Abstract

Financial identity formed during emerging adulthood is important for the regulation of youth financial behaviors, decisions, and long-term financial goals. This three-wave short-term longitudinal study investigates how youth develop a distinct manner of approaching and managing personal finances and reveals the structure and dynamics of financial identity development during emerging adulthood. Using the cross-lagged panel model analysis, it also investigates longitudinal reciprocal associations between financial identity processes, financial behaviors, and financial well-being of emerging adults. The sample consists of 533 Lithuanian higher education students (56.8% women; Mage = 18.93, SDage = 0.71) who took part in three assessment waves. The findings support the use of the three-factor model of financial identity formation and show that financial identity formation is shaped by emerging adults’ financial situation and contribute to the formation of financial behaviors and financial well-being. Practical implications of study results are also discussed.

Keywords

Developing the ability to engage in positive financial behaviors to achieve financial goals is considered a major developmental task for emerging adults (Serido et al., 2013). While it promotes financial and overall well-being (Ranta & Salmela-Aro, 2017; Serido et al., 2013), it also contributes to the achievement of independence in the life domain of personal finances (Butterbaugh et al., 2019), which is an important milestone on the road to adulthood (Arnett, 2014; Li et al., 2019). However, emerging adults engage in positive financial behaviors in different ways.

Emerging adults differ in how much they care about obtaining money management skills or how much they explore the possibilities of personal finance management (Bosch et al., 2016; Sorgente et al., 2020). The similarity between the process of developing financial skills and the process of general personal identity formation (the main psychosocial task for adolescents and emerging adults; Arnett, 2014) has been underlined by some authors (Bosch et al., 2016; Shim et al., 2013). The construct and a measure of financial identity status were introduced (Shim et al., 2013) to study emerging adults’ distinct manner of approaching and managing personal finances. Subsequent studies of financial identity status led to important insights into the formation of positive financial habits and how financial identity contributes to financial well-being; however, very few studies used a longitudinal approach to study these associations (Bosch et al., 2016; Shim et al., 2013; Sorgente et al., 2020; Vosylis & Erentaitė, 2020). Thus, the directionality of effects is in question. That is especially so given that financial identity was operationalized using the identity status approach, and very few studies have addressed the factors that drive the processes of financial identity development.

The present study seeks to expand and extend this line of research and has two interrelated objectives. The first aim is to investigate financial identity by adopting the process approach to financial identity formation (Crocetti et al., 2008). The second one is to longitudinally test the relationships between financial identity processes, engagement in positive financial behaviors, and financial well-being. That is, our study examines how emerging adults’ financial condition and positive financial behaviors contribute to financial identity formation and how financial identity contributes to positive financial behaviors and financial well-being. We address these questions by using a three-wave short-term longitudinal design and by studying individuals who are in the early years of emerging adulthood. This is the period when individuals become independent from the perspective of social and legal responsibility and are forced to take responsibility for their behaviors (Tanner, 2006). During this period, emerging adults also begin to gradually attain financial independence (Arnett, 2014), and skills related to personal finance management become increasingly important (Serido et al., 2013).

Financial Identity

The period of emerging adulthood (years 18–25/29) is a time of intensive identity exploration (Arnett, 2014) and the period of life when most individuals assume financial responsibilities and achieve independence in personal finance-related decision-making (Butterbaugh et al., 2019). In fact, achieving independence from parental financial support is one of the most important markers for reaching adulthood (Arnett, 2014). Success in making this transition, however, depends on one’s level of financial skills and the manner in which a young person approaches financial responsibilities (Shim et al., 2013). According to the developmental model of financial capabilities (Serido et al., 2013), which we use as a framework in our study, knowledge, attitudes, and behaviors required for effective management of personal finances are indicators of financial capabilities, and the outcome of financial capability development is financial well-being. To explain the different ways in which emerging adults approach financial issues, manage personal finances, and handle financial responsibilities, the concept of financial identity was proposed (Shim et al., 2013).

To operationalize financial identity, researchers utilized one of the most widely recognized models in personal identity research—the classical identity status model. This model, grounded in Erikson’s writings on the salience of personal identity formation in adolescence (Erikson, 1963), specifies personal identity development in terms of two processes: exploration and commitment. Based on the presence or absence of these processes, this model also differentiates four possible identity statuses (Marcia, 1966). In line with this model, there were also assumed to be four financial identity statuses: achieved, foreclosed, moratorium, and diffused. The first two reflect existing commitments to a financial management style. However, in the achieved status, these commitments were made after exploring some alternatives, while the foreclosed status involves the adoption of the default—one’s parents’ style of managing personal finances. The latter two statuses involve the lack of commitment to any specific financial management style. However, the moratorium status is characterized by engagement in the exploration of alternative financial management styles, while the diffused status is characterized by a lack of interest in finding one’s financial management style (Bosch et al., 2016; Shim et al., 2013; Sorgente et al., 2020).

Research on financial identity indicates that it plays an important role in the development of financial behaviors (Shim et al., 2013), and contributes to the financial and overall well-being of emerging adults (Sorgente et al., 2020; Vosylis & Erentaitė, 2020). In particular, achieved status was linked with favorable financial behaviors and other positive outcomes, while foreclosed status was not, suggesting that developing a style of financial management after a deliberate personal exploration of alternatives is a much more effective approach than simply adopting one’s parents’ style (Shim et al., 2013; Sorgente et al., 2020). Moreover, lack of commitment to any money management approach (diffused and moratorium statuses) was found to be linked to problematic functioning in the domain of personal finances (Shim et al., 2013; Sorgente et al., 2020; Vosylis & Erentaitė, 2020).

One limitation of existing financial identity research is that the majority of it is cross-sectional rather than longitudinal (see Shim et al., 2013; Sorgente et al., 2020; Vosylis & Erentaitė, 2020). This does not permit determination of the directionality of effects in relationships between financial identity and its hypothesized antecedents and outcomes. For example, from the perspective of a developmental model of financial capabilities (Serido et al., 2013) financial identity can be viewed as a set of “self-beliefs” that improves financial behaviors and promotes financial well-being. However, in identity research, the links between identity formation and developmental outcomes are considered to be bi-directional, i.e. the unsuccessful formation of identity can contribute to less favorable developmental outcomes, but developmental issues can also impair the identity formation process (see Becht et al., 2019; Klimstra & Denissen, 2017; Schwartz et al., 2011).

Drawing a parallel to the financial domain, it has been argued that financial identity formation can lead to changes in financial behaviors and well-being (Shim et al., 2013), a view with which we concur. However, we speculate that one’s financial condition (or a sudden change in it), as well as practiced financial behaviors, can also trigger shifts in commitment and intensify the process of exploration of alternative ways of managing personal finances. Given that instability in many areas of life is characteristic of many emerging adults’ lives (Arnett, 2014), we further speculate that this period is also saturated with life changes (e.g., exit from parental home) that impact emerging adults’ financial situation and may create a necessity to rethink their approaches to managing personal finances. Shedding more light on these reciprocal associations, however, requires a longitudinal investigation.

Financial Identity Processes

While financial identity studies have mostly relied on a status approach, we believe that this line of inquiry could also be meaningfully supplemented by taking an approach proposed in newer process-oriented models of identity formation. In particular, based on some criticisms of the identity status model (Bosma & Kunnen, 2001; Crocetti & Meeus, 2015; Kunnen & Metz, 2015), we suggest that financial identity statuses are best suited to capturing the outcome of the financial identity formation process at a given moment in life. That is, the status approach and the Financial Identity Status scale (Sorgente et al., 2020) developed to assess financial identity statuses target a theoretical configuration of exploration and commitment processes, but not the actual processes. As such, it is not particularly suitable for capturing and investigating factors that drive the processes of exploration and commitment. Studying these processes, on the other hand, could shed more light on life circumstances that lead to such outcomes.

While a few alternative process-oriented views on identity formation exist (see Luyckx et al., 2008, for an alternative model), the three-factor model (Crocetti et al., 2008) may be the most parsimonious one for financial identity formation research. This model assumes that two iterative cycles underlie identity development (formation and evaluation) and conceptualizes three core processes involved in identity development. Commitment reflects a process of making, holding on to, and enacting life domain-specific choices. In-depth exploration reflects a process of active reflection of the enacted commitments. Reconsideration of commitment reflects a process of comparison of current commitments to possible alternatives and efforts to change them (Crocetti, 2018; Crocetti et al., 2008). In line with this model, the three processes in the financial domain of life could be defined as (a) the process of making and holding on to a certain manner of managing personal finances (commitment), (b) the process of active reflection on current financial management practices (in-depth exploration), (c) and the process of comparison of current commitments to possible alternatives emanating from dissatisfaction with the current manner of personal finance management (reconsideration of commitment).

Several important assumptions of the three-dimensional model that make this model distinct from the status approach are worth mentioning. First, this model distinguishes between two processes of exploration that contribute to the two commitment development cycles: reconsideration, which contributes to the commitment formation cycle, and in-depth exploration, which contributes to the commitment evaluation (or maintenance) cycle. Studies on identity formation in other life domains tested and found support for this differentiation (e.g., Crocetti et al., 2015; Karaś et al., 2015; Zimmermann et al., 2012).

Second, instead of lack of commitment (as hypothesized in the status model), the three-dimensional model assumes that identity crisis starts when existing commitments are deemed unsatisfactory and the process of reconsideration is initiated (Crocetti, 2018). As such, this model also predicts that reconsideration weakens existing commitments, while the presence of strong commitments weakens reconsideration (Crocetti et al., 2008). International cross-sectional and longitudinal studies on general and educational identity also support these predictions (e.g., Becht et al., 2017, 2021; Crocetti et al., 2015, 2008; Karaś et al., 2015; Pop et al., 2016; Zimmermann et al., 2012). Third, the three-factor model assumes that the process of in-depth exploration requires at least some commitments to be present, and as such, it predicts that stronger commitments strengthen this (in-depth exploration) process.

Finally, in-depth exploration is hypothesized to have a dual nature: it can either further strengthen existing commitments or lead to reconsideration, i.e. a reevaluation of current commitments (Crocetti, 2018; Crocetti et al., 2008). In line with these predictions, findings of person-oriented studies show that individuals characterized by high in-depth exploration are also characterized by high commitments (see Crocetti & Meeus, 2015, for an overview). Results of variable-oriented longitudinal studies, which investigated reciprocal associations between identity processes in the educational and interpersonal domains, showed that commitment strengthens in-depth exploration, while in-depth exploration strengthens commitments (Becht et al., 2021; Pop et al., 2016). The association between in-depth exploration and reconsideration is somewhat less clear. A longitudinal study that measured variables at longer time intervals than prior research (around 4 months) found that the reconsideration process can indeed strengthen in-depth exploration (Pop et al., 2016), while an intensive longitudinal study with short periods between measurement occasions (daily measurements) found that in-depth exploration can reduce reconsideration (Becht et al., 2021) However, in general, reciprocal longitudinal links between these three processes are somewhat less well-documented. Furthermore, to our knowledge, longitudinal associations between these processes in the financial domain have never been studied.

The Current Study

The goals of the current study are two-fold. The first goal is to investigate financial identity by adopting the three-factor model of identity formation (Crocetti et al., 2008) to capture identity formation processes in the domain of personal finances. The second objective is to investigate longitudinal relationships between financial identity processes and engagement in positive financial behaviors and levels of financial well-being in emerging adulthood.

To achieve these goals, first, we adapted a set of items from the U-MICS (The Utrecht-Management of Identity Commitments Scale) questionnaire that we considered most suitable to assess the three financial identity processes and tested the previously discussed assumptions of the three-factor model. In particular, we examined whether a three-factor structure was present and hypothesized (H1) that a three-factor model would have a better fit than two- and one-factor models.

To further test identity model assumptions, we investigated longitudinal reciprocal relationships between the three processes of financial identity. Based upon the predictions of the three-factor model and the results of previous studies (e.g., Crocetti et al., 2015, 2008; Pop et al., 2016) we hypothesized that, over time, (H2) higher reconsideration would weaken existing commitments. We also hypothesized that, over time, (H3) stronger commitments would weaken reconsideration of commitments. As the process of in-depth exploration requires at least some commitments to be present, we also hypothesized that (H4) stronger commitments would strengthen the in-depth exploration process over time. Finally, we hypothesized that over time, the in-depth exploration process would strengthen (H5) identity commitments and (H6) reconsideration of commitment.

Finally, we investigated longitudinal reciprocal relationships between three financial identity processes and positive financial behaviors and financial well-being. This analysis is aimed at shedding more light on the directionality of effects in the relationships between financial identity and its assumed antecedents and outcomes, taking into account the identity process and not identity status. While doing so, it also examines how favorable financial behaviors and financial well-being contribute to financial identity formation, and vice versa. In terms of positive financial behaviors, we target financial planning, saving, cash-flow monitoring, and control over spending, as they are most relevant for emerging adults living in the European context. While many U.S.-based studies address behaviors related to the use of credit cards (Serido et al., 2013), we do not consider them relevant, as most European emerging adults rely on debit cards (in 2017, credit card ownership among 15–24-year-olds living in eurozone countries and Lithuania was 18% and 14.4%, respectively; World Bank, 2018). To address levels of financial well-being, we targeted income, parental financial support, financial strain, and financial satisfaction (methods section provides definitions). While we did not specify any exact hypothesis regarding the associations between financial identity processes and financial behaviors and well-being, we expected to find some reciprocal associations between these dimensions.

The data for the study was collected in Lithuania, a country located in North-Eastern Europe. Earlier generations of Lithuanian emerging adults, especially those who lived through their emerging adulthood years during and after the 2008 global financial crisis, have experienced relatively high levels of poverty, underemployment, and delayed exit from the parental home. However, in very recent years, the economic situation of Lithuanian emerging adults has substantially improved. In terms of indirect indicators of economic well-being and timing of adulthood transitions, the Lithuanian emerging adult population became more similar to European averages. Based on Eurostat data for 2018, around 69% of Lithuanian 20–24-year-olds were living in the parental home, which is just below the EU (European Union) average of 77% (Eurostat, 2020a). Around 50% of Lithuanian 20–24-year-olds were employed, which, again, is very close to the EU average of 51% (Eurostat, 2019). Also, around 21% of Lithuanian 20–24-year-olds were considered at risk of poverty (compared to the EU average of 28%; Eurostat, 2020b).

Method

Participants and Procedures

The data for this study come from a larger research project that examined the development of financial capabilities among Lithuanian emerging adults, as well as the antecedents of this process and its outcomes (Vosylis & Klimstra, 2020). In total, 533 emerging adults (57.2% women; Mage = 18.94, SDage = .73, range 18–21 years), freshly enrolled in a diverse set of programs at three higher education institutions, took part in this three-wave short-term panel study, which covered the first academic year in college or university. The three assessments took place in October 2018, February 2019, and May 2019, with an average timespan between them of 13 weeks. Participants signed consent forms and completed an online questionnaire after being informed about the purpose and length of the study, the content of the survey, and the intended use of the data. Participants were not rewarded for participating in the first assessment, but were rewarded with small (worth of ∼1 euro) and larger (worth 5–6 euro) prizes in the second and third assessment, respectively.

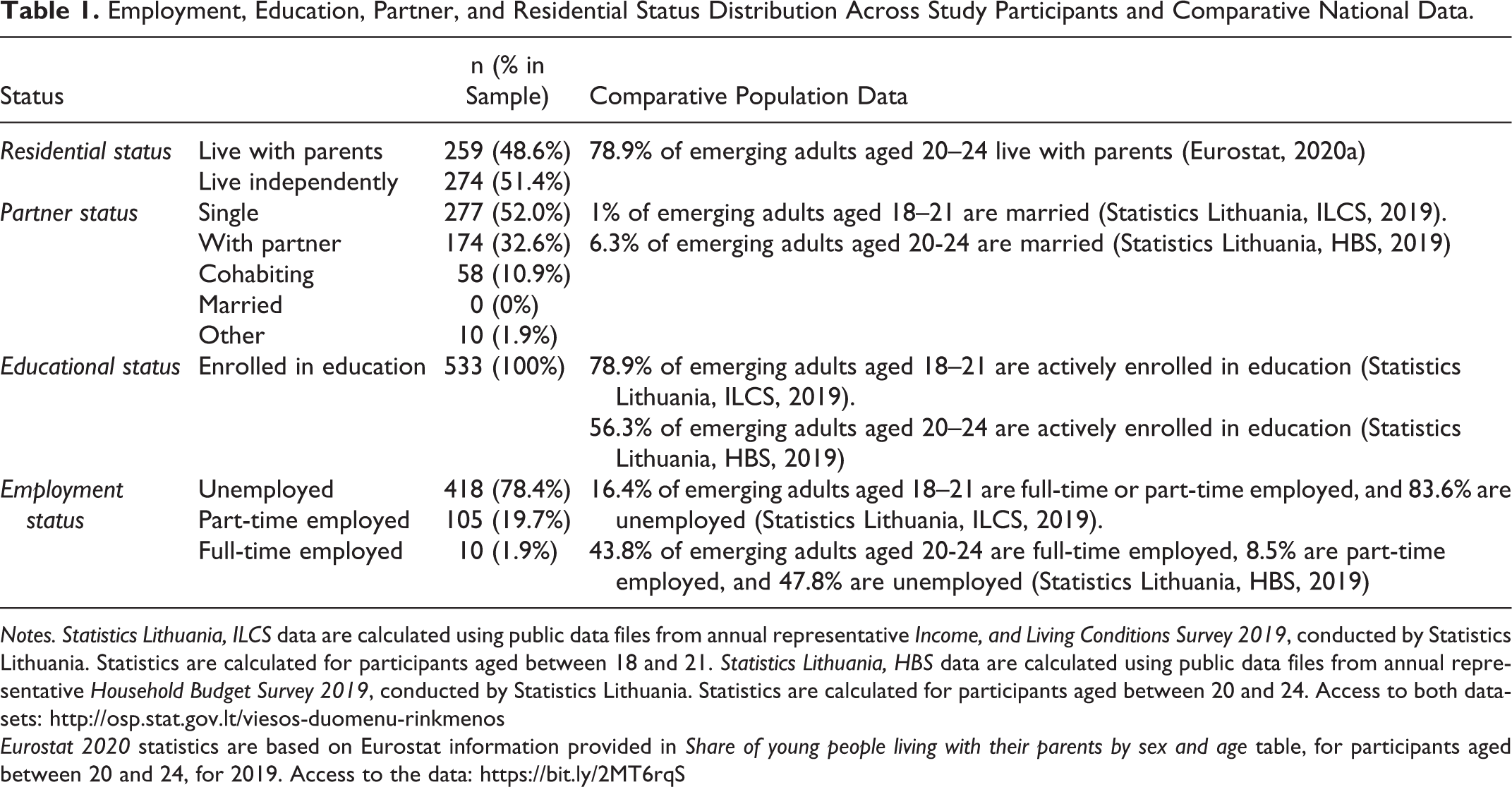

At the start of the study, around half the participants were living with their parents and around a fifth (22%) were employed. Most (87%) received at least some financial support from their parents and around a third (36%) were completely dependent on it. Table 1 provides more details on study participants’ demographic characteristics and some comparative population data.

Employment, Education, Partner, and Residential Status Distribution Across Study Participants and Comparative National Data.

Notes. Statistics Lithuania, ILCS data are calculated using public data files from annual representative Income, and Living Conditions Survey 2019, conducted by Statistics Lithuania. Statistics are calculated for participants aged between 18 and 21. Statistics Lithuania, HBS data are calculated using public data files from annual representative Household Budget Survey 2019, conducted by Statistics Lithuania. Statistics are calculated for participants aged between 20 and 24. Access to both datasets: http://osp.stat.gov.lt/viesos-duomenu-rinkmenos

Eurostat 2020 statistics are based on Eurostat information provided in Share of young people living with their parents by sex and age table, for participants aged between 20 and 24, for 2019. Access to the data: https://bit.ly/2MT6rqS

Participant retention rates were 84% (n = 448) and 77% (n = 411) at the second and third assessment, respectively. While Little’s (1988) MCAR test, conducted with variables in this study, showed that missingness (due to attrition) was at least somewhat related to existing data (χ2 = 217.586; df = 163; p = .003), the normed version of the test showed that this association was rather weak and data were missing mostly at random (χ2/df = 1.33). To minimize the bias of parameter estimates, which can occur when data are not missing completely at random, Full Information Maximum Likelihood estimation was used (Enders, 2010).

Measures

To assess the hypothesized financial identity processes, nine items from the U-MICS questionnaire (Crocetti et al., 2008) were used and modified for our purposes, three regarding the process of commitment (e.g., “The way I manage my money gives me self-confidence”), three regarding in-depth exploration (e.g., “I often reflect on how I manage my money”), and three regarding reconsideration of commitment (e.g., “I often think that if I managed my money differently my life would be better”). Composite reliability for the commitment scale was .93, for in-depth exploration it was .83, and for reconsideration of commitment, it was .86. Composite reliability was estimated using the output of a longitudinal measurement model with factor loadings and error variances that were equal across three measurement waves. The confirmatory factor analysis of this scale is presented in the Results section, while the items of the scale are presented in Supplementary Online Materials (SOM).

Also, at each wave of assessment, participants were asked to indicate their levels of financial well-being: income, parental financial support, financial strain, and financial satisfaction. Income, defined as the total amount of all income sources, was measured with a single item: “Please indicate your total recent monthly income that includes all sources of your income, such as parental support, salary, stipend, etc.” Participants responded on the following scale: “up to 100 euros” (scored as 1), “101–200 euros” (2), “201–300 euros” (3), “301–500 euros” (4), “501–700 euros” (5), “700–1,000 euros” (6), “1,000–1,500 euros” (7), “More than 1,500 euros” (8). Economic dependency, defined as the proportion of total income that comes from parental support, was measured with an item asking participants to indicate “How much of your current income comes from parental support?” Participants responded on the following scale: “0%” (scored as 1), “Around 25%” (2), “Around 50%” (3), “Around 75%” (4), and “100%” (5). Financial strain, defined as the experience of insufficient income, was measured by asking participants to think about the last couple of months and indicate how often they ran out of money before the next typical time that they received their monthly money, on a scale from “Never” (scored as 1), “Once every couple of months” (2), “Once a month” (3), “A couple of times during the last month” (4), or “Always” (5). Financial satisfaction, defined as the participant’s general satisfaction with their current financial situation, was measured using the General Subjective Financial Well-being Scale from The Multidimensional Subjective Financial Well-Being Scale for Emerging Adults (Sorgente & Lanz, 2019). This scale consists of 10 items (e.g., “I’m satisfied with my present financial situation”; ωT1 = .94, ωT2 = .94, ωT3 = .94).

Also, at each wave of assessment, participants were asked to indicate how often they engage in four positive financial behaviors: financial planning, cash-flow monitoring, saving, and controlled spending. Financial planning, defined as the propensity to plan and set short-term financial goals, was assessed using a Generalizable Scale of Propensity to Plan in Money domain (Lynch et al., 2010). This scale consists of two subscales targeting short-term (six items, e.g. “I set financial goals for the next few days for what I want to achieve with my money”) and long-term (six items, e.g., “I set financial goals for the next 1–2 months for what I want to achieve with my money”) financial planning. As the subscales were strongly correlated, we combined them into a 12-item single indicator (ωT1 = .93, ωT2 = .94, ωT3 = .94). Cash-flow monitoring, defined as tracking and monitoring monthly purchases and expenses, was assessed with the Cash-flow Monitoring subscale from the Brief Money Management Scale (Ksendzova et al., 2017), which consists of four items (e.g., “I review and evaluate spending on a regular basis”; ωT1 = .73, ωT2 = .74, ωT3 = .75). Saving, defined as saving money to achieve certain financial goals, was assessed with the Saving subscale from the Brief Money Management Scale (Ksendzova et al., 2017), which consists of four items (e.g., “I regularly set aside money for saving”; ωT1 = .81, ωT2 = .85, ωT3 = .85). Controlled spending, defined as exercising self-control in spending decisions, was assessed with the Consumer Spending Self-control Scale (Haws et al., 2012), which consists of 10 items (e.g., “I carefully consider my needs before making purchases”; ωT1 = .85, ωT2 = .89, ωT3 = .87).

All items were presented at every measurement occasion. All items belonging to financial behavior scales and financial satisfaction were scored on a scale ranging from 1 (completely disagree) to 5 (completely agree). Considering the time interval between the measurement occasions, which was around 13 weeks, participants were asked to think about the last several months when responding to the items.

At the first measurement wave, participants were also asked to indicate their parents’ income range, employment status, and level of education. These responses were used to create an indicator of family socioeconomic status, i.e. a rank variable with three categories: low (n = 137; 26%), medium (n = 331; 62%), and high (n = 65; 12%). Supplementary Online Materials (SOM) provide more information about this variable.

Data Analysis Strategy

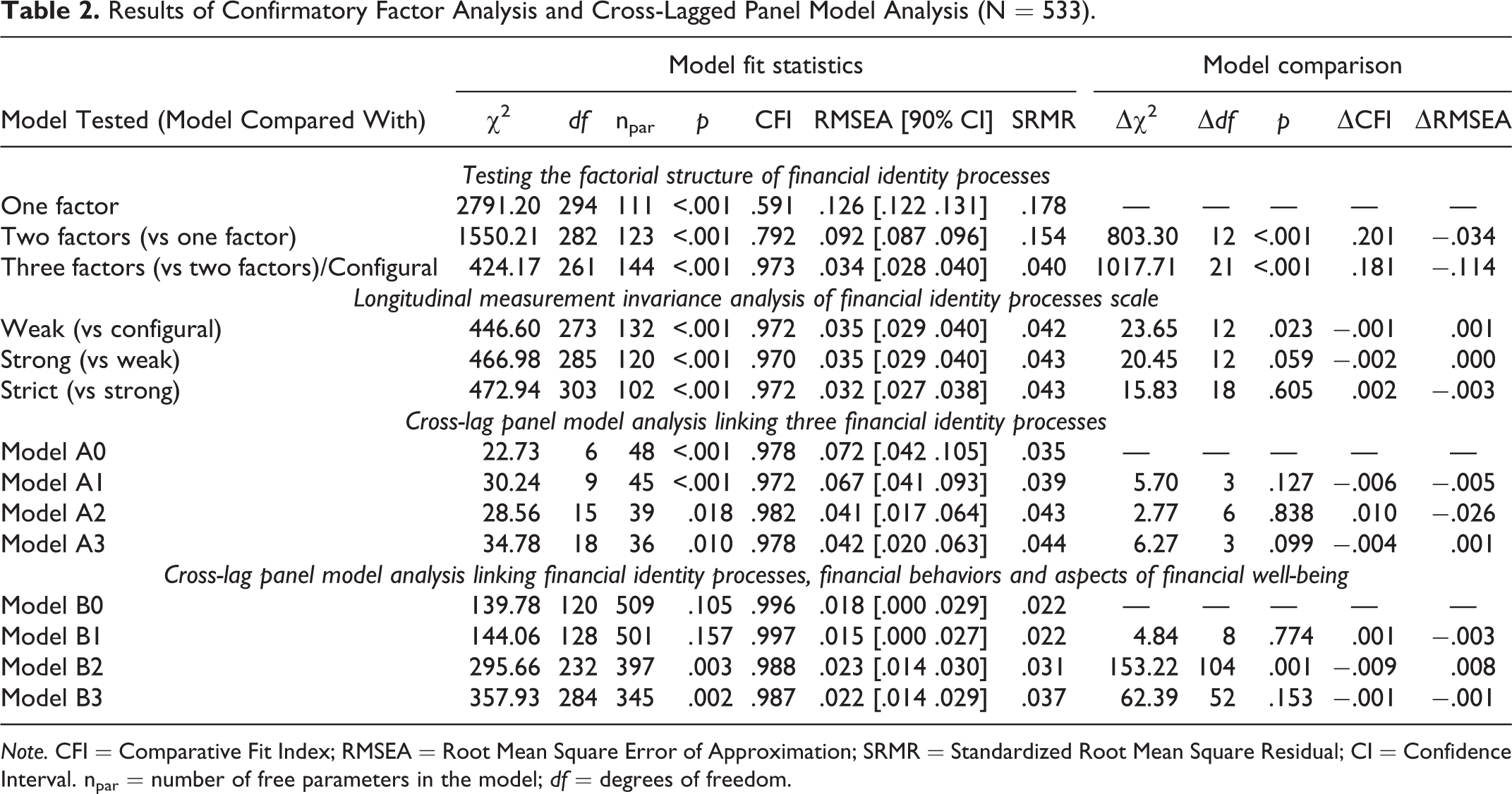

All analyses of the study were conducted using Mplus version 7.4 with Maximum Likelihood Robust (MLR) estimation. The comparative fit index (CFI), root mean square error of approximation (RMSEA), and standardized root mean square residual (SRMR) were used to assess model fit. CFIs equal to or higher than .90 and RMSEAs and SRMRs equal to or lower than .08 indicated acceptable fit. CFIs equal to or higher than .95 and RMSEAs and SRMRs equal to or lower than .05 indicated a good fit (Little, 2013). Statistically significant differences between nested models were tested using the Scaled χ2 Difference test (Satorra & Bentler, 2001), while the practical significance of these differences was assessed using model fit statistics: a decrease of CFI equal to or higher than .01 (ΔCFI ≥ −.01) was considered to indicate a substantial decrease in model-data fit (Little, 2013).

Before proceeding to our main analysis, we conducted longitudinal confirmatory factor analysis (CFA) for every multi-item measure. The presence of weak longitudinal measurement invariance (equivalence of factor loadings), which is an important assumption of cross-lagged panel model analysis (Little, 2013), was assessed for each scale, separately. The results of these analyses are presented in SOM. The unstandardized parameter estimates of weak invariance models were used to assess the composite reliability (denoted here as ω) index (Raykov & Marcoulides, 2011) for each wave.

The initial step of the analysis examined whether the expected three-factor model had a good fit for the newly adapted measure of financial identity processes across the three measurement occasions (results reported in Table 2). Specifically, we tested and compared three models, i.e. the one-factor model (all items load on one “financial identity” factor), the two-factor model (one commitment factor and one exploration factor for items targeting in-depth exploration and reconsideration of commitment), and the three-factor model (three latent variables targeting three financial identity processes). Every model was tested with longitudinal data; therefore, these factors were modeled at each wave simultaneously. Every model also included correlations between the residual variances of the same items on different occasions (Little, 2013).

The next step in the analysis examined the reciprocal associations between study variables. Specifically, two sets of cross-lagged panel model (CLPM) analyses were conducted: one set which included only three identity processes (labeled as Model A in Table 2), and another which included financial identity processes, financial behaviors, and financial well-being aspects (labeled as Model B in Table 2). In both sets of CLPM analyses, the following strategy was used. First, we specified a baseline CLPM model, which included (a) first-order autoregressive effects and covariance between T1 score and disturbance score at T3 of the same construct, (b) within time associations between all constructs, (c) cross-lagged effects (reciprocal links) among all constructs between adjacent time points (Model A0 and Model B0). Next, by equating the autoregressive effects for the same variables across different waves, we examined whether stability effects were time-invariant (Model A1 and B1). Subsequently, in the same manner, we examined whether cross-lagged paths were time-invariant (Model A2 and B2). Finally, we tested the time-invariance of correlated change parameters (Model 3A and 3B). In the second set of CLPM analyses, we controlled for parental SES, which was included in the model and used as a predictor of all study variables measured at T2 and T3 (for T1 covariances were estimated).

Results

The Structure of Financial Identity Processes Scale and Their Invariance Over Time

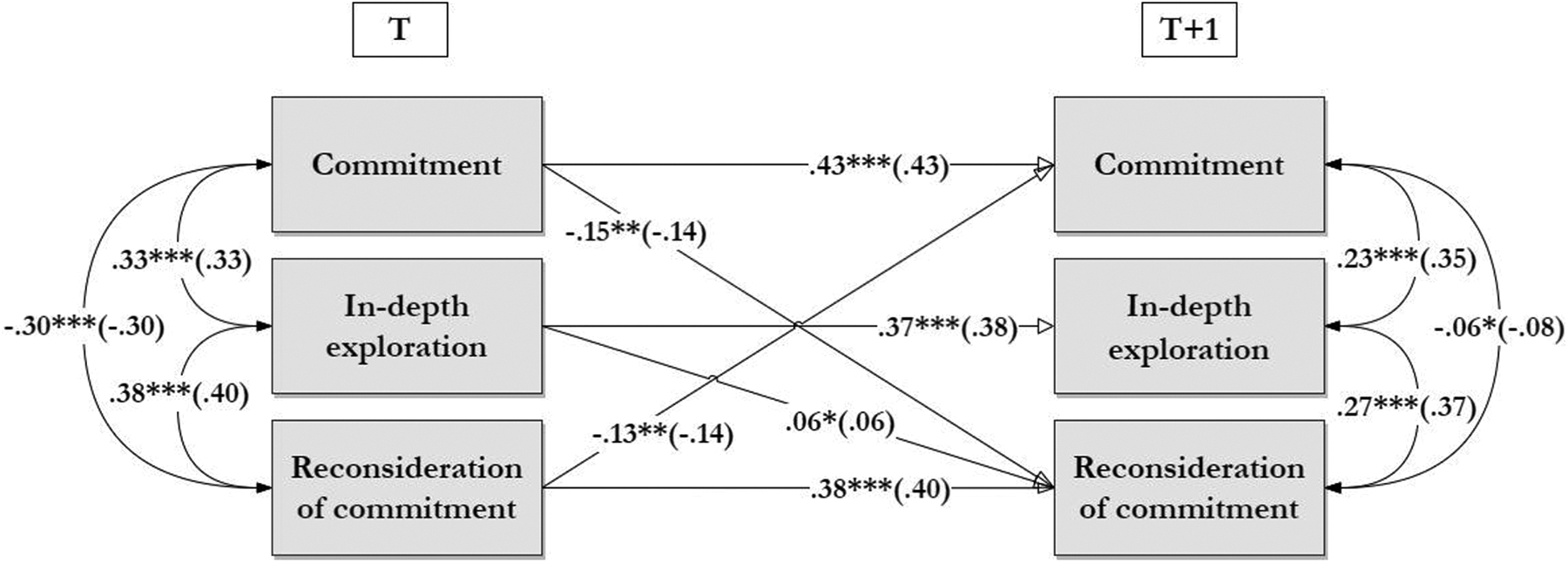

The analysis of the dimensional structure of the financial identity process scale supported the first hypothesis (H1), which predicted that a three-factor model would have a better fit than the two- and one-factor models. Specifically, for both comparisons of the one-factor model vs. the two-factor model and the two-factor model vs. the three-factor model, the change of the model-data fit was statistically and practically significant, and the three-factor structure had the best fit with the data (Table 2 presents the results). Modest correlations between the three factors (Figure 1) also indicated differentiation between the three dimensions. Assuming the three-factor structure, we also analyzed whether the parameters of the model were time-invariant. In a sequential manner (Little, 2013), we tested for weak (equivalence of factor loadings), strong (equivalence of intercepts), and strict (equivalence of residual errors) invariance. The results supported strict invariance (ΔCFI < .01; see Table 2). In sum, we confirmed the three-process model of identity formation (commitment, in-depth exploration, and reconsideration of commitment) in the financial domain and we found that the factors measuring these three processes were invariant over time.

Results of Confirmatory Factor Analysis and Cross-Lagged Panel Model Analysis (N = 533).

Note. CFI = Comparative Fit Index; RMSEA = Root Mean Square Error of Approximation; SRMR = Standardized Root Mean Square Residual; CI = Confidence Interval. npar = number of free parameters in the model; df = degrees of freedom.

Unstandardized and averaged standardized (in parenthesis) estimates of the cross-lagged panel model linking financial identity processes (N = 533). * p < .05, ** p < .01, *** p < .001.

Reciprocal Links Between Three Financial Identity Processes

The initial CLPM model linking three financial identity processes had an acceptable fit. Furthermore, the inclusion of longitudinal constraints (Model A1–A3) did not worsen the model’s fit with the data, as indicated by a non-significant change of model χ2. The final model (Model A3), which included all constraints, also had a good fit with the data and was used for interpretation (Figure 1 presents the simplified results). The longitudinal reciprocal associations between identity processes supported our second and third hypotheses. Specifically, as predicted by our second hypothesis (H2), a higher degree of financial identity reconsideration weakened existing financial identity commitments over time (β = −.13; p < .001). Also as predicted by our third hypothesis (H3), stronger financial identity commitment was related to weakened reconsideration of financial identity commitments (β = −.15; p < .001). Our fourth hypothesis (H4) predicted that stronger commitments would strengthen the in-depth exploration process over time, while the fifth (H5) predicted that in-depth exploration would strengthen commitments.

However, the results did not provide strong evidence in support of either of these two hypotheses. Stronger financial identity commitments did not significantly predict increased in-depth financial identity exploration over time, and in-depth exploration did not strengthen financial identity commitments. However, the initial level of financial identity commitment was positively correlated with in-depth financial identity exploration, and the residualized change in financial identity commitment was positively correlated with the residualized change in in-depth financial identity exploration, suggesting the presence of a dynamic relationship between in-depth exploration and financial identity commitments. Finally, as predicted by our sixth hypothesis (H6), higher in-depth financial identity exploration was related to greater reconsideration of commitment (β = .06; p = .01).

Reciprocal Links Between Financial Identity Processes, Financial Well-Being Aspects, and Positive Financial Behaviors

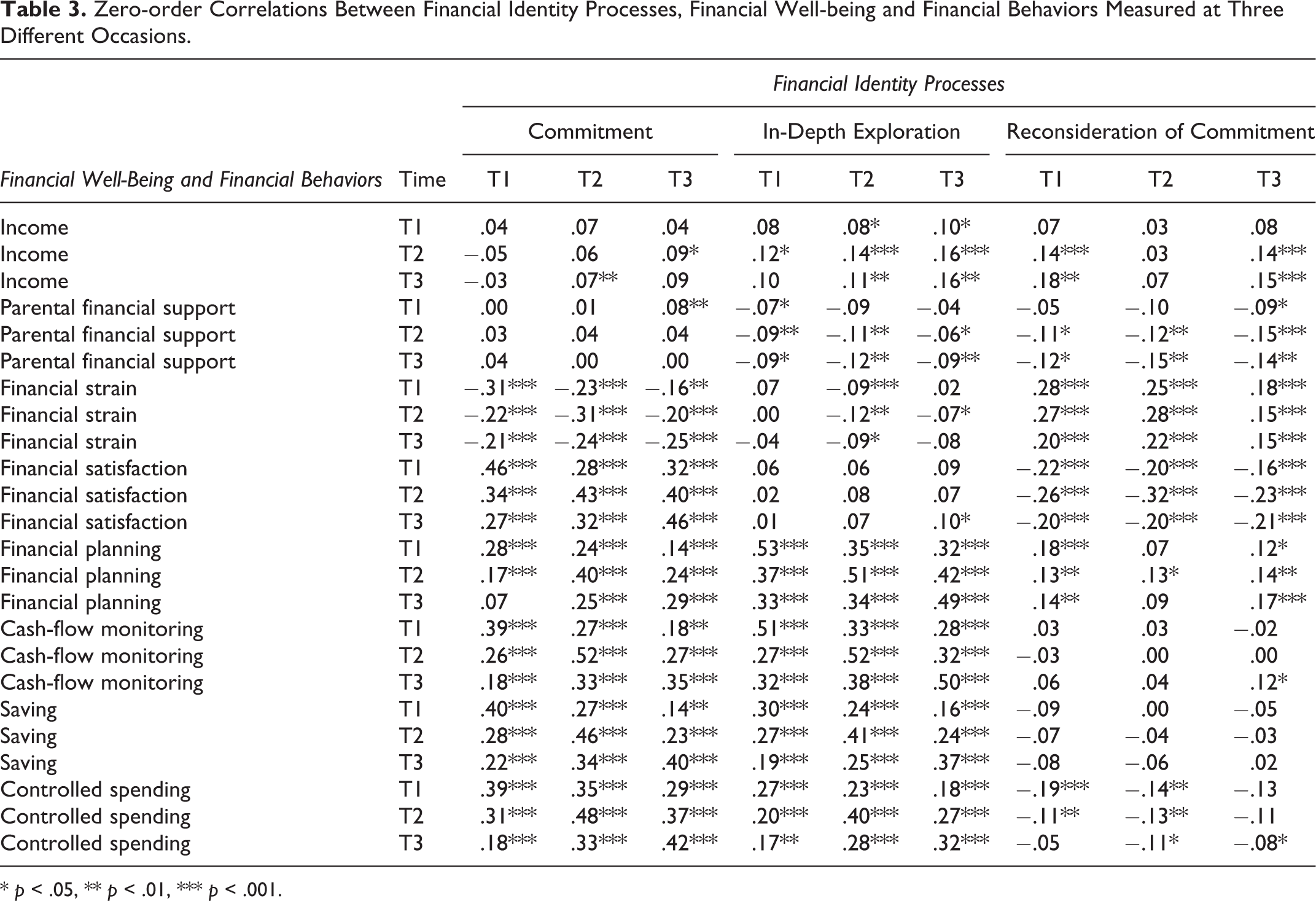

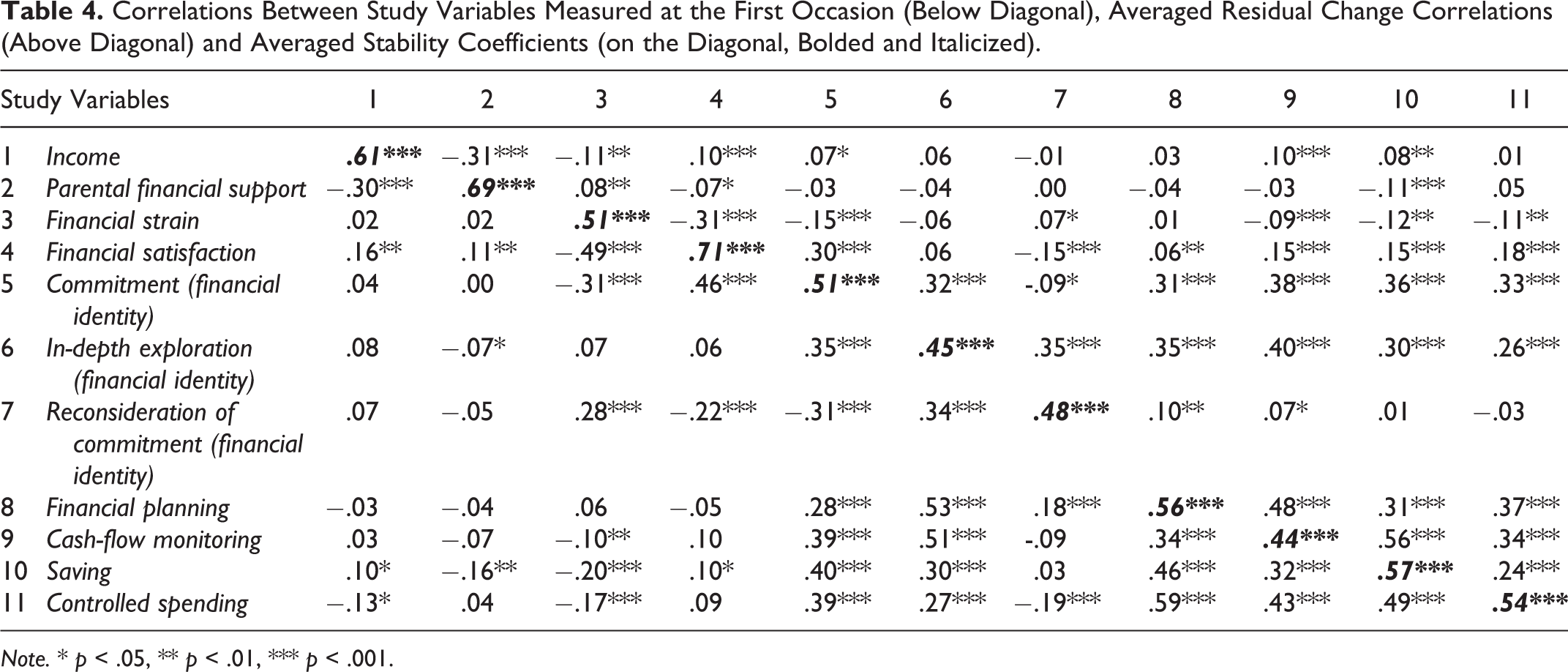

Zero-order correlations between financial identity processes, financial behavior, and financial well-being variables measured on three different occasions are presented in Table 3. Small-to-strong-sized (Cohen, 1988) correlations were found. Stability levels (autoregressive effects) for each construct, reported in Table 4, were estimated separately (running separate auto-regression models for each construct), to avoid any attenuation of these estimates that can occur when cross-lagged paths are included in the model (Newsom, 2015).

Zero-order Correlations Between Financial Identity Processes, Financial Well-being and Financial Behaviors Measured at Three Different Occasions.

* p < .05, ** p < .01, *** p < .001.

Correlations Between Study Variables Measured at the First Occasion (Below Diagonal), Averaged Residual Change Correlations (Above Diagonal) and Averaged Stability Coefficients (on the Diagonal, Bolded and Italicized).

Note. * p < .05, ** p < .01, *** p < .001.

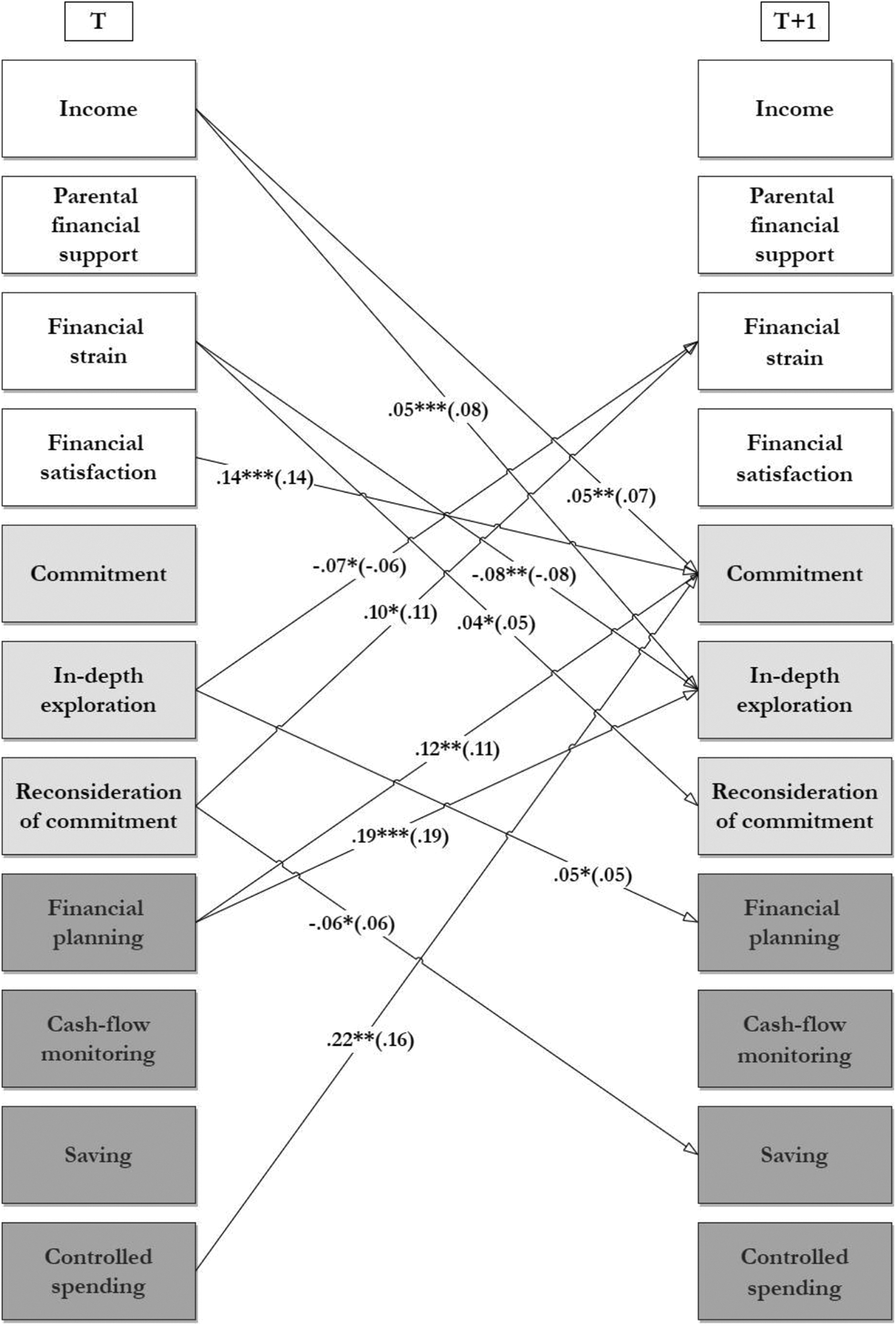

The baseline CLPM model linking financial identity processes, positive financial behaviors, and aspects of financial well-beingfit the data very well, as indicated by non-significant model χ2 and alternative fit indices (Model B0 in Table 2). The inclusion of stability (Model B1) constraints did not worsen its fit (Δχ2 p-value was not significant and ΔCFI did not exceed the “−.01” threshold). The inclusion of equality constraints on cross-lagged associations (Model B2) resulted in a significant model Δχ2. The inspection of modification indices did not show specific areas of model strain. Since ΔCFI also did not exceed the threshold of −.01, these constraints were retained. The inclusion of equality constraints on residual correlations (Model B3) also did not worsen model-fit. These results suggested that dynamic associations between financial identity and other study variables were very similar across the three waves, and we turned to the inspection of parameter estimates. Figure 2 represents the reciprocal relationships between financial identity processes and financial behaviors and financial well-being, while Table 4 presents correlations, and residualized change correlations estimated in the final model (Model B3). The paths less relevant to this study (between financial behaviors and aspects of financial well-being) are presented in the SOM.

Unstandardized and averaged standardized (in parenthesis) estimates of the cross-lagged panel model linking financial identity processes, aspects of financial well-being, and financial behaviors (N = 533). Only reciprocal links between financial identity processes and other variables are displayed in this figure, to increase readability. * p < .05, ** p < .01, *** p < .001.

The results suggested that the relative increase of financial identity commitments was predicted by higher levels of income (β = .05; p = .004), financial satisfaction (β = .14; p < .001), financial planning (β = .12; p = .001), and controlled spending (β = .22; p = .001). In-depth financial identity exploration was predicted by income (β = .05; p < .001) and financial planning (β = .19; p < .001), but negatively predicted by financial strain (β = −.06; p = .008). Increased ireconsideration of identity commitments was predicted by financial strain (β = .04; p = .047). In addition to these effects, higher levels of in-depth exploration predicted decreased financial strain (β = −.07; p = .04) and increased financial planning (β = .05; p = .04). In contrast, higher levels of reconsideration of financial identity commitments predicted increased financial strain (β = .10; p = .01) and decreased savings (β = −.06; p = .03). Higher initial levels of commitment were not significantly associated with a change in financial well-being or positive financial behaviors. In sum, we found that there is a bi-directional relationship between financial identity and financial behaviors and well-being.

Discussion

The goal of the current study was two-fold: to investigate financial identity by adopting the three-factor model of identity formation and to investigate longitudinal relationships between financial identity processes and engagement in positive financial behaviors and levels of financial well-being in emerging adulthood. Study results support the applicability of the three-factor model to processes of identity formation in the financial domain. A model comparison approach showed the superiority of the three-factor structure and supported the first (H1) study hypothesis. Measurement model parameters were also invariant over the three occasions and the reliability of each scale was high. These findings indicate sufficient validity of the score structure and accuracy of item-total scores. The positive correlations between commitment and in-depth exploration and between in-depth exploration and reconsideration, and the negative one between commitment and reconsideration of commitment were similar to those found in other research on identity (Crocetti et al., 2010, 2015). As far as these findings are concerned, the structure of the newly adapted measure closely resembled the adaptations of the U-MICS questionnaire designed to target the three identity processes in other domains.

In line with our second (H2) and third (H3) hypotheses, our data also showed the certainty-uncertainty dynamic of financial identity commitments, which is an established characteristic of identity formation in other domains (e.g., Becht et al., 2019; Pop et al., 2016). That is, emerging adults who were dissatisfied with their current money management practices and in the process of exploring alternative ones (high reconsideration) decreased their commitment to their current practices over time, while those who were satisfied decreased their reconsideration over time. The picture was somewhat less clear for the in-depth exploration process, however.

Supporting the sixth (H6) hypothesis, reflection on one’s current manner of managing money led to reconsideration and uncertainty regarding these practices (see Figure 1). This closely resembles patterns of identity formation in other domains, such as the relational and occupational domains (Crocetti, 2018; Crocetti et al., 2008). However, there were no statistically significant longitudinal reciprocal links between commitment and in-depth exploration processes. Thus, our results did not support our fourth (H4) or fifth (H5) hypotheses and were inconsistent with previous longitudinal studies (e.g., Pop et al., 2016). From a theoretical point of view, this finding suggests that during the early years of emerging adulthood, young people are only starting to reflect on their money management practices and any reflection on these practices leads to the exploration of new ones, rather than committing to these practices. However, evidence of a positive residual correlation (the change unaccounted for by earlier levels of identity processes) between these processes indicates that processes of in-depth exploration and commitment are, in some way, dynamically interrelated. This makes it hard to draw conclusions about the absence of reciprocal influences. Given that the time lag between the occasions may moderate the strength of reciprocal longitudinal associations (Newsom, 2015), we speculate that these associations may be observable in longitudinal designs that use shorter or longer time intervals.

Notably, commitment to a certain money management style did not predict any changes in financial well-being or financial behaviors. This finding may seem somewhat contradictory to those reported in studies of financial identity statuses indicating substantial positive associations between “achieved financial identity” status and emerging adults’ positive financial behaviors (Shim et al., 2013; Sorgente et al., 2020). However, this result should be considered in light of the differences between the status and process approaches in identity research.

“Achieved financial identity” status implies that financial identity commitments were made after a period of personal exploration, and this is expected to be associated with many favorable outcomes financially. In line with this approach, the “foreclosed financial identity” status, which involves commitments made without personal exploration, was not found to be substantially related to financial behaviors (Shim et al., 2013; Sorgente et al., 2020). The commitment dimension within the three-factor model, on the other hand, is conceptualized as a process of holding on to a certain money management style, without any indication of whether these commitments were formed after a period of personal exploration or not. In our three-factor model of financial identity, holding on to a certain manner of managing personal finances may involve persistence in either effective or ineffective money management practices. Considering these theoretical differences, this result is not surprising and concurs with earlier findings indicating that commitment to a style of personal finance management is only adaptive if it is made after deliberate exploration of alternatives (Shim et al., 2013; Sorgente et al., 2020; Vosylis & Erentaitė, 2020).

The aforementioned result also suggests that the use of a person-oriented approach to investigate profiles characterized by different levels of financial identity processes could be an important avenue in this line of research, e.g. the person-oriented approach could uncover statuses not hypothesized by the financial identity status model. As far as the already discussed findings are concerned, the results provide substantial support for a three-factor model of identity formation in the domain of personal finances. The subsequent investigation of reciprocal associations with other study variables provides novel evidence with implications for financial capability research and interventions.

Importantly, we also found that financial identity exploration can contribute to experiences of financial strain, i.e. insufficient income to cover living expenses. In particular, the process of active reflection on one’s current financial management style (in-depth exploration) anticipated increased financial planning and decreased financial strain experiences, while reconsideration was associated with increased financial strain experiences and decreased saving. These results indicate that uncertainty regarding the most suitable manner of managing money is an unfavorable condition during these important transitions and may be associated with a subsequent increase in financial difficulties, while an ongoing healthy reflection on money management practices can reduce the occurrence of financial difficulties. These results also parallel those of previous studies documenting a substantial association between moratorium status and problematic functioning in the financial domain (Sorgente et al., 2020; Vosylis & Erentaitė, 2020) and demonstrate the need for interventions aimed at helping those experiencing uncertainty and dissatisfaction regarding their financial situation (Li et al., 2019).

Importantly, in line with our speculations that changes in one’s financial condition can also trigger changes in financial identity processes, we found that over time, emerging adults with higher levels of income and financial satisfaction increased their level of commitment to their current manner of managing money and tended to reflect more on their way of managing money, while those with higher levels of financial strain became more unsure of their money management practices over time and reduced their efforts to reflect on these practices. As these associations were significant even after accounting for the previous level of financial behaviors, the findings indicate that emerging adults with a more advantageous financial situation are less likely to experience uncertainty regarding the preferred way of coping with existing funds. while those in a less favorable financial situation are prone to experience more uncertainty over time.

We also found reciprocal associations between financial identity processes and positive financial behaviors. Specifically, we found that financial planning and spending control strengthened financial identity commitments, while financial planning strengthened the in-depth exploration process. That is, by creating some sense of security regarding their approaches to managing money, these two specific behaviors mostly contribute to more certainty in financial identity commitments, and thus may be the most important for healthy management of personal finances for young people of this age. This result also suggests that financial identity and financial behaviors develop in tandem and may influence each other, i.e. financial identity uncertainty may contribute to less healthy financial behaviors, while engaging in positive financial behaviors may reduce uncertainty.

The findings of the study have two important implications. Specifically, the results imply that interventions aimed at improving youths’ financial habits should focus more on emerging adults experiencing financial difficulties, as they experience more uncertainty and may need more guidance on financial issues in their lives. Considering the link between family financial difficulties and moratorium status of financial identity (Vosylis & Erentaitė, 2020), financial behavior interventions could also be very useful to those who have a history of financial troubles in their families. The positive associations between in-depth exploration and positive financial behaviors demonstrate that interventions focused on promoting positive financial behaviors and active reflection on actual financial behaviors should be effective in providing support to emerging adults facing a financial identity crisis (uncertainty regarding the best ways of coping with financial responsibilities). Such interventions could also be effective in promoting transition to adulthood (Li et al., 2019) and strengthening financial and overall well-being during this process (Serido et al., 2013; Shim et al., 2013; Sorgente & Lanz, 2017).

Limitations and Future Directions

The findings of the study should be considered in light of its limitations. The first and most evident limitation is that this study only addressed changes in study variables that happened during the 1st year after high school completion and only among emerging adults who entered higher education. Therefore, it is mostly generalizable to emerging adults of this age enrolled in higher education. Considering the negative effects of financial strain uncovered in the study, it may be that effects would be somewhat different (perhaps stronger) if the sample had included those not employed or in school. Notably, however, the site of the study (Lithuania) is characterized by a very high percentage of enrollment in higher education (∼70% of those who finish high school,] enroll in some kind of higher education; Statistics Lithuania, 2019). As such, it is still generalizable to a large portion of young emerging adults of this age, living in this context.

The rather short time frame that was investigated in the study could also be considered a limitation. While this design proved to be useful in capturing the reciprocal relationships between study variables, these effects should be considered short-term effects. Thus, it is somewhat unclear whether the reciprocal links that were identified would be found in longitudinal studies spanning longer time periods. Further investigation of the effects using more long-term longitudinal designs may be a good direction for future research.

One more limitation of the study relates to the measure of financial identity processes. In particular, we used only three items for each dimension, to create a scale that suitable for research with large samples. Future research could address the underlying dimensions more thoroughly by including more (suitably adapted) items from the U-MICS questionnaire to target financial identity processes. The extended version of the scale could lead to even higher precision of the factor scores, which in turn might lead to identification of more effects. Furthermore, future research should assess the convergent validity of the scale. In particular, this study did not address the association between the newly created scale and the Financial Identity Scale (Sorgente et al., 2020) that targets four financial identity statuses.

Conclusions

Despite these limitations, our findings support the applicability of the three-factor model to the study of financial identity processes and indicate that this model could be used to investigate how various life circumstances shape the formation of positive financial habits. The new measure could also be used as a screening tool to select individuals in need of financial education programs. More importantly, the findings also show that financial identity formation is shaped by emerging adults’ financial circumstances, and that those in poorer financial situations may be in need of financial behavior interventions. Finally, our findings also suggest that interventions focused on promoting in-depth financial identity exploration as well as positive financial behaviors could be beneficial for the more general process of becoming an adult.

Supplemental Material

Supplemental Material, sj-pdf-1-eax-10.1177_21676968211016142 - The Role of Financial Identity Processes in Financial Behaviors and Financial Well-Being

Supplemental Material, sj-pdf-1-eax-10.1177_21676968211016142 for The Role of Financial Identity Processes in Financial Behaviors and Financial Well-Being by Rimantas Vosylis, Angela Sorgente and Margherita Lanz in Emerging Adulthood

Supplemental Material

Supplemental Material, sj-docx-2-eax-10.1177_21676968211016142 - The Role of Financial Identity Processes in Financial Behaviors and Financial Well-Being

Supplemental Material, sj-docx-2-eax-10.1177_21676968211016142 for The Role of Financial Identity Processes in Financial Behaviors and Financial Well-Being by Rimantas Vosylis, Angela Sorgente and Margherita Lanz in Emerging Adulthood

Footnotes

Author Contributions

Vosylis, R. contributed to conception and design, contributed to acquisition, analysis, and interpretation, drafted manuscript, critically revised manuscript, gave final approval, and agrees to be accountable for all aspects of work ensuring integrity and accuracy. Sorgente, A. contributed to conception, contributed to analysis and interpretation, drafted manuscript, critically revised manuscript, gave final approval, and agrees to be accountable for all aspects of work ensuring integrity and accuracy. Lanz, M. contributed to conception, contributed to interpretation, critically revised manuscript, gave final approval, and agrees to be accountable for all aspects of work ensuring integrity and accuracy.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Ethical Approval

All procedures performed in studies involving human participants were in accordance with the ethical standards of the institutional and/or national research committee and with the 1964 Helsinki Declaration and its later amendments or comparable ethical standards.

Funding

The authors disclosed receipt of the following financial supportfor the research, authorship, and/or publication of this article: This research was funded by the European Social Fund under the No. 09.3.3-LMT-K-712 “Development of Competencies of Scientists, Other Researchers, and Students through Practical Research Activities” measure. Grant recipient: Rimantas Vosylis. Grant no: 09.3.3-LMT-K-712-02-0156.

Supplemental Material

Supplemental material for this article is available online.

Open Practices

The raw data, analysis code, and output described in this manuscript are openly available (![]() ). Materials (print-out of an electronic survey, questions, and questionnaire items) used in the survey are not openly available. These can be obtained from the corresponding author upon request. No aspects of the study were pre-registered.

). Materials (print-out of an electronic survey, questions, and questionnaire items) used in the survey are not openly available. These can be obtained from the corresponding author upon request. No aspects of the study were pre-registered.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.