Abstract

The study tested a model of first-year university students’ financial socialization focusing on parents as financial socialization agents and students’ present financial outcomes. Results from 395 Austrians (70% females) and 412 Slovenes (55% females) revealed significant pathways from recollected socialization experiences to students’ self-perceived financial learning outcomes (adopting parental role modeling and financial knowledge) and financial behavior control. Financial knowledge and behavioral control partly mediated the effect of prior socialization experiences on students’ financial behavior, financial relationship with parents, and financial satisfaction. Among country-specific pathways, adopting parental role modeling indirectly influenced financial outcomes in the Slovene students, whereas for the Austrian students, it was directly associated with better financial relationships with parents. Our findings on the pathways to healthy financial outcomes provide important suggestions to parents and emerging adult students.

Keywords

Introduction

Financial decisions nowadays are more complex for young generations than in the past (Lusardi & Mitchell, 2014) and are likely to have considerable consequences for individuals’ life pathways, well-being, and wealth. In addition, consumer economy entices to buy, with online platforms providing a comfortable way of shopping while easy options to get one’s own credit card may tempt individuals to excessive expenditures. At the same time, increasingly more young people in Western societies prolong their education and delay overtaking adult roles than decades ago, which provides them an extended period of identity exploration in different areas (Arnett, 2000), including the financial domain. Depending on socioeconomic conditions, social welfare systems, and cultural norms, reaching financial self-sufficiency for young people differs across macro-systems and brings about diverse ways of attaining financial independence—an important developmental task of becoming adult.

Emerging Adulthood in Austria and Slovenia

Differences in macro-systems (e.g., social policies toward family and youth) contribute to different models of the transition to adulthood (Arnett, 2015; Zupančič & Sirsch, 2018; Žukauskiene, 2016). Based on differences in the social welfare systems, Douglass (2007) organized European countries into the Nordic, the German- and French-speaking (including Austria), the Anglo-Saxon, the post-socialist Eastern European, and the Mediterranean cluster of countries (including Slovenia; Kuhar & Reiter, 2014). The two participating countries in our study presently differ in their social welfare systems and transitions to adulthood.

Regarding their historical roots and cultural traditions, Austria and Slovenia shared some similar background for many centuries, but they differed in sociopolitical and economic development for 45 years after WW-II. Parents of current generations of emerging adults in Slovenia grew up in socialism but raised their children in democracy and a capitalist economy. Austria gained its independence after WW-II and remained relatively stable politically and economically. Regarding gender equity, full-time work for all women has become a common practice in Slovenia after the WW-II, including state-funded, high-quality childcare options after mothers’ 1-year paid maternity leave (Puklek Levpušček & Zupančič, 2007). Although supporting gender equity is an important topic in Austria (Mayr & Adamek, 2007), many women with young children do not work full-time due to somewhat poor availability of affordable out of home child day care, and perhaps a longer embeddedness of traditional gender roles in the culture (Wernhart, Dörfler, Halbauer, Mazal, & Neuwirth, 2018).

The transition to adulthood in Austria and Slovenia at present parallels different social welfare systems, with high levels of governmental support for the former and a strong dependence on family support for the latter. Relative to Austria, it is a cultural norm in Slovenia that parents protect emerging adults from taking economic risks, providing them with substantial socioemotional, residential, and financial support for an extensive period of time (Zupančič & Sirsch, 2018). Accordingly, emerging adults from the two countries differ in mean ages of moving out of parental home (males at 26.3 and females at 24.8 years in Austria vs. 29.2 and 27.0 years in Slovenia, respectively; Eurostat, 2019b). Thus, a vast majority of all Slovene students in tertiary education (constituting 46% of the population, aged 20–24 years vs. 28.8% in Austria; Eurostat, 2019a) co-reside with parents (or semi-reside if they attend school during the semester days but return home regularly for weekends and/or holidays), whereas 33% of the Austrian first-year students (mean age 21.9 years) live with parents or relatives (Institute for Advanced Studies, 2016; Zupančič & Sirsch, 2018).

Among similarities, both countries provide tertiary education for free (thus, students have no loan to pay back) and offer specific welfare mechanisms for individuals or families (e.g., parents’ health insurance covering students also, extended family allowances/tax reductions for families with students). Furthermore, students’ ability to get their own credit card is firmly restricted (resulting in them not having credit card debts). Thus, the conditions for emerging adults to deal with their financial issues are different from those in some other countries (e.g., the United States). In addition, money matters and personal finances may have a different meaning in Europe compared to the United States, specifically when it comes to attitudes toward money, personal financial management, and/or parent–child communication about financial issues.

However, regardless of the differences in social welfare systems (or attitudes toward money matters), financial conditions provide limitations regarding money for most young people. Their pathway to financial independence, an important developmental task of becoming adult, as well as subjectively highly important for emerging adults (Zupančič & Sirsch, 2018), requires financial knowledge, skills, and healthy financial behavior.

Financial Socialization and Emerging Adults’ Healthy Financial Outcomes

Research on well-being over recent decades and the 2008 financial crisis in the United States gave rise to an increase in studies on young people’s financial well-being, their financial habits, attitudes, and behavior. Three disciplines, such as psychology, sociology, and economics, contributed mainly to this research. Accordingly, diverse theoretical frameworks, concepts, and/or labels for the same constructs were used in dealing with how to describe, explain, and predict individuals’ development in the financial domain.

Much research about financial socialization was carried out in the framework of consumer socialization (Danes, 1994) aiming to explain the development of consumer attitudes, knowledge, and behavior, as conceptualized by the consumer socialization theory (Ward, 1974). It contends that children develop those consumer features from various socialization agents (e.g., parents; Moschis, 1985). Ward, Wackman, and Wartella (1977) portrayed methods used by mothers to teach their children consumer skills, which include direct teaching and acting as a role model. Later, the framework of consumer socialization to explain “effective functioning in the marketplace” (Ward, 1974, p. 2) was extended, and the term financial socialization was introduced to explicate the process of acquiring and developing financial knowledge, beliefs, and behavior from parents in a more general way. Danes (1994, p. 129) states that “children learn financial management behavior through observations and participation (incidental learning) and through intentional instruction by socialization agents.” Thus, various conceptual models of financial socialization processes were developed, suggesting that parents influence their offspring’s future financial practices. Jorgensen and Savla (2010) empirically supported the important role of parents in the development of children’s financial attitudes, which in turn affect their financial behavior. Their conceptual framework was partly based on Bandura’s (1986) social learning theory and captured children’s implicit, as well as explicit learning from parents.

A model that includes recollected implicit and explicit learning from parents as well as their offspring’s financial behavior control was presented by Shim, Barber, Card, Xiao, and Serido (2010). Their hierarchical four-level financial socialization model was guided by the consumer socialization theory and the theory of planned behavior (Ajzen, 1991). The latter links individuals’ behavior to attitudes toward the behavior, subjective norms, and behavioral control. Shim et al. (2010) proposed anticipatory socialization during childhood and adolescence (Level 1) to predict emerging adults’ financial learning outcomes (Level 2), which are linked to financial attitudes (Level 3), and ultimately, foretell “healthy” financial outcomes (Level 4). Their research with first-year U.S. college students showed that anticipatory financial socialization indicators—student recollected parental financial behavior and direct financial teaching, high school work experience, and financial education—as well as parental SES predict students’ current adopting parental financial role modeling and/or financial knowledge (financial learning outcomes). Parents who were perceived as engaged in positive financial behavior and financial teaching were more likely seen as financial role models, which in turn, helped their emerging adult children feel they could control their financial behavior in a better way. The learning outcomes were also linked to student-perceived parental norms, and financial attitudes, which along with students’ self-perceived financial behavior control further predicted their favorable financial relationship with parents, satisfaction with money management, and positive financial behavior.

Gudmunson and Danes (2011) conceptualized a model of financial socialization processes by integrating demographic characteristics, family interactions and parent–child relationships, and financial attitudes, knowledge, and capabilities, which were all hypothesized to affect financial behavior and financial well-being. Based on this model, Jorgensen, Rappleyea, Schweichler, Fang, and Moran (2017) investigated family socialization and financial behavior of emerging adults. They considered locus of financial situation control in the domain of financial attitudes, knowledge, and capabilities and measured the former as emerging adults’ sense of influence and control over events in their lives, as well as having control over their financial matters. As their results show, locus of control mediated the association between parent–child relationship and emerging adults’ financial behavior. Similar to Shim et al. (2010), financial control was considered an important factor in the development of healthy financial behavior. However, research on parental financial socialization processes and their outcomes, specifically regarding emerging adults, was predominantly conducted in the United States.

Study Aim and Hypotheses

This study aimed to extend our knowledge on the pathways from parental financial socialization toward students’ healthy financial outcomes to contexts other than the United States by selecting two European countries, which differ in their social welfare system and transition to adulthood.

Conceptualizing our first-year student financial socialization model, we focused on parents as financial socialization agents affecting their offspring’s financial outcomes. Several studies stressed the lower importance of early work experiences, financial education in schools (e.g., Gudmunson & Danes, 2011; Shim, Barber, Card, Xiao, & Serido, 2010), friends, and informal self-learning (Shim, Serido, Tang, & Card, 2015) compared to parental financial socializing endeavor. Furthermore, work experience for Austrian and Slovene emerging adults on a university track is occasional, short term, low paid, with earnings usually spent on entertainment and luxuries but not on necessities, security, or saving for education. In neither country is financial education specifically provided in school.

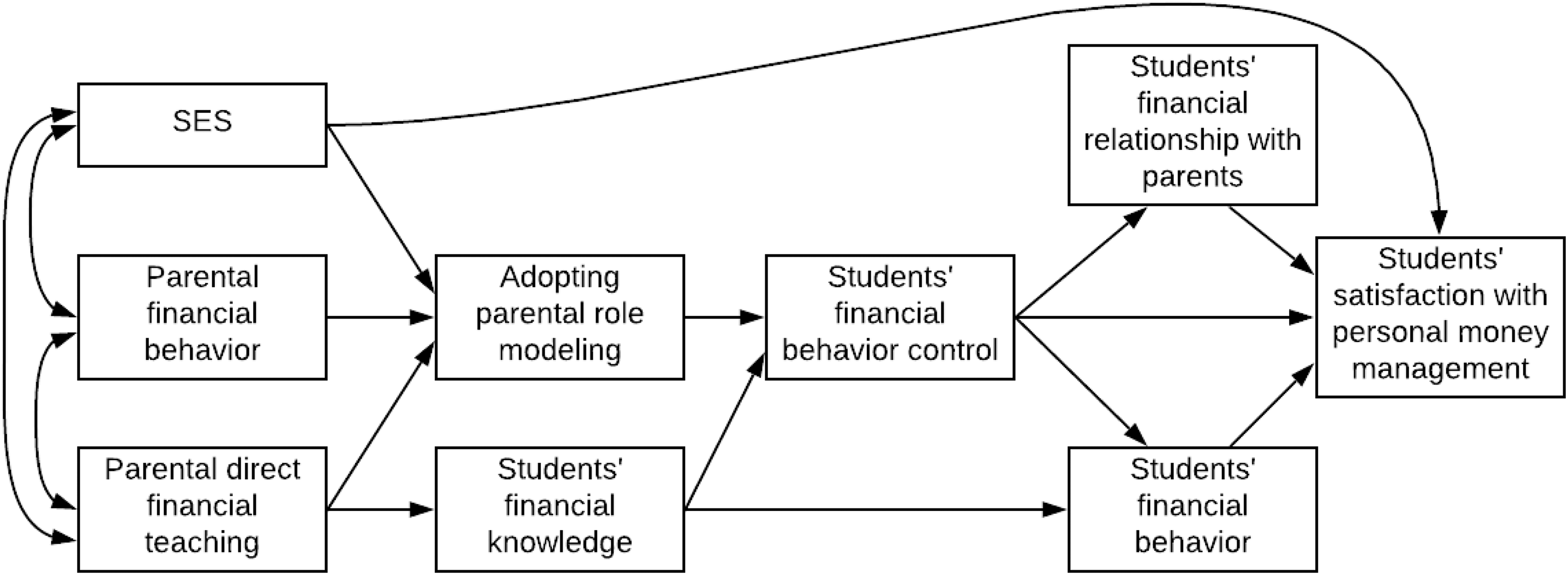

We were inspired by the part of Shim et al.’s (2010) model, which includes anticipatory financial socialization indicators of implicit and explicit financial learning based on social learning theory (Bandura, 1986) and consumer socialization (within families see Moschis, 1985). We considered student-observed parental behavior as an indicator of implicit learning and parental teaching as an explicit learning indicator, both prior to the students’ university entry. In line with Shim et al. (2010), we expected Austrian and Slovene first-year university students’ recollections of parental financial behavior and direct financial teaching as well as parental socioeconomic status (SES) (i.e., anticipatory financial socialization by parents) to predict the current adoption of parents as financial role models and self-perceived financial knowledge (learning outcomes).

We also presumed both learning outcomes to further influence students’ self-perceived control over financial behavior. Behavioral control namely reflects self-regulatory capacities as an outcome of socialization processes in line with the sociocultural theory of Vygotsky (1930/1978) but is referred to as locus of control (Jorgensen et al., 2017) or delay of gratification (Novilitis & MacLean, 2010). Relying on the theory of planned behavior (Ajzen, 1991), Shim et al. (2010) considered financial behavior control as an attitudinal indicator (Level 3 of their model), influenced by learning outcomes and subsequently influencing financial behavior outcomes. Likewise, Gudmunson and Danes (2011) labeled the intermediary financial socialization outcomes in their model as the domain of attitudes, knowledge, and capabilities. Accordingly, we presumed that student-perceived financial behavior control would further contribute to the three financial outcomes under study, namely, financial relationship with parents, students’ financial behavior, and their financial satisfaction.

Based on more recent literature (Serido, Shim, & Tang, 2013; Sorgente & Lanz, 2017), we finally proposed that students’ self-perceived financial behavior and financial relationship with their parents due to financial matters would predict the students’ satisfaction with money management (Figure 1).

Parents as socialization agents: the proposed first-year student financial socialization model.

Regarding the two countries under study, we expected that parental influence may be somewhat stronger and/or spread across a wider range of learning and behavioral outcomes in Slovenia, a country with a tradition of strong reliance on parents as a source of all kinds of support and services (among them, residential and financial) to emerging adults in order to protect the young generation from economic risks (Kuhar & Reiter, 2014; Zupančič & Sirsch, 2018).

Method

Participants and Procedure

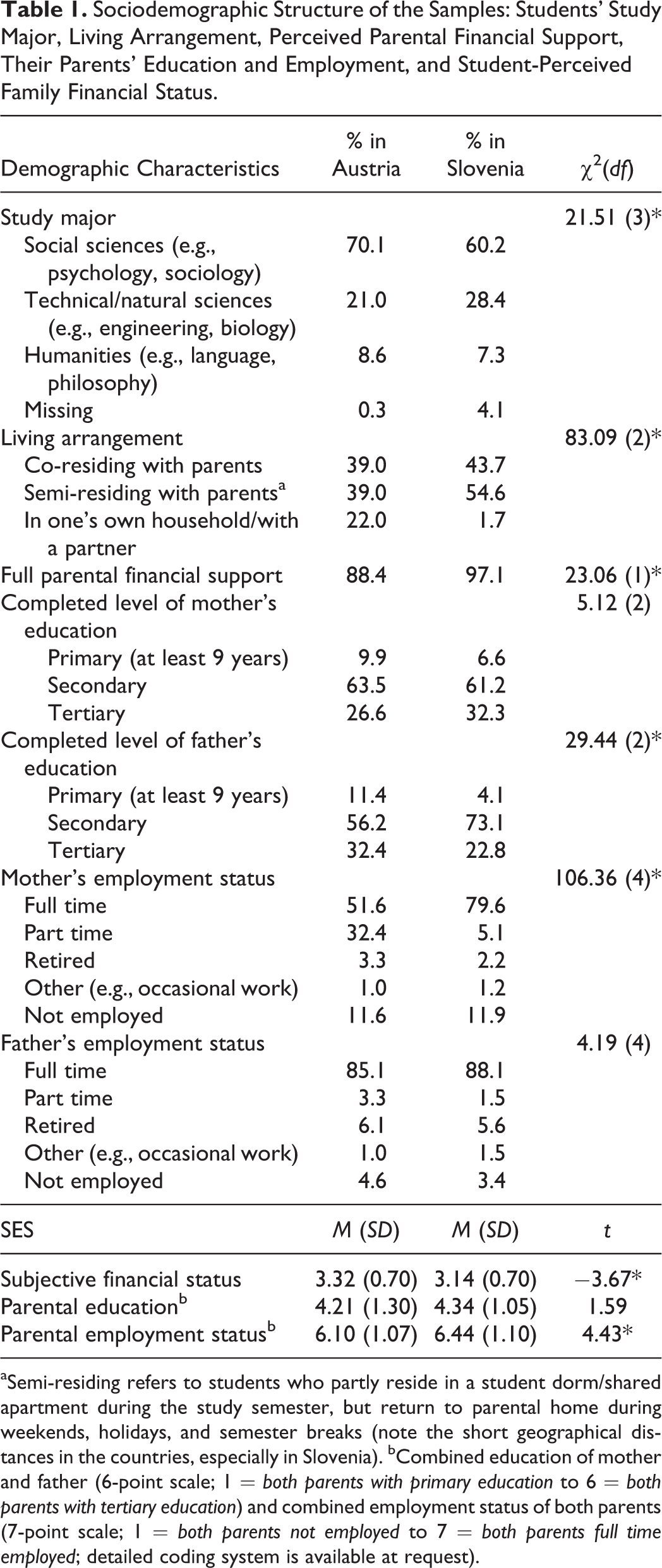

Data were collected from 412 first-year public university students (54.6% females) in Slovenia and 395 first-year public university students in Austria (70.1% females). There were significantly less males in the Austrian sample, χ2(1) = 20.65, p < .001. The Austrians were significantly older (M age = 22.06 years, SD = 2.05) than the Slovenes (M age = 19.46 years, SD = 0.90), t(805) = 23.58, p < .001. However, the mean ages were quite representative of first-year student populations in Austria (Institute for Advanced Studies, 2016) and Slovenia (Statistical Office of the Republic of Slovenia [SURS], 2018). Other characteristics of both samples are displayed in Table 1.

Sociodemographic Structure of the Samples: Students’ Study Major, Living Arrangement, Perceived Parental Financial Support, Their Parents’ Education and Employment, and Student-Perceived Family Financial Status.

aSemi-residing refers to students who partly reside in a student dorm/shared apartment during the study semester, but return to parental home during weekends, holidays, and semester breaks (note the short geographical distances in the countries, especially in Slovenia). bCombined education of mother and father (6-point scale; 1 = both parents with primary education to 6 = both parents with tertiary education) and combined employment status of both parents (7-point scale; 1 = both parents not employed to 7 = both parents full time employed; detailed coding system is available at request).

As indicated in Table 1, the samples differed significantly in their study major (more Austrians attended social science programs), living arrangement (more Slovenes co-resided and semi-resided with parents), paternal education (more Austrian fathers completed primary and tertiary education, and more Slovenes finished secondary programs, i.e., 11–13 years), and maternal employment status (more Slovenes were full-time employed, whereas more Austrians were employed part time). Concordantly, parental employment status was significantly higher in Slovenia, although the Austrian students assessed financial status of their family significantly higher than the Slovenes. In contrast, significantly more Slovenes deemed to get full parental financial support they need.

We used a snowball sampling by contacting and inviting first-year students of psychology or social science university programs. They were also asked to recruit first-year students from other study programs. The participation was voluntary and anonymous. Data were collected through an online survey. Institutional review board approval was attained for the main study on financial socialization of emerging adults and received by the principal investigator who initiated an international cooperation with Austria and Slovenia as participating countries.

Measures

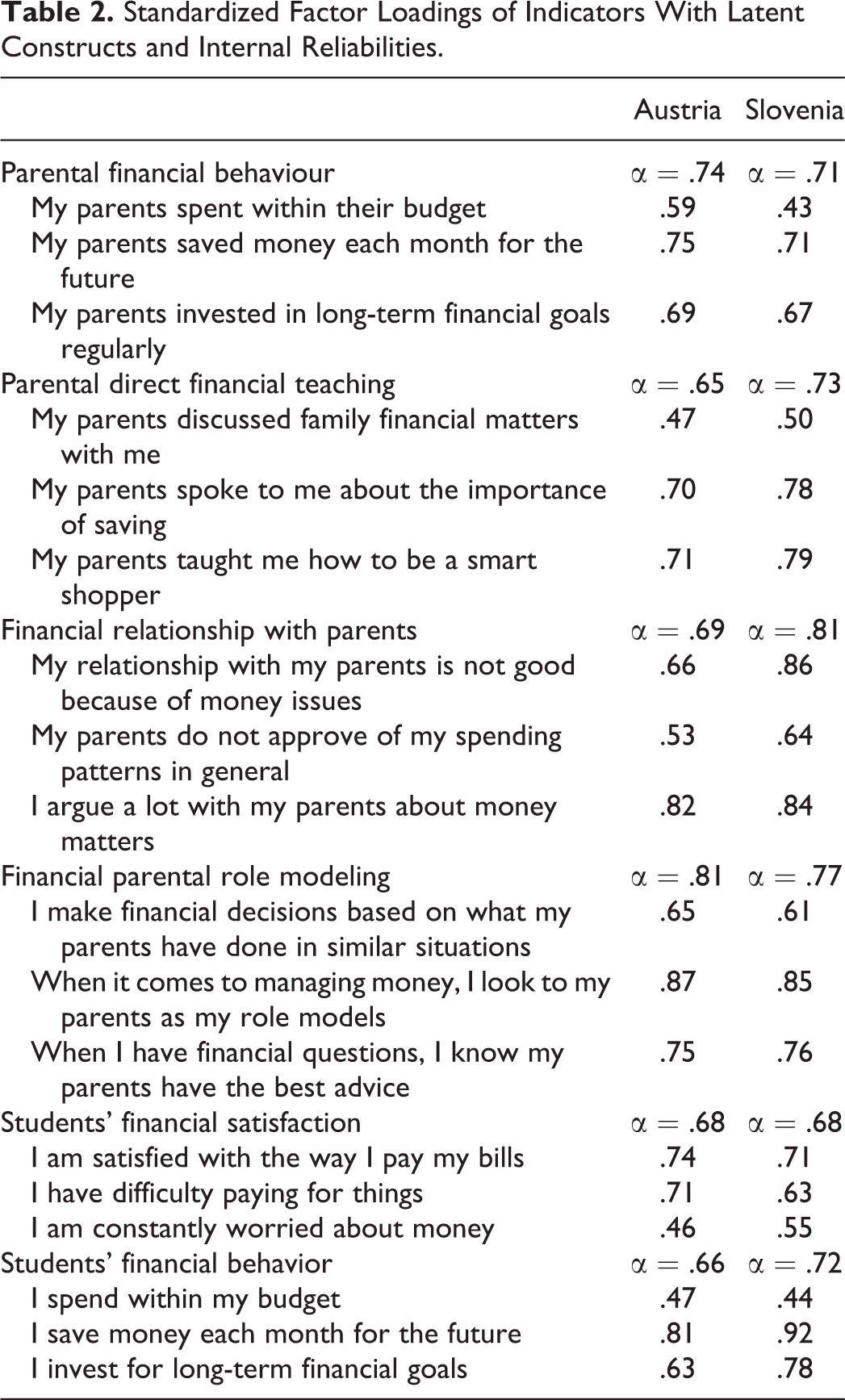

Along with sociodemographic questions (characteristics reported in Table 1), students responded to the questions based on measures used by Shim et al. (2010). However, we omitted a few items as they did not apply to the Austrian and Slovene students’ context (e.g., “Paying credit card balances in full each month. Discussed how to finance my college education with me.”). If not specifically stated, we used identical full scales/questions as Shim et al. (2010). For measures requiring students’ responses in relation to mother and father separately, we used aggregated item ratings because all of the cross-parent correlations exceeded .50, with an average correlation of .64. All items, information about the structure of the items, and internal reliabilities of the measures are presented in Table 2.

The SES measure used by Shim et al. (2010) was not applicable in Austria and Slovenia (income is an individual’s private matter). Thus, we determined SES by average standardized scores for parental education, employment status (reported by students), and financial status (Table 1) of one’s family (compared to other families in Austria/Slovenia, indicated on a 5-point rating scale—low, lower middle, middle, upper middle, or upper).

Parental/students’ financial behavior. From originally 5 items used by Shim et al. (2010), we applied 3 items (Table 2). Students indicated their recollections of maternal and paternal (separately) financial behavior prior to their enrollment to the university on a 5-point rating scale from strongly disagree to strongly agree. Using a self-report form of the items, students also assessed their current financial behavior.

Parental direct financial teaching. From originally 6 items used by Shim et al. (2010), we selected 3 items that fit the Austrian/Slovene context (Table 2). Participants assessed their mother’s and father’s engagement in teaching them financial management over preuniversity years on a 5-point rating scale (1 = strongly disagree, 5 = strongly agree).

Financial relationship with parents. The 3 items used (Table 2) to measure financial relationship with parents referred to the extent to which students agree with statements regarding conflict and stress in their current relationship with mother and father (separately) due to financial matters. They answered on a 5-point scale from 1 (strongly disagree) to 5 (strongly agree); the higher the score, the lower the quality of the relationship.

Adopting parental role modeling. Adopting parental role modeling measured the extent to which students adopt the financial roles of their mother and father (separate ratings) at present. Subjects indicated their agreement with three items (Table 2) on a 5-point rating scale (1 = strongly disagree, 5 = strongly agree). The first 2 items were taken from the 4-item scale by Shim et al. (2010), and the third one was newly developed.

Satisfaction with personal money management. Satisfaction with personal money management was assessed with 3 items (Table 2), asking students to which extent they are currently satisfied with paying their bills, managing purchases, and being worried about money. A 5-point rating scale from 1 (strongly disagree) to 5 (strongly agree) was used.

Financial knowledge. Financial knowledge was indicated by means of a single item asking students to rate their current overall understanding of money management on a 5-point scale (1 = very low, 5 = very high). In contrast to Shim et al. (2010), we only relied on the subjective measure because the objective test they used was not applicable in our contexts; in their U.S. sample, the authors also reported its unacceptable reliability and a considerably lower factor loading of the objective than the subjective measure on the financial knowledge construct.

Financial behavior control. This one-question measure examined students’ perception of how easy or difficult it is for them to stick to money management plans at present. They answered on a scale from 1 (very difficult) to 5 (very easy).

Standardized Factor Loadings of Indicators With Latent Constructs and Internal Reliabilities.

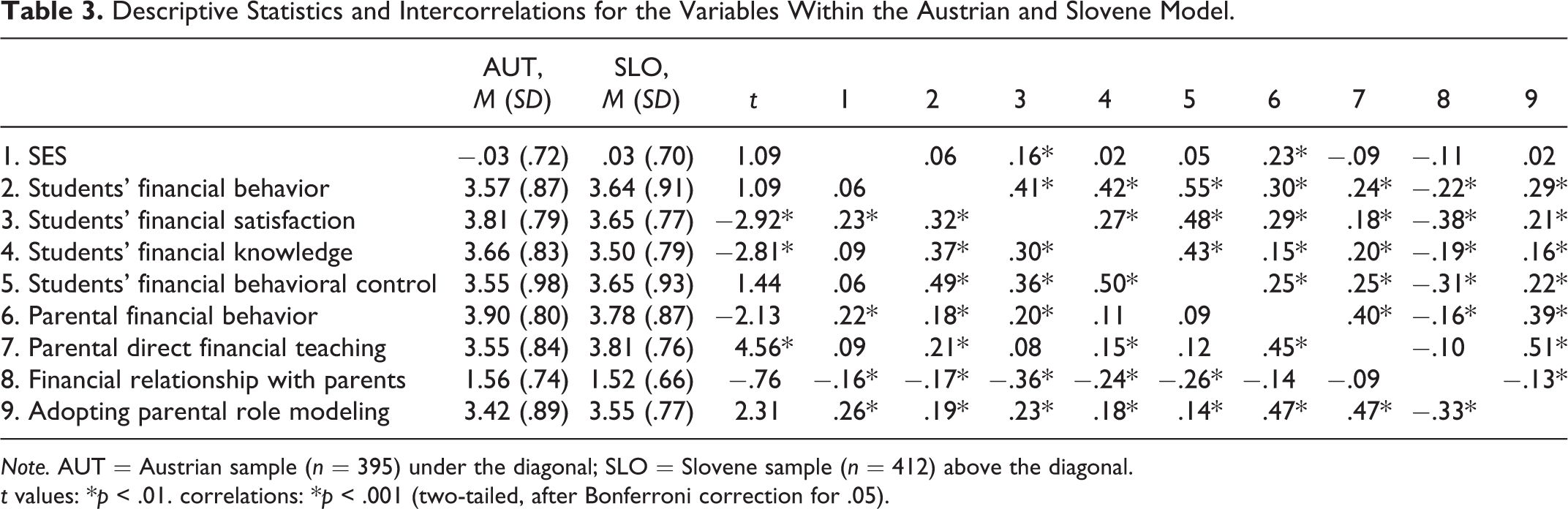

Descriptive Statistics and Intercorrelations for the Variables Within the Austrian and Slovene Model.

Note. AUT = Austrian sample (n = 395) under the diagonal; SLO = Slovene sample (n = 412) above the diagonal.

t values: *p < .01. correlations: *p < .001 (two-tailed, after Bonferroni correction for .05).

Results

Measurement Model and Descriptive Statistics

To test the proposed path model, we undertook a two-step procedure using Mplus 7.4. First, we evaluated the measurement structure of the items by means of confirmatory factor analysis (CFA; maximum likelihood robust estimation method). The CFA was conducted for aggregated data, which included student self-perceptions and ratings in relation to mother and father (averaged by item). The multigroup measurement model fit the data modestly well, χ2(358) = 813.78, p < .001,

Austrians reported higher levels of understanding of money management and satisfaction with the respective management, but lower levels of previous parental engagement in teaching them to manage personal finances than Slovenes. Statistically significant correlations were similar across the two samples. Noteworthy (moderate in effect size) were the associations of (i) students’ financial behavior with (financial) knowledge, behavior control, and satisfaction; (ii) financial satisfaction with financial relationship with parents; (iii) students’ (financial) knowledge with behavior control; (iv) parental (financial) behavior with parental direct teaching, and adopting parental role modeling; and (v) parental direct teaching with adopting parental role modeling. Few modest associations in Slovenia (financial satisfaction with parental direct teaching; financial knowledge, and behavior control with parental financial behavior; financial behavior control with direct parental teaching) were not statistically significant in Austria, whereas SES was linked to financial relationship with parents, and adopting parental financial role modeling in Austria, but not in Slovenia.

Multi-Group Path Model

Second, we tested the path model (Figure 1). The initial multigroup path model fit the data modestly well, χ2(40) = 119.72,

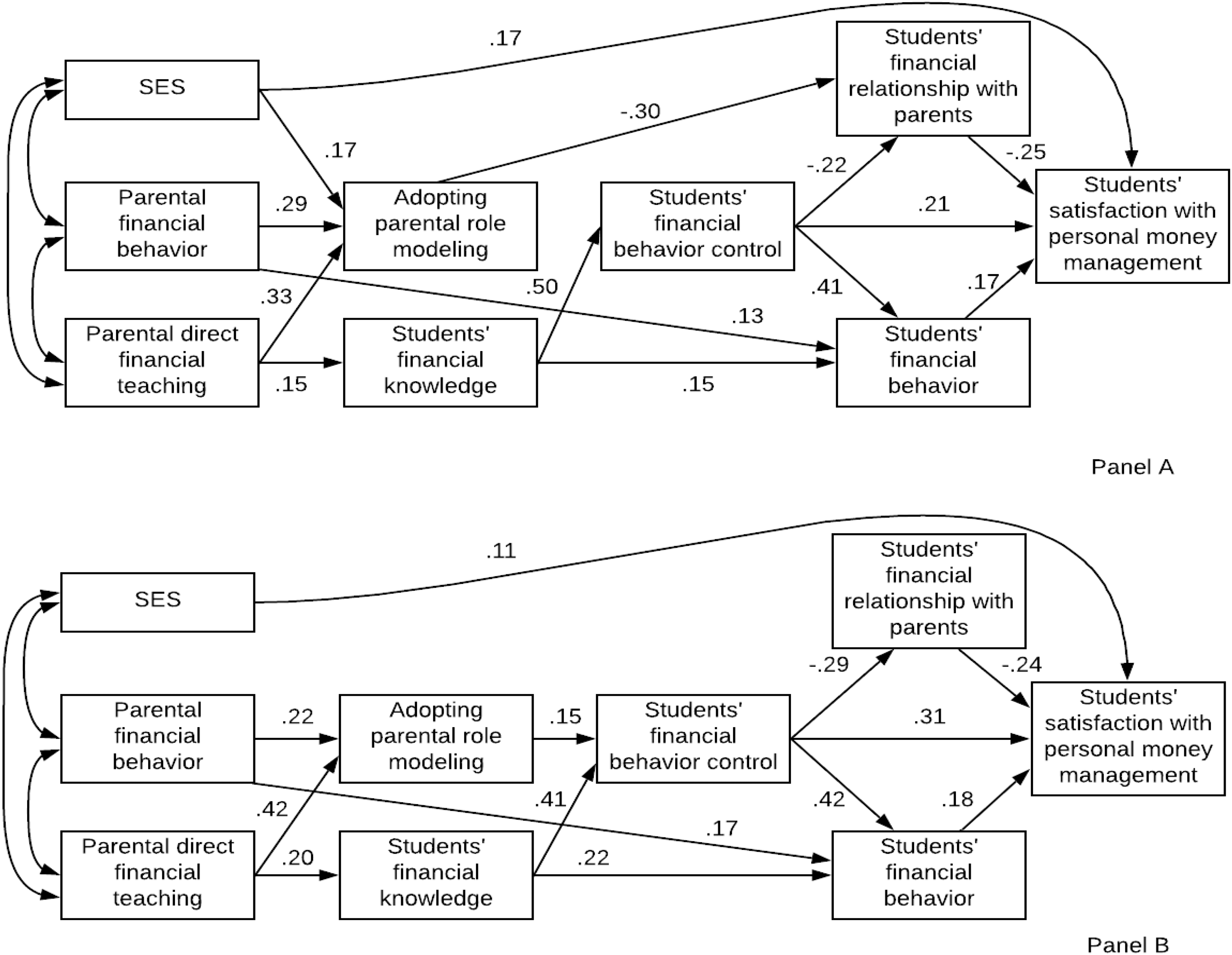

Parental financial socialization model of pathways to indicators of financial behavior in the Austrian (Panel A) and Slovene (Panel B) first-year university students. Note. Standardized path coefficients are presented (all ps < .05).

The final models explained moderate portions of variance in both students’ financial satisfaction (

Consistent Direct and Indirect Effects

The final model in each country (Figure 2) supported the pathways of students’ past financial socializing experiences with self-assessed financial learning outcomes, as proposed by the initial model. Specifically, we endorsed direct positive effects of students’ recollections of parental financial behavior on their current adopting parental role modeling (βAUT = .29; βSLO = .22) and self-perceived financial behavior (βAUT = .13; βSLO = .17) and of students’ recollections of parental financial teaching on both adoption of parents as financial role models (βAUT = .33; βSLO = .42) and subjective financial knowledge (βAUT = .15; βSLO = .20). This means that the students’ reports on past parental financial behavior tended to translate into their similar self-perceived behavior at present, and the students who perceived higher parental positive financial behavior as well as more direct parental financial teaching over their preuniversity years deemed adopting parental financial role modeling to a greater extent; those who reported more parental financial teaching also tended to rate their financial knowledge higher. Likewise, parental SES was directly associated with the students’ financial satisfaction (βAUT = .17; βSLO = .11), meaning that the students from a more favorable family background claimed more satisfaction with their money management.

As for significant associations of financial learning outcomes with the students’ self-perceived financial behavior control and financial outcomes (all in line with our initial model), the students who claimed better financial knowledge reported greater levels of both self-rated financial behavior control (βAUT = .50; βSLO = .41) and positive financial behavior (βAUT = .15; βSLO = .22). Also, the students’ subjective financial knowledge partly mediated a positive effect of prior parental direct financial teaching on their self-assessed financial behavior control (βAUT = .07; βSLO = .08; see also Table 4 for indirect effects). Self-perceived behavioral control further influenced the three “healthy” financial outcomes, financial behavior (βAUT = .41; βSLO = .42), financial relationship with parents (βAUT = −.22; βSLO = −.29), and financial satisfaction (βAUT = .21; βSLO = .31) and mediated (Table 4) the effect of financial knowledge on two outcome measures. Precisely, higher students’ self-perceived financial behavior control enhanced their (self-assessed) positive financial behavior, relationship with parents due to financial matters, and satisfaction with money management; moreover, the students who deemed more financial knowledge perceived themselves in a better control of financial behavior, which in turn contributed to their self-rated positive financial behavior (βAUT = .20; βSLO = .17) and financial relationship with parents (βAUT = −.11; βSLO = −.12).

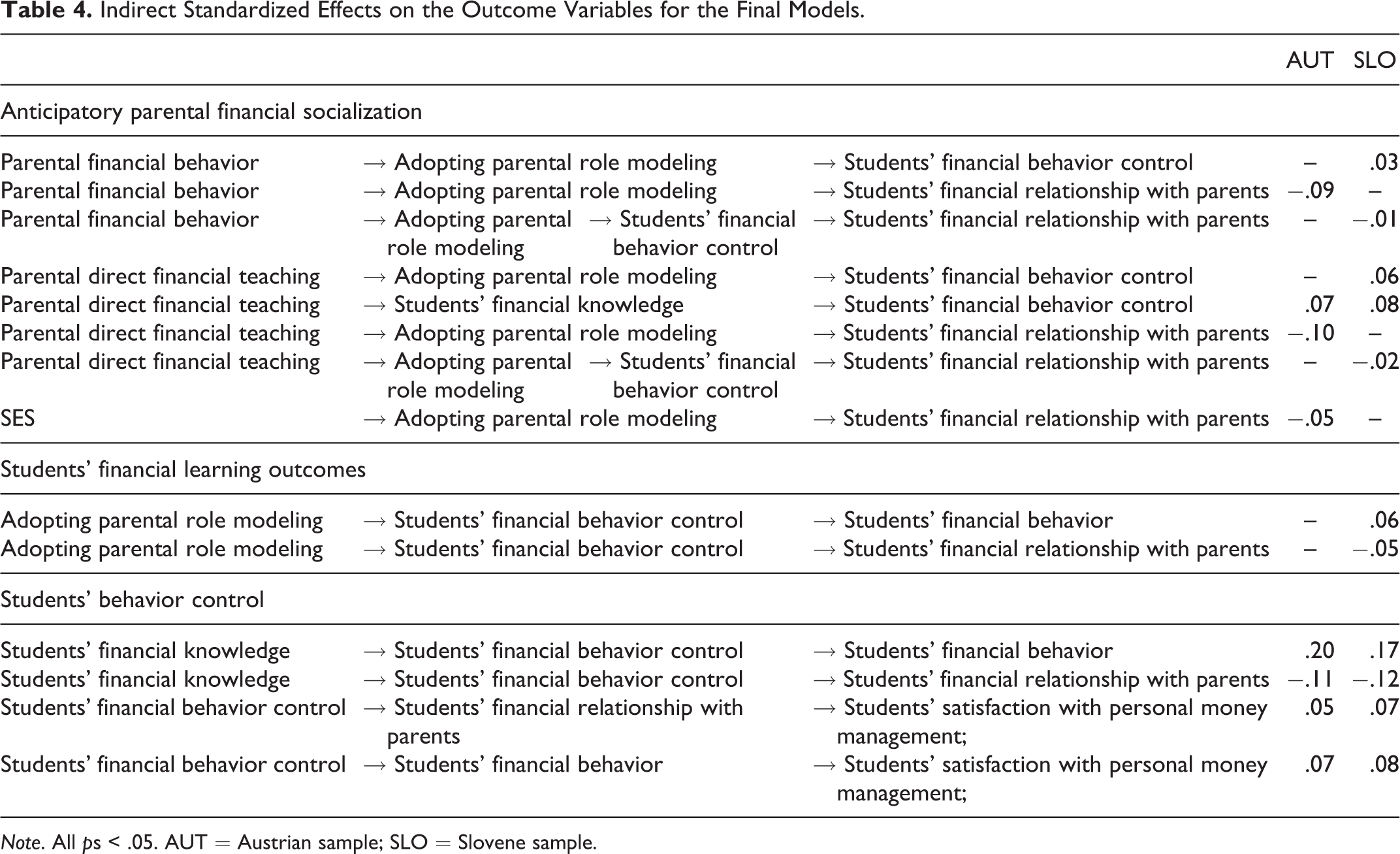

Indirect Standardized Effects on the Outcome Variables for the Final Models.

Note. All ps < .05. AUT = Austrian sample; SLO = Slovene sample.

As suggested by the initial model and in addition to Shim et al. (2010), our results supported significant pathways of both financial relationship with parents and students’ financial behavior toward their financial satisfaction (βAUT = −.25; βSLO = −.24 and βAUT = .17; βSLO = .18, respectively). Specifically, those who reported better relationship with parents due to financial matters and rated their financial behavior more favorably tended to experience higher satisfaction with their money management. In addition, both students’ perceptions of their financial relationship with parents (βAUT = .05; βSLO = .07) and financial behavior (βAUT = .07; βSLO = .08) mediated the influence of self-perceived financial behavior control on the students’ financial satisfaction (Table 4).

Country-Specific Pathways

In addition to the initial model, we determined direct and indirect country-specific pathways (Figure 2). In contrast to the Slovenes, adopting the parents as financial role models directly contributed to the Austrian students’ financial relationship with parents (βAUT = −.30), but not to self-perceived financial behavior control (βSLO = .15). Parental SES positively influenced adopting parents as financial role models (βAUT = .17), which also mediated the effect of SES on the Austrian students’ financial relationship with parents (βAUT = −.05; Table 4). The Austrians who adopted the parents as models in the financial domain to a greater extent reported a more favorable relationship with parents due to financial matters, and higher parental SES partly contributed to this relationship through enhancement of the students’ adoption of parents as financial role models. On the other hand, the Slovene students (but not the Austrians) who reported adopting parents as financial role models to a greater extent felt in a better control of their financial behavior (βSLO = .15).

Previous financial experiences provided by parents further indirectly affected the students’ financial relationship with parents in country-specific ways (Table 4). Whereas both recollections of parental direct financial teaching (βAUT = −.10) and parental financial behavior (βAUT = −.09) positively influenced the Austrian students’ current financial relationship with parents (note reverse coding) via greater adoption of parents as financial role models (as a learning outcome), the effect of those financial socializing experiences in the Slovene students was further mediated through stronger (self-perceived) financial behavior control (βSLO = −.02 and βSLO = −.01 for teaching and parental behavior, respectively). In addition, there was a unique mediation effect of prior parental financial socializing experiences on the Slovene (but not the Austrian) students’ self-perceived financial behavior control through their greater adoption of parents as financial role models at present (βSLO = .06 and βSLO = .03 for teaching and parental behavior, respectively). Likewise, the Slovene students’ adopting parental financial role modeling positively influenced both their financial behavior (βSLO = .06) and their relationship with parents (βSLO = −.05) via greater financial behavior control. This means that for the Slovenes, a higher amount of recollected parental financial socialization and/or a stronger adoption of parents as financial role models enhanced their relationship with parents (in an instance also financial behavior) through an increased (self-perceived) financial behavior control.

Discussion

The purpose of this study was to examine the role of parental financial socialization in financial learning, financial behavior control and finance-related functioning among first-year university students from Austria and Slovenia. Comparing the pathways of students’ recollections of anticipatory parental financial socialization through self-reported financial learning outcomes (including financial behavior control) toward indicators of healthy financial outcomes (financial behavior, financial relationship with parents, and financial satisfaction), we found similarities, but also differences between the two European samples. Findings of multigroup path modeling highlight the importance of investigating financial socialization models among students in different sociocultural contexts.

Similarity of Links Among Anticipatory Financial Socialization, Financial Learning, and Outcomes

Concordant to the findings in the United States (Serido, Shim, Mishra, & Tang, 2010; Shim et al., 2010), the Austrian and Slovene students coming from more favorable family background deemed greater satisfaction with money management, perhaps because they can more easily get money for unexpected expenditures from parents. The pathways of our students’ financial socializing experiences by parents toward the indicators of healthy financial outcomes furthermore suggested the importance of prior parental involvement in predicting those outcomes. The participants who recalled higher levels of parental positive financial behavior and financial instruction prior to entering university were more likely to adopt parents as financial role models. Recollections of parental teaching about financial matters also led toward another financial learning outcome—self-perceptions of greater financial knowledge. Higher subjective financial knowledge then facilitated students’ sense of control over financial behavior, which translated directly to their self-perceived positive financial behavior.

Furthermore, the students’ financial behavior control was involved in mediation of significant effects of their subjective financial knowledge on self-perceived financial behavior and financial relationship with parents in both countries under study, which concurs with findings by Shim et al. (2010) in the United States. Higher financial behavior control may suppress impulsive financial decisions, promote resistance to temptation of immediate gratification, decrease the likelihood of engagement in risky financial actions, and enhance students’ responsible financial behavior, their relationships with parents due to financial matters, as well as their satisfaction with money management. From a broader scope, it seems that financial behavioral control has a critical and perhaps a universal role in a wide range of healthy financial behaviors and satisfaction across various consumer-oriented societies (e.g., Shim et al., 2010; Shim, Xiao, Barber, & Lyons, 2009; Zupančič, Sirsch, & Poredoš, 2018).

In addition, we showed that both the students’ self-perceived positive financial behavior and financial relationship with parents due to financial matters enhance the students’ satisfaction with money management, as also reported in the United States by Serido, Shim, Mishra, and Tang, (2010), who referred to financial coping, perceived parental financial communications, and the reverse of financial stress, respectively. It appears that the associations mentioned thus far are robust across developmental ecologies of the first-year Austrian, Slovene, as well as U.S. university students (Serido et al., 2010; Shim et al., 2010), especially in the light of the fact that (due to a different life context of the European students) we had to apply a reduced and somewhat adjusted set of measures and relied on a less sound measurement model (though acceptable) to those in the United States. In this regard, it is of note that both parental and student financial behavior item “tracking monthly expenses” showed low factor loadings on the respective construct in both European samples in our preliminary test of the measurement model. Therefore, we omitted this item from further analyses. Perhaps tracking monthly expenses is more important when students use their own credit cards and get student loans (e.g., in the United States), which is not possible in Austria and Slovenia without (at least) substantial amount of permanent income. Students thus use cash and debit cards or smartphone modes of payment; exceeding an overdraft frame on a bank account is fairly restricted for them if at all possible, and money available on the account is immediately shown on a display of money machine and/or one’s smartphone after each outflow.

In contrast to the U.S. (Shim et al., 2010) and Canadian (Angulo-Ruiz & Pergelova, 2015) undergraduate university students, both the Austrians and the Slovenes seemed to directly emulate recollected parental behavior regarding spending, saving, and managing money issues. Given that the Austrian participants were older, more likely led their own household and less likely to receive full parental financial support than the Slovenes (corresponding to the respective population differences, Eurostat, 2019b; Institute for Advanced Studies, 2016; SURS, 2018), our results suggest that simply enacting past parental financial behavior does not diminish with students’ age, moving out of parental household, and overtaking more financial responsibilities. Differences in European and North American cultural contexts may be involved and warrant further cross-national research.

Country Differences in Pathways to Healthy Financial Outcomes

Country-specific pathways indicate an important role of context in the development of financial behavior as suggested by Jorgensen, Foster, Jensen, and Vieira (2017) in regard to geographical locations or regions. Our findings suggest few distinct avenues to students’ financial outcomes. Adopting parental financial role modeling seems to directly prevent Austrian students’ arguing with parents about financial issues. In contrast (and in line with Shim et al., 2010), overtaking parents as financial role models appears to promote both Slovene students’ financial relationship with parents and financial behavior by means of enhanced students’ sense of control over financial behavior. The differences in the pathways involving recalled parental financial behavior and instructions as a model young people are willing to imitate may be explained within a broader process of identity exploration, a prominent developmental feature of emerging adulthood (Arnett, 2015). As our Austrian participants were older, less likely to co-reside with parents and get full financial support from parents, they may have been more involved in independent daily life, which may have promoted experimentation in the financial domain, and led to beneficial learning experiences in dealing with money. Such experiences may have improved their financial behavior control and helped them find patterns of financial behavior that suit them best. Likely to this explanation, the Austrian students also reported better understanding of money management and more satisfaction with the respective management than the Slovenes.

For the younger Slovene first-year students, still more enmeshed in a network of family relationships as they are most likely to live with the parents (or partly away), with parents willingly and widely providing them economic well-being (e.g., Kuhar & Reiter, 2014; Zupančič & Sirsch, 2018), parental financial socialization and internalization of parental financial instructions may have somewhat more influential role in their financial functioning than for the Austrian students. This may have been reflected in the Slovenes’ higher level of recalled parental engagement in teaching how to manage personal finances, stronger association of parental financial teaching with adopting parents as financial role models, indirect influences of parental socialization on students’ financial outcomes through adopting parental role modeling, and indirect effects of the latter on the outcomes through enhancement of students’ self-perceived financial behavior control.

Taken together, we provided support for the hypothesis that first-year university students’ recollections of anticipatory parental financial behavior and parental teaching about financial matters shapes (directly and/or indirectly) their healthy financial behavior and parent–child financial relationships, which in turn contribute to young people’s satisfaction with money management. We also showed similarities and differences in pathways of perceived parental financial socialization toward indicators of students’ self-reported financial outcomes in contexts beyond the United States.

Limitations of the Study and Future Directions

Several limitations of this study should be noted. We relied on single-informant data, which may have inflated the predictive associations due to shared method variance. Multiple informant approach (e.g., parent reports) to students’ management of financial issues is thus needed to provide a more complex view on the topic from various perspectives. Parents are primary financial socialization agents, they still (more or less) financially support their emerging adult children and, as our results along with many other studies (e.g., Jorgensen & Savla, 2010; Serido et al., 2010; Shim et al., 2010, Shim et al., 2015) suggest, remain relevant actors for their offspring’s financial behavior and well-being. Hence, it would be essential to determine how parents promote emerging adults’ financial autonomy and how the latter build their financial identities to manage the developmental task of attaining financial independence.

Our samples were confined to the first-year university students, and the findings should not be generalized to their employed/unemployed age peers or older emerging adults. In prospect, it would be necessary to follow up first-year students to ascertain how the proposed pathways of prior family financial socialization processes toward subsequent students’ financial management and financial satisfaction may change. Related to this argument, the one time-point data collection and correlational nature of our study did not allow us to test plausible bidirectional pathways, which requires a cross-lagged design and awaits future inquiry.

Given the specific research problem, we collected data on a restricted number of variables based on student reports, including retrospective assessments of parental financial socialization. The range of measures relevant to emerging adults’ financial functioning needs to be extended, for example, by applying objective measures of financial knowledge and behavioral control, and/or explore the extent to which young peoples’ financial socialization-related mental and behavioral outcomes are shaped by their peer groups (not only friends), intimate partners, financial professionals, and financial information obtained by online media.

Our findings imply a long-term significance of parental financial behavior and verbal teaching about financial matters for their offspring’s financial learning across two European contexts. However, research suggests that many adults are financially illiterate (Kočar & Trunk, 2016; Lusardi & Mitchell, 2014). Thus, to enhance a healthy learning context for their offspring parents themselves should be financially knowledgeable, skilled, engaged in positive financial practices, and successful in dealing with financial issues. Parents could be provided advice and appropriate support to teach (and learn) their children how to manage financial matters and foster their ability to delay immediate gratification (e.g., financial behavior control). In the future, parents will be also more up to educate their children to select and use appropriate online information on financial issues.

Our study further suggests that there are some likely differences in pathways of parental contribution toward their emerging adult children’s financial management, relationships, and satisfaction across developmental ecologies. Future research has to clarify possible reasons for those differences by addressing emerging adults from various geographic regions, associated with different social welfare systems and models of transition to adulthood. As identity exploration is a common feature of emerging adulthood (e.g., Arnett, 2015; Zupančič & Sirsch, 2018), research should also consider the perspective of identity theory that has been only recently applied to the financial domain (e.g., Bosch, Serido, Card, & Shim, 2016; Shim, Serido, Bosch, & Tang, 2013). Adopting parents as financial role models, for example, could apply to the normative identity style, defined as “internalizing and adopting prescriptions and expectations of significant others in a relatively automatic fashion” (Berzonsky, Branje, & Meeus, 2007, p. 326) but may, according to Marcia (1966), reflect the foreclosed identity status (doing what parents find right without any previous exploration) or perhaps the achieved status (accepting those parental norms and expectations, which an individual established to suit him/her best after exploring many alternatives). Including aspects of financial identity development into financial socialization models offers another promising avenue to understanding how the processes of parental financial socialization operate in emerging adults’ attainment of healthy financial management, financial independence and well-being in different socio-cultural contexts.

Supplemental Material

Supplemental Material, Badge_1 - Does Parental Financial Socialization for Emerging Adults Matter? The Case of Austrian and Slovene First-Year University Students

Supplemental Material, Badge_1 for Does Parental Financial Socialization for Emerging Adults Matter? The Case of Austrian and Slovene First-Year University Students by Ulrike Sirsch, Maja Zupančič, Mojca Poredoš, Katharina Levec and Mihaela Friedlmeier in Emerging Adulthood

Supplemental Material

Supplemental Material, Badge_2 - Does Parental Financial Socialization for Emerging Adults Matter? The Case of Austrian and Slovene First-Year University Students

Supplemental Material, Badge_2 for Does Parental Financial Socialization for Emerging Adults Matter? The Case of Austrian and Slovene First-Year University Students by Ulrike Sirsch, Maja Zupančič, Mojca Poredoš, Katharina Levec and Mihaela Friedlmeier in Emerging Adulthood

Footnotes

Author Contributions

Ulrike Sirsch and Maja Zupančič contributed to conception and design, acquisition, analysis, and interpretation; drafted the manuscript; gave final approval; and agrees to be accountable for all aspects of work ensuring integrity and accuracy. Mojca Poredoš and Katharina Levec contributed to acquisition, analysis, and interpretation; drafted the manuscript; and gave final approval. Mihaela Friedlmeier (principal investigator) contributed to conception and design, acquisition, and interpretation; critically revised the manuscript; gave final approval.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Open Practices

Data and materials for this study have not been made publicly available. The design and analysis plans were not preregistered.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.