Abstract

Being at the forefront in the public discussion about sustainable finance (SF) has become a competitive advantage for financial corporations. This study investigates op-eds by representatives of major global investment banks and asset managers (Black Rock, Goldman Sachs, HSBC, Morgan Stanley, UBS) published between 2018 and 2019 in the Financial Times regarding SF. Using an in-depth textual analysis approach, five overarching frames emerged: (1) climate crisis consensus and the urgency to act, (2) sustainable finance as powerful leverage, (3) sustainability in the name of profit and capital growth, (4) need for transparency, quantification, and datafication, and (5) shifting responsibilities. The results imply that SF is used as a public relations tool to promote new, lucrative financial activities that fit within the prevailing neoliberal market model. Rather than providing alternatives to the prevailing financial markets, the investment industry shifts responsibilities to the government, businesses and individuals to fight climate change.

Sustainable finance (SF) has recently become a buzz word in the financial sector (Webb, 2020). However, the conceptualization, understandings, and measurements of SF vary vastly within the financial industry (EY, 2017; Ferrua Rotaru, 2019). Given these ambiguities, ongoing discussions, and the need for innovation in this field, it has become a decisive factor of competition in the financial industry to place oneself at the forefront of SF these days (see shareholder letter by Larry Fink, the CEO of Black Rock: Sorkin, 2020). In fact, the communication about SF by financial institutions has been increasing in the past years by means of press releases sent to journalists, events, roadshows, and website marketing (Strauß, 2021). Another effective PR tool for financial corporations to position themselves in the public debate about SF are op-eds (opposite the editorial page) (Smith & Heath, 1990).

Op-eds have regularly been used in the past by corporations, such as ExxonMobil (Livesey, 2002), to present their views on the debate over climate change (see also Craig, 2008) and to reach their target audiences with strategic communication. However, similar to the fossil fuel industry in the early 2000s, the financial sector is more recently being accused of “greenwashing” when presenting conventional funds and financial products as sustainable (Fancy, 2021; Hellsten & Mallin, 2006). Hence, with reference to the recent discussions and ambiguities about SF, it becomes of interest to investigate how global financial corporations place themselves in the public debate by means of op-eds and to research what message and framing strategies they use when communicating about this trend.

Literature Review

Ever since the Global Financial Crisis 2007 to 2009, the financial industry is only slowly recovering from a tarnished image (Davies, 2010; Thompson, 2009). More recently, the industry has been at the center of criticism regarding their ignorance of climate risks by, for example, supporting industries that contribute to the destruction, pollution, and degradation of the environment, nature, and biodiversity (Carney, 2015; Philipponnat, 2020). Thus, facing increasing public pressure, positioning oneself at the center of the discussion about SF becomes a reputational advantage for financial corporations (cf. cultural change; Strauß, 2015). Previous research has shown that being associated with topics such as sustainability can be considered beneficial for corporate/brand reputation and corporate profitability (Khojastehpour & Johns, 2014). As a result, investment banks, asset managers, and financial institutions around the globe are currently strongly engaged in raising their voice about activities in the area of SF (e.g., advertising campaigns, conferences, and events, working papers). While in the past, topics such as corporate social responsibility (CSR; Reilly & Larya, 2018), ethical business (DesJardins, 2007), and greenwashing (Parguel et al., 2011; Reilly & Hynan, 2014) have been widely discussed in communication research, the topic of SF has not been researched in depth so far and critical analysis of business communication in that area is lacking.

Legitimizing Sustainable Finance in a Neo-Liberal System

Sustainable finance (SF) it not necessarily a new phenomenon. Socially responsible investment or sustainable investment have already emerged in the late 1960s and 1970s in the U.S. and spread to Europe in the 1980s (Boxenhaum & Gond, 2006). However, particularly in the past 2 years, SF has attracted increasing attention among investors (PRI, 2021) and has repeatedly been identified as a “mainstream” trend by the media (The Economist, 2018; Webb, 2020). However, it has been criticized more recently that the concept of sustainability is (over)used in the public debate, and that it has become a synonym for the promotion of economic growth and capitalism (Cox & Béland, 2013; Redclift & Woodgate, 2013). Boehnert (2016), for example, has pointed out that the “green economy” is simply an “intensification of the neoliberal model, and an exceptional opportunity to create new financial instruments” (p. 409). With industry estimates expecting global ESG funds to reach $53 trillion by 2025 (from $22.8 trillion in 2016) (Bloomberg Intelligence, 2021) and more than 3,800 asset owners, investment managers and service providers who have signed the UN Principles for Responsible Investment by April 2021 (PRI, 2021), the financial markets have made use of the sustainability trend by creating new financial vehicles (e.g., ESG funds, green bonds) which, however, continue to work based on the neoliberal market model by aiming at excessive return rates. Given these contradictions, it becomes of interest to investigate how global financial actors frame the concept of SF in the public discourse, and how they legitimize their continued engagement in neoliberal financial activities as a way to combat climate change.

Framing Strategies, Op-Eds, and the Financial Press

Framing can generally be defined as “selecting and highlighting some facets of events or issues, and making connections among them so as to promote a particular interpretation, evaluation, and/or solution” (Entman, 1993, p. 54). Using Entman’s definition, corporate communication research has investigated in various ways how corporations make use of framing strategies in their communication to present themselves in a specific light that is assumed to be beneficial for their reputation or image among the public (Mitra, 2011; Strauß & Vliegenthart, 2017; Tengblad & Ohlsson, 2010; Wickman, 2014). Either such frames are directly communicated via corporate communication tools (e.g., advertisement, press releases, speeches) to the respective target audience, or the frames are indirectly being placed in various channels such as the news media, for example, via quotations, interviews, or op-eds.

Op-eds have been identified as effective public relations tools, for example, in the area of public diplomacy (e.g., Golan, 2013), political communication (e.g., 2003 Iraq War: Sahlane, 2013), and corporate communication about climate change (e.g., ExxonMobil: Livesey, 2002). Kiousis and Strömbäck (2015) assert that information subsidies such as news releases, press conferences, or op-eds are used by organizations as a “widespread approach for effective issue management via strategic communication” (p. 390) to exert influence over the news media and other stakeholders. What is more, op-eds have become a popular method for communication by CEOs, NGO representatives, politicians and other advocates when placing messages about corporate social responsibility, sustainability, or environmental concerns (e.g., Craig, 2008; Smith & Heath, 1990). Hence, for global financial corporates who have to defend, explain and justify their engagement with sustainability vis-à-vis their critical stakeholders, being vocal about their commitment to SF becomes part of their strategic communication plan.

The international newspaper, the Financial Times (FT), is considered to be one of the most prestigious news outlets for (financial) corporate communication to position strategic messages. The FT is not only widely read by business professionals, decision-makers, investors, and opinion leaders in the financial markets, but it is also a popular newspaper among wealthy and discerning consumers (Financial Times, 2020). Previous research has in fact shown that the FT does not only play a crucial role in developing an elite sphere, for example, for debates surrounding European politics (Corcoran & Fahy, 2009), the newspaper is also considered to be one of the most widely read newspaper in the financial industry (Davis, 2015). As such, the FT qualifies as a key outlet for discussions about SF (e.g., EU taxonomy on SF), and placing an op-ed with pre-defined corporate messages about the topic can be seen as an effective reputational tool to reach the respective target audience (cf. Cox & Schwarze, 2015). However, research on framing strategies in op-eds and the strategic use of this communication tool for corporates remain a niche, and more research is urgently needed in this area (cf. Golan, 2013). Hence, this study seeks to fill this research gap by studying op-eds in the FT and providing answers to the following two research questions:

RQ1: What frames do global financial actors (asset managers, investment banks) use when communicating about sustainable finance in op-eds in the Financial Times?

RQ2: How do they legitimize their engagement with sustainable finance to combat climate change?

Data and Method

Case Selection

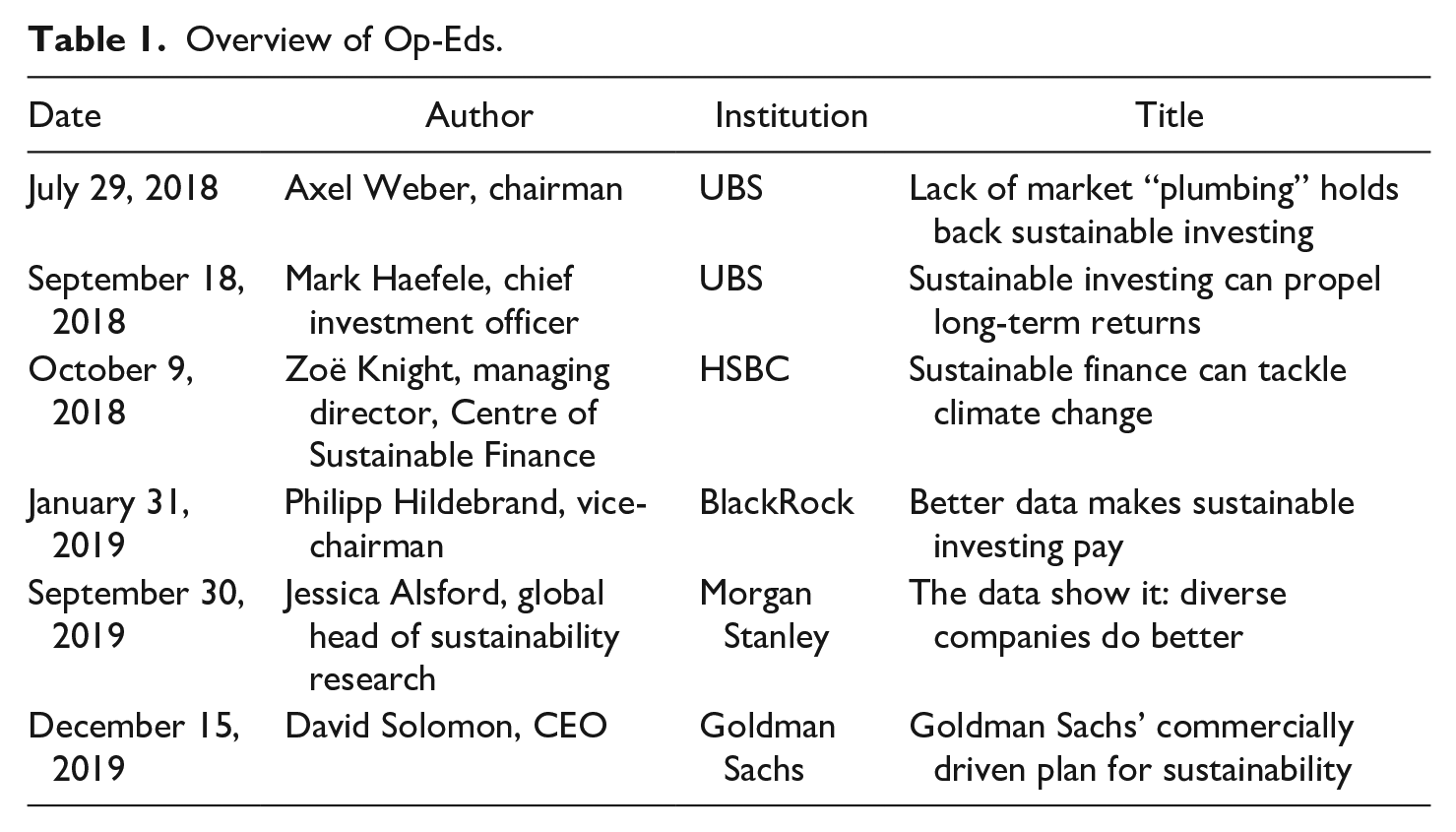

The FT online website was searched for relevant articles by using the keywords “sustainable finance,” “sustainable investing” and “impact investment,” and restricting the search for op-eds and texts published between 01/01/2018 and 01/01/2020. After a thorough search through all op-eds (N = 99) shown by ft.com with the given search terms, six op-eds dealing with SF which were written by representatives of large international investment banks and asset management firms (Black Rock, Goldman Sachs, HSBC, Morgan Stanley, UBS) were identified (see Note 1 for links to the six op-eds in full lengths). Surely, the selection of only six op-eds in the FT (see Table 1) does not allow to draw conclusions about the entire global financial industry, but the op-eds of the respective corporations are representative for the international mainstream investment and asset management industry.

Overview of Op-Eds.

Qualitative Text Analysis

The op-eds were analyzed by means of a qualitative text analysis in line with Golan (2013), who has similarly researched frames and key arguments in op-eds. Qualitative framing analysis is a common approach employed in environmental communication (e.g., Wickman, 2014) and corporate or strategic communication (e.g., Mitra, 2011; Strauß, 2015). Following the theoretical framework as outlined above, the guiding principle of the textual analysis in this study is based on the framing definition by Entman (1993). Hence, the analysis is aimed at identifying what sort of interpretation, evaluation, and/or solution the authors of the op-eds are proposing regarding SF and climate change. To identify the frames, all op-eds were thoroughly read, and first observations were attached as codes to passages of the op-eds. Afterwards, these codes were compared across the op-eds and the emerging frames were identified.

Results

Climate Crisis Consensus and the Urgency to Act

Across all six op-eds, there appears to be a common consensus on climate change and the urgency to become active in order to limit carbon emissions, and thus global warming. David Solomon, for example, the CEO of Goldman Sachs, states that the “evidence of climate change is clear,” and Zoë Knight, managing director of the Centre of Sustainability at HSBC, speaks of a “wide consensus” that action to prevent problems that arise due to climate-change are “in everyone’s best interest.” Furthermore, the urgency to act and save the environment from continuing and increasing carbon dioxide emissions has been pointed out by almost all authors. Zoë Knight lists the looming dangers of climate change, such as “heavier rain,” “rising sea levels” or “storm surges” and acknowledges that “there is no time to lose,” highlighting the timely pressure and need for immediate action. Similarly, Solomon warns that “(w)e don’t have the luxury of that limited perspective any more” and corroborates that there is an “urgent need to act.” In a similar vein, Philipp Hildebrand from Black Rock uses the word “inflection point” to stress that investors find themselves in a position in which they become responsible in deciding what the future will hold.

Sustainable Finance as Powerful Leverage

As a response to the looming climate crisis, all of the op-eds convey a positive and optimistic picture of the future and offer solutions how the financial sector could help to fight climate change. Axel Weber, chairman of UBS, suggests that the private and public sector should put their shared interests in concrete actions to solve social and environmental challenges. Jessica Alsford from Morgan Stanley emphasizes the role of corporations, asserting that “the positive improvement in corporate practices (that) is at the heart of much of the sustainability movement.” In fact, there is an overall agreement among the authors in the op-eds that SF represents a powerful leverage to tackle climate change. Philipp Hildebrand from BlackRock turns to the investment industry and reaffirms: “Together we can be a positive catalyst for change.” While David Solomon, the CEO of Goldman Sachs, believes that the market will find an answer to climate change, he is convinced that “financial institutions can play a critical role” and will be necessary to eventually drive sustainability and adapt the global economy. Furthermore, Zoë Knight from HSBC even promulgates in the headline of her op-ed: “Sustainable finance can tackle climate change” and closes her op-ed by presenting sustainable finance as “the answer” to climate change. The self-confident and optimistic statements by the investment professionals is a way to signal the readership of the FT that the financial industry does not only take a decisive stance to limit carbon emissions, but that they also consider themselves to be at the forefront in fighting climate change.

A common method used by the authors to prove this conviction is by presenting concrete examples of the success of sustainable investments (SI) so far. Axel Weber reports that SI have risen by 25% between 2016 and 2018. Jessica Alsford (Morgan Stanley) refers to data by the Global Sustainable Investment Alliance, showing that SI has reached $31 trillion in 2018. Similarly, Mark Haefele cites an UBS Investor Watch survey according to which “39% say that they already have some sustainable investments in their portfolios.” In a similar vein, Philipp Hildebrand from BlackRock argues that millennials are the future drivers of ESG investments by inheriting $24 trillion of wealth over the next 15 years. To show how the sector is reacting to this trend, David Solomon proudly announces how Goldman Sachs will target “$750 billion of financing, investing and advisory activity” to various areas to promote climate transition and inclusive growth and presents a case of an Italian utility that Goldman Sachs has accompanied in putting sustainability to the core of its business strategy.

Sustainability in the Name of Profit and Capital Growth

Indeed, after having analyzed the six op-eds, it occurred to be one of the main objectives of the authors to present SF as a new financial market opportunity where investors can generate considerable profits and returns. In all the op-eds, it seems that the representatives of the international investment banks and asset managers want to prove that green, sustainable or responsible investments are (at least) as lucrative as conventional investments. Solomon, for instance, talks of a “powerful business and investing case.” Hildebrand from BlackRock, who points out that responsible investments meant “trading returns for values” in the past, says “(t)oday, sustainability considerations do more than fulfill an investor’s value—they can drive successful investment decisions.” Similarly, Mark Haefele from UBS reassures that “compelling evidence” suggests that SI is boosting returns rather than harming them and states right in the beginning of his op-ed: “If you aren’t investing responsibly then you are investing irresponsibly.” The op-eds are filled with examples that are aimed at demonstrating how sustainable investments perfectly fit within the status-quo of the neoliberal economic model.

A rather plain statement with regard to the importance of generating profit is brought forward by David Solomon (Goldman Sachs): “Profitability will always matter—capital must be deployed to those opportunities that have the greatest potential for success, and we must generate strong returns on invested capital to serve those saving for retirement.” This statement reveals that SF is just another way of generating profit on the financial market to please and further enrich investors and capital holders. Although intending to do good and contribute to sustainable development by shifting capital to the areas in need, the financial actors remain active in a capitalistic market model. The investment banks and asset managers need to ensure their clients that they are not radically shifting their business model by putting sustainability before profitability. Rather, they seem to reinforce the current neoliberal system by treating SF as a convenient add-on to traditional investment models: making returns and soothing one’s conscience by investing money in sustainable businesses. Axel Weber (UBS) summarizes this mindset adequately by stating that “investors look to do well while also doing good.”

This implicit re-affirmation of the neoliberal economic system applies to all op-ed contributors. The authors use various examples to show how they have used the principle of SF to create new investment products, such as sustainability indices (e.g., ESG indices), funds (e.g., Green Climate Fund), or bonds (e.g., development bank bond) that are profitable and an attractive investment instrument. Jessica Alsford presents in this regard an index that Morgan Stanley has developed to measure gender diversity in companies and its positive impact on investment returns. She argues that it is important to demonstrate that “ESG is a source of incremental alpha generation,” thus generating an excess return or beating the market. To show another success rate of SF, Philipp Hildebrand from BlackRock cites one of the in-house research reports and concludes that “sustainable indices. . .have the same risk and return characteristics as traditional benchmarks.”

Need for Transparency, Quantification, and Datafication

The framing analysis made clear that the authors are heavily reliant on data, scientific studies (e.g., meta-study Friede et al., 2015), and other metrics that show the success of SF on the market and the positive return rates that they generate. Zoë Knight from HSBC speaks, for example, of clear “signals” that would incentivize governments to invest in the energy transition, and Axel Weber (UBS) sees it as imperative for the further success of SF to “simplify and standardize” terms and products of the sustainable investment industry that will enable to prove the positive outcomes on society and the environment. However, making SF transparent, quantifying the impacts of SI and getting data that allow to draw informed and reliable decisions about SI present major challenges for the financial industry.

While Philipp Hildebrand from BlackRock points out that ESG data “continues to improve,” he also criticizes that “different data providers can come to different conclusions on the ESG attributes of the same company” and urges the investment industry to deliver better tools. Many of the representatives of investment banks and asset managers therefore outline in their op-eds how they master the challenge of quantifying SF by means of their in-house expertise or collaboration with industry alliances. Goldman Sachs, as David Solomon reports, now has “a set of metrics” about sustainability that they can use to track the companies they invest in and Jan Hildebrand (BlackRock) presents an in-house research analysis that proves the success of sustainability indices. Similarly, Jessica Alsford proudly reports the results of the Morgan Stanley diversity index and also applauds the efforts of organizations such as the Sustainability Accounting Standards Board (SASB) that require ESG reporting from companies.

However, there was an overall agreement among the authors of the op-eds that there is a need for transparent and reliable data for SF. Solomon (Goldman Sachs) is asking for “objectives with measurable results,” Hildebrand (BlackRock) emphasizes that “reliable data” is a must, and Jessica Alsford (Morgan Stanley) demands clear “evidence” that show a correlation between ESG and investment returns and bemoans that “consistent, comparable, and high frequency data” is lacking. She criticizes that too few companies report their carbon or greenhouse gas emissions and that the identification of ESG metrics “requires a search through many data points.” Similarly, Zoë Knight (HSBC) laments that the strategy on energy transition is often “varied and opaque,” and therefore demands more transparency and information on sustainable capital flows. The ambiguity of data, according to Solomon (Goldman Sachs), poses an arbitrariness in the application of ESG factors for investments, as many choices at this stage are neither “black or white,” nor “right or wrong.”

Shifting Responsibilities

Given the remaining challenges that SF poses to the financial industry, a common strategy among the authors of the op-eds is to shift the responsibility to governments, politics, companies, and individuals to deal with climate change. More specifically, Solomon from Goldman Sachs points out right in the beginning of his op-ed that “governments must put a price on carbon.” Although he acknowledges that the markets are powerful in addressing climate change, he fears that this will not be enough “given the magnitude and urgency of this challenge.” Solomon actively requests governments to introduce a carbon tax, and he is not alone. Zoë Knight from HSBC equally supports the idea of “charging emitters of carbon dioxide” and requires governments to remove “fossil fuel subsidies.”

Another common strategy among the op-ed authors to shake off responsibility is to call the companies to take more action. While Jessica Alsford (Morgan Stanley) criticizes the missing data by companies on carbon emissions, Solomon points out that companies have treated “sustainability as a peripheral issue” in the past. Similarly, Axel Weber (UBS) argues that SF will only become mainstream “if both the public and private sector work together” and Philipp Hildebrand (BlackRock) and Mark Haefele (UBS) both request global guidelines and clearer definitions on SF and sustainable investment products. While there are already industry alliances (e.g., SASB) and policy initiatives (e.g., EU HLEG) that are working out solutions—and that also find support by some of the representatives (e.g., Axel Weber, UBS)—most of the authors underline that more actors need to get engaged to fight climate change. For example, Zoë Knight (HSBC) reinforces that “climate change has to involve everyone everywhere” and that “everyone must do more.”

Discussion

To get a better understanding of how leading investment banks and asset managers frame SF and how they legitimize their SF activities in light of climate change, this study has analyzed six op-eds published in the Financial Times by representatives of international investment banks and asset managers. Based on the analysis, five re-occurring frames were identified across the six op-eds: (1) climate crisis consensus and the urgency to act, (2) sustainable finance as powerful leverage, (3) sustainability in the name of profit and capital growth, (4) need for transparency, quantification, and datafication, and (5) shifting responsibilities. A re-occurring observation among the op-eds was that the financial actors oftentimes contradict themselves when talking about SF. On the one hand, the authors express their deep concerns for climate change and an understanding for the big challenges that the world is facing; but on the other hand, they are re-affirming the neoliberal capitalistic ideology by focusing mostly on the argument of profitability, growth and returns when advocating for SF and related products.

This contradiction when it comes to SF has been outlined by other researchers more recently. Lagoarde-Segot (2019), for example, criticizes that the “finance function” in SF “is reduced to the status of a mere tool enabling an organization to sustain its business over the long term” (p. 2) and that practitioners are confronted with an “increased complexity” (p. 2) when trying to include social criteria into investment decisions. This contradiction also resonates with what Baeten (2000) has identified as the “conservative movement” of sustainable development. SF, as discussed by the representatives of the financial institutions in the op-eds, does not challenge capitalism; rather, SF is presented as a continuation and convenient add-on of the profit-seeking and growth-oriented neoliberal market model, whereas financial capital is directed to ecological and environmental investments as long as it generates profit and secures the maintenance of established market operations and principles.

Surely, there is the question of what would be the alternative? There are many alternative economic models and theories that have been widely discussed in academia and the public sphere such as the “doughnut economy” (Raworth, 2017) or circular economy concepts (see for an overview: Kirchherr et al., 2017). In fact, there are numerous examples of places where a circular economy model works well or is under way (e.g., Amsterdam: Boffey, 2020; Thornton, 2019). While circular models pose a challenge for the economic system at large, given the dependency of societal processes on the global financial markets (e.g., hedging risks, insurances, pensions), there are successful alternatives of green and ethical banking around the globe (e.g., Triodos in Europe, GLS in Germany, Alternative Bank in Switzerland) that also offer truly sustainable banking and investment opportunities. Such business models that operate strictly according to ethical, responsible and sustainable guidelines would allow a more sustainable financing of societal, environmental and corporate needs.

Yet, rather than transitioning the core of the business models and the financial market, the representatives of the investment and asset management industry seem to be mainly worried about not repelling their clients with the new trend of SF, signaling them that the main purpose of doing business is still generating respectable returns for them. Hence, it does not come as a surprise that none of the authors criticizes the current economic system, let alone dares to imply that the core of the economy is inherently unsustainable in its current form (cf. striving for growth by exploiting markets and resources). As Lagoarde-Segot (2019) argues, there is an “apparent inability of mainstream financial models to grasp the reality of sustainable finance” (p. 2). Following Lagoarde-Segot (2019), academic finance, but also the financial sector, fail to align finance with societal needs due to a misconceived social ontology. In a similar vein, Boehnert (2016) asserts that “(e)cological processes are simply too complex to be captured absolutely through financial valuation processes” (p. 404).

Instead of discussing how the banking and investments system could change (e.g., sustainable/ethical banking, circular economy, doughnut economy), the authors of the op-eds are shifting the responsibilities to fight climate change to the broader public and the government in particular. This is a reoccurring strategy that has been employed by the financial sector beforehand; namely in the aftermath of the Global Financial Crisis 2007 to 2009. Back then, a common argument was that market and regulatory failures were the real cause of the crisis (Helleiner, 2011). The op-eds similarly imply that the industry again shifts the responsibility to politics with regard to finding a solution for climate change and to reduce carbon emissions. Instead of focusing on how the investment industry could integrate climate awareness at the core of their business practices, they are calling upon politicians and corporations to set the framework that would incentivize, secure or even restrict financial activities to sustainable actions (e.g., carbon tax).

Nevertheless, the investment professionals still consider themselves as a powerful leverage to fight climate change, with presumably considerable amounts of capital and impact to influence and incentivize sustainable business endeavors. In so doing, they make use of the op-eds as an advertising platform to promote their own research, analyses, and financial products that should presumably prove the success of sustainable investments to their stakeholders (e.g., shareholders). In line with previous research (e.g., public diplomacy: Golan, 2013; political communication: Sahlane, 2013), the financial industry strategically uses these op-eds in the FT to legitimize their activities in the area of SF and to maintain a favorable reputation in the midst of public pressure on the industry’s active contribution to climate change and environmental destruction (cf. Carney, 2015; Philipponnat, 2020).

To conclude, the framing analysis of the op-eds in the FT by investment bank and asset management representatives about SF can best be summarized by referring to Enzensberger’s (1974) seminal article on the critique of political ecology. Following the discussion about the environmental ideology, he concludes that there are often interests of the discourse that are concealed and promoted at the same time. Thus, although the financial representatives are highlighting their overall aim to fight climate change with SF in their commentaries, their engagement with SF can be traced back to their singular interests as financial market actors to take advantage of the current market trend in terms of reputational and monetary benefits. After all, financial institutions do not necessarily see their main societal function in safeguarding the environment. When looking at their corporate self-description, the central purpose is helping businesses and economies to grow and prosper. Having this conflicting self-image in mind, SF appears to be just another financial marketing stunt. To truly provide a convincing answer to climate change, the financial industry would need to walk their talks (Pager & Quillian, 2005), not shifting responsibilities to politics or the public, and offer clear solutions on how to transition toward a more sustainable economy.

Footnotes

Declaration of Conflicting Interests

The author declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: The author declares that she has no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper. The manuscript is original and is not under consideration or published elsewhere.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This project has received funding from the European Union’s Horizon 2020 research and innovation programme under the Marie Skłodowska-Curie grant agreement No 834638.