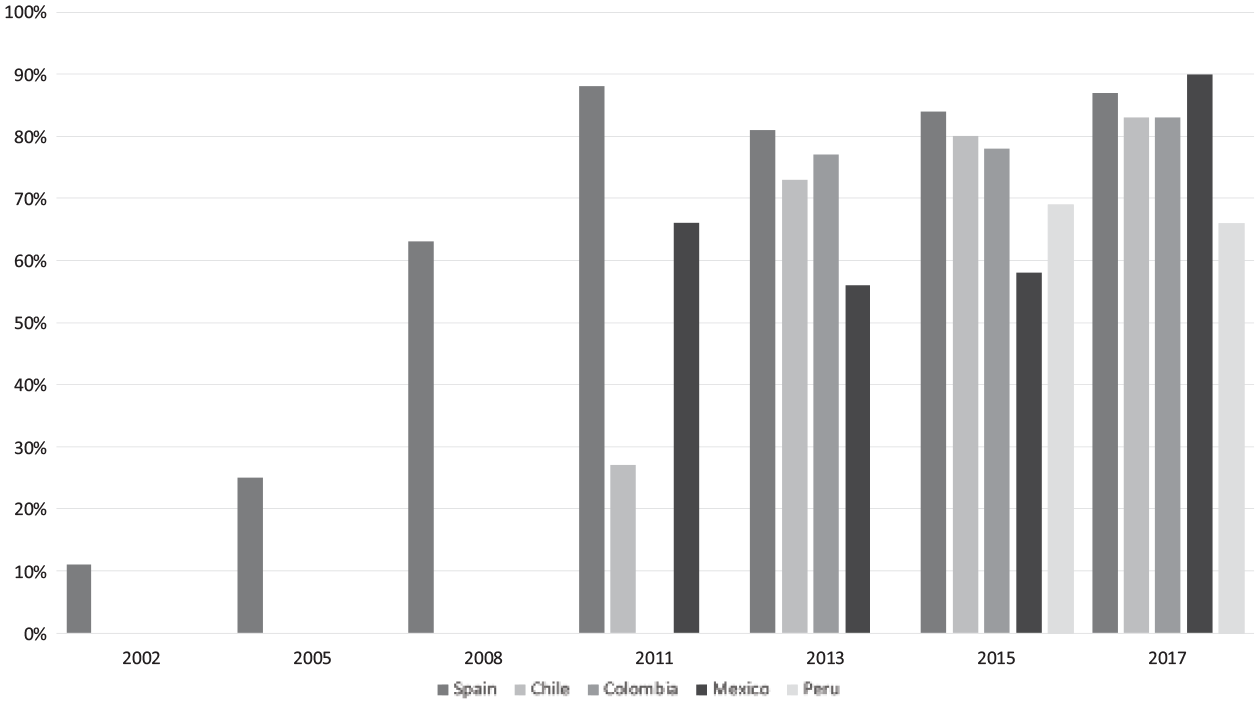

But circumstances are changing dramatically. In Spanish-speaking Latin America, CS(R) reporting has grown substantially in recent years, with Chile, Colombia, and Mexico all showing reporting rates above the global average (KPMG, 2017b). Nevertheless, Latin American companies’ adoption of GRI guidelines remains moderate relative to their Spanish counterparts (Alonso-Almeida et al., 2015).Figure 2shows the evolution of reporting rates in Chile, Colombia, Mexico, Peru, and Spain based on KPMG studies of each country’s 100 largest companies (KPMG, 2005,2008,2011,2013,2015,2017b). The absence of data for a particular country in a particular year does not indicate a total lack of reporting, but rather that the country concerned was not considered in the KPMG report for that year.

Evolution of CSR (corporate social responsibility) reporting rates among countries’ 100 largest companies based on KPMG studies of each country’s 100 largest companies.

Irrespective of the reasons that may be driving the tendency to report more frequently on nonfinancial issues, and of the reporting system used, the trend undoubtedly means that more data are available for analysis. Moreover, the research gap has already been noted, and in the past few years, CS(R) communication in the Spanish-speaking countries of Latin America has ceased to be such a neglected field. Nevertheless, the problem remains that some of this research has not been published in leading international journals. Instead, it has appeared in more local academic publications and/or in Spanish (see, e.g.,Madero Gómez & Navarro Garza, 2010;Vives & Peinado-Vara, 2011;Wendlandt Amezaga et al., 2015). This makes the dissemination of possibly valuable results difficult and, thus, also results in previous research being simply ignored.

As regards the rationale behind CS(R) efforts in Latin America, the findings of some previous works hint at mostly philanthropic motivations rather than ethical or legal reasons (Calderón, 2011). This fits with the reliance of the region on aid (Visser, 2008).Calderón (2011)found a possible business motivation, in that Latin American companies issuing separate CS(R) reports had higher sales, profit, and market value than those not doing so. This conclusion, however, runs counter to the results obtained byDurán and Rodrigo (2018)using a much larger sample. Their study suggested that, in Latin America, poorer financial performance triggers nonfinancial disclosure. Indeed, these authors even argue that reporting could be used as a justification for poor returns (Durán & Rodrigo, 2018, p. 12).

Not surprisingly given its size and economic importance, Mexico is one of the Latin American countries where CS(R) disclosure in Spanish has been most studied. Some research attempts to frame a particular understanding of CS(R) in Mexico as linked not only to culture and values (e.g., Catholicism) but also to endemic corruption (Logsdon et al., 2006). Connections have also been made with the general lack of emphasis on reporting in the country (Paul et al., 2006) and of a clear, distinctive evolution of CS(R) disclosure (Meyskens & Paul, 2010).

Among these works, some have even addressed CS(R) communication through web pages. Thus,Madero Gómez and Navarro Garza (2010)carried out a qualitative analysis of the sites of Mexican companies given awards for being socially responsible. The authors show how differently the awards were publicized, with some recipients not even mentioning them and others placing them prominently on their websites. Finally,Wendlandt Amezaga et al. (2013)conducted a content analysis of the websites of 150 large Mexican companies. They found that the most common motivation behind CS(R) reporting was to improve the company’s performance in terms of sales volume and profitability (as opposed to value-driven or stakeholder-driven motives). Only a few very recent studies have addressed CS(R) communication elsewhere in Latin America:Correa-García et al. (2018)andLoza Adaui (2020)on reporting in Colombia and Peru, respectively; Wendlandt Amezaga (2015) on the situation in Chile as compared with Mexico; andGómez & Borges-Tavárez (2017)on CSR communication via social media platforms.

Thus, some studies on how CS(R) is communicated in particular sectors or countries are indeed available. However, as already mentioned, no attempt has yet been made to carry out a general overview of companies using Spanish as their main corporate language. It is that research gap that this work aims to fill.

Objectives

This study focuses on how Spanish and Latin American companies using Spanish as a corporate language currently present information about CS(R) on their websites. It aims to improve our understanding of CS(R) online communication in Spanish and the way in which such communication has evolved. As noted above, Spanish is the corporate language of many companies operating in Spain and in numerous Latin American countries, which is one of the main reasons why comparing the two groups, as is done in this article, seems pertinent. This study aims to explore, in the first instance, how top-performing Spanish corporations in sustainability terms compare with their counterparts in Spanish-speaking Latin America in communicating their CS(R) practices on corporate websites. The cultural differences within Latin America notwithstanding, for the purpose of this research, we can think in terms of two different cultural areas sharing Spanish as a common language. In one of them, Spain, companies must comply with the European Union’s CS(R) regulations (relating to both implementation and disclosure). In the other, Latin America, regulations are either still evolving or not yet well established.

The research objectives have been defined using the following research questions:

Research Methodology

The sample used for this study consists of the corporate websites of a selected group of Spanish and Latin American companies considered top performers in CS(R). Specifically, they are those included in the FTSE4Good IBEX Index (26 companies) and the Dow Jones Sustainability MILA Pacific Alliance Index (42 companies). FTSE4Good IBEX is a Spanish index made up of companies from the IBEX 35 Index and the FTSE Spain All-Cap Index that meet particular environmental and social criteria (FTSE Group & Bolsas y Mercados Españoles, 2007). It was created in 2008 with the aim of providing a tool for socially responsible investment. As of May 2019, 26 companies were included in this index (see theappendix). Most of them are also included in the IBEX 35, which is the basic reference for the Spanish stock market both domestically and internationally. Among the criteria for inclusion in the FTSE4Good IBEX are environmental sustainability, positive relations with stakeholders, and preservation of human rights; excluded from the index are tobacco companies, weapon manufacturers, and operators of nuclear power plants (FTSE Group & Bolsas y Mercados Españoles, 2007). The Dow Jones Sustainability MILA Pacific Alliance Index was created in 2017. It includes those companies from Chile (18), Colombia (10), Mexico (13), and Peru (1) with the highest sustainability scores as measured byRobecoSAM’s (2018)CS assessment, based on long-term environmental, social, and governance factors (see theappendix).

The web pages of the 68 sample companies were examined between May and June 2019. First, the accessibility of information was noted by measuring the number of clicks needed to arrive at CS(R) topics from the main page. Once a relevant heading was found, either on the home page or at deeper levels, the particular terms used by the company to refer to CS(R) topics at that moment were recorded. A screenshot of the current home page was taken and filed to allow for later comparison. To allow for a diachronic perspective, previous versions of the companies’ home pages were examined using data archived in the Internet Archive’s Wayback Machine (https://archive.org/web/) and archive.today (https://archive.ph). A total of 536 screenshots were collected and filed to enable tracing of changes in CS(R)-related terminology.

Findings

Research Question 1: Accessibility of CS(R) Content in Spanish and Latin American Websites

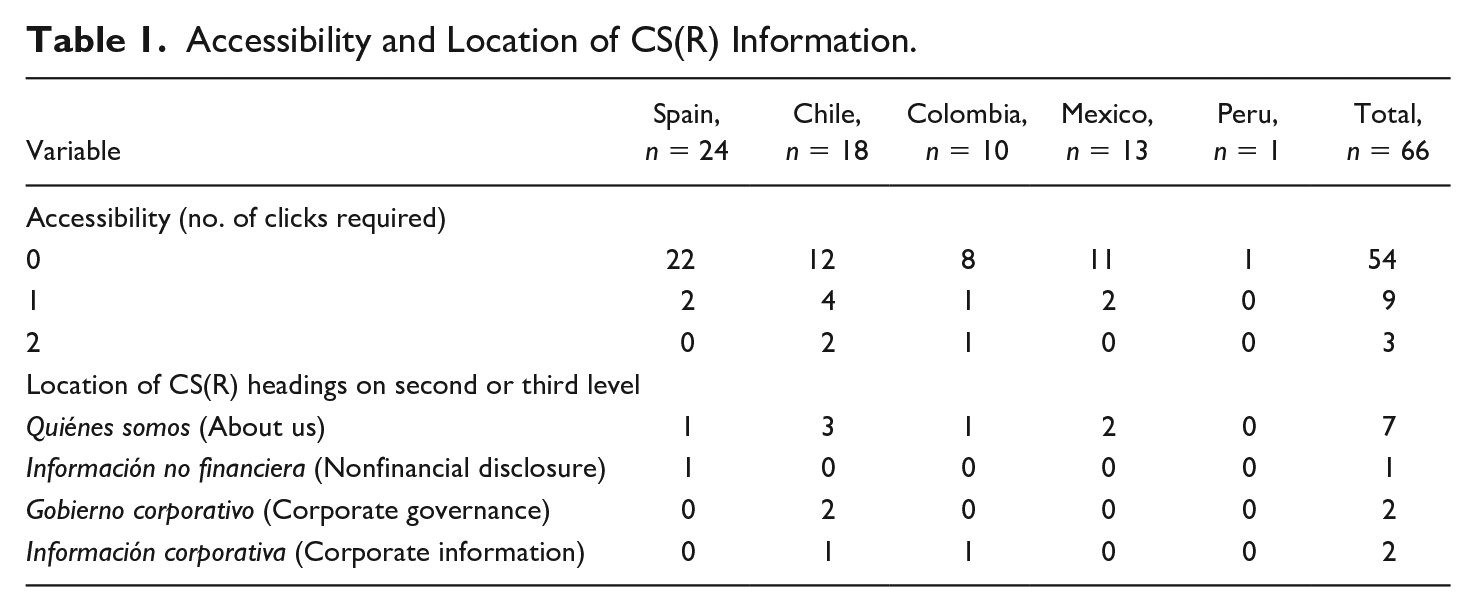

Of the 68 companies examined, all but two offered CS(R) information on their websites. The majority (54 in total) had headings on the first-level page (i.e., on the home page) dealing with CS(R). This means that, on accessing the page, a relevant item is found immediately, on the navigation menu, and there is no need to click on any other item in order to access the information sought. Of the remaining 12 companies, nine placed CS(R) content on the second level and three on the third, as shown inTable 1.

Accessibility and Location of CS(R) Information.

Of the 12 companies placing CS(R) content on a second or third level, seven located it in theQuiénes somos(About us) section, which sometimes had a different name such asNuestro banco(Our bank). The remaining five placed the content variously under the subheadingsInformación no financiera(Nonfinancial disclosure),Gobierno corporativo(Corporate governance), andInformación corporativa(Corporate information). The majority of these subheadings were found in theQuiénes somos(About us) section or equivalents. By and large, companies locating CS(R) content on a lower level seemed mainly to be those whose websites offer direct services to private clients (e.g., banks, airlines). In such cases, corporate information in general must be accessed indirectly.

Research Questions 2 and 3: Terminology Related to CS(R) Used on the Sample Sites: Comparison Between Spain and Spanish-Speaking Latin American Countries

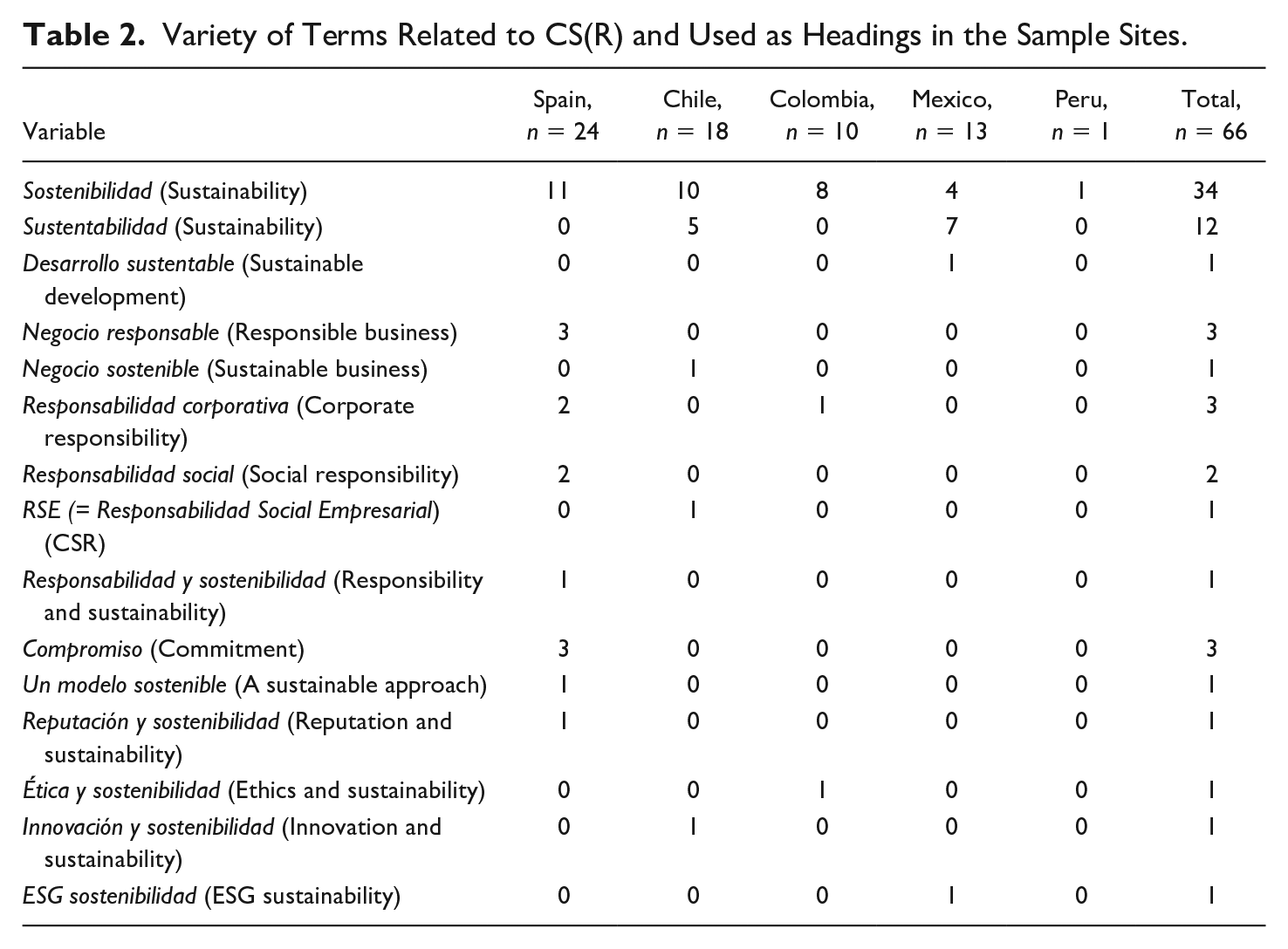

The variety of terms used as headings to introduce CS(R) topics in the various countries is shown inTable 2.

Variety of Terms Related to CS(R) and Used as Headings in the Sample Sites.

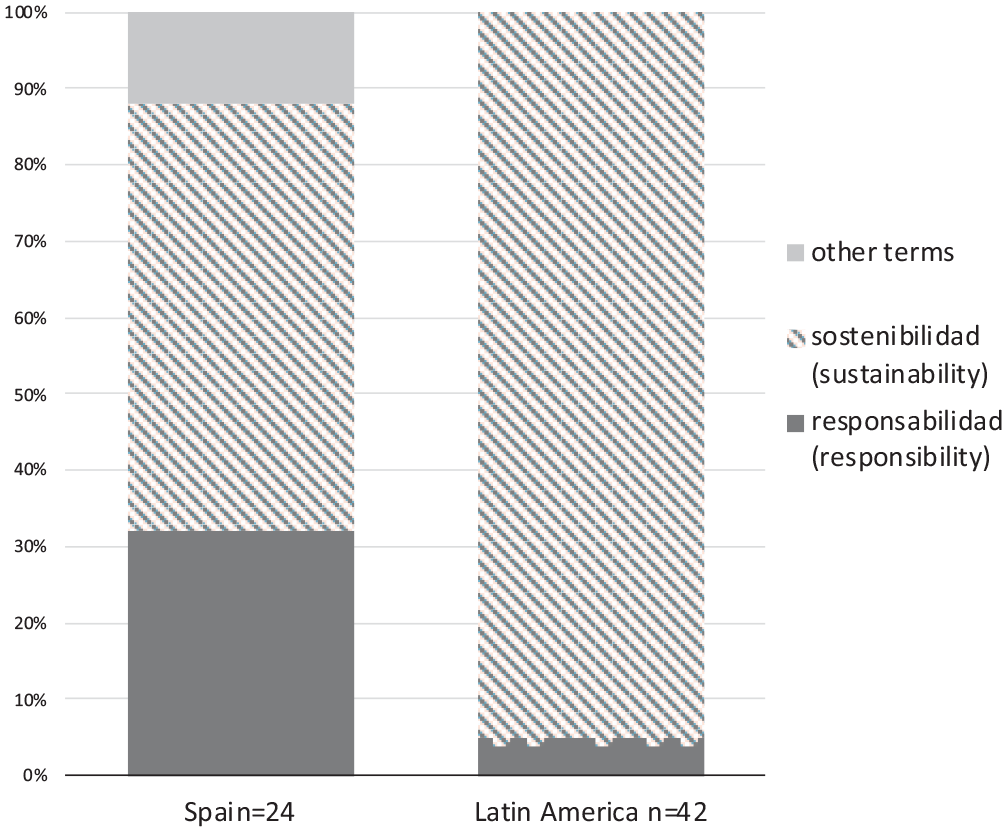

As shown there, the widest variety of terminology is found in Spain, which may of course simply reflect the country’s relatively large sample. Of the headings identified there, more than half includesostenibilidad(sustainability) or a related term. However,responsabilidad(responsibility) and related terms also occur frequently, accounting for 32% of the examples. The remaining 12% of headings (those of three companies) include the wordcompromiso(commitment). This range of terminology is very different from the pattern seen in the Latin American sample, where virtually all headings includesostenibilidador its synonymic variantsustentabilidad(sustainability), or their cognates. The two distributions are contrasted inFigure 3.

Distribution of the termsresponsibility,sustainability, andcognatesin CS(R) headings in Spain and Latin America.

As just remarked, Spanish has two different equivalents to “sustainability.” It has been argued thatsostenibilidadis the Spanish variant, whereassustentabilidadis the Latin American one. However, the distribution found here seems to run partly counter to this conception. Thus, companies in both Spain and Colombia usesostenibilidad(or other members of the same word family) without exception, whereas those in Mexico and Chile display mixed usage of the two terms and their respective cognates (Chile: fivesustentabilidadvs. 13sostenibilidad; México: sevensustentabilidadvs. sixsostenibilidad). In these two countries, there is a tendency for companies that self-define asglobalto usesostenibilidad, but word choice is not consistent, with individual companies alternating between the two word families in their reports.

Research Question 4: Changes Over the Years in Web-Based CS(R) Terminology in Spain and Latin America

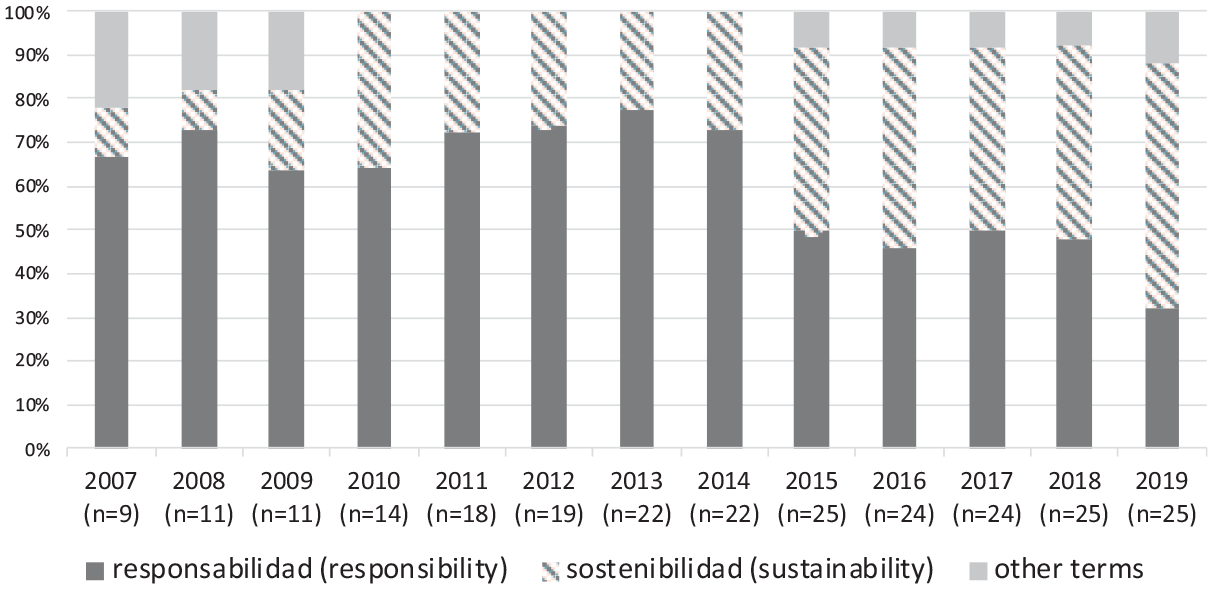

In the Spanish sample, there is clear evidence that terminology use has changed. While in the period 2007-2014 there was a clear preference for terms related toresponsibilidad, from 2015 onward a shift towardsostenibilidadis apparent. There is also evidence of a tendency to introduce new terms as headings. Thus, in the earlier period, a number of the companies examined referred tomedio ambiente(environment), orreputación(reputation). From 2015, however, some major players began usingcompromiso(commitment) as a broad heading for their CS(R) visions and strategies. The evolution of terminology since 2007 is illustrated inFigure 4, in which the data are presented as percentages of the total number of companies (n) that mentioned CS(R) on their home page in the year concerned. In 2010, for example, 14 of the 24 companies studied had a CS(R)-related heading located on their home pages. Up to 2015, the number of such companies grew constantly before levelling off at 24. One company used the headingResponsabilidad y sostenibilidad; this was counted as an example of both groups, which is why the sample number in 2018 and 2019 comes to 25 instead of 24.

Changes in the use of CS(R) terminology 2007-2019, Spanish sample.

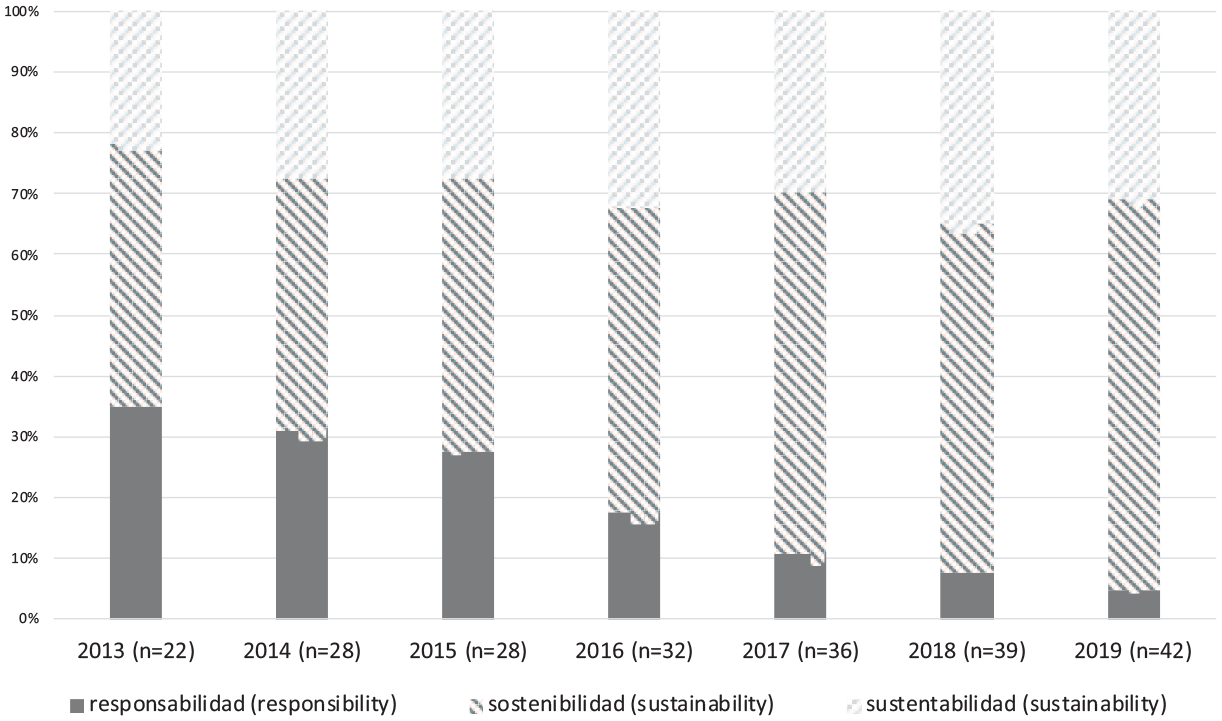

The Latin American data do not allow changes in terminology to be traced back as far as those for Spain. In part, this is because the companies included in the sample started to include CS(R) discourse in their webpages later than their Spanish counterparts. All we can state is that they have generally given CS(R) content less prominence, as it is often not present on the home page or the web menu. However, from 2013 onward, the decline in the use ofresponsabilidad-related terms is even more pronounced than in Spain, not least because the abbreviationRSE(Responsabilidad Social Empresarial) had been relatively widespread in Latin America. Here, too, there is notable variation in the distribution of the synonymic termssostenibilidadandsustentabilidad(with the latter, as mentioned above, appearing only in Mexico and Chile).Figure 5summarizes these results.

Changes in the use of CS(R) terminology 2013-2019, Latin American sample.

Discussion and Conclusion

In the foregoing, it has been shown that the importance given to CS(R) communication via web pages is growing, both in Spain and in Latin America. The vast majority of the sample companies now present their CS(R) content on the first level of their pages. Moreover, this content has been steadily gaining in importance, being accorded an increasingly prominent place there. In the case of Spain,responsabilidad-related terms have lost ground tosostenibilidadand their cognates. Nevertheless, the term “R(S)C” (Responsabilidad (Social) Corporativa) and its variants are still being used by about a third of companies in the service sector, such as banks, which have relatively little environmental impact. Some global players with a strong focus on corporate communication have sidestepped the choice between “responsibility” and “sustainability.” Instead, they have sought other terminology to imply that CS(R) is not merely a part of their business strategy but rather an overarching concept imbuing the totality of their activities. Examples includeInditex’s use ofUn modelo sostenible(A sustainable approach) andFerrovial’s ofCompromiso(Commitment).

At one time, the websites of those few Latin American companies concerned about their relationship with society also showed variation between “responsibility”- and “sustainability”-related terms. However, as more embarked on CS(R) discourse, they jumped on the sustainability bandwagon that by then was already rolling. As a result, “responsibility” and its cognates are now practically nonexistent in Latin American sites (Colombia: two instances; Chile: one instance). In Chile and Mexico, as already noted, the two Spanish equivalents to “sustainability” appear to be used indiscriminately, and there seems to be a trend toward replacingsustentabilidadwithsostenibilidad. In particular, companies that self-define as global tend to favor the latter, although in many cases, the choice of one term as a heading does not rule out use of the other in texts presented on the same site.

Previous research has addressed the evolution of CS(R) terminology on corporate websites in general (Argenti, 2006;Smith, 2017). In a few cases, there is evidence that changes in terminology have reflected changes in underlying ideas or strategy, as is illustrated by the evolution of the website ofInditex, Spain’s most valuable company. There, changes in heading terminology seem to parallel a redesign of the home page itself. Thus, the headingResponsabilidad Corporativaused in 2013 (Inditex, 2013) was changed toSostenibilidadin 2016 coinciding with a new web design (Inditex, 2016). More recently, the newest redesign of the home page included the substitution ofSostenibilidadas a heading with the more comprehensiveUn modelo sostenible(Inditex, 2017). This sort of change may hint at the adoption of a new communication strategy, or at least to general changes in the way in whichInditexpresents itself and its activities to its stakeholders.

More generally, though, a diachronic analysis of Spanish language sites provides little or no evidence to suggest that a simple change in terminology has reflected more profound factors. The point is illustrated inFigure 6, where the introduction of the headingSostenibilidad(Enagás, 2015) on the website of the Spanish companyEnagásto substitute the previously usedResponsabilidad Corporativa(Enagás, 2014) is unaccompanied by any significant redesign and does not seem to coincide with a more comprehensive change in the company’s communication strategy. Given this evidence, and the fact that even researchers find it hard to differentiate the two concepts CSR and CS,Gatti and Seele’s (2014)contention that companies are consciously adopting a change in denomination as a consequence of new strategic approaches seems questionable at best.

Enagás home page headings in 2014 and 2015.

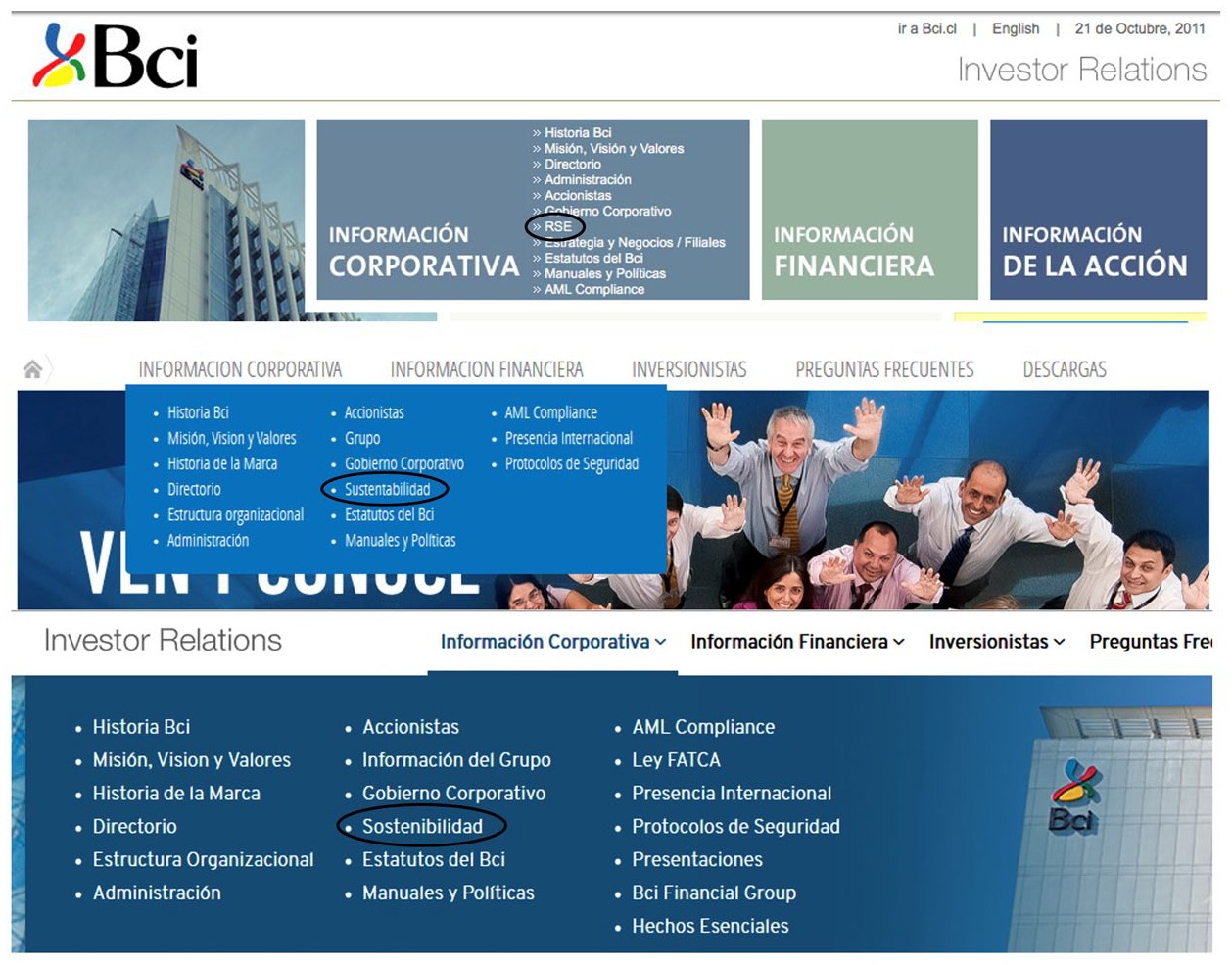

On the other hand, it does seem plausible to ascribe some changes in terminology, as well as preferences for a particular variant, to two other factors. The first plausible factor is a trend toward greater uniformity in reporting, which is designed to allow comparability of both communication and performance, and the second is a mere imitation of competitors. This can be seen in the case of the Chilean bankBci, as shown inFigure 7. In 2011, its website page had a subheadingRSE(Bci, 2011). In the 2016 version (Bci, 2016), this changed toSustentabilidad, while the term used in 2019 wasSostenibilidad(Bci, 2019). The first of these changes—fromresponsabilidadtosustentabilidad—exemplifies the Latin American trend (Figure 5above) of “responsibility”-related terms gradually disappearing to be replaced with others drawn from the word family of “sustainability.” The second change—fromsustentabilidadto its more common synonymic variantsostenibilidad—could be also seen as a quest for uniformity, driven by the imitation of both competitors and international reporting agencies.

Bci home page headings in 2011, 2016, and 2019.

Previous research has already suggested the existence of a trend in the titles of CS(R) reports, away from using previously common terms including the words “social” or “environmental” and toward use of “sustainability.” In the case of Europe, this trend was identified byGatti and Seele (2014)and in major U.S. corporations bySmith (2017). The results of this particular study are certainly consistent with the European and American trend, even if the pace at which “sustainability”-related terms are adopted appears to vary between Spain and the Latin American countries studied. But, of course, further research focusing on CS(R) communication in Asia and Africa, as well as Latin America, will be needed to establish whether the trend is a truly global one.

By the time CS(R) began to be adopted in Latin America, worldwide reporting standards had already been established with the GRI. Moreover, many multinational corporations established in the region set standards and transferred approaches that were then imitated by local companies. Thus, the preference in the region for “sustainability”—as opposed to “responsibility”—can be explained in part by the ever-growing influence of both theGlobal Reporting Initiative (n.d.)and theUnited Nation’s Global Compact (2020). When the UN Sustainable Development Goals were launched in 2015, the trend toward replacing CSR with CS in corporate communication was given new and decisive momentum.

The primary limitation of this preliminary study is determined by the characteristics of my data. While they clearly show an evolution in terminology use, they reveal nothing directly about the reasons driving these changes, which can therefore only be the subject of speculation. Going beyond that will require further research that incorporates a cultural perspective and the consideration of power issues.

At the same time, these rapid changes in corporate communication clearly indicate that limiting the researchers’ conclusions to a specific time period increases their applicability. That is undoubtedly the case for this article, which describes the way in which a sample of companies communicated CS(R) through their websites during the period up to 2019—something that may well have changed since the research was conducted. For this reason, future research should consider not only the situation at a particular moment but also its evolution, as the present study has done. A further limitation of its applicability is linked to the sample, which consists of top performers in CS(R) reporting. As a result, the findings are not necessarily representative of Spanish or Latin American companies as a whole.

One final reflection prompted by the data examined in this work concerns the speed with which corporate communication—and especially web-based communication—is evolving. The speed of evolution clearly has implications for both communication practitioners and for teachers of business communication. First, it means that concrete usage should be checked continuously by examining the most recent company-issued documents. Second, as stressed before, the redefinition of concepts does not necessarily run parallel to changes in terminology.

Footnotes

Appendix

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Author Biography