Abstract

The shortage of literature regarding the tax administration burden, particularly in the hospitality and tourism sector in the context of least developed countries, still exists. This study, therefore, investigates the tax administration burden in the tourism sector in the Zanzibar Islands. It specifically examines the structure of tourism taxes and the fiscal regime, measures the uncertainty and complexity of tax laws, and assesses the role played by business associations in facilitating collective action to reform the business environment of the tourism sector in this Archipelago. The study involved a survey of stakeholders (N = 135), including tourism investors, business associations, and relevant government agencies. The findings showed that uncertainty concerning the value added tax laws centered on calculation of the input tax, the input tax refund from mainland Tanzania, and the registration procedure. The confusion was also pronounced regarding the specific laws affecting tour operators, restaurants, and the hotel levy. Similarly, there is still uncertainty concerning the infrastructure tax and the imposition of a tax of US$1 per day per guest staying in a hotel. Moreover, uncertainty and complexity regarding the income tax laws is centered on calculating the income tax liability of businesses, investments, and employment. However, the role of business associations in reforming the business environment for tourism has been encouraging, as a good number of public–private dialogues and initiatives have been geared at negotiating the various forms of taxes and levies imposed on tourism and hospitality services in the Archipelago. The study concludes with managerial, policy, and research recommendations.

Introduction

A considerable amount of literature exists on the impact of tourism taxation on business performance (e.g., Alexander, Bell, & Knowles, 2005; Bird, 1992; Braunerhjelm, Eklund, & Thulin, 2015), on the economy (Gooroochurn & Sinclair, 2005), and on the welfare of the general public (Fjeldstad & Semboja, 2001; McKerchar & Evans, 2009). However, the shortage of literature regarding the tax administration burden or the uncertainty and complexity of the tax laws, particularly in the tourism sector in least developed countries, is still pronounced. Tourism taxation has become an increasingly important area in public finance for tourism investors, host governments, and researchers today (Dubin, Graetz, & Wilde, 1987; Council, 1998). Its importance is manifest in public–private dialogues, and the lobbying and advocacy of both practitioners and academic literature (Anderson et al., 2017; Bettcher, Herzberg, & Nadgrodkiewicz, 2015; World Bank Group, 2014). The contribution of tourism is well recognized as a sector having a comparative advantage in spreading economic benefits and providing alternative economic opportunities, through investment, revenue for the government in the form of taxes and levies, employment generation, foreign exchange earnings, and sustainable development (Anderson & Juma, 2011; Council, 1998; World Trade Organisation, 1998; World Tourism Organization, 2010).

Specifically, tourism is a significant source of income for the Zanzibar economy, and the largest source of foreign exchange. Tourism contributes 27% of the isles’ government revenue and 80% of its foreign exchange earnings (Anderson, 2013; Steck, Wood, & Bishop, 2010). Tourism has many components, including travel experience, accommodation, food and beverages, shopping, entertainment, aesthetics, and special events. The providers include travel agents, tour operators, transporters/carriers, attraction developers, tourist information and guiding centers, accommodation, and catering services (Pasape, Anderson, & Lindi, 2013). The Council (1998) defined tourism taxes as taxes that are “. . . applicable specifically to tourists and the tourism sector or, alternatively, if not specific to the tourism sector, those which are applied differently in tourist destinations” (p. 16). Many governments tax tourism activities to generate revenue and to repair tourism-related damage (Bird, 1992). Meanwhile, tourism investors see tourism taxes as negatively affecting their businesses, as taxes increase prices. Consequently, these parties focus on the tourism taxation system, the amount of taxes, and their impact on business and government revenue.

Globally, tourism taxation has received a lot of attention. For example, Fish (1982), Gooroochurn and Sinclair (2003), and Hazari and Ng (1993) investigated the objectives of tourism taxation, while Gooroochurn and Sinclair (2005), Jensen and Wanhill (2002), Balke (2000), and Kweka (2004) studied the impact of tourism taxation on tourists, the economy, and the welfare of the general public. However, there has been no work on the burden of tourism tax administration or the uncertainty and complexity of the tax laws. This lack of focus limits academic discussion on how to tax the tourism sector efficiently and effectively, leading to a meaningful policy being formulated. Consequently, this study sought to make a contribution by researching the structure of tourism taxes and the fiscal regime, measuring the uncertainty and complexity of the tax laws, and assessing the role of business associations in facilitating collective action to reform the business environment of the tourism sector.

Moreover, the tourism and hospitality sector is dominated by the private sector, which eventually shares the benefits of the industry with the public sector in the form of taxes, contributions, fees, and levies (Anderson et al., 2017). This is the main idea behind this study, which is to find out stakeholders’ perspectives on the tax administration burden when running a tourism business, and to propose an appropriate framework that would improve the business climate, leading to private sector development and eventually to poverty reduction among local communities.

We expect the article to contribute to the literature on tourism taxation, public–private dialogues and partnerships. The article utilizes the measurement of the complexity of tax laws devised by Jones, Rice, Sherwood, and Whiting (2015) to estimate the complexity of tourism taxation, with a view to identifying areas where simplification is greatly needed, and to explore the uncertainty of the tax laws. Moreover, this study adds to the few articles examining tax administration costs in Tanzania (Mahangila, 2017; Shekidele, 1999) and public–private dialogues and partnerships (Anderson et al., 2017). This is because, many studies from developed countries (e.g., Alexander et al., 2005; Pope, 1995; Sandford & Hasseldine, 1992; Schoonjans, Van Cauwenberge, Reekmans, & Simoens, 2011) have mainly focused on estimating tax compliance costs. We expect the findings also to provide lessons on how to promote the right conditions for private sector development, to inform good practice, and policy formation and to improve the business environment in Zanzibar.

To this end, the “Literature Review” section offers a review of the literature. The “Research Method” section presents the study’s research methodology. The “Findings” section presents the data analysis and findings. The “Conclusion” section discusses the findings and draws conclusions from the study.

Literature Review

Conceptualizing Tax Compliance in the Tourism Sector

Tax compliance is important for the provision of public services because without adequate tax revenue the quality of public services may deteriorate. Tax compliance means taxpayers fulfilling their obligations (Kirchler, 2007). However, gathering enough tax revenue is a problem faced by many countries because of tax evasion and avoidance. Tax evasion is a deliberate illegal act intended to reduce someone’s tax liability, while actions taken to legally reduce one’s tax liability is tax avoidance (Alm, 1999; Slemrod, 2007). Tax compliance may be more important today than in previous years because many countries are tackling budget deficits. Moreover, tax compliance is important for achieving fairness and enhancing resource allocation (Alm, 1999).

Previous studies have shown that tax compliance is a function of both economic and noneconomic factors. Economic factors include tax rates, income level, penalties, and tax audit rate (Allingham & Sandmo, 1972). It has been observed that high tax rates, lower penalty rates, and a lower perceived audit rate decrease the tax compliance level (Dubin et al., 1987; Dubin, Graetz, & Wilde, 1990). On the contrary, the tax compliance level increases with a reduction in tax rates, higher penalty rates, and higher perceived audit rates (Andreoni, Erard, & Feinstein, 1998). Noneconomic factors include the age of taxpayers, the educational level of taxpayers, confidence in the tax laws, social norms, and perceptions of the justice of the tax system. It has been found that older taxpayers, educated taxpayers, and taxpayers with greater confidence in the tax laws are more likely to pay their taxes than young taxpayers, poorly educated taxpayers, and taxpayers with less confidence in the tax laws (Cadsby, Maynes, & Trivedi, 2006; Fjeldstad & Semboja, 2001; Saad, 2010). Also, taxpayers residing in a tax-compliant society are reported to be more compliant than those coming from a noncompliant one (O. H. Chang, Nichols, & Schultz, 1987). More importantly, the tax compliance level is reported to be positively related to procedural justice (Mahangila & Holland, 2015). It has also been reported that compliance costs and compliance levels are negatively related (Mahangila, 2017). Tax compliance costs are those relating to taxpayers fulfilling their responsibilities (Evans, 2003). These tax compliance costs comprise the time spent complying with tax laws, printing costs, the cost of administering tax laws, and corruption that mainly takes place in administrative procedures.

Tourism taxation embodies those taxes imposed on tourists and/or the tourist industry (Council, 1998). There are many reasons why governments focus on taxing the tourism sector, but, for the purpose of this research, we focused on the major ones. First, in tourism-based countries or regions, the sector is the major economic activity, leaving the country or region with fewer options when determining what activities to tax (Dombrovski & Hodžić, 2010; Gooroochurn & Sinclair, 2003), and so most of the tax revenue may come from that sector.

Second, due to the specific nature of tourism, economists believe that taxing tourism activities will only have a small impact on taxpayers’ behavior (i.e., consuming less, or more, of the activity) if most of the taxes are borne by foreign tourists (Gooroochurn & Sinclair, 2003). Consequently, governments favor imposing more taxes and levies on activities mostly undertaken by foreign tourists (Sheldon & Var, 1985), as a heavy local taxation burden may cause public discontent and negatively affect the political environment (Anderson, 2009). In some cases, an increase in the tax rate may cause some minor economic distortions, when, for example, a tourist destination is unique in its nature, as this leaves tourists without alternative choices, and lowers the elasticity of substitution. The elasticity of substitution is a measure of the ease with which varying factors can be substituted for others (Hicks, 1932). In this case, it refers to how easily tourists can substitute one tourist destination (let us say Zanzibar) for competing destinations (e.g., Mombasa, Mauritius, etc.).

Third, for destination managers, imposing taxes on tourism activities serves as a means to recover the costs of the public services and goods consumed by tourists (Varela, 2011). For example, tourists consume infrastructure, such as roads, health services, and security while in a destination country. Thus, taxes simply recover the costs of servicing tourists. Environmental conservationists use taxation as one of the measures to regulate a destination’s carrying capacity. A growth in the number of tourists, and the associated facilities, is associated with increased pollution, congestion, depletion of natural resources, and a reduction in aesthetic value (Böhringer, Ferris, & Rutherford, 1998; Green, Hunter, & Moore, 1990). Consequently, funds are collected from tourism activities to restore the damage caused by the industry.

Fourth, tourism taxation can be used to encourage the smooth flow of tourists through the variability of tax rates (Varela, 2011). For example, in high season, an increase in tax rates for tourism may discourage some tourists from visiting a given destination in that period, whereas a decrease in tax rates in low season may attract some tourists to visit such a destination at that time, as the tourism package is cheaper.

Tax Compliance and Complexity of Tax Laws

Complex tax laws are those with which it is difficult and expensive to comply (Mulder, Verboon, & De Cremer, 2009). However, tax compliance occurs when a taxpayer

registers with the revenue authority as required; files the required returns on time; accurately reports tax liability (in the required returns) in accordance with the prevailing legislation, rulings, return instructions and court decisions; pays any outstanding taxes as they fall due; and maintains all records as required. (McKerchar & Evans, 2009, pp. 172-173)

Generally, the literature on how the complexity of tax laws affects tax compliance behavior remains controversial. Scotchmer (1989) claimed that tax revenue authorities prefer complex tax laws to simple ones, because uncertainty is more likely to induce tax compliance. Scotchmer (1989) argued that, even when taxpayers seek professional help to resolve complex tax problems, not all uncertainties are resolved. As taxpayers are penalized for noncompliance, they, together with their tax return advisors, might react to the remaining uncertainties by paying more in tax (Scotchmer, 1989). Similarly, White, Curatola, and Samson (1990) suggested that complex tax laws may help tax authorities to win tax disputes and increase tax revenue. On the contrary, the conclusion that taxpayers might increase their compliance level, because the uncertainties and complexities of the tax laws boost the likelihood of tax authorities winning cases, has no empirical evidence to back it up.

Nevertheless, when tax fairness causes complexity in tax laws, the complexity might increase tax compliance, because tax fairness is an important factor in tax compliance decision making (Milliron, 1985). Indeed, Milliron (1985) found an increase in the inclination to pay taxes when distributive fairness increased tax complexity. Distributive justice refers to the fair allocation of the tax burden, and to governments providing goods and services for taxpayers (Wenzel, 2002).

Cuccia and Carnes (2001) supported the view that tax fairness can increase tax compliance levels, even when the tax laws are complex. Cuccia and Carnes (2001) conducted a hypothetical experiment to determine how participants’ perceptions of procedural justice change when the complexity of tax laws was justified or not. They found that, when complex tax laws were justified, and when participants were provided with tax relief, their perceptions of procedural justice were more favorable than when the complexity of the tax laws lacked justification and they had less tax relief (Cuccia & Carnes, 2001). Concern about the fairness of the distribution of the tax burden and providing the public with goods and services is known as procedural justice (Leventhal, 1980; Thibaut & Walker, 1978). However, as that study was confined to the effect of the complexity of tax laws on taxpayers’ perceptions of procedural justice, tax compliance decisions were excluded from it. Also, J. B. Chang, Lusk, and Norwood (2009) showed that hypothetical intentions may differ from actual behavior.

Nevertheless, opposing evidence has suggested that complex tax laws produce negative attitudes toward tax compliance (Kirchler, Niemirowski, & Wearing, 2006; Milliron, 1985). For instance, participants’ attitudes toward tax compliance were most unfavorable when the complexity of tax laws offered more tax noncompliance opportunities and when taxes were perceived to be unfair (Milliron, 1985). Likewise, a hypothetical experiment revealed that tax avoidance decreases with precise tax laws (Richardson, 2006; Spilker, Worsham, & Prawitt, 1999).

Furthermore, the difficulty inherent in separating errors from deliberate tax evasion (Slemrod, 2007) could lead to the punishment of innocent taxpayers, resulting in less confidence in the tax laws, which lowers taxpayers’ disposition to pay taxes (Frey & Torgler, 2007). In this regard, Mills (1996) suggested that complex tax laws increase tax compliance costs, create room for evasion and, when tax compliance costs are far greater than the tax evasion opportunities, tax compliance may suffer.

Tax Compliance Costs and Tax Administration Burden

Tax compliance costs are probably the major by-product of the complexity of tax laws. Tax compliance costs have been found to be significant and regressive (Alexander et al., 2005; Pope, 1995; Sandford & Hasseldine, 1992; Schoonjans et al., 2011). Alexander et al. (2005) kept a record of the time and money spent complying with tax laws by small firms in New Zealand for 2 months and found a similar pattern.

Nevertheless, there has been concern that taxes in Zanzibar in general, and the tourism sector in particular, may not conform to the efficiency criterion of a good tax system (Zanzibar National Chamber of Commerce, Industry, and Agriculture [ZNCCIA], 2013). Although there is a general consensus that taxation is a necessary part of building a healthy economy, taxes must be reasonable, transparent, and fair. In Zanzibar, this has not been the case because there is a general feeling in the tourist industry that taxation has become a burden for taxpayers (The Citizen, 2015). This has been reflected in an economic downturn, resulting in investors migrating from Zanzibar, taking with them their potential for investment, transferable skills, and the potential for creating employment. The World Bank (2010) positioned Zanzibar at 155 out of 183 in the world ranking of the business environment. Zanzibar’s tax regime is perceived to be complex and uncertain because of the tax administration burden.

As a result of this tax administration burden, there is a high level of discontent regarding Zanzibar’s business environment. For instance, it has been discovered that medium-sized businesses in Zanzibar make 48 tax payments, their profits are taxed at 40%, and they spend nearly 160 hr annually complying with tax laws (World Bank, 2010). According to the World Bank (2010), small island countries made an average of 28 tax payments, while Sub-Saharan Africa made an average of 38 tax payments. In contrast, businesses in similar tourism islands, such as the Maldives, made a single tax payment, their commercial profits were taxed at 9.1%, and they spent less than 1 hr per year on tax compliance. Thus, the Zanzibar tax regime lags far behind similar economies.

According to the ZNCCIA (2013), the complexity of Zanzibar’s tax regime reduces the competitiveness of the business environment, including its vibrant tourist industry. Tourism is a significant source of income for Zanzibar and currently generates 15,000 direct and 50,000 indirect jobs relating to the industry (Anderson, 2015; The Citizen (2015). If the unfavorable climate persists, Zanzibar faces the possibility of losing the benefits of the tourist industry. The industry is well-known for its ability to create jobs for Zanzibaris and Tanzanians in general, to develop the human resource base, to provide capital across the industry, to protect and conserve natural attractions, to preserve and celebrate Zanzibar’s unique culture, to contribute substantially to the tax base, and to contribute to poverty alleviation, by working with local communities. The fact that foreign investors are migrating from Zanzibar due to, among other factors, the quantity, cumbersomeness, and complexity of the taxation system and its administrative procedures, means that the economy of Zanzibar will continue to decline if the necessary interventions continue to be ignored. Thus, this study was aimed at investigating the tax administration burden on the tourism sector in the Zanzibar Islands.

Research Methodology

This study used a qualitative-descriptive approach (Lambert & Lambert, 2012) by collecting primary and secondary data through in-depth interviews and reviewing the literature and documents. This in-depth interview approach is important for gaining an understanding of the research problem (Hammersley & Atkinson, 2007). Secondary sources of data were chosen to reveal the complexity and uncertainty of tax laws, which previous research has not done. Specifically, the secondary sources of data were the East Africa Customs and Management Act of 2004; The Income Tax Act of 2004; The Value Added Tax (VAT) Act Number 4 of 1998, local excise duty, the petroleum levy, under the Petroleum Levy Act Number 7 of 2001, Stamp Duty, supervised under Act Number 6 of 1996, Infrastructure Tax Act, under Act Number 9 of 2015, and the Hotel, Restaurant and Tour Operation Levy, which all fall under the Hotel Levy Act of 1995. In addition, the Public Finance Acts from 2010 to 2015 were included in this study.

The interviews took place between July and November 2015. The population consisted of tourism stakeholders, namely, tax authorities, hoteliers, airline staff, tour operators, restaurateurs, the Zanzibar International Film Festival (ZIFF), and Sauti ya Busara, together with other service providers supporting tourism investors, such as auditors and tax consultants in Zanzibar. Each business was either directly related to the tourism sector or helping it to comply with taxation laws in Zanzibar.

Sixty-nine of the interviewees were tourism investors: hoteliers (52%), tour operators (29%), sky-diving business operators (2%), restaurateurs (13%), and festival organizers, that is, ZIFF and Sauti ya Busara (4%). Also, 30 tax consultants were interviewed about uncertainty, tax administration procedures, and the complexity of the tax laws, because many tourism investors depend on their tax consultants to enable them to comply with the tax laws. In addition, 36 respondents came from the Zanzibar Investment Promotion Agency (17%), the Zanzibar Commission for Tourism (8%), the Tanzania Revenue Authority–Zanzibar (11%), the Ministry of Tourism (8%), the Copyright Society of Zanzibar (6%), the Ministry of Finance and Planning (14%), the Zanzibar Revenue Board (ZRB; 17%), the Zanzibar Airport Authority (3%), the Ministry of Land–Zanzibar (3%), the Zanzibar Office of Statistics (8%), and the Ministry of Local Government (3%).

Because the qualitative approach was taken by this research, an open-ended questionnaire was used to solicit detailed responses from the respondents. The guiding questions ranged from “What areas or sections of the Income Tax Act 2004 do you consider to be uncertain?” and “Why do you consider them to be uncertain?” to “What should be done to improve certainty in these areas?” Similar questions were asked about other tax laws. A question on the role of business associations in reforming the business environment of the tourism sector in Zanzibar was asked of business associations in the tourism and associated sectors. The data provided were important for identifying the fees and taxes payable by the tourism sector in Zanzibar. It should be noted that the results were limited to a discussion of the responses from those involved in the tourist industry and their consultants, and that responses from government officials were used for triangulation purposes and to validate the findings. Finally, descriptive and reflective approaches were adopted to analyze and report on the qualitative data (Eisenhardt, 1989). The findings are presented below.

Findings

Structure of Tourism Taxes and Fiscal Regime in Zanzibar

There are three tax authorities in Zanzibar, namely, the Tanzania Revenue Authority (TRA; Zanzibar), the ZRB, and the local government authorities. The TRA administers income tax under the Income Tax Act of 2004, which includes both corporate and personal incomes, and customs and excise duty, under the East Africa Customs and Management Act of 2004. On the contrary, the ZRB manages VAT, under the VAT Act Number 4 of 1998, local excise duty, the petroleum levy, under the Petroleum Levy Act Number 7 of 2001, stamp duty, which is paid by all traders, at 3% of their sales, and supervised under Act Number 6 of 1996, the infrastructure tax, under Act Number 9 of 2015, and the hotel, restaurant, and tour operator levy, which all fall under the Hotel Levy Act of 1995 (see Figure 1).

Classification of Zanzibar’s tax structure.

In total, the Zanzibar taxation system charges 10 different taxes, three of which are specifically for the tourist industry. The general taxes are income tax, petroleum levy, customs and excise tax, infrastructure tax, VAT, stamp duty, excise duty (local), and property tax. In addition to the seven general taxes, the tourist industry has to pay a hotel levy, a restaurant levy, and a tour operator levy in accordance with the ZRB (see Figure 1).

Measuring the Uncertainty and Complexity of the Tax Laws

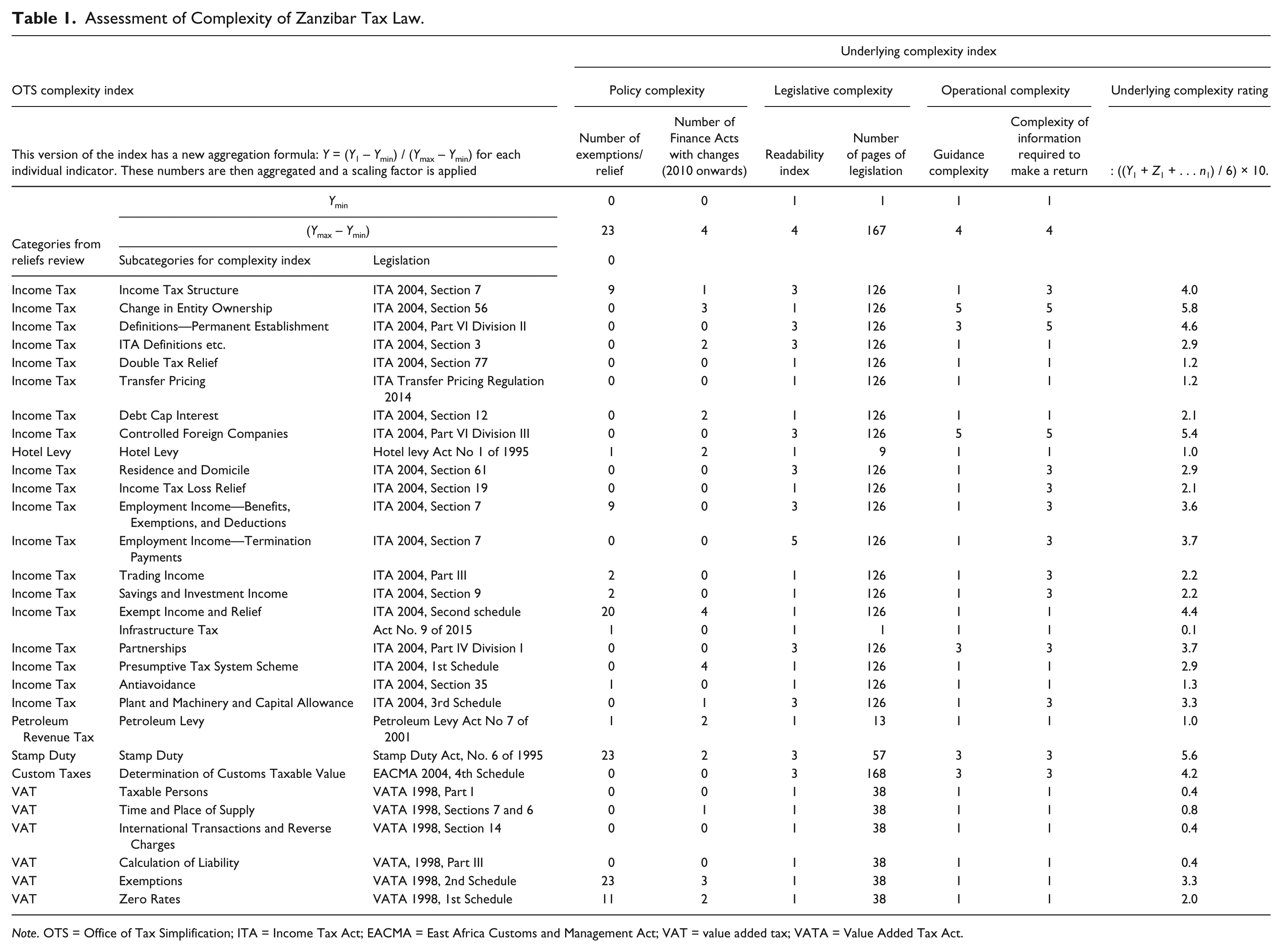

Measuring tax complexity has been a difficult area for tax researchers. A complexity index developed by Jones et al. (2015) was used to assess the complexity of Zanzibar’s tax laws. The index is an investigative instrument used to identify necessary and unnecessary complexities. According to Jones et al. (2015), necessary complexities are those needed to achieve the objectives of the tax policy, and they can only be changed if the objectives are changed, while an unnecessary complexity is that which can be changed without changing the tax policy objectives. This index divides tax laws into several important tax areas, and considers small tax laws as single, distinct tax areas. Ironically, stamp duty, the infrastructure tax, petroleum levy, customs, and hotel levy tax laws were taken as a single tax area. However, the income tax law was divided into 20 separate tax sections, and the VAT law was divided into six separate tax areas. These areas are indicated in the rows in Table 1.

Assessment of Complexity of Zanzibar Tax Law.

Note. OTS = Office of Tax Simplification; ITA = Income Tax Act; EACMA = East Africa Customs and Management Act; VAT = value added tax; VATA = Value Added Tax Act.

The index comprises measures of “underlying complexity” and the “impact of complexity.” The authors defined underlying complexity as “a measure of the complexity of the ‘maze’ through which a taxpayer would be required to go to comply with their tax responsibilities and to understand their tax obligations (and the result of those obligations) with no prior knowledge” (Jones et al., 2015, p. 5). The impact of complexity measures the impact of underlying complexity in terms of how many taxpayers are affected by a particular indicator, the total tax compliance and administration costs, the ability of taxpayers affected by an indicator, and the potential loss of revenue due to a specific cause (Jones et al., 2015). However, there was no information to enable measurement of the impact of complexity and, therefore, only the underlying complexity was measured in this study.

The underlying complexity measure comprises policy complexity, legislative complexity, and operational complexity. Policy complexity measures the complexity resulting from the governmental policy objectives of giving tax exemptions and tax relief and changing tax laws. Consequently, the policy complexity of a tax law is identified by two indicators: the number of exemptions plus the number of those receiving tax relief in that law and the number of finance acts with tax law changes. It is generally accepted that a tax law that increases the number of exemptions or those given tax relief increases its complexity, in terms of deciding whether or not a taxpayer/income/transaction is exempt from tax (Barazzoni, Cerri, & Hepburn, 2006). Also, frequent changes in tax laws, through the passing of Finance Acts or otherwise, increases the complexity of tax laws, as taxpayers or tax consultants have to spend more time familiarizing themselves with the changes (Barazzoni et al., 2006).

Legislative complexity measures how difficult it is to understand a tax law. This indicator is measured using a readability index, scoring 1 when it is simple to read, 3 when it is of medium difficulty, and 5 when it is difficult. This score is subject to participants’ perception of the scores and, therefore, two tax consultants were involved in scoring this index. Legislative complexity is also measured by the number of pages in the legislation because it is assumed that people associate longer texts with complexity (Jones et al., 2015).

Finally, operational complexity indicates how complex it is to use the guidance provided by the tax authorities to facilitate compliance with the tax laws. The tax guidance documents include, but are not limited to, practice notices, brochures containing tax information, and regulations about how to apply tax laws. Complexity of the guidance given by the TRA and ZRB was assigned 1, 3, or 5 if it was straightforward, of medium complexity, and complex, respectively. The scoring was based on the length of the guidance, the ease of navigation, other guidance information, and the frequency of change. Furthermore, operational complexity relates to the complexity of the information required to make a tax return, which measures the degree of difficulty of gathering information to meet tax compliance obligations. In this case, the complexity of information was assigned 1, 3, or 5 if it was straightforward (using available information), of medium complexity (simple computation), and complex (requiring difficult computation), respectively. Again, these scorings are subjective, and so the scoring was done by the two tax consultants mentioned previously.

After the scoring was completed, the scores of each indicator was normalized to get a scale of values of between 0 and 1 using the standardization formula: Y1 = (Y – Ymin) / (Ymax – Ymin) (Jones et al., 2015), where “Y” is the value of the indicator of a tax measure, “Ymin” represents an indicator’s lowest value across all tax measures, and Ymax indicates the highest. An aggregation formula ((Y1 + Z1 + . . . n1) / 6) × 10 was then used to transform the index to give scores of between 1 and 10, where n1 represents a normalized indicator and 6 represents the indicators of underlying complexity, which are indicated in the third row from number of exemptions/relief to complexity of information required to make a return. The multiplying factor 10 was included to produce a final index of a definite number between two defined points, 1 and 10, whereby 1 meant the least complex and 10 the most complex (see the study by Jones et al., 2015, for further information). In this case, all six indicators had equal weightings to increase clarity, remove the need to change weightings when the tax system changes, enable comparability of the complexity of the system over time as the scores are not weighed (Jones et al., 2015), and reduce subjectivity in measuring complexity.

Complexity of Tax Laws in Zanzibar

There is a general feeling among private sector stakeholders that the main challenges facing the tourism sector include having too many unpredictable taxes. Tourism providers (such as tour operators and accommodation providers) complain about spending much more time complying with the regulatory changes than concentrating on the business itself. According to a report by the ZNCCIA (2013), complexities of the Zanzibar tax regime reduce the competitiveness of the business environment, including its vibrant tourist industry, and in fact they are of the opinion that there is unfair treatment and many complexities when it comes to tax administration in the sector (see Figure 2). More specifically, the Zanzibar Income Tax Act, 2004, shows the underlying complexity of tourism taxes in general. For instance, Section 7 of the Income Tax Act (2004) has nine types of tax relief or exemptions, whereas other sections in the Income Tax Act 2004 have between zero and two exemptions. Section 7 has listed employment income and exempt employment income, repeating most of the employment income, but granting exemptions when certain conditions are met. This repetition of the same items makes it difficult to calculate employment income. However, the second schedule of the Act contains a list of 20 exempted incomes or taxpayers. This schedule was created to streamline the exemptions to income tax into a single list.

Simplifying the process of paying taxes will improve the ease of doing business, encourage compliance, stimulate economic growth, and boost employment.

Section 56 of the Income Tax Act (2004) was amended 3 times between 2010 and 2015 by the passing of Finance Acts. This section deals with changes in the ownership of an entity and attempts to prevent tax avoidance practices by imposing taxes on capital gains when ownership of the entity changes by more than 50%. Thus, these changes in the sections may reflect the TRA’s efforts to protect tax revenue.

In terms of the readability index, the definition of permanent establishment covered in Part VI Division II, Section 3 of the Act defines key terms and individual income tax structures, and Section 66, dealing with residential status, both scored 3 points, meaning they had medium readability complexity. These sections and the first schedule treated the various tax issues they presented differently, and section 7 in particular lacked clarification and used long sentences to explain the taxation of employment income, which confused readers. These findings implied that the legislative complexity of these factors was medium. Also, the number of pages of the Income Tax Act (2004) remained constant, at 126 pages, during this period.

Section 56 and the taxation of foreign-controlled entities were perceived to have greater guidance complexity and required complex information to file returns. These perceptions may be attributed to the lack of clear guidance by the TRA and because the information that is supposed to be filed, or recomputed, is different from the common information that taxpayers are given. The remaining sections of the Income Tax Act were perceived to be either simple or of medium operational complexity.

The complexity of the The East Africa Customs and Management Act, 2004

This was generally perceived to be simple, although it was the longest Act, with 168 pages. The readability index was of medium complexity as there was little taxpayer guidance information and so the operational complexity was medium.

The complexity of the VAT Act, 1998

Most of the changes in the VAT Act were made in the first schedule (11) and the second schedule (23), while only one change in each was made in Sections 6 and 7. These findings imply that the policy was not complex, due to few changes in the Act and because many of the exemptions/relief were listed in the first and second schedules of the Act. In terms of the readability index, the Act was rated as simple due to its short and straightforward explanations, while the number of pages remained constant at 38 for the study period. This signifies that the Act was not complex. The operational complexity of the VAT Act of 1998 was generally at a low level because most of the sections were simple and had straightforward explanations, while the numbers of its pages remained the same during the reporting period. Regarding operational complexity, all sections were rated simple due to their clear and straightforward explanations. Thus, the VAT Act was found to be simple and clear.

The complexity of the Hotel Levy Act, 1995

The Act had only one exemption/relief, and only two Finance Acts changed this Act between 2010 and 2015. Its readability was rated simple and the Act had only nine pages, which remained constant during the reporting period. These findings imply that the policy was not complex nor was the legislative index of the hotel levy, which had clear and straightforward explanations. Similarly, the guidance provided and the information needed for filing a return were both perceived to be simple and straightforward.

The complexity of the Infrastructure Tax law

This was a new law, which had only one page and no changes. It was clear and straightforward in terms of readability, guidance, and the information required to fill in returns.

The complexity of the Stamp Duty Act, 1995

The Act had 23 exemptions/relief and had changed twice between 2010 and 2015. These findings imply that policy complexity was medium, as well as the legislative index, as indicated by a readability index score of 3 and the number of pages of the Act at 57. The readability index was rated medium because some sections used difficult vocabulary or terms.

Finally, it was perceived that both the guidance provided and the information needed to make a return were of medium complexity as the guidance was not straightforward and additional information, other than that commonly available, was required when filing returns.

Uncertainty of the Tax Laws in Zanzibar

The Income Tax Act 2004

The areas perceived to be uncertain were the calculation of income tax liability from business, investment, and employment incomes. Calculation of the depreciation allowance, unallocated income, and the residential status of taxpayers were also mentioned as areas of uncertainty, probably because the legislation had been badly drafted. Moreover, it was difficult to differentiate sources of business income from investment income. For example, tourism investor respondents commented that

It is unclear if rental income from the lease of a hotel should be categorized as business or investment income. The way a foreign-controlled corporation is treated in terms of distributing its unallocated income to its members is ambiguous. Sources of employment income are listed followed by another list of exempt employment income repeating almost the same sources of employment income.

Accordingly, uncertainty of the income tax laws was mainly caused by limited practice and training, incomplete definitions of the key terms, and inadequate drafting of the tax law. These findings are in line with the findings of the complexity index previously presented.

The East African Customs and Management Act 2004

Many respondents were unaware of the customs tax laws. However, a few were of the opinion that customs tax liability on imported goods was uncertain as this was usually determined by tax officials. One tourism investor respondent stated,

Customs tax liability is usually charged according to a tax official’s decision and not based on the actual goods imported into the country.

The introduction of customs tax calculators, where taxpayers can enter details of imported goods and know their tax liability, could resolve this uncertainty. However, it is possible that tax officials might be exploiting taxpayers’ ignorance to collect more taxes.

The VAT Act 1999

The ZRB failed to properly communicate a change in the treatment of the input tax paid in mainland Tanzania, where taxpayers continued to deduct it. However, the new treatment does not allow the input taxes paid on the mainland to be deducted by taxpayers in Zanzibar, as noted by two of the tourism investors:

ZRB tends to refuse the input tax from Mainland Tanzania and there is no clear regulation on it. Where a taxable person pays tax to a taxable person in mainland Tanzania for any taxable supply, the taxable person in Zanzibar is unable to claim the input tax. It is a problem.

Clearly, this finding implies that taxpayers were unaware of this change. When following this up with ZRB, it was discovered that input tax paid in mainland Tanzania was no longer deductible in Zanzibar, following the abolition of the reciprocal arrangement with mainland Tanzania. This arrangement allowed the TRA in mainland Tanzania to collect output taxes from persons on the mainland who purchased goods and services for the purpose of importing them into Zanzibar. Then, after collection, the TRA in mainland Tanzania paid the amount to the Zanzibar Revolutionary Government.

It seems that the limited time between the introduction of tax law changes and implementation of the changes may have caused this inconsistency between taxpayers and the tax authorities.

Likewise, VAT registration criteria and procedures were uncertain as they were used to calculate penalties for various breaches of the Act, as well as interest. Moreover, undue delays in refunding VAT was cited as one of the uncertainties of this Act. These delays may cause businesses financial stress as their working capital is stranded at the ZRB. One respondent from the tourism investors stated,

There are no known registration procedures as it all depends on the decision of the commissioner.

The Hotel Levy Act 1995

This Act covers three taxes: Hotel Levy, Tour Operator Levy, and Restaurant Levy. This consolidation of three taxes was perceived to be a source of uncertainty when determining what, and how much, tax to pay. As one tourism investor stated,

There is no specific law for the tour operator levy or restaurant levy which has been included in the Hotel Levy Act.

It is arguable that it would be better to have three separate laws for these three taxes. However, consolidation of the tax laws was advised so as to reduce the administrative burden (Barazzoni et al., 2006). Therefore, the Hotel Levy Act should comprise separate sections for hoteliers, restaurateurs, and tour operators to remove this confusion.

Also, some tour operator respondents complained about being forced to pay the US$5,000 tour operator levy during the low season, when income from tourism is low. This not only denied investors badly needed working capital, but also increased compliance costs.

The Infrastructure Tax Law 2015

This Law lacked definition of key terms, although it was the simplest law, but the lack of definitions limited its implementation. For instance, the law imposed an infrastructure tax of US$1 per day per guest staying in a hotel. A hotel investor respondent said,

The law does not define all legal terms, including “guest” in this law, the guest can be either an adult or a child, but the law is silent on this.

There were also concerns about why the tax was being paid in U.S. dollars when the taxpayers did not receive an income in dollars (a reply from a hotel investor respondent), particularly when guests were residents of Zanzibar or mainland Tanzania.

Tax Administration Burden

The Zanzibar tax system operates through self-assessment, whereby taxpayers determine their tax liability and pay their taxes to the tax authorities: the TRA-Zanzibar, the ZRB, the local government authorities, and other regulatory authorities. However, the tax system still requires taxpayers to visit several offices and file several documents to fulfill their obligations (see Figure 3). In addition, taxpayers make more than 48 compulsory payments included in these estimations per year, as shown in Table 2.

Zanzibar tax administration burdens.

Frequency of Filing and Paying Taxes.

Note. VAT = value added tax; PAYE = pay as you earn.

In this study, we asked tourism investors to estimate the time spent complying with the tax regime. This time was then used to estimate compliance costs, based on the unit costs found in Doing Business in Zanzibar (World Bank, 2010) and Zaki and Alex (2010) in the Tanzanian tourism sector. These were the costs of printing/photocopying, transport, time spent processing information, those associated with disputes, such as reprinting costs, labor time, and consultancy costs. The average cost of complying with the selected taxes in Zanzibar is more than TZS 1,428,000 (US$640.36) per annum. However, Zanzibar has an estimated 5,000 registered taxpayers and, when this cost is extrapolated, the impact of tax administration costs was TZS 7,140,000,000 (see the appendix). This finding is similar to the findings of P. E. Lignier, Evans, and Tran-Nam (2014), who discovered that tax compliance costs were growing, despite the government’s efforts to reduce them.

The Role of Business Associations in Reforming the Business Environment of the Tourism Sector in Zanzibar

There are several associations that support the development of the tourism sector in the Archipelago. The main ones are the ZATI (ZATI), the Zanzibar Association of Tour Guides (ZATOGA), the Zanzibar Employees’ Association (ZANEMA), the Tanzania Private Sector Foundation (TPSF), the ZNCCIA, the Ecotourism Association, and the Hotel Restaurants’ and Alliance Union. However, ZATI is the largest association, which was established in 2003 to represent the interests of all tourism investors in Zanzibar and acts as the voice of the tourism private sector. With around 106 members from various industries in the tourism sector, such as hotels (60), tour operators (10), suppliers (eight), water space (eight), restaurants (five), shops (three), a consultant (one) and health official (one; also see Pasape et al., 2013), ZATI unites and represents all members in the tourism sector of Zanzibar and defends the rights and interests of stakeholders in it.

Moreover, the Association acts as a link between members of the tourism sector and the government on matters of socioeconomic policies; advises and cooperates closely with the government in formulating policies and programs relating to the tourist industry and its promotion internally and externally; supports, stimulates and catalyzes socioeconomic development; and conducts research on socioeconomic development and the tourist industry and shares its findings with stakeholders. By so doing, ZATI has been successful recently in pushing for changes to the VAT Amendment and reviewing the tax regime, with the aim of improving the ease of doing business in Zanzibar. The Association has also been successful in initiating and implementing a public–private partnership (PPP) to create a better tourism environment for both investors and tourists. Moreover, ZATI represents the private sector in meetings with government authorities in Zanzibar to discuss business challenges. ZATI frequently commissions studies (including the most recent ones by Mahangila & Anderson, 2016) to compile evidence to feed into dialogue with the government. The most recent studies, for example, have enabled ZATI to convince the government to speed up the creation of an electronic tax system to allow businesses to pay taxes not only in U.S. dollars, but also in the local currency (i.e., Tanzanian Shillings), to extend the VAT filing date from 7 to 10 days, to consolidate existing taxes and to stop introducing new taxes (also see Masare, 2016). Generally, the role of business associations in reforming the business environment of the tourism sector in Zanzibar has been felt by it.

Conclusion

Complexity and uncertainty in the tax system lead to a greater administrative burden and thus to higher compliance costs, based on earlier arguments, than to lower compliance costs. However, this study has revealed tremendous uncertainty regarding the income tax laws in Zanzibar centered on the calculation of input taxes, input tax refunds from mainland Tanzania, and the registration procedure. There is no specific law for the tour operator levy, restaurant levy, and hotel levy, which caused uncertainty regarding the Hotel Levy Act. Similarly, uncertainty regarding the infrastructure tax was due to the absence of a clear interpretation of certain terms used in the law and to the imposition of the tax of US$1 per day per guest staying in a hotel. Furthermore, there was uncertainty about the change in the treatment of input tax paid in mainland Tanzania, the calculation of penalties and offenses, and the registration procedure. The results show that many respondents identified that uncertainty concerning the income tax laws centered on the calculation of the income tax liability for businesses, investors, and employers. Although some laws were found to be simple, most were found to be of medium complexity. This calls for minor modifications in the tax system, to make it simpler for both users and the TRA. Specifically, Section 56, the second schedule, Section 7 of the Income Tax Act 2004, and the Stamp Duty Act were the most complex areas, whereas the Infrastructure Tax Act was found to be the simplest tax law.

Moreover, the Zanzibar tax regime was found to be complex and uncertain and it imposed a heavy burden on the tourism sector, both in terms of the amount of tax paid and the administrative burden. The Ministry for Finance should issue more detailed regulations concerning the tax laws and should implement rules whereby these regulations should clarify any uncertainty and areas identified as being complex should be given practical examples. Furthermore, it would be helpful to collate and circulate data from time to time and to publicize the results of proceedings and the differences of opinion between the TRA, the ZRB, or local government authorities (LGAs) and the taxpayer.

Furthermore, the creation of binding rules, a “prior taxation agreement” (with characteristics similar to the “rulings” existing in other countries and in mainland Tanzania under Section 11 of the Tax Administration Act, 2015), would ensure that taxpayers would be certain, in terms of Zanzibar’s domestic taxes, about the taxation for a specific transaction or activity before engaging in it. Certainty could also be provided for taxpayers in relation to legislative changes, by ensuring that these are adopted by them before they come into force. This would enable taxpayers to establish adequate systems and to incorporate the legislative framework in their business planning. Consequently, the Ministry of Finance, working with the TRA, the ZRB, and local government authorities, should consolidate taxes to target the same tax base and the same taxpayer. Without reducing government revenue, excise duty would become TZS 2000, which would reduce tax administration costs and the amount of work needed to collect the excise duty.

The tax administration burden not only consumes government revenue (Mahangila, 2017), but it has also been discovered that heavier tax burdens can significantly prevent the formation of new enterprises (Braunerhjelm et al., 2015). Specifically, a 10% increase in taxes might reduce the formation of businesses by 4%. It is important to reduce this burden, which could be done through consolidating taxes and fees, introducing an electronic tax system, avoiding the duplication of information required by the government, raising business owners’ awareness of new regulations, and creating One-Stop Centers (Mattia & Shawn, 2010). This would reduce the number of payments to one, rather than taxpayers having to make three payments each time. There should be a combined (single payment) reporting and collection arrangement for Employers’ Pay As You Earn (PAYE), Pension Fund, and Health Contributions, because all of them are payable on the 15th of each month. To simplify the tax regime, social security contributions, health insurance, and PAYE should be paid together as one payment (see Figure 4).

Electronic one-stop-shop and e-tax: Reducing the Zanzibar tax administration burden.

Furthermore, the introduction of an electronic system would enable the ZRB to have access to taxpayers’ data, and the frequency of filing VAT returns should be reduced to being semiannual, as is done with PAYE, as this would reduce the bureaucratic burden of businesses. Reducing the frequency of filing returns and combining tax payments would also reduce tax administration costs. Moreover, combining tax payments would not affect the financial position of any of the stakeholders involved as the tax burden and contribution to it are constant. With public–private dialogue and partnerships, the tax administration burden would be a lot less. Future studies should measure the impact of public–private dialogue on tax reforms. Moreover, the TRA-Zanzibar and ZRB should simplify the areas of complexity and uncertainty identified, either by redrafting the tax laws or their sections, not only because a certain tax system enables the government to make realistic tax estimations but also because it makes it easier to comply with tax laws. The provision of comprehensive guidelines is strongly recommended to reduce the uncertainty and complexity of tax laws. Similarly, a stable and predictable tax system enhances simplicity of tax laws as taxpayers know what is expected of them.

Last but not least, the government should avoid frequent changes in the laws and, when changes are necessary, it should engage taxpayers in a consultative process through public–private dialogues. The use of public–private dialogues when setting policy priorities, informing policy design, improving legislative proposals, and incorporating feedback in regulatory implementation is always encouraged (World Bank Group, 2014). Joint decision making by the private and public sector usually leads to better policies that are properly executed. However, as this study focused on the tax administration burden, we encourage future studies to obtain insights into the role of public–private dialogues and partnerships in tax formulation and administration—the extent, opportunities, and the gaps—so as to safeguard the interests of the public sector without compromising the quality of the business environment, economic growth, and poverty alleviation.

Footnotes

Appendix

Specifically, these costs are based on the following assumptions:

Acknowledgements

The data analyzed in this article came from the database of the research funded by ZATI, to whom the authors are very grateful. We greatly appreciate the constructive comments from David Irwin and other anonymous reviewers.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was funded by Business Environment Strengthening for Tanzania (BEST)-dialogues through the Zanzibar Association of Tourism Investors (ZATI) to whom the authors are grateful.