Abstract

This study aims to investigate the potential interaction between leadership and the internal control structure and determine whether this interaction can benefit emerging market businesses by increasing the effectiveness of their internal controls. Drawing upon the cognitive consistency and expectancy theories, this study develops and tests a mediated moderation model to examine how leadership consistency and quality can be integrated to regulate the effectiveness of internal control systems toward enhancing firm performance. The partial least squares structural equation modeling (PLS-SEM) results from survey data from 206 Vietnamese firms indicated the following: (a) internal control effectiveness mediates the effect of the internal control structure on firm performance; (b) leadership consistency positively moderates the impact of the internal control structure on internal control effectiveness; and (c) the moderating effect of leadership consistency is strengthened with a higher level of leadership quality. These findings lead to several theoretical and practical implications.

Keywords

Introduction

The waves of globalization and international competition have emphasized the importance of corporate governance in both developed and developing economies. However, poor corporate governance remains a significant problem that firms in emerging markets face (Puni & Anlesinya, 2020). As a result, these firms are under pressure to leverage their internal control system, which is an essential pillar of corporate governance (Aziz, 2013). As a result of this challenge, interest in the various roles of internal control systems in business operations is growing in the emerging market context, including preventing law violation (Le et al., 2021), promoting innovation capability (Chan et al., 2021; Li et al., 2019), and lowering equity capital and agency costs (Khlif et al., 2019; Zhang et al., 2022). In this context, many recent studies have been conducted to explore the internal and external factors that are related to the effectiveness of internal control, including corporate culture (Shu et al., 2018), the characteristics of audit and market competition (Kim & Kim, 2017), and the separation of the roles of the board chair and chief executive officer (CEO) (Abernethy et al., 2019). However, in developing countries, the literature on the interaction between internal control systems and leadership attributes remains limited (e.g., Abdo & Feghali, 2017; Alam et al., 2019; Aziz et al., 2015).

Previous studies indicated that leadership is not only critical for business survival, developing effective business strategies, and enhancing firm performance but is also a contingent factor that dominates internal control systems (e.g., Carmeli et al., 2010; Liu et al., 2017; Zhu et al., 2004). Leadership is defined as the capacity to articulate compelling visions and goals based on the organization’s values (Holmberg & Tyrstrup, 2010) and is often assessed based on properties, such as leadership consistency and quality and the leaders’ ability to inspire and influence people (De Cremer, 2003; Zhou et al., 2008). Among these characteristics, leadership consistency is recognized as a vital element (Sorek et al., 2018). Leadership consistency is generalized as maintaining unity in words and actions throughout different contexts (Leventhal, 1980). Consistency builds employee trust (Wang & Hsieh, 2013), contributes to the fairness of corporate policies (De Cremer, 2003), and endows leaders with specific social values, including self-esteem and trust (De Cremer, 2003). In contrast, inconsistent leadership degrades work performance and eventually becomes the primary cause of corporate failure (Aboyassin & Abood, 2013; Bodolica & Spraggon, 2021). In addition to leadership consistency, leadership quality is another critical factor that is demonstrated by the exceptional characteristics of the leader’s personality, motivation, values, and abilities (Zhou et al., 2008). Leadership quality enables businesses to achieve their internal control objectives more efficiently. As a result, we argue that there could be an interaction between these leadership characteristics, namely leadership consistency and quality, to promote effective internal control and optimize business performance.

Although recent research on the interaction between leadership and internal control is extensive in emerging markets (e.g., Abdo & Feghali, 2017; Aziz et al., 2015; Khlif et al., 2019; Shen et al., 2021; Yin et al., 2020; Zhang et al., 2022), studies on the interface between leadership factors (i.e., leadership consistency and quality) and the internal control structure are still lacking. Little is known about the mechanism through which the internal control structure and leadership factors can be integrated to promote internal control effectiveness and increase firm performance. Our research question focuses on whether leadership consistency and quality can act as boundary conditions for the relationship between the internal control structure and effectiveness.

In doing so, we aim to examine the potential interactions between leadership consistency and quality and the internal control structure and whether these interactions can benefit businesses in emerging countries by enhancing the effectiveness of their internal controls. Given the importance of leadership in internal control practices (Aziz et al., 2015) and the current state of corporate governance in emerging markets (Puni & Anlesinya, 2020), the regulatory role of the leadership attributes (i.e., leadership consistency and quality) in enhancing the effectiveness of internal control is not well defined. If this role were clearly delineated, emerging market businesses could engage in and cultivate leadership attributes, which would encourage them to interact effectively with the internal control systems and improve business performance.

The preceding arguments underscore the importance of determining the moderating roles of leadership consistency and quality in promoting firms’ internal control effectiveness in emerging markets. Integrating leadership consistency and quality and the internal control structure enables researchers to explore and apply a mechanism to optimize internal control practices. In this study, the cognitive consistency (Gawronski & Strack, 2012) and expectancy theories (Vroom et al., 2005) are employed to explain the moderating effects of leadership consistency and quality on the relationship between the internal control structure and effectiveness in the context of Vietnam, which is an emerging economy. In doing so, this paper contributes to the internal control and leadership literature by providing a nuanced view of how the internal control structure affects business performance through the intervening role of leadership in an emerging economy context.

The rest of this paper is organized as follows. The following section discusses the theoretical foundations and formulation of the hypotheses. Then, the data analysis and collection methods will be discussed. After that, the hypothesis testing results will be presented and discussed. The paper concludes with discussing the findings and their implications, the limitations, and recommendations for further research.

Theoretical Background and Hypothesis Development

Cognitive Consistency Theory

Gawronski and Strack (2012) argued that cognitive consistency refers to the process of connecting, unifying, and resolving conflicts between thoughts, beliefs, knowledge, opinions, attitudes, and intentions. The connection, unification, and resolution of conflicts must be consistent with how individuals perceive themselves and their future behavior (Gawronski & Strack, 2012). Cognitive consistency plays a significant role in changing employee attitudes (Russo et al., 2008; Simon et al., 2004). To address employees’ asymmetry in their perceptions, attitudes, and behaviors, promoting employees’ cognitive consistency could be a possible solution. Asymmetry, according to the cognitive consistency theory, results in stress and psychological distress. Individuals who are under pressure to resolve cognitive conflicts must seek change to adapt, reduce stress, and achieve a psychological balance (Gawronski & Strack, 2012).

In our study, the consistency theory is used to explain the moderating role of leadership consistency in determining the effect of the internal control structure on internal control effectiveness. We claim that leadership is responsible for increasing a business’s value while demonstrating corporate responsibility to its employees, stakeholders, and society (Harrison & Freeman, 1999; Jogulu, 2010). High-quality leaders are expected to guide businesses toward positive outcomes (Chan, 2010) because they are the creators of an enticing narrative about ethics and values in organizations (Freeman & Stewart, 2006). Numerous studies have established a positive correlation between employee attitudes or behaviors and the attitude or behavior of a leader (e.g., Dimoff & Kelloway, 2019; van Knippenberg et al., 2007). Moreover, employee awareness and confidence will increase due to the alignment of leadership speech and behavior (Wang & Hsieh, 2013; Zhu et al., 2004). As a result, consistency in providing excellent leadership will positively affect employee perception, attitude, and behavior. Employees will have a cooperative attitude, support the leader’s policy, easily comply with regulations, and devote themselves to the business. These results will help the internal control and promote the enterprise protection role (Akresh, 2010). According to the cognitive consistency theory, leaders must actively demonstrate their willingness to advocate and create a policy of internal control that increases its effectiveness.

Expectancy Theory

Vroom proposed the expectancy theory in 1964, and several other researchers have since updated and supplemented it (e.g., Hackman & Porter, 1968; Lawler, 1968; Vroom et al., 2005). Vroom et al. (2005) asserted that people’s actions and motivation for work are not always determined by current events but by their perceptions of their expectations and the foreseeable future. In other words, individuals behave differently in response to their expectations for a specific outcome or its desirability. Consistent leadership anticipates the leader’s ability to deliver the best results for the business in various situations. They are constantly cultivating themselves to become quality leaders who can implement appropriate business policies and develop an effective internal control strategy. Experienced leadership that is developed through learning and experience significantly improves the enterprise’s internal control strategy (Zhang et al., 2022). We assert that if a business values the potential of internal control systems, then effective leadership will seek to leverage those values as a driving force for sustainable development.

In this study, the expectancy theory explains the effect of leadership quality on the moderating role of leadership consistency to determine how the internal control structure promotes internal control effectiveness. Vroom et al. (2005) contended that leaders who aim to lead their team to success must be motivated by expectancy, instrumentality, and valence. These qualities will ensure that the leadership fully supports the implementation of employees’ goals (Vroom et al., 2005). Leaders who encourage and meet employee expectations will reap numerous benefits in business operations (Awamleh & Gardner, 1999), which in turn, serve as a critical foundation for the effective delivery of internal control systems.

In addition, influential leaders frequently believe that their consistency in directing and operating internal controls will positively affect their operations. If the business achieves favorable operating results, employee compensation will be further increased. As a result, employees’ expectations for a bright future can rise due to consistent leadership and organizational fairness. At that point, the high-quality leaders’ self-expectations could motivate them to seek ways to modify their behavior and maintain consistency in internal controls to foster optimal operations. Furthermore, we proclaim that when consistent and high-quality leaders govern enterprises, more attention is placed on the organization of a well-developed internal control mechanism by the leaders. Internal controls with an adequate and optimized structure can provide numerous benefits by guiding the organization in the right direction and increasing the likelihood of achieving its objectives (Jokipii, 2010). Furthermore, effective leadership is frequently expected to secure employees’ futures and promote employee goal orientation (Paparoidamis, 2005). From there, a high level of employee goal orientation with active participation in internal control activities can assist internal controls with enhancing task execution efficiency. Therefore, the strong synergy between leadership consistency and quality can aid businesses in establishing an effective internal control structure.

The Mediating Role of Internal Control Effectiveness

According to the Committee of Sponsoring Organizations of the Treadway Commission (COSO), internal control is defined as a process that is undertaken by an entity’s board of directors, management, and other personnel that is designed to provide reasonable assurance regarding the achievement of objectives in terms of operational effectiveness and efficiency, financial reporting reliability, and compliance with legal and regulatory requirements (Committee of Sponsoring Organization [COSO], 2013). Additionally, it is a critical mechanism for monitoring and managing company practices (Akresh, 2010) and a tool to promote functional interoperability and cooperation (Hunziker, 2017). According to COSO (2013), internal control effectiveness is demonstrated through the achievement of the business’s objectives, which include the following: (a) honest and reasonable financial reporting; (b) effective and efficient operation; and (c) compliance with applicable laws and regulations (Agbejule & Jokipii, 2009; Changchit et al., 2001). To ensure that the internal control achieves these three objectives, enterprises must establish and operate internal controls following their organizational characteristics (COSO, 2013).

Our study is driven by the motivation to examine the effects of internal control structure and effectiveness. We claim that if businesses understand how to effectively utilize the available resources to construct an internal control system with complete elements, they will accomplish well-defined objectives and improve internal control effectiveness. An organized internal control structure that comprises all necessary components facilitates effective internal control (Jokipii, 2010; Länsiluoto et al., 2016). In addition, Hunziker (2017) affirmed that the adequacy of the internal control structure would help businesses to minimize material misstatements in their financial statements and ensure that their resources were used optimally by creating linkages and close collaboration between departments to achieve operational efficiency and effectiveness. Although internal control systems can have inherent and potential limitations, they can also assist leaders in identifying and mitigating potential risks before they become a severe problem (Sutton et al., 2008). Furthermore, whenever a business experiences an abrupt collapse, there is often a suspicion that the internal control mechanism was inadequate (Agyei-Mensah, 2016), which emphasizes the critical role that the structure of the internal control system plays in its effectiveness. Therefore, we propose the following hypothesis:

H1: The internal control structure positively affects the internal control effectiveness.

It can be argued that enhanced internal control effectiveness can drive firm performance. Previous studies concluded that the internal control effectiveness could provide a competitive advantage to businesses by increasing management and operational efficiency (Cheng et al., 2018; Lopez et al., 2009), lowering the cost of capital (Ashbaugh-Skaife et al., 2009; Khlif et al., 2019), directly influencing the effectiveness of corporate governance by minimizing errors and preventing fraud (Johnstone et al., 2011), and enhancing enterprise value (Gao & Jia, 2016). Moreover, internal control is responsible for risk mitigation (Jokipii, 2010), assisting businesses in achieving their objectives (Cheng et al., 2018), and is critical to the long-term development of businesses (Nguyen & Thi Bui, 2018). Tetteh et al. (2022) asserted that internal control has a significant and beneficial effect on business performance. In many instances, the ineffectiveness of internal control is the primary reason for a business’s poor performance (Zhou et al., 2016). As a result, the following hypothesis is suggested:

H2: Internal control effectiveness positively affects firm performance.

Both hypotheses H1 and H2 demonstrate that internal control effectiveness may act as a mediating factor in the link between the structure of internal controls and firm performance. Therefore, we proposed the following hypothesis:

H3: Internal control effectiveness mediates the impact of internal control structure on firm performance.

The Moderating Role of Leadership Consistency

Yoon and Suh (2019) stated that leadership is critical in most business activities. The unique role of leadership is to inspire and motivate employees to work together toward common goals (Lievens Pascal Van Geit Pol Coetsie, 1997). Awamleh and Gardner (1999) noted that the success of leadership in this role is highly dependent on the leader’s behavior and ability to elicit motivation in each employee. Moreover, as employee perception is influenced by leadership behavior (Awamleh & Gardner, 1999), consistent leadership inspires employee awareness and motivates employees to perform well (Wang & Hsieh, 2013). Simultaneously, consistency will assist leaders in achieving exceptional outcomes, such as satisfaction, trust, enthusiasm for staff activities, and engagement (Wang & Hsieh, 2013; Zaccaro, 2007). As a result, we affirm that firms with consistent leadership have a better chance of establishing internal controls using an integrated and appropriate structure.

This motivated us to examine whether consistent leadership is a prerequisite for enhancing corporate value by promoting internal control system effectiveness. We argue that if a business wishes to increase its value and establish a competitive advantage, its leaders must be consistent in most internal control decisions. This translates into a more effective internal control system in firms with consistent leadership than those with inconsistent leadership.

Based on the cognitive consistency theory (Gawronski & Strack, 2012), we claim that if leadership is consistent and there is no conflict in the internal control policy, the activities under their direction will be carried out with precise information, uniformity, and contradiction. This will instill a positive attitude toward internal control and the belief that internal control practices are necessary. Then, employees will implement these activities correctly and effectively. In contrast, inconsistency in leadership creates an asymmetry in command information, which results in unfavorable attitudes, stress (Gawronski & Strack, 2012), negative emotions, and underperforming employees (Cha & Edmondson, 2006; Intagliata et al., 2000). Moreover, Gawronski and Strack (2012) argue that other consequences of inconsistency are possible, such as the following: (a) decreased productivity; and (b) employees actively seek negative change to mitigate asymmetric information and alleviate psychological distress. These consequences require significant resources from employees to resolve their issues and diminish the effectiveness of the internal control activities that they are engaged in. If leadership inconsistency persists, the employees’ resources will be diverted away from their primary job and activities to adapt, relieve stress, and achieve mental balance.

We claim that a properly organized structure of internal control combined with consistent leadership will fully implement employee participation in internal control, reduce loss, increase job focus, and improve occupational skills. An alternative perspective is that if the internal control structure is adequately organized but the leadership is inconsistent, the employees’ participation in internal control activities could also be fully implemented. However, employees will appear uncomfortable, stressed, and distracted at work, which will make the internal control systems less efficient than expected.

Internal control is more effective when designed with a complete set of components (i.e., control environment, risk assessment, control activities, information and communication, and monitoring) (Jokipii, 2010). Additionally, it is effective when implemented under a consistent leadership context. We posit that consistent leadership can help to direct guidelines and decisions consistently in each internal control activity. Consistent guidelines during the development and implementation of internal control activities can eliminate role ambiguity, increase employee concentration, and make it easier for an internal control system to accomplish its objectives. Furthermore, leadership that maintains consistent views and actions will enable the components of internal control to promote their role further, thus strengthening the internal control effectiveness. Based on the previous arguments regarding the consistency theory, we hypothesize the following:

H4: Leadership consistency positively moderates the relationship between the internal control structure and effectiveness.

The Moderating Role of Leadership Quality

Internal control is critical for ensuring efficient operations and mitigating risk (Akresh, 2010; Sutton et al., 2008). As a result, leadership consistency is a necessary condition for the business to meet this requirement. However, in today’s highly competitive business environment, business leaders must fully converge quality conditions.

We argue that leadership consistency and quality can interact and resonate to increase the effectiveness of internal control systems. According to the expectancy theory, employees will expect both leadership quality and consistency. They anticipate competent leadership to guide the design and implementation of internal controls that will facilitate their work. If employees value leadership as a confluence of positive characteristics, innovation, creativity, and an appreciation for collective consciousness (Zhou et al., 2008), employees will experience positive leadership, which will increase their confidence in a bright future and motivate them to perform better (Apak & Gümüş, 2015).

Based on the expectancy theory (Vroom et al., 2005), we claim that the moderating role of leadership consistency in determining the relationship between the structure of internal controls and their effectiveness increases with the quality of leadership. Leadership develops when leaders model positive behaviors for their employees, dare to innovate, take calculated risks to ensure organizational success (Zhou et al., 2008), and demonstrate verbal consistency. The more employees trust their leaders’ words and actions (Leventhal, 1980), the more they will believe in the correctness of internal control activities (Zhu et al., 2004), which increases their confidence in their leaders (Zhu et al., 2004). When internal control is properly structured and organized, employees who trust the leadership quality (Avolio & Gardner, 2005; Paparoidamis, 2005) and consistency (Wang & Hsieh, 2013) will strive to do a good job (Paparoidamis, 2005), thereby augmenting the effectiveness of internal control.

In contrast, if leaders are perceived as low quality, they may not meet the employees’ expectations, even if they are consistent. At that point, staff will lose confidence in the internal control policies, cooperation will dwindle, and destructive behavior will develop, which will diminish internal control effectiveness (Zhu et al., 2004). Should leaders lack capacity, vision, and management thinking, businesses would face numerous challenges in implementing strategic goals and building and developing a positive reputation in a competitive market (Love et al., 2017).

Furthermore, the expectancy theory is applied from a leadership perspective. The more consistent and high quality the leadership, the more leaders prioritize their ability and consistency in developing and maintaining internal control practices. Effective internal control is a critical resource that enables leaders to exercise effective control over daily activities (Bowrin, 2004), contributes to positive business results (Tetteh et al., 2022), and propels businesses toward prosperity and sustainable development (Akisik & Gal, 2017). Therefore, we propose the following hypothesis:

H5: Leadership quality has a positive moderating effect on the moderating role of leadership consistency in determining the impact of the internal control structure on the internal control effectiveness.

Figure 1 shows the proposed model and its hypotheses.

Proposed model and hypotheses.

Research Method

Sampling

The research subjects are businesses located in Vietnam, which is a developing market. Vietnam is a crucial setting for investigating this topic because most companies in the country are young, and internal control applications have only recently been promoted (Le et al., 2021). This study used a purposive convenience sampling strategy to recruit relevant respondents by screening for their work positions and experience. The target respondents fit the following criteria: (a) middle-level managers working in Vietnamese enterprises; (b) at least 2 years of experience working in the representative company responding to the survey; and (c) work in departments, such as accounting, finance, sales, marketing, production, and research and development. This is because these departments have a strong relationship with internal control. These conditions are in place to ensure that respondents have sufficient experience and knowledge regarding the research subject to complete the survey questionnaires. The middle-level management team must process a great deal of data at various levels (from operational to strategic). Mahama and Cheng (2013) represented the business responding to the questionnaire. Additionally, middle managers can assess leadership (i.e., senior managers) by responding to the survey questions regarding the leadership consistency and quality rather than having the leaders (senior managers) self-evaluate.

The survey’s email list was compiled by extracting personal emails from the professional social network LinkedIn. LinkedIn is a well-developed professional social network (Mintz & Currim, 2013) and has been used to extract the emails of potential respondents in several prior works, such as Mintz and Currim (2013) and Ouakouak and Ouedraogo (2017). We noted that sending survey questionnaires from emails that were extracted from LinkedIn enables us to solicit feedback from many administrators working in various regions throughout Vietnam, whereas sending questionnaires to respondents via mail or in-person is difficult to implement, particularly due to the COVID-19 pandemic. This method of data collection protects both researchers and participants from infection.

We collected data in two stages to avoid common method bias (Podsakoff et al., 2003; Tehseen et al., 2017). To avoid a high drop rate and memory bias, following Einarsen et al. (2009), we employed a short period interval of 2 months between two stages. During stage one, we sent the survey form to 2,083 potential informants and obtained 548 completed responses. Respondents provided their emails and demographic information and evaluated the internal control structure and leadership and quality. During stage two, data on the mediating and dependent variables (i.e., internal control effectiveness and firm performance) was collected by sending the second part of the survey form to the respondents from stage one. The two stages of data collection were connected via an identification number that was attached to each participant.

The final sample comprised 206 Vietnamese business organizations and yielded a response rate of 9.89%, which is acceptable for email survey research in Vietnam. Following Armstrong and Overton’s (1977) recommendation, we conducted independent t-tests for a potential nonresponse bias, which revealed no differences between the first and fourth quartiles of responses in terms of demographic and key variables. This result implies that our study was free from nonresponse bias.

To confirm the informant competency of the respondents, we followed the procedure that was suggested by Morgan et al. (2004). As such, the respondents were required to rate their level of knowledge regarding the questions, the accuracy of the information provided, and their confidence in providing answers to the questions. This data was gathered using a seven-point Likert scale (one = “very low”; seven = “very high”). The mean score for the respondents’ level of knowledge was 6.37 (SD = 0.71), their response accuracy was 6.25 (SD = 0.70), and their confidence in answering the questions was 6.35 (SD = 0.70). This result indicates that the respondents could appropriately respond to the questions.

The demographic information of the informants and corresponding firms is summarized in Table 1.

Demographic Information of Participating Firms (n = 206).

Measurement Scales

All the measurement scales were adopted from the literature. Specifically, the internal control structure was measured using a 25-item scale that was adopted from Jokipii (2010). This is a second-order construct with the following five dimensions: control environment (five items), risk assessment (five items), control activities (five items), information and communication (five items), and monitoring (five items). These scales are formative. The internal control effectiveness was assessed using a 12-item scale that was adapted from Hunziker (2017). This scale has the following three dimensions: financial reporting (four items), operations (four items), and compliance (four items). The scale for leadership consistency, which comprises three items, was adopted from Cels (2017), whereas the five-item leadership quality scale was adopted from Zhou et al. (2008).

Due to the lack of objective data on firm performance in Vietnam, we used a self-assessment approach to assess firm performance, which is commonly adopted in various accounting and leadership studies (e.g., Eisenbeiss et al., 2015; Rao et al., 2015). The self-assessment and objective assessment results are strongly correlated (Venkatraman & Ramanujam, 1986). The scale of firm performance (six items), which was adapted from Liang and Gao (2020), asked informants to compare their firm’s effectiveness with that of main competitors over the previous 3 years in the following aspects: market share, new customer acquisition, customer satisfaction, sales, return on investment, and overall profitability. Seven anchors were included in the design of each of the scales. Specifically, the verbal anchors that were assigned to firm performance ranged from one = “poor” to seven = “excellent,” whereas those that were assigned to the other variables ranged from one = “strongly disagree” to seven = “strongly agree.”

Following previous research in accounting and leadership (e.g., Eisenbeiss et al., 2015; Zhu et al., 2014), we included the following four demographic variables as the control variables of firm performance: firm age (number of years in operation since establishment); firm size in terms of assets; firm size in terms of full-time employees; and ownership structure (one = “with foreign capital”; two = “without foreign capital”).

Results

Reliability and Validity Tests

The proposed model’s estimates were obtained using partial least squares structural equation modeling (PLS-SEM). In comparison with the traditional covariance-based structural model, PLS-SEM has higher statistical power under similar conditions and is even applicable when the data is non-normal and the sample size is small (Reinartz et al., 2009). After determining the constructs’ reliability and validity, the proposed model and hypotheses were empirically tested using 5,000 bootstraps resamples. All outer loadings for the reflective constructs (from 0.62 to 0.95) exceeded the cut-off value of 0.50 (Bagozzi & Yi, 2012). Moreover, the composite reliabilities of the reflective constructs were significantly greater than 0.70 (ranging from 0.82 to 0.96). The average variance-extracted values for the constructs (ranging from 0.52 to 0.88) were greater than 0.50, which indicates a high degree of convergent validity.

Table 2 indicates that the square root of the average variance that was extracted from each of the reflective constructs (between 0.68 and 0.94) was greater than the corresponding absolute values of the correlations between this construct and the others, which indicates that the measurements had discriminant validity (Fornell & Larcker, 1981). Moreover, the Heterotrait-Monotrait (HTMT) values between 0.61 and 0.85 were lower than the cut-off of 0.85, which indicates satisfactory discriminant validity (Henseler et al., 2015).

Analysis of Discriminant Validity.

Note. First value = correlation between variables (off diagonal); Second value (italic) = HTMT ratio; Square root of average variance extracted (bold diagonal); **: Correlation is significant at the 1% level (two-tailed t-test); N/A: Square root of the average variance that was extracted is not applicable for formative constructs.

Multicollinearity Issues and Common Method Bias

Following O’Brien (2007), we investigated possible multicollinearity by calculating the independent variable’s variance inflation factor (VIF) values. These values were significantly less than the cut-off point of 10, which suggests no significant multicollinearity issues. The data was collected in two phases, which decreases the risk of the results being influenced by a common method bias. However, because we gathered data from a single source, a Harman test to assess for common method bias was conducted upon the recommendation of Podsakoff et al. (2003). Because the first factor only explained 35% of the 69.47% explained variance, this study is free from the common method bias.

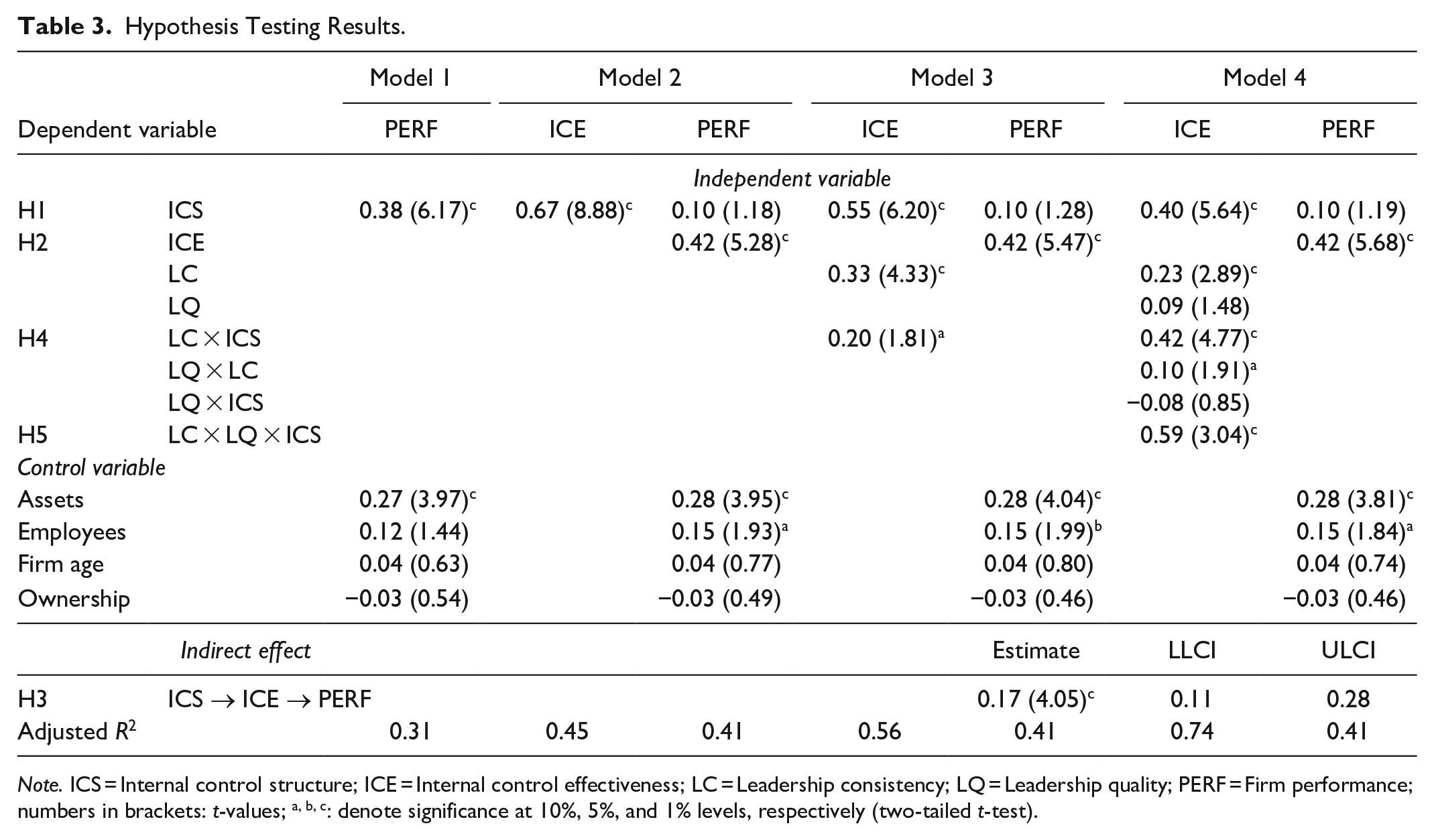

Hypothesis Testing Results

We used PLS-SEM to test the proposed model and hypotheses. The sample size of 206 was sufficient because this exceeds tenfold the number of paths leading to the variables (Hair et al., 2017). Additionally, the standardized root mean square residual value of the full model of 0.08 suggests that the proposed model fits the data well (Henseler et al., 2016).

In testing the hypotheses, four hierarchical PLS-SEM models were developed. Model 1 established a direct link between the internal control structure and firm performance. Model 2 was adapted from Model 1, with internal control effectiveness added as a moderating variable in the relationship between the internal control structure and firm performance. Model 3 enhanced Model 2 by including leadership consistency as a moderator in the relationship between the internal control structure and effectiveness. Model 4 was the final and complete model, with the addition of leadership quality to counterbalance the moderating effect of leadership consistency.

Table 3 presents the indices, including the adjusted R2 values for internal control effectiveness and firm performance, and those used to determine the strength of the individual relationships, which are the β coefficients and t-values. These indices were computed using 5,000 bootstrap runs. The adjusted R2 values for internal control effectiveness and firm performance were greater than .10 (ranging from .31 to .74), which indicates that the dependent variable’s variance is acceptable (Falk & Miller, 1992).

Hypothesis Testing Results.

Note. ICS = Internal control structure; ICE = Internal control effectiveness; LC = Leadership consistency; LQ = Leadership quality; PERF = Firm performance; numbers in brackets: t-values; a, b, c: denote significance at 10%, 5%, and 1% levels, respectively (two-tailed t-test).

H1 suggests that the internal control structure positively influences the internal control effectiveness. This hypothesis was supported (Model 2: β = .67, t-value = 8.88; Model 3: β = .55, t-value = 6.20; Model 4: β = .40, t-value = 5.64). H2 proposes that firm performance is positively influenced by internal control effectiveness. Because the path between internal control effectiveness and firm performance was positive and significant (Model 2: β = .42, t-value = 5.28; Model 3: β = .42, t-value = 5.47; Model 4: β = .42, t-value = 5.68), H2 was supported. H3 conjectures that the internal control effectiveness mediates the path from the internal control structure to firm performance. This hypothesis was confirmed because there was a significant change regarding the strength of the impact of the internal control structure on firm performance when internal control effectiveness was introduced as a mediator (Model 1: β = .38, t-value = 6.17; Model 2: β = .10, t-value = 1.18). Moreover, the indirect effect of the internal control structure on firm performance via internal control effectiveness was significant (β = .17, t-value = 4.05; CI = [0.11; 0.28]), which supports H3. This result was validated by a significant Sobel statistic of 3.49 (p-value = .00). Therefore, H3 regarding the connecting role of internal control effectiveness in the link between the internal control structure and firm performance is accepted.

To test H4, which proposes that leadership consistency has a positive moderating effect on the link between the internal control structure and effectiveness, following Aiken et al. (1991), we mean-centered the moderating and independent variables (i.e., LC and ICS) and created the interaction term LC × ICS to avoid multicollinearity. Table 3 indicates that leadership consistency has a positive moderating effect on the impact of the internal control structure on internal control effectiveness (Model 3: β = .20, t-value = 1.81; Model 4: β = .42, t-value = 4.77). Therefore, H4 was accepted. Finally, the three-way interaction term LC × LQ × ICS was formed to test H5, which posits that leadership quality strengthens the moderating role of leadership consistency on the impact of the internal control structure on internal control effectiveness. This hypothesis was supported with the positive and significant effect of the interaction term LC × LQ × ICS on the internal control effectiveness (Model 4: β = .59; t-value = 3.04).

Discussion of Research Results

This section discusses the hypothesis testing results. First, the result of the H1 test regarding the impact of the internal control structure and effectiveness is consistent with previous studies (e.g., Hunziker, 2017; Jokipii, 2010). Effective internal control systems enable organizations to mitigate the risk of material misstatements in financial statements to ensure that resources are used appropriately and effectively, improve coordination between functional departments, and are compliant with applicable regulations and laws, all of which contribute to the effective and efficient operation of organizations (Changchit et al., 2001; Hunziker, 2017; Jokipii, 2010).

Second, the confirmation of H2 supports the resource-based view (Barney, 1991) in the context of internal control research and is consistent with previous accounting studies in Vietnam (e.g., Nguyen, 2018). This indicates that the resource-based view (RBV) is an appropriate theoretical framework for explaining the relationship between accounting resources (e.g., management accounting systems, internal control systems) and a competitive advantage.

Third, the confirmation of H3 indicates that internal control effectiveness is a necessary device that connects the internal control structure to enhanced organizational performance. This is a novel finding compared to previous studies, which focused exclusively on the direct impact of the internal control structure on internal control effectiveness (e.g., Jokipii, 2010; Länsiluoto et al., 2016) or the direct impact of the internal control effectiveness on performance outcomes, such as risk management, corporate governance, operational efficiency, investment efficiency, financial efficiency, and capital costs (e.g., Al-Thuneibat et al., 2015; Cheng et al., 2013; Khlif et al., 2019).

Fourth, while knowledge regarding leadership-related moderating variables on the direct effect of the internal control structure on internal control effectiveness remains limited in the emerging market context, the support of H4 regarding the moderating role of leadership consistency is a novel point, which builds on previous internal control studies (e.g., Jokipii, 2010; Länsiluoto et al., 2016; Wardiwiyono, 2012). This result implies that in an emerging market context, such as Vietnam, if organizational leaders maintain a high level of consistency, the effectiveness of internal control could be enhanced through a well-organized internal control structure.

Finally, the H5 tests found that the high-quality leadership can strengthen the role of leadership consistency in moderating the effect of the internal control structure and effectiveness. This demonstrated that when the internal control structure is well-organized and employees believe in the consistency of leadership, if employees are motivated by high-quality leaders, they will strive to perform tasks well. Both leadership quality and consistency conditionally promote internal control effectiveness. While the expectancy theory has previously been used to explain the relationships between self-esteem, budgetary participation, and managerial performance (Chong & Chong, 2002; Orpen & Nkohande, 1977), the result of the H5 test emphasizes the applicability of the expectancy theory in the internal control context by demonstrating how the interactions between leadership attributes (i.e., leadership consistency and quality) and internal control systems can be theorized.

Conclusion, Implications, Limitations, and Future Research Directions

Conclusion

The global competitive landscape has necessitated that enterprises operating in emerging markets improve the effectiveness of their internal control systems. This study found empirical evidence for the critical role of leaders in this setting by examining how the interactions between two leadership attributes (i.e., leadership consistency and quality) and the internal control structure can improve internal control effectiveness and organizational performance using data from Vietnamese firms. This study contributes to the body of knowledge regarding leadership and internal control studies. Furthermore, it provides managers with guidance on effectively integrating leadership and internal control practices to foster performance. These implications are discussed in greater detail below.

Theoretical Implications

This study has several theoretical implications. First, it adds to the limited studies on leadership and internal control (e.g., Abdo & Feghali, 2017; Alam et al., 2019; Shen et al., 2021; Zhang et al., 2022) by examining the performance implications of the interaction between internal control components and leadership characteristics. Specifically, this study investigated and tested the interaction and resonance between leadership consistency and quality and the internal control structure in enterprises that have been overlooked in previous research.

Second, our study contributed to the internal control literature in the context of emerging markets (e.g., Le et al., 2021; Nguyen, 2021) by empirically validating a theoretical argument that leadership consistency moderates the influence of the internal control structure on internal control effectiveness. This discovery adds to our knowledge of the boundary conditions that influence the performance effects of the internal control structure.

Third, our research findings indicate that the higher the leadership quality, the more profound the moderating role of leadership consistency on the effect of the internal control structure and effectiveness. This contributes to our understanding of the complex nature of the leadership–internal control relationship by implying that higher leadership consistency may facilitate internal control structures when the leadership quality is higher. This study provides empirical evidence on how to transform the structure of internal control and the elements of leadership into added value for firms through a moderated mediation model of internal control in the context of emerging economies.

Fourth, this research demonstrates how the cognitive consistency and expectancy theories (Gawronski & Strack, 2012; Vroom et al., 2005) explain the performance implications of the combination of leadership and internal control, which can boost the efficiency of companies in emerging markets. Therefore, our study shows that when business organizations in emerging markets prioritize leadership consistency and quality enhancement, their internal control mechanisms can produce positive results.

Finally, our study applies the cognitive consistency theory to a specific accounting study to explain the beneficial interaction between leadership and internal control. This is because this theory has historically been applied to studies on social cognition, behavioral psychology, and organizational coordination (Gawronski & Strack, 2012). For instance, in other fields, such as marketing, Fraedrich and Ferrell (1992) used this theory to examine managers’ consistency when making ethical decisions. Additionally, Prince (2020) employed this theory to develop a model of consumers’ willingness to purchase domestic goods and gain an insight into consumers’ minds as they interact with the plethora of available products. In doing so, our study contributes to the field of accounting by the employing the cognitive consistency theory to explain the relationship between leadership consistency and the structure and effectiveness of internal control in emerging market firms.

Managerial Implications

Our study has several managerial implications. First, our research findings provide insights into allocating scarce resources appropriately to human resource management activities and optimizing the internal control system for business activities. In the current context, the interaction between leadership characteristics (i.e., the consistency and quality of the leadership) and the internal control system can result in beneficial outcomes, such as protecting assets, operating effectively, improving compliance with government regulations, increasing business results, adding value, and improving the reputation of businesses. Second, this study has implications for business leaders regarding how they should approach and develop internal control to achieve the best results for management requirements and business results. Filling this research void has managerial implications for emerging market business leaders regarding the skillful combination of leadership characteristics and the control system’s superiority toward future stable and sustainable development.

Limitations and Future Research Directions

Our study has several limitations, which provide avenues for future research. First, despite having a 2-month time lag between the independent and moderating variables (i.e., internal control structure and leadership consistency and quality) and the mediating and dependent variables (i.e., internal control effectiveness and firm performance), we were unable to make causal claims due to our inability to handle variables or use randomly assigned variables. Future studies could avoid this constraint by employing an experimental design or a longitudinal method with at least a 1-year lag between data collection and the study variables. Second, this research focused on business organizations in Vietnam. As a result, the study’s findings are restricted regarding their generalizability, and extrapolation to other countries should be done with caution. As a result, further research into our proposed model in advanced economies is encouraged. The third drawback relates to the inadequacy of the leadership traits that were considered because the study only examined the consistency and efficiency of leadership. Future studies should be conducted to examine other leadership attributes, such as experience; trustworthiness; being just, honest, encouraging, positive, motivational, and dynamic; and building confidence (Leong & Fischer, 2011). These attributes can influence internal control practices or interact with the internal control system, thus affecting enterprise performance.

Footnotes

Ethics Statement

This study was approved by the Ethics Committee of the University of Economics Ho Chi Minh City (Committee approval number: 3524/QD-DHKTQLKH).

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was funded by the University of Economics Ho Chi Minh City (Grant number: 2021-05-19-0358).