Abstract

The interests of the agent (manager) are not always aligned with the interests of the principal. It is possible that the agent will act for himself and not in the best interest of the principal. In deciding the intention to take aggressive tax action, managers will consider the advantages and disadvantages of their actions. One way to limit counterproductive manager behavior is that the principal will pay compensation costs in the form of incentives. This research examines the compliance behavior of taxpayers represented by company managers. The main idea is to analyze various factors that shape taxpayer behavior regarding compensation in tax compliance. This research is based on a survey of managers at companies registered at the Central Tax Service Office in Bandung, West Java. Primary data was analyzed using Structural Equation Modeling (SEM). The research results show empirical evidence that company managers’ intentions toward tax compliance are supported by perception of control behavior and compensation. Counterproductive work behavior mediated by job satisfaction also supports tax compliance. Managers’ behavior toward the interests of utility principals is influenced by the compensation provided and reduces counterproductive work behavior. So that agency conflicts can be reduced and avoided.

Keywords

Introduction

Tax reform in Indonesia began in 1983, with the introduction of the principle of self-assessment, which has given full trust to the public to exercise their rights and obligations. Apart from Indonesia, several developed countries have taken steps to change their tax application system to keep up with technological developments. They have also implemented a comprehensive tax system (Downer, 2016). Tax compliance is important because it forms the basis for the development and sustainability of a country’s financial system. Inaccurate tax declarations can reduce revenue, increase costs and result in an uneven tax burden. The tax law still emphasizes the aspect of offering punishment rather than the spirit of offering imbalance. On the other hand, tax rules tend to be complex. Taxpayer awareness is supported by the psychological aspects of individuals who carry out certain actions (Kan & Fabrigal, 2017).

The self-assessment system can cause losses in tax revenue when taxpayers do not voluntarily comply with tax rules (Nguyen et al., 2020). Tax compliance and avoidance are the results of a rational decision-making process under risk with the aim of maximizing utility. However, the psychological approach says that there are non-economic factors that play a role, trust in the state shaping taxpayer behavior (Enachescu et al., 2019). Taxpayers will do everything they can to avoid taxes or be disobedient. Conflicts of interest arise between tax authorities and taxpayers (agents). Taxpayers have the intention of paying as little tax as possible, while the state wants to increase its tax revenue. (De Widt & Oats, 2024). Taxpayers carry out various tax planning strategies to minimize tax payments in order to save taxes (Artemenko et al., 2017).

In fact, compliance problems have been around for a long time. This supports the statements of Damayanti et al. (2016) and Harinurdin (2018). Taxpayer compliance is the most important factor in the modern tax system. Tax compliance is when taxpayers comply and carry out their tax obligations in accordance with the provisions of tax regulations (Purnamasari et al., 2016).

According to the research, the Status of Tax Justice 2020: Tax Justice in the period Covid-19 research by the Tax Justice Network, corporate tax evasion in Indonesia costs up to US$ 4.78 billion or Rp 67.6 trillion. The remainder was carried out by individual taxpayers amounting to US$ 78.83 million or almost Rp. 1.1 trillion. Because paying taxes is usually seen as a burden for the business world due to the large amount of tax that becomes a barrier to company income, the level of corporate taxpayer compliance is still low. Meanwhile, the company’s goal is to maximize shareholder value by maximizing company profits. Apart from that, the size of the profits achieved will affect the bonuses that management will receive. So management must act in accordance with the owner’s wishes, so that their interests are achieved. This is often referred to as the agency problem.

Agency conflicts must be minimized. The company owner is the party who has the right to manage the company, but due to differences in entities, the owner is not allowed to manage the company’s technical and operational affairs. The job of a company manager is to convey information related to the company to the company owner. Most agents will think about improving their performance and goals by minimizing all possible costs including tax costs. To achieve this, business advocacy strategies must be implemented (Indrady, 2018).

According to the hypothesis, remuneration will inhibit agency costs because CEOs are more likely to behave in the best interest of shareholders when there is a strong correlation between salary and performance. If employee needs are met, it will create feelings of satisfaction and ease in working so that performance can increase. Work motivation has a significant effect on performance (Setiawan & Siagian, 2017). According job satisfaction theory, job satisfaction is the satisfaction of an employee’s attitude toward work which is related to the work situation, the imbalance received and matters related to physical and psychological factors Sutrisno (2019).

According to Asfa and Meiranto (2017) explaining the Theory of Planned Behavior (TPB), individual behavior arises due to behavioral intentions. Intention arises due to internal and external factors. Individual attitude to behavior Related to belief in a behavior, evaluation of behavioral results, subjective norms, normative beliefs and motivation to obey. TPB is considered related to the factors that influence whether or not taxpayers comply with their behavior in fulfilling tax obligations. Before the individual does something, they certainly have beliefs about the results that will be obtained from the related behavior that makes the individual choose whether to carry it out or not. This is related to taxpayer awareness. Taxpayers who are aware of taxes, have beliefs regarding the importance of paying taxes in assisting the implementation of development (behavioral beliefs).

Perceived behavioral control in the context of taxpayer compliance can also be seen from the complex influence of taxes which can be a challenge for taxpayers in achieving compliance (Taing & Chang, 2021).

The counterproductive work behavior theory approach places great emphasis on bad behavior. These actions may be as minor as taking too long of a break or against policy or as substantial and harmful to the organization as possible, including disrespecting coworkers or engaging in internal fraud. These issues, which range in size from small to large, have a negative impact on organizational effectiveness (Mohamed Badawy & Fathy El-Fekey, 2017).

The gap in this research is that business development is increasingly global, transactions are increasingly complex, tax planning is increasingly aggressive, indicating that the old tax compliance paradigm is no longer effective (Enachescu et al., 2019). In addition, taxpayers make rational decisions in uncertainty by considering all risk factors in making tax decisions (Neuman et al., 2020).

The self-assessment system gives confidence to taxpayers to carry out their tax obligations in calculating, paying taxes and reporting. An opportunistic nature can make corporate taxpayers make efforts to minimize taxes, including through tax planning, tax avoidance, and tax evasion. Tax is an aspect that needs to be managed properly (Bronkhorst & Lesak, 2016). Cooperative compliance is used to reduce information asymmetry between taxpayers and tax authorities through transparency. So that with transparency state revenues will increase, compliance costs can be reduced, and avoid aggressive tax planning practices. Material compliance of taxpayers will become a compliance risk for the tax authorities due to information asymmetry. Taxpayers know more about the information in the company that can act for company goals. This conflict of interest creates an agency problem. The dimensions of power and trust are factors that influence taxpayer compliance behavior (Gangl et al., 2015).

This research combines tax compliance theory and planned behavior theory in the perspective of agency theory. Compliance research cannot be separated from compensation and job satisfaction as well as Counterproductive Work Behavior attached to taxpayers. Violation of tax regulations such as reducing tax payments will increase tax risk (Artemenko et al., 2017, p. 457). Few studies have combined these three concepts. A better understanding of taxpayer behavior can help countries develop effective and efficient ways to improve compliance (Walsh, 2012) and make better decisions (Gobena & Van Dijke, 2017; Randlane, 2016). his needs to be a topic for future research.

This study raises the problem of how compensation factors and counterproductive work behavior can affect taxpayer compliance by using the Theory of Planned Behavior framework and adding job satisfaction as a moderating variable. In line with these problems, this study aims to analyze the factors in the Theory of Planned Behavior, intention, compensation and Counterproductive Work Behavior on taxpayer compliance with job satisfaction as a moderating variable. Therefore, this study aims to determine the effect of Perceived Behavioral Control on intention; to determine the effect of manager compensation on intentions; to determine the effect of intention on tax compliance; to determine the effect of compensation on Counterproductive Work Behavior; to determine the effect of Counterproductive Work Behavior on tax compliance through job satisfaction moderating variables.

Literature Review and Hypothesis Development

Agency Theory

Based on the perspective of Jensen and Meckling (1976, p. 162) in Agency theory, it is said “ a company is a contractual relationship between various parties.” The company has contracts with various stakeholders, one of which is the government. Agency theory arises because of the existence of agency relationships between principals and agents.

“Agency relationship is a contract under which one or more person (the principal(s) engage another person (the agent) to perform some service on behalf of which involves delegating some decision-making authority to the agent” (Jensen & Meckling, 1976).

The principal in classical agency theory is the shareholder and the agent is the company’s management. In terms of taxation, state ownership is similar to shareholders, the state participates in the profits and losses of the company so that the state is entitled to a share in the company’s profits in the form of taxes. In this relationship an agency problem arises because the agent may not act in the interests of the principal. Agency problems arise because of information asymmetry, which can arise from either party. The agency paradigm is used to determine the optimal value of risk sharing between individuals and groups and apply appropriate control mechanisms so that the behavior and actions of individuals can be monitored (Namazi, 2013, p. 40). These elements are used in the theory of tax compliance.

The perspective of principal and agent settings in self-protection can explain compliance to strengthen the predictions of agency theory. To reduce information asymmetry through a cooperative compliance approach requires companies to use and improve internal tax risk management and voluntarily disclose information including corporate tax risks as a form of transparency (OECD, 2018). This form of transparency is a form of initial certainty and alignment of tax risks between agents and principals to reduce information asymmetry (Eberhartinger & Zieser, 2021). Managers are obliged to manage corporate tax affairs for the benefit of non-state shareholders. So that management decisions will affect the amount of tax payable that must be paid to the state as the principal. One way of making tax management decisions is through tax planning activities and considering all the risks that occur.

Tax Compliance

Tax compliance is all the activities of taxpayers consisting of reporting taxes on time, reporting tax debts accurately according to applicable regulations. According to the OECD (2018) “tax compliance is taxpayers paying the right amount of tax at the right time, filing the tax return accurately and submitting the return in time.”

OECD (2010b rights 5) Taxpayer compliance is seen based on four tax compliance obligations that in general must be managed by the state, namely registering taxes, reporting on time according to the date specified in the law, reporting tax obligations correctly and paying taxes on time according to the date determined by law.

Taxpayers comply with regulations when registering, reporting on time, reporting taxes payable accurately and paying taxes owed and maintaining books of account. Failing to fulfill all of these matters constitutes tax non-compliance. Kirchler and Hoelzl (2017, p. 261) stated that tax non-compliance is non-fulfillment of tax obligations by taxpayers, whether intentional or unintentional. Intentional non-compliance is one of the planned behaviors with the aim of maximizing utility. Tax non-compliance is divided into tax evasion and tax avoidance (OECD, 2008b).

The tax avoidance measure is mainly designed to estimate the effective income tax expense (income tax as a percentage of accounting profit or cash flow), the implicit tax effect, the tax uncertainty, the marginal tax rate, the difference between accounting profit and taxable income representing a company’s tax avoidance scheme after control the impact of accounting accruals and earnings management. The theory of taxation begins with economic theory, but along with the increasingly complex behavior of taxpayers, compliance theory continues to develop through various branches of economics, psychology, social, law, and politics (Kirchler & Hoelzl, 2017, p. 118).

Theory of Planned Behavior

Theory of Planned Behavior was developed by Ajzen (1991). A person’s behavior is driven by three factors; (1) behavioral beliefs are the result of beliefs and evaluation of results, a function of individual beliefs about the behavior to be carried out or tax compliance behavior is determined by beliefs about the consequences of a behavior related to individual subjective judgments, behavior based on individual evaluation whether compliance behavior provides benefits or disadvantages. Behavioral beliefs will shape the attitude of certain behavioral deterrent variables, (2) normative beliefs are a function of individual beliefs obtained from the views of others on attitude objects related to individuals, individual beliefs in normative expectations of other people such as family, friends, company leaders, officers tax and tax consultants, (3) control beliefs are behavioral controls that are determined by individual beliefs that the individual has good competence and facilities, or are personal beliefs because of things that encourage behavior. Controlling beliefs will lead to controlling behavior. Regarding the Theory of Planned Behavior one will consider attitudes, subjective norms, and perceived behavioral control in building intentions to comply with rules (Ajzen, 1991).

According to Damayanti et al. (2015), Nurwanah et al. (2018), the nature of tax compliance, subjective norms, perceived behavior, and taxpayer perceptions of the government have a certain effect on the intention to comply with tax obligations. The behavioral approach uses the concept of willingness which emphasizes the behavior of taxpayers to comply with tax obligations voluntarily in accordance with government regulations. economic and behavioral approaches should support each other to increase voluntary tax compliance.

Compensation

According to Amri (2017) compensation is a tool to motivate employees to work harder by providing for employee needs. Compensation can be interpreted as a form of financial return, tangible services and benefits obtained by employees as part of an employment relationship. Agency theory explains that differences in interests between owners and management will cause management to carry out something if it benefits from that action. Based on this, managers as operational leaders of the company will be willing to make tax policies only if they gain benefits from these actions. For this reason, high compensation is one of the best ways to implement company tax efficiency through tax avoidance. This is because they will feel they will benefit from receiving higher compensation so that it will improve the company’s performance even better. One of the ways in which this performance is achieved is through efforts to efficiently pay taxes. High compensation for managers in implementing corporate tax efficiency is the behavioral intention of managers or management not to comply with taxes by implementing tax avoidance. Research on the effect of management compensation on tax avoidance was also conducted by Hanafi and Harto (2014) and Meilia and Adnan (2017). The results of his research state that manager compensation has a positive effect on tax avoidance. This means that the higher the compensation to management, the higher the tax avoidance carried out by the company. The results are different from research by Dewi and Maria (2015) which states that executive compensation does not affect tax avoidance. The results of this research are also supported by Amri (2017) who state that management compensation has a negative effect on tax avoidance.

Counterproductive Work Behavior

Counterproductive work behavior is an action taken by a worker that can harm the entire work environment. Counterproductive work behavior is work behavior that greatly disrupts organizational performance in general and reduces employee work productivity in particular (Rusdi, 2015). Besides that, counterproductive work behavior can directly disrupt organizational functions or with the aim of reducing employee work effectiveness (Wahyuni & Nugraheni, 2016). Counterproductive work behavior is behavior carried out by employees with effects that can be detrimental to the organization and work members. Counterproductive work behavior is a type of deviant work behavior to disrupt the organization and organizational members (Bai et al., 2016).

Job Satisfaction

Job satisfaction is a positive and optimistic emotional state regarding the assessment of work results and work experience (Padmanabhan, 2021). High employee job satisfaction will usually improve employee performance. Organizations that have employees with high levels of job satisfaction tend to be more productive and effective (Eliyana et al., 2019). An employee’s job satisfaction depends on things related to their work (Seema & Saini, 2021). An organization reflects the performance of its employees. Organization and employee performance are fundamental things that are very important to be able to adapt and create competitive advantages (Khtatbeh et al., 2020). Almost all organizations want to be a good organization. Optimal employee performance in an organization can be achieved if the organization can manage its employees to become reliable personnel (Eliyana et al., 2019). A good organization is reflected in the good performance of its employees. An effective workplace and management processes play an important role in increasing employee productivity, thereby improving organizational performance. One of the factors that influences employee performance is job satisfaction. Job satisfaction and performance have a very close relationship (Eliyana et al., 2019). But in reality, many organizations pay little attention to the job satisfaction of their employees. Employees will get job satisfaction if there is stability and stability in their work. Both their career and the world of work (Kader et al., 2021).

Hypothesis Development

Perceived behavioral control with taxpayer compliance. The higher the perceived behavioral control, the higher the taxpayer compliance. Behavior control is formed from individual beliefs whether or not there are factors that support or hinder the emergence of behavioral behavior. Perceived behavioral control is external control that influences taxpayer behavior to comply with applied tax controls. The stronger the perception of a taxpayer on the applied tax control, the more obedient the taxpayer will behave toward taxes. Behavioral control describes an individual’s ability to perform behavior. Behavior control is also determined by the individual’s past experiences and individual estimates of how difficult or easy it is to carry out a behavior (Oktaviani, 2017). The results of this study show that taxpayers have a high perception of behavioral control over taxpayer compliance so that it can be resolved that the taxpayer’s belief in the government’s preventive and repressive actions is good enough to be able to support taxpayer compliance behavior.

Perceived behavioral control influences taxpayer intentions (Sulistianingtyas et al., 2018). Intention has a positive effect on adherence. The stronger the obligatory intention to comply with tax provisions, the taxpayer will try to realize this compliant behavior (Nurwanah et al., 2018).

The level of income (compensation) of a person can affect compliance in implementing legal provisions and tax obligations. The better the level of reason for the taxpayer, the greater the compliance of the taxpayer in carrying out his obligations (Widia & Yasa, 2021). This is proven by research conducted by Syah and Krisdiyawati (2017) stating that income levels have a significant effect on taxpayer compliance:

H1: The effect of perceived behavioral control on intentions.

H2: Effect of compensation on intention.

H3: The effect of intention on tax compliance.

The executives will analyze the consequences of an action with the aim of getting the best decision, including in determining corporate tax avoidance decisions. Executives make decisions based on available information. In addition, the existence of alternative choices and control that the executive has in the decision-making process makes the theory of reasoned action increasingly explain the reasons for executive risk preferences. The theory of reasoned action assumes that humans act consciously, consider all information, and consider the implicit and specific consequences of the actions taken (Utari & Supadmi, 2017). Counterproductive work behavior is a characteristic that harms the organization and the people in it.

Compensation Justice is a part of Organizational Justice that does not have a negative impact on Counterproductive Work behavior (Wu et al., 2016), especially in terms of providing fair prices to workers according to the contribution made to the organization.

Job Satisfaction influences Counterproductive Work Behavior. This is demonstrated by research conducted by Nemteanu and Dabija (2021) which shows that job satisfaction has a negative and significant effect on counterproductive work behavior, although the intensity is not too great. Job satisfaction is an individual’s general attitude toward the work they do. So Job Satisfaction is a positive feeling toward a job resulting from an evaluation of its characteristics (Robbins & Judge, 2016). Job satisfaction is an important target in human resource management because it affects worker performance and productivity.

Counterproductive behavior is employee behavior that goes against significant organizational norms so that it can affect the member organization and both (Tuna et al., 2016). Cahyani (2016) Counterproductive behavior in the workplace is behavior displayed by each individual in the form of unforgivable badness or fatal badness which can cause harm to the organization, members or both. Job satisfaction is a feeling of happiness that an employee feels because of the results of the work he has done so far. The relationship between job satisfaction and counterproductive behavior can be seen from salary. If the salary received does not match the work performed, the employee is accused of carrying out negative actions.

Compliance is a powerful trigger for individuals. Compliance is an essential element that is important for the formation of an orderly and orderly society. The complexity of tax regulations is also another challenge that must be faced. Harbolt (2019) argues that this can increase the potential for tax avoidance.

H4: Effect of manager’s compensation on Counterproductive Work Behavior.

H5: There is a mediating role from Job Satisfaction in the effect of Counterproductive Work Behavior on Tax Compliance.

Research Method

The population in this research is corporate taxpayers in West Java Province, especially those registered at the Bandung Central Tax Service Office, namely 423 companies. Corporate taxpayers were chosen as respondents because they carry out all their tax obligations. The sampling technique in this research used stratified random sampling. The selection of cities as samples used simple random sampling. Data collection in this research used a questionnaire. The questionnaire distributed to respondents consisted of closed questions based on the variables, dimensions and indicators of the research questions required and given answer choices in the form of a Likert scale Sugiyono (2018, p. 152). Next, the respondent will determine the answer independently according to their perception, attitude or opinion regarding the question at hand.

Out of the 423 questionnaires distributed, there are 236 (55.79%) questionnaires were returned and could be processed. This was because 108 questionnaires were not returned and the questionnaires could not be processed (79 questionnaires).

This research was analyzed using Structural Equation Modeling (SEM) using Lisrel. The aim of using SEM is to estimate a structural model based on strong theoretical studies by examining causal relationships between constructs or latent variables, as well as measuring the feasibility of the model, and confirming it based on empirical data. The consequence of using SEM is that it requires a strong theoretical basis, satisfies the fit test, uses reflective indicators, small indicator complexity (<100), and sample size above 100 (Andryani & Rahayu, 2021).

The analysis model is defined as a simple description of the relationship between one variable and another (Supomo & Indriantoro, 2020). Based on the existing descriptions, the analytical model that will be used in this study is as shown in Figure 1.

Research analysis model.

Results and Discussion

Descriptive Statistics

Of the 423 questionnaires distributed, 236 (55.79%) returned questionnaires that could be processed. This was due to 108 questionnaires that were not returned and questionnaires that could not be processed (79 questionnaires). Most of the sample had an Postgraduate were 36 respondents (15.25%), while those with an undergraduate education were 183 respondents (77.54%), Bachelor’s degree/applied bachelor’s degree graduates were 14 respondents (5.93%) and 3 high school graduates respondents (1.27%).

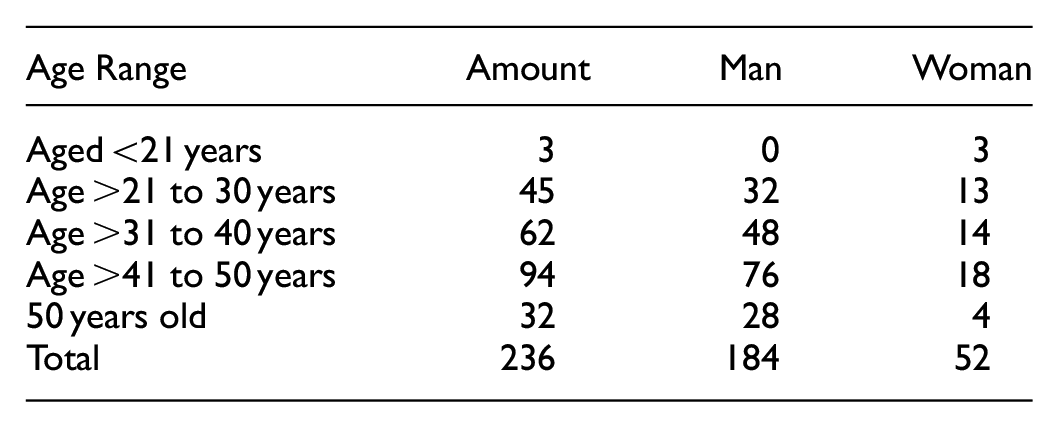

Respondent profile data based on age can be seen in the table below.

From the table above it can be seen that out of a total of 236 respondents, there were 52 women or 22.03% and 184 men or 77.97%. The age range of respondents who were under 21 years old was three male respondents. The age range of respondents aged between 21 and 30 years total 45 respondents consisting of 32 men and 13 women. For those aged between 41 and 50 years, all were men with a total of 94 respondents or 29.83%, which was the age group with the most respondents in the study. Furthermore, the respondent’s profile data based on assignment or position can be seen in the table below.

From the table above it can be seen that the profile of respondents seen from the assignment that the most assignments as company managers were 186 or 78.81% which were represented by 152 men and 34 women. Whereas for the assignment of the head of tax division there were 50 or 21.19% of respondents consisting of 32 men or 13.55% and 18 women or 7.62%.

In general, these companies have formal accounting information systems that enable tax professionals (managers) to prepare their corporate tax reports and research sites apply modern tax fees using information technology systems to improve tax compliance. Thus the majority of respondents carry out tax obligations.

Validity and Reliability Test

Validity and reliability testing was carried out to measure whether the questions used to measure indicators in the questionnaire met the statistical requirements or not. To see the test results can be seen in the Table 1 below.

Questionnaire Data Reliability Test Results.

Source. Results Processed by Researchers, 2023.

Based on Table 1 above, overall the observed variables or questions in the questionnaire have a Cronbach’s Alpha value above .821 which indicates that these results have fairly good reliability. This is in line with Sekaran & Roger (2017) who stated Cronbach’s Alpha as a reliability coefficient which indicates how good the correlation and consistency of reliability is which indicates how good the correlation and consistency between items is. The value of Cronbach’s Alpha is getting better the closer it is to 1.

To see the validity of each item using Confirmatory Factor Analysis (CFA). The minimum required Reliability value is 0.700 and the required variance extracted value is 0.50 (Ghozali, 2017). Apart from that, the loading value of each indicator is 0.50. The validity of each item can be seen in the description of Table 2 below.

Validity and Reliability.

Source. Results Processed by Researchers, 2023.

From Table 2 above, it can be explained that each variable tested has several indicators. The Perception of behavior Control (PBC) variable consists of six indicators PBC_1 to PBC_6. Compensation variable (C) consists of nine indicators C_1 to C_9. The Intention ((IN) variable consists of three indicators IN_1 to IN_3. The Counterproductive work behavior (CWB) variable consists of eight indicators CWB_1 to CWB_8. The Job Satisfaction (JS) variable consists of three indicators JS_1 to JS_3. Finally, the Tax Compliance (TC) variable consists of eight indicators TC_1 to TC_8.

The test results of the variables through the indicators can be explained; First, the Variable Perception of Behavior Control has three valid indicators; PBC_1, PBC_2, and PBC_6. These three items are valid because they have an SLF value greater than 0.50. The Construct Reliability (CR) value obtained was 0.76 which was greater than 0.70 and the Variance Extracted (VE) value obtained was 0.51 which was greater than 0.50. Based on these results, it is concluded that the Perception of Behavior Control Variable has met the criteria of Validity and Reliability with three valid indicators.

Second, the compensation variable has six valid indicators; C_2, C_4, C_5, C_6, C_7 and C_9. The six items are valid because they have an SLF value greater than 0.50. The Construct Reliability (CR) value obtained was 0.94 which was greater than 0.70 and the Variance Extracted (VE) value obtained was 0.74 which was greater than 0.50. Based on these results, it is concluded that the Compensation Variable has met the criteria of Validity and Reliability with six valid indicators.

Third, the Intention Variable has three valid indicators; IN_1, IN_2, and IN_3. These three items are valid because they have an SLF value greater than 0.50. The Construct Reliability (CR) value obtained was 0.90 which was greater than 0.70 and the Variance Extracted (VE) value obtained was 0.75 which was greater than 0.50. Based on these results it is concluded that the Intention Variable has met the criteria of Validity and Reliability with three valid indicators.

Fourth, the Variable Counterproductive Work Behavior has eight valid indicators; CWB_1, CWB_2, CWB_3, CWB_4, CWB_5, CWB_6, CWB_7, and CWB_8. The eight items are valid because they have an SLF value greater than 0.50. The Construct Reliability (CR) value obtained was 0.96 which was greater than 0.70 and the Variance Extracted (VE) value obtained was 0.73 which was greater than 0.50. Based on these results, it is concluded that the Counterproductive Work Behavior Variable has met the criteria of Validity and Reliability with eight valid indicator items.

Fifth, the Job of Satisfaction Variable has three valid indicators; JS_1, JS_2, and JS_3. These three items are valid because they have an SLF value greater than 0.50. The Construct Reliability (CR) value obtained was 0.82 which was greater than 0.70 and the Variance Extracted (VE) value obtained was 0.60 which was greater than 0.50. Based on these results, it is concluded that the Variable Job of Satisfaction has met the criteria of Validity and Reliability with three valid indicators.

Sixth, the Tax Compliance Variable has six valid indicators; TC_3, TC_4, TC_5, TC_6, TC_7 and TC_8. The six items are valid because they have an SLF value greater than 0.50. The Construct Reliability (CR) value obtained was 0.96 which was greater than 0.70 and the Variance Extracted (VE) value obtained was 0.80 which was greater than 0.50. Based on these results, it is concluded that the Tax Compliance Variable has met the criteria of Validity and Reliability with six valid indicators.

Structural Equation Modeling

Overall Model Testing

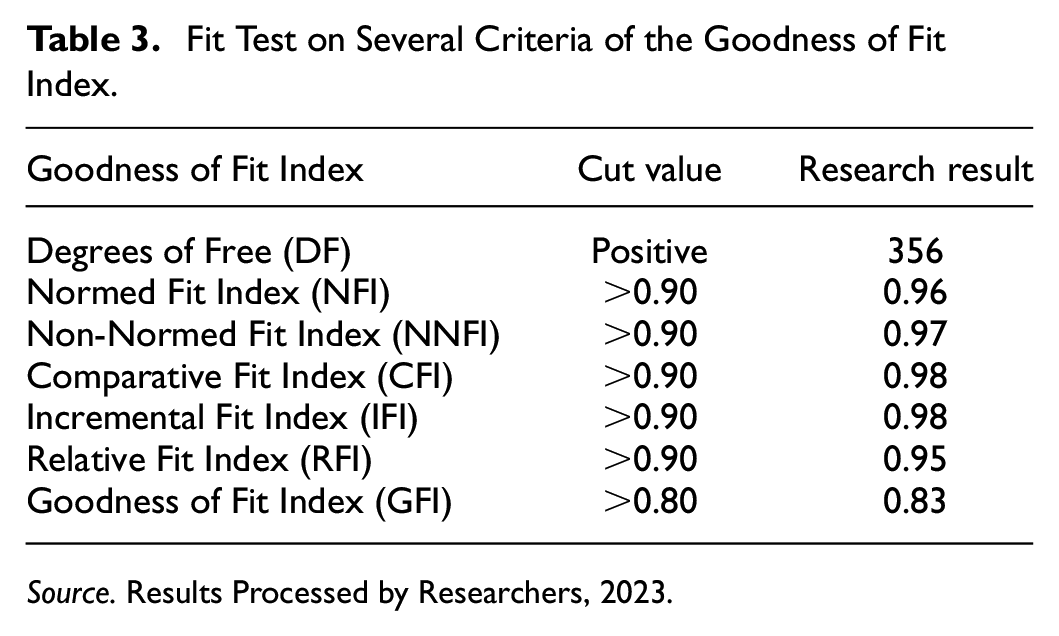

Based on the output of the SEM analysis using LISREL 8.54 software, these values are used as a reference in the overall model. Testing the suitability of the all model is based on the Goodness of Fit measure compiled by Rahmad and Suhardi (2019). Based on the table below, it can be concluded that the overall model is fit. In other words, all variables meet the criteria and the degree of suitability of the measurement model is good (good-fit). So it can be concluded that the overall content model has a high fit between all latent variables and all observed variables (used). This conclusion can be seen from the following Table 3.

Fit Test on Several Criteria of the Goodness of Fit Index.

Source. Results Processed by Researchers, 2023.

The measurement model is estimated and calculated by determining the setting value, namely the initial weight. The initial weight uses a value of 1 for all latent constructs suggested by Hair et al. (2017) and in testing the measurement model it is carried out through a path weighting scheme and stopping criteria which is carried out in testing the measurement model. The measurement model test results show the loading values (indicators) of the latent construct values and exogenous construct values through the Goodness of Fit (GoF) criteria consisting of DF, NFI, NNFI, CFI, IFI, and RFI.

The Goodness of Fit coefficient above shows that there is a fit model with a good level of suitability. The required GFI is obtained close to 1. The NNFI value of 0.96 (a value greater than 0.90) indicates a good-fit model. The higher the NNFI value or the value closer to 1, the better the model. Based on the coefficient values above which meet the fit requirements of a model, it can be concluded that in general, the model obtained has a good level of fit.

Individual Path Testing—Measurement Model

After carrying out overall testing, the next step is to carry out individual testing, namely seeing whether all the hypothesized paths have a good level of significance or not. To find out whether each path has a high level of significance or not, it is done by looking at the t-count obtained. A path is said to be significant if the t value for that path is greater than 1.96. The following data table and diagram (shown in Figure 2) contain the Standard Solution and T-Value values and for all path coefficients.

Standardized solution.

In general, the SEM model obtained met good criteria, namely NFI, NNFI, CFI, IFI, and RFI values greater than 0.90; and the GFI and AGFI values are greater than 0.80 so that based on these GoF points, the model can be declared fit. The summary of the T-values and p-values results can be seen in the Table 4 below.

Loading Factor and Calculated T Value.

From the figure and Table 4 above it can be seen that all hypothesized paths have t-counts greater than 1.96 and p-values below .05 so it can be concluded that all path coefficients are significant.

Individual-Structural Model Path Testing

For individual path testing, each variable can be seen from the T-value of each variable. The T-value of each variable can be seen in the Table 5 below.

T-Value and Significance.

Source. Results Processed by Researchers, 2023.

Discussion

In the test results table above, it can be seen that H1 is supported by a positive coefficient. The Perceive of Behavior Control variable has a significant positive effect on intention to obey. This means that the higher the Perceive of Behavior Control regarding tax compliance, the higher the Perceive of Behavior Control will increase the taxpayer’s intention to comply. The influence of Perceived Behavior Control on Intentions in this research is also found in poetry by Damayanti et al. (2016), Harinurdin (2018) and Taing and Chang (2021).

The test results obtained empirical evidence that supports H2. The relationship value obtained is 0.65, in other words there is a positive influence of 0.652 = 42.25% given the reason for the intention. The existence of a significant causal influence between compensation and compliance intentions in this research also strengthens the findings of previous research, namely Indrady (2018), Sulistianingtyas et al. (2018), and Nurwanah et al. (2018).

The next test results obtained empirical evidence that supports H3. Intentions have a significant effect on tax compliance. The relationship value obtained is 0.35, in other words there is a positive influence of 0.352 = 12.25% Intention toward Taxpayer Compliance. The significant influence of intention on taxpayer compliance in this research also strengthens the findings of previous research, namely Damayanti et al. (2015) and Oktaviani (2017).

Several studies have been conducted to obtain empirical evidence that perceived behavioral control and compensation influence the intention to comply. In addition, perceived behavioral control and intention to comply influence tax compliance behavior.

The current research also obtained empirical evidence that is consistent with previous studies. Thus, it can be concluded that perceived behavioral control and compensation are determining factors in compliance intentions. Intention to comply is a determining factor in tax compliance behavior.

The next test results obtained empirical evidence that H4 was supported by a negative coefficient. Compensation has a significant effect on counterproductive work behavior. The relationship value obtained is −0.16, in other words there is a negative influence of 0.162 = 2.56% which is caused by reasons for counterproductive work behavior. There is a significant causative influence on Counterproductive Work Behavior according to the findings of Wu et al. (2016), Tuna et al. (2016), and Cahyani (2016).

The next test results obtained empirical evidence that H5 was also supported by a negative coefficient. The relationship values obtained were −0.26 and 0.66, in other words, there was a negative influence of 0.26 × 0.66 = 17.16% given Counterproductive Work Behavior on Compliance through Job Satisfaction. The significant influence of Tax Compliance on Counterproductive Work Behavior mediated by Job Satisfaction is also supported by the research results of Purnamasari et al. (2016), Harbolt (2019), and Kan et al. (2020).

This research shows that the respondents in this study were mostly compliance-oriented. This is stated by the results of previous research, namely a condition where job satisfaction in Indonesia is oriented. The impact of job satisfaction is realistic optimism, and low avoidance of non-compliance. This is thought to cause compliance to be supported by job satisfaction as a moderating variable.

The research results show that the role of compensation still has a higher level of emphasis compared to other variables. This shows that taxpayer compliance for medium-sized companies in Indonesia is still dominated by compensation through intention. The existence of counterproductive work behavior also increases tax compliance.

Medium-scale companies relatively have a tax control framework for managing corporate tax compliance. In an indirect relationship, job satisfaction is present to minimize the risk of counterproductive work behavior faced by companies in managing corporate taxes. Job satisfaction mediates the influence of counterproductive work behavior on tax compliance, meaning that job satisfaction to minimize the risk of counterproductive work behavior of managers (agents) has a significant effect on the tax compliance variable, this shows that the problem of job satisfaction still has a significant effect on tax compliance. As seen from Table 5, compensation and counterproductive work behavior have the most dominant influence in influencing tax compliance compared to other variables. It can be said that compensation and counterproductive work behavior are the things that are most dominantly felt by managers (agents) of medium-scale taxpayers in Indonesia.

The current research also obtained empirical evidence that is consistent with previous studies. Thus, it can be concluded that perceptions of behavioral control and compensation on intention to comply and job satisfaction are moderating variables in strengthening the influence of intention to comply on tax compliance behavior.

Conclusion

The results of this study empirically show that perceived behavioral control and compensation influence the intention to comply. Taxpayers who have a more positive perception of behavioral control over tax compliance, have the perception that there is pressure on tax compliance, have a higher perception of behavioral control, will have a higher intention to comply. This research also proves empirically that compensation variables and counterproductive work behavior are higher than others. Behavioral control influences taxpayer compliance behavior in West Java.

In addition, this research also shows empirically that behavioral control and compensation for tax compliance strengthen the influence of intention to comply and tax compliance. Empirical evidence shows that taxpayers with high behavioral control and compensation can strengthen the influence of compliance intentions on tax compliance behavior. Empirical tests on Corporate Taxpayers in West Java in this research can prove empirically that behavioral control and compensation strengthen the influence of intentions on taxpayer compliance. This is thought to be due to the job satisfaction of taxpayers in West Java.

This research provides recommendations regarding the importance of the intention to comply in creating tax compliance. Intention to comply is determined by perceived behavioral control and compensation. The results of this research can be used by tax officers to pay more attention to taxpayers’ compliant intentions. The finding that job satisfaction with tax compliance is a moderating variable for counterproductive work behavior for compliance and tax compliance behavior can be used by tax officers to increase taxpayers’ confidence that the tax administration system has been carried out well, and taxpayers are not made into disadvantaged parties. The existing tax system is able to improve the economy and all state revenues have been used for state development and are free from tax avoidance efforts so taxpayers must be given confidence in this.

Providing a job satisfaction orientation that can be proven as a moderating variable in this research, encourages the importance of further achievement of the work satisfaction orientation measurement instrument. Thus, future research should be able to reconstruct questions to measure job satisfaction orientation.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported and funded by the Directorate of Research and Development, University of Indonesia under the 2022 PUTI Grant (Grant No. NKB-1491/UN2.RST/HKP.05.00/2022).

Data Availability Statement

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.