Abstract

This article aims, in the context of financial liberalization, to examine the impact of several internal and external factors in relation to the profitability of banks listed on the Moroccan stock exchange. The study uses the panel data method on a sample of the six banks with the largest market shares over the 2010–2019 period to investigate the influence of ownership structure, bank governance, capital structure, prudential regulation, and also a macroeconomic variation on bank profitability. Accordingly, the empirical results indicate a negative relationship between concentration, foreign ownership, and bank profitability. Further, high capital structure ratios, especially solvency, liquidity, and capitalization ratios appear to have an undesirable effect on the performance of Moroccan banks. In contrast, the impact of domestic institutional ownership is positive, implying that profitability is more favored by domestic ownership than by foreign ownership. Our findings also highlight the importance of independent directors and board size. Therefore, liberalizing ownership and opening up the board to the expertise of outside directors is essential for the banking sector’s development.

In terms of policy implications, central banks and regulators need to ensure that banks rigorously adhere to specified leverage and fixed capital adequacy ratios while ensuring optimal liberalization for bank performance.

Keywords

Introduction

In an increasingly liberalized context, the Moroccan financial and banking sector occupies a crucially important place in the Moroccan and African economies. The financial turmoil of 2008, accentuated by accelerated financial liberalization, revealed the importance of some macroeconomic and financial factors (liquidity, solvency, internal and external governance, type of shareholding, and prudential regulation) for the financial sector performance (Belcaid & El Ghini, 2021). Capital liberalization, board diversity, external expertise, and international regulation are essential factors that demonstrably play a determining role in the banking sector’s development. However, conducting and directing the liberalization process ought to be led prudently and wisely despite the evidence exhibiting indicators of success in terms of banking profitability at its initial stages. Incidentally, many Moroccan banks have made progress in banking reforms, supervision, and regulation, as well as in implementing structural reforms to reduce risks and promote financial progress. Banks continue nonetheless to operate in risky financial environments, particularly in the context of accelerated financial openness. Risk, therefore, seems appears to be at the core of a plausible explanation for high returns. In fact, bank profits are an important source of equity capital. It is a priori logical to suppose that if bank profits are reinvested, it can be safely assumed that it may lead to safer banking and, by extension, to higher profits in an environment that enjoys and encourages financial stability.

This article expands on previous relevant works by first affirming several previous findings on banking profitability by presenting empirical and theoretical evidence with respect to Basel III regulations. We therewith apply measures of liquidity, solvency, and capitalization to test their effects on Moroccan banks’ profitability. Our study also focused on the impact of relevant economic and financial variables, such as economic growth, credit allocated to the private sector, bank size (total assets), inflation rate, trade openness, and foreign direct investment (Henceforth, FDI).

The main pursuit is to identify what the determinants of bank profitability in Morocco are in relation to financial liberalization. For this reason, we describe in the second section the financial context and the process of financial liberalization implemented to expand the Moroccan banking structure. Then, in the third section, we present the empirical and theoretical literature dealing with banking profitability. In the fourth section, we describe the methodology, the variables, and the study hypotheses. Afterward, the fifth section is devoted to the empirical results exposing the bank profitability determinants while analyzing the implications on the Moroccan banking and financial system. In conclusion, we summarize the main findings and provide some recommendations and policy implications.

Moroccan Financial and Banking Context

The Moroccan financial system is the most arguably efficient in North African countries. This position is attributed to the measures undertaken over the past decades. The financial sector’s performance has received considerably more attention following the financial turmoil of 2007, which highlighted the relevance of capital liberalization, liquidity, and solvency for the sake of the proper functioning of the financial system. In Morocco, the uncertainty inherent in the crisis effects has had an impact on the liberalization of its financial market and thus on economic development (Belcaid & El Ghini, 2019a, b, c). The banking sector plays an essential role in financing economic activities in different segments. However, the challenge is to remain financially liberalized while maintaining stability and competitiveness. Since the beginning of the twenty-first century and thanks to numerous successive and interrelated reforms, Moroccan banks have become important players in the African financial scene and have begun to play an important role in Africa ever since. Relatedly, in order to moderate the problems of risk management and financial shocks, the law of December 24, 2014, implemented new rules of macro-prudential supervision, as well as the new solvency ratios, liquidity, capital requirements, and risk control provided by the Basel III rules. The Basel III rules have been applied in a transitional manner between 2013 and 2019 (Maghlazi, 2020). According to the African Development Bank, Moroccan banks have one of the best-performing portfolios of banks in Africa and are the leading banks investing in Africa. Similarly, the nine largest Moroccan banks are all in the top 50 best-performing African banks, they are also among the top 15 best-performing in Francophone Africa according to Young Africa ranking in 2020. 1 They also have the largest networks in Africa, ahead of South African, Nigerian, Kenyan, and Gabonese banks. In Morocco, the banking sector plays a major role in the economy. It is the core machine of financing economic development through its two main activities: collecting and managing savings, and credit allocation. Moreover, Moroccan banks have engaged in recent years in large-scale expansionary projects: development in Morocco and the conquest of Africa and a greater presence at the regional and international levels.

According to Bank Al-Maghrib’s annual report on banking supervision for 2020, 2 the number of credit institutions and organizations subject to Bank Al-Maghrib supervision is 91. The population of listed credit institutions amounted to 10 in 2020, comprising six banks and four financial companies. These institutions represent 34% of the market capitalization. Their presence in Africa is operated through 45 subsidiaries and 4 branches, which are spread across 10 countries in West Africa, six countries in Central Africa, three in North Africa, six in East Africa, and two countries in Southern Africa.

It is worth noting that among the 19 Moroccan banks, there are eight so-called universal banks, six of which are listed on the Casablanca stock exchange and which are studied in this study given their concentrated presence on the Moroccan banking market that constitute the banking actors in the Moroccan economy, namely Attijariwafa Bank (AWB), Bank of Africa (BOA), La Banque Populaire du Maroc (BPM), Banque Marocaine pour le Commerce et l’Industrie (BMCI), Crédit Immobilier et Hôtelier (CIH Bank) and Crédit du Maroc (CDM). The choice was therefore made to focus on these six banks with the largest market shares and whose combined total share exceeds 85% of the national market. The other two unlisted banks are Crédit Agricole du Maroc (CAM) and Société Générale Marocaine Des Banques (SGMB).

Foreign banks have a large presence in the private banking sector. At the top, BNP Paribas, Société Générale France, and Crédit Agricole (SA) hold a majority stake in BMCI, SGMB, and CDM, respectively, with shares of 67%, 57%, and 79% (as of the end of 2018). Furthermore, Grupo Santander is a 5% shareholder of Attijariwafa Bank through Santusa Holding; while CM-CIC Group holds, through its holding company, Banque Fédérative du Crédit Mutuel—BFCM—, 27% of the capital of Bank of Africa. According to Bank Al-Maghrib, the shareholding status remains dominated by the majority of Moroccan private capital (more than 60%), while the majority of public and foreign capital remains a minority (less than 20%), particularly in terms of credits, assets, and deposits.

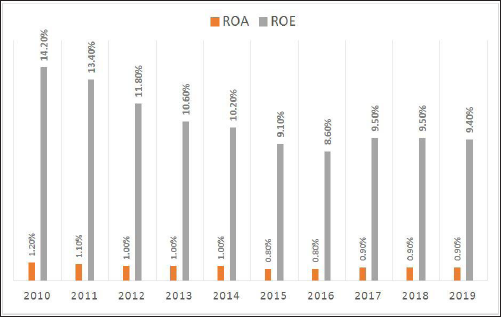

In terms of Moroccan banks’ performance, the period studied between 2010 and 2019 was marked by a relatively downward trend in return on assets (ROA) and return on equity (ROE). This decline is not due to deterioration in the net income of banks, but rather to the strengthening of assets and equity in recent years (see Figure 1).

Literature Review

Although some of the border determinants are involved in explaining bank profitability (Almaskati, 2022; Karadžić & Đalović, 2021), non-traditional banking activities can affect the banking result and efficiency as well (Ghouila & Jilani, 2019). Hence, an attempt is made to relate the theoretical aspect of the macroeconomic context, corporate governance, management style, and capital structure that are likely to influence risk and banking performance (Ben Jabra et al., 2017; Himaj, 2014).

Bank Governance and Board Composition

Bank governance was born out of the need to address the crises that are increasingly occurring with financial liberalization. According to Gillan (2006), bank governance admits two dimensions, external and internal: the internal dimension is the bank administration mode, while the external dimension is manifested through prudential regulation. The internal dimension is defined as the set of legal provisions, institutions, and rules designed to prevent the crowding out of minority investors by management, the directors’ board, and the majority shareholders. Good bank governance requires a clear labor partition between the directors’ board and the executive management (Daadaa, 2020, 2021). In the governance theory by financial contract, the directors’ board intervenes by incentivizing managers to perform, either through compensation schemes or by threatening to oust them. For its part, the bank’s size has a potential impact on the bank’s performance. By increasing its size, a bank can exert good control over efficiency, which also increases its performance. Roy (2008) explains in this context that large banks can engage in different activities, allowing them to diversify their business portfolio and thus reduce credit risk and increase performance. The composition of the directors’ board is another critical component of performance. According to Fuzi et al. (2016), independent non-executive directors monitor the performance and the executive directors’ activities. In general, independent and also foreign directors have a positive impact on banking performance (Handa, 2021). Indeed, some studies argued that a highly independent board does not lead to better performance and may even lead to worse performance (Adams & Mehran, 2008; de Andres & Vallelado, 2008).

Concentration, Structure, and Ownership Type

The property structure can influence performance either in a positive or negative way. Many studies have been conducted to investigate this phenomenon as well as deal with the question of how concentration and ownership structure can influence performance and banking risk (Siddika & Haron, 2020).

There are several important dimensions of ownership concentration that may not be captured in a single variable (Pandey & Sahu, 2021). Ownership concentration can be measured as the shares held by major shareholders, such as the government, financial institutions, and individuals. According to Johnson et al. (2000), in a dispersed ownership structure with increasing ownership rights, performance will be better because the free-rider problem will be resolved. On the contrary, when ownership rights of the largest shareholders widen, the increase in ownership may reveal to be a reason to weaken performance. Similarly, the study results conducted by Foroughi and Fooladi (2012) indicate that concentrated ownership can have a negative influence on banking performance. In fact, it allows controlling managers to adopt policies in their favor at the expense of minority stockholders.

In the case of banks, most studies find that private and domestic banks are more profitable than state banks, while foreign banks are more profitable than domestic private banks operating in transition and emerging economies (Tochkov & Nenovsky, 2011). According to agency theory, domestic institutional investors play a significant role in corporate governance. Maama et al. (2019) argue that domestic institutional investors are experts who can exercise more effective control and auditing over managers when they hold large equity shares. In addition, institutional investors have an informational advantage, regarding the environment and industry characteristics over other shareholders. In this framework, Berger and Bonaccorsi di Patti (2006) show that institutional investors improve US bank performance through their control.

The financial liberalization facilitated the banks’ capital opening to foreign investors. Previously, this was hampered by regulatory restrictions, particularly in developing countries. The local banks’ acquisition through privatization policies and the creation of subsidiaries is the main catalysts for foreign investors (Nachum & Ogbechie, 2019). Similarly, foreign ownership can allow the transfer of new management methods and knowledge to local banks. However, according to Bøhren et al. (2007), international investors are sometimes reluctant to engage in active corporate governance. From an investor’s perspective, this is a universal phenomenon where investors prefer to invest domestically rather than take optimal risk-return positions due to their knowledge and lack of foreign markets. In this regard, Matthew and Laryea (2012) report a negative relationship between foreign ownership and the financial performance of 25 Ghanaian banks due to insufficient knowledge of the Ghanaian terrain.

Prudential Regulation, Capital Structure, and Bank Risk

Faced with the bank risk rise, international authorities, like the Basel III Committee, have set up banking supervision standards. Banks are required to comply with these standards to ensure their liquidity and solvency vis-à-vis their customers. The shortcomings in financing and liquidity management have motivated the creation of new rules in the Basel III regulatory framework. Particularly, the Basel III norms cover other liquidity coverage and stable funding requirements (Bonfim & Kim, 2012; Hong et al., 2014).

For example, the current ratio, defined as the ratio of loans to deposits, reflects a firm’s position at a given time. It is a liquidity ratio, a high value of which may indicate a potential source of insolvency and illiquidity. Indeed, deposits are the main source of bank funding and therefore should have a significant impact on profitability (Demirguc‐Kunt et al., 2013). The relationship between liquidity roles and bank profitability has been the focus of a large body of research. One group of researchers (Chen et al., 2018; Dang & Nguyen, 2020) suggests that banks with high liquidity risk generally lack stable funding. A second group of researchers argues that an illiquidity risk has the opposite effect as liquid assets have lower returns than illiquid assets (Trujillo-Ponce, 2013).

Solvency can also provide information about the relative amount of debt in the capital structure, earnings adequacy, and cash flow for covering interest and fixed charges. Two types of solvencies are usually used: (a) debt ratios, and (b) leverage ratios:

Debt to assets ratio and debt to equity ratio: they are the share of assets or equity that is financed by debt. A higher ratio implies higher financial risk and lower solvency. Thus, many studies have shown that there is a negative relationship between these ratios and bank profitability (Khidmat & Rehman, 2014; Nawaz et al., 2015). Leverage ratio (capitalization or equity multiplier) = Total assets/total equity: this indicator assesses the share of assets that are financed by equity rather than debt. The Basel Committee decided to limit leverage in the banking sector in order to mitigate the financial instability risk. In addition, a high ratio of capital to assets allows for prudent lending and better profitability due to the cushion available to make risky investment decisions (Tan & Floros, 2018). It is also a sign that well-capitalized banks face lower costs.

Macroeconomic Determinants of Bank Profitability

Several studies have incorporated macroeconomic factors (Ahmad et al., 2016; Nguyen et al., 2017) and argued that in addition to bank-specific proxies, country-specific controls are needed to explain bank performance. Based on previous reports in the literature, we decided to include some indicators describing the macroeconomic environment in which banks operate. For the degree of trade openness, Otuori (2013) concludes that exports and imports are positively associated with commercial banks’ profitability. For the inflation rate, the empirical work conducted by Tan and Floros (2012), using a panel of 101 banks in China, reveals that inflation was positively related to bank profitability. Likewise, Flamini et al. (2009) study the determinants of 389 banks’ profitability in 41 countries from sub-Saharan Africa. They conclude that inflation has a positive effect on bank profits. However, Mouldi et al. (2011) find a significant negative effect of inflation on the nine Tunisian banks’ profitability over the period 1980–2009. Indeed, a fully anticipated inflation rate increases profits, as banks can adjust interest rates appropriately to increase revenues, while an unexpected variation could amplify costs due to inadequate interest rate adjustment.

Regarding the FDI impact on banking performance, foreign direct investment in the banking and financial sector for a host country can reap the maximum benefits, especially with a well-developed financial sector, as pointed out by Sghaier and Abida (2013). Thus, FDI is expected to influence the banks’ performance through new customers and business opportunities that will require the banks’ service.

With respect to the exchange rate, for a country that depends largely on imports and exports, its exchange rate stability is important for credit allocation and firm performance (Monday et al., 2017). It is in this context that this article attempts to systematically assess the effects of exchange rate variations on the financial performance of banks listed on the Casablanca Stock Exchange.

Methodology, Data, and Research Hypotheses

We opted therewith for an empirical analysis of bank profitability in the context of financial liberalization in Morocco. To do so, we chose a panel of the six Moroccan banks listed on the Casablanca Stock Exchange: Attijariwafa Bank (AWB), Bank of Africa (BOA), Banque Populaire du Maroc (BPM), Banque Marocaine pour le Commerce et l’Industrie (BMCI), Crédit Immobilier et Hôtelier (CIH) and Crédit du Maroc (CDM). Our objective is to test the implications of the set of defined variables and conclude the nature of their impact on the bank’s results. Amid the details of this analysis, it is important to point out that the period covered by our study (2010–2019) is one of the major regulations and liberalization reforms experienced and which were empirically shown to affect the economic and financial system. Hence, we used panel analysis techniques by extracting data from the banking institution’s annual reports.

Methodology

The panel data technique was used in this study to deal with the dual dimension (spatiotemporal) of our data: N = 6 banks, and T = {2010:2019} 10 years. Static panel data modeling was adopted (and not dynamic) because N is not greater than T. Thus, the general equation to be modeled is of the following form:

i = {1, …, 6} Code for each bank.

t = The year.

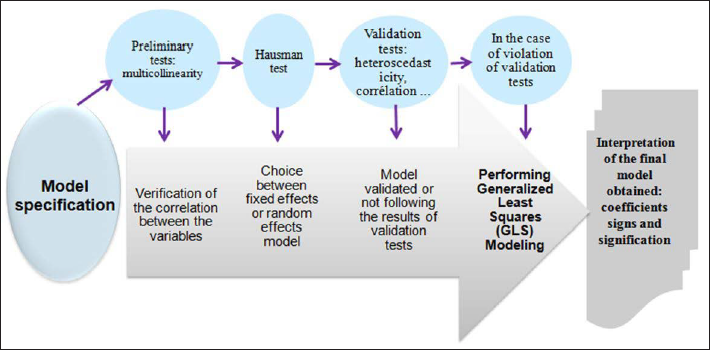

The schema of the econometric methodology in panel data techniques to be used is presented in Figure 2:

Summary of the Panel Data Modeling Approach Adopted.

Hypotheses and Models Specification

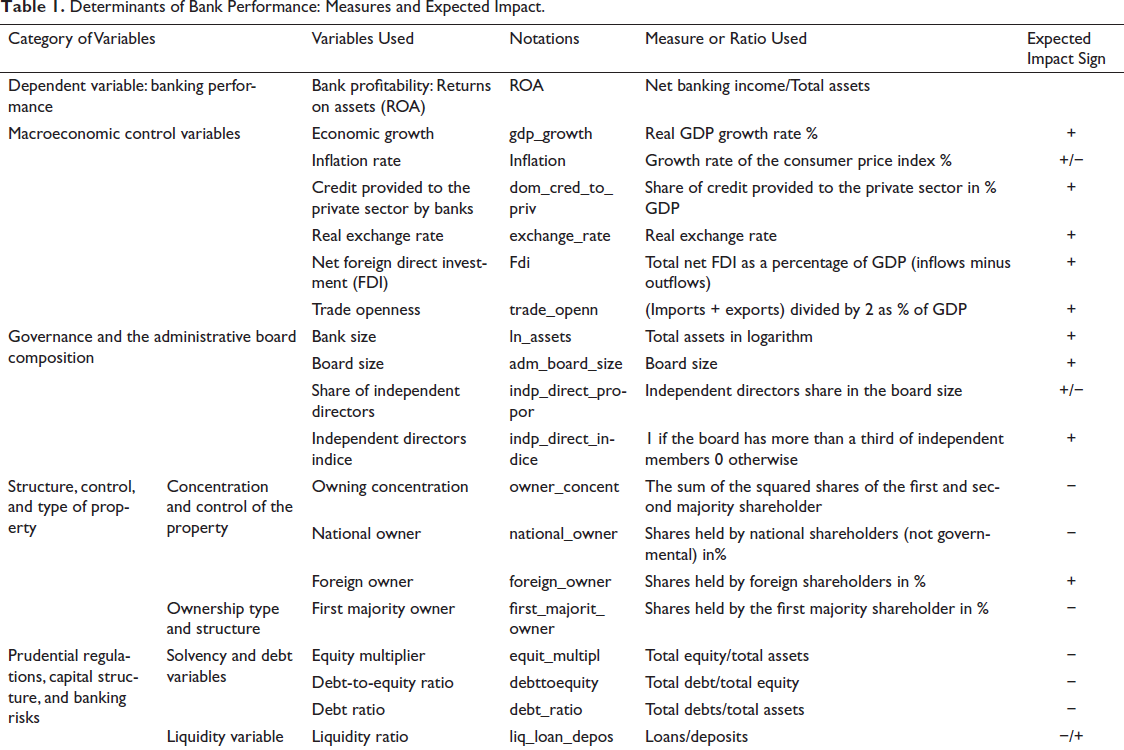

We chose ROA as the dependent variable that explains bank profitability. It represents the ratio of net income to total assets and therefore indicates the bank’s ability to generate profit from its assets. According to Tijjani (2017), as a measure of performance, ROA is generally considered a good internal management ratio, as it measures profit in relation to all the assets an organization uses to achieve those gains. This article uses also independent variables classified into bank-specific variables and macroeconomic indicators to analyze their impact on Moroccan banks’ profitability. Based on the theoretical and empirical works previously conducted, the variables’ details, that is, their measures and their expected impact on bank profitability are described below (see Table 1).

Determinants of Bank Performance: Measures and Expected Impact.

Based on these hypotheses, we determined the models providing an analysis of the relationship between governance, ownership, capital structure, and bank profitability. The correlation analysis between the independent variables counting the three determinant categories (governance, ownership structure, and capital structure) allowed us to opt for five different sub-models including variables that do not present a multicollinearity risk. The variable notations used in different specifications are well explained in Table 1. The detailed equations to be estimated for models 1, 2, and 3 are presented as follows:

(i) Model (1): The influence of governance on bank profitability: Sub-model (1.1): Influence of bank and board size:

Sub-model (1.2): Influence of board member independence:

(ii) Model (2): The influence of ownership types and shareholding on bank profitability: Sub-model (2.1): Influence of the concentration and national owning:

Sub-model (2.2): Influence of the foreign and majority shareholders:

(iii) Model (3): The influence of capital structure and prudential regulatory standards:

with: The coefficients { i = {1, …, 6} bank code. t = The year.

Empirical Results and Discussion

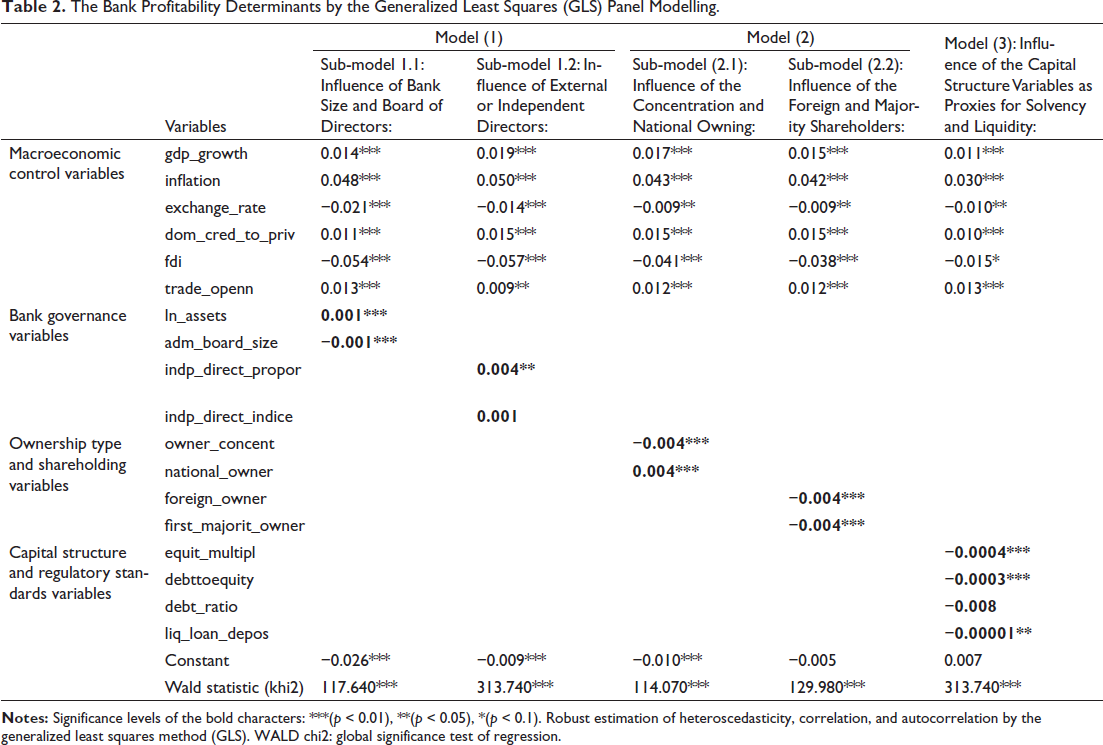

Using the Hausman test for each sub-model, the random and fixed effects were tested consistently for several sub-models. In addition, Breush–Pagan modified Wald, and Wooldridge tests were used and identified problems with contemporaneous correlation, heteroscedasticity, and autocorrelations, respectively. Finally, the generalized least squares (GLS) technique was adopted to mitigate potential problems of endogeneity, heteroscedasticity violation, correlation, and autocorrelation assumptions. The results of the impact of the determinants (governance, ownership, and capital structure) on bank profitability are presented in Table 2:

The Bank Profitability Determinants by the Generalized Least Squares (GLS) Panel Modelling.

For the majority of the models carried out and concerning the macroeconomic variable’s impact, the significance and sign of the estimated coefficients indicate that the banks’ profitability increases with the increase in the real GDP growth rates, credit provided to the private sector, and inflation. Indeed, the macroeconomic context significantly affects Moroccan bank performance in Morocco: Inflation has a positive effect on their profits because banks correctly forecast future variations to adjust their margins. The national economic growth and the good economic environment positively affect the banks’ trajectory of development by encouraging them to innovate and offer more loans. On the contrary, bank performance decreases as the real exchange rate increases. The rise in exchange rates can be thus negative for the banks. In fact, depreciation generates significant losses to the capacity of lenders. On the other hand, trade openness has a significant and positive impact on banking performance in Morocco, which means that more exports and imports can simulate banking activity. For foreign direct investment, we find that its increase can negatively influence the Moroccan bank’s profitability. This is possibly related to the fact that FDI financing can replace bank loans and thus investors are in a comfortable financing capacity.

As presented in Table 2 above, the estimated parameters of the governance variables indicate that profitability increases with the bank size and decreases with its board size. The positive and significant coefficient at the 1% level for the variable “ln_assets” support the hypothesis that large Moroccan banks achieve higher efficiency gains and profits because they do not operate in highly competitive markets. In addition, we find that increasing the number of independent board members has a positive influence on bank performance. In the context of board liberalization, a fairly large proportion of independent directors will be able to provide valuable services by offering external financial expertise. Strengthening board independence actively contributes to the strategic decision-making process and ensures access to critical resources that will, in turn, improve bank performance. While independent directors are expected to perform a better oversight function, their ability to do so may be enhanced by the expertise and resources available on the board of a large bank. For its part, board size has a significant and direct negative influence on bank profitability. Indeed, small boards are the most profitable for banks. Large boards with a majority of affiliated (non-independent) directors may pose problems with minority shareholder representation. Thus, it is good to note that a small board size with many independent members is very favorable for bank performance. This finding is consistent with the argument that too many boards lead to problems of organization, control, and flexibility in decision-making, as well as with some studies’ findings of banking governance in emerging economies.

Regarding ownership type and shareholding variables, our results stipulate that a highly concentrated shareholding characterized by a single dominant shareholder impacts negatively the banks’ profitability. Thus, as the first majority shareholder concentrates more shares than the other shareholders, the more the bank’s performance will tend to decline. As a result, majority shareholders tend to make decisions that maximize their profits, even though these decisions may increase banks’ risks and jeopardize their long-term viability. This relationship is consistent with the point that concentration in transition economies can have a negative effect on performance, as inadequate protection of minority shareholders can give the majority shareholder the opportunity to expropriate substantial amounts of the bank’s wealth. Indeed, in a dispersed ownership structure, Moroccan banks’ performance can be better because the free-rider problem is solved. Furthermore, we suggest that banks, with a dominant national (institutional, domestic investors among others) ownership structure, experience perfectly designed managerial and financial incentive efficiency that promotes their performance. In contrast, banks with dominant foreign ownership seem to suffer from the competition and informational disadvantages in Morocco.

Several categories of variables representing capital structure and prudential standards were studied, such as solvency, leverage, and liquidity. In detail, the results show that the solvency and debt variables, such as the equity multiplier (ratio of assets to equity), the debt ratio (ratio of debt to assets), and the debt-to-equity ratio (ratio of debt to equity), had a negative impact on profitability as measured by the ROA. For its part, the variable measuring bank liquidity risk (loan-to-deposit ratio) has a negative relationship with bank profitability. In fact, high non-performing loans do not translate into healthy profitability if their recovery is low. Similarly, the decrease in profitability occurs whenever total liabilities increase. Good solvency and liquidity risk management and the prudential standards introduction to stabilize the capital structure at optimal levels can lead to good outcomes. Indeed, the higher these ratios are, the more the bank will resort to debt and other liabilities like loans to finance its assets. This gives an idea of the extent to which the banking institution relies on debt to finance its capital structure. In contrast, lower ratios of solvency, leverage, and liquidity are considered very favorable, as banks are less dependent on debt and loan financing and do not need to use additional cash flow to service debt. A low equity multiplier implies that the bank has fewer debt-financed assets. This is generally seen as a positive, as debt service costs are lower. Hence, well-capitalized banks earn higher returns.

In general, bank-specific variables deeply influence Moroccan banks’ profitability. The findings at hand provide some important policy suggestions for bank management on how they can improve profitability. This performance is associated with banks that hold an optimal amount of liquid assets, and lower levels of non-performing loans combined with effective management of capital and governance. It can be enhanced by strengthening asset quality and capital structure, and improving debt management and liquidity. At the same time, any uncontrolled increase in nonperforming loans, leverage, and risk can alter financial stability and therefore reduce bank profitability.

Conclusion and Policy Implications

In a liberalized financial environment, profitability is enhanced when the banking structure is effectively controlled by appropriate regulatory and prudential standards.

In this study, we choose a selection of macroeconomic factors and other bank-specific variables that may affect bank performance in Morocco. Using models (1), (2), and (3) as written in the previous sections, we estimated panel data models for a sample of six Moroccan largest banks over the period from 2010 to 2019 to test our hypotheses. In empirical terms, robust GLS estimation was performed to control serial correlation and heteroscedasticity. The choice was made to focus on the six banks with the largest total market shares, while the choice of variables was related to data availability and empirical theory.

With respect to the macroeconomic context, the results showed a positive and significant relationship between the macroeconomic indicators (inflation rate and GDP growth rate) and bank performance measured by the ROA ratio. Within this framework, policymakers can design medium- and long-term strategies taking into account macroeconomic risk. In addition, central banks can forecast the impact of macroeconomic and financial factors on the banking sector and formulate policies for its stable and sustainable development. Furthermore, the study indicated the importance of large size to the realization of scale economies and profitability for banks. Similarly, the presence of several independent directors on the board protects the shareholders’ interests and improves performance. Therefore, liberalizing ownership and opening the board to the expertise of outside directors is important for the banking sector’s development. Certainly, liberalization of ownership and bank control can further boost their profitability since the ownership concentration in the hands of a dominant shareholder can undermine overall performance. In addition, according to our findings, due to informational competition, Moroccan banks’ profitability is favored more by domestic ownership than by foreign ownership.

On the other hand, ROA is negatively affected by financial leverage. Less capitalized and less liquidated banks have room to weather negative shocks and make riskier and more profitable investment decisions. In fact, a negative relationship found between the liquidity ratio (loans/assets) and profitability may confirm that the more a bank uses loans, the worse it performs in terms of returns. Hence, banks’ financial leverage and capital structure should be monitored and aligned with regulatory standards. Leverage ratios should be fixed to the lowest possible level so that funds can be reinvested at interest rates higher than the interest paid by banks to depositors. Likewise, central banks and regulators need to ensure that banks respond carefully with the specified minimum capital adequacy ratios while ensuring optimal liberalization for bank performance. In the wake of the implications, the findings are important for policymakers as they will facilitate the formulation of policies regarding governance, ownership, and prudential regulatory standards, through the implementation of effective capital, risk, and liquidity management in banks. It is imperative for banks and regulators to continue to promote the implementation of effective management. This could help avoid the potential threat of insolvency or bankruptcy. It is also important for practitioners to model banks’ risks and enable them to improve their management practices. We conclude then that compliance with regulatory thresholds and standards for governance, capital, solvency, and liquidity are relevant for policymaking in the sense that commercial banks should strive to manage them in order to achieve more profits.

Given the strong competition among Moroccan banks, tapping into new investment markets abroad, particularly in Africa, is an innovative and profitable strategy. Controlling the capital outflows liberalization remains necessary, even though it is fruitful in terms of bank profitability. In an increasingly liberalized and globalized world, the adaptation of banks to the evolution of customer demand is fundamental to maintaining and gaining market share. The banking system as a whole has so far maintained a growing level of profitability, as revealed by the results. However, non-performing loans may increase due to an economic situation marked by a slowdown in growth, and to the evolution of companies operating in areas of activity exposed to the external demand decline. In this context, the improvement in the quality of deposit and asset risks allows a reasonable level of credit coverage to be tolerated. Recently, overall performance indicators have relatively declined since 2017 the year of the participatory banking system launch, followed by the shift to a more flexible exchange rate regime for the dirham since January 2018, and reinforced by the advent of the COVID-19 pandemic in 2020. These three events seem to influence the functioning of the traditional banking system. This prompts us to open up to questions of great importance: Is the current financial system capable of keeping up with the changes in the exchange rate regime and the Moroccan economic context? How can we assess the effects of shocks and uncertainty transmitted to the Moroccan banking system while identifying the main structural changes that have occurred? Will the introduction of a participatory banking system enrich the existing traditional system, or compromise its proper functioning? Admittedly, Moroccan banks are multiplying the formulas by offering new products (e.g., Islamic finance products) in order to convince and attract new customers and increase their market share. Moreover, the creation of a financial cluster in Casablanca (Casa Finance City) to attract foreign capital is an asset for a new dynamic development of the Moroccan financial and banking system. In terms of perspectives, it would be very interesting and rewarding if the study sample could be extended to several banks and by including other variables (e.g., Bank age, recent liquidity coverage ratio [LCR]), and other bank profitability indicators, such as “Return On Equity ROE,” “Tobin’s Q,” and “earnings per share EPS.”

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.