Abstract

This study investigates the possibility of forming a monetary union across West Africa. This was achieved by employing the structural VAR framework. Data on real GDP, inflation, and exchange rate were used to represent supply, monetary, and demand shocks from the period 1986 to 2020. The impulse response and variance decomposition results showed that shocks affecting the West African region are idiosyncratic, while the residuals of the structural VAR were used to compute the correlation coefficient. The correlation coefficient revealed that the demand and monetary shocks were symmetric across WAEMU countries and asymmetric for the rest of the region. The study suggests that the West African region is not ripe for a monetary union. However, the study opined that the WAEMU countries are the closest to forming a West African monetary union and a piecemeal approach may be adopted such that the WAEMU countries are the first to form the union, while the rest may join when they meet the convergence criteria. In essence, West African countries’ central banks need to focus on harmonizing their monetary policies and remove all barriers to factor mobility for the synchronization of shocks and for all countries to meet the convergence criteria.

Plain Language Summary

Purpose: This study aims to establish whether the West African region is ripe for a monetary union in light of recent global events affecting the world. Methods: The study adopted the SVAR methodology and correlation coefficients to achieve the objectives of the study. Conclusion: The study concludes that the region is not yet ripe for a monetary union. Implications: The implication of the results is that central banks need to focus on harmonizing their monetary policies and remove all barriers to factor mobility for the synchronization of shocks and for all countries to meet the convergence criteria. Limitations: The limitation of the study is based on the fact that data was gathered from only 14 of the 15 countries within the region. This is due to the data limitation of the only country excluded from the analysis.

Introduction

The pursuit of monetary integration in West Africa started with the establishment of the Economic Community of West African States (ECOWAS) in May 1975. At its inception, fifteen member countries ratified the treaty in Lagos. These member countries include Benin, Burkina Faso, Côte d’Ivoire, Gambia, Ghana, Guinea, Guinea-Bissau, Liberia, Mali, Mauritania, Niger, Nigeria, Senegal, Sierra Leone, and Togo. Cape Verde joined the member states a year later, while Mauritania left in the year 2000, leaving the countries at their original 15 members. At the inception of Ecowas, the West Africa Economic Monetary Union (WAEMU) existed among Francophone countries in West Africa (these countries include Benin, Burkina Faso, Côte d’Ivoire, Mali, Niger, Senegal, and Togo). These countries adopted a common currency known as the CFA. Since France colonized these nations, the Francophone nations have collectively adopted a common currency and monetary policy framework.

The 6 Anglophone member countries (The Gambia, Sierra Leone, Liberia, Ghana, Nigeria, and some parts of Cameroon were colonized by the British) all had independent currencies, and they decided to form a common monetary union known as the West African Monetary Zone (WAMZ) under the umbrella of the West African Monetary Institute (WAMI). The idea was to merge WAEMU with WAMZ to form an Eco currency across West Africa (Bossuyt, 2016). The idea of the monetary integration process entails three basic arrangements: a common monetary policy, a common currency, and a common central bank (Plasmans et al., 2006). The essence of these arrangements is to have a common monetary policy framework across the region.

A theory in the economic literature that supports the unification process is the Optimum Currency Area (OCA) proposed by Mundell (1961) and further reinforced by McKinnon (1963) and Kenen (1969). Mundell (1961) proposed that the condition for the implementation of a monetary union is that shocks across these countries must be symmetric; that is, they must not be country-specific. McKinnon (1963) further noted that these economies need to be open to trade, while Kenen (1969) opined that these economies must be diversified. More recently, Plasmans et al. (2006) buttressed the role of fiscal integration in achieving a monetary union. They believed that if a monetary union were to be possible, the fiscal authorities would also play a part in the integration process, ensuring that a single institution would be in charge of coordinating the fiscal policies of the member nations. Finally, Alesina and Barro (2002) opined that factor mobility within the region is another major determinant of a currency union, such that factors of production must be easily movable among member countries to guide against the problems of asymmetric shocks. Consequently, countries within the union can achieve stable prices and full employment (Alesina & Barro, 2002). The OCA convergence criteria are divided into two categories, which are the primary and secondary categories. Table 1 gives a brief overview of these requirements.

Primary and Secondary Convergence Criteria for ECOWAS.

Source. ECOWAS convergence reports, 2017.

From the above primary criteria, only Guinea, Liberia, and Nigeria met the very first primary criteria in 2015, while all West African countries except Ghana recorded inflation rates of less than 10% in 2015 (ECOWAS, 2017). In 2022, Guinea-Bissau, Nigeria, and Sierra Leone recorded inflation rates over 10%, which may be linked to exchange rate depreciation across these countries during the period, while Ghana’s inflation soared to 54.1% in December 2022, further highlighting the vulnerability of the Ghanian economy. Furthermore, the target of 6-month imports from the nation’s reserves (later reduced to 3 months) was not met by Gambia, Ghana, and Guinea in 2016, while Guinea, Nigeria, Gambia, and Sierra Leone did not meet the Central Bank fiscal deficit financing of less than or equal 10% (ECOWAS, 2017). In the secondary criteria, Cape Verde, Gambia, and Togo did not meet the less than 70% debt to GDP ratio criterion, while the criterion of the nominal exchange rate being within the ±10% bound was not met by Guinea, Nigeria, and Sierra Leone (ECOWAS, 2017). In 2021, Nigeria did not meet up the tax-to-nominal GDP ratio of above 20%. The inability of the ECOWAS countries to meet these criteria led to another shift in the monetary integration process until 2027.

There are several benefits and costs that could be attached to the convergence within the region. These include (but are not limited to) price stability and convergence (Fischer, 2009), reduction in exchange rate risk (Nkwatoh et al., 2019), elimination of trade barriers (Houssa, 2008), and improved resource allocation and investment risk (Bogdanova, 2009). However, the costs of a monetary union will be very grave if member countries respond asymmetrically (differently) to global macroeconomic shocks. It is imperative to note that while the primary focus of the integration process revolves around a common currency, the importance of monetary policies as well as the integration of the capital and money markets of member countries must not be overlooked. A major reason for this is that regional stability is a precursor to sound macroeconomic policies among member countries.

The importance of monetary integration in West Africa stems from the fact that the region has been planning to form a union in line with the monetary union of Euro member countries. However, the West African experiences differ due to their heterogeneous characteristics and the fact that some countries are of the view that Nigeria, the biggest nation in the region by GDP and population, would dominate the bloc and may be the ultimate decider on policy decisions in the bloc. While these concerns may hold, it is important to note that the policy design around a monetary union is meant to benefit all member countries without excluding any member, which is the reason why the precursor for forming a union is for member countries to simultaneously meet the convergence criteria.

The COVID-19 pandemic has more recently wreaked havoc on the global economy. The pandemic forced countries to shut down as lives and jobs were lost. Furthermore, the pandemic deteriorated the chances of member countries to attain convergence as of the proposed date of July 2020, the fifth time member countries have been unable to achieve monetary convergence (the first convergence was set for January 1, 2003, the second was set for July 1, 2005, the third convergence within the region was set for December 1, 2009, while the last convergence was set for January 1, 2015). This led to speculation of another deadline set for 2027. Several studies have investigated the possibility of forming a West African monetary union. From these studies, Debrun et al. (2002), Chuku (2012), Harvey and Cushing (2015), and Mensah (2015) were of the view that the region is not ripe for a union. While O. J. Nnanna (2006; U. J. Nnanna, 2013), Bakoup and Ndoye (2016), Alagidede et al. (2012), Ekpo and Udoh (2012), and Adediran et al. (2020) were of the notion that a union is possible and the region may be better off forming a union.

The outcomes of these studies may differ due to the examined period or the selection of countries within the region. Nevertheless, this study would contribute to this discussion in several ways. First, the study would be the first to examine a potential monetary union by collecting data on 14 of the 15 West African countries within the region. The reason for the selection is that Liberia is the only country from which the study could not gather its data from 1986. Second, the study adopts a four-shock model, comprising supply, monetary, demand, and global shocks, to establish the consistency of the results across the models. Adding monetary and global shocks is also very important because, unlike other studies that only looked at demand and supply shocks, when a union is formed, the monetary policies of these countries will become more in line with each other. For global shocks to be possible, they must have the same effect on all of these countries for a union to be possible. Finally, in exploring global shocks, the study would also establish how these countries respond to global demand, supply, and monetary shocks. This is important because if these countries respond to global shocks asymmetrically, then forming a monetary union may not be in their best interest as global shocks would affect these countries differently and it becomes difficult to align a monetary policy that would cater to all the countries concurrently.

Considering the above, this study intends to examine the key issues around monetary integration and convergence and determine whether the region is ripe for monetary integration since evidence from the ECOWAS convergence reports and recent global shocks makes it impossible for convergence to be feasible in 2020 due to the pandemic. Therefore, this study adds to the existing literature by measuring the role of global supply and demand shocks in addition to domestic demand and supply shocks within the region to ascertain the suitability of the region for a monetary union. The study will also consider the role of global and domestic monetary shocks within the region, as this may yield further insights into the monetary integration process for West Africa. Finally, the study will provide lessons for the sustainability of monetary integration if the West African region decides to go ahead with the monetary integration process in the future.

In essence, empirical investigation of a monetary union in the West African region would help identify whether the region is indeed ripe for a union. If this is the case, then fears of domination may not be an issue, especially when we consider the way the European Union is being run. On the other hand, if the region is not ripe for a union, then the study would highlight the reasons for this and offer policy options for the region to be able to form a monetary union by the next proposed timeline. Therefore, it becomes expedient to confirm if the region is indeed ripe for a union and whether the region would respond to shocks homogeneously. The rest of the paper is organized as follows:. Section two revisits the literature, while the third section discusses the methods. The fourth section analyzes the results, while the final section concludes the paper with some policy recommendations.

Empirical Issues on Monetary Integration

Harvey and Cushing (2015) tested the validity of a common currency across West Africa using the SVAR framework. Their study found that West African countries responded asymmetrically to macroeconomic shocks across the region. Furthermore, the correlation coefficient outcomes also proved that shocks affecting the ECOWAS region are asymmetric in nature. This result was further reinforced by Mati et al. (2019) who tested the validity of a common currency across West Africa using inflation and output to test the validity of a monetary union across the region. Furthermore, Nkwatoh et al. (2019) reiterated that for the region to be able to form a union, they must satisfy the optimum currency area criteria; otherwise, the region might be savaged by the current problems faced by some European Union countries. Chuku (2012) within a four-shock model, also found the ECOWAS region not to be ready for the monetary integration process. The outcome by Chukwu was also corroborated by Alinsato (2022) who in addition found an increase in income disparities among the countries within the union using the sigma-convergence analysis. However, Ogunkola (2005) believed that the Structural Adjustment Program brought about a reasonable level of convergence across West Africa and that the region was close to convergence, with a caveat of wider differences in real exchange rate shocks facing the CFA and non-CFA countries.

Goshit (2013) in a theoretical survey, found that problems hindering the monetary integration process among ECOWAS member countries include lower levels of trade among member countries, uneven benefits from integration, and fears of dominance by the more prominent and wealthier economies. The study noted that for monetary integration to be possible, the region must overcome several barriers to trade, while fiscal policies must be harmonized across the region. Asongwu et al. (2015) carried out a meta-analysis of the literature on the subject matter. Their study considered different aspects of the monetary integration process, including the African Monetary Union (AMU), East African Monetary Union (EAMU), South African Monetary Union (SAMU), and West African Monetary Zone (WAMZ). Several issues were observed across each region, and the study recommended that more emphasis be placed on lessons generated from the European Union and WAEMU. Debrun et al. (2002) developed a multi-country model and incorporated the role of fiscal authorities within the monetary integration process. The study found that monetary integration would not be beneficial for West African countries unless Nigeria improved its fiscal responsibility and discipline.

Mensah (2015) investigated the possibility of a union across WAMZ and the possibilities of trade between WAMZ and other countries in Africa, Europe, and Asia. Although the study supports earlier works on the subject, it also found some possibilities for marginal integration, especially when variables such as output, inflation, and monetary policy rate were considered. However, Bakoup and Ndoye (2016) and O. J. Nnanna (2006) were of the view that the monetary integration process was an opportunity for the region to have a common monetary policy and to pool resources together to foster the growth of the region. Similarly, Alagidede et al. (2012) found that the prospects of a monetary union across West Africa could lead to an improvement in trade among West African countries. These results were also reinforced by studies such as those by Ekpo and Udoh (2012) and U. J. Nnanna (2013). Also, Adediran et al. (2020) using fractional integration and cointegration techniques, supported the convergence of a monetary union in West Africa, with a special emphasis on pegging the currency against the U.S. dollar.

On the nature of the financial system and the development of the economies of the Union Économique et Monétaire Ouest Africaine (UEMOA), Ehigiamusoe and Lean (2019b) revealed that financial development has an effect on economic growth in both UEMOA and non-UEMOA nations. It turns out that UEMOA nations and non-UEMOA countries have quite different relationships between financial wellness and economic development. To be more precise, in UEMOA nations, financial development has a strong positive effect on growth, but in non-UEMOA countries, the effect is less. Furthermore, Ehigiamusoe and Lean (2019a) in another study of developing and developed countries, showed that the assertion that forming a union would necessarily lead to the growth of all countries was not entirely the case, as their study found inconclusive results on the impact of a potential monetary union on the economic growth of the countries.

Gammadigbe and Dioum (2022) examined the role of the business cycle in the monetary integration process across West Africa. The study found a positive influence of trade intensity on the convergence process and believed that the initial asymmetric nature of the business cycles of West African countries does not represent a hindrance to the convergence process. Furthermore, Oyadeyi and Akinbobola (2020) were of the view that global shocks affect the monetary policy transmission of developing countries. These results were corroborated by other studies, such as Oyadeyi (2022a, 2023a) and Oyadeyi and Akinbobola (2022).

Jefferis (2007) examines the monetary union of Southern African Development Countries (SADC). The study revealed that countries such as Botswana, Lesotho, Mauritius, Mozambique, Namibia, Swaziland, and South Africa are ripe for convergence based on their performance. However, the other SADCs were not found to be ripe for convergence based on their performance. Cobham and Robson (1994) were of the opinion that the African region could benefit from other unions in existence, such as the union formed in Europe and other unions such as the CFA countries. Gammadigbe and Dioum (2022) opined that the asymmetric nature of the variables was not a core reason for ECOWAS countries not to converge. They suggested that convergence should be a priority based on the beta coefficients of their analysis, and the more open these countries are to trade, the better their convergence.

Ndao et al. (2019) examined the current discussion on monetary unions by confirming whether convergence would lead to income convergence among member countries of the CFA union. The results revealed that the union has not led to income convergence within the CFA bloc. Onye and Umoh (2023) explored the role of fiscal policy in forming a union in ECOWAS. The paper found that fiscal policy is important in the discussions of a monetary union as fiscal policy operations became counter-cyclical in the formation of a union post-convergence era between 2003 and 2018 compared to the pre-convergence era between 1995 and 2002. Furthermore, Ekpo (2018), Amadou and Kebalo (2019), and Kébalo (2019) note that for convergence to occur, all the respective countries have to fulfill the criteria for convergence and use trade as a major tool to achieve this; otherwise, the convergence may harm the respective economies and they may be worse off.

Asongu and Diop (2023) created an index for monetary union convergence in Africa. The study improved on the models published by the African Union and other development agencies and recommended ways of improving the convergence criteria. Asongu et al. (2020) for the Southern African Monetary Union (SAMU), Ndongo (2020) for CFA countries, Osabuohien et al. (2019), Oyadeyi (2022b), and Oyadeyi (2023b) recommended ways of improving the solidarity of countries and how they can strengthen their economies. In essence, it is clear from the reviewed literature that the convergence criteria within the ECOWAS region have generated mixed findings. Therefore, achieving a common currency is assured only if these countries respond to shocks symmetrically. The next sections will detail the investigation carried out in the study.

Methodology

The Model

To estimate monetary integration across West Africa, this study adopts the Blanchard and Quah (1989) model to test the level of symmetry across the region. This model was also adopted by previous studies such as Bayoumi and Eichengreen (1997), Houssa (2008), Chuku (2012), and Harvey and Cushing (2015). This model is premised on the aggregate demand-supply framework, which posits that demand shocks do not have an influence on output in the long run, while supply shocks have an influence on output and prices both in the short and long run. The decision in determining whether these countries may be unified is the level of shock asymmetry within the region. That is, unification will be possible if shocks are symmetric, thereby implying that the use of union-wide policies may be adopted to correct distortions among member countries. However, if shocks across the region are asymmetric, then unification might be counter-productive since individual countries will respond to shocks differently.

As an extension of the literature, this study considers three separate four-shock models for global supply shocks, global demand shocks, global monetary shocks, and domestic shocks, extending the previous two shock models, consisting of aggregate demand and supply shocks (Buigut & Valev, 2005; Houssa, 2008), three shock models (Harvey & Cushing, 2015), and four shock models for output alone (Chuku, 2012). The shocks considered consist of a global supply shock, global demand shocks, and global monetary shocks, against domestic supply shock in the first model, domestic demand shock in the second model, and domestic monetary shock in the third model. The essence of incorporating global demand and supply shocks is due to the primary export-oriented nature of the region as well as the import-oriented nature of semi-finished and finished goods the region is known for. The essence of the monetary shock is to be able to determine how the region will respond to a change in the direction of global monetary policy shocks and to test the viability of monetary integration within the unification process.

Let

where

this can be re-specified as

Equation (3) can further be simplified as

where

Suppose (as in Blanchard & Quah, 1989; Clarida & Gali, 1994; Harvey & Cushing, 2015) the moving average representation of the reduced form of equation (4) is given by:

and the true moving average is represented as

from equation (3),

Putting equation (10) into (8)

Therefore, comparing equations (9) and (11) shows that

Equation (12) depicts the underlying relationships between the vector of structural shocks

The Structural Decomposition

Since the variables have been specified, we decompose the series such that

The decompositions in equations (14) to (17) state that global supply shocks (equation (14)) are exogenous and cannot be determined within any of the observed countries since their contribution to global output is very little, while global demand shocks (equation (15)) are determined by shocks from itself and global supply shocks, since supply shocks are known to be the unexpected changes in output in many developing economies. Global monetary shocks (equation (16)) are affected by global supply and demand shocks, and themselves. Finally, domestic shocks are driven by the three global shocks and itself. That is, domestic shocks are largely affected because developing countries are highly import-dependent. Changes in global consumer prices and real exchange rates also have an impact on domestic shocks. It is important to note that for the purpose of this study and as an extension to other studies, domestic shocks are divided into domestic supply, domestic demand, and domestic monetary shocks. Therefore, a change in global output, a change in import demand, and a change in global monetary policy will determine the level of changes in domestic supply shocks, the exchange rate level within these economies and prices within these economies. Domestic monetary policy shocks come last in our matrix because money plays a neutral role in the economy in the long run. In essence, the above narration can be displayed as:

The narration in equation (18) states that global demand is affected by global supply shocks only in the long run, while both global supply and demand shocks affect global monetary shocks in the long run. However, global monetary policy shocks have a neutral effect on demand and supply shocks in the long run. These implies that

and

where Xt is a vector of domestic shocks.

where

and F is the impulse response function derived from

In other words, structural shocks (innovations) are recovered as linear combinations of the model in its reduced form. Finally, the correlation coefficient will be used to determine the level of symmetry or asymmetry and to ascertain the region’s potential for monetary unification. A positive and significant correlation coefficient—that is, 0.5 and above—implies the region may go ahead with a unified monetary policy and currency, while a negative or insignificant coefficient (less than 0.5) implies individual countries will respond to shocks differently and it would not be suitable for these countries to adopt a unified monetary policy framework. Our methodology from equation (1) to (23) would be replicated for each domestic shock.

Data Sources and Representation

To achieve the objectives of this study, we adopted annual time series data on 14 West African countries from the period 1986 to 2020. These countries include Benin, Burkina Faso, Cape Verde, Côte d’Ivoire, Gambia, Ghana, Guinea, Guinea-Bissau, Mali, Niger, Nigeria, Senegal, Sierra Leone, and Togo. This study also extends previous studies that have made use of 4 to 8 West African countries to represent the region. The only West African country excluded from the list is Liberia, and this is due to the unavailability of data from 1986. These 14 countries will provide a robust representation of the region to confirm if the region can form a monetary union. The data collected were sourced from the 2022 editions of the IMF’s International Financial Statistics (IFS, 2022) and the World Bank’s World Development Indicator (WDI, 2022). For each country, we adopt the log of real GDP (in U.S. Dollars), the log of the exchange rate, and inflation to represent domestic supply shock, domestic demand shock, and domestic monetary shock respectively.

For our measures of global shocks, the World GDP sourced from WDI (2022) will proxy for global supply shocks. The U.S. real effective exchange rate will be our proxy for global demand shocks, while the U.S. inflation rate will be our proxy for global monetary shocks. The reason for adopting the U.S. real effective exchange rates and inflation is because the United States is the most dominant player within the international arena and most of these countries (especially the Anglophone countries) measure their currency against the U.S. dollars. Furthermore, some previous studies have used the United States to represent the global economy (see, for example, Chow & Kim, 2003; Mati et al., 2019; Regmi et al., 2015). Even though France has been influential in the Francophone countries, it is not considered part of the global economy since it has already joined the European Monetary Union (EMU).

Empirical Results

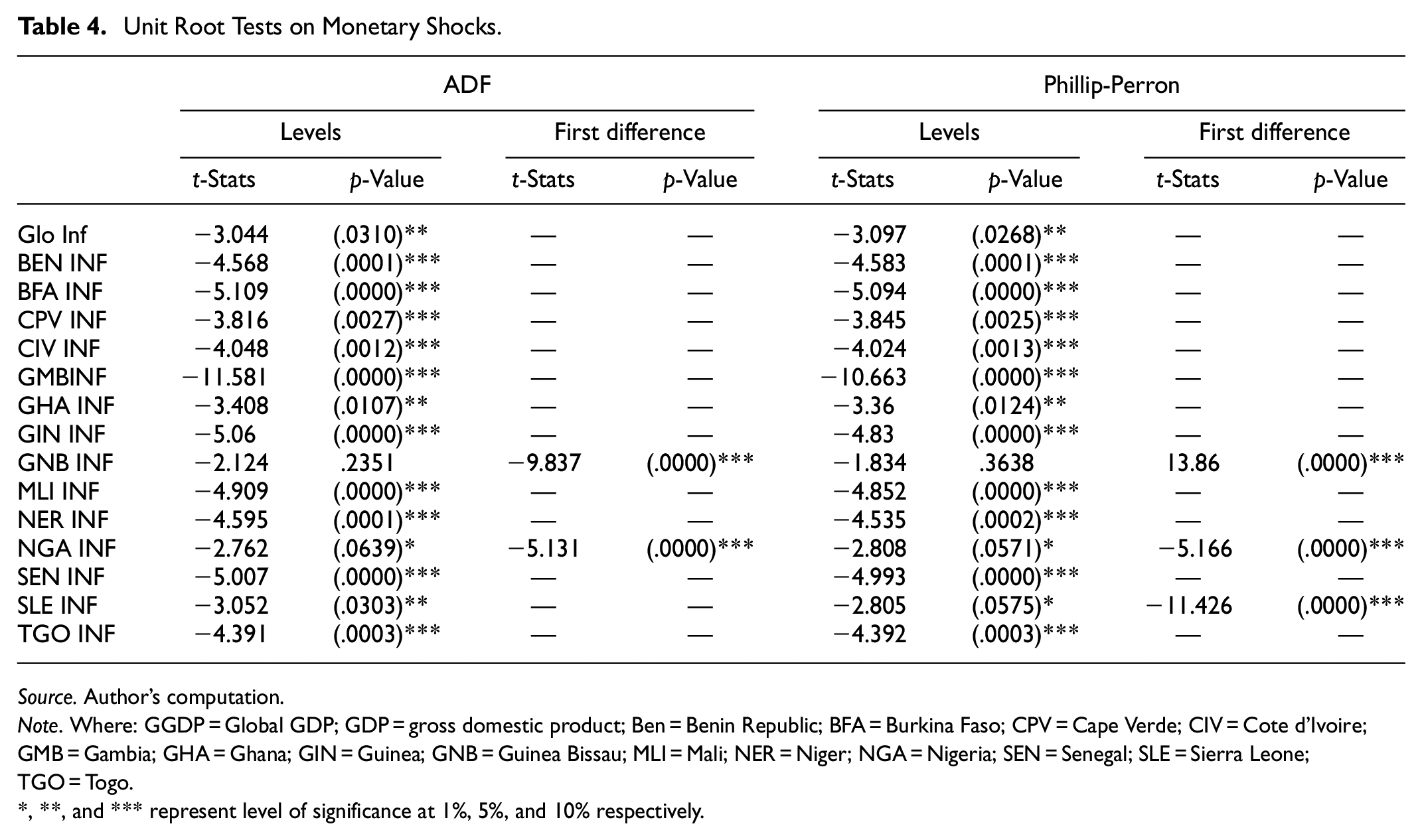

The main tools of analysis in this paper are structural vector autoregression, impulse response, variance decomposition, and correlation of shocks. We start the analysis by providing information on the stationarity properties of the variables. We employ the Augmented Dickey and Fuller (1979) and Phillips and Perron (1988) unit root tests to confirm stationarity. The unit root analyses in Tables 2 to 4 confirm the stationarity of the variables and also show that no variable is I(2). This implies that the selected variables are fit for the analysis. However, to further confirm the ADF and PP results, the paper also adopted the Zivot and Andrews (1992) unit root test. This was used to check for the possibility of structural breaks in the series. The results of the Zivot and Andrews tests showed that for the GDP series, all the variables were stationary in first difference except for Guinea-Bissau. For the exchange rate series, the results were a mixture of I(0) and I(1), while for the inflation series, the results were I(0) except for Guinea-Bissau and Sierra Leone. Therefore, the unit root result confirms the variables are fit for the analysis.

Unit Root Test on Supply Shocks.

Source. Author’s computation.

Note. Where: GGDP = Global GDP; GDP = gross domestic product; Ben = Benin Republic; BFA = Burkina Faso; CPV = Cape Verde; CIV = Cote d’Ivoire; GMB = Gambia; GHA = Ghana; GIN = Guinea; GNB = Guinea Bissau; MLI = Mali; NER = Niger; NGA = Nigeria; SEN = Senegal; SLE = Sierra Leone; TGO = Togo.

, **, and *** represents level of significance at 1%, 5%, and 10% respectively.

Unit Root Tests on Demand Shocks.

Source. Author’s computation.

Note. Where: GGDP = Global GDP; GDP = gross domestic product; Ben = Benin Republic; BFA = Burkina Faso; CPV = Cape Verde; CIV = Cote d’Ivoire; GMB = Gambia; GHA = Ghana; GIN = Guinea; GNB = Guinea Bissau; MLI = Mali; NER = Niger; NGA = Nigeria; SEN = Senegal; SLE = Sierra Leone; TGO = Togo.

, **, and *** represents level of significance at 1%, 5% and 10% respectively.

Unit Root Tests on Monetary Shocks.

Source. Author’s computation.

Note. Where: GGDP = Global GDP; GDP = gross domestic product; Ben = Benin Republic; BFA = Burkina Faso; CPV = Cape Verde; CIV = Cote d’Ivoire; GMB = Gambia; GHA = Ghana; GIN = Guinea; GNB = Guinea Bissau; MLI = Mali; NER = Niger; NGA = Nigeria; SEN = Senegal; SLE = Sierra Leone; TGO = Togo.

, **, and *** represent level of significance at 1%, 5%, and 10% respectively.

Zivot and Andrews Unit Root Tests.

Source. Author’s computation.

Note. The ZA critical value with intercept are −5.34 (1%), −4.93 (5%), and −4.58 (10%).

Impulse Response Results

The Impulse From Global Supply Shocks to Domestic Supply Shocks

The purpose of this estimation is to confirm how each country within the West African region responds to a global supply shock. If these countries respond in a similar way to a given global shock, then we can argue that a common monetary policy is beneficial for the region; otherwise, each country will need to develop its own individual monetary policy in response to a global supply shock. If these countries go-ahead and adopt a common monetary policy when the results prove otherwise, then it may prove costly to the region. We divide the graphs into two since plotting impulse responses of 14 countries on a single chart may look clumsy, while also representing the information on 14 different charts may also look unnecessarily too many. Therefore, we represent the impulse response function of the 14 African countries in two charts.

Figure 1(a) and 1(b) display the response of domestic countries in the Western African region to a global supply shock. All Francophone countries are plotted in Figure 1(a) while the remaining countries are represented in Figure 1(b). From Figure 1(a), the paths of Burkina Faso, Niger, and Senegal are similar as they both rise and fall together. This may be attributed to their origins as Francophone countries. The paths of Cote d’Ivoire and Togo are also similar, with different orders of magnitude. They both rise and fall over the period of estimation. This may also be because, as Francophone countries, they have a lot in common. The paths of Mali and Benin republic are very different from the rest of the group. An implication of these results is that global supply shocks affect Burkina Faso and Niger differently and permanently, while it affects the remaining countries within the first 8 years.

(a) The response of West African countries to a global supply shock; (b) The response of West African countries to a global supply shock.

From Figure 1(b), the paths of Sierra Leone and Guinea Bissau follow a similar pattern since they rise and fall together although at different magnitudes. Cape Verde, Guinea, Ghana, Gambia, and Nigeria is uniquely different from the rest of the two groups. Comparing the two charts, the paths of Cape Verde and Mali are almost similar, while the rest of the countries have different paths as earlier explained. The implication of this result is that the shocks derived from the global environment affect these countries in the short to medium term. However, in the long term, these shocks vanish and the unresponsive nature of these countries to global shocks over the long run becomes permanent. Therefore, we may conclude that a global supply shock affects the West African countries differently, with a bit of similarity between the Francophone countries; hence, the low level of integration within the region.

The Impulse From Global Demand Shocks to Domestic Demand Shocks

As estimated for supply shocks, the paper also use the impulse response to confirm how these countries respond to a global demand shock. However, all the countries were examined within a single graph this time around. This is because WAEMU countries adopt a uniform currency (CFA Franc), and impulse response results were also found to be the same across these seven countries. Therefore, a single chat was used to represent these countries that have ties to France as members of Francophone countries, and we compare how they perform to the rest of the group (Cape Verde, Ghana, Gambia, Guinea, Guinea-Bissau, Nigeria, and Sierra Leone).

The results show that Nigeria and Sierra Leone respond almost the same way to a global demand shock with different orders of magnitude, while Ghana, Cape Verde, and the CFA Franc countries respond almost the same way to a global demand shock over the 10-year horizon. This may be because Cape Verde and Ghana have stronger currencies compared to Nigeria and Sierra Leone. Furthermore, Ghana and Cape Verde’s similarity in their responses to a global demand shock with the CFA Franc countries may imply that these countries may have reasons to integrate if they meet other conditions. Finally, Gambia has a uniquely different path from the rest of the entire group, while Guinea and Guinea-Bissau have the same path. This is, however, surprising since they were never colonized by the same masters, and they adopted a different currency. However, as neighbors, they might have reasons to adopt a similar approach across their economies. This also may imply that the two countries may have reasons to integrate if they are able to fulfill other integration criteria. In essence, the impact of global monetary shocks on these West African countries are temporary (in the short to medium term). In the long run (8–10 years), these countries become unresponsive to global demand shocks (Figure 2).

The response of West African countries to a global demand shock.

The Impulse From Global Monetary Shocks to Domestic Monetary Shocks

As earlier stated, if the West African countries respond in a similar way to impulses from global monetary shocks, then they may integrate. Figure 3(a) and 3(b) displays the responses of West African countries to a global monetary shock. From Figure 3(a), it can be found that Benin, Burkina Faso, Côte d’Ivoire, Mali, Senegal, and Togo have almost similar experiences as they rise and fall almost together during the 10-year horizon. Thus, impulses from global monetary policy affect these countries in an almost similar way but with different magnitudes. This may be a result of the fact that these countries are all Francophone countries, and they adopt the same currency. However, Niger has a completely different path from the rest of its group.

(a) The response of West African countries to a global monetary shock; (b) The response of West African countries to a global monetary shock.

From Figure 3(b), Ghana and Guinea follow similar paths with different degrees of impulses as they fall together. Gambia and Nigeria are also slightly similar over the 10-year horizon, but the shocks from an impulse in global monetary policy affect them slightly differently. Cape Verde and Sierra Leone also rise and fall together from an impulse in global monetary policy, but Sierra Leone has a higher magnitude compared to Cape Verde. Finally, Guinea Bissau has its own unique path compared to the rest of the group. This may be because it is the only Lusophone country.

In essence, the West African region may not be able to integrate if they respond differently to a global monetary shock since they may need to adopt a different approach due to impulses from global monetary policy. We can then conclude that since West African countries respond differently to global supply, demand, and monetary shocks, it will be in the best interest not to form a monetary union. The result further buttresses previous outcomes by Houssa (2008) and Mati et al. (2019), whose studies adopted the impulse response function in determining the response of West African countries to global shocks.

Variance Decomposition Results

The variance decomposition results in Table 6 show how each country is affected by global and domestic (demand, supply, and monetary) shocks. The idea is that if these countries are affected to a higher degree by domestic shocks, then their paths should be idiosyncratic, and forming a monetary union may not be beneficial to the region. However, if these countries are dominated by global shocks, then a monetary union is beneficial for the region. For the global shocks, we consider the global supply shocks, global demand shocks, and global monetary shocks against each country’s individual shocks (supply, demand, and monetary shocks). If the addition of the three global shocks outweighs each country’s shocks, then we can argue that the region is dominated by global shocks and vice versa if the variance decomposition results of the domestic shock outweigh the three global shocks. We compute this result over a period of 10 years to verify whether the region is dominated by global or domestic shocks.

Variance Decomposition of Global Shocks to Domestic Supply Shocks.

Note. Where: GSS = the Global Supply Shocks; GDS = Global Demand Shocks; GMS = Global Monetary Shocks; B. Faso = Burkina Faso; C. Verde = Cape Verde; C. d’Ivoire = Cote d’Ivoire; S. Leone = Sierra Leone.

Table 6 displays the variance decomposition result of global shocks on domestic supply shocks. With the exception of Cape Verde, the results show that idiosyncratic shocks dominate all West African nations in the short- and medium-term. In the long run, Cape Verde responds more to global supply shocks compared to its domestic supply shock. Furthermore, the Senegalese economy is driven by a combination of global supply, demand, and monetary shocks, and the combination of these global shocks outstrips domestic supply shocks. The rest of the countries in the West Africa group are dominated by domestic or country-specific shocks.

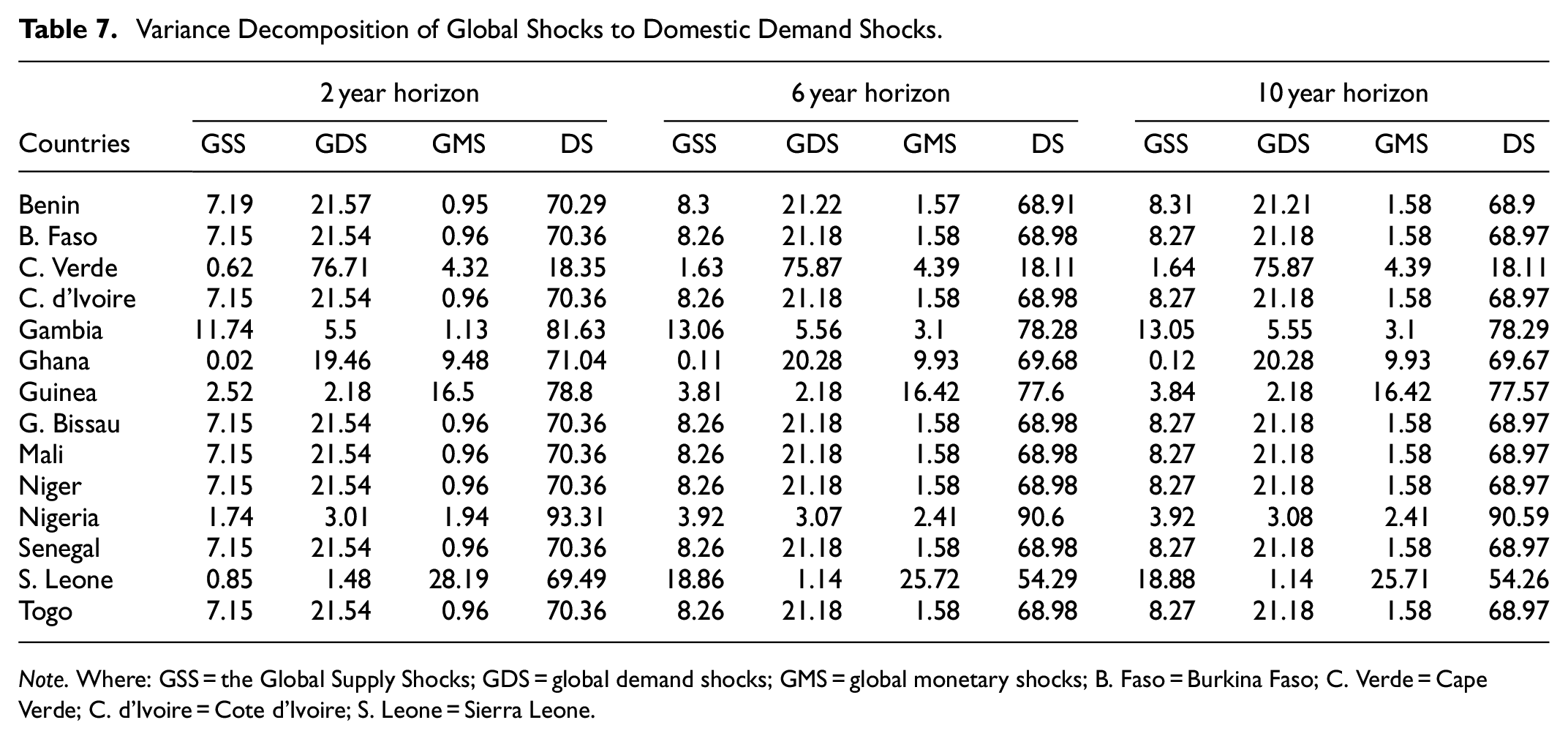

Table 7 displays the results of global shocks on domestic demand shocks. From the results, it can also be inferred that all the West African countries are dominated by domestic shocks rather than global shocks, except for Cape Verde whose economy is dominated by global demand shocks. This result was inline with the medium-term (6-year horizon) and long-term (10-year horizon) results. The implication of this result is that it may be wise for the West African countries to all have an independent monetary policy since 13 of the 14 examined countries have shocks that are idiosyncratic.

Variance Decomposition of Global Shocks to Domestic Demand Shocks.

Note. Where: GSS = the Global Supply Shocks; GDS = global demand shocks; GMS = global monetary shocks; B. Faso = Burkina Faso; C. Verde = Cape Verde; C. d’Ivoire = Cote d’Ivoire; S. Leone = Sierra Leone.

Table 8 displays the variance decomposition result of global shocks on domestic monetary shocks. The results show that in the short term (2-year horizon), all the West African countries are dominated by domestic shocks. That is, individual country monetary policy shocks affect individual countries more than global policy shocks. Over the 6-year horizon, this result changes for Cape Verde and Sierra Leone. These two countries are mostly driven by a combination of shocks within the global space. To be more specific, Cape Verde and Sierra Leone are driven by a combination of global supply and global monetary shocks and these shocks affect their domestic monetary policy more than the domestic monetary policy shocks.

Variance Decomposition of Global Shocks to Domestic Monetary Shocks.

Note. Where: GSS = the Global Supply Shocks; GDS = Global Demand Shocks; GMS = Global Monetary Shocks; B. Faso = Burkina Faso; C. Verde = Cape Verde; C. d’Ivoire = Cote d’Ivoire; S. Leone = Sierra Leone.

These outcomes were also found in the long run (10-year horizon) as a combination of global shocks affects monetary policy decisions in both Cape Verde and Sierra Leone. For the other West African countries, shocks affect them in an idiosyncratic way. That is, country-specific shocks have a more pronounced influence on monetary policy decisions than global shocks. The implication of these results as earlier mentioned is that it may be in the best interest of these West African countries not to form a monetary union since their economies are all thought to be affected by country-specific shocks except for Cape Verde and Sierra Leone over the medium to long term. But these cases for Cape Verde and Sierra Leone are not strong enough to ask the region to go into a monetary union.

Correlation of Shocks

We employ correlation analysis on the residuals of the structural VAR for the individual countries. Our focus here is on the residuals of the domestic shocks (or individual country shocks rather than the global shocks). For a country to form a monetary union, the probability value of their correlation coefficient has to be significant. Furthermore, if the correlation coefficient of these shocks is found to be negative, or less than 0.5, then we can say that these countries’ shocks are asymmetric, and it may not be in the best interest of these countries to form a union. A monetary union may become possible if these countries’ shocks are symmetric or positive and above 0.5. Therefore, the coefficient of correlation has to be significant, positive, and above 0.5 for a country to go into a monetary union. Tables 9 to 11 display the results of the correlation shocks amongst the 14 West African countries.

Correlation of Supply Shocks.

Note. Where: Ben = Benin Republic; BFA = Burkina Faso; CPV = Cape Verde; CIV = Cote d’Ivoire; GMB = Gambia; GHA = Ghana; GIN = Guinea; GNB = Guinea Bissau; MLI = Mali; NER = Niger; NGA = Nigeria; SEN = Senegal; SLE = Sierra Leone; TGO = Togo.

, **, and * represents significance at 1%, 5%, and 10%.

From Table 9, the correlation coefficients are negative and below .5, except for the coefficients of correlation for Burkina Faso and Mali. This implies that domestic supply shocks are affected by different factors across Ecowas countries and making a case for Burkina Faso and Mali alone may be too small. In Table 10, domestic demand shocks across all Francophone countries (Benin, Burkina Faso, Cote d’Ivoire, Guinea Bissau, Mali, Niger, Senegal, and Togo) are perfectly symmetric. That is, their correlation coefficient is 1 and significant, which implies that these countries’ shocks are common within the Ecowas region. The rest of the West African countries have correlation coefficients less than 0.5 and, in some cases, negative. This implies that shocks affecting them are specific to the individual countries.

Correlation of Demand Shocks.

Note. Where: Ben = Benin Republic; BFA = Burkina Faso; CPV = Cape Verde; CIV = Cote d’Ivoire; GMB = Gambia; GHA = Ghana; GIN = Guinea; GNB = Guinea Bissau; MLI = Mali; NER = Niger; NGA = Nigeria; SEN = Senegal; SLE = Sierra Leone; TGO = Togo.

,**, and * represents significance at 1%, 5%, and 10%.

Finally, Table 11, displays the correlation coefficient of domestic monetary shocks across the West African region. The results show that all Francophone countries (except for Guinea Bissau) have a strong and positive correlation coefficient. This may be because these countries all use the CFA Franc as their official currency. Furthermore, Guinea Bissau does not have a strong positive correlation with the rest of the Francophone countries. This maybe because it has not been using the CFA Franc as its official currency. The rest of the West African countries have correlation coefficients that are less than 0.5 and, in some cases, negative or insignificant. This implies that these countries’ monetary shocks are asymmetric, and a monetary union may not be possible. If they however decide to enter a monetary union, it may prove more harmful than good since individual countries will be responding to shocks differently. These results were in line with earlier studies such as Chuku (2012), Houssa (2008), Harvey and Cushing (2015), Mati et al. (2019), who also found correlation shocks to be asymmetric across the region.

Correlation of Monetary Shocks.

Note. Where: Ben = Benin Republic; BFA = Burkina Faso; CPV = Cape Verde; CIV = Cote d’Ivoire; GMB = Gambia; GHA = Ghana; GIN = Guinea; GNB = Guinea Bissau; MLI = Mali; NER = Niger; NGA = Nigeria; SEN = Senegal; SLE = Sierra Leone; TGO = Togo.

, **, and * represents significance at 1%, 5%, and 10%.

Discussion

The paper used annual data from 1986 to 2020 to establish whether the West African region is ready to form a monetary union. The data was sourced from WDI (2022) and IFS (2022) in order to establish the objectives. The paper adopted the SVAR methodology as well as used the residuals from the SVAR to compute the correlation analysis to establish if indeed the region is ripe for a monetary union. Based on the analysis, the results revealed that there are similarities in the ways by which global supply shocks affect some Francophone countries (Burkina Faso, Niger, and Senegal), while Cote d’Ivoire and Togo, as well as Sierra Leone and Guinea-Bissau, had similar responses to global supply shocks. The rest of the West African countries had dissimilar responses to global supply shocks. For global demand shocks, the results show that Nigeria and Sierra Leone follow a similar pattern, while Ghana, Cape Verde, and the CFA Franc countries also follow a similar pattern. For global monetary shocks, the findings demonstrated that Benin, Burkina Faso, Côte d’Ivoire, Mali, Senegal, and Togo follow an almost similar pattern. On the other hand, some other countries follow similar patterns in pairs. Take, for instance, Ghana and Guinea, Gambia and Nigeria, Cape Verde, and Sierra Leone. The results buttress previous studies by Houssa (2008) and Mati et al. (2019), whose studies also adopted the impulse response function in determining the response of West African countries to global shocks.

For the variance decomposition results, the paper showed that all West African countries except for Cape Verde were mostly driven by country-specific supply shocks in the short to long term. This implies that most of the supply shocks inherent in these countries are driven domestically and not globally. The results of the demand shocks were similar to those of the supply shocks. This implies that demand shocks affecting these countries were mostly country-specific, except for Cape Verde. For monetary shocks, the paper demonstrated that, in the short term, all West African countries are mostly driven by domestic shocks. However, over the medium to long term, domestic and international shocks are what primarily drive Cape Verde and Sierra Leone, while domestic monetary shocks are what primarily drive the remaining West African nations.

The results of the correlation analysis showed that West African countries are not driven by global supply shocks, as their coefficient of correlation fell below 0.5, or 50%. On the other hand, the Francophone countries had a similar demand shock, except for Guinea Bissau, meaning that their shocks were symmetric, implying that they may potentially form a monetary union. Similarly, the results of the monetary shock illustrated that shocks affecting Francophone countries were symmetric, implying that they may potentially form a monetary union. The rest of their West African pairs, however, were found to respond asymmetrically to shocks, meaning that it may not be in their best interest to form a union. These findings were in line with earlier studies such as Houssa (2008), Chuku (2012), Harvey and Cushing (2015), and Mati et al. (2019), who also found correlation shocks to be asymmetric across the region.

In essence, the results have shown that the West African countries are not yet ready for a monetary union as they have not satisfied the set criteria for a monetary union. Furthermore, the region has been unable to meet either of the primary or secondary convergence criteria. While some countries do meet some criteria, most do not meet these criteria. This result is valid across the impulse response, variance decomposition, and correlation coefficient (global supply shocks) results. However, this does not completely rule out the formation of a monetary union in the region. In fact, the West African countries that adopt the CFA currency seem closer to forming a monetary union than the rest of their West African counterparts. Even though the variance decomposition results of most of them are dominated by domestic shocks, their impulse response results are almost similar, while the correlation shock results of domestic demand and monetary shocks give strong reasons for the formation of a monetary union across the Francophone countries (apart from maybe Guinea Bissau).

The outcome of this study is also consistent with earlier studies such as Houssa (2008), Alagidede et al. (2012), Chuku (2012), Harvey and Cushing (2015), and Mati et al. (2019) which suggest that the behavior of global shocks (in our own case, global demand, supply, and monetary shocks) in the West African region is heterogeneous, while the region is dominated by domestic shocks rather than global shocks. Furthermore, the study showed that shocks across the region are idiosyncratic, and this outcome is in consonance with earlier studies such as Mati et al. (2019) and Chuku (2012). In essence, the main outcome from the study is that the West African region is not yet ripe for a monetary union, and it may be harmful if the region proceeds with a monetary union.

Conclusion

This study investigated the possibility of forming a monetary union within the West African region from the period of 1986 to 2020. The study adopted the structural VAR four-shock model based on the earlier works of Blanchard and Quah (1989). The results suggest that the West African region is not ripe for a monetary union. The study also suggests that even though the region is not yet ripe, the Francophone countries within the region are the closest to forming a West African monetary union compared to the rest of the West African countries based on the correlation of shocks and impulse response results. Despite the results, a piecemeal approach may be adopted where the Francophone countries (except for Guinea Bissau) who have already adopted a common currency continue the arrangement by adopting a common monetary policy, while the rest of their West African peers ascend to join over time.

This arrangement may however affect countries who do not join from the outset because as Bayoumi and Eichengreen (1997) as shown in his paper that the gains of the monetary union are only limited to its members, while the losses of not being part of the monetary union are borne by the remaining West African countries. In addition, the central banks of the West African countries cannot be coordinated by a regional central bank because shocks and policies that affect the region are idiosyncratic across countries within the region. A major policy implication would then be for the central banks to focus on how they can harmonize their monetary policies and remove all barriers to factor mobility for the synchronization of shocks and for all countries to meet the convergence criteria. This study concludes by echoing the recommendations of Ogunkola (2005) whose study opined that a convergence is necessary for the region to adopt a stable region-wide monetary union.

Despite the robust findings, the study results come with a limitation. It may be difficult to interpret the results for Liberia, which is within the bloc but was excluded from the analysis due to data unavailability from the period of 1986. However, the results are still robust because most of the other West African countries had dissimilar outcomes, meaning the findings from Liberia may not uniquely change the outcomes of the other countries within the study. For future research, the paper suggests carrying out a further test on all the West African countries, inclusive of Liberia, especially when there would not be any form of data constraint on any of the West African countries.

Footnotes

Acknowledgements

None.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Ethics Statement

The paper was conducted with integrity, fidelity, and honesty. The author openly takes responsibility for writing this paper without any form of assistance.

Data Availability Statement

Data available on reasonable request from the author.