Abstract

In today’s dynamic market environment, information technology (IT) enables firms to obtain knowledge they need to achieve superior performance. To this end, the present study explores the effects of IT, absorptive capacity (ACAP), and dynamic capabilities (DCs) on firm performance (FP) by employing empirical research design. In addition, the study focuses on the DCs perspective and ACAP as a firm knowledge-based view focusing on those firms where technology involved in either a particular unit of the firm or as a whole in operational processes. The data (total 241) was analyzed through AMOS, a mathematical analysis methodology focused on structural equation modeling (SEM). Moreover, through Sobel test we further verify the indirect impact of IT on FP.

Introduction

Recently, firms made significant advancements in network technology and information systems (IS) as a result of increased digital business strategy. As a result, traditional business strategies are being reshaped by accepting innovations in the context of a resource-based view (RBV) approach (Garcia-Morales et al., 2018). The utilization of IT and its infrastructure has played a crucial part in the firm’s long-term development; nevertheless, only a few studies have found the value of IT in achieving superior performance. In addition, ACAP which is frequently perceived as a firm’s information-based perspective, not only acquires and utilizes external knowledge to enhance the firm’s innovation activities, but it may also impacts the firm’s internal structure for the advancement of operational tasks and business performance. It is impossible for firms to incorporate and implement external expertise in the absence of ACAP (Khan et al., 2017a). In literature, limited studies investigate the relationship between IT and ACAP, even though IT utilization and infrastructure are the important factors in the firm’s development, especially for SMEs (Chang et al., 2018).

Firms will only succeed if they improve their environmental consciousness both internally and externally (Teece, 2016). DCs must be built to incorporate and reconfigure internal and external competencies to counter major developments in the firm’s work environment (Khan et al., 2019; Teece et al., 1997). Unfortunately, very few studies address this relationship (Simon et al., 2015), and much of the literature has been rooted in a single case study (Grant & Verona, 2014). Based on these findings, we have conducted an empirical research focusing on the relationship between IT, DCs, and FP in the view ACAP as a mediator.

The main motivation of the study is a limited research in the relationship between IT and ACAP. In order to provide the better understanding of FP, this article uses as a basic study to explore the factors involved in FP by providing empirical evidence of IT, ACAP, and DCs influencing FP. Second, having strong IT team with dynamic capabilities to handle latest technologies and a bulk of information will enhance the performance. As a result, this study employs an empirical technique to validate and assess the relationship of IT, ACAP, and DCs of FP. thus, the current study is a unique and first attempt to address the query. The current thesis deal with the following question.

What is the role of information technology to achieve firm performance in a dynamic work environment?

What is the role of absorptive capacity to achieve firm performance in a dynamic work environment?

What is the role of dynamic capabilities to achieve firm performance in a dynamic work environment?

Theoretical Background

The present study is based on dynamic capability theory, an extension of the resource-based view (RBV), and ACAP as a knowledge-based view of the firm. DCs are essential to recognize, evaluate, and analyze new opportunities in the workplace. According to DC theory, markets are more dynamic, and firms differ in the capacities they acquire and employ diverse resources. These discrepancies explain for inter-firm’s variation in performance over time (Wang & Kim, 2017). Teece et al. (1997) describes DCs as higher-order capacities for the selection, development and coordination of ordinary capabilities, that is, sensing, seizing, and transforming. These capabilities also allows firms to transform information based their requirements. It also promotes learning and experimentation, recombines resources for the creation of new goods, and transforms existing systems (Jiang et al., 2018) all of which increase the firm’s performance. A firm with DCs can integrate and redeploy knowledge sources to achieve higher performance. Previous studies accepted that DCs can lead the firms to achieve higher performance (Khan et al., 2021). Acquiring, assimilation, and development of new knowledge is necessary to upgrade operational capabilities with new knowledge and skills (El Sawy & Pavlou, 2008).

Changes in the dynamic environment will have an impact on the creation, search, and dissemination of knowledge, which has been recognized as an improved indicator of knowledge creation capability (Denford, 2013). In such cases ACAP serves as a knowledge-based view of the firm. ACAP is a multidimensional framework for which various scholars have identified different aspects and measures. Some studies have linked ACAP to organizational learning (Lane & Lubatkin, 1998), innovation (Guisado-González et al., 2017), and DCs (Andreeva & Kianto, 2012) by offering RBV (Barney, 1991), and Knowledge-based view (Sasson & Douglas, 2006). Cohen and Levinthal (1990) described ACAP as a collection of processes involved in knowledge acquisition, assimilation, transformation, and exploitation of knowledge (Zahra & George, 2002). The capacity of a firm to investigate and recognize the knowledge required by an organization is referred to as acquisition capability. Once the knowledge has been identified, it may be translated in accordance with organizational requirements (Daspit & D’Souza, 2013). Secondly, the ability to acquire new knowledge is also known as assimilation ability. It encourages corporations to analyze and interpret newly acquired knowledge in term of existing knowledge (Jansen et al., 2005). Thirdly, the ability to adapt to new knowledge and integrate existing knowledge with new possibilities is known as the transformation ability. Finally, knowledge exploitation involves leveraging knowledge to produce value for firms and customers (Daspit & D’Souza, 2013).

Hypothesis Development

Information Technology and Absorptive Capacity

In this study, we offer IT as a source for fostering knowledge processes at the organizational level. IT provides many implementations to establish more resilient contact networks and a better connectivity to external knowledge (Bolívar-Ramos et al., 2013). However, rich knowledge structures may be developed through inter- and intra-organizational knowledge sharing, whilst powerful IT platforms can add innovative potential to the firms (Srivardhana & Pawlowski, 2007). These capabilities include knowledge infrastructure capabilities such as technology framework and technology culture, as well as knowledge processing capabilities, such as acquisition, transformation, application, and knowledge security, which develops the base of organizational knowledge. These capabilities improve the firm’s capacity to recognize, assimilate, and apply new knowledge (Gold et al., 2001). An IT application, on the other hand, provide quick and easy access to external knowledge while also opening up new and more intensive communication channels (Corso et al., 2003). Interaction between organizational members can be fostered through the use of technology-based resources such as emails, chat, video conferencing, web-based cloud systems, and instant messaging, which encourages knowledge collection processes (Bolívar-Ramos et al., 2013). These technologies enable knowledge to be gained and disseminated inside the firm and teams that participate in interdependent activities, as well as to gather more information for the organization (Griffith et al., 2003). IT broadens the breadth of knowledge processes for transferring expertises (Young-Choi et al., 2010), and it is expected that expanding IT use would improve organizational ACAP to achieve firm’s performance. Thus, we argue that:

H1: Information technology positively influence on firm’s absorptive capacity

Information Technology and Dynamic Capabilities

DCs are skills that enable an organization to build learning and knowledge management processes. Zaidi and Othman (2014) suggest that in times of significant technical and market instability, it is important to connect technology management with DCs. According to Kyläheiko and Sandström (2007), firms must manage market dynamics and technological volatility to maintain competitive advantages. Aside from firm effectiveness, managers are the key individuals for effective information availability (Dwivedi & Madaan, 2020), demonstrating the relevance of dynamic capabilities of managers in firms. According to the literature on IT architecture flexibility, coevolution is the key tenant of IT-enabled dynamic capabilities, which means flexibility in the line-up of IT resources (Mikalef et al., 2021). Together, information technology and its dimensions enable firms to improve their IT dynamic capabilities which help in the improvement of organizational processes (Mikalef et al., 2016). Literature has also identified IT-enable DCs, which support the firm’s evolutionary fitness by increasing agility that leads to improved firm performance (Mikalef & Pateli, 2017). In this article we address IT at firm level to support DCs sensing (SN), seizing (SZ), and transforming (TF). Employees may use IT to integrate existing knowledge across firms, harness creative thoughts and strategies, help in the connection of various disciplines, and exchange ideas with known and unknown personalities (Plattfaut et al., 2015).

IT is a critical component in the DCs context, supporting software in inter-functional collaboration and co-ordination of knowledge in practice; this is dependent on the firm’s ability to facilitate integration mechanisms that support local (function-based) and global (computer-embedded) levels of knowledge and activity (Sher & Lee, 2004). These processes often play a crucial role in the generation and maintenance of DCs. The preceding explanation illustrates the significance of IT in searching for and absorbing external knowledge that is available in the workplace to improve DCs; thus we propose the following hypotheses:

H2: Information technology positively influence on firm’s dynamic capabilities

Absorptive Capacity and Firm’s Performance

Previous research linked ACAP to a variety of corporate sectors, with some of them delving into the organizational learning perspective. In this study, we aim to provide ACAP as view of firm’s efficiency. Researchers also noted that the over all aim of the firm is to improve its financial performance (Kim & Lee, 2010), and that improving the firm’s financial performance without ACAP is challenging. ACAP refers to knowledge obtained from external sources (Cohen & Levinthal, 1990); hence, ACAP has helped in the maintenance of firm’s performance in highly volatile markets (Lane et al., 2006; Zahra & George, 2002). Firms must regulate each dimension of ACAP concurrently with their achievement to achieve performance development (Zahra & George, 2002).

The authors also referred two subcategories of ACAP, Potential absorptive capacity (PACAP), and realized absorptive capacity (RACAP), both of which impact a firm’s competitive advantage and performance. PACAP is responsible for the development and assimilation of external knowledge to facilitate the organization to produce new knowledge. PACAP alone will not suffice to achieve higher performance until it is turned into RACAP by incorporating new knowledge into products and processes (Murray & Peyrefitte, 2007). Firms with higher ACAP levels will better understand and utilize the current knowledge to facilitate their innovation activities (Tsai, 2001). Without ACAP, the firm’s ability to absorb and transmit knowledge from outside sources will be limited. As a result, effective internalization of external experience will improve the firm’s development and success (George et al., 2001). Dobrzykowski et al. (2015) suggests that the firm’s overall objective is to optimize financial efficiency by raising the variance of client needs, making a significant commitment to improved information management capabilities, and consistently developing the links between IT and customers. In addition, the authors contend that the firm’s financial performance is linked to its knowledge processing practices. Since this study investigate the influence of ACAP on FP by employing all ACAP measurements to obtain superior performance. With these dimensions, the firm may create expertise by integrating new and established knowledge in accordance with its job requirements. Therefore, we offer the following hypotheses:

H3: Absorptive capacity positively influence on firm performance

Dynamic Capabilities and Firm’s Performance

By maintaining FP via innovation, DCs increases the capacity to be better positioned to scan opportunities in a competitive market (Yoshikuni et al., 2021). Firms with dynamic capabilities can respond with opportunities and challenges by expanding, changing, and producing first-order changes (Hoopes & Madsen, 2008). DCs is conceptualized differently in information system literature owning to their approaches, for example, DCs ACAP is one form of DCs or ambidexterity that can encompass of the three capabilities (sensing, seizing, and transforming) (Steininger et al., 2021). DCs are the firm’s processes that utilize resources, that is, integrated for reconfiguration, procurement, and release of resources in order to balance and also establish demand transition (Peteraf et al., 2013; Ringov, 2017). DCs have been viewed as a strategic option that allows firms to shape their existing functional competencies when the opportunity or demand arises (Pavlou & El Sawy, 2006). DCs are related to the firm through a number of aspects, including their impact on the firm’s performance by allowing challenges to be explored through the implementation of new processes, products, and services (Makadok, 2010). Similarly, these capabilities increase the firm’s pace, productivity, and efficiency in adjusting to the environment (Tallon, 2008). Furthermore, it improves the firm’s ability to deal with environmental change and effectively affect FP by allowing the company to capitalize on revenue-enhancing opportunities while reducing costs. Last but not least, offer a firm with previously unavailable choice options and the potential to allow higher-performance contributions, such as increased sales or profits (Drnevich & Kriauciunas, 2011). Eisenhardt and Martin (2000) discovered that DCs may evolve by increasing conventional capabilities—expanding existing resource configurations in such a way that results in completely new sets of decision options. According to DCs literature, the effect of DCs may not be automatic. Thus, DCs should be positively correlated to competitive advantage and performance (Pezeshkan et al., 2016). Furthermore, DCs stimulate firm’s sensing capabilities, allowing them to be more creative in their product and service offering; by acquiring knowledge from the web, raising revenue and financial performance, improving information and knowledge, and stimulating the firm’s innovate measures (Hang et al., 2014). However, product innovation is driven by knowledge flow to provide financial performance (Zahra & Hayton, 2008). As a result, the preceding discussion demonstrate the direct and indirect relationships (Pavlou & El Sawy, 2011) between DCs and FP. Despite existing literature that uses DCs to analyze organizational environment and its influences on firm’s innovation, we associated DCs with FP. Firms that use DCs improve their performance more than that do not have these capabilities. Therefore, we argue that:

H4. Dynamic capability positively influence on firm performance

Absorptive Capacity and Dynamic Capabilities

According to Zahra and George (2002), research reveals the ability of ACAP to generate DCs, where the four suggested capabilities—acquisition, assimilation, transformation, and utilization are integrated, and together they produce complex organizational capabilities. The authors describe ACAP as a capability for producing DCs, emphasizing the construct’s strategic character. The authors discuss that how the four capabilities generate and modify expertise to build additional operational capabilities. Research demonstrates that these capabilities allow firms to gain a competitive advantage and increase their performance (Zahra & George, 2002). ACAP deals with the evaluation and utilization of external knowledge, that is, learning with potential partners, integrating external information and transforming into ingrained capability within the organization (Alves et al., 2016), allowing firms to respond inefficient way to strategic changes (Sun & Anderson, 2008). In addition, Zahra and George (2002) consider ACAP to be a DC in and of itself. In this article, we are presenting ACAP and its effect on the firm’s DCs. Firms can only improve their capabilities if they have effective knowledge management. ACAP enhances knowledge management capabilities in terms of acquiring and transforming knowledge to meet the needs of the firm. Therefore, we argue that:

H5: Absorptive capacity positively influence on firm’s Dynamic capabilities

Information Technology Support the Firm’s Performance

IT and its impact on FP is growing research area (Peng et al., 2016; Wu et al., 2015), which not only draws the interest of executives and decision makers, but also developers and funding agencies (Ilmudeen & Bao, 2018). IT is a critical enabler for gaining strategic flexibility since firms rely on IT to cut costs, automate processes, and improve job performance (Bhatt & Grover, 2005). Bharadwaj et al. (2013) argued that IT encourages firm’s business models, supports or transforms policies and strengthens relationships between firms, partners, and consumers. It offers advanced computational capability in firms as well as various capabilities such as knowledge management, analytical, and enhanced empowerment capabilities, allowing them to enter new markets and develop new business approaches. According to Ilmudeen and Bao (2018) good IT management contributes to FP by coordinating operations across various units, simplifying operational processes, reducing development costs, organizing units, managing IT properties, and allocating IT assets on time (Wang et al., 2015). IT has been proven in a large group study of manufacturing firms to promote the development of firm profitability by enhancing their inventories (Shah & Shin, 2007). Firms that use web-based technology to expand their online sales channels, realizing synergies between online and offline sales channels, and expanding into the global market (Wu et al., 2017). Classical studies define the relevance of IT to the viability of firm profitability and address their direct relationship (Shin, 2001). For example, in early research, Cron and Sobol (1983), analyze the effect of IT expenditure on the financial output of wholesale medical suppliers . Markus and Soh (1993) investigate the relationship between a variety of IT-related steps, such as expenditure, computerization optimization, the share of IT services, and firm profitability. Rai et al. (1997) investigate IT investments for firm performance by using three types of IT investments, aggregate IT, client/server system, and IT infrastructure, and three types of performance measures firm-out, economic, and intermediate (labor/organizational productivity) performance. Keeping these classical and modern studies in view, we argue that,

H6: Information technology positively influence on firm’s performance

Mediating Role of Absorptive Capacity

According to the literature from the early 1990s, knowledgeable firms know where new opportunities can be found and how to exploit them (Cohen & Levinthal, 1990); however, unless they are willing to take advantage of these opportunities (Pérez-Luño et al., 2011). This might explain why some firms can acquire and assimilate knowledge produced form outside but are unable to utilize it to create innovation (Caccia-Bava et al., 2006). In addition, Tsai (2001) claimed that ACAP could mitigate complicated problems and improve firm’s capacity to recognize and respond to new opportunities. Researchers from the early 2000 established the connection between ACAP and FP (Liao et al., 2003). ACAP, they added, is a complex set of knowledge-based activities. The relationship between knowledge flow and ACAP (George et al., 2001), and ACAP is linked to firm performance (Daspit et al., 2014).

The role of PACAP and RACAP are not mutually exclusive, but rather complementary. Both ACAP subsets co-exit and learn to improve the FP. In addition, firms may acquire and assimilate knowledge, but they may lack the ability to transform and leverage that knowledge. Therefore, a high PACAP does not inherently mean an increase in performance. The transition is included in RACAP (Khan et al., 2017b) and exploiting the acquired knowledge by integrating it into the activities of the firm. PACAP can be viewed as an accumulation of new knowledge, whereas RACAP can be considered as a mechanism for the exposing and implementing this valuable knowledge. It is also highly advisable to store and preserve newly-generated knowledge within the organization, thus enabling the accessibility for the organizational participants that leverage it. Otherwise, RACAP will be destroyed as well as the valuable knowledge (Leal-Rodríguez et al., 2014). Recent IT research has focused on the influence of ACAP on the FP in both the public (Khan et al., 2017a) and private sectors. In addition, the development and use of ICTs inside an organization provides an intelligence channel to promotion of ACAP-related knowledge, including assimilation, acquisition, transformation, and exploitation (Bolívar-Ramos et al., 2013). According to the preceding explanation, IT has positive impact on ACAP and ACAP has a positive impact on FP. Therefore, we predict that:

H7: ACAP has a positive mediating role between information technology and firm performance

Based on the above literature, we proposed a research model providing a relationship between IT, ACAP, DCs, and FP. More specifically, we empirically investigate these relationships and their influence on FP.

Method

Prior studies are used to establish context for relationships between the variables in this study (Bhatt & Grover, 2005; Cohen & Levinthal, 1990; Duncan, 1995; Makadok, 2010; McDermott, 1999; Zahra & George, 2002). Figure 1 depicts the proposed model, in which FP is viewed as a dependent variable, while IT is viewed as an independent variable, ACAP and DCs are either influenced by IT or effect FP. H1 predict the impact of IT on ACAP, H2 predict the effect of IT on DCs, H3 predict the impact of ACAP on FP, H4 predict the influence of DCs on FP, H5 predict IT’s impact on FP, and H6 predict the influence of ACAP on DCs. Whereas, ACAP act as a mediator between IT and FP. In this study we follow (Anderson & Gerbing, 1988), Confirmatory techniques to test the measurement and structural model (Garver & Mentzer, 1999) and Analysis of Moment Structure (AMOS) 24.0 to validate our results and support the predicted hypothesis

Conceptual model.

Process

For this study, a structural questionnaire based on prior studies was used to collect data. The target group was selected as the initial stage in testing the aforementioned hypothesis. IT officers, IT executives, IT directors, IT managers, business managers are all included in the targeted group. The study used a Likert Scale ranging from 1—strongly disagree to 7—strong agree. A total of 241 samples were obtained from respondents who represented their firms. Table 1 shows the demographic information for the samples. We gathered data from private firms locating in different geographic location in China, that is Anhui Tary Tongda Mechanical & Electrical Co., Ltd located in Hefei, Anhui; and Anhui Quanmeng Electric Power Technology Co., Ltd, Youfei High Tech Zone. The survey was conceived and maintained in English language before being translated into Chinese language by Chinese natives. In the knowledge management industry, these translators serve as professors. This process was followed to ensure a reliable translation by the professors familiar with the concepts of information management. The questionnaire was then sent online to the intended demographic, with each item being obligatory to eliminate missing values. We utilized this approach to minimize the cost of paper while maximizing rapid responses (Kaplowitz et al., 2004). The questionnaire comprised an introduction, the study’s goal, and respondent confidentiality (Hsu et al., 2007).

Demographic Details of Sample (N = 241).

In Figure 1, we followed Zahra and George (2002) study to measure ACAP in four dimensions: acquisition, assimilation, transformation, and exploitation. DCs are measured by three dimensions “sensing, seizing, and transforming” (Teece, 2007). Moreover, Firm performance demonstrates the firm’s financial measurements, namely Sales and Market share (Dobrzykowski et al., 2015) of the firm.

Measures

For this study, the measurement items were adopted from past research and modified according to the current study.

Dependent variables

Firm performance is a dependent variable in this study. We analyze FP based on financial indicators, that is, “Sales and Market share”—using three items to gage overall FP were adapted from Dobrzykowski et al. (2015). These three items reflects the degree to which the firms improve their sales market share (α = .900). The three items were averaged as an overall FP measure.

Control variables

In our study, we used three control variable: industry type (i.e., service or manufacturing), we treated the type of industry as a dummy variable, for example, 1 indicates the service industry and 2 indicates the manufacturing industry (Liu et al., 2013). The age of the firm range from less than 1 year to more than 20 years. Firm size necessary for the firm’s abilities and performance (Zhou & Li, 2010). As a result, we measured firm size as a control variable, counting the number of full-time employees starting from less than ten employees to more than 1000 employees. We considered size as a control variable since larger firms will gain access to more information as more employees obtain higher data rates and distribute the higher rate of knowledge in the firms to perform routine procedures, while a smaller number of companies would be more agile and be able to create DCs faster. We have controlled the company age as older firms have great experience in the work environment, and workers in these firm know where the knowledge is be gathered and how information is processed to achieve high performance. One the other, younger firms are more enthusiastic about their performance and work harder, whereas older firms trail them in numerous ways. This process helps them to benefit about the knowledge they obtain in the work environment.

Independent variables

In our study, three independent variables are effecting FP. First, IT is assessed using a scale adapted from prior literature (Duffy, 2000a; Nonaka & Takeuchi, 1995). The measure contains four items that reflect the overall impact of IT on the FP (α = .905).

Second, ACAP is measured by using the scale adapted from Flatten et al. (2011). The scale contains a total of 11 items that are oriented to measure the four dimensions of ACAP, that is, acquisition measured by three items, assimilation measured by three items, transformation measured by three items, and finally exploitation measured by two items. These four dimensions reflect the firm’s total knowledge processes (α = .936). Third, we utilized measures adapted from Plattfaut et al. (2015) and Pöppelbuß et al. (2011) for DCs. DCs are measured in three subcategories in this study: SN, SZ, and TRF, each measure include two items. These three measures of DCs are reflecting the dynamic capabilities of the firm (α = .913). Please see Appendix 1.

Data Analysis

Before using structural equation modeling (SEM) for the predicted hypothesis, we performed an exploratory factor analysis (EFA) and confirmatory factor analysis (CFA) to validate the psychometric validity of the survey construct (Churchill & Jr, 1979). We used SPSS 25.0 to test EFA and AMOS 24.0 to analyze CFA and the research model.

Exploratory Factor Analysis

Before applying any statistical technique on the data sample, we applied EFA to ensure that all items load into their respective measures, that is, IT, DCs, ACAP, and FP. EFA is used for items which are less than .40 and cross loading on two or more variables at ≥.40. The reliability analysis should indicate an item-to-total correlation of over .40. Table 2 summarizes the construct factor loadings and illustrates that the loading of all elements on a single factor suggests one-dimensionality.

EFA of Study Construct.

Note. IT = information technology; ACQ = acquisition; ASSI = assimilation; TRF = transformation; EXPL = exploitation; SE = sensing; SZ = seizing; TRF = transforming; FP = performance.

As a result, the fact that no item had multiple cross-loadings supports the scale’s preliminary discriminant validity. To assess convergent validity, we used Cronbach’s alpha, composite reliability (CR) of constructs, and average variance extracted (AVE). Table 2 reports, Cronbach’s alpha verified from .900 to .936, significantly above the benchmark of .70 (Liu et al., 2013). These findings indicate that the measurement model’s convergent validity is adequate.

Confirmatory Factor Analysis

CFA denotes a suitable reliability measuring approach for theoretical construct space (Chin & Todd, 1995) by demonstrating the connection between the observed items and the construct they measure. We initially examine each component’s convergent validity using within-scale factor analysis before comparing the item load to the suggested minimum value of .60 (Chin et al., 1997). Table 2 describes the loading of the items and demonstrates that all of the measures are significant on their path loading, indicating satisfactory convergent validity. Furthermore, Table 3 also presents the loading of the measurements, which can also be seen in Figure 2.

Factor Loading and t-Values.

Amos loading.

We carry out a multi-collinearity test since the multiple inter-constructs in Table 4 exceed the .60 benchmark. The thumb rule for estimating multicollinearity is whether the variance inflation factor (VIFs) is >10 or <0.10. The results reveal that the highest and lowest VIF are 2.378 and the 1.008 respectively, indicating that multi-collinearity was not a problem.

Model Validity Measures.

***p < .001.

Results

Using Amos, we assessed construct reliability (CNR) and average variance extracted (AVE), which represents the internal consistency of the indicators measuring in the given construct (Fornell & Larcker, 1981). Table 4 describes all the values for composite reliability (CR) are above the benchmark .70, showing adequate reliability (Nunnally & Bernstein, 1994). Furthermore, the AVE values are above benchmark .5 (Huang et al., 2013). The maximum shared variance (MSV), and maximum reliability (MaxR (H)) is above .70 and presenting a significant correlation between the measurements.

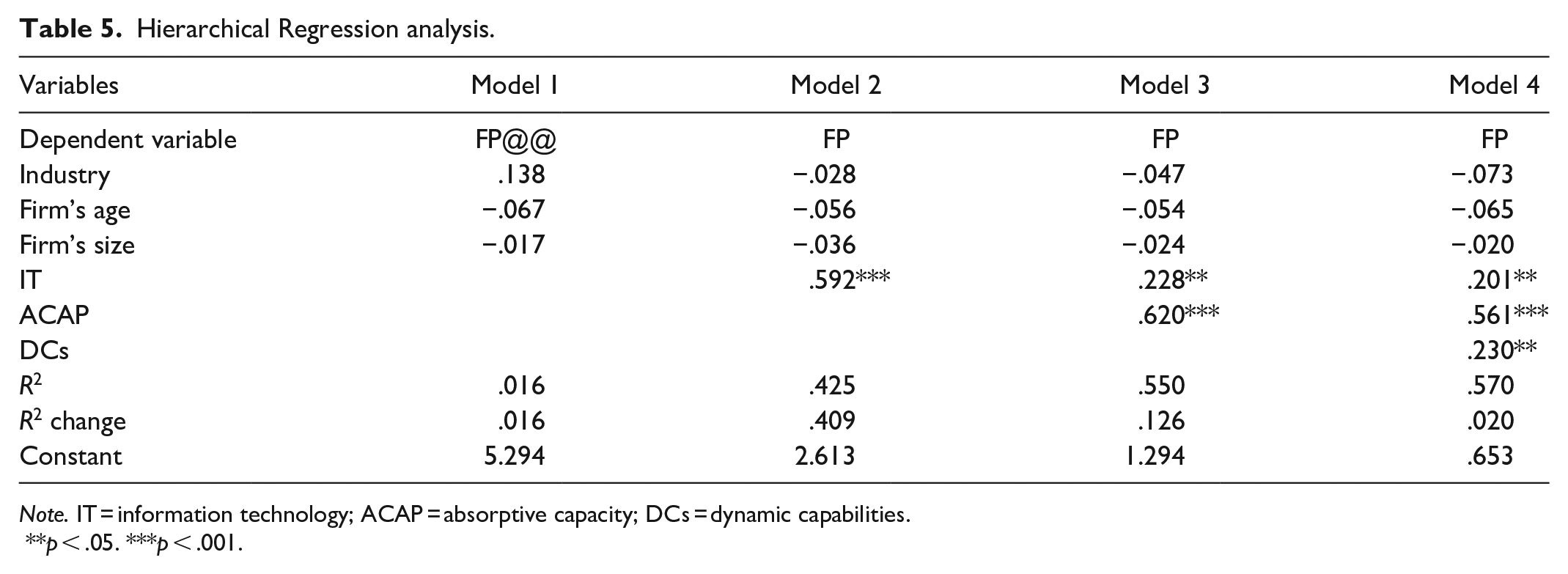

Table 5 shows the FP as a dependent variable; in Model 1 we test the relationship between control variables industry (service and manufacturing), firm’s age, firm’s size, and FP. however, we did not find a significant relationship between control variables and FP. Model 2 presents the positive relationship between IT and FP (β = .592, p < .01). Model 3 demonstrate the relationship between IT, ACAP, and FP β = .228 p < .05, β = .620 p < .01 respectively. Whereas, Model 4 demonstrate the positive relationship between IT, ACAP, DCs, and FP β = .201 p < .05, .561, p < .01, and .230 p < .05 respectively.

Hierarchical Regression analysis.

Note. IT = information technology; ACAP = absorptive capacity; DCs = dynamic capabilities.

**p < .05. ***p < .001.

Model Fit Indices and Hypotheses Testing

Table 6 presents the overall model of fitness of the proposed variables. The results show that chi-square normalization by degree of freedom (χ2/df) is 1.747 which should be less than 5, Comparative Fit Index (CFI), Incremental Fit Index (IFI), and Normed Fit Index (NFI) should be ≥.9 (Bentler, 1983, 1988; Bollen, 1989a; Browne & Cudeck, 1993). Moreover, the result shows .957, .957, and .905 for, CFI, IFI, and NFI respectively, which are significant values as per criteria (Browne & Cudeck, 1992). The commonly accepted value of root means square error of approximation (RMSEA) should be ≤.08 (Dudgeon, 2004; Jöreskog & Sörbom, 1993). Adjusted goodness of fit index (AGFI) should be ≥.8, for current model RMSEA is .056 and AGFI is .842, which shows the significant values and support the proposed model.

Model Fit Indices.

Hypotheses testing

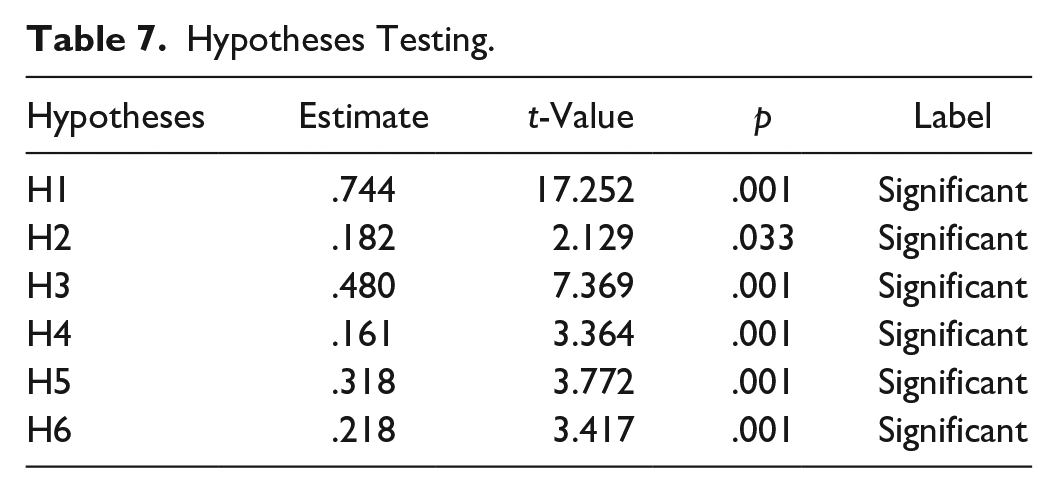

Table 7 presents the hypotheses that were tested; the first hypotheses predicted that information technology would have an impact on the absorptive capacity for knowledge processes. As predicted, IT has an influence on ACAP (β = .744, p < .001), therefore H1 is supported. We also predicted that IT will have a positive influence on DCs (β = .182, p = .033), and the findings reveal a significant relationship between these variables, supporting H2. The authors also predicted that ACAP has a positive influence on FP (β = .480, p < .001), which is corroborated by the data and confirms H3. As predicted earlier, DCs have a positive influence on the FP, and the data in Table 6 demonstrate (β = .161, p < .001) that support H4. We also predicted that ACAP has a positive influence on DCs (β = .318, p < .001), and our findings corroborate this relation and H5. Finally, we predicted that IT would have a positive influence on FP; the data reveal that IT has a significant impact on performance (β = .218, p < .001), confirming H6. Using AMOS 24.0, Figure 3 depicts the overall connection of these variables. Our findings show that the control variables (industry, firm size, and firm age) had not effect on FP. This might be owing to the current study, which compares the FP to that of its major competitors. Small variations in the control variables between firms and their competitors might restrict their capacity to explain disparities in business performance.

Hypotheses Testing.

Results of the structural equation modeling.

The Indirect Effect of Information Technology on Firm Performance

Table 5 shows that there is a positive interaction between IT and FP, indicating that ACAP and DCs play a mediating role in this study. We followed Zhao et al. (2010) recommendations of Sobel tests (Sobel, 1982), and the bootstrapping mediation test (Preacher & Hayes, 2008), to examine the mediating impact of ACAP and DCs. Since the relationship between IT and FP is substantial, the authors identify a partial mediation role of ACAP and DCs. The Sobel test findings show that ACAP play a substantial partial mediating role (t-stat = 11.660, p < .001), and a significant partial mediating role of DCs (t-stat = 8.048, p < .001).

Studies Preacher and Hayes (2008) and Zhao et al. (2010) questions the proposed mediation test of Baron and Kenny (1986), highlighting the superiority of statistical tests such as bootstrapping procedures. In this study, we follows Preacher and Hayes (2008) recommendations and perform bootstrapping to examine the mediating relationship between IT and FP in depth. However, using Amos with 500 bootstrapping samples demonstrates the indirect mediation effect of the variables (Spiller, 2011; Zhao et al., 2010). Thus, the indirect path from IT to FP from ACAP is (β = .492), and the path from IT to FP from DCs (β = .193) has a 95% confidence interval, indicating that ACAP and DCs play a partial mediating role.

Discussion

The study’s goal is to define the value of IT in order to achieve higher performance. The report’s contribution focuses on six key areas. First, IT has a significant impact on ACAP, second, IT has a positive impact on DCs; and third, ACAP has a positive effective on FP. Fourth, DCs have a positive effect on FP; fifth, ACAP has a positive effect on DCs and, eventually, a clear impact of IT on FP. The robustness of the structural model results was validated using 241 datasets acquired from firms where IT plays a major or minor role in organizational activities. prior research has established these frameworks for competitive advantage generation (Zahra & George, 2002). However, few studies have been conducted to comprehend the relationship in an interconnected manner, that is, to determine how it interacts with and influences the FP. There is a lack of appropriate comprehension of this area of study as to whether and how IT supports the firm’s competencies and performance (Chen et al., 2017). Prior research focused on a subset of business activities, such as online procurement and customer services (Fink & Neumann, 2007; Jeffers et al., 2008). As a result, to investigate the aggregated impacts of IT on FP at the organizational level, we operationalized the construct performance improvements at the organizational level by two factors: sales and market share (Dobrzykowski et al., 2015). At the end the study provided (Appendix 2).

Findings and Theoretical Implications

According to our findings, IT has both a direct and indirect impact on FP; using IT firms will improve their financial performance. Our analysis focuses on IT as a critical component in gaining a competitive advantage and improving FP; implying that investigating IT in terms of the firm’s capabilities is a promising research direction. We believe that IT affects FP in terms of sales and market share. In this study, this argument was statistically proven (β = .218), demonstrating the importance of IT in achieving higher performance. IT tends to maximize individual autonomy and encourage centralization in the organization, where the dissemination of information becomes more comfortable and quick; when decisions from different sectors are made at once; the firm’s efficiency improves. IT facilitates internal communication and strengthens firm networking. As a result, the development of networks can also be associated to centralization in order to make the decision-making more manageable and to sustain FP. We concentrate primarily on the fundamental relationship between IT and FP, which is driven by our theoretical predictions. We demonstrate that organizations that rely more on IT have a substantial advantage in identifying the external knowledge that is required in the current situation through quick communication.

IT enables firms to fulfill the demands for more knowledge processing while also being more adaptable in their information processing. Due to the globalization, market challenges, need form innovation, and strengthening ACAP for firm performance (Maria Teresa Bolivar-Ramos et al., 2013), it is essential component for success in the recent era. IT is critical for creating and sustaining a firm’s ACAP (Roberts et al., 2012), as well as affecting the development of FP (Kostopoulos et al., 2011). Thus, when information and communication technologies are applied correctly, they provide significant opportunities for ACAP development (Roberts et al., 2012). Therefore, firms must examine this issue in order to remain competitive and enhance their performance (Jansen et al., 2005). IT does not improve productivity or business performance (Jean et al., 2008), but its practical implementation may improve both FP and competitive advantages (Dehning & Stratopoulos, 2003). In this vein, the current study adds to the literature by recognizing the significant direct and indirect effect of IT on performance, as well as the usage of IT in independent tasks on the development of ACAP and DCs. Our findings indicate that the use of IT facilitates the relation between individuals executing tasks on an interdependent basis and encourages information sharing beyond geographical boundaries (Rico & Cohen, 2005). IT is utilized to facilitate a rich exchange of knowledge and abilities (Alavi & Leidner, 2001). Thus, the current article provides both theoretical and empirical evidence that all of these processes have an influence on the development of ACAP. This finding is essential since ACAP is linked to the development of the FP (Kostopoulos et al., 2011). This article is also expending our understanding of the importance of ACAP in improving the FP. Prior research investigates ACAP as a facilitator for the organization to successfully acquire and utilize external knowledge, enhance its learning ability, adapt to business environmental changes, and innovate (Jiménez-Barrionuevo et al., 2011) to achieve superior FP (Kostopoulos et al.,, 2011). In order to analyze such relationship, our investigation provides both theoretically and empirically evidence that ACAP has a relationship with the firm’s financial performance. The findings support the argument that, besides acquiring external knowledge, firms need to exploit knowledge effectively to improve FP (Jiménez-Barrionuevo et al., 2011; Zahra & George, 2002). Over time, ACAP evolves with time, as Cohen and Levinthal (1990) argues, that the more a firm follow the ACAP processes, the more efficient the external acquisition of knowledge can be. This statement is consistent with our findings, which indicate that firms with low ACAP are unable to cope with external knowledge as successfully as a firm with a high-level ACAP. Moreover, in this study, we considered ACAP as a mediator, which enhance the capability of the firm in terms of knowledge processes.

Thus, this study represents that ACAP is a partial mediator between IT and FP, as well as a direct impact on FP. As it evaluates the firm’s knowledge capabilities, this article contributes to the firm’s knowledge-based view. furthermore, it assists us in improving our understanding of knowledge-related aspects that contribute to performance.

Finally, our study contributes to the literature on DCs. Prior research has focused on DCs in terms of innovation and enhancing firm’s knowledge capabilities (Zahra & George, 2002), despite from past studies, we analyze firm’s capabilities in terms of financial performance. The study adds to the existing literature on DCs by addressing their application both in both the service and manufacturing sectors. Previous studies has demonstrated a biasness toward products and technological innovation while ignoring firm financial performance. Furthermore, in this study, dynamic capabilities were identified as a key factor for FP. This article contributes to the literature by providing empirical evidence of DCs in service and manufacturing settings. Previous research has found that DCs are more closely connected to products, and that innovation is important. The point of departure for the study reported here is the proposition that in order to compete effectively in the market, firms must focus on their capabilities to stand out and perform well as compare to other market competitors. In testing hypothesis H4 (β = .161), we noted that DCs contributes positively to FP. This also illustrates the significant contribution of DCs to the firm on different levels. A firm with fewer DCs faces more challenges in managing knowledge, and delays in knowledge processes can have an impact on performance.

Furthermore, the impact of competition on the relationship between DCs and FP is a fundamental premise of DC theory. However, some researchers believe that context has an important effect (Teece, 2007; Teece et al., 1997), others believe that it does not (Zahra et al., 2006). We support the positive impact of DCs since the findings demonstrate a positive relationship, implying that firms may improve their performance by developing their capabilities, particularly in a turbulent environment. DCs allow firms to perform well during environmental changes; we identified several studies, for example, Makkonen et al. (2014) and Nair et al. (2014) support DCs and allow firms to perform better during financial crises.

Practical Implications

The study has some implications for business practitioners. First, organizations must adapt IT for the development of knowledge processes. For this firms must use IT to enhance their capabilities, especially knowledge acquisition and possession, through educating and training current employees. According to this viewpoint, top management must continuously strive to support the establishment of a of dynamic working atmosphere to promote the application of external knowledge (Chou, 2005). Second, by encouraging the use of IT in interdependent tasks, it should be considered as a means of achieving the firm’s competitive advantages, because organizations may create teams beyond the member’s physical positions, influencing the capabilities of knowledge processes (Griffith et al., 2003). Moreover, organizations will be able to develop their ACAP, which is an essential ability in this knowledge-intensive business era (Kostopoulos et al., 2011). Third, Managers should prioritize technology to support the growth of knowledge processes. To this end, firms must develop clear policies to support knowledge generation, determine the vital knowledge for their firm under different circumstances, focus on knowledge transfer and integration within the organization, and develop knowledge maps that should determine the firm’s individual and knowledge system. Fourth, firms must improve their capabilities through creating internal capabilities. They can enhance their capabilities by utilizing IT for knowledge search; the more knowledge they obtain, the more development they can make in terms of performance. Fifth, the study facilitate governments in growing both the public and private sector firms by increasing employee’s dynamic capabilities. These competencies include the capacity to employ information technology and to turn information beneficial for government and public organization using ACAP. These capabilities will not only increase the productivity of public and private sector firms, but will also enable them to perform well in crucial situations. The government may use these capabilities by applying private-sector techniques in which information usage is an art form to improve the functioning of the government organizations.

Limitations and Future Research

Beside contributions, this study has a few limitations. First of all, survey data was self-reported, which may be subject to social desirability bias (Podsakoff & Organ, 1986). Even if the reaction is related to the sensitive subject, the assurance of anonymity can be minimized (Maria Teresa Bolivar-Ramos et al., 2013). Second, Harman’s one-factor test and other method tests did not identify common method variance as an issue, it may have been (Konrad & Linnehan, 1995; Podsakoff & Organ, 1986), Thus future research should be focused on more in-depth analysis to prevent bias in the studies. We also recommend that future studies collect measurements of the suggested variables from diverse geographic locations to reduce the influence of any response bias. Third, this study is limited to the IT-intensive sector; in future, the investigation should be considered other sectors or firms of varying sizes to offer a better knowledge of the relationships in this subject area.

Footnotes

Appendix

Table of Abbreviations.

| Words | Abbreviations |

|---|---|

| Absorptive Capacity | ACAP |

| Adjusted Goodness of Fit Index | AGFI |

| Average Variance Extracted | AVE |

| Confirmatory Factor Analysis | CFA |

| Construct Reliability | CNR |

| Comparative Fit Index | CFI |

| Composite Reliability | CR |

| Dynamic Capabilities | DCs |

| Exploratory Factor Analysis | EFA |

| Firm Performance | FP |

| Information technology | IT |

| Maximum Reliability | MaxR |

| Maximum Shared Variance | MSV |

| Normative Fit Index | NFI |

| Potential Absorptive Capacity | PACAP |

| Realized Absorptive Capacity | RACAP |

| Resource Based-view | RBV |

| Root Mean Square Error of Approximation | RMSEA |

| Seizing | SZ |

| Sensing | SN |

| Transformation | TF |

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Scientific and technological innovation 2030 - new generation of artificial intelligence major project 2020AAA0108505.