Abstract

This study investigates the dynamics of fiscal policy and economic stabilization using a panel dataset from Sub-Saharan Africa (SSA) sourced from the World Development Indicators (WDI) between 1985 and 2019. The study utilized a panel vector error correction model (VECM) rather than panel vector autoregression (PVAR) after ascertaining the presence of cointegrating equations (existence of long-run relationships). Also, both homogenous and heterogeneous panel unit root processes were utilized to test the panel data’s stationarity before estimating the panel VECM. Again, the cyclical decomposition (Hodrick-Prescott Filter) is adopted in examining the effect of fiscal policy on economic stabilization across countries in SSA. Essentially, the VECM estimation result reveals that both government expenditure (GEX) and total reserves (TRS) have significant long-run relationships but are not substantial enough to stimulate economic growth and stability in the short run. Simultaneously, the Hodrick-Prescott Filter’s (HP-filter) cyclical decomposition confirms the non-stability of economic growth and stabilization in SSA over time. In line with other numerous policy recommendations, the SSA countries’ governments should improve on the policies targeted toward controlling the financial (fiscal) leakages to ensure more robust economic stabilization in the region through increases in total revenue and reserves both in the short and long-run.

Keywords

Introduction

Most countries in the Sub-Saharan African region are still evolving and struggling to meet up with growth threshold. The slow rate of development is attributable to low incomes and revenues due to inadequate export generation from trade. It is proven that income and revenue generation within a stable economic context can reduce debt levels and contribute to total reserves. To achieve desired regional development, stability and growth, optimal macroeconomic policies are needed to drive up trade and exports.

What is seriously lacking in the literature is how revenue, reserves, trade, debt and inflation influence economic growth, development and stability, especially in the SSA region. For instance, most recent studies, such Kassouri and Altıntaş (2021), examine cyclical drivers of fiscal policy without factoring in trade, export, trade, reserves, inflation, and other core macroeconomic components, which in part, prompted this study.

Recently, a renewed call for effective policy, especially fiscal policy, has gained momentum, specifically in developing countries and regions. The call is motivated by substantial levels of economic instabilities orchestrated by notable global, regional, and country-specific economic, financial, and stock market crises and recessions. Together with the most recent COVID-19 pandemic, these crises have left many economies, mainly SSA countries struggling to reach a substantive stability threshold.

In most developed and developing economies, fiscal policy is often utilized as a veritable tool of controlling macroeconomic fluctuations as it smoothens volatility in major macroeconomic indicators, boosts the real GDP by 0.1% in developing countries, and 0.3% in advanced economies, and thus act as an economic stabilizer (WHO, 2015).

The choice of optimal macroeconomic policy in stimulating economic growth to achieve desirable economic stability is one of the central bank’s major tasks of any economy around the globe. Any performing country’s economic stability requires a prudential mix of macroeconomic policies that can be either monetary or fiscal. Fiscal policy revolves around government expenditure and taxation, and it is determined at different levels of government, such as local, state and national. On the other hand, monetary policy is controlled by financial authorities such as central banks and revolves around the money supply in a given economy (Abel & Bernanke, 2001).

Constant fluctuations and volatilities in exchange and interest rates have caused severe disturbances in government expenditures, revenue, trade, and inflation targeting, thereby exerting economic stabilization issues, especially in developing countries such as countries in Africa. The reverse is the case in most industrialized nations with less economic volatility due to stable macroeconomic indicators such as quarterly GDP, exchange, and interest rates with minor business cycle problems (Issing, 2005). Also, inadequate fiscal policies in most developing countries worsen inflation and thus contribute negatively to economic stabilization, as evidenced in some African countries such as Nigeria, Ghana, and Kenya, among others recently. Most of these developing countries lack discretionary policymaking, especially from the government and taxes, which could provide the needed stability during changes in economic activities (Issing, 2005).

Furthermore, the monetary policy uses money demand and supply measures to control money circulation within an economy; the fiscal policy uses fiscal instruments such as taxes and budgets to regulate the country’s economic activities. Fiscal policy is linked to revenues, public expenditures, and inflationary pleasure and can be achieved with a pragmatic and sustainable fiscal stance (Chowdhury & Afzal, 2015). According to the Keynesian hypothesis, fiscal policy could be contractionary or expansionary. The idea behind the contractionary fiscal policy is that the supply of money in a hypothetical economy is controlled to lower the disposable income and private consumption of economic agents, thereby controlling inflationary pressure. On the other hand, the expansionary fiscal policy is of the view that government expenditure or spending should be increased by injecting more money into an economy that will invariably increase disposable income and private consumption. However, either the fiscal policy stance or pursuit has a policy target to achieve depending on the current economic situation or phenomenon. Generally, the tools or instruments of fiscal policy can be classified according to the hierarchy (Figure 1).

The Flow Chart Shows the Hierarchical order of Fiscal Policy Instruments.

This study is centered around forty-eight (48) economies in Sub-Saharan Africa: Angola, Benin, Botswana, Burkina Faso, Burundi, Cabo Verde, Cameroon, Central African Republic, Chad, Comoros, Congo-Dem. Rep., Congo - Rep., Cote d’Ivoire, Equatorial Guinea, Eritrea, Eswatini, Ethiopia, Gabon, Gambia, Ghana, Guinea, Guinea-Bissau, Kenya, Lesotho, Liberia, Madagascar, Malawi, Mali, Mauritania, Mauritius, Mozambique, Namibia, Niger, Nigeria, Rwanda, Sao Tome and Principe, Senegal, Seychelles, Sierra Leone, Somalia, South Africa, South Sudan, Sudan, Tanzania, Togo, Uganda, Zambia, and Zimbabwe (World Bank, 2021).

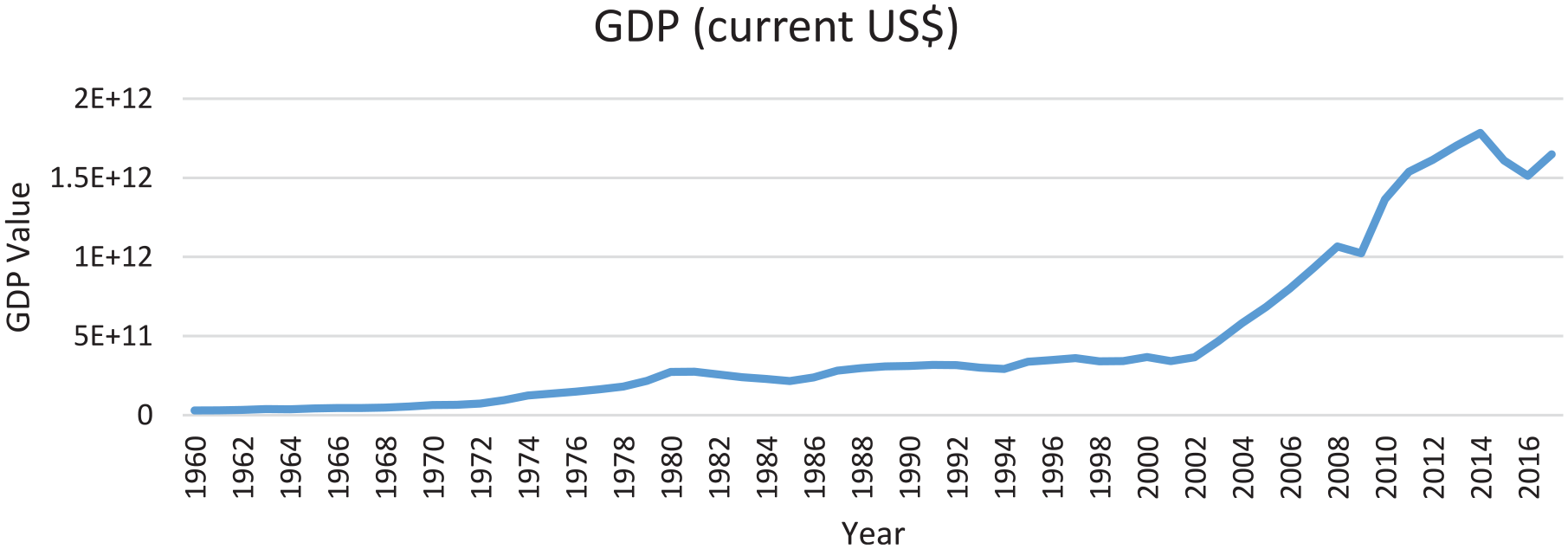

Additionally, the gross domestic product (GDP) of the aggregated economies in Sub-Saharan Africa (SSA) has experienced steady growth over time, considering the inefficiencies of the financial instruments and policies in addressing much-desired economic stability in the region.

From Figure 2, GDP of Sub-Saharan Africa was as low as about $29.924 billion in 1960 but continued growing at an increasing rate of about $366.214 billion in 2002 when it starts gaining significant momentum. The GDP continued rising from about 1.066 trillion in 2008 to about 1.784 trillion in 2014, before experiencing a sharp decline to about 1.512 trillion in 2016, and then started rising again to about 1.649 trillion in 2017.

The Gross Domestic Product (GDP) Trends of Sub-Saharan Africa.

Based on the foregoing, this study’s motivation is derived from the lacuna in both practice and empirical literature in addressing fiscal policy phenomena in Sub-Saharan African countries. Consequent to the motivational drive, some studies in this area either investigated fiscal policy in isolation or studied the economies individually. However, some studies in the literature are on selected economies in Sub-Saharan Africa with considerable deficiencies in synthesizing the concept of fiscal policy and economic growth in engendering economic stabilization and sustainability. Therefore, this study examines the dynamic effects of fiscal policy instruments on economic growth and stabilization over time, thus prescribing the optimal policy option targeting achieving economic stability and sustainability in the countries of Sub-Saharan Africa (SSA). This justification for this study is motivated by the non-performing fiscal policy instruments (e.g., public revenues) to engender stability in major macroeconomic indicators (such as GDP, inflation, exchange and interest rates) needed for economic development, stabilization and sustainability in most countries in SSA. The economic stabilization component of the study is well captured/analyzed using the Panel VEC model, Impulse-Response Function (IRF) and cyclical decomposition (Hodrick-Prescott Filter: H-P Filter). The econometrics model and techniques are best suited for analyzing the study objectives in relation to longitudinal data and the heterogeneous nature of economies SSA region (Hansen, 2001; Nkalu, 2023).

This paper is organized into five sections. The introductory section (Section 1) deals with the study’s overview and background, while Section 2 presents a detailed review of the related literature. Section 3 covers the methodology and panel econometric model specifications, followed by the empirical result presentations (Section 4), while Section 5 concludes the study with robust policy recommendations.

Review of Related Literature

A myriad of literature exists on fiscal policy, economic growth and stabilization. One of the central objectives of fiscal policy is to ensure an optimal mix of budget balance and taxes to drive economic growth and development to stabilize its growth (Nkalu, 2015). This study is anchored on the conventional growth theory known as endogenous growth theory in line with the theoretical and empirical literature review. The Endogenous growth theory is a modern growth theory that holds that internal (endogenous) forces are the significant determinants or drivers of economic growth rather than the external (exogenous) forces (Romer, 1994). The theory postulates that a substantial economic growth level can be recorded endogenously through an incentive for innovations, investment in human capital development, knowledge, and technological change (Pack, 1994). The theory believes that relative long-run growth can be attainable in an economy through robust policy measures that are not limited to education, research, development, and subsidies (Aghion & Howitt, 1992).

Empirically, a good number of studies exist in this subject area; for instance, the most recent amongst the studies is the work of Emmanuel Adegoriola (2018), who employed an error correction model (ECM) in determining the effectiveness of monetary and fiscal policy instruments in stabilizing the economy of Nigeria using data from world development indicators. The study covers a period ranging from 1981 to 2015. The study employed the cumulative sum of squares method (CUSUM) to identify the country’s growth under the study’s stability. The empirical analysis results find a long-run relationship between monetary policy and economic stabilization in Nigeria. The estimated ECM result shows a negative effect with less than one (unity), which confirms a positive nexus between government expenditure, money supply, and revenue, with a negative impact between budget deficits and interest rates in economic growth.

Yoshin et al. (2018) adopted Japan and Greece as case studies in investigating the fiscal policy conditions for government budget stability and economic recovery. The study employed the Domar and Bohn conditions is evaluated the levels of constraints of government debt situation within the two economies of Japan and Greece concerning economic stability. The study’s findings revealed that fiscal and economic sustainability could be achieved in the Japanese and Greece economies if the revenue and expenditure sides can be adjusted concurrently through the downward adjustment of the government expenditures in both countries.

In Nigeria, Atuma and Eze (2017) investigated the fiscal instruments in Nigeria using Vector Error Correction Model (VECM) with annual time series data ranging from 1970 to 2015 sourced from the Central Bank of Nigeria’s statistical bulletins of various years. The study employed fiscal policy instruments like tax revenue, government recurrent and capital expenditure, domestic debt, and total exports. The cointegration test revealed a long-run relationship among the variables of interest in the study. The VECM estimation results showed the significant and negative impact of tax revenue and government capital expenditure on economic growth instead of the positive and significant impact of recurrent government expenditure and total export on Nigeria’s economic growth.

Ugwuanyi and Ugwunta (2017) studied fiscal policy and economic growth in some selected economies in Sub-Saharan Africa using panel data with fixed effects. Even though the study indicated no exact source of data and the scope, the finding revealed that government expenditure has a distortionary effect on economic growth with a positive but insignificant impact on economic growth. Similarly, Onwe (2014) utilized the baseline model to analyze fiscal policy instruments’ impact on Nigeria’s economic growth with economic stabilization. The annual time series data sourced from the 2013 Central Bank of Nigeria’s statistical bulletin were employed to estimate the study objectives, though there was no indication of the time covered under the study period. The estimation results revealed that government expenditure as an instrument of fiscal policy is insufficient to achieve the desired economic growth and economic stabilization in Nigeria.

Socol and Feraru (2017) studied fiscal policy tools in solving the economic-financial crisis in the Central and Eastern European (CEE) economies. The study utilized fiscal reaction functions in evaluating the pre and post-financial crisis. The result showed that fiscal components are helpful tools in stabilizing the CEE states’ economies irrespective of the volatility caused by the economic crisis. A similar study was carried out in Indonesia by Kuncoro (2015), who made an empirical enquiry into the effectiveness of fiscal policy in stabilizing macroeconomic indicators, especially prices in Indonesia, using quarterly data between 2001 and 2013. The study revealed that credible fiscal policy is robust in achieving macroeconomic price stabilization if adequately employed, while incredible fiscal policy does not positively control fluctuations in inflation. In another related study in Serbia, Rakić and Rađenović (2013) studied monetary and fiscal policy effectiveness in achieving macroeconomic stability by adopting both Keynesian and monetarist approaches. The study adopted quarterly data ranging from 2003Q1 to 2012Q4. The study arrived at an inconclusive result, concluding that neither of the two methods is superior in achieving Serbia’s significant stability.

To prescribe a suitable policy option to end protracted policy issues and stimulate the acceptable level of inflation in the European area, Corsetti et al. (2016) reviewed different standard models of economic stabilization. The study concluded that a prudential monetary-fiscal policy mix is necessary to stabilize economies within the European area. In Bangladesh, Chowdhury and Afzal (2015) examined monetary and fiscal policies’ effectiveness in stimulating growth and stability with annual time-series data sourced from world development indicators (World Bank, 2021). The study scope ranges between 1980 and 2012. The study opined that the choice between monetary or fiscal policy centers on the economy’s current economic and political condition. The simple linear regression equation results revealed that both fiscal and monetary policy promotes growth in Bangladesh.

In Nigeria, Agu et al. (2015) conducted an empirical study on the relationship between fiscal policy and economic policy, emphasizing various public expenditure components over 1961–2010. The study adopted the ordinary least squares (OLS) technique to estimate the annual time series data sourced from Nigeria’s central bank (CBN) 2011 statistical bulletins. The study found a significant positive relationship between fiscal policy (especially from government spending) and economic growth in Nigeria. The study concluded by affirming that Nigeria’s desired growth and economic stability could be feasible in the face of stable government revenue and the private sector’s effectiveness.

In Kenya, Mutuku and Koech (2014) used the autoregressive (VAR) approach as well as the impulse response functions (IRF) in estimating both monetary and fiscal policy shocks on economic growth with time series data ranging from 1997 to 2010. The estimation output result revealed fiscal policy’s positive and significant impact on real economic growth, while monetary policy is not significant. Again, Audu (2012) employed an error correction model (ECM) and cointegration to study the causal nexus between fiscal deficits, money supply, and exports and how they influenced Nigeria’s economy between 1970 and 2010. The study equally engaged a cumulative sum in testing the stability of Nigeria’s economy; however, the study showed a significant level of instability in the economy under study. The GDP exert a significant nexus with other variables in the model. Above all, the study found a positive and significant fiscal policy effect on Nigeria’s economic growth.

Bergman and Hutchison (2014) utilized the basic dynamic Panel in studying fiscal policy and economic stabilization of 81 advanced, developing and emerging economies between 1985 and 2012. The study developed fiscal rule indices and examined how the rules can enhance the countries’ pro-cyclical policies under study. On the other hand, the study investigated how fiscal policy responds to the economies’ economic growth over time. The estimation result revealed that the degree of effectiveness of fiscal policy rules goes a long way in downsizing policy pro-cyclicality in the economies and spurring growth. In Spain, Maravalle and Claeysb (2010) modeled the effects of fiscal policy using the RBC model of the small open economy following Mendoza (1991). The study looked at the effects of pro-cyclical fiscal policy on economic stabilization using data from Ireland. The study reveals a high level of instability in the economy due to big volatile shocks in investment, consumption, and current accounts.

Gnip (2013) evaluated the effect of fiscal policy in stabilizing Croatia’s economy using a structural vector autoregression approach (SVAR). The study’s result revealed that one of the fiscal policy components, such as government expenditure, positively influences the economic output of the Croatian economy, thereby validating the Keynesian hypothesis. In the Philippines, Halcon and De Leon (2004) adopted St. Louis Model to determine the efficiency of the two competing approaches, fiscal and monetary policy, in stabilizing the Philippines’ economy. The study found that fiscal policy is more viable than monetary policy in stabilizing the Philippines’ economic growth.

In industrialized and developing economies, Lee and Sung (2008) adopted ordinary least squares (OLS) in examining fiscal policy and economic stabilization within the business cycle environment. The study’s scope spans from 1972 to 1998. The datasets for the analysis are majorly sourced from the World Bank’s WDI and Organization for Petroleum Exportation Countries’ (OPEC) annual statistical bulletins. Aside from examining the effect of fiscal policy components on economic growth in the 92 industrialized and developing countries, the study adopted the HP filter to capture business cycle fluctuation and economic stabilization. The study found the asymmetric fiscal policy response to economic stabilization in both the industrialized and developing countries and recognizes government expenditure’s effectiveness in determining economic stabilization in the economies under business cycles.

In the review of the related literature, most empirical studies in fiscal policy are prevalent in developed countries, with very few studies in developing regions. Even fewer studies in developing regions, especially in Africa, are more country-specific (see Mutuku and Koech (2014) in the Kenyan economy). Unlike some studies that chose to analyze some selected countries in SSA, this study engaged all 48 economies in SSA to ensure more excellent study coverage, robustness and efficient policymaking. Again, the study is so unique that it analyzes both the short and long-run scenarios of fiscal policy and economic growth nexus through economic stabilization. The economic stabilization component of the study is well captured/analyzed using the Panel VEC model, Impulse-Response Function (IRF) and cyclical decomposition (Hodrick-Prescott Filter: H-P Filter). The econometrics model and techniques are best suited for analyzing the study objectives in relation to longitudinal data and the heterogeneous nature of economies SSA region (Hansen, 2001; Nkalu, 2023). The scope of the analysis (1985–2019) provides enough coverage and updates on the study area, and all these gaps are the serious lacuna that this study has filled in the literature.

Methodology

Theoretical Framework

The theoretical framework supporting the empirical model is rooted in the “Mundell-Fleming” model. The theoretical framework of the Mundell-Flaming Model provides a simple understanding and linkage of a small open economy to international trade and partners in both financial assets and goods markets in the monetary/fiscal policy discussion/analysis. Small open economies characterize most Sub-Saharan Africa (SSA) economies, given the international trade features. Nevertheless, the Mundell-Fleming Model captures essential components of government expenditure and international trade (export) as the extension of Keynesian investment-savings (IS) and liquidity preference-money supply (LM), that is, the IS-LM model (Abel & Bernanke, 2001).

The introduction of international trade, such as net export (NX) as the fourth component of the aggregate expenditure equation, yields the traditional Mundell-Fleming Model.

Such that;

Where; AE stands for aggregate expenditure, C indicates consumption (domestic), I implies investment, G means government expenditure, and NX signifies net export (which means; according to Abel and Bernanke, 2001 as the total monetary value of export minus the total monetary value of import). Net exports (NX) consist of income generated from domestic goods sold abroad (export) minus income abroad from consumption of domestic goods produced abroad (import) (McCausland, 2020).

Hence;

Note that net exports (NX) is something referred to as trade balance or current account (CA), where;

Therefore, the aggregate expenditure can be linked-to aggregate output, Y, which total trade, reserves, revenue, inflation, debts, and the level of competitiveness of the domestic economy in international trade can determine.

Empirical Model

The previous section provides the theoretical framework for understanding fiscal policy and economic growth/stabilization. Hence this study empirically adopted a panel vector autoregressive (VAR)/vector error correction (VEC) Model in examining the endogenous interactions of fiscal policy instruments and economic growth. It also incorporates the Hodrick-Prescott (HP) filter to verify the stabilization aspect of economic growth in Sub-Saharan Africa (SSA). The final rationale for adopting either Panel VAR/VEC model largely depends on the outcome of the cointegration test result. If the cointegration test result identifies the presence of cointegrating equation(s) in the model, the VEC model will be more suitable; otherwise, the VAR model is upheld. This study is based on 48 economies of Sub-Saharan Africa. The panel data for the study analysis are sourced from the World Bank database via World Development Indicators (WDI), which ranges from 1985 to 2019. Therefore, the panel VAR model follows a traditional panel vector autoregression approach that allows endogenous interactions of all the system variables and control for unobserved individual heterogeneity (Love & Zicchino, 2006). The panel VAR specification for cross-section i follows the non-stationary VAR process:

where

where C and B are the parameters of the explanatory variables. Hence, in the panel analysis, dependent and independent variables in the empirical model include gross domestic products (GDP), government expenditure (GEX), total revenue (TRV), total reserves (TRS), trade (TRD), total debt (TDT), and inflation (INFL). The above equation could be concisely transformed into the VEC model as follow:

where

Economic Stabilization Analysis

In modern macroeconomics, Hodrick and Prescott (1980, 1997) popularly referred to H-P filter is the standard technique of removing or de-trending cyclical component of time-series data mainly in the real business cycle theory with the target of obtaining the smoothed curve of the time-series representation for long-run analysis (Ravn & Uhlig, 2001). The H-P filter can be applied to monthly, quarterly or annual data in the real and nominal data analysis, especially in studies where artificial datasets are compared with the actual (Blackburn & Ravn, 1992). Therefore, the HP filter is utilized in this study to cater to the cyclical economic stabilization component over the long-run scenario in SSA. Thus the HP filter detaches the smooth trend τ t from the given number of data yt by computing the “minimizing” mathematical equation:

where;

In sum, if

Presentation of Empirical Results and Discussions

This section presents all the generated outputs and estimation results from the previous section’s panel data model (Methodology). One of the necessary steps in conducting a panel VAR/VECM analysis is to ascertain its stationarity. The panel stationarity tests for time-series data help confirm the consistency of the mean and variance over a given period (Mohr, 2018). Thus panel stationarity analysis is followed immediately after presenting a summary or descriptive statistics. Then, the panel estimation result is presented following other pre-estimation analyses.

Summary Statistics

Table 1 below summarizes descriptive statistics for the macroeconomic variables in the panel estimation model. Though the variables have been mentioned and briefly explained in the methodology section, it is still pertinent to state the complete acronyms. The GDP = gross domestic product, GEX = government expenditure, TRV = total revenue, TRS = total reserves, TRD = trade, TDT = total debt, and INF = inflation. The information described in the summary statistics includes measuring central tendencies such as the mean, median, minimum and maximum values. The summary statistics also consist of other necessary measures like skewness, kurtosis, Jarque-Bera, and others such as probability, sum square deviation, and the number of observations. The statistics present an X-ray of behavioral data patterns in the econometrics model. Hence there is a need to test further to confirm the stationarity of the dataset before estimation.

Descriptive/Summary Statistics.

Source. Authors’ computation from World Bank (2021).

Stationary (Unit Root) Test for Panel Regression Analysis

This section presents the stationarity test result in the homogenous (common) and heterogeneous (individual) panel unit root processes. Levin-Lin-Chu’s (LLC) panel unit root process is utilized under the homogenous (common) panel unit root. The LLC panel unit root result, as presented in Table 2 implies that the variables are stationary at the first difference I(1). On the other hand, the result from the Im-Pesaran-Shin under the heterogeneous (individual) panel unit root process revealed that the variables are all stationary at the first difference I(1). The result suggests that the null hypothesis (no unit root) is rejected in the test. In the precise interpretation, the “statistic values” of the tests are greater (in numerical values) than the probability values (the values in bracket) at 5% levels of significance. Therefore, the evidence that the variables are all stationary and integrated in the same order I(1), further confirms the cointegration amongst the variables to ascertain the possible existence of long-run joint relationships.

Stationarity/Unit Root Tests Results for Panel Regression Analysis.

Source. Authors’ computation from World Bank (2021).

Note.**Denotes significant at 5%.

Selection of Lag Length

This study follows the Schwarz Information Criterion (SIC) to determine the suitable lag length for the analysis. The rationale behind the appropriate selection of optimal lag goes a long way in avoiding multicollinearity. Therefore, lag two(2) is adopted in the study, and the choice is anchored on the Schwarz Information (SIC) criteria.

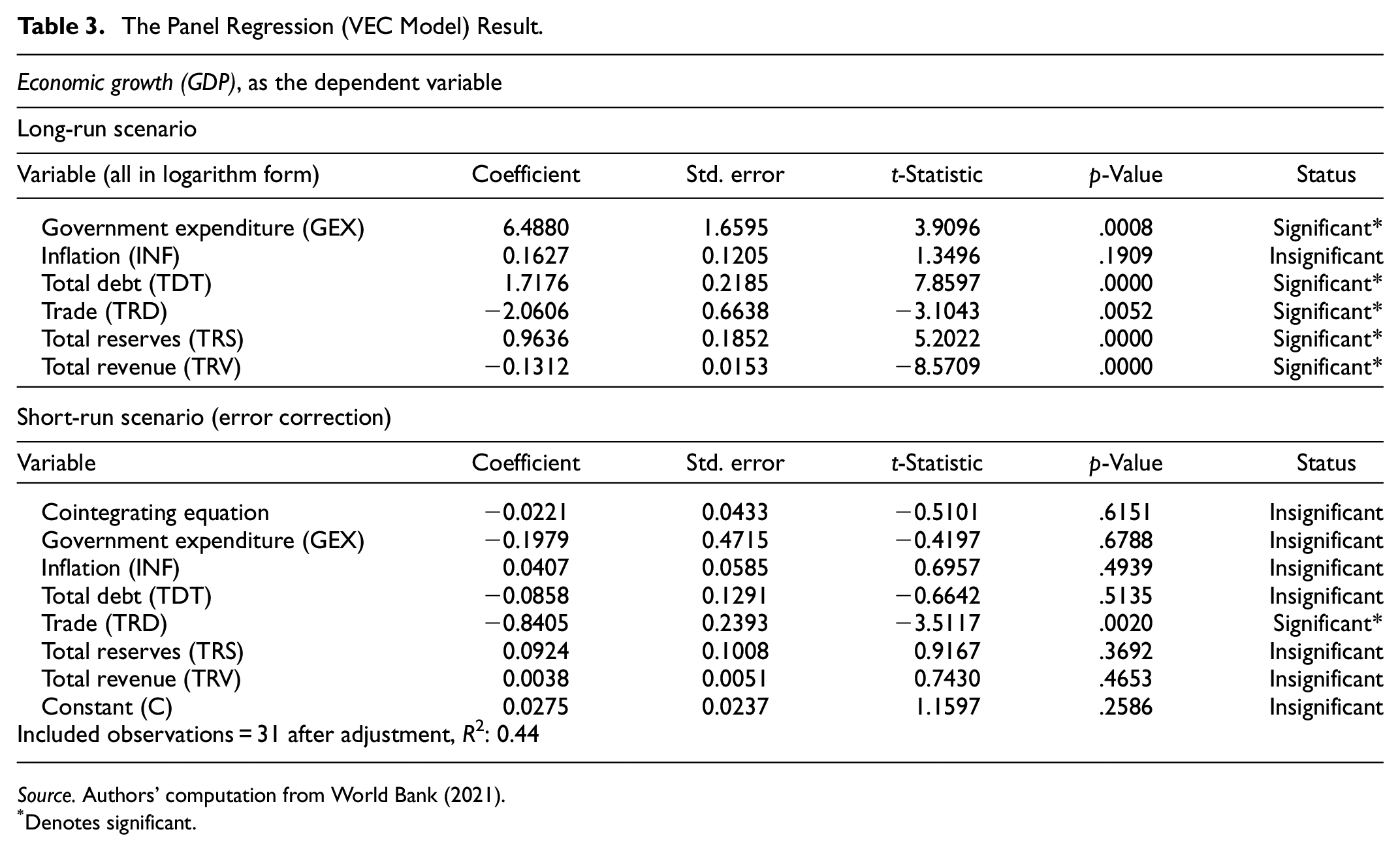

Vector Error Correction Model Result Presentation/Discussions

Table 3 presents the estimation result from the panel Vector Error Correction Model (VECM). The coefficient results can be interpreted in long-run elasticities, given that the variables are in logarithms (Nkalu et al., 2020; Solnik, 2000).

The Panel Regression (VEC Model) Result.

Source. Authors’ computation from World Bank (2021).

Denotes significant.

As presented in Table 3, the result is grouped under long and short-run scenarios. In the long run, trade (TRD) and total revenue (TRV) have not positively affected economic growth and stabilization but exert adverse shocks with statistically significant results. On the other hand, government expenditure (GEX), inflation (INF), total debt (TDT), and total reserves (TRS) have been able to provide a positive influence on economic growth and stabilization with statistically significant results except for inflation (INF). In the long-run, government expenditure (GEX), total reserves (TRS), and even total debt (TDT) are positively significant in adjusting to the long-run equilibrium. At the same time, inflation (INF) is positive but not statistically significant in the long run.

Still under the long-run scenario and narrowing down the levels of these influences of the right-hand side variables (i.e., independent variables) on the left-hand side variable (dependent variable) shows; a percentage increase in government expenditure (GEX) will result in approximately 6.49% increase in economic growth (GDP) on average while holding every other variable constant in the long-run. This is because most economies in Sub-Saharan Africa (SSA) are developing countries. As such, channeling tremendous energy to capital infrastructural developments will ensure more remarkable economic growth and significantly influence all-inclusive economic development positively in the long run. Also, a percentage increase in inflation (INF) will lead to a nearly 0.16% increase in economic growth (GDP) on average in the long run while holding every other variable constant.

Similarly, a percentage increase in total debt (TDT) and total reserves (TRS) will result in about 1.72% and 1.96% increase in economic growth (GDP), respectively, in the long-run ceteris paribus. This result shows that keeping inflation at a moderate level could positively stimulate economic growth and inflation theory. On the other hand, a percentage rise in trade (TRD) and total revenue (TRV) will result in approximately 2.06% and 0.13% decrease in economic growth (GDP) in the long run, with all the variables, held constant. The results show low trade and revenue-generating trends in most Sub-Saharan Africa (SSA) economies, which need to be reviewed appropriately.

Furthermore, the value of the cointegration equation of the vector error correction (VEC) model shows a negative sign which complied with a priori expectation even though the value is statistically insignificant. Again, the coefficient value of the VEC model error correction (the cointegrating equation) highlighted that last year’s equilibrium deviation is re-adjusted at a speed of nearly 0.02%.

Under the short-run result, the estimation outcome from the cointegrating equations shows that the last year’s equilibrium deviation from the long-run equilibrium is corrected in the present period at a re-adjustment speed of approximately 0.02%. In the Government expenditure (GEX) result, a percentage increase in GEX is associated with a nearly 0.20% increase in economic growth (GDP) on average (other things being equal) in the short run. For Inflation (INF), a rise in inflation is associated with about 0.04% decrease in economic growth (GDP) on average (other things being equal) in the short run.

For total debt (TDT) and trade (TRD), a percentage rise in the total debt and trade is connected to about 0.09% and 0.84% fall in economic growth (GDP) on the average ceteris paribus in the short-run, respectively. Given these findings’ outcomes, the negative contributions of total debt and trade on SSA economic growth in the short run explain these findings’ outcomes. The economic implications of these findings are not far-fetched. Bad debts are growth-reversal in the SSA economies due to the proportion of financial commitments being channeled to debt servicing. Also, a continuous record in trade deficits, on the other hand, acts as a clog in the wheels of economic growth and stabilization in the region.

Nevertheless, a percentage increase in total reserves (TRS) and total revenue (TRV) are associated with approximately 0.09% and 0.004% rise in economic growth (GDP), respectively, on average (other things being equal), in the short-run. This shows that both total reserves and total revenue positively affect economic growth in the short run though not significantly. In sum, inflation, total reserves, and revenue positively affect economic growth, while government expenditure, total debt, and trade impact economic growth in the short run.

Impulse Response Function—IRF

The IRF is equally utilized to support further the result generated from the cointegration test. Followed by Asari et al. (2011), Cholesky contemporaneous restrictions are engaged to elicit or infer robust interpretation in the impulse response function. The recursive line graph in each of the IRF chart denotes that the first variable appearing on the chart headline is contemporaneously influencing the last variable and not vice versa. The following is the IRF chart:

In Figure 3, the initial response of economic growth (GDP) to a unit shock in government expenditure (GEX) is positive, while the response to inflation (INF) to a unit shock in economic growth (GDP) is positive. Also, trade (TRD), total reserves (TRS), and total revenue (TRV) respond positively to a unit shock(s) in economic growth (GDP), while total debt (TDT) responds negatively to a unit shock in economic growth (GDP). Similarity, total debt (TDT), trade (TRD), and total reserves (TRS) respond negatively to a unit shock(s) in government expenditure (GEX). In general, the evidence is bound from the IRF that the speed of re-adjustment to short-run equilibrium is fast.

The IRF Chart.

Other Robustness Tests

Other diagnostic tests, such as VEC residual serial correlation, show no serial correlation in the model. The VEC residual normality test shows that all the variables in the model are normally distributed. In conclusion, a further test for VEC residual heteroscedasticity shows that the model is not heteroscedastic.

Cyclical Decomposition

This sub-section presents the cyclical decomposition of the economic growth variable (GDP) to determine if the growth in Sub-Saharan African economies is stable over the years (1985–2019).

The blue line denotes the trend (nominal GDP trend as a proxy to economic growth) in Figure 4. In contrast, the red line shows the decomposed trend in GDP over the years, and the green line is the cyclical component of economic growth in Sub-Saharan Africa. This simply shows that fiscal policy has not achieved economic sustainability in Sub-Saharan Africa over the study period given the high level of variability or fluctuation in the GDP’s cyclical component; hence, non-stability exists in economic growth and stabilization in SSA over the study period.

Hodrick-Prescott Filter (H-P Filter).

Summary, Conclusion, and Policy Recommendations

This study centered on fiscal policy and economic stabilization in the 48 economies made up of Sub-Saharan Africa. While panel data generated from the WDI were utilized in the estimation analysis, the study covers a sufficient period from 1985 to 2019. The study engaged panel VEC model, panel unit root, Johanson cointegration test, impulse response function (IRP), and cyclical decomposition (H-P filters) to analyze the empirical study’s objectives.

The stationarity test result using homogenous (Levin-Lin-Chu) and heterogeneous (Im-Pesaran-Shin) approaches revealed that all the model variables are stationary at first different, which prompted a cointegration test using the Johanson approach. The cointegration result showed cointegrating equations that signified the existence of long-run relationships among the variables in the model, thereby motivating the adoption of Panel VECM instead of panel VAR. The VECM estimation result showed that both government expenditure (GEX) and Total reserves (TRS) have a significant long-run relationship but are not substantial enough to stimulate economic growth and stability in the short run. The VECM estimation is followed by the impulse response function (IRF) to ascertain the speed of adjustment to the short-run equilibrium. The IRF attested that the variables are relatively fast in the short-run adjustment process.

Based on the empirical findings, it is recommended that; the SSA countries’ governments should improve the policies targeted toward controlling the financial (fiscal) leakages to ensure more robust growth and economic stabilization. In SSA countries, most channels and processes of providing financial disciplines in government expenditures are not well streamlined, controlled and monitored, thereby giving an avenue for corruption and the diversion of public funds to personal or individual accounts. Also, income and revenue generation improvements are tantamount to growth and substantial contributions to the GDP in any economy, which SSA economies are not excluded. Therefore, the governments in these region’s economies should look inward to improve income generation through exportation and international trade to attract more favorable trade and foreign exchange for a positive/significant contribution to economic growth and stabilization.

In addition, fiscal authorities in the SSA economies should ensure optimal tax policies and create efficiency in tax administration to monitor government fiscal disciplines in terms of excess spending and increased earnings to ensure growth and stabilization of the economies in the region. Moreover, the SSA countries’ governments should always keep inflation under constant checks to avoid adverse effects on the cost and ease of doing business within the region. This will go a long way in ensuring stability in the economies through positive contributions to the GDP, economic growth and stabilization. Recognizing that most economies in Sub-Saharan Africa (SSA) are still at the developing stage, the governments of the SSA countries should engage in more radical capital infrastructural development. In the long run, this could be the primary driver of economic growth and development, resulting in an increment in the region’s total revenue. Besides, the international trade policies in Sub-Saharan Africa’s economies need to be reviewed positively to ensure robust revenue generation through efficient multilateral trade policies.

Similarly, the government of SSA countries should solidify the total reserves as it contributes more significantly to the economic growth and development in the SSA region. This is because total reserves succor to any shortfalls in income generation necessary to boost economic activities and stabilize the SSA region. Finally, prudential macroeconomic management should be adequately and continuously checked to moderate vital macroeconomic indicators such as inflation to ameliorate their devastating effects on Sub-Saharan Africa’s economic growth and stability. This will go a long way in alleviating inflation’s negative consequences on other macroeconomic indicators, economic development, sustainability and stabilization in the SSA region. Again, the external debt component of total debt should be adequately utilized to manifest the primary objective(s) of the borrowing’s initial cause to achieve desirable growth and sustainability in Sub-Saharan African countries.

To summarize, further studies are needed to close a wide gap in the literature. For more studies, the macroeconomic determinants and comparative analysis of productivity slowdown in the SSA region vis-a-vis other developed economies are similar gray areas to be X-rayed. Further studies will provide more insights into how revenue from exports and manufactured products relates to the region’s productivity slowdown and structural change.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethics Statement

Not Applicable.