Abstract

The small savings scheme plays a vital role in mobilizing savings for the economy, and the post office provides a variety of products to people to promote a savings habit. The current research attempts to analyze the moderation effect of financial consultants in relationship between the small savings scheme of the post office, financial literacy and behavior, and the savings habit of people. The study exhibits a significant positive impact of predictors and moderation variables on savings habits. In this regard, a two-phase structural equation modeling (SEM) has been employed to validate the hypothesized measurement model using confirmatory factor analysis (CFA), and in the next phase, the structural model verifies the hypothesized association between exogenous and endogenous variables to draw rational inferences. And a positive effect of predictors and interaction variables is observed. Finally, the study concluded with an important suggestion for the investment manager and other intermediaries: integrate the financial engineering process by giving due importance to investor needs.

Introduction

Small savings schemes are generally designed for small investors to mobilize and grow savings habits (Vasudevan, 2009) and provide economic benefits, mostly to limited income groups, rural people, and financially backward urban communities (Ganapathi, 2010). Household savings in formal financial institutions work as capital for large corporations. In India, 65% of the population lives in rural areas, and the small savings of rural households become a large reservoir of capital that can be allocated to various needy sectors through a proper channel of formal financial institutions (World Bank, 2020). Credit obtained by corporations can be used as capital for investment in new economic activities and help in the development of a nation’s economic output. Hence, savings can be mobilized and rotated in the economy by financial institutions. The accumulation of fixed capital is only possible through sufficient savings. Therefore, the deployment of savings plays a crucial role in the economic development of rural areas (Olori et al., 2021). Savings can help in the smooth consumption of and investment in human capital at the household level and the prediction of future economic growth at the macroeconomic level; thus, the mobilization of savings is crucial for societal and individual welfare (Karlan et al., 2014, p. 36). To make small savings programs more appealing and competitive, the government has embraced the financial engineering process by forming numerous committees over the years, including the Malhotra Committee (1989), Rangarajan Committee (1991), Gupta Committee (1998), and Dave Committee (1999). So, the structural changes in the financial sector and diffusion of technology boost productivity within the sector and enhance profitability. As a result, it promotes the economic growth of the nation (Abid et al., 2022; Beaman et al., 2021; Mohanta et al., 2017).

People want safe and secured products with a convenient way of payment and guaranteed return along with a capital appreciation, for which they prefer fixed deposits in banks, followed by postal savings schemes, insurance, and government securities (Chawla & Joshi, 2021; Mittal & Aggarwal, 2022). Investors’ level of knowledge, skill, overall experience and experience intensification (Sivakumar & Rajadurai, 2021), and attitude play an important element in framing financial decisions (Agbo & Abu, 2020; Bhatia et al., 2021; Gumus & Dayioglu, 2015; Singh & Rahman, 2018). It is seen that age, educational qualification, and sex are not important in making financial decisions; however, income and occupation are important (Ezilarasi & Kavitha, 2020). In lower and middle-income groups, people prefer simple and reliable small savings schemes for securing their principal amount first than the return (Korniotis & Kumar, 2011). Further, it is observed that the purchase decisions of people are influenced by the structure of the financial services industry (Chopra et al., 2021) and community pressure (Lewellen et al., 1977; Sahi & Arora, 2012). Information about intermediaries and their performance and ease of use of information (Healy & Palepu, 2001) and herd behavior are also accountable for purchase decisions (Fromlet, 2001). Further, studies show that the convincing behavior of agents and intermediaries play an important role in shaping the savings behavior of people (Sorropago, 2014).

Therefore, it is observed that small savings schemes of the post office, financial literacy and people’s behavior, and guidance of financial consultants play important role in shaping savings habits (Sofi & Hakim, 2018); however, the researcher did not observe any study that considers a financial consultant as a moderator in determining savings behavior. Thus, the researcher proposes to consider the financial consultant as the moderator in the relationship between the small savings scheme of the post office, financial literacy and behavior, and savings habits of people. Therefore, the researcher got an opportunity to throw more light on this issue.

Literature Survey and Theoretical Framework

Small Savings Scheme of Post Office and Savings Habit

The rural economy is developing with the help of different banking and nonbanking institutions, and rural investors are gradually moving from a savings-based economy to an investment-based economy (Singh & Rahman, 2018). And in this connection, the postal department is considered the backbone for developing the rural economy and acts as an important catalyst of communication (Anand, 2019) for developing savings habit among people by offering different savings schemes with diverse features (Vasudevan, 2009). The old-age requirements, the tax benefits of the instrument (i.e., the National Savings Certificate), safety, security, convenience, liquidity, and assured returns are some of the major attributes that attract people to invest in post offices for their progressive growth (Chawla & Joshi, 2021; Gavini & Prashanth, 1999; Mohanta & Deabasish, 2011). Further, it is seen that during the time of financial crisis, they invested less in risky assets and more in less risky assets to meet their personal as well as social obligations (Bhattacharya & Gandhi, 2021; Gurbaxani & Gupte, 2021; Wang et al., 2021). The majority of teachers want to invest their money in things like their children’s education and marriage expenses and purchase popular time deposit plans like Kisan Vikas Patra (KVP) and Indira Vikas Patra (IVP) that are similar to and meet the needs of products like commercial banks (Prajapati et al., 2021). The National Council of Applied Economic Research (NCAER) of India’s survey (Government of India, 2017–2018) reveals that the department of post contributes a considerable portion of overall savings to the economy and that significant growth in domestic savings habits is being noticed (Soni et al., 2022). Hence, it can be assumed that:

H1: Small savings schemes of the Post Office contribute to cultivating savings habit.

Financial Literacy, Behavior, and Savings Habit

Individuals’ well-being and prosperity depend on their ability to make better economic decisions. Financial literacy provides a platform for taking advantage of market opportunities, and investors’ levels of financial literacy and awareness are reflected in their savings and investing habits (Rao et al., 2018). Inadequate awareness campaigns discourage people from setting aside a substantial amount of their income for savings, which leads to the development of unfavorable behavioral attitudes toward saving. Additionally, research demonstrates that people’s socioeconomic status and demographic traits affect their level of financial literacy (Jacob, 2009; Lusardi, 2019; Venkatesan & Jacob, 2019). Aside from that, it exhibits their emotion (i.e., fear and sadness) and emotional maturity level, that is, emotional stability, social adjustment, and personality integration (Nehra & Rangnekar, 2021); attitude, that is, lifestyle, efficiency, convenience, trust, and perceived ease of use (Chawla & Joshi, 2021); and sentiment, that is, bad mood and anxiety affect savings behavior of potential savers (Aren & Hamamci, 2021; Liu et al., 2020). Women tend to have lower levels of financial literacy than men, and they frequently miss the right opportunity to make critical economic decisions. To protect their families from financial risk and suffering, they do want to maintain enough liquid funds on hand nevertheless (Netemeyer et al., 2018). People are conscious of post office savings and investment vehicles (Velsamy & Amalorpavamary, 2015), and studies depict that older investors are more aware than younger in semi-urban and urban areas and prefer to fulfill their life necessities and tax benefit needs (Korniotis & Kumar, 2011). Furthermore, it was found that financial behavior significantly improved by family financial socialization through formal and informal training and education (Khawar & Sarwar, 2021; Ullah & Yusheng, 2020). Additionally, training is more effective in fostering savings habit than borrowing behaviors in individuals (Grohmann et al., 2018). Hence, it can be proposed that:

H2: Financial behavior and financial literacy promote savings habit.

Financial Consultant and Savings Habit

In the case of financial evaluation, financial counselors are better able to describe how people’s psychological, cultural, and emotional relationship with money affect their financial behavior (Gounaris, 2005; Joo & Durri, 2018). According to Bartholomew and Horowitz (1991), dismissive savers are more prone to switching advisers because they rely on their owning habits, while preoccupied depositors are only interested in forming a relationship after having a thorough conversation about their investing goals. Because of this, regular communication with financial counselors eliminates preexisting restrictions and encourages saving behavior. People compare their present utility with their discounted future benefit before making an economic decision. Further, their follow-up visit also converts people’s savings behavior into accounting behavior in the future (Rodríguez & Saavedra, 2019; Valaskova et al., 2019). Studies also show that social penalties, which are typically applied when people do not meet their financial obligations on time and are typically announced in a public forum by the financial advisor, have a substantial impact on people’s savings habit (Breza & Chandrasekhar, 2019).

Working women are conservative, and research shows that they save more money than men do. They prefer small savings plans to make the best use of their earnings, and they save to ensure a brighter future. The Indian postal system offers them better financial services by branching out into non-traditional businesses such as e-banking, e-governance, and e-commerce (García-Santillán et al., 2021). Investors’ social relationships influence business practices (Farzin et al., 2022). When faced with a decision made by a big group, investors display herd behavior (Fromlet, 2001; Viswanathan et al., 2020). Similar to this study notes that most people learn about postal savings plans from their peers, families, and financial experts and change their options according to the situations they meet because they do not have predetermined decisions (Gomes et al., 2021). Therefore, in an agent-based system, financial consultants take an important position in influencing their savings habits (Liu et al., 2020). They have the potential to eliminate psychological hurdles for superior customer relationship management and client retention by resolving their multifaceted set of expectations (Sofi & Hakim, 2018). Greater disclosure and secure connections remove negative worries and foster a positive and healthy investment environment (Collins, 1996). Additionally, the government is making various efforts to raise financial literacy among the communities and integrate them into society using various learning modalities at various levels (García-Santillán et al., 2021). Research demonstrates that better financial decisions can only come from groups that are financially literate (Grohmann, 2018). Therefore, it can be proposed that:

H3: Financial consultants moderate small savings scheme of the post office and financial literacy and behavior of people, by promoting savings habit.

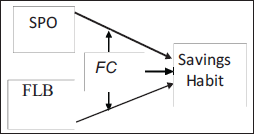

Based on the above argument, the following research framework may be proposed, as presented in Figure 1.

Research Objective

The sole intention of the study is to analyze the moderation effect of financial consultants on the relationship between the small savings scheme of the post office, financial literacy and behavior of people, and savings habit of people.

Research Methods

Research Design

A suggested research framework to study the predictors of investment decisions and moderating role of a financial advisor on investment decisions is shown in Figure 1. Furthermore, to examine the association between exogenous (small savings scheme of post office and financial consultant) and endogenous (savings habit) variables experientially, an investigation was made using the descriptive research design by taking 12 Indian districts with a significant portion of the rural and semi-urban population over 6 months from February 2021 to July 2021.

Sample Frame and Data

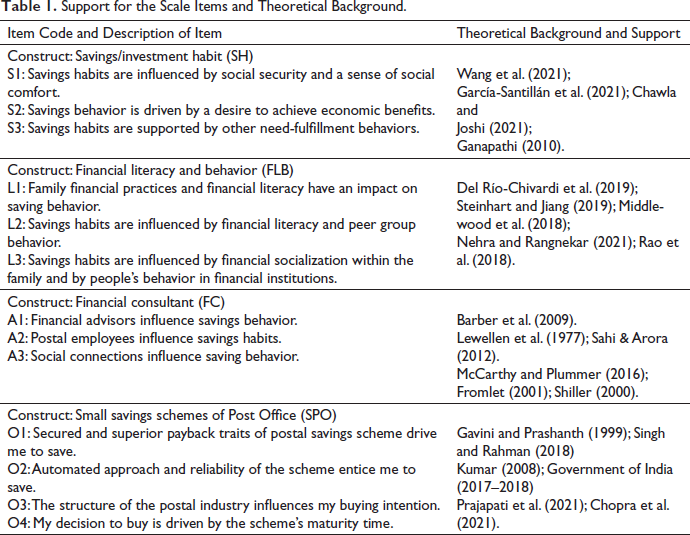

To save time and resources and to get the highest rate of response, the researcher has employed the convenience sampling technique for data collection (Bryman & Bell, 2015).Data were collected through a well-designed survey instrument consisting of 13 questions from 343 semi-urban and rural respondents, and a final sample of 313 was taken for study after ignoring missing values and wrong responses and finding an adequate response and sample size (Cochran, 1977; Reilly & Wrensen, 2007). A pilot test was conducted with a sample size of 30 respondents to assess the validity and reliability of the survey instrument, and it was found to be adequate and satisfactory. Internal consistency of the survey instrument was verified through Cronbach’s alpha (Nunnally, 1978) and observed values greater than 0.7 thus confirmed the reliability of the instrument. Further, the scale reliability and validity were verified through confirmatory factor analysis (CFA). The survey instrument is a 13-item, 5-point Likert scale that assesses respondents’ savings habits based on different parameters, and the research framework for the item selection has been detailed in Table 1. SPSS 24.0 and AMOS 24.0 were used to analyze the responses.

Support for the Scale Items and Theoretical Background.

Result Discussion

Scale Reliability Assessment

The reliability of the scale was assessed through Cronbach’s alpha (Churchill, 1979), and values for all the constructs are being observed to fulfill the cut-off value of 0.7 (Nunnally, 1978). The Cronbach’s alpha values for the four factors, that is, small savings scheme of the post office (SPO), financial consultant (FC), financial literacy and behavior (FLB), and savings habit (SH) were 0.767, 0.778, 0.882, and 0.880, respectively. To validate the proposed model, a two-stage SEM was executed (Hair et al., 2013). Initially, confirmatory factor analysis was performed to confirm the hypothesized measurement model (MM), and in the next step, the structural model (SM) was constructed to validate the association between the variables based on the proposed model.

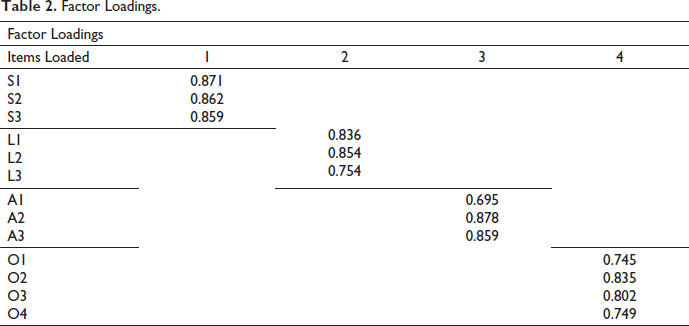

Exploratory Factor Analysis

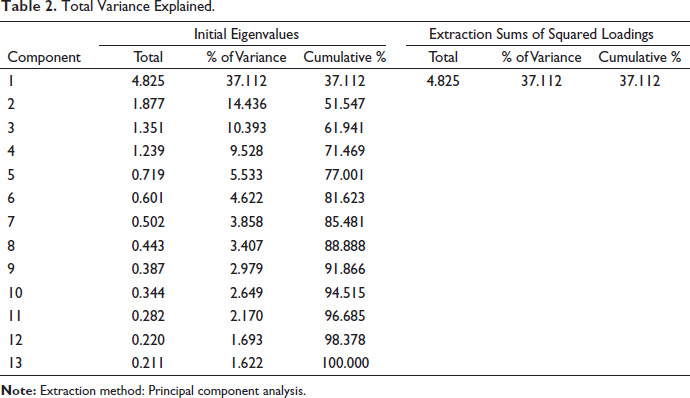

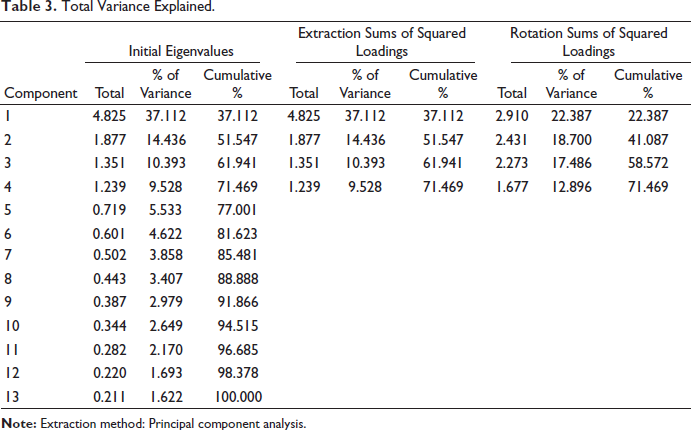

The adequacy of the sample for factor analysis was measured through Kaiser–Meyer–Oklin (KMO) and Bartlett’s sphericity tests and found the value to be 0.806 for KMO statistics, which is more than 0.50 (Hair et al., 2013). As shown in Annexure Table 1, the principal component extraction with the varimax rotation method was employed to perform factor analysis in SPSS 24.0. It produced an approximate chi-square value of 1188.243 with 78 degrees of freedom and observed significance at a 5% level of significance. The ceiling points of factor loadings and cross-loadings were taken (>0.5) (Karatepe et al., 2005) and (>0.40) (Hair et al., 2010), respectively, and an eigenvalue greater than 1 was taken as the base. Annexure Table 3 shows the extracted four factors from exploratory factor analysis that have explained 71.469 percent of the total variance and all the items have been taken after exploratory factor analysis (EFA) for confirmatory factor analysis and detailed factor loadings are presented in Table 2. Harmon’s single-factor method was used to validate the common method bias (CMB) by employing the principal component extraction method without applying rotation in factor analysis. The extracted single factor has explained 37.112% of the total variance, which is less than the acceptable threshold of 50%. Thus, common method bias is eliminated, and it is presented in the annexure in Table 2.

Factor Loadings.

Measurement Model

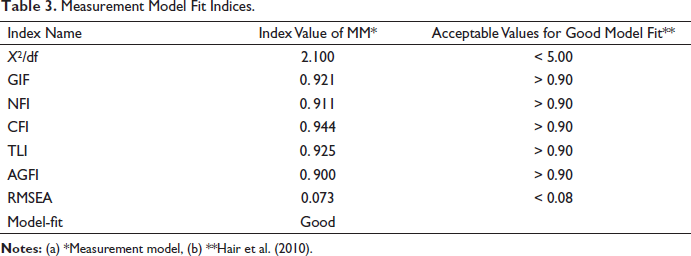

The goodness-of-fit indices are calculated through confirmatory factor analysis for the entire set of four latent constructs in a single model to assess its goodness of fit (Schreiber et al., 2006).

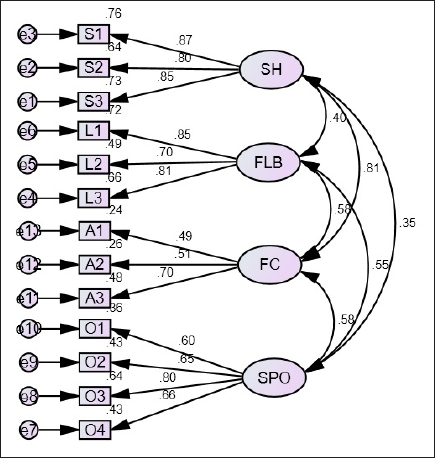

It is noticed that the values CMIN/DF = 2.100, GIF = 0.921, NFI = 0.911, CFI = 0.944, TLI = 0.925, AGFI = 0.900, and RMSEA = 0.073 of the model fit indices are within the acceptable ranges and are presented in Table 3. Further, the measurement model is demonstrated in Figure 2.

Measurement Model Fit Indices.

Measurement Model.

The construct soundness of the measurement model (MM) is being measured through convergent validity and discriminant validity. The convergent validity is being assessed from the value of average variance extracted (AVE) and the composite reliability from the result of confirmatory factor analysis (CFA). MM model is observed to have convergent validities as AVE > 0.5 and CR > 0.7 (Fornell & Larcker, 1981). The outcomes of convergent validity and discriminant validity are presented in Tables 4 and 5, respectively. It is found that the diagonal discriminant values are larger as compared to correlation values by the side of the relevant row and column values; hence the discriminant validity of the constructs is validated (Fornell & Larcker, 1981).

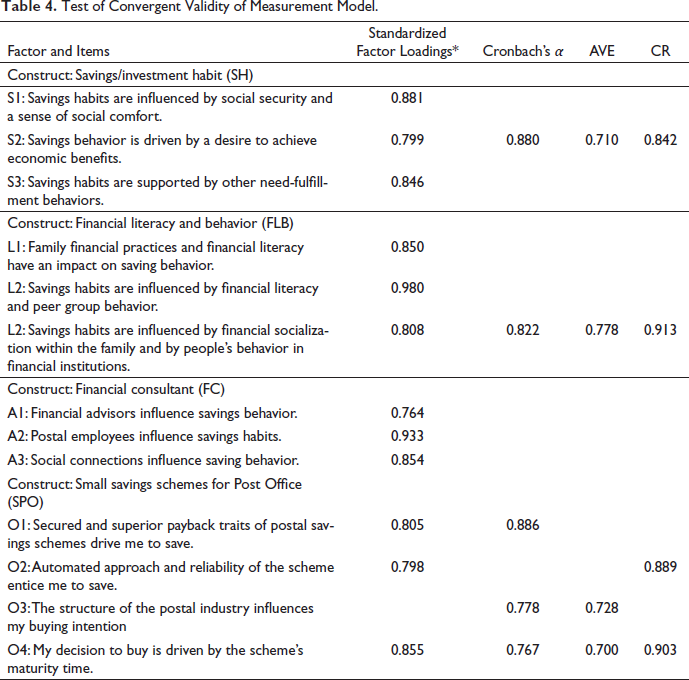

Test of Convergent Validity of Measurement Model.

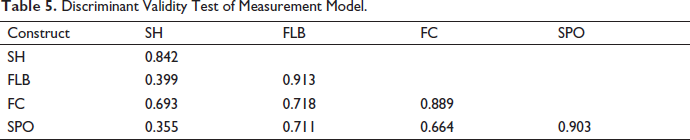

Discriminant Validity Test of Measurement Model.

Structural Model

In this part, the assessment and justification of the hypothesized model were done using the maximum likelihood estimation technique by concentrating on the statements of the model. The validation of the hypothesized model has been done through different model fit indices and other parameters.

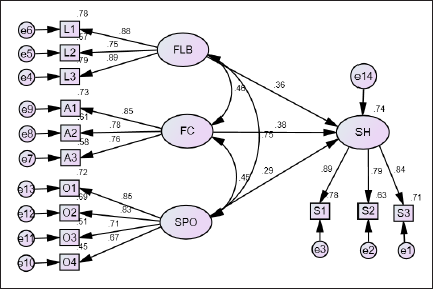

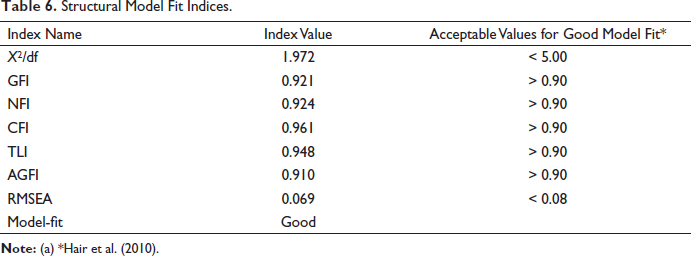

Analysis reveals a better result for the model, and we obtained better and superior values in our model compared to the standards suggested for the model fit indices, which would fall between 0.5 and 0.8 to be regarded as a superb model in social science research (Hair et al., 2010). All the values are floating above 0.9, indicating the well fit of the proposed model with the data. The RMSEA is 0.069 (<0.08) and X2/df is 1.972 (<5.0) indicating the well fit of the data for the model. In this model, R2 = 0.74 indicates that 74% of the variance is explained by the exogenous variables. The structural model is demonstrated in Figure 3, and the model fit indices are demonstrated in Table 6. From this, it can be said that the exogenous variables like the small savings scheme of the post office (SPO), financial literacy and behavior (FLB), and financial consultant (FC) have significant association with the savings habits (SH).

Structural Model.

Structural Model Fit Indices.

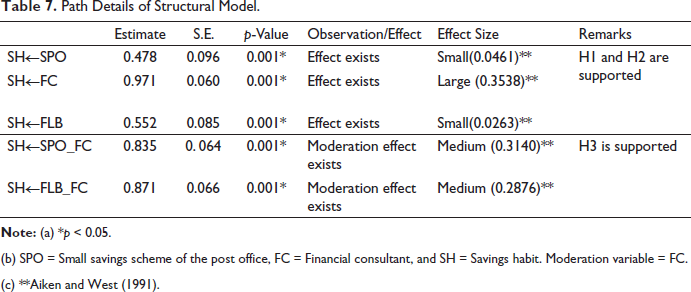

The latent constructs that were found after due validation and proved to be significant and favorable to the suggested model are shown in Table 7 along with their path details and effect sizes. It shows a positive association between the exogenous variables, such as the small savings scheme of the post office (SPO), financial literacy and behavior, financial consultant (FC), and the endogenous variable, such as savings habits (SH).

Path Details of Structural Model.

(b) SPO = Small savings scheme of the post office, FC = Financial consultant, and SH = Savings habit. Moderation variable = FC.

(c) **Aiken and West (1991).

Discussion

The hypothesized model has been validated by the outcomes of the study. And, it was observed that these three predictors, that is, small savings schemes of the post office (SPO), financial literacy and behavior (FLB), and financial consultants (FC) have a significant positive influence on savings habits (SH). The model is acceptable as 74% variance of the dependent (endogenous) variable is explained by exogenous variables, since R2 for the model is 0.74 (Cohen, 1988; Falk & Miller, 1992). The results demonstrated that financial consultants (FC) are the important and effective predictor in influencing the savings habit, with a factor loading of 0.38 and an f-squared value of 0.353846, indicating a large effect size. Next to it, small savings schemes of the post office (SPO) and financial literacy and behavior (FLB) come with a small effect size of 0.023747 and 0.026316, respectively. Furthermore, it is found that financial consultants and small savings schemes (FC_SPO), and financial consultants, and financial literacy and behavior (FC_FLB) as interaction variables have a medium effect on savings habits. Therefore, the significant influence of the moderating variable, that is, financial consultants, cannot be refuted. Hence, it can be concluded that the financial consultant, as a moderating variable, has a synergistic influence on the savings habit. In light of this, the company employing financial advisors to promote its financial goods ought to see them as assets rather than liabilities.

Conclusion

The current study’s foundation was shaped by a thorough examination of the significant literature. This study examined the influence of predictors on building saving habits and the moderating effect of financial consultants in emerging nations like India. Few studies have shown the significant impact of predictors’, that are, small savings schemes of the post office, financial literacy and behavior, and financial consultants on the savings habit of people. This research work exhibited a significant association between the hypothesized variables (i.e., exogenous and endogenous). Furthermore, the study empirically examined the significant effects of predictors (small savings schemes and financial literacy and behavior) and the moderator (i.e., financial consultants) on the savings habit of people. To assess the influence of predictors on the savings habit, researcher employed SEM. Utilizing measurement and structural models, the data were statistically validated in order to measure the goodness of fit using various fit indices. Moreover, the study explores a good fit of data for both measurement and structural model supporting the proposed model. Among these three factors included in the study, financial consultant, and financial literacy and behavior have a significant influence on financial behavior (Christian et al., 2021; Grohmann, 2018; Khawar & Sarwar 2021; Toms et al., 2021), which is in line with our study. However, little study can be found as precedent in the Indian context to show the effect size of the predictors and interaction variables, that is, SPO_FC and FLB_FC. The study exhibits that the financial consultants as the moderating variable show a better effect size, that is, a large effect size (f-squared value = 0.1714) over the other two predictors, that is, small savings schemes of the post office and financial literacy and behavior when compared with individual predictors’ effect sizes. Furthermore, it demonstrates synergistic influence in developing saving habits as the moderator and exhibits the largest effect size compared to all other predictors. As a result, it can be concluded that financial advisors play a crucial role in moderating between small savings schemes offered by the post office (SPO) and people’s financial behavior and literacy (FLB) in terms of fostering saving habits. Furthermore, the current study also reveals the considerable contribution of financial consultants contribute to beneficiaries’ endeavors to achieve the sustainable development goals (SDGs) for economic and social development.

Since this area of study is still in its infancy, a thorough investigation may be conducted to ascertain the relative importance of different predictors, including emotion, moods, and other variables, in influencing savings behavior. Additionally, more research could be encouraged to examine the probable reasons why people are not actively participating in savings and investments.

Managerial Implications

The sole intention of the research was not to present support that the financial consultants individually, as predictor and moderator, influences savings and investment habits of people, but rather to explain the reality in this regard. The study will be more beneficial for financial institutions and other intermediaries in providing better services by giving due importance to the needs of the people. Further, it will contribute to the academic literature for enhancing the knowledge base and will provide a road map for the academic community to investigate further to gain a better insight into it.

Limitations of the Study

The major limitations of the study are the constraints of time and material resource requirements. Further, the survey is restricted to analyzing the moderation effect of predictor (i.e., financial consultants) only. The study can be improved by putting together different internal and external factors and by widening the scope of the study to examine the savings behavior of people.

Annexure

KMO and Bartlett’s Test.

Total Variance Explained.

Total Variance Explained.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.