Abstract

The current study sought to explore the predictors of financial behaviour among working adults based on the theory of planned behaviour. This study employed the correlational cross-sectional questionnaire-based research design. In total, 558 samples were obtained through a purposive sampling technique. The measurement model and proposed research model were evaluated using partial least squares structure equation modelling. The findings revealed that financial knowledge is positively associated with the attitudes towards retirement, perceived behavioural control, subjective norms, and financial behaviour of working adults. In addition, the findings demonstrated that retirement attitude, perceived behavioural control, and subjective norms each had a positive relationship with behavioural intention towards planning for retirement. Furthermore, the results showed that behavioural intention and perceived behavioural control are positively associated with the financial behaviour of working adults. The findings could aid financial educators and advisors in delivering the correct blend of financial knowledge to assist working adults in making better financial decisions and practising proper financial behaviour.

Keywords

Introduction

With the rise of globalization and financial market liberalization, individuals bear greater responsibility for their financial behaviour and wealth management. Financial planning has significantly evolved, making financial management a rather complicated process (Lusardi & Mitchell, 2017). In developing a financial planning strategy, one must be able to utilize their resources to meet their needs and desires, particularly during retirement, as it reflects the financial stability and protection everyone aspires to gain (Lusardi & Mitchell, 2017; Topa et al., 2018; Xiao, 2008). Numerous research has discovered that effective financial management skills protect people from overspending and debt (French & McKillop, 2016; Ksendzova et al., 2017). However, managing one’s finances can be daunting, especially for those without much financial knowledge. Strömbäck et al. (2020) discovered that a critical factor in developing financial capability and managing one’s wealth is the financial capability to comprehend numbers and have an emotional attitude towards numbers. Pre-retirees with low financial skills have been found to have a flat wealth trajectory than those with high financial skills, which makes financial skills necessary for wealth management and retirement security (Banks et al., 2010). Literature reveals the necessity of enhancing financial knowledge and responsible financial behaviour as they are essential for working adults’ retirement preparedness. For example, people with a higher level of financial knowledge and sound financial behaviour are accountable for credit card use, prompt bill payments, spending within budget, handling money matters, and credit cardholders’ decision-making (Hamid & Loke, 2021; Loke, 2015; She, Rasiah, et al., 2022). However, the fact remains that most of working adults or pre-retirees lack basic knowledge of finance and do not manage their finances properly, which may lead to low living standards in the post-retirement period (Butt et al., 2018; Lusardi & Mitchell, 2017).

The global ageing population is rapidly increasing, and there are 727 million people aged 65 years and above globally (United Nations, 2020). It is further estimated that by 2050, the number of older people worldwide will be more than doubled, reaching over 1.5 billion and making up more than one-fifth of the world’s population (United Nations, 2020). The fact—people live longer lives due to medical advancements and economic and social progress—results in extended retirement periods (Bloom et al., 2015; Rasiah et al., 2022). In Malaysia, an estimated 2.4 million people over 65 accounts for 7.4% of the total population (Department of Statistics Malaysia, 2021). With Malaysia’s increasing ageing population, many potential retirees can spend almost as much time in retirement as they would during their working years (Rasiah, et al., 2022), leading to untold financial, social and psychological consequences that many are unprepared to face (NoorAni et al., 2018). Another fact is that many Malaysians neither are adequately prepared nor have planned well for their retirement, as their spending is much more than their savings; thus, the situation worsens when they can easily access credit terms and online purchasing (Mustafa et al., 2023; Rasiah et al., 2022). People spend years getting an education and developing their skills and knowledge over a long period to prepare themselves for the job market, after which they spend a few decades working and planning for their lives (Liu-Farrer & Shire, 2021). Earlier studies (Kadoya, 2016; Kadoya & Khan, 2018) indicated that people at a younger age do not particularly worry about their financial future and retirement, though they only start to think and worry about retirement planning during their middle age (e.g., 40 years and above). Moreover, Froidevaux et al. (2016) argued that making a successful transition from work to retirement and achieving good retirement adjustment has become the main concern for working people aged 40 and above as they are now at the life stage of transitioning into older workers gradually. However, in most cases, there is no systematic preparation for retirement (Klapper & Lusardi, 2020). Many either do not know how to plan for their retirement or do not think about it and therefore do not have any retirement plan (Butt et al., 2018). The primary reason could be that many employees lack basic financial knowledge and are not fully prepared to manage their finances (Lusardi & Mitchell, 2017). For this purpose, people must be taught basic money management skills, failing which government expenditure on healthcare, welfare and social security would continue to rise inexorably.

The present study is expected to add to the body of knowledge by understanding the mechanisms through which financial knowledge influences financial behaviour through cognitive financial beliefs (attitudes towards retirement, subjective norms, perceived behavioural control) and behavioural intention. In addition, using the theory of planned behaviour (TPB), the present research model provides a novel pathway to understanding working adults’ financial behaviour and its determinants from the viewpoint of personal finance and retirement preparedness. Next, following Kadoya and Khan’s (2018) suggestion, this study focuses on working adults aged 40 years and above, as age 40 is considered the critical time point for employees to look into their retirement. Many previous studies on financial management planning and financial behaviour conducted in Malaysia only focused on college students and young adults (e.g., Pahlevan Sharif et al., 2020; Yong et al., 2018; Zainudin et al., 2019). The study has parallels with the early research by Xiao et al. (2014), who suggested that future research on personal finance should focus on developing countries to enhance a better understanding of financial behaviour among different populations.

Literature Review

Theory of Planned Behaviour

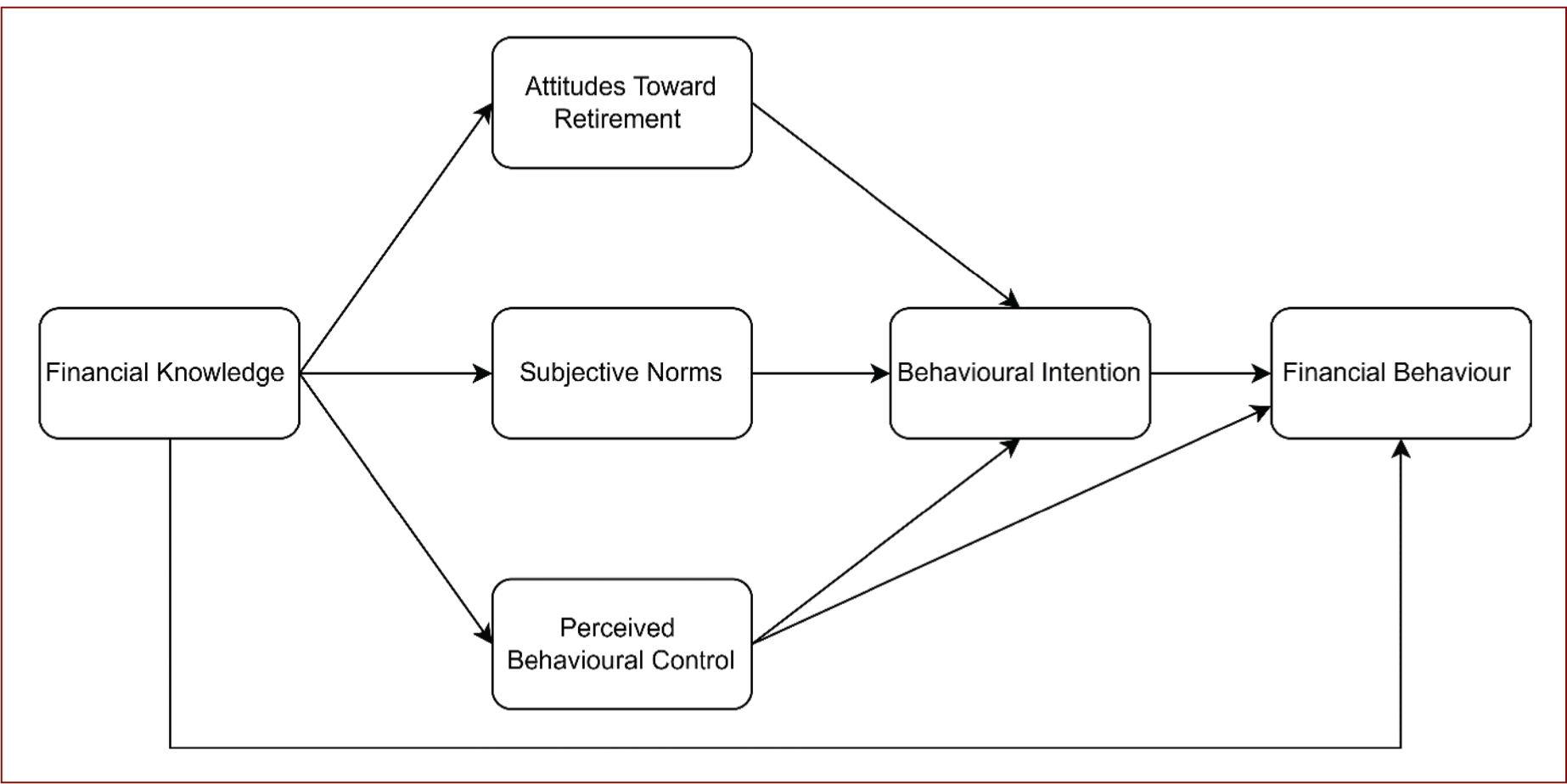

The TPB was initially proposed by Ajzen (1985), who stated that most human behaviour results from an individual’s intention to take on specific behaviour and the capability of an individual to make a precise decision about it. The TPB is also the superior model theory to assess or understand human behaviour (Ogiemwonyi, 2022). According to Ajzen (1991), an individual’s attitude, perceived behavioural control, and subjective norms can predict the intention to behave in a particular manner. Perceived behaviour control, when combined with intention, will culminate in realizing the actual behaviour (Ajzen, 1991; Ogiemwonyi & Harun, 2021). Ajzen et al. (2011) state that TPB is also open to including additional predictors upon meeting the different criteria, in addition to the existing predictors recommended by the TPB. It has to be conceivable and empirically supported that such a predictor could influence motivational factors (e.g., attitude, subjective norms, and perceived behavioural control), behavioural intention or actual behaviour (Ajzen et al., 2011). In this sense, Ajzen et al. (2011) proposed that an individual’s level of knowledge can be a prerequisite for effective behaviour, being independent of the TPB’s existing predictors and impacting motivational factors. Similarly, personal finance studies have supported that one’s knowledge of finances influences motivational factors and financial behaviour (Ajzen et al., 2011; Guy et al., 2014; Serido et al., 2013; She, Rasiah, et al., 2022). Although TBP has been extended and tested in various settings (Agu, 2021; Agu et al., 2022; Bongini & Cucinelli, 2019). The TPB has been utilized to predict early retirement previously (van Dam et al., 2009), but its use in planning behaviour is still nascent and obscure in its application. However, the TPB has been successfully applied to behaviours such as exercising (Hagger & Chatzisarantis, 2005) and dieting (Biasini et al., 2021) that are not only effortful but also have a delayed benefit, which is particularly characteristic of behaviours similar to the domain of retirement planning. In the current study, we use a revised version of the TPB that includes behavioural norms together with subjective norms, attitudes and perceived behavioural control as predictors of behaviour. This study is the first one that attempts to extend the TPB by adding the additional predictor (e.g., financial knowledge) as the starting point and suggests that: (1) financial knowledge be taken as the starting point for influencing working adults’ retirement attitude, perceived behavioural control, subjective norms and financial behaviour (Ajzen et al., 2011; Serido et al., 2013), (2) attitude towards retirement, perceived behavioural control and subjective norms lead to the behavioural intention of retirement planning, (3) behavioural intention and perceived behaviour control lead to the implementation of the financial behaviour (Ajzen, 1991).

Financial Behaviour

Financial behaviour is any behaviour relevant to money management and planning, such as borrowing, saving, investing, insuring and spending (She, Rasiah, et al., 2022; Xiao, 2008). In addition, financial management behaviour is a means of managing money, expenditure patterns, savings, budgeting, credit and investments (Hamid & Loke, 2021; Huston, 2010; Loke, 2017). Also, financial behaviour is a significant predictor determining one’s financial well-being, retirement preparedness, workplace productivity and quality of life (Bamforth et al., 2017; Koh et al., 2021; Sabri & Aw, 2020; She, Ma, et al., 2022). According to Aguila et al. (2011), retirees tend to control their spending and practice responsible financial behaviour due to changes in lifestyle and better money management. Moreover, individuals who practice responsible financial behaviour, especially in financial planning and regular savings, have higher financial stability and better living standards (Alshebami & Aldhyani, 2022; Sabri & Aw, 2020; Topa et al., 2018; Xiao, 2008). In addition, a review of past studies reveals that financial behaviour plays an essential role in retirement preparedness (Hauff et al., 2020; Noviarini et al., 2021). Hauff et al. (2020) stated that an individual’s financial behaviour for retirement depends on two assumptions. The first assumption is that the individual should understand basic financial concepts, and the second assumption is that they should be able to control their financial beliefs. This aligns with the earlier argument of the present study, stating that working adults’ financial knowledge and financial beliefs (e.g., retirement attitude, perceived behavioural control, subjective norms and behaviour intention) are vital in enhancing responsible financial behaviour.

Financial Knowledge

A financially literate person is one who understands and is able to apply the basic knowledge of some financial concepts (Garg & Singh, 2018). Most of the time, studies have considered financial literacy and financial knowledge to be synonyms (Huang et al., 2013; Lusardi & Mitchell, 2014). However, according to Huston (2010), financial literacy has to be examined from at least two dimensions beyond just financial knowledge: (1) how well an individual can understand financial-related concepts and (2) how well the individual can use and apply those concepts (Huston, 2010). Some studies also indicated that one of the critical dimensions of financial literacy apart from financial attitudes and behaviour, is financial knowledge (Garg & Singh, 2018; Rai et al., 2019). Knowledge of finance is vital for economic survival, as most people do not live in financial isolation (Lusardi & Mitchell, 2014). Financial knowledge is crucial in today’s society as it affects every aspect of life, such as student loans, mortgages, credit cards, savings and health insurance (Klapper & Lusardi, 2020). Research has shown that having financial knowledge enables an individual to be more prepared for particular financial roadblocks, which reduces the likelihood of experiencing personal financial distress (Karakara et al., 2021). Financial knowledge has a significant and consistent role in financial decision-making (Karakara et al., 2021), as well as in transforming financial beliefs (such as financial attitude and perceived behavioural control) and behavioural intentions into behaviours (Popovich et al., 2020). Financial knowledge enhances people’s financial behaviour by increasing their confidence in managing their finances (Radianto et al., 2021). Also, financial knowledge significantly reduces compulsive spending off the credit card (Khandelwal et al., 2021), increases retirement preparedness (Lusardi & Mitchell, 2014), and has greater wealth accumulation (Jappelli & Padula, 2013), among others.

Financial Knowledge and Financial Behaviour

Individuals’ decision-making processes are heavily influenced by financial knowledge. A review of past literature shows that low financial knowledge results in unreasonable financial behaviour about stocks, pension plans, pensions and debt (Lusardi & Mitchell, 2017). This simply means individuals with limited knowledge of finances are usually ill-prepared in making financial decisions and are therefore susceptible to making uninformed decisions, leading to detrimental consequences. Extensive research confirms the importance of financial knowledge in determining financial behaviour and the accumulation of wealth (Behrman et al., 2012; Jappelli & Padula, 2013; van Rooij et al., 2012). Grohmann et al. (2018) revealed that financial knowledge increases financial inclusion, supporting the real economy. Niu et al. (2020) discovered that financial knowledge significantly and positively affected various aspects of retirement planning among Chinese citizens, including assessing retirement financial needs, developing long-term financial plans, and buying private pension insurance. In addition, Tomar et al. (2021) stated that financial knowledge is essential in determining retirement planning. Higher financial knowledge increases one’s likelihood of contributing to retirement savings plans and displaying responsible financial behaviour (Howlett et al., 2008; Sabri & Aw, 2019; Tomar et al., 2021). This study, therefore, hypothesises that:

H1: There is a positive relationship between financial knowledge and financial behaviour among working adults.

Financial Knowledge and Attitude Towards Retirement

Studies (Akhtar & Das, 2019; Serido et al., 2013) noted that one’s perception of their financial knowledge could translate into financial self-beliefs, and then leads to financial behavioural intention, which ultimately affects financial behaviour (Akhtar & Das, 2019). Serido et al. (2013) proposed a model examining financial capability to understand better how financial knowledge, self-beliefs and financial behaviour relate to financial and overall well-being among young adults. Through a two-time longitudinal survey, the study found that the foundation that transformed one’s financial attitude was financial knowledge, and this led to positive changes in financial behaviour and financial and overall well-being. At this point, it is evident that financial knowledge can influence financial attitudes, leading to changes in financial behaviour. Several experimental studies also supported the findings of the impact of financial knowledge on financial attitudes and, consequently, financial behaviour. For example, Batty et al. (2015) found that those who have undergone financial education exhibited improved financial attitudes and were later found to display better financial behaviour than those in the control group. In addition, Bir (2016) concluded that positive financial attitudes could lead to better financial management behaviour among fresh graduates, with financial knowledge being the foundation of this relationship. Hence, the following hypothesis is proposed:

H2: There is a positive relationship between financial knowledge and attitude towards retirement among working adults.

Financial Knowledge and Subjective Norms

The broader conceptualization of financial knowledge considers it a continuum of demographic and socioeconomic factors. This has prompted researchers to view financial literacy or knowledge from the lens of consumer socialization theory to understand the influence of financial knowledge on social norms, often through the concept of financial socialization (Brown et al., 2018; LeBaron et al., 2018). The idea of financial socialization considers the process by which individuals acquire and learn attitudes and behaviours affecting their financial behaviour (Ameer & Khan, 2020). The agents of financial socialization, or those responsible for applying the pressure of social norms—for example, parents, colleagues and peers—influence mental and behavioural outcomes in the long term (Ameliawati & Setiyani, 2018). The literature also points to the fact that individuals primed in financial management in their early life often carry dormant knowledge of financial literacy, which can only be applied later in life. For example, when they possess financial access, there is a need to effectively utilize what they have previously learned—with parental influence on financial management-related matters extending well into mid-life/late-life individuals (Ameliawati & Setiyani, 2018; Goyal & Kumar, 2021). Past studies have tested the varying level of financial knowledge in determining social norms (as presented by peers, colleagues and relatives) and their influence on an individual’s financial behaviour (Ameer & Khan, 2020; Gudmunson et al., 2016; LeBaron et al., 2018), positing that high financial knowledge does strengthen the effects of social norms surrounding savvy in financial management within social groups (affecting value judgement as normative means on determining acceptable/unacceptable saving for retirement). Thus, the hypothesis the present study posits is:

H3: There is a positive relationship between financial knowledge and subjective norms among working adults.

Financial Knowledge and Perceived Behavioural Control

The performance of behaviour (such as financial planning for retirement) is influenced by both (1) adequate resources towards the intended behaviour and (2) the capacity to regulate the constraints on the desired behaviour. According to Lim and Weissmann (2021), people feel more in control of their behaviour and have a higher intention to engage in the behaviour when they have access to more resources and fewer barriers to doing so. When making decisions, an important factor that people need is ‘knowledge’ in processing information to facilitate behavioural performance (Brucks, 1985; Kaiser et al., 2022). In the context of financial products, this knowledge is represented by ‘financial knowledge’ (Huhmann & McQuitty, 2009). Over the years, several definitions of financial knowledge have emerged. Mandell and Klein (2009) defined financial knowledge as the required knowledge that individuals must be equipped with to enable them to make essential financial decisions in their best interest. Lusardi and Mitchell (2014) defined financial knowledge as the comprehension of the basic concepts of inflation, risk diversification and the ability to do calculations related to interest rates. In recent times, financial knowledge has been readily accepted as an important factor influencing people’s financial decision-making abilities (Mouna & Anis, 2017; Raut, 2020). It is arguably documented that deficiencies in financial knowledge contribute to inertia and suboptimal financial decision-making, frequently linked to poor perceptions of behavioural control (Serido et al., 2013). Hence, the hypothesis proposed for this study is as follows:

H4: There is a positive relationship between financial knowledge and perceived behavioural control among working adults.

Attitude Towards Retirement and Behavioural Intention

The term ‘attitude towards retirement’ reflects an individual’s favourable or unfavourable retirement assessment (Davies et al., 2017). Most studies established that a positive attitude towards retirement influenced individuals’ behavioural intention, financial behaviour, and basic money management skills favourably, and this contributed to retirement preparedness (Hoffmann & Plotkina, 2020; Lim et al., 2018; Segel-Karpas & Werner, 2014; Tomar et al., 2021). According to Segel-Karpas and Werner (2014), individuals’ retirement plans were positively influenced by attitude towards retirement, indicating that attitudes mattered. Therefore, it is extremely important that awareness be raised among employees of the importance of establishing stable financial and retirement plans. Lim et al. (2018) found that attitude towards retirement significantly impacted retirement savings intention among adults in Malaysia. An individual’s financial mindset or attitude towards money substantially affects his/her long-term financial success. The decision to retire, save, invest, plan, or manage one’s finances depends very much on their attitude towards retirement as it influences their retirement planning behaviour and financial success. Attitudes towards retirement tend to transform people’s financial outlook, affecting their intention to save or spend and how well they manage their finances (Hoffmann & Plotkina, 2020). People with a positive attitude are confident and goal-oriented with a long-term perspective, often resulting in financial success (Koropp et al., 2013). They generally spend less than they earn, save for the future, manage their credit, give to others and plan for unexpected expenses. Individuals display optimistic attitudes by prioritizing retirement savings due to more opportunities to invest and save (Millar & Devonish, 2009). Empirical evidence suggests that a positive attitude towards savings results in favourable behavioural intention on financial practices (Lim et al., 2018; Rüfenacht et al., 2016). The study, therefore, proposes the following hypothesis:

H5: There is a positive relationship between attitude towards retirement and working adults’ behavioural intention.

Subjective Norms and Behavioural Intention

An individual’s engagement in behaviour is dependent upon the support, approval and perception given by significant potential reference groups such as spouses/partners, family members, work colleagues and friends/peers, affecting one’s choices (Ajzen, 1991). Individuals are reported to be more prone to engage in specific financial behaviour if people around them advise or think they should (Phan & Zhou, 2014). Hence, individuals can develop the intention to act on a particular behaviour under social pressure, even if they want to carry out that behaviour (Akhtar & Das, 2019). Past studies have linked subjective norms or social norms in determining one’s decision for retirement planning (Croy et al., 2010a, 2012; Kimiyaghalam et al., 2017; Radl & Himmelreicher, 2014). For example, individuals who face pressure from their spouses retire earlier than those without this pressure (Radl & Himmelreicher, 2014). In contrast, individuals tend to participate in post-retirement work if their spouses are still employed (Kim & Feldman, 2000). In addition, the approval or expectation from other parties, such as peers and family, is also a major factor in the participation of older employees in bridge employment (Peng & Min, 2020), behavioural intention (Akhtar & Das, 2019) and retirement planning (Croy et al., 2010a). Subjective norms are highly correlated with elderly buying intention in a retirement village (Ng et al., 2020) and intention for retirement planning behaviour (Sniehotta et al., 2014). In the same vein, van Dam et al. (2009) found that subjective norms significantly affect individuals’ intention to save in a voluntary retirement fund. Therefore, this study proposes:

H6: There is a positive relationship between subjective norms and behavioural intention among working adults.

Perceived Behavioural Control and Behavioural Intention

Perceived behavioural control refers to one’s perception of how simple or complex a certain behaviour is to carry out (Ajzen, 1991). More specifically, perceived behavioural control indicates an individual’s perception of correctly performing a particular behaviour (Martinez & Lewis, 2016). Meanwhile, TPB and previous studies have supported the direct effect of perceived behavioural control and behavioural intention towards financial management behaviour (Ajzen, 1991; Akhtar & Das, 2019; Croy et al., 2015). Peng and Min (2020) examined the factors that affect 469 US nurses’ intentions to participate in bridge employment or post-retirement work and found that participants’ perceptions of their behavioural control had a significant effect on their intention and actual planning for bridge employment. In another study, Ng et al. (2020) examined the factors that may motivate or hinder the buying intention of a retirement village unit among 261 Malaysian elderly. The findings of the study revealed that perceived behavioural control, subjective norm, attitude, and social sustainability were significant predictors. Similarly, perceived behavioural controls had the largest predictive power in explaining one’s intention to save in a voluntary retirement fund, followed by attitude and subjective norms (van Dam et al., 2009). Therefore, this study proposes:

H7: There is a positive relationship between perceived behavioural control and behavioural intention among working adults.

Perceived Behavioural Control and Financial Behaviour

According to Ajzen (1991), perceived behaviour control and intention work together to produce actual behaviour. Similarly, literature on financial management supports that a higher perception of behavioural control has been associated with an individual’s greater control in performing an intended financial behaviour (Serido et al., 2013). This has been empirically tested and has extended the applications of the TPB to predict saving behaviour (Serido et al., 2013), use of online financial services (Shih & Fang, 2004), stock trading (Raut, 2020), tax filing (Fu et al., 2006) and general financial contentment through financial behavioural performance (Dew & Xiao, 2011). Accordingly, the present study examines how much control individual working adults have on supporting intention to perform intended financial behaviour (retirement planning). Indeed, there have been claims that several forms of responsible financial behaviour in terms of saving habits, budgeting and control depend on one’s perception of control over life and finances (Perry & Morris, 2005). Furthermore, when using the TPB, most studies only examined the function of perceived behavioural control in explaining behavioural intention. Kimiyagahlam et al. (2019) recommended that future studies should examine the influence of perceived behavioural control on financial behaviour in retirement planning. This study, therefore, proposes the following hypothesis:

H8: There is a positive relationship between perceived behavioural control and financial behaviour among working.

Behavioural Intention and Financial Behaviour

Ajzen (2002) has described behavioural intention as an immediate antecedent of behaviour. It is a vital indicator of individuals’ willingness to act on a specific behaviour (Yadav & Pathak, 2017). The behavioural intention in personal finance refers to people thinking of financial management behaviour, such as retirement planning or preference, and such preferences or planning direct impact the decision to retire (Topa et al., 2009). Ofili (2017) found that the behavioural intention of mid-career African American professionals towards participation or nonparticipation in a retirement savings plan was important. Similarly, Croy et al. (2010b) investigated 2,300 retirement savings fund members and their motivations to contribute more to savings and to manage their investment strategy. They discovered that a significant percentage of the variation in financial planning behaviours may be attributed to behavioural intention. In the same vein, Brüggen et al. (2019) highlighted the effectiveness of interactive online pension planners that can enhance one’s attitude, behaviour, knowledge, perceived ease of use, behavioural intentions, usefulness, enjoyment and participation in retirement planning. In addition, Conway et al. (2016) emphasized that financial incentives that nurture succession and retirement from farming foster positive attitudes and intentions amongst elderly farmers, which influence farmers’ concerns regarding the potential loss of identity, status and control upon transferring management and ownership of the family farm and retiring. Hence, this study proposes:

H9: There is a positive relationship between behavioural intention and financial behaviour among working adults.

Methods

Study Design

This study adopted a correlational cross-sectional research design to investigate the predictors of financial behaviour among working adults in Malaysia. Figure 1 shows the proposed research framework based on the TBP (Ajzen, 1991; Ajzen et al., 2011). The online questionnaire was used to collect data. Such a questionnaire-based survey could help to verify the proposed model statistically and form an association between the theoretical proposals and the business scenarios (She et al., 2023). The online survey was conducted in Malaysia from July to October 2021 using google docs. The hyperlink of the self-administrated was disseminated on social media (e.g., WhatsApp, Facebook and LinkedIn). The following inclusion criteria were used to identify participants for this study: (1) those aged 40 years during the baseline survey period and (2) those employed on a full-time basis. The questionnaire consisted of three sections. Participants were asked in the first section of the questionnaire whether they fulfilled the inclusion criteria of the research. Only when they selected ‘Yes’, then they could proceed to the second and third sections of the questionnaire. As for the second section of the questionnaire, the respondents were required to choose the appropriate option for the statements that measure respondents’ financial knowledge, attitude towards retirement, perceived behavioural control, subjective norms, behavioural intention for retirement and financial behaviour. In the third section, respondents needed to fill in their gender, age, marital status, race, education level, job sector and income level. Moreover, to avoid type I or type II errors, this study used a priori sample size estimation to compute the minimum sample size required during the research planning stage (Beck, 2013; She, Rasiah, et al., 2021). Using six latent variables, 30 observed variables, a probability level less than .05, a power level of 0.8, and an effect size of 0.18 (Cohen, 2013), this study needed at least 503 samples to achieve the desired level of power.

Participants

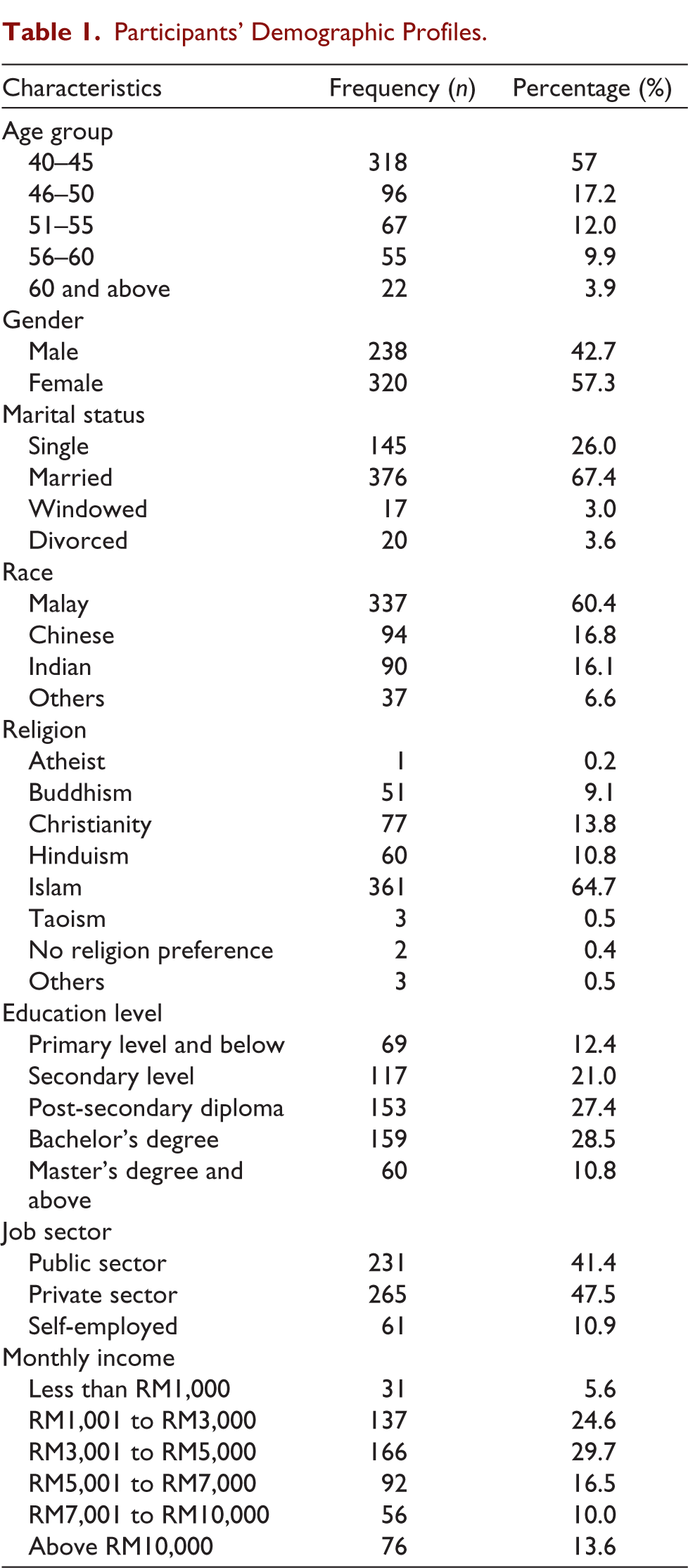

In total, through a purposive sampling technique, 558 participants fulfilled the inclusion of this study. This study’s sample also met the minimum sample size requirement. Moreover, the study’s participants were Malaysian working adults above 40 years old. Most participants were between 40 and 45 years old (57%). The participants included 238 males (42.7%) and 320 females (57.3%). A majority of the respondents were Malays (60.4%), Muslims (64.7%) and married (67.4%) (Table 1).

Participants’ Demographic Profiles.

Measures

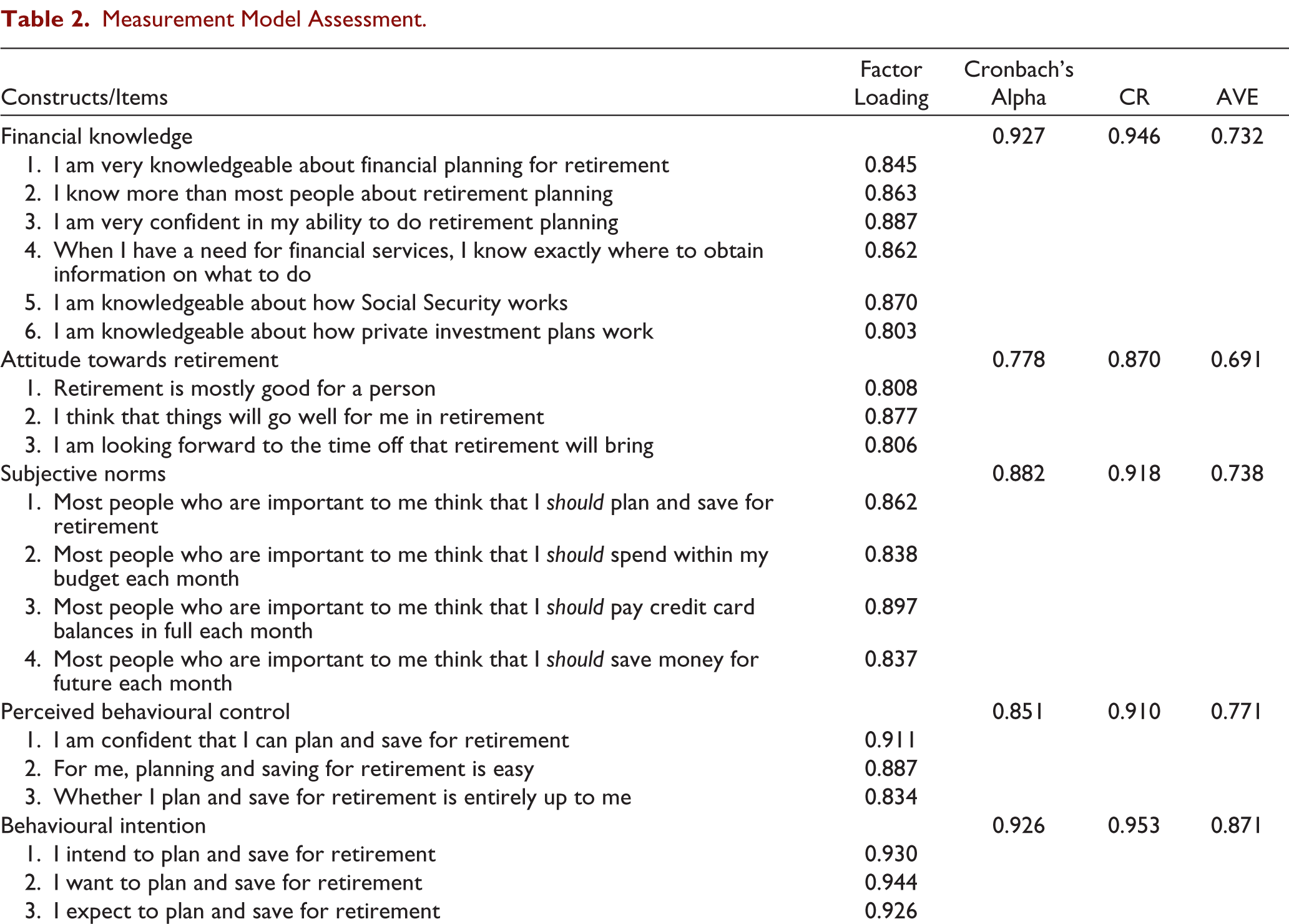

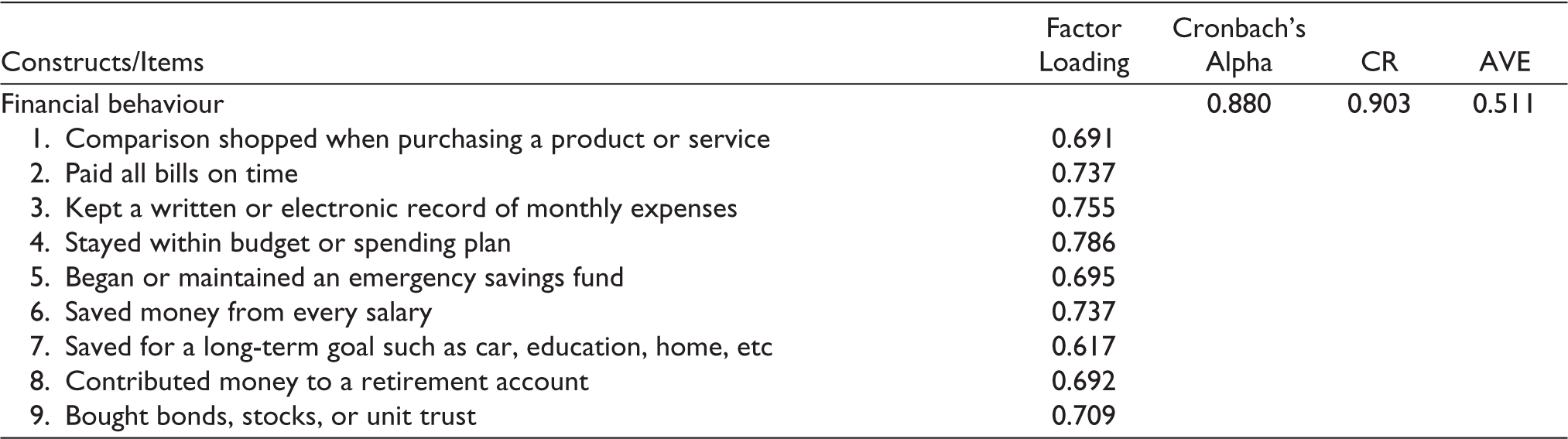

This study adopted a nine-item financial behaviour scale by Strömbäck et al. (2020) to measure financial behaviour. The scale was employed to evaluate the financial management behaviour of the participants (e.g., ‘I keep track of my expense’). This study used a six-item scale adopted from Hershey et al. (2007) to measure respondents’ degree of financial knowledge on retirement (e.g., ‘I am very knowledgeable about financial planning for retirement’). In terms of attitude towards retirement, this study employed the five-item Attitude Towards Retirement Scale developed by Glamser (1976) to measure participants’ attitudes towards retirement. Respondents were asked to indicate their agreement towards each of the five statements (e.g., ‘I am looking forward to (am enjoying) the time off that retirement brings’). Moreover, the four items were adopted and modified by Shim et al. (2009) to measure respondents’ subjective norms towards retirement planning (e.g., ‘Most of the people I care about think I should plan and save for retirement’). Perceived behavioural control for retirement was measured using three items scale by Davis and Hustvedt (2012). The respondents were asked to indicate the extent to which they agreed or disagreed with each statement (e.g., ‘For me, planning and saving for retirement is easy’). Lastly, behavioural intention towards retirement planning was measured using three items by Davis and Hustvedt (2012). The respondents were asked to indicate the extent to which they agreed or disagreed with each statement (e.g., ‘I intend to plan and save for retirement’). A 7-point Likert scale with a range of 1 (strongly agree) to 7 was used to record all of the items (strongly agree).

Data Analysis

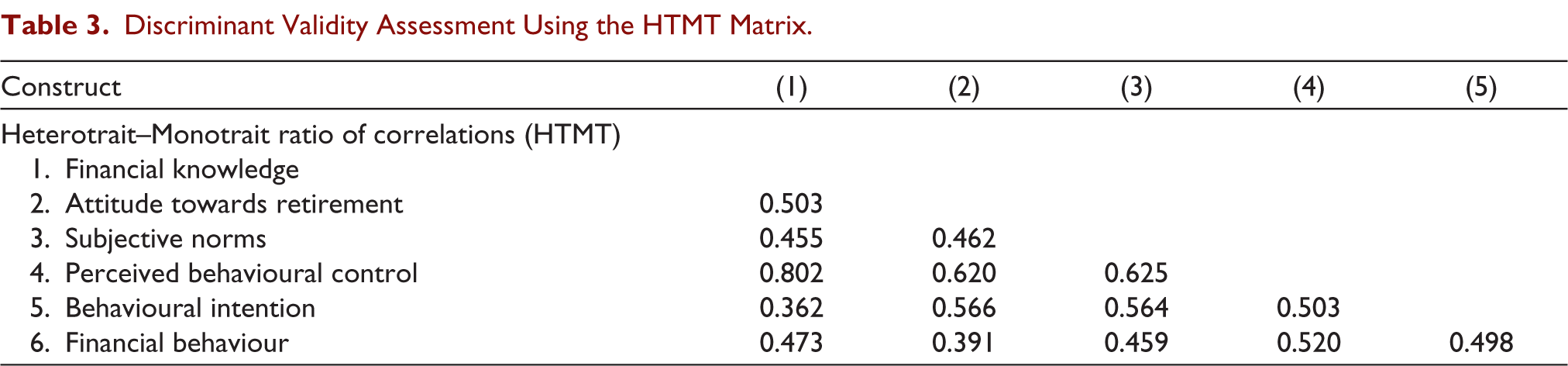

This study applied the partial least squares structural equation modelling and SmartPLS version 4.0 to assess the measurement and proposed structural models. Following a two-step approach suggested by Henseler (2009), a confirmatory factor analysis (CFA) was first performed to assess the measurement model. The SRMR model fit index with a value of less than 0.08 was used to assess the model fit (Henseler et al., 2015). Cronbach’s alpha of more than 0.7 was used to evaluate the construct’s internal consistency (She, Pahlevan Sharif, et al., 2021). Through composite reliability (CR) and average variance extracted (AVE), the construct reliability and convergent validity were also examined (Fornell & Larcker, 1981; She, Pahlevan Sharif, et al., 2021). To achieve good construct reliability, the acceptable value of CR should be 0.7 and above (Pahlevan Sharif & Sharif Nia, 2018). Convergent validity requires that each construct’s CR exceed its AVE and that each construct’s AVE be more than 0.5 (Pahlevan Sharif & Sharif Nia, 2018). Regarding the discriminant validity, all values of the Heterotrait–Monotrait ratio of correlations (HTMT) matrix should be less than 0.85 (Henseler et al., 2015). Next, the structural model was established and assessed using a bias-corrected bootstrapping technique with 5,000 replications. A p-value of less than .05 was regarded as statistically significant, and all tests were one-tailed.

Findings

Common Method Bias

Prior to assessing the measurement and structural models, the common method variance (CMV) was first tested using Harman’s one-factor test (Podsakoff et al., 2003). The findings revealed that the most variance explained by the single factor is 25.85%, less than the cut-off value of 50% suggested by Podsakoff et al. (2003). Furthermore, the variance inflation factor (VIF) was computed to further confirm the absence of the common method bias. The results showed that the VIFs for all constructs (ranging from 1.069 to 1.411) were less than the suggested cut-off value of 3.3 for the common method bias test (Podsakoff et al., 2003). It follows that there is no reason to be concerned about common method bias in the current study.

Results of the Measurement Model Assessment

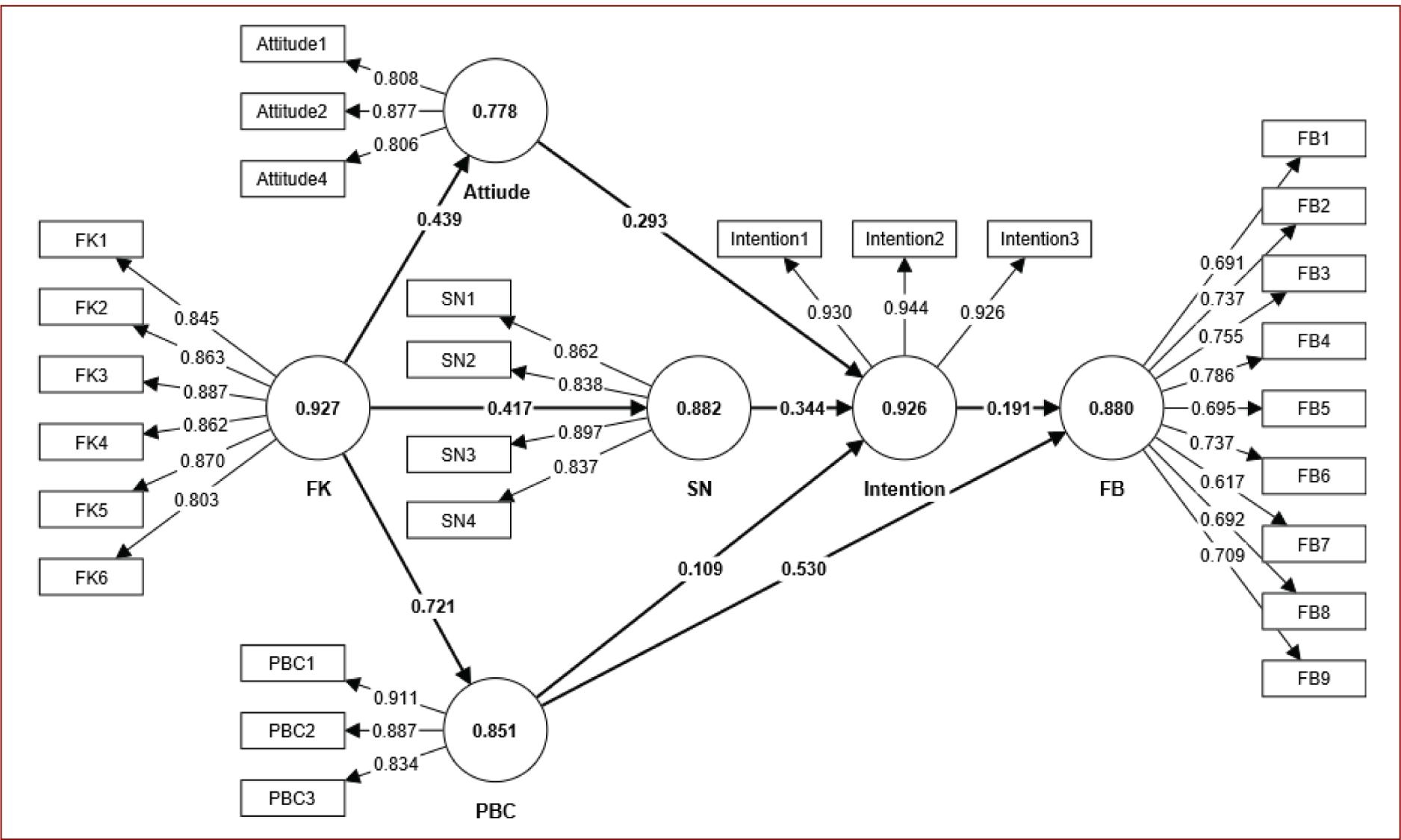

The CFA results revealed that the measurement model fits the data well (Henseler et al., 2015), as evidenced by the value of SRMR being less than 0.8 (0.053). Furthermore, item 3 and item 5 of the attitudes towards retirement were removed as their factor loadings were less than the recommended value of 0.5 (She, Pahlevan Sharif, et al., 2021). All factor loadings of the items in the final measurement model were greater than 0.5 (Figure 2). All constructs have Cronbach’s alpha values of more than 0.7, as shown in Table 2, demonstrating strong internal consistency (She, Pahlevan Sharif, et al., 2021). Moreover, the CR for all constructs was more than 0.7 demonstrating good construct reliability. Each construct’s AVE was higher than 0.5 and less than its CR, demonstrating good convergent validity (Fornell & Larcker, 1981; She, Pahlevan Sharif, et al., 2021). Finally, all values of the HTMT matrix were less than 0.85 (Table 3), establishing the discriminant validity of all constructs (Henseler et al., 2015).

The Results of the Measurement Model Assessment.

Measurement Model Assessment.

Discriminant Validity Assessment Using the HTMT Matrix.

Results of the Structural Model Assessment

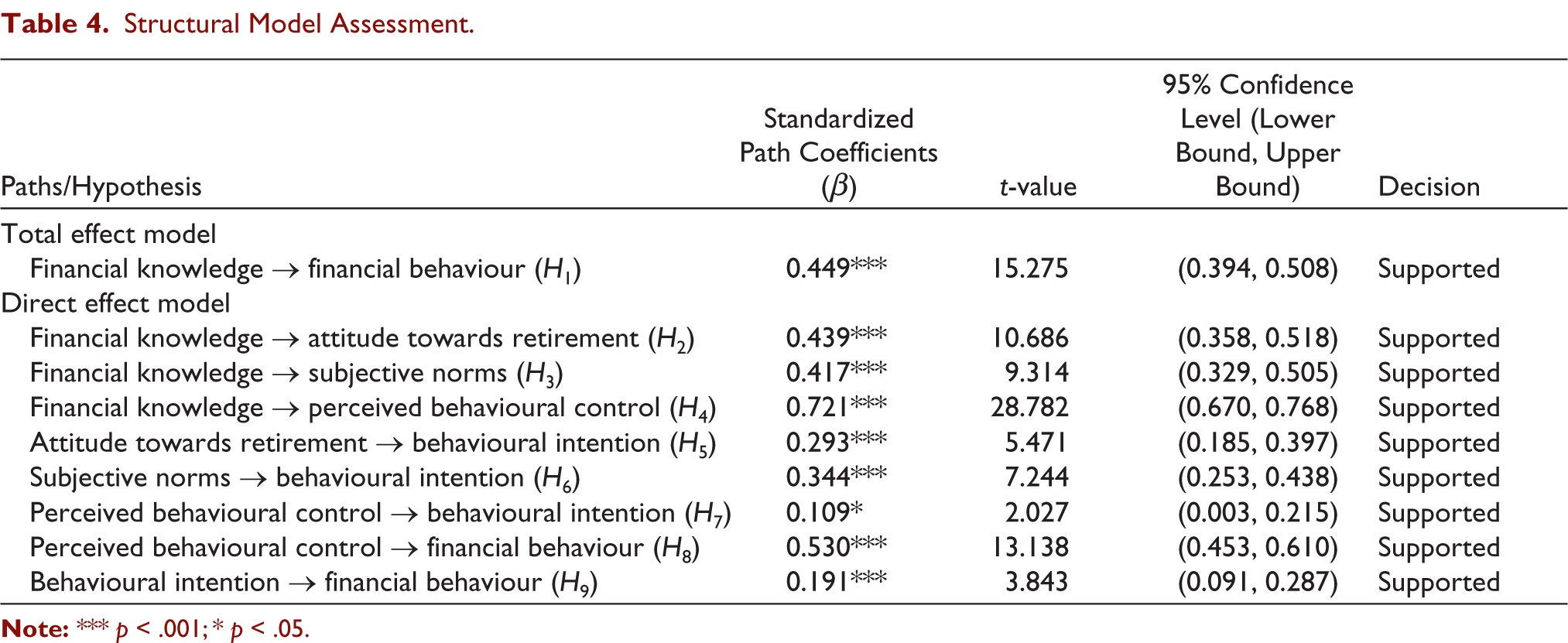

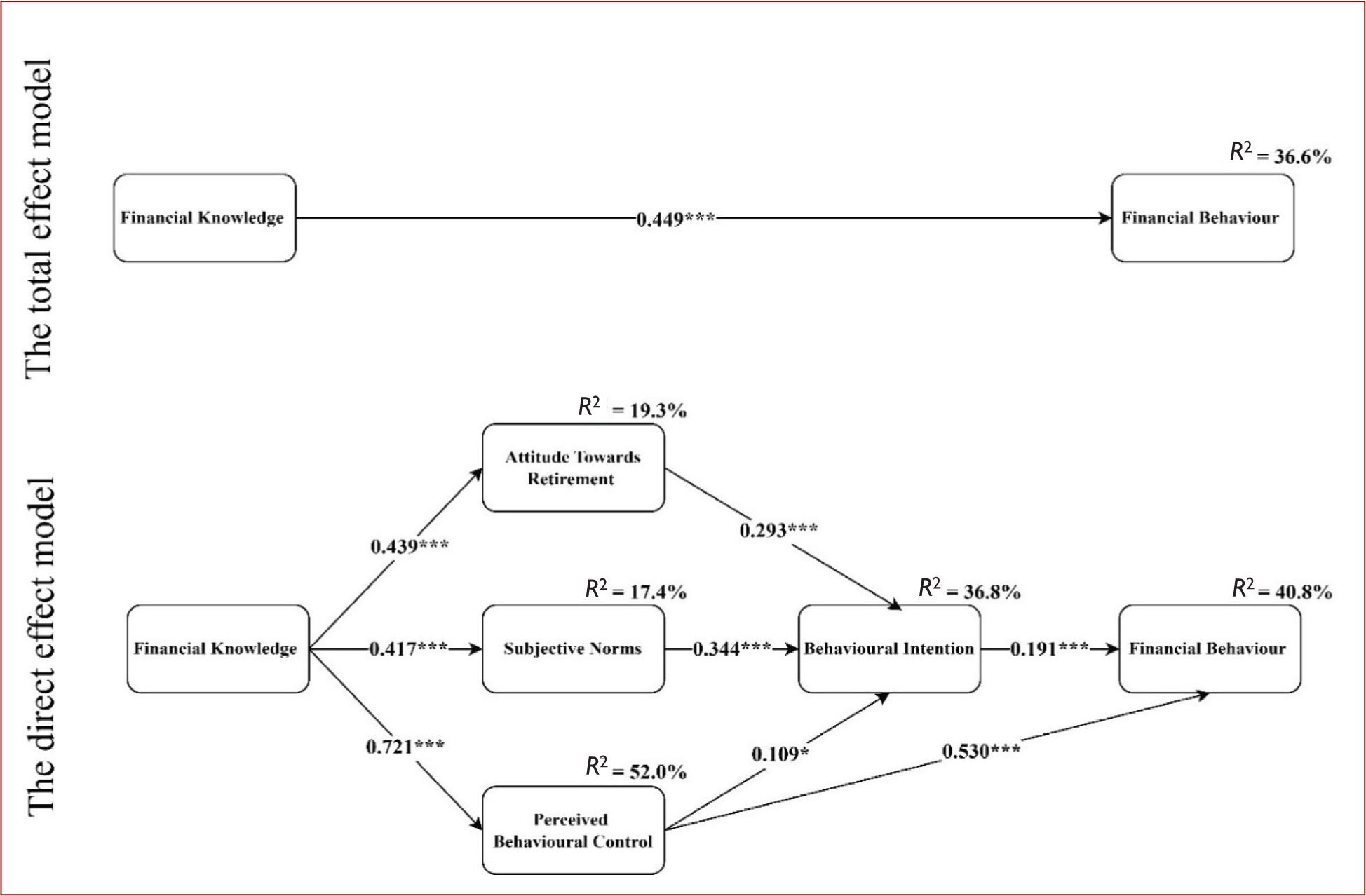

Next, this study assessed the proposed structural model and tested the developed hypotheses. As shown in Table 4, assessing the total effect showed a positive relationship between financial knowledge and financial behaviour (β = 0.449, t-value = 15.275, p < .001), which supported H1. The total effect model explained 36.6% of the total variance of financial behaviour. Moreover, the findings of the structural model’s assessment of the direct effects revealed the positive relationships between financial knowledge and attitude towards retirement (β = 0.439, t-value = 10.686, p < .001), financial knowledge and subjective norms (β = 0.417, t-value = 9.314, p < .001), and financial knowledge and perceived behavioural control (β = 0.721, t-value = 28.782, p < .001), providing supports of H2, H3 and H4. Moreover, the results of this study provided support for H5, H6 and H7 on the positive relationship between attitude towards retirement (β = 0.293, t-value = 5.471, p < .001), subjective norms (β = 0.344, t-value = 7.244, p < .001) and perceived behavioural control (β = 0.109, t-value = 2.027, p < .05) with behavioural intention. Finally, the findings reveal that perceived behavioural control (β = 0.530, t-value = 13.138, p < .001) and behavioural intention (β = 0.191, t-value = 3.843, p < .001) positively related to financial behaviour, thus supporting of H8 and H9. The model explained 40.8% of the variance of financial behaviour, 36.8% of the variance of behavioural intention, 19.3% of the variance of attitude towards retirement, 17.4% of the variance of subjective norms, and 52.0% of the variance of perceived behavioural control. Figure 3 provides a snapshot of the overall results of the structural model assessment.

Structural Model Assessment.

Discussion

Drawing upon the TPB, this study investigated the influence of financial knowledge, attitude towards retirement, perceived behavioural control and subjective norms on behavioural intention and financial behaviour among working adults. In a world of global uncertainties, individuals face increasing financial challenges due to significant global transformations in financial markets. Financial planning has greatly advanced, making wealth management a fairly complex procedure. For most people, shouldering the burden of responsibility for their financial behaviour has resulted in many feeling financially and mentally stressed.

This research’s findings reveal that financial knowledge has a positive relationship with financial behaviour among working adults in Malaysia (H1), which indicates that working adults with greater perceived financial knowledge tend to practice more responsible financial behaviour. The result aligns with previous studies stating that working adults with more financial knowledge demonstrate better financial behaviour (Niu et al., 2020; She, Rasiah, et al., 2022; Tomar et al., 2021), such as saving and investing. Lusardi and Mitchell (2014) revealed that financially savvy people were more likely to accumulate wealth because they acquired more financial knowledge, gaining more confidence to apply their knowledge to manage their finances better. The positive relationship between financial knowledge and financial behaviour provides greater insight into the complexity of human behaviour. The nexus of knowledge-to-behaviour indicates the pertinence of providing adequate financial education to people, as it encompasses the process of obtaining general financial knowledge, personal financial awareness, and financial skills. Although insufficient, financial knowledge is a necessary component for financial behaviour change (Klapper & Lusardi, 2020).

This study also found a significantly positive relationship between financial knowledge with attitude towards retirement (H2), subjective norms (H3) and perceived behavioural control (H4), respectively. The findings reveal the importance of providing people with more opportunities to improve their financial knowledge as it enhances their behavioural domains (Radianto et al., 2021). Hence, this allows them to make sense of economic and financial information and make informed decisions about managing their finances (Lusardi & Mitchell, 2017). Specifically, individuals with a greater perceived level of financial knowledge have a more optimistic attitude towards retirement. Individuals demonstrate a good attitude towards saving and investing due to greater opportunities and higher confidence to invest and save, which enables them to prioritize their retirement savings (Lusardi & Mitchell, 2017). In addition, it was also found that subjective norms were positively influenced by financial knowledge, aligning with the argument that high levels of financial knowledge enhance the benefits of savvy financial management social norms among social groups (Ameliawati & Setiyani, 2018; Goyal & Kumar, 2021). With increased levels of financial knowledge, working adults in the pre-retirement stage tend to have stronger beliefs that an important person or group would approve and support a particular financial behaviour which may be good for their retirement planning (Ajzen, 1991). Understandably, having greater financial knowledge tends to improve subjective norms, as the higher levels of financial knowledge enhance the ability of important others to counsel or advise one on the need to improve one’s financial behaviour and basic money management skills (Akhtar & Das, 2019). Moreover, the positive financial knowledge-perceived behavioural control nexus is not surprising, as it is in line with the earlier study by Serido et al. (2013). Individuals with greater levels of financial knowledge would grasp the repercussions of overspending and not saving or using money sustainably. This ties in with people’s perceived behavioural control. Being equipped with good financial knowledge enhances the level of control individuals exert on their behaviour in terms of managing their finances better (Serido et al., 2013).

Moreover, the study’s findings revealed positive relationships between attitude towards retirement (H5), subjective norms (H6) and perceived behavioural control (H7) with behavioural intentions. The findings are aligned with the TPB and support the TPB regarding retirement planning, where individuals’ behavioural intention for retirement planning is shaped by their attitude, subjective norms and perceived behavioural control (Ajzen, 1991, 2015). Indeed, when people have a favourable outlook on retirement planning, their intention to engage in retirement planning behaviours such as saving and investing becomes higher (Hoffmann & Plotkina, 2020; Lim et al., 2018). The support, approval and perception of potential reference groups such as spouses/partners, family members, coworkers and friends/peers all play a significant role in shaping working adults’ intention to plan for retirement (Ajzen, 1991). However, the results showed that working adults who perceived they had more control over their finances had a higher intention to plan for retirement. The results concur with previous studies, revealing that perceived behavioural control is likely to be a significant predictor of behavioural intention in retirement planning (Akhtar & Das, 2019; Croy et al., 2015; Ng et al., 2020).

Lastly, this study found that perceived behavioural control (H8) and behavioural intention (H9) had a positive relationship with financial behaviour among working adults. The results are aligned with earlier findings stating that individuals with a higher ability to control their finances (Griffin et al., 2012), and a higher tendency of behavioural intention for retirement planning (Croy et al., 2010b; Hoffmann & Plotkina, 2020), are demonstrating better financial management behaviour. The results also align with the TPB, which postulates that the combination of behavioural intention and perceived behaviour control ultimately results in the actual behaviour being conducted (Ajzen, 1991), where actual behaviour refers to the financial behaviour of working adults. It is to say that the perceived behavioural control and behavioural intention for retirement preparedness among working adults are evidenced as an alternative measure of financial behaviour. Individuals need to improve how they manage their finances and consider retirement preparedness ahead. Such ability and intention may assist them in making better financial decisions that will directly affect their financial future in retirement.

Implications

Theoretical Implication

The research’s findings have several theoretical and practical implications. The TPB has been used in retirement planning before, but this study is the first to provide theoretical justification for its expansion to incorporate financial knowledge as the starting point of the original model. The results also supported the important role of financial knowledge in determining working adults’ financial motivators (e.g., attitude, subjective norms and perceived behavioural control) and financial behaviour towards their retirement planning, offering new insights when applying the TBP in retirement planning and personal finance. The present study supports the rhetoric that there is a positive relationship between financial knowledge and financial behaviour, whereby age acts as a catalyst that prompts working adults aged 40 years and above to consider personal finance and retirement preparedness readily. It is one of the first analyses that shows that planned retirement is increasing in a developing country and provides necessary context as to how national citizens in their older age view retirement planning. This study’s examination of the research model elucidates the crucial part that working adults’ financial knowledge plays in the success of their retirement plans.

Managerial Implication

This research has important practical implications for Malaysia since it draws attention to the need for workplace financial education and financial interventions. First, the efforts to enhance working adults’ financial knowledge through financial education programmes are indeed recommended to help working adults improve their financial capability towards retirement planning. In this regard, adequate and easily accessible financial education programmes should offer in the workplace through the collaboration between private, public and non-profit organizations. Second, the present study acknowledges the important role of motivational factors in retirement preparedness. Policymakers in Malaysia should also focus on developing the working adults’ financial values and beliefs through financial interventions since many of the existing financial programmes (e.g., Malaysian Financial Planning Council’s [MFPC] financial education programmes) with little or no emphasis on financial empowerment. In Malaysia, there is increasing evidence of the lack of financial values and beliefs in financial education programmes, which is believed to be a reason for the lack of improvement in financial behaviour among working adults (Farrell et al., 2016; She, Rasiah, et al., 2022). Lastly, employers play an essential role in keeping their employees financially informed. They may engage with external financial counsellors or financial planners to offer advisory services to enhance the employees’ awareness of how important retirement preparedness is, and how to develop positive financial beliefs that can provide for a secure financial future. As working adults account for a sizable proportion of Malaysians, this study is both topical and pertinent. It provides significant insights for policymaking and may be applied to the design and implementation of workplace financial education programmes aimed at enhancing working adults’ financial capabilities in retirement planning.

Limitations and Future Directions

While the study provided significant insights into the important role of workplace financial education programmes in enhancing working adults’ retirement planning, it is not without limitations. First, the study’s sample of working adults in Malaysia may not fully reflect the working adult population as a whole, which limits the results’ generalizability. More representative samples from various social and macroeconomic contexts should be collected for future studies. Moreover, the self-administrated questionnaire may be subject to exaggeration and lead to social desirability bias. Next, the cross-sectional research design could not effectively assess the causal inferences. Thus, future studies may use longitudinal or experimental design to provide causal evidence to concur with the findings of this research. Lastly, it is suggested that future studies shall further investigate and link the current research model with the different populations (e.g., single mothers) and contexts (e.g., credit card repayment behaviour), as suggested by previous studies (Aw & Sabri, 202; Hamid & Loke, 2021).

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.