Abstract

Prior research shows that corporate innovation enhances firm value. Using a novel text-based measure of corporate innovation, we explore how the effects of corporate innovation on firm performance change in the presence of economic policy uncertainty. We use a large sample of US firms over the period 1996 to 2010 to test the relationship by executing firm-fixed effect regressions. Our results show that corporate innovation significantly positively affects firm performance. However, our results also reveal that the favorable effect of corporate innovation on firm value is reduced substantially in times of greater economic policy uncertainty. The latter result highlights the urgent need for policymakers to maintain the long-term consistency of economic policies to encourage firms’ innovative activities. Several robustness checks including three proxies for firm performance and four instrumental-variable analyses confirm our original results.

JEL Classification: E66, O31, G32

Keywords

Introduction

This paper investigates how the effects of corporate innovation on firm performance change in the presence of economic policy uncertainty (EPU). The operating environment is an important factor that affects firm performance and influences a firm’s choice of strategies (Rodriguez Lopez et al., 2017). The constant change in economic policies can make the operating environment complex and difficult to predict, as uncertainty can affect firm decision-making and firm performance (Gulen & Ion, 2015). Thus, firms should consider operating environmental factors when devising their strategic positioning (Banerjee & Homroy, 2018; O’Regan et al., 2012).

EPU has been steadily growing in the United States since the 1990s (Baker et al., 2020). Several events such as 2007 to 2008 financial crisis, presidential elections, U.S.-China trade war Covid-19 pandemic and the Russia-Ukraine war have pushed the government to respond in unprecedented ways such as large fiscal expansions, unconventional monetary policies and unpredictable trade policy. One of the most recent events, the Covid-19 pandemic has caused an upsurge in EPU, making this study more urgent to address than others at this time. Recognition of the fact that EPU might have affected the performance of innovative firms and non-innovative firms differently has therefore made the policy actions in response to EPU relevant and urgent. Therefore, the empirical evidence on the link between corporate innovation and firm performance under the influence of EPU appears very timely. Furthermore, since innovation has been gaining attention from academicians and practitioners, our study aims to make clear the true benefit of innovation. Additionally, it is an important opportunity to utilize the availability of novel text-based innovation data for the investigation of innovation issues at the firm level.

Grasping the concept of the resource-based view (RBV), innovation is considered as a crucial resource for firm competitive advantage and firm performance (Awan et al., 2018; Penrose, 1959). However, prior studies reveal mixed results. Some research claims that innovation improves firm performance in the following ways: increases profit (Eberhart et al., 2004; Sougiannis, 1994), improves productivity level (Damanpour & Aravind, 2012; Damanpour & Evan, 1984; Hall & Mairesse, 1995), increase market value (Armstrong et al., 2006; Chauvin & Hirschey, 1993), and strengthen competitive advantage (Aw & Batra, 1998). However, another strand of research argues that the high cost of innovation and uncertain return may outweigh the benefit and cause firm performance to deteriorate (Chan et al., 2001; Coad et al., 2016; Hall & Rosenberg, 2010). One of the reasons for the mixed results is inadequate innovation proxies commonly used such as patent and R&D expenditure (Kriebel & Debener, 2019; Mukherjee et al., 2017; Ranta et al., 2021). Patent counts face critique when used as a proxy for innovation because it cannot capture the true extent of innovation output as not all innovations are patentable. R&D expenditure only captures the input of the innovation process but it does not effectively capture the output or quality of innovation (Aghion et al., 2013). Thus, we fill the gap by adopting a novel text-based innovation index which is constructed from a textual analysis of analyst reports of S&P 500 firms (Bellstam et al., 2021). Unlike other innovation proxies, the text-based innovation index can capture firm innovation quantitatively and qualitatively (Bellstam et al., 2021). Consistent with RBV, our empirical results reveal that innovation has a favorable effect on firm performance.

Furthermore, unlike prior papers, we extend the concept of RBV framework as well as the existing literature on the association between corporate innovation and firm performance (e.g., Guo & Wang, 2022; Su et al., 2020; YuSheng & Ibrahim, 2020) by incorporating the EPU factor into our study. We examine the relationship between corporate innovation and firm performance in the presence of EPU. Our study is related to two strands of literature. On one hand, the literature suggests that the favorable effect of corporate innovation on firm performance is reduced because during high EPU financing innovation and intangible asset tends to be costlier due to poor ability to raise capital in the credit market and ineffective use as loan collateral (Holthausen & Watts, 2001; Shleifer & Vishny, 1992; Williamson, 1988). On the other hand, a strategic growth option suggests that EPU increases the potential gain of innovation and intangible assets, and leads to improved firm performance (Christiano et al., 2008; Gilchrist et al., 2014; Kulatilaka & Perotti, 1998). We fill the gap by including the interaction term between text-based innovation and EPU index in the regression, and empirical results reveal that the favorable effect of innovation is reduced substantially when EPU is heightened.

In light of the preceding argument, we fill the research gap by investigating how EPU influences the association between corporate innovation and firm performance using text-based innovation measures. Drawing on RBV conceptual framework, we address the following research questions: (1) Does corporate innovation improve firm performance? (2) How do the effects of corporate innovation on firm performance change in the presence of EPU? The answers to these questions will guide academics, policymakers and practitioners in understanding the importance of a supportive operating environment for firm innovation.

In terms of academics, our study contributes to the literature in two aspects. First, it clarifies the relationship between corporate innovation and firm value in the presence of EPU. RBV and previous research on innovation focus on how corporate innovation impacts firm value (e.g., Guo & Wang, 2022; Su et al., 2020; YuSheng & Ibrahim, 2020). However, little is known about how the link between corporate innovation and firm value changes under the influence of EPU. We address this gap and our results reveal that in times of great EPU, the favorable effect of corporate innovation on firm value is reduced substantially. This highlights the role of firms’ operating environment, EPU in influencing corporate innovation value because in the presence of EPU, bankruptcy and financing costs are heightened for innovative firms. In this way, our study improves the understanding of the mechanism and conditions of the effect of corporate innovation on firm value. This study contributes to theory on RBV and the related literature on innovation and EPU (e.g., Abdul-Shukor et al., 2008; Borghesi & Chang, 2020; Gulen & Ion, 2015; Xu, 2020).

Second, prior studies on innovation often face limitations when drawing any causal inferences between innovation and firm performance because of the inadequate innovation proxy namely patent count and R&D expenditure (e.g., Kriebel & Debener, 2019; Mukherjee et al., 2017; Ranta et al., 2021). We fill this research gap by adopting a novel text-based measure of innovation developed by Bellstam et al. (2021). We believe that our text-based measure provides a superior innovation measure because it captures firms’ innovation with reference to patenting and R&D. Thus, we contribute to the debate on whether corporate innovation is beneficial to the firm by using text-based innovation measure and show that corporate innovation is positively associated with firm value.

These contributions help researchers, policy makers, managers and investors to understand the importance of a supportive operating environment for firms to fully harness the benefit of innovation.

The remainder of the paper is organized as follows. Section 2 discusses the related literature. Section 3 presents the methodology. Section 4 presents descriptive, empirical results and robustness tests. Section 5 concludes the paper.

Related Literature

In this section, the literature on corporate innovation and firm performance will be discussed. In Section 2.1, RBV is discussed. In Section 2.2, we discuss the contradictory literature on the association between corporate innovation and firm performance. In Section 2.3, we discuss how EPU impacts firm performance. In Section 2.4, we discuss the interaction effect of corporate innovation and EPU on firm performance.

Resource-Based View

Our conceptual framework is grounded in the resource-based view. The resource-based view (RBV) was initially promoted by Penrose (1959) and expanded by others (Awan et al., 2018; Barney, 1991; Conner, 1991; Wernerfelt, 1984). The RBV postulates that resources that are valuable, rare, difficult to imitate, and non-substitutable best position a firm for long-term success. Because resources with respect to innovation are usually difficult to imitate, RBV suggests that innovation may enhance firm’s competitive advantage and contribute to firm performance. Examples of such resources are intangible assets including employee intelligence, skills, insight from the manager and improved production process. Thus, RBV highlights how firms can achieve performance outcomes by investing in innovation (Awan et al., 2018). We adopt RBV conceptual framework and expand it by examining how different operating environments such as EPU can affect the contribution of innovative resources to firm performance. Our study provides a better understanding of how innovation and intangible assets are deployed to promote firm performance.

Corporate Innovation and Firm Performance

According to RBV, firms gain competitive advantage through firm’s own resources that are heterogeneous and immobile (Penrose, 1959). However, whether corporate innovation can improve firm performance is still under debate because of inadequate innovation proxies. Much theoretical and empirical evidence documents that corporate innovation tends to improve firm performance (Awan et al., 2022; Guo & Wang, 2022; Su et al., 2020; YuSheng & Ibrahim, 2020). For example, studies found that an increase in corporate innovation will lead to the following effects on firm; increase firm profitability (Branch, 1974; Sougiannis, 1994), positive impact on firm’s profit margin (Eberhart et al., 2004), increase firm’s market value (Armstrong et al., 2006), and increase in firm’s intangible assets (Kramer et al., 2011). In many studies, innovation is regarded as intangible assets (Kramer et al., 2011; Skinner, 2008). Examples of intangible assets are intellectual capital, human capital (the value of employee training, morale, loyalty, knowledge, etc.), and process-related capital (the value of information technology, production processes, etc.) (Skinner, 2008). Empirical studies show that intangible assets create value-added to the firm, lower cost of production and are positively associated with firm performance (Pulic, 1998; Riahi-Belkaoui, 2003). To illustrate this point, the know-how and trademark help the firm to strengthen its competitive advantage, putting the firm in a better position to utilize the existing resources (Aw & Batra, 1998; Crepon et al., 1998; Mohnen & Hall, 2013). Thus, it is generally believed that an innovation-orientated firm is likely to have better firm performance than a firm that is not innovation-driven (Baum & Silverman, 2004; Hsu & Ziedonis, 2008; Mann & Sager, 2007).

Despite the numerous findings on the positive association between corporate innovation and firm performance, some studies argue that the high cost of innovation investment may outweigh the benefits because the innovation development process requires a huge amount of capital investment while taking a substantial risk (Chan et al., 2001). Additionally, the process involves firms repeatedly making mistakes and failures, such that the lessons learned can be applied to improve product and service, therefore only firms with sufficient capital and accumulated profit will be able to handle investment failure (Coad et al., 2016). In short, investment in innovation is risky and challenging due to its uncertain outcomes, exacerbating the information asymmetry and conflicts of interest with financers (Freel & Robson, 2004). Consequently, the firm may face financial constraints while engaging in innovation. Thus, it is possible to argue that the characteristic of innovation including high uncertainty, high-risk nature, and high cost of investment may not be beneficial to firm performance.

Economic Policy Uncertainty and Firm Performance

Firms are operating in a dynamic environment, which is constantly influenced by changing decisions of policymakers. Therefore, firms’ decision and firm performance is continuously subjected to the amount of uncertainty of economic policy (Kang & Ratti, 2015). The existing literature documents various conclusions on the effects of EPU such as increases in corporate tax burden (Dang et al., 2019); reduction in investment and debt issuance (Baker et al., 2016); and increases in cost of capital (Drobetz et al., 2018). From a theoretical standpoint, continuous change in policies poses a risk of decreasing firm performance, which leads to increase in cost of finance (Iqbal et al., 2020; Makosa et al., 2021; Waisman et al., 2015). To be more specific, EPU poses a risk toward firm performance which increases firm credit risk (Gilchrist et al., 2014; Ohanian et al., 2013; Pástor & Veronesi, 2013). Study done by Pástor and Veronesi (2013) confirms the statement. Pástor and Veronesi (2013) demonstrate that the predicted risk premium associated with political uncertainty is higher during high EPU. This increase in credit risk impedes firms easy access to external finance and firms generally found more difficulty in getting access to bank loans (Bordo et al., 2016; Gilchrist et al., 2014; Jiang et al., 2022). Additionally, Jiang et al. (2022) found that when EPU is heightened, banks tighten loan approval criteria.

Apart from that, various literature also found links between EPU and the impact on macro-level such as fall in unemployment (Baker et al., 2016). Thus, extant literature suggests that the frequent change in policy creates uncertainty in firm’s operating environment, leading to negative impact on overall firm performance. Given the significant effect of the operating environment, EPU on firm performance, the link between corporate innovation and firm performance under EPU has not yet been extensively explored in the existing studies.

Corporate Innovation and Firm Performance When EPU is High

The increase in EPU means that the economic policy such as monetary and fiscal policy, might change, thereby indicating an increase in risk in the external environment (Pástor & Veronesi, 2013). In this section, we will extend the RBV framework by discussing the theoretical connection of how EPU influences the change in association between corporate innovation and firm performance. The mechanism discussed is via firm financing cost. On one hand, in the presence of EPU, intangible assets or innovation assets would be less value relevant compared to during a normal operating environment (Abdul-Shukor et al., 2008). The first reason is that when the operating environment is uncertain, the firm’s default risk increases especially for firms that rely largely on risky innovation projects and intangible assets. During high EPU, financing innovation and intangible assets tends to be costlier because of the high uncertainty of investment outcomes (Lerner & Hall, 2010). Secondly, innovative firms generally rely on intangible assets. However greater dependence on intangibles distorts firms’ ability to raise capital in the credit market due to low redeployability, higher information asymmetry and uncertain liquidation value inherent in intangibles which restrict their effective use as loan collateral (Holthausen & Watts, 2001; Shleifer & Vishny, 1992; Williamson, 1988). Consequently, lenders demand higher loan spread as compensation for intangible asset, higher recovery risk, and costly due diligence (Mohnen et al., 2008; Nemlioglu & Mallick, 2017). Thus, in the presence of EPU, these characteristics affect firm performance negatively because bankruptcy and financing costs are heightened for firms in high-intangible-intensity industries and for those investing in R&D (Borghesi & Chang, 2020).

On the other hand, Kulatilaka and Perotti (1998) develop a strategic growth options model to show that uncertainty in firm’s operating environment increases the potential gain of the investment project especially when the investment is irreversible such as investment in innovation. When EPU is high, investment in innovation is considered as acquisition of firm’s future growth, which allows the firm to gain competitive advantages over other competitors (Gilchrist et al., 2014). Additionally, Hartman (1972) concludes that innovative firms benefit from an increase in value of a marginal unit of capital during uncertainty periods. Thus, when EPU is high firms with high corporate innovation are able to better expand their existing market share and earn higher profit relative to firms with low corporate innovation which have no growth option (Vo & Le, 2017). Consequently, the growth option model suggests that in the presence of EPU, innovative firms will benefit more in terms of firm performance compared to non-innovative firms.

Methodology

Research Design

To investigate the impact of corporate innovation on firm performance in the presence of EPU, we proposed a conceptual model as shown in Figure 1, as well as executed the following model:

Conceptual framework.

Where i represents each firm, t represents each time period, and

In a regression analysis, it is imperative to control for other factors that may influence firm performance. We include six firm characteristics as control variables in our regression analysis; firm size (natural logarithm of total assets), leverage (total debt/total assets), R&D (R&D/total assets), advertising (advertising expense/total assets), growth (capital expenditures/total assets), profitability (EBITDA/total assets). We also include board variables: board size (natural logarithm of number of directors on the board), independent directors (proportion of independent directors on the board), and female directors (proportion of female directors on the board).

Mindful of possible endogeneity that arises due to simultaneity and reverse causality, it is conceivable that both text-based corporate innovation and firm performance are simultaneously determined by a third variable that is unobservable. If this is the case, the association between text-based corporate innovation and firm performance may be spurious. Thus, we run a fixed-effects analysis, which controls for unobservable firm-specific characteristics that remain constant over time. The regression model includes year fixed-effect and industry fixed-effect to ensure the robustness of the results. Our results are unlikely driven by heterogeneity.

Sample Selection

The original sample with respect to firm characteristics is gathered from COMPUSTAT database, data on directors are from ISS database (Institutional Shareholder Services, formerly RiskMetrics). The financial and utility firms, whose SIC codes range from 6,000 to 6,999 and 4,900 to 4,999 respectively, are excluded as they tend to have financial and accounting characteristics that are unique and different from the others. We obtained the largest sample size possible utilizing data available from COMPUSTAT and ISS database. We addressed the issue of outliers in the sample by excluding firms with Peters and Taylor’s (2017) q less than −.238 at the first percentile and those greater than 9.789 at the 99th percentiles. Using text-based corporate innovation index from Bellstam et al. (2021) which has data from 1990 to 2010, limited our sample to that period. The final sample consists of 2,720 observations from 431 unique firms from 1997 to 2010.

Variable Description

Measuring innovation

Traditionally, scholars often rely on patent activities and R&D expenditure as proxies for innovation (Acharya & Subramanian, 2009; Hsu et al., 2014; Lerner et al., 2011). However, these commonly used proxies pose some serious limitations as they do not fully capture the nature and scope of innovative output (Bellstam et al., 2021). While R&D expenditures measure observable input, it fails to capture the quality of innovation output (Aghion et al., 2013). On the other hand, patent count can only measure innovation output with respect to intellectual properties, so one of the serious problems has been an inability to consider other aspects of innovation output such as a new marketing method, a new organizational method in business practices, workplace organization or new external relations. This is because such innovation aspects of output are not patentable (Moser, 2012).

Due to the shortcoming of the existing corporate innovation proxies, we adopt a novel measure of corporate innovation derived from textual descriptions of firm activities by financial analysts called text-based corporate innovation index developed by Bellstam et al. (2021). This index is constructed by using a textual analysis of analyst reports of S&P500 firms utilizing a topic modeling tool called the Latent Dirichlet Allocation (LDA) method (Blei et al., 2003). It draws content from a common set of topics, or clusters of words related to innovation (e.g., service, system, technology, product, solution) in the text of a large corpus of analyst reports and then measure the level of a firm’s corporate innovation by the intensity with which analysts write about the innovation topic. Thus, this measure is able to capture a broad notion of innovative processes, products, and systems, which cover overall innovation in firms (Bellstam et al., 2021). Bellstam et al. (2021) demonstrates that the text-based corporate innovation index not only strongly correlates with patenting efficiency but also captures innovation activities by firms that do not generate patents. Recently, the textual analysis method had gained popularity and is used by many researchers when conducting empirical research (e.g., Kriebel & Debener, 2019; Mukherjee et al., 2017; Ranta et al., 2021). Thus, we believe that our chosen text-based corporate innovation index is a superior measure of corporate innovation, which can overcome the limitations imposed by the other innovation proxies. An important advantage of the chosen text-based corporate innovation measure is that it can be computed for firms that do not disclose their R&D expenditure. As a robustness check, we found that 1,098 observations out of 2,718 observations (40%) from our sample have R&D expenditure variable equal to zero, indicating no recognition of innovation when using R&D expenditure as an innovation proxy. At the same time, our text-based corporate innovation index is not equal to zero showing that it is able to capture the corporate innovation from the sample firms. For ease of interpretation, the text-based index was standardized to have a mean of 0 and a standard deviation of 1.

Measuring economic policy uncertainty

EPU is uncertainty arising from an inability to predict future economic policies. The examples of events related to EPU are uncertainty about tax regime, trade war and electoral. To proxy for EPU, we use the EPU index constructed by Baker et al. (2016). The EPU index measures the EPU by counting the frequency of articles containing the words in the following trio of the terms: “economic” or “economy”; “uncertain” or “uncertainty”; and one or more of “congress,”“deficit,”“Federal Reserve,”“legislation,”“regulation,” or “White House” from 10 leading US newspapers. Baker et al. (2016) conducted several robustness checks such as human readings of 12,000 newspaper articles, which indicate that the EPU index proxies for movements in policy-related economic uncertainty. In fact, this particular EPU index is especially interesting because it has been used by commercial data providers such as Bloomberg, FRED, Haver and Reuters to meet demands from banks, hedge funds, corporates, and policy makers (Baker et al., 2016). The fact that EPU index has been adopted in various academic studies (e.g., Gulen & Ion, 2015; Shen et al., 2020) and market-use validation in just a short time period suggests that it is a useful measure of EPU in a wide range of circumstances. Finally, the approach of using text search methods in particular by using newspaper archives to measure a variety of outcomes, is growing in a number of studies. Examples include Gentzkow and Shapiro (2010), Hoberg and Phillips (2010), Boudoukh et al. (2013), and Alexopoulos and Cohen (2015). Newspaper-based measures of uncertainty are forward looking as they reflect the real time uncertainty perceived by journalists. For all the reasons discussed above, EPU index appears to be an advantageous measure of EPU.

Measuring firm performance

To measure the firm performance, we employ both accounting-based and market-based measures to ensure the robustness of our empirical results. Although both types of measures provide insight into firm performance, they express different meanings. Theoretically, the accounting-based measures reflect the profitability of the company in a given year, while the market-based measures reflect the expectations of the shareholders concerning the firm’s future performance. Therefore, we use both types of measures to provide a clearer picture of firm performance. The accounting-based methods employed in this study are return on assets (ROA) and earnings before interest and taxes ratio (EBITR). ROA and EBITR are measures often used by scholars to gauge the past operational performance of firms (Anderson & Reeb, 2003; Mehran, 1995). The market-based measure employed in this study is Peters and Taylor’s (2017) q, which reflects how the capital markets value the company. Peters and Taylor’s (2017) q captures firm-level estimates of intangible assets and shows that including intangible capital in the definition of Tobin’s q produces a superior proxy for firm performance (Ayyagari et al., 2020).

Hence, our analysis concentrates on three key indicators of firm performance: they are (a) ROA, (b) EBITR, and (c) Peters and Taylor’s (2017) q. One of the advantages of using ROA is that accounting returns provide information on value-added to the firm from the major corporate decisions, including the firm’s innovation policy (Paul, 1992). Alternatively, EBITR provides an accurate reflection of the efficiency of the firm’s operation as well as the firm’s cash-generating ability. Thus, ROA and EBITR are often used by scholars to gauge the financial and operating performance of the firms (e.g., Anderson & Reeb, 2003; Mehran, 1995). According to Hutchinson and Gul (2004), accounting-based measures reflect the management action-outcome and are preferred over market-based measures when the relationship between corporate governance and firm performance is investigated. The chosen Peters and Taylor’s (2017) q measure is the firm’s market value divided by the sum of its physical and intangible capital stocks. The highlight of this measure is that it includes firm’s externally purchased intangible assets. Although the commonly used proxy of firm market value by researchers in corporate finance literature is Tobin’s q, Peters and Taylor (2017)’s q is proven to be a superior proxy as it includes the intangible assets in the measure, making it better at explaining physical, intangible, and total investment, as well as R&D investment (Peters & Taylor, 2017). Peters and Taylor (2017) emphasize measurement error in intangible capital, and show that properly accounting for intangibles substantially improves the performance of firm performance proxy.

Data Analysis

Although, our fixed-effects analysis helps alleviate concern for the omitted-variable bias, which is one type of endogeneity, the other type of endogeneity is caused by reverse causality. So far we assume that the direction of causality runs from corporate innovation to firm performance. It could be argued, nevertheless, that the direction of causality might be reverse, that is, when EPU is high, firms with good performance have more resources to invest in innovation and thus allow firms to consolidate know-how and have high text-based corporate innovation.

To alleviate endogeneity concerns, we adopt four instrumental variables (IV) analyses. The purpose of running an instrumental variables test is to ensure that our result is not the consequence of possible measurement error, unobservable characteristics omitted in the model, or reverse causality. In particular, we employ four instrumental variable analyses. This method calls for instrumental variables that are exogenous. To be more specific, this method requires instrumental variables that are related to text-based corporate innovation but cannot be correlated with firm performance, except through text-based corporate innovation. The four instrumental variables are (1) industry-average text-based corporate innovation index, (2) industry-mean text-based corporate innovation index, (3) city-average text-based corporate innovation index, and (4) state-average text-based corporate innovation index. The reason for adopting industry-average text-based corporate innovation index and industry-median text-based corporate innovation index as our first and second instrumental variables is that although the performance of a given firm might influence the same firm level of text-based corporate innovation index, it is unlikely to be related to industry-level text-based corporate innovation index. Performance of a given firm may have influence over its own level of text-based corporate innovation index, but it should have little influence, if any, on other firm’s text-based corporate innovation index. Changes in text-based corporate innovation index at the industry level are beyond one firm’s control and are more likely exogenous. This is why industry-level text-based corporate innovation index is likely exogenous and should function as a valid instrument. This approach of using industry-level as instrumental variable is employed by a number of recent studies including John and Knyazeva (2006) and Jiraporn et al. (2012). Exploiting the insight in Jiraporn et al. (2014) and Chintrakarn et al. (2017), the other two instrumental variables selected are based on geographical identification: city-average text-based corporate innovation index and state-average text-based corporate innovation index. We employ the average text-based corporate innovation index of the surrounding firms in the same state and city as our third and fourth instrumental variable. These variables should be a legitimate instrument for two reasons. First, the variable is clearly related to the text-based corporate innovation index of a given firm due to the cluster effect. To elaborate this point, for example when a high concentration of innovative firms are located in a cluster, it is highly likely that firm located in the same area is likely to be innovative as well, vice versa. However, changes in text-based corporate innovation index at the city and state level are beyond one firm’s control and are more likely exogenous. So, it does meet the relevance requirement for an instrumental variable. Second, it plausibly meets the exclusion requirement, that is, it is not directly correlated with firm performance (except through the text-based innovation index of firm). The variation in text-based corporate innovation index across the city and state are unlikely related to firm performance and therefore likely to be exogenous.

Results

Descriptive Results

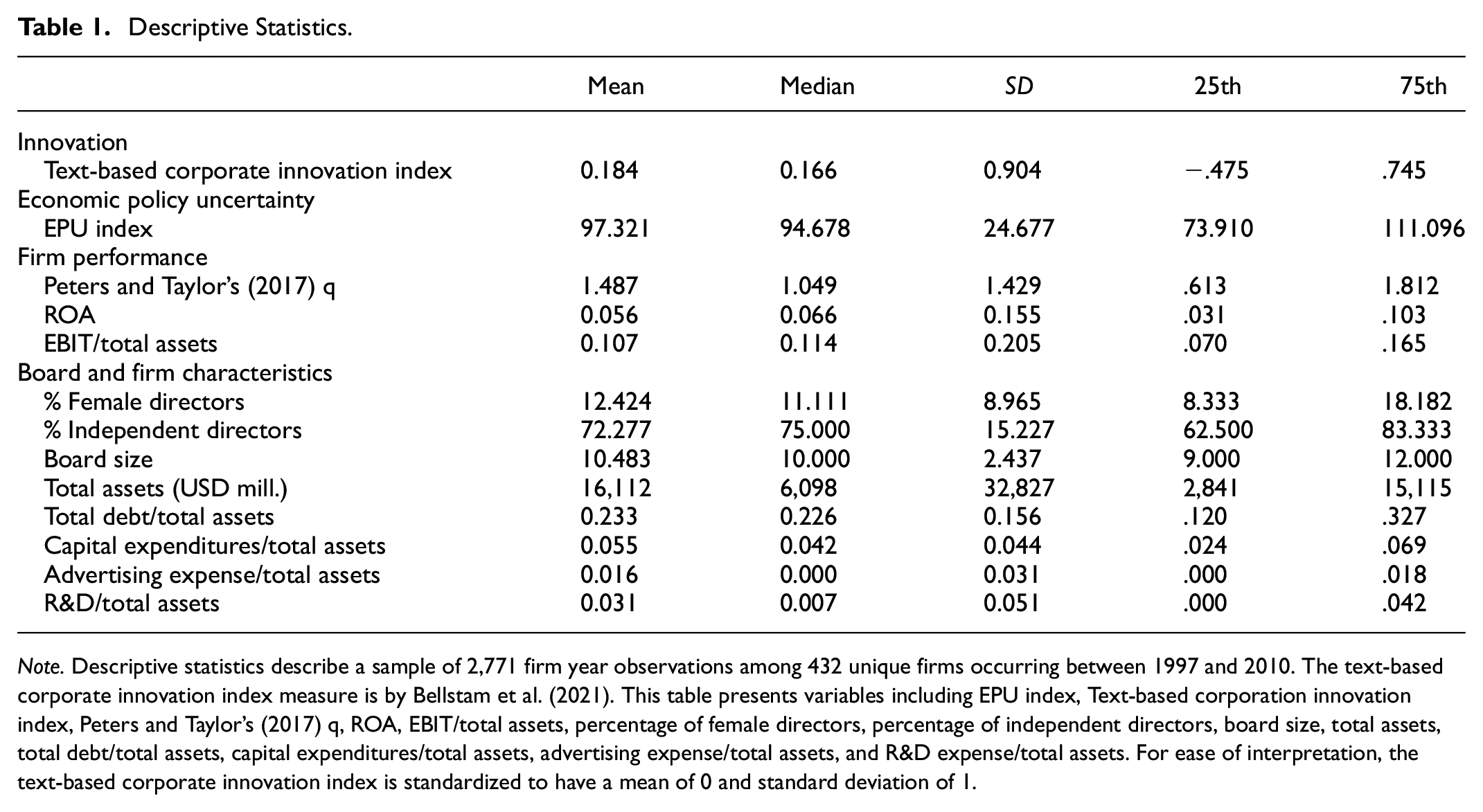

Table 1 shows the descriptive statistics of the variables used in this study. The mean value of the Text-Based Corporate Innovation Index is .184. On average, firms in the sample are large and profitable with the average ROA and EBIT/Total Assets ratio of 5.6% and 10.7% respectively. Peters and Taylor’s (2017) q is employed as a measure for firm value. The average Peters and Taylor’s (2017) q is 1.487. Last, overall observation indicates that the test variables and continuous control variables are mostly normally distributed.

Descriptive Statistics.

Note. Descriptive statistics describe a sample of 2,771 firm year observations among 432 unique firms occurring between 1997 and 2010. The text-based corporate innovation index measure is by Bellstam et al. (2021). This table presents variables including EPU index, Text-based corporation innovation index, Peters and Taylor’s (2017) q, ROA, EBIT/total assets, percentage of female directors, percentage of independent directors, board size, total assets, total debt/total assets, capital expenditures/total assets, advertising expense/total assets, and R&D expense/total assets. For ease of interpretation, the text-based corporate innovation index is standardized to have a mean of 0 and standard deviation of 1.

Analysis of Regression Results

Table 2 shows the baseline regression. In Model 1, we use Peters and Taylor’s (2017) q as the dependent variable. In Model 2, we replace Peters and Taylor’s (2017) q with ROA. Finally, in Model 3, we use EBIT/Total Assets as dependent variables. The independent variable of interest is the interaction term between the Text-based corporate innovation index and EPU index. As expected, in all models, the coefficients of the text-based corporate innovation index are positive and significant at a 1% confidence level, implying that corporate innovation has a positive impact on firm performance. The result is in line with most prior studies that find a positive significant relationship between corporate innovation and firm performance (e.g., Armstrong et al., 2006; Branch, 1974; Eberhart et al., 2004; Sougiannis, 1994). Our focus, however, is on the interaction term between text-based corporate innovation index and EPU index. This interaction term shows the effect of corporate innovation on firm performance when an exogenous operating environment factor is included, EPU. The coefficients of the interaction term for all models are negative and significant at a 1% confidence level. This suggests that in times of greater uncertainty, it is more difficult to value corporate innovation. Therefore, the favorable effect of corporate innovation on firm value is reduced substantially. A possible explanation for this might be the significant increase in the cost of finance for the innovative firm due to its possession of intangible assets when EPU is high. This is consistent with the previous related literature that found a negative effect of intangible assets on firm performance when EPU is high (Borghesi & Chang, 2020; Mohnen et al., 2008; Nemlioglu & Mallick, 2017).

Fixed-Effect Regression Analysis.

Note. Standard errors in parentheses. This table presents fixed-effect regressions in three models. The dependent variables in Model 1, 2, and 3 are Peters and Taylor’s (2017) q, ROA and EBITR, respectively. All models control for percentage of female directors, percentage of independent directors, board size, total assets, total debt/total assets, capital expenditures/total assets, advertising expense/total assets, R&D expense/total assets, and include year fixed effects. For ease of interpretation, the text-based corporate innovation index is standardized to have a mean of 0 and standard deviation of 1. Stars *, **, and *** indicate statistical significance at the 10%, 5%, and 1% level, respectively.

p < .1. **p < .05. ***p < .01.

In terms of economic magnitude, the coefficient of the interaction term in Model 1 is −.005 and significant at a 1% confidence level. According to Model 1, the effect of corporate innovation on firm performance measure by Peters and Taylor’s (2017) q is .825 − .005*EPU index. Thus, when firms experience an average EPU level at 97, the effect of corporate innovation on firm Peters and Taylor’s (2017) q is .34. However, in time of greater EPU when the 75th percentile is at 111, the effect of corporate innovation on Peters and Taylor’s (2017) q is lower at .27. However, when EPU at the 25th percentile is at 73, the effect of corporate innovation on Peters and Taylor’s (2017) q is higher at .46. Therefore, the negative coefficient on the interaction term implies that the positive effect of corporate innovation is reduced as EPU increases. For the interaction terms in Models 2 and 3, we found similar evidence that corporate innovation plays an important role in affecting firm performance in terms of accounting measures, ROA, and EBIT/Total Assets. The coefficient of the interaction term in Models 2 and 3 are both at −.01 and significant at a 1% confidence level. The coefficient of the text-based corporate innovation index in Models 2 and 3 are .052 and .087, respectively. This implies that the favorable effect is reduced by the interaction effect, in time of greater EPU.

Robustness Test

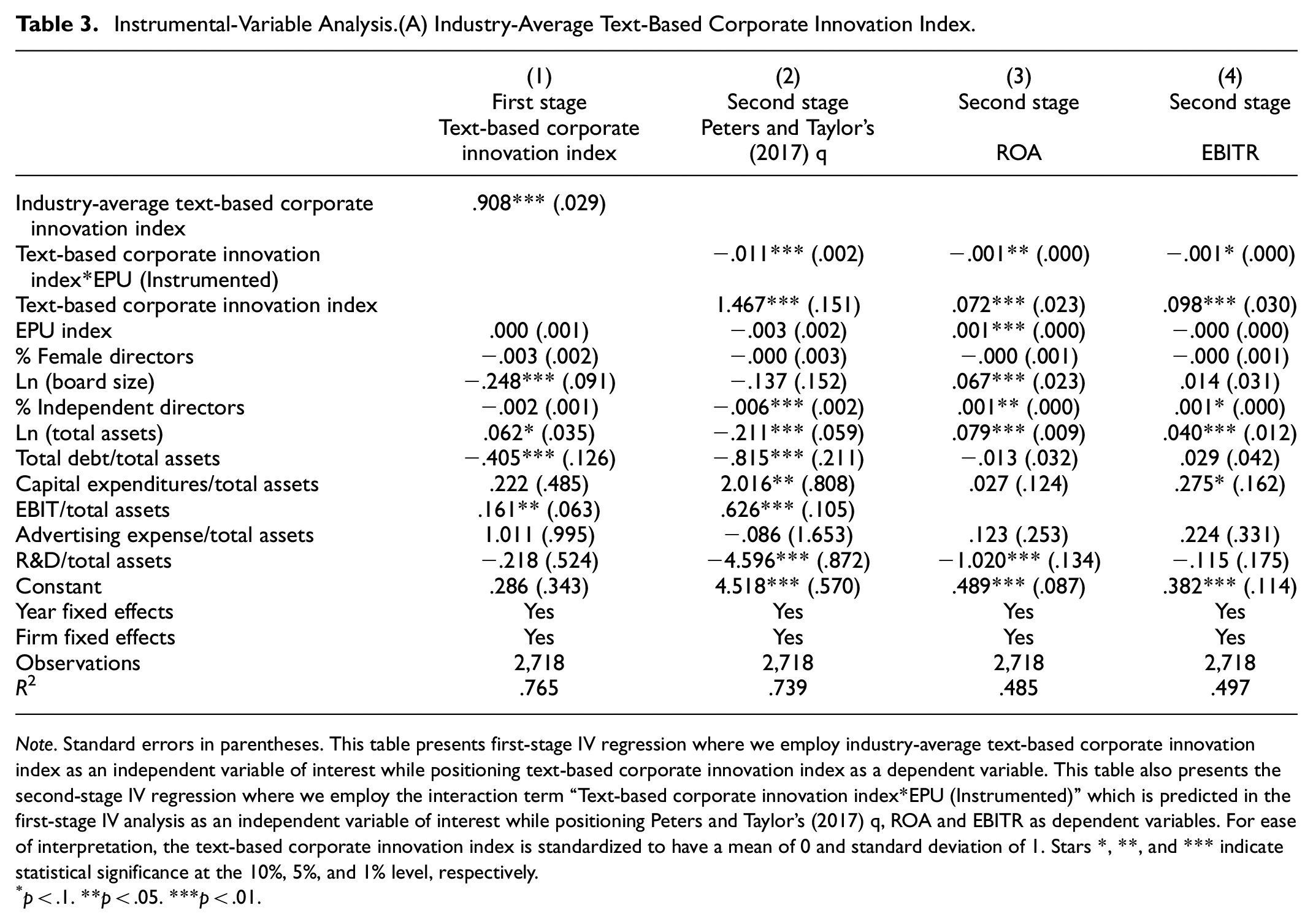

The first instrumental variable used is the industry-average text-based corporate innovation index. Although the firm performance of a given firm might influence the level of firm innovation, it is unlikely to be related to industry-level innovation. This is why the industry-average text-based corporate innovation index should function as a valid instrument. It is related to firm-level of corporate innovation but unlikely related to firm performance. The results of the two-stage least square (2SLS) regression analysis are shown in Table 3A. Model 1 is the first-stage regression, where the dependent variable is text-based corporate innovation index. The coefficient of industry-average text-based corporate innovation index is positive and significant, indicating that the industry-level innovation significantly explains firm-level innovation, consistent with our expectations. Model 2 is the second-stage regression, where we regress the instrumented value of the interaction term between text-based corporate innovation index and EPU index on Peters and Taylor’s (2017) q. The coefficient of the instrumented interaction term is negative and significant at a 1% confidence level. When EPU is greater it leads to less favorable effect of corporate innovation on Peters and Taylor’s (2017) q, which is firm performance. Because the two SLS analysis helps alleviate the endogeneity bias, our results do not seem to be driven by endogeneity and therefore appear to be robust. Model 3 and Model 4 are the second stage regressions where we replaced the dependent variables with ROA and EBITR respectively. The coefficients of the instrumented interaction term in Model 3 and Model 4 are again negative and significant at 5% and 10% confidence level, respectively. Thus, reverse causality is unlikely. Apart from the industry-average text-based corporation innovation index, we execute another two-stage least square (two SLS) regression based on the concept using industry-mean texted-based corporate innovation index as our second instrumental variable. Industry-mean texted-based corporate innovation index should function as a valid instrumental variable because the performance of a given firm might influence the level of firm innovation, but it is unlikely to be related to industry-level innovation. Table 3B shows the results of the second instrumental variable analysis, industry median text-based corporate innovation index. The first stage regression shows that the coefficient of industry median text-based corporate innovation index is positive and significant at a 1% confidence level, indicating that industry-mean text-based corporate innovation index substantially explains firm-level corporate innovation. The coefficients of the instrumented interaction terms in Models 2, 3, and 4 are negative and significant at 1% confidence level.

Instrumental-Variable Analysis.(A) Industry-Average Text-Based Corporate Innovation Index.

Note. Standard errors in parentheses. This table presents first-stage IV regression where we employ industry-average text-based corporate innovation index as an independent variable of interest while positioning text-based corporate innovation index as a dependent variable. This table also presents the second-stage IV regression where we employ the interaction term “Text-based corporate innovation index*EPU (Instrumented)” which is predicted in the first-stage IV analysis as an independent variable of interest while positioning Peters and Taylor’s (2017) q, ROA and EBITR as dependent variables. For ease of interpretation, the text-based corporate innovation index is standardized to have a mean of 0 and standard deviation of 1. Stars *, **, and *** indicate statistical significance at the 10%, 5%, and 1% level, respectively.

p < .1. **p < .05. ***p < .01.

(B) Industry Median Text-Based Corporate Innovation Index.

Note. Standard errors in parentheses. This table presents first-stage IV regression where we employ industry-median text-based corporate innovation index as an independent variable of interest while positioning text-based corporate innovation index as a dependent variable. This table also presents the second-stage IV regression where we employ the interaction term “text-based corporate innovation index*EPU (Instrumented)” which is predicted in the first-stage IV analysis as an independent variable of interest while positioning Peters and Taylor’s (2017) q, ROA, and EBITR as dependent variables. For ease of interpretation, the text-based corporate innovation index is standardized to have a mean of 0 and standard deviation of 1. Stars *, **, and *** indicate statistical significance at the 10%, 5%, and 1% level, respectively.

p < .1. **p < .05. ***p < .01.

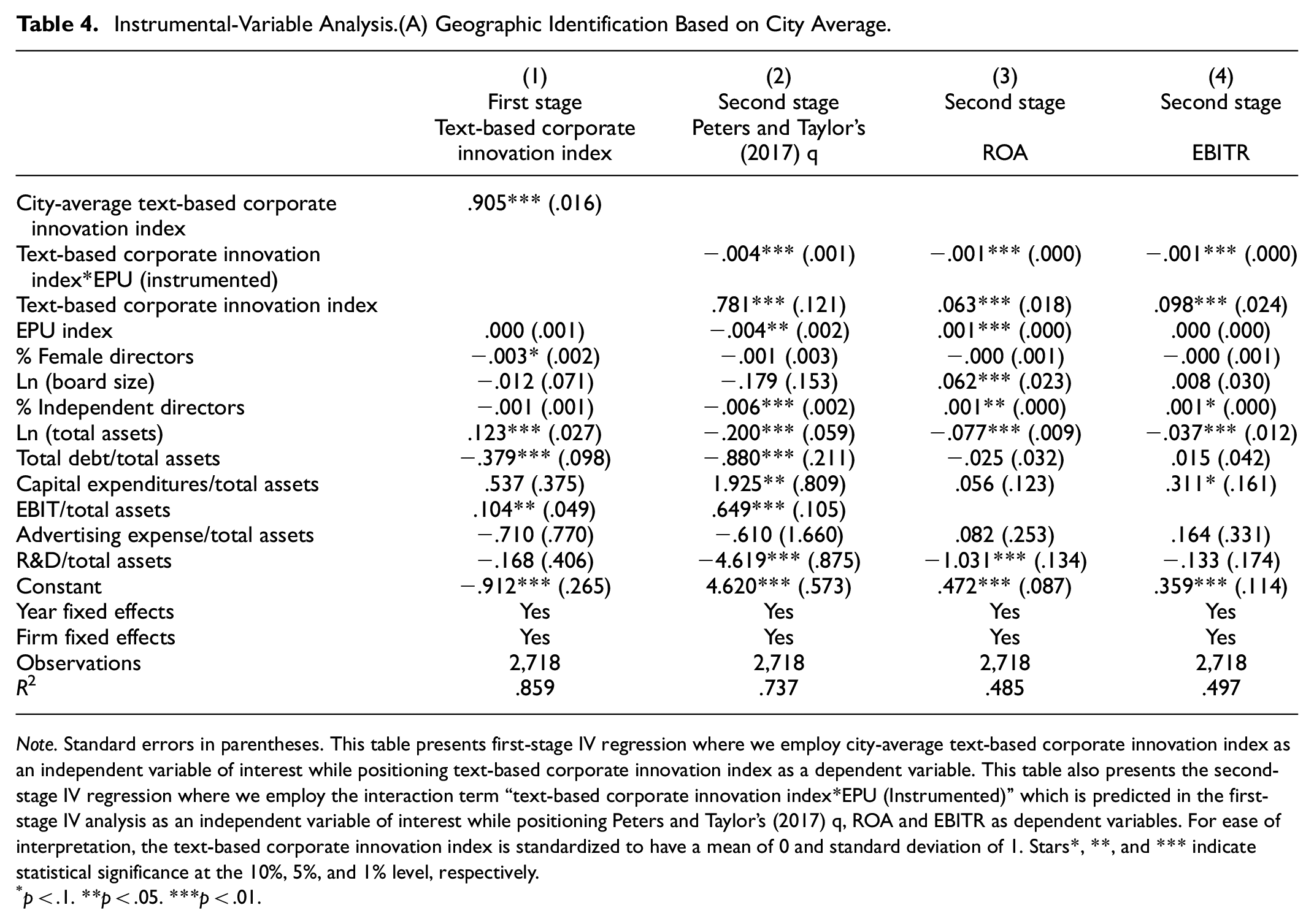

To further confirm the results, we employ two additional instrumental variables analyses. The third and fourth instrumental variables chosen are city-average texted-based corporate innovation index and state-average text-based corporate innovation index. Following prior literature, we rely on geographic identification and use the average text-based corporate innovation of firms located in the same city and state (Withisuphakorn & Jiraporn, 2018). The assumption is that firms located in an area that is highly concentrated with innovative firms are likely to engage more in innovation activities. However, the distribution of the firms is likely exogenous and is unlikely related to firm performance. Table 4A shows the result of our third instrumental variable based on the city in which firms are located. Model 1 is the first stage regression where text-based corporate innovation index is the dependent variable. The coefficient of city-average text-based corporate innovation index is positive and highly significant at 1% confidence level, suggesting that it is not a weak instrument. Model 2 is the second stage regression where the dependent variable is Peters and Taylor’s (2017) q, which represents proxy of firm performance. The coefficient of the instrumented interaction term is negative and significant at 1% confidence level. Model 3 and Model 4 are also the second stage where the dependent variables are ROA and EBITR, respectively. Again, instrumented interaction term exhibits significantly negative coefficients. The instrumental variable analysis, which is substantially less vulnerable to endogeneity, confirms that in the time of greater EPU, the favorable effect of corporate innovation on firm performance is reduced substantially. Table 4B shows the instrumental variable analysis using state-average text-based corporate innovation index, which yields consistent results.

Instrumental-Variable Analysis.(A) Geographic Identification Based on City Average.

Note. Standard errors in parentheses. This table presents first-stage IV regression where we employ city-average text-based corporate innovation index as an independent variable of interest while positioning text-based corporate innovation index as a dependent variable. This table also presents the second-stage IV regression where we employ the interaction term “text-based corporate innovation index*EPU (Instrumented)” which is predicted in the first-stage IV analysis as an independent variable of interest while positioning Peters and Taylor’s (2017) q, ROA and EBITR as dependent variables. For ease of interpretation, the text-based corporate innovation index is standardized to have a mean of 0 and standard deviation of 1. Stars*, **, and *** indicate statistical significance at the 10%, 5%, and 1% level, respectively.

p < .1. **p < .05. ***p < .01.

(B) Geographic Identification Based on State Average.

Note. Standard errors in parentheses. This table presents first-stage IV regression where we employ State-average text-based corporate innovation index as an independent variable of interest while positioning text-based corporate innovation index as a dependent variable. This table also presents the second-stage IV regression where we employ the interaction term “Text-Based*EPU (Instrumented)” which is predicted in the first-stage IV analysis as an independent variable of interest while positioning and performance: Peters and Taylor’s (2017) q, ROA and EBIT/Total Assets as dependent variables. For ease of interpretation, the Text-Based innovation measure is standardized to have a mean of 0 and standard deviation of 1. Stars *, **, and *** indicate statistical significance at the 10%, 5%, and 1% level, respectively.

p < .1. **p < .05. ***p < .01.

Consistent with previous studies Mohnen et al. (2008) and Nemlioglu and Mallick (2017), our empirical results reveal that EPU drives up the financing cost of innovation and intangible assets causing the favorable effect of corporate innovation to reduce. A possible explanation is that in times of greater EPU, intangible assets and innovation would be less value-relevant due to the characteristic of high risk, low redeployability, higher information asymmetry and uncertain liquidation value compared to during a normal operating (Holthausen & Watts, 2001; Shleifer & Vishny, 1992; Williamson, 1988). We investigate this possibility by examining the firm-fixed effect regression. An interaction term between the text-based corporate innovation index and the EPU index is included to capture the effect of text-based corporate innovation index on firm performance with varying levels of EPU.

Conclusion

This study contributes to a growing field of research in corporate innovation and economic policy uncertainty. Grasping the concept of resource-based view, many empirical results provide mixed results on association between innovation and firm performance because of inadequate innovation proxies. On one side, existing empirical evidence reveals that innovation enhances firm performance (Awan et al., 2022; Guo & Wang, 2022; Su et al., 2020; YuSheng & Ibrahim, 2020). On the other side, researchers argue that innovation is detrimental to firm performance due to its high cost and high risk (Chan et al., 2001; Coad et al., 2016). Using a novel text-based measure of corporate innovation, we provide evidence that corporate innovation is a valuable resource that spurs firm performance, which is aligned with RBV. Furthermore, we extend the concept of RBV by demonstrating how the effects of corporate innovation on firm performance change in the presence of EPU. We test this by including the interaction term between text-based innovation and EPU index in the regression. We found that the coefficient of the interaction term is negative and significant. Our empirical result is similar to previous related studies (Holthausen & Watts, 2001; Shleifer & Vishny, 1992; Williamson, 1988), which provide evidence for how EPU negatively affects the value of innovation and intangible assets. Our result indicates that, in times of greater EPU, the favorable effect of corporate innovation is reduced substantially. When innovative firms or firms with high intangible assets are faced with EPU, the cost of financing innovation and intangible assets increases. Therefore, our results highlight the importance of the role of operating environment in promoting innovation.

We test the research questions by examining the interaction effects of text-based corporate innovation index and economic policy uncertainty on the U.S. sample firms. In this study, we use the text-based innovation index constructed by Bellstam et al. (2021) and EPU index constructed by Baker et al. (2016). The data on firm characteristics is gathered from COMPUSTAT database, data on directors are from ISS database. In total, we have 2,720 observations from 431 unique firms from 1997 to 2010. We perform several additional robustness tests, including three alternative performance measure and four alternative instrumental variable analyses, and all show that our results are robust.

Implications

Such findings can be beneficial to various stakeholders. First, our findings indicate that the favorable effect of corporate innovation is reduced in the presence of EPU. Corporate innovation is essential for a country’s economic growth and firms’ competitive advantage (Romer, 1986; Solow, 1957). Thus, policymakers should focus on the frequency and intensity of the policy adjustment to maintain the long-term consistency of economic policies in order to create a supportive business environment for firms to innovate. When facing unpredictable events such as Covid-19 or trade war, policymakers should avoid lengthy debates and communicate clearly to the public, the direction of the strategies they are going to endorse. Clear and consistent policies will encourage firms to invest more in innovation.

Secondly, our findings suggest that managers should consider the EPU factor when planning long-term innovation projects. Since innovation projects entail high investment risk, require a huge amount of capital investment and long return period, in the presence of EPU these characteristics can result in firm financing costs increasing (Holthausen & Watts, 2001; Shleifer & Vishny, 1992; Williamson, 1988). Consequently, when EPU rises, innovative firms may encounter financial constraints and cash flow problems during the course of their innovation investment (Freel & Robson, 2004). This is especially serious if the particular innovation project entails high fixed cost to maintain. Thus, managers should conduct annual risk assessment of their innovation projects to ensure that risk and impact of EPU are kept at the optimal level for the firm. Additionally, when innovative firms are undergoing a period of high EPU, managers are advised to take extra precautions in managing cash reserve, and source of finance as well as cash flow. Our results suggest that corporate innovation is most beneficial to firms when operating in a supportive operating environment.

Thirdly, our findings have implications for shareholders. Our paper suggests that in time of EPU, innovative firms may suffer from inferior firm performance compared to non-innovative firms. Thus, according to agency theory, for their personal benefit managers may be motivated to invest in short term project and avoid investing in innovative project. Because of this, in the presence of greater EPU, shareholders should put more effort into monitoring managers to ensure that innovation projects continue to be supported for the optimal benefit of shareholder

Finally, short-term investors should avoid investing in innovative firms when the economy is undergoing EPU. To illustrate this point, investors should be careful about investing in firms that rely heavily on innovation for growth during periods of governmental elections or trade wars. On the other hand, long-term investors are encouraged to invest in innovative firm during high EPU due to the possible undervaluation of the stock price and the opportunity for long-term benefit.

Limitations and Future Research Direction

This study has limitations that lead to room for future research. First, data on text-based innovation index is only available up to 2010. However, despite this limitation, to date, there is no other widely available measure that can better capture corporate innovation. Future research can extend the research to more recent year.

Second, although our findings suggest that innovation is beneficial to performance, while the favorable effect of corporate innovation is reduced in the presence of economic policy uncertainty, the term “economic” is broad and includes various types of events into the measurement. Further research could examine how more specific uncertainty such as geopolitical uncertainty, trade policy uncertainty and Covid-19 pandemic uncertainty affect the value of corporate innovation. Examination of more specific type of uncertainty will help firms to better understand the impact of the dynamic of operating environment on the firm as well as help improve an important research area for academics.

Another limitation of our study is that our results are based on firms conditions in the USA, which present insight for developed countries. Future study could attempt to draw comparison on how the effect of corporate innovation on firm performance changes in the presence of EPU in developing counties. An example is China, which is undergoing through a phase of transitioning, where the influence of EPU on corporate innovation and firm performance may exhibit a different result when compared with those observed for developed countries.

Lastly, since green innovation has been gaining attention from researchers (e.g., Begum et al., 2022), it would be interesting to examine whether different types of innovation could lead to a different impact on firm performance in the presence of EPU. Examples of green innovation include green process innovation and green technology. Such findings will help to narrow down the different types of innovation and help innovative firm to gauge better the impact of EPU of their firm’s performance.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This project is funded by National Research Council of Thailand (NRCT): N42A650683. Part of this research was carried out while Pornsit Jiraporn served as Visiting Professor of Finance at Sasin School of Management, Chulalongkorn University in Bangkok, Thailand.