Abstract

There is a widespread uncertainty regarding the usefulness of shareholder activism (SA) as a part of corporate governance for firms and banks. SA has wide acceptance across the board among all the stakeholders’ participation. Since banks are the backbone of any economy, any endeavor (support to SA) creating difficulty may boomerang. Such actions do more harm than good; therefore, it is imperative to determine whether SA is beneficial to the banks or not. In this study, the SA index is built for Indian banks. The data relating to bank performance and valuation is gathered for 2016–2019. Panel data econometrics is applied to determine the impact of SA on banks performance. Results reveal that SA impacts bank performance. Furthermore, transparency and disclosure significantly moderates the association of SA with the performance. However, SA is not impacting bank valuation. It is a unique study of its kind to provide insights on SA for the banking sector.

Introduction

Shareholder activism (SA) is a growing concern, especially in emerging economies. The extant literature on SA is skewed toward developed economies (Sarkar & Sarkar, 2000). Evidence shows that SA is in its infancy in emerging economies like India (Shingade et al., 2020). In a multi-country study on SA, Judge et al. (2010) show that the relevance and impact of SA differ as to the system of the law and income disparity changes. Therefore, SA has a varying influence on the firms belonging to the different nations. Before delving deeper into the issues of SA, its association with firms and society at large, it is pertinent to define SA. In the literature, SA is defined as the usage of ownership position to manipulate the company policy and practice (Judge et al., 2010; Rose & Sharfman, 2014; Sjöström, 2008). SA is believed to influence corporate financial performance (CFP) (Goranova & Ryan, 2014) and the firms’ functioning.

There is strong evidence that SA is also propagated by the block of shareholders having their vested interest overlaying the interests of the other shareholders. Bebchuk and Jackson Jr (2012) highlight this issue of the influence of block shareholders on corporate governance (CG) and disclosures of the firms, which is usually on the cost of the other shareholders. Briggs (2007) also emphasize the dubious role being played by block shareholders (at times in the connivance of institutional investor activism). They reveal that SA is instrumental, especially when the management control or takeover of the firms is concerned. Such evidence inheres to the concern of a few shareholders on the costs of the other shareholders. Cornelli and Li (1997) find evidence that the presence of large shareholders creates trouble in exercising management control. Such situations may not be in the welfare of the firms and their shareholders. Artiga González and Calluzzo (2019) highlight the principal to principal cost due to the presence of large shareholders (private benefits). Similar concerns of private benefits due to SA by the significant shareholder or shareholder groups (clustered shareholders or institutional shareholders) are reported by other studies (Bebchuk & Jackson Jr, 2012).

There is literature having SA focused on environmental issues (Clark & Crawford, 2012; Perrault & Clark, 2016; Yang et al., 2018) and social issues (King & Gish, 2015; O’Rourke, 2003; Sjöström, 2008). Some studies deal with SA having political connotations (Goranova & Ryan, 2014). SA having concerns for CG, private benefits, environmental, social, and political issues may not necessarily add anything concrete to the firm’s financial benefit. SA adds cost to the firm as firms have to react to the concerns raised by the shareholders’ activism. A firm’s goal is Shareholder Wealth Maximization (SWM) (Denis, 2016; Dobson, 1999). There are obvious questions on the sanctity of SA. Primarily when the issues of SA and its probable outcomes are not aimed at SWM; instead, it is diametrically opposite of it (Fox & Lorsch, 2012).

The tangible benefits to a firm or bank are viewed in two ways: operating performance and valuation. Thus, the study’s objective is to explore how SA influences the tangible measure of performance. Lack of clarity on the purpose of SA is the primary motivation for this study. Even if the SA has a genuine purpose, the question remains to be seen whether (a) it is being used in that spirit and (b) if it is delivering tangible benefits to the corporate. Corporate is perceived to chase the goal of SWM in their efforts to deliver goods, services, and whatever else they have to offer to their customers. Consequently, while changing SWM, corporate serves the twin purpose of doing good to themselves and everybody else in the fray (Parmar et al., 2010; Wright, 2001). An attempt is made through this study to determine whether SA helps banks in this or not.

In addition to these issues, it makes more sense to explore the issue of SA for the tangible benefits of the banks because of the following two reasons: (a) evidence of SA for banks are quite less and (b) banks are opaque by design (Cao & Juelsrud, 2020; Fosu et al., 2018; Jiang et al., 2016) and hence the association of SA for tangible gains of the banks should be handled differently as compared to the firms.

The findings of the paper present that SA influences the performance of the banks positively. The non-linear association of SA for return ratio contributes that it (SA) supports increasing the return ratios initially, and gradually the positive influence is tapered off. Furthermore, the current study significantly contributes by having empirical evidence of moderating the role of the disclosure on the association of SA for the bank’s performance. These findings of significant moderating role on SA for the performance of the banks are not observed earlier and ensure the novelty of the findings. The results have substantial managerial and policy implications as SA is in a relatively embryonic stage in the emerging economies, including India. The findings can be the tipping point. In consonance with the paper’s findings, it can be framed for more effectiveness, especially policies regarding SA and disclosures, which are yet to be firmed up and consolidated.

The rest of the paper is arranged to include the relevant literature, hypotheses formulation, data and methodology, results, discussion, contribution, implications, and conclusion.

Theoretical Framework, Literature Review, and Hypotheses Formulation

Shareholder Activism: A Historical Perspective and Current Status

We do not have any formal announcement or date of commencement of shareholder activism (SHA) across the world. There is some evidence in 1980 that shareholders used shareholder proposals to bring forth their concern mainly centered at governance issues in the firms as the starting point (Karpoff, 2001). Smith (1996) also highlights shareholder proposals to raise the shareholders’ concerns. However, the main involvement of SA starts with the activities of the institutional investors, especially in the developed nations (Gillan & Starks, 2000; Proffitt Jr. & Spicer, 2006). Hedge funds were the leading contenders among the institutional investors who took the baton of SA and tried to make the change during the initial phase (Cheffins & Armour, 2011).

Broadly, as discussed earlier, SA can be categorized into governance-related (including both financial and non-financial), social, environmental, and political issues. Among all the four categories mentioned above, the various issues raised can also be clubbed under the following four groups (Shingade & Rastogi, 2020): (a) board of director related matters, (b) executive/senior management related matters including their compensation, (c) financial performance and valuation-related issues, and (d) idle cash and capital structure-related issues. However, one more issue that is quite often discussed implicitly is the SA targeted for takeover (or management control). SA may be camouflaged in any category mentioned above or groups. It carries the intention of a management change or takeover bid (which is hostile) (Armour et al., 2011; Black, 1992; Pound, 1992).

Earlier in India, separation of ownership with management was missing, attempts to hostile takeover were less, and institutional investors were either not united or not active as shareholders (Sridhar, 2016). SA in India is still in its early stages (Shingade & Rastogi, 2019; Shingade et al., 2020). A lot has been changed gradually regarding SA due to (a) changes in the regulation and legislation concerning SHA, (b) succession issues become rampant, balance sheets are over-levered, and (c) international investors become part of the shareholders of the Indian firms (Sarkar & Sarkar, 2000; Varottil, 2012). The most crucial change is introduced in India concerning SHA is the amendment of The Companies Act and introduction of a revamped version of it—The Company Act, 2013 (Aggarwal et al., 2020; Das & Dey, 2016; Manchiraju & Rajgopal, 2017). Necessary among them is the provision of defining minority shareholder and their rights to present shareholder proposals to raise their issues and provide for the class action. Subsequently, many reforms were implemented by Securities Exchange Board of India (SEBI) to give more teeth to SA in India. Important among them are voting methods-allowing ballot voting and letting intermediation by international institutional investor groups like Institutional Shareholder Services (Sarkar & Sarkar, 2000; Sridhar, 2016; Varottil, 2012).

SA and Non-Performing Assets of the Banks

We did not observe many studies on the association of SA and non-performing assets (NPA) in the banks. Becht et al. (2011) aptly present that the issue of governance in a bank is different from the other firms. The study focuses on the post-crisis of 2007–2008 and highlights the governance dissimilarities between financial (a bank) and non-financial firms. Roman (2015) links the SA with the banks’ risk-taking. He uses the Altman Z score (Altman, 1977) as a proxy for risk-taking in banks. Although distress in the bank is not only due to NPA but they also are reasonably related. He presents that SA does not help reduce the financial distress in the banks, but it increases banks’ risk-taking. He presents that governance issues due to conflict of varied reasons between shareholders, managers, and creditors are significantly impacted by SA. Managers have their governance approach, leading to shareholders’ involvement in the form of SA (Malmendier & Tate, 2008; Srivastav et al., 2018).

However, no study links the SA to NPA directly, and there are incontrovertible issues of governance in the banks, which have direct linkages to the financial distress in the banks (Barakat & Hussainey, 2013; Chen & Lin, 2016; Wanderi, 2016). NPA in itself is a significant issue in the banks (Joseph & Prakash, 2014; Mamatha & Shivaraj, 2016; Shajahan, 1998). Hence, it is appropriate to look for empirical evidence on how SA influences the NPA or distressed assets in the banks. Thus, the following hypothesis is constituted in the alternate form for the empirical testing:

H1: SA impacts in reducing the NPA in the banks.

SA and Earnings Management

Significant associations between SA and the operating performance of firms are easily found in the literature (Goranova & Ryan, 2014). There is equivocal evidence that SA have positive (Hadani et al., 2011), negative (Prevost & Rao, 2000), and no impact (Wahal, 2009) on the operating performance of the firms. There is a veritable lack of unanimous literature on the association of SA with the operating performance of the banks. Roman (2015), in a study on US banks during 1994–2010, finds that SA does not influence the operating performance of the banks. Loderer and Zgraggen (1999), in the classic example of SHA and its influence on CFP, find evidence that substantial shareholders can detriment the interests of the banks for their vested interests. Another epitomized and definitive study by Ferreira et al. (2021) and Ferreira et al. (2013) show that SA can create troubles in the crisis management of the banks. Managers, insulated by SA, can ensure better performance during bank crises, and may have a lesser probability of bailouts than the cases where managers are not insulated.

We find literature where CG significantly and positively influences the CFP in the banks. Barako and Tower (2007) present that board and government ownership have negative, foreign ownership positive, and institutional ownership no impact on the CFP of Kenyan banks. Elyasiani and Jia (2008) evince that institutional investors do effect the CFP of the banks in the United States, but they have a lesser influence on the CFP of the equivalent firms. The reason is the regulatory mechanism of the banking sector. A study on the Russian banks during the period of the financial crisis of 2008 (Orazalin et al., 2016) finds CG to significantly influencing the CFP of the banks except during the crisis. Moreover, the influence is increased after the crisis. Furthermore, the impact of SA on the CG is widely accepted in both firms (Fabrizio et al., 2019; Souha & Anis, 2016) and among banks (Deudon et al., 2015; Dube & Mkumbiri, 2014). Since SA impacts the CG (in banks too) and CG impacts the CFP in banks, it can be postulated easily using the deduction that SA would impact the CFP in the banks too. However, this deduction needs empirical vetting. Hence, the following hypothesis is formulated in an alternate form.

H2: SA supports banks’ CFP.

SA and Valuation of the Bank

SA is supposedly linked to CG-based issues. CG is undoubtedly impacting the valuation. Therefore, this can easily be deduced that SA would impact the valuation, which is affirmed by the eclectic research findings, albeit on the firms. There are two significant points related to the current research on SA and valuation that need further exploration. First, there are abysmally low or almost no studies on SA leading to impacting the valuation of the banks. There is literature on SA impacting the valuation. However, all such studies are for the firms, not exclusively for the banks. Roman’s (2015) is the only study focused on SA and its impact on the banks. He finds evidence that SA significantly influences the bank value. Other than Roman (2015), we do not observe any other study which links SA with the valuation of the banks.

Second, the evidence concerning SA and firm value (not banks) are there, but they are equivocal and lack unanimity. One set of studies presents that SA adds value to the firms (Alexander et al., 2010; Brav et al., 2008; Cai & Walkling, 2011). Another set of studies exhibits the findings diametrically opposite that SA depletes the firm’s value (Clifford, 2008; Edmans, 2014). The third and last set of studies finds no significant association of SA on the value of the firms (Gillan & Starks, 2000; Karpoff et al., 1996).

It is evident that both the issues still prevail: lack of evidence of SA supporting banks’ value and the lack of unanimity on the existing findings of SA on the value of the firms. It is prudent to look for fresh evidence. Hence, the following hypothesis is formulated in the alternate form for the empirical testing:

H3: SA supports the valuation of the banks.

SA and Performance of the Banks: Moderation by Disclosures

As discussed in the previous section, it is evident that the literature on SA and CFP is scarce. However, bank performance, whether measured in terms of NPA or CFP (Rastogi et al., 2021), has issues of CG and transparency and disclosure (TD) linked to it (Grassa et al., 2019; Younas et al., 2021). Issue of TD goes even to the extent of even having an impact on the financial distress in banks (Baklouti et al., 2016; Halteh et al., 2018; Wanke et al., 2015) and bank failures (Flannery et al., 2013; Manganaris et al., 2017; Moosa, 2010). Bank opacity is an accepted reality, and it is present in the banks by design and not by choice (Fosu et al., 2018; Fosu et al., 2017; Morgan, 2002). The significance of TD in the bank operations and performance makes it apt to postulate that TD can influence the association of SA and the performance of the banks. This premise makes sense irrespective of the relationship between SA and the performance of the banks. Therefore, the following hypothesis is formulated in the alternate form for empirical testing.

H4: TD moderates the association between SA and banks’ performance.

Data and Methodology

Data and Sample

The study utilizes secondary data from a sample of 34 banks listed in India. Four years of data from the financial year (FY) 2015–2016 to FY 2018–2019 is collected for analysis in this study. CMIE Prowess is the primary data source, while the financial statements and annual reports were used to fill in a few missing data points. Thus, 4 years of data for 34 banks formed 34 × 4 = 136 bank year observations for analysis are used. Reforms in recent years signify the policymakers’ motivation toward rebalancing the Indian banking arena, mainly to reduce the NPAs that has remained a long-standing challenge (Singh, 2013). The Ministry of Finance, in its Economic Survey 2015–2016, proposed four Rs—recognition, recapitalization, resolution, and reform—to address the problem of NPAs. Consequently, according to the Reserve Bank of India data in 2019, the NPAs have shown a significant downward trend. Therefore, 4 years of data from FY 2015–2016 (denoted as 2016, for brevity) till FY 2018–2019 (denoted as 2019, for brevity) includes the richness of insights and implications for the banking sector from such recent policy initiatives. In econometrics terms, panel data (though for a short period), is capable of providing richer insights, as compared to simple cross-sectional or time series analysis, provided the methodology used is justified (Kim et al., 2018; Lai et al., 2014; Singh & Rastogi, 2022).

Variables

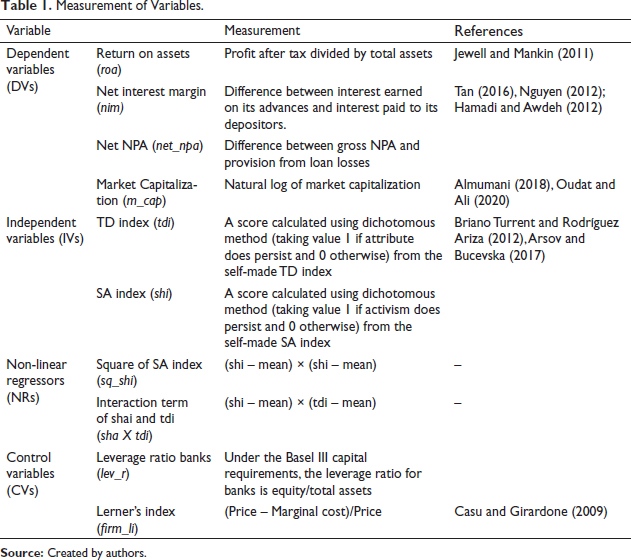

The variables used in this study are reported in Table 1. The dependent variables include return on assets (roa), net interest margin (nim), net NPA (net_npa) and market capitalization (m_cap). Two independent variables included in this study are measures of CG, defined as two indices, namely the SA index (shi) and the TD index (tdi). In addition, two non-linear variants of the independent variables are included as regressors in this study. First, a square term (sq_shi) of the SA index (shi) is included to test if a non-linear relationship exists between shi and the included dependent variables. The square term (sq_shi) is calculated by first demanding the variable shi and then squaring the demanded value (McIntosh & Schlenker, 2006). Second, an interaction term (product term), shi X tdi, is included as a regressor to test if tdi moderates the relationship between shi and the selected dependent variables. The regression models include two control variables: leverage ratio banks (lev_r) and Lerner’s index (firm_li). The variable firm_li represents an inverse proxy for market competition and is measured as price-cost margin. This method to proxy product market competition follows the work of Choua et al., 2011).

Measurement of Variables.

Descriptive Statistics and Multicollinearity

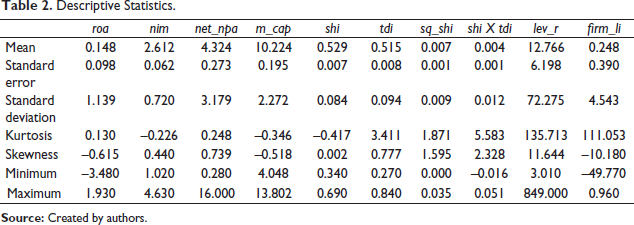

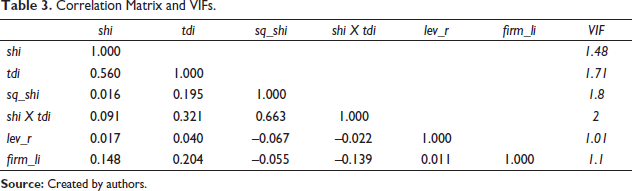

Table 2 presents the descriptive statistics of the sample. Table 3 presents the regression coefficients and variance inflation factors (VIFs). Notably, the VIFs for all the regressors are less than 2, an acceptable value. The possibility of multicollinearity was not a concern.

Descriptive Statistics.

Correlation Matrix and VIFs.

Model Specification

We specify the random effects models based on the significance of the Hausman test (p > .05, in all cases, see Table 4). In general, the random effects model is specified as:

where,

The models specific to this study are:

In addition, for the valuation variable, both the Hausman test (p > .05) and the Breusch Pagan Lagrange multiplier test (p > .05) were insignificant. Therefore, Pooled OLS regression is used to examine the impact of independent variables on the m_cap. The OLS Model, in general, is stated as follows:

where,

The pooled OLS model specific to this study is, therefore, specified as:

Analysis and Results

Regression and Diagnostics

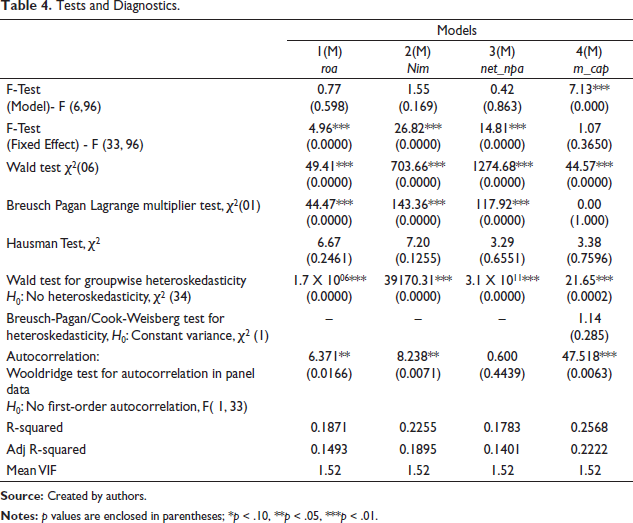

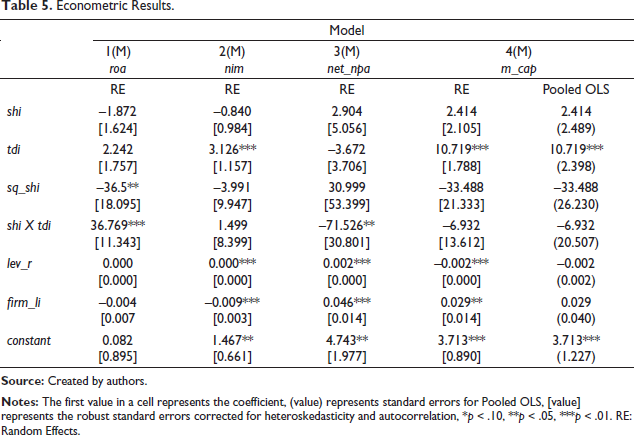

Panel data regression was used to conduct the econometric analysis. The selection between fixed effects and random effects models (for models 1 to 3) followed the Hausman test, which was insignificant (p > .05). The failure to reject the null indicated random effects were present; hence, the random effects models were preferred (Baltagi, 2013). Table 5 includes the regression outputs.

The diagnostics revealed the presence of heteroskedastic and autocorrection of order one. Therefore, we calculated robust standard errors following Wooldridge (2012). Table 4 includes the diagnostics.

The selection of pooled OLS model (Model 4) follows from the insignificance of the Hausman test (p > .05) and the Breusch Pagan Lagrange multiplier test (p > .05). In addition, the diagnostics revealed that the Wald test was significant while the Breusch-Pagan/Cook-Weisberg test for heteroskedasticity was insignificant. Therefore, we report the normal and standard errors and the robust standard errors for Model 4 (see Table 4). Interestingly, the significance of both the variables of interest (shi, tdi, sq_shi, and shi X tdi) remain the same in both cases.

Tests and Diagnostics.

Econometric Results

Table 5 presents the regression results. The results of the models [1(M), 2(M), 3(M), and 4(M)] indicate that shi is not significant on any of the selected dependent variables roa, nim, or net_npa. The variable tdi is insignificant on roa and net_npa but positively significant on nim at a 1% significance level. In addition, the variable tdi is positively significant on m_cap at a 1% significance level, but shi is not significant on m_cap.

Econometric Results.

Among the non-linear regressors, the square term sq_shi is negatively significant on roa at a 5% significance level. However, sq-shi is significant on nim, net_npa, and m_cap. The interaction term shi X tdi is positively significant on roa at 1% significance level and negatively significant on net_npa at 5% significance level. The interaction term is, however, insignificant on nim and m_cap.

Endogeneity and Robustness

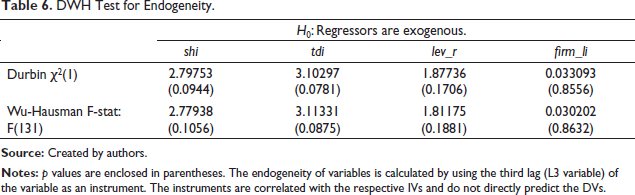

The literature signifies that the problem of endogeneity may cause the estimates to be biased. Therefore, we applied the Durbin-Wu-Hausman (DWH) test to check the presence of endogeneity. The results reported in Table 6 rule out the endogeneity of variables in this study. Furthermore, we found that none of the independent regressors was prone to endogeneity issues as DWH tests are insignificant.

DWH Test for Endogeneity.

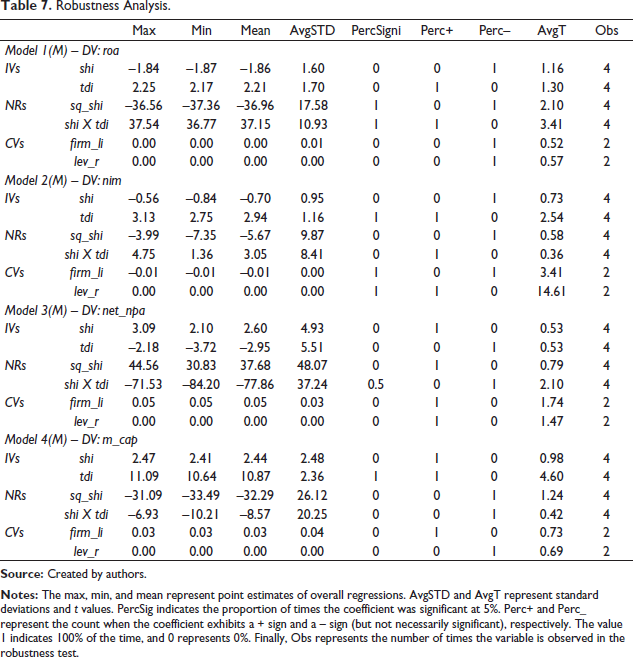

Finally, we conducted a succession of probit regressions to check the sensitivity of the estimated coefficients to the omission of control variables to the robustness of econometric results (Barslund et al., 2007). Table 7 presents the robustness results. The regressor variables of interest were robust, without any sign change against all combinations of control variables included in the series of regressions conducted.

Robustness Analysis.

Discussion

Hypothesis Testing and Comparison with Earlier Research

The present study aims at determining the association of SA on the performance of the banks. The four hypotheses are framed for empirical testing to serve the study’s objectives. The first hypothesis that SA helps reduce the NPA is rejected due to the lack of supportive evidence (Table 5). There is no evidence in any of the four models of significant association of SA with NPA. The second hypothesis that SA supports the operating performance of the banks cannot be rejected. We find a negative non-linear association between the two (Table 5). As a result of non-linear significant negative association, it can be construed that at the low levels of SA, roa would increase. However, the association between SA and roa will taper down beyond a point. The third hypothesis that SA supports valuation is rejected due to a lack of supporting evidence (Table 5). The fourth and last hypothesis of the moderating role of TD for the association between SA and the performance of the bank cannot be rejected (Table 5). The moderating term of SA and TD (sha X tdi) is positively significant with roa and negatively significant with NPA. With the increased disclosures, SA helps in better operating performance and lower levels of NPA.

Literature on the association between SA and the performance of the banks is relatively scarce (as discussed in second section). We could observe only one study Roman (2015), on the topic. The findings of the current study contradict the finding of Roman (2015) in all aspects. He presents that SA increases the banks’ financial distress (risk-taking). However, we present that SA, along with TD, significantly helps in reducing the NPA in the banks. He presents that SA does not influence the operating performance of the banks, whereas we find SA along with TD significantly and positively influences the operating performance of the banks. The contradiction persists even for SA’s influence on the valuation of banks. In contradiction with his findings, we find no association between SA and banks’ value. The difference between Roman (2015) and our findings can be explained. It may be due to the differences in developed and emerging economies as the countries of the respective studies and the different law and regulatory environments.

Contribution and Implication

This study is the first of its kind. We do not observe any other study on this topic on emerging economies, including on India. Roman (2015) limits itself to the impact of SA on operating performance, risk, and valuation.TD is added in the current study as a moderator to the association of SA with performance and valuation. This advancement is also not observed in the literature. This study is a significant improvement to the earlier work because TD plays a vital role in the regulatory setup of banks across the world. The findings of this study can be generalized for other developing or emerging economies. The scope of the study is for all the emerging economies where SA is in nascent stages, similar to India.

One of the main implications of the study is to answer a perplexing question about the role of SA in the banking sector. The findings of the current study answer the question in unequivocal terms that SA influences the operating performance of the banks. SA and TD can significantly help improve the return on investments and reduce the stressed assets in the banks. Furthermore, this study emphasizes that SA does not impact the valuation of the banks even with the interaction of TD. SA fails to influence value in the banks.

The findings of the current study provide a roadmap to both managers and policymakers to accept the significant role of SA in improving the performance of the banks. The current study’s findings provide one more reason to support TD in the Banks. The study’s findings will let the policymaker and regulatory bodies design the eco-system favoring the mechanism of SA for the betterment of the banks, including TD.

Conclusion

This study aims to determine the role of SA on the performance of banks in India. As expected, it is found in the study that SA supports the performance of the banks. The supporting feature of SA for the performance of banks can further be enhanced through TD. However, we do not find any association of SA on the value. This study is critical and significant as no other study is found on the association of SA on the performance of the banks in emerging economies, including India. The study’s implications are pretty significant, and it can help set the overall policy on SA and TD in a bank. The regulatory framework can redirect itself to incorporate the study’s findings to better the banking sector. The study’s findings can be extended to other industries or sectors equally regulated and have broader public involvement, similar to banking.

One of the limitations of the study is a small panel. Due to various reasons, including the availability of TD data, significant churning in the banking sector in India, and massive involvement of digitalization recently, we decide to use the panel of 4 years only. However, we did the data analysis keeping the short-panel in mind. Despite that, we believe that the results can be influenced by replicating the analysis on a large panel. This limitation can be taken care of in some future studies.

Based on the study findings, we recommend a more effective and flexible SA mechanism in emerging economies, including India. SA is an offshoot of CG mechanism in the firms, including banks. SA is debatable for its utility and hence may not be appreciated by the management of the banks. SA can be viewed as a problem or a cost by the management of the banks. However, the findings of the current study can help break such stereotypes. Keeping in view the high risks involved in the banking sector and stakes of the general public, a robust mechanism of SA may significantly improve the performance of the banks and improve the trust of the people in the banking sector. TD is already part of the upgraded regulatory framework of the banking sector. SA can enhance it further to the next level.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.