Abstract

In this paper, we have developed a new approach to macroeconomic modelling by proposing to introduce the agent’s behaviour in a pandemic situation. In the form of health frictions that alter the economic agent’s behaviour in crisis situations, we have set up a DSGE model whose behavioural functions take into account the existence of healthy and infected populations. The novelty of this work is the inclusion of the two frictions; health and financial, the idea is to succeed in describing the macro-financial dynamics in a pandemic situation. The results obtained confirm the existence of a health accelerator that amplifies macroeconomic shocks.

Plain language summary

we have developed a new approach to macroeconomic modelling by proposing to introduce the agent’s behaviour in a pandemic situation. In the form of health frictions that alter the economic agent’s behaviour in crisis situations, we have set up a DSGE model whose behavioural functions take into account the existence of healthy and infected populations. The novelty of this work is the inclusion of the two frictions; health and financial, the idea is to succeed in describing the macro-financial dynamics in a pandemic situation. The results obtained confirm the existence of a health accelerator that amplifies macroeconomic shocks.

Introduction

If the behaviours of economic agents are influenced by pandemic circumstances, we may be witnessing a profound transformation. In the labor market, for instance, remote work has become increasingly prevalent, suggesting that what began as a pandemic response has evolved into an endogenous shift in behaviour. Recruiters and employers are now encountering new expectations from employees and households, signalling the emergence of a change in the leisure-work balance that could reshape macroeconomic models

The COVID-19era has amplified this phenomenon, revealing new dimensions in macroeconomics and finance. In this context, our work aims to rehabilitate the behavioural functions of economic agents, enabling the modelling of various states of work and leisure under exposure to shocks such as the COVID-19 pandemic. The pandemic’s impact has prompted a paradigm shift in macroeconomic modelling, as the behaviour of economic agents has undergone significant transformations during epidemic situations. Our current focus is to develop a model that accounts for these atypical behaviours, with the core objective of endogenizing adaptive responses to extreme and pandemic-related events.

Currently, numerous studies address this question, with the body of work steadily expanding Berger et al. (2020), Bootsma et al. (2007), Coeurdacier and Gourinchas (2008), de Walque et al. (2020), Farhi et al. (2012), Ferguson et al. (2006), Firano (2016a), Firano (2016b), Firano et al. (2012), Ginsberg et al. (2009), Glover et al. (2023), Guerrieri et al. (2022); Kaplan et al. (2016); Kermack & McKendrick (1972); Kozbial (2010); Perrings et al. (2014); Philipson (2000), Stock (2020) & Verity et al. (2020). Drautz-burg and Uhlig (2015) and Faria-e-Castro (2021) employ dynamic stochastic general equilibrium mode (DSGE) to simulate recession scenarios, incorporating financial sector interventions such as asset purchases in unconventional policy contexts. Benigno et al. (2020) explore the role of monetary and fiscal policies in mitigating the recessionary effects of the pandemic. Similarly, Eichenbaum et al. (2020) integrate the canonical SIR epidemiological model into a real business cycle framework. By endogenizing the epidemic’s dynamics, their model examines optimal health policy responses, revealing that severe recessions, driven by agents’ rational decisions to reduce consumption and working hours, can help mitigate the epidemic’s impact.

Faria-e-Castro (2021), in more recent work, treats the epidemic as exogenous and investigates how fiscal policies can stabilize income and consumption during the crisis. Relatedly, Guerrieri et al. (2022) demonstrate that supply shocks in a multisectoral economy with incomplete markets can produce effects akin to aggregate demand shocks under specific conditions. They also analyze fiscal policies during the pandemic, showing that supply shocks may mimic aggregate demand shocks depending on parametric assumptions. Lastly, studies by Bayer et al. (2020) and Elenev et al. (2020) delve into the impacts of fiscal measures, with Bayer et al. focusing on household transfers and Elenev et al. on corporate bailouts in response to the COVID-19 crisis.

In addition to the aforementioned studies, other research examines the effects of the COVID-19 pandemic on health and economic contexts, albeit with limited reliance on macroeconomic models grounded in microeconomic foundations. For instance, Adda (2016), Manski (2016), and Philipson (2000) explore how private incentives for vaccination influence epidemic dynamics and inform optimal public health policies. Atkeson (2020) provides a comprehensive overview of SIR models and their relevance to the COVID-19 pandemic. Alvarez et al. (2020) analyse optimal lockdown strategies in an extended SIR framework, where the mortality rate rises with the number of infections. Toda (2020) applies an SIR model to investigate the pandemic’s impact on stock markets, while Jones et al. (2020) study optimal mitigation policies in models that integrate economic activity with epidemic dynamics.

Jones et al. (2020) additionally focus on the role of learning-by-doing in remote work, incorporating a behavioural assumption of fatalism regarding future infection risks. These studies utilize compartmental modelling methodologies, segmenting heterogeneous populations based on infection status. However, despite their insights, these models remain rooted in partial equilibrium frameworks, which are inherently limited in capturing the complexities of a general equilibrium context.

In this research, we propose the introduction of a new rigidity into a macroeconomic model grounded in microeconomic foundations: health frictions. The central objective of this study is to model the rationing of consumption in the presence of health-related rigidities that impede the utility-maximizing behaviour of economic agents, particularly households. Furthermore, we incorporate the financial system into the model by introducing financial frictions, including bank heterogeneity and the potential existence of an interbank market. This integration is essential for capturing the financial system's dynamics under pandemic conditions. In essence, the inclusion of the financial system enables the endogenization of money, facilitating an analysis of the pandemic’s impact on the economy’s financial conditions.

Our approach to incorporating the pandemic into an economic framework is grounded in the SIR model with differential equations, originally developed by Kermack and McKendrick (1972). We extend this framework by integrating key macroeconomic variables to capture the interactions between epidemic dynamics and economic activity. This study builds upon prior research, such as Zakaria et al. (2020), which follows a similar principle. The central hypothesis of this work posits that containment measures, while effective in mitigating the severity of the epidemic-as measured by the total number of fatalities-also reduce consumption, employment, and production, thereby exacerbating the economic recession caused by the pandemic.

Moreover, this research seeks to broaden the scope of analysis to encompass various sectors, particularly the banking sector. The proposed model acknowledges both supply- and demand-side effects. On the supply side, the outbreak increases the risk of exposure to the virus for workers, prompting a reduction in labor supply. On the demand side, the risk of exposure to the virus while purchasing consumer goods leads to a decline in consumption. These combined effects on supply and demand result in a deep and persistent recession (Martin et al., 2020).

This paper examines the dynamics altered by the interplay between health and financial shocks. The disruption of households’ economic activity, particularly their labor supply, has significant repercussions on overall economic productivity and output. This behavioural shock propagates to banks through two primary channels: the credit channel and the deposit channel. A contraction in supply and demand within the banking system exacerbates the risk of default and intensifies liquidity tensions in financial markets, thereby amplifying financial frictions.

However, we demonstrate that fiscal and unconventional stabilization policies can effectively mitigate the adverse effects of these shocks. Our analysis also highlights the need to reconsider behavioural assumptions in future macroeconomic models. Rigid, binary representations of agents’ choices between leisure and work are no longer adequate. Instead, macroeconomic models should adopt greater flexibility to better capture the dynamics of optimal equilibrium in evolving economic contexts.

Agent’s Behaviour

The objective of this work is to describe the dynamics of the economy within the context of a pandemic. To achieve this goal, it is crucial to model the behaviour of economic agents while making the possibility of a pandemic endogenous to the system. In this regard, we propose a model that endogenizes the potential for pandemic-induced behaviour among households. The central idea is to model the impact of a pandemic on household demand, which, in turn, influences the production conditions of firms and financial institutions (supply effect).

To facilitate this, we have developed a macroeconomic model that captures the various potential behaviours in an epidemic context. Specifically, we construct a DSGE model that incorporates the banking system. This model is inspired by the work of Firano et al. (2012) and features five agents: households, production firms, the central bank, and two heterogeneous commercial banks. The first bank’s role is to collect deposits from households, while the second bank is responsible for addressing the liquidity needs of firms by providing loans and financing working capital. The inclusion of two banks allows us to capture one of the key financial frictions: the heterogeneity of financial institutions.

The representative household is assumed to be the owner of both banks, and its savings generate a return that allows for an increase in future consumption. The household’s second source of income comes from wages earned through its participation in the productive sector. The business sector is modelled as monopolistic, with firms producing output in the manufacturing sector. The output produced by the representative firm is used to meet the needs of both the firm itself and households. To achieve its production goals, the firm utilizes capital from the commercial (investment) bank, in exchange for a return on the loans it receives.

The relationship between the two banks in the system is established through the existence of an interbank market. The bank denoted as δ utilizes the funds deposited by households to grant loans to the bank denoted as γ, which acts as an intermediary between the financial system and the productive sector. The bank γ also receives loans from the central bank and extends loans to the productive sector. The profit of the two banks is as follows: for bank δ, it is the difference between the remuneration it receives from bank γ and the interest paid on deposits, while for bank γ, it is the difference between the interest charged to the productive sector and the interest paid to both bank δ and the central bank. Competition between the two banks is assumed to be absent, which allows a monopolistic market structure to prevail in both the supply and demand markets. The interbank market is considered to be complete, meaning that transactions between the two banks occur continuously and without interruption.

The central bank plays a role in this economic structure through its ability to inject money into the money market. The model assumes that the central bank intervenes via open-market operations, enabling it to increase interventions during periods of significant liquidity needs and to meet additional demands in the money market. In this framework, the model disregards the existence of a Taylor rule, with the central bank focusing solely on its role as a liquidity provider.

The five economic agents in the model are assumed to be rational, capable of maximizing their expected intertemporal utility at time t = 0, while considering all the relevant objective constraints. We focus on the set of discrete time periods

Households

In addition to the behaviour outlined in the previous section, we assume that households are the sole source of pandemic propagation. This assumption implies that the pandemic will impact their consumption, work capacity, and the overall conditions for financing the economy.

The spread of an infectious agent within a population is regarded as a dynamic process, where the numbers of healthy and infected individuals change over time. This evolution depends on interactions during which the infectious agent is transmitted from an infected individual to a susceptible, non-immunized person, who then becomes infected in turn. Such a phenomenon can be modelled using differential equations, with its dynamics determined through the numerical solution of these equations.

The basic model used is the SIR model, where “S” represents the number of susceptible (healthy) individuals, II denotes the infected individuals, and “R” refers to those who have recovered and are assumed to be permanently immune. This model operates under the assumption that once an individual is cured, they are no longer susceptible to reinfection. The sizes of each of these populations vary over time, and this can be represented as functions of the independent variable t, time: S(t), I(t), and R(t). If, during the course of the epidemic, the total population size “P” is considered constant, we can write the following relationships:

Each compartment is associated with a state variable: S, I, and R. It is now a question of writing a system of differential equations which links the derivative of the functions,

The spread of the epidemic arises from contaminating contacts between infected individuals and susceptible (healthy) individuals. Analogous to the predation dynamics in the hare-lynx model, the number of infections increases as a function of the interactions between infected and susceptible individuals. This rate of transmission is proportional to the product of the sizes of the infected population “I” and the susceptible population “S.” Additionally, the total population is assumed to be constant and normalized to a value of 1).

Where:

The incorporation of health dynamics into household behaviour will affect the utility function that needs to be optimized. In this context, the household population can be modelled using the previous equations, with the health status influencing the decision-making process and utility maximization. The interaction between health variables and household behaviour will be reflected in how the utility function adjusts in response to changes in health-related factors such as infection rates and recovery:

Therefore, the utility function is described in the following form:

With

By replacing the population with the description in differential equations, we can have the following constraint:

with:

On the basis of the two functions, utility and the budget constraint, the Lagrange function (M) after simplification is as follows:

Using this formulation of the utility function taking into account pandemic behaviours and also the existence of financial frictions, the first order conditions are:

The first order conditions make it possible to set up two important equations namely the labour supply and the Euler function:

Firms

We will represent all the manufacturing production companies by a representative firm noted “

Under the constraints:

(i.e., Expenses of f devoted to salaries = Credits of firme “f”—Cost on credits of the previous period)

The representative firm maximizes its expected intertemporal profit subject to two main constraints. The first constraint pertains to the repayment obligations associated with its bank debts, while the second concerns the remuneration of the various inputs that contribute to the generation of value-added. These constraints guide the firm’s decisions regarding investment, production, and financial obligations over time.

The production function is assumed to be verified;

With:

The Lagrange function is described in the form below:

The first order condition (CPO) is:

Through these conditions we can derive the price formation function and also the optimal quantity of production:

Changes in the equilibrium conditions are assumed to occur following a fluctuation in the technological factor of the firm. To simulate the shocks on the technological factor of the firm, we will assume that the factor

Where

Another type of shock can arise that endangers the activity of the firm, it is that relating to the credit risk when the firm is confronted with problems of solvency towards the investment bank.

where

Deposit Bank

The first type of bank considered in this model is a deposit bank, whose role is to collect savings from households. To grow these funds, the deposit bank partners with the second bank in the interbank market, aiming to finance investment and contribute to economic growth. In this framework, the deposit bank maximizes its expected intertemporal utility at each point in time, optimizing its decisions based on future returns and liquidity needs.

Under the constraint:

(i.e. Interbank loan from the deposit bank

With the profit:

Variables and parameters are defined by:

The Lagrange function is described by the following formulation:

Through this function, we can define the first order conditions:

The first order conditions make it possible to define the optimal conditions for fixing the interest rates and also the quantity of deposits to be used.

The profit of the deposit bank is influenced by the dynamics of the interbank interest rate and the savings behaviour of the representative household. The evolution of the household’s deposits with the deposit bank is contingent on fluctuations in the repayment rate between the bank and the household, which, in turn, affects the default penalty. In order to bring out the effects of a contraction in deposits, we assume that the default penalty

Where

Investment Bank

By benefiting from the resources emanating from the deposit bank, the investment bank

Under constraint:

(i.e., the loan from bank γ to firm f = monetary endowment of γ+ loan from γ in the interbank market—cost of interbank credit for γ)

With:

With:

The Lagrange function takes the following form:

The CPO are: For more details please see the appendix

The optimality conditions are deduced by the expansion of the first order conditions:

It is assumed that the default penalty

where

Economic Policies

In the aftermath of the COVID-19 crisis, authorities are faced with a situation characterized by low interest rates and weakened fiscal conditions, as countries, including Morocco, are recovering from the financial crisis. To address these challenges, the Moroccan government established a fund specifically aimed at mitigating the adverse effects of the health crisis. This fund, amounting to over 3 billion USD, is designed to counter the negative economic impacts of the pandemic. In this context, exogenous currency can be defined as liquidity injected into the economy by the government or through foreign transfers. This exogenous currency enters the system, is free from any obligations, and accumulates within the economy, providing temporary relief and supporting economic recovery. If

The aggregate monetary endowment is distributed over all economic agents:

Where:

We assume that in the model the agents receive their endowment with the same proportions:

Where the weights check:

In order to stationarize the variable

To simulate the budget shock, we assume that the growth rate

Where

The budget shock leads to an increase in the liquidity available to economic agents, which, in turn, triggers changes in their savings, consumption, and production behaviours. With an abundance of liquidity in their portfolios, agents experience an improvement in their ability to meet various financial commitments. However, as currency becomes more readily available to households, businesses may respond by reducing production levels in anticipation of a potential decline in prices. This behaviour leads to lower production, reduced value-added output, and a decrease in wages and employment.

In response, households are likely to adjust by reallocating resources away from savings and deposits in an effort to smooth consumption and stabilize their consumer baskets. Meanwhile, banks, facing an altered economic environment, may reduce the amount of credit they extend to the economy, opting instead for a credit rationing policy. As a result, the reduction in deposits and loans will drive up both debit and credit interest rates, as well as the interbank rate. This, in turn, leads to a decline in asset prices and may trigger a cycle of deleveraging and deflation, which ultimately proves detrimental to economic agents, particularly in a context of credit rationing.

The endogenous currency represents the interventions of the Central Bank on the interbank market. The injected liquidity leaves the system when the investment banks repay their bonds. We model endogenous currency shocks by changes in open market operations.

The parameter

where

Model Estimation and Calibration

The application of a macroeconomic model with microeconomic foundations, which incorporates health frictions (such as changes in leisure and productivity behaviours), is now essential for preparing for an uncertain economic environment. The use of Moroccan data within this modelling framework is intended to account for the specificities of developing economies, which are more vulnerable to the effects of crises compared to high-income countries. Furthermore, the choice of Moroccan data is justified by the successful management of the health crisis, which underpins the rationale for this selection.

Based on Moroccan economic and financial data from 2000 to June 2020 (quarterly frequency), we have identified the key parameters and initial values necessary for simulation purposes. The data were sourced from official Moroccan institutions responsible for publishing public data related to the country’s financial and economic conditions. Initially, the selection of the model's initial values followed two approaches: the first based on the average of macroeconomic series for which we have comprehensive data, and the second based on the choice of a base year, which we determined to be 2020.

The endogenous variables, initialized through the average of their evolution between 2000 and 2010, include credits to the economy, customer deposits, inflation rate, value-added, money supply, and the interbank interest rate.

According to the evolutions recorded during the year 2009, the interbank indebtedness, the profitability of the banks, the proportion to be consumed and the borrowing and borrowing rates showed the following values (Table 1):

Initial Value.

The calibration of the model was carried out following an analysis of the evolution of the country’s macroeconomic aggregates. This stage involved first identifying the elasticities of certain model equations and then incorporating these elasticities based on empirical work applied to other countries. The discount coefficient for both households and banks were hypothetically estimated to be close to unity. The various repayment rates for bilateral debts were considered to be near 1, indicating that there is no insolvency among the economic agents in an equilibrium scenario. The technological factor was assumed to be equal to unity, in line with the theoretical approach.

As for corporate profit rates, it was assumed that these rates are approximately 20%, reflecting an internal rate of return higher than the cost of capital in the Moroccan financial market. Other parameters that capture inertia within the system were evaluated using time series models. The table below presents the values retained for these parameters. Additionally, the initial distribution of money across all agents was assumed to be equal, with each agent holding 25% of the total currency in circulation (Tables 2, 3).

Initial Value 2.

Calibrate Parameters.

Finally, to initialize the effects of health frictions in the model, we calibrated the pandemic parameters using the data officially provided by the Ministry of Health in Morocco. To account for the effects of the 2008 financial crisis and isolate its impact on macroeconomic conditions, we employed a long-term average calibration of the various aggregates to define the model’s optimal equilibrium level. The use of long-term averages helps mitigate seasonal effects and allows us to control for the influence of the crisis on the model’s dynamics (Table 4).

Pandemic Variable Calibration.

Results Analysis

The estimation method employed is the Bayesian approach, utilizing Markov Chain Monte Carlo (MCMC) algorithms to determine the various parameters, with their distributions calibrated accordingly. The estimates were based on data from 2000 to June 2020, with a quarterly frequency. The results of the model estimates are presented in the table below, alongside the baseline values retained for the Moroccan economy (Table 5).

Estimation Results.

The incorporation of sanitary conditions, as modelled in this paper, will have significant implications for the behaviour of economic agents. These effects will be clearly illustrated through the shocks we have implemented. To guide the analysis, we will compare two models: the first includes real, nominal, and financial frictions, while the second incorporates health frictions in addition to the previous ones. The comparison between these two models will allow us to highlight the combined effects of different frictions and provide insight into the macroeconomic dynamics during a health crisis.

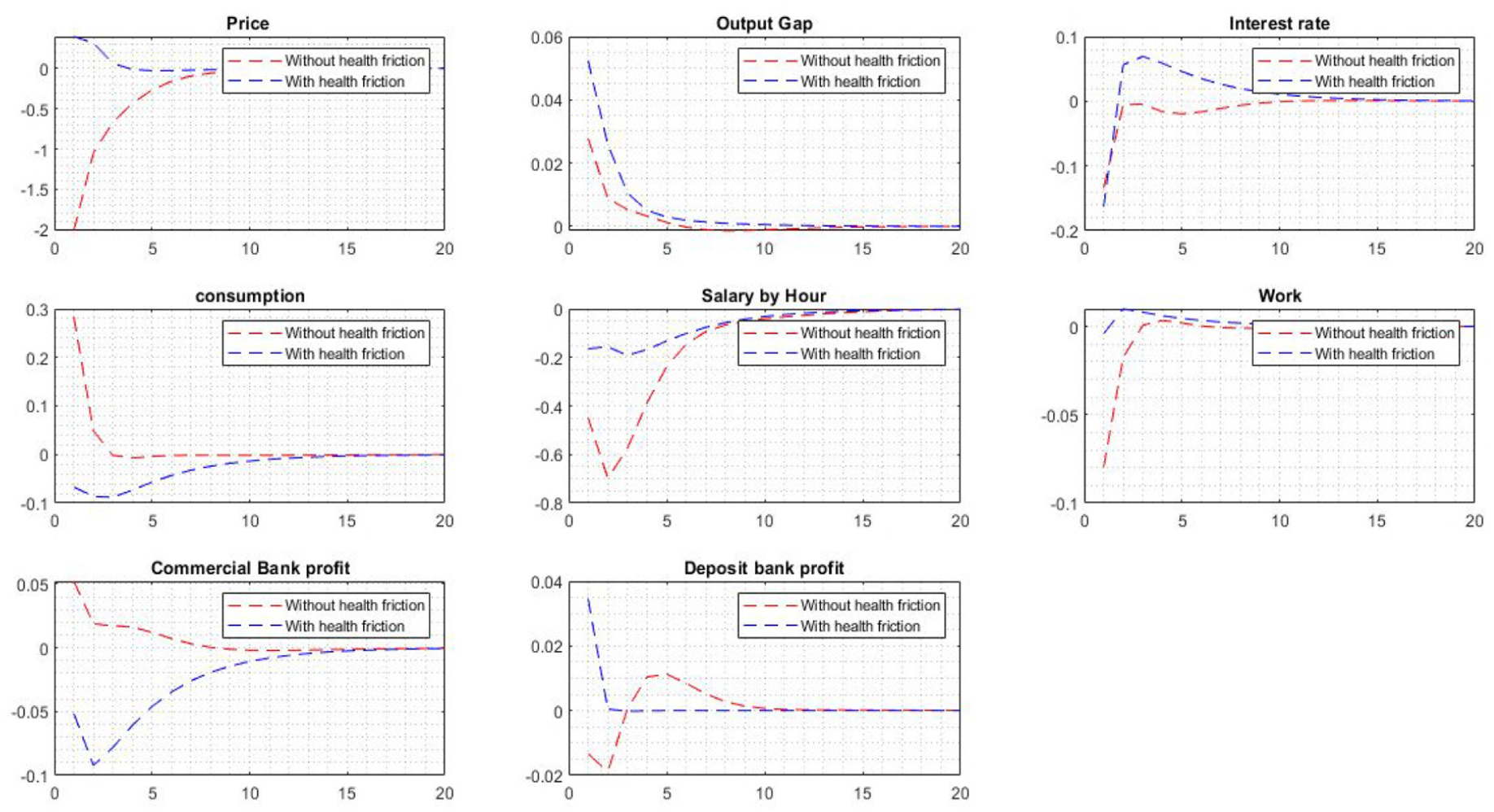

Before comparing the two models, we first examine the effects of a health shock on the economy as a whole. This shock is represented by an increase in contamination, driven by a rise in the infected population (I). The epidemic shock and the corresponding increase in the infection rate have a profound impact on economic equilibrium. Specifically, we observe a significant decline in economic growth, accompanied by worsening price levels and rising interest rates. The slowdown in growth leads to a deterioration in savings capacity, as households prioritize consumption over investment. Consequently, the health shock results in a reduction in the profits of deposit banks and a slight decrease in the profits of commercial banks in the short term. Additionally, a decline in the labor force is observed, although wages remain relatively stable in the short term (Figure 1).

Health shock.

The first shock that could impact the economy is an increase in productivity (productivity shock). In this context, we would typically expect expansionary behaviour in the economy, with growth, consumption, and investment all increasing. However, an analysis of Figure 2 reveals rather anomalous effects when pandemic behaviour is integrated into the household behaviour function. Specifically, despite the increase in capital productivity, the labor force declines, which leads to a decrease in wages and, consequently, a reduction in consumption.

Productivity shock.

Regarding banking activity, the productivity shock within a pandemic context generates a significant decline in the profits of commercial banks, driven by the reduction in consumption and investment. On the other hand, deposit banks tend to see an increase in their profits due to the rise in savings and the slowdown in investment. This can be attributed to a liquidity trap, where economic agents prefer holding money in liquid form rather than investing in other financial assets.

The second shock is that of a budgetary nature, the inclusion of the latter being justified by the fact that most governments have responded with policies of budgetary support to households and businesses affected by the pandemic situation. The fundamental idea to be extracted from Figure 3 is the fact that the existence of pandemic effects in the dynamics of agent behaviour has helped to mitigate the effects of expansionary fiscal policies. In other words, the inflationary effects of such a policy were contained when including epidemic behaviour since the money allocated to agents was used only for consumption without having to affect growth and productivity. This dynamic makes it possible to maintain the behaviour of bank profits in the model. It is therefore clear that fiscal policy is the best in a pandemic situation, especially with the objective of maintaining macroeconomic balances.

Fiscal shock.

Monetary policy’s primary objective is to maintain macroeconomic equilibrium. However, in the context of a pandemic and considering the endogenous behaviour of economic agents, particularly households, the effects of such a policy are more pronounced. The explanation here is that, during a health crisis, economic agents tend to adopt a more basic survival-oriented behaviour, leading to an exaggerated response to any expansionary policy. It is important to note that, in this model, monetary policy is based on quantitative measures rather than conventional policy tools, due to the aftermath of the 2008 crisis, where banks largely relied on such policies. Increased cash injections facilitate a more robust economic recovery, resulting in a significant rise in growth, prices, consumption, and wages. The evidence shows that quantitative monetary policy is more effective in a pandemic scenario because it focuses on money supply rather than real economic aggregates. Given the current economic situation, which is harder to control and predict, the monetary circuit approach becomes more appropriate. However, it is important to recognize that the effects of monetary policy will be marginal on banks, as consumption is preferred over investment, and interest rates are falling.

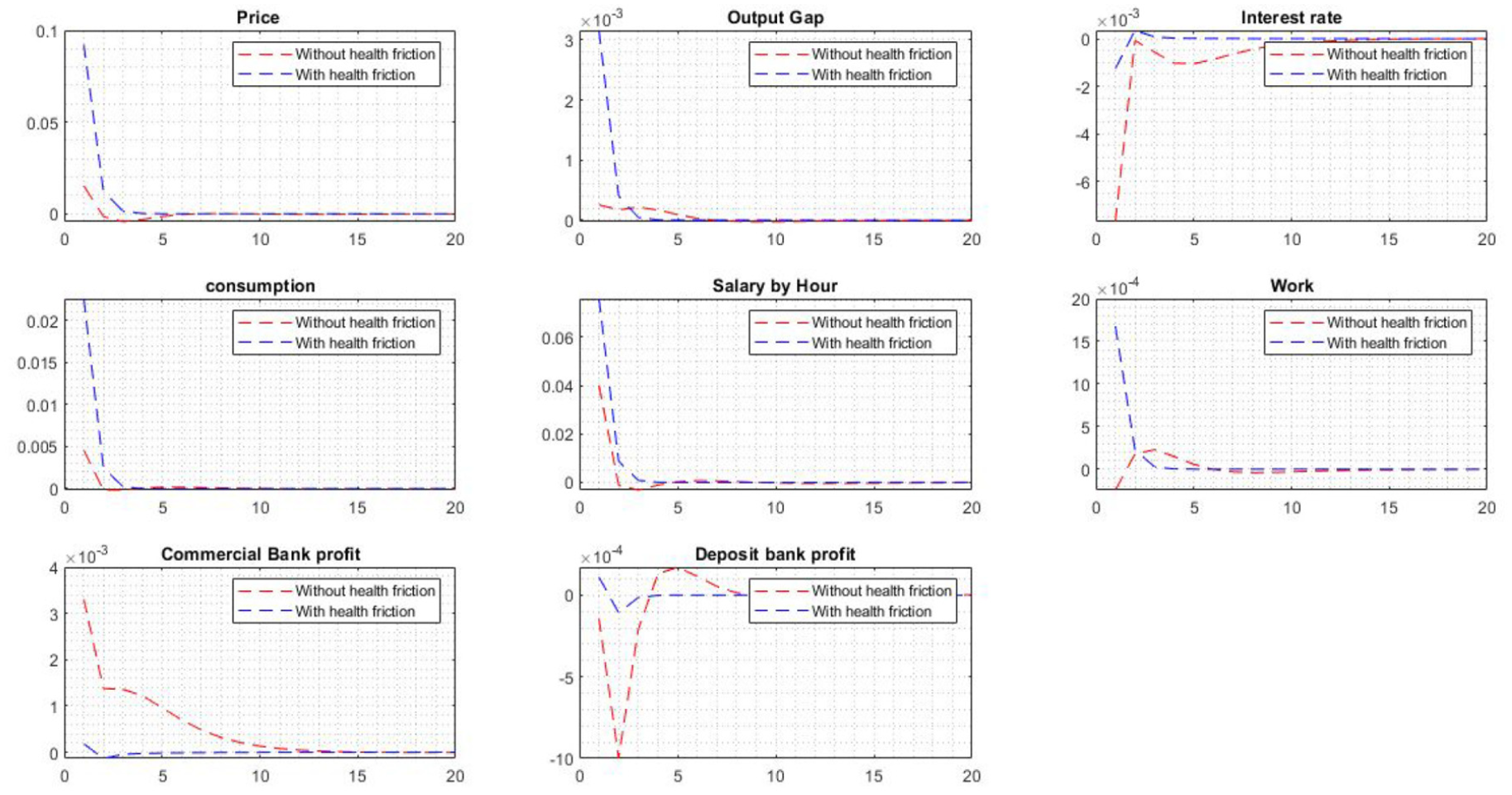

To highlight the relationship between health conditions and the behaviour of the banking system, we considered a shock in the interbank market. It is in fact linked to the possibility of having a contagion crisis in the interbank market following a payment default by the commercial bank. The Central Bank and the economy as a whole fear a crisis in the banking system following slowdowns in growth and also changes in household habits. In this regard, we considered that there is a correlation between the two shocks of corporate defaults and those of the commercial bank and we simulated the impact on the interbank market and on the counterparty relationships of banks.

The first remark is that the simulated economic conditions are different with or without an epidemic. We find that the contagion shock has the greatest effect when considering the pandemic. With a very significant drop in consumption in a pandemic situation, due to the fall in wages and in the workforce, we are therefore witnessing a major reaction in terms of prices which are starting to increase, unlike the situation where the pandemic is absent (Figure 4 and 5). This price increase is stimulated by the rise in the business cycle influenced by the fall in interest rates in the dynamics of the model. The shock of default of the commercial bank induces a regression of its profit despite the increase in the profit of the deposit bank, this however will not be long in reducing after a few quarters even more drastically than the situation without health problem. In this sense, we can say that the sanitary condition causes a certain shock accelerator which is added to other existing frictions.

Monetary policy shock.

Systemic risk shock: Interbank contagion risk.

Conclusion

The need for advanced macroeconomic modelling is more urgent now than ever. As time progresses, it becomes increasingly clear that understanding the endogenous behaviour of economic agents is complex, dynamic, and even chaotic. From this perspective, macroeconomic models grounded in microeconomic foundations offer a promising solution to such challenges. However, the complexity of these patterns has grown, making them harder to capture. Initially, models focused on nominal rigidities, then real rigidities, and after the 2008 financial crisis, financial frictions were incorporated. Now, following the COVID-19 health crisis, it has become essential to revise the modelling framework to account for new health-related frictions.

In this paper, we adopt this approach by incorporating all these rigidities with the goal of understanding the dynamics of the economy and the macro-financial system in the context of a pandemic. The core idea of this work is to posit that health frictions arise solely from the household sector, which, while a strong assumption, offers an idealized framework for the COVID-19 period.

The results of our analysis confirm that the presence of health frictions, in conjunction with financial frictions, serves to amplify the economic shocks. This amplification is primarily due to changes in consumption and labor behaviours during an epidemic. As discussed, a health shock has profound effects on most macroeconomic aggregates, and it also negatively impacts the financial stability of the banking system. Furthermore, we have found that fiscal stimulus policies are more effective than monetary policies in mitigating the effects of a pandemic-induced shock. This is attributed to the fact that increased public spending is a more direct and impactful response compared to monetary interventions during such a crisis.

Footnotes

Appendix

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.