Abstract

Identity is at the core of a rich body of business communications research, spanning studies on organizational identity, branding, and corporate social responsibility. This work has, however, neglected the question of corporate identity from the perspective of co-operatives—democratically-controlled businesses owned and controlled by their users—and the existential challenge posed by an operating environment often hostile to the business model. At the same time, the question of identity permeates the scholarly organizational and co-operative literature, shaping studies into co-operative identity crises, isomorphism, and from a transactions-cost economics perspective, the co-operative lifecycle. Bridging these literatures, we develop a first-ever conceptual dictionary of terms that we associate with co-operative and investor-owned firms (IOFs). Using text-as-data techniques, we apply the dictionary to a 15-year sample of credit union (a type of co-operative) and bank (IOFs) annual report texts. The resulting model ranks credit unions and banks on a co-op versus IOF firm scale and identifies credit unions that may be at risk of losing their identity because of their use of IOF language. To validate our results, we employ a variety of strategies, including novel machine learning models. Generally, these strategies support the findings from our dictionary model but also suggest the model may not be picking up on some creeping isomorphic pressures on credit unions to conform to IOF language. We conclude by noting that identity questions have important real-world implications, noting potential legal and public policy implications (e.g., loss of preferential tax measures) and pointing to literature that associates co-operative “identity crises” with business failures and demutualizations which, in turn, can lead to higher consumer prices.

Introduction

Identity is at the core of a rich body of business communications research. Scholars have approached the question by investigating the shifting nature of organizational identity (OI) and how it influences the way organizations of different sizes “identify, approach, and resolve issues, as well as how they allocate resources” (Huang-Horowitz & Evans, 2020, p. 238). Others approach it from the perspective of brand identity and the important role it can play in firm reputation (Vernuccio, 2014). Still others have looked at the challenges of adapting corporate identities to changing social norms, particularly around corporate social responsibility (CSR; Chaudhri, 2016; Schmeltz, 2014; Vernuccio, 2014) and related expectations around environmental, social, and governance (ESG) objectives.

Business communications scholars, however, have not attended to the question of corporate identity from the perspective of the co-operative business model and the existential challenge posed by an economic and social environment that is oriented toward investor-owned firms (IOFs). The co-operative business form differs markedly from IOFs. The International Co-operative Alliance (ICA) defines a co-operative as “an autonomous association of persons united voluntarily to meet their common economic, social, and cultural needs and aspirations through a jointly owned and democratically-controlled enterprise” (ICA, n/a). To put this definition into practice, co-operatives adhere to seven principles: voluntary and open membership; democratic member control; autonomy and independence from government; education, training, and information for members; co-operation among co-operatives; and concern for community. The ICA definition and related principles also find expression in legislation, with particular emphasis usually given to the principle of democratic control and the idea that members are users of the co-operative’s good and services rather investors. As a result, and unlike IOFs, co-operatives are expected to focus on member service rather than profit maximization. Despite being less well known than IOFs, co-operatives play an important economic role globally. According to the ICA, three million co-operatives account for 10% of the world’s employed population and combined, the top 300 co-operatives have an annual turnover of just under US$2.2 trillion (ICA, 2022). Well-known examples include financial co-operatives such as Rabobank (Netherlands), Crédit Mutuel (France), and State Farm (United States), agricultural co-operatives such as Sunkist and Land O’Lakes (United States) and Fonterra (New Zealand), industrial co-operatives such as Mondragon (Spain), and retail co-operatives such as REI (United States) and the Co-operative Group (UK).

Building on a growing body of research that explores questions of co-operative identity, we ask whether the language used by co-operatives might be an early-warning indicator of a looming organizational “identity crisis,” a recurring idea in organizational and co-operative scholarship (Côté, 2009, 2013; Nelson et al., 2016; Rixon, 2013a). This question is premised on the idea that language shapes and filters interpretation and decision making and as such is a kind of organizational glue, a point stressed by Chaudhri (2016) in her discussion of how the “constitutive” view emphasizes the role language plays in making organizations possible.

To address this question, we develop the first-ever theory-informed conceptual dictionary of terms that we hypothesize are associated with co-operatively structured credit unions (a type of co-operative bank) and another parallel set of terms, that we hypothesize are associated with IOF structured banks. To assess the validity of our dictionary, we test our model on a sample of statements (the “corpus”) from Canadian credit union and bank board chairs and chief executive officers (CEOs). Drawing on text-as-data techniques from the disciplines of political science and computational linguistics, we apply a logit model to our corpus and rank credit unions and banks on a scale stretching from co-operatives at one end to IOFs at the other. If the model scores a credit union as an IOF, this may signal a loss of co-operative identity.

Co-operative identity matters because its loss has potential legal, public policy, and business consequences. For example, U.S. credit unions have long defended their tax exempt status against bank lobbies by appealing to their co-operative identity (National Association of Federally-Insured Credit Unions, 2023). From a business perspective, research suggests that a loss of co-operative identity is associated with business failure and demutualization (Couchman & Fulton, 2015; M. Fulton & Girard, 2015), outcomes that can lead to less competition, choice, and ultimately, negative impacts on consumer welfare.

The rest of our paper is structured as follows. Section 2 sets out the theoretical considerations that informed our research question. Section 3 discusses the conceptual dictionary. Section 4 sets out our data sample. Sample 5 discusses our methodology and the model we applied to the data. Section 6 discusses our results and applies several validation tests. Section 7 concludes, discusses limitations, and reflects on next steps.

Literature Review: Communicating Co-Operatives and Isomorphism

While largely neglected in the management literature, questions around co-operative identity permeate the work of organizational and co-operative scholars. In his study on the emergence of the seven co-operative principles, Fairbairn (1994) for example discusses the difficult conversations on co-operative identity that helped define, refine, and modernize the seven co-operative principles. Côté (2009, 2013) has proposed a “new co-operative paradigm” to address what he calls a co-operative identity “crisis” born of pressures on co-operatives to adopt business practices more proper to investor-owned firms (IOFs). Drawing on DiMaggio and Powell’s (1983) concept of isomorphism, others have used a mix of qualitative (e.g., interviews with practitioners) and quantitative data (e.g., surveys; financial data) to document how co-operatives come under coercive, mimetic, and normative pressure to conform to IOF business and governance practices (Bager, 1994; Bretos et al., 2020; Groeneveld, 2020; Michaud, 2022; Miner & Novkovic, 2020). Drawing on interviews, Rixon (2013a) for example says that some credit unions are experiencing an identity crisis because their leaders have low awareness of the co-operative principles and do little to monitor or report on how their activities link to the principles. Similarly, Kleanthous et al. (2019) finds that credit union members and employees have only a weak understanding and commitment to the co-operative principles.

Scholars have also looked at the identity crisis issue from the perspective of co-operative business failures and conversions or demutualization into IOFs. Couchman and Fulton (2015) argue that an absence of management and board-level understanding of the co-operative model is associated with co-operative failures and demutualizations. Drawing on a transaction cost economics framework, Cook (2018) and Hansmann (2000) argue that governance costs associated with increasing member heterogeneity create pressures on co-operatives to fail or convert into IOFs, with Cook arguing that co-operative invariably face some kind of “recognition and introspection” moment in their “lifecycle.” Others, however, say there is nothing pre-ordained about co-operative identity crises and associated failures or conversions, arguing instead that governance and organizational culture, plus understanding of the co-operative model, are determining factors (Couchman & Fulton, 2015; M. Fulton & Girard, 2015; Gertler, 2001; Novkovic, 2006; Novkovic & Powers, 2005; Pigeon, 2020). There is widespread recognition, however, that co-operatives struggle to operationalize and measure co-operative values, principles, or the “co-operative difference” (Birchall, 1997, 2005; Birchall & Simmons, 2004; Brown & Hicks, 2007; Philp, 2004; Spear, 2004). Building on these findings, scholars have worked with practitioners to devise co-operative accounting standards and performance metrics that could help management and boards know whether the business is aligned with co-operative principles and values or whether it is morphing into an IOF (CEARC, 2022; Rixon, 2013a, 2013b).

The failure or conversion of co-operatives can have significant societal consequences. The demutualization of eight UK Building Societies (a type of co-operative) representing two thirds of the sector’s assets in the late 1980s and early 1990s has been associated with higher prices on loans and lower prices on deposits (Heffernan, 2005). The demutualization of a number of U.S. savings and loans mutuals in the 1980s has been associated with increased risk taking and failure relative to S&Ls that retained their mutual form (Chaddad & Cook, 2004; Fonteyne, 2007; Hansmann, 2000), although other studies paint a more mixed picture (see Heffernan, 2005, for a discussion). More generally, to the extent that co-operatives address market gaps (Hansmann, 2000), a failure or conversion can have negative effects on consumer welfare. The identity question also plays out in law and public policy, including around access to tax measures (see above) but also around language use. In 2017, Canada’s bank regulator took steps to enforce financial and criminal penalties of up to five years in prison against credit union use of the terms “bank” and “banking,” both reserved for banks, relenting only in the face of a counter-lobby (see Nicholls, 2019 for a discussion). Co-operative legislation also, typically, reserves the descriptors “co-operative,” “credit union,” and “mutual” to entities that operate on a co-operative basis in a way consistent with the co-operative identity.

Despite a significant literature on co-operative failures and conversions and the associated literature on co-operative identity crises, very little of the scholarship has addressed the question of co-operative identify from the perspective of language use. Some have, however, documented the decline of co-operative discourse in modern introductory economics textbooks (Hill, 2002; Kalmi, 2006) and how enterprise discourse has gradually displaced more traditional community service discourse among volunteers in Irish credit unions in the early 2000s (Mangan, 2009). Nelson et al. (2016) conclude, based on a review of the organizational and isomorphism literature, that co-operatives need to creatively straddle a line between remaining distinctive but also relatable in a world where the co-operative form is less understood than IOFs. Fairbairn (2006), for his part, suggests that while people may have an intuitive understanding of the benefits of co-operatives, few have the vocabulary to describe the differences between co-operatives and IOFs.

Developing a Conceptual Dictionary

The use of conceptual dictionaries rests on the notion that text is a form of data. This idea has long informed scientific content analysis (Neuendorf, 2017). Political scientists have been particularly active in this space, employing text-as-data methods for agenda setting research (e.g., Soroka, 2002) but also applying new computational and conceptual tools that reduce the need for human coding. Maerz and Schneider (2020) for example use a theoretically-motivated dictionary of political ideology to analyze thousands of political speeches, drawing inferences about the degree to which well-known political leaders can be characterized along a liberal-illiberal scale. Others have used similar methods to re-estimate and validate human-based coding of political documents for their evolving positions on an ideological (Left vs. Right) or policy issue scales (Lowe et al., 2011). More generally, this text-as-data approach underpins the science of information retrieval and relatedly, popular internet search engines (Manning et al., 2008) and modern artificial intelligence (AI) tools.

As Neuendorf (2017, p. 149) cautions in her popular guide to empirical content analysis, the development of a conceptual dictionary is “typically a long, iterative, and painstaking process.” Our work is no different. We undertook iterative steps to develop and validate our dictionary, beginning with a theoretical presupposition common to all dictionary approaches, namely the idea of “semantic differentials” (Neuendorf, 2017, p. 98). It says that language use is associated with, and reveals something important, about the underlying structures that give rise to communications output. Different structures imply different language use.

It is instructive, therefore, to briefly contrast credit unions and banks. Credit unions are small—the largest Canadian credit union, Vancity, is only three-quarters the size of the smallest bank. Credit unions are local—all but three of Canada’s credit unions are incorporated and regulated provincially, often to local standards; banks are regulated federally, according to international standards, and operate nationally and internationally. Credit unions disproportionately cater to small businesses and agriculture—they have an 11% market share in each, well out of proportion to their overall 7% share of banking-sector assets (Canadian Credit Union Association, 2021).

With these considerations in mind, we assumed (CU1) credit unions tend to use language consistent with their form by appealing to members as users and owners through use of words like “member” and pronouns like “us” and “we.” We also expected credit unions to emphasize their purpose and encourage dialogue with members. Second (CU2), given their local rather than pan-Canadian focus, we expected credit unions to make greater use of terms related to community, regions and their province of incorporation. Third (CU3), we expected credit unions to refer to core co-operatives principles, values, and ethical norms such as democratic governance. Fourth (CU4), and finally, we expected credit unions to refer to themselves as “credit unions” and the French equivalent, “caisses.”

For banks, we (B1) assumed they direct their communications to investors around themes related to profit maximization such as “return on equity.” Second (B2), we expected banks to use language neutral to geography, with a pan-Canadian or international perspective. Third (B3), we expected banks to make less use of “us” and “we” and downplaying references to mission, vision, and purpose. Fourth (B4), given the weight of Canada’s federal regulation, we expected banks to include references to capital standards but diversity targets set by the federal government. Fifth (B5), we expected banks to make liberal use of the word “bank,” a brand of considerable value in Canada given a history of bank stability.

Based on these assumptions, we crafted our dictionary and selected, wherever possible, words that were oppositional (e.g., member vs. customer). We then distributed a precis of our research and a draft of the dictionary to 111 individuals consisting of 96 practitioners and 15 specialized academics. We asked respondents to indicate, in Survey Monkey, whether they associated each term in our dictionary with co-operatives, IOFs, both, or neither. We then asked respondents to suggest terms that might be missing from our dictionary. In all, 29 people—or 26% of invitees—completed the survey, of which 4 (19%) were scholars and the remaining 25 (81%) practitioners.

We refined our survey using a combination of judgment and general rules. We kept, for example, terms where 60% or more of respondents indicated that a word was strongly associated with co-operatives. These included terms like “member,” and “democracy.” Where a term generated less than 60% support, we exercised discretion drawing on co-operative principles and values, retaining terms like “education,” “ethics,” and “values.” For investor-owned firms, we set the cutoff point lower, at 40%, in recognition that it is challenging to identify terms strongly and uniquely associated with IOFs and banks given their ubiquity. Again, we included a selection of terms that fell below this threshold but aligned with our assumptions, most notably geographic terms (CU2, B2) like “Canada” or “national.” We also added terms suggested by respondents like “surplus” and “co-operative” that in hindsight, were obvious candidates for inclusion in our dictionary. For IOF/banks, respondents suggested two terms—clients and stocks—that we added to our dictionary. Finally, we added a handful of terms that, while not part of the survey, emerged as we reflected on the survey results, reviewed textual samples, and deepened our thinking. For example, we added the names of the 10 Canadian provinces because credit unions operate inside these jurisdictional boundaries. We also added value-laden words like “equality,” “openness,” and “mutual assistance” to the co-operative category. For the IOF category, we added seemingly obvious terms (again, in hindsight) like “market.”

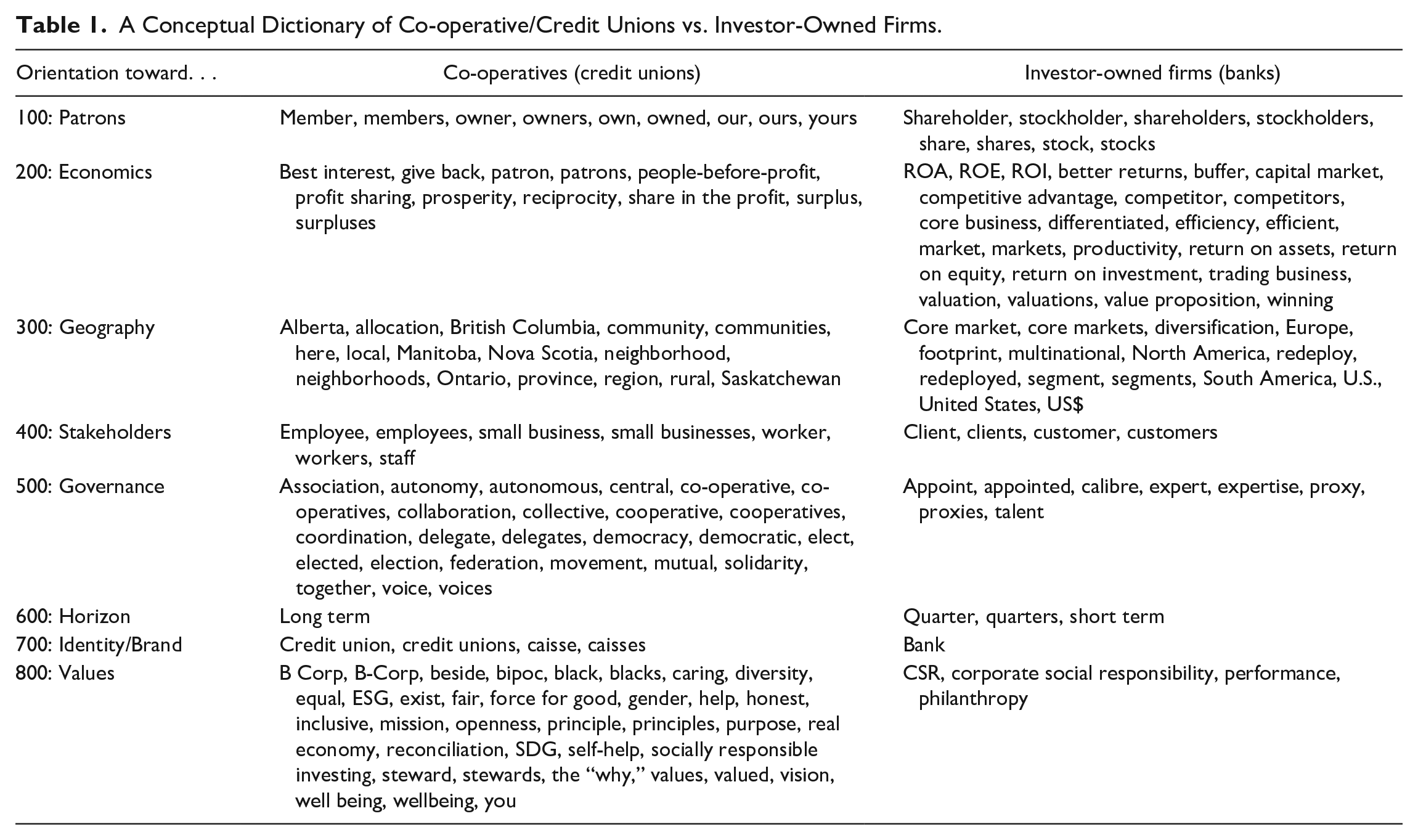

As our research and reflection process unfolded, we refined the theoretical foundation of our dictionary by organizing the terms into eight sub-categories, each representing the way in which credit unions are expected—by law and inspired by the co-operative principles and values—to orient themselves relative to banks. Table 1 depicts these eight sub-categories, each distinguished by an arbitrary index value. In all, our final dictionary consisted of 176 keywords, of which 109 are associated with credit unions. Based on our key-word-in-context analysis, described below, we chose not to stem keywords but instead included variations of importance (e.g., co-operative and co-operatives).

A Conceptual Dictionary of Co-operative/Credit Unions vs. Investor-Owned Firms.

Data Sample and Descriptive Statistics

While our over-arching interest is around issues of organizational identity from a co-operative perspective, we focused more narrowly on credit unions versus banks for three reasons. First, like many financial co-operatives (Ferri & Pesce, 2012), credit unions are often pressured by regulators to adopt prudential standards designed for internationally-active banks, introducing a degree of coercive isomorphic pressures. Second, credit unions increasingly recruit former bankers to work in, and in many cases, lead their organizations. Relatedly, they often recruit staff who have pursued conventional accounting or business degrees, usually without any instruction on the distinct nature of co-operatives. Both factors increase the risk of mimetic and normative isomorphic pressures and a co-operative identity crisis. Third, and finally, credit unions face considerable pressure to conform to conventional banking practices simply because Canada’s banking sector is dominated by banks.

For our unit of analysis, we focused on credit union and bank chair and CEO statements from annual reports because content analysis tends “to work better when the text is focused” (Grimmer & Stewart, 2013, p. 272; Neuendorf, 2017). We hypothesize that we can learn about what management and the board think is important to their patrons by analyzing these targeted statements using our dictionary model. While we recognize that chair and CEO annual report statements are often written by staff, particularly in banks, it is also true that they reflect direction from the chair, CEO, and the organization’s strategic plan.

To build our sample, we collected annual reports on the 50 largest Canadian credit unions, by year, from 2005 to 2020. Membership in the “top 50” credit unions varied slightly over this period and we ended up with 53 different credit unions that together, accounted for 86 % of 2021 credit union assets. We collected identical data on Canada’s 10 retail banks that together, account for nearly 100 % of bank assets. We obtained a complete set of bank annual reports but had uneven access to credit union reports. We pursued three strategies to address this gap, including: (a) searching for missing reports archived by Internet Archive’s WayBack Machine; (b) purchasing a set of annual reports from a consultant who collects and analyzes credit union financial data; and (c) phoning and emailing credit unions to request missing copies. While these efforts did not produce a full set of annual reports, our analysis focused on an aggregate assessment of content by entity rather than year-over-year analysis.

We next developed code to extract the board chair and CEO statements and convert these into a text file suitable for computational analysis. While in most cases, the statements were in separate reports, several credit unions provided an integrated report signed by the chair and CEO. In all, we collected 2220 chair, CEO, and joint statements. To avoid complications, we combined the chair and CEO statements into a single document for all available annual reports, leaving 764 units of analysis. On average, credit union chair/CEO statements are a little more than half the size of their bank equivalents—1,240 tokens versus 2,389 at the banks (tokens are defined as alphanumeric strings separated by white space). We suspect this disparity is related to different target audience. Bank executives and boards speak to four distinct audiences, shareholders, creditors, regulators, and federal policymakers; credit unions by contrast communicate primarily with members. Based on other (not shown) statistical analysis, we find that relatively speaking, credit unions talk more about members and membership, member service, staff, communities, local, services, assets, online offerings, and patronage. Banks talk relatively more about clients and customers, shareholders, Canada, strategy, markets, their global footprint, executives, and performance.

Methodology and Modeling

Methodologically, our approach follows a “bag of words” strategy in that we infer meaning by considering the relative presence of words across a sample of documents grouped by organization but with no importance given to the order or location in which words appear (Lucas et al., 2015). Unlike “bag of words” methodologies however, we pre-select the meaningful words based on theoretical considerations, namely that organization form shapes language use and thus the relative frequency of our dictionary terms.

While content analysis scholarship often calculates indices or scales based on summing and comparing the occurrences of words or phrases as a ratio of total words or sentences in a document, we apply a log-scale probit model to avoid the pitfalls associated with these “normalization” approaches, including giving insufficient weight to extreme positions and bounding positions on a restricted scale (Lowe et al., 2011). Following Lowe et al. (2011) and Maerz and Schneider (2020), we define ϴl as a log scale that measures intervals not ratio level measurements (i.e., “0” has no special meaning) and as such, allows for measuring relative position on a co-operative/IOF scale. Rather than a (L)eft versus (R)ight) or Liberal versus Illiberal political scale in the political science literature, we are interested in a co-operative (=CO-OP) versus investor-owned (=IOF) scale:

This distribution is approximately normal where C + IOF ≥ 10. We can calculate the

To arrive at confidence intervals that allow us to account for uncertainty around our estimates and measurement errors, we use the following measure of variance (σ2) and related standard errors. Again, we follow Lowe et al.’s formulation but with variables substituted as appropriate:

The resulting confidence interval is as follows:

Results and Validity Checks

Results

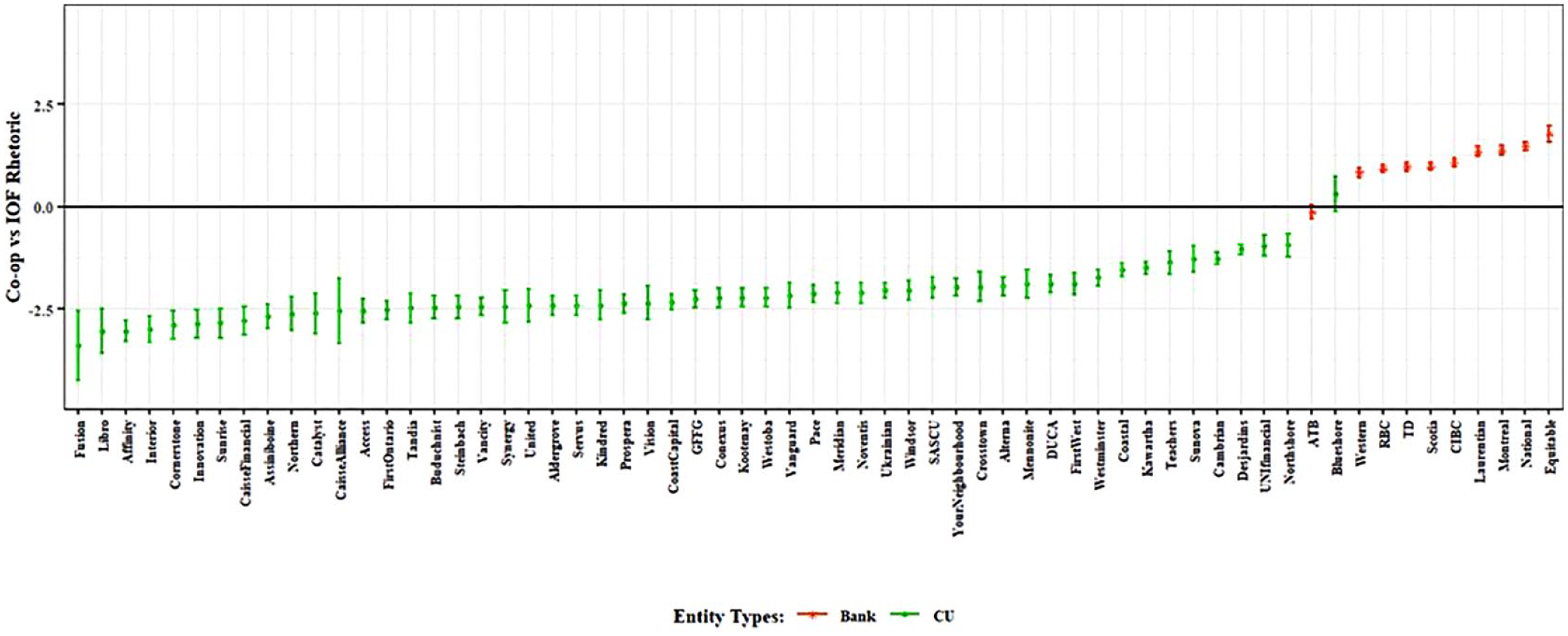

Figure 1 depicts the results of applying this model to our sample. It ranks our sample of 53 credit unions and 10 bricks-and-mortar retail banks in terms of our CO-OP–IOF scale. The model categorizes 52 credit unions as co-operatives and 9 of the banks as IOFs. There is no clear categorization for two entities, ATB and BlueShore credit union. In the next sections, we consider the robustness of our findings.

Scaling credit unions and banks on a CO-OP/IOF scale.

Criterion Validity

To assess the validity of our model and conceptual dictionary, we consider whether the resulting categorizations align with each entity’s formal incorporation status. In other words, does our model categorize, as we might expect, entities that are legally incorporated as credit unions into “co-operatives” and entities legally incorporated as banks into “IOFs”? If the categorizations do not align with the underlying corporate form, can we reasonably explain these discrepancies or are they misclassified? This last question is of particular importance given our research question, namely can we develop a conceptual dictionary that when applied to a corpus of texts, provides an early warning about possible loss of co-operative identity and, ultimately, failure, or demutualization?

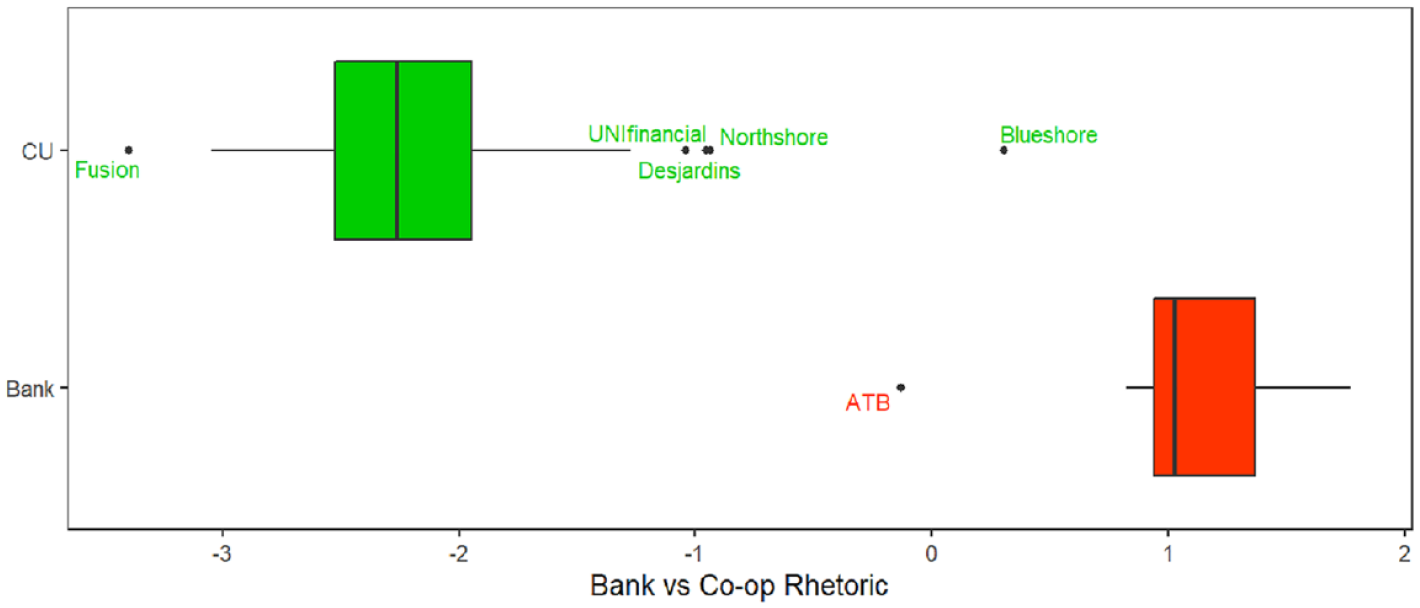

As noted, Figure 1 categorizes all but two entities in a way that aligns with their formal incorporation: below the line, we see only one bank entity—ATB financial—and above the line we see only one credit union entity (BlueShore). Again, however, the associated confidence intervals do not allow us to conclude that either is associated with one category or another. We can however obtain a richer understanding of the performance of our model and dictionary results by considering the box plot in Figure 2, which aggregates the results for credit unions and banks. The black line depicts the median score of each entity type, while the outer edges represent the interquartile range (i.e., from 25th to 75th percentiles). The whiskers are depicted by the lines extending beyond the rectangles and reflect model scores that are 1.5 times the 25th and 75th percentile values. Finally, dots outside the whiskers identify outliers. Figure 2 shows that all but one credit union (in green)—BlueShore—is to the left of the line separating co-operatives from investor-owned firms and all but one bank (in red)—ATB—is to the right of the same line. Figure 2 also identifies four other outliers, namely Fusion credit union, which has a very high “co-operative” score, and Uni Financial, Desjardins, and Northshore, which do not. We discuss these outliers in turn, beginning with BlueShore and ATB.

Criterion validity of CO-OP/IOF dictionary.

BlueShore is a $4.8 billion (in assets as of 2020) credit union based in British Columbia. It originated as “NorthShore” credit union because its founding members were dock workers in what was, at the time, a working-class part of Vancouver. In 2013, it changed its name to BlueShore to reflect the north shore of Vancouver’s increasingly gentrified and upper-income population. Today, BlueShore is known for branches that double as spas and its focus on high net-worth members. To illustrate the way its language deviates from what we theorize as co-operative, consider the following extracts from a joint statement by its chair and CEO in the 2020 annual report (emphasis added): 2020 was a year of unique challenges. It demanded that BlueShore Financial demonstrate agility and resiliency in the face of change; and that we find new ways to connect with and serve

This extract shows that BlueShore refers to members as “clients” and describes itself as a “financial partner” rather than a credit union. It does not discuss commitment to community, investment in local projects, its co-operative nature, the democratic process, patronage, surplus, or its credit union identity. By contrast, consider the following extracts from the 2020 annual report of Fusion, a $1.2 billion credit union in Manitoba. Its chair and CEO statements touch on core co-operative themes such as community, empathy, connection, and the credit union identity as exemplified from the following extract from the CEO statement:

Our

Consider next ATB Financial, a $56 billion entity owned by the province of Alberta. It is the only retail-facing public bank in Canada. Its annual reports draw on themes such as communities and “impact” normally associated with credit unions, as show in the following extract from the annual report statement by its CEO (emphasis added).

Because we also knew our

Finally, the box plot suggests that Desjardins and Uni Financial are edging close to the line separating co-operatives from IOFs. Again, these findings are plausible. Uni Financial, with $4.8 billion in assets and based in New Brunswick, became Canada’s first federal credit union in 2016. As such, it is regulated under the same legislation, and in the same way, as the 10 banks in our sample, suggesting that our model may be picking up some coercive isomorphic pressures. Similarly, Desjardins, a $245 billion financial co-operative based in Quebec, is regulated almost identically to the federal banks and has often been the target of criticism that it has lost its co-operative identity (Posca, 2019).

Qualitative Coding

Despite these promising findings, there is widespread recognition that expert human coding is the benchmark against which to assess dictionary, supervised, and unsupervised machine learning approaches. Nevertheless, we chose to leave that work to a future iteration of our research for three reasons. First, comparatively speaking, our study is less complex than equivalent political science scholarship. We explore co-operatives and IOFs language using only eight, relatively simple, orientations, or dimensions; most comparable analysis considers many more dimensions. Second, while political speech is rich with euphemisms, “dog whistles,” and other markers of ideological disposition, this is far less true in annual report statements which target a (relatively) narrow audience (i.e., investors or members). Third, and finally, human-coding is laborious, time consuming, and costly, all considerations that pushed beyond the near-term objectives in this research.

Nevertheless, we applied three different “expert lenses” in our work. First, we surveyed, as described earlier, fellow experts to develop our dictionary. Second, we developed a draft “coding book” that helped deepen our understanding of the eight orientations. We plan to deploy this tool in a future iteration of the work. Finally, we applied our expert-based assessment of the dictionary’s relevance by producing a “keyword in context (KWIC)” report that we independently assessed. In a KWIC analysis, the user specifies a set number of words (10 in our case) that precede and follow each dictionary term. Using an early version of the dictionary, our KWIC report generated nearly 10,000 entries. Based on a comparative analysis of our respective findings, we refined our dictionary, removing terms that we initially hypothesized might be associated with credit unions or IOFs but turned out to have unclear associations. For example, we removed the term “main street” because the KWIC analysis revealed that it is used to identify branches located on streets by that name rather than as a differentiator from banks, most of which are headquartered in downtown Toronto on “Bay Street.” Similarly, we posited that credit unions made greater use of the term “enough” to contrast with banks, which in theory at least, are in the business of pursuing limitless profits. KWIC analysis revealed the term is used abundantly in credit union annual reports but almost never to infer that there should limits on the pursuit of profit.

Latent Topics

We can also assess the validity of our dictionary approach by comparing the resulting classifications with topics generated by an unsupervised machine learning model using a probabilistic topic-modeling package in R called STM. This machine-learning tool identifies a series of latent topics defined as multinomial distributions over words. Each topic represents words that the model identifies as co-occurring across the corpus documents. Each document is assumed to represent a mixture of topics, with a data generation process that assigns words to a document according to the distribution of topics. The researcher’s task is to assign labels to the resulting topics. As of this writing, there is no one universally accepted method of setting the number of topics, designed as “K” in the literature (Grimmer & Stewart, 2013; Maerz & Schneider, 2020; Roberts et al., 2014). As a result, researchers must specify in advance the number of topics, run the model, and rely on a qualitative assessment of the substantive value or usefulness of the resulting topics (Grimmer & Stewart, 2013; Roberts et al., 2014).

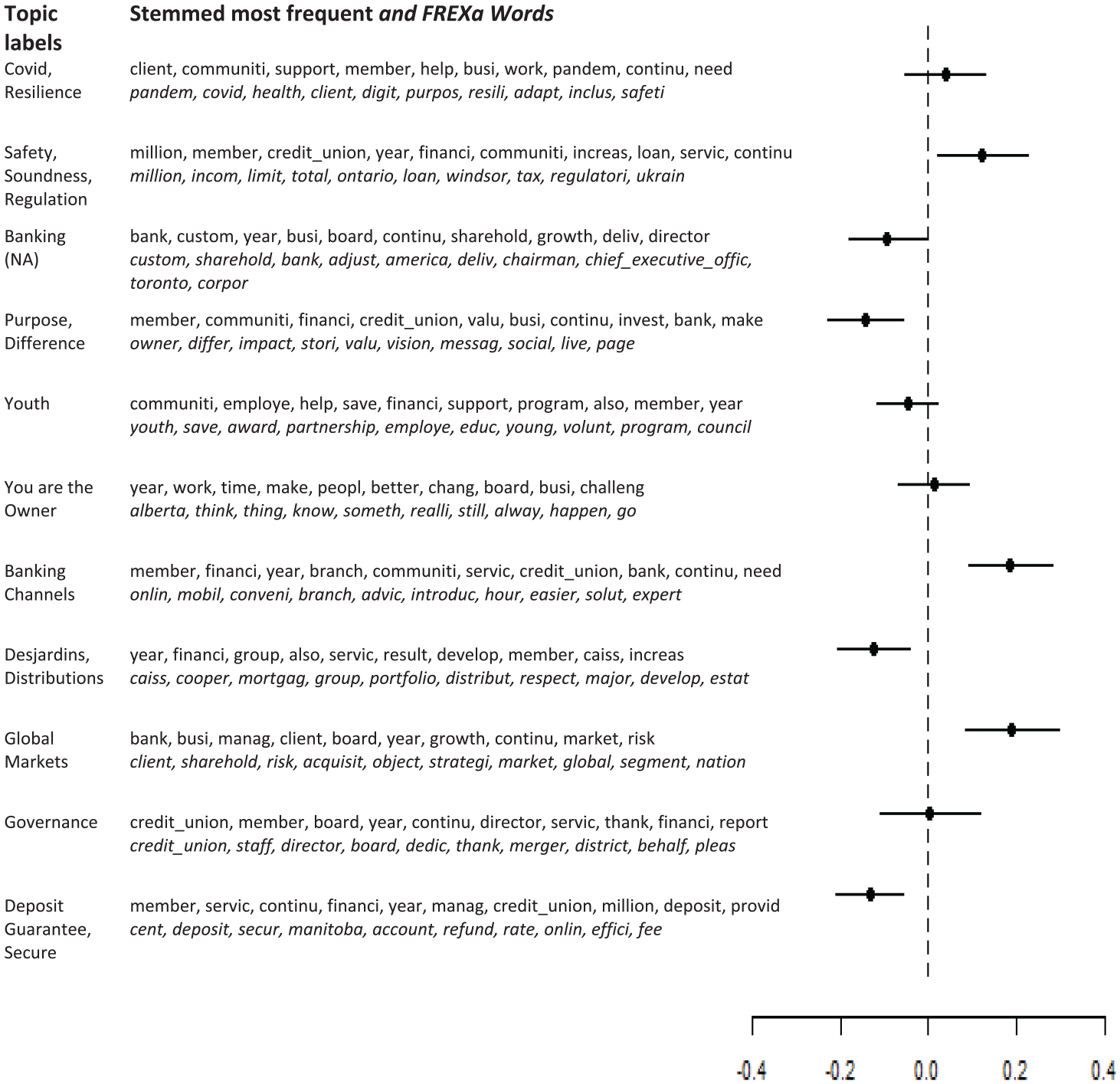

We tested several iterations of K ranging from 3 to 20 to identify the appropriate number of topics. We used STM tools to inform the labelling of these topics, including lists of words with the highest probability of being associated with a given topic, words that are most frequent and most exclusive to that topic, and words that are given more weight given their infrequent association with other topics (Roberts et al., 2019). We also reviewed texts that the STM package identified as most representative of a topic to validate the labelling. Finally, we used the network analysis to understand how sub-categories in larger K specifications might “emerge” from categories in smaller K specifications. After careful consideration of specifications of K = 7, 9, 11, and 13 topics, we settled on K = 11.

We next looked at the association between the 11 topics and our dictionary categorizations. The results were mixed. Figure 3 shows there is no statistically significant correlation between four of the topics—COVID and Resilience, Governance, You are the Owner, and Youth—and our IOF or co-op categories. COVID was a universal phenomenon, affecting banks and credit unions alike. “Governance” is another cross-cutting issue. Through the findtexts function in STM, we see that the concept of ownership embodied in the label “You are the Owner” is strongly associated with ATB, one of the model outliers discussed earlier, and a credit union called Your Neighborhood Credit Union. The “Youth” theme is more difficult to explain. We expect it to cleave more neatly to the credit union category given the sector’s long-standing efforts to attract young people but it does so only mildly.

Topics, keywords, and correlation to Co-op/IOF categories for 11 topic model.

Other topics however align, in a statistically significant way, with our categories. The topics of “Safety, Soundness, Regulation,” “Banking Channels,” and Global Markets” align with entities that our model classifies as IOFs. This is a plausible finding given that Canadian banks are IOFs with global ambitions and the ability to deliver services across a variety of banking channels. The model also plausibly associates the topics of “Banking (NA),” “Purpose and Difference,” “Desjardins and Distributions,” and “Deposit Guarantee” to the co-operative category. Co-operatives in general should tend to emphasize their purpose and difference from other entities. Desjardins is a large financial co-operative that emphasizes its (patronage) returns to members, while “Deposit Guarantee, Secure” is a theme that credit unions in the four western provinces, but especially Manitoba, emphasize given the availability of unlimited deposit insurance in those jurisdictions.

The “Banking (NA)” is more difficult to explain since the top keywords associated with this topic are intuitively associated with banks as IOFs, namely customers, shareholders, and America (NA = “North America”). The “Findtexts” function does not clarify matters, invariably returning bank chair and CEO statements that elaborate on these IOF-focused themes despite the topic’s correlation with co-operatives. We reconcile this association by noting that the term “bank” and derivatives are used, as noted earlier, by credit unions to describe their services (e.g., “online banking”). Moreover, the credit unions associated with this topic operate in southern Ontario, which is proximate to Canada’s large automotive sector and the U.S. border. As a result, these credit unions may be discussing North American market conditions in their annual reports. Nevertheless, the strong association between the topic “Banking (NA)” and credit unions does suggest some creeping, generalized, mimetic, and normative isomorphism that our dictionary model does not reveal.

Conclusion, Limitations, and Future Research

Identity permeates much of modern academic research and debates, whether related to gender, race, class, ethnicity, or in the management literature, corporate identity. Invariably, these debates implicate the use of language, whether it be gender-neutral pronouns, language appropriation, or introducing new language to capture evolving understandings of identity. In short, language is a cite of struggle, a “place” where views of the world and orientations are most visible and contested. Thus, the premise of this research is that language matters. It is both organizational glue and a frame that filters information and helps organizations make sense of the world, shape decisions, and communicate about what they do and who they are.

This leads to our research question, namely are co-operatives using language consistent with their organizational structure and if not, is this a possible indicator of a looming identity crisis? To answer that question, we developed a novel dictionary of terms we hypothesize are associated with co-operatives and IOFs, organized, respectively, in terms of eight orientations. We tested a draft of the dictionary with practitioners and scholars and then refined and tested it and the related model by applying it to a 15-year sample of credit union and bank chair/CEO statements. This generated a ranking scheme that we validated with several strategies, finding that notwithstanding a handful of notable exceptions, there does not appear to be a broad-based identity crisis amongst credit unions at least judging by their language use. For the time being, credit unions appear to be drawing on language that resonates with co-operative principles and values.

Limitations

There are important limitations to this study. There is scope to refine and improve our dictionary and we invite scrutiny and replication of our findings. While chair/CEO statements represent a narrow and constant unit of analysis across time and space, annual reports, as a form, impose restrictions on the range of topics. Finally, there are potential challenges associated with our data sample. Collecting and working with annual report statements is difficult and time consuming. In extracting chair/CEO statements, we had to engage in the challenging process of converting some statements from image files into text. In others, we had to manually extract the text because our code could not sort out alternating languages (e.g., English and Ukrainian). In still other cases, we had to transcribe, manually, video statements. Despite our best efforts, there is a risk that residual, unusual, text coding may have influenced our findings.

Implications and Future Areas of Study

We believe our research has important policy, practitioner, and scholarly implications. For policymakers, our research method could inform efforts to enforce organizational boundaries around issues such as taxation or the “bank” and “banking” terminology conflict between Canada’s federal regulator and provincial credit unions discussed earlier. For practitioners, our findings suggest co-operatives may need to pay more deliberate attention to language use as a means of maintaining identity—and market position—relative to IOFs. Finally, for scholars, our findings should inform academic research into organizational identity in general—we can imagine extension into non-profit research for example—but in particular, research into the association between co-operative identity crises and co-operative failures or demutualizations, outcomes that can, as discussed, engender negative societal consequences. Building on our work, we could also imagine correlating language use with corporate decision-making, much like Schmeltz (2014) for example does by comparing corporate CSR statements with data from interviews with senior management. There would also be value in turning to newspapers, trade publications, websites, social media, and google document repositories to look at how language within the co-operative sector more broadly has evolved over time relative to alternatives.

Finally, we also see an opportunity for this work to influence ongoing discussions about the evolution of the seven co-operative principles which, again, often find their way into legislative frameworks and are therefore important guideposts for policymakers. As Fairbairn (1994) has argued, there is evidence that the principles have changed in ways that mirror broader society and related existential debates about the co-operative identity. The ongoing debate over the next iteration of the principles should be informed by empirical research into how co-operatives already are talking about what matters to them and how those points of emphasis differ from IOFs. In these ways and others, we will be reminded of the underlying premise of this work, namely that words matter.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.