Abstract

Materiality assessments play an important role in helping firms to select the environmental, social, and governance (ESG) topics to include in their sustainability report. This article presents the six main steps of materiality assessments, the methods used, and how the complexity, uncertainty, and evaluative nature of sustainability issues complicate them. This article draws two conclusions: the selected materiality perspective influences how the other steps are conducted, and assessment results should not only focus on selecting win-win scenarios, but also on “tensioned topics,” which indicate material societal impact but lack a business case.

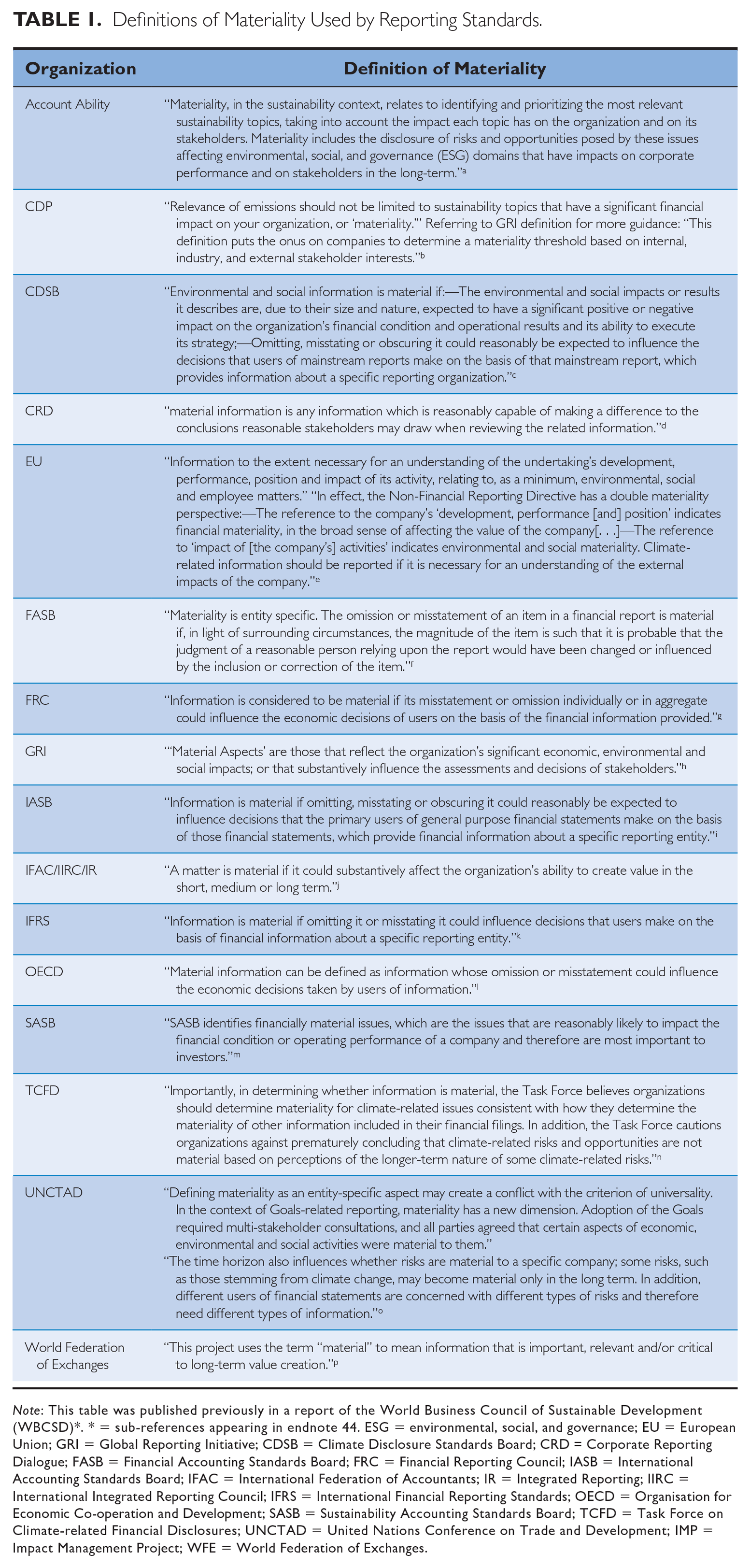

Definitions of Materiality Used by Reporting Standards.

Note: This table was published previously in a report of the World Business Council of Sustainable Development (WBCSD)*. * = sub-references appearing in endnote 44. ESG = environmental, social, and governance; EU = European Union; GRI = Global Reporting Initiative; CDSB = Climate Disclosure Standards Board; CRD = Corporate Reporting Dialogue; FASB = Financial Accounting Standards Board; FRC = Financial Reporting Council; IASB = International Accounting Standards Board; IFAC = International Federation of Accountants; IR = Integrated Reporting; IIRC = International Integrated Reporting Council; IFRS = International Financial Reporting Standards; OECD = Organisation for Economic Co-operation and Development; SASB = Sustainability Accounting Standards Board; TCFD = Task Force on Climate-related Financial Disclosures; UNCTAD = United Nations Conference on Trade and Development; IMP = Impact Management Project; WFE = World Federation of Exchanges.

The lack of a common materiality definition allows room for managerial discretion on materiality decisions. 5 While for financial reports, managerial discretion is limited by mandatory reporting standards and materiality thresholds that are set independently by auditors; for non-financial reports, materiality assessments are conducted by the firm itself without standardized methodologies. 6 This lack of standardized methods facilitates greenwashing, that is, “disclosure of positive information about a company’s environmental or social performance, without full disclosure of negative information on these dimensions, so as to create an overly positive corporate image.” 7 The purpose of greenwashing is to mislead consumers and other stakeholders, often to cover up acts of decoupling within an organization. 8 In decoupling, whether intentional or unintentional, the activities and performance of the organization do not align with the firm’s communicated objectives and related policies. 9 This alignment can be especially difficult in acting upon a sustainability strategy, as firms face the inherent tensions between divergent stakeholder demands, which result in a plurality of competing organizational goals. 10 In responding to this performing paradox, firms often make trade-offs between stakeholder demands, choosing the demands that deliver short-term financial gains over demands where such gains are questionable or only achievable in the long term. 11 When transparently communicating their materiality assessments, such trade-offs become visible, which damages the trust of stakeholders whose demands are ignored. 12 Therefore, firms are seen to provide vague descriptions of their materiality assessment, leaving readers in the dark on the data and criteria underlying their materiality decisions and leaving room for management to engage in greenwashing.

To combat obscure materiality decisions, scholars have previously called for standardizing materiality per industry. 13 Standard setter Sustainability Accounting Standards Board (SASB) has responded to this call by creating their materiality map, which provides a standardized list of material topics per industry. 14 Conversely, other scholars have pointed out that often multinational enterprises (MNEs) are not bound to one industry. 15 Furthermore, industry-level materiality ignores the characteristics of the firm and simplifies the complexity, uncertainty, and evaluative nature of sustainability challenges. 16 These three characteristics of sustainability challenges create inherent tensions in firms, which surface in different ways depending on the organization. 17 As Puroila and Mäkelä explained, “Due to the complexity of sustainability topics, their materiality varies in terms of time, context and perspective.” 18 Materiality should thus be seen as organization-specific and time-sensitive.

To prevent vague or biased materiality assessments while still treating materiality as organization-specific, materiality assessment for non-financial information should be further standardized. In a first step, the five main standard setters for non-financial reporting have started to consolidate their definitions and have come to a consensus that there are two main perspectives on materiality. 19 In this article, we describe these perspectives as the business case perspective—that is, an ESG topic is material when it significantly influences the financial performance of the firm; and the societal impact perspective—that is, an ESG topic is material when it reflects a significant part of the firm’s economic, environmental, or social impact on society. By asking the firm to take in both perspectives, also referred to as “double materiality,” the European Union (EU) Commission mandates firms to go beyond the business case perspective. 20 While this consolidation of definitions is the first step toward transparency regarding materiality decisions, it does not address the methods to assess materiality. Without consensus on these methods and how to report on them, descriptions of materiality assessment can be incomplete and vague, making it difficult for readers to evaluate and compare materiality decisions of firms. 21

To support standardization of materiality assessments of ESG topics, this article provides an overview of the methodological decisions taken in these assessments. The complexity, uncertainty, and evaluative nature of sustainability challenges complicate the materiality assessment. Building on previous research, 22 our analysis of 427 corporate reports and 20 interviews identified six main steps of materiality assessments and how these are influenced by the three sustainability challenges. Materiality assessments are often seen as tick-the-box exercises, needed to comply with reporting standards but not supported by sound methods. As one of our interviewees stated, “Materiality assessment is more of an art than a science.” Some firms do take this exercise seriously and use the results to (re-)couple the firm’s strategy, activities, and reporting. Firms can use materiality assessments to identify and explore tensions and discuss the limitations of these assessments to prevent greenwashing.

The Three Characteristics of Sustainability

To determine which non-financial data to disclose, firms need to assess and compare the materiality of ESG topics for their business. Underlying these ESG topics are sustainability challenges regarding human welfare and well-being that go beyond the boundaries of a firm. 23 These sustainability challenges have three characteristics that complicate the assessment of materiality: complexity, uncertainty, and an evaluative nature. 24

First, sustainability challenges are complex as they result from the interactions of many actors, and no single actor can be identified as the root cause of the problem. 25 This shared responsibility is referred to as “the problem of many hands,” 26 where multiple actors are involved and none of the actors is in control of the full problem. 27 For some sustainability issues, change can be facilitated by one actor in the chain but the costs for this change are borne along the chain, for example, working conditions in agriculture, fashion, or mining. In other sustainability issues, tensions arise between responsibilities at the individual, organizational, and system levels, whereby individual and organizational actions insufficiently address the problem at a system level. 28 For example, problems of plastic waste are not solved by a retailer not handing out plastic bags. It requires behavioral change of all stakeholders involved, for example, consumers, manufacturers, and waste management companies. Consequently, whether a sustainability issue is material for a firm is influenced by how the responsibility is distributed among actors and whether the firm can facilitate change at the individual, organizational, and/or system levels. Both factors are difficult to determine and vary between contexts and over time.

Another aspect that makes sustainability challenges complex is their interconnectedness. Interconnectedness can lead to unintended, negative consequences, as illustrated by the case of biofuel, whereby the use of agricultural land to produce ethanol led to local food scarcity. 29 Interconnectedness also complicates acting on only one issue at a time without accounting for the impact on other issues. For example, in combating deforestation, problems like economic inequalities, Indigenous rights, and corruption issues should also be tackled. Such interconnectedness complicates a materiality assessment in which the ESG topics are compared individually.

Second, sustainability challenges are uncertain. Three sources of uncertainty can be identified. The complex systems behind sustainability challenges complicate predicting the behavior of each actor in the system and how other actors will respond to these behavioral changes. In addition, new scientific insights on the causes and consequences of sustainability challenges are produced every day, and many insights are still to be uncovered. Changes in preferences of societal actors, captured in public opinion or regulation, can make ESG topics more or less material. 30

This uncertainty tempts firms to conform to established practices and institutional pressures, while sustainability challenges ask for innovation and alternative pathways that challenge the status quo. 31 Uncertainty also facilitates short-termism. 32 Creating social and environmental value requires a long-term orientation, accounting for the needs of future generations. 33 However, these long-term outcomes are highly uncertain, making the eventual economic value created unpredictable. Therefore, firms are seen to prefer outcomes that provide economic value in the short term. 34 Favoring ESG topics with short-term impact in their materiality assessments might provide firms a feeling of certainty, but their reports end up underestimating or even ignoring ESG topics with long-term impacts.

Third, sustainability challenges are evaluative in nature. Societal actors have opposing views of what the problem is and what solutions are acceptable and urgent. 35 Although firms are used to dealing with competing and conflicting claims of their stakeholders, 36 sustainability issues enlarge these conflicts. Sustainability issues cross the boundaries between disciplines, making it impossible to classify a problem as solely an economic, environmental, or social problem. 37 In addition, because sustainability challenges cross jurisdictional and cultural boundaries, conflicts between the needs and values of multiple communities may arise, 38 which are not easily solved due to a lack of transnational governance. 39 The materiality assessment can be seen as a reflection of how the firm perceives stakeholders’ expectations and how decisions are made in light of these conflicts. 40 They could provide insights into how firms handle the performance paradox, in which firms pursue their own interests and collective interests simultaneously. 41 In addition, when engaging with individual stakeholders, the materiality assessment can expose where the individual value systems collide with collective value systems and identities, the so-called belonging paradox. 42 However, as Eccles and Krzus previously observed, firms rarely disclose these tensions and resulting trade-offs transparently. 43

The observations of previous research give us some indication that these three characteristics of sustainability challenges can complicate the materiality assessment for ESG topics. However, in supporting firms in conducting materiality assessments and avoiding selective disclosure, a more in-depth analysis of these challenges is required.

Challenges in the Materiality Assessment

To investigate how the three characteristics of sustainability—complexity, uncertainty, and evaluative nature—complicate materiality assessments, we analyzed 477 corporate reports (annual/sustainability/integrated) published by the members of the World Business Council for Sustainable Development (WBCSD) in the years 2017, 2018, and 2019. 44 Of those reports, 427 (89.7%) contained information on materiality assessments conducted by the firm. To triangulate these data and strengthen the validity of the research, 45 we conducted semi-structured interviews with managers of 20 MNEs who were responsible for their firm’s materiality assessments. The 20 MNEs responded to an invitation, sent to 53 firms purposefully selected from the report dataset to create a representative sample of the WBCSD membership in terms of region, country, industry, and the number of reports available. For several cases, multiple persons were interviewed in group interviews, as in those firms, the coordination and execution of the materiality assessment were carried out by multiple persons. The interviews took 50 to 90 minutes and were conducted between April and June 2020.

The interview guide was based on the steps of materiality assessments previously identified by Eccles and Krzus. 46 To analyze the reports and interviews, an initial coding scheme was created and then adjusted based on the first 100 reports. The final coding scheme contained six steps for materiality assessments (see Conclusions, Table 2) and a code “tensions,” inductively extended with sub-codes for specific tensions. After coding all reports and interviews, the tensions were summarized for each step and compared with the three characteristics of sustainability challenges, that is, complexity, uncertainty, and evaluative in nature. 47

Choosing the Materiality Perspective

In the first step of a materiality assessment, a firm needs to decide what makes an ESG topic material to their organization. Of the 427 reports with a materiality assessment, 65.1% mentioned the perspective(s) used, mostly as the axes of their materiality matrix. In total, three perspectives on materiality were identified: the business case perspective, the societal impact perspective, and the stakeholder view.

From the business case perspective, an ESG topic is material when it significantly influences the financial performance of the firm. In interviews and reports, this perspective was also referred to as “materiality in the traditional sense,” “financial materiality,” and “ESG-related risks and opportunities”; 57.6% indicated using the business case perspective as one of their dimensions in their materiality assessment.

From the societal impact perspective, an ESG topic is material when it reflects a significant part of the firm’s economic, environmental, or social impact on society. This perspective was also referred to as “impact of the firm,” “impact on society,” or “environmental and social impact”; 11.5% of the reports mentioned the societal impact perspective.

Regarding the third perspective, 54.8% of the reports referred to materiality as the importance of topics according to (external) stakeholders. This perspective is problematic as it cannot be clearly distinguished from the other two perspectives. How this perspective is defined depends on the question asked the stakeholders: Were they asked to rank the topics based on their impact on the business or based on the firm’s impact on society? The majority of the reports indicating this “stakeholder view” did not elaborate on the question that was asked and thus overlap with the other two perspectives cannot be ruled out.

Finally, in 16.4% of the reports, the descriptions of materiality were too vague to determine the perspective used. These vague descriptions (e.g., “level of significance,” “relevance of topic”) could be a consequence of firms having difficulty navigating the multiple perspectives. As one interviewee indicated, “[The perspectives on materiality] need to be more standardized because having all these different definitions starts to get very conflicting for a company and time-consuming” (Interview Case 05).

In choosing the materiality perspective, one particular tension is visible: the tension between organizational interests and collective interests caused by the evaluative nature of sustainability issues. With the organizational interests represented by the business case perspective and the collective interests represented by the societal impact perspective, the existence of two perspectives shows that differences between these interests are recognized. When firms score the ESG topics on both perspectives, several interviewees indicated that conducting the assessment allowed them to identify which departments experience these interests and tensions between them:

When I go to other people in the company and talk about materiality, it’s challenging to focus their attention on our impact outside. To explain that some things may not feel material in the traditional sense: that it has a larger effect on our business, but it’s material in the sense that our stakeholders are very interested in it. Things that may not be costing us money necessarily but may cause an impact on the environment. It really is a challenging thing to get the team engaged to talk about it in the way that you need to report. (Interview Case 17)

When the different perspectives on materiality clashed, it was harder to reach a consensus internally on the material topics.

However, not all firms appeared to perceive or use these two perspectives on materiality. In 61.2% of the reports, the firm described materiality as a combination of two perspectives. The other reports used only one materiality perspective, often focusing on the business case perspective. These firms did consult external stakeholders but asked them to rank the ESG topics based on the financial risks and opportunities for the firm. Other reports included both perspectives but indicated no tensions between them, making it seem like the organizational and collective interests were completely aligned.

Specifying the Topics

As the second step in materiality assessments, a firm needs to define the topics to be included. Many firms start by summarizing the ESG topics mentioned in reporting standards and sustainability indices. Firms then adjust the terminology to their context, aligning it with the language of their organization and their stakeholders. The contextualization explains the large variety of labels for ESG topics across the reports. To illustrate, in the 2017 reports, we identified 49 different labels for topics related to climate change and greenhouse gas emissions. Interviewees indicated that this step was more challenging than they initially anticipated: “I think for us—we’re such a large, diversified organization—identifying a set of issues that are relevant across the enterprise was the most challenging part” (Interview Case 15).

The labels of ESG topics vary in their specificity and their framing. Concerning specificity, an ESG topic can be given its own specific label or can be grouped with other topics under a general label. As one interviewee explained it,

We now have 19 issues, and 169 topics underlie those issues. Because some of the topics have now become an issue such as “biodiversity.” Previously, that was at the topic level, but it has been coming up on the agenda. [The topic] has been promoted [to issue]. And some issues have now become topics within issues and some topics merged, according to changes in the landscape. (Interview Case 09)

The framing of the topics relates to the aspect of the impact that the label describes: a business activity (e.g., the CO2 management system), an immediate output of business activities (e.g., low carbon operations), a medium- or long-term outcome of the firm (e.g., reduction of CO2 emissions), or a general societal issue (e.g., climate change). These framings were not consistently used, meaning that within one assessment, some topics were framed as a business activity or immediate output while others were framed on a societal level. The downside of using diverse framings in one assessment is that topics become less comparable. For example, how to compare societal issues like “climate change” with business activities like “supply chain management” or “whistleblower procedures” and with an immediate output like “gender equality within the workforce” or “equal payment’? Another drawback is that topics can start to overlap. For example, one assessment included both “climate change” and “greenhouse gas emissions.”

The specification and framing exercises were used to handle the tensions created by the complexity and uncertainty of sustainability. Regarding the complexity, grouping specific topics in general labels seemed to be a solution to handle the interconnectedness between topics. These groupings allowed the firm to minimize the number of topics in the assessment, creating a clearer overview in their final materiality matrices. To illustrate,

A global issue [is] deforestation, but that’s not our business. We are not in natural forests. We are using plantation material. Our industry peers would have a collective term such as “responsible forest management” or “sustainable forest management,” where the term was initially “deforestation” or “conversion.” [Thus,] we try to connect to those [terms] and say, “Let’s talk about a wider concept than the issue [of deforestation].” (Interview Case 12)

Yet, in some cases, this grouping of topics also led to too general labels that are hard to interpret, for example, “Indirect Impact & Influence,” “Social Responsibility,” and “Constructing a Sustainable Society.” When asked about such general labels, two interviewees had to look up the definitions and showed confusion about the topics covered by the label.

In addition, the framing of topics was used to handle shared responsibilities for sustainability challenges. Firms used different framings to indicate for which aspect of the sustainability issue they perceive control and responsibility. The labels concerning business activities or specific outcomes were used for topics that fell within the firm’s control and that the firm was able to monitor. For the societal issue framings, the firm had often not pinpointed its specific role in the shared responsibility.

To break out “diversity & inclusion” as its own materiality topic would have been a bit too light. . . . As important as it is for [our firm], we have a very high percentage of male employees. That’s just the nature of the construction industry. There is a limitation to what we can do to increase. (Interview Case 05)

General framings were also used for sustainability issues of which the causal chains are still uncertain due to a general lack of knowledge. For example, in the reports, the topic “biodiversity” was more often referred to using general framings. As an interviewee explained,

There’s a lot of discussion on the company’s responsibility [for] biodiversity. If you are a manufacturing company and you have a factory that produces products, what is your impact on biodiversity and what should you be aiming to contribute to this topic? (Interview Case 02)

Due to this lack of knowledge, a sector might not have established how they affect or are affected by the sustainability issue. Therefore, firms in this sector may choose less explicit framings for these topics.

Determining the Information Sources

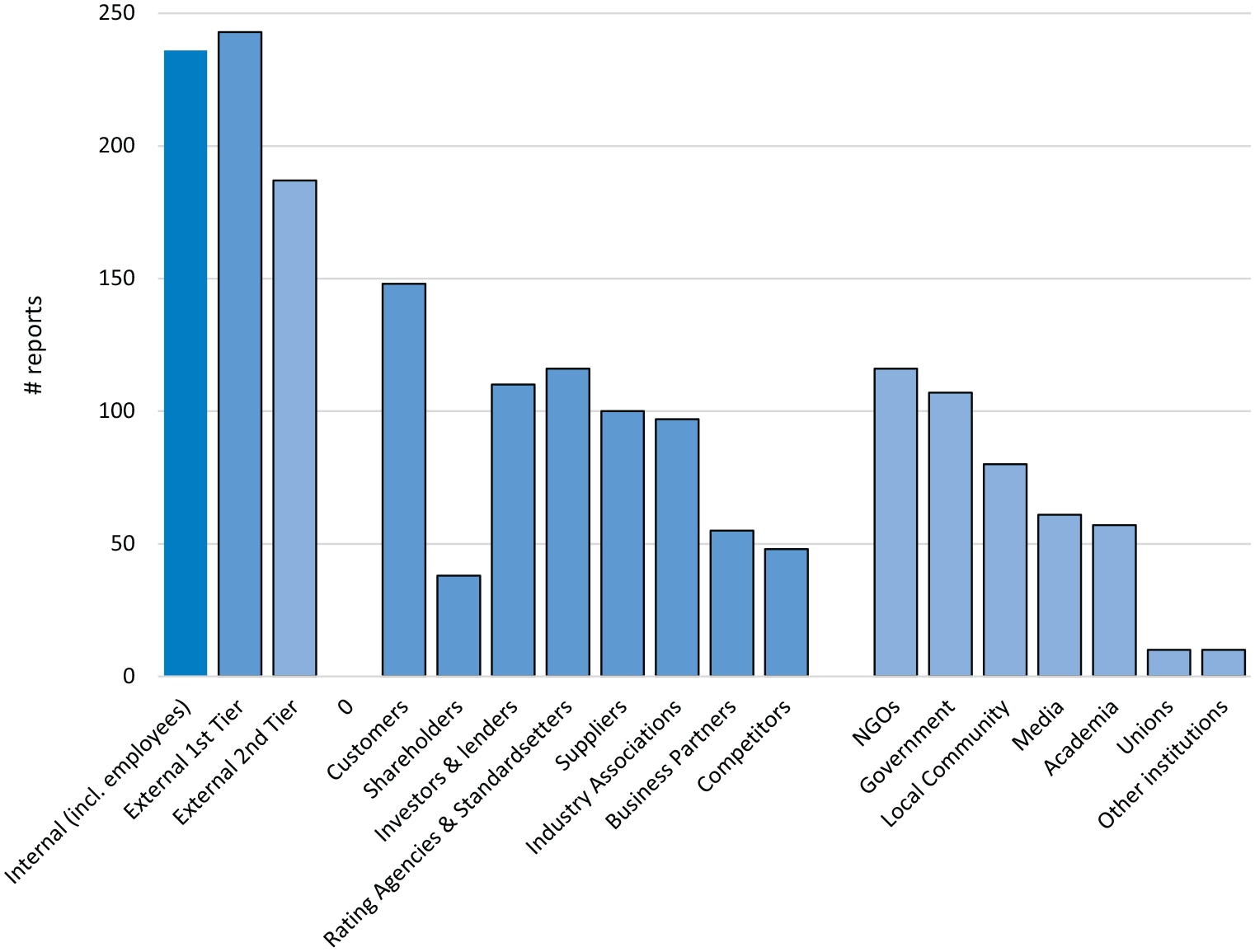

The third step in the materiality assessment is to decide which information sources to use for determining the materiality of ESG topics. Figure 1 presents the stakeholder groups included in the investigated materiality assessments. Further analysis showed that the selected sources differ per materiality perspective. For the business case perspective, the firms are consulting their management teams and internal topic experts (i.e., internal stakeholders). In addition, external consultants and market analysts (i.e., business partners) can be used to make estimations of (financial) risks and opportunities per topic. For the societal impact perspective, firms are most likely to consult external stakeholders, both first- and second-tier stakeholders. For the “stakeholder view,” there is no clear pattern in source selection: some reports include employees, whereas others focus on external stakeholders from either the first or second tier.

Overview of stakeholder groups explicitly mentioned in reports as actors the firm engaged with for their materiality assessment.

Also, in this step, the three sustainability characteristics result in tensions. In acknowledging the shared responsibility for complex sustainability issues, firms broaden the scope of their information sources. For the business case perspective, the scope includes aspects up and down the supply chain that could provide potential risks and opportunities. Firms perceive that they are no longer only held accountable for their own actions, but are also held accountable for the actions of their business partners. One interviewee explained that the scope of their materiality assessment changed after a firm that they co-owned was involved in a corruption scandal. Even though they only had a minority share, their reputation took a hit. Intelligence about subsidiaries, local operations, and reputational risks was taken more seriously in their subsequent materiality assessment. From the societal impact perspective, the shared responsibility for sustainability issues also stimulates firms to broaden the stakeholders involved in their assessment. To illustrate, one business-to-business firm indicated that they involved academics with expertise in their customers’ environmental and social impact: “Our [questionnaires] also embedded much more our customer’s value chain. When we enable our customers to reduce their energy consumption, the impact on CO2 is much bigger than if we just would focus on our own operations” (Interview Case 10).

Related to the uncertainty surrounding sustainability issues, tensions between the short and long term appear in the selection of sources. From the business case perspective, sources on immediate effects on financial performance are easier to find than data providing a forward-looking view on long-term, uncertain effects. As one interviewee explained,

This is where we have an issue with software that uses artificial intelligence to bring up the issues that are appearing the most in documents on social networks and so on. Because that gives you what was material to your stakeholders in the last six months. It doesn’t tell you what will be material next year or five years from now. (Interview Case 03)

This situation is similar to the case of the societal impact perspective. While finding stakeholders that experience the firm’s short-term impacts are easily pointed out, firms are struggling to have the voices of future generations represented in their assessments. A few firms reported the use of youth panels, but these panels have trouble forecasting the future impact of the firm on their lives.

The evaluative nature of sustainability issues shines through in the representativeness of information sources used. Do the information sources give a complete picture, detailing the diversity between and within stakeholder groups? Selection bias and lack of sources for certain stakeholders are the biggest challenges in creating such a representative sample. Selection bias arises when firms depend only on their own network. The advantage of stakeholders from their network is that these actors are familiar with the firm and thus have a good understanding of the firm’s impact:

[The selected] NGOs have worked with us. They already know what our potential issues are, they are more familiar. Their input is quite important and more comprehensive or insightful than maybe NGOs or other organizations that don’t have anything to do with us. (Interview Case 04)

This argument was expressed for the selection of both first- and second-tier stakeholders. However, the drawback of sources close to the firm is that these actors are likely to have a similar value system as the firm and might not be able to recognize new material topics. This selection bias was recognized as problematic by a few firms, and preventive actions were taken. From the business case perspective, some firms reported actively searching for new external experts to provide new insights, trying not to only draw on internal expertise. From the societal impact perspective, a few firms were seen to actively reach out to societal actors that previously opposed his firm’s actions. However, these actions were not always fruitful, as one interviewee indicated: “Some of [the NGOs] didn’t really want to engage in our process because they may not [like] our ways. I suppose they didn’t want to be biased towards any company or anything like that” (Interview Case 05).

The lack of information on certain stakeholder groups—for example, caused by non-response—also led to unbalanced samples. Missing representation was an issue for stakeholders that are not allowed to have a voice (e.g., employees without the right to unionize or without legal immigration status) and non-human actors that do not have a voice (e.g., animals): “Actually, I was quite keen to have the planet as a stakeholder. But then how do you measure that? Or who is that?” (Interview Case 01). Although the NGOs and activists represent these “voices of the unheard” that they are engaged with, interviewees indicated hesitations to provide these actors the same weight as other stakeholders.

When stakeholder groups are underrepresented in the assessment, giving their representatives more weight can (partly) remedy bias. Weights were used in practice but not to correct for missing representation. Instead, the higher weights were often provided to the stakeholders with the biggest influence on the firm’s short-term financial performance. According to the interviewees, using these weights would provide a more realistic image of the stakeholders’ pressures that their firm experiences:

I don’t know if their opinion matters more. It’s more that they are a priority to [our firm] being able to deliver on the business strategy. One thing that we learned early on is that you can’t cater to all stakeholders. We had to prioritize, it makes for a much more effective strategy. (Interview Case 15)

Whereas they represent a business case perspective, these weighing criteria were also used for the societal impact perspective. Furthermore, details on the weighing criteria were not reported.

To check whether the sample was representative, firms are seen to conduct validity checks on the final results, sometimes externally but mostly internally. The difficulty of these validity checks is that the final result combines the views of stakeholders into average materiality scores, and individual stakeholders will no longer recognize their views in this total picture:

The only difficulty is that the matrix does not represent any of our functions or businesses. But it represents the group, speaks of all the functions and our businesses. Our [separate] businesses should recognize some of what’s in here, but they cannot recognize all of it. (Interview Case 02)

Therefore, the effectiveness of these validity checks is questionable.

Assigning Materiality Scores

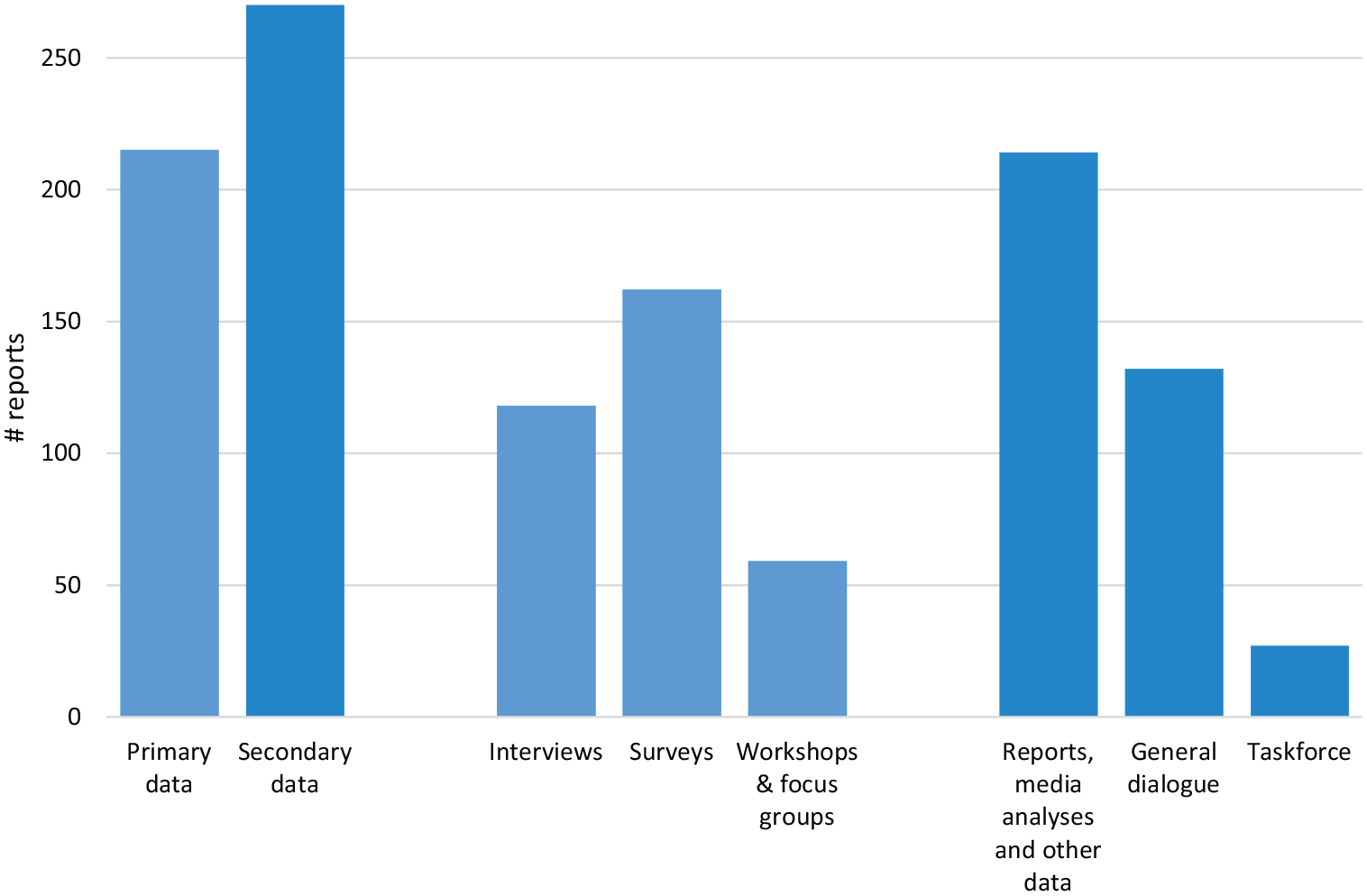

After selecting information sources, data need to be collected from these sources to assign the materiality scores. Of the reports, 25.2% did not specify what type of data was collected for determining materiality scores. To collect data about either perspective, firms can choose primary data sources in which they engage with stakeholders directly. Examples are surveys, interviews, or focus groups. A firm can also use secondary data sources collected from and about stakeholders to deduce the stakeholders’ views on materiality. With the increased availability of text analysis methods, the use of secondary data for materiality assessments is becoming more popular. Of the analyzed reports, 50.1% used secondary data externally created, such as media articles and publications by stakeholders themselves. In addition, in 30.9% of the reports, internal data from stakeholder meetings throughout the year (i.e., general dialogue) were re-used to determine materiality (Figure 2).

Overview of data sources mentioned in reports as used for materiality assessments.

As with any data collection, the reliability and validity of the method determine the quality of the data. The three sustainability characteristics complicate ensuring this reliability and validity. Data reliability concerns whether the data were consistently produced and analyzed. When multinational firms need to collect data across the world, the evaluative nature of sustainability causes tensions. When using one survey design or interview guide, the global managers struggled to manage the consistency of the implementation while being sensitive to geographical differences. First, they needed to establish a common vocabulary to ensure alignment in the interpretation of topics and concepts. Besides language barriers, cultural differences in stakeholder engagement practices also needed to be overcome. To stimulate consistency, sharing of assessment results and providing feedback motivated local collaboration.

For validity, the data need to capture what you are aiming to capture. In ensuring the validity of the materiality scores, each of the three sustainability characteristics creates tensions, but these tensions differ per materiality perspective. The complexity of sustainability issues complicates the validity of scores for both perspectives. From the business case perspective, the firm needs to know how the costs of negative impacts or revenues of positive impacts will be distributed among the actors to calculate risks and opportunities. The shared responsibility makes this division of risks and opportunities cloudy. Similarly, from the societal impact perspective, a firm needs to determine which impact is caused by its actions. In practice, that leads to confusion in how to take into account indirect impacts caused by shared responsibility. Should they be valued with the same importance as direct impacts? In addition, the interconnectedness of sustainability issues complicates the decision as to which ESG topic to attribute a risk/negative impact or opportunity/positive impact, making sure the impact is not counted twice.

The uncertainty of sustainability issues also affects the validity of scores of both perspectives. Unknown causes and effects of sustainability issues make accurately estimating the size and likelihood of an impact difficult. These estimations are already difficult for the business case perspective where the assessment period is set at either one, five, or ten years. From the societal impact perspective, however, the period over which the impact should be assessed is also unclear. The urgency of the topic was in several reports mentioned as a factor considered, but how this urgency was determined was not reported.

In addition, all estimations of future impacts are based on experiences in the past. This tension between past-present-future raises several issues in assigning scores. Two interviewees raised the issue of recency bias, which causes stakeholders to evaluate recent experiences as more important and more likely than events that happened further in the past. “If I look at my own survey behavior, when there are quantitative questions asked, I put something in the spirit of the moment” (Interview Case 16). Also, in secondary data analysis, the predictive ability of data of past events was questioned, with interviewees using the COVID-19 crisis as an example of the unpredictable dynamics of society. At the same time, the knowledge of stakeholders on recent events was indicated as beneficial for anticipating the future, especially in highly dynamic environments. To support these future outlooks, firms are seen to inform stakeholders on their strategy for the next years before surveying them:

[Information on] why we are asking these questions, how it would feed into the strategy, our reporting, et cetera, we sent all of this ahead of time so that the stakeholder could read and really understand. [In that way, we’re] making sure that we’re all on the same page and that they have the right context. (Interview Case 15)

The evaluative nature makes it difficult to establish a common denominator to compare the ESG topics. From the business case perspective, this denominator is the monetary impact of the topic on the firm’s financial performance. Although estimation methods for risks and opportunities are well-developed, the impact of ESG topics cannot always be monetized. When it comes to environmental damage, how much does the extinction of an animal species cost? 48 What if these costs are valued differently across the world and between generations?

From the societal impact perspective, there is no common denominator for impact, and there are no standardized methods that cover all business activities. Even if the impacts could be quantified, comparability is still an issue: “How can you really say that climate change is more important than human rights or workforce transformation? How can you [rank] them against each other?” (Interview Case 07). For example, if the impact of a firm on topic A affects 100,000 individuals and on topic B affects 1,000 hectares of tropical forest, which impact is more important? In response, firms use surveys in which they ask their stakeholders to rank or score a wide set of ESG topics, often using vague phrasing, such as “Please indicate which ESG topic is most important.” These unspecified questions confused the stakeholders, and their final answers were hard to compare due to multiple interpretations of the questions.

I got feedback that the questionnaire was very difficult to understand. Because they were quite odd questions, and it is a lot of gut feeling that you have to express. To express your gut feeling in numbers is for some people easy and for some less. When you have broad topics and broad questions, then it’s even more difficult to answer. (Interview Case 10)

To avoid multiple interpretations, several firms further specified their questions, asking about the impact of the topic on their stakeholders’ daily lives or their satisfaction with the firm’s attention to the topic. In other cases, separate economic, social, and environmental rankings were made. While these increased the validity and informativeness of the results, how to combine these specifications and separate rankings to compare the materiality across different ESG topics remained a question.

Selecting the Material Topics

After assigning the materiality scores, the insights need to be combined to rank and select the material ESG topics. A common graphic used to analyze and present the results is the “materiality matrix.” In total, 56.9% of the reports presented this matrix with each axis representing one of the three materiality perspectives. This matrix is used to provide a comprehensive overview of the materiality scores of ESG topics and to quickly show how the firm selected its material topics. Other ways of presenting the results were with tables or other figures, sometimes in combination with the matrix.

Although using the matrix for presenting their results, interviewees also criticized it as an oversimplified picture of reality, especially concerning the evaluative nature of ESG topics. First, in several reports, tensions between organizational and collective interests seemed to be “washed away.” In these matrices, topics were shown to have similar scores for both axes and were located on a diagonal line. This alignment was indicated as highly unlikely by several interviewees: not all collective or stakeholder interests can be translated to business risks or opportunities, and thus some discrepancy between the scores on both axes is expected.

Second, by grouping the stakeholders on one or two axes, the heterogeneity of stakeholder views is lost and the tensions between stakeholders are not visible.

When an aspect is in the middle of the vertical axis—material to stakeholders—does it mean that it’s of moderate materiality to all stakeholders or very high materiality for some and very low materiality for others? We see that as an issue. (Interview Case 03)

The matrix, thereby, does not present the conflicting demands that firms need to navigate when selecting their material topics. In recognizing this drawback, firms are seen to complement the matrix with a table or figure that displays the materiality scores per stakeholder group. Besides diversity between groups, the interviewees warned not to lose sight of the variety within stakeholder groups. A stakeholder group, such as investors, should not be treated as a homogeneous group, and firms should look beyond the average group scores. These within-group differences might be too detailed to be reported but can be insightful for decision making within the firm, according to multiple interviewees:

We differentiate stakeholders and regions. We have publicly [reported] the final [general] materiality matrix, but [internally] we have one for communities, one for clients, and one for suppliers. Then we can extract this information and set our strategy taking into consideration these outputs. (Interview Case 04)

Finally, firms are seen to use more than two criteria for selecting material topics, often dividing the two perspectives up in categories (e.g., impact on sales, growth, or reputation; urgency of impact; environmental or social impact) and displaying the outcomes of these criteria in tables besides the materiality matrix.

Third, although the materiality matrix presents the selection of material topics based on quantitative scores, the interviews indicated that the scores resulting from the assessment do not always fully determine the final selection. Often the initial scores are presented to senior management, and only then are the thresholds for materiality decided.

Our executive committee, they were given the opportunity to review it, and also see from their perspective things that they would like to have shifted. . . . There are normally one or two reasonably major changes. It’s especially around the topics that are close to the line. Should it be above or below the line? (Interview Case 02)

Although these changes are based on the extensive experience of senior management and their vision of the firm, they can be perceived as “cherry picking.” Besides showing their evaluative nature, the complexity and uncertainty of sustainability issues bias these final selections. Regarding the complexity of shared responsibility, the topics over which the firm has direct control were indicated to be prioritized over topics that require systemic change. Furthermore, these arbitrary selections are also sensitive to short-termism: choosing topics with short-term impacts as opposed to uncertain long-term impacts. To counteract these biases, interviewees indicated the following steps: set the materiality thresholds before data collection, present the results to senior management without leaving them open for discussion, and instead focus on the implications of the results for the firm’s report and activities.

Deciding the Materiality Cycle

As sustainability issues, as well as the context of firms, are dynamic, the materiality of ESG topics also changes over time. All interviewees indicated that a materiality assessment requires being repeated every so often, whether due to changes within the firm or its environment; 53.0% of the reports lack a timeframe for their materiality cycle. Other reports indicated a period between materiality assessments ranging from one year (23.5%), two to three years (20.2%), and more than three years (3.0%). The timeframe was, according to the interviewees, also determined by how firms use the materiality results. If the results are mainly used to determine report content, the firm is likely to repeat the assessment annually for each report. However, when firms connected the assessment to the development of a new (sustainability) strategy or the evaluation of an existing strategy, the timeframes were longer.

Repetition did not always mean that the full assessment was repeated. In the annual cycles, the firms often switched between an extensive assessment in one year to a smaller update in the next. Overall, maintaining consistency in methods across the years was perceived by firms to be challenging. The dynamic nature of sustainability issues led to new definitions of ESG topics, new connections between topics, and new stakeholders to be involved. In addition, reporting authorities are seen to change their standards for assessing materiality. Several interviewees indicated that they try to keep up with new developments by adjusting their methods and being responsive to new best practices.

On the contrary, a consistent method allows for collecting longitudinal data on materiality. Several interviewees indicated that they limit method adjustments so that their results can show changes in materiality over time instead of just providing a snapshot. Multiple departments are then likely to be consulted on how to interpret and use the materiality results. One interviewee explained how assessing materiality dynamically was valuable for more than just their reports:

We have an information system so [local divisions] can see in real-time this kind of information. You have a map that shows the number of stakeholder engagement activities in different countries. We use the system to share the best practices in different countries, and then we try to define the correct way to involve the stakeholder. (Interview Case 08)

Deciding how to measure materiality over the years, thus, shows to be a trade-off between responding to the latest developments in assessment methods and capturing dynamic materiality with a consistent method.

Conclusions and Discussion

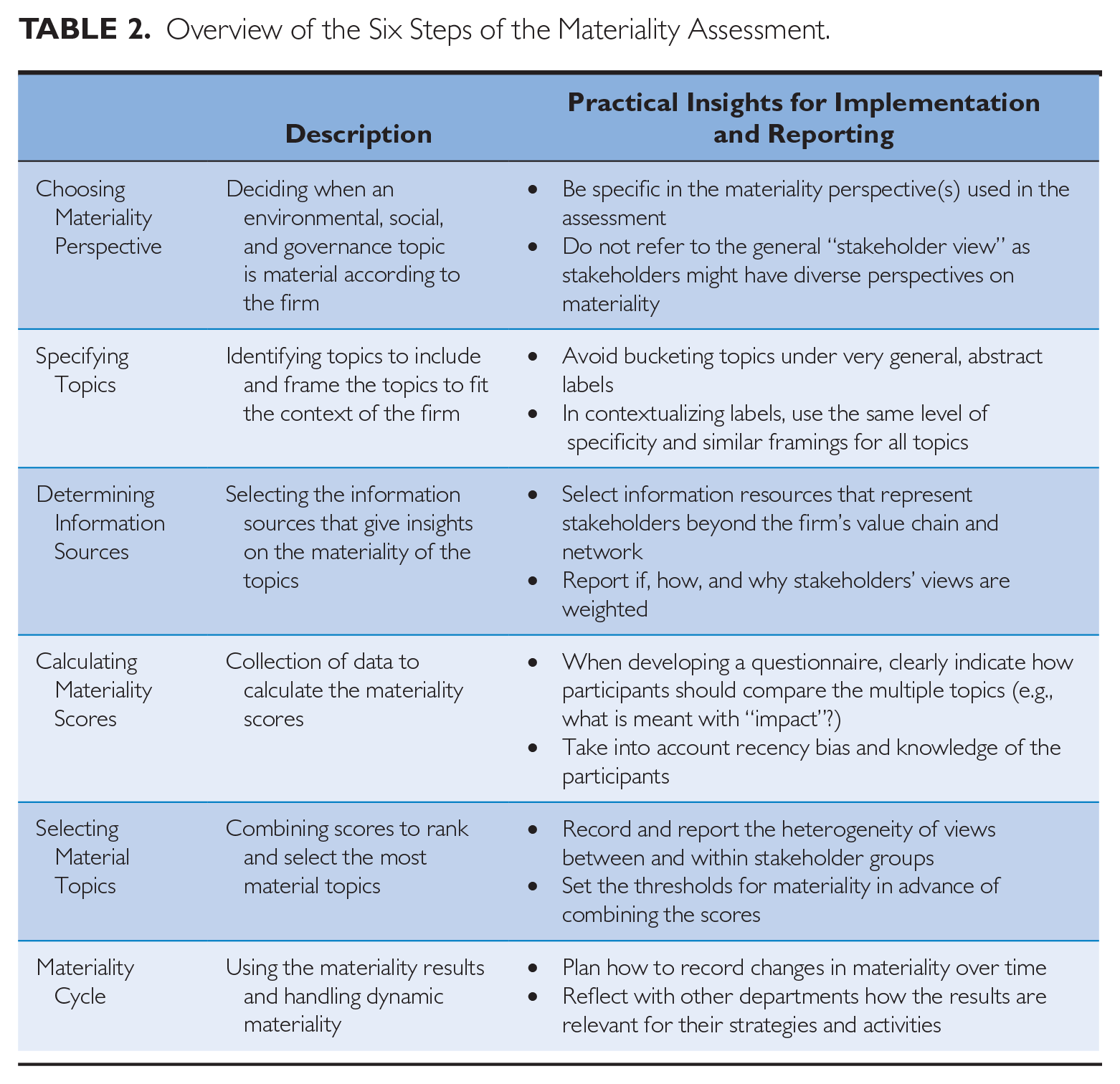

We have shown the main steps taken in materiality assessments and how the complexity, uncertainty, and evaluative nature of sustainability create tensions in conducting these steps. Table 2 provides an overview of the six steps and practical insights on how firms navigate these tensions.

Overview of the Six Steps of the Materiality Assessment.

Our investigation of the materiality practices leads to two conclusions. Our first conclusion is that the choice in materiality perspective between the business case and societal impact influences how all the other steps are conducted. The chosen perspective determines the identification and framing of topics, which sources and stakeholders are deemed informative, the way materiality is assigned to the topics (i.e., the impact on the firm vs. the impact of the firm), how the most material topics are selected, and how the dynamic nature of materiality is captured. The business case perspective has been the accepted view for at least five decades, 49 which was ample time to develop methods for materiality assessments from this point of view. The societal impact perspective represents the integrative view of the firm, which has only come to the forefront in the last decade. 50 Our investigation shows that methods for data collection and analysis for this perspective require further development. Since the new EU directive on non-financial reporting requires firms to take into account both perspectives (i.e., “double materiality”), this development has been speeding up. 51 At the same time, our analysis shows that these new methods raise new questions by firms, particularly concerning the complexity, uncertainty, and evaluative nature of sustainability issues.

Our second conclusion is that every firm experiences the tensions between the business case and societal impact perspectives. This leads to “tensioned topics,” which are material according to one perspective but not to the other. Since the psychological bias toward immediate gratification instead of long-term gains is inherent in consumers, capital providers, and managers alike, 52 firms will always experience pressure to take a business case perspective with a short-term focus. At the same time, societal actors will judge firms on their contribution to the long-term prosperity of society. Environmental and social goals are seen as having intrinsic value on their own and are not to be excluded or traded off, even if they do not contribute to the (short-term) profitability of the firm. 53 Thus, firms need the societal impact perspective to defend their social license to operate. 54

One way for firms to avoid the tensions between the business case perspective and societal impact perspective is to only focus on the “win-win” scenarios, that is, the sustainability challenges that serve both perspectives simultaneously. By doing so, many sustainability challenges may be left unattended. We, therefore, suggest aligning the materiality assessment with the paradox view on corporate sustainability. The paradox logic indicates that tensions between organizational goals should not be eliminated but explored. 55

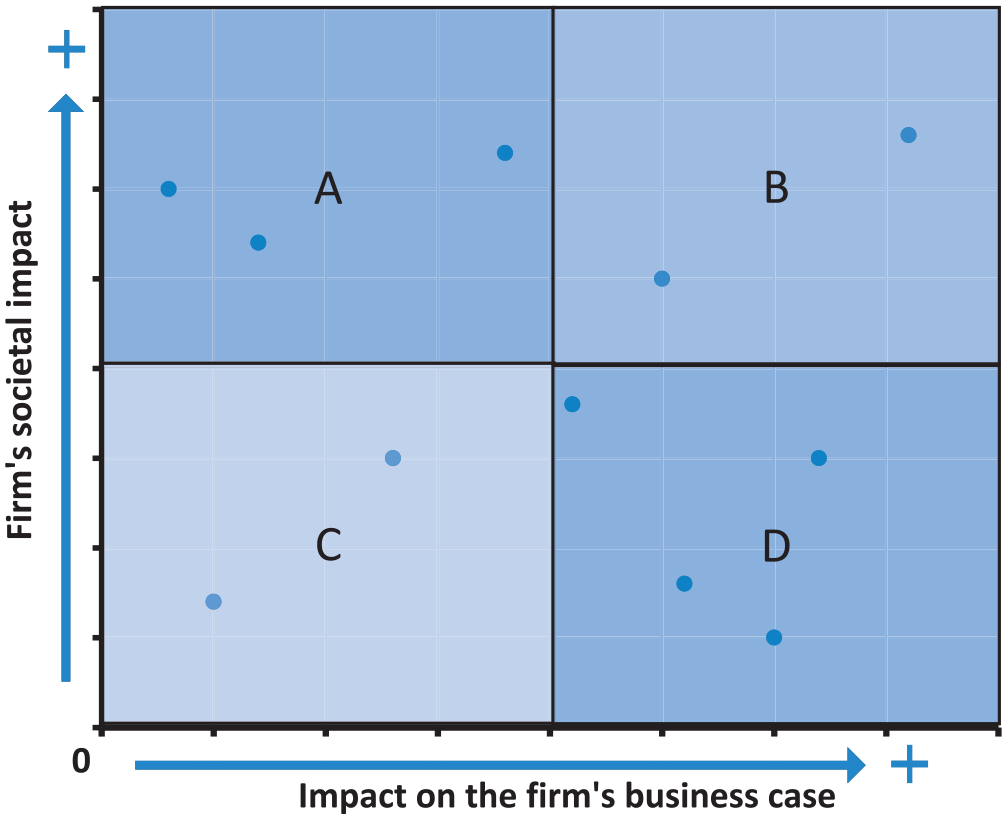

For the materiality assessment, this means that both perspectives on materiality are independently assessed and placed on the opposing axes of the materiality matrix. The matrix can then help identify tensioned topics. To illustrate, Figure 3 presents an example of such a matrix, divided into four quadrants. In quadrants B and C, the scores on both axes seem to align, meaning little tension exists between the business case and societal impact perspective. The topics in quadrant B are so-called “win-win” scenarios or “low-hanging fruits,” whereas quadrant C shows topics that require less attention according to both perspectives. For quadrants A and D, however, the scores of the axes do not agree, indicating tensions. The topics in quadrant A score high on the societal impact axis but low on the business case axis, meaning that investments in these topics are expected to improve societal impact but do not (directly) pay off for the firm. Quadrant D shows the opposite situation: these topics are seen as important for maintaining or increasing financial performance (in the short term) but represent only a small part of the firm’s societal impact.

A materiality matrix to illustrate how the business case and societal impact perspectives can be combined to show the complementarities and tensions.

With this new way of looking at the materiality matrix, we want to show that a materiality assessment can provide not just a list of ESG priorities but also insights into the tensions firms face in acting more sustainably. When a firm reports honestly about their struggles with these tensions in sustainability, this transparency could not just prevent accusations of selective disclosure, 56 but also open doors for internal and external dialogue about these struggles and innovative solutions. The materiality assessment can thus be a conversation starter, activating the sensemaking function of sustainability reporting, that is, walk the talk. 57

However, our overview of the six steps in materiality assessments and our re-positioning of the materiality matrix as presented here cannot answer all questions regarding materiality assessments. We identify three remaining points of discussion.

First, in collecting information about the firm’s performance and impact, one could ask whether the axes of the matrix do justice to the complexity of a firm’s reality. As one of our interviewees indicated, “One of the challenges of materiality is that you are trying to make things that are incredibly complex look very simple and neat. But the reality is incredibly messy” (Interview case 09). A first simplification is the combination of views into one unified average per stakeholder group, not showing any divergence within stakeholder groups. 58 Thereby, it neglects to show the “belonging paradox,” that is, tensions that arise when an individual’s values do not align with the value system of the organization or group they belong to. 59 These tensions are present both in external stakeholder groups as well as in the firm’s internal organization. While these tensions can undermine collective action, they are also seen as sources for innovation and institutional change needed for corporate sustainability. 60 Next, these averages are then aggregated into two axes, further reducing the diversity of viewpoints. 61 As we have seen in our cases, two criteria might not be enough to represent all materiality considerations of stakeholders. To explore tensions within and across stakeholder groups and prevent the loss of information, firms are seen to make separate analyses for stakeholder groups, dividing them per region, sector, or business activity. However, analyzing and disclosing all these intricacies might make the assessments and the reports very complex. Finding a balance between telling a clear and concise story and representing the complex reality remains a challenge.

Second, there are the ethical considerations in materiality selections. When looking at the main purpose of materiality assessments, one could ask whether there is a universal, “morally right” way of selecting ESG topics. Any selection leads to trading-off ESG topics and thus choosing some stakeholders’ demands over others. What the “morally right” trade-offs are depends on cultural beliefs and ideologies. 62 In our matrix, we oppose the financial performance of the firm to their societal impact, similar to the “double materiality” idea of the EU. These two axes reflect the dichotomy between individual corporate interests and collective prosperity, which scholars have previously attributed to European liberal thinking. 63 Other cultures might not agree with this dichotomy: some ideologies indicate that collective prosperity is only achieved through the pursuit of individual corporate interests, while others indicate that collective prosperity is the only goal worth pursuing. 64 Therefore, instead of prescribing which materiality perspectives firms should use, we want to draw attention to the ability of materiality assessments to identify the tensions that firms face: whether between corporate interests and collective prosperity; between short and long term; between economic, social, and environmental value creation; or between other perspectives on materiality. To provide a realistic image of their performance, firms should be transparent about these tensions, the beliefs underlying these tensions, and the trade-offs they make in response. However, how to respond to stakeholders that disagree with the firm’s beliefs and trade-offs remains unanswered.

Finally, one could ask the question of whether a well-informed and transparently disclosed materiality assessment prevents greenwashing. The short answer to that is: no, it does not. One of the main problems with greenwashing is the reporting of symbolic actions instead of substantive actions. 65 Although transparently disclosing a materiality assessment shows how the firm prioritizes ESG topics, the assessment does not dictate how a firm should act upon and report about the topics resulting as material. Standard setters need to indicate what kind of action is expected on material ESG topics and how firms should report on this action. Such standards are in development by organizations such as GRI but also with the new EU taxonomy for sustainability activities. In the meantime, firms can use their stakeholder engagement activities conducted for materiality assessments to also gain insights into what their stakeholders consider substantive action.

To conclude, some firms might see the materiality assessment as a tick-box exercise, copying the practices of peers or outsourcing it to a consultant, only to comply with reporting standards. However, when using materiality assessment to its full potential, it can provide deeper insights into tensions in their sustainability activities. When transparently communicated, such insights might not only prevent stakeholders from accusing the firm of greenwashing, but also allow for more honest and open conversations about the tensions firms face in setting priorities for substantive action on sustainable development.

Footnotes

Acknowledgements

The authors are very grateful to the editor and the anonymous reviewers for their comments in developing this article. We are indebted to Andy Beanland, Johanna Tähtinen, and the members of the World Business Council for Sustainable Development for their invaluable support and insights. We would also like to acknowledge the valuable feedback we received from participants of subtheme 21 of the 37th EGOS Colloquium, organized by Frank Wijen, Shon Hiatt, and Rodolphe Durand.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Author Biographies

Jilde Garst, PhD, is Researcher at the Accounting, Auditing & Control group of the Erasmus School of Economics (Rotterdam, The Netherlands) (email:

Karen Maas is Endowed Professor Accounting and Sustainability at the Open University and Academic Director of Impact Centre Erasmus (Rotterdam, The Netherlands) (email:

Jeroen Suijs is Chair of the Accounting, Auditing and Control group, and Director of the Business Economics Department of the Erasmus School of Economics (Rotterdam, The Netherlands) (email: