Abstract

The COVID-19 pandemic has significantly altered consumer behavior. The significant influence of COVID-19 pandemic on consumption has been documented in an increasing amount of literature; however, limited focus has been placed on how consumer spending decisions differ depending on whether they employ contactless or contact payment methods under COVID-19 and normal conditions. The results of this study, which used a laboratory experiment carried out in the northern part of China, demonstrate that: (1) consumers’ intentions to spend more money when using contactless payments than when they use contact payments; (2) disgust and negative contamination act as mediating factors on the relationship between the degree of contact and consumer spending intention; and (3) COVID-19 moderates this mediating effect. This study concludes by discussing its theoretical contributions and managerial implications, alongside limitations and future research directions.

Plain Language Summary

Sanitation has become a major concern due to contagious feature of COVID-19. Under disease-rich environments, contact could be perceived as a contamination and disgust-inducing cue. There is surprisingly lack of research in degree of contact of payment and its influence on spending behavior since people tend to normatively believe that money is dirty. To test this, a 2 (degree of contact: Contactless payment vs. Contact payment) × 2 (consumption context: COVID-19 condition vs. Normal condition) between-subjects design was employed. This study further proposes and empirically tests two theoretical frameworks to explore its psychological mechanisms and boundary conditions. Results indicate that degree of contact as a payment attribute negatively influence spending intention, specifically, contact payment increases disgust and negative contamination, thus decreases intention to spend, and COVID-19 pandemic exerts a moderating effect on the relationship. Practitioners will be able to use the findings from this study to improve quality of payment services in the context of COVID-19 pandemic.

Introduction

The outbreak of coronavirus diseases (COVID-19) pandemic has affected nearly every aspect of people’s daily life. Consumers began to change their consumption patterns and spending habits involuntarily and voluntarily due to wide spread of the virus (Zwanka & Buff, 2021). With concerns about the transmission of virus through cash and payment surfaces, the use of contactless payment methods has become increasingly popular and favored by consumers to prevent physical contact with cash or banknotes during the crisis (Flavián et al., 2020). According to an online survey conducted in 2020 by Rapyd, a global fintech organization, as the result of COVID-19 pandemic, 54% of US consumers surveyed are concerned about handling physical banknotes or coins, and 60% of them have plan on using contactless payment in the future.

A growing body of research has been generated to examine the disruptive and negative impact of COVID-19 pandemic, specifically, the pandemic has been linked to negative psychological outcomes, including anxiety and depression (Mazza et al., 2020), COVID-19-related fear (Ahorsu et al., 2022), and feelings of loneliness and social isolation. Such psychological consequences may subsequently prompt irrational consumer behavior such as conformity (Li et al., 2021). Furthermore, the pandemic has also led to financial stress and economic challenges, for example, Guo et al. (2022) observed that COVID-19 affects household financial behaviors, such that saving and borrowing behaviors were more sensitive to COVID-19 than insurance and investment behaviors. Individuals may engage in impulsive and irrational buying behaviors as a means of coping with negative psychological consequences such as stress and anxiety (Burke et al., 2010).

Most previous literature on contactless payment predominantly concentrates on mobile payment, building their research rationale based upon existing frameworks such as Technology Acceptance Model (Flavián et al., 2020), Innovation Diffusion Model(Oliveira et al., 2016), Mental Accounting Model (J. Park et al., 2019), to explain consumer response toward contactless payment. While another stream of literature, which is more relevant to our research, delves into the consumer evaluation process regarding payment types based on specific payment attributes such as payment denomination (single large denomination vs. multiple smaller denominations) as examined by Raghubir and Srivastava (2016), and physical appearance of payment (crisp vs. worn) as explored by Di Muro and Noseworthy (2013).

The current paper is timely in its focus on consumer evaluations of contactless and contact payment types under COVID-19 pandemic. Though existing research has divided payment in terms of appearance or denomination, this research is among the first to consider degree of contact as a key attribute of money and explore consumer decision making of contact and contactless payment. Specifically, contact payment is less preferred by consumers because of the emotional responses of negative contamination and disgust, which is strengthened by COVID-19 pandemic. We further identify and empirically test the psychological mechanism explaining consumer evaluation process of choosing contactless and contact payment, and the moderating effect of COVID-19 pandemic. Finally, we provide theoretical and managerial implications based on the moderated mediation models identified and validated in this paper. This study will contribute to the understanding of how COVID-19 pandemic has impacted consumer payment preferences. The findings may help businesses and policymakers develop strategies for promoting the use of contactless payment methods, which may be viewed as a safer option and which could contribute to reducing the risk of infection. The primary contribution lies in connecting these emotional responses elicited by physical contact of payment, which has not been observed in existing research. Further, this paper contributes to the growing body of research on the impact of COVID-19 pandemic on consumer behavior and decision making. By exploring the specific social context of payments, this study provides valuable insights into how the pandemic is shaping our monetary interactions and spending patterns.

Theoretical Background

Payment Type and Spending

The basic notion of invariance has been challenged by previous research in the context of payments that looked at payment effect and how various payment methods affect consumer spending behavior (Chatterjee & Rose, 2012; Hirschman, 1979; Raghubir, 2006; Raghubir & Srivastava, 2002). According to Raghubir (2006), the representativeness heuristic in the payment domain implies that the type and denomination of payment could skew consumers’ evaluations of it. Prior knowledge has discovered that there is a “Credit Card Premium” phenomenon—that is, when people use credit cards instead of cash or debit cards, they tend to spend more (Incekara-Hafalir & Loewenstein, 2009; Prelec & Simester, 2001). Furthermore, Laran and Salerno (2019) showed that the mode of payment may have an impact on the degree of self-control displayed during the purchase. Raghubir and Srivastava (2016) conducted a study in which participants were given either real money or monopoly money to make purchases. They found that participants who used real money were more reluctant to spend compared to those using monopoly money. This indicates that the psychological detachment from actual currency can lead to more reckless spending behavior. In addition to type of payment, perceived control and psychological ownership associated with a payment method can also influence spending behavior. Wang et al. (2020) found that consumers who felt a higher level of control and psychological ownership over their payment method were more likely to make impulsive purchases. This suggests that when consumers feel a sense of ownership and control over their payment method, they may be more prone to spending without careful consideration.

In recent years, digital payments have drawn a lot of interest, which has led to the accumulation of a sizable body of research on the factors that influence adoption. For example, de Luna et al. (2019) suggests that four distinct constructs—perceived utility, perceived ease of use, perceived security, and subjective norms—be considered in the context of mobile payments when analyzing the literature on technology adoption. Convenience, perceived usability, expressiveness, perceived ease of use, and trust are among the motivational factors that influence behavior (Chawla & Joshi, 2023; Jaiswal et al., 2022). The main obstacles to contactless technology acceptance are potential hazards such premium pricing, complexity or difficulty in use, and a lack of critical mass (Ismail et al., 2022). Menapace et al.’s (2018) study on the impact of time constraints on the adoption of digital payments discovered that when customers faced time constraints, they were more likely to engage in impulsive buying through mobile payment methods. Besides, perceived ease of use and the perceived technological opportunities of mobile payment systems positively influenced consumers’ using intentions (Sánchez-Fernández & Iniesta-Bonillo, 2017).

Most studies that describe consumer attitudes toward digital payments are based on well-known theories. For instance, Flavián et al. (2020) used research based on the technology acceptance model (TAM), Oliveira et al. (2016) used the innovation diffusion theory, and J. Park et al. (2019) used the mental accounting theory. Trütsch (2014) looked into how digital payments affected expenditure in terms of transactions and proposed that contactless credit and debit cards raise the ratio of spending to income. Daragmeh et al. (2021) investigated the drivers that impact behavioral intention to accept Fintech payments in the COVID-19 era. They expanded TAM to include perceived COVID-19 risk and subjective norm. While they discovered both direct and indirect effects of subjective norm on behavioral intention, they also discovered significant direct effects of perceived COVID-19 risk on behavioral intention. After critically analyzing previous studies on digital payments, Dahlberg et al. (2015) came to the conclusion that the overemphasis on technology and adoption, together with the results and conclusions generated, is still lack of diversity in this context. It is therefore encouraged to investigate new research subjects, particularly comparisons with non-digital payment methods during and after the COVID-19 pandemic.

Disgust

Disgust is an unpleasant emotion that is often associated with the avoidance of certain stimuli. In the context of consumer behavior, disgust can influence the way people evaluate and purchase products and services. Research has shown disgust is associated with repulsive feelings and a strong desire to avoid or reject something that might hasten the initiation of protective mechanism (Argo et al., 2006; Rozin et al., 1989; Rozin & Fallon, 1987; Rozin & Nemeroff, 1990). Disgust is frequently felt by consumers, for example, six of the top-10 frequently purchased products (like trash bags, diapers and cat litter in supermarket) elicit feelings of disgust (Morales & Fitzsimons, 2007). Research on the psychological endowment effect provides theoretical evidence that receiving a specific object perceived as unpleasant leads to a negative affective reaction toward the object and consequently lowers valuation of the object. For example, Lerner et al. (2004) explain that consumers’ negative emotional states like disgust (or sadness) can lower the appreciation of the endowed object. In the context of payment, consumers may normatively tend to believe that payment is dirty. Indeed, Abrams and Waterman (1972) has found that there are harmful germs like fecal bacteria on 13% of coins and 42% of bills. Di Muro and Noseworthy (2013) argue that consumers want to get rid of worn bills because they are disgusted with contamination from others, and disgust affects consumer spending decisions.

There is a strong correlation between physical contact and disgust. It usually takes less to make someone feel disgusted to think about touching or even being close to certain objects than it does to actually touch them. Regardless of the specific object that consumers find repulsive, the effects of these objects can be comparable. According to a body of prior studies (Rozin et al., 1986, 1992; Rozin & Fallon, 1987), consumers routinely lower their ratings of handled objects because they are disgusted by the contamination from others.

Negative Contamination

Negative contamination refers to the value of an object is decreased through physical contact. Consumers perceive less values on products when they have been touched by others (Argo et al., 2006). This justifies the phenomenon that second-hand goods are often devalued and consumers show aversion or low desirability for used items. Positive contamination, on the other hand, can be interpreted as the opposite value of negative contamination, which refers to the value of an object could be increased through contact, for example, fans may feel positively toward items used by the celebrities they support.

A frequently handled object like cash, transferred numerous times on a daily basis, has a low ownership value (Peck & Shu, 2009). Moreover, the more frequently money is contacted, the more likely negative contamination would occur, especially under the condition that people who touched the money before remain largely anonymous (Argo et al., 2006). Therefore, although both positive and negative contamination are under investigation in the previous literature, consumer spending decisions are largely biased by negative contamination (Di Muro & Noseworthy, 2013).

Consumers often utilize the signal of physical contact as a contamination cue, according to product contagion theory. Contamination can even happen in the absence of actual physical contact since the perception of contact between objects is enough to trigger a contagion effect (Argo et al., 2006). For instance, Morales and Fitzsimons (2007) contend that when customers thoroughly examine a product on a store shelf or place it in a supermarket cart, they will strongly feel polluted. Meng and Leary (2021) have brought attention to the fact that a product’s recycled nature might act as a contagion cue, causing feelings of disgust and perceived contamination, which in turn lowers purchase intentions for those products.

Social Context Effect of COVID-19

Consumer spending behavior is significantly influenced by specific consumption situation, and COVID-19 pandemic has surpassed the impact of a typical disease. This global health crisis has brought profound changes to consumer attitudes and behaviors, triggering strong emotional responses that affect decision-making tendencies (Galoni et al., 2020). During this pandemic, people’s sanitary concerns are expected to be higher than ever before in their daily lives. Although scientific evidence suggests that the possibility of transmitting the virus through banknotes is low compared to other frequently-touched objects, negative emotions associated with cash usage are expected to be heightened during the COVID-19 era. Despite these trends, the behavioral changes and emotional consequences elicited by this pandemic remain largely understudied. COVID-19 can be viewed as a social context, and therefore, its tremendous impact on consumer decision-making should be thoroughly examined within a modified framework.

Research Model and Hypotheses

A compressive review of literature on contagion has achieved a consensus that physical contact elicits negative psychological consequences and further exerts influence on consumer behavior. Product contagion theory suggests that disgusting products are believed to pass their offensive properties through contact (Morales & Fitzsimons, 2007). This contamination effect not only occur in product area, in money domain, Di Muro and Noseworthy (2013) found that money appearance affects spending intentions through the mediating effects of disgust and negative contamination. However, disgust and negative contamination can inherently correlate highly with each other. Note that, due to the multicollinearity problem of regression analysis, it is difficult to simultaneously examine the effects of highly correlated constructs using a statistical model. Thus, we build two causal models (hereafter, CM 1 and CM 2) examining COVID-19 effect in consumer decision to spend with contactless and contact payment. CM 1 uses disgust as a mediator and CM 2 uses negative contamination as a mediator. It is possible to interpret the link between the two causal models based on the causal relationship between the two mediators, since disgust (in view of consumer emotional response to payment) is the cause of negative contamination (in view of consumers’ valuation on payment) (Argo et al., 2006; Morales & Fitzsimons, 2007; Rozin et al., 1992).

A system of two regression models can be used to specify each of the two causal models. A mediator model is one that depicts how a focal predictor affects a mediator. A moderator modifies the focus predictor’s effect on the mediator in the mediator regression model. The other is a regression model for dependent variables that captures how the mediator and focal predictor affect a dependent variable. Mathematically, the system of two regression models is expressed as a four-variable system, which is stated as:

where X, M, W, and Y indicate the focal predictor (degree of contact: contact payment vs. contactless payment payment), the mediator (disgust in CM 1 and negative contamination in CM 2), the moderator (consumption context: COVID-19 condition vs. Normal condition), and the dependent variable (intention to spend), respectively, and

One may argue that it is possible to consider the interaction term between the focal predictor and the mediator. However, the interaction effect implies that the mediator is also a moderator in the relationship between the focal predictor and the dependent variable. We do not consider such a case in the dependent variable regression model. In addition, this modified framework (not considering such an interaction effect) is also consistent with the framework used by Di Muro and Noseworthy (2013). We illustrate the causal relationships in the two systems of two regression models in Figures 1 and 2.

Causal model with disgust as mediator (CM 1).

Causal model with negative contamination as mediator (CM 2).

We empirically examine the psychological mechanism for the impact of COVID-19 pandemic based on the causal paths (represented with the regression coefficients) in the two systems of regression models (see Equations 1 and 2). In other words, we empirically validate the psychological mechanism with hypotheses on the regression coefficients in systems of regression models.

The causal effect of the focal predictor on the dependent variable implies that consumers make different spending decisions with contactless and contact payments (as well as credit cards and cash examined in previous research). This notion is summarized and tested using Hypothesis 1. The causal effect of the focal predictor on the mediator implies that consumers perceive disgust and negative contamination differently resulting from contactless and contact payment, which have been summarized and tested with Hypothesis 2 and 3. In addition, the moderation effect of COVID-19 pandemic implies that the virus alters consumer perceptions of disgust and negative contamination. The moderation effects have been summarized and tested through Hypothesis 4 and 5. All the hypotheses are represented as follows.

Experimental Study

Experimental Design

Two hundred five participants were recruited from a university campus in a Northern city of China to enroll in this experiment in exchange for a small monetary reward following the convenience sampling technique. They were randomly assigned to a 2 (degree of contact: Contactless payment vs. Contact payment) × 2 (consumption context: COVID-19 condition vs. Normal condition) between-subjects design. To address biases that arise from self-reported measures (Ng & Feldman, 2013), we employed various metrics. All respondents were informed that collected data will only be used for research purpose and anonymity issue will be maintained; additionally, we reversed the coding of some items to reduce monotonic responses from the participants (Malhotra et al., 2006); besides, an attention-check question (“This question is just to make sure that you are paying attention to this survey. Please mark ‘6’ as your response”) was employed. After excluded five of them who failed this attention-check question from the sampling, 200 valid cases remained as the sample (among whom, 51% females; Mage = 32 years) and enrolled in a laboratory study.

We conducted this experiment in a Northern city of China, considering the fact that user number and penetration rate of contactless payment in China are relatively high, and most young people in China use contactless payments (mobile payment) in their daily life. We applied a mobile payment (WeChat pay) as contactless payment scenario, and cash (CNY) as contact payment scenario. because WeChat Pay (together with Alipay) has dominated person-to-person, retail or other business transactions in China, and mobile payments requires less contact than other payment types including credit cards. In addition, we manipulated the consumption context into two scenarios: whether COVID-19 pandemic is in a serious state or whether it ended and returned to normal, based on manipulation used in Grashuis et al. (2020).

After reading one of the two scenarios about COVID-19 pandemic, participants were instructed to engage in a virtual shopping task in the next step. They were asked to use either contactless payment or contact payment depending on whether they are allocated to the Contactless payment condition or the Contact payment condition. Then they were asked to see the picture of the cash form of 50 CNY if they are allocated into Contact payment condition, or Wechat transfer screenshot of 50 CNY if they are in Contactless payment condition, and they commonly are shown a product list. The product list included 10 products (e.g., bar soap, toothpaste, shampoo, hand cream, etc.), which were adapted from Di Muro and Noseworthy (2013). The prices of the products ranged from 5 CNY (for bar soap) to 42 CNY (for hand cream). At the end of the questionnaire, participants were asked to do virtual shopping with the virtual payment they received and keep the remaining money.

Measures

Disgust was measured by using the items as follows. “The current payment type is disgusting,”“The current payment type is unclean,”“The current payment type is dirty,” and “The current payment type is revolted” (Morales & Fitzsimons, 2007). The items were measured with a nine-point Likert scale. Negative contamination was measured by asking participants the two following questions. “How dirty was the payment type you just used?” and “How unsanitary was the payment type you just used?” This measure was adapted from Argo et al. (2006). The items were measured with a nine-point Likert scale.

Spending intention was measured by asking participants the following question. “How likely/probable/certain are you going to spend and buy the products from the list?” Participants were asked to respond three times with the range of “Unlikely (1) - Likely (9), Improbable (1) - Probably (9), and Uncertain (1) - Certain (9).” This measure was adopted and modified from J. Park et al. (2005).

In addition, participants were asked to respond to basic demographic profile questions, such as gender and age. All the measurement items were firstly constructed based on previous literature in English. We developed Chinese versions for the use of the questionnaire because the study was conducted in China, following the back-translation method recommendation by Brislin (1980).

Experimental Results

Manipulation Checks

A manipulation check for the consumption situation was conducted with the following question. “How do you consider the current seriousness of COVID-19 pandemic?” The item was measured with a nine-point Likert scale. Results indicated that participants rated more seriously COVID-19 pandemic in COVID-19 condition (manipulated with a scenario for increasing new cases of COVID-19) than in Normal condition (manipulated with a scenario for the end of COVID-19 due to the successful development of a vaccine) (M = 8.09 in COVID-19 condition and M = 1.93 in Normal condition; t = 55.788, p < .001). This implies that the manipulations of COVID-19 and Normal conditions were accomplished.

A manipulation check for contact was conducted with the following question. “How do you consider the degree of contact of the current payment type you just used?” The item was measured with a nine-point Likert scale. Results indicated that participants rated the lower degree of contact in Contactless payment condition than in Contact payment condition (M = 2.68 under the Contactless payment condition and M = 7.55 under the Contact payment condition; t = −42.744, p < .001). This implies that the manipulation worked as intended.

Reliability and Validity

Before we test the hypotheses with the two causal models (CM 1 and CM 2) represented by the system of the regression models (Equations 1 and 2), we conducted Principal Component Analysis with SPSS 24.0 program to test the convergent validity of disgust (measured by the four items) and spending intention (measured by the three items) used in CM 1, and the convergent validity of disgust (measured by the two items) and spending intention (measured by the three items) used in CM 2.

Table 1 summarizes the results of Principle Component Analysis for CM 1 and CM 2. The PCA for CM 1 showed that two components were extracted for disgust and spending intention, explaining cumulatively 92.9% of the total variances. The PCA for CM 2 showed that two components were extracted for negative contamination and spending intention, explaining cumulatively 91.1% of the total variances. In addition, reliability test was examined with operation of Cronbach’s Alpha. The Cronbach’s Alpha values for disgust, negative contamination, and spending intention were .978, .896, and .953, respectively. They were all above .7, indicating a good internal consistency for each construct. Finally, we confirmed that disgust and negative contamination were highly correlated with each other: the correlation between the average of the four items for disgust and that of the two items for negative contamination was .974. The correlation explains why we test the hypotheses with the two independent causal models (CM 1 and CM 2).

Factor Matrix and Reliability Test.

Note. The factors were extracted by Varimax with Kaiser Normalization Extraction Method.

Testing Hypotheses

We tested the hypotheses with CM 1 (using disgust as the mediator) and CM 2 (using negative contamination as the mediator) represented with the system of two regression models. In the two causal models, we measured the degree of contact (as the focal predictor) with a binary variable where “1” indicates the contactless payment (WeChat payment as contactless payment) and “0” does the contact payment (CNY as contact payment), and the consumption context (as the moderator) with a binary variable where “1” indicates COVID-19 condition and “0” does Normal condition. In addition, we averaged the items for disgust (as the mediator in CM 1), negative contamination (as the mediator in CM 2), and spending intention (as the dependent variable), respectively. We then used the averages in the two causal models.

Testing Hypotheses in CM 1

We used PROCESS macro for SPSS to estimate CM 1 corresponding to Model 7 in Hayes (2017). The results were summarized in Table 2. The mediator regression model (Equation 1) showed that disgust was affected negatively by the degree of contact measured with the contact and contactless payment in that the effect of the contactless payment on disgust was negative (α = −3.05, t = −25.50, p < .001), where the effect of the contact payment remains fixed as zero. However, disgust was affected positively by the consumption context measured with COVID-19 and Normal conditions (

The Estimation Results in CM 1.

Note. X indicates the degree of contact (0 and 1 indicate the contact and contactless payment, respectively). M indicates disgust. W indicates the COVID-19 Pandemic (0 and 1 indicate the Normal and COVID-19 conditions, respectively). Coeff. indicates unstandardized regression coefficients.

The direct effect of the focal predictor (degree of contact) on the dependent variable (spending intention) did not cross zero and was significant (95% CI [1.59, 3.12]). This implies that contactless payment type elicited higher spending intension than contact payment. Thus, H1 was given support. This confirmation is consistent with previous explanations for interpreting consumer spending decisions with cash and credit cards, such as the temporal separation of the consumption decision and the actual payment (Prelec & Loewenstein, 1998), pain of payment (Prelec & Loewenstein, 1998; Raghubir & Srivastava, 2008), and consumers’ focuses on cost-related aspects and benefit-related aspects (Chatterjee & Rose, 2012). The index of the moderated mediation model (represented by CM 1) was significant (Effect = 1.42; 95% CI [0.92, 1.95]), suggesting that COVID-19 moderated the effect of the focal predictor (degree of contact) on the mediator (disgust), and subsequently on the dependent variable (spending intention).

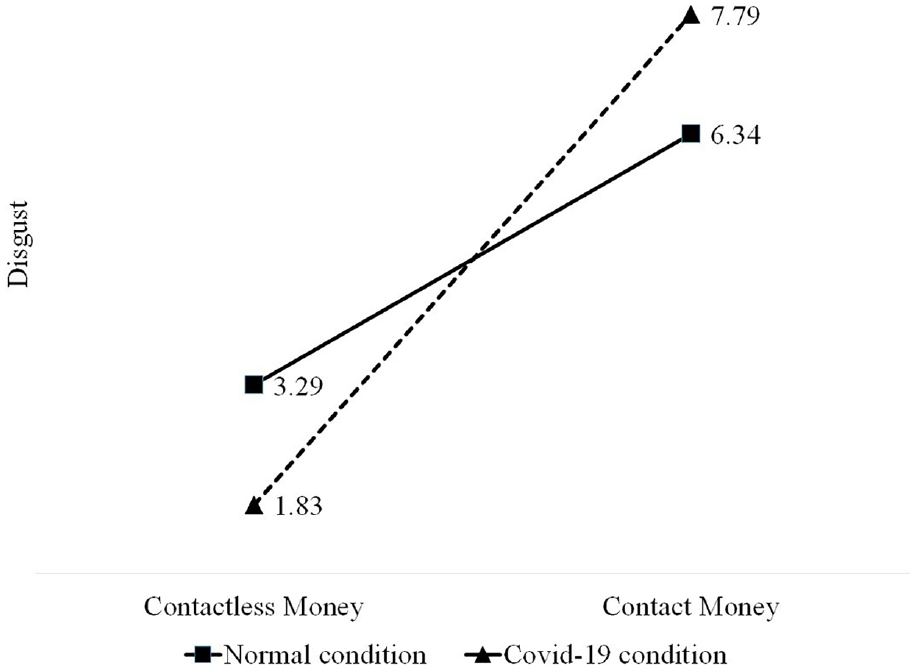

Figure 3 summarizes the estimation results using the unstandardized regression coefficients. The causal relationships reported in Table 2 can be understood graphically with Figure 3. In addition, Figure 4 illustrates the interaction effect between the focal predictor (measured with 0 for the contact payment and 1 for the contactless payment payment) and the consumption context (measured with 0 for Normal Condition and 1 for COVID-19 Condition) on the mediator (disgust). In Figure 4, we displayed the two estimated simple regression lines representing the effect of the focal predictor on disgust at the two levels of the consumption context (as the moderator), according to the recommendations by the literature on moderation effects (Aiken et al., 1991; Dawson, 2014). Consequently, disgust in Figure 3 was calculated using the unstandardized regression coefficients estimated by the mediator regression model in CM 1. The slope of each simple regression line indicates the simple effect of degree of contact (as the focal predictor) at each level of the consumption context (as the moderator). The simple effect captures the total effect of the focal predictor at a specific level of the moderator in the simple slopes analysis used as a subsequent analysis of the moderated regression analysis (Irwin & McClelland, 2001; Jaccard & Turrisi, 2003; MacCallum et al., 2002). According to Figure 4, one can interpret that COVID-19 moderated the effect of degree of contact on disgust. Therefore, H2 and H4 were verified (see Table 2 and Figure 3).

Graphical Results of CM 1.

Moderation Effect of COVID-19 pandemic in CM 1.

Testing Hypotheses in CM 2

We used PROCESS macro for SPSS to estimate CM 2 (using negative contamination as the mediator) corresponding to Model 7 in Hayes (2017). The results are summarized in Table 3. The mediator regression model (Equation 1) showed that negative contamination was affected negatively by the degree of contact measured using the contact and contactless payment (

The Estimation Results in CM 2.

Note. X indicates the degree of contact (0 and 1 indicate the contact and contactless payment, respectively). M indicates negative contamination. W indicates the COVID-19 Pandemic (0 and 1 indicate the Normal and COVID-19 conditions, respectively). Coeff indicates unstandardized regression coefficients.

The direct effect of the focal predictor (i.e., degree of contact) on the dependent variable (spending intention) did not cross zero and was significant (95% CI [2.00, 3.59]). This result can be interpreted in the same way that was used to interpret the direct effect in CM 1. The index of moderated mediation model (represented by CM 2) was significant (Effect = 1.08; 95% CI [0.60, 1.60]), suggesting that COVID-19 moderated the effect of the focal predictor (degree of contact) on the mediator (negative contamination), and subsequently on the dependent variable (spending intention).

Figure 5 summarizes the estimation results using the unstandardized regression coefficients. Along with Figure 5, the causal relationships reported in Table 3 can be understood graphically. Figure 6 illustrates the interaction effect between the focal predictor (measured with 0 for contact payment and 1 for contactless payment payment) and the consumption context (measured with 0 for Normal Condition and 1 for COVID-19 Condition) on the mediator (negative contamination), based on the procedure used in the analysis of CM 1. Accordingly, Figure 6 shows that COVID-19 conditions moderated the effect of degree of contact on negative contamination. Therefore, H3 and H5 were verified (see Table 3 and Figure 5).

Graphical results of CM 2.

Moderation effect of COVID-19 pandemic in CM2.

Discussion

This study investigated the relationship between degree of contact, disgust, negative contamination, and consumer spending in the context of COVID-19 pandemic. The current research revealed that consumers perceive contact payment to be more negatively contaminated and disgusting than contactless payment, and this difference in perception affects their spending intention. The results obtained were consistent with our pre-registered predictions indicating that COVID-19 pandemic has mitigated the consumer perceptions of disgust and negative contamination associated with contact payment. Thus, the psychological mechanisms specified and validated in this paper provides the intuitive explanation for the increasing trend of digital transformation of payment.

Theoretical Contributions

First, this study provides an initial comprehension of how consumers perceive contactless and contact payments and its impact on consumer spending behavior. Specifically, this research is among the first to reveal an implicit association between the contact nature of payment and negative contamination and disgust. Although previous studies have identified touch as a crucial source of contamination felt by consumers (Argo et al., 2006), scant attention has been given to investigate whether touch is involved in payment and how it may be linked to psychological responses of negative contamination and disgust that could impact consumer intentions. This research aligns with existing knowledge that emphasizes how consumers’ spending decisions are significantly influenced by how they perceive and interpret payment. However, this research differentiates from existing literature in that prior research on payment attributes has mainly focused on comparing payment types that require contact, such as cash and credit cards. This article contributes uniquely to the literature by exploring another crucial aspect of payment (i.e., the degree of contact) and categorizing payments into contact and contactless forms. This classification of payment could be applied generally to all payment methods since payment systems now encompass a variety of digital technologies beyond traditional cash or card transactions (de Luna et al., 2019).

Second, the current study enriches the literature on consumer behavior under crisis and social emergencies. Extensive research has already delved into the momentous influence that COVID-19 has had on consumption patterns, including preferences for online shopping and conformity behavior (Donthu & Gustafsson, 2020; Li et al., 2021), and it is highly probable that these changes in consumer behavior will continue to persist even when the pandemic ultimately recedes (Sheth, 2020). Despite the increasing significance of digital technology in allowing payment via electronic means and the impact of the pandemic on consumer behavior, a thorough understanding of the changes in payment method decision making during the pandemic remains unexplored. This paper makes a unique contribution since it identifies the psychological mechanism for consumers’ digital shift toward contactless payment after the outbreak of COVID-19. The acceleration of consumer adoption and usage of contactless payment can be explained by the psychological mechanism driven by disgust and the possibility of being contaminated by contact with contact payment (such as cash or other touching screens or credit cards). The psychological mechanism implies that the pandemic is leading to major changes toward contactless payment from consumer psychology perspective. This is consistent with the assumption that people become more health conscious after the outbreak of the pandemic and try to keep away from contamination cues (Meng & Leary, 2021).

Managerial Implications

The rapid technological development over the past several decades transformed the way people live and consume (Alkhowaiter, 2020). This study highlights a growing preference for contactless payment as consumers seek safer and more hygienic payment alternative during the pandemic. This is consistent with the prior knowledge suggesting that when individuals are exposed to disease cues, they tend to avoid typified products. This can be attributed to the intrinsic desire to avoid the possibility of infection, with typified products often being linked to a larger population and potentially posing a higher risk of being infected (Huang & Sengupta, 2020).

Our research findings offer valuable insights into the implementation of contactless payment strategies for companies seeking to improve their operations in this area. Based on these results, we provide several recommendations that can guide companies and entrepreneurs toward successful implementation. First, although contactless payment (e.g., mobile payment) have gained popularity in recent years, the adoption rate of contactless transactions varies across countries, regions and individual characteristics, the tendency becomes even more obvious especially under crisis time like COVID-19 pandemic, resulting in a noticeable imbalance in the development of contactless payment. Managers in the payment industry could consider adapt their marketing strategies to emphasize the touch-free nature of contactless payment, other strategies boosting contactless payment adoption may include broaden the implementation scenarios that accept contactless payment, for example, Apple Pay and Google Pay allow consumers to make payments both on brick-and-mortar and online retailers, which can help to drive the adoption of contactless payment methods among existing and potential customers. Managers could also invest in necessary technical infrastructure to support contactless payment options, including upgrading POS systems, training employees on how to use these systems, and integrating them with customer relationship management systems. Upgrading infrastructure to support contactless payments allows for faster and more efficient transactions. This, in turn, leads to improved customer satisfaction and helps to reduce queuing times at point-of-sale terminals. Contactless payments eliminate the need for customers to fumble around with cash or input their PIN, thereby speeding up the transaction process. Improved infrastructure also ensures enhanced security when it comes to contactless payments. Newer technologies like near-field communication (NFC) and radio-frequency identification (RFID) chips have made it easier for customers to make payments without having to share sensitive information such as personal identification numbers (PINs) or card details. Advanced security features such as tokenization, encryption, and biometrics can be implemented using infrastructure upgrades. Besides, managers should address security and privacy concerns by implementing robust security systems, familiarizing staff with contactless technologies, and equipping them with the skills needed to assist customers with contactless transactions to prevent unauthorized transactions and protect customer data.

Second, considering the prolonged nature of COVID-19 pandemic, it is imperative that the government takes an active role in various interventions aimed at promoting public health. Some essential components of public health that require government attention include disease prevention and control, which entails identifying and tracking diseases, implementing measures to prevent their spread, and controlling outbreaks when they occur. Another crucial aspect is health promotion and education, whereby information and resources are provided to assist individuals in making healthy choices and preventing diseases. Addressing environmental health is equally important, which focuses on identifying and addressing factors that can impact health such as air pollution, unsafe drinking water, and hazardous waste. Furthermore, the government should control the spread of rumors associated with COVID-19 pandemic to prevent excessive panic. Emergency preparedness and response are also critical, involving planning for and responding to public health emergencies such as natural disasters, disease outbreaks, and bioterrorism. Health policy and advocacy are imperative, which involves creating policies and laws that impact public health and advocating for policies that promote health and well-being. Finally, the provision of psychological counseling is crucial in managing the pandemic. Psychological reactions of disgust and negative contamination perceptions are not limited to situations where individuals come into contact with physical currency. These responses also arise when individuals encounter second-hand items or products made from recycled plastic bottles in the fashion industry, even though such practices are generally regarded as ethical (Meng & Leary, 2021). The underlying rationale for this phenomenon is that people perceive these items as contaminated, leading to a decrease in purchase intentions. The perception of contamination and feelings of disgust are further exacerbated by the ongoing threat of the pandemic. Consequently, offering psychological counseling both online and offline and implementing other strategies aimed at mitigating negative emotions and promoting rational decision-making could fundamentally enhance individuals’ behavior in response to the pandemic.

Limitations and Direction for Future Research

Notwithstanding the theoretical and managerial implications suggested in the current research, it is imperative to acknowledge the presence of certain limitations that could potentially form the basis for future research. First, the experiment in this study was conducted using offline purchase scenarios, where participants were instructed to imagine entering a store, select the products they would like to buy, and then pay. With the rapid development of online shopping, various e-commerce payment systems and online payment systems are becoming increasingly popular. Thus, scholars may extend the research boundaries and investigate consumers’ spending decisions in online environments. It is also worth examining consumers’ spending decisions in various consumption contexts, because consumers tend to make different decisions to spend different payment types in different situations.

Second, this research has examined the effect of COVID-19 pandemic using two manipulated scenarios. From the experimental study in this paper, it can be logically assumed that the adoption pace and usage rate of contactless payment by consumers will increase during the spread of COVID-19 and decrease after the end of COVID-19 pandemic. In other words, this research has not considered the difference between two possible effects of COVID-19 pandemic. One is the effect resulting from the spread of COVID-19 and the other is the effect resulting from end of the COVID-19 pandemic. The former (and the latter) is expected to accelerate (and decelerate) consumers’ adoption of contactless payment and increase (and decrease) consumers’ usage rate of contactless payment. However, the latter effect may be offset by other effects such as the positive social effect from previous adopters increased during the spreading period of COVID-19. The social effect (referred to as the imitation effect or the external effect) is well documented in the diffusion literature (e.g., Bass, 1969; Mansfield, 1961; S. J. Park & Choi, 2016; Ram, 1989). The difference between the two effects can be systematically investigated. To this end, future research may consider a unified framework used in this research (examining contactless and contact payment types in view of consumer evaluation process) and the frameworks used in other research (examining the payment types in view of consumer attitude, based on the well-known theories such as the TAM model, the diffusion theory, and the mental accounting theory).

Conclusion

This research shed light on the significance of degree of contact with respect to consumer spending intention during payment process. The unique perspective of the present study is aimed at finding out the underlying reason through which the degree of contact is linked to consumer spending, thus disgust and negative contamination are explored as psychological mechanisms. We proposed and found that COVID-19 pandemic moderates the relation between degree of contact and the psychological outcomes such that the associations are stronger when COVID-19 outbreaks. Overall, the current research contributes to the body of knowledge on payment by indicating that degree of contact is a crucial factor that should be considered in shaping consumer perceptions and their spending behavior, particularly during time of emergencies and crisis.

Footnotes

Acknowledgements

The authors would like to acknowledge the anonymous reviewers who provided insightful suggestions and comments on improving the quality of this manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research was funded by International Joint Research Project of Shandong University of Finance and Economics [Grant No. 1717002011].

Ethical Statement

The authors of this paper have carefully studied the international research ethics, and this paper does not involve animal and human studies.