Abstract

Frequent health events and rising household economic vulnerability highlight the importance of understanding how health risks impact economic stability. Using data from the 2016 to 2022 China Family Panel Studies (CFPS), this study investigates how health risks affect household economic vulnerability across two dimensions: finance and poverty risk. The analysis reveals that health risks significantly heighten economic vulnerability, primarily by weakening households’ financial positions rather than directly causing poverty. During the initial stages of COVID-19, health risks sharply increased households’ vulnerability to poverty; however, this effect gradually diminished over time, whereas the impact on financial vulnerability persisted consistently. Declining health status contributes to household vulnerability through three main pathways: higher medical expenses, lower income, and increased difficulty accessing credit. Heterogeneity analysis identifies that those with abundant material resources, robust social networks, comprehensive health insurance coverage, and well-developed digital finance systems primarily face heightened financial vulnerability. In contrast, households with limited material resources, social support, medical insurance coverage, and access to digital finance services are more susceptible to poverty risks. Additionally, the vulnerability impacts are stronger among households with older adults compared to others.

Introduction

Health risks have increasingly become a significant issue for households and broader socioeconomic development. Rising rates of chronic illness and hospitalization are closely associated with demographic aging (Khow & Visvanathan, 2017), environmental deterioration (Chen & Liao, 2006), and health-related behaviors (Siegrist & Rödel, 2006). In China, chronic diseases accounted for 88.5% of all deaths in 2019, with cardiovascular diseases, cancer, and chronic respiratory conditions responsible for more than 80% of those fatalities (National Disease Control and Prevention Administration, 2020). These statistics underscore the growing importance of health issues for household economic well-being.

Globally, health risks present substantial economic burdens to households across all income levels. In high-income countries, even well-developed healthcare systems cannot entirely prevent financial hardship from serious illnesses. For example, high medical costs in the United States remain a leading cause of household financial distress (Spithoven, 2009). In middle-income countries such as Brazil, many families use savings or loans to finance healthcare, which can exacerbate their financial vulnerability (Luiza et al., 2016). In resource-constrained regions such as sub-Saharan Africa, limited healthcare access restricts households’ coping options, increasing medical costs, lowering productivity, and heightening poverty risks (Atake, 2018).

Health risks thus transcend individual health outcomes, becoming systemic threats to household economic stability through both immediate and lasting impacts. Sudden medical expenses often create immediate financial pressures, reducing household liquidity (Goetzel et al., 1998; Lynch et al., 2005). Additionally, illness-induced income losses—due to reduced working hours or health conditions leading to work limitations for primary earners—may permanently decrease household income (Burton et al., 2005; Nguyet & Mangyo, 2010; Pelletier et al., 2004). Furthermore, health crises can impair household creditworthiness, limiting access to credit and making it difficult for families to recover economically or maintain stable consumption (Planchet et al., 2022). Collectively, these effects amplify household vulnerability.

Despite a growing focus on household economic vulnerability, existing studies mainly examine macroeconomic factors like inflation (Fujii, 2013), household debt (Kaplan et al., 2018; Martín-Legendre & Sánchez-Santos, 2024), and asset liquidity (Brunetti et al., 2016). Other research emphasizes protective factors such as financial development (Choudhury, 2014; Koomson et al., 2020), social security (Akotey & Adjasi, 2014), government assistance (Imai et al., 2010), trade liberalization (Vo & Nguyen, 2021), financial literacy (Brunetti et al., 2016), and social capital (Dershem & Gzirishvili, 1998). Yet, systematic exploration of how health risks specifically influence household economic vulnerability remains limited. While some studies address the financial consequences of health events (Ma et al., 2022), most research focuses either on short-term financial distress or long-term poverty without examining how health risks affect both outcomes simultaneously through interconnected pathways (Liao et al., 2022; Novignon et al., 2012; Ouadika, 2020). In particular, distinctions between short-term financial vulnerability and sustained poverty risks remain inadequately understood, as do changes in these effects over time. Major public health events, such as the COVID-19 pandemic, likely alter households’ economic responses to health shocks, yet research has not fully addressed this temporal variability. Consequently, how health risks broadly influence household economic resilience under crisis conditions remains poorly understood.

To address these gaps, this study employs data from the 2016 to 2022 China Family Panel Studies (CFPS) to examine how health risks affect household economic vulnerability across two related dimensions: financial vulnerability in the short term and poverty vulnerability over the long term. The analysis identifies key transmission mechanisms and examines differences across household groups. Specifically, this research makes four main contributions. First, it develops a comprehensive analytical framework that separates short-term financial pressures from long-term poverty risks, enriching theoretical understanding of household vulnerability. Second, by treating the COVID-19 pandemic as an external shock, the study assesses how health risks’ impacts evolved before, during, and after this crisis, highlighting how public health emergencies intensify economic vulnerability. Third, the article identifies three core pathways through which health risks destabilize household finances: rising medical costs, declining income, and restricted credit access. Fourth, the research conducts an extensive heterogeneity analysis based on key household characteristics, such as economic resources, social capital, health insurance coverage, digital financial participation, and demographic factors. The findings demonstrate that wealthier households are more susceptible to immediate financial shocks, whereas households with more limited economic resources face greater long-term poverty risks. These insights can inform targeted health insurance and economic strategies aimed at mitigating household vulnerability.

Theoretical Analysis

Health risks significantly increase household economic vulnerability through three primary channels: higher medical costs, reduced disposable income, and tighter credit constraints. This section discusses each mechanism in detail.

Medical Burden

Health issues often result in substantial financial burdens due to unexpected medical expenses. Households facing health challenges are more likely to encounter sudden and costly medical treatments (He & Zhou, 2022). Even with insurance coverage, out-of-pocket medical costs typically remain high, leading to significant financial strain for affected families (Li et al., 2014). Households with limited liquid assets may face difficulties covering these sudden expenditures, raising their risk of financial hardship (Morudu & Kollamparambil, 2020).

Beyond immediate health crises, households may also proactively spend on preventive care to reduce future health risks (Hodor, 2021; Wang et al., 2023). Such anticipatory spending further consumes available resources and reduces liquidity, limiting households’ ability to manage other financial challenges (Liu et al., 2022). To offset these rising healthcare costs, households may reduce expenditures on areas such as education, transportation, or leisure, which may increase the risk of consumption-related deprivation (Kumara & Samaratunge, 2017; Wang et al., 2023). These shifts not only compromise short-term quality of life but also hinder long-term asset accumulation and economic resilience. Thus, health-related costs contribute directly to increased short-term and long-term household vulnerability.

Disposable Income

Health risks also negatively affect household income (Zhang et al., 2014), primarily by reducing labor supply. Since wages and business earnings largely depend on individuals’ productivity and working hours, health shocks can significantly disrupt income generation. Declining health status can reduce individuals’ capacity to work, causing decreased work hours or even complete withdrawal from the labor market (Pintor et al., 2024). Moreover, employers often favor employees who are able to maintain consistent attendance and productivity (Drydakis, 2010; Sabatier & Legendre, 2017). Consequently, individuals experiencing health limitations may face disadvantages, potentially losing jobs or facing reduced wages (Nguyet & Mangyo, 2010).

Additionally, health shocks frequently result in caregiving responsibilities that further reduce overall household labor supply. Family members, especially spouses or parents, often scale back their work commitments to care for a family member experiencing health challenges (Li, 2023). This effect is particularly pronounced when children experience serious illness, causing significant disruptions in parents’ employment and earnings (Eriksen et al., 2021; Skoy, 2024). With limited immediate options to offset these income losses, households face greater financial instability, increasing their long-term economic vulnerability.

Credit Constraints

Health risks can further exacerbate household vulnerability by limiting access to credit. Households experiencing health-related challenges may be perceived as higher risk by lenders, as health problems may undermine their ability to repay loans (Planchet et al., 2022). This perception restricts borrowing options across formal institutions, such as banks, and informal sources, including friends and family (Madeira, 2019). Financial institutions frequently factor health status into lending decisions, potentially offering less favorable loan terms or denying access altogether (Mols et al., 2012). Similarly, informal lenders may hesitate to provide support, concerned about repayment risks associated with health limitations.

Consequently, health shocks significantly increase the likelihood of loan default—not because of unwillingness to repay, but due to reduced repayment capacity (Madeira, 2023). Credit constraints stemming from health conditions therefore play a critical role in deepening household economic vulnerability (Kumar et al., 2013; Peng et al., 2021). Without adequate credit access, households become less able to manage liquidity during emergencies, further intensifying their susceptibility to income shocks and financial exclusion. Thus, health risks impose immediate financial burdens while simultaneously reducing households’ economic flexibility, compounding overall vulnerability. Based on these theoretical considerations, this study proposes two hypotheses:

Model Specification and Data

Model

To examine how health risks influence household economic vulnerability, this study adopts a two-dimensional framework that distinguishes short-term financial vulnerability from long-term poverty vulnerability. Short-term financial vulnerability refers to households’ difficulty in managing immediate liquidity shocks, while poverty vulnerability represents the risk of experiencing persistent poverty. Given that the dependent variable—household vulnerability—is binary, we use Probit models for baseline estimation, consistent with existing literature (Koomson et al., 2020; Wang & Fu, 2021; Zhang et al., 2024). The models are specified as follows:

Where, Vul_Poverty indicates household’s poverty vulnerability, reflecting long-term poverty risk, while Vul_Fin represents short-term financial vulnerability. The variable Health_risk reflects household-level exposure to health risks. X is a set of control variables covering household, household-head, and regional characteristics. To account for unobserved heterogeneity across provinces, we include provincial dummy variables in the model. ε is the error term.

Variable Description

Dependent Variables

To comprehensively capture household economic vulnerability, this study uses two dependent variables: financial vulnerability and poverty vulnerability.

Financial Vulnerability

Following Brunetti et al. (2016), financial vulnerability is measured based on two criteria: (i) whether household income covers expected daily consumption and (ii) whether liquid assets can meet unexpected emergency expenses. Specifically, expected consumption includes regular expenses excluding durable goods, while unexpected expenses are proxied by out-of-pocket medical expenditures. Households that can cover daily costs but have limited liquidity to manage medical shocks are categorized as financially vulnerable. Formally:

Where, DI denotes household disposable income, EE expected expenditure, LA liquid assets, and UE unexpected expenditure (medical costs).

Poverty Vulnerability

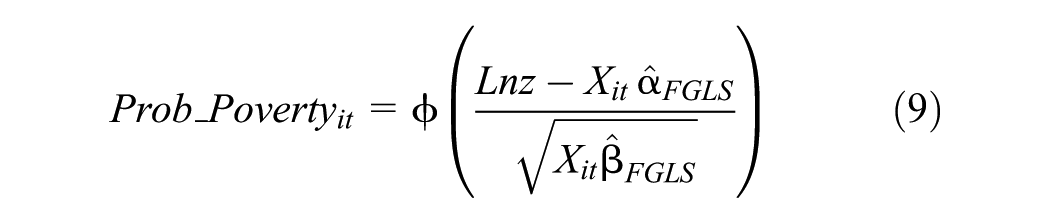

Long-term poverty vulnerability is assessed using the Vulnerability as Expected Poverty (VEP) method (Chaudhuri et al., 2002). This approach estimates the probability that future household consumption remains below a predefined poverty line. Assuming household consumption follows a log-normal distribution, the probability of future poverty is computed via a three-stage Feasible Generalized Least Squares (FGLS) method:

Where, Prob_Poverty denotes the probability that household i at time t will fall below the poverty line z in the future; c + 1 is predicted per capita household consumption; and z is the poverty line.

The calculation proceeds in several steps. First, estimate the expected log consumption and its variance. Specifically, X includes household and head-of-household characteristics, ε is the residual term, and σ denotes the variance of consumption:

Second, estimate the expected log of future per capita consumption and its variance using three-stage FGLS:

Third, assuming a normal distribution, compute the probability of falling into poverty:

Fourth, compare this probability against the preset threshold to identify whether a household is considered vulnerable to poverty:

In these equations, Vul_Poverty denotes household poverty vulnerability and Line is the vulnerability threshold. We follow World Bank standards for poverty, applying daily per capita consumption of USD 3.1 in our baseline analysis and USD 1.9 in robustness checks, with both figures adjusted for purchasing power parity and the USD–RMB exchange rate.

Traditional studies often use a 50% threshold (Chiwaula et al., 2011) to define poverty vulnerability, but this cutoff may overlook at-risk households below that level. In line with more research, we set a 29% threshold to capture households at risk of poverty (Günther & Harttgen, 2009). Thus, if a household’s future poverty probability exceeds 29%, Vul_Poverty = 1; otherwise, Vul_Poverty = 0.

Core Explanatory Variable

The core explanatory variable in this study is household health risk, measured through subjective health assessments collected by the China Family Panel Studies (CFPS). Respondents were asked, “How would you rate your health status?” with five response options: “very healthy,”“healthy,”“fairly healthy,”“average,” and “unhealthy.” Subjective health perception is widely recognized as a reliable proxy for both actual health conditions and potential medical needs and has been extensively used in prior research as an indicator of health risk (Zou et al., 2020). Following established approaches (Godlonton & Keswell, 2005; Porter, 2012), this study uses household members who self-assess their health status as “unhealthy” to quantify household-level health risk. This measure captures the potential health burden and future medical expenditure risk faced by the household.

Mechanism Variables

To empirically examine the channels through which health risks affect household economic vulnerability, three mediating variables are introduced: medical burden, income level, and credit constraints. Medical burden is measured in both absolute and relative terms. The absolute burden is represented by the natural logarithm of annual household medical expenditures. The relative burden is captured using a binary indicator for high medical burden spending, defined as whether a household’s medical expenses exceed 20% of total household expenditure (Chamon & Prasad, 2010). Income level is assessed through three indicators: the natural logarithms of wage income, operation income, and total household income. These capture the household’s ability to generate income through labor and entrepreneurial activities. Credit constraints are examined in both aggregate and segmented forms. A household is classified as credit-constrained if it reports having been denied a loan. Further distinction is made between formal credit constraints (rejections from banks or financial institutions) and informal credit constraints (unsuccessful borrowing attempts from family, friends, or informal lenders). These indicators reflect barriers to financial access from both institutional and social networks.

Control Variables

To account for confounding factors and reduce omitted variable bias, the analysis includes a comprehensive set of control variables based on previous literature (Koomson et al., 2020; Wang & Fu, 2021; Zhang et al., 2024). These are grouped into three categories: household characteristics, household head characteristics, and regional-level conditions. At the household level, controls include total income and assets (economic capacity), household registration type (urban-rural status), household size, child and older-adult dependency ratios (demographic support ratios), receipt of government subsidies (policy support), homeownership (wealth buffer), participation in agricultural or business activities (economic engagement), and enrollment in pension and health insurance programs (social security coverage). At the household head level, the models control for age and its square (life-cycle effects), gender identity and marital status (household structure), and years of education (human capital). At the regional level, provincial per capita GDP is included to control for local economic development, and the Digital Inclusive Finance Index is used to capture financial infrastructure and accessibility, which may influence household financial resilience and decision-making.

Data

This study uses micro-data from the China Family Panel Studies (CFPS), conducted by the Institute of Social Science Survey at Peking University. Four waves of data—2016, 2018, 2020, and 2022—are employed to ensure temporal consistency and allow panel analysis. The CFPS is widely recognized for its national representativeness and high data quality and has been extensively used in empirical research on household behavior. It provides rich information on income, consumption, assets, liabilities, health status, demographic characteristics, and education, making it well-suited for investigating the relationship between health risks and household economic vulnerability. To ensure data quality and robust estimation, the following procedures were implemented during sample construction. First, observations with missing values in key variables were not included in the analytic sample. Second, households with extreme outliers in income or consumption were excluded. Third, observations where the household head was under 16 years of age or where demographic variables indicated inconsistencies were omitted. After filtering, the final sample consists of 37,992 valid household-level observations. To reduce the influence of extreme values, all monetary variables were transformed using natural logarithms. Additionally, all monetary figures were adjusted for inflation using the Consumer Price Index (CPI), ensuring comparability across survey years and eliminating potential bias due to price level changes (Table 1).

Variable Descriptions and Descriptive Statistics.

Empirical Results

Baseline Regression Results

Table 2 presents the baseline regression results for the impact of health risks on household economic vulnerability. Column (1) shows the relationship between health risks and financial vulnerability without any control variables. The coefficient is positive and statistically significant at the 1% level, with a marginal effect of .0372. This means that each additional household member reporting poorer health status raises the probability of financial vulnerability by 3.72 percentage points. Column (2) adds a comprehensive set of control variables, including household characteristics, attributes of the household head, regional factors, and provincial dummy. After introducing these controls, the marginal effect decreases to .023 but remains highly significant. Thus, even after accounting for various observable factors, health risks continue to significantly increase short-term financial vulnerability. Specifically, each additional household member reporting poor health status increases financial vulnerability by 2.3 percentage points. Columns (3) and (4) report similar analyses for poverty vulnerability. Without controls, the marginal effect is strong and statistically significant, indicating that each additional household member reporting poor health status increases the probability of being vulnerable to poverty by 7.68 percentage points. However, once the full set of control variables is included, the marginal effect drops significantly to .0034, although it remains statistically significant. In other words, each additional household member reporting poor health status raises the probability of being vulnerable to poverty by only .34 percentage points, a substantially smaller economic impact. Overall, these findings clearly demonstrate that health risks meaningfully influence household economic vulnerability, predominantly through short-term financial constraints rather than long-term poverty risk.

Results About the Impact of Health Risk on Household Economic Vulnerability.

Note. Standard errors clustered at the household level are in parentheses. All reported coefficients are marginal effects.

denote statistical significance at the 1% levels.

To examine whether the COVID-19 pandemic altered the relationship between health risks and household economic vulnerability, the sample was divided into three periods: pre-pandemic (2016–2018), early pandemic (2020), and post-pandemic (2022). Separate regressions were performed for each period, with results presented in Table 3.

Results About the Impact of Health Risk on Household Economic Vulnerability by Pandemic Period.

Note. *** denote statistical significance at the 1% levels.

Columns (1) to (3) show the effects of health risks on financial vulnerability. Across all three periods, health risks consistently demonstrate a positive and statistically significant influence, with marginal effects of 2.22 percentage points pre-pandemic, 2.10 during the early pandemic, and 2.25 post-pandemic. The stability of these effects indicates that health risks persistently increase short-term financial vulnerability, with little change resulting from the pandemic’s onset. However, Columns (4) to (6) reveal considerable temporal variation in the effect of health risks on poverty vulnerability. Before the pandemic, each additional household member reporting poor health status increased poverty vulnerability by .30 percentage points, significant at the 1% level. During the early stages of the pandemic, this effect rose notably to .47 percentage points, reflecting heightened vulnerability due to combined health and economic shocks. By 2022, the effect diminished to .22 percentage points and was no longer statistically significant. This pattern suggests that while health risks intensified long-term poverty risks at the pandemic’s outset, enhanced public health measures, medical assistance programs, and expanded health insurance coverage subsequently mitigated these risks. Overall, the findings indicate that although health risks consistently impact short-term financial vulnerability, their influence on long-term poverty vulnerability was particularly sensitive to the systemic disruptions caused by COVID-19.

Testing for Endogeneity

When estimating how health risks affect household economic vulnerability, potential endogeneity issues must be carefully considered. First, the main explanatory variable—self-rated health status—is subjective and susceptible to measurement errors stemming from individual perceptions, cultural influences, and personal expectations. Second, unobserved factors such as psychological stress, diet, or lifestyle could simultaneously influence health and economic vulnerability, introducing omitted variable bias. Finally, reverse causality may exist. Households experiencing economic vulnerability may report worse health outcomes due to stress, inadequate nutrition, or limited access to healthcare. To address these challenges, an instrumental variable (IV) strategy is employed.

The chosen instrument is the number of individuals self-reporting poor health status in other households within the same community. This instrument meets the two critical conditions for valid IV estimation—relevance and exclusion. Regarding relevance, individuals typically assess their health status relative to their social surroundings (Kawachi & Berkman, 2001; Subramanian et al., 2002). A higher prevalence of self-reported poor health in the community likely influences an individual’s own perception of health due to shared experiences, social norms, and heightened health awareness. Additionally, neighbors often share similar environmental conditions, healthcare availability, and exposure to health risks, reinforcing the connection between community-level and individual health outcomes (Case & Deaton, 2017; Cutler et al., 2006). Concerning the exclusion condition, although neighbors’ health influences self-assessed health status, it should not directly affect a household’s financial or poverty vulnerability except through its impact on household health perceptions.

Table 4 reports the results from IV-Probit estimations. Columns (1) and (2) show the results for financial vulnerability. The first-stage regression indicates that the instrument strongly predicts household health risk, with a t-statistic of 17.51 and an F-statistic of 292.22, well above the common threshold of 10, confirming its strength. In the second stage, the marginal effect of health risks on financial vulnerability is significant at .1427, meaning each additional household member reporting poor health status increases short-term financial vulnerability by 14.27 percentage points. Columns (3) and (4) present IV estimates for poverty vulnerability. The marginal effect here is .0232, significant at the 1% level, suggesting that each additional household member self-reporting poor health status raises poverty vulnerability by 2.32 percentage points. The Wald test for exogeneity rejects the null hypothesis, confirming that health risk is endogenous. This result validates the appropriateness of the IV approach and highlights the necessity of correcting for endogeneity bias. Overall, addressing endogeneity further confirms that health risks significantly increase both short-term financial vulnerability and long-term poverty vulnerability among households.

IV-Probit Estimates of the Impact of Health Risk on Household Economic Vulnerability.

Note. ** and *** denote statistical significance at the 5% and 1% levels.

Robust Test

Alternative Measures of Dependent Variables

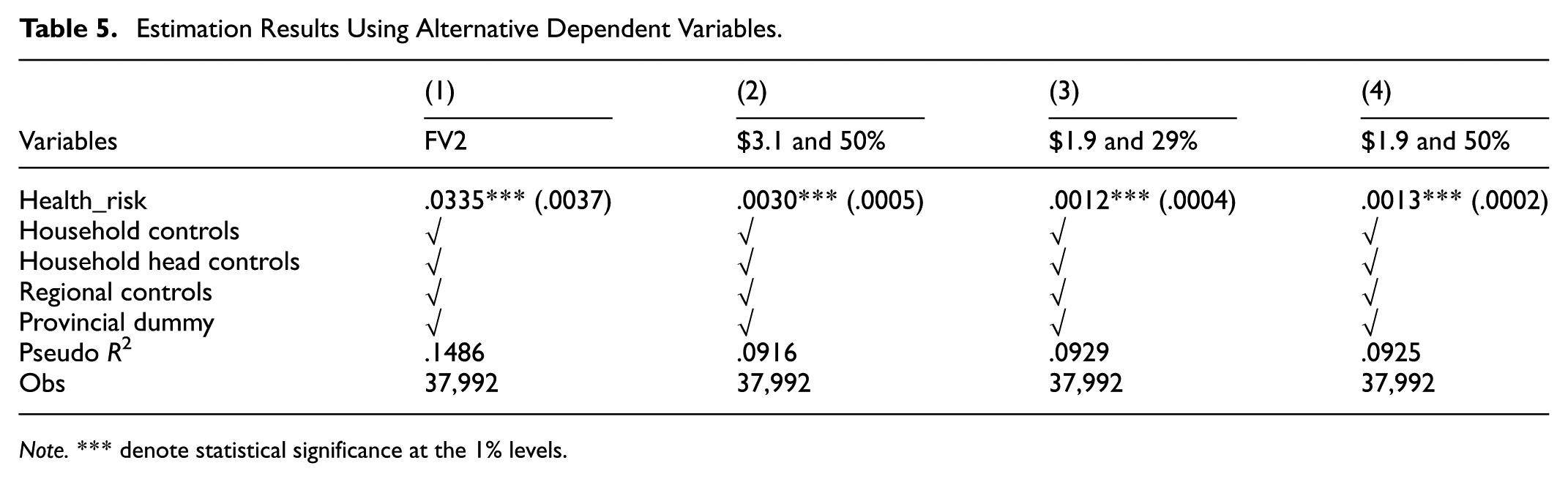

To confirm the reliability of our main findings, we conducted robustness checks by adopting alternative definitions of financial and poverty vulnerability. For financial vulnerability, we utilized the “financial margin” approach developed by Ampudia et al. (2016). Under this method, households are categorized as financially vulnerable if their income is insufficient to cover regular expenses and essential debt repayments, and their liquid assets provide inadequate resources to cover this shortfall for at least three consecutive months. This measure provides a realistic assessment of short-term financial distress by focusing on households facing financial strain or operating with limited financial buffers.

For poverty vulnerability, we re-estimated our model using alternative poverty thresholds and vulnerability probabilities. Besides our baseline measure (daily per capita consumption below $3.10 and a 29% vulnerability threshold), we tested stricter poverty criteria, including a higher vulnerability probability (50%) and the lower poverty line ($1.90 per capita per day). These alternative definitions allow us to verify whether health risks impact households across different severity levels of poverty and vulnerability. Persistent effects under these conditions would imply that health risks affect both households at the margin of vulnerability and those experiencing severe poverty conditions.

Table 5 presents these robustness check results. Column (1) shows that under the alternative financial margin measure, health risks remain significantly associated with financial vulnerability, with a marginal effect of .0335. Columns (2) through (4) present poverty vulnerability outcomes using varying thresholds and poverty lines. Each model maintains positive and statistically significant results at the 1% level, although the magnitudes vary slightly. This consistency indicates the baseline findings are robust across alternative specifications. Thus, health risks have a stable and significant impact on household economic vulnerability, regardless of the precise measures employed.

Estimation Results Using Alternative Dependent Variables.

Note. *** denote statistical significance at the 1% levels.

Alternative Measures of Independent Variable

To further validate the robustness of our findings, we replaced the primary measure of health risk with two alternative variables—one objective and one subjective. First, Health_risk2 measures household health objectively, defined as the number of household members who experienced hospitalization for health-related conditions. This measure captures severe and recent health shocks more directly, reducing potential bias from subjective self-assessments. Second, Health_risk3 aggregates subjective health perceptions by calculating the average self-rated health score of household members (rated from 1, “very healthy,” to 5, “unhealthy”). This measure reflects overall household health status and perceptions.

Table 6 presents the results of these alternative health risk measures. Columns (1) and (3) report results using the hospitalization-based measure (Health_risk2). The marginal effects are .0123 for financial vulnerability and .0005 for poverty vulnerability. Columns (2) and (4), using average self-rated health (Health_risk3), produce marginal effects of .0467 and .0019, respectively, both significant at 1%. These results consistently demonstrate a robust and significant relationship between health risks and household economic vulnerability, irrespective of whether objective hospitalization data or subjective health assessments are employed. Thus, the core conclusions of the analysis remain credible and stable across alternative definitions of health risk.

Estimation Results Using Alternative Independent Variables.

Note. ** and *** denote statistical significance at the 5% and 1% levels.

Mechanisms

Health risks affect household economic vulnerability through multiple channels. First, from an expenditure perspective, health shocks impose substantial medical costs on households. Second, from an income perspective, declining health status may limit households’ earning capacity by reducing labor participation and productivity. Third, health challenges may affect households’ perceived creditworthiness, restricting access to borrowing and making it more difficult to manage financial stress. To clarify how these mechanisms operate, we empirically investigate three dimensions: medical expenditures, income shock, and credit constraints, using the following models:

Where, Med, Inc, and Credit denote medical burden, income level, and credit constraints, respectively. All other variables match those in Model (1).

Medical Burden

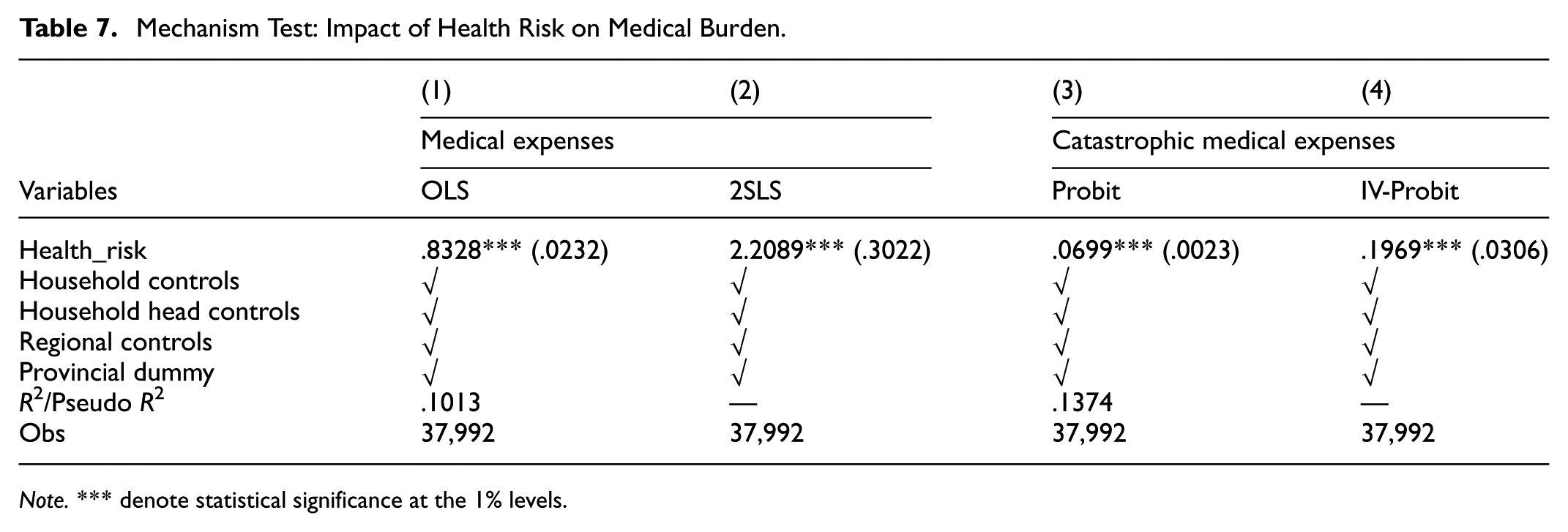

This section examines the medical burden as a key mechanism through which health risks affect household economic vulnerability, focusing specifically on healthcare expenditure as a channel. To clearly illustrate this mechanism, two measures of medical burden are employed. The first is the natural logarithm of total medical expenditure, capturing the household’s overall healthcare costs. The second is a binary indicator representing catastrophic health expenditure, defined as healthcare spending exceeding 20% of a household’s total expenditure, highlighting severe and unexpected financial pressures.

Table 7 summarizes the regression results that illustrate how health risks influence these medical burden indicators. Columns (1) and (2) present the relationship between health risks and total medical spending, using OLS and 2SLS methods, respectively. Under the OLS approach, each additional household member reporting poor health status is associated with an 83.28% increase in medical expenses, an effect statistically significant at the 1% level. After correcting for potential endogeneity using the 2SLS method, the estimated impact becomes even larger, rising to approximately 220.89%, also significant at the 1% level. Columns (3) and (4) investigate how health risks affect the likelihood of experiencing catastrophic medical expenditures, employing Probit and IV-Probit estimations. The Probit analysis reveals that each additional household member reporting poor health status raises the probability of catastrophic healthcare spending by about 6.99%. When accounting for endogeneity through the IV-Probit model, this probability increases substantially to approximately 19.69%, again significant at the 1% level.

Mechanism Test: Impact of Health Risk on Medical Burden.

Note. *** denote statistical significance at the 1% levels.

Taken together, these findings clearly demonstrate that health risks significantly amplify a household’s medical burden, both through elevated healthcare costs and increased vulnerability to severe financial shocks. Higher medical expenses reduce household liquidity, constraining households’ ability to manage additional financial pressures and ultimately heightening economic vulnerability. These results confirm that medical expenditure serves as a critical pathway through which health risks threaten household financial stability.

Income Shock

In addition to increased expenditures, this section explores how health risks contribute to household economic vulnerability by causing income losses. It specifically assesses whether declining health status reduces households’ ability to generate income, analyzing three main components: total income, wage income, and operation income. The analysis uses the natural logarithm of each income measure to clearly reflect percentage changes and differences across income sources.

Table 8 presents the regression results of this analysis. Columns (1) and (2) show the relationship between health risks and total household income, using OLS and 2SLS estimations, respectively. According to the OLS results, each additional household member reporting poor health status is associated with an 11.02% decrease in total household income, statistically significant at the 1% level. After addressing potential bias using the 2SLS method, this estimated effect increases substantially to 85.8%, indicating a significant impact of self-reported poor health status on household income. Columns (3) and (4) examine the impact of health risks specifically on wage income. The OLS results suggest that wage income declines by 35.27% for each additional household member reporting poor health status. When potential endogeneity is accounted for using 2SLS, this reduction grows significantly to 239.59%, both findings being highly significant at the 1% level. These outcomes highlight that declining health status substantially reduces labor participation and earning capacity, particularly for households dependent on wage employment. Columns (5) and (6) focus on the effect of health risks on operation income, which includes earnings from self-employment, farming, or entrepreneurial activities. The OLS estimation indicates a 20.85% decrease in operation income per additional household member reporting poor health status, whereas the 2SLS estimation reveals an even larger drop of 135.46%, both statistically significant at the 1% level. These results indicate that health challenges substantially affect households’ involvement in productive self-employment and business activities.

Mechanism Test: Impact of Health Risk on Income.

Note. *** denote statistical significance at the 1% levels.

Collectively, these findings clearly demonstrate that health risks significantly diminish household income across various sources. The pronounced reductions in wage and operation incomes confirm that income loss is a critical pathway through which health issues amplify household economic vulnerability. Weakened earning capacity not only undermines immediate financial stability but also reduces households’ ability to manage future economic shocks, increasing their likelihood of experiencing financial distress or poverty.

Credit Constraints

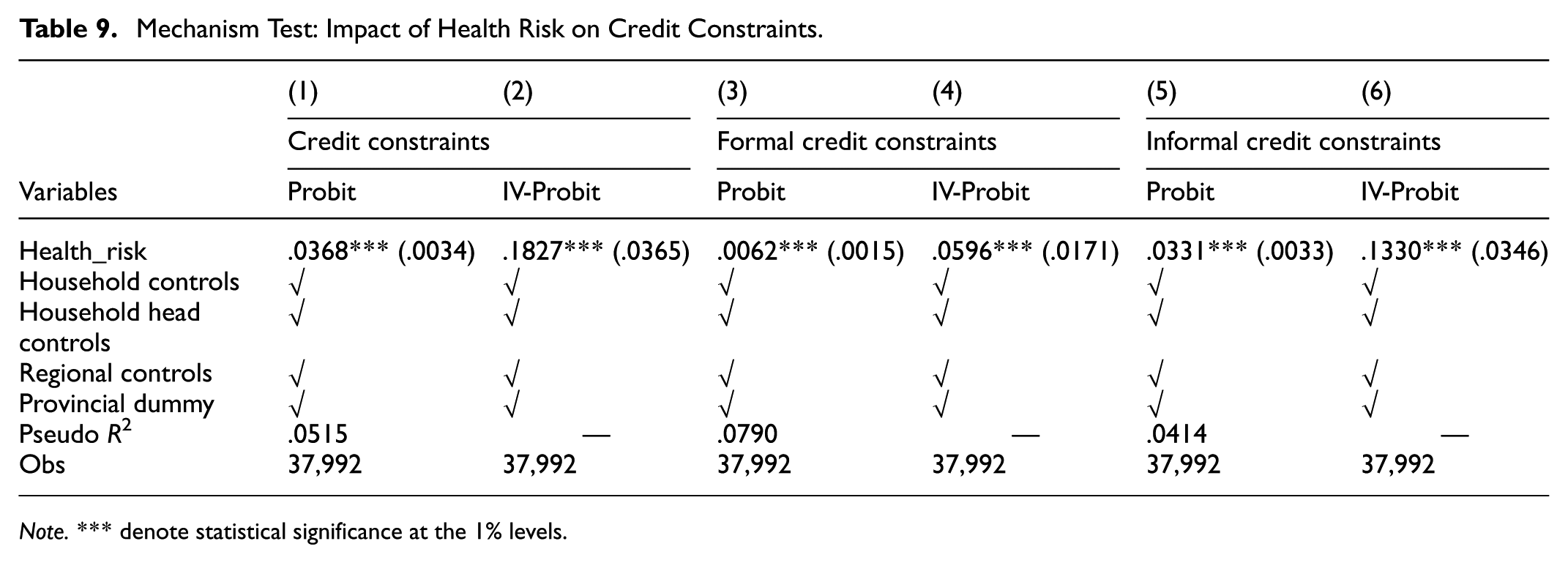

This section investigates how credit constraints act as an additional mechanism through which health risks increase household economic vulnerability. Specifically, it evaluates whether declining health status exacerbates financial strain by limiting households’ access to credit, further intensifying economic hardship when combined with increased medical expenses and reduced income. Credit constraints are assessed by examining instances where households have experienced loan application rejections, categorized into three distinct groups: overall credit constraints, formal credit constraints, and informal credit constraints.

Table 9 reports the results linking health risks to these credit constraints. Columns (1) and (2) show results from Probit and IV-Probit models for overall credit constraints. The Probit results reveal a marginal effect of 3.68%, meaning each additional household member reporting poor health status raises the likelihood of loan rejection by approximately 3.68%. After accounting for potential endogeneity using IV-Probit estimation, the marginal effect increases significantly to 18.27%, both effects statistically significant at the 1% level. Columns (3) and (4) focus specifically on formal credit constraints. The results show marginal effects of 0.62% in the Probit model and 5.96% in the IV-Probit model, both significant, indicating that declining health status is associated with reduced access to formal lending institutions. Columns (5) and (6) present findings on informal credit constraints, highlighting that health challenges increase the probability of unsuccessful credit requests from family and social networks by 3.31% in the Probit model and 13.30% in the IV-Probit model, again statistically significant at the 1% level.

Mechanism Test: Impact of Health Risk on Credit Constraints.

Note. *** denote statistical significance at the 1% levels.

Overall, these findings underscore that health risks considerably heighten households’ likelihood of encountering credit constraints from both formal financial institutions and informal networks. Limited access to credit thus emerges as a crucial channel through which health shocks intensify financial vulnerability and undermine households’ economic resilience.

Heterogeneity

Age Heterogeneity

According to the Life-Cycle Hypothesis (Modigliani & Brumberg, 1954), households at different life stages differ significantly in their ability to generate income, their spending patterns, and their risk-bearing capacities. Consequently, the impact of health risks on economic vulnerability is expected to vary by age group. To investigate this, households are classified into three categories based on the age of the household head: younger (<40 years), middle-aged (40–59 years), and older (≥60 years). The distinct effects of health risks on financial vulnerability and poverty vulnerability across these groups are presented in Table 10.

Test Results for Age-Based Heterogeneity.

Note. The group difference test p-values are as follows: between Columns (1) and (2) = .418; between Columns (2) and (3) = .021; between Columns (1) and (3) = .035; and between Columns (5) and (6) = .062.

and *** denote statistical significance at the 5% and 1% levels.

Columns (1) to (3) indicate that health risks significantly increase financial vulnerability for all age groups, demonstrating that declining health status poses short-term financial challenges irrespective of age. However, the severity of this impact differs notably across groups. Younger and middle-aged households exhibit similar marginal effects of .019 and .0174, respectively, whereas older households show a substantially higher effect at .031. This implies that older households are more likely to experience short-term financial shocks resulting from health-related challenges. This increased sensitivity among older households likely arises from factors such as lower employment participation, reliance on fixed incomes such as pensions or family transfers, limited asset liquidity, and less flexibility in medical care expenses. In contrast, younger and middle-aged households typically maintain greater employment opportunities, potential income growth, and flexibility in labor supply or credit access, enabling them to manage financial pressures from health shocks more effectively.

Columns (4) to (6) examine poverty vulnerability, revealing even clearer age-related disparities. Health risks significantly affect only middle-aged and older households, with the magnitude of the effect increasing with age. These results suggest that as households grow older, health-related financial shocks evolve from immediate liquidity constraints into long-term poverty risks. Older households face specific structural barriers, including limited access to financial services, insufficient social protections, and fewer opportunities for employment recovery, making them more susceptible to prolonged poverty following health shocks. Younger households, conversely, often have advantages such as better baseline health, stronger employment prospects, and greater resilience, which reduce the likelihood that temporary financial distress will lead to chronic economic hardship. In summary, age emerges as a crucial factor influencing how health risks translate into economic vulnerability. Older households are particularly susceptible, displaying greater financial strain and relatively lower resilience to health-related economic disruptions.

Material Capital Heterogeneity

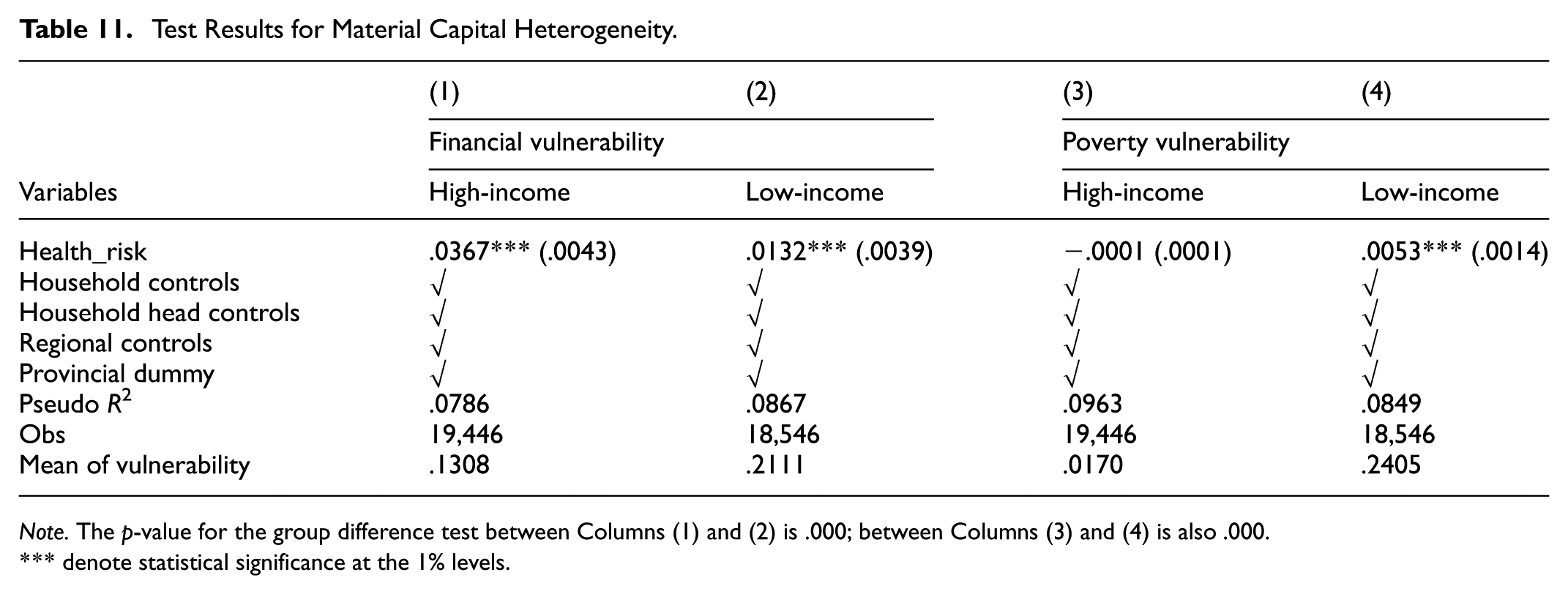

Drawing on Buffer-Stock Saving Theory (Carroll, 1997), households build savings as a precaution against unexpected expenses or income disruptions. Typically, households with higher income levels demonstrate greater financial resilience due to their ability to save more and access additional resources, enabling them to manage health shocks through savings or asset sales. Consequently, household income significantly influences vulnerability to health-related economic risks. To analyze differences based on household material capital, this study categorizes households into higher-income and lower-income groups using median total household income as the threshold. The effects of health risks on financial and poverty vulnerability are then separately examined for each group, with results presented in Table 11.

Test Results for Material Capital Heterogeneity.

Note. The p-value for the group difference test between Columns (1) and (2) is .000; between Columns (3) and (4) is also .000.

denote statistical significance at the 1% levels.

Columns (1) and (2) show the effects of health risks on financial vulnerability for both income groups. The analysis finds significant impacts in each group, but notably, the effect is considerably larger for households with higher income levels compared to households with lower income levels, with the difference being statistically significant. Although initially surprising, this outcome highlights that households with higher income levels frequently hold a substantial proportion of assets in illiquid forms—such as real estate or long-term investments—which cannot be easily or quickly converted into cash during emergencies. Moreover, due to their higher standard of living and preference for premium healthcare services, their health-related expenditures tend to be substantially greater, amplifying their short-term financial vulnerability when faced with sudden health expenses.

Columns (3) and (4) report the findings on poverty vulnerability, revealing a contrasting pattern. Here, health risks have a significantly stronger and longer-lasting impact on households with lower income levels, with a marginal effect of .0053. This indicates that while households with higher income levels might encounter temporary liquidity challenges, their overall financial resources, income stability, and credit accessibility typically prevent them from descending into poverty. Conversely, households with lower income levels often have limited savings or less access to effective safety nets, increasing their likelihood of experiencing sustained economic hardship following health shocks. For these households, health challenges may contribute to prolonged economic difficulties, resulting in long-term vulnerability. In summary, while households with higher income levels primarily face short-term liquidity issues due to asset illiquidity and substantial medical costs, households with lower income levels experience greater long-term poverty risks from health-related financial shocks.

Social Capital Heterogeneity

According to Social Capital Theory (Coleman, 1988), households can leverage relationships with family members, friends, and broader community networks to obtain informal support such as financial assistance, caregiving, or useful information, particularly during crises. These social connections act as informal insurance, partially mitigating the economic impact of unexpected events, including health shocks. To examine this, the study measures social capital using household spending on gifts and ceremonial payments—commonly referred to as Renqing spending. Households are categorized into groups with relatively higher and relatively lower levels of social capital based on median expenditures, with separate analyses conducted to evaluate how social networks influence financial and poverty vulnerability resulting from health risks. Results are summarized in Table 12.

Test Results for Social Capital Heterogeneity.

Note. The p-value for the group difference test between columns (1) and (2) is .036.

denote statistical significance at the 1% levels.

Columns (1) and (2) show the impact of health risks on financial vulnerability. Health risks significantly increase financial vulnerability for both groups, but notably, the effect is larger for households with relatively higher levels of social capital than for those with relatively lower levels, with this difference statistically significant. This outcome suggests that although households with stronger social connections may access better informal support, they also tend to maintain higher living standards and seek higher-quality healthcare. Consequently, these households are more likely to incur significant out-of-pocket medical expenses for treatments such as hospitalization or specialized care, which may intensify their short-term financial pressures. Thus, in terms of immediate financial vulnerability, higher levels of social capital may, in some cases, be associated with greater economic strain from health shocks.

Columns (3) and (4) report results on poverty vulnerability, illustrating a more beneficial role of social capital in the long run. The marginal effect of health risks for households with relatively lower levels of social capital is significant at the 1% level, while it is much smaller and statistically insignificant for households with relatively higher levels of social capital. This indicates that strong social networks provide crucial long-term support, effectively reducing the likelihood of experiencing sustained economic hardship after a health shock. Informal assistance—whether financial, practical, or emotional—from family, neighbors, and friends acts as a critical safety net, helping households prevent short-term financial stress from developing into chronic vulnerability. In contrast, households with fewer social connections may have less access to this form of informal support, increasing their risk of long-term poverty following health-related financial stress.

Digital Finance Heterogeneity

The emergence of digital inclusive finance has significantly transformed financial accessibility, addressing traditional obstacles such as limited service availability, high borrowing costs, and inadequate coverage. For households with greater economic vulnerability, digital finance enhances access to essential financial tools including credit, insurance, and payment services, thus improving convenience and availability. These digital services enable households to effectively manage external shocks, smooth consumption, and diversify risk (Duan et al., 2024; Yue et al., 2025). Real-time, accessible solutions such as mobile payments, digital lending, online mutual aid, and digital insurance help households become more resilient against health-related financial shocks. To investigate whether the impact varies by region, the study divides the sample into regions with relatively higher and relatively lower levels of digital finance access based on the median value of the provincial-level Digital Inclusive Finance Index. Separate regression analyses examine how health risks influence financial and poverty vulnerability in each region, with results presented in Table 13.

Test Results for Digital Finance Heterogeneity.

Note. The p-value for the group difference test between columns (1) and (2) is .036; between columns (3) and (4) is .064.

denote statistical significance at the 1% levels.

Columns (1) and (2) indicate that health risks significantly raise financial vulnerability in both groups of regions. Notably, the effect is stronger in regions with relatively higher digital finance access compared to regions with relatively lower access, and this difference is statistically significant. This result suggests that despite improved access to financial services and credit through digital finance, short-term liquidity risks may actually increase. Easy access to digital credit can create risks of over-borrowing or challenges in financial management, particularly for households with limited financial literacy or unstable incomes. This situation may lead to increased repayment pressures and heightened short-term financial instability.

Conversely, Columns (3) and (4) demonstrate that the impact of health risks on poverty vulnerability is smaller in regions with relatively higher digital finance access than in regions with relatively lower access. This finding indicates that digital finance can effectively reduce long-term poverty risks associated with health shocks. Enhanced financial inclusion through digital services allows households to better smooth consumption, pool risk, and obtain timely financial assistance. These advantages help prevent short-term economic disruptions from developing into sustained financial hardship, underscoring the critical role of digital finance in promoting household economic resilience.

Heterogeneity Based on Medical Insurance Participation

Health insurance provides a fundamental mechanism to help protect households from the economic impacts of illness and to reduce the risk of poverty associated with health-related shocks. However, whether insurance effectively moderates the relationship between health risks and economic vulnerability remains an empirical question. This section examines how health insurance coverage influences households’ economic responses to health risks, specifically assessing both the protective role and potential unintended effects of insurance participation. The analysis compares two groups: households with full insurance participation and households without insurance coverage. Regression results are summarized in Table 14.

Test Results for Medical Insurance Participation Heterogeneity.

Note. The p-value for the group difference test between columns (3) and (4) is .043.

denote statistical significance at the 1% levels.

Columns (1) and (2) reveal the impact of health risks on financial vulnerability. For insured households, the marginal effect is statistically significant at .0250, whereas for uninsured households, the marginal effect is smaller (.0074) and lacks statistical significance. This suggests that while insurance enhances access to healthcare services, it might also be associated with greater use of higher-cost medical services. Such increased utilization can increase short-term financial pressures, consistent with prior studies identifying an “induced expenditure effect,” whereby coverage reduces care barriers but may also increase out-of-pocket spending due to greater use of higher-cost services.

Columns (3) and (4), examining poverty vulnerability, present a different pattern. The marginal effect of health risks is higher for uninsured households compared to insured households, with both effects statistically significant. This indicates that although insurance participation may contribute to greater short-term financial pressures, it significantly reduces long-term vulnerability. By improving access to essential medical care and limiting catastrophic expenses, health insurance effectively acts as a safety net, helping prevent health shocks from leading to sustained economic hardship.

Conclusion and Policy Recommendation

Conclusion

This study uses data from the 2016 to 2022 China Family Panel Studies (CFPS) to systematically examine how health risks affect household economic vulnerability. By distinguishing between financial vulnerability and poverty vulnerability, the analysis addresses an important gap in existing research regarding the multidimensional nature of household vulnerability. Additionally, by considering the context of the COVID-19 pandemic, the study investigates how the effects of health shocks evolved during a major public health crisis. The paper identifies specific mechanisms through which health risks impact economic stability, including medical expenses, household income, and access to credit. Furthermore, the analysis explores differences across household characteristics such as income, social capital, insurance coverage, digital finance accessibility, and age, highlighting which characteristics are associated with greater resilience or heightened vulnerability.

The main findings are as follows. First, health risks significantly increase both financial and poverty vulnerability, but their effect on financial vulnerability is particularly pronounced. This indicates that although health shocks may not always lead to poverty, they frequently create notable short-term financial pressures. Second, during the initial phase of the COVID-19 pandemic, health risks had a heightened effect on poverty vulnerability, though this intensified impact diminished in the post-pandemic period. In contrast, the effect on financial vulnerability remained stable. Third, health risks primarily influence household vulnerability through increased medical costs, reduced income, and limited access to credit. Fourth, households with higher material resources, strong social networks, full insurance coverage, or access to digital financial tools mainly experience short-term financial pressures from health shocks. Conversely, households with fewer resources face greater long-term poverty risks. households headed by older adults are more susceptible to both financial and poverty impacts of health shocks, while younger and middle-aged households generally demonstrate greater resilience.

Policy Recommendations

Based on these findings, the study proposes targeted policy recommendations: First, strengthen healthcare security systems to enhance household financial resilience. Policymakers should expand coverage and benefits of medical assistance programs, ensuring households maintain financial stability during health crises. Additionally, establishing comprehensive poverty risk monitoring and early-warning systems that integrate health insurance, social welfare, and poverty alleviation databases can help proactively manage health-induced poverty.

Second, implement strategies that address expenditure, income, and credit simultaneously to improve household economic stability. On the expenditure side, reform medical insurance payment systems to increase reimbursement rates for commonly used medical services and chronic disease management. On the income side, introduce protection mechanisms linked to health status, such as disability insurance and employment protection schemes. Regarding credit, encourage financial institutions to offer affordable emergency health loans without overly stringent collateral requirements, thereby reducing financial exclusion and inequities in credit access.

Third, adopt context-specific policies that account for regional and household-level differences to strengthen the overall coping capacity of households facing higher vulnerability. Enhance grassroots social security networks, unify urban-rural health protection standards, and integrate them with health risk prevention efforts. Promote digital financial inclusion in underserved areas through infrastructure improvements and tailored financial products such as health-specific savings accounts, micro-loans, and digital insurance platforms. For households with higher levels of economic resources, initiatives should focus on enhancing financial literacy and supporting prudent asset allocation to mitigate health-related financial risks.

Limitations

Despite the contributions of this study, several limitations should be acknowledged. First, the measurement of health risks partly relies on self-rated health status. Although several robustness checks with alternative indicators were conducted, the analysis has not yet incorporated more precise data from medical institutions. Second, the study primarily focuses on the Chinese context, and the results may not be directly generalizable to households in different institutional or cultural settings.

Future Outlook

Future research should enhance the empirical analysis by integrating administrative health data, such as medical records, health insurance claims, and disease-specific information. Utilizing these objective and continuous data sources can lead to more precise measurement and dynamic monitoring of household-level health shocks, further strengthening research reliability and depth.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work is supported by National Social Science Foundation Program “Research on multi-dimensional measures, influencing factors and improvement path of middle-income households resilience” (23BJL046). Taishan Scholars Program for Young Experts of Shandong Province (tsqn202408145).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statements

The data that support the findings of this study are available on request from the corresponding author.