Abstract

This paper aims to empirically examine whether foreign experienced CFOs (FCFOs) affect financial reporting quality (FRQ). Analyzing Chinese listed firms from 2005 to 2018, this study employs methods such as ordinary least square, fixed effect model (FEM), generalized method of moment (GMM), two-stage least square (2SLS), propensity score matching method (PSM), and change analysis to find the relationship between FCFOs and FRQ. The results show that FCFOs significantly positively impact FRQ, which means that FCFOs improve FRQ in Chinese firms. We argue that international experience imprints CFO cognition, elevates his moral standards, and makes him more transparent in dealings, leading to a better information environment and robust corporate governance mechanism. In addition, this study indicates that the relationship between FCFOs and FRQ is significant in non-state-owned enterprises (NSOEs), suggesting that NSOEs outperform state-owned enterprises (SOEs) in terms of FRQ. Finally, we find that both foreign work and study experiences of CFOs affect FRQ. The findings suggest that asymmetric information problems can be alleviated by encouraging foreign experienced individuals to the firm’s CFO position. The study provides empirical evidence that a CFO’s foreign experience determines a firm’s FRQ.

Plain language summary

Purpose – This paper aims to empirically examine whether foreign experienced CFOs (FCFOs) affect financial reporting quality (FRQ). Design/methodology/approach – Analyzing Chinese listed firms from 2005 to 2018, this study employs methods such as ordinary least square, fixed effect model (FEM), generalized method of moment (GMM), two-stage least square (2SLS), propensity score matching method (PSM), and change analysis to find the relationship between FCFOs and FRQ. Findings – The results show that FCFOs significantly positively impact FRQ, which means that FCFOs improve FRQ in Chinese firms. We argue that international experience imprints CFO cognition, elevates his moral standards, and makes him more transparent in dealings, leading to a better information environment and robust corporate governance mechanism. In addition, this study indicates that the relationship between FCFOs and FRQ is significant in non-state-owned enterprises (NSOEs), suggesting that NSOEs outperform state-owned enterprises (SOEs) in terms of FRQ. Finally, we find that both foreign work and study experiences of CFOs affect FRQ. Practical implications – The findings suggest that asymmetric information problems can be alleviated by encouraging foreign experienced individuals to the firm’s CFO position. Originality/value – The study provides empirical evidence that a CFO’s foreign experience determines a firm’s FRQ.

Introduction

Upper echelon theory stipulates that top management team members’ personality traits significantly contribute to the firm’s outcomes (Hambrick & Mason, 1984). They use their cogitations to assess situations, process information, and make strategic decisions. Extant literature highlights various attributes such as gender, age, education, and experience of top management team members that affect their decisions (White & Borgholthaus, 2022). Chief financial officer (CFOs hereafter) belongs to the firm’s top executive cadre, are primarily responsible for financial reporting, and are viewed as a watchdog for its quality (Bishop et al., 2017; Sun et al., 2019). Several attributes of a CFO’s personality play a significant role in financial reporting quality (FRQ hereafter), such as their risk preferences (Chava & Purnanandam, 2010), gender (J. Liao et al., 2019), and financial expertise (Aier et al., 2005). However, a new phenomenon emerged in China, with the return of an increasing number of Chinese individuals with foreign education and experience in the last two decades; firms are hiring CFOs with foreign qualifications and/or work experience. One important reason is that Chinese firms face an acute shortage of executives that can effectively perform in international settings (Farrell & Grant, 2005). The scarcity of foreign executives in the local labor market impedes all firms to attract foreign experienced individuals to the corporate top cadre. Therefore, the demand for foreign executives, including foreign CFOs, is high. Secondly, almost all provincial governments of the country have incentivized the return of highly skilled workers from abroad (Giannetti et al., 2015). The introduction of attractive policies for foreign experienced workers led to an exogenous change in the supply of potential CFOs with foreign experience. But, existing literature lacks empirical evidence of whether foreign-experienced CFOs (FCFOs hereafter) contribute to firms’ FRQ in China settings. This study aims to fill this gap.

FRQ is a qualitative characteristic of a firm’s financial reporting that shows the accounting reports’ precisions to the current and potential stakeholders (Biddle et al., 2009; Dechow et al., 2010; Dierynck & Verriest, 2020). Literature shows various benefits associated with higher FRQ (Biddle et al., 2009; Dierynck & Verriest, 2020; Houcine, 2017; Tran, 2022). The conceptual framework (International Accounting Standard Board, 2010) also emphasizes higher FRQ by saying that accounting information must be faithfully presented. However, FRQ might be affected by the flexibility in the framework to allow the firm’s management to use their discretion in making specific accounting estimates, such as depreciation and bad debts. Prior studies highlight various characteristics of CFO’s personality, such as gender, age, and education, that significantly contribute to their discretion accrual quality (Aier et al., 2005; Duan et al., 2020; J. Liao et al., 2019; Sun et al., 2019). Likewise, a CFO experience affects a firm’s information environment (Bishop et al., 2017; Muttakin et al., 2019). Similarly, we investigate FCFOs as a promising avenue for a firm’s FRQ. We have several arguments in support of this association. First, FCFOs in Chinese firms have qualifications and/or experience in advanced countries. In developed economies, the stakeholders’ interests are well-protected, and a robust corporate governance mechanism exists. Imprints from early career (e.g., qualification or experience from a particular institution or country) determine one’s cognition and successive behavior. Therefore, the presence of FCFO may improve the firm’s FRQ. This is in line with the imprinting theory (Marquis & Tilcsik, 2013) that suggests “during one or more sensitive periods in a person’s life, a person develops characteristics that reflect prominent features of the environment, and these characteristics persist despite significant environmental changes in subsequent periods.” Second, one’s foreign education and/or work experience enhances his understanding of the situation and helps one better cope with the situation. One’s decisions reflect the knowledge and management practices learned abroad. For instance, prior studies show that managerial foreign experience is positively related to corporate innovations (X. Cao et al., 2022; Yuan & Wen, 2018), analyst forecasts accuracy (Dai et al., 2021), and negatively correlated with corporate fraud (Luo & Wang, 2022). Therefore, we argue that CFO’s foreign experience and/or education will help envisage accurate accounting estimates, which increases FRQ. Finally, extant literature shows that human capital acts as a mobile career of governance (Dai et al., 2018; G. Liao et al., 2022). In emerging economies (e.g., China) the corporate governance mechanism is weaker and CEOs and controlling shareholders significantly influence the CFOs’ reporting judgments and decisions (Bishop et al., 2017; Giannetti et al., 2015). Therefore, an FCFO, with superior knowledge and chief architect of the firm’s accounting policies, will fortify the firm’s corporate oversight, thereby ensuring transparency in its financial reporting. This study, therefore, provides an answer to the question “Do foreign experience and/or qualification of CFO contribute to the firm’s FRQ while controlling firm-specific factors, audit quality, and board-related attributes and CFO’s personality traits”?

We show evidence that FCFOs positively affect the FRQ of Chinese firms, suggesting that CFOs with foreign experience improve a firm’s information environment. The analyses further highlight that the effect of FCFOs on FRQ is more pronounced in non-state-owned enterprises (NSOEs) than in state-owned enterprises (SOEs). Additionally, we find that both CFO’s foreign experience and work experience significantly contribute to the firm’s FRQ. We perform several tests to ensure the robustness of our findings. First, we use alternative FRQ measures and find consistent results. Second, to alleviate the omitted variable problem, we include several additional variables suggested by recent literature in the regression model, and the result remains unchanged. Third, we use the FEM to control problems due to omitting time-invariant firm-specific attributes. Fourth, we use the lag of the independent variable to handle the endogeneity issue. Fifth, we use the GMM approach because this approach offers potential instruments that deal with unobserved heterogeneity, which is essential to mitigate any endogeneity issues. Sixth, we use 2SLS regression to deal with endogeneity issues. Seventh, we also use the PSM approach to handle the endogeneity concerns. Finally, we use change analysis to illustrate the impact of CFOs with foreign experience on FRQ. The results hold robust.

This study contributes to the literature in the following ways. First, we add to the stream of FRQ literature by investigating the FCFOs and FRQ nexus. Though, literature shows that CFO’s personality traits such as age, gender, and experience significantly influence the firm’s FRQ (Aier et al., 2005; Chava & Purnanandam, 2010; J. Liao et al., 2019; Sun et al., 2019). However, the CFO’s foreign education and/or work experience as sources of new knowledge are rarely investigated with the firm’s FRQ. Though, Dauth et al. (2017) analyzed the CFO internationalization and FRQ nexus and reported significant results. However, they studied in a capitalist democratic country, that is, Germany, which has different institutional arrangements than China. Moreover, their findings show that CFO’s nationality does not contribute to the firm’s FRQ, while we find sufficient evidence for Chinese FCFOs. Finally, they analyzed the dataset from 2005 to 2010, whereas our data set consists of 2005 to 2018. Therefore, the results of this study will further clarify the nexus between FCFO and FRQ.

Second, our study provides empirical evidence on FCFO and FRQ relationships from one of the world’s fastest emerging economies, that is, China. Unlike advanced countries, information asymmetry and governance problems are more exacerbated in emerging economies. Furthermore, Chinese firms have different ownership structures, as the government holds a significant portion of the corporate ownership landscape. SOEs pursue different objectives (such as socio-political ones) than NSOEs, which solely work for shareholders’ wealth maximization. This makes the Chinese firms’ financial reports more vulnerable to manipulation. Finally, the Chinese government has introduced attractive policies for talented individuals with foreign experience to return and join local firms (Bishop et al., 2017; Giannetti et al., 2015). Therefore, China sets a peculiar setting for FCFO and FRQ relationship.

Third, we provide empirical evidence on foreign experience as a source of new knowledge. Literature shows a consensus that a firm’s CFO significantly contributes to the corporate FRQ. However, the literature does not examine the extent to which the mapping of economic events is affected by the CFO’s foreign experience. FRQ may go both ways, that is, improve or deteriorate. For instance, on the one hand, foreign experience allows the CFO to offset institutional barriers and improve FRQ. While on the other hand, a new assignment brings new challenges, which may lead to FRQ deterioration. Therefore, this study answers “whether the foreign experience is a determinant of new knowledge.”

The remainder of this paper is as follows. Section “Background and Hypotheses Development” discusses the background and hypotheses development; section “Research Design” shows the research design; section “Results” presents the results; section “Robustness Tests” discusses the robustness of our findings; section “Endogeneity Checks” deals with the endogeneity concerns; Section “Additional Analysis” reports the additional analyses, while section “Conclusion” concludes the study.

Background and Hypotheses Development

Foreign Experienced Executives

Over the last few decades, globalization has significantly boosted global talent’s mobility, which may be viewed as a new medium of knowledge and skills spillover (Liu et al., 2009). Given their superior knowledge learned abroad, foreign talent is considered a precious resource in their home countries, especially in the emerging ones, and often labeled as “brain gain” (Dai et al., 2018; Yuan & Wen, 2018). Previous studies (e.g., Liu et al., 2009; Saxenian, 2005) show that foreign experienced talent provides value to the home country’s businesses and economy by increasing efficiency, knowledge spillover, innovation, and economic development.

Upper echelon theory (Hambrick & Mason, 1984) provides theoretical substance to the foreign experience and significantly impacts the firm’s strategic outcomes. The theory suggests that the background characteristics of top management team members affect strategic decisions and organizational outcomes. Among many factors (e.g., expertise, tenure, education, and gender), foreign experience is an essential factor that significantly influences one’s decisions. In addition, the imprinting perspective advocates that experience (e.g., education or working) during the sensitive period of life shapes one’s cognition and is reflected in his behavior for a more extended period, even substantial changes occurring in the successive period (Marquis & Tilcsik, 2013). Literature shows inconclusive results of the executives’ foreign experience and its effects on the firm. For instance, on the one hand, executives’ foreign experience positively contributes to the firm’s performance (Zhang & Fu, 2020), analysts’ forecast accuracy (Dai et al., 2021), foreign initial public offerings (IPOs) (Duan et al., 2020) and negatively with stock price crash risk (F. Cao et al., 2019) and earning management (Du et al., 2017). On the other hand, some researchers report that foreign experienced managers perform worse (Duan & Hou, 2017; Zhang & Li, 2021).

However, to what extent the executives’ foreign experience influences the firm’s information environment is an interesting question that needs to be answered. Two contrary effects are expected. On the brighter side, foreign experience equip one with superior knowledge and skills and enable one to be more transparent and professional in dealings (Dai et al., 2021; Du et al., 2017; G. Liao et al., 2022). Therefore, the quality of accounting estimates may be more precise in the presence of foreign experienced executives, leading to an improved firm’s information environment. Literature also supports this view and documents that executives’ foreign experience reduces their fraudulent activities (Luo & Wang, 2022), tax avoidance (Wen et al., 2020), information opacity (Li et al., 2016) and improves investment efficiency (Dai et al., 2018). On the darker side, being a novice to the organization, the presence of foreign experienced executives may create challenges that could be detrimental to the firm’s financial reporting quality. Opportunistic perspective and/or fear hypotheses may explain the negative effect. For instance, an opportunistic manager with better knowledge and skills in weaker governance settings may easily manipulate the accounting information in his personal favor. Similarly, according to the fear hypotheses, the foreign experienced executive may lack firm-specific knowledge, which may make them more vulnerable to mistakes and pressure from the local executives, such as the CEO and controlling shareholders to manipulate the accounting information in their favor (Bishop et al., 2017; Giannetti et al., 2015). As a result, the firm’s information environment can deteriorate in the presence of foreign experienced executives.

FRQ

The primary aim of a firm’s financial reporting is to serve as a basis for funds allocation in capital markets. However, the quality of a firm’s reporting is affected by the firm’s fundamentals, such as the business model and its operating environment, and the discretionary reporting choices made by the managers. FRQ is a qualitative attribute of the firm’s financial reporting showing the accounting reports’ precisions to the current and potential stockholders (Dechow et al., 2010; Dierynck & Verriest, 2020). Higher FRQ alleviates agency costs and improves firms’ information environment (Choi et al., 2019; Tran, 2022). Prior studies show various benefits associated with higher FRQ. For instance, higher FRQ is positively associated with a firm’s investment efficiency (Biddle et al., 2009; Houcine, 2017) and negatively with the cost of debt (Muttakin et al., 2020). Likewise, higher FRQ encourages corporate social responsibility reporting quality (Martínez-Ferrero et al., 2015) and discourages tax avoidance (Wen et al., 2020). Therefore, factors contributing to the firm’s FRQ must be explored. Contemporary researchers have investigated financial reporting standards, board-specific attributes, and a firm’s top management personality characteristics concerning the firm’s FRQ. For instance, the studies of Yip and Young (2012) and Brochet et al. (2013) show that mandatory IFRS adoption improves the firm’s financial reporting. Likewise, prior research shows that board size, independence, diversity, directors’ characteristics, and social ties among board members play essential roles in shaping a firm’s financial reporting environment (e.g., Fan et al., 2019; Giannetti et al., 2015; Klein, 2002; Krishnan et al., 2011). Finally, a firm’s CEO and CFO personality attributes, such as gender, age, education, and expertise, significantly influence the firm’s FRQ (Aier et al., 2005; Duan et al., 2020; Faccio et al., 2016; J. Liao et al., 2019; Sun et al., 2019). Therefore, extending the later stream of research, this study empirically investigates whether CFO’s foreign experience and/or qualification affect the firm’s information environment, that is, FRQ.

FCFOs and FRQ

Foreign experience is viewed as additional human capital and a new channel of knowledge spillover. If foreign experienced individuals join the top management cadre in their home country’s corporate settings, the firms’ strategic choices will be affected. The upper echelon theory supports this view. Existing literature also shows various benefits associated with the firm’s top cadre foreign exposure. For instance, managerial foreign experience is positively related to corporate innovation (X. Cao et al., 2022; Yuan & Wen, 2018), investment efficiency (Dai et al., 2018), and negatively associated with tax avoidance (Wen et al., 2020) and information opacity (Li et al., 2016). Consequently, foreign experience is now considered a defining attribute of one’s personality, affecting his decisions.

In the same vein, this study investigates CFOs’ foreign experience, an under-investigated attribute of CFOs literature, and the FRQ nexus in China’s settings. We expect a significant positive impact of FCFOs on the firm’s FRQ. We present several arguments for this association. First, Chinese FCFOs are usually from advanced countries. They spent their formative years in developed economies, which imprints their personality and makes them more transparent in dealings. Further, developed countries’ corporate governance mechanisms are relatively stronger, and shareholders’ interests are well protected. Therefore, experience in advanced countries would have a positive impact on one’s behavior and ethical values. As a result, FRQ may be improved in the presence of FCFOs, which enhances the firm’s information environment and alleviates agency costs.

Second, foreign experience is an additional source of human capital (Dai et al., 2018; Yuan & Wen, 2018). The knowledge gained abroad improves one’s cognitive capabilities, which helps one in solving complex problems and making informed decisions. For example, literature shows that foreign experience increases corporate innovations (X. Cao et al., 2022; Yuan & Wen, 2018) and analyst forecasts accuracy (Dai et al., 2021). As the CFOs’ job consists of a significant portion of making accounting estimates, which determines the FRQ. Therefore, foreign exposure enables CFOs to see the multifaceted understanding of complex scenarios. As a result, FCFOs will have more alternatives when analyzing a situation and making accounting estimates, leading to informed decision-making and quality accruals.

Third, foreign experience at the firm’s upper echelon acts like an internal corporate governance mechanism (G. Liao et al., 2022). Like many other emerging economies, information asymmetry is aggravated in China (Wang & Wu, 2011). The information opacity in the Chinese capital market can be attributed to the concentrated ownership structure of Chinese firms (F. Jiang et al., 2020). A highly concentrated ownership structure encourages entrenched managers to join the club of controlling shareholders. This illicit block holders-managers nexus limits the flow of information to the firm’s other stakeholders, especially non-controlling shareholders. Hiring FCFOs to the firms’ top cadre makes it difficult for the block holders to pressure them because of their high moral standards, cognitive abilities, and distinctive personalities. Consequently, internal corporate governance strengthens, and agency costs mitigate. Finally, prior studies show that human capital may act as a mobile career of governance (Dai et al., 2018; G. Liao et al., 2022). Therefore, the returnee CFO will be a positive addition to the Chinese firm’s internal governance mechanism. Hence, we assume that FCFO would significantly influence the firm’s FRQ.

Research Design

Data and Sample Selection

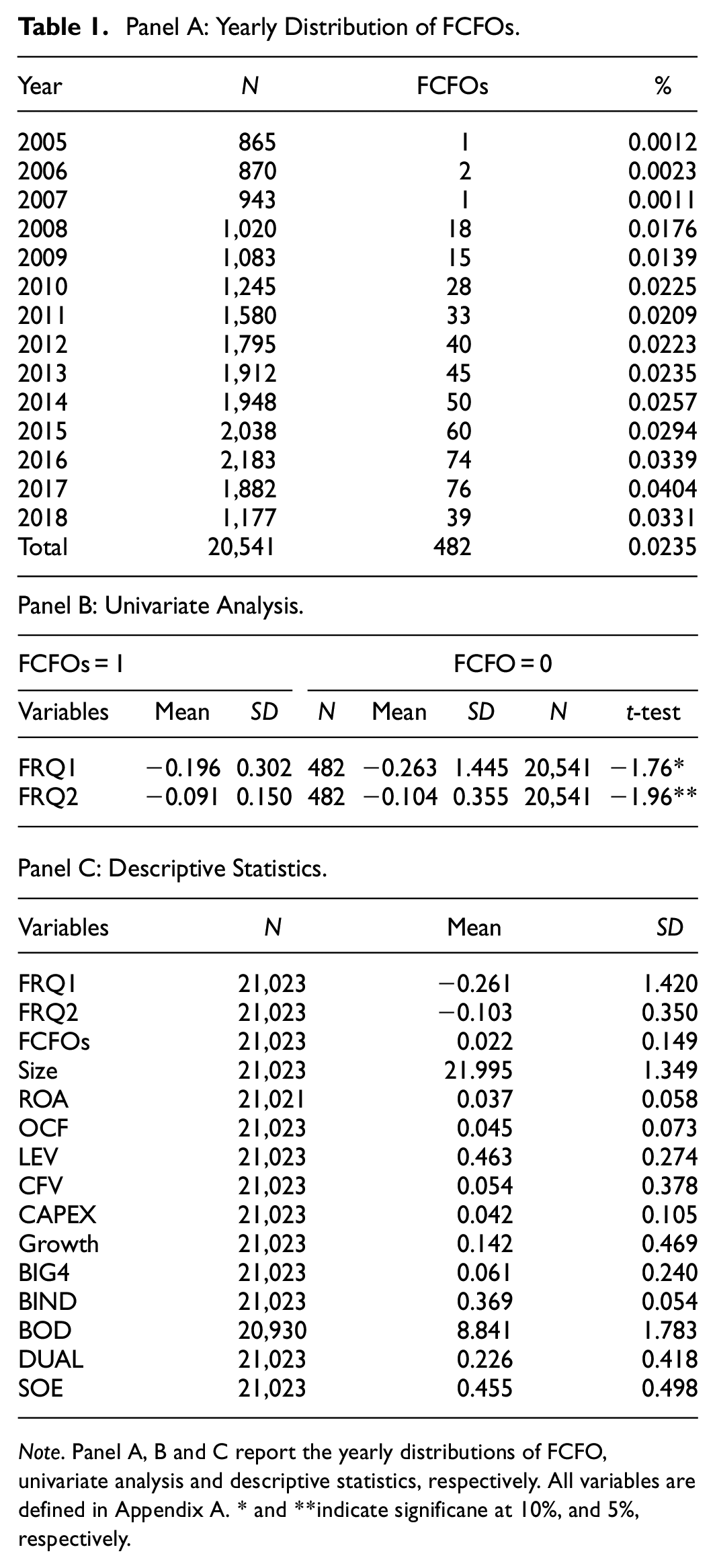

Our initial sample encompasses all Chinese’ A-listed firms listed on Shanghai and Shenzhen Stock Exchanges from 2005 to 2018. Following prior literature (e.g., Yuan & Wen, 2018), we exclude financial, ST, and PT firms. ST and PT represent “special treatment” and “particular treatment” firms. The shares of such firms are omitted due to certain financial issues. Likewise, we eliminate all those firms whose CFOs’ background data is unavailable. Therefore, our final sample consists of 20541 firm-year observations. Panel A of Table 1 shows the year-wise observation of the sample. The data of the concerned variables are collected from China Stock Market and Accounting Research (CSMAR) database. We winsorize our continuous variables set at the 1st and 99th percentile to mitigate the effect of the outlier.

Panel A: Yearly Distribution of FCFOs.

Note. Panel A, B and C report the yearly distributions of FCFO, univariate analysis and descriptive statistics, respectively. All variables are defined in Appendix A. * and **indicate significane at 10%, and 5%, respectively.

Variables

FRQ

We use two different measures for the firm’s FRQ: FRQ1 and FRQ2. FRQ1 is an accrual quality model which measures the manager’s earnings manipulation. However, accruals are often based on estimates and assumptions that, if erroneous, may be rectified in future estimates and accruals. Therefore, we use the accrual model suggested by Dechow and Dichev (2002), which takes into account the adjustment or shift in a firm’s cash flow accruals over time. Furthermore, the model emphasizes working capital accruals and operating cash flows as the initiation and reversal of estimates and accrual in these areas can be precisely tractable within a year. More specifically, the model is as follows:

Our second measure of a firm’s FRQ is FRQ2. Unlike FRQ1, which focuses on working capital accruals, FRQ2 encompasses total accruals. We use it because the total accrual model captures a larger portion of managers’ manipulation and performs better (Dechow et al., 1995). In addition, FRQ2 also considers the managers’ performance matching by adding the lagged profitability term to the model. This measure is proposed by (Kothari et al., 2005) and is as follows;

Where

FCFOs

Following extant literature (Dai et al., 2021; Giannetti et al., 2015; Yuan & Wen, 2018), FCFOs are identified as those with education and/or work experience outside of mainland China. We exclude all CFOs who worked, studied, or lived in Hong Kong, Macau, and Taiwan. We create a dummy variable (FCFOs) that takes the value of 1 if the firm’s CFOs have foreign working and/or studying experiences, otherwise 0.

Empirical Model

To examine the impact of FCFOs on a firm’s FRQ, we estimate the following baseline regression model:

Where

Results

Descriptive and Summary Statistics

Panel A of Table 1 shows the frequency distribution of FCFOs across the years. The results show that FCFOs increase with each passing year, except in 2007. For example, in 2005, the total number of FCFOs was just 1, which jumped to 76 in 2018. Likewise, their percentage also raised from 0.0011 to 0.0331 from 2005 to 2018. Overall, Panel A depicts the rising trends of FCFOs in the study period.

In Panel B, we document the univariate comparison of a firm’s FRQ with FCFOs and without FCFOs. It is evident from the t-test values that the average FRQ1 and FRQ2 values are higher in the FCFOs case, signifying that FCFOs significantly contribute to the firm’s FRQ.

Panel C presents descriptive statistics. The mean values (SD) of FRQ1 and FRQ2 are −0.261 (1.420) and −0.103 (0.350), respectively. The average of FCFOs is 2.2%, which shows that, on average, Chinese firms have approximately 2.2% of CFOs with foreign experience. Regarding control variables, the firms in our sample have an average firm size of 21.995, ROA of 3.7%, OCF of 4.5%, LEV of 46.3%, CFV of 5.4%, and Growth of 14.2%. In addition, the mean (SD) values of BIG4, BIND, BOD, DUAL, and SOE are 0.061 (0.240), 0.369 (0.054), 8.841 (1.783), 0.226 (0.418), and 0.455 (0.498), respectively.

Table 2 shows Pearson’s correlation coefficient. The findings indicate that FCFOs are significantly correlated with all measures of FRQ. These statistics preliminary support our core hypothesis.

Correlation Matrix.

, **, and *, denote p < 1%, 5%, and 10%. Refer to Appendix A for variable definitions.

Effect of FCFOs on Firm’s FRQ

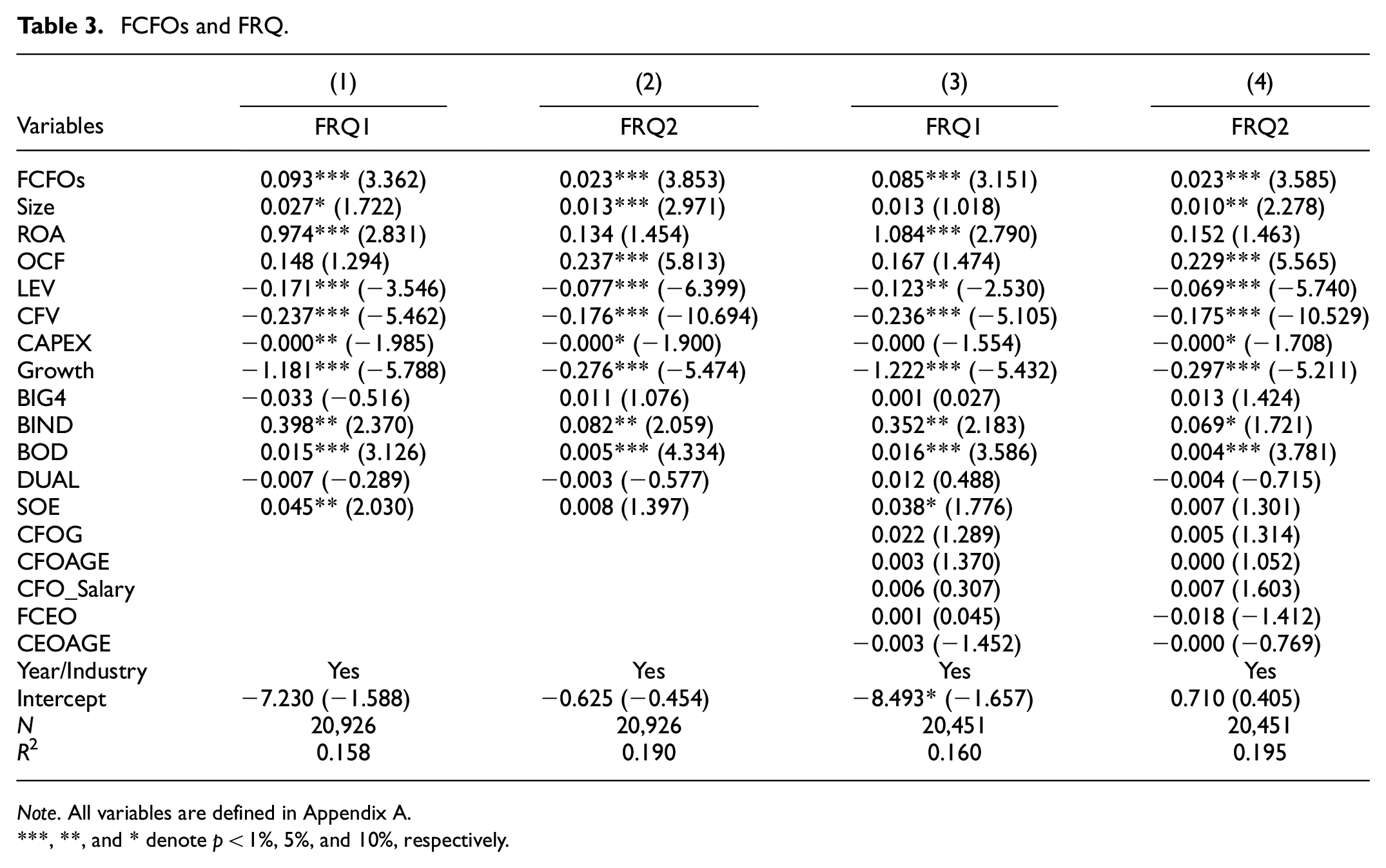

Table 3 reports the results of our baseline regression. Columns (1) and (2) show the estimated results of the FCFO and other variables on the firm’s reporting quality, using FRQ1 and FRQ2 as measures of the firm’s financial reporting quality. The regression models are estimated in the presence of year and industry dummies. Robust standard errors are shown in the parenthesis under the coefficients. It is evident from the results that FCFO has a significant positive influence on the firm’s FRQ. For instance, the coefficients of FRQ1 and FRQ2 are 0.093 and 0.023 in Columns (1) and Column (2), respectively, are significant at a 1% level. In columns (3) and (4), we add a few variables that incorporate the personality attributes of the firm’s two important positions of the firm, that is, CEO and CFO, to the control variables’ set and re-estimate the nexus between FCFOs and FRQ. More specifically, we add the gender of the CFO (CFOG), age of the CFO (CFOAGE), remuneration of the CFO (CFO_Salary), gender of the CEO (CEOG), and age of CEO (CEOAGE) to the variables list and re-estimated the models. The results reported in columns (3) and (4) are consistent with the earlier ones, that is, columns (1) and (2). Furthermore, the impact is also significant economically. For example, the coefficient of FRQ1 in column one (i.e., 0.093) shows that an increase of one standard deviation in FCFO increases the standard deviation of the firm’s financial reporting quality by almost one percent ((0.093*0.149)/1.420). Therefore, we find substantial evidence supporting our hypothesis that CFO’s foreign experience significantly impacts a firm’s FRQ. The results are also in line with the imprinting perspective and earlier studies that consider one’s foreign exposure (i.e., education and/or work experience) as a source of new knowledge and personality development (Dai et al., 2021; Duan et al., 2020; Hao et al., 2021; Wen et al., 2020). However, our findings contradict the results of Dauth et al. (2017), which suggest that CFO’s nationality does not contribute to the firm’s FRQ.

FCFOs and FRQ.

Note. All variables are defined in Appendix A.

, **, and * denote p < 1%, 5%, and 10%, respectively.

Regarding control variables, Size has a significant positive relationship with FRQ, indicating that a larger firm leads to higher FRQ. This aligns with the view that larger firms are more transparent than smaller ones (Dechow & Dichev, 2002). BIND has a significant positive impact on FRQ. This means that an increase in independent directors on the boardroom minimizes information opacity, strengthens the board’s governance mechanism, and mitigates agency conflicts between principals and agents. Similar results are also reported by Bao et al. (2019). We also find a positive relationship between BOD and FRQ. The findings posit that BOD plays a vital role in limiting principal-agent conflicts by mitigating information asymmetries (Jensen & Meckling, 1976). LEV is associated with lower reporting quality, indicating that higher leverage firms manage their earnings to be more appealing to the fund providers. This aligns with the extant literature (Dhole et al., 2020). In addition, CFV, CAPEX, and Growth hurt FRQ and support previous research (Bao et al., 2019). The effect of SOE and ROA is statistically significant in terms of FRQ1 only. Moreover, OCF has no considerable impact on FRQ1 but has a significant positive effect on FRQ2. Finally, we find no significant relationship between BIG4, DUAL, CFOG, CFOAGE, CFO_Salary, FCEO, and CEOAGE with FRQ.

Robustness Tests

To increase the validity of our findings, we employ two robustness tests. First, we use alternative proxies for FRQ. And second, we use an alternative econometric technique, that is, a fixed effect model (FEM).

Alternative Proxies of FRQ

We use two proxies of FRQ for robustness analysis. First, we employ the model proposed by Kasznik (1999), denoted by FRQ3, to calculate FRQ. The model is as follows;

Where

Second, we use the model proposed by Jones (1991) to calculate FRQ (denoted as FRQ4). The model is as follows:

Where

The findings are reported in models (1) and (2) of Table 4. The results are similar to those reported in Table 3. Thus, it is inferred that the proxies of FRQ do not drive our results. Further, we also find that the control variables indicate consistent behavior.

FCFOs and FRQ.

Note. All variables are defined in Appendix A.

, **, and * denote p < 1%, 5%, and 10%, respectively.

Alternative Econometric Technique (Fixed Effect Model):

We use an alternative technique, that is, FEM (Selection is based on the Hausman test), to investigate the association between FCFOs and FRQ. FEM is employed to control for problems that occur due to omitting time-invariant firm-specific attributes that may affect both FRQ and the likelihood of hiring foreign experienced CFOs. The results are reported in models (3) and (4) of Table 4 and are consistent with the previous ones, that is, Table 3.

Endogeneity Checks

In the previous section, we find that FCFOs enhance FRQ; however, statistically identifying the direct influence of FCFOs on FRQ is difficult. In this context, an ideal experimental design will need the random assignment of firms to treatment and control groups, which is improbable and impossible to achieve. In the previous assumptions, the presence of FCFOs is considered exogenous. However, it is likely to be endogenous and depends on the firm’s demand for FCFOs and the willingness of FCFOs to join the firm. We employ five tests to address this issue. First, following prior literature (Wintoki et al., 2012), we use lag of independent variables. Bennouri et al. (2018) and Wintoki et al. (2012) posit that “using a lag of variable is considered a potential tool to reduce endogeneity concerns, particularly in governance research.” Therefore, we take the lag of FCFOs (i.e., LFCFOs) and re-estimate the regressions. Panel A of Table 5 depicts the results. These results are similar to those reported in Table 3.

Endogeneity Checks.

Note. All variables are defined in Appendix A. The t-value are reported in parentheses.

, **, and * denote p < 1%, 5%, and 10%, respectively.

Second, we use GMM to handle endogeneity problems. The GMM approach offers potential instruments that deal with unobserved heterogeneity, which is essential to mitigate endogeneity issues (Wintoki et al., 2012). The results, reported in Panel B of Table 5, show that FCFOs increase FRQ. Thus, our results are not driven by any unobserved heterogeneity.

Third, we employ instrumental variable (IV) regression with a 2SLS estimator. Following X. Jiang and Yuan (2018), and Chen (2015), We use the industry mean of the FCFOs (i.e., IMF) as the IVs. Leary and Roberts (2014) find that listed firms imitate one another’s financial decisions and are significantly affected by the financial decisions of peers in the same industry. Faccio et al. (2016) take the percentage of a firm’s peers with a female CEO as the instrumental variable for firm CEOs. Meanwhile, Ye et al. (2019) use the industry mean of female directors as an instrument variable. Following those studies, we believe that IMF is suitable for this paper’s instrument.

We use FCFOs as a dependent variable in the first stage while treating the other variables and IV (IMF) as independent variables. Then we estimate the “fitted values” of endogenous variables. We then substitute the endogenous variables with the fitted values generated in the first-stage regression in the second stage. The findings, depicted in Panel C of Table 5, confirm that FCFOs increase FRQ. Therefore, we conclude that our main results are robust.

Although we use three important techniques, that is, lag of independent variable, GMM, and 2SLS, to remove endogeneity issues, there is still a possibility that some unobservable heterogeneity may affect our results. To address these issues, we compare firms with FCFOs (treatment firms) to a sample of control firms without FCFOs (control firms) matched on the propensity for a firm to hire foreign experienced CFOs. The benefit of using a control sample matched on propensity scores is that it allows us to attribute any unobserved effect more clearly to the hiring of FCFO rather than to the firm’s attributes linked with hiring FCFOs (Bowen et al., 2010). We re-estimate Equation 3 using the treatment and matched control sample and report the results in Panel D of Table 5. The results show that the coefficients on FCFOs are significantly positive, suggesting that FCFOs enhance FRQ.

Our findings show a significant positive effect of FCFOs on a firm’s FRQ, using both FRQ1 and FRQ2, at 1% level. However, one may argue that firms having higher FRQ in the past could have hired FCFOs. If so, then the causality runs from the opposite side. Following prior studies (Aggarwal et al., 2011; Jebran et al., 2020), we use change analysis to encounter this. Panel E of Table 5 presents the results. The coefficient of ΔFCFOs is positive and statistically significant, suggesting that our results remain valid and support our argument that causality flows from FCFOs to FRQ.

Additional Analyses

FCFOs and FRQ: SOEs and NSOEs

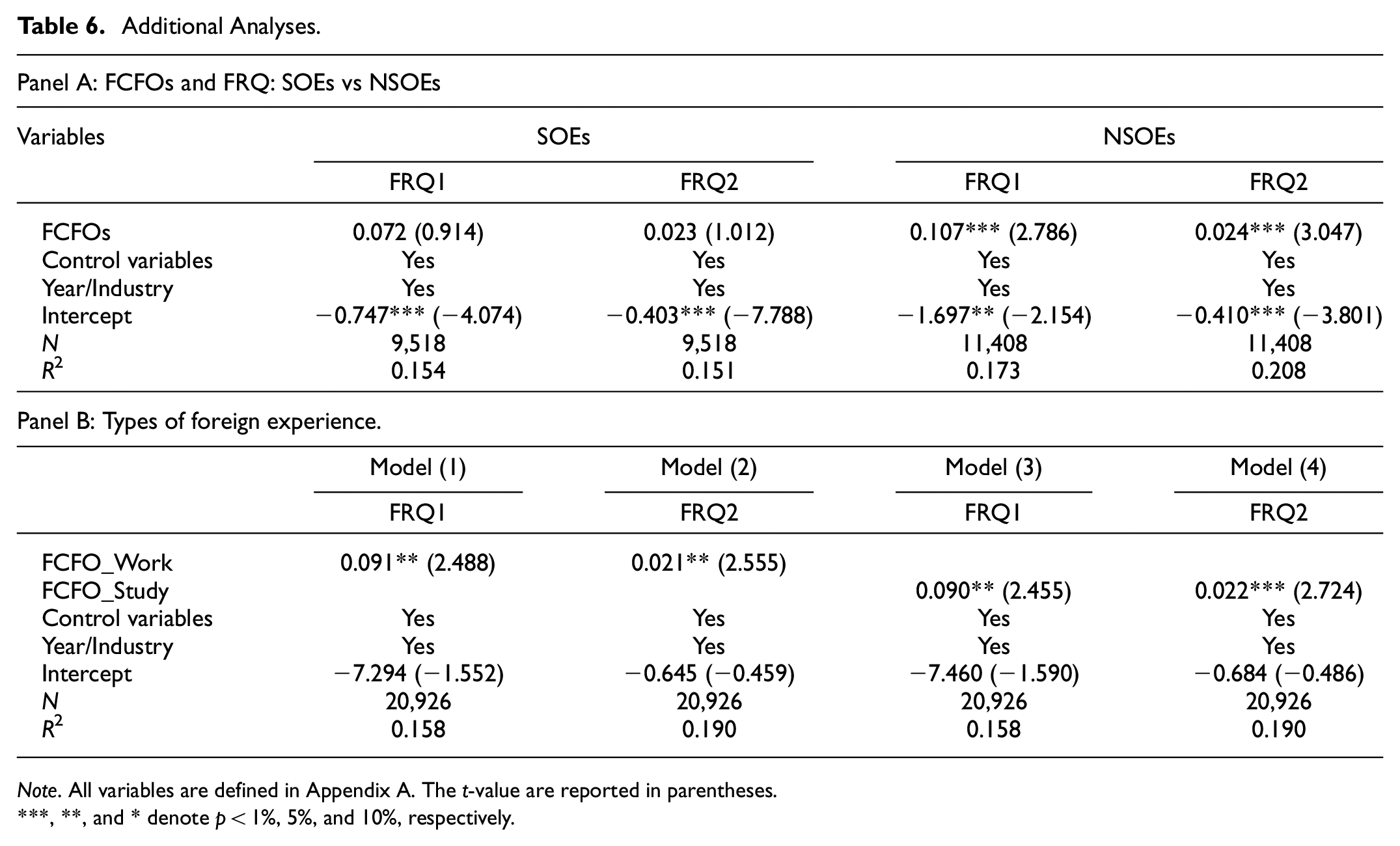

Contrary to developed economies, the corporate ownership landscape is different in China. As an emerging economic giant, the Chinese economy is in transition from command to the free market. However, the government still holds a significant percentage of ownership of various industries. Companies directly controlled by the government may have different objectives, for example, socio-political objectives, than private firms (Faccio, 2006). Further, Chinese government intervention in the firm’s affairs through its nominated persons such as CEO and CFO, tall bureaucratic structure, weak governance mechanism, and lesser financial and career incentives to the CFO make the SOEs more vulnerable to reporting manipulation. While on the hand, companies that come in the orbit of NSOEs solely work for shareholders’ wealth maximization, where the performance of the executives is judged from the financial information provided by the firm’s CFO. Any reporting distortion may hurt the CFO’s integrity and his current and subsequent employability. Therefore, we classify our sample into SOEs and NSOEs to check whether the statistics vary across the two types of firms. Panel A of Table 6 presents significant differences in the statistics of SOEs and NSOEs. More specifically, we document that FCFOs enhance FRQ in NSOEs only. The findings are consistent with the notion that NSOEs outperform SOEs in reporting quality and have better governance mechanisms. Therefore, the impact of FCFOs is more pronounced in NSOEs.

Additional Analyses.

Note. All variables are defined in Appendix A. The t-value are reported in parentheses.

, **, and * denote p < 1%, 5%, and 10%, respectively.

Work Experience Abroad versus Study Abroad

We further examine the positive nexus between FCFOs on FRQ to determine whether it is due to the CFO’s foreign education or foreign work experience. Following earlier studies (Dai et al., 2021; Yuan & Wen, 2018), we consider CFO work experience abroad (i.e., FCFO_Work) a dummy variable that takes the value of 1 if a given firm’s CFO has foreign work experience, and zero otherwise. Panel B of Table 6 reports the results. Models (1) and (2) depict the effect of FCFO_Work on FRQ. The coefficients are positive and statistically significant at the 5% level, indicating that the CFO’s foreign work experience determines FRQ. Likewise, CFO’s foreign education (i.e., FCFO_Study) is also a dummy variable which equals 1 if CFO has completed his education from abroad and zero otherwise. The results reported in models (3) and (4) are positive and significant at 5% and 1%, respectively. Our findings suggest that CFO’s foreign work experience and education significantly contribute to the firm’s FRQ.

Conclusion

This study empirically examines whether FCFOs contribute to the firm’s information environment by improving its financial reporting quality. Chinese firms listed on Shanghai and Shenzhen Stock Exchanges are analyzed from 2005 to 2018. Using the panel data estimation technique, we find substantial evidence supporting that FCFO significantly positively affects the firm’s FRQ. This implies that the firm’s information environment improves and agency costs mitigates in the presence of FCFO. This is in line with the imprinting/upper-echelon perspective. To check the reliability of the results, we use two additional measures of FRQ, that is, FRQ3 and FRQ4, and alternate econometric technique and find consistent results. However, one may argue that more transparent firms appoint FCFOs. To counter this and other endogeneity concerns, we use a battery of econometric techniques to check the reliability of our results. Specifically, this study uses lag of independent variables, 2SLS, PSM, and GMM, to deal with potential endogeneity issues. The results hold robust. In an additional analysis, we show that the effect of FCFOs on FRQ is significant in NSOEs only, suggesting that private firms outperform state-owned firms. This is in line with extant literature. One possible explanation for the insignificant relationships between FCFO and FRQ in SOEs may be due to the lesser independent position of CFO in SOEs and the government intervention in the firm’s affairs. Finally, our findings show that both elements of FCFOs, that is, foreign education and foreign work experience, significantly contribute to the firm’s FRQ.

Our study enriches the literature on the firm’s FRQ by adding a new determinant, that is, FCFO, to its list. We find substantial empirical evidence that a CFO’s foreign exposure acts as a governance mechanism and alleviates information opacity in Chinese firms. Furthermore, our study empirically shows that foreign experience is a source of new knowledge and imprints one’s personality. We also provide empirical evidence on the brain gain effect, suggesting that emerging economies can improve their governance framework by attracting FCFOs to the firms’ top cadre.

The study has important implications for the firm’s current and potential stakeholders. Investors and regulators should encourage FCFOs to the firm’s CFO position to protect their interests, mitigate agency problems and improve the corporate information environment. However, the study’s findings may be a generalization issue as China is an emerging economy with weak governance mechanisms, and mostly, the experience of CFO comes from the developed countries. Secondly, this study does not consider the country of education or the nature of the work experience of FCFOs. Therefore, we encourage future studies to investigate these and other such factors in relation to the firm’s FRQ and to other strategic decisions. Finally, our results show that FCFO significantly impacts. Therefore, factors that cause cross-country variations need to be investigated.

Footnotes

Appendix

Variable Definitions.

| Variable | Definition |

|---|---|

| Panel A: Financial statement comparability variables | |

| FRQ1 | Absolute value of discretionary accruals estimated through (Dechow & Dichev, 2002) model multiply by −1. See section “FRQ” for further explanation. |

| FRQ2 | Absolute value of discretionary accruals derived from Kothari et al. (2005) model multiply by −1. See section “FRQ” for further explanation. |

| Panel B: Board diversity variables | |

| FCFOs | Dummy variable that takes the value of one if the CFOs has foreign working experience or foreign studying experience, and zero otherwise. |

| Panel C: Firms specific control variables | |

| Size | Natural log of the firm’s total assets. |

| ROA | Net income scaled by total assets. |

| OCF | Operating cash flow scaled by total assets. |

| LEV | Total liability divided by total assets. |

| CFV | Standard deviation of quarterly operating cash flows over the year. |

| CAPEX | Capital expenditure scaled by total assets |

| Growth | Equals to sales in current year minus sales in previous year divided by sales in previous year. |

| Panel D: Board characteristics | |

| BIG4 | The indicator variable equals to one if the auditor is from one of the Big 4 auditing firms, and zero otherwise. |

| BIND | Proportion of independent directors on the board. |

| BOD | The number of board of directors on the board. |

| DUAL | Equals to 1 if the CEOs also serve as chairman of the board, and 0 otherwise |

| Panel E: Additional control variables | |

| CFOG | The dummy variable equals to one if the CFO is female, otherwise zero. |

| CFOAGE | The natural logarithm of the age of the CFO. |

| CFO_Salary | Total salary of the CFO. |

| FCEO | The dummy variable equals to one if the CEO is female, otherwise zero. |

| CEOAGE | The natural logarithm of the age of the CEO. |

| Panel D: Variables in additional tests | |

| SOEs | Equals to 1 if the firm is owned by the state, and 0 otherwise. |

| FCFO_Work | Dummy variable that equals to one if the CFOs have foreign work experience, and zero otherwise. |

| FCFO_Study | Dummy variable that equals to one if the CFOs have foreign study experience, and zero otherwise. |

Author’s Note

This research was conducted while Dr. Irfan Ullah was at Dongbei University of Finance and Economics. Dr. Irfan Ullah is currently working as an Associate Professor at Jiangxi Normal University, China. This research was conducted while Dr. Muhammad Arif Khan was at Dalian University of Technology, China. Dr. Muhammad Arif Khan is currently working at Dalian Maritime University, China. We are thankful to Khalil Jebran for many helpful comments on initial draft.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.