Abstract

This study explores how different factors affect tax compliance behavior among Romanian individual taxpayers. By unpacking tax compliance into nine drivers—tax system fairness, trust in government and tax authorities, efficiency, and transparency of government spending, knowledge of tax legislation, tax legislation simplicity, personal financial constraints, personal ethics, and moral standards, the social environment, and coercive measures—this study develops clear-cut paths of the drivers of tax compliance from the perspective of a developing country. The proposed research hypotheses were tested with a sample of 402 individual taxpayers and quantitative data analysis was carried out using partial least squares-structural equation modeling. The results showed that seven drivers (tax system fairness, trust in government and tax authorities, knowledge of tax legislation, personal financial constraints, coercive measures, moral standards, and tax legislation simplicity) were significant factors that increase the likelihood of tax compliance among individual taxpayers. Our findings are expected to provide tax authorities and governments new insights on tax compliance behavior that enable them to develop fiscal methods, strategies, policies, and legal measures tailored to local context, and constraints.

Introduction

Our contemporary society faces various challenges related to rapid economic and social change, globalization, digitalization, new business models, taxpayer mobility, pandemic recovery, and conflict context. As a result, governments and tax authorities must focus more on improving tax system efficiency by strengthening tax discipline via innovative methods of tax collection and efficient use of fiscal resources worldwide (Cirman et al., 2021; Pop & Pelau, 2017). In some countries, governments have achieved major fiscal, administrative, and policy reforms, as well as significant revenue mobilization improvements. However, such successes have been unevenly distributed and continue to pose significant obstacles for others (Dom et al., 2022).

The European Union’s (EU) landmark financial instrument for pandemic recovery, known as the Recovery and Resilience Plan (PNRR), was developed as a set of sustainable reform measures and investments that each member state aims to implement by 2026 (European Commission, 2021). The year 2021 was designated as the starting point for the development and implementation of PNRR for Romania and other EU member states. For the Romanian National Agency for Fiscal Administration (ANAF), this new European financial instrument represents one of the most important opportunities in recent years as it offers the largest source of non-refundable financing (over 350 million Euros) for the implementation of fundamental reforms with the final objectives of modernization, performant services, and efficient tax collection (ANAF, 2021). According to the PNRR, Romania has an excessive deficit and requires a variety of reforms, particularly in the areas of increasing budget revenues, strengthening revenue collection, and optimizing budget expenditures. These goals can be accomplished primarily by increasing voluntary tax compliance, which is a more efficient, and cost-effective method to achieve collection targets than restrictive, or punitive measures or higher taxes (European Commission, 2021).

Although enforcement has been and will continue to be the basis of most reform strategies, governments face a significant challenge in determining the optimal balance of enforcement, facilitation, and trust-building measures to maximize revenue while simultaneously advancing broader development goals (Dom et al., 2022; European Commission, 2017). Although all of these factors clearly matter, a consensus has yet to be reached on how to combine them in a holistic manner. Most likely the answer will depend on defining the specific goals and constraints in various contexts while viewing enforcement, facilitation, and trust as complementary rather than distinct strategies (Dom et al., 2022).

Creating a taxpaying culture in which citizens see paying taxes as an integral aspect of their relationship with their government and tax authorities (OECD, 2021) is fundamental to provide countries a stable, predictable, and sustainable fiscal environment, public goods, and a wealth distribution system (Wahl et al., 2010). All this depends on the existence of an effective engagement between the state and citizens and the pivotal role played by the tax system in this relationship (Dom et al., 2022). Strengthening social contracts is emphasized not only to enhance tax compliance but also to develop political support for sustainable reform and to consistently deliver more effective, equitable, and accountable tax systems (Dom et al., 2022).

This study aims to explore the underlying key challenges of tax compliance for Romanian individual taxpayers that represent barriers to tax reform. Based on this research question, we proposed several research hypotheses and tested them using a sample of 402 individual taxpayers. The data analysis was performed using partial least squares-structural equation modeling (PLS-SEM). Specifically, this study provides an empirical assessment of nine independent variables associated with tax compliance behavior arising from economic, social, institutional, and behavioral issues. The independent variables are fairness of the tax system, tax coercion, trust in government and tax authorities, efficiency and transparency of government spending, tax knowledge, personal financial resource constraints, personal ethics and moral standards, the taxpayer’s social environment, and tax simplicity. The primary rationale for selecting these variables is that the current tax compliance research has focused primarily on the corporate tax rate or trust in tax authorities (Jimenez & Iyer, 2016; Wahl et al., 2010), procedural justice (Gobena & Van Dijke, 2016), complexity of taxes and tax knowledge (Saad, 2014), taxpayers’ religiosity (Mohdali & Pope, 2014), taxpayers’ emotional experiences (Enachescu et al., 2019), and tax awareness (Cyan et al., 2016).

Examining these variables collectively in a single study better explains voluntary tax compliance levels than the single-study method employed in the previously mentioned studies, especially in countries such as Romania, which has the lowest tax revenue as a percentage of GDP of all the EU member states. At the opposite end of the scale, Denmark, France, and Belgium registered the highest ratio of tax revenue to GDP (European Commission. Directorate-General for Taxation and Customs Union, 2021). According to Danquah and Osei-Assibey (2018), a country’s inability to reduce the tax gap results in slow growth and inadequate provision of public goods and services. Furthermore, Dell’Anno and Davidescu (2019) find that Romania has the highest level of tax evasion and one of the worst performing tax collection systems. Additionally, it has experienced considerable economic, social, and political movements in the last two decades and is characterized by a weak reform process. In particular, similar to other Eastern European countries, Romania has experienced a discontinuous socio-economic development process with events that have influenced its economic environment (e.g., joining the EU, the onset of the global crisis, and several episodes of economic and political instability) (Dell’Anno & Davidescu, 2019).

Our research contribution is supported by the actual significance given to boosting budget revenues and strengthening tax revenue collection in Romania, as outlined the objectives assumed through the Annual Strategies by the Romanian National Agency for Fiscal Administration (ANAF). According to published ANAF (2021), budgetary stability and construction of an institutional framework and a favorable business climate are essential in the current circumstances. Tax payment must be viewed by as a civic duty and a priority for every taxpayer and fiscal administration, respectively. To the best of our knowledge, in Romania, little research has been conducted on this topic, especially comprehensive research incorporating economic, social, psychological, cultural, and behavioral tax compliance issues. Previous studies (Batrancea et al., 2019; Mitu, 2016), have tended to focus on the limited determinants of the tax compliance behavior. In addition, there is no empirical research investigating tax compliance behavior using a quantitative approach and PLS-SEM. Therefore, our study is significant in that it contributes to the limited prior research in Romania on this subject.

The present study will contribute in the following ways. First, this study attempts to extend the existing body of knowledge by adding to the debate and by providing a clearer image and a more comprehensive view of taxpayer compliance behavior from a developing country perspective. Second, the study seeks to supplement the limited literature available in Romania on this subject. Finally, this study is expected to provide tax authorities and government agencies insights on tax compliance factors, thus enabling them to develop tailored fiscal methods, strategies, and policies as well as legal measures to improve the tax compliance behavior of all taxpayers in the country. A better knowledge of taxpayer compliance behavior can better position tax authorities and the government to develop and apply effective compliance strategies that in turn contribute to economic development and improved welfare. Because it would increase government income and support better economic growth to improve citizen welfare, the entire community stands to benefit from enhanced tax compliance. Moreover, our study is relevant not only for Romanian tax authorities and government but also for tax authorities and governments in other countries with similar historic backgrounds. Since in recent years almost all Eastern European countries have embarked on programs aimed at reforming and improving their tax systems, it is critical to embrace the most appropriate strategy to increase the level of compliance. Similar studies applied to this geographical area may lead to comparable conclusions.

The remainder of this paper is organized as follows. Section 2 presents the literature review and hypotheses development. Section 3 describes the research methodology. The research results are reports in Section 4. Section 5 concludes the study and offers recommendations for future research.

Literature Review

Earlier scholars have defined tax compliance from different perspectives. According to James and Alley (2002), one of the simplest definitions of tax compliance is the degree to which taxpayers obey the tax law. Additionally, James and Alley (2002) explain that, from a legal perspective of taxpayer action, tax compliance should be viewed in terms of complying with both the letter and the spirit of the law. Using a psychological and social approach, Kirchler (2007) define tax compliance as taxpayers’ willingness to pay their taxes, while Roth et al. (1989) describe tax compliance as the correct reporting of the tax liability according to the tax law. According to Inasius (2019) and e Hassan et al. (2021) tax compliance refers to a taxpayer’s ability and willingness to comply with tax law, to accurately declare income annually, and to pay all taxes on time.

Understanding why taxpayers comply or do not comply with the tax law is key to achieving high levels of tax compliance in the future and effectively solving the fiscal gap (Department of the Treasury, 2007; Saad, 2012). Tax compliance has always been an important challenge for many governments in both developed and developing countries owing to the government’s interest in finding revenue it requires to meet public needs (Musimenta et al., 2017). Even though managing tax compliance is a common issue for multiple nations, the drivers of tax compliance decisions differ from country to country. Scholars such as Palil (2010) explain this variation by highlighting the fact that countries opt for different approaches when designing policies to promote tax compliance and each has different tax laws and regulations. However, in light of the dynamic environment, continuous research in the tax compliance field is required given that changes in conditions over time may result in different findings.

Different taxpayer motivations result in varying levels of tax compliance (Wahl et al., 2010). These differences manifest at personal levels and take individual forms as taxpayers come from a wide variety of cultural contexts, backgrounds, and have different income, tax knowledge, and educational levels (e Hassan et al., 2021). Furthermore, when individuals interact, they tend to copy the behaviors of their peers and others with whom they identify. Moreover, as a result of the interactions between taxpayers and tax authorities, experiences (both positive and negative) are gained by both sides (Mitu, 2016).

In the past few decades, tax researchers have increased their efforts to better understand issues such as tax compliance behavior, tax morale, and tax evasion. Their findings support the theory of behavioral economics as a theoretical framework (Vincent, 2021). According to this line of research, various economic and behavioral factors affect tax compliance decisions. The economic components of behavioral economics theory highlight the taxpayers’ predisposition toward non-compliance when the estimated gains outweigh the costs (Vincent, 2021). Coercive measures may be used as tools for driving taxpayers to exercise compliant behavior. Regarding the behavioral approach, taxpayers’ different perceptions of tax compliance are related to their attitudes, values, ethics, beliefs, culture, demographic characteristics, peer influences, norms, and roles (Vincent, 2021). The behavioral component is also referred to as social effects, which are influenced by a taxpayer’s sociocultural environment (Vincent, 2021; Weber et al., 2014). Sociocultural factors include social norms, psychological factors, prestige, fairness, and peer influences. Besides coercive measures, psychological factors can deter a taxpayer from failing to pay taxes (Vincent, 2021). Psychological factors arise from people’s fear of being detected or openly shamed (Vincent, 2021).

Nevertheless, previous studies have yet to reach a consensus regarding the factors influencing tax compliance behavior, which is the aim of the current study in the context of Romanian individual taxpayers. Accordingly, this study tries to determine various relevant factors using a holistic approach that add value to the emerging literature on tax compliance behavior.

Hypotheses Development

Tax System Fairness

According to prior research, taxpayers perceive the tax system as unfair when their taxes exceed what they receive from the government and/or when their taxes are higher than those paid by other taxpayers (Chau & Leung, 2009; e Hassan et al., 2021). Gilligan and Richardson (2005) point out that society’s perceptions of tax system fairness and equity is essential in maintaining compliance. If the community perceives the tax system as fair and just, voluntary compliance will also increase. Individuals desire to be treated fairly when they contribute to society’s resources by giving up a share of their income. Therefore, the process of taxation should be fair, simple, and transparent, including the filing of tax returns, collections, audits, and interactions with tax authorities (e Hassan et al., 2021). According to Dissanayake and Kirchler (2021), individuals require fair treatment not only because they believe that fair distribution will result but also because the opportunity to express one’s own opinion has intrinsic value. Prior research has shown that the way tax authorities treat taxpayers impacts tax morale and compliance decisions (Dissanayake & Kirchler, 2021). Therefore, procedural fairness is considered a key factor in tax compliance. Indeed, studies have shown that lower tax compliance occurs when individuals feel they have been treated unfairly (Alm, 2019; Dissanayake & Kirchler, 2021).

The extant literature has further established that taxpayers are more likely to not pay their taxes if they perceive tax unfairness as a result of unfair fiscal income redistribution (Spicer & Becker, 1980; Vincent, 2021). According to Etzioni (1986), an unfair tax system is more prone to non-compliance than an increased tax rate. Even if the tax rate remains stable, taxpayers are more likely to evade taxes if they believe the tax is unfair (Vincent, 2021). According to Hite and Roberts (1992) and Vincent (2021), the perception of fairness has a strong correlation with the perception of an improved tax system and dissuades taxpayers from deciding on non-compliance. Determinants of tax attitudes and perceptions are fairness and equity in fiscal revenue distribution, trustworthiness and accountability for taxes collected by the government, the peer influence of other taxpayers, and the taxpayer’s moral obligation to file complete tax returns (Francis, 2019; Sapiei et al., 2014; Vincent, 2021).

Overall, citizens’ trust and compliance levels improve in correlation with their judgments of the appropriateness and fairness of government acts. The perceived effectiveness of fiscal measures, procedural fairness, and distributive and redistributive justice are thus essential in building and maintaining trust, as well as for ensuring cooperation willingness. Based on these arguments, we propose the following hypothesis:

Hypothesis 1 (H1). The perception of tax system fairness is positively related to tax compliance behavior.

Coercive Measures

According to the theoretical economic model, Allingham and Sandmo (1972) describe tax compliance as the decision to declare actual income to the tax authorities in charge under uncertain situations (Bani-Khalid et al., 2022; Taing & Chang, 2021). The assumption in this model is that taxpayers make rational choices in their attempts to minimize their taxable income. Tax compliance decisions are based on an analysis of the benefits and costs of complying with the utility of their non-compliance. Thus, a rather small penalty and a low probability of being caught result in non-compliant behavior in comparison with the utility gained through non-compliance. By creating a higher probability of detection and the related penalties for non-compliant taxpayers, governments seek to ensure that the consequences of non-compliance exceed its costs (Horodnic, 2018; Williams, 2014). According to this model, taxpayers make rational choices, exhibit selfish behavior, and attempt to retain their money. In this case, taxpayers can either make a safe or risky choice by declaring their gross income accurately and paying the full tax amount or by under-reporting their gross income and evading their taxes, respectively. In addition, it is important to note that taxpayer income cannot be verified by tax authorities unless a tax audit is performed (Weber et al., 2014).

The previous research provides empirical evidence that economic considerations or high risk aversion are insufficient to explain taxpayers’ compliance decisions (Cirman et al., 2021; Horodnic, 2018). According to Alm (2012), behavioral aspects are needed to solve the tax compliance puzzle. Individuals do not always make rational and economic choices with complete information. In addition, they have limited capacity to assess actual costs and benefits and their behavior is shaped by various social contexts (Cirman et al., 2021).

According to the European Commission (2017), enforcement; that is, compelling taxpayers to do the right thing using the full power of the tax authority, has been and will continue to be an essential tool for tax authorities in their efforts to improve the fairness of tax systems. This includes building cross-border cooperation, conducting effective audits, having access to information and intelligence, and establishing timely recovery procedures. Even though sanctions are indispensable to tax enforcement, they may not always be the first choice. An overly severe tax system is an important obstacle to business formalization, and raising the level of penalties has the opposite effect. Therefore, instead of repressing taxpayers, sanctions must be used to deter and motivate them to voluntary comply (Swistak, 2016).

Empirical research concludes that taxpayers’ decisions cannot be described just from an economic perspective. By incorporating various approaches, we can gain a better understanding of taxpayers’ irrational behavior and expand our toolkit for implementing an efficient tax policy (Kirchler, Muehlbacher et al., 2007). Past research has demonstrated that increased coercive measures produce inconclusive results (Horodnic, 2018). For instance, some studies found a strong correlation between perceived detection or sanctions and tax morale, while others found no evidence for this correlation. Moreover, special importance must be given to the fact that increased levels of coercive measures may affect the trust between taxpayers and their government, thus leading us to the following assumption:

Hypothesis 2 (H2). Coercive measures are negatively associated with tax compliance behavior.

Trust in Government and Tax Authorities

Rather than being perceived by taxpayers as competitors, according to Cirman et al. (2021), tax authorities should aim to be seen as their partners in achieving common goals. In this regard, tax authorities ought to build public awareness of why taxes are needed, and emphasize their connection to public spending. Therefore, building trust in institutions, fostering a sense of responsibility toward the community, and supporting taxpayers in fulfilling their obligations are crucial tasks for tax authorities (Cirman et al., 2021; Güzel et al., 2019). Hofmann et al. (2008) assert that in a climate of mutual trust, citizens spontaneously cooperate and have a positive perception of the tax system and tax authorities. As such, institutional trust can be viewed as a fundamental characteristic of modern democracies and is essential to ensure social, economic, and political stability. Also, institutional trust is negatively correlated with discretionary policy measures (Canale & Liotti, 2019; Cirman et al., 2021). According to Batrancea et al. (2019), trust and the power of authorities increase the intention to comply with taxes and reduce the intention to engage in tax evasion across countries with different economic, political, sociodemographic, and cultural backgrounds.

Kirchler et al. (2008) define trust as individual taxpayers and social groups’ perception that the tax authorities take action and promote the common welfare. Earlier researchers make reference to the relational aspects of trust and distinguish between social and calculative trust (Wahl et al., 2010). Feld and Frey (2007) and Wahl et al. (2010) explain what drives taxpayers to be loyal and honest in their tax payments and emphasize the significance of how taxpayers feel treated by tax authorities, namely a psychological contract and sense of mutual trust between taxpayers and tax authorities. According to Kirchler et al. (2008) and Wahl et al. (2010), reciprocal confidence between taxpayers and tax authorities creates a synergistic fiscal climate. On the one hand, tax authorities trust that taxpayers pay their taxes honestly and accordingly treat them with respect and courtesy; on the other hand, taxpayers trust that tax authorities provide quality services and subsequently pay their fair share of taxes (Kirchler et al., 2008; Wahl et al., 2010).

Previous studies have provided empirical evidence that citizen tax compliance is related to how efficiently the government spends its resources (Vincent, 2021). Vincent (2021) explains that an individual’s decision to obey tax laws is influenced by the level of government spending on public goods. In this view, tax compliance decisions are the result of taxpayers’ perceptions of the benefits they receive in return for their tax payments. According to Barone and Mocetti (2011) when the government allocates resources efficiently, tax compliance improves. However, when the government engages in wasteful spending, taxpayers may be dissatisfied, and retaliate by engaging in tax evasion (Vincent, 2021). Torgler (2012) has also shown that trust in the government, the justice system, and the quality of governance have a major impact on citizens’ tax morale in Eastern European countries. Moreover, reducing the social distance between taxpayers and tax authorities increases taxpayers’ acceptance of the tax burden and their compliance with tax laws (Cirman et al., 2021).

Therefore, when trust in the authorities is high, taxpayers perceive a synergistic climate, feel motivated to contribute to the general welfare, and pay their taxes rather than trying to increase their individual profit. As such, tax payments originating from trust correspond to voluntary behavior where in taxpayers fulfill their duties. Based on this discussion, we hypothesize the following:

Hypothesis 3 (H3). The perception of the efficiency and transparency of government spending is positively correlated with tax compliance behavior.

Hypothesis 4 (H4). The perception of trust in government and tax authorities positively influences tax compliance behavior.

Taxpayers’ Knowledge of Tax Legislation

Education plays a significant role in shaping an individual’s behavior, values, and attitudes (Cirman et al., 2021). According the OECD (2021) and Cirman et al. (2021), the more taxpayers know about the tax system and the vital role it plays in their daily lives, the more receptive they will be to supporting it. According to Engida and Baisa (2014) and Hofmann et al. (2008), while educated taxpayers may become more aware of ways to avoid paying taxes, they will better understand the tax system, and their increased development level promotes a more favorable attitude toward taxes and increased compliance with tax law. In addition, the education of young people as future taxpayers must be prioritized (OECD, 2021). Cirman et al. (2021) and the OECD (2021) highlight that young people’s education and their engagement in different forms of fiscal activity will develop a “culture of compliance” via increased understanding of the role of taxation, their rights, and obligations, and how they can support the growth of public financial revenues.

According to Cirman et al. (2021), education is a method of empowering taxpayers by providing them with the knowledge and tools required to better understand the tax system and boosting their tax morale, which ultimately improves tax compliance. Thus, taxpayer education initiatives can be an efficient and effective method of establishing trust and increasing public engagement. These initiatives will increase people’s commitment to the common good, emphasizing the social value of the tax and its connection to public spending (Cirman et al., 2021; OECD/FIIAPP, 2015). New taxpayer education and communication initiatives can encourage future taxpayers to be more ethical in paying their taxes by explaining why it is essential that everyone pays their fair share of taxes (European Commission, 2017). According to Cirman et al. (2021), educating young people can act as a lever that boosts the national tax culture and has a constructive influence on the country’s tax compliance and tax morale.

Prior research has established that, in addition to tax education, knowledge of tax regulations has a significant impact on taxpayers’ compliance behavior (Bandara & Weerasooriya, 2021; Cyan et al., 2017). According to Krause (2000), people who are more educated about tax laws appreciate the importance of taxes, thus increasing the state revenue generated by the tax sector. Taxpayer awareness of the importance of timely filing and payment of taxes is also essential to ensure tax law compliance (Bandara & Weerasooriya, 2021).

Taken together, higher education is associated with increased knowledge of tax laws and the benefits of taxation. As a result, we anticipate that increased tax knowledge will have a beneficial effect on tax morale for net welfare state beneficiaries and a net influence on contributors, leading to the following hypothesis:

Hypothesis 5 (H5). Taxpayers’ knowledge of tax legislation is positively related to tax compliance behavior.

Personal Financial Constraints

The existing literature has identified that individual financial circumstances and family responsibilities both moderate the correlation between an individual’s commitment and performance (Alabede et al., 2011; Mathieu & Zajac, 1990). According to Alabede et al. (2011), when an individual is financially secure or has a minimal financial need, the association between commitment, and performance is strong. Engida and Baisa (2014) find that financial constraints may encourage individuals to prioritize certain payments to support their fundamental necessities or allocate financial resources to where there are pressing needs in the case of a limited income (e.g., the perceived threat of action by money lenders) rather than to tax obligations. Collectively, these factors can be seen as drivers of tax evasion. According to previous researchers, individuals experiencing personal financial constraints are more prone to engage in tax evasion than individuals who are not in this financial situation (Engida & Baisa, 2014; Feher et al., 2019).

Thus, an individual’s decision to comply or not comply with tax laws can be affected (positively or negatively) by their financial circumstances, independent of the relationship between tax compliance and the influencing factors (Alabede et al., 2011). Financial circumstances can elicit an unpleasant sense of distress for an individual. Likewise, the inability to pay taxes may bring about an uncomfortable feeling. In this case, individuals may perceive tax payments as a significant restriction, which encourages non-compliant tax behavior (Alabede et al., 2011). Financial strain was considered by Bloomquist (2003) as one of the causes of individual taxpayer stress. Therefore, an individual with limited financial resources may be prone to tax non-compliant decisions when their household expenses exceed their income (Alabede et al., 2011; Bloomquist, 2003). Previous scholars have found that a person with a sound financial situation is more willing to comply with tax laws than a person with limited financial resources (Alabede et al., 2011). According to Bloomquist (2003), a higher probability of non-compliance is attributed to taxpayers with limited financial resources because they are more vulnerable to financial strain. Similarly, Carroll (1986) demonstrates that individuals seeking opportunities to commit tax crimes are often motivated by a lack of funds.

Income level and occupation are seen as variables that represent opportunities for non-compliance. Previous empirical research has established a correlation between these variables and tax compliance behavior (Alabede et al., 2011). According to Ritsema et al. (2003), reported income levels are favorably related to the amount of taxes owed. Manaf et al. (2005) conclude that middle-level income taxpayers are more tax compliant. In addition, Fjeldstad and Semboja (2001) find that employees who pay their taxes through a withholding method have the least opportunity for non-compliance.

Clearly, personal financial constraints can play an important role in ensuring tax compliance. Taxpayers’ financial constraints can motivate them to prioritize their financial burden over their tax liability. We expect that taxpayers facing financial constraints tend to be less compliant, leading to the following assumption:

Hypothesis 6 (H6). Personal financial constraints are negatively related to tax compliance behavior.

Personal Ethics and Moral Standards and the Taxpayer’s Social Environment

The term “tax morale” is most frequently used to define an individual’s intrinsic motives to pay taxes (Horodnic, 2018; Torgler, 2002, 2005; Torgler & Schneider, 2007). According to Horodnic (2018), tax morale can be viewed as the sum of non-monetary motivations and variables for complying with taxes that fall outside of expected utility maximization. Dissanayake and Kirchler (2021) consider that individual compliance behavior depends primarily on descriptive norms, which are usually recognized as perceptions of how other individuals behave based on observations of one’s peers and significant others. One possible outcome of this is conformity, which means changing one’s behavior to conform to that of others (Dissanayake & Kirchler, 2021). Consequently, the behavior of others can serve as an individual’s “license to cheat” (Dissanayake & Kirchler, 2021). Accordingly, previous scholars have pointed out that observations of other taxpayers’ non-compliance may lead some taxpayers to be less compliant (Dissanayake & Kirchler, 2021; Fochmann et al., 2019).

According to Horodnic (2018), the behavioral sciences examine individuals as part of their social groups and cultures rather than as isolated entities. Therefore, according to Horodnic (2018), the informal institutions related to societally shared unwritten rules, values, and beliefs shape an individual’s attitude and behavior. As such, an act that defies accepted social norms can result in internal (e.g., guilt, shame) or external (e.g., social stigma) sanctions (Horodnic, 2018; Torgler & Schneider, 2007). Previous studies highlighting culture as a broad social norm identify a correlation between tax morale and informal institutions (Horodnic, 2018; Luttmer & Singhal, 2014). A study by Kountouris and Remoundou (2013) analyzes individuals who live in the same area but have different cultural backgrounds and concludes that the tax morale of individuals in their native country has an effect on their tax morale in their host country.

Similarly, a positive correlation was found when comparing tax morale with church attendance frequency (Horodnic, 2018). Accordingly, it can be presumed that apart from religious beliefs, having a stronger community feeling in general has a constructive effect on tax morale (Horodnic, 2018). According to Horodnic (2018), tax morale increases with the sense of belonging to the community, social responsibility, and civic participation, measured as active involvement in the community, participation in elections, or civic duty. Moreover, when some honest individuals, in discussions with their friends and family, realize that other individuals are cheating on their tax liability, their own tax morale declines as a result of reduced horizontal trust (Horodnic, 2018).

Taken together, when people in a community have a high level of trustin each other, their tax morale increases (Horodnic, 2018; Torgler et al., 2008). On the other hand, when the perceived level of tax evasion is high and other taxpayers are viewed as non-compliant, tax morale falls (Horodnic, 2018; Togler etal., 2008). Therefore, analyzing the impact of informal institutions suggests that cultures, communities, and reference groups influence tax morale (Horodnic, 2018). Tax morale improves when compliance with tax laws is recognized as a societal norm and fraudsters face marginalization and social disapproval (Horodnic, 2018).

As such, tax morale among honest taxpayers declines in societies where horizontal trust is low and the individual perceives that a substantial portion of the population is evading taxes. Hence, we make the following assumptions:

Hypothesis 7 (H7). The influence of the reference group is positively correlated with tax compliance behavior.

Hypothesis 8 (H8). Personal ethics and moral standards positively influence tax compliance behavior.

Tax Legislation Simplicity

According to e Hassan et al. (2021) an ideal tax system is simple, fair, and enforceable and encourages economic growth. Therefore, tax legislation simplicity may have a significant effect on taxpayers’ compliance decisions (e Hassan et al., 2021; Palil & Mustapha, 2011; Richardson, 2006). By simplifying the tax return process, taxpayers will no longer transfer the duty to professionals, but instead consider completing it themselves (e Hassan et al., 2021). According to Chau and Leung (2009), tax system complexity is a major factor in tax evasion. According to Murphy (2009), the simplicity of taxes influences our opinion on the proposed fair fiscal policies. Earlier scholars provide evidence that simplifying tax payments is a relevant factor in voluntary compliance, implying that a complicated tax system can act as a deterrent to taxpayers’ voluntary compliance (e Hassan et al., 2021; Saad, 2014; Santoro, 2021).

Tax systems will be significantly less complicated when tax legislation and regulations are uniform in their application and performance, which can encourage tax compliance and leads us to the following hypothesis:

Hypothesis 9 (H9). Tax legislation simplicity is positively related with tax compliance behavior.

Based on the aforementioned arguments and hypotheses, the conceptual framework of this study is illustrated in Figure 1.

Conceptual framework.

Research Methodology

To empirically validate the proposed research hypotheses, a quantitative research method based on a questionnaire distributed online was employed. This study used a quantitative research method in which, according to Saunders et al. (2009), the researcher has a reduced opportunity to manipulate factors that could influence results. The quantitative research was based on a self-administered questionnaire distributed online to make it easier for respondents to fill it out. The purpose of the questionnaire-based research was to evaluate and validate the theoretical model of this research. No ethics approval was required for this research. Before commencing the data collection, participants were informed about study purpose. Their involvement was entirely voluntary, so they were free to withdraw at any time. We did not obtain any names, addresses, or contact information, and we did not publish any personal information. Also, participants did not receive any incentives to complete the research questionnaire.

The target population of the current research was Romanian individual taxpayers. Initially, a total of 443 questionnaires were received. Among the received responses, 41 questionnaires were excluded because they were incomplete. Therefore, the final sample consists of 402 responses used for analysis. According to Hair et al. (2019), a minimum of 200 samples is suggested for PLS-SEM. Likewise, Kline (2015) recommends a minimum of 100 observations for estimating PLS-SEM and 200 observations for reliable estimates. Our research sample size (N = 402) fulfilled this criteria. To ensure that our study is representative, respondents are drawn from a range of backgrounds, educational levels, sectors, ages, and job experiences. It is anticipated that these differences would enable them to present views and arguments from different perspectives and provide rich information for the study. The respondents’ characteristics are summarized in Table 1.

Demographics of the Respondents (N = 402).

Source: Authors estimation.

The demographic information pertaining to the respondents is summarized as follows: There were 260 (64.7%) male respondents and 142 (35.3%) female respondents. Most of the respondents (143 (35.6%)) were aged 35 to 50 years. In terms of education level, 130 (32.3%) of the respondents had a master’s degree. Concerning the respondents’ occupation, 41.5% had a private job. Most of the respondents 157 (39.1%) have a job experience, ranging from 3 to 9 years. Regarding respondents’ income levels, 142 (35.3%) had an income of LEU 5,000 to 10,000 per month.

To test the postulated relationships depicted in the proposed model (see Figure 1), a questionnaire-based research study incorporating measuring items for all variables of the model was conducted. The questionnaire-based research consists of two parts. The first contains a series of questions about respondents’ demographics, while the second addresses tax-related issues. The questionnaire comprises 34 items, measured using a 5-point Likert-scale, with responses ranging from 1 = strongly disagree to 5 = strongly agree. The researchers developed constructs based on the items that were most relevant to their research question. The questions were developed based on research literature (Benk et al., 2012; Bobek & Hatfield, 2003; Bobek et al., 2007; Dragojlovic, 2008; Joulfaian, 2009; Musimenta, 2020; Poudel, 2018; Vincent, 2021; Wahl et al., 2010; Wenzel, 2005).

This study used 10 constructs in which tax compliance behavior was measured with four items, using taxpayers’ commitment to tax obligation and their honest intention to report the correct income for each year and pay the correct amount of taxes on time. The fairness of the tax system was measured with three items focused on the perception of fairness and equity in fiscal revenue distribution and government acts. Tax coercion was measured with four items using indicators about compelling taxpayers to do the right thing using the full power of the tax authority by creating a higher probability of detection and the related penalties. Four items were used for tax knowledge of respondents. It focuses on taxpayers’ knowledge about tax law, tax regulations, their rights and obligations, and the benefits of taxation. Personal financial constraints were measured with three items related to taxpayers’ limited income that create them a financial stress and motivate them to prioritize their financial burden over their tax liability. Trust in government and tax authorities was measured with four items, focused on the perception of the appropriateness and legitimacy of government actions. Efficiency and transparency of government spending were measured with three items related to the perception that tax compliance decisions are the result of taxpayers’ awareness of why taxes are necessary and emphasizing their connection to public spending and the actions of tax authorities to promote the common welfare. Personal ethics and moral standards, the taxpayer’s social environment, and tax legislation simplicity were measured with three items each. Personal ethics and moral standards in this study was measured using honest indicators in tax payment, not violating ethics, carrying out the right actions, having a strong community feeling, and see the tax payment as a civic duty. A taxpayer’s social environment was measured using the perception of how others behaved based on observations of the individual’s peers and significant others. Tax legislation simplicity was measured using indicators focused on the simplicity of the tax system, tax legislation, regulations, and their application, which will be able to encourage tax compliance. Our research constructs are presented in Appendix A.

The authors used structural equation modeling (SEM) through smart partial least squares (PLS) to test the hypothesized proposed relationships among the constructs (see Figure 1). The analysis was performed in two parts. The first part confirmed the measurement model, and the second examined the hypothetical relationships between the constructs.

Research Results

As presented in Table 2, the normality test of the data was validated because all constructs had skewness and kurtosis values that fell between the standard levels (−2 and +2). In this study, Harmon’s one-factor test revealed a 31.4% variance of the first factor, which is smaller than the recommended cut-off value 50%, indicating that common method bias (CMB) was not a concern.

Measurement Model.

Source. Authors estimation.

Note. FL = factor loadings; CA = Cronbach’s alpha, CR = composite reliability; AVE = average variance extracted; FTS = fairness of tax system; CM = coercive Measures; FR = financial resource constraints; KTL = Knowledge of tax legislation; PEMS = personal ethics and moral standards; RG = Referral group; TCB = tax compliance behavior; TGS = trust on government spending; TLS = tax legislation simplicity; TTA = trust in government and tax authority.

According to Table 2, the composite reliability (CR) and Cronbach’s alpha (CA) values for almost all constructs exceeded the .70 threshold, indicating that the collected data are consistent and reliable. The CR values ranged from 0.801 to 0.909 for all constructs, which exceeds the 0.70 threshold, and the CA values of exceeded the recommended threshold of 0.70, with the smallest CA being 0.642, which is considered a moderate value (Hair et al., 2003). Our findings support good convergent validity as the values of factor loadings (FL) of most items are above the specified threshold (0.60), and also the value of average variance extracted (AVE) fulfills the criteria (>0.50).

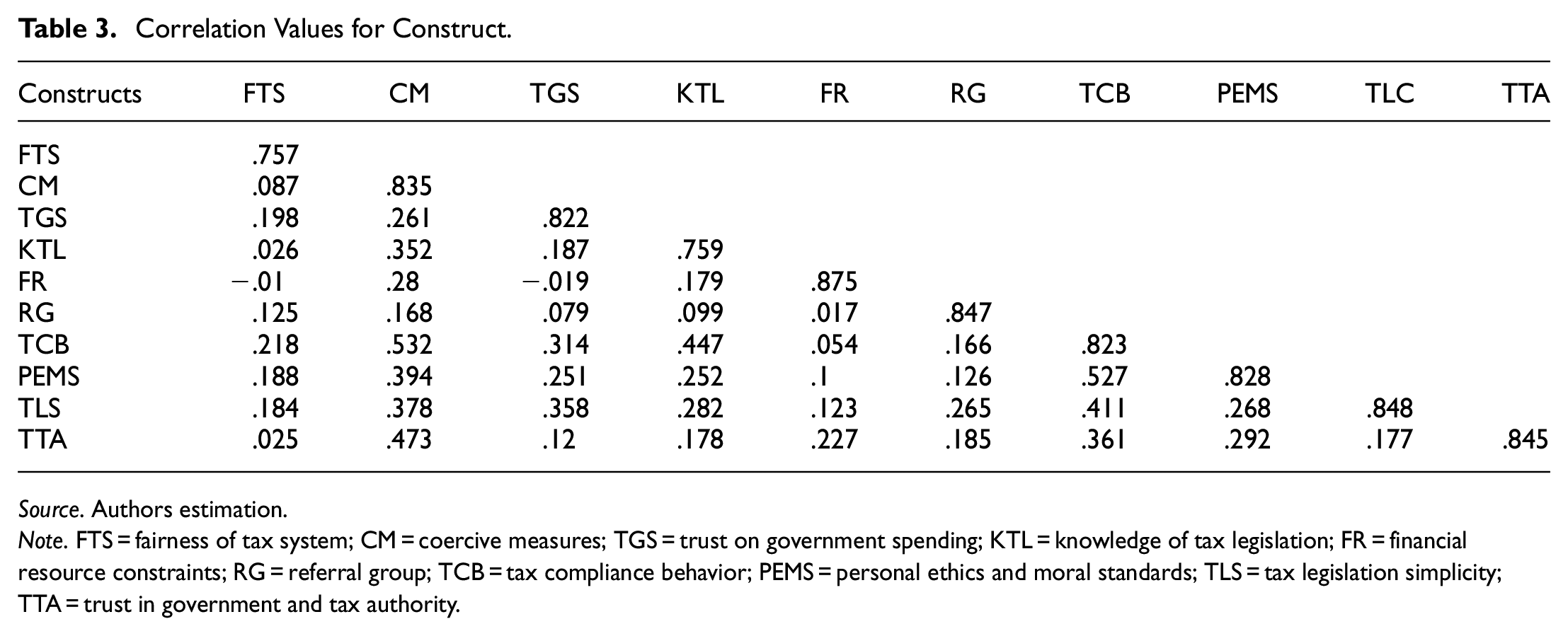

As revealed in Table 3, the AVE square root values are greater than the corresponding correlation values of the constructs. Thus, the Fornell-Larcker test (square root of AVE values) was greater than the corresponding latent variable correlations, indicating satisfactory discriminant validity. Moreover, as shown in Table 4, the cross-loading values of other variables are lower than the FL values of each construct, indicating good discriminant validity.

Correlation Values for Construct.

Source. Authors estimation.

Note. FTS = fairness of tax system; CM = coercive measures; TGS = trust on government spending; KTL = knowledge of tax legislation; FR = financial resource constraints; RG = referral group; TCB = tax compliance behavior; PEMS = personal ethics and moral standards; TLS = tax legislation simplicity; TTA = trust in government and tax authority.

Cross Loading.

Source. Authors estimation.

Note. FTS = fairness of tax system; CM = coercive Measures; TGS = trust on government spending; KTL = knowledge of tax legislation; FR = Financial resource constraints; RG = referral group; TCB = tax compliance behavior; PEMS = personal ethics and moral standards; TLS = tax legislation simplicity; TTA = trust in government and tax authority.

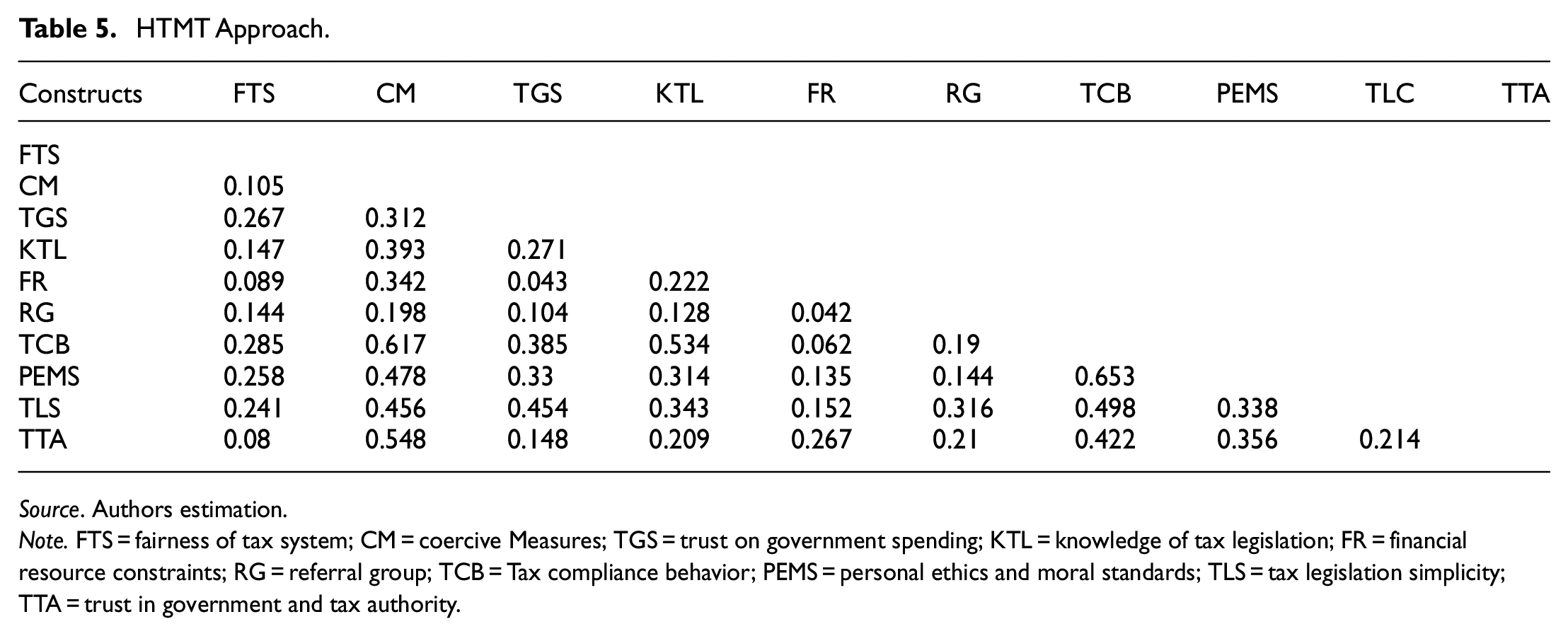

Table 5 reveals that the Heterotrait-Monotrait ratio (HTMT) values of all the variables were less than the threshold level of 0.80. Consequently, in this study, the discriminant validity criteria were fulfilled for all constructs.

HTMT Approach.

Source. Authors estimation.

Note. FTS = fairness of tax system; CM = coercive Measures; TGS = trust on government spending; KTL = knowledge of tax legislation; FR = financial resource constraints; RG = referral group; TCB = Tax compliance behavior; PEMS = personal ethics and moral standards; TLS = tax legislation simplicity; TTA = trust in government and tax authority.

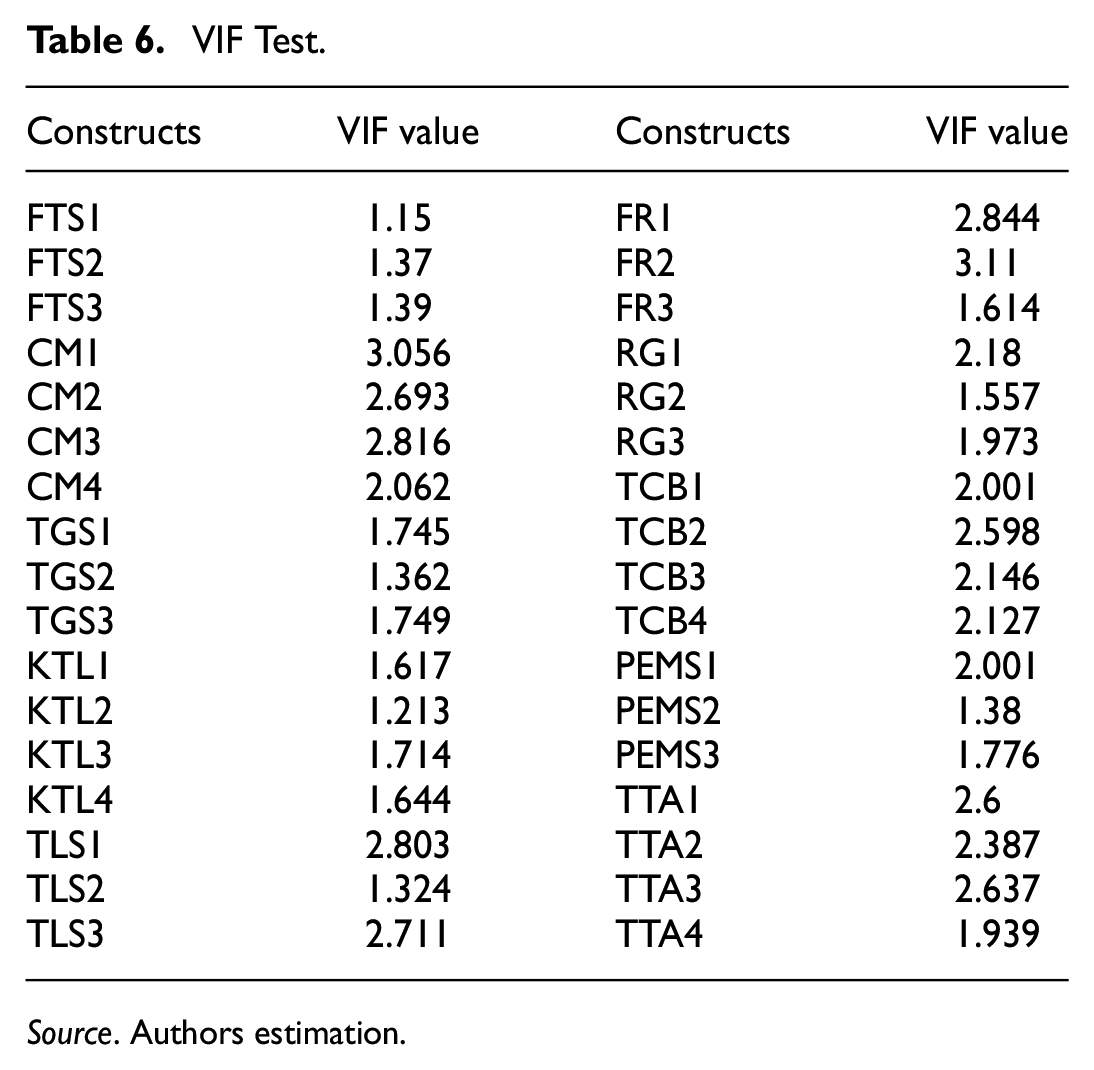

Table 6 depicts the results of the variance inflation factor (VIF) to estimate the multicollinearity among the variables. The VIF values, which varied between 1.15 and 3.11, were less than the cut-off value of 5, indicating that our model does not exhibit multicollinearity.

VIF Test.

Source. Authors estimation.

Testing the Proposed Hypotheses

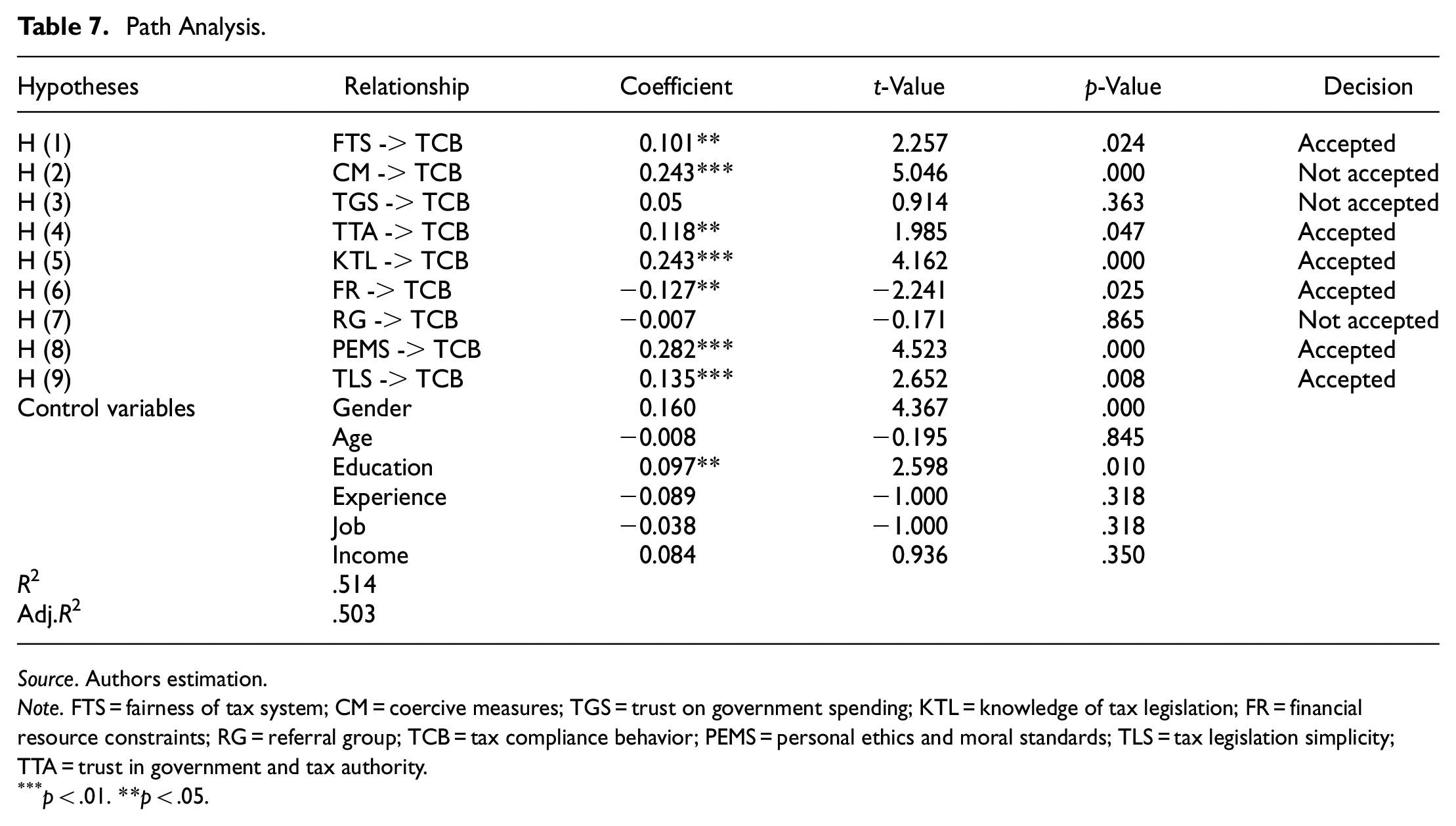

Table 7 depicts the path analysis that exposes the relationships between the understudy constructs. To test the validity of the relationship, a bootstrapping process with 5,000 iterations was applied using the SmartPLS 3.0 software. The predictor variables explain approximately 51% of the variability in tax compliance behavior, as indicated by R2 = .514.

Path Analysis.

Source. Authors estimation.

Note. FTS = fairness of tax system; CM = coercive measures; TGS = trust on government spending; KTL = knowledge of tax legislation; FR = financial resource constraints; RG = referral group; TCB = tax compliance behavior; PEMS = personal ethics and moral standards; TLS = tax legislation simplicity; TTA = trust in government and tax authority.

p < .01. **p < .05.

According to Table 7, the results show that the fairness of the tax system has a significant and positive impact on tax compliance behavior (β = .101; t = 2.257; p = .024 < .05). Therefore, H1 is accepted and well supported. Regarding H2, the results depict that coercive measures have a significant and positive impact on tax compliance behavior (β = .243; t = 5.046; p = .000 < .01). Therefore, H2 is not supported because it predicts that tax coercion will negatively influence tax compliance behavior, whereas our findings suggest a high probability of coercion may result in increased tax compliance behavior. H3 predicts that the perception of the efficiency and transparency of government spending is positively correlated with tax compliance behavior. However, the structural analysis indicates an insignificant relationship between the perception of government spending and tax compliance behavior (β = .051; t = 0.914; p = .363). The insignificant coefficient indicates that a positive perception of how the government spends taxpayer money may have no effect on tax compliance behavior. Thus, H3 is not supported. We examined the effect of trust in government and tax authorities on tax compliance behavior in H4 and found that trust in government and tax authorities is positively associated with tax compliance behavior (β = .118; t = 1.985; p = .047). Thus, H4 is supported. Regarding H5, we predicted that taxpayers’ knowledge of tax legislation has a significant and positive impact on tax compliance behavior. In line with this prediction, the results show a significant and positive relationship between tax knowledge and tax compliance behavior (β = .243; t = 4.162; p = .000 < .01). Therefore, H5 is well supported. The results indicate that personal financial constraints have a significant negative relationship with tax compliance behavior (β = −.127; t = −2.241; p = .025 < .05). Our findings fall in line with the expectation that personal financial constraints would reduce taxpayer tax compliance tendencies as financial distress may encourage an individual to prioritize what must be paid first. Therefore, H6 is well supported. In H7, we predicted a significant and positive relationship between the taxpayers’ reference group and tax compliance behavior. However, the results indicate an insignificant relationship between the taxpayers’ reference group and tax compliance behavior (β = −.007; t = 0.171; p = .865). Therefore, H7 is not supported. Regarding H8, our study assumes that personal ethics and moral standards are positively associated with tax compliance behavior. In support of this prediction, we find a significant and positive coefficient (β = .282; t = 4.523; p = .000 < .01) for personal ethics and moral standards, thus indicating that they have a positive relationship with tax compliance behavior. H9 predicts that tax legislation simplicity is positively related with tax compliance behavior. The findings indicate a significant and positive relationship between tax legislation simplicity and tax compliance behavior (β = .135; t = 2.652; p = .008 < .01). Therefore, H9 is supported.

Prediction Power

The prediction is defined as Q2. Any result above 0 has a good prediction, whereas those below 0 are not useful for a prediction. Previous scholars suggest that results of 0 or lower have a very low level of prediction, those 0.15 or lower are on a middle level, and those higher than 0.35 havehigh predictive power for the variable (Sander & Teh, 2014). In our case, the structural model has good prediction since the results for Q2 are all above the standard value for all the variables, falling between 0.30 and 0.69.

Conclusion and Recommendations

The purpose of this study was to identify the key factors affecting individual taxpayers’ compliance behavior in Romania given that this country has the lowest tax revenue as a percentage of GDP of all the EU member states.

According to our study findings, coercive measures remain an important tax compliance tool for Romanian individual taxpayers, thus implying that increasing coercive measures, such as tax audit, detection likelihood, and coercive sanction, encourage taxpayers to comply with tax laws. Our findings are consistent with those of previous studies. Williams and Horodnic (2016) find a positive association between tax compliance and the perceived penalties or detection. However, our findings contradict the conclusion of Torgler et al. (2010), who report no evidence for this association. Moreover, increased levels of deterrence may damage the trust between taxpayers and their governments (Pommerehne & Frey, 1992).

As coercive measures remain a significant determinant of tax compliance behavior, tax auditing, and detection systems should be strengthened in Romania. As a proposed practical measure, tax authorities should strengthen their inspection of taxpayers’ tax declarations, payments, and refunds. Based on our study’s findings, we recommend the government and tax authorities introduce large-scale digitization and design tax detection systems in the development of future tax practices.

From the empirical analysis, we find that the fairness of the tax system is a significant driver of tax compliance behavior. Furthermore, this finding reveals that if an individual’s tax burden is comparatively higher than others, tax compliance behavior decreases. A fair and stable tax law system may promote compliance among individual taxpayers. The overall conclusion is consistent with previous studies. Gilligan and Richardson (2005), emphasize that society’s perception of a tax system’s fairness and equity is essential for compliance. If the community perceives the tax system as fair and just, voluntary compliance increases. In addition, according to Alasfour et al. (2016), taxpayers care about the fairness of outcomes and expect to be treated fairly based on their accomplishments and efforts. Moreover, taxpayers perceive the tax system as unfair when their taxes exceed what they receive from the government and/or when their taxes are unjustifiably higher than those paid by other taxpayers (Chau & Leung, 2009; e Hassan et al., 2021).

Additionally, our findings suggest that the relationship among taxpayers, the government, and tax authorities is essential for tax compliance decisions because evidence reveals that the way in which the government and tax authorities gain taxpayers’ trust has a significant impact on their tax compliance decisions. To reduce tax non-compliance, the government and the tax authorities must consistently operate the tax system in an efficient manner, which means tax authorities must redesign their tax information strategies to provide more efficient service and tax compliance decisions. Tax authorities must be strengthened and empowered through a digital movement, efficient investment in technology, improvements in the working environment, cultural transformation, and training. Digitization will allow the achievement of transparency in budgetary allocations and the budget structure, which can lead to better information for citizens regarding how the public’s taxes are spent. In addition, mutual trust between taxpayers and tax authorities may act as a deterrent to non-compliance behavior. Citizens’ involvement in the construction of the budget and the allocation of public funds for various community and national interest projects can potentially increase citizens’ commitment to tax compliance. From a practical point of view, it is possible to achieve both financial support for disadvantaged social groups and a certain customization of the taxation system at the level of disadvantaged groups’ incomes.

According to our study, tax authorities must be able to identify and adapt to different types of taxpayers—depending on their actions—through targeted responses with the role of preserving, consolidating, and encouraging voluntary tax compliance behavior; counseling and providing support for those who wish to comply but have difficulty doing so; and the application of measures to stimulate compliance for taxpayers who do not want to comply with tax laws. This study demonstrates that tax administration services can foster tax compliance behavior by increasing tax morale, creating a more positive perception of the tax system, and by decreasing perceptions of the complexity of tax filing procedures. For instance, tax authorities can disseminate information about tax compliance procedures through media campaigns, educational programs, or collaborations with opinion leaders. This information should not only raise individual taxpayer awareness of the importance of tax compliant behavior but also educate them concerning their right to a transparent and coherent assessment of their tax liability while also teaching them how to obtain owed tax refunds and how to defend themselves against corrupt officials.

According to our findings, individuals experiencing personal financial constraints are more likely to engage in tax non-compliance than those who are not. Financial strain may encourage individuals to prioritize what needs to be paid first, which means that it is more probably that individuals with limited financial resources will seek to evade taxes as owing to their vulnerability to financial strain (Engida & Baisa, 2014). As a result, a taxpayer’s personal financial constraints may encourage him/her to prioritize his/her financial burden over his/her tax obligations and tax compliance.

Personal ethics and moral standards are important subjective factors with a strong impact on tax compliance behavior. These findings imply that individual taxpayers with high personal ethics and moral standards will not choose to engage in tax evasion, even if they might gain an economic benefit from it. Our findings support the prior empirical research of Battiston and Gamba (2016), which likewise asserts that ethics and moral standards have a significant positive effect on tax compliance behavior. According to Nguyen et al. (2020), when one person holds an imbalanced set of values, decisions based on that set may produce deviant behavior such as daily offenses. Since there has been a decline in the moral values of society, the possibility of unethical acts, such as tax evasion, may increase (Nguyen et al., 2020). The promotion of ethical and moral values at the individual and societal levels through formal education and church and religion is recommended to increase the level of moral awareness regarding tax compliance behavior. Moreover, in this context, it is useful to implement an early education system in terms of fiscal citizenship and tax compliance behavior.

As a result of our findings, authorities should realize that the taxpayer knowledge is an important factor in creating and maintaining a culture of paying taxes. Education of young people as future tax payers must be prioritized. By educating and involving them in various aspects of fiscal activity, we can foster a taxpaying culture in which individuals understand the role of tax in society, their rights and obligations, and how they can contribute to state financial revenues. According to Cirman et al. (2021), the more taxpayers know about the tax system and the vital role tax plays in their daily lives, the more receptive they will be to support it. According to Krause (2000), the more people comprehend tax laws, the more they appreciate the importance of taxes, thereby increasing the state revenue generated by the tax sector. Authorities can organize meetings and talks in colleges and universities so as to ensure that future taxpayer generations have the proper mindset toward taxes.

In terms of tax legislation simplicity, our findings indicate that, from the taxpayer’s perspective, simplicity is the best way to ensure tax compliance behavior. Therefore, it is necessary to simplify the tax system in general and, more specifically, the laws, the forms, the filing, the appeals system, and payment procedures. The legislative framework must be designed in such a way that it can be applied and respected both in its letter and in its spirit. Simplification of laws and tax forms, the use of plain language, rule reductions, and eliminating bureaucratic procedures are just a few steps to ensure tax compliance behavior in the future. Simplifying the tax system will result in an increase in taxpayers’ positive attitudes toward their tax obligations on the one hand, and increased tax revenues on the other. Our findings support the prior empirical research of Richardson (2006) and Palil and Mustapha (2011), which concludes that tax legislation simplicity has a strong correlation with tax compliance. Additionally, earlier scholars (e Hassan et al., 2021; Saad, 2014), provide evidence that simplifying tax payments is one of the major factors that contribute to voluntary compliance, which implies that a complex tax system can be a deterrent to voluntary tax compliance.

At present, digitization is a useful method that can simultaneously address issues related to simplifying tax legislation, tax obligations, and taxation so that taxpayers can more easily grasp this information. Digital integration leads to the simplification and clarification of fiscal procedures, as well as the operative knowledge of fiscal obligations and easier payment procedures. An evolved system would allow for operative solutions to some inconsistencies, requests, or unforeseen situations. Accelerating the move to a digital revenue administration enables the design and development of an efficient system of direct and timely communication between taxpayers and tax authorities. Admittedly, designing new services for taxpayers will be a challenge for those lacking the necessary skills, technological resources, or infrastructure to participate in digital inclusion. In this case, tax authorities must provide both self-service and traditional services. Additionally, designing and developing new services requires professional retraining of tax authority employees and managing their resistance to change.

The empirical analysis does not provide evidence of the relationship between the efficiency and transparency of government spending and taxpayer compliance behavior. Therefore, perceptions of government spending will not increase the compliance behavior of Romanian individual taxpayers, which conflicts with the previous conclusions presented in the literature. According to Barone and Mocetti (2011), tax compliance improves when the government allocates resources efficiently. However, when the government indulges in wasteful habits, taxpayers can be disappointed and retaliate through tax evasion (Vincent, 2021). The inconclusive relationship between efficiency and transparency of government spending and taxpayer compliance behavior can be partially explained by the lack of trust in the government and tax authorities, which leads to an attitude of indifference to the use of public funds. According to Inasius (2019), taxpayers’ low trust in the government and tax authorities may explain their indifference toward government spending.

We also provide evidence that an individual’s reference group has an insignificant effect on tax compliance behavior, implying that the opinions and actions of others do not influence an individual’s decision to comply with tax laws. Therefore, the influence of reference groups does not appear to be significant in the decision-making process, especially when monetary and fiscal compliance considerations are involved. The result of our study is consistent with that of Inasius (2019), who concluded that family members or friends do not play a significant role in improving taxpayers’ compliance behavior.

To summarize, in Romania, tax compliance is the result of a complex interaction of economic, social, institutional, and psychological factors. The findings of this study provide implications on the determinants and the mechanisms underlying tax compliance or non-compliance behavior, which subsequently help to deduce a set of practical considerations and develop tailored fiscal methods, strategies, and policies, as well as legal measures, to ensure tax compliance. This study is useful for the Romanian tax authorities to analyze the determinants of tax compliance behavior and allows them to develop future tax policies and reforms that are tailored to and focused on individuals’ voluntary compliance behavior. As the Romanian tax authorities are still experiencing difficulty in achieving tax compliance, our findings indicate that the aforementioned variables have a significant influence on the individual taxpayers’ behavior, except for government spending and the influence of the reference group.

The findings obtained by our study must taking into account the following limitations. First, the sample only comprised individual taxpayers. Second, the respondents could have misinterpreted or answered the questions untruthfully. In addition, the sample size was limited to a single country’s institutional environment, which may limit the generalization of the results. In this regard, future authors can employ the study model and test it in other countries. Future studies may also consider international or multiple country contexts to provide more insights into the taxation systems across countries. Another limitation is the use of a quantitative approach. This quantitative study can be supplemented with qualitative or mixed studies that allow a deeper analysis into the topic and provide a more accurate validation of the findings. Future research might consider the use of the experimental method, where the compliance behavior of taxpayers is measured through a controlled experiment.

Footnotes

Appendix

Research Constructs.

| Variable name | Variable code | Variable description | Items code | Items | Variable type |

|---|---|---|---|---|---|

| Tax compliance behavior | TCB | Taxpayers’ commitment to tax obligation and their honest intention to report the correct income for each year and pay the correct amount of taxes on time. | TCB1. | I pay my taxes in full and on time because, for me, it is obvious that this is what I have to do. | Dependent |

| TCB2. | I report my income with honest intention and I pay my taxes on time. | ||||

| TCB3. | I pay my correct amount of tax liability. | ||||

| TCB4. | I report the correct income for each year and pay the correct amount of taxes on time. | ||||

| Fairness of tax system | FTS | Taxpayers’ perception of fairness and equity in fiscal revenue distribution and government acts. | FTS1. | I pay taxes because in relation with tax authorities I perceive fairness and equity in fiscal revenue distribution and government acts. | Independent |

| FTS2. | I pay taxes because the revenue agency adheres to fair procedures when interacting with taxpayers. | ||||

| FTS3. | I pay taxes because the revenue agency collects taxes fairly. | ||||

| Coercive measures | CM | Compelling taxpayers to do the right thing using the full power of the tax authority by creating a higher probability of detection and the related penalties. | CM1. | I pay taxes because the probability of auditing is high. | Independent |

| CM2. | I pay my taxes because the related penalties are high. | ||||

| CM3. | I pay my taxes because if the tax authorities detect me then paying the tax with a fine will be the consequence. | ||||

| CM4. | I pay my tax, otherwise I will be detected. | ||||

| Knowledge of tax legislation | KTL | Taxpayers’ knowledge about tax law, tax regulations, their rights and obligations, and the benefits of taxation. | KTL1. | I have knowledge of all aspects of tax legislation. | Independent |

| KTL2. | I have knowledge and I understand tax system. | ||||

| KTL3. | I have knowledge and I understand the benefits of my tax payments. | ||||

| KTL4. | I have knowledge and I understand my rights and obligations as taxpayer. | ||||

| Financial resource constraints | FR | Perception that taxpayer limited income create them a financial stress and motivate them to prioritize their financial burden over their tax liability. | FR1. | My financial burden must take priority over my tax obligations. | Independent |

| FR2. | The timely payment of taxes causes a financial burden for me. | ||||

| FR3. | The tax burden is high relative to my income. | ||||

| Trust in government and tax authorities | TTA | Perception of the appropriateness and legitimacy of government actions. | TTA1. | I see tax authorities as my partners in achieving common goals. | Independent |

| TTA2. | I have full confidence in working with the tax authorities. | ||||

| TTA3. | I believe that tax authorities are well prepared and apply the tax legislation accurately. | ||||

| TTA4. | My collaboration with the tax authorities is based on mutual respect and honesty. | ||||

| Trust on government spending | TGS | Perception that tax compliance decisions are the result of taxpayers’ awareness of why taxes are necessary and emphasizing their connection to public spending and the actions of tax authorities to promote the common welfare. | TGS1. | I believe that public money is distributed appropriately and transparently. | Independent |

| TGS2. | I believe that public spending promote the common welfare. | ||||

| TGS3. | I believe that money collect are spent on project that benefit me. | ||||

| Personal ethics and moral standards | PEMS | Honest indicators in tax payment, not violating ethics, carrying out the right actions, having a strong community feeling and viewing tax payment as a civic duty. | PEMS1. | I feel morally obligated to pay my taxes. | Independent |

| PEMS2. | I pay my taxes because I have a strong community feeling. | ||||

| PEMS3. | I pay my taxes because this is my civic duty. | ||||

| Referral group | RG | Perception of how others behaved based on observations of the individual’s peers and significant others. | RG1. | I pay my taxes because all my family member do so. | Independent |

| RG2. | I pay my taxes because everyone else also pays their tax debts. | ||||

| RG3. | I pay my taxes because all my friends pay. | ||||

| Tax legislation simplicity | TLS | Perception that the simplicity of the tax system, tax legislation, regulations and their application. | TLS1. | I pay taxes because tax regulations are simple and it’s easy for me to do it. | Independent |

| TLS2. | I pay taxes because tax system is simple. | ||||

| TLS3. | I pay taxes because tax legislation, regulations and their application are simple. |

Source. Authors work.

Acknowledgements

The authors want to thank the editor and the reviewers for the insightful comments to improve the manuscript.

Availability of Data and Material

Data is available upon reasonable request.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Code Availability

Not applicable.

Ethics Approval

Not applicable.

Consent to Participate

Not applicable.

Consent for Publication

Yes, consent is granted for publication.