Abstract

A public budget consists of financial input for implementing governmental operations. It is generally expected that financial resources will increase organizational performance because they can be used to obtain other types of resources. This study aims to make a theoretical contribution to the punctuated equilibrium theory literature by examining how the different patterns of budget changes affected the competing dimensions of public service performance (3Es: efficiency, effectiveness, and equity) before and after the Myanmar budget reform in 2011. We collected a two-level dataset including budget allocation data at the ministry level and public service providers’ perceptions of performance at the individual level and employed multilevel modeling. Our results show that the effectiveness of public services can be improved by increasing a significant amount of budget allocation (positive punctuations), but this has no effect on efficiency or equity. However, any level of budget reduction can decrease the efficiency and equity of public services.

Keywords

Introduction

The allocation of public funds is crucial for a country’s socioeconomic and multisectoral development and strategic goals, especially in developing countries (Khujamkulov, 2024). In addition to thinking of public budgeting as an annual financial arrangement, such planning has evolved into a multiyear financial and development process. To comply with macroeconomic policies, budgetary actions are also being developed. Governments implement a series of budget reforms with the goal of making public budgetary systems more rational and sustainable (Willoughby, 2014). The most important goal is to effectively manage the finite public budget to successfully implement projects and deliver public services to citizens efficiently, effectively, and equitably.

Incorporating performance information into budget documents is critical for strengthening public bureaucrats’ accountability for outputs and outcomes based on the budget inputs appropriated to them. These performance data can be used to assess how inputs are converted to outputs (efficiency), the level at which stated objectives are achieved (effectiveness), and whether the results of budget allocations are fair (equity) (Oh et al., 2014). This study aims to analyze Myanmar’s budget dynamics and their effect on multiple performances of public service delivery. Several theoretical perspectives assume a positive relationship between financial resources measured as a static concept and organizational performance (Boyne, 2003; Fisher, 2007; Walker et al., 2024; Williamson, 1999). However, a budget is one of the measurements of organizational size, and changes in organizational size have different effects on performance outcomes. Therefore, a budget should be viewed as a dynamic rather than a static aspect (Walker et al., 2024). This study also assumes that budget changes may have different magnitudes and directions and that these different changes lead to different performance outcomes. Therefore, this study makes a theoretical contribution to the punctuated equilibrium theory (PET) literature by defining the different patterns of budget changes (i.e., positive, negative, or no punctuation).

Most previous studies have analyzed the impact of financial resources on the quality of public services without differentiating the dimensions of public service performance (Chen & Flink, 2022; Flink & Molina, 2021). However, the assessment of the performance of public organizations can be approached through various dimensions by incorporating perceptions from different stakeholders and utilizing diverse data sources and types (George et al., 2019). Therefore, this study focuses on diverse aspects of public service performance. That is, the impacts of budget allocation changes on public service delivery are assessed in terms of competing public values such as efficiency, effectiveness, and equity (the 3Es). Based on these assumptions, we aim to analyze the impact of different magnitudes and directions of budget changes on the three competing dimensions of public service performance (the 3Es) in the context of Myanmar.

The Myanmar government has been implementing a fiscal reform process since 2011, including decentralizing the budget process, improving budget transparency, implementing public financial management (PFM) reform, and so on. According to budget decentralization processes, state and regional governments should prepare their own budgets in line with local citizens’ preferences. As different states and regions have different demands and needs, allowing state and regional governments to control public spending to supply local goods and services may lead to improved efficiency, effectiveness, and equity (Shotton et al., 2016). Some scholars have examined Myanmar’s budget system, processes, and procedures and made recommendations for improving them (Deshpande, 2017; Shotton, 2019); others have discussed budget decentralization and the role and budgeting processes of state and regional governments (Dickenson-Jones et al., 2015; Kyaw, 2015; Nixon & Joelene, 2014; Robertson, 2017; Shotton et al., 2016). Still others have provided an overview of and recommendations for the public finance management system (Oo et al., 2015; PEFA, 2020). However, there are only a few empirical studies on the impact of budget allocation on public service delivery performance after the Myanmar budget reform began in 2011. This study intends to fill this gap in the existing PET literature by providing useful information about budget allocation and evaluation. To answer the research question, “Have changes in budget allocation made after the Myanmar budget reform of 2011 improved the efficiency, effectiveness, and equity of public service delivery?,” we examine the annual budget changes in 18 ministries over a 14-year period that includes years before and after the budget reform. Most of the previous public service performance studies have been based on the service recipients’ perceptions and indices that measure the quality of outputs in only a particular sector. However, this study conducted a multilevel analysis based on a two-level dataset using hierarchical linear modeling (HLM). At the ministry level, we used budget allocation data from several ministries, while at the individual level, we used individual public service providers’ perceptions of how the changes in budget allocation caused by the policy change (i.e., budget reform) affected service performance.

The subsequent sections of this study are structured as follows. Section “Budget Changes and Public Service Performance” presents an overview of the existing literature on budget changes and public service performance in terms of efficiency, effectiveness, and equity. Section “Hypotheses” outlines the hypotheses of the study. Section “Data and Methodology” describes the data and methodology utilized in our analysis. Section “Results” offers a discussion of the empirical findings. Lastly, final section concludes with policy implications, research limitations, and suggestions for future research endeavors.

Budget Changes and Public Service Performance

A public budget is critical for providing public services because public organizations cannot function or produce services without it (Willoughby, 2014). Therefore, the budget itself is considered a policy input for delivering efficient and effective public services, which is the basic purpose of governmental operations (Chen & Flink, 2022). As a policy tool, public budgeting allocates a society’s limited financial resources among numerous conflicting interests and competing problems (Wang, 2002). It is also an economic tool used to promote a country’s economic growth and development (Bartle & Shields, 2008). As an administrative tool, a public budget provides the methods and means by which public services are delivered, as well as the criteria used to evaluate and review those services (He, 2011; Lim & Oh, 2016).

According to non-incremental social demands and changes, the budget allocation model reflects a dynamic system that changes from year to year. In the twentieth century, budget decisions were made rationally based on the problems faced by organizations and the potential solutions to those problems (Reddick, 2003). According to Baumgartner and Jones (1993), punctuated equilibrium indicates a transition from stable to unstable conditions, and instability occurs when a stable system is shaken by organized activities (or mobilizations). Budget punctuations can be caused by changes in external circumstances, such as shifting public attention, striking and compelling new information, or changes in policy decision-makers (True et al., 2007, p. 165).

While PET is generally employed within policy agenda-setting contexts to explain the decision-making process and dynamic theoretical aspects, in budgetary decision-making contexts, it is utilized to examine budget dynamics and conduct empirical analyses (Peng & Cao, 2023). Many studies on public budgeting have employed PET to examine and explain the occurrence of budget punctuations across diverse circumstances. For example, studies have investigated budgetary changes in democratic and highly centralized political systems across four distinct countries (Baumgartner et al., 2017), examined Nepalese budget punctuation patterns under various political changes and economic challenges (Guragain & Lim, 2019), analyzed Macao’s budgetary punctuation patterns before and after its transition to Chinese control (Li et al., 2022), discussed how the Eurozone crisis and the pandemic acted as triggers for Italian budget punctuation (Cavalieri, 2023), and extended the PET literature to explore the impacts of political and institutional changes on the directions and frequencies of budget punctuation (Myaing & Lim, 2023). This study also uses PET to examine how the different patterns of budget changes affected public service performance before and after Myanmar’s budget reform.

Resource allocations decided by public authorities that are in line with citizens’ preferences tend to improve the quality of public services (Kahkonen & Lanyi, 2001). Therefore, understanding how organizational performance changes as a result of budget changes is absolutely critical. Generally, an increase in budget is expected to improve organizational productivity and performance (Andersen & Mortensen, 2010; Boyne, 2003; Carpenter, 1996). Some research empirically shows that budget allocation changes have an impact on public organization performance. For instance, Andersen and Mortensen (2010) investigated how resource allocation patterns affected organizational performance. They used multilevel models to assess the impacts of resource stability and incremental changes on student performance by controlling for individual-, school-, and municipal-level variables. According to their findings, budget does matter for performance outcomes, but incremental increases have a more favorable effect on performance outcomes than higher levels of increases. The reason why incrementalism matters in the result is that a long period of incremental budget changes provides schools with more economic security, allowing them to focus on education itself rather than on the economy. Other scholars have extended the PET literature by incorporating the literature on organizational performance to examine how budget changes affect organizational performance. For example, Flink (2018) also examined the effects of different magnitudes of budget changes on organizational performance. She broke down budget changes into five categories: large negative (below −33%), large positive (above 35.5%), medium negative (−33% to −2%), medium positive (10% to 35.5%), and incremental (−2% to 10%) changes. The findings show that different magnitudes of budget changes have different performance outcomes (i.e., large and medium positive budget changes are expected to increase performance achievement by 9% and 12% over small positive budget change, respectively, while large and medium negative budget changes lead to a decrease in performance achievement by approximately 3% and 3.5% over small negative budget changes, respectively). However, performance changes are smaller than budget changes. With negative shocks to budgets, organizations experience only a small decrease in performance. This means that organizations can maintain some consistency in their performance even when their budgets are unstable. However, according to Chen and Flink (2022), large or medium budget increases do not result in significant performance improvements for state transportation agencies since agency managers may not commit all fund increases to the enhancement of road qualities or may just spend the funds on nonproductive events. In previous studies, public performance was mainly assessed based on a singular dimension that typically focused on the output quality of a specific public sector.

Brewer and Selden (2000) proposed an organizational performance measurement in terms of three competing administrative values: efficiency, effectiveness, and fairness. The 3 Es—efficiency, effectiveness, and equity—have been used as critical criteria with which to evaluate the performance of multiple systems, programs, and organizations in diverse contexts. For example, the 3Es have been used to evaluate organizational performance (Davis et al., 2013), assess research impacts (Hinrichs-Krapels & Grant, 2016), monitor the policy development of inclusive education systems (Watkins & Meijer, 2016), and evaluate the system performance of humanitarian logistics location strategies (Liu et al., 2021).

Generally, efficiency is concerned with obtaining the most outputs from inputs (Goddard, 1989; Mamokhere et al., 2022; Muda et al., 2023) or utilizing resources to achieve an organization’s objectives (Daft, 2015). In public service, inputs are easily defined and assessed as budgeting or labor, while the outputs of some public services are difficult to measure, necessitating the use of numerous measurements (Jörden et al., 2024; Savas, 1978). For example, a city’s police department cannot be said to be inefficient because no one has been arrested (i.e., no output in this case) as a result of there being no crime within a jurisdiction during a certain period. Effectiveness refers to obtaining the expected results from the outputs (Mamokhere et al., 2022) and measures how well an organization achieves its own goals or how an organization’s output engages with the economy and society (Daft, 2015; Jörden et al., 2024; Rainey, 2003). It also refers to the degree to which unwanted negative consequences are avoided (Savas, 1978). The effectiveness of public services can be measured by the level of citizen satisfaction (Savas, 1978; Shi et al., 2023) or the successful execution of major public policies or programs (Andrews et al., 2017). Equity is characterized by a distributional principle that aims to achieve an equal allocation of resources, benefits, and public services to all individuals, including underserved groups in society (Andrews et al., 2017; Guo et al., 2017; Swe & Lim, 2019). Moreover, it is crucial to recognize the diverse standards of equity in service provision. While certain services, such as waste collection and water quality, require equal treatment for fairness, other services must be prioritized to address unfair consequences caused by disparities in initial conditions. This includes historical inequities that affect disadvantaged groups such as women, people of color, individuals with disabilities, and others (Mamokhere et al., 2022). However, when the government allocates limited resources for multiple-dimensional public services, there may be trade-offs made among different sectors, groups, or regions (possibly producing winners and losers in a society). Such situations indicate that if one type of public service requires more funding due to urgent economic, policy, or environmental concerns, then allocations for other types of public services will be sacrificed.

While financial resources are a key parameter for predicting performance, there are other parameters that should be considered as well. Caiden and Sundaram (2004) argued that simply increasing budget allocations will not guarantee better development outcomes for target populations in the absence of improved delivery and administration procedures. Boyne (2003) derived five sets of variables for public service improvement, namely, resources, regulation, markets, organization, and management, based on five critical theoretical viewpoints on the sources of improvement. In particular, governance structures are changing along with evolving governance paradigms in the public sector. Harlow (2001) stated that it is no longer possible for central governments to rely on command-and-control tools; instead, they must adopt market-based tools and build strong partnerships with organizations in other sectors. Mauro (2021) discussed the key governance structures in three different paradigms, namely, public administration (PA), new public management (NPM), and new public governance (NPG). In the PA paradigm, hierarchy is a key governance structure. In contrast, the NPM paradigm focuses on marketization or more business-like practices to deliver public services. Finally, the NPG emphasizes that a network developed through collaboration with internal and external stakeholders can enhance the level of responsiveness to citizens’ needs, thereby increasing the efficiency, effectiveness, and equity of public services. Yoo and Kim (2012) discussed these three ideal types of governance modes—hierarchy, market, and network—as service delivery mechanisms. In this study, these three governance modes were considered control variables to determine public service performance.

Hypotheses

Several theoretical perspectives, including economic, voter, and managerial perspectives, support the idea that financial resources and organizational performance have a positive relationship. First, Fisher (2007) stated that public sector theory is inseparable from the body of economic theory and highlighted that the production processes of the government and private sectors are very similar. In the government production process, budget allocation is the main input for producing public services (outputs). Economists also view a budget as a tool for achieving the basic goals of government and society (Khan & Hildreth, 2002). Therefore, from the perspective of the theory of economics, public spending can enhance the outcomes of public services.

Since voters are interested in the final service results provided by public agencies, public spending effectiveness is used to describe the results of public resource utilization (Burkhead & Miner, 2007; Fisher, 2007). To fulfill the demands of voters, governments try to improve public service performance. Therefore, from the voters’ perspective, the utilization of public financial resources is expected to enhance the quality of public services.

In the literature on strategic management, the resource-based view (RBV) is the dominant theory. This theory argues that greater organizational resources can lead to sustainable competitive advantages (S.-Y. Lee & Whitford, 2013; Lim et al., 2017; Lubis, 2022; Wernerfelt, 1984) and have a positive influence on the growth and performance of the firm (Williamson 1999, p. 1098). Public organizations also use a variety of resources, including administrative, human, financial, physical, political, and reputation resources, to achieve their organizational goals and objectives (S.-Y. Lee & Whitford, 2013).

From the perspective of public service improvement, more public spending will increase the quantity and/or quality of public services (Boyne, 2003). Kioko et al. (2011) studied the effect of public financial resources on public services based on two management perspectives, namely, public financial management (PFM) and public administration and management (PAM). According to PFM, the use of public financial resources aims to improve public services by assessing the cost and effectiveness of outputs. According to PAM, the use of public financial resources aims to achieve political gains by offering public services that satisfy citizens’ preferences. In the spirit of NPM, decentralization can enhance the efficiency and effectiveness of public service performance by dividing the duties and responsibilities across different levels of government.

Previous research has examined how financial resources affect public service performance, and their analyses have shown mixed results. For example, in an analysis of educational performance, Wenglinsky (1997) indicated that there is no strong relationship between school expenditure and students’ performance, while Hedges et al. (1994) reported a positive relationship between these factors. S.-Y. Lee and Whitford (2013) examined how organizational resources affect federal agencies’ performance (i.e., the level of goal achievement). Their analysis showed that financial resources have a positive but nonsignificant effect on agencies’ effectiveness. Andersen and Mortensen (2010) and Flink (2018) found that budgetary changes have a positive effect on the effectiveness of organizational performance by focusing on pupils’ standardized test rates or student examination scores. By analyzing data from the public education sector in the United States, Flink and Molina (2021) discovered that increasing spending is associated with improving performance. Xu and Flink (2022) reported that severe budget cuts make minority representation at a managerial level of public schools more difficult and, as a result, reduce organizational performance. Walker et al. (2024) stated that increased resources result in improved services, but effective management is essential to ensure better services. To improve organizational performance, it is obvious that we need to consider several types of resources other than simply increasing financial resources. However, in general, it can be expected that financial resources will increase performance, as financial resources can be used to obtain other types of resources, including human resources, equipment, advertising campaigns, and administrative and technical capacities (Fernandez & Rainey, 2006; Fry et al., 2004).

Since 2011, Myanmar has worked to decentralize its budget to improve government agencies’ level of responsiveness, to increase the quality of its public services, and to better align with residents’ preferences. Moreover, Myanmar has implemented a PFM reform with the aim of improving all aspects of PFM, such as the planning and budgeting processes; budget execution; monitoring, accounting, and reporting systems; and audit and external scrutiny (Oo et al., 2015, p. 35). After 2011, as Myanmar began its transition to democracy, voters’ perspectives became more important in elections. To fulfill the voters’ desires, more efforts were made to spend the public budget more effectively. Since necessary financial management reforms have been implemented, we can expect that these increases in the budget have led to better public services. Moreover, according to the abovementioned theoretical and empirical discussions, we can expect that more financial resources have enhanced outcomes for public services. Therefore, this study hypothesizes that a positive relationship will be found between the utilization of financial resources and public service performance after controlling for other variables such as the public governance modes of hierarchy, market, and network, as proposed in the following hypotheses:

Hypothesis 1: Positive public budget changes are associated with positive changes in the efficiency, effectiveness, and equity of public service delivery.

Hypothesis 2: Negative public budget changes are associated with negative changes in the efficiency, effectiveness, and equity of public service delivery.

Data and Methodology

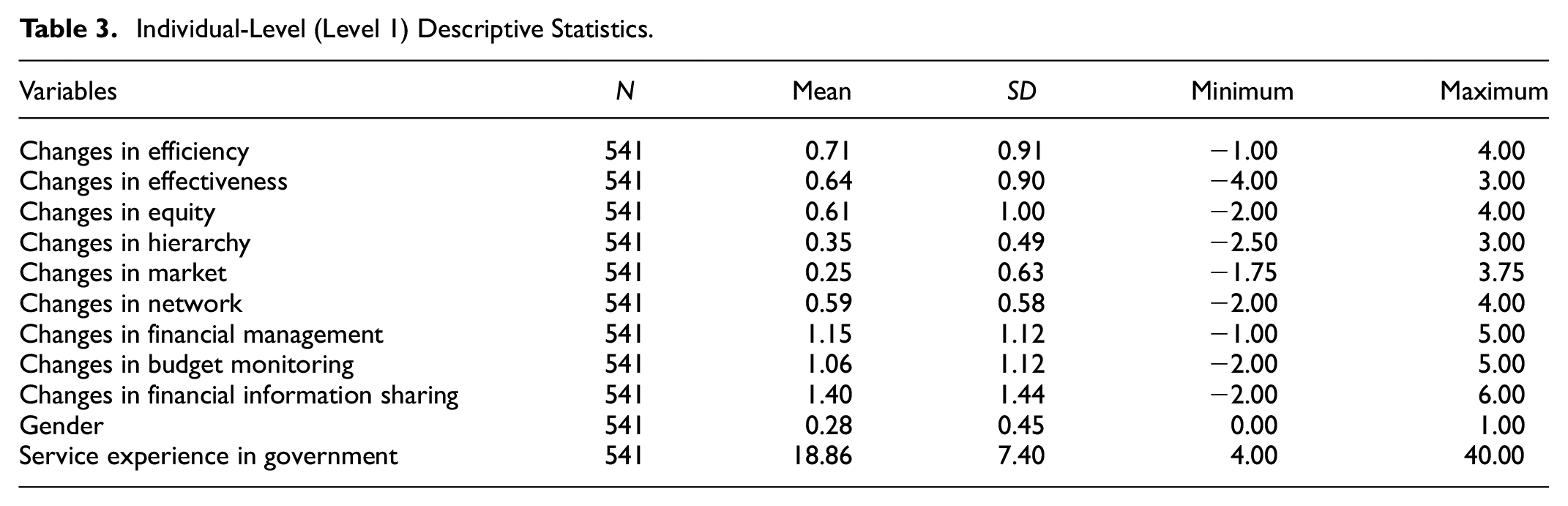

The impact of budget changes on the quality of public services was examined in this study using both hard and soft data. In most previous studies, the performance of public services has been evaluated by various stakeholders, such as consumers, taxpayers, and politicians, using various criteria, including quality, effectiveness, and delivery speed (Boyne, 2003). However, in this study, public service performance was investigated based on the service providers’ perception of their public service quality, as they have more accurate information about the quality of the services that they actually produce and deliver than do service recipients (i.e., citizens) or service evaluators/controllers (i.e., legislators) (Niskanen, 1971; Ohemeng et al., 2018). Data were collected by distributing survey questionnaires to government officials across the ministries to obtain their perception of the quality of their public services. Individuals in the same ministry are highly likely to share similar characteristics, and within-group information cannot be assumed to be independent of observation (Raudenbush & Bryk, 2002). Therefore, a two-level dataset was constructed in this study, involving respondents from different levels (i.e., 18 ministries at the ministry level and 541 public officials at the individual level). For the ministry-level data, this study used the budget allocation data of 18 ministries in Myanmar across 14 fiscal years. For the individual-level data, at least 20 public officers from each ministry were asked about their perceptions of the efficiency, effectiveness, and equity of the public services they deliver on an individual basis. When independent variables are measured at different levels, HLM can be used to investigate the variation in the outcome variables (Chien & Wu, 2020; K. H. Lee et al., 2013; Woltman et al., 2012). HLM provides the unique advantage of examining the associations between the variables measured at different hierarchical levels. The definitions and sources of measurements and the sources of data are summarized in Table 1.

Definitions/Measurements of Variables and the Sources of Measurements/Data.

Ministry-level (level 2) variables.

Regarding the dependent variables, this study focused on the terms of competing public values such as efficiency, effectiveness, and equity of public services provided by 18 Myanmar government ministries to measure the quality of public services. To measure efficiency, this study asked the respondents whether their organization efficiently delivers public services to citizens. To measure effectiveness, it asked whether the public services of the organization meet the needs of citizens. Finally, to measure equity, it asked whether the organization fairly and equally distributes public services to citizens. These outcome variables (3Es) were assessed using a seven-point Likert-type scale (strongly disagree to strongly agree) to score how much the public officers agreed or disagreed with a set of the abovementioned survey items on their organization’s public services.

The major independent variables at the ministry level were determined based on the annual percentage changes in budget appropriated to the ministries. To evaluate the changing budget distribution trends, the dataset included budget allocation data from 18 Myanmar government ministries across 14 fiscal years, that is, 4 years before the budget reform (FY 2001–2002, 2004–2005, 2007–2008, 2010–2011) and 10 years after the budget reform (FY 2011–2012 to 2020–2021). Due to the lack of budget transparency in some years before 2011, we were unable to collect data from consecutive years prior to 2011, which resulted in data from nonconsecutive years. The data were gathered from two sources: state budget regulations (before 2011) and the Myanmar budget dashboard website (after 2011). The following outlines how the study determined annual percentage changes in budget allocation by following Baumgartner and Jones (1993, p. xxii):

where % Δ Bt = the percent change in the current year’s budget allocation over the previous year’s allocations,

Bt = the current year’s budget allocation value, and

Bt−1 = the previous year’s budget allocation value.

We considered that different magnitudes and directions of budget changes have different performance outcomes. With regard to the measurement of the magnitudes and directions of budget changes, this study considered two methods. The first method measures positive or negative % changes in annual budget allocation without considering whether these changes show budget punctuations, which produces two different independent variables, namely, Average Positive Annual % Change (defined by the mean value of all positive annual % change values) and Average Negative Annual % Change (defined by the mean value of all negative annual % change values).

The second method considers budget punctuations (i.e., large-scale changes) and their direction (positive or negative). First, we defined three categories of budget punctuation depending on the degree of annual percentage changes in budget allocation from a previous year (t−1) to a current year (t), as follows (Baumgartner & Jones, 1993):

- There is no punctuation (i.e., an incremental change) if the annual percentage change is between ±25%;

- There is a positive punctuation if the annual percentage change is more than +25%; and

- There is a negative punctuation if the annual percentage change is less than −25% of that of the previous year.

Then, we counted the total numbers of positive punctuations and negative punctuations, which are the other two independent variables, namely, Number of Positive Punctuations and Number of Negative Punctuations. Table 2 describes the descriptive statistics of the ministry-level (the upper level in this study) variables. As shown in Table 2, during the 14 fiscal years examined, the minimum and maximum numbers of positive punctuations across the ministries were 5 and 8, respectively, while those of negative punctuations were 1 and 3, respectively.

Ministry-level (Level 2) Descriptive Statistics.

Since other factors should also be considered as affecting public service performance, this study specified other control variables in the models. The three public governance modes (hierarchy, market, and network), financial management capacity, budget monitoring capacity, financial information sharing capacity, gender, and service experience in government were controlled for at the individual level. These variables were measured by respondents’ perceptions of which public governance modes were employed by their ministries after the budget reform and their evaluations of the ministry’s budget management, monitoring, and information sharing capacities in the periods both before and after the reform. These respondents’ perceptions were assessed using a seven-point Likert-type scale (strongly disagree to strongly agree). Afterward, we defined the changes in those variables by differentiating the average values before and after the reform.

In particular, this study used Yoo and Kim’s (2012) measurements of the three governance modes composed of the following six task characteristics: rules, discretion, supervision, clients, goals, and environment. Then, we examined the structural relationships between each governance mode (latent variable) and the six task features (observed variables) using a confirmatory factor analysis (Brown, 2015). The observed variables for the hierarchy mode appeared to have good fitness results; the likelihood ratio chi-square value was 29.213, the p-value for the Chi-square test was .001, the root mean squared error of approximation (RMSEA) value was 0.06, and the comparative fit index (CFI) value was 0.963. However, neither the market nor network mode appeared to have good fitness results; thus, we dropped some task items from both of these modes. Goals and supervision, the two items with the lowest factor loading values, were excluded from the market mode. Supervision, which had a negative factor loading value, was eliminated from the network mode. After dropping those items, the market and network modes had good fitness results; for the market and network modes, the likelihood ratio chi-squares were 6.158 and 17.479, the p-values for the Chi-square test were .046 and .004, the RMSEA value was .06 for both, and the CFI values were .97 and .914, respectively. Therefore, the hierarchy mode was based on the six task characteristics, whereas the market and network modes were based on four and five task characteristics, respectively. Gender was coded as 0 for females and 1 for males. Table 3 shows the descriptive statistics of the individual-level variables.

Individual-Level (Level 1) Descriptive Statistics.

To manage the abovementioned two-level datasets, the following regression equation was used for the individual level in the multilevel analysis:

Yij = the outcome variable,

β0j = the intercept,

β1j = the slope of explanatory variable X1,

β2j = the slope of explanatory variable X2, and …

eij = the usual residual error term for individual i inside ministry j

The ministry is represented by the subscript j (j = 1…J), while the individual officer is represented by the subscript i (i = 1…nj). On subsequent levels, the individual-level slope(s) and intercept become dependent variables that are predicted from a ministry-level independent variable Z1. The following regression equation was used for the ministry-level analysis:

In the aforementioned regressions, γ00 is the intercept, while γ01 is the slope of a ministry-level independent variable Z1. Using these multilevel approaches, we were able to model the impacts of not only level-1 (individual-level) variable but also a level-2 (ministry-level) variable on the outcome variables of the study.

Results

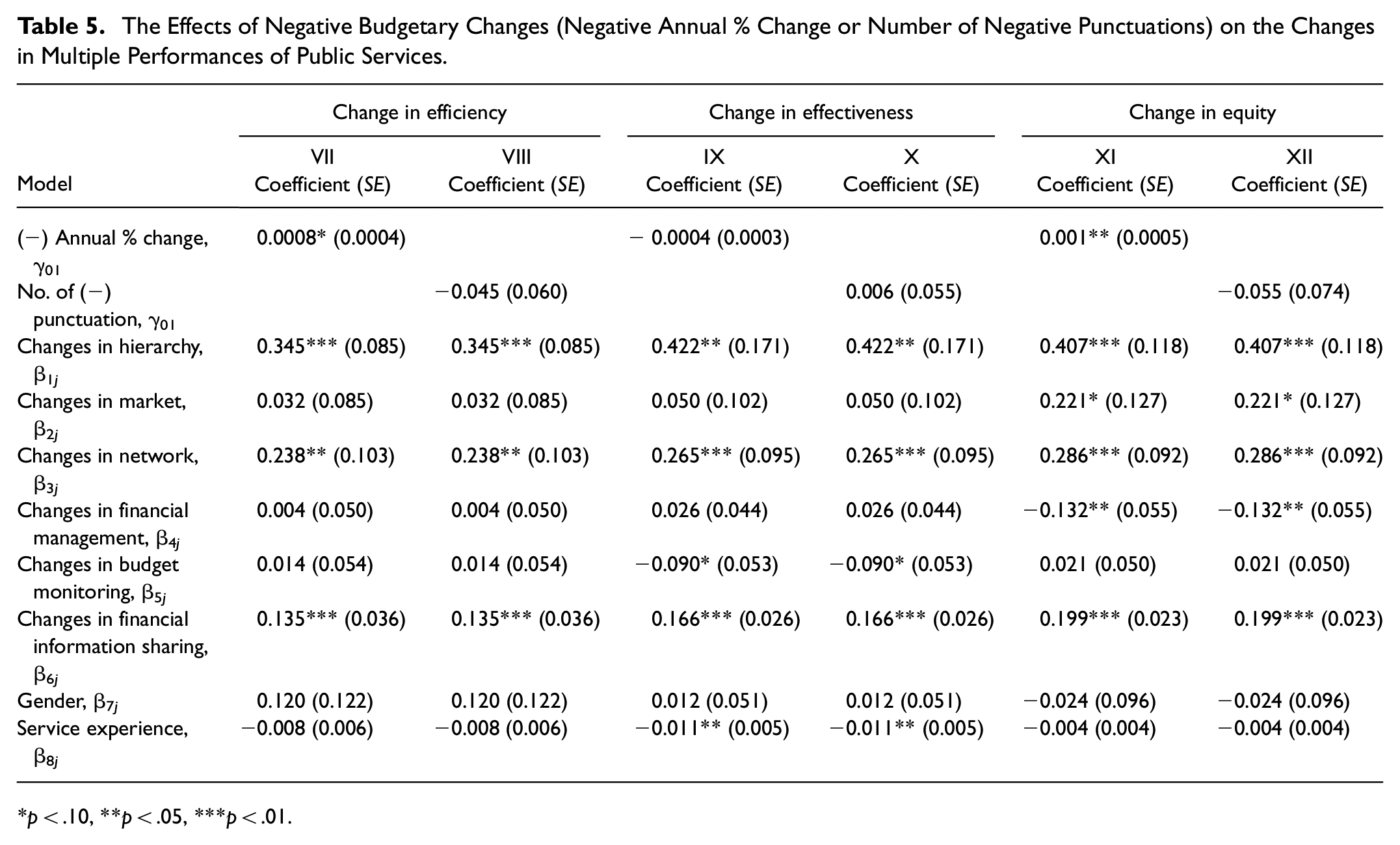

To answer our research question, we tested our proposed two hypotheses through the execution of twelve regressions utilizing HLM. Table 4 reports the results of the six regressions used in the multilevel modeling to test the effect of positive annual percentage changes and the number of positive punctuations on changes in efficiency (Models I and II), effectiveness (Models III and IV), and equity (Models V and VI). Table 5 has the same structure as that previously shown for Table 4, but the ministry-level main independent variables are changed to a negative annual percentage change and a number of negative punctuations. As shown in Tables 4 and 5, the coefficients of individual-level variables (β1j…β8j) have similar results consistently across different models. For example, the individual-level independent variable has a similar effect on the change in efficiency (in Models I, II, VII, and VIII) even though it uses a different ministry-level independent variable. It is the same for the changes in effectiveness (Models III, IV, IX, and X) and equity (Models V, VI, XI, and XII).

The Effects of Positive Budgetary Changes (Positive Annual % Change or Number of Positive Punctuations) on the Changes in Multiple Performances of Public Services.

p < .10, **p < .05, ***p < .01.

The Effects of Negative Budgetary Changes (Negative Annual % Change or Number of Negative Punctuations) on the Changes in Multiple Performances of Public Services.

p < .10, **p < .05, ***p < .01.

Ministry-level independent variables have different results for all the models, as shown in the first and second rows of Tables 4 and 5. As shown in Table 4, the positive annual percentage changes in budget allocation have no significant effect on all 3Es. This outcome suggests that increasing the annual budget (without considering whether significant amounts are increased or not) has no impact on all 3Es of public services. The results do not support Hypothesis 1, that is, that positive public budget changes are associated with positive public performance changes. Then, we used the number of positive punctuations as a ministry-level independent variable to determine what happens if the budget increases significantly. We found that positive punctuations have a positive and statistically significant effect on effectiveness (γ01 = .100, p < .10 in Model IV) but no significant effect on efficiency and equity. This means that a significant budget increase over a long period will improve the effectiveness of public services, whereas a positive punctuation cannot enhance the efficiency and equity of public services. Therefore, these results partially support Hypothesis 1.

Based on the results shown in Table 4, the budget increase cannot improve all 3Es simultaneously, and performance outcomes may be realized differently depending on the magnitude of the budget increase. Contrary to previous literature suggesting that financial resources enhance performance (Andersen & Mortensen, 2010; Flink, 2018; Flink & Molina, 2021; Hedges et al., 1994), our results indicate that every level of budget increase does not uniformly enhance all aspects of public services (efficiency, effectiveness, and equity). Positive budget punctuation has a significant impact only on effectiveness, which is a singular aspect of public performance, while efficiency and equity remain unaffected. This suggests that with a significant budget increase, it is possible to deliver public services that meet the needs of citizens. To increase the efficiency of public service delivery and ensure a fairer and more equal distribution of public services, factors other than financial resources must also be considered. Here, we did not assess effectiveness from the customers’ perspective. Instead, we assessed effectiveness by asking whether government employees could deliver their service to a satisfactory level for the public. That is, government personnel believe that if the budget is raised substantially, their services will be able to match the public’s expectations. However, they do not expect that their efficiency and equity of service delivery can be improved only by increasing the budget. Based on these findings, to enhance efficiency, we propose that only a budget increase is not sufficient. Effective management, such as performance and human resource management practices, is also required. This aligns with the findings of previous studies suggesting that increased resources result in improved services, but effective management is essential to better services (Walker et al., 2024) and performance management is positively related to efficiency (Andrews & Van de Walle, 2013). For more equity in service provision, policymakers should address disparities in society, as suggested by Mamokhere et al. (2022).

As shown in Table 5, the negative annual percentage change has a positive and significant effect on the changes in efficiency (γ01 = .0008, p < .10 in Model VII) and equity (γ01 = .001, p < .05 in Model XI). This implies that reducing the annual budget allocation (any level of budget reduction) would decrease the efficiency and equity of public services. In other words, if the budget is reduced, the existing inefficiency and inequality inherent in public service delivery will continue to deteriorate. These results support Hypothesis 2. Our study aligns with Hernandez’s (2021) observation and indicates that budget cuts would lead to a lack of investment in infrastructure and capacity buildings as well as inequity in the distribution of services across various sectors and geographical areas.

To examine what happens if the budget decreases significantly, we used the frequencies of negative punctuation as a main independent variable. The number of negative punctuations has no significant effect on all 3Es, which does not support Hypothesis 2. Our findings are not consistent with the findings of Xu and Flink (2022) that severe budget cuts reduce organizational performance. However, according to our findings, it cannot be interpreted that the 3Es would not be reduced by negative punctuations. According to our data, negative budget punctuations were not observed continuously over several years, which means that there was no continuous negative punctuation trend (Flink & Robinson, 2020, p. 103) in the case of Myanmar’s budget spending. Reducing a large amount of the budget (i.e., negative punctuation) was achieved only when the government intended to maintain a budget equilibrium point by correcting a previous year’s dramatic budget increase (Myaing & Lim, 2023). For instance, the budget appropriated to a certain public agency or policy domain in a particular year could be positively punctuated compared to a previous year for a specific reason. After positive punctuation, the government may want to return to the budget’s previous level; thus, a significant amount of the budget could be reduced in the following year to regress to that original level. This is regarded as a budget equilibrium point. In Myanmar, negative punctuation was observed very rarely and only in relation to the purpose of maintaining budget equilibrium (in most ministries, negative punctuation was found only once or twice in the 14 years of data); the results show that negative punctuation has no significant effect on the 3Es. Therefore, it can be assumed that more frequent negative punctuations over the course of several years may reduce the 3Es.

Regarding individual-level independent variables, we found the following significant results in Tables 4 and 5. Changes in the hierarchy mode had a positively significant effect on all 3Es (for efficiency: β1j = .345, p < .01; for effectiveness: β1j = .422, p < .05; for equity: β1j = .407, p < .01). The results show that hierarchical governance can generate positive effects on 3Es, implying that strict rules, regulations, and close supervision can enhance the performance of Myanmar’s public servants. Myanmar’s public sector cannot incentivize public servants to work hard by themselves since finances and promotion are already constrained by civil law. Therefore, it may be assumed that strict rules and close supervision are the best ways to improve employees’ performance.

Changes in the market mode had a positively significant effect on only equity (β2j = .221, p < .10). This implies that there is at least a small possibility that the adoption of more market-based practices by or competition among Myanmar governmental agencies could benefit even marginalized groups within society to some extent. However, there are no significant effects found in regard to efficiency and effectiveness. According to market characteristics, public servants need to follow a few basic rules; they have their own discretion and a lower level of supervision, and the main goal of their work is to obtain the highest number of payable outcomes. However, most public services are not profitable. Moreover, public employees might complete their work under rules, regulations, and supervision rather than being motivated to work hard by incentives or rewards. Hence, the market governance approach does not work as expected in the public sector and fails to improve the efficiency and effectiveness of public services.

Changes in the network mode had a positive significant effect on all 3Es (for efficiency: β3j = .238, p < .05; for effectiveness: β3j = .265, p < .01; for equity: β3j = .286, p < .01). These results indicate that when there is increasingly more communication, collaboration, and coordination among public organizations and stakeholders with diverse interests and priorities, the performance of public services (all 3Es) will improve.

The results of the three governance modes demonstrate that both hierarchical and network structures enhance the 3Es simultaneously, whereas market mechanisms specifically promote equity. These findings suggest that government organizations in Myanmar employ a combination of the three governance modes. This observation is consistent with prior research indicating that the three governance modes coexist and mutually reinforce each other in practice rather than one mode replacing another (Haveri & Anttiroiko, 2023; Osborne, 2010), although the influence of these governance modes on the 3Es may vary depending on the context of a country (Meuleman, 2008; Swe & Lim, 2019).

Financial information sharing had a positive significant effect on all 3Es (for efficiency: β6j = .135, p < .01; for effectiveness: β6j = .166, p < .01; for equity: β6j = .199, p < .01). This means that if the government releases more budget information, it will increase the efficiency, effectiveness, and equity of public services. Jung (2022) revealed that budget information sharing using participatory budgeting programs leads to a significant improvement in government efficiency. Our findings imply that an increase in the ministries’ budgetary information-sharing capacity would promote stakeholders’ engagement in the public budgetary process, which would in turn make the functions and operations of budget implementation, as well as public service delivery agencies, more efficient, accountable and equitable for citizens.

Public officer’s years of service for government had a negative effect on effectiveness (β8j = −.011, p < .05 in Models III, IV, IX, and X). This result can be interpreted as public employees who have more working experience within the government possibly being able to obtain more accurate internal information about the qualities of services delivered to their target recipients, tending to better underestimate the effectiveness of the public service and believing that it needs to be improved.

In sum, we can conclude that positive public budget changes have a positive impact on effectiveness depending on the magnitude of budget changes. However, care should be taken with any amount of budget cutting, as public budget reductions can decrease the efficiency and equity of public service delivery to a certain extent. In Myanmar's public sectors, hierarchical governance, network governance and financial information sharing can improve public service performance (all 3Es), while market governance can improve only equity to some extent.

Conclusion

According to our results, increases in budget allocation cannot improve all 3Es at the same time. Depending on the magnitudes and directions of the budget changes, there are different effects on the 3Es. The effectiveness of public services can be improved by increasing a significant amount of budget allocation, as indicated by positive punctuations (annual percentage changes greater than +25%) in this study. However, even positive punctuations have no effect on efficiency and equity. To deliver public services more efficiently, the capacity of public employees must also be enhanced. That is, to deliver public service efficiently, not only public finances but also other resources, such as human resources, need to be reinforced together. Equity depends not only on a department’s service delivery policies or programs but also on a society’s underlying equity level. Public finance alone may not be able to easily address deeply rooted structural inequalities within a society. If a society lacks fairer social policies aimed to eradicate or mitigate injustice (such as discrimination based on ethnicity, religion, urban-rural, income, and age), simply increasing the budget cannot improve the equity of service distributions.

Any level of budget reduction (including small and large budget reductions) can diminish the efficiency and equity of public services. Budgetary or policy decision-makers should be aware that while an increase in budget allocation may not necessarily affect the performance of public services (i.e., all 3Es), even a small budget reduction can harm the efficiency and equity of public services. Regarding the three governance modes, Myanmar still relies mainly on hierarchical governance, but there is also a growing trend toward network governance; both governance modes have a positive impact on all 3Es. However, there is relatively less emphasis on market characteristics. Another important finding is that sharing financial information is one of the crucial factors for improving all 3Es at the same time. Therefore, our findings support the role of financial information sharing among stakeholders, which should be considered to provide better public services in various public sectors in the future, especially for policymakers in Myanmar.

The policy implications are that policymakers should not simply focus on increasing the budget to improve all 3Es. Although the budget is essential for public services, it alone may not be sufficient to improve all 3Es. As discussed above, financial resources can be utilized to obtain other types of resources. Therefore, to improve all 3Es, it is necessary to use financial resources effectively to acquire or reinforce other types of resources. For instance, in labor-intensive sectors, financial resources should be used to improve human capital resources. An increased budget will definitely improve the capacity of public employees, which can consequently improve the efficiency and effectiveness of their services. On the other hand, while an increase in financial resources may not necessarily increase equity in public service delivery, it is necessary for policymakers to be cautious about the possibility that equity could also be sacrificed with any budgetary stringency.

In the fields of public budgeting and administration, some studies have already analyzed the linkages between budget inputs and public organizations’ performance (outputs or outcomes); however, this paper has some distinctions. In most of the previous studies, public performance was measured mainly based on a certain aspect or single dimension of output quality (Andersen & Mortensen, 2010; Chen & Flink, 2022; Flink, 2019; Flink & Molina, 2021; S.-Y. Lee & Whitford, 2013). However, some researchers have proposed the multiple dimensions of public values, i.e., efficiency, effectiveness, and equity (fairness), to evaluate organizational performance (Brewer & Selden, 2000; Davis et al., 2013). Moreover, to comply with the argument of Walker et al. (2024) that the budget should be viewed as a dynamic rather than a static aspect, this study contributes to the PET literature by examining how the different patterns of budget changes we define affect three dimensions of performance (the 3Es). Furthermore, most of the prior studies have focused on only one single sector or policy domain. Their results are thus too mixed to be generalized to all sectors because each sector has unique features. However, our study’s findings are based on the performance of 18 ministries. Therefore, it is reasonable that our findings can be generalized to more diverse sectors.

There are some limitations to this study. We focus only on public service providers’ perceptions. We argue that if service providers themselves believe that their own service qualities are poor, policymakers should concentrate more on the circumstances and obstacles faced by service deliverers. This is one emphasis of this study. However, some studies have stated that different evaluations are used for the quality of public service performance between citizens and government servants (Scott & Enu-Kwesi, 2018) and that assessing the complexity of public service performance should involve using perceptual and archival data collected from both internal and external stakeholders (Walker et al., 2024). Therefore, future research that aims to examine the quality of public service performance should utilize perceptual and archival data collected from both public servants and service recipients.

Footnotes

Data Availability Statement included at the end of the article

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are available from the corresponding author upon reasonable request.