Abstract

Islamic law prohibits Muslims from investing in certain businesses such as banking, alcohol, and speculation. As such, Islamic investment is different from traditional investment, as investment principles emphasize ethical investing and compliance with Shariah, the Islamic rule that controls every aspect of a Muslim’s life. However, a fair review of the literature failed to find any questionnaire to measure Islamic investor sentiment. In order to create and standardize a technique to gauge Islamic investors’ attitudes about share market investment, a research was conducted. Islamic investors’ attitudes were the dependent variable, while the study identified Islamic investing ethics, religious considerations, profitability, social impact, and information accessibility as independent variables. Python programming was used to evaluate the data gathered from 391 respondents using a 24-item structured questionnaire. According to the study’s findings, each of the characteristics has a big influence on how Islamic investors feel. Furthermore, this study shows that participation in religious activities elevates the spirits of Islamic investors. The verified Islamic investor’s feelings questionnaire in this study is expected to inspire more investigation in this fascinating field.

Introduction

Investor sentiment (IS) has a substantial impact on price dynamics in the stock markets (Baker & Wurgler, 2006; Gong et al., 2022; Ho & Hung, 2009; Jing et al., 2021; Naeem et al., 2021). The irrational and systematic bias of the market has a significant influence on stock returns. It also represents the expectations of investors toward the financial markets. The amount and scope of financial activities categorized as “Islamic finance” have increased during the past several years (Khan et al., 2021). An international competitor to traditional financial intermediaries is this burgeoning financial industry (Jaziri & Abdelhedi, 2018; Saleem et al., 2021). Islamic investment is different from conventional investment in that Muslims are not allowed by Islamic law to speculate, receive or charge interest, or participate in some businesses, such as those that manufacture alcohol. According to Misra et al. (2019):

Islamic finance is thought of as a big money pot with nothing better to do than toss money around aimlessly. That is not the case, though. Investors in Islamic financial goods are highly educated, knowledgeable consumers who understand the market and spreads. The idea that money is easy to get by there is untrue.

Islamic equity funds, like conventional mutual funds, invest in the stock market on behalf of Islamic investors (Peillex et al., 2019). Islamic financial organizations were established with the use of contemporary financial institutions, markets, and commodities. In India, there are 177 million Muslims, or 12% of the whole population (Kalimullina & Orlov, 2020). A number of investment products have been created using Islamic banking and financial principles (Khan et al., 2019; Nawi et al., 2018). The usage of derivatives, forward, swaps, and futures is likewise prohibited under Islamic law. Additionally, day trading, chopping, leverage trading, and long- and short-term trading are all forbidden (Kumar & Sahu, 2017). Islamic investment is sometimes referred to as “ethical investing,” “faith making investments,” and “socially responsible investing” because of its roots in Shariah principles (Bordoloi et al., 2020; Sulphey, 2015). One of the most crucial aspects of investing in Islamic stocks is using Shariah screening criteria to evaluate if companies and shares are compliant with Islamic law (Derigs & Marzban, 2008). Businesses that engage in prohibited behavior under Shariah law, such as those who deal in the exchange of gold and silver, interest-bearing loans, alcohol, obscenity, gambling, and cigarettes, are likewise excluded. Furthermore, businesses with capital structures that are more debt-heavy—often greater than one-third of total capital—should be ignored (Ho & Mohd-Raff, 2019; Naim et al., 2020; Osman et al., 2016). Several nations, including India, collaborated to build the Shariah-compliant in stock market index, which follows Shariah stock screening guidelines (Natarajan & Dharani, 2012). The Bombay Stock Exchange (BSE) and the National Stock Exchange (NSE) have developed and calculated Islamic indices based on Shariah, promoting the use of Shariah-compliant finance in the Indian economy (Bordoloi et al., 2020). Shariah-compliant finance has drawn a lot of attention recently and is affecting the Indian financial sector more and more. Therefore, it is essential to analyze Indian Muslims’ equities market investing behavior in light of Shariah principles in light of the establishment of Shariah-based BSE and NSE Islamic indexes (Irfan, 2021; Nihar & Modekurti, 2021; Sahu et al., 2009).

The study’s objective is to develop and validate the potential measures to analyze the Islamic investor sentiments (IIS) on the stock market. Islamic investment principles strongly emphasize ethical investing that complies with Shariah, the Islamic rule that controls every aspect of a Muslim’s life. These investments are also referred to as Shariah-compliant investments. Investments in financial instruments that have a fixed income, such as preferred stocks, bonds, and some derivatives and options, are unsuitable since they guarantee a set rate of return while granting no voting rights (Haseeb et al., 2022). Additionally, Islamic investors are not allowed to buy the stock of businesses primarily engaged in selling alcohol, gambling, traditional financial services, entertainment, and products connected to pork, cigarettes, and weapons (Narayan et al., 2021). Furthermore, organizations have been screened using specific financial ratios (Tajuddin et al., 2018). For instance, Haseeb et al. (2022) investigated that stocks are not Shariah-compliant when corporate debt levels exceed one-third of market capitalization. The portfolio is subsequently purified to get rid of interest income and other illegal sources of income (Alsartawi et al., 2021; Sabtu et al., 2018).

The relationship between investor attention and the Islamic stock market is particularly significant because, at least theoretically, Islamic finance has built its ethical investment rules in accordance with Sharia-compliant investors’ principles, whereas conventional investors or speculators might act differently, occasionally engaging in mispricing activities in order to maximize their profits (Adekoya, 2022; Albaity et al., 2022; Chowdhury et al., 2022; Ftiti & Hadhri, 2019). The effect of IS on the Islamic stock market will differ depending on the prominent players in light of this and the fact that investors come in many shapes and sizes (Khan et al., 2019). According to Shariah law, immoral investors who operate only as drivers of conventional stock markets or investor attention in line with the stabilizing actions of ethically oriented investors can both influence the dynamics of the Islamic stock market (Alhomaidi et al., 2018; Amalia & Saputri, 2022; Khan et al., 2019).

The objective of this article is to investigate and validate the potential measures to understand the sentiment of Islamic investors toward share market investment. In this study, we included Islamic investment ethics (IIE), profitability (PRO), religious factors (RF), social influence (SI), and information availability as independent variables, while dependent variables included IIS. The next section focuses on literature review based on the included variables in the study.

Literature Review

Islamic Investor’s Sentiments

The relationship between sentiment of the investors and stock returns and performance has been the subject of extensive study (Abbes & Abdelhédi-Zouch, 2015; Adam et al., 2022; Aloui et al., 2021; Di et al., 2021). Brown and Cliff (2005) examined how an investor behavior affects collection and portfolio cross-sectional lot size and book returns to market returns. They found that large organizations are more susceptible to corporate sentiment than small companies. The stock performance may be explained by Islamic investor attitudes, suggested by Septyanto et al. (2021) and Di et al. (2021). Investor gloom and cross-section returns have a considerable negative association, according to Baker and Wurgler (2006). Stocks of small-cap companies are very volatile.

Theoretically, there are two complementing grounds for both emotion and Sharia-compliant stock returns (volatility). The first point is that investors with a religious stance and stringent, ongoing Sharia supervision are present in Sharia indexes. This may prevent sentiment-driven mispricing and prevent Islamic stocks from tending toward sentiment. Second, the Sharia-screening procedure (qualitative and quantitative) may make stocks more susceptible to limit arbitrage and short-selling impediments (Miller, 1977), which could mean that Sharia stocks are more susceptible to being influenced by noise traders who diverge their prices from fundamentals over the long term. To ascertain whether active Shaira monitoring and faith-based investing are anticipated to have more influence on the volatility of Islamic stock returns, this supplementary claim has to be empirically investigated.

Researchers have recently become interested in researching investor mood and stock performance because to the complementing arguments surrounding Islamic stocks and emotion. For addition, Narayan and Bannigidadmath (2017) examined the impact of financial news on Islamic stock returns using sentiment-induced keywords. In contrast to non-Islamic equities, their findings showed higher predictability of sentiment-induced phrases in Islamic stocks. However, the emotion sensitivity and return volatility of Sharia-compliant equities have received little attention (Perez-Liston et al., 2014). For example, Perez-Liston et al. (2014) examined the impact of IS on the returns and volatility of Islamic stocks and discovered that stronger sentiment in the immediate term is associated with reduced implied volatility in the next period. Similar to this, Wasiuzzaman (2018) investigated the impact of Hajj pilgrimage sentiments on the Suadi stock market’s return volatility. His research showed a strong inverse correlation between emotion and return volatility.

The correlation among non-dividend-paying equities, common shares, unprofitable stocks, extreme-growth companies, and distressed stocks is greater. When investor mood is low, there is a negative association between volatility and returns, according to research by Trichilli et al. (2020) and Yang and Wu (2011). The empirical evidence shows that sentiment assessments have a big impact on returns, and returns have a big impact on sentiment changes (Adekoya, 2022; Albaity et al., 2022). According to the existing literature review and research gap, IIE, SI, RF, availability of information (AOI), and PRO were identified as major factors that influenced IIS toward share market investments.

Islamic Investment Ethics

The Qur’an, which Muslims believe was inspired to Muhammad in 7th Arabia, and the sunnah, which are the Prophet Muhammad’s documented sayings and acts, serve as the foundation for the Islamic ethical system (Abbasi & Raj, 2021; Denny, 2022; Saeed, 2006). Islam’s objectives are not just purely materialistic (Chapra, 1992). According to this reasoning, investing in Islam is just investing morally. Islamic investment, however, is more complicated than it first appears since it also needs to take into account the holy Qur’an’s restrictions on what is and is not permitted. (Adekoya, 2022; Chong et al., 2008). Concerns exist, nevertheless, regarding the funding sources that will be employed. This is due to the need on the part of every Muslim to ensure that her/his money always comes from “clean” sources (Beekun, 1997). According to Kolk et al. (2004), any financial organization that adheres to a universally accepted code of ethics is ethical.

Due to the fact that halal investing is founded on religious conviction, all investments must adhere to Shariah laws. Therefore, halal investment must adhere to Shariah rules, which state that it must be free of aspects that are forbidden under the law, such as riba (interest), maysir (gambling), and gharar (uncertainty) (Abbasi & Raj, 2021). The Quran specifically forbids riba or interest. In essence, riba is the extra cash provided to the lender by the borrower in addition to the principal in exchange for using the lender’s funds for a specific length of time. Financial goods with the element of riba, such as equity loans, securities, private debt securities, and money market transactions, are therefore seen as being prohibited (haram) (Saeed, 2006).

Maysir, which literally translates to “a method of effortlessly getting something and generating unjust profit,” are motivated only by chance (Abbasi & Raj, 2021). Gambling, which is a game based on chance, frequently causes people to take huge risks and act recklessly in an effort to win big. Islam forbids taking extremely high risks without knowledge or value-adding components because of the potential for financial loss (Abbasi & Raj, 2021). Gharar generally refers to contractual provisions that are unclear and may be exploited or misrepresented, which may result in conflicts and contract manipulation. Halal investment is founded on the idea that Islam forbids doing business with any non-permissible (haram) activities, such as liquor, wine, adultery, gambling, cigarettes, traditional banking, finance and insurance, and pork, in addition to the three banned items. Shares in corporations that have any of the forbidden features are, therefore, seen as being against Shariah (Saeed, 2006).

Contrarily, ethical investing entails combining one’s own moral principles with societal issues when making financial decisions. Ethical investing takes into account an investor’s financial demands as well as the effects of their investments on society at large (Abbasi & Raj, 2021). Applying moral and social standards to the selection and administration of investment portfolios is known as ethical investing. Investors are worried about the traits of the businesses in which their money is invested as well as the investment rewards of their investments and the dangers associated. This comprises the type of products or services the firm offers, where it is located, and how it manages its affairs and commercial operations (Saeed, 2006). Based on the above factors, following hypothesis was framed.

H1: IIE has a positive and significant impact on the IIS.

Religious Factors

Islamic law encompasses all facets of business, finance, law, politics, and the government and its several branches, as well as social, moral, and religious issues including morality and social justice (Asutay, 2007; Iqbal, 1997; Ramazanova et al., 2022). Due to the fact that Islam regulates every aspect of a believer’s personal and professional life, shariah has traditionally set rules for the financial markets. Riba, interest, and usury are prohibited in Islam because they constitute a declaration of war against the Almighty Allah and His Messenger (Muhammad, peace be upon him) Al-Bakara Sura (2:279) (2:279) (Adekoya, 2022; Ahmad & Humayoun, 2011; Ahmad et al., 2010 Shaikh et al., 2021). Riba is the name for every additional cent that is contributed to the principle amount due to any other benefit associated with this transaction. Islamic and traditional banking have different goals, interest-based transactions, and risk-sharing structures. Based on the above factors, following hypothesis was framed.

H2: RF have a positive and significant impact on the IIS.

Profitability

According to Sura-e-Al-Bakara, all types of usury, interest, and riba are prohibited in Islam since doing so would be the same as declaring war on Almighty Allah and His Message (Muhammad, peace be upon him) (2:279) (Ahmad & Humayoun, 2011; Fajri et al., 2022). Riba is the name for any additional cent that is added to the principal amount of any other benefit associated with this transaction. The goals, risk-sharing arrangements, and interest-based transactions between Islamic and conventional banking are unlike (Ahmad et al., 2010; Osmanovic & Alvi, 2022). Diversification resulted in worse PRO and higher expenses, according to Berger et al.’s (2010) examination of a panel data of 88 Chinese banks between 1996 and 2006. According to Maudos (2017), increasing the share of non-interest revenue has a negative impact on PRO. Li and Zhang (2013) illustrated the advantages of diversification that result from increasing non-interest revenues by using information from Chinese banks between 1986 and 2008. Because non-interest income is more irregular and cyclical than net interest profits, relying on it more could increase the risk/reward trade-off. Non-interest operations do not improve banking performance in banks from 22 Asian nations, claim Lee et al (2014). Elsas et al. (2010) discovered that diversity boosts bank PRO rather than decreases shareholder value using banking data from Australia, France, Canada, Germany, the United Kingdom, Italy, the United States, Switzerland, and Spain. Profitability and revenue heterogeneity are connected, claimed by Sanya and Wolfe (2011). According to Saunders et al. (2014), bank income diversification increases US banks’ PRO and decreases their risk of failing (Le et al., 2022). Based on the above factors, following hypothesis was framed.

H3: PRO has a positive and significant impact on the IIS.

Social Influence

Social influence, as according Venkatesh et al. (2003), is the idea that someone must think that others must think that they utilize new services or live up to others’ expectations. Even if a behavior or its repercussions are detrimental to them, people may choose to engage in it if other significant people in their life support them in doing so (Alaiad & Zhou, 2014; Saygılı et al., 2022; Zhao et al., 2014). In fact, whether they agree or disagree, what key others think of a person engaging in a behavior has a big impact on their decision-making. Social influence directly affects the intention to behave (Veerasingam & Teoh, 2022). Social influence has been shown to have a major impact on intention in earlier research (Kijsanayotin et al., 2009; Shahid et al., 2022). The idea is that a person’s behavior is influenced by their family or peers. Based on the above factors, following hypothesis was framed.

H4: The IIS are positive and significant impacted by SI.

The Availability of Information

One of the key elements that may boost the appeal of Sukuk and investors’ choice for Islamic financial products in particular is improved consumer understanding of the differences between Sukuk and traditional financial instruments. Two of the most well-known Islamic personalities in the world are Al-Tamimi and Duqi. It is crucial for Islamic banks to first comprehend their customers’ demands in order to draw in new consumers (Lo & Leow, 2014; Rohmania & Ghoniyah, 2022). The reputation and image of the bank, as well as affordable service fees, are important to customers of Islamic banks (Warsame & Ireri, 2016). There is evidence that information asymmetries are more durable than traditional ties in the case of Sukuk (Klein & Weill, 2016; Sahabuddin et al., 2022). Sukuk instead of bonds may be chosen by businesses with greater information asymmetry to avoid effective market supervision. Investment-grade organizations prefer conventional bonds because they do not wish to share significant profits with Sukuk investors, whereas low-quality enterprises favor Sukuk, according to Godlewski et al. (2016). According to Halim et al. (2017), companies with larger equity and debt agency expenses are more inclined to issue Sukuk than conventional bonds. Based on these factors, we hypothesize the following:

H5: The AOI has a positive and significant impact on the IIS.

The goal of the study was to investigate the connections between Islamic investing ethics, the religious component, financial success, social impact, the accessibility of information, and the attitudes of Islamic investors. At the same time, earlier research had a narrow focus on Islamic investor emotions, PRO, and religious issues. As a result, no research has looked at how IIE, the religious component, PRO, SI, the AOI, and IIS relate to one another. The methodology, scale development, demographic data, reliability, and validity metrics of the study are highlighted in the following section.

Methodology

Scale Development

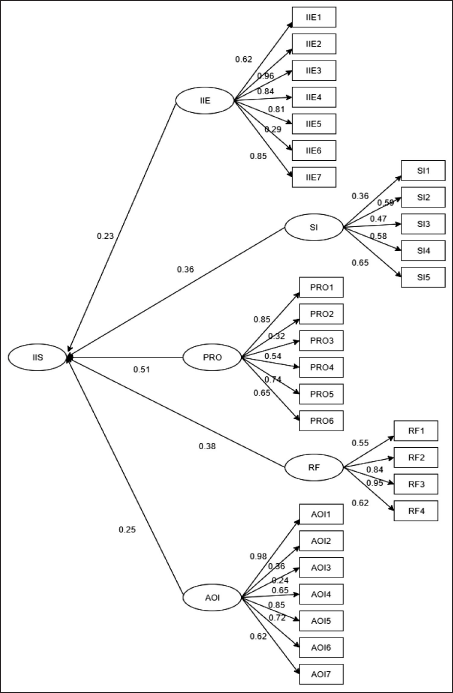

Item creation is the initial phase of scale development (Ftiti & Hadhri, 2019; Sulphey & Jasim, 2020). Following a thorough examination of the literature, many aspects of Islamic investor attitudes were discovered (Aloui et al., 2021), and suitable scales were employed to assess the constructs (Roberts & Lattin, 1991). The topics discussed include IIE, RF, PRO, SI, information availability, and IIS.

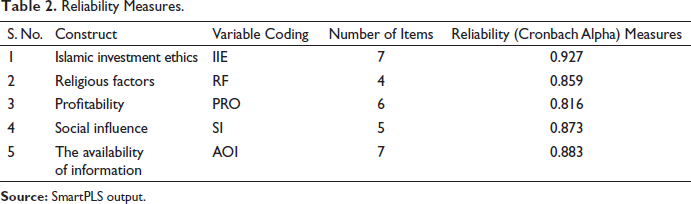

Islamic investment ethics: This variable was measured using the scale with measures created by Talha et al. (2013). Five questions make up the Islamic investing ethics scale, which has been proven to have extremely high internal consistency and great validity with a Cronbach’s alpha measure of 0.86. The indicators “caring,” “instrumental,” “rules,” “law and code,” and “independence” are also included in the study. Religious factors: This variable was evaluated using the Amin et al. (2011) scale. The RF scale consists of four items that are scored on a three-point scale. The scale demonstrated internal consistency and strong validity with a Cronbach’s alpha measure of 0.932. “RF is in keeping with an Islamic notion of performing banking and financial business,” the list reads. “RF is based on Islamic principle for doing business and business transactions.” Religious component introduction is based on Hadith and al-Quran. Profitability: This variable was measured using the questionnaire created by Gait and Worthington (2008). It had a strong validity, an excellent internal consistency, and a Cronbach’s alpha of 0.81. The PRO scale has six components and a five-point scoring system. With a Cronbach’s alpha measure of 0.81 and good robust validity, the internal consistency was high. “Any party to a financial transaction should not be exploited as a consequence of the prohibition of gharar, riba, investing in immoral activities, being socially irresponsible, or having a direct or indirect connection to an actual economic transaction” are among the items listed. Social influence: This variable was measured using a scale developed by Gait and Worthington (2008). The SI scale has six items and a five-point scale. With a Cronbach’s alpha measure of 0.935 and good validity, internal consistency was high. One of the statements made in the list is, “Most people assume I am aware of the need for Shariah, and most people who are close to me believe that I must choose, that others expect me to choose, that most people who are important to me believe that is helpful, that most people who are important to me believe that is beneficial.” The availability of information: To quantify this variable, Duqi and Al-Tamimi (2019) developed a scale. The SI scale has seven items that are scored on a five-point scale. With a solid validity and a Cronbach’s alpha measure of 0.735, the internal consistency was high. “Data analysis tools, the cost and quality of information, the use of financial and statistical tools to handle information, professional businesses that aid in information management, and brokerage firm account coverage are all factors to consider” are some of the topics covered.

Methods

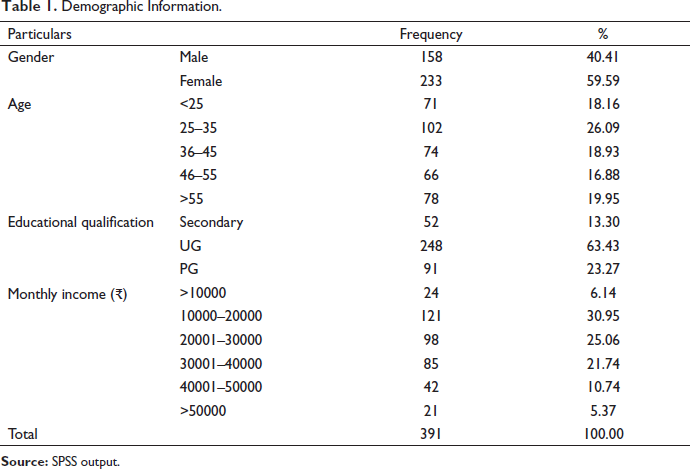

After carefully reviewing the literature on IIE, the RF, PRO, SI, the accessibility of information, and Islamic investor’s attitudes, the research model was developed. Data collection was completed with the help of a structured questionnaire. The data were collected from the Islamic investors from Tamil Nadu, India and samples were identified based on the private share broker databases, referrals, Islamic religious-oriented meetings, and gatherings. Muslims who invest in the stock market were personally given questionnaires. A follow-up call and email were made to encourage participation after 2 weeks. Investors were not obliged to divulge their names or any other personal information in the questionnaire in order to ensure confidentiality. However, specifics such as age, gender, best academic achievement, number of years spent working as a fund manager and the kind and size of the fund being managed were requested. Completed questionnaires were sent to the researchers in addressed, stamped envelopes. In 8 weeks, 391 samples returned the questionnaire. Measurement model and SEM analysis were performed on the gathered surveys using programs namely Python and SPSS. Table 1 displays the sample’s demographic information.

Demographic Information.

To measure the demographic the profiles of the respondents, frequency and percentage analysis were deployed. Male respondents make up 40.41% (158), while female respondents make up 59.59% (233). Less than 25 years old (18.16%), 25–35 years old (26.09%), 36–45 years old (18.93%), 46–55 years old (16.88%), and above 55 years old (19.95%) made up the age range of the replies. With undergraduates making up 63.43% (248) and postgraduates making up 23.37% (91) of the total, 13.30% (52) of the participants were dropouts. Among the respondents, 25.06% (98) earns between ₹20,001 and 30,000, followed by 30.95% (121) who earn between ₹10,000 and ₹20,000. 21.74% (85) make between ₹30,001 and ₹40,000. According to Table 1, 10.74% (42) of the participants earn between ₹40,001 and ₹50,000, while 5.37% (21) earn over ₹50,000.

Reliability and Validity Measures

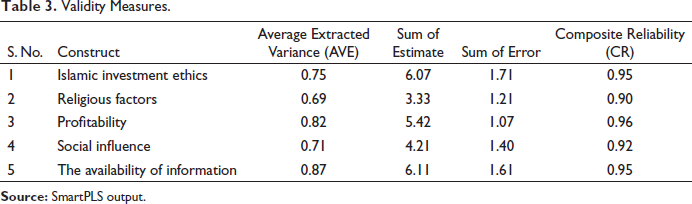

Table 2 displays the study’s validity and reliability metrics. As Kleijnen et al. (2007) suggested, reflective scales were added for all variables in connection with this analysis. Cronbach’s alpha, composite reliability (CR), factor loadings, and average variance extracted (AVE) coefficients were used to analyze the reliability. Based on “where the threshold value is the value of CR, and AVE coefficients values are also larger than 0.50,” all metrics for the factor loadings were 0.70 (Table 2).

Reliability Measures.

Investigations were conducted on the AVE and CR (Anderson & Gerbing, 1988; Hair et al., 2010). All constructions’ CR indices above 0.70, while the AVE indices exceeded 0.50, both falling inside the required range (Anderson & Gerbing, 1988; Hair et al., 2010). Each standardized relapse weight was also higher than 0.50. Regarding discriminant validity, it was discovered that the between-connection of all components was less than the AVE square base for each section (Table 3).

Validity Measures.

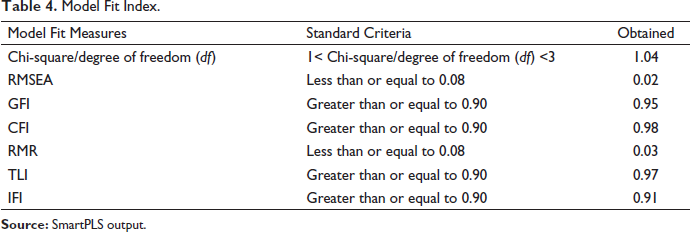

Table 4 displays the fit index. Chi-square/degrees of freedom (CMIN/df), normed-fit index (NFI), comparative fit index (CFI), goodness-of-fit index (GFI), root mean square error of approximation (RMSEA) and adjusted goodness-of-fit index (AGFI) are some widely suggested indices for evaluating model fitness. Initial fit indices for the measurement model (Chi-square/degree of freedom (df) = 1.04561, RMSEA = 0.026, GFI = 0.96, RMR = 0.032, IFI = 0.93, CFI = 0.98, and TLI = 0.98) were found to be within standard levels of prescribed ranges (Anderson & Gerbing, 1988; Bagozzi & Yi, 1988; Byrne & Van de Vijver, 2010). Factor loading and validity measures for each included construct, indicators, and modification factor index were rigorously explored, as suggested by Hair et al. (2006) and Byrne & Van de Vijver (2010).

Model Fit Index.

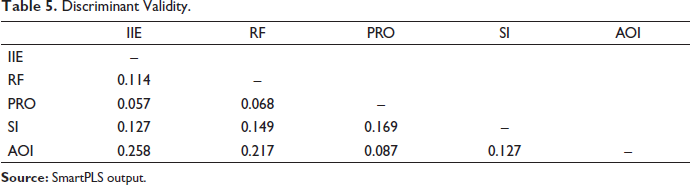

Discriminant validity is used to evaluate the measurement quality of incorporated constructs. Two methods can be used to evaluate discriminant validity. In this study, the Cross Different loading conditions Fornell-Larcker Criterion are used to measure the discriminating validity. Table 5 shows component correlations, the Fornell-Larcker criteria analysis, and the square root of AVE (off-diagonal elements). It demonstrates that the off-diagonal components of the row and column are smaller than the square root of AVE. The findings are all encouraging, indicating that discriminant validity has been established at the concept level. The correlations between both the latent constructs in the matrix are represented by the diagonal values. The next section discusses the results and hypotheses testing of the proposed research model.

Discriminant Validity.

Results

Structural model analysis and measurement model analysis were used to examine the data. Bollen (1989) asserts that this method enables researchers to carry out the necessary route analysis utilizing latent variables. Hwang and Kim (2007) recognized structural model analysis and measurement model analysis as a potent extension of the generic linear model. The measurement model and the structural model were used in tandem to analyze the data in this study. The data were examined using the python (semopy library) program. Python (semopy library) has grown in popularity as a more approachable method for expressing structural models because of its graphical interface. The results are summarized in Table 6.

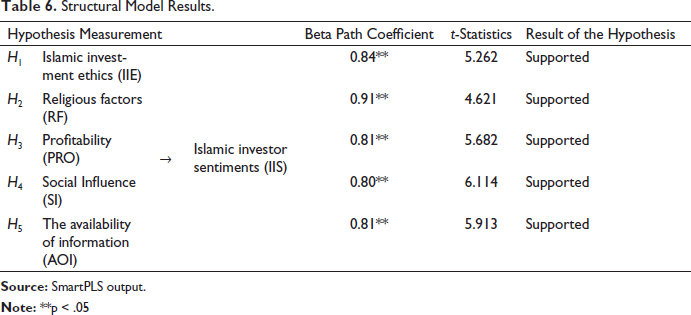

Structural Model Results.

The H1 looks at the relationship between Islamic investors’ attitudes and their investing ethics. The IIS test is used as the dependent variable to assess the Islamic investing principles, which are employed as independent variables. The study’s findings confirmed the hypothesis by showing a statistically significant positive association between Islamic investing ethics and IIS with a t-value of 5.26 (H1). This demonstrates the correlation between greater levels of IIS and higher levels of Islamic investing ethics. The H2 is set up to look at the relationship between religious elements and the attitudes of Islamic investors. The attitudes of Islamic investors are treated as dependent variables in this study whereas religious elements are treated as independent variables. The study’s results supported hypothesis H2 by showing a significant positive relationship between religious characteristics and the attitudes of Islamic investors with a t-value of 4.62. This suggests that more intense religious influences are related to more positive feelings among Islamic investors.

The H3 is set up to investigate the relationship between PRO and investor attitudes among Muslims. PRO is treated as an independent variable in this study, while the attitudes of Islamic investors are treated as a dependent variable. The study’s results confirmed hypothesis H3 by showing a significant positive relationship between PRO and Islamic investors’ feelings with a t-value of 5.68. This suggests that more PRO and more positive attitudes among Islamic investors are related.

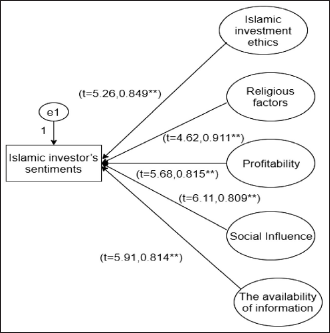

The H4 is set up to investigate the relationship between SI and investor emotions among Muslims. In this study, SI is seen as an independent variable and investor attitudes among Islamic investors as a dependent variable. The study’s conclusions demonstrated a strong positive relationship between SI and the attitudes of Islamic investors, supporting hypothesis H4 with a t-value of 6.11. This suggests that more social impact and more positive investor emotions among Muslims are related. The H5 is then developed to investigate the relationship between information accessibility and investor attitudes among Islamic investors. The AOI is considered an independent variable in this study, whereas the attitudes of Islamic investors are considered a dependent variable. The study’s results confirmed hypothesis H5 by showing a significant positive relationship between the AOI and IIS with a t-value of 5.91. This shows that there is a correlation between increased investor mood among Islamic investors and increased information availability (Figure 1).

The measures of latent variables PRO (0.815, p < .001), SI (0.809, p < .001), IIE (0.849, p < .001), and the AOI are shown to impact IIS (0.814, p < .001). As a result, every concept met the requirements for validity and reliability (Figure 2).

The study’s findings indicate that when choosing firms on the stock market, Islamic investors’ attitudes are most influenced by Islamic investors investment ethics (IIE), the PRO, RF, SI, and the AOI. The next section focuses on the discussions of the study.

Discussion

Islamic investing ethics, religious considerations, PRO, social impact, and the accessibility of information are taken into account as major aspects in the development and potential validation of the ideal Islamic investor’s feelings scale for stock markets. The purpose of the study was to ascertain whether or not Islamic investors chose to engage in the stock market and how they feel about doing so (Duqi & Al-Tamimi, 2018). Each and every industry in the globe is controlled by laws and regulations. As a consequence, while designing and implementing policies and regulations to enhance the feelings of Islamic investors, policymakers and regulators should take into account the information provided by this study concerning the sentiments and perceptions of Islamic investors.

The current work has theoretical implications and adds to the body of knowledge. This study enhanced current knowledge of the importance of Islamic sentiment while choosing companies for the stock market. By establishing a set of five crucial features that should be taken into consideration, the comprehensive analysis of this study added to the body of current research to measure the relationship among IIE, SI, the AOI for IIS. In addition, the study supported other studies’ findings that highlighted the significance of particular traits for Islamic investors’ sentiments. The next section provides the implications of the study.

Implications

Islamically considered, stock trading is allowed. These securities must, however, adhere to Shariah law. Muslims think that trading stocks on the stock market is equivalent to gambling and is thus forbidden. This assumption is false. Muslims would raise their economic position and contribute significantly to the nation’s economic growth if they take part in the capital markets. However, only Shariah-compliant businesses should be the subject of investing. Muslims must often monitor the Shariah conformity of listed firms since it is dynamic. Muslims should avoid investing in the stock of companies that engage in forbidden activities, such as traditional banking and financial services, insurance, stockbroking in general, companies that deal with alcohol, pork, tobacco, gambling, casinos, betting, prohibited pictorial advertisements, and entertainment based on music, movies, and the like. In general, Shariah-compliant equities are those whose 95% of income comes from sources other than those mentioned above. The IIS scale created and confirmed in the current study is the optimal scale for evaluating Muslim investors’ attitude. It is anticipated that the scale created for the study would lead to rigorous empirical investigations in this fascinating field. The next section focuses on the conclusion of the study.

Conclusion

The impact of Islamic investor sentiment on stock markets is well supported by empirical data. The objective of the project was to create and standardize a technique to gauge Islamic investor sentiment that would be useful for stock markets. Scientifically, a 24-item scale was created using the right statistical methods. The findings of the study indicate that elements such as PRO, SI, information accessibility, religious considerations, and IIE have a greater influence on the attitudes of Islamic investors. Furthermore, this study shows that participation in religious activities elevates the spirits of Islamic investors. The estimation findings show important information that supports the study of Islamic finance. First, we demonstrate how significantly the stock market is impacted by the mood of Islamic investors. Second, IIE, RF, PRO, SI, and AOI are having a greater impact on stock market success. The current study has significant limitations that should be considered in future research in this field. The study’s sample size is rather tiny to begin with. As a result, the conclusions cannot be applied to all Islamic investors. Second, as the components and dimensions used in this study were insufficient, future research should incorporate more variables and dimensions to provide more detailed results. Third, more investigation is required to broaden the current paradigm’s application to novel circumstances.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.