Abstract

Drawing on an analysis of 208 articles, this paper argues that while the fraud literature varies on the diagnosis of fraud, it is rooted in a common narrative as to its nature and causes. Specifically, this paper adopts an investigative approach to understand how fraud is often researched and shapes audit policies and practices. The findings reveal that fraud is generally looked at as an individual and/or organizational phenomenon, thereby allowing the meso-level of analysis to escape scrutiny. A gap, therefore, exists in being able to detect fraud at the meso-level, such as in financial services (i.e., LIBOR rigging). A meso-level analysis of fraud will allow researchers to highlight problems across the general field like the banks rigging the LIBOR or distorting the currency market as in the forex scandal. A meso-level analysis of fraud is important because it highlights the contagious behavior across the field and offers insights for fraud prevention and detection. Recognizing this unique epistemology will allow researchers to uncover new knowledge and not remain wedded to a reified understanding of fraud and fraud risks. Policymakers can derive insights and draft policies that reflect practitioners’ needs.

Introduction

Corporate crimes such as those committed by Parmalat, Cattles Plc, Carillion, and Luckin have one commonality: their perpetrators were complicit in the gross accounting misstatements of the companies’ books (Steer, 2018). The individuals in charge of these companies employed accounting tricks to hide losses and mask the companies’ true financial performance. Shortly after these frauds were uncovered, the auditing firms admitted that their auditors failed to meet the high standards for performing an audit. Although audit firms must be applauded for coming forward and acknowledging the misconduct of their auditors, there are serious concerns about auditors’ ability to conduct their work properly and detect accounting fraud (Association of Certified Fraud Examiner, 2020). Auditors are not necessarily looking for fraud and would not find what they are looking for because they have absolved themselves of the responsibility for finding fraud; they claim that the onus is on others and that fighting fraud is too difficult, especially when collusion is involved (Fox, 2020; Fulop et al., 2019).

Even if the failure to detect fraud is a by-product of inadequate training, the scope and magnitude of audit failures suggest a systematic problem (Fulop et al., 2019). As it is categorized in the accounting and finance literature, fraud is defined through two conceptual frames. One strives to explain fraud from a micro-psychological perspective, while the other combines sociological and criminological analyses to explain fraud from a wider macro-psychological perspective. Two epistemological clusters inform these frames: financial statement fraud (M. E. Lokanan, 2015) and asset misappropriation (Matthews, 2005; Van Akkeren & Buckby, 2017). Financial statement fraud involves misstatements resulting from fraudulent financial reporting (M. E. Lokanan, 2015, p. 203). Asset misappropriation includes “fraud that involves third parties or employees abusing their position to steal from an organization, for example, embezzlement through the manipulation of accounts, false invoicing, deception by employees, payroll fraud, and intellectual property theft” (Van Akkeren & Buckby, 2017, p. 384). These classifications represent the basic tenets upon which fraud research and scholarship have been built. It should be noted from these conceptualizations that fraud is defined by the fragile morality of the individual offender or through a wider structural and collective lens to suggest that collusion is at play. The focus on the “risky individual” shifts the narrative of fraud detection from legal violations to the rogue individual who needs to be monitored and controlled through new skills and competencies related to audit technology (Camfferman & Wielhouwer, 2019; Fülöp et al., 2022; Morales et al., 2014; Power, 2013).

The micro-macro-level explanations of fraud reflect a shift in general sociological and psychological inquiry that emphasizes the importance of micro-macro connections as a more robust representation of corporate accounting fraud. The validity of the micro- and macro-level analyses of fraud has been thoroughly discussed by critical accounting scholars (see Choo & Tan, 2007; Morales et al., 2014; Soepriyanto et al., 2022), and from these accounts, it is safe to declare a consensus that fraud is a consequence of both micro- and macro-variables intersecting in various ways. Ironically, the consensus of the theoretical micro- and macro-level explanations of fraud lacks substantial empirical support, making it an unresolved empirical problem in accounting fraud research.

Critical fraud researchers can take the lead in examining the micro- and macro-connection, which to date has been a fledgling enterprise of fraud research that has been making slow but steady progress not only in explaining corporate accounting fraud but also, more generally, in fraud theory. A crucial element missing in this synthesis is the inclusion of the meso-level analysis of fraud, that is, research on the determinants and characteristics of fraud at the field (institutional level) of analysis. More meso-level studies may be possible if we classify earlier research as micro or macro. Historically, the field has played a critical role in white-collar crime and deviance, as in the London Inter-Bank Offered Rate (LIBOR) and forex scandals (Huan et al., 2022). More critically, the setting where white-collar criminality occurs provides the breeding ground for micro-individual processes to interact with macro-organizational forces, thus affecting individuals’ action alternatives within the setting (see M. Lokanan, 2018). The field provides a window where social actions are interconnected with institutional goals and individual deviance so that illegality becomes normalized in the setting. While critical fraud researchers are addressing the micro-macro research gap in the causes of fraudulent behavior, significant progress can be made in understanding how interconnected agents in a field setting make decisions to circumvent ethical rules and laws governing their conduct.

This paper aims to critically synthesize the volume of work on fraud in the accounting literature. Through a systematic literature review (SLR), this study aims to: (i) comprehensively report on the critiques and challenges of how fraud and fraud risks have been conceptualized and researched in the accounting literature and (ii) identify knowledge gaps in the literature and suggest areas and opportunities for further research. Fraud is described as situated action concerning agents and their structured social systems. Bourdieu’s (1998, 1993) field theory and economic sociology (Granovetter, 1985, 1992) is invoked to establish the link between the meso-level field analysis of individuals’ situated actions and structured agency relationships.

The analytic review of the literature presented here will extend and deepen critical fraud research and advance the scholarship on fraud and fraud risks across several disciplines. First, we contribute significantly to the fraud scholarship, which needs a critical interdisciplinary review. With fraudulent activities on the rise, fraud risks in accounting have become a significant concern for organizations and regulators. A comprehensive review of the existing literature on fraud and fraud risks in accounting has been undertaken to provide insights into these issues. The review aims to identify the critiques and challenges surrounding how fraud and fraud risks have been conceptualized and researched in accounting. A review of the fraud scholarship is particularly significant as it can help identify the limitations of current research and inform future research directions.

Second, this study addresses the calls from several authors to delve into the existing literature surrounding fraud and identify the knowledge gaps that require further exploration (Matsueda, 2017; Vaughan, 2007; Walters, 2023). This paper provides a roadmap for researchers to focus on addressing these gaps and propel the field of fraud research forward. By identifying these gaps and opportunities, future research on fraud can enhance our understanding of the subject matter and improve the detection and prevention efforts across various domains. The findings of this study provide a more comprehensive analysis of fraud, enabling stakeholders to make better-informed decisions when dealing with fraud-related issues.

The remainder of the paper is organized into the following sections: Section 2 discusses the methodology employed to conduct the literature review. Section 3 presents an analysis of the descriptive findings. Section 4 briefly introduces the micro- and macro-level explanations of fraud. Section 5 reviews the literature on the micro-level analysis of how fraud is represented in the accounting literature. Section 6 provides a comprehensive review of the macro-level analysis of fraud. Section 7 addresses the literature on the audit apparatus designed to address fraud and fraud risks. Section 8 identifies the theoretical gap in critical fraud research. Section 9 presents a conclusion and offers directions for future research.

Scope of Research and Methodology

Research Questions

The scope of this review consists of quantitative and qualitative scientific research on accounting fraud that was published in peer-reviewed journals between 2000 and 2020. This time interval is chosen because it represents and captures two major financial crises: the Enron Scandal of 1999–2000 and the global financial crisis (GFC) of 2009 to 2010. A 10-year gap between each crisis was preferred for two reasons. First, the onslaught of articles and special issues on fraud in top accounting journals, as defined by lists compiled by the Australian Business Deans Council (ABDC) and the Chartered Association of Business Schools (ABS), precipitated a veritable explosion of scientific inquiry on corporate accounting fraud and the preferred course for reforms. Second, in the provided coverage, critical fraud researchers had much to say about the scandals as distinct financial events and financial reporting and regulation more generally. The wider discussion of audit technology and the fight against accounting fraud represents the most intriguing aspect of this scholarship. The following research question guides the inquiry in this area:

RQ1: How is fraud conceptualized in the accounting literature?

The scholarly and practitioner communities need to understand better how fraud has been theorized in the literature and the frameworks/mechanisms that have come to represent fraud risks. Therefore, the following research question was developed:

RQ2: What are the risk mitigation strategies that have been adopted by the critical accounting fraud research?

With the increase in corporate accounting fraud, the research and scholarly communities are interested in the challenges and knowledge gap that remain. A better understanding of the knowledge gaps will help guide research into new areas of critical fraud inquiries. In this regard, the following research question guides the inquiry:

RQ3: What are the knowledge gaps in critical fraud research?

Inclusion and exclusion criteria were applied to ensure that the studies were within the relevant boundaries of the research. The study undertakes an SLR based on the guidelines set out in Kitchenham’s (2004) work that has been widely adopted in engineering and medical research. The aim is to be inclusive and mutually exclusive enough to minimize bias. As shown in Table 1, the inclusion criteria were applied to peer-reviewed articles in English and studies that were ranked in the ABDC and ABS journal rankings. Studies that were not peer-reviewed, edited books, reports, or non-scholarly works were excluded from the sample.

Study Inclusion and Exclusion Criteria.

Study Inclusion and Exclusion Criteria

Sample Selection and Search Criteria

The search was conducted using specific databases to explore the articles for review. As shown in Table 2, the search was conducted using the most widely used journal database that housed accounting journals on the ABDC, and ABS lists. These databases were located through Google Scholar and encompassed the top journals in accounting. The selected database was highly relevant and provided a comprehensive list of the leading journals in accounting and literature on critical fraud research.

Search Procedures.

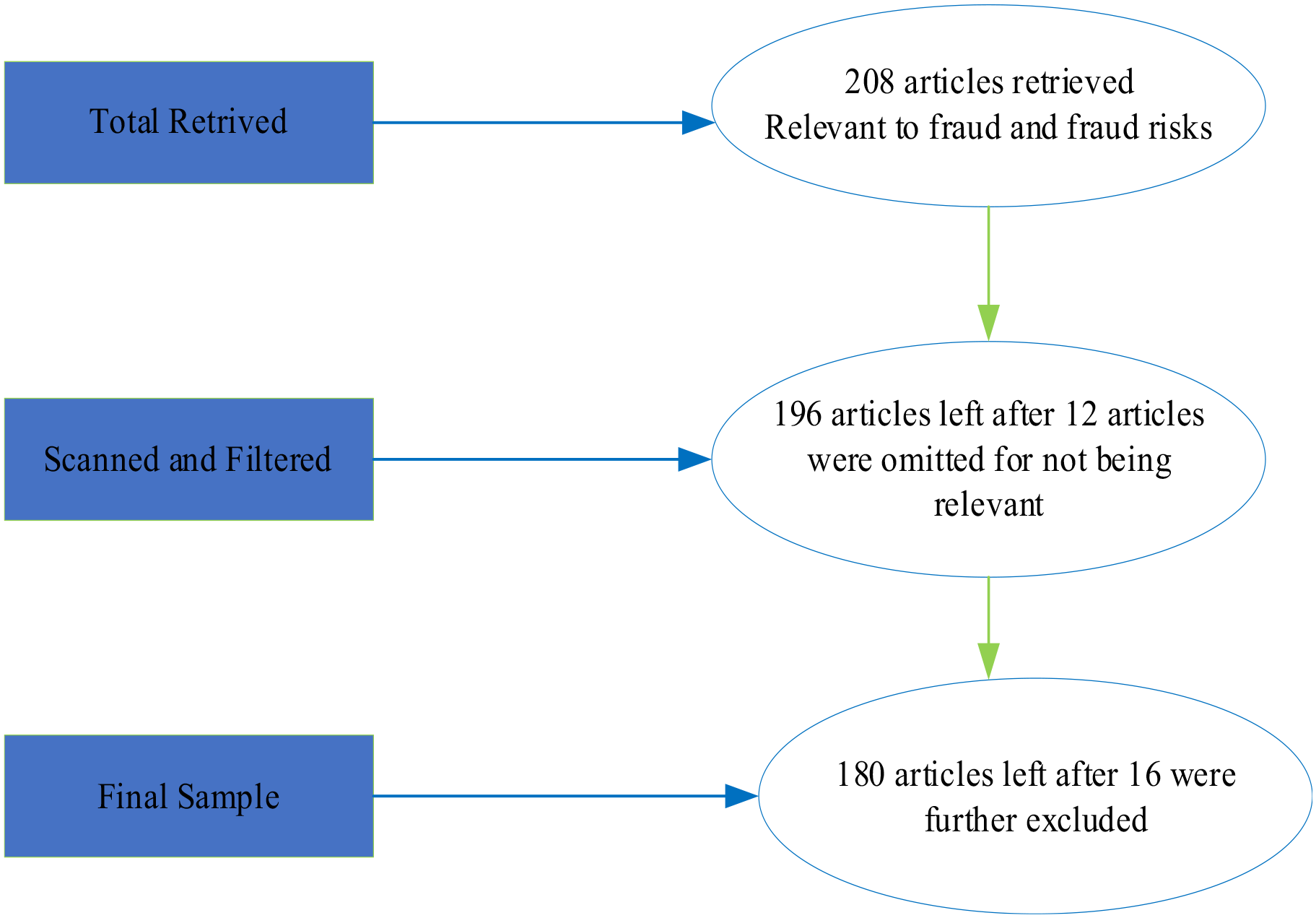

The literature review was conducted according to the guidelines established by Webster and Watson (2002) to identify articles on fraud. Table 2 shows the search terms for relevant articles on critical fraud research. Given the objective of the study, the selected search term includes keywords such as “fraud,” “financial crimes,” “misappropriation,” “deceit,” “cheat,” “rip-off,” “fraud risks,” and “fraud prevention.” Apart from the individual search terms, the boolean operators AND and OR were applied to retrieve as many results as possible. To verify the comprehensiveness of the search, a backward search was carried out to ensure all the articles dealt with fraud and fraud risks (see Baader & Krcmar, 2018). Excluding all articles not addressing fraud and fraud risks, the search yielded 208 peer-reviewed articles that were potentially relevant and covered the conceptualization of fraud, determinants of fraud, fraud detection techniques, methods to prevent fraud and audit processes.

Figure 1 presents the process of selecting and retaining the relevant articles for this study. Initially, the title and abstract were scanned to verify that the articles dealt with fraud and fraud risks. Despite the search terms appearing in the titles and abstracts, some studies were not contextually concentrated on fraud and fraud risks and were deemed irrelevant. During this process, 12 articles were excluded from the sample. After filtering the data for papers, not in peer-reviewed journals and according to the inclusion and exclusion criteria identified in Table 1, 16 articles were deemed irrelevant. The final sample was reduced to 180 articles.

Selection and retention process.

Quality Assessment

The final step in the selection process includes assigning a score to the articles. To assign scores, the ADBC journal ranking was used. An article in an “A*” ranked journal was scored as 1, an article in an “A” ranked journal was scored as 2, an article in a “B” ranked journal was scored as 3, and an article in a “C” ranked journal was scored as 4. As shown in Figure 2, the final sample consists of 62 articles in A*- ranked journals, 59 articles in A-ranked journals, 52 in B-ranked journals, and seven in C-ranked journals. Taken together, the final sample consists of enough observations to analyze the research questions of this paper.

Number of articles and journal quality.

Descriptive Findings

Table 3 presents the results of the journals that published the most articles on fraud and fraud risks. Of the “A*” accounting journals, The Accounting Review and Accounting, Organization, and Society had the most articles published on fraud and fraud risks. Of the “A-ranked journals,”The Critical Perspective on Accounting and Accounting Horizons had the most articles on fraud and fraud risks. Concerning the “B-ranked journals,”Accounting Forum published the most articles on fraud. The point to underscore here is that the journals cited in Table 3 accounted for 129 (or 71.6%) out of the 180 articles in the publication outlets ranked according to the ABDC rankings. Of these top journals, The Accounting Review remains the top journal of choice for accounting fraud research. The “C” ranked journals were not included in Table 3.

Journal Ranking and Number of Publications.

Figure 3 presents the publications per year from 2000 to 2020. Note that there were only a few publications between 2000 and 2004. These findings are quite surprising, considering that an outbreak of accounting fraud (Arthur Anderson, Adelphia, Enron, and WorldCom) occurred around 2000 to 2002 (Eisenberg & Macey, 2004). The time needed to collect data, write research papers, submit, and publish them logically might explain the lack of publications related to early 2000 financial scandals between 2000 and 2004. Around this time, the stock market collapsed as there was news of large corporations restating their earnings. Inversely, there was an uptick in fraud publications immediately following the GFC of 2008/2009.

Publication by year 2000 to 2020.

Type of Methodology

Figure 4 presents the different types of research methodologies used in this research. Of the 180 articles, 91 (51%) were quantitative studies. The rest of the articles comprise 44 (24%) conceptual, 28 (16%) case studies and 17 (9%) qualitative research. These results suggest that quantitative research has been the dominant methodology for studying accounting fraud. The results presented in Figure 4 are not surprising, considering that most top accounting journals will only accept quantitative studies. Most quantitative studies used survey methodologies to collect data and conducted parametric analyses or experiments. The qualitative studies mostly used interviews as the data collection strategy.

Type of methodology.

Type of Research Design

The findings from Table 4 reveal that most of the studies were experiments (45). The number of articles (195 vs. 180) discrepancies is because some studies involve two or more research methodologies. Secondary data was mainly retrieved from the U.S. Securities and Exchange Commission Accounting and Auditing Enforcement Releases (AAER) and financial databases (e.g., CompStat, S&P Global, and Thomson Securities). These articles used various statistical techniques, most notably regression, ANOVA analysis, descriptive statistics, and logit and probit models. Of the conceptual papers, 24 analyzed existing theoretical frameworks, and 20 were involved in designing new ones. Most (21) of the case studies were undertaken using existing reports and documents (e.g., 10 Ks and annual reports). Most of the 21 qualitative studies were conducted using interviews.

Types of Research Design.

As shown in Figure 5, the geographic concentration of studies is primarily in the United States. However, other regions, such as Canada, Australia, and the United Kingdom, have also seen an increased focus on research concerning fraud and fraud risks. A few studies on fraud research have focused on East Asia and Western Europe. These findings demonstrate that fraud is a global issue that affects different regions. Researchers can focus on tailored solutions to combat fraud effectively, considering the different regions and their unique challenges.

Geographic regions.

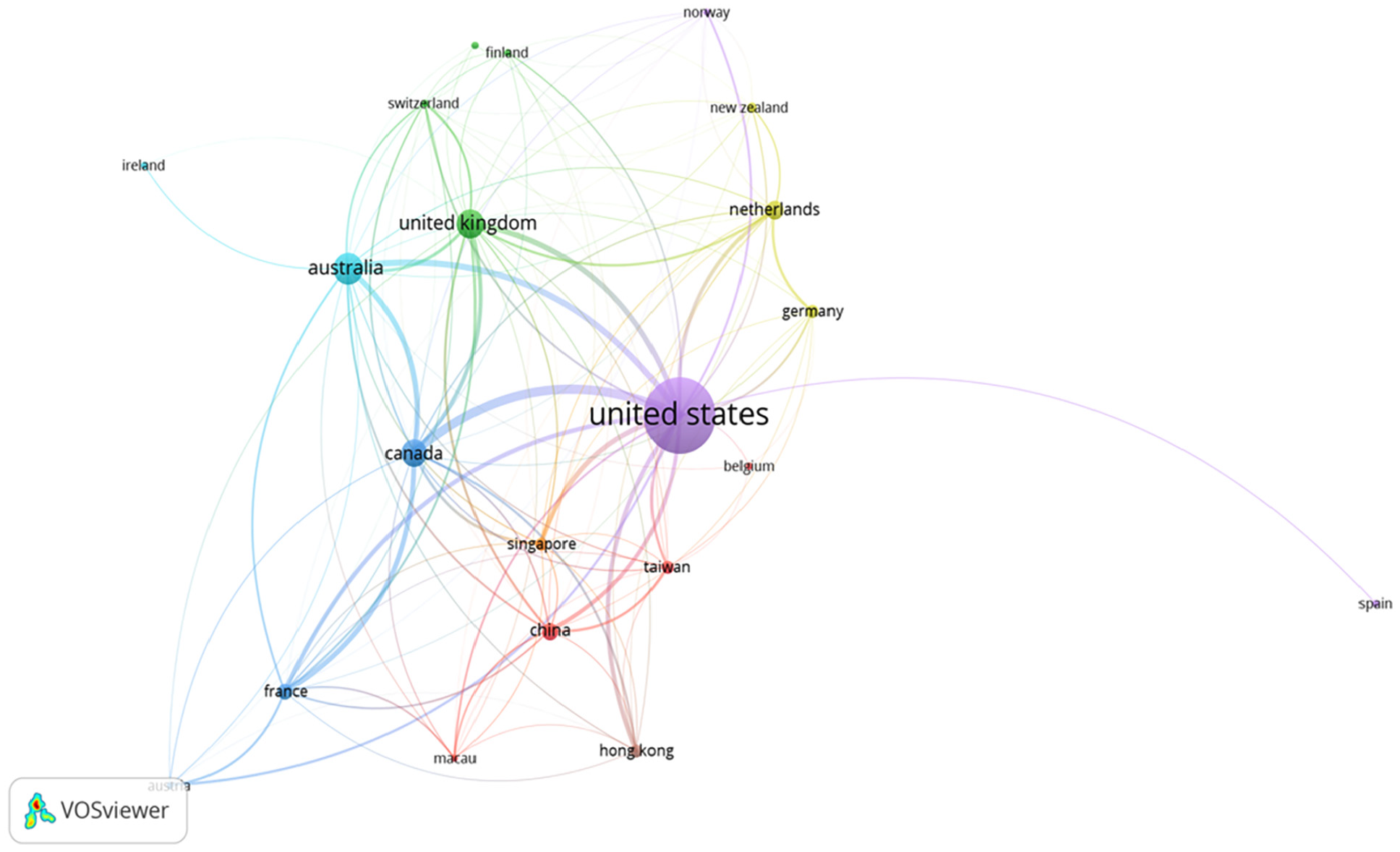

Figure 6 also shows the bibliographic coupling of articles between countries and the shared number of references they contained. Authors from the United States, Canada, Australia, and the U.K. share many references in their articles. These findings indicate extensive collaboration and knowledge exchange between authors from these countries on fraud research. Researchers from the United States and Canada are also collaborating more strongly with researchers from East Asia. These findings highlight the international scope of fraud research and have far-reaching implications for the fight against financial crimes.

Bibliographic coupling of countries.

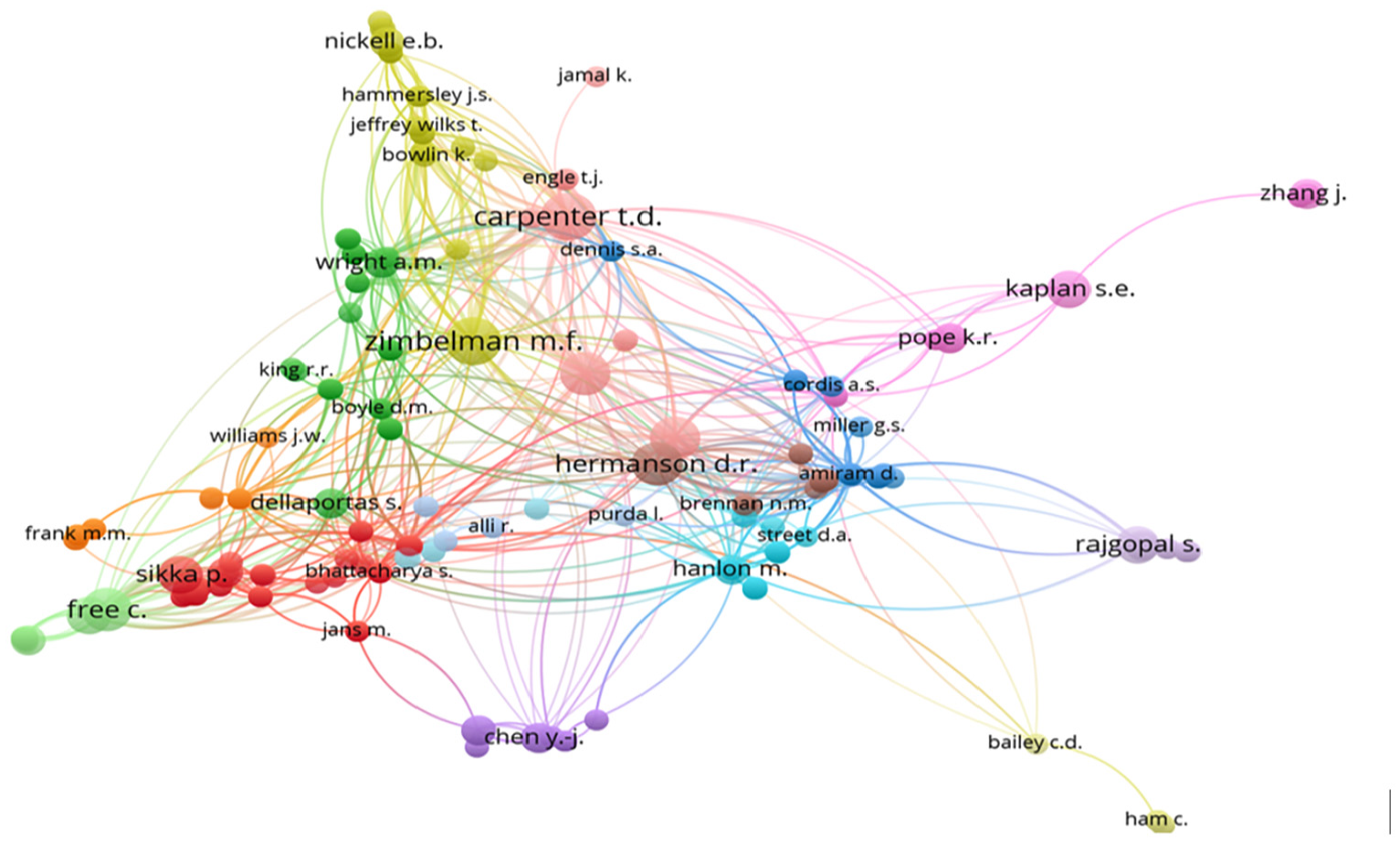

Figure 7 shows the authors with the highest number of citations: Carpenter, Hermanson, Zimbleman, Free, and Sikka. In the context of fraud research, these authors have contributed significantly to developing theories and methodologies for detecting and preventing fraud. These results suggest that these authors have conducted research into the causes and consequences of fraud and the legal and ethical implications associated with fraudulent activities (e.g., see Carpenter, 2007; Free & Murphy 2015; Sikka, 2017; Street & Hermanson, 2019; Trompeter et al., 2014; Wilks & Zimbelman, 2004). Being highly cited meant that the works of these authors have been recognized as influential and valuable to other researchers in critical fraud research. The findings also indicate that these authors have significantly contributed to advancing research on fraud risks and fraud.

Authors with the highest citations.

Figure 8 shows the journals that published fraud research. Accounting Review, Accounting, Organization, Society, the Critical Perspective on Accounting, and the Journal of Emerging Technologies in Accounting have the most research on fraud and fraud risks. Other notable journals that publish critical fraud research are the Accounting Forum, Contemporary Accounting Research, Journal of Accounting Research, and Behavioral Research in Accounting. Figure 9 shows the bibliographic coupling of critical fraud research in accounting and finance. Note from Figure 9 that these journals relate to each other in terms of citations, which suggests they take a more analytical approach to the study of critical fraud research. These findings suggest that research published in these journals is considered influential in critical fraud research and is often cited by others in fraud scholarship. In summary, there seems to be a community of scholars actively engaged in critical fraud research and targeting specific journals to disseminate their findings.

Sources that published fraud research.

Bibliographic coupling of fraud research.

The Conceptualization of Corporate Fraud in the Accounting and Audit Research

Much of the research in the accounting literature that has materialized to date has analyzed fraud from a micro-individual and a macro-institutional perspective. The micro-individualized strand of literature is built on constructing the offender as a “lone wolf” predator who circumvents internal controls to maximize his or her self-interests (Cordoş & Fülöp, 2015; M. E. Lokanan, 2015; Morales et al., 2014; Murphy, 2012). Fraud risks are presented with a moral dimension that is articulated concerning the risk-taking and moral defects of the individual offender (Davis & Pesch, 2013; Gietzmann & Pettinicchio, 2014; Power, 2013; Tommasetti et al., 2021). The literature in this area provides theoretical anchors for organizing and interpreting known facts and provides explanations of fraud from which effective prevention strategies can be devised. What follows, then, are theories that individualize fraud and fraud risks to the rogue offender who can be monitored by audit frameworks and controlled by management (E. Lokanan, 2014; Morales et al., 2014; Power, 2013) and not critical matters that relate to auditing reports (Cordoş & Fülöp, 2015).

Drawing primarily from the social and behavioral science literature, authors of another stream of literature evaluated how structural variables and macro-level features contribute to fraud in organizations and society. The macro-level analysis emphasizes the relationship between the broader structural elements and fraud. These factors can “focus on the broader historical, economic, and political factors that impact organizations” (Morales et al., 2014, p. 174). In this interdisciplinary review, a significant body of work on fraud is highlighted and provides valuable insights into fraud’s collective and systemic nature. In examining the decision to break the law, particular attention is given to socio-legal conditions and the political and economic factors contributing to fraud.

Determinants of Fraud: Micro-Level Analysis

Individual Factors

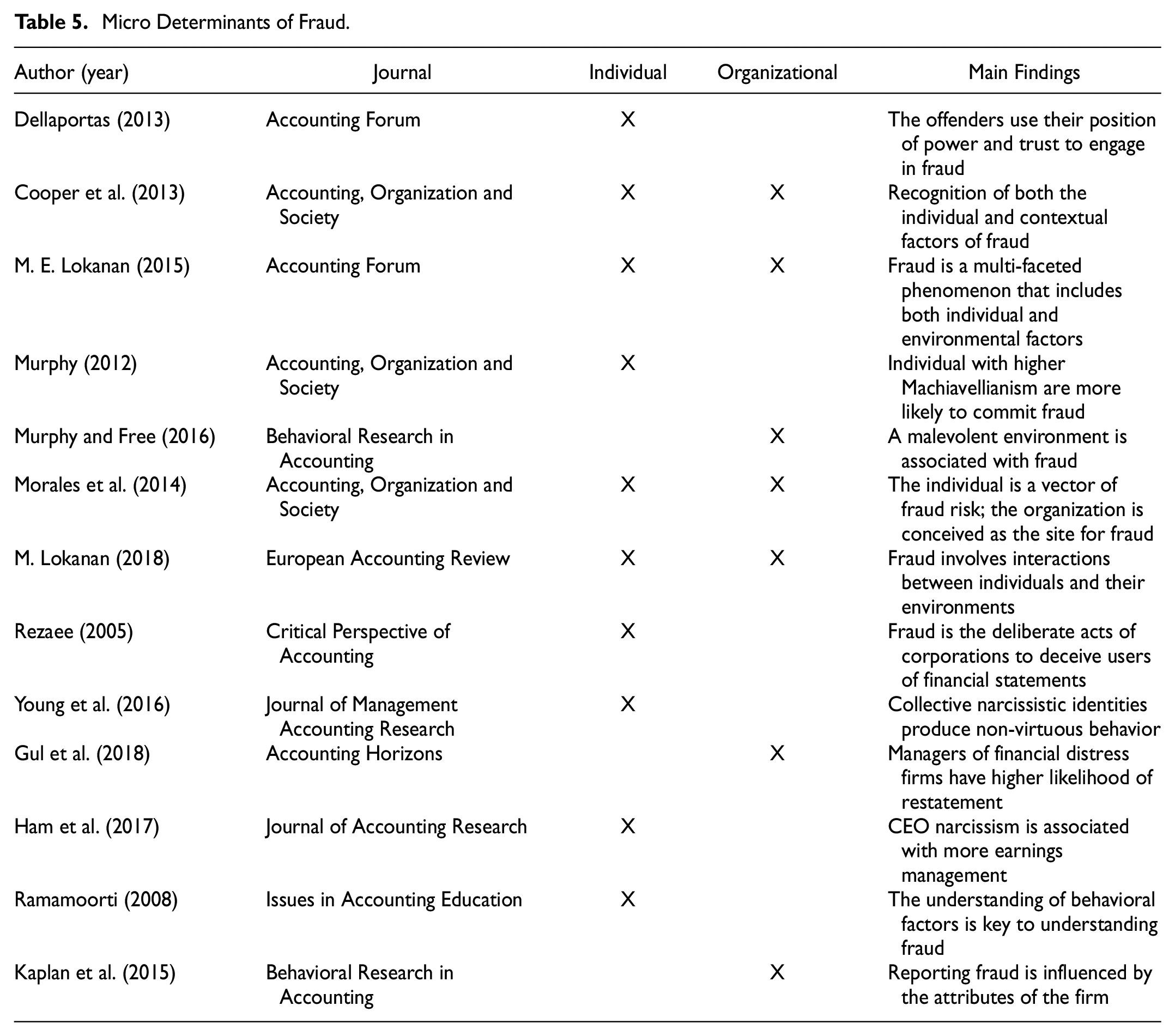

Table 5 presents an overview of the articles that examine the micro-level analysis of fraud. Due to word limitations and to make the paper more stylistically readable, only a sample of the articles were listed in Tables 5 to 7. The micro-level analysis focused on the individual propensity to commit fraud (Cooper et al., 2013; Morales et al., 2014). Morales et al. (2014) defined micro-level analysis as a tool that “focuses on the causes of crime that are located within the individual rather than the social environment” (p. 174). An individual’s moral values and ability to exercise self-control are the key developmental factors influencing his or her action alternatives (M. Lokanan, 2018). Individuals who are unable to control themselves tend to choose acts of crime as a viable action alternative in response to their temptations and motivations (Dellaportas, 2013; Donegan & Ganon, 2008; Murphy, 2012; Murphy & Free, 2016). Individuals who readily consider criminal acts as an alternative they are ready to carry out may be regarded as crime-prone, whereas those who rarely or never consider criminal acts as an action alternative may be regarded as crime-averse (Wikström et al., 2012, p. 15). This general reasoning applies to financial crimes as well. Also, at play in this representation of fraud are accounts that relate fraud not to complex environmental factors but to defects of individual morality and the breakdown of internal controls, both of which combine to produce the predatory offender (Donegan & Ganon, 2008; Morales et al., 2014; Murphy & Free, 2016; Power, 2013).

Micro Determinants of Fraud.

Macro—Determinants of Fraud.

Audit Response to Fraud.

Micro-level determinants emphasize how the interaction of the individual traits of an employee or manager within the organizational framework or environment determines the action alternative chosen by the individual. The individuals’ involvement in a crime depends on their crime propensity (i.e., moral values and the ability to exercise self-control) and the interplay with their exposure to a criminogenic moral context (Cooper et al., 2013; Morales et al., 2014). Individuals engage in crime because of a perception–a choice process that comprises two stages: (1) coming to see such an action as a viable alternative in response to a particular motivation; and (2) the process of choosing (habitually or deliberately) to commit such acts (M. Lokanan, 2018).

Organizational Factors

The individual may also respond to friction from other people in the organization or from other sources of friction, leading to a contagion effect. By virtue of sheer repetition, an argument can then be made that criminogenic behavior becomes ingrained when breaking the law is the first action alternative the fraudster perceives and, subsequently, the action becomes the habitual and only alternative (Matthews, 2005; Mayhew & Murphy, 2014; Rezaee, 2005; Tommasetti et al., 2021). According to Morales et al. (2014) and later M. Lokanan (2018), fraudulent activities are driven by personal gain, either for power and prestige or wealth. For instance, it cannot be proven that top executives are incentivized to boost corporate earnings (Perols & Lougee, 2011; Persons, 2005). In other cases, such as Enron, lax internal controls and increased earnings management were seen as influenced by the narcissistic attitude of top management—self-centered and eager for recognition (Bailey, 2019; Ham et al., 2017; Young et al., 2016). Rezaee (2005) noted that these practices become more prevalent when a firm is financially distressed because the incentives earned through fraudulent activities can positively boost its financial condition. Likewise, Gul et al. (2018) found that financially distressed firms that employ more competent managers and pay higher audit fees possess lower accrual quality and are more likely to undergo a financial reassessment. Influenced by the debt covenant hypothesis, the managers of these firms might engage in material misreporting to lower the cost of debt (Stanley & Sharma, 2011) and relieve the pressure exerted on the firm to perform well (Morales et al., 2014). These findings show that other than the personal Machiavellian nature of the perpetrators (Murphy, 2012), it is the interaction between the individual moral norms and the organizational setting that determines their response to a particular motivator to circumvent ethical standards (Donegan & Ganon, 2008; Ramamoorti, 2008). The rules and practices relating to the organizational setting can significantly impact an individual’s alternative action of engaging in criminogenic behavior.

Previous researchers found that most financial statement fraud is committed with the complicity of top management (Brennan & McGrath, 2007; E. Lokanan, 2014; Rezaee, 2005). Although having an independent board is crucial, having the right attitude and commitment to preventing fraudulent activities is equally important. A lenient enforcement record and an organizational culture conducive to risk can lead to the rationalization of occupational deceit (Kumar et al., 2018). Yu (2014) noted that in the case of Fannie Mae, the CEO’s compensation was tied to earnings manipulation and the firm’s market valuation. Elsewhere, Lennox et al. (2013) and Shafer et al. (2016) found that professional accountants who were highly committed to ethical practices were encouraged by senior management to be aggressive in pursuing cost-saving tax avoidance schemes. Likewise, Kaplan et al. (2015) noted that employees who discovered fraud reported the activities to senior management. According to Kaplan et al. (2015), employees consider the following aspects before blowing the whistle: the positive attributes and attitude of the firm, the correct intention of their managers, and the nature of the fraud. These findings highlight the idealized notion that organizational culture sets the tone for fraudulent activities and, more importantly, that the choice by employees to abstain from reporting fraud is not only a question of personal self-interest but also an assessment of expected utility.

Determinants of Fraud: Macro-Level Analysis

Socio-Legal Conditions

Table 6 presents an overview of articles on the macro-determinants of fraud. Social and legal conditions are responsible for socializing and shaping people’s responses to law and order. The now-famous Enron case exposed how individuals are socialized into fraudulent conduct and the social and legal environments conducive to fraudulent action alternatives (Lehman & Okcabol, 2005; Omurgonulsen & Omurgonulsen, 2009). A business culture with a “business is business” mentality, coupled with the silently seeping corruption of the banks involved and the pressure to meet Wall Street’s expectations, was responsible for Enron’s downfall (Morales et al., 2014). Lehman and Okcabol (2005) took this complicity further to argue that “accounting and issues regarding fraud and crime are part of a broad social fabric: including issues of regulation, governance, economic crises, poverty, race, youth, politics, and class” (p. 616). Similarly, Cooper et al. (2013) explained that not only should fraud be contextualized in terms of “organizational norms, structures, practices, and culture,” but “societal corruption needs to be appreciated concerning distributions of wealth, inequality, and deprivation, as well as regional and tribal rivalries and histories” (p. 441). Invariably, these sensibilities and contexts positioned fraud not only as a product of moral defects but also as an intersection where individual actions are intertwined with the various structural elements of society (Choo & Tan, 2007; Cooper et al., 2013; Gabbioneta et al., 2013; Tommasetti et al., 2021).

One such element is the laws or moral rules that govern individual behavior in institutional and organizational life. To render individuals as rule-guided actors is to subscribe to the view that a fraudulent action is a breach of moral rules defined in law (M. Lokanan, 2018, p. 903; see also Cooper et al., 2013; Murphy & Dacin, 2011; Neu, Everett, Rahaman, & Martinez, 2013; Neu, Everett, & Rahaman, 2013; Schuchter & Levi, 2015). The problem with defining laws as exogenous to structural dynamics is that it invariably exonerates the moral context of the fraudulent action in favor of laws designed to address the frail morality of the offender (Morales et al., 2014; Power, 2013). By their very nature, some acts draw universal public condemnation, which justifies using criminal law to intervene (Devlin, 1959, as cited in Dworkin, 1966, p. 986). This position seems inconsistent with the tradition of individual liberty espoused by Hart (1959). Hart (1959) borrowed from Mills (1859)“harm principle” and argued that the state is not entitled to criminalize behavior unless it causes widespread harm to the public interest. Thus, even though the masses may condemn an act unless it has the potential to cause harm to the public interest, it should not be criminalized (Gabbioneta et al., 2013; Neu, Everett, Rahaman, & Martinez, 2013). In cases where behaviors are criminalized, an act must satisfy two criteria, actus reus (guilty act) and mens rea (guilty mind), to be classified as a criminal offense. Criminal sanctions can only be imposed when these two criteria are met: in other words, the offender is guilty of the act, and at the time of committing the act, he or she had a guilty mind. An offender (no matter how heinous his or her actions are) cannot be found guilty by a court unless their guilty intent can be proven.

Other intractable socio-legal problems concern regulatory frameworks in different jurisdictions. England, unlike Canada and the United States, does not have a criminal code. Criminal law is set out in a series of statutes, each dealing with a specific type of crime, such as the Serious Fraud Act (2006). Acts of Parliament create criminal offenses, and it is left to judges to interpret the text of the legislation (see, e.g., Pepper v. Hart, 1993, and Thet v. DPP, 2006). As it relates to financial crime, common law governs the law of evidence and criminal procedures. This enforcement framework has been criticized for not allowing common-law jurisdictions to be sufficiently responsive and effective in prosecuting financial crimes. Chief among these criticisms is the high evidentiary threshold needed to secure a conviction (Tomasic, 2009, 2011). Because each offense has its constituent parts (i.e., elements), the burden of proof remains high because the prosecution must demonstrate that all the elements exist to prove the offender’s guilt (Woolmington v. DPP [1935] AC 462). This standard of proof is not easily achievable in financial crime because it requires proof beyond a reasonable doubt. The strict rules governing the collection of evidence, the accused’s right against self-incrimination, and the need to protect individual rights (Chappell v. UK, 1990) all combine to make prosecuting financial crimes difficult.

Political Economic Conditions

Other than socio-legal conditions, macro-economic and political factors are seen as determinants of corporate accounting fraud (Dellaportas et al., 2019; Soepriyanto et al., 2022; Stalebrink & Sacco, 2007; Street & Hermanson, 2019). Mironiuc et al. (2012), in their study on financial indicators and the risk of fraud, found that, ostensibly, economic instability was one of the critical determinants of accounting fraud. The pressure exerted by poor economic conditions and weak financial positions is seen as a determinant that leads firms to conceal deteriorating financial positions and commit financial statement fraud (Rezaee, 2005). Similarly, Rezaee (2005) and Brennan and McGrath (2007) found that economic pressures and the perceived “incentives” tied to deceptive financial reporting are the main factors in the decisions of publicly traded companies to indulge in fraudulent accounting. The normalization of fraud as a natural by-product of poor economic conditions weaponized the competitive spirit attached to the capitalist economic system (Drogalas et al., 2017; Morales et al., 2014; Neu, Everett, & Rahaman, 2013; Sikka, 2017).

Though macro-economic factors are among the key indicators of the propensity for fraud, the effect of political factors on criminogenic behavior cannot be ignored (O’Connell, 2004; Stalebrink & Sacco, 2007). A case in point is the Enron fraud. Enron’s executives maneuvered the political establishment in the United States to establish Enron as the leading energy provider in California (Froud et al., 2004). Other macro-political examples include the LIBOR and forex scandals. Both scandals occurred in connection with the GFC and involved players from some of the largest banks involved in a corrupt conspiracy network that rigged the rates (M. Lokanan, 2018). Barclays, for example, lowered its LIBOR submissions to manage analysts’ perceptions that it had a liquidity problem, based in part on its high LIBOR submissions relative to the low submissions by the other panel banks in the United Kingdom’s interbank scheme. In a more systemic and illegal manipulation of the U.S. dollar LIBOR, UBS made false submissions to present an image of financial strength amid analysts’ speculation that the bank was financially unstable during the GFC. Both these examples suggest a relationship between stressful economic conditions and banks’ decisions to choose fraudulent action alternatives (Stalebrink & Sacco, 2007). Macroeconomic stresses expose the fault lines between fraud and the pursuit of profit in the neoliberal economy.

The Audit Response: Fraud Prevention Strategies

Individual Surveillance

Table 7 presents an overview of the articles representing the audit establishment’s response to fraud and fraud risks. The conceptualization of fraud and fraud risks is articulated within narrow limits concerning the type and range of responses reasonably appropriate by standard setters (Camfferman & Wielhouwer, 2019; Dorminey et al., 2012; Nieschwietz et al., 2000; Power, 2013). These limits focus reform efforts on internal and audit controls designed around individuals’ moral defects and the internal control weaknesses of the organizations (Davis & Pesch, 2013; Dilla & Raschke, 2015; Gabbioneta et al., 2013 ; McVay & Szerwo, 2021; Morales et al., 2014; Wilks & Zimbelman, 2004). The outcome is that fraud is seen as a by-product of the risks inherent in a well-functioning system that can be addressed with audit analytics strategies as the normal treatment of reform (Fulop et al., 2019; Neu, Everett, Rahaman, & Martinez, 2013; Norman et al., 2010; Ramamoorti, 2008). It is unsurprising that the discourse on surveillance has caused crime prevention and detection techniques to be seen in specific ways (Cooper et al., 2013, p. 453; Power, 2013; Williams, 2013). The need to establish a micro-socio-psychological perspective on fraud necessitates prevention efforts that are based on the surveillance of individual ethics (Albrecht & Albrecht, 2004, p. 5; Dellaportas, 2013, pp. 31–32; Free & Murphy, 2015, p. 6; Morales et al., 2014, pp. 15–16; Power, 2013, p. 526; Wells, 1997, pp. 3–6).

From these accounts, fraud is conceptualized as solo offending, where surveillance efforts are aimed at the frail morality of the individual offender (Farber, 2005; Morales et al., 2014). The individualistic explanation of fraud is built on the construction of fraud risk that sees fraud as rooted in the individual offender’s frail morality (Braithwaite, 2013; Cooper et al., 2013; Morales et al., 2014; Neu, Everett, Rahaman, & Martinez, 2013; Power, 2013). This diagnostic project promotes a discourse of fraud as not being related to complex environmental factors but to defects in the individual’s frail morality and breakdown of organizational controls, both of which combined and contribute to action alternatives that are criminogenic (Davis & Pesch, 2013; Donegan & Ganon, 2008; Morales et al., 2014; Power, 2013). Of prime interest in the individualization of fraud risk are the processes by which the organizational setting comes to have particular moral norms conducive to fraud and the levels of enforcement associated with those moral norms concerning the opportunities they present (Neu, Everett, Rahaman, & Martinez, 2013; Sikka, 2015 ).

Organizational Surveillance

The interrelated dynamics of institutional and structural variables all contribute to offending behaviors (Gabbioneta et al., 2013; Morales et al., 2014). Given this interconnection, structural theorists argue that crime is socially constructed and, as such, macro-level variables must be incorporated into the explanation. The emphasis on macro-level fraud analyses focuses on audit prevention and intervention efforts into the various realities of organizational and structural life (McVay & Szerwo, 2021; Morales et al., 2014; Powers, 2103). This method of preventing and detecting fraud creates a new risk category known as “fraud risk” (Power, 2013). Crime prevention self-consciously becomes risk-based, and shapes risk management as a functional necessity of evaluating fraud (p. 525).

This approach ignores the intense emphasis on monetary success, which has led to financial misbehavior being consumed and regularized by the fraudulent mechanics of a fraudulent system (i.e., modern capitalism) (Ashforth & Anand, 2003; Choo & Tan, 2007; Galbraith, 2004). In so doing, the practice of criminal law in enforcing legal violations is geared toward certain forms of misconduct, namely crimes perpetrated by offenders who are caught up in corporate life and whose actions are monitored and captured by regulatory technology (Davis & Pesch, 2013; Fülöp et al., 2022; Williams, 2013). Regulatory efforts precede an expanded set of controls and restrictions (e.g., SOX) imposed on organizations to legitimize the audit process and render it thorough and comprehensive for monitoring audit enforcement (Ramamoorti, 2008; Ugrin & Odom, 2010). Companies that follow through on legal regulation reflect a positive organizational commitment to fraud (Rezaee, 2005). The need to cultivate an environment that follows due process supported by proportionate penalties is seen as the tool to ensure that fraud is detected and prevented early (Fulop et al., 2019; Ugrin & Odom, 2010; Wang et al., 2019).

Knowledge Gap: Meso-Level Institutional Connection

Theories of causality must correspond to the empirical realities of fraud. Most human interactions take place in their natural environment. The natural environment combines situational and organizational factors that characterize one’s setting. Rather than confining the study of fraud to the individual circumstances in which it occurs, critical accounting research is best served by uncovering the relationship between the two diverse sociological inquiries (Choo & Tan, 2007; Donegan & Ganon, 2008; Morales et al., 2014). This argument is a common thread that runs through the sociological inquiry into white-collar crime by Becker (1963), Braithwaite (1985), and Coleman (1985, 1987).

Two significant developments, one in field theory and one in economic sociology, reinforced the roles of agents and institutions in criminogenic behavior. In economic sociology, organizational structure and human behavior take the form they do because of the prevailing values and beliefs that have become normalized in situated action (Granovetter, 1985, 1992). In expanding upon this argument, Granovetter (1985) points to the autonomy and dependence of economic action and organizational structure and shows how they are firmly embedded in social interaction. Agency (i.e., individual or organizational) is central, and because of this centrality, planned economic actions can come in various forms that cannot be explained simply as situated actions that occur in organizations.

In field theory, organizational practice occurs in a social space and is characterized by a network of power relationships between agents and the establishment (Bourdieu, 1972, 1990). Field theory is mainly concerned with the role of cultural practice in shaping and understanding the power relations of social action (Killian & O’Regan, 2016; Malsch et al., 2011; Ramirez, 2001; Xu & Xu, 2008). The field is a structured social space (i.e., the institutional setting) where social actors are conditioned to act in a certain way (Bourdieu, 1993). The social spheres (e.g., health care, finance, sports, etc.) have norms and values that govern the activities within their respective settings (Gracia & Oats, 2012; Kurunmäki, 1999; Neu, Everett, Rahaman, & Martinez, 2013; Xu & Xu, 2008). By virtue of their unique practices, fields have their regulative principles, or as Bourdieu (1998) called them, “rules of the game” and “logic of practice” (Bourdieu, 1990), that guide people’s actions.

The combination of economic sociology and field theory draws attention to the need for research that addresses institutional forces and shows how they influence individuals to choose specific action alternatives (M. Lokanan, 2018). Both economic sociology and field theory make the organization central to situated action and human interaction and lay the groundwork for researchers to go beyond the micro and macro and into the meso-level of analysis. Within the purview of economic sociology, the organization is seen as a force, while in field theory, the organization is seen as operating in a social space where economic capital and power relations act to structure the dynamics of human behavior (Bourdieu, 1990). In explorations of the micro-macro connection, the institution mediates between organizational forces and the agents who act as purveyors of the field in which there is strategizing and competition for contested resources (Gracia & Oats, 2012).

Based on these accounts, a comprehensive theoretical explanation of the etiology of fraud must consider individual actions and how those actions are structured by organizational forces in their respective institutional settings. For example, the actions of the traders and banks implicated in the LIBOR fraud must be analyzed within the context of both structure and agency. Critical accounting research cannot accept the notion that fraud results from an individual’s frail morality and position within the organizational and broader social structure without acknowledging the meso-level institutional connection. Re-conceptualizing fraud requires researchers to explore the micro-macro- and meso-connections to explore the individual, organizational, and institutional variables that contribute to individual choices to circumvent regulations.

A meso-level analysis of fraud considers the actors’ institutional space, consisting of a network or configuration of relations between their positions. Micro-macro- and meso-connections create links between the complexity of the field (as an institutional space) that addresses environmental concerns (i.e., competitive pressures); between the different cultural frames that are parts of the field; and between the corresponding structural and cultural routines that are enacted within the field (Hoffman, 2001). The field is represented as a space with several dimensions where fraud is committed by agents or groups capable of exerting power and influence over institutions and corporations (Gabbioneta et al., 2013; M. Lokanan, 2018). The field-level analysis of fraud goes beyond individuals and organizations as the fundamental sources of actions to the distinctly structured field of intelligibility governed by its rules. The field is seen as autonomous and the purveyor of its own space, in which criminogenic behavior is tied to complex interactions among laws governing financial markets, institutional codes and guidelines, corporate appearances, and elite interpersonal networks (Nakpodia & Adegbite, 2018).

Conclusion and Areas for Future Research

In the accounting literature, fraud is conceptualized to signify acts committed by predatory offenders within a set of well-defined limits (M. Lokanan, 2018; Morales et al., 2014). This definition of fraud in the accounting and finance literature is not broad in that it specifically mentions a method (financial statement contortion) and a victim group (external stakeholders). This seems to be a definition specific to financial statement fraud in publicly traded companies rather than a general definition. These limits are structured in two distinct schools of thought. On one side are those who examine fraud through an individualistic lens and emphasize the individual offender’s frail morality (Cooper et al., 2013; M. Lokanan, 2018; Morales et al., 2014; Murphy, 2012). The emphasis is on “understanding the personal traits that place an individual at high risk for offending” (Price & Norris, 2009, p. 538). This “individualization” and “responsibilization” of corporate offending (Power, 2013, p. 526) frames “fraud risks” around vectors on the individual morality of the offender (Norman et al., 2010) and aligns with crime-control policies designed and executed by the criminal justice system to address such misbehavior (Choo & Tan, 2007; Dellaportas et al., 2019; Donegan & Ganon, 2008; M. E. Lokanan, 2015; Morales et al., 2014; Murphy & Dacin, 2011). On the other side are scholars who deviate from this dominant explanation and argue that the causes of fraud do not lie simply in the individual’s frail morality—today’s policy obsession—but rather in the situational mechanisms that link the individual’s action to his or her wider structural environment (see also, Beneish & Vargus, 2002; Choo & Tan, 2007; Cooper et al., 2013; Donegan & Ganon, 2008; Free & Murphy, 2015). A renewed look at crime control policies must focus on prevention as opposed to after-the-fact intervention that ignores the environmental and institutional characteristics of crime causation (Choo & Tan, 2007; Cooper et al., 2013; Donegan & Ganon, 2008; M. E. Lokanan, 2015).

What is notable about these two schools of thought, however, is that they are endowed with a false sense of representation. Both positions are articulated within narrow conceptual frames concerning how fraud is conceptualized and the subsequent audit apparatus that encourages auditors to focus on measures to mitigate individual risks (Davis & Pesch, 2013; Power, 2013). Risk mitigation is constituted most profoundly at the outer boundaries of reforms and shifts organizational surveillance to systems of controls that are reasonable techniques to detect and prevent fraud (M. Lokanan, 2018, p. 907; see also Gietzmann & Pettinicchio, 2014; Power, 2013; Williams, 2013). The conceptualizations of fraud portray it as the hegemonic abuse of power by individuals and organizations predicated on the frail morality of the predatory offender and on vectors of riskiness that must be tightly controlled by the risk management enterprise (Power, 2013; Williams, 2013). These accounts represent a conceptual and implementation-based closure, which, by definition, excludes far more intensive and comprehensive reforms that, although detrimental to fraud prevention, may function to perpetuate fraudulent behavior. Consequently, accounting researchers have overlooked several broader theoretical questions over the past two decades regarding how fraud and fraud risks are conceptualized and studied.

Future researchers must come to terms with these limited discursive frames and modes of knowledge that have come to represent fraud in the accounting literature. The focus, instead, must be on the totality of the actors and their behavior within their structured space (i.e., field settings), where they compete for personal, group, and institutional gains. This interest in the narrowly conceptualized scholarship on fraud needs to be shifted from its linear focus to one that integrates the field and its structured setting—including the role of context as not simply an object of organizational discourse in the analysis but as a critical ingredient that shapes the interactions of individuals and institutions within systems of control. The emphasis should be on stepping out of the ontological box that has long shaped fraud scholarship and into research that uncovers the distal order of the operative elements and hidden complexities constituting fraud and, by extension, fraud risks. This stream of research can consider the geographic context of fraud research and conduct comparative analyses across different regions to identify patterns or differences in fraud occurrences. The interest in understanding fraud at the field level of analysis requires critical fraud researchers to emerge from the ontological frame of unmasking individual and organizational deceit and come to terms with theoretical tools that will better allow them to unearth new knowledge that embodies a reified view of criminogenic behavior. A broader theoretical framing of understanding fraud from several dimensions represents future research in this area. This strand of research is expected to bring a new form of realism to fraudulent behavior and present a reified view of finance, markets, and the network of corporate institutions. Research in this direction extends the coverage of business and institutional space more generally and considers autonomous calculation and the totality of individual actions in fraud scholarship.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Funded by Social Sciences and Humanities Research Council of Canada