Abstract

Japanese and Korean financial systems are distinct from those in the western economies. Considering this, we examine how the dividend policy of the firms in two of the largest economies of East Asia is determined by the internal attributes of firms. Firm-level data from 1,773 Japanese and 1,035 Korean firms were evaluated using panel data techniques, and some interesting similarities and differences in the dividend policies of both countries were unearthed. For example, in both countries, larger firms pay higher dividends, whereas those firms with volatile earnings pay low dividends. It was also determined that Korean firms pay more dividends when their profitability surges. On the other hand, cash dividends in Japanese firms decline when there is an increase in their profitability level. Overall, the dividend policy of Korean firms resembles more to those in Anglo-Saxon countries, while the dividend policy of Japanese firms bears little resemblance to other established financial systems. This study is the first to compare and contrast the internal dynamics of dividend policy for both the Japanese Keiretsus and Korean Chaebols while evaluating a huge universe of firms from both countries. Transnational studies are important to draw parallels and differences. The findings of this study offer important implications for various stakeholders, including managers, investors, and policymakers. Also, the results pave the way for a theoretically enriched understanding of dividend policy by comparing and contrasting diverse financial systems.

Introduction

Miller and Modigliani (1961) argue that under certain frictionless assumptions, the value of a particular firm is determined by the ability of its assets to generate income (optimal investments). Specifically, income as retained earnings and dividends has nothing to do with the cost of capital or share price and is thus irrelevant. They further suggest that a dividend policy can be made at home as per investors’ requirements. However, empirical findings suggest that capital gains in the future are seemingly less certain and risky than cash dividends (Gordon, 1963; Lintner, 1962). Therefore, the required rate of return for higher dividend-paying firms is lower than their counterparts. Consequently, dividend-paying firms may reduce their cost of capital, and hence, dividend policy is relevant to the firm’s value.

From two extremes, for example, irrelevance (Miller & Modigliani, 1961; Miller & Scholes, 1978) to relevance in terms of bird in hand (Gordon, 1963; Lintner, 1962), agency theory based explanations (Easterbrook, 1984; Jensen & Meckling, 1976; La Porta et al., 2000), clientele effect (Allen et al., 2000; Pettit, 1977), information content (Bhattacharya, 1980; John & Williams, 1985; Miller & Rock, 1985), life cycle theory (DeAngelo et al., 2006), and catering theory (Baker & Wurgler, 2004); dividend policy has been scrutinized from various aspects. These theoretical perspectives suggest different factors affecting the dividend policy. However, the lack of consensus in the extant literature makes dividend policy one of the major controversial and extensively studied areas of corporate finance (Brealey et al., 2008) and referred to as a “dividend puzzle” (Aivazian et al., 2003a; Bernstein, 1996; Black, 1976).

However, most of the aforementioned models have been developed in the context of Anglo-Saxon countries, where the financial system is based on a capital market (open financial system). In these countries, ownership is diversified, and firms mostly rely on capital markets for equity capital. As a result, there is greater information asymmetry and higher agency costs in terms of monitoring (Jensen & Meckling, 1976). On the other hand, there are countries where firms either rely on banks or affiliated group partners for capital. Consequently, firms in such countries are expected to face lower information asymmetry and agency costs due to close relationships with banks or intra-group mechanisms. Such differences cast doubts on the validity of the aforementioned dividend models.

This study examines how firms’ internal dynamics affect dividend policy, considering the non-financial firms in Japan and South Korea. The motivation for this study stems from the fact that Japan and South Korea are the two developed economies in East Asia. Both are depicted as successful examples of industrial group-based financial systems (i.e., Keiretsu and Chaebol). Japanese and Korean conglomerates not only differ from one another but are quite unique to those open market financial systems (such as in the US and UK). Western conglomerates are based on the economic rationale of diversification, synergy creation, and cost-savings. The East Asian conglomerates (Keiretsu & Chaebol) are based on the governments’ backed “too-big-to-fail” strategy and national industrialization programs (Chung, 2004) after WWII. Further, Japanese Keiretsus are groups of different firms heavily reliant on a financial institution (also equity holder) for financing and managed by entrenched managerial elites. Within Keiretsu, firms have interlocking shareholdings (Debnath & Tokuda, 2013). Unlike the Keiretsu system, Chaebols are comprised of firms horizontally integrated and controlled mainly by founding families (Chung, 2004). In the Korean Chaebols, families have ownership stakes in a business, which in turn controls another business, and so on. This chain-ownership relationship is also referred to as a pyramid ownership structure (Almeida et al., 2011). These unique attributes make it further interesting to compare the corporate payout policy of Japanese and Korean firms.

For an empirical estimation of the proposed hypotheses, firm-level data from 1,773 Japanese and 1,035 Korean firms were evaluated, and some interesting similarities and differences in the dividend policies of both countries were unearthed. Overall, the dividend policy of Korean firms resembles more to those in Anglo-Saxon countries, while dividend policy of Japanese firms bears little resemblance to other established financial systems.

This study contributes to expanding the extant dividend policy literature in two ways. First, this study adds to the determinants of dividend policy literature by comparing and contrasting the internal dynamics of dividend policy for both the Japanese Keiretsus and Korean Chaebols while evaluating a huge universe of firms from both countries. Second, with a special focus on two of the largest economies of East Asia, the empirical results and theoretical discussion of this study provides new insights into the dividend policy across countries and pave the way for future cross-country research.

The rest of the study is organized as follows. Section 2 discusses literature and underlying hypotheses; Section 3 explains data collection and research methods; Section 4 discusses regression results; and Section 5 concludes this study.

Literature Review and Hypotheses

Relaxation of frictionless assumptions suggests that dividend policy mainly matters under the assumptions of tax clientele and information asymmetries. Models based on the assumption of information asymmetries such as signaling, agency, free cash flow, and tax-adjusted are based on the clientele effect. These models have identified several firm-specific factors that can affect dividend policy. These factors include size (Jaara et al., 2018; Labhane & Das, 2015), profitability (Ahmed, 2015; King’wara, 2015), leverage (Boanyah et al., 2013; Gill et al., 2010; Jabbouri, 2016), growth opportunities (Baker & Powell, 2012; Yarram & Dollery, 2015), business risk (Holder et al., 1998; Miller & Rock, 1985), free cash flows (Anil & Kapoor, 2008; Kadioglu & Yilmaz, 2017), and taxes (Gill et al., 2010; Pattenden & Twite, 2008). This study examines the impact of the aforementioned attributes on firms’ dividend policies in Japan and South Korea.

Firm Size

According to Jensen and Meckling (1976), larger firms with dispersed ownership structures face higher agency costs. To minimize such costs, larger firms can pay more dividends as a signal to promote confidence in management (Lloyd et al., 1985; Sawicki, 2009). Similarly, large firms can tape several financing sources at a comparatively lower cost than smaller ones. Thus lower transaction costs and easier access to capital markets may also encourage larger firms to pay out dividends (Manneh & Naser, 2015). Empirical findings also suggest that large firms are mature, having low information asymmetry, stable cash flows, and low probability of financial distress (Al-Najjar & Kilincarslan, 2018; Bhattacharya, 1979; Cwynar et al., 2015; Gaud et al., 2005; Jaara et al., 2018; Mitton, 2004; Ramcharran, 2001). Such attributes of large firms make them less reliant on external funds for future expansion purposes. Consequently, they are better positioned to pay more dividends (Yusof & Ismail, 2016). Thus in line with agency cost theory and free cash flow hypothesis, we hypothesize that:

Hypothesis 1 (H1): The higher the firm size, the higher is the dividend payout.

Profitability

Dividend is an offshoot of leftover earnings; therefore, profitable firms are considered more suitably positioned to pay dividends than their counterparts. Baker and Jabbouri (2016) argue that a firm’s current profitability is a key factor of dividend policy. According to Khan and Akhtar (2018), managers of profitable firms can accumulate funds through retained earnings to avoid risky external financing. Consequently, a firm’s probability of financial distress and reliance on external financing decreases. Hence, such firms are expected to devise more appropriate and stable dividend policies. Much of the empirical findings suggest that highly profitable firms pay more dividends compared to those having lower profitability (Ahmed & Javid, 2009; Ain et al., 2021; Aivazian et al., 2003a; Amidu & Abor, 2006; Anwer et al., 2021; Denis & Osobov, 2008; Ling et al., 2008). A positive payout-profit relationship is also in line with the signaling theory. Hence, we formulate the following hypothesis:

Hypothesis 2 (H2): The higher the profitability, the higher is the dividend payout.

Leverage

Firms can rely on both internal and external financing for expansion and future growth opportunities. Higher dividend payments may decrease internal funds (retained earnings) and increase firm dependence on risky external financing (Manneh & Naser, 2015). Therefore firms are expected to make appropriate decisions because the dividend-paying ability of highly levered firms decrease due to the payment of fixed interest and principal amount (Boanyah et al., 2013). Such highly levered firms cannot sustain a stable and higher dividend policy due to an increase in the probability of bankruptcy and transaction costs (Rozeff, 1982). Numerous empirical studies (e.g., Al-Kuwari, 2009; Iqbal & Zhang et al., 2020; Jaara et al., 2018; Kowaleski et al., 2007; Yusof & Ismail, 2016) suggest that an increase in financial leverage reduces dividend payouts of firms. Hence, our study formulates the following hypothesis:

Hypothesis 3 (H3): Leverage is negatively associated with dividend payouts.

Growth Opportunities

Life cycle theory (DeAngelo et al., 2006) suggests that firms in their initial stage of life have more opportunities to invest, while internally generated funds are not enough. Due to higher costs, such younger firms find it difficult to rely on external information-sensitive financing. To reduce their dependency on costly external financing, growing firms are expected to accumulate and retain more earnings and pay less dividends. Several empirical studies (e.g., Chen & Dhiensiri, 2009; Fama & French, 2002; Holder et al., 1998; Yarram & Dollery, 2015) support these results. Conversely, mature firms have lower investment expenditures due to fewer growth opportunities and stable cash flows. Hence such firms have higher payouts (Gaver & Gaver, 1993; Grullon et al., 2002; Prakash & Yogesh, 2021). The negative relationship between dividend payout and growth is also consistent with the agency theory. If firms lack investment opportunities to utilize internal funds, then paying higher dividends can reduce agency costs of idle cash. Thus firms are expected to substitute investment policy for dividend policy to mitigate agency costs (Myers, 1984). In line with the above evidence, we hypothesize that:

Hypothesis 4 (H4): Growth opportunities reduce dividend payouts.

Earnings Volatility

Managers may adjust dividend policy during uncertain situations (Attig et al., 2021; Prakash & Yogesh, 2021). Managers would be careful to initiate (if the firm is not paying) or increase (if the firm is paying) dividends during periods of volatile earnings. Because, under the signaling mechanism, dividend payout influences a firm’s share price. Higher dividend payouts during periods of volatile earnings may increase a firm’s dependence on costly external financing and its vulnerability to financial distress (Alli et al., 1993). Therefore, firms are expected to reduce dividend payout (McCabe, 1979). Several empirical studies (Amidu & Abor, 2006; Kowaleski et al., 2007) support a negative association between earnings volatility and dividend payout ratio. However, some studies (Crutchley & Hansen, 1989) suggest that firms with volatile earrings and those in need of external financing may use higher dividend payout to signal a better prospect of the firm. Following the literature, we formulate our hypothesis as:

H5: Higher business risk reduces a firm’s ability to pay dividends.

Corporate Tax

An increase in tax liability reduces after-tax earnings, consequently, earnings available for distribution also decreases. Therefore tax liability is expected to negatively affect dividend payouts of the respective firms. The negative tax-dividend relationship is also consistent with tax preference theory (Barclay, 1987). However, there is not much consensus in the literature regarding the tax-dividend relationship. As per tax-adjusted models of dividend policy, investors maximize their after-tax profit. Therefore, dividend tax clientele changes when a firm changes its dividend policy (Masulis & Trueman, 1988; Modigliani, 1982). Several studies (e.g., Anil & Kapoor, 2008; Khan & Ahmad, 2017; Rafique, 2012) document an insignificant relationship between tax and dividend policy. In contrast, some studies (e.g., Amidu & Abor, 2006; Daunfeldt et al., 2009) report a positive relationship between tax and dividend payout ratios. Following the tax preference theory, this study hypothesizes that:

Hypothesis 6 (H6): Corporate tax is negatively associated with dividend payouts.

Cash Flow

To reduce agency costs of free cash flows and curb managerial opportunistic behavior, firms with higher idle cash are more likely to pay dividends (Boanyah et al., 2013). Paying dividends from free cash restricts not only managers’ lavish spending but also increases firms’ dependency on external financing. Consequently, agency costs of idle cash decline due to management vigilance (Jensen, 1986). According to La Porta et al. (2000), distributing free cash reduces information asymmetry. Consequently, firms with higher cash flows are expected to pay higher dividends. Empirical studies (Amidu & Abor, 2006; Kadioglu & Yilmaz, 2017; Manneh & Naser, 2015; Sawicki, 2009) suggest a positive association between cash flows and dividend payout. In line with agency cost theory and free cash flow hypothesis, we hypothesize that:

Hypothesis 7 (H7): Cash flows increase a firm’s dividend-paying ability.

Data and Methodology

Sample Selection and Data Sources

The sample of this study consists of 1,773 Japanese and 1,035 South Korean non-financial firms. Data for Japanese and Korean firms are collected from the WorldScope database. Financial firms have been excluded because of different financial characteristics. The sample initially considers the period from 2007 to 2017, but because of the calculation of standard deviation variable, the sample from the year 2007 was eliminated. Therefore, the final sample period is from 2009 to 2017.

Variables Measurement

Dividend policy

Following prior literature (e.g., Ain et al., 2021; Ferris et al., 2003; García-Meca et al., 2022; Khan & Ahmad, 2017), this study uses the ratio of cash dividends paid to net income available for common shareholders as a measure of dividend policy (DIVPAY).

Firm size

In line with prior literature (Iqbal et al., 2013; Jaara et al., 2018), this study uses the natural-log of total annual sales as a proxy for firm size (LOGSIZ).

Corporate profitability

This particular study uses EBIT scaled by book value of total assets as a measure of profitability (COPROF). A similar measure has been used by de Jong et al. (2008) and Iqbal et al. (2016, 2022).

Leverage

Following the literature (e.g., Iqbal et al., 2017, 2020; Vo & Nguyen, 2014), we use the ratio of the book value of long term debt and the book value of total assets to measure leverage (COLEVE).

Growth opportunities

Following Titman and Wessels (1988), we use the ratio of capital expenditure to total assets to measure a firm’s growth opportunities (GROWTH).

Earning volatility

To proxy earning volatility (EARVOL), this study uses variation in the ratio of EBIT to total assets over the last 3 years. A similar measure has been used in literature (Booth et al., 2001; Karacaer et al., 2016).

Cash flow

Free cash is a better measure to authenticate a firm liquidity position than current earnings (Alli et al., 1993) because the free cash flow is less vulnerable to accounting tinkering. Following Gill et al. (2010), this study uses a natural log of net cash flows (from the operations) to proxy cash flow (CASHFL).

Corporate tax

In line with the literature (Amidu & Abor, 2006; Khan & Ahmad, 2017), this study uses the ratio of corporate tax to earnings before tax as a proxy of tax effects (CORTAX).

Table 1 provides a brief description of all variables.

Variables Definitions.

Variables Treatment

Negative dividend payout ratios indicate that firms, although recorded losses even then, paid dividends. King’wara (2015) censored such negative dividend payout ratios as zero. We also censor negative payout as zero. Leverage ratios greater than 1 suggest that total long-term debt exceeds the total assets of the respective firms. This may be an indication of financial issues. Hence, such firms are not representative of normal firm behavior. Therefore, we excluded such firms both from Japanese and Korean samples. Similarly, the natural log of negative cash flows is not possible, which were considered as zero.

Estimation Model

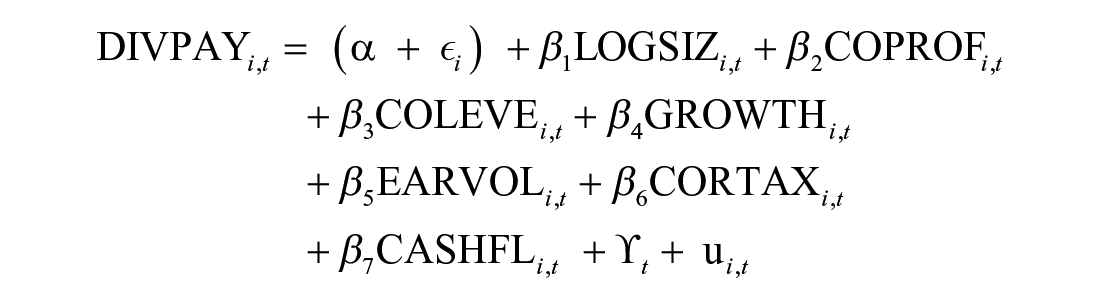

This study analyzes the impact of seven explanatory variables on the dividend-paying behavior of non-financial firms in Japan and South Korea. In the case of both countries, our panel is not balanced due to missing observations. Given the panel nature of the data, this paper employs panel data models for estimations. We use both Least Square Dummy Variable Model (LSDV) and Error Component Model (ECM).

To deal with cross-sectional heterogeneity, the LSDV model allows each cross-sectional unit in the sample to presume its own intercept using a dummy. The basic LSDV model for our analysis with year fixed effects (γt) is as follow;

On the other hand, error component model is based on the presumption that heterogeneity is due to entity specific random term (ϵ i ). Thus our ECM model with year fixed effects (ϒt) can be as follow;

Replacing entity specific random term (ϵ i ) and idiosyncratic error term (u i,t ) for a composite error term (ϵ i,t ) and rearranging above model we arrive as follow;

Where

DIVPAYi,t = Dividend payout ratio for unit “i” at period “t”

α = Common y-intercept

μi = Time invariant and unit specific intercept

β = Slope coefficients of respective explanatory variables

LOGSIZi,t = Natural log of sales for unit “i” at period “t”

COPROFi,t = EBIT over BV of total assets for unit “i” at period “t”

COLEVEi,t = BV of long term debt and BV of total assets for unit “i” at period “t”

GROWTHi,t = Capital expenditure to total assets for unit “i” at period “t”

EARVOLi,t = Variation in EBIT over total assets over the last 3 years for unit “i” at time “t”

CORTAXi,t = Corporate tax scaled by earnings before tax for unit “i” at period “t”

CASHFLi,t = Natural log of net cash flows (from operation) for unit “i” at period “t”

ϒt = Year fixed effects

ui,t = Stochastic error term for unit “i” at period “t”

ϵi,t = Composite error term

This study uses the Breusch Pagan LM test to assess the homogeneity hypothesis across units. To decide appropriation of model Hausman_Chi2 has been estimated. Furthermore, to ensure the statistical validity of estimation and tackle the issues of serial correlation, heteroskedastic standard errors, and clustering effects, we adjust standard errors corrected for clustering at firm and year level (Petersen, 2009).

Results and Discussion

Descriptive Statistics

Panel A and panel B of Table 2 presents the descriptive statistics for Japanese and Korean sample firms, respectively. Japanese sample contains 1,773 firms with 14,138 observations and 1,035 Korean firms with 8,657 observations during 2009 to 2017. The median and mean values of dividend payout (DIVPAY) are 0.253 and 0.266 for Japanese and 0.082 and 0.122 for Korean firms, respectively. This reveals that Japanese firms pay more dividends than Korean firms. Further, the mean and median values in Japanese firms are closer than that of Korean firms. This shows more symmetrical dividend policies in Japanese firms than in Korean forms. The mean and median of firms’ size (LOGSIZ) in Korea seems slightly higher than Japanese ones.

Descriptive Statistics.

Note. This table reports descriptive statistics for both the Japanese and Korean samples. See Table 1 for variable definitions.

Mean and median values of profitability (COPROF) in Japan are 0.080 and 0.092, and 0.076 and 0.070 in Korea, respectively. This reveals that Korean firms’ average profitability ratios are lower than Japanese firms. Similarly, mean and median leverage ratios (COLEVE) show that Japanese firms, on average, borrow more compared to Korean firms. The mean and median growth rates (GROWTH) and earning volatility (EARVOL) in Korean firms are higher than Japanese firms indicating that Japanese firms are ahead in maturity with stable or less volatile earnings than Korean firms. The mean and median of corporate tax (CORTAX) shows that the Japanese non-financial sector pays on average a higher percentage of their earnings in the form of tax than firms in Korea for the period under consideration.

Correlations

Panel A and panel B of Table 3 present correlation coefficients between explained variables and explanatory variables for Japan and Korea. Panel A of Table 3 shows that dividend payout (DIVPAY) in Japan is positively correlated with both firm size (LOQSIZ) and growth opportunities (GROWTH). The rest of the explanatory variables, for example, firm profitability (COPROF), financial leverage (COLEVE), earning volatility (EARVOL), taxes (CORTAX), and free cash flows (CASHFL), are all negatively associated with the dividend policy (DIVPAY) in the Japanese sample.

Correlation Analysis.

Note. This table reports correlation analysis for both the Japanese and Korean samples. See Table 1 for variable definitions.

, **, and *** indicate significance level at 10%, 5%, and 1%, respectively.

Similarly, Panel B in Table 3 suggests that dividend policy (DIVPAY) in Korea is negatively correlated with financial leverage (COLEVE) and earning volatility (EARVOL) while positively correlated with the rest of the explanatory variables.

To assess for multicollinearity, as a general rule, serious and problematic multicollinearity issues arise when correlation coefficient “r” exceeds .9 or variance inflation factor (VIF) equals 10 (Asteriou & Hall, 2007). A probe of the correlation matrices of both Japanese and Korean data (Tables 4 and 5), we conclude that data is not suffering from serious multicollinearity issues.

Regression Results for Japanese Firms.

Note. Robust standard errors in parentheses.

p < .01. **p < .05. *p < .1.

Regression Results for Korean Firms.

Note. Robust standard errors in parentheses.

p < .01. **p < .05. *p < .1.

Regression Output

Tables 4 and 5 report regression results of the impact of firms’ internal attributes on dividend-paying behavior in Japan and South Korea. In both tables, the Breusch-Pagan LM test is strongly robust, thus rejecting the possibility of zero cross-sectional variance (homogeneity assumption) across units. Hence, due to the high robustness of the Breusch-Pagan test and the very restrictive nature of cross-sectional homogeneity in panel data, we are not reporting pooled OLS results or a common constant model. In both tables, the high robustness of Hausman-Chi2 indicates the negation of independent distribution of entity-specific effects. This means that the fixed effects model is appropriate for explaining the impact of explanatory variables on dividend policy in Japan and Korea. Regression results from the fixed-effects model are reported for Japan and Korea along Hausman-Chi2 in their respective tables.

Positive and robust regression coefficients on firm size (LOGSIZE) in column 1 of both tables suggest that larger firms in Japan and Korea pay more dividends to their shareholders than smaller firms. This substantiates hypothesis H1 for both countries. This particular relationship is the same in both countries, consistent with life-cycle and agency cost theories. Several empirical studies (e.g., Fama & French, 2001; Manneh & Naser, 2015; Sawicki, 2009) also verify that larger firms are better positioned to pay higher dividends.

The significantly negative coefficient of profitability (COPROF) in column 1 of Table 4 suggests precisely the opposite of what the signaling and agency theory predicts in the Japanese context. This rejects Hypothesis H2 and implies that highly profitable Japanese firms pay low cash dividends (retain more and distribute less). A possible reason for this behavior may be the Keiretsu structure, where there is low information asymmetry due to the close relationship between lenders and borrowers. As a result, profitable firms feel no need to pass signals about future prospects by paying higher dividends. There is also a possibility that the financial crisis 2007–2008 has decreased the responsiveness of cash dividends to earnings. Empirical studies (Ho, 2003; Morakinyo et al., 2018) report a similar impact of profitability on dividend-paying behavior. On the other hand, the regression coefficient of profitability (COPROF) for the Korean sample firms (column 1 in Table 5) is significantly positive and in line with prior literature (Ain et al., 2021; Arsyad et al., 2021). This implies that profitability is considered an important positive attribute of dividend policy in the Korean non-financial sector. The theoretical justification for this relationship may be signaling of good future prospects, mitigation of agency costs of free cash, or reduction of wealth expropriation effects. Thus our hypothesis H2 substantiates in the case of Korea.

Transaction cost theory implies that heavy financial leverage is expected to negatively influence dividend payments. A substantial portion of debt in capital structure is indicative of firms’ reliance on external financing. This can make payouts difficult for firms (Gugler & & Yurtoglu, 2003). The negative coefficient of corporate leverage (COLEVE) in Japan (column 1 of Table 4) and the positive coefficient in South Korea (column 1 of Table 5) imply a different impact of leverage on dividend policy. However, in both cases, the effect is trivial and insignificant. Therefore H3 is not validated in either case.

Generally, firms need for financing increases as investment opportunities arise. Consequently, the dividend payout is expected to decline. However, insignificant positive coefficients of growth (GROWTH) in column 1 of Tables 4 and 5 suggest that growth opportunities have no significant impact on the dividend policy in both countries. Thus H4 doesn’t validate life cycle theory and empirical findings (Gaver & Gaver, 1993; Smith & Watts, 1992) in Japanese and Korean contexts. The rationale may be that Japanese and Korean firms decide dividend policy independent of investment policy. Many empirical studies (Amidu & Abor, 2006; Partington, 1983) suggest that firms use target dividend policy independent of financing and investment decisions. Previous empirical results (D’Souza & Saxena, 1999) also report a positive dividend-growth relationship.

Similarly, negative and highly significant coefficients of earning volatility (EARVOL) in column 1 of both Tables 4 and 5 suggest that both Japanese and Korean firms restrict payouts when earnings volatility (EARVOL) is higher. This validates hypothesis H5 and previous results (Attig et al., 2021; Prakash & Yogesh, 2021) in both countries. This implies that Japanese and Korean firms avoid aggressive and costly signaling. These findings are in line with empirical studies (Alli et al., 1993; Amidu & Abor, 2006; Kowaleski et al., 2007; McCabe, 1979), which suggest that earning variations cause restriction of dividend payout due to the possibility of exposure to financial distress.

The coefficients of corporate tax (CORTAX) in column 1 of Tables 4 and 5 suggest that corporate tax has a positive relationship with dividend payouts in Japan, but this relationship is negative in South Korea. However, this relationship is insignificant in both cases and does not validate H6.

The free cash flow hypothesis suggests that increased free cash flow induces managers to take risky projects. As a consequence, information asymmetry and agency costs increase. Thus payment of dividends acts as a mitigation mechanism of agency costs and information asymmetry. Therefore, under the agency framework, higher cash flows are directly associated with dividend payout ratios (Fairchild, 2010; La Porta et al., 2000; Sawicki, 2009). The negative regression coefficient of cash flows (CASHFL) in column 1 of Table 4 suggests that Japanese results contradict the theoretical justifications based on agency costs and information asymmetry. The reason may again be low agency costs and information asymmetry in the Japanese system due to interlocking shareholdings. However, this relationship is insignificant, and hypothesis H7 does not hold in the Japanese case. The same relationship is not only reversed but robust as well in the Korean case. Column 1 (Table 5) suggests a positive coefficient on Korea’s cash flows (CASHFL). This implies that Korean firms pay more dividends when cash flows are high. These results justify that Korean firms payout more to tackle agency costs and information gap issues when cash flows are high. Hence, hypothesis H7 holds true in the Korean case.

Conclusions

This study aims to examine how the dividend policy of the firms in two of the largest economies of East Asia is determined by the internal attributes of firms. Firm-level data for 1,773 Japanese and 1,035 Korean firms were collected from WorldScope during the 2009 to 2017 period. The analysis was carried out using panel data techniques.

The results provide important insights into dividend policies in Japan and Korea. Larger firms in both countries are paying higher dividends than smaller ones. This particular relationship is almost the same in the Anglo-Saxon context. Both life-cycle theory and agency cost theory support this relationship. However, profitable firms in Japan pay lower dividends, whereas those in Korea pay higher dividends. This implies that Japanese firms are either facing low information asymmetry (agency costs) or managers in those firms feel no need to pass signals about future prospects. Another possibility of a negative profitability-dividend relationship may be that the financial crisis 2007–2008 has decreased the responsiveness of cash dividends to earnings in Japan. The negative profitability-dividend relationship in Japan is not consistent with the free cash flow hypothesis. On the other hand, the positive profitability-dividend relationship in Korea is in line with the free cash flow hypothesis. This implies that Korean firms have higher information asymmetry and agency costs, and managers feel the need to mitigate these issues by paying higher dividends. This study also suggests that both Japanese and Korean firms pay low dividends when earning volatility is high. This implies that firms in both countries avoid costly or aggressive signaling. Further, free cash flow has no significant impact in the Japanese context, but firms pay higher dividends in Korea when cash flows are higher. This again points to higher agency costs and information gap issues in the Korean case. Overall, the results suggest both similarities and differences in the dividend policies of Japan and Korea. Korean firms’ dividend policy resembles more than those in Anglo-Saxon countries, while dividend policy in Japan is to some extent different.

The findings of this study offer important implications for various stakeholders. Transnational studies are important to draw parallels and differences. From a theoretical point of view, this study highlights the need to look deeper into different contexts and investigate similarities and differences among different countries and their underlying reasons. The findings of this study may also help investors’ clientele design their investment policies in both countries. Overall, the results pave the way for a theoretically enriched understanding of dividend policy by comparing and contrasting diverse financial systems.

With the growing flow of information, future research on dividend policy may extend by adding unique characteristics of Japanese and Korean corporate governance such as board composition, power structure, and firms’ affiliation to different groups for an in-depth understanding of dividend policy in both countries.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.