Abstract

This study aims to investigate how sociocultural factors shape financial practices in fragile contexts such as Somalia. This study employs structural equation modeling (SEM) to analyze survey data collected from various sectors of Somali society in March 2024. The measurement model was tested for validity and reliability, whereas the structural model examined the hypothesized relationships among sociocultural factors, financial practices, and regulatory environments. The analysis reveals a statistically significant positive relationship between sociocultural factors and financial practices, affirming the centrality of trust, communal norms, and informal institutions in shaping financial behavior. The regulatory environment was found to play a mediating role, either facilitating or constraining the influence of sociocultural dynamics. Furthermore, communal financial perceptions and participation were strongly linked to broader socioeconomic outcomes. The findings underscore the need for culturally attuned financial policies that legitimize and integrate informal financial systems. This study proposes a novel multitheoretical framework in the context of Somalia, urging policymakers in fragile states to design hybrid regulatory systems that align financial inclusion efforts with the social and cultural embeddedness of financial behavior. By situating informal finance within its sociocultural and institutional context, mainstream development narratives that marginalize informal systems as transitional or deficient are challenging. The research extends the theoretical discourse by empirically validating the interplay between sociocultural dimensions, institutional environments, and financial practices in fragile states. It also advances methodological rigor in the field by applying SEM to model latent relationships in an underresearched context such as Somalia.

Plain Language Summary

In many countries experiencing conflict or weak government systems—often referred to as fragile states—people rely heavily on informal financial systems to manage their money. This study focuses on Somalia, where most individuals do not use traditional banks but instead depend on community-based financial practices such as hawalas (informal money transfer services) and rotating savings groups. These systems are built on trust, shared cultural values, and social networks. The research aimed to understand how these socio-cultural factors shape financial behavior and how government rules and policies might support or disrupt these informal systems. To investigate this, researchers conducted a survey with 118 participants from various sectors of Somali society in March 2024. They used a method called Structural Equation Modeling (SEM) to examine the relationships between community trust, cultural norms, financial practices, and regulatory environments. The results showed a strong link between cultural and social factors and financial behavior. People tend to make financial decisions—like saving, borrowing, and sending money—based on social connections and community expectations. The study also found that formal regulations can either strengthen or weaken these financial practices depending on whether they align with local customs and realities. The findings suggest that informal financial systems are not simply a temporary solution, but a resilient and functional part of economic life in Somalia. They offer stability, access, and flexibility where formal institutions are limited. For governments, NGOs, and development agencies, this means that successful financial inclusion policies must respect and work with existing community practices rather than try to replace them. Supporting these culturally embedded systems can help improve economic well-being and promote more sustainable and inclusive development in fragile contexts like Somalia.

Keywords

Introduction

Somalia presents a complex sociopolitical and economic landscape shaped by decades of conflict, institutional collapse, and persistent efforts toward national reconstruction. The social structure of Somali society remains deeply rooted in clan-based affiliations, which continue to function as pivotal systems of governance, conflict resolution, and social support in the absence of strong state institutions (Hashi & Hock, 2025; Menkhaus, 2007). These clan networks serve as informal governance mechanisms that facilitate social cohesion and resource distribution, thereby compensating for the long-standing vacuum in centralized authority.

After the collapse of Siad Barre’s rule in 1991, Somalia entered a prolonged era of statelessness, marked by political fragmentation, insecurity, and the rise of armed factions (Menkhaus, 2014). Despite these challenges, Somalia has experienced a succession of transformative advancements in recent years, encompassing the incremental reconstruction of its federal system, the attainment of the Highly Indebted Poor Countries (HIPC) debt relief initiative, and membership in the East African Community (EAC), signifying renewed endeavors toward institutional and economic stabilization (Nor & Moge, 2024).

Somalia’s economy is predominantly dependent on agriculture, livestock, remittances, and a dynamic informal sector, especially in telecommunications and mobile financial services (Mubarak, 1997; Osman & Abebe, 2023). Given the lack of dependable formal financial infrastructure, informal financial systems—such as hawalas, rotating savings and credit associations (ROSCAs), and community-based savings groups—have become crucial for facilitating liquidity, credit accessibility, and cross-border remittances (Nor, 2012; Virak & Bilan, 2022). These methods not only demonstrate economic adaptation but are also intricately woven into the sociocultural fabric of Somali society.

However, prevailing financial development theories have historically sidelined these systems, perceiving them as temporary or informal measures rather than as legitimate and sustainable economic institutions. This marginalization frequently overlooks the integration of financial activities within social norms, cultural values, and communal trust frameworks—an omission that considerably restricts the relevance of traditional economic models in precarious environments.

This paper argues that informal financial practices in Somalia cannot be fully understood without considering the sociocultural factors that influence and sustain them. Communal trust, community norms, and religious beliefs are crucial in legitimizing and regulating financial transactions in environments lacking formal institutions or where such organizations are distrusted. Mainstream finance research often overlooks these processes, focusing instead on formal regulatory mechanisms and institutional efficiency.

Somalia, as a prototypical fragile state, offers a compelling case for examining the intersection of finance and culture. While much of the literature on fragile states focuses on macrolevel governance and institutional rebuilding, less attention has been given to how local financial systems evolve and persist under conditions of chronic instability. Similarly, the literature on financial practices in fragile contexts often emphasizes regulatory frameworks and institutional roles, with scant attention to the influence of sociocultural factors (see, for instance, Brinkerhoff, 2010; Dirani, 2006; Thornton et al., 2011). By focusing on the microfoundations of informal finance, this study addresses a significant gap in the literature and contributes to a more holistic understanding of economic behavior in fragile environments.

The primary objective of this research is to evaluate the sociocultural factors influencing informal financial practices in Somalia. It seeks to examine how these activities not only enable commercial transactions but also foster social cohesiveness and resilience in an environment characterized by minimal governmental presence. This study specifically examines the influence of trust, social norms, and communal values on savings, borrowing, and investment behaviors beyond formal institutional frameworks.

This study makes three key contributions. First, it provides empirical evidence on how sociocultural norms, communal financial perceptions, and regulatory environments interact to shape financial practices in a fragile, postconflict setting, using Somalia as a case study. Second, by applying a multitheoretical framework and a structural equation modeling (SEM) approach adapted to the realities of small-sample research, the study demonstrates a methodological pathway for rigorous quantitative analysis in challenging contexts. Third, the findings have direct implications for policymakers, financial institutions, and development agencies seeking to design culturally sensitive and context-specific interventions that enhance financial inclusion and stability in fragile states. Collectively, these contributions advance the scholarly understanding of the sociocultural dimensions of finance while offering practical insights for sustainable economic development in Somalia and comparable environments.

Literature Review

Global Perspectives on the Socio-Cultural Dimensions of Financial Practices

The sociocultural aspects of finance have received increasing attention in the global development literature, especially in situations where formal institutions are deficient or unattainable. Preliminary research conducted by Geertz (1978) on the bazaar economy in Morocco revealed that economic behavior is profoundly influenced by social norms and cultural expectations. Their ethnographic research demonstrated that trust, reciprocity, and reputation function as essential mechanisms for regulating trade in informal markets. Portes and Sensenbrenner (1993) further developed this perspective by analyzing how immigrant groups in the United States leveraged dense social networks to enable informal financial transactions, frequently establishing economic systems alongside official banking institutions.

In Latin America, researchers have noted the efficacy of informal credit systems among cohesive communities, which depend on social capital and mutual accountability. Jaffe et al. (2007) discovered that trust-based lending solutions address significant financial deficiencies for small businesses lacking access to formal credit. Correspondingly, research in South Asia, including Brown et al. (2019) and Ghate (1988), emphasized that familial connections and local customs support informal lending practices among small-scale traders and farmers, providing both economic benefits and social security.

Research in sub-Saharan Africa (SSA) has highlighted the dual function of rotating savings and credit associations (ROSCAs) as both financial and social entities. Verhoef and Hidden (2022) and Adeola et al. (2022) discovered that these associations function as both credit mechanisms and venues for communal solidarity and mutual support. These findings question the conventional economic development narrative that depicts informal finance as a temporary or inferior substitute for formal systems.

Critical scholarship, exemplified by Elyachar (2005), contends that foreign development paradigms frequently marginalize indigenous financial practices by neglecting their cultural contextualization. Elyachar (2005), on the basis of fieldwork in Cairo, argues that informal economies are not just operational but also frequently more adaptable and participatory than the formal institutions established through neoliberal changes. This global literature emphasizes the need to reevaluate financial inclusion initiatives while considering sociocultural factors, particularly in fragile or postconflict environments.

Regional Insights: Informal Finance in East Africa

The East African region presents a complex array of informal financial practices influenced by many cultural and historical factors. Shipton (1990) offered a comprehensive analysis of financial decision-making within the Luo community in Kenya, demonstrating that economic transactions are intricately linked to social expectations, familial obligations, and traditional customs. In this setting, money serves not only as a medium of commerce but also as a social resource regulated by ethical responsibilities.

Hydén (1980) concept of the “economy of affection” in Tanzania illustrates the significant impact of personal relationships on economic activity within rural communities. His work positioned informal finance not as a divergence from modernity but as a fundamental element of the social contract between extended families and local communities.

Research conducted by Bastiaensen et al. (2005) in Uganda indicates that informal savings clubs, particularly those managed by women, enhance financial resilience, and promote community agency. These entities serve as multifaceted institutions, integrating economic collaboration with emotional assistance and social acknowledgment.

Recent research has broadened this discussion to include regional differences and the legacies of postcolonial institutions. van den Boogaard and Santoro (2022) examined the influence of local governance institutions and trust dynamics on informal taxes and savings habits. Nguyen and Albright (2022) and Kwarkye (2021) noted that colonial histories and structural adjustment initiatives have generated disparate informal banking systems throughout the area. Although trust-based financial systems exhibit commonalities, localized responses to governance deficiencies have resulted in varied institutional adaptations, necessitating context-specific economic interventions.

East African studies validate the significance of sociocultural studies in comprehending informal finance. Nonetheless, they emphasize the necessity for more comprehensive, nation-specific inquiries—particularly in environments characterized by enduring state fragility, such as Somalia.

Somalia-Specific Research: Financial Practices in a Fragile Context

The literature on informal financial practices in Somalia is influenced by the distinctive convergence of enduring conflict, clan rule, and religious principles. Lindley (2007) analyzed how remittances sent through informal channels, such as hawalas, not only offer essential cash support but also strengthen social duties and clan affiliations. Remittance flows are frequently perceived not merely as economic transactions but also as manifestations of loyalty, solidarity, and moral obligation within diasporic networks.

The Islamic influence on financial practices in Somalia is well recorded. Hassan et al. (2025) and Yusuf et al. (2024) examined the adaptation of Sharia-compliant finance to local requirements, providing culturally acceptable financial services in the absence of a strong formal banking sector. These systems function via trust-based procedures that adhere to Islamic values, resulting in a robust match between religious ethics and economic conduct. Warsame (2016) demonstrates the evolution of Islamic financial concepts in Somalia, integrating global norms with indigenous values.

Menkhaus (2000) underscored the pivotal function of the Somali clan system in economic governance. Clan-based trust networks furnish the social capital essential for informal transactions, particularly in the absence of governmental enforcement. Little (2003) expanded this research to encompass cross-border trading, demonstrating how clan attachments surpass national boundaries to facilitate intricate, transnational financial transactions.

Subsequent contributions by Nor (2012), Nor and Tajul (2018, 2019), and Ingiriis (2020) examine how Somalia’s informal economy functions not only as a survival mechanism but also as a complex adaptive system. These studies demonstrate the integration of financial activities into Somali social life, regulated by principles of mutual assistance, religious duty, and communal trust. Mubarak (1997) previously contended that informal finance in Somalia fulfills institutional roles—providing dispute resolution, credit distribution, and social services—in manners analogous to those of formal institutions.

Despite the expanding corpus of knowledge, substantial gaps persist. Limited research has utilized integrated theoretical frameworks, such as social capital or institutional theory, to evaluate the influence of sociocultural factors on financial behaviors. Moreover, there is a paucity of empirical research examining how these systems might guide development policy in fragile contexts.

In summary, the literature across global, regional, and Somalia-specific contexts illustrates that informal financial systems are not aberrations but contextually embedded institutions. They respond to local needs and values, often outperforming formal mechanisms in fragile or underdeveloped settings. However, much of the existing research lacks a unified theoretical approach and repeatedly treats cultural factors as secondary rather than central. This study builds on and seeks to extend the literature by using Somalia as a focused case study to examine how informal financial practices are shaped by—and in turn reinforce—sociocultural structures in fragile states. It aims to fill a critical gap by integrating theoretical insights with empirical data to inform more inclusive and locally grounded financial development strategies.

Summary

Research on informal financial practices in fragile and postconflict states consistently underscores the centrality of sociocultural norms, trust networks, and reciprocal obligations in sustaining economic activity where formal institutions are weak or absent. Studies from diverse contexts such as Afghanistan, South Sudan, and the Democratic Republic of Congo demonstrate that informal mechanisms—often grounded in kinship, religion, and local governance traditions—serve both as substitutes for and complements to formal financial systems (Kass-Hanna et al., 2022; Meagher, 2013; van den Boogaard & Santoro, 2022). These findings parallel earlier anthropological and sociological accounts (Geertz, 1962; Portes & Sensenbrenner, 1993) that frame informal finance as being embedded within wider systems of moral economy and collective identity. Such work highlights how social capital both facilitates financial exchange and imposes constraints, for example, through obligations that limit individual economic mobility.

In East African contexts, the interaction between sociocultural norms and financial behavior has been well documented. Shipton (2007) and examine how trust, reciprocity, and moral economy shape rotating savings and credit associations (ROSCAs) and other community-based finance systems in Kenya and Tanzania. Ugandan evidence (Bastiaensen et al., 2005) further illustrates the dual role of informal networks in fostering resilience while reproducing inequalities. Cross-regional analyses (Kwarkye, 2021) reveal that while such systems are adaptive, their effectiveness depends heavily on the broader regulatory and institutional environment—especially the extent to which state actors either accommodate or attempt to formalize these practices. These comparative perspectives offer important parallels to Somalia, where informal systems are deeply entrenched yet operate within a unique postconflict political economy.

Within Somalia, scholarship on remittance systems (Lindley, 2009), clan-based governance (Menkhaus, 2014), and Islamic finance (Hassan & Kayed, 2009; Mohamed & Nor, 2021) provides a rich foundation for understanding the intersection of cultural identity, religious norms, and financial behavior. These studies show how clan structures and religiously informed financial principles (such as prohibitions on ribs) influence both the design and uptake of financial services. Informal hawala networks, in particular, exemplify the fusion of trust-based relationships with transnational financial flows, sustaining household and community livelihoods despite the absence of robust formal institutions. By integrating this Somalia-specific literature with comparative insights from other fragile states, the present study situates its inquiry within a broader scholarly conversation while also addressing the country’s distinctive sociofinancial realities.

Research Gap

Despite the growing body of research on financial practices in fragile and developing states, significant gaps remain in understanding how sociocultural norms, communal financial perceptions, and regulatory environments jointly shape financial behaviors in postconflict contexts. Existing studies on informal finance in Africa and Asia (e.g., Kass-Hanna et al., 2022; Meagher, 2013) have explored related dynamics, yet few have applied an integrated multitheoretical framework combining social capital theory, institutional theory, embeddedness theory, and economic anthropology within Somalia’s unique socioeconomic and political landscape. Moreover, empirical research employing robust quantitative techniques such as structural equation modeling (SEM) in such contexts remains scarce, particularly where sample sizes are constrained and construct validity challenges arise. This study addresses these gaps by providing context-specific evidence from Somalia, offering both theoretical refinement and practical insights for policy and development interventions in similar fragile states.

Theoretical Frameworks

To scientifically examine the sociocultural aspects of financial behavior in precarious environments such as Somalia, it is crucial to employ a theoretical framework that encompasses both the economic and the cultural integration of informal financial practices. This study largely utilizes social capital theory and institutional theory while judiciously integrating insights from embeddedness theory and economic anthropology to contextualize the investigation. These theories provide complementary insights into the legitimization, maintenance, and regulation of informal financial systems by social norms and cultural values in contexts where formal institutions are deficient or nonexistent.

Social Capital Theory

Social capital theory, as developed by Putnam (1993), underscores the importance of trust, norms of reciprocity, and social networks in enabling cooperative behavior. In contexts where state capacity is limited or contested, such as in Somalia, interpersonal trust, and community ties become critical mechanisms for facilitating financial transactions. The theory helps explain how informal systems such as hawalas, ROSCAs, and community-based lending groups can function reliably even in the absence of formal enforcement mechanisms (Coleman, 1988; Narayan & Pritchett, 1999). These systems derive legitimacy not from regulatory oversight but from embedded social relationships that emphasize mutual accountability and collective benefit.

In Somalia, the strength of clan-based social networks and religious affiliations enhances the credibility of informal financial actors, allowing them to operate transnationally with minimal default risk (Lindley, 2009). Social capital thus provides both a theoretical and empirical foundation for understanding the persistence and efficiency of informal financing in fragile settings.

Institutional Theory

This theory is particularly relevant to Somalia, where informal institutions have evolved to fill the governance void left by the collapse of the state. These institutions provide mechanisms for trust enforcement, dispute resolution, and financial intermediation, all of which are grounded in culturally sanctioned norms. Institutional theory highlights how informal financial practices are not merely the result of market failure but are often rational adaptations to existing institutional constraints (Brinkerhoff, 2010; Helmke & Levitsky, 2006)

Embeddedness and Social Networks

Building on these perspectives, Granovetter (1992) concept of

In the Somali context, financial behavior—such as lending, borrowing, and saving—is often influenced by cultural expectations of reciprocity and support within kinship groups or religious communities. These social structures not only shape access to financial resources but also determine the trustworthiness and risk perceptions of potential transactors (Woolcock & Narayan, 2000).

Closely aligned with this view is

Economic Anthropology

This is particularly applicable to Somalia, where informal financial systems are not merely substitutes for formal banking but are embedded within broader cultural practices and moral economies. For example, the hawala system is not only a means of remittance transfer but also a culturally significant institution built on Islamic principles of trust, honor, and collective responsibility (Maimbo & Passas, 2003; Nor, 2012).

Summary

Taken together, these theoretical frameworks provide a robust and context-sensitive foundation for analyzing financial behavior in fragile states.

Research Framework and Hypothesis Development

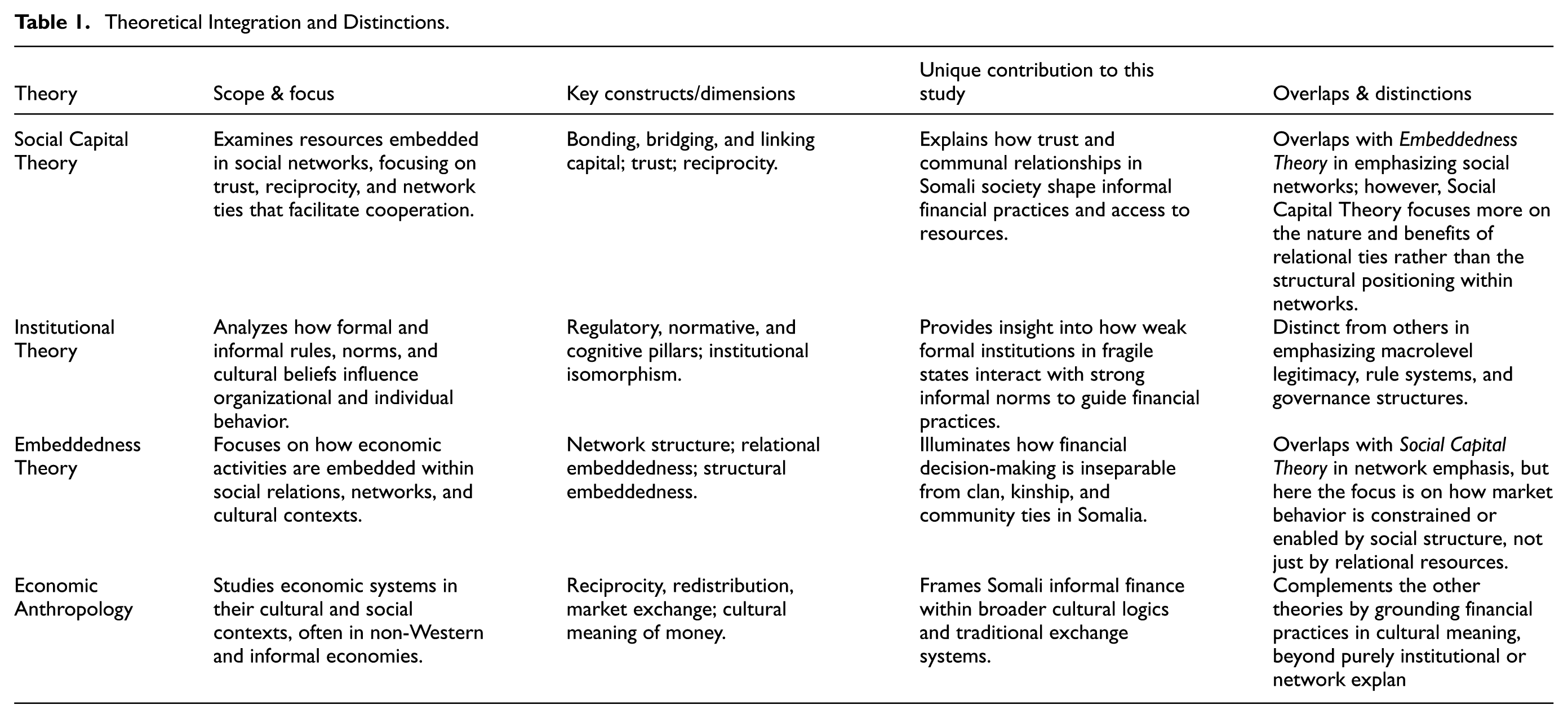

In exploring the sociocultural dimensions of financial practices in East Africa with a focus on Somalia, the research framework integrates the foundational principles of social capital theory and institutional theory (see Figure 1). Social capital theory underscores the importance of social networks and norms in facilitating cooperative behaviors that can enhance economic outcomes (Coleman, 1988; Putnam et al., 1994, 2000; Richardson, 1986). North (1990) contributes to this framework through institutional theory, which examines how formal and informal rules and regulations shape economic behavior and development. By applying these theories, this study seeks to unravel how sociocultural factors in Somali society influence financial practices, highlighting the role of communal relationships and regulatory frameworks in shaping economic activities. The integration of these theoretical perspectives provides a comprehensive lens for understanding the intricate relationships among culture, financial practices, and socioeconomic development in the region (see Table 1). The hypotheses developed in this study aim to systematically investigate the proposed relationships within the framework.

Research framework.

Theoretical Integration and Distinctions.

The development of

The formulation of

In the proposed research on the sociocultural dimensions of financial practices in East Africa, with a focus on Somalia,

Building upon the foundational hypothesis,

Methodology and Data

Research Design

This study adopts a quantitative design to assess the sociocultural dimensions of financial practices in Somalia, a representative fragile state. The design is grounded in institutional theory, social capital theory, and embeddedness theory, which inform the development of constructs related to trust, social norms, and financial behavior. To analyze the interrelations between observed and latent variables, this study employs

To assess the measurement model, we evaluated factor loadings, composite reliability (CR), average variance extracted (AVE), and heterotrait–monotrait (HTMT) ratios against widely accepted thresholds (factor loadings ≥ 0.60, CR ≥ 0.70, AVE ≥ 0.50, and HTMT ≤ 0.90). Where individual items or constructs fell slightly below these thresholds—such as the economic impact construct—we considered both theoretical relevance and empirical implications before deciding on retention, removal, or respecification (e.g., formative modeling). This transparent reporting ensures that the validity and reliability of our constructs can be independently evaluated.

Sampling Strategy and Data Collection

A

In March 2024, a structured survey was disseminated digitally across

The final sample consisted of 118 participants drawn from diverse regions of Somalia. While modest in size, this reflects the realities of data collection in fragile and postconflict settings, where security concerns and accessibility limit large-scale surveys (Brück et al., 2019). In line with the methodological literature, we adopted partial least squares structural equation modeling (PLS-SEM), which is well suited for smaller samples and complex models and can produce robust estimates when guided by strong theoretical foundations (Hair et al., 2019; Henseler et al., 2009). For single- and two-item constructs, inclusion was based on their theoretical importance and prior validation in similar sociocultural contexts (Bergkvist & Rossiter, 2007). These constructs were carefully evaluated for reliability and validity, with results reported transparently in the measurement model assessment.

The data validation process employed stringent criteria to ensure the integrity and reliability of the dataset. Entries were excluded if they contained incomplete responses, specifically if more than 20% of the data were missing. Additionally, responses exhibiting patterned or inconsistent answers on reverse-coded items were flagged and removed, as these may indicate inattentiveness or misunderstanding. To further refine the dataset, outliers were identified and excluded via Mahalanobis distance tests, which were used to detect multivariate anomalies that could skew the results. These steps collectively enhanced the quality and robustness of the final analytical sample. This sample size meets acceptable thresholds for SEM on the basis of

Construct Development and Measurement

Variable selection was guided by the theoretical frameworks underpinning this study and informed by prior research in fragile and postconflict economies. The constructs were operationalized into multi-item scales via context-adapted survey instruments (see Table 2), most of which were derived or modified from validated sources in the development finance, social capital, and behavioral economics literature (El-Zoghbi & Tarazi, 2013; Narayan & Pritchett, 1999).

Construct Development and Operationalization.

Results

Measurement Model

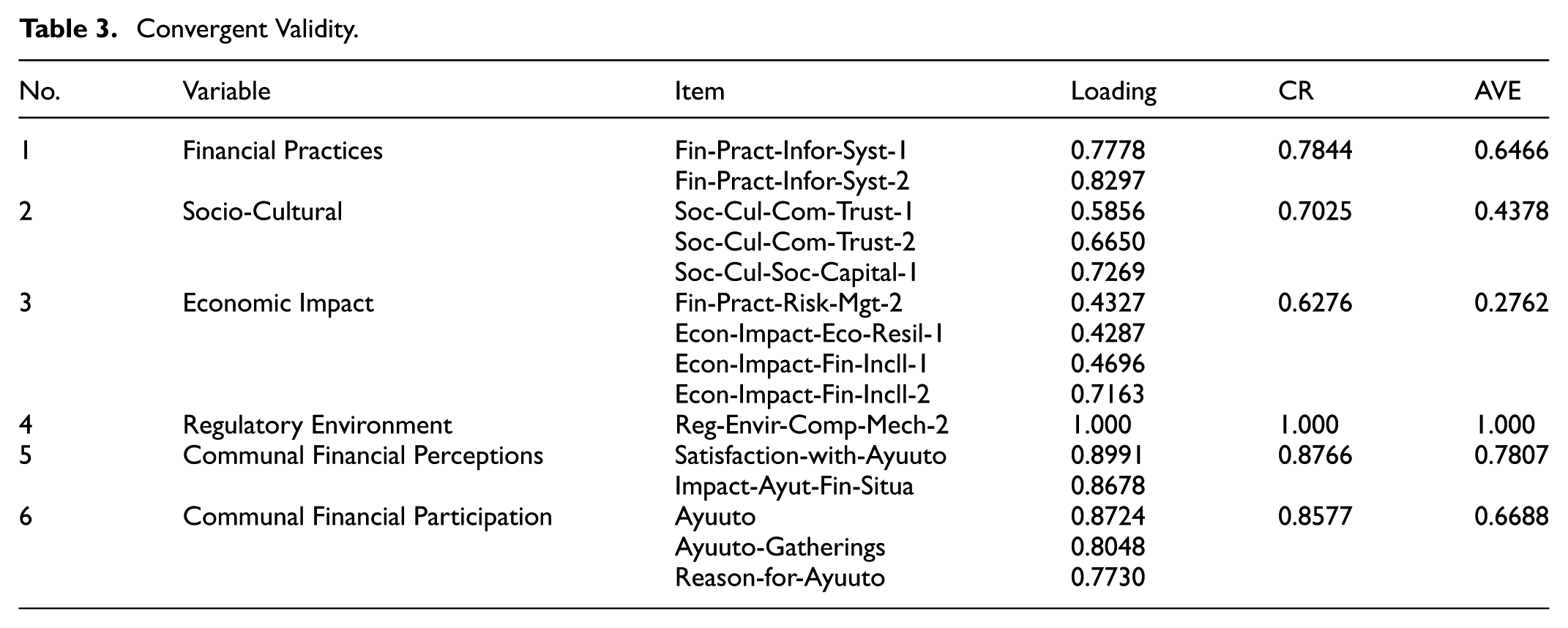

In structural equation modeling (SEM), the measurement model plays a pivotal role in defining and validating the relationships between observed variables and their underlying latent constructs. This model is crucial, as it establishes the groundwork for substantiating theoretical constructs posited to influence the observed data. Through careful analysis of convergent validity, reliability metrics, and factor loadings, the measurement model reveals the degree to which observed variables are accurate indicators of latent constructs. This study evaluated both convergent validity and discriminant validity, adhering to the guidelines proposed by Hair et al. (2017). Convergent validity is evaluated primarily through the average variance extracted (AVE), which quantifies the proportion of variance a construct captures relative to the variance attributable to measurement error. In this study, constructs such as sociocultural, financial practices, the regulatory environment, communal financial perceptions, and communal financial participation demonstrated AVE values surpassing the acceptable threshold of 0.50 (except for economic impact), indicating robust convergent validity.

The reliability of the constructs in the measurement model is assessed via several indicators, including Cronbach’s alpha, Dijkstra–Henseler’s rho (ρA), and Jöreskog’s rho (ρc). These measures ascertain the internal consistency of the constructs, ensuring that they are stable and uniformly measure the intended underlying latent variables. In this analysis, all the constructs presented reliability coefficients above the generally accepted benchmark of 0.70, with the exception of economic impact. Factor loadings further corroborate these findings, with most indicators meeting the desired threshold of 0.70, thereby affirming their suitability in representing the respective latent constructs. These metrics collectively attest to the internal consistency and measurement precision of the model (see Table 3).

Convergent Validity.

Discriminant validity, an essential aspect of construct validation, was examined via the heterotrait–monotrait (HTMT) ratio of correlations, as proposed by Henseler et al. (2015), an innovative approach derived from the multitrait–multimethod matrix. The assessment of discriminant validity is crucial for ensuring that distinct theoretical constructs are empirically uncorrelated, thus affirming the integrity and specificity of the measurement model. Discriminant validity is evaluated primarily through the Heterotrait–Monotrait Ratio of Correlations (HTMT), a rigorous criterion that quantifies the distinctiveness between pairs of constructs. A threshold value of less than 0.90 is generally adopted, following the recommendations of Gold et al. (2001), indicating that lower HTMT values represent a stronger demarcation between constructs, hence confirming good discriminant validity. This threshold ensures that the constructs reflect unique dimensions and are not merely different manifestations of the same attribute. According to the results detailed in Table 4, all the constructs adhered to this threshold except for Economic Impact. The ability of the measurement model to maintain distinct, nonoverlapping constructs underscores its structural integrity and reinforces its ability to accurately capture and differentiate between the theoretical phenomena posited in the study. These results clearly delineate the constructs as representing different underlying phenomena, with minimal conceptual or empirical overlap. This strong discriminant validity enhances the structural integrity of the measurement model and supports the construct validity of the scale, thereby bolstering the overall credibility and reliability of the model’s capacity to capture distinct and relevant theoretical dimensions within the SEM framework.

HTMT Ratios.

Structural Model

The reported factor loadings, CR, AVE, and HTMT values were assessed against the thresholds outlined in the Methodology section, with deviations explicitly noted and discussed. Where necessary, modifications were guided by both statistical indicators and theoretical considerations to preserve construct validity.

The robustness of the structural model in this study was methodically assessed through a bootstrapping procedure with a substantial sample size of 5,000 resamples, adhering to the recommendations of Hair et al. (2017). This approach was pivotal in providing a rigorous evaluation of the model’s parameters, including the coefficients of determination (R2), standardized beta coefficients (β), t values, and effect sizes (f2). Such a comprehensive analysis is critical in structural equation modeling (SEM) to ensure the reliability and validity of the theoretical framework tested. This investigation into the sociocultural dynamics of financial practices and their socioeconomic impacts employed a rigorous structural equation modeling (SEM) approach, as outlined by Hair et al. (2017), to examine the relationships posited in the theoretical framework of the study.

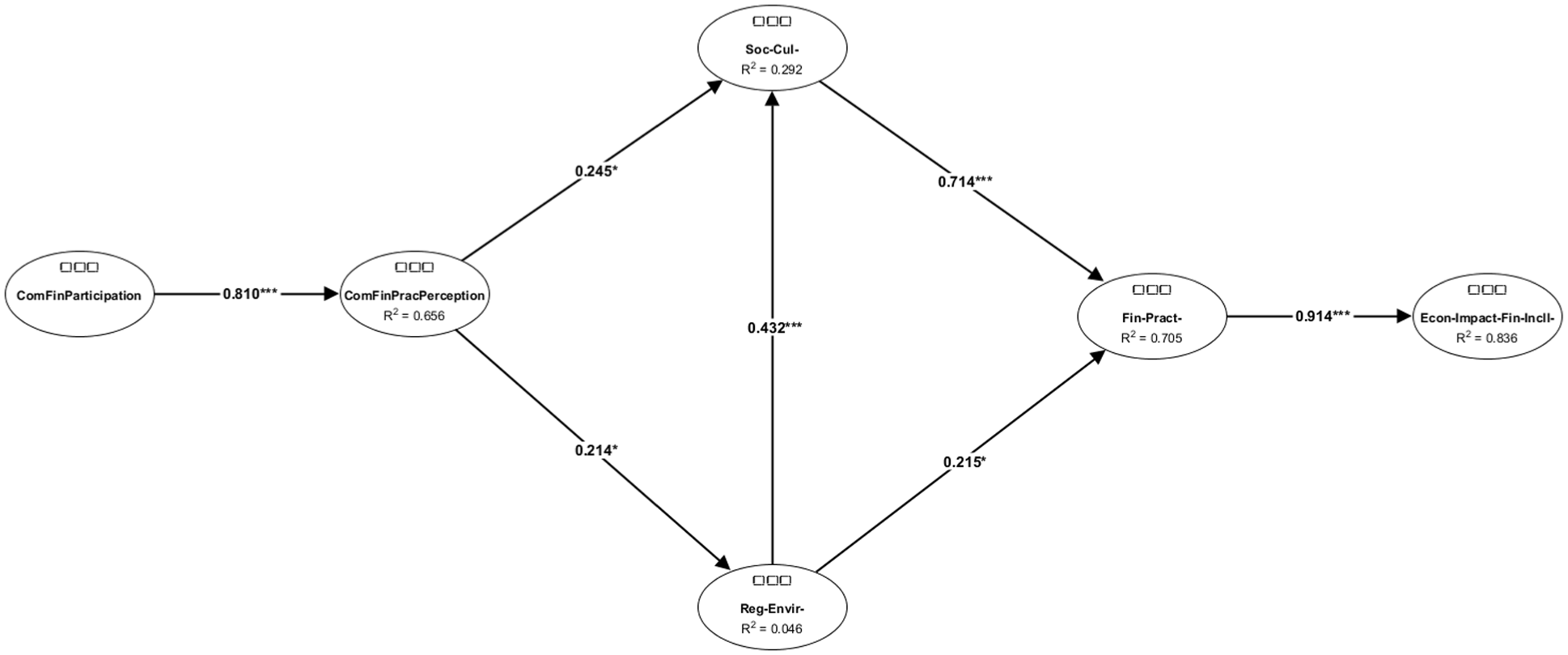

The findings of this study, as detailed in Table 5, provide robust empirical support for all seven hypotheses posited, highlighting significant relationships among sociocultural, financial, and regulatory constructs. Notably, the analysis reveals a statistically strong positive relationship between sociocultural factors and financial practices (β = .7242, p < .01), suggesting that cultural norms and values have a substantial influence on financial behaviors within communities. This relationship underscores the idea that sociocultural context plays a critical role in shaping financial practices, potentially guiding how financial decisions are made and how financial policies are received and implemented.

Structural Model.

Additionally, the analysis reveals a statistically significant positive correlation between financial practices and socioeconomic impact (β = .9144, p < .01), indicating that the financial behaviors endorsed and practiced within a society can have a profound impact on its economic health. This relationship is crucial for policymakers and economic planners, as it emphasizes the importance of fostering sound financial practices to ensure positive economic outcomes. Moreover, the relationships between the regulatory environment and both sociocultural (β = .4318, p < .01) and financial practices (β = .2147, p < .05) reveal the regulatory framework’s role in mediating the influence of sociocultural aspects on financial actions, suggesting that regulations can either reinforce or mediate the effect of cultural influences on financial behavior.

Further analyses demonstrated statistically significant positive relationships involving communal financial perceptions with sociocultural factors (β = .2450, p < .05) and the regulatory environment (β = .2137, p < .05), as well as between communal financial participation and communal financial perception (β = .8099, p < .01). These findings highlight the interconnectedness of communal perceptions and broader socioeconomic and regulatory contexts, illustrating how communal beliefs and participation in financial systems are intertwined with both cultural and regulatory frameworks (see Figure 2). Such insights are critical in understanding the dynamics of sociocultural dimensions of the financial system of the economy, suggesting that enhancing communal financial participation and aligning regulatory frameworks with the sociocultural context may mitigate financial challenges at both the micro and macro levels. Collectively, these results not only validate the study’s hypotheses but also provide a nuanced understanding of the multiple layers of influence that govern financial practices and their broader economic implications.

Structural model.

Discussion

This study explored the sociocultural dimensions of financial practices in Somalia. Drawing on social capital theory, institutional theory, embeddedness theory, and economic anthropology, this research sought to understand how sociocultural factors influence financial behaviors and outcomes, particularly in the absence of robust formal financial institutions. Through the application of structural equation modeling (SEM) and fussy data collection methods, this study explored the relationships among sociocultural factors, financial practices, regulatory environments, communal financial perceptions, communal financial participation, and socioeconomic impacts.

The main findings of the study revealed significant positive relationships between sociocultural factors and financial practices, indicating the profound influence of cultural norms and values on economic activities in Somali communities. Additionally, the study identified a strong correlation between financial practices and socioeconomic impacts, highlighting the critical role of sound financial behaviors in fostering economic stability and growth. Furthermore, the analysis revealed the mediating role of the regulatory environment in shaping the influence of sociocultural aspects on financial actions, emphasizing the importance of aligning regulatory frameworks with cultural contexts to mitigate financial challenges. Overall, the study provides valuable insights into the complex dynamics of financial practices in fragile states such as Somalia and underscores the need for tailored interventions that consider the unique sociocultural landscape of the region.

This study highlights the intricate interplay between sociocultural dynamics, financial practices, and regulatory environments in Somalia, revealing how communal trust, norms, and beliefs profoundly shape financial behavior. The strong positive relationship between sociocultural factors and financial practices underscores the central role of the cultural context in influencing savings, investment, and borrowing decisions. Moreover, the regulatory environment emerges as a critical mediating factor, shaping how these cultural influences translate into financial actions. The findings also demonstrate that sound financial practices contribute significantly to socioeconomic well-being, suggesting that efforts to promote financial inclusion and literacy must be both culturally informed and supported by effective governance. Together, these insights emphasize the need for holistic, context-specific approaches to financial development in fragile states such as Somalia.

The financial landscape of Somalia is deeply shaped by complex contextual factors, including prolonged conflict, political instability, and the absence of strong formal institutions. The clan-based social structure plays a dual role—providing essential social cohesion and informal governance in lieu of state institutions while also contributing to political fragmentation that hinders centralized reform. Economically, Somalia relies heavily on agriculture, livestock, diaspora remittances, and robust informal financial networks, which have demonstrated remarkable resilience amid infrastructural limitations and recurring crises. The informal economy operates as a lifeline for many, functioning outside the reach of formal banking yet facilitating widespread financial access. International developments, such as Somalia’s accession to the East African Community and the partial lifting of the UN arms embargo, signal a move toward greater integration and potential stability. However, ongoing insecurity and the legacy of state collapse continue to challenge reform efforts. These internal and external dynamics underscore the need for context-sensitive, culturally informed financial policies and regional cooperation to foster resilience, inclusive growth, and sustainable economic development in Somalia and beyond.

While this study focuses specifically on Somalia’s postconflict sociocultural and institutional landscape, several findings hold relevance for other fragile and postconflict states. The observed interplay between sociocultural norms, communal trust networks, and regulatory environments aligns with patterns documented in contexts such as South Sudan, Afghanistan, and parts of the Democratic Republic of the Congo, where formal financial infrastructures remain underdeveloped. Nevertheless, Somalia’s unique historical trajectory, clan-based governance structures, and the adaptive resilience of its informal financial systems introduce nuances that limit direct generalization. Therefore, our findings should be interpreted as context-informed insights that may inform comparative analyses or policy approaches in similar environments rather than as universally applicable conclusions. This cautious framing allows for meaningful contributions to the broader discourse on financial practices in fragile contexts while acknowledging the specificities that anchor our results in the Somali setting.

The findings of this study carry important implications for policymakers and practitioners working in financial regulation and economic development in Somalia and other fragile states. They highlight the critical need to align regulatory frameworks with local sociocultural realities, recognizing that informal financial practices—rooted in trust, communal norms, and traditional governance—play a central role in economic life. Designing policies that integrate these informal systems, such as incorporating traditional dispute resolution or legitimizing community-based savings groups, can enhance financial inclusion and regulatory effectiveness. Furthermore, promoting financial literacy through culturally tailored education initiatives, in partnership with community leaders, can help overcome barriers such as institutional distrust and limited banking access. Expanding inclusive financial infrastructure—particularly mobile banking and microfinance—can support broader participation in formal systems while preserving the strengths of informal networks. Ultimately, a holistic approach that bridges regulatory reform with cultural understanding is essential for fostering sustainable financial resilience and economic growth in fragile contexts such as Somalia.

The study findings align closely with the literature on financial practices in fragile states, particularly in terms of their emphasis on the importance of sociocultural factors and informal financial systems (Chai et al., 2019; Lahai & Koomson, 2020). Previous research has highlighted the resilience and adaptability of informal financial networks in contexts characterized by political instability and weak formal institutions (Khuong et al., 2021; Nguyen & Canh, 2021). Similarly, this study underscores the importance of informal financial practices such as hawalas and rotating savings and credit associations in Somalia’s economic landscape, demonstrating their vital role in providing financial services and liquidity where formal banking systems are lacking (Fowowe & Folarin, 2019; Nor, 2012). By integrating sociocultural insights into the analysis of financial systems, this study contributes to a more nuanced understanding of economic dynamics in fragile settings, challenging the prevailing narratives that marginalize informal mechanisms as barriers to formal economic development (Kass-Hanna et al., 2022).

Moreover, the study’s emphasis on the mediating role of the regulatory environment in shaping the influence of sociocultural factors on financial practices aligns with theoretical frameworks such as social capital theory and institutional theory (Coleman, 1988; North, 1990). These frameworks highlight the importance of formal and informal rules and regulations in governing economic behavior and development (Meagher, 2013; Putnam et al., 1994). By demonstrating the interplay between regulatory environments, sociocultural dynamics, and financial practices, this study provides empirical evidence that supports and extends existing theoretical perspectives (Omri, 2020; Vlasov et al., 2022). Additionally, the study’s use of structural equation modeling (SEM) represents a methodological advancement in the field, allowing for a more rigorous analysis of the relationships between variables and their underlying constructs (Hair et al., 2017). Overall, the alignment of the study findings with literature reaffirms the importance of considering sociocultural dimensions in financial development initiatives and underscores the need for context-specific approaches to economic policy and practice in fragile states.

The findings of this study offer significant theoretical insights into the dynamics of financial practices in fragile contexts by integrating multiple theoretical frameworks that emphasize the embeddedness of financial behavior in sociocultural and institutional environments. By extending social capital theory, the study illustrates that trust, reciprocity, and social cohesion not only function within local Somali communities but also extend across transnational networks—particularly in systems such as hawalas and diaspora-led remittances. These informal financial channels operate effectively because of shared cultural and religious norms that transcend borders, facilitating cross-border financial cooperation in the absence of formal regulatory mechanisms. This translocal manifestation of social capital challenges traditional community-bound interpretations and calls for an expanded theoretical view that includes globally networked, trust-based systems as legitimate actors in financial development discourse.

The study also broadens institutional theory by showing that informal institutions in fragile contexts such as Somalia are not temporary substitutes for formal systems but are deeply rooted, contextually responsive structures that perform critical governance functions. These institutions operate through culturally sanctioned norms, offering dispute resolution, capital circulation, and social protection in ways that formal institutions often cannot. In addition, the research affirms Embeddedness Theory, demonstrating that economic actions in Somalia—such as saving, lending, and borrowing—are not individualistic choices but rather socially embedded practices governed by kinship, moral obligation, and religious values. Finally, through the lens of economic anthropology, particularly Polanyi’s substantivist approach, the study reveals that financial behavior is part of a broader moral and cultural system, challenging market-centric perspectives. Informal mechanisms such as hawala are shown to be not only functional alternatives but also morally and culturally legitimate systems. Collectively, these insights underscore the need to build inclusive, context-sensitive financial theories that reflect the lived realities of fragile states and emphasize the importance of sophisticated analytical tools such as SEM to empirically model the complexities of financial behavior in such environments.

The novelty and unique contribution of this study lies in its integrated theoretical and methodological approach to examining the sociocultural dimensions of financial practices in fragile contexts, with Somalia as a focused case. By grounding the analysis in

This study significantly enriches the literature on financial practices in fragile states by demonstrating how sociocultural factors—such as communal trust, norms, and social networks—are central to the functioning of informal financial systems in Somalia. Moving beyond the conventional focus on formal institutions highlights the resilience and adaptability of mechanisms such as hawalas and Ayuuto in delivering essential financial services where formal banking is absent. This contribution not only challenges dominant development narratives but also provides a more nuanced, culturally grounded understanding of financial behavior in fragile contexts.

Conclusion

This study explored the sociocultural dimensions of financial practices in Somalia, a fragile state characterized by institutional weakness and reliance on informal economic systems. Using structural equation modeling (SEM), the research identified strong, statistically significant relationships between sociocultural factors and financial practices, confirming the central role of cultural norms, trust, and communal values in shaping financial behavior. The study also revealed the mediating effect of the regulatory environment, demonstrating that financial practices are shaped not only by culture but also by the interaction between formal and informal institutions. Additionally, communal financial perceptions and participation were shown to have broader socioeconomic implications.

The findings contribute to the theoretical advancement of financial studies in fragile contexts through an integrated multitheoretical lens. The study extends social capital theory by showing how trust and reciprocity function both locally and transnationally through informal financial networks. It expands institutional theory by demonstrating that informal financial systems in fragile states are not residual but represent rational adaptations to institutional voids. Drawing on embeddedness theory, this research illustrates how financial practices are shaped by deep-rooted social relationships. Through economic anthropology, the study confirms that financial behavior is embedded in cultural and moral systems, reinforcing the need for substantivist understandings of informal economies.

These findings have important implications for policymakers in Somalia and other fragile states. Regulatory frameworks should be context-specific and culturally sensitive, recognizing the legitimacy and utility of informal financial systems such as hawalas and ROSCAs. Policies that aim to promote financial inclusion must integrate traditional dispute resolution mechanisms and align with religious and communal norms. Rather than imposing rigid formal systems, policy interventions should seek to bridge formal and informal structures, ensuring that financial reforms are both effective and socially acceptable.

Practitioners working in financial development, humanitarian aid, and postconflict reconstruction can draw on these findings to design more inclusive and responsive financial systems. Programs aimed at improving financial literacy should be community-led and culturally grounded, utilizing trusted figures such as clan elders and religious leaders. Financial technologies such as mobile banking can be introduced in ways that complement rather than disrupt existing informal networks, enhancing accessibility while preserving trust-based mechanisms.

This study provides one of the few empirical examinations of the interplay between sociocultural factors, institutional environments, and financial behavior in a fragile state setting. It highlights the adaptive capacity and institutional logic of informal financial systems and challenges the prevailing development narratives that portray such systems as transitional or deficient. This research contributes to a more holistic and nuanced understanding of financial inclusion, which respects cultural diversity and institutional plurality in fragile economies.

In conclusion, this study underscores the centrality of sociocultural dynamics in shaping financial practices in fragile contexts such as Somalia. Informal financial systems are not merely responses to institutional failure but also culturally embedded, socially legitimate, and economically functional mechanisms. By embracing a multitheoretical and empirically grounded approach, this research advances both academic understanding and practical policymaking in the field of financial development. The findings call for a paradigm shift: from viewing informal finance as a problem to recognizing it as a potential foundation for inclusive and resilient economic systems in fragile states.

Limitations and Future Research

While this study offers valuable and contextually rich insights, it is not without limitations. The use of purposive sampling—although appropriate for exploratory research in fragile contexts such as Somalia—limits the generalizability of the findings beyond similar sociopolitical settings. Furthermore, while SEM provides a robust framework for modeling complex relationships between constructs, it cannot fully capture the qualitative nuances underlying financial behaviors, cultural dynamics, and informal institutional logics. The cross-sectional nature of the data also restricts the ability to draw causal inferences.

These methodological constraints have been acknowledged and addressed by positioning the study’s contribution as Somalia specific, with implications that are particularly relevant for policymakers and stakeholders operating in fragile-state environments. Future research could strengthen and broaden this contribution by adopting a mixed-methods approach, integrating qualitative interviews and ethnographic perspectives to deepen the understanding of cultural meanings and local financial practices. Longitudinal studies could track changes in financial behaviors over time, particularly in response to regulatory reforms or shifts in sociopolitical dynamics. Comparative research across other fragile states in East Africa could also enhance the theoretical generalizability and practical relevance of the findings, providing a stronger evidence base for policy design in such contexts.

Footnotes

Funding

There is no funding information to disclose, and no funding statement is applicable for this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data supporting the findings of this study will be made available by the authors upon reasonable request.