Abstract

The impact of board gender diversity on corporate social responsibility has attracted considerable attention in recent years. However, the study of the relationship between board gender diversity, corporate social disclosures, and national culture has been scarce. Therefore, in this study, we measured the corporate social disclosures data of multinational corporations (MNCs) from China, Japan, the United Kingdom, and the United States using content analysis. Then, we investigated the relationship between board gender diversity and the corporate social disclosures of MNCs as well as the moderating effect of national culture on that relationship. The results show that (1) board gender diversity positively impacts the corporate social disclosures of MNCs and that (2) masculinity negatively moderates the relationship between board gender diversity and the corporate social disclosures of MNCs. The findings emphasize the importance of board gender diversity in the stakeholder management of the board of directors and how it could be affected by different national cultural environments from the stakeholder theory perspective. This study established a link between board gender diversity, corporate social disclosures, and national culture as well as promoted the development of corporate social responsibility (CSR) disclosure measurement methods. Additionally, our results provide suggestions to policymakers and MNCs in how to effectively adopt board gender diversity to promote CSR in specific national cultural environments.

Keywords

Introduction

Multinational corporations (MNCs) have made great contributions to the growth of the world economy, while the social issues attracted much attention from stakeholders because of their operations. According to United Nations Conference on Trade and Development (UNCTAD, 2021), the majority of world foreign direct investment was contributed by MNCs. MNCs are the most important economic contributors (Porter, 1990), and there is no doubt regarding their contributions. However, the social issues caused during the MNCs’s globalization cannot be ignored, especially in the manufacturing sector, such as child and forced labor issues pertaining to Nike’s sweatshops (Dana, 1997), working condition issues of Apple suppliers (Mark, 2019), and Shell’s indirect civilian killing incidents (Polgreen, 2006). These irresponsible behaviors have let to huge boycotts and strikes worldwide by consumers (Harrison & Scorse, 2010). Therefore, MNCs from the manufacturing sector are faced with greater demands for public supervision and social legitimacy from stakeholders compared with other sectors (Fernandez-Feijoo et al., 2014). Evidently, the social responsibility of MNCs must not be ignored.

Existing literatures have investigated the motives of corporate social responsibility (CSR) from different perspectives (Carroll & Einwiller, 2014; Marano & Kostova, 2016; Peng et al., 2021). From the viewpoint of stakeholder theory, CSR could enhance the relationship between enterprises and stakeholders (Carroll & Einwiller, 2014) and establish a good social image for enterprises through effective information disclosures (Garriga & Melé, 2004). From the institutional theory point of view, CSR is constrained by institutional environments (Marano & Kostova, 2016). Enterprises have to comply with laws and regulations to ensure legitimacy (Matten & Moon, 2008) and gain competitive advantage by synchronizing CSR practices and social values (Marano & Kostova, 2016). Moreover, concerning CSR as the outcome of corporate strategic decision-making (Rao & Tilt, 2016), the impact of corporate governance on CSR has also received much attention. Effective corporate governance not only improves the supervisory function of the board of directors in terms of corporate executive management (Fama & Jensen, 1983; Jo & Harjoto, 2011) but also enhances corporate information transparency (Jizi et al., 2014) and CSR commitment (Enric Ricart et al., 2005). Rao and Tilt (2016) have argued that corporate governance is the key of the board’s CSR decision-making, especially board gender diversity.

Recently, studies on the relationship between board gender diversity and CSR have gradually emerged (Francoeur et al., 2019; Katmon et al., 2019; Peng et al., 2021). The proportion of female directors to total directors on the board describes board gender diversity (Francoeur et al., 2019; Katmon et al., 2019). Existing literatures have shown that the difference between female and male directors in terms of knowledge, experience (Hillman et al., 2007), and ethical behavior (Terjesen et al., 2016) could enhance the board’s focus on less powerful stakeholders (Francoeur et al., 2019). With the increasing attention paid to stakeholders, the board’s stakeholder management level has also improved (Peng et al., 2021). However, the results of previous studies have been inconsistent. The empirical results of Setó-Pamies (2015) and Katmon et al. (2019) show that board gender diversity positively impacts corporate social disclosure. Conversely, several studies have shown the insignificant relationship between board gender diversity and CSR (Bear et al., 2010) as well as the insignificant impacts of board gender diversity on corporate social performance (Boulouta, 2013). This means that the role of board gender diversity in CSR is more complex than the expectations of previous studies and that there may have been other influencing factors.

The relationship between board gender diversity and CSR may be affected by national culture. On the one hand, CSR could be affected by the national culture. Michelon and Parbonetti (2012) considered that CSR disclosure describes the corporate practices in relation to the environment, social issues, and economics. Gray (1988) argued that information disclosure could be affected by national culture worldwide. Therefore, based on the Hofstede’s (1980) concept of national culture dimensions, existing studies have empirically examined the impact of national culture on social performance (Thanetsunthorn, 2015), carbon disclosure (Luo & Tang, 2016), and CSR disclosure (Gallén & Peraita, 2018). On the other hand, existing literatures suggest that the key to board gender diversity for enhancing CSR decision-making is improving the board’s attention on vulnerable stakeholders (Francoeur et al., 2019), which is affected by the social value difference between female and male directors. Meanwhile, the social value of an individual is closely related to national culture (Hofstede et al., 2010). The experience and ethical behavior of female directors may differ under different national culture environments, which may lead to varying impacts of board gender diversity on CSR decision-making. Based on the aforementioned reasons, there may be a potential link between board gender diversity, national culture, and corporate social disclosure.

Therefore, we believe that national culture can moderate the relationship between board gender diversity and corporate social disclosure. However, studies on the relationship between board gender diversity, national culture, and corporate social disclosure are scarce. Thus, this study investigates the corporate social disclosure of 151 MNCs from the Forbes list by using content analysis. Further, it theoretically discusses and empirically tests the relationship between board gender diversity and corporate social disclosure as well as the moderating effect of national culture on the aforementioned relationship. We expect to establish a link between board gender diversity, national culture, and corporate social disclosure and fill the gap in the literature to expand the present understanding of board gender diversity in CSR, especially regarding the judgment differences between female directors in CSR decision-making under the different national cultural environments. Additionally, we intend to enrich the CSR research field and provide suggestions for improving CSR, based on board gender diversity and national culture, for both policymaker and MNCs.

The remaining parts of this article are structured as follows. Section 2 provides the literature review and hypotheses, Section 3 presents the methodology, Section 4 details the empirical results and robustness check, and Section 5 presents our discussion (including results, contributions, limitations, and future research).

Literature Review and Hypotheses

Stakeholder theory explains how groups and individuals influence organizations toward achieving their goals (Freeman, 1984). Freeman (2014) suggested that a shareholder is not merely a consideration for modern corporations. Enterprises should also think about responsibilities toward other stakeholders, including consumers, suppliers, employees, and the community (Freeman, 2014). Deegan (2006) argued that all stakeholders have an equal right to convey their demands and that enterprises should voluntarily disclosure the related information as a response to their moral obligations. Meanwhile, corporate social disclosure is the outcome of a board’s decision-making (Freeman et al., 2010), which is also important in relieving stakeholders pressure (Fernandez-Feijoo et al., 2014). Therefore, with the increased pressure on stakeholders, the demand for non-financial information disclosure from shareholders and executive management has also increased (Fernandez-Feijoo et al., 2014).

From the perspective of stakeholders, corporate social disclosure could be affected by board gender diversity and national culture. On the one hand, the moral cognition differences because of gender differences could affect the board’s stakeholder management. Gilligan (1977) argued that men are more inclined toward power and obligation, whereas women are more inclined to listen and care about others and maintain long-term relationships. This moral cognition difference enhances the focus of female directors on vulnerable stakeholder groups (Francoeur et al., 2019) and reduces workplace injustice tolerance levels (Galbreath, 2011). Moreover, women also have better abilities to respond to social issues than men (Williams, 2003). This result in female directors may willing to supervise corporate social issue and privde diverse opinions in CSR (Post & Byron, 2015; Zahid et al., 2020), which could affect the board’s stakeholder management level (Peng et al., 2021). On the other hand, national culture could affect corporate social disclosure because of varying stakeholder characteristics. Hofstede et al. (2010) argued that national culture directly affects politics, social values, and individual orientation. Under the influence of national culture, stakeholders tend to have different demands based on their differing stakeholder characteristics, leading to varying corporate social disclosures (Gallén & Peraita, 2018; Orij, 2010). Therefore, the following sections will theoretically discuss the relationship between board gender diversity, national culture, and corporate social disclosures from the perspective of stakeholder theory.

Board Gender Diversity and Corporate Social Disclosures

Board gender diversity could improve board’s stakeholder management by enhancing the board’s attention on various stakeholder groups. The enhancement of stakeholder management in organizational decision-making is an ethical requirement, which also helps improve the organization’s competitive advantages (Freeman, 2014). Corporate CSR practices are prescribed by board members (Kaymak & Bektas, 2017), especially board gender diversity (Rao & Tilt, 2016). Female directors are more inclined to bring unique perspectives, experiences, and work styles to the board than male directors (Huse & Grethe Solberg, 2006), which manifests as caring for others (Eagly, 1987), not tolerating of inequality (Galbreath, 2011), and better social orientation (Eagly & Karau, 1991). Furthermore, female directors are likely to pay considerable attention to vulnerable stakeholders, such as the community, consumers, contractors, and employees (Francoeur et al., 2019). A study by Daily and Dalton (2003) argued that stakeholder management could be enhanced by driving directors to meet considerable stakeholder demands, which also made board gender diversity become an advantageous resource of the board to achieve this purpose (Peng et al., 2021). Therefore, Rao and Tilt (2016) argued that board gender diversity is important for enhancing CSR decision-making. With the different values, knowledge, and expertise, which are created by female directors in relation to the board’s decision-making (Mathisen et al., 2013), corporate practices will also be concerned about social issues. Existing studies have also provided similar evidences. Francoeur et al. (2019) investigated the corporate social performance data of U.S. firms, listed on Fortune 500, the results of which show that board gender diversity positively affects corporate social performance, especially supplier performance as well as the community. Katmon et al. (2019) investigated the CSR disclosures data of Malaysian non-financial listed firms; the empirical result show that board gender diversity positively impacts CSR disclosures. Another study also identified the positive association between board gender diversity and greenhouse gas disclosures in the U.K. (Liao et al., 2015). However, few studies have also show that the relationship between board gender diversity and voluntary disclosures (Al-Shammari & Al-Sultan, 2010) and board gender diversity and environmental performance (Birindelli et al., 2019) are insignificant.

Considering that the stakeholder management is the key to improve the board’s CSR decision-making, we follow the arguments of Francoeur et al. (2019) and Rao and Tilt (2016) and assume that female directors could increase attention toward various stakeholder groups in the board’s CSR decision-making, thus enhancing stakeholder concerns in corporate practices and leading to better corporate social disclosures. Therefore, we propose the following hypothesis:

National Culture

The role of board gender diversity in boards’ stakeholder management enhancement may be influenced by national culture. After examining the survey data of IBM employees, Hofstede (1980) introduced the four dimensions concept of national culture (power distance, individualism, masculinity, and uncertainty avoidance) to describe the varying thought sets of people from different cultural environments. Hofstede et al. (2010) argued that societies have different ethical standards and codes of conduct that are determined by national culture dimension differences. These characteristics not only affect individuals’ behavior, communication between superiors and subordinates within the organization, and ethical expectations of the members of a society (Hofstede et al., 2010) but also impact information sharing in decision-making (Rowley & Bae, 2002). Meanwhile, national culture also affects corporate decision-making because of the deferring ethics of managers (Okpara, 2014), autocratic level of the management (Rowley & Bae, 2002), and loyalty of subordinates (Patel et al., 2002). This means that the divergent perspectives brought by female directors and their social value sharing may be affected by national culture dimensions differently, thus influencing the board’s stakeholder management. Consequently, the impact of board gender diversity on corporate social disclosures may be enhanced or weakened by different national culture dimensions. Therefore, we will discuss the possible impact of different national culture dimensions on female directors in improving board’s stakeholder management to explain the moderating effect of national culture on board gender diversity in relation to corporate social disclosures.

Power distance

The positive role of board gender diversity in board’s stakeholder management may be influenced by the high level of power tolerance in high-power distance environments. Power distance explains the degree of tolerance of the less powerful members of society to a power hierarchy and inequality (Hofstede et al., 2010). Hofstede et al. (2010) argued that members of a society characterized by high-power distance believe that inequality caused by power differences is reasonable and that an organization’s members tend to follow their superiors’ arrangement. In such societies, the authority normally cannot be questioned (Weaver, 2001), and the subordinates tend to follow the authority, even when principles are unethical (Okpara, 2014). This may result in a centralized decision-making style, which is controlled by powerful individuals (Hofstede et al., 2010). Therefore, under the influence of high-power distance cultural characteristics, female directors may tend to follow the powerful board members’ decision-making without question, which could weaken the board’s stakeholder management because of fewer challenges from divergent viewpoints of female directors when unethical decision is made.

Conversely, the board’s attention on stakeholders may improve because of board gender diversity in low-power distance environments. The members of low-power distance societies believe that power should be distributed equally, and responsibility sharing is encouraged by the community (Hofstede et al., 2010). Under the influence of low-power distance, stakeholders have strong demands to be treated equally (Gallén & Peraita, 2018), and the authority is also willing to share their decision-making power (Earley, 1999). The relationship between the authority and a subordinate is not about commanding and obeying but tends more toward collaboration and consultation (Hofstede et al., 2010), which not only decentralizes the management style (Hofstede et al., 2010) but also makes the decision-making more decentralized (Dimitratos et al., 2011). This may result in encouraging female director to challenge the unethical behaviors of managers or the board’s CSR decision-making and take advantage of female directors’ divergent viewpoints to enhance the board’s attention on stakeholders. Existing studies have shown that power distance negatively affects managers’ business ethics (Okpara, 2014). Ringov and Zollo (2007) found that power distance negatively impacts corporate social performance. Further, there are other evidences demonstrating that power distance negatively affects greenhouse gas disclosures (Luo & Tang, 2016) and environmental reporting (Gallego-álvarez & Ortas, 2017).

Considering the influence of power distance on CSR decision-making, we follow the arguments of Hofstede et al. (2010) and Dimitratos et al. (2011) to assume that the challenges put forward by female directors to managers or board’s CSR decision-making are encouraged in the low-power distance environment, which could increase the board’s attention on various stakeholder groups and lead to better corporate social disclosures. Thus, we propose the following hypothesis:

Individualism

The collective interests advocated by low-individualism environments may amplify the impacts of board gender diversity on board’s stakeholder management. Individualism emphasizes the difference between the focus of society members concerning individual and collective interests (Hofstede et al., 2010). Hofstede et al. (2010) argued that members of a society with low-individualism characteristics believe that they are willing to dedicate their lifetime to protect their group, which is why they tend to pay more attention on collective interests. In such societies, people demonstrate teamwork and share values for the purpose of collective interests (Griffith et al., 2006) and thus organizations tend to adapt collaborative methods and encourage communication (Mitchell et al., 2000) to reduce internal conflicts between departments (Newburry & Yakova, 2006). This may promote the divergent viewpoints of female directors in CSR decision-making and increase the board’s stakeholder management.

Conversely, the emphasis on individual interests in high-individualism environments may weaken the impact of board gender diversity on the board’s stakeholder management. Hofstede et al. (2010) argued that compared with low-individualism environments, people from high-individualism environments tend to pay more attention to their personal interests and their relatives than collective interests. In such environments, people significantly identify with concept of “I” (Hofstede et al., 2010), which could lead to reduced efficiency in lateral communication within the organization (Dimitratos et al., 2011). Moreover, Westerman et al. (2007) found that decision-making is normally adapted in line with the ethical standards of internal and not external members in high-individualism environments. Therefore, female directors may be more inclined toward the ethical standards of the board’s internal members. Further, the challenges put forward by independent female directors regarding the board’s decisions could be ignored by decision-makers, which may reduce the board’s attention on the various stakeholder groups. Previous studies have indirectly supported this theory. In Italy (an high-individualism environment), corporate decision-making is more focused on the interests of one’s own affiliated group than others (Westerman et al., 2007). Thanetsunthorn (2015) found that individualism negatively affects corporate social performance. The empirical result of Gallén and Peraita (2018) demonstrate that individualism negatively impacts CSR disclosures.

Considering the aforementioned, we follow the arguments of Mitchell et al. (2000), Griffith et al. (2006), and Hofstede et al. (2010) to assume that—in the low-individualism environments—the impacts of board gender diversity on board’s stakeholder management could be enhanced by emphasizing the value of collective interests and encouraging collaboration and communication within the organization. This may lead to increasing corporate social disclosures. Thus, we propose the following hypothesis:

Masculinity

The value of material achievements and desire for success, which are emphasized in high-masculinity environments, could affect the impacts of board gender diversity on board’s stakeholder management. Hofstede et al. (2010) argued that people from high-masculinity environments are keen on competition, heroism, and pursuing high material achievements, making them believe that victory represents success. To achieve success, people normally exhibit strong self-determination that also strengthens managers’ problem-solving skills (Chinta & Capar, 2007). However, the remuneration of managers is normally related to corporate financial performance (Bai & Elyasiani, 2013), which could make them more likely to pursue corporate short-term financial performance rather long-term sustainable development performance. Under the influence of such cultural characteristics, female directors are likely to agree with the manager’s short-term financial performance decisions and reduce the board’s attention on various stakeholder groups. Peng et al. (2012) found that corporate CSR engagement in high-masculinity environments is lower than that of enterprises in low-masculinity environments.

Conversely, members from low-masculinity environments are focused more on quality of life and less on material achievements (Hofstede et al., 2010). Gray (1988) argued that in environments with such a culture, people tend to greatly value society and pay considerable attention to social harmony. The result of this is that managers could less exhibit financial advancement and pay more attention toward improving environmental protection (Luo & Tang, 2022). Corporate decision-making practices also tend to focus highly on environmental protection and community development rather than economic performance (Gallego-álvarez & Ortas, 2017). Therefore, in such an environment, the attention of female directors on stakeholders in the board’s CSR decision-making is likely be enhanced. Existing studies have also provided evidence concerning the negative impact of masculinity on CSR. Ringov and Zollo (2007) reported a negative relationship between masculinity and CSR performance. Gallego-álvarez and Ortas (2017) empirically tested the relationship between national culture and CSR disclosures, showing a negative relationship between masculinity and CSR disclosures.

Considering the different impacts between high- and low-masculinity environments on CSR and management, we follow the arguments of Gray (1988), Hofstede et al. (2010), and Luo and Tang (2016) to assume that—in low-masculinity environments—the impacts of board gender diversity on board’s stakeholder management could be enhanced by placing less value on material achievements, emphasizing social harmony, and reducing concerns in terms of financial advancement. This could improve the corporate social disclosures. Thus, we propose the following hypothesis:

Uncertainty avoidance

The role of board gender diversity on board’s stakeholder management could be affected by the characteristics of conservatism and low tolerance for uncertainty in high-uncertainty avoidance environments. Hofstede et al. (2010) argued that uncertainty avoidance describes how people feel threatened from uncertainties and the degree of concern about future uncertainties. In high-uncertainty avoidance environments, people frequently exhibit high-levels of tension during emergencies (Hofstede et al., 2010). Organizations and individuals tend to adopt a structured approach to relieve tensions, leading to additional conservative social characteristics (Hofstede et al., 2010). In particular, enterprises tend to reduce employees’ tension through structured processes (Garrett et al., 2006) and exhibit low corporate transparency through high secrecy and confidentiality regarding information disclosures (Gray, 1988) to avoid the impacts of uncertainty and ambiguity (Minkov, 2018). Because of this enterprises could hardly adapt to new CSR requirements (Ringov & Zollo, 2007) and may discourage female directors from paying increased attention to the emerging demands of stakeholders.

Conversely, people from low-uncertainty avoidance environments feel less tension and threatened by uncertain situations and exhibit curiosity toward the unknown (Hofstede et al., 2010), which may enhance the board’s stakeholder management. Hofstede et al. (2010) argued that low-uncertainty avoidance environments exhibit strong open social characteristics, where people try their hand at various activities, such as painting and carpentry, by themselves rather than hiring someone else, and they believe that decision-marking is determined by morality. Regarding CSR decision-makings, the ambiguity in CSR strategies could increase through relevant challenges (Setyorini & Ishak, 2012); moreover, the attitudes toward ambiguity are different in high- and low-uncertainty avoidance environments. In high-uncertainty avoidance environments, people resent ambiguity and adapt structured processes to deal with it; in low-uncertainty avoidance environments, people believe that ambiguity could be a necessary condition to stimulate innovation (Hofstede et al., 2010). Because of this differing result, enterprises could easily adapt to new CSR demands and requirements (Ringov & Zollo, 2007), and sustainable development practices could be widely accepted in low-uncertainty avoidance environments (Gallego-álvarez & Ortas, 2017). Therefore, in such environments, female director challenges to management decisions are more likely be recognized by the board’s members, and the board’s attention regarding the emerging demands of stakeholder also improves. Existing studies have shown that uncertainty avoidance negatively impacts corporate environmental proactivity (Calza et al., 2016) and that there is a negative relationship between uncertainty avoidance and CSR (Halkos & Skouloudis, 2017).

Considering the aforementioned, we follow the arguments of Gray (1988), Ringov and Zollo (2007), and Hofstede et al. (2010) to assume that—compared to low-uncertainty avoidance environments—female directors’ attention on various stakeholder groups could be reduced through the characteristics of conservatism in high-uncertainty avoidance environments, especially with emerging stakeholder demands, which may weaken the impacts of board gender diversity on the board’s stakeholder management, leading to a decrease in corporate social disclosures. Thus, we propose the following hypothesis:

Methodology

Sample Design

This study uses MNC samples from four countries: China, Japan, the United Kingdom, and the United States. We screened 151 MNCs from the manufacturing sector based on the Industry Classification for National Economic Activities of China (our sample covers 16 specific industries in the manufacturing sector). These MNCs are listed in the 2019 Forbes Global 2000 list, as illustrated in the industry distribution in Table 1. The four countries were selected to ensure diversity of national cultural characteristics and avoid problems that may be caused because of large deviations from national economic development levels. According to the DataBank of the World Bank, the United States was the largest economy of the world in 2017, followed by China and Japan, whereas the United Kingdom ranked sixth.

Industry Distribution.

According to Table 1, there are 33 samples from the computing and other electronic equipment industry (21.85%), 17 samples from the automobile industry (11.26%), 16 samples from the pharmaceutical and medical equipment industry (10.60%), and 85 samples from 13 other specific industries (56.29%).

Data Collection

In this study, we referred to Hussain et al. (2018) and Cui et al. (2020) to adapt MNCs’ CSR reports, annual reports, and proxy statements (financial years 2017–2018) as data sources of corporate social disclosures of MNCs. Further, we borrowed the measurement methods of van Staden and Hooks (2007) and Cui et al. (2020) to measure the relevant reports using content analysis. For the date of board gender diversity and control variables, we borrowed the approach by Peng et al. (2021) collected from annual reports and proxy statements. For the national culture data, we borrowed the approach by Ringov and Zollo (2007) and Cui et al. (2020) to collect data from Hofstede’s study. Additionally, we performed reliability check on corporate social disclosures results. We spent approximately 1,000 hour for data collection and reliability checks.

Variables of Interest

Board gender diversity

We followed Francoeur et al. (2019) and Katmon et al. (2019) and used the proportion of the number of female directors to the total number of board members to measure board gender diversity (BGD) as the independent variable.

Corporate social disclosures

The dependent variable of this study is the corporate social disclosures of MNCs (SD). We describe corporate social disclosures of MNCs by following the GRI 4.0 structure and the approach by Hussain et al. (2018). Hussain et al. (2018) selected four sub-dimensions (human rights, labor, product responsibility, and societies) to measure corporate social performance. After considering the GRI 4.0 structure, we selected 40 indicators to describe corporate social disclosures of MNCs, with 9, 15, 5, and 11 indicators for human rights, labor, product responsibility, and societies, respectively. Then, we used Cui et al. (2020) and van Staden and Hooks’s (2007) measurement methods to measure the MNCs’ CSR report through content analysis. Moreover, we used van Staden and Hooks’s (2007) multigrade scoring system and evaluation principles, which include “0 to 2” CSR-related regulation indicators and “0 to 4” CSR regulation and performance-related indicators. The standard scores for the “0 to 2” scoring system are “0” for related disclosures, “1” for minimum disclosure, and “2” for detailed disclosures. The standard scores of the “0 to 4” scoring system are based on the “0 to 2” scoring system with “3” and “4” as additional scores. Further, “3” represents “2” score for disclosures with quantitative data, and “4” represents “3” score for disclosures with data comparison (such as data in numbers of years) (see Table 2 for details). Our measurement process has detected quantitative and qualitative data of MNCs’ CSR report through content analysis, which could describe corporate social disclosures of MNCs more comprehensively than only using quantitative or qualitative data.

Example of Scoring Standards for Corporate Social Disclosures of MNCs.

Examples are hypothetical.

The calculation formula of SD is as follows:

After the measurement, we also calculated Krippendorff’s alpha by using online tools (http://dfreelon.org/utils/recalfront/recal2) to ensure the reliability of our measurement method and results. The alpha value of the multigrade scoring system and standard scoring is 0.85 and the reliability value is 0.92. These results are greater than Krippendorff’s (1980) suggestion (0.80). Additionally, we used Boesso and Kumar’s (2007) approach to test the stability of our measured data. After a 1-month data collection, we re-measured the CSR reports from the top 20% MNCs for each country and compared the stability test data with the original data. After calculating Krippendorff’s alpha, the stability result is 0.90, thus passing the stability test.

National culture

We measured national culture based on the same approach as Ringov and Zollo (2007), Khlif et al. (2015), and Cui et al. (2020) by using the measurement scores and four dimensions concept from Hofstede’s (1980) study. Hofstede’s (1980) four dimensions concept of national culture has been assessed as moderator variables in this study, which include power distance (PDI), individualism (IDV), masculinity (MAS), and uncertainty avoidance (UAI).

Control variables

We selected CSR committee (CSRCOM), the Big Four accounting firms (BIG4), profitability (ROA), debt-to-asset ratio (DEBT), and firm size (SIZE) as the control variables. These control variables are selected because of the following reasons. First, Enric Ricart et al. (2005) and Hussain et al. (2018) have reported that there is a positive link between CSR committee and SP. Second, previous study has shown that audit quality influences enterprises’ information disclosures (Harandi & Khanagha, 2013). Third, evidence shows that there is a positive relationship between profitability and social sustainability performance (Hussain et al., 2018). Fourth, leverage (debt-to-asset ratio) also significantly affects CSR disclosures (Lan et al., 2013). Fifth, compared with small-sized enterprises, large enterprises frequently face greater pressure from stakeholder demands, resulting in the enterprises’ better disclosures (Bonsón & Bednárová, 2015; Brammer & Pavelin, 2006). Table 3 presents the measurement of all variables.

Summary of All Variables.

Empirical Results

Descriptive Statistics and Correlation Analysis

Table 4 presents the results of variable statistics and Pearson’s correlation. Column 1 lists the variable names, followed by the descriptive statistics (mean, standard deviation). The remaining columns show the correlation coefficients of the variables.

Variables Statistics and Pearson Correlation. a

Note. This table presents the results of Pearson’s bivariate correlation coefficients. The first variable is corporate social disclosures of MNCs (SD), which is the dependent variable. The correlation results of SD are followed by the independent variables board gender diversity (BGD). Independent variables are followed by the moderator variables (national culture dimensions), which introduced by Hofstede (1980). National culture dimensions variables include power distance (PDI), individualism (IDV), masculinity (MAS) and uncertainty avoidance (UAI). Moderator variables are followed by the control variables. We selected CSR committee (CSRCOM), four largest accounting firm (BIG4), profitability (ROA), debt-to-asset ratio (DEBT), and firm size (SIZE) as control variable.

Mean and standard deviation for all the variables were calculated by original data (except SIZE was processed by natural logarithm), the Pearson correlation was based on the data processed by natural logarithm and winsorized tail reduction (1% and 99% levels), which used in our regression analyses.

, **, and * represent statistical significance at 1%, 5%, and 10%, respectively.

Variable statistics

The average score of the corporate social disclosures of MNCs (SD) is 69.77 (in a scale between 0 and 114), whereas the mean of BGD is 0.164. The average values of the moderator variables are as follows: power distance (PDI) is 54.70, individualism (IDV) is 57.79, masculinity (MAS) is 72.74, and uncertainty avoidance (UAI) is 52.15. Regarding the control variables, the average value of CSRCOM is 0.212 and that of the Big Four as external auditors (BIG4) is 0.874, whereas the average profitability (ROA) is 0.070 and DEBT is 0.605. Average firm size (SIZE) is 10.82 (natural logarithm of total employees).

Pearson’s correlation

Table 4 shows that the correlation coefficients between BGD and SD (.409), IDV and SD (.655), and UAI and SD (.389) are positive at 1% significance level. PDI and SD (−.658) have a negative correlation coefficient at 1% significance level. This means that MNCs with higher board gender diversity also perform better corporate social disclosures and that different national culture dimensions can have varying impacts on corporate social disclosures of MNCs. The correlation coefficients between CSRCOM and SD (.221), BIG4 and SD (.460), and SIZE and SD (.226) are also positive at 1% significance level. This indicates that the MNCs, which established a CSR committee, that hire the Big Four as external auditors or large firms also perform better corporate social disclosures. National culture dimensions and the control variables have positive and negative correlation coefficients at different significance levels—that is, these variables affect each other differently. Moreover, we observed that the correlation coefficients between PDI and IDV (.989) and UAI and MAS (.866) are extremely high. These results are higher than Gujarati’s (1995) suggested standard (lower than 0.8) to avoid multicollinearity. Eisend et al. (2016) and Aggarwal and Goodell (2018) also reported similar results. This phenomenon may be related to the interaction between national cultural dimensions (Hofstede et al., 2010). To avoid multicollinearity, we borrowed the approach from Eisend et al. (2016) and included only one national culture dimension in one model. Additionally, we calculated variance inflation factors (VIFs) of all variables for each model to check the multicollinearity issue. The results show that the highest VIF for all models is 2.67, the lowest VIF is 1.06, and the mean of VIF is between 1.09 and 1.58. Therefore, our regression models have no multicollinearity issues (see Table 5 for details).

Variance Inflation Factors (VIFs) of Each Model.

Multivariate Regression Results

In this study, Stata 13 was applied to empirically test the hypotheses. Table 6 shows the multivariate regression results. Model 1 reports the regression of the dependent variable (SD) with control variables. Model 2 reports the impact of BGD on SD with control variables. Model 3 addresses the impact of BGD on SD with the interaction term PDI * BGD, moderator variable PDI, and control variables. Models 4 to 6 illustrate the regression of BGD on SD with of the remaining interaction terms (IDV * BGD, MAS * BGD, and UAI * BGD), moderator variables (IDV, MAS, and UAI), and control variables. The empirical test in this study has two parts, as explained below.

Regression Results of Board Gender Diversity and Corporate Social Disclosures of MNCs (with Interaction Terms).

, **, and * represent statistical significance at 1%, 5%, and 10% levels, respectively.

Board gender diversity and corporate social disclosures of MNCs

The first part of the empirical test evaluates the relationship between board gender diversity and corporate social disclosures of MNCs. Table 6 shows that BGD is positively related to SD at 1% significance level in Model 2—that is, board gender diversity could enhance corporate social disclosures of MNCs. Further, existing studies have presented similarly finding, including the positive relationship between board gender diversity and corporate social performance in the U.S. (Francoeur et al., 2019) and the positive impacts of board gender diversity on CSR disclosures in Malaysia (Katmon et al., 2019). This result supported the argument that female directors are more focused on various stakeholder groups (Francoeur et al., 2019) and confirmed that board gender diversity could improve corporate social disclosures of MNCs by enhancing the board’s stakeholder management, which is consistent with our hypothesis. Thus, H1 is supported.

Moderating effect of national culture

The second part of the empirical test evaluates the moderating effect of PDI (Model 3), IDV (Model 4), MAS (Model 5), and UAI (Model 6). Figures 1 to 4 show the interaction plots for the moderating effect of national culture.

Interaction plot for the moderating effect of PDI on the relationship between board gender diversity and corporate social disclosures of MNCs.

Interaction plot for the moderating effect of IDV on the relationship between board gender diversity and corporate social disclosures of MNCs.

Interaction plot for the moderating effect of MAS on the relationship between board gender diversity and corporate social disclosures of MNCs.

Interaction plot for the moderating effect of UAI on the relationship between board gender diversity and corporate social disclosures of MNCs.

Model 3 reports the results of BGD and shows that the interaction term PDI * BGD is insignificant, indicating that power distance does not moderate the relationship between board gender diversity and corporate social disclosures of MNCs. Moreover, Figure 1 shows the interaction plots for the moderating effect of PDI, where the slopes between two lines have no significant difference (high- and low-power distance). This also indicates that power distance may have no moderating effect. Regarding the relationship between power distance and CSR, the empirical result of Gallén and Peraita (2018) demonstrated that in higher GDP per capita countries, the impacts of power distance and CSR disclosures are insignificant. Additionally, Halkos and Skouloudis (2017) found that there is an insignificant relationship between power distance and CSR. These results are similar to ours. Our empirical results clarify that the positive role of board gender diversity in improving the board’s stakeholder management is not significantly affected by power distance, which is inconsistent with our hypothesis. Thus, considering the regression result (Model 3) and interaction plots (Figure 1), H2a is not supported.

Model 4 shows that the result of BGD and the interaction term IDV * BGD is not significant, which means that individualism does not moderate the relationship between board gender diversity and corporate social disclosures of MNCs. Additionally, Figure 2 displays the interaction plots of IDV and indicates that the slopes between two lines (high-individualism and low-individualism) are approximately the same, which also show the same result as our regression result. Likewise, previous studies have also shown that the relationship between individualism and CSR performance (Ringov & Zollo, 2007), individualism and environmental reporting (Gallego-álvarez & Ortas, 2017), and individualism and CSR disclosures of lower GDP per capita countries (Gallén & Peraita, 2018) are insignificant. Our empirical results indicate that the positive role of board gender diversity in improving the board’s stakeholder management in high- or low-individualism environments are not significantly different, which inconsistent with our hypothesis. Thus, considering the regression result (Model 4) and the interaction plots (Figure 2), H2b is not supported.

Model 5 shows the positive correlation between BGD and SD, at 5% significance level, and that the interaction term MAS * BGD negatively impacts SD, at 5% significance level, which means that masculinity negatively moderates the relationship between board gender diversity and corporate social disclosures of MNCs. Moreover, Figure 3 shows the interaction plots for the moderating effect of MAS, where the line of high-masculinity decreases as BGD increases. Meanwhile, the line of low-masculinity increases as BGD increases. The interaction plots indicates the same result as our regression, which supports the evidence that masculinity negatively impacts CSR performance (Ringov & Zollo, 2007) and CSR disclosures (Gallén & Peraita, 2018). This result also indirectly supports the argument that enterprises are likely to adopt green policies (Wang et al., 2021) and that managers could be more engaged with non-financial corporate practices (such as climate change) in low-masculinity environments (Luo & Tang, 2022). Our empirical results indicate that in the low-masculinity environments, the positive role of board gender diversity in improving the board’s stakeholder management could be enhanced; this could increase the corporate social disclosures of MNCs, which is consistent with our hypothesis. Therefore, considering the regression result (Model 5) and the interaction plots (Figure 3), H2c is supported.

Model 6 indicates that the result of BGD and the interaction term UAI * BGD are not significant, meaning that uncertainty avoidance does not moderate the relationship between board gender diversity and corporate social disclosures of MNCs. Additionally, Figure 4 shows the interaction plots for the moderating effect of UAI, where the slopes between two lines (high- and low-uncertainty avoidance) are not significantly different. The results of regression in Model 6 and the interaction plots are the same. Similarly, existing studies have found an insignificant relationship between uncertainty avoidance and CSR performance (Ringov & Zollo, 2007). Orij (2010) reported an insignificant relationship between uncertainty avoidance and CSR disclosures. Our empirical results indicate that the difference in terms of the positive role of board gender diversity in improving the board’s stakeholder management between high- and low-uncertainty avoidance environments is insignificant, which is inconsistent with our hypothesis. Additionally, this is also inconsistent the argument that information disclosures in uncertainty avoidance environments exhibit high secrecy and conservatism (Gray, 1988). Considering the regression result (Model 6) and the interaction plots (Figure 4), H2d is not supported.

Robustness Check

We used an alternative corporate social disclosure measurement to test the robustness of our results. We used the social score from Thomson Ruters’s ASSET4 to measure corporate social disclosures. This is because the ASSET4 database has been widely used in CSR disclosure studies (Cheng et al., 2014; Shaukat et al., 2016). After screening the database, we found 100 matching samples. Then, we used the social score of these 100 samples and applied the same multivariate regression models for the robustness check.

Table 7 displays the result of the robustness check. In Model 2, BGD is positively related to SD at 5% significance level, whereas in Model 5, BGD is positively related to SD at 1% significance level, and the interaction term MAS * BGD is negatively related to SD at 1% significance level. These results are similar to our empirical results. Therefore, H1 and H2c passed the robustness checks. In Model 5, BGD is positively related to SD at 1% significance level, and the interaction term UAI * BGD is negatively related to SD at 1% significance level, which is inconsistent with our empirical results.

Regression Results of Board Gender Diversity and Asset4’s Social Score (with Interaction Terms).

, **, and * represent statistical significance at 1%, 5%, and 10% levels, respectively.

Discussion

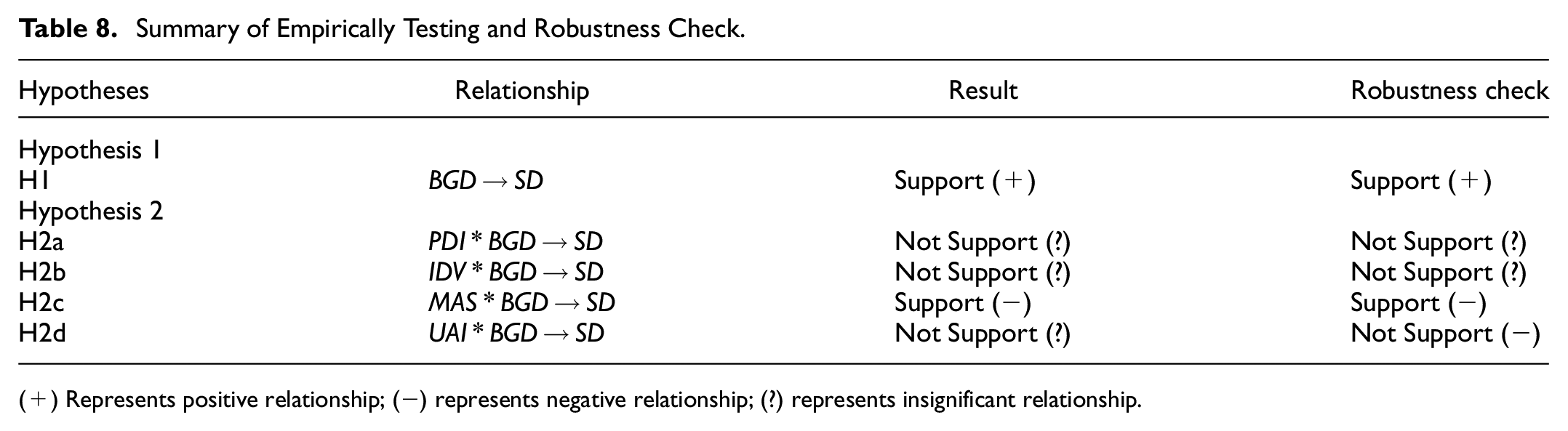

Recently, the importance of board gender diversity in CSR issues has received much attention. The existing literatures have shown that the moral cognition is affected by national cultural (Hofstede et al., 2010), and the moral cognition difference between male and female directors is the key to increase the board’s attention to stakeholders, which could effectively enhance CSR (Francoeur et al., 2019). Therefore, we assumed that board gender diversity could improve the corporate social disclosures of MNCs by enhancing the stakeholder management of the board’s CSR decision-making. Meanwhile, the impacts are likely to vary under the different national culture environments. Thus, we theoretically discussed and empirically tested the relationship between board gender diversity and corporate social disclosures of MNCs as well as the moderating effect of national culture on that relationship (see Table 8 for the results’ summary).

Summary of Empirically Testing and Robustness Check.

(+) Represents positive relationship; (−) represents negative relationship; (?) represents insignificant relationship.

After the investigation, we discovered some interesting findings. First, board gender diversity effectively enhances the corporate social disclosures of MNCs (H1), which supports the argument that board gender diversity is the key to improve CSR decision-making (Rao & Tilt, 2016) and that female directors are more concerned about vulnerable stakeholders (Francoeur et al., 2019). This result reveals that board gender diversity could promote the board’s attention on various stakeholder groups in CSR decision-making, leading to an increase in corporate social disclosures of MNCs.

Second, masculinity negatively moderates the relationship between board gender diversity and the corporate social disclosures of MNCs (H2c). This result confirms the arguments that in low-masculinity environments, there is a enhancing of social value in social harmony (Gray, 1988) and less material achievement (Hofstede et al., 2010), which could lead managers to focus less on financial advancement (Luo & Tang, 2016). The moderating effect of masculinity indicates that in the low-masculinity environments, female directors are more likely to be recognized by the board and managers when they are promoting the board’s attention on various stakeholder groups in CSR decision-making. This could effectively improve the board’s stakeholder management and result in better corporate social disclosure of MNCs.

Third, the moderating effect of power distance is insignificant (H2a). This does not supports the argument that in the high-power distance environments, organization exhibit centralized management styles and that decision-making (Hofstede et al., 2010) may negatively impact corporate social performance (Ringov & Zollo, 2007). This may be because of the differences in research methods and control variables (Ho et al., 2012) or that the unquestionable authority in high-power distance environments (Weaver, 2001) make the board’s CSR decision-making more efficient, when the authority is inclined toward CSR. Additionally, the moderating effect of individualism is also insignificant (H2b), which does not support the argument that collaboration and communication encouragement (Mitchell et al., 2000) and tendency toward collective interests in low-individualism environments (Hofstede et al., 2010) could enhance the board’s stakeholder management. This may because in the high-individualism environments, the demands of stakeholder is encouraged (Peng et al., 2012), which potentially has the possibility to force enterprises to increase corporate social disclosures for the purposes of legitimacy. This may the reason to behind these results.

Finally, our empirical results show that the moderating effect of uncertainty avoidance is insignificant (H2c). Our empirical results neither consistent with the argument that voluntary information disclosures exhibit the characteristics of secrecy and conservatism in high-uncertainty avoidance environments (Gray, 1988), nor the argument that corporate adaption of new CSR requirements become more difficulty in such environments (Ringov & Zollo, 2007). This may be because even the adaption issue exisits; however, the structured processes (Garrett et al., 2006) and tendency to follow rules (Hofstede et al., 2010) may lead the enterprise to comply with relevant standards for corporate social disclosures. Meanwhile, under the influence of low-uncertainty avoidance, enterprises could easily adapt to new CSR demands (Ringov & Zollo, 2007), which may also enhance corporate social disclosures. Therefore, the corporate social disclosures of high- and low-uncertainty avoidance environments may have different motivations for disclosures. Moreover, the robustness check shows that the moderating effect of uncertainty avoidance is significantly negative. This may because the subtle difference of measurement methods between ASSET4 and this study. Our measurement method uses multigrade scoring system to measure CSR reports using content analysis, which could more clearly identify the difference between corporate CSR regulations and CSR practices than ASSET4. Therefore, the moderating effect of uncertainty avoidance is not significant in our empirical results. Further investegation is needed.

This study has the following contributions:

Theoretically, our study establishes the link between board gender diversity, national culture, and corporate social disclosures from the perspective of stakeholder theory and promotes the disclosures measurement method. We emphasized the importance of board gender diversity in enhancing board’s stakeholder management by improving the board’s attention toward various stakeholder groups. With the increase in attention in CSR decision-making, corporate social disclosures also increase. Further, this study reveals that the impact of board gender diversity on board’s stakeholder management could be affected by the differences in power tolerance, collective interest, recognition of material achievements, and adoption of new demands in different national culture environments. These findings contribute to the CSR and corporate governance research field and fill the gap in the literature on the relationship between board gender diversity, national culture, and corporate social disclosures. Finally, our measurement method more comprehensively describes corporate practices in social responsibility than previous studies through a multigrade scoring system, which promotes the development of disclosures measurement methods in the CSR field.

Practically, our findings provide suggestions to policymakers and MNCs. For the policymakers, the importance of board gender diversity in improving board’s stakeholder management and national culture should be reinforced. Policymakers should adopt relevant corporate governance laws and regulations to improve the proportion of female members in the board of directors to achieve the purpose of increasing the concerns of enterprises on various stakeholder groups as well as promote the development of CSR. Moreover, policymakers also need to consider the potential impacts of local national culture environments on female directors in improving the board’s stakeholder management to maximize the efficiency of governance tools. For the MNCs, we suggest they consider the role of board gender diversity in the board’s CSR decision-making and the influence that national culture has on it. MNCs should take board gender diversity as an advantage in corporate governance mechanism to challenge the conventional thinking of CSR decision-making, which could enhance the board’s CSR concerns and the response of various stakeholder demands. This could improve the MNCs’ social recognition and corporate reputation. Additionally, based on the characteristics of cultural environment, MNCs also need to adjust the corporate governance structure (board gender diversity) in host countries, which will help to understand and meet the demands of stakeholders.

The limitation of this study and prospects for future studies are as follows. The limitation of this study is its small sample size. The reason we manually measure CSR reports of sample MNCs using content analysis is to comprehensively describe CSR practices. Because of this, data collection was more difficult than using secondary data. Consequently, our data collection and data reliability checks amounted to approximately 1,000 hour. Therefore, we will try our best to expand the sample size in the future research. Moreover, we found some unexpected results in empirical tests. After the discussion, we believe that the insignificant moderating effect may be related to the motivation of CSR in different cultural environments. Thus, the additional consideration of CSR motivation in different cultural environments should be added into our regression model to further investigate the impact of national culture on the relationship between board gender diversity and the corporate social disclosures of MNCs from different motivational perspectives.

Footnotes

Acknowledgements

The authors gratefully acknowledge the helpful comments and suggestions of the editor and anonymous reviewers. The authors also gratefully appreciate the contributions of Shanshan Li—happy birthday.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets used and/or analyzed during the current study are available from the corresponding author on reasonable request.