Abstract

This paper investigates how bank funding diversity and lending affect bank performance, especially during the Covid-19 pandemic. We employ the Generalized Method of Moments to analyze unbalanced panels of commercial banks in China, Taiwan, and Vietnam. The empirical results show that a percentage increase in bank funding diversity and bank lending in the sample negatively affects profitability. In contrast, the results are mixed in each country due to different market microstructures. While holding diversified funding strengthens bank profitability during the pandemic, increasing lending activities dampers the bank’s performance. Finally, this research has important implications for bank managers and regulators to develop sustainable banking performance in emerging markets, especially during pandemics.

Plain Language Summary

This paper investigates how bank funding diversity and lending affect bank performance, especially during the Covid-19 pandemic. We employ the Generalized Method of Moments to analyze unbalanced panels of commercial banks in China, Taiwan, and Vietnam. The empirical results show that a percentage increase in bank funding diversity and bank lending in the sample negatively affects profitability. In contrast, the results are mixed in each country due to different market microstructures. While holding diversified funding strengthens bank profitability during the pandemic, increasing lending activities dampers the bank’s performance. Finally, this research has important implications for bank managers and regulators to develop sustainable banking performance in emerging markets, especially during pandemics.

Introduction

Banking institutions are essential in stabilizing the financial market and developing local economies (Duong et al., 2023). However, banks operate in a fiercely competitive environment that requires banks to pursue a diversification strategy to increase income (Vo, 2020). Diversification can help banks manage their risk by spreading it across different types of assets and businesses. By diversifying their loan portfolios, banks can reduce their exposure to any industry or sector, which can help them avoid losses during economic downturns or other unexpected events. Prior studies have examined the diversification strategy and bank performance, such as income, product, and geographical diversification (Cai et al., 2016; Li et al., 2021; Saghi-Zedek, 2016). Diversification also supports banks in generating more revenue by offering customers a comprehensive range of products and services. Diversification can also give banks a competitive advantage by enabling them to provide a broader range of products and services than their competitors. This strategy helps banks attract and retain customers, ultimately driving profitability. However, only a few papers examine the funding diversification sources in banking operations (Vo, 2020).

Diversification theory states that when banks can access more sources of funding, which helps banks extend credit and improve their performance (Duong et al., 2023). In addition, funding diversity can help banks manage their risk by reducing their reliance on any one source of funding (Pham & Nguyen, 2023). By diversifying their funding sources, banks can spread their risk across different types of funding, which can help them avoid liquidity and funding challenges during periods of stress (Abbas & Ali, 2022). By accessing diversified funding sources, banks can offer more attractive interest rates, which can help them attract and retain customers and drive profitability (Papadamou et al., 2021). Therefore, Vo (2020) suggests that maintaining diversity and stability in the capital is essential for sustainable banking development. However, other studies state that funding diversification reduces bank profitability it is costly to maintain diversified funding sources (Abbas & Ali, 2022; King, 2013). In addition, the pecking order theory and the trade-off theory do not emphasize diversifying capital structure but instead focus on optimizing the benefits derived from internal and external sources of capital. Therefore, the role of funding diversity in banking profitability needs further investigation.

On the other hand, bank lending is also an issue that brings much attention to banks because credit creation is the main income-generating activity for the bank (Ekinci & Poyraz, 2019). When banks organize credit activities well, banks can improve bank performance and positively affect the financial system (Duong et al., 2023). Ghenimi et al. (2017) also stated that banks’ assets and capital structure have a close relationship. Therefore, banks must effectively manage lending activities to maximize banking performance (Ekinci & Poyraz, 2019). However, some theories emphasize the diversification of asset portfolios, such as the Markowitz theory, to ensure risk reduction and achieve suitable profitability. Therefore, if banks focus excessively on lending without diversifying their investment in other items of the asset side of the balance sheet, they will face significant risks, particularly during periods of uncertainty. Previous studies reported that bank lending has a mixed effect on bank performance, such as Maudos and De Guevara (2004), Kasman et al. (2010), and López-Espinosa et al. (2011), Ekinci and Poyraz (2019). Therefore, it is worth investigating the effect of bank lending on bank performance.

Several reasons motivated us to conduct this study in Vietnam, China, and Taiwan. According to the ADB, the banking sectors in Vietnam, China, and Taiwan have witnessed rapid development, positioning them as potential markets for banks and other financial services. Secondly, the banking system in Vietnam, China, and Taiwan has many similarities. Vietnam and China are transition economies with many similarities (Orden et al., 2007). The economic growth of these countries has contributed significantly to the development of the financial system (Calderón & Liu, 2003; Christopoulos & Tsionas, 2004). Vietnam and China have banking systems with similar structures and have undergone liberalization reform since the 1990s (T. P. T. Nguyen et al., 2016). Similarly, the banking in Taiwan and China are identical because they have a common language and traditions (Hwang et al., 2004). Finally, very few studies investigate the impact of bank funding diversity and bank lending on profitability in these countries.

This study examines the impact of bank funding diversity (BFD) and lending (LENDING) on bank profitability in Vietnam, China, and Taiwan. We follow Saksonova (2014) to employ Net Interest Margin (NIM) as the primary profitability proxy of commercial banks because it is the most fundamental banking indicator. NIM measures the difference between interest paid to depositors and interest received from credit activities, which capture the primary function of banking institutions (Suu et al., 2020). On the other hand, banking revenue in China and Vietnam mostly comes from interest income (Hou et al., 2018; Suu et al., 2020). In addition, we also follow Vo (2020) and Duong et al. (2023) to measure bank funding diversity (BFD) by estimating the modified Herfindahl-Hirschman Index (HHI) and use the ratio of total loans to total assets to estimate bank lending (LENDING) because this ratio reflects the level of capital used for credit activities and the asset quality of banks (Ekinci & Poyraz, 2019).

This study contributes to the growing literature on bank performance for the following reasons. Firstly, this study complements Vo (2020), Duong et al. (2023), and Pham and Nguyen (2023) to investigate the impact of funding diversity and lending on profitability. However, Vo (2020), Duong et al. (2023), Pham and Nguyen (2023) only examine data from Vietnam, while our study expands the data sample to cover three countries such as Vietnam, China, and Taiwan. The data of multinational datasets enables our study to compare the impact of bank funding diversity and lending on bank performance more comprehensively than studies conducted solely within one country or territory. Secondly, in addition to examining the effect of bank funding diversity and lending on bank profitability, our study also investigates the impact of the Covid-19 pandemic on bank profitability and the interaction terms between covid-19, bank funding diversity, and lending. This allows us to draw important implications for bank management and provide recommendations for bank executives, particularly during the Covid-19 pandemic. Finally, our study differs from Vo (2020) and Duong et al. (2023) because we employ Net Interest Margin (NIM) as a proxy for bank profitability. NIM reflects the financial intermediary functions of commercial banks. It also captures both interest revenue and interest costs management of commercial banks. Therefore, NIM is more relevant to commercial banks than ROA and ROE, which widely appeared in prior banking studies.

This study generates three striking results. Firstly, our findings suggest that BFD and LENDING negatively impact bank profitability. Our findings indicate that a percentage increase in funding diversity and lending reduces NIM by 0.417 and 0.024%, respectively. In contrast, when comparing each country, funding diversity and bank lending have mixed effects on NIM. This result in full sample supports diversification on assets but does not support diversification on liabilities. Our findings align with King (2013) and T. L. A. Nguyen (2018) because they suggest that it is costly to maintain diversified funding sources, especially in the competitive banking sector. Therefore, maintaining higher funding diversity also incurred financing expenses, reducing profitability (T. L. A. Nguyen, 2018). Secondly, this study shows that the Covid-19 pandemic adversely affects bank profitability because banks face more difficulties due to business disruptions and economic stagnates during the pandemic (Pham & Nguyen, 2023). Finally, our findings indicate that banks with higher funding diversity generate additional profits, whereas focusing solely on lending without diversifying asset portfolios will reduce profits during the pandemic.

This study has the remaining structure as follows. Section 2 is the literature review. Section 3 presents the data and research methodology. Section 4 discusses the empirical results. The conclusion and policy implications are in section 5.

Literature Review

Efficient Capital Structure Theory

Capital Structure Theory explores the relationship between a firm’s capital structure and its value, cost of capital, and overall financial performance. Franco Modigliani and Merton Miller in the 1950s suggest that in a perfect capital market, the value of a company is independent of its capital structure. However, perfect markets are nearly non-existent, so the exploration of optimal capital structure remains a relevant and ongoing concern in the present day. Capital structure theory examines the optimal mix of debt and equity that maximizes a company’s value and minimizes its cost of capital. However, Trade-off Theory, Pecking Order Theory, Agency Theory, and Market Timing Theory only focus on addressing the issue of utilizing internal or external funding, and their theories contradict each other and do not prioritize diversifying capital sources. In addition, selecting an optimal capital structure according to each theory is not unanimous and still subject to consideration.

Diversification Theory

Diversification theory has become a prominent issue about assets and capital in recent years. Diversification can be implemented in the asset and capital portfolios on the balance sheet. Overall, diversification theory supports the implementation of diversification in asset portfolios and capital sources in the balance sheet.

Markowitz (1952) suggests that investors can diversify their assets by spreading their investments across different types of assets to reduce investment risk, balance the overall performance of the investment portfolio, and optimize returns. It is referred to as the Markowitz theory. In banking operations, lending is also one of the investment activities that banks use to generate income. Therefore, considering the diversification of investment portfolios by banks is also a matter of concern.

On the other hand, funding diversity is a diversification issue originating from the capital sources on the balance sheet. Funding diversity is the ability to access various sources of capital, including deposits, interbank loans, and capital markets (Duong et al., 2023). Previous studies have shown that diversifying funding helps banks increase lending, enhance efficiency, and be resilient to financial shocks (Duong et al., 2023; Vo, 2020).

Bank Funding Diversity and Profitability

Ritz and Walther (2015) suggest that funding uncertainty originates from competition, which causes difficulties in attracting deposits and granting loans. Ghosh (2018) supports the diversification theory and indicates that higher funding diversity effectively promotes the financial intermediaries’ role, enhancing liquidity and positively affecting bank profitability. Therefore, banks must increase funding diversity to increase lending and profitability. Duong et al. (2023), Vo (2020), Moudud-Ul-Huq et al. (2018), and Vo and Tran (2016) also report that funding diversity increase bank profitability, especially in time of crisis (Pham & Nguyen, 2023). However, some studies show that funding diversity adversely affects bank profitability because it is costly to maintain diversified funding sources (Abbas & Ali, 2022; King, 2013). Therefore, investigating the role of funding diversity in banking profitability still needs more attention.

As there are controversial findings between funding diversity and profitability, we propose the first hypothesis as follows:

Hypothesis 1: Bank funding diversity positively affects a bank’s profitability.

Bank Lending and Profitability

Suu et al. (2020) argue that credit is the most significant proportion of the asset portfolio because interest income accounts for 70 to 85% of the bank’s revenue in Vietnam. Therefore, in theory, credit activities significantly affect banks’ profitability. Prior studies use bank lending as a control variable and investigate the impact of bank lending on bank performance, such as Suu et al. (2020), Ekinci and Poyraz (2019), Ghenimi et al. (2017), and Zhou and Wong (2008). Prior studies report that increasing bank lending positively empowers profitability. However, diversification theory states that credit risks are associated with lending concentration because they will have higher non-performing loans (NPLs). Supporting this viewpoint, Ekinci and Poyraz (2019) indicate that inadequate monitoring in the lending analysis leads to higher NPLs. Thus, banks must reserve higher provisions for overdue debts, which erodes their profitability.

There are controversial findings between bank lending and profitability, so we propose the second hypothesis.

Hypothesis 2: Bank lending positively affects a bank’s profitability.

The Covid-19 Pandemic and Bank Performance

The Covid-19 pandemic has caused severe consequences and profoundly impacted the economy (Pham & Nguyen, 2023; Shafeeq Nimr Al-Maliki et al., 2023). Elnahass et al. (2021) suggest that the Covid-19 pandemic has caused considerable difficulties for the banking sector due to business disruption and social lockdown. The Covid-19 pandemic has decreased operational efficiency and income (Pham & Nguyen, 2023). Banks face difficulties in a reduction in capacity to obtain funds as businesses and individuals increase their cash holdings to cope with economic instability caused by the pandemic (Amore & Minichilli, 2018; Doan et al., 2020; Madanoglu & Ozdemir, 2018). Additionally, banks encounter challenges in lending and other investment activities as businesses restrict their investments amid uncertainty, and consumers reduce their spending to mitigate personal risks (Mirzaei et al., 2022).

Moreover, banks also face delayed repayments and increased credit risk (Elnahass et al., 2021). Therefore, the pandemic affects funding diversity and bank lending, reducing performance. Although governments have implemented stimulus measures and relaxed disease prevention regulations, the effectiveness of these measures remains a significant question.

This study chose three countries, Vietnam, China, and Taiwan because they are three geographically close nations. More importantly, when the Covid-19 pandemic broke out, these countries implemented effective isolation and disease management before the emergence of the Delta variant in 2021 and 2022. As prior studies report the negative impact of the pandemic on bank performance, we propose the following hypothesis.

Hypothesis 3: Covid-19 pandemic negatively impacts banks’ profitability.

Data and Research Methodology

Data

This study collects data from 38 commercial banks in Vietnam, 16 in China, and 14 in Taiwan. We only collect data from listed banks in Taiwan and China, whereas Vietnam’s banking data includes listed and unlisted banks. Therefore, the number of banks in Vietnam in our sample is higher than in China and Taiwan. We collect data from the listed Chinese and Taiwanese banks from the Taiwan Economic Journal (TEJ) database and Vietnamese data from the Fiinpro database. We also used the annual financial reports to collect other missing data in Vietnam. We also manually cross-check to ensure that data from Fiinpro and the audited financial statements are consistent. We also remove observations with insufficient data to calculate the required variables. Our final data is an unbalanced sample that contains 750 bank-year observations.

The paper uses several financial indicators such as Net Interest Margin (NIM), Bank Funding Diversity (BFD), Bank Loan to Total Assets (LENDING), Risk Aversion (RA), Bank’s Total Assets (SIZE), Quality of Management (QOM), Implicit Interest Payments (IIP). The variable definitions are explicitly described in Appendix A, Table A1.

Research Methods

Firstly, we perform the Hausman Test to choose between the Fixed Effects Model (FEM) and Random Effects Model (REM). The FEM method assumes that the error of the model has unobservable factors that are different between the objects but do not change over time and affect the independent variables, so the removal of these factors will help the estimation results to be reliable while following the REM method, the unobservable error factor that unchanged over time do not affect the independent variables, and the removal of those factors make the result of the model reliable though inefficient. However, FEM and REM carry inefficiency terms and heterogeneity, drastically affecting outcomes (Duong et al., 2023; Tran et al., 2022). Therefore, this study implements the System Generalized moment method (Sys-GMM) to overcome the endogeneity issue (Duong et al., 2023). The Sys-GMM is more efficient than the Dif-GMM (Chi et al., 2022). This study chose the two-step estimator because it is more efficient than the singer-step estimator (Chi et al., 2022; Huynh & Dang, 2021).

We employ two tests to validate the GMM estimations. First, the Hansen test checks the validity of the instrument variable. If the p-value of the Hansen test is above 10%, the instrumental variables are appropriate. Second, the model has no quadratic autocorrelation if the AR (2) p-value is above 10% (Chi et al., 2022).

Vo (2020) suggests that commercial banks in Vietnam with diversified funding sources typically earn higher profitability. Following Vo (2020), this study employs a modified Herfindahl-Hirschman Index (HHI) to measure funding diversification. HHI index range from zero to one, with a higher value indicating banks have more funding diversity (Vo, 2020).

To measure bank lending (LENDING), we use the ratio of total loans to total assets. This ratio is a strong positive predictor of NIM (López-Espinosa et al., 2011). Besides, Zhou and Wong (2008); Suu et al. (2020) also reported that bank interest income increased with a higher bank lending ratio.

Previous studies also indicate that various factors affect the NIM in banks, such as management quality (QOM), bank size (SIZE), implicit interest payments (IIP), risk aversion (RA) (Doliente, 2005; Maudos & De Guevara, 2004; Suu et al., 2020; Zhou & Wong, 2008). Maudos and De Guevara (2004) report that QOM has a negative relationship with NIM. Furthermore, Williams (2007) also argued that QOM is crucial in determining a bank’s net interest margin. Banks with higher quality management are cost-efficient, with a lower net interest margin. In addition, many studies indicate that bank size, interest payments, and risk aversion have mixed effects on NIM (Maudos & De Guevara, 2004; Suu et al., 2020; Zhou & Wong, 2008). Given the mixed results, it is worth testing the impact of bank size, interest payments, and risk aversion on the commercial profitability of banks. Appendix A provides detailed variable definitions.

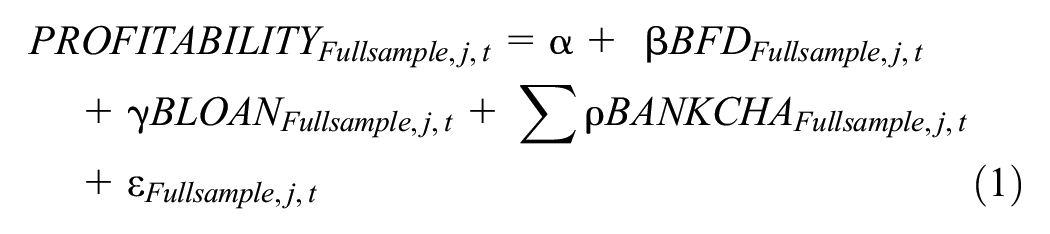

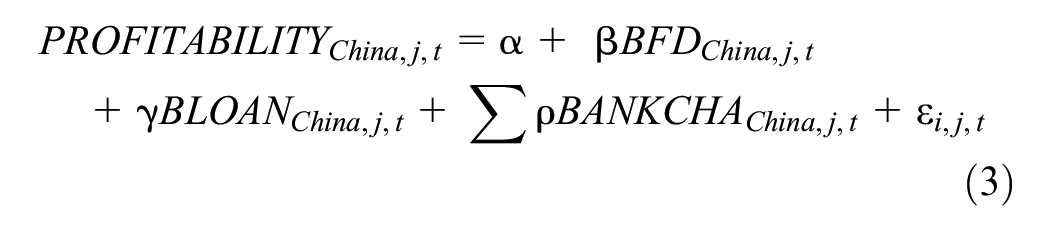

To investigate the impact of bank funding diversity and bank lending on bank profitability in the entire sample, we construct model 1. We then construct models 2 to 4 to compare the impact of funding diversity and bank lending in different markets such as Vietnam, China, and Taiwan. Models l to 4 support us in testing the first and second hypotheses.

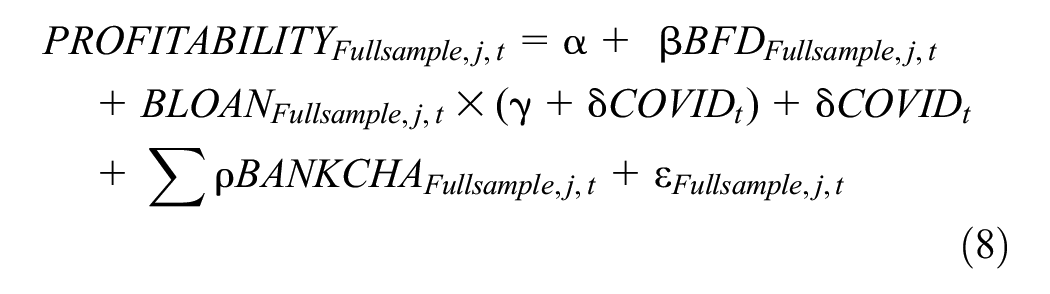

Then, to examine the impact of the Covid-19 pandemic on bank profitability, we follow Pham and Nguyen (2023) and Doan et al. (2020) to construct study model 5. In addition, to investigate the interaction between funding diversity, bank lending, and covid on bank performance, we follow (Doan et al., 2020) to construct models 6 to 8. The coefficient of the interaction term BFD*COVID test whether the bank funding diversity affects profitability during the pandemic. Similarly, BLOAN*COVID examines whether higher bank lending during the pandemic improves or reduces profits. The interaction term between BFD*BLOAN analyzes whether banks that concurrently pursue funding diversity and prioritize lending activities enhance or impede banks’ profitability. Therefore, the Models 5 to 8 support us to test hypothesis 3.

Where “j,” and “t” stand for bank j at time t. PROFITABILITY is proxied by NIM. BFD is bank funding diversity, and BLOAN is bank lending. BANKCHA is a set of control variables, including management quality (QOM), bank size (SIZE), implicit interest payments (IIP), and risk aversion (RA). Covid-19 is defined by COVID. All variables are defined in Appendix A.

Empirical Results and Discussion

Descriptive Statistics

Table 1 presents the descriptive statistics of the research sample. Table 1 reports that the average value of NIM is about 0.039, with a standard deviation of 0.159, consistent with Suu et al. (2020) and T. V. H. Nguyen et al. (2020), Vo (2020), and Duong et al. (2023). The BFD ranges from 0.341 to 0.755, with a mean of 0.572 and a standard deviation of around 0.086. Our finding is consistent with Vo (2020) and Duong et al. (2023). The mean of LENDING is 0.485, and the standard deviation is around 0.211. Therefore, credit is the main business activity of the banks in the sample. Table 1 also shows descriptive statistics for control variables. The mean of SIZE is 26.262 and ranges from 18.674 to 34.955, while the mean and standard deviation of RA are 0.080 and 0.032, respectively. The QOM’s mean is 0.401, ranges from 0.075 to 7.185, and the mean of IIP is 0.008.

Descriptive Statistics for the Entire Sample.

Note. Table 1 highlights the descriptive statistics variables in this study. The sample comprises Vietnamese, Chinese, and Taiwanese banks from 2009 to 2020.

Table 2 reports descriptive statistics for NIM, BFD, and LENDING for each country in our sample. The mean of NIM in Vietnam, China, and Taiwan is 0.034, 0.019, and 0.071, respectively. In our sample, the NIM in Taiwan is the highest, then come Vietnam and China. Similarly, BFD (0.662) and LENDING (0.647) in Taiwan are the highest compared to Vietnam and China. The result in Table 2 indicates differences in average for NIM, BFD, and LENDING in China and Taiwan compared with other countries in the sample. In contrast, BFD and LENDING in Vietnam are different on average from other countries in the sample.

Mean by Countries’ Characteristic.

Note. Table 2 highlights the mean value and the difference between NIM, BFD, and LENDING. The sample comprises Vietnamese, Chinese, and Taiwanese banks from 2009 to 2020. The symbols ***, **, and * represent the significant level at 1, 5, and 10%, respectively.

Pearson Correlation Matrix

Table 3 shows the Pearson correlation matrix between independent variables. The coefficient correlations are moderate, with no perfect relationships, indicating that multicollinearity is not a problem in our sample (Tran et al., 2022). On the other hand, we examine the variance inflation factor (VIF) to test the multicollinearity issue. As shown in Table 2, the maximum value of VIF is 1.59. Therefore, multicollinearity is not an issue because the VIF of all variables is less than ten (Duong et al., 2023).

Pearson Correlation Matrix.

Note. This table reports the Pearson correlation matrix of independent variables. The sample comprises Vietnamese, Chinese, and Taiwanese banks from 2009 to 2020. The p-value is in parentheses. The symbols ***, **, and * represent the significant level at 1, 5, and 10%, respectively.

Impacts of Bank Funding Diversity and Bank Lending on Profitability

Before discussing the results in Table 4, we conducted the Hansen and AR(2) tests to diagnose GMM estimations. The p-values of the Hansen and AR(2) tests are greater than 10%, indicating that the selected instrumental variables in the model are appropriate and the model has no quadratic autocorrelation. Therefore, the results in Table 4 are deemed suitable (Chi et al., 2022).

Impacts of Bank Funding Diversity and Bank Lending on NIM.

Note. This table reports the impact of bank funding diversity and bank lending on NIM, estimated by GMM estimations. The definitions of the variable are provided in Appendix A. The value of the p-value is in parentheses. The symbols ***, **, and * represent the significant level at 1, 5, and 10%, respectively.

Table 4 reports the GMM estimations. Models 1 to 4 show the result for equation (1), including the entire sample and each country. We find that bank funding diversity is statistically significant in all cases, and it negatively affects the profitability of banks in the whole sample and Taiwan. In contrast, it positively affects banks’ profitability in Vietnam and China. The finding indicates that banks have lower profitability under increasing funding diversity on average, while vice versa in Vietnam and China. Model 1 and Model 4 suggest that the coefficients of BFD are −0.417 and −1.385, respectively. This finding indicates that a percentage increase in funding diversity reduces NIM by 0.417 and 1.385% in the total sample and Taiwan. However, models 2 and 3 show that higher BFD tends to increase NIM. For instance, the coefficient of BFD in models 2 and 3 are 0.050 and 0.445, respectively. This finding suggests that a percentage increase in funding diversity increases NIM by 0.05 and 0.445% in Vietnam and China. The result in the full sample and Taiwan state that it is costly to maintain diversified funding sources, and it will reduce bank profitability because banks must pay extra interest expenses to maintain stable funding, negatively eroding NIM (King, 2013). However, the result in Vietnam and China are consistent with Acharya and Naqvi (2012), Vo (2020), and T. L. A. Nguyen (2018) but inconsistent with King (2013) and Abbas and Ali (2022). This evidence supports the diversification theory because increasing funding diversity effectively promotes the financial intermediaries, enhancing liquidity and improving bank profitability (Ghosh, 2018). The entire sample and Taiwan results do not support hypothesis 1 and the diversification theory. However, the findings from China and Vietnam support hypothesis 1 and the diversification theory.

Table 4 also shows the mixed effect of bank lending on NIM. Specifically, bank lending significantly impacts bank performance in the entire sample, Vietnam and China. However, it has a statistically insignificant impact on NIM in Taiwan. These findings indicate that an increase in higher bank lending ratio reduces NIM in the full sample and China. Models 1 and 3 suggest that the lending coefficients are −0.024 and −0.104, respectively. This finding indicates that a percentage increase in banking lending reduces NIM by 0.024 and 0.104% in the full sample and China. These results support the view that banks extending credit activity may increase the non-performing loans if these banks do not have an efficient risk management system. The higher non-performing loans cause higher provisions and decrease profitability (Ekinci & Poyraz, 2019). However, model 2 shows that higher lending banks will have higher NIM in Vietnam. This result aligns with Maudos and De Guevara (2004), Kasman et al. (2010), and López-Espinosa et al. (2011). These result support view that credit activities generate an essential source of interest income. Therefore banks can increase lending to obtain higher marginal returns in Vietnam (Suu et al., 2020). Our findings in the full sample and Taiwan do not support hypothesis 2. However, it supports Markowitz’s diversification theory because banks reduce risk by diversifying their assets and spreading investments across different asset classes.

Table 4 also shows that bank size (SIZE) positively affects NIM in China, while it is not statistically significant in the remaining models. This result is consistent with Ugur and Erkus (2010) and Amuakwa-Mensah and Marbuah (2015) because a large bank’s size can increase a bank’s net interest margin. Table 4 reports that Quality of Management (QOM) adversely influences NIM in the entire sample, while it is not statistically significant in Vietnam, China, and Taiwan. Our results are consistent with Maudos and De Guevara (2004), Zhou and Wong (2008), Maudos and Solís (2009), and Suu et al. (2020). The QOM indicates the operating costs over gross income. This higher QOM ratio means the bank has lower profits with a higher cost of liabilities. The higher ratio of QOM reflects inefficiency in banking management. Thus, banks must pay more significant expenses for their inefficient operating activities, decreasing banks’ NIM. Table 4 also presents the positive effect of Risk Aversion (RA) and NIM in the full sample and China. This result is consistent with Maudos and De Guevara (2004), Maudos and Solís (2009), and Ugur and Erkus (2010). In addition, Table 4 documents show that Implicit Interest Payment (IIP) positively impacts NIM in China. Kasman et al. (2010) suggest that banks with accessible banking services have a higher interest margin. On the other hand, our findings are statistically insignificant in the entire sample, Vietnam and Taiwan.

Impacts of Bank Funding Diversity and Lending on Bank Profitability During the Covid-19 Pandemic

To investigate the impacts of BFD and Lending on NIM during the Covid-19 pandemic, we follow Elnahass et al. (2021) and Pham and Nguyen (2023) to add COVID as a dummy variable that takes a value of zero before the pandemic and one during the pandemic. We also use GMM estimations to analyze our findings during the pandemic.

Before discussing the finding in Table 5, we conducted the Hansen and AR(2) tests to assess the reliability of the GMM estimations. The p-values of the Hansen and AR(2) tests are greater than 10%, indicating that the selected instrumental variables in the model are appropriate and the model has no quadratic autocorrelation. Therefore, the results in Table 4 are deemed suitable (Chi et al., 2022).

Estimation Results During the Pandemic.

Note. This table reports the impact of bank funding diversity and bank lending on NIM during the Covid-19 pandemic. The definitions of the variable are provided in Appendix A. The p-value is in parentheses. The symbols ***, **, and * represent the significant level at 1, 5, and 10%, respectively.

Table 5 shows that the Covid-19 pandemic reduces the NIM of commercial banks statistically significantly in models 5 to 8. The pandemic significantly reduces bank performance due to social lockdowns, business disruptions, and a sluggish economy (Baret et al., 2020; Pham & Nguyen, 2023). This finding is consistent with Elnahass et al. (2021) and Pham and Nguyen (2023) and support Hypothesis 3.

In addition, the interaction variable BFD*LENDING in model 6 shows that compared to banks that pursue specific objectives such as BFD or lending, banks that simultaneously follow BFD and lending policies experience reduced profitability during the pandemic. Specifically, the interaction variable BFD*LENDING coefficient is −2.671, which explains an equivalent 2.671% decrease in NIM for banks that diversify their funding but do not diversify their asset portfolios when focusing on lending. This result indicates that banks should also diversify their lending portfolios to avoid the negative impacts of the pandemic on their profitability.

Models 7 and 8 report the impact of BFD and Lending during the pandemic through two interaction variables, BFD*COVID and LENDING*COVID. Specifically, the coefficient of the BFD*COVID variable in Model 7 indicates that, compared to banks without funding diversification, banks that diversify their funding will positively impact bank profitability during the Covid-19 pandemic. On the other hand, Model 8 demonstrates that a concentration on lending impairs profitability during the Covid-19 pandemic. Specifically, during the Covid-19 pandemic, a percentage increase in funding diversity leads to a 0.270% increase in NIM more than banks with less funding diversity. The results from Model 7 support the viewpoint that enhancing diversification helps banks fulfill their role as financial intermediaries and increases operational efficiency (Ghosh, 2018), especially during a pandemic (Pham & Nguyen, 2023).

On the other hand, a one percentage increase in lending by banks will result in a 0.047% decrease in NIM more than banks that scale down their lending activities during the pandemic. The finding from model 8 supports the perspective that the Covid-19 pandemic increases non-performing loans, resulting in higher costs for banks and reduced bank profitability (Elnahass et al., 2021). Overall, our findings in the Covid-19 pandemic support the diversification theory, implying that banks should diversify their funding sources and assets on the balance sheet to achieve stability and increase operational efficiency during the Covid-19 pandemic.

Conclusion

This study analyzes the impacts of funding diversity and bank lending on bank performance before and during the pandemic. This study collects data from commercial banks in Vietnam, China, and Taiwan from 2009 to 2020. We employ the GMM method to analyze an unbalanced sample of 750 bank-year observations from 38 commercial banks in Vietnam, China, and Taiwan.

Our findings indicate that banks with higher funding diversity and bank lending reduce bank profitability in the entire sample, while there are different results in subsamples for each country. Our study also examines the impact of the Covid-19 pandemic on bank profitability. Our results show that the Covid-19 pandemic reduces bank profitability, and this impact is even more pronounced if banks extend lending activities during the pandemic. However, the adverse effects of the pandemic on bank performance can be mitigated if they implement funding diversity strategies.

Our study contributes empirical evidence for bank managers and policymakers to develop sustainable banking systems in emerging nations, especially during the pandemic. Firstly, the findings demonstrate that bank funding diversity and lending reduce profitability. However, the results vary for each country in the data sample and during the study period due to the unique characteristics of each market and country. Therefore, bank managers and policymakers in each country can devise tailored policies that align with the specific characteristics of their country to enhance banks’ profitability. Secondly, the Covid-19 pandemic has negatively affected banks’ profitability.

Nevertheless, this negative impact can be mitigated if banks implement funding and asset diversification following the principles of diversification theory. Consequently, bank managers and policymakers can make informed decisions or enforce policies to assist banks in diversifying their funding and assets, thereby minimizing the adverse impact of Covid-19. Finally, diversification theory underscores the importance for banks, once they have achieved funding diversification, also to diversify their assets to mitigate risk exposure.

Although our study contributes to the growing literature on bank performance during the pandemic, it has the following limitations. The first limitation of our study is data coverage because our study investigates three countries with the same traditions. Therefore, future studies may extend the data coverage to compare the impacts of funding diversity on NIM in Islamic and conventional banks or banks in developed and developing countries. Second, some hypotheses still need to be more conclusive due to mixed findings between countries. We notice that NIM may rely on converting deposits to loans that funding diversification has yet to capture. Future studies analyze the interrelationship between core funding sources, intermediary operations, funding conversion, and profitability of commercial banks. The second limitation is that our study does not include external factors affecting funding diversity, such as bank risk-taking behavior and each country’s local culture. Ashraf et al. (2016) report that bank risk-taking behavior is likely due to differences in national culture, and the local culture of a country strongly influences banks’ risk-taking behavior. Therefore, future studies may examine the interaction role between cultural factors and funding diversity on bank performance.

Footnotes

Appendix A

Variable Definition.

| Variables | Notation | Variable descriptions |

|---|---|---|

| Dependent variable | ||

| Net interest margin | NIM | The difference between interest income and interest expenses is divided by total earning assets (Saksonova, 2014) |

| Independent variables | ||

| Bank funding diversity | BFD |

Following Vo (2020) and Duong et al. (2023), EQ is the total equity, GOV is debt from the government and central bank, ID is the interbank deposit, the CD is total customer deposit, DER is derivatives instrument and other financial debt, FIT is the source of funds for an investment trust, and OTH is other sources of funding, FUND is the bank’s total funding. |

| Operating cost | OC | The ratio of operating expenses to total assets (Maudos and De Guevara, 2004) |

| Bank size | SIZE | Natural logarithm of total assets (Kasman et al., 2010) |

| Risk aversion | RA | The ratio of equity to total assets (Ugur & Erkus, 2010) |

| Implicit interest payments | IIP | The ratio of non–interest expense to total assets (Maudos & De Guevara, 2004; Zhou & Wong, 2008) |

| Quality of management | QOM | The ratio of operating expenses to income (Suu et al., 2020; Williams, 2007) |

| Loan ratio | LENDING | Total loans divided by total assets (Vo, 2020) |

| Covid pandemic | COVID | The dummy variable takes a value of zero when there is no Covid-19 pandemic and otherwise (Elnahass et al., 2021) |

Acknowledgements

We also thank anonymous reviewers for their constructive feedback, which helps us revise our manuscript.

Author Contribution Statement

Khoa Dang Duong (duongdangkhoa@tdtu.edu.vn ) conceived and designed the experiments, performed the experiments, analyzed and interpreted the data, and wrote the first draft of the manuscript. Hoi Vu Le (hoi.levu@sbv.gov.vn) and Duy Nhat Vu (duyvn@techcombank.com.vn) performed the experiments, contributed reagents, materials, analysis tools, or data. Ai Ngoc Nhan Le (ai.lnn@vlu.edu.vn) analyzed and interpreted the data and wrote the first and final drafts of the manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work is supported by Ton Duc Thang University and Van Lang University.

Ethics Statement

This study does not involve animals or humans.

Data Availability Statement

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request